Embed Size (px)

Citation preview

E-Commerce Logistics DriversJohn Callan – UrsaMajor Associates

Shea Felix - EndiciaCooper Smith – Business Insider

The Future of DeliveryMatt Swain – InfoTrends

Gary Reblin - USPS

E-Commerce Logistics Drivers / The Future of Delivery

Cooper Smith – Business Insider

Brody Buhler - Accentúre

Matt Swain - InfoTrends

Gary Reblin - USPS

Amine Khechfé - Endicia

PostalVision2020

March 2015

3

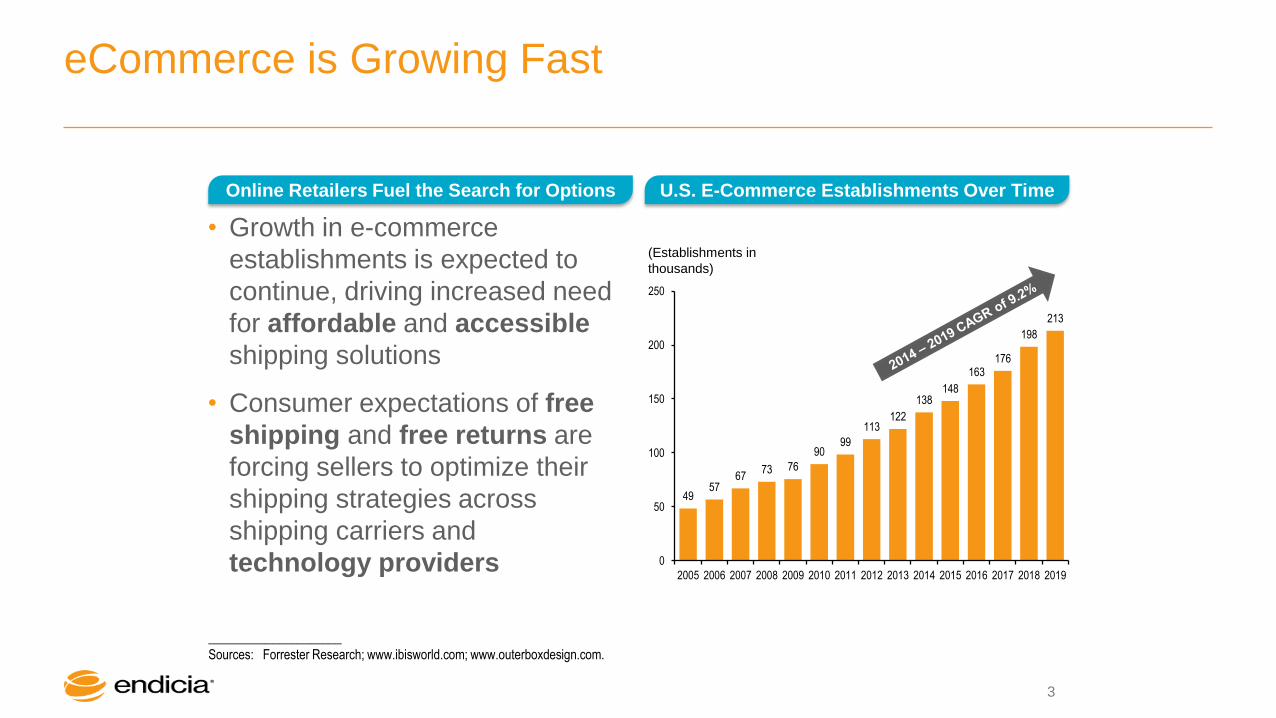

eCommerce is Growing Fast

U.S. E-Commerce Establishments Over Time

_____________________

Sources: Forrester Research; www.ibisworld.com; www.outerboxdesign.com.

4957

6773 76

9099

113122

138148

163176

198

213

0

50

100

150

200

250

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

(Establishments in

thousands)

Online Retailers Fuel the Search for Options

• Growth in e-commerce

establishments is expected to

continue, driving increased need

for affordable and accessible

shipping solutions

• Consumer expectations of free

shipping and free returns are

forcing sellers to optimize their

shipping strategies across

shipping carriers and

technology providers

BuyersBuyers

BuyersBuyers

Buyers Buyers

Desktop Cloud Mobile APIs

Shipping / Delivery Technology

Online

RetailersMarketplaces Brick & Mortar

Retailers

Warehouse

Shippers 3PLs

Login / Authentication / Sign-up Preferences & ConfigurationSecurity & Profiles

Printing EngineLabel

Customization

Integration

Batch

Management

Reporting,

Analytics, Audit

Account & User

Management

Address Book

Compliance

(Rating, Rules)

Value Added

Services

Business Rules

Engine

Application

Security

Billing &

Payments

External

Systems

Database / OMS

/ XML

Emails,

Notifications

3rd party

(eBay, shopping

cart, etc.)

Hardware

Customer Rules

Engine

Others…

POSTAL OPERATORS & CONSOLIDATORS

thanks!

