Embed Size (px)

Citation preview

E-TDS RETURNSProcedure & Problems

Gautam NayakChartered Accountant

Bombay Chartered Accountants’ Society23rd March 2007

APPLICABILITYS.200(3) – Quarterly statements of TDSS.206 – Electronic TDS Returns mandatory for Government and companiesElectronic Filing of TDS Returns Scheme 2003 notified u/s.206(2)Second proviso to rule 31A Optional for deductors other than corporate and government deductors to file TDS returns in electronic form - can file in physical form

TDS Statements –Forms and Periodicity

With each quarterly e-TDS statement

Physical control chart containing control totals mentioned in quarterly TDS statement furnished electronically. Form 27A also in physical form along with electronic TDS statement.

27A

14th July / Oct/ Jan/ Apr or June

Quarterly TDS statement from payments to non-residents

27Q

Quarterly TDS statement of other than "Salaries"*

26Q

For first 3 quarters: within 15 days from end of quarter*.For last quarter: up to 15th

June

Quarterly TDS statement from "Salaries"*

24Q

Last Date of Furnishing Statement ParticularsForm No.

QUOTING PAN / TAN

In case of Deductees :1. PAN2. Need not be quoted for persons to whom

second proviso to section 139A(5B) applies

In case of Deductors :1. PAN & TAN2. PAN not required if TDS made by or on behalf

of Government

Rule 31A - Person responsible for deducting TDS and preparing quarterly statements to quote :

Modes of Furnishing e-TDS Statements

Through TIN Facilitation Centres

Through Web Based Facility

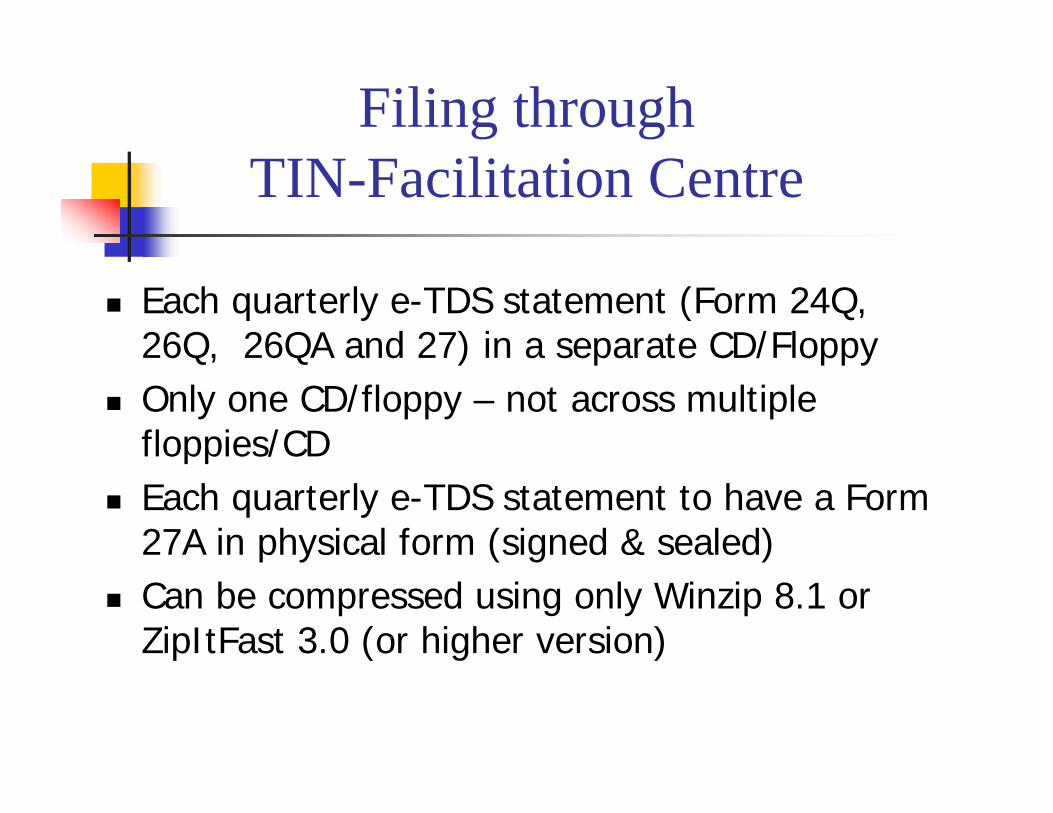

Filing through TIN-Facilitation Centre

Each quarterly e-TDS statement (Form 24Q, 26Q, 26QA and 27) in a separate CD/FloppyOnly one CD/floppy – not across multiple floppies/CDEach quarterly e-TDS statement to have a Form 27A in physical form (signed & sealed)Can be compressed using only Winzip 8.1 or ZipItFast 3.0 (or higher version)

The quarterly e-TDS statement has to be successfully processed through the latest version of the FVU.Verify Control totals, TAN and name mentioned in the quarterly e-TDS statement with those mentioned on Form 27A.