A Research Service By Business Insider

E-Commerce Logistics Drivers

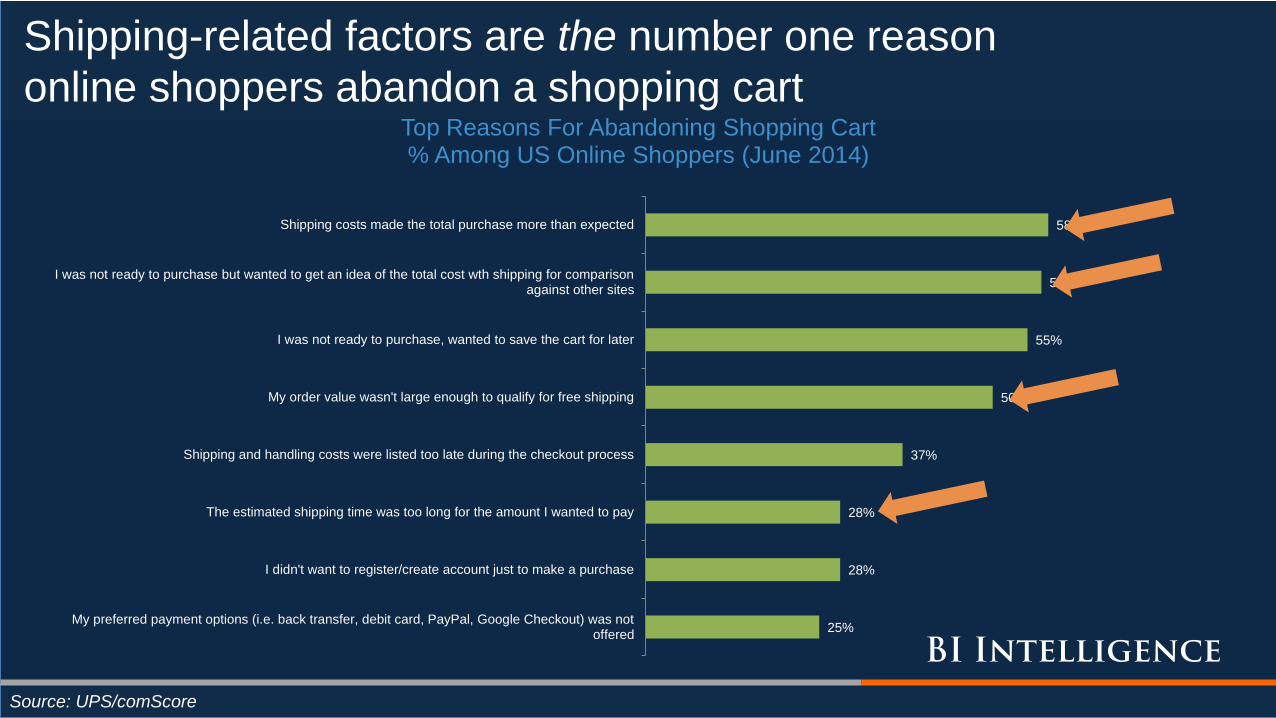

How important a factor is delivery to online shoppers?

Shipping-related factors are the number one reason

online shoppers abandon a shopping cart

Source: UPS/comScore

25%

28%

28%

37%

50%

55%

57%

58%

My preferred payment options (i.e. back transfer, debit card, PayPal, Google Checkout) was notoffered

I didn't want to register/create account just to make a purchase

The estimated shipping time was too long for the amount I wanted to pay

Shipping and handling costs were listed too late during the checkout process

My order value wasn't large enough to qualify for free shipping

I was not ready to purchase, wanted to save the cart for later

I was not ready to purchase but wanted to get an idea of the total cost wth shipping for comparisonagainst other sites

Shipping costs made the total purchase more than expected

Top Reasons For Abandoning Shopping Cart% Among US Online Shoppers (June 2014)

Consumers also say they would shop more online

if given more shipping flexibility

Source: Boston Consulting Group, 2012

7%

9%

9%

15%

15%

18%

19%

25%

25%

35%

50%

74%

Flexibility of delivery time and place

Same-day delivery

Guarenteed delivery timing

Faster delivery options

Can chat with salesperson

Compare different products

Insurance against credit card fraud

Better virtual view of products

More-secure websites

Free returns

Lower prices

Free delivery

Percent Of US Consumers Who Say The Following Factors Would Motivate Them To Shop More

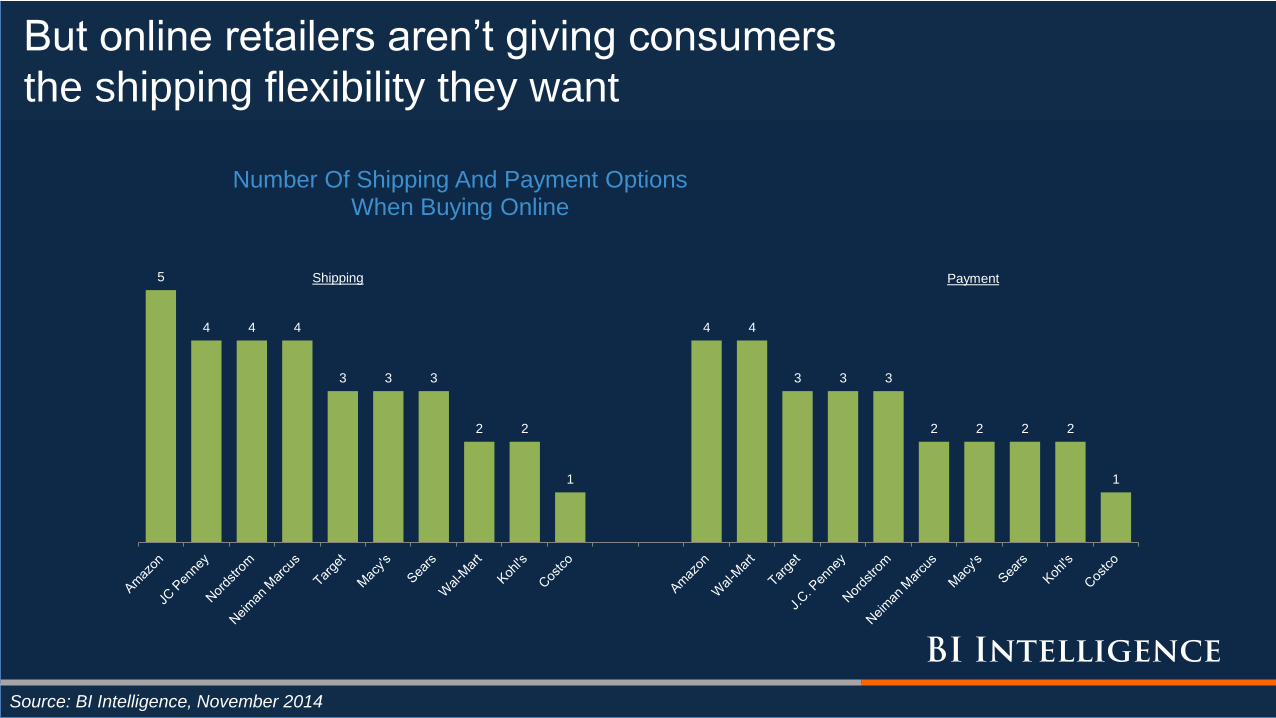

But online retailers aren’t giving consumers

the shipping flexibility they want

Source: BI Intelligence, November 2014

5

4 4 4

3 3 3

2 2

1

4 4

3 3 3

2 2 2 2

1

Number Of Shipping And Payment Options When Buying Online

Shipping Payment

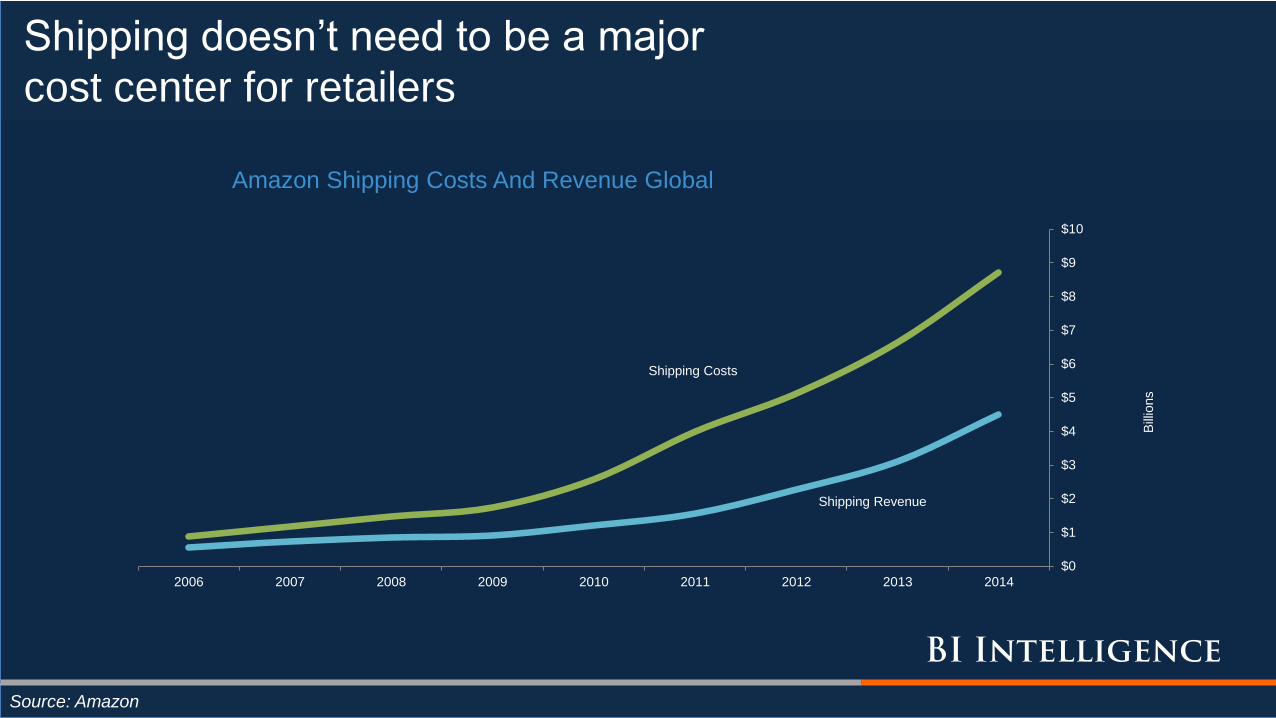

Shipping doesn’t need to be a major

cost center for retailers

Source: Amazon

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

$10

2006 2007 2008 2009 2010 2011 2012 2013 2014

Bill

ions

Amazon Shipping Costs And Revenue Global

Shipping Revenue

Shipping Costs

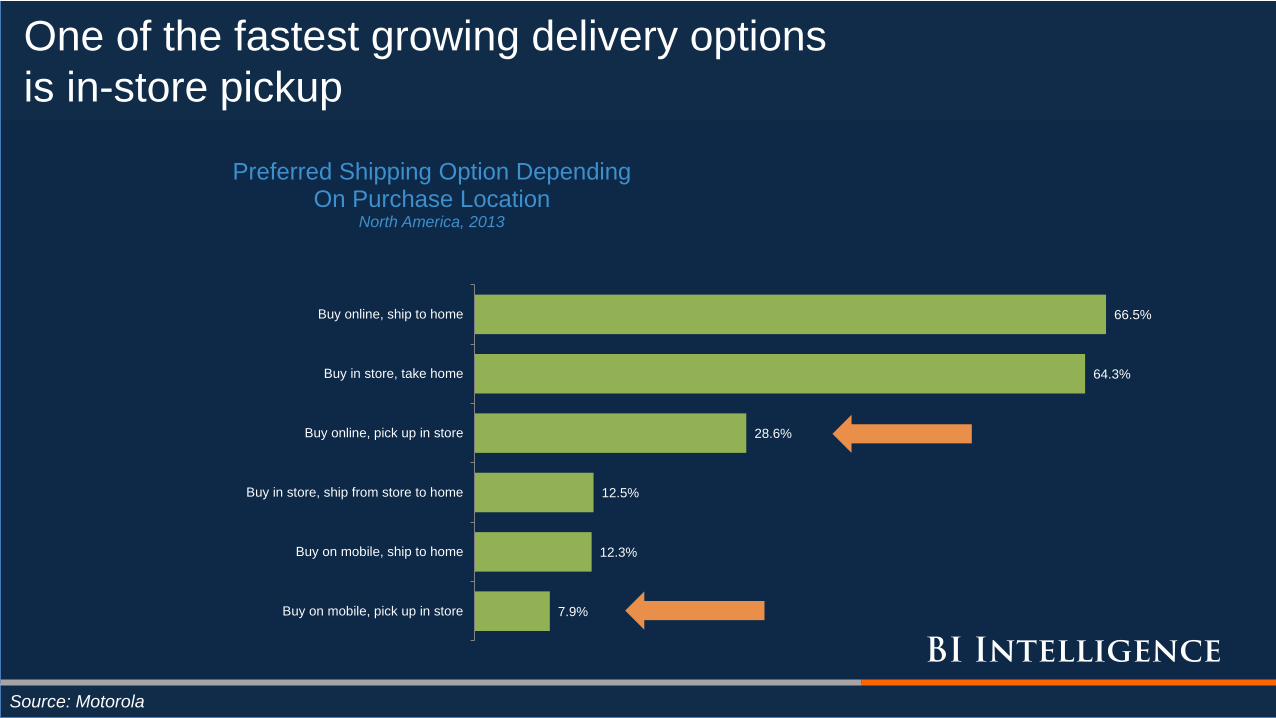

One of the fastest growing delivery options

is in-store pickup

Source: Motorola

7.9%

12.3%

12.5%

28.6%

64.3%

66.5%

Buy on mobile, pick up in store

Buy on mobile, ship to home

Buy in store, ship from store to home

Buy online, pick up in store

Buy in store, take home

Buy online, ship to home

Preferred Shipping Option Depending On Purchase Location

North America, 2013

Same-day delivery is one way that online retailers

can provide a sense of instant gratification

Source: BI Intelligence Estimates

$0.62

$1.97

$3.35

$4.03

$0.16

$0.49

$0.84

$1.01

$0

$1

$2

$3

$4

$5

E2014 E2015 E2016 E2017 E2018

Bill

ions

US Same-Day Delivery Market Forecast*Annual Estimates In $ Billions, Delivery By Human Couriers Only