Filing through TIN-Facilitation Centre….

Filing through TIN -Facilitation Centre….

On validation three files generated by FVU-i. Form 24Q/26Q.html - TDS statement statistics

report (summary of e-TDS return successfully validated)

ii. Form 24Q/26Q_PAN Statistics.html - PAN statistics report (list of deductee PAN deficiencies)

iii. Form 24Q/26Q.fvu – upload file

Only fvu file to be submitted on floppy/CD

Label to be affixed on each CD/floppy with TAN Name of deductorPeriod of statement (quarter and F.Y.) Form no. (24Q, 26Q or 26QA) to be affixed on each CD/floppy for the purpose of identification.

No overwriting/striking on Form 27A – any correction to be signed

Filing through TIN-Facilitation Centre….

No bank challan, or copy of TDS certificate to be furnished along with the statements.Mandatory to first obtain TAN using latest Form 49B TAN details (name, address, etc.,) of deductor as provided in quarterly e-TDS statement should be verified with database maintained by ITD.

Filing through TIN-Facilitation Centre….

Filing through TIN -Facilitation Centre….

Upload Fee for each quarterly e-TDS statement by demand draft or cashTIN-FC carries out format level validations (as performed by FVU) & other checks to validate quarterly e-TDS statementAfter validation, TIN-FC issues Provisional Receipt, which is a proof of filing the e-TDS statement Provisional Receipt gives count of ‘PANINVALID’, ‘PANNOTAVBL’ and ‘PANAPPLIED’TIN-FC will retain CD/floppy containing the e-TDS statement and physical Form 27A

In case of discrepancies/inconsistencies (vis-à-vis challan uploaded by Bank) identified in the TIN central system, NSDL to intimate deductorabout discrepancies/ inconsistencies in e-TDS statement by email and registered letterDeductor to rectify e-TDS statement and furnish a correction statement as per correction file formats prescribed by ITD

Acceptance through TIN -Facilitation Centre…

Filing through Web-Based Facility

NSDL provides facility to directly furnish quarterly e-TDS statements to NSDL through its web-site (www.tin-nsdl.com) Process of registration takes about 15 daysOnline Registration using Digital Signature Quarterly e-TDS statements to be digitally signed using same Digital Signature as used for registration

Filing through Web-Based Facility……

Deductor to upload digitally signed quarterly e-TDS statement to the web based facility as per the procedure TIN website will validate digital certificate provided by deductor at time of registration and at time of login and quarterly e-TDS statement uploadIf certificate verification successful, direct upload facility will issue a file reference number for each quarterly e-TDS statement uploaded

Filing through Web-Based Facility…..

If format level validation fails, statement not accepted - Status shown as ‘rejected’ If advance available not sufficient to cover upload charges, statement not accepted - status shown as ‘rejected due to insufficient balance’On successful validation, TIN system generates provisional receipt giving count of missing PANs, which deductor can view/print On successful upload, deductor’s account debited with upload fee for each accepted statement

Filing through Web-Based Facility….

Deductor can view result of validation 24 hours after upload of statementTIN system provides online statement of utilisation of upload fees paid in advance.

Shows details ofopening balance quarterly e-TDS statement uploadedclosing balance available to the credit of TAN.

Deductors uploading digitally signed quarterly e-TDS statements directly on TIN system not required to submit Form 27A, CD/floppy to TIN-FC or NSDL

If not able to upload quarterly e-TDS statement to TIN system through TIN website, may submit at TIN-FCs with normal procedure

Filing through Web-Based Facility….

Common Reasons for Non Acceptance

Each quarterly e-TDS statement (Form 24Q, 26Q or 26QA) not furnished in separate CD / FloppySeparate Form 27A not furnished for each quarterly e-TDS statementStriking and overwriting on Form 27A not duly ratified by person who has signed Form 27AMore than one CD/floppy is used for furnishing one quarterly e-TDS statement