Value Of Merchandise Ordered Annually Via

Same-Day Delivery

Shipping Fees Generated Annually

By Same-Day Delivery Services

Five-Year CAGR 111%

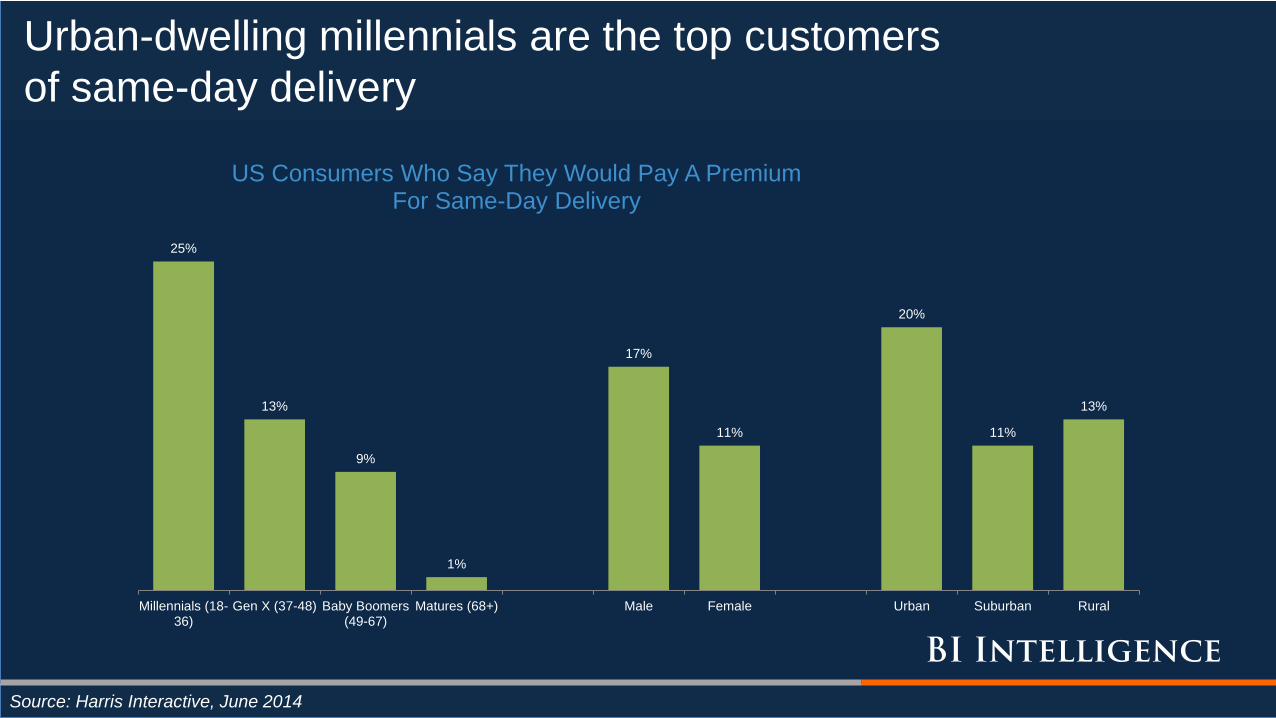

Urban-dwelling millennials are the top customers

of same-day delivery

Source: Harris Interactive, June 2014

25%

13%

9%

1%

17%

11%

20%

11%

13%

Millennials (18-36)

Gen X (37-48) Baby Boomers(49-67)

Matures (68+) Male Female Urban Suburban Rural

US Consumers Who Say They Would Pay A Premium For Same-Day Delivery

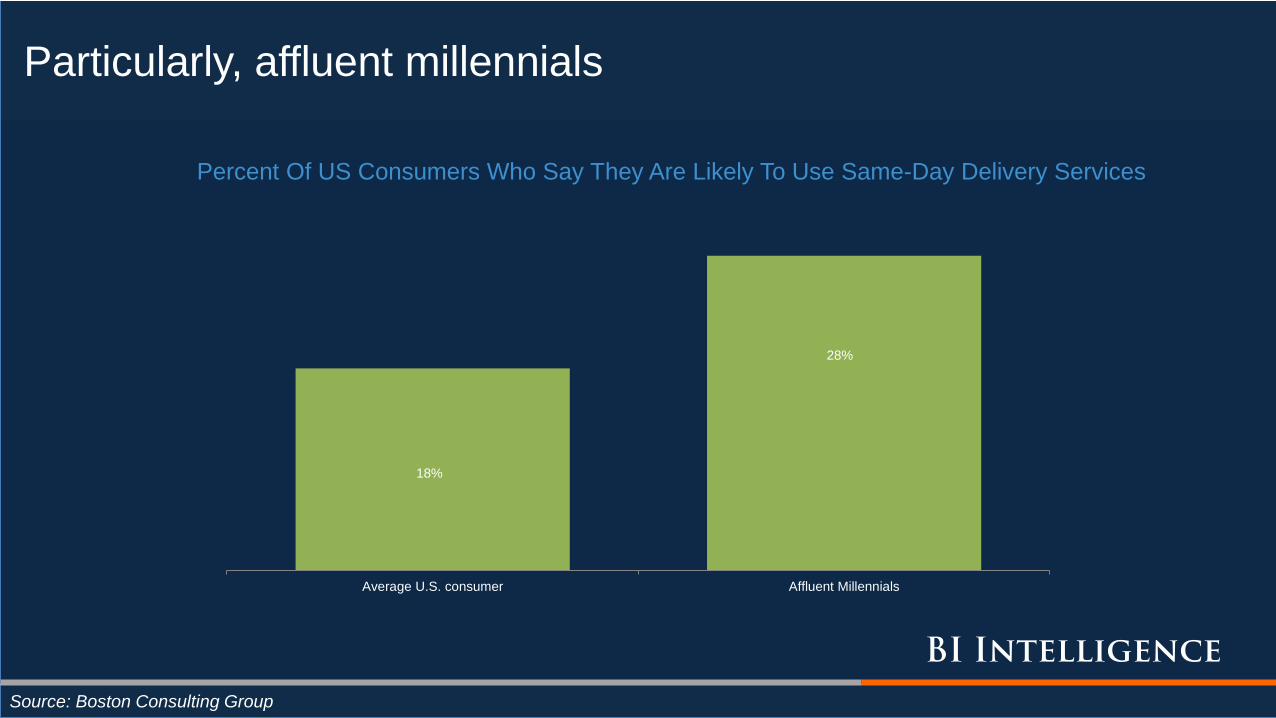

Particularly, affluent millennials

Source: Boston Consulting Group

18%

28%

Average U.S. consumer Affluent Millennials

Percent Of US Consumers Who Say They Are Likely To Use Same-Day Delivery Services

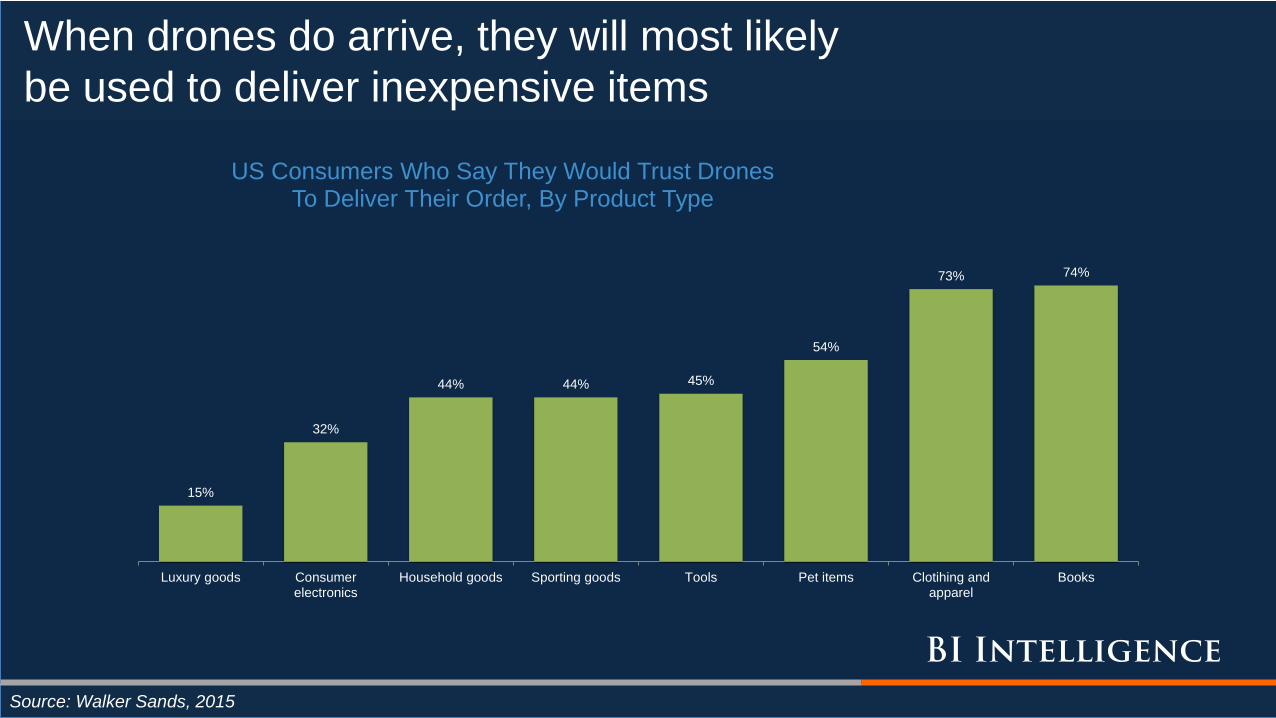

When drones do arrive, they will most likely

be used to deliver inexpensive items

Source: Walker Sands, 2015

15%

32%

44% 44% 45%

54%

73% 74%

Luxury goods Consumerelectronics

Household goods Sporting goods Tools Pet items Clotihing andapparel

Books

US Consumers Who Say They Would Trust Drones To Deliver Their Order, By Product Type