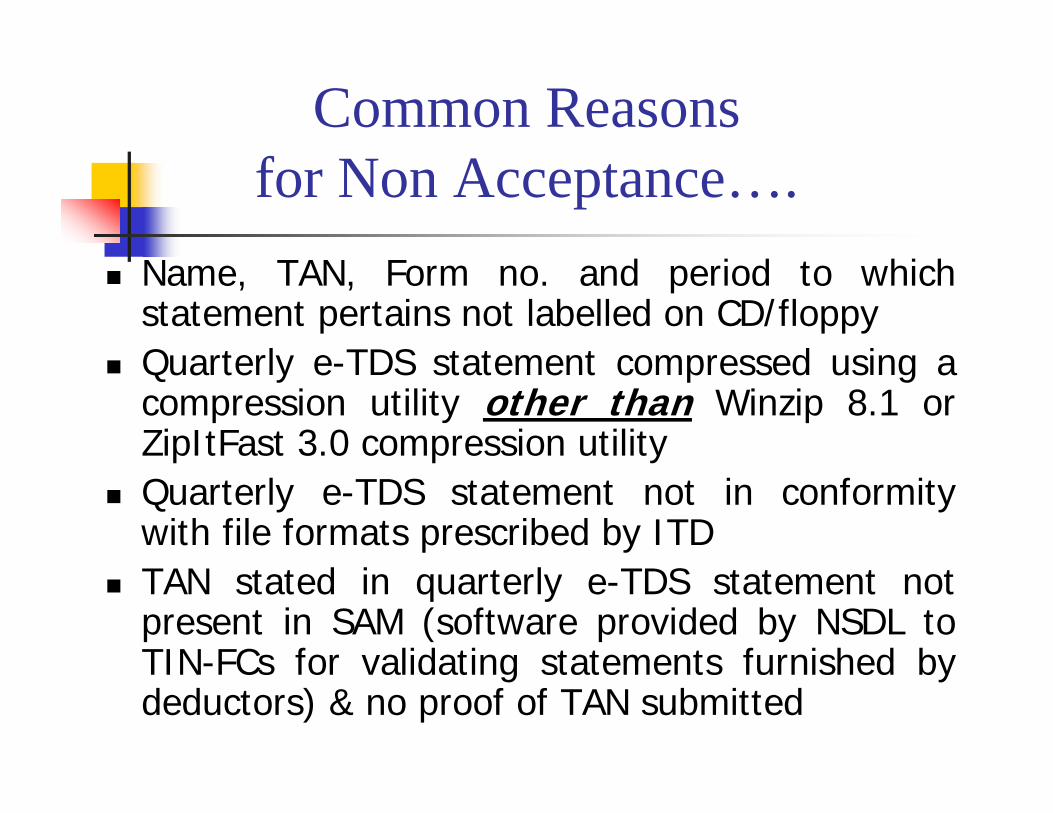

Common Reasons for Non Acceptance….

Name, TAN, Form no. and period to which statement pertains not labelled on CD/floppy Quarterly e-TDS statement compressed using a compression utility other than Winzip 8.1 or ZipItFast 3.0 compression utilityQuarterly e-TDS statement not in conformity with file formats prescribed by ITDTAN stated in quarterly e-TDS statement not present in SAM (software provided by NSDL to TIN-FCs for validating statements furnished by deductors) & no proof of TAN submitted

Common Reasons for Non Acceptance….

Name/address of deductor displayed on SAM not matching with name/address on Form 27A & no TAN change requestMismatch of control totals generated by SAM with Form 27AQuarterly statement not successfully processed through latest version of FVUQuarterly e-TDS statements do not pertain to period for which deductors are allowed to submit their statementsCD/floppy is not virus free.

Correction Process

TIN-FC to issue pre-printed Non - Acceptance Memo to deductor to carry out necessary corrections containing possible reasons for non-acceptanceIn case of non-acceptance, TIN-FC to return CD/floppy, any other documents furnished and physical Form 27A to deductorNo fee charged for e-TDS statement that is not accepted

Form 26ASForm 26AS- consolidated tax statement issued under Rule 31 AB of Income Tax Rules to PAN holdersAnnual Statement displays details of TDS,TCS & Income Tax deducted, collected & paid by each person (deductor) who made a specified kind of payment

Form 24Q – Some IssuesIf estimated income of employee for whole year after deduction for savings like PPF, GPF, NSC etc. below taxable limit, particulars need not be included in Form No. 24QIf estimated annual income of an employee exceeds exemption limit during the course of the year, tax to be deducted in that quarter and particulars reported in Form No. 24Q from that quarter onwards

TDS figures entered are based on annual calculations of tax and the TDS is spread evenly - does not give a fair picture of TDS in each quarterFor salary, if certificate for nil/ lower deduction of TDS received, mention needs to be made in relevant column and certificates filed with e TDS returnNo such certificate required to be filed for non-salary quarterly statements

Form 24Q – Some Issues

Thank you!