intelligence.businessinsider.com

BI Intelligence

Henry Blodget

CEO & Editor-in-Chief

Emily Adler

Senior Research Editor

Marcelo Ballvé

Editorial Director

Cale Weissman

Reporter

Evan Bakker

Research Associate

John Greenough

Research Analyst

Jessica Smith

Research Associate

Tony Danova

Senior Research Analyst

Mark Hoelzel

Research Analyst

John Heggestuen

Research Analyst

Cooper Smith

Senior Research Analyst

PostalVision 2020 – New

Delivery ModelsMarch 2015

19

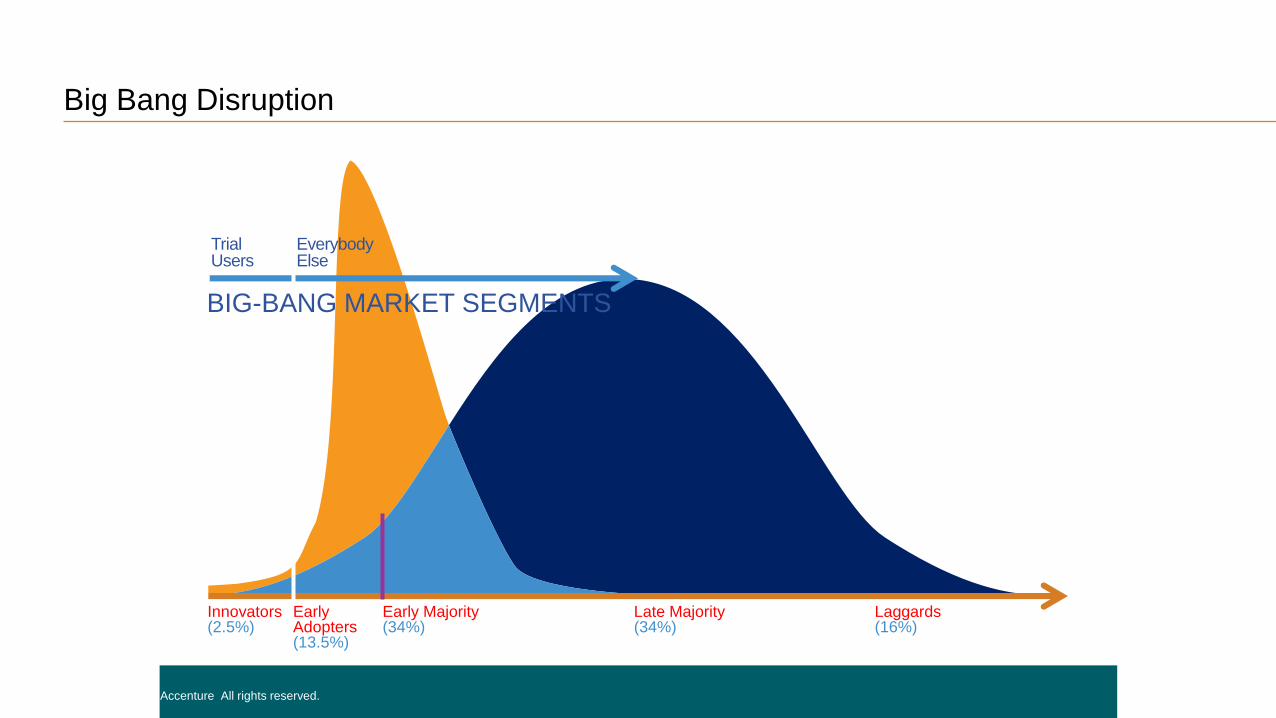

Big Bang Disruption

Copyright © 2015 Accenture All rights reserved.

Trial Users

Everybody Else

Innovators(2.5%)

Early Adopters (13.5%)

Early Majority (34%)

Late Majority (34%)

Laggards(16%)

BIG-BANG MARKET SEGMENTS

20

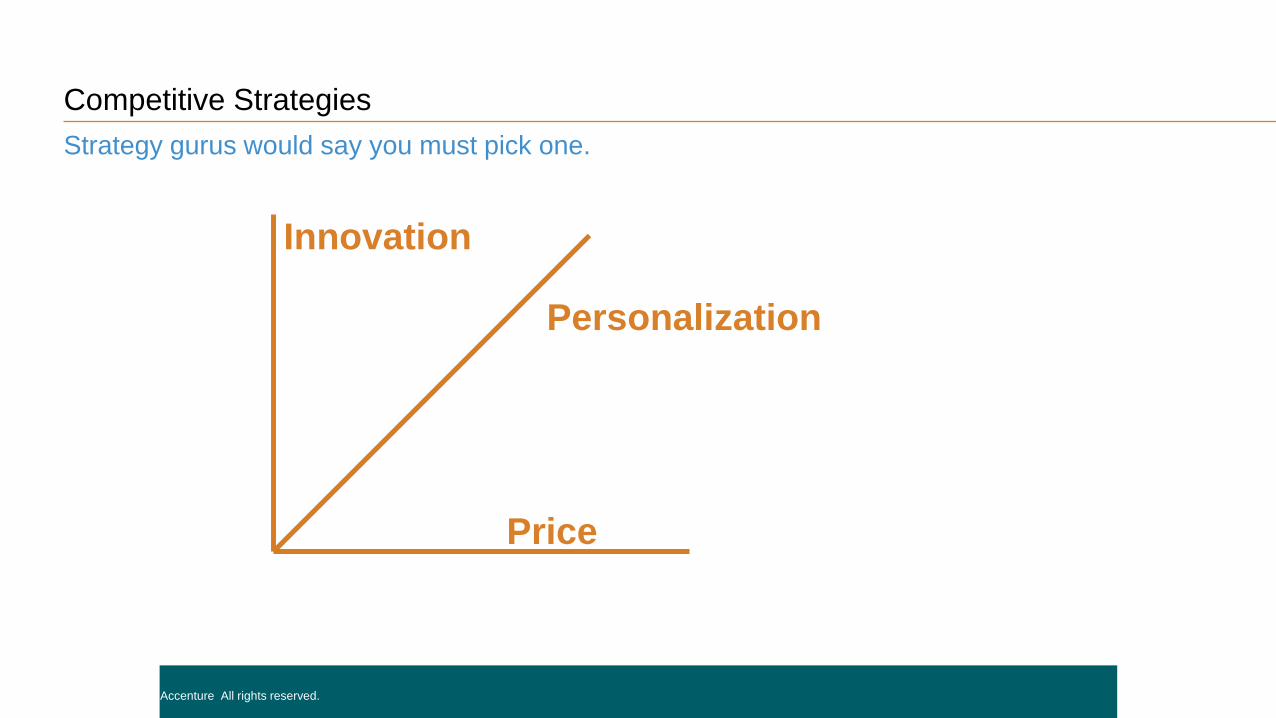

Competitive Strategies

Strategy gurus would say you must pick one.

Copyright © 2015 Accenture All rights reserved.

Price

Innovation

Personalization

21

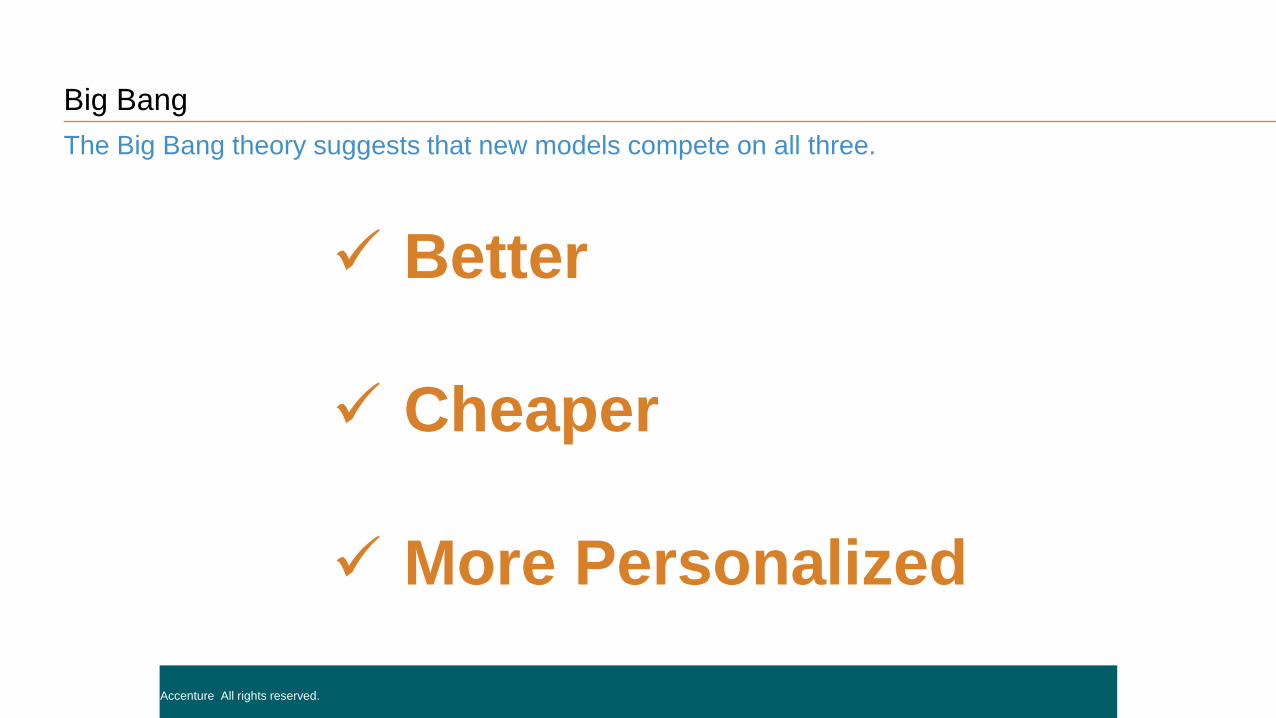

Big Bang

The Big Bang theory suggests that new models compete on all three.

Copyright © 2015 Accenture All rights reserved.

Better

Cheaper

More Personalized

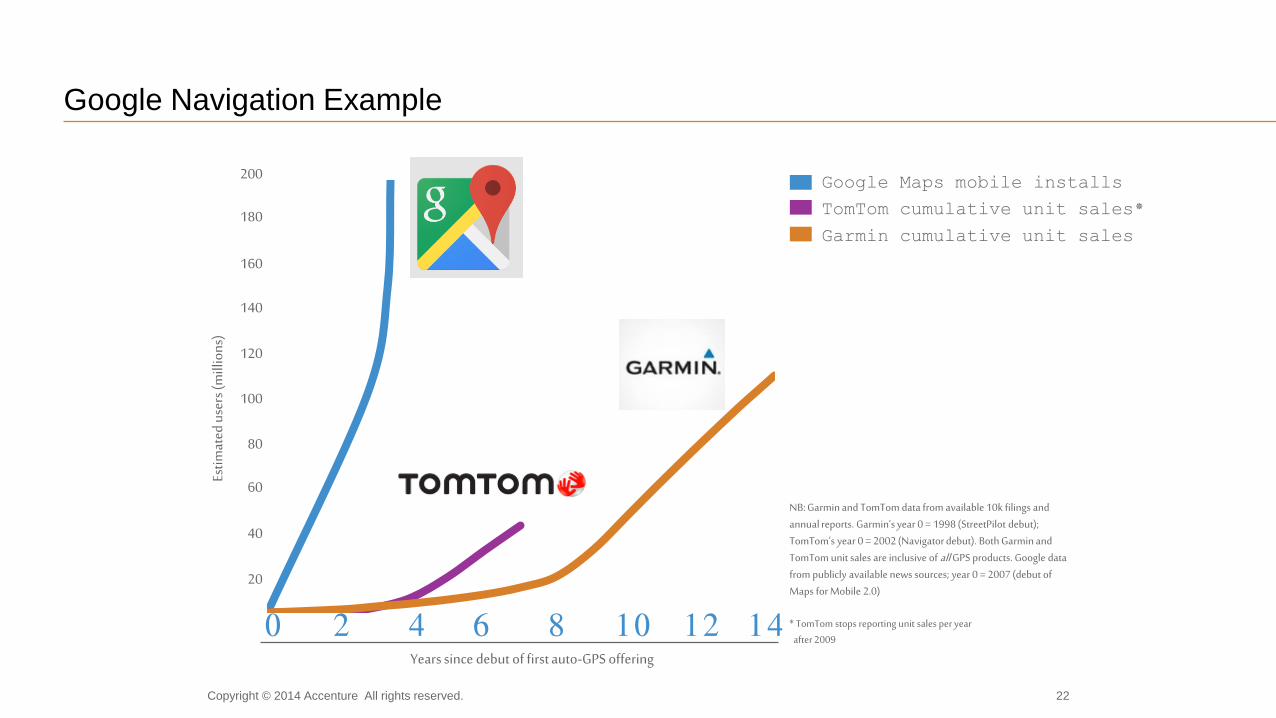

Google Navigation Example

NB: Garmin and TomTom data from available 10k filings and annual reports. Garmin’s year 0 = 1998 (StreetPilot debut); TomTom’s year 0 = 2002 (Navigator debut). Both Garmin and TomTom unit sales are inclusive of all GPS products. Google data from publicly available news sources; year 0 = 2007 (debut of Maps for Mobile 2.0)

* TomTom stops reporting unit sales per yearafter 2009

0 2Years since debut of first auto-GPS offering

4 6 8 10 12 14

200

180

160

140

120

100

80

60

40

20

Estim

ated

use

rs (m

illio

ns)

Google Maps mobile installs

TomTom cumulative unit sales*

Garmin cumulative unit sales

Copyright © 2014 Accenture All rights reserved. 22

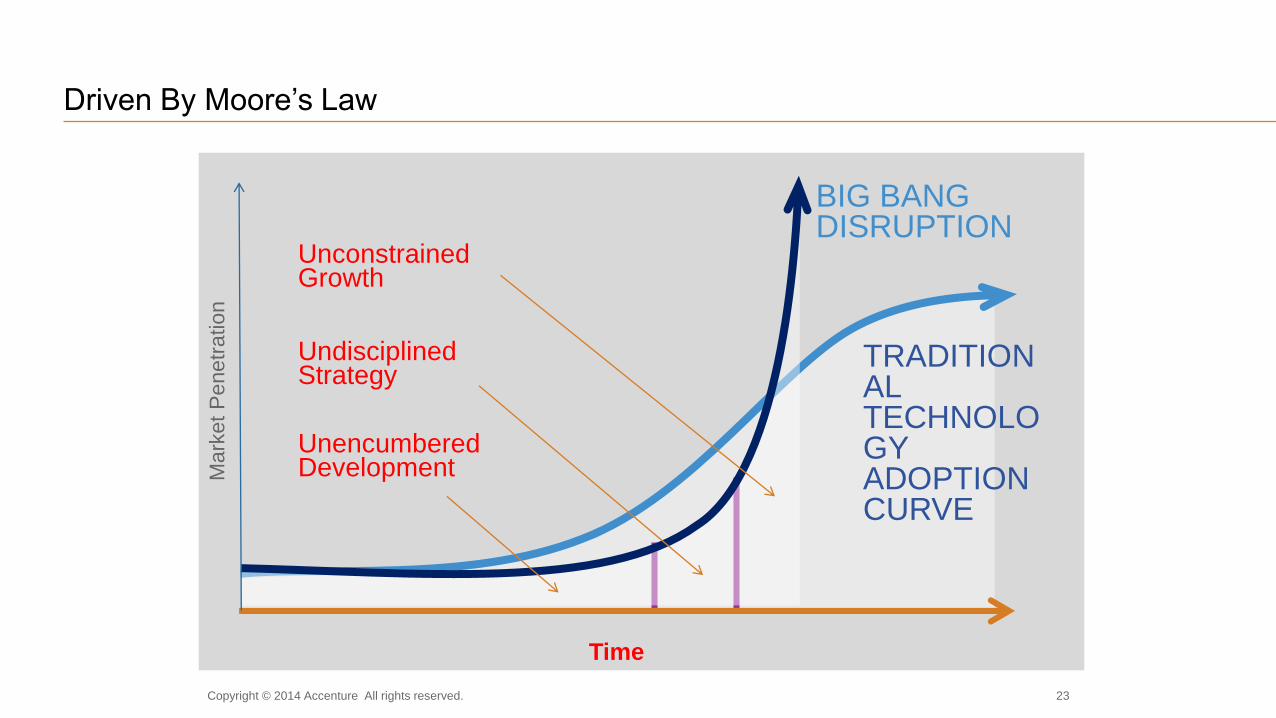

Unencumbered Development

BIG BANG DISRUPTION

Time

Mark

et

Pene

tration

TRADITIONALTECHNOLOGYADOPTION CURVE

Undisciplined Strategy

Unconstrained Growth

Driven By Moore’s Law

Copyright © 2014 Accenture All rights reserved. 23

24

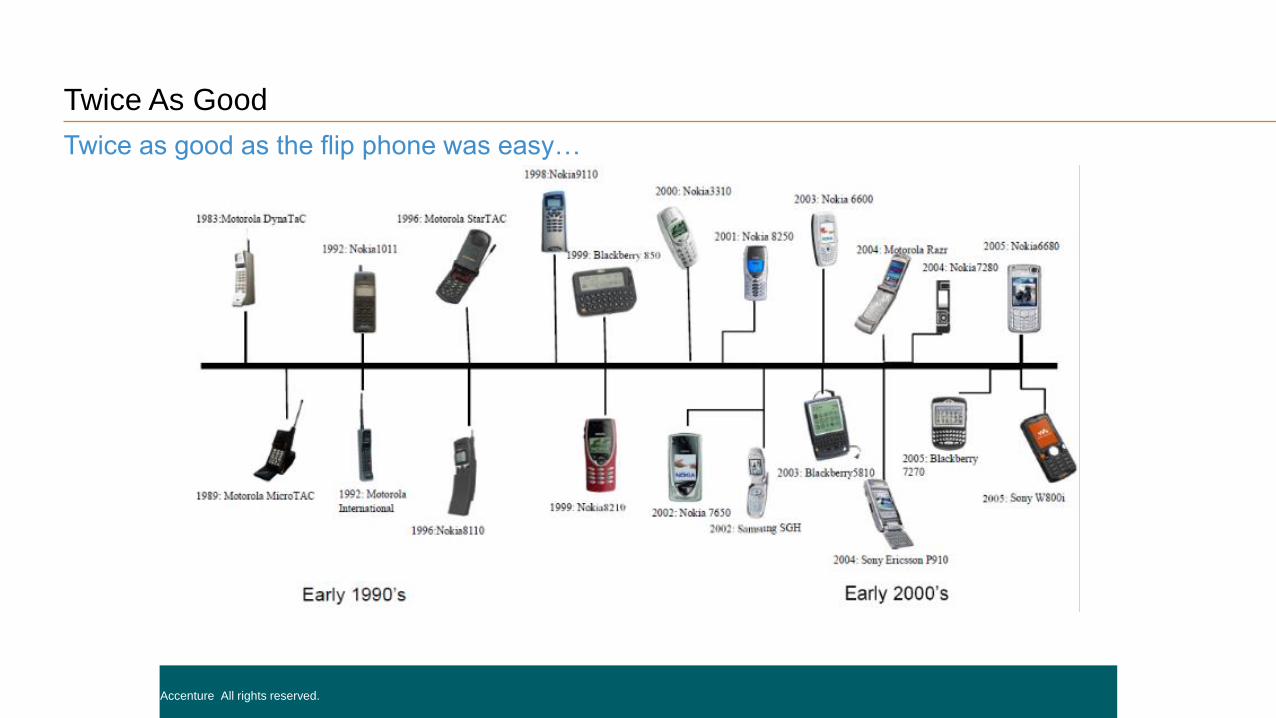

Twice As Good

Twice as good as the flip phone was easy…

Copyright © 2015 Accenture All rights reserved.

25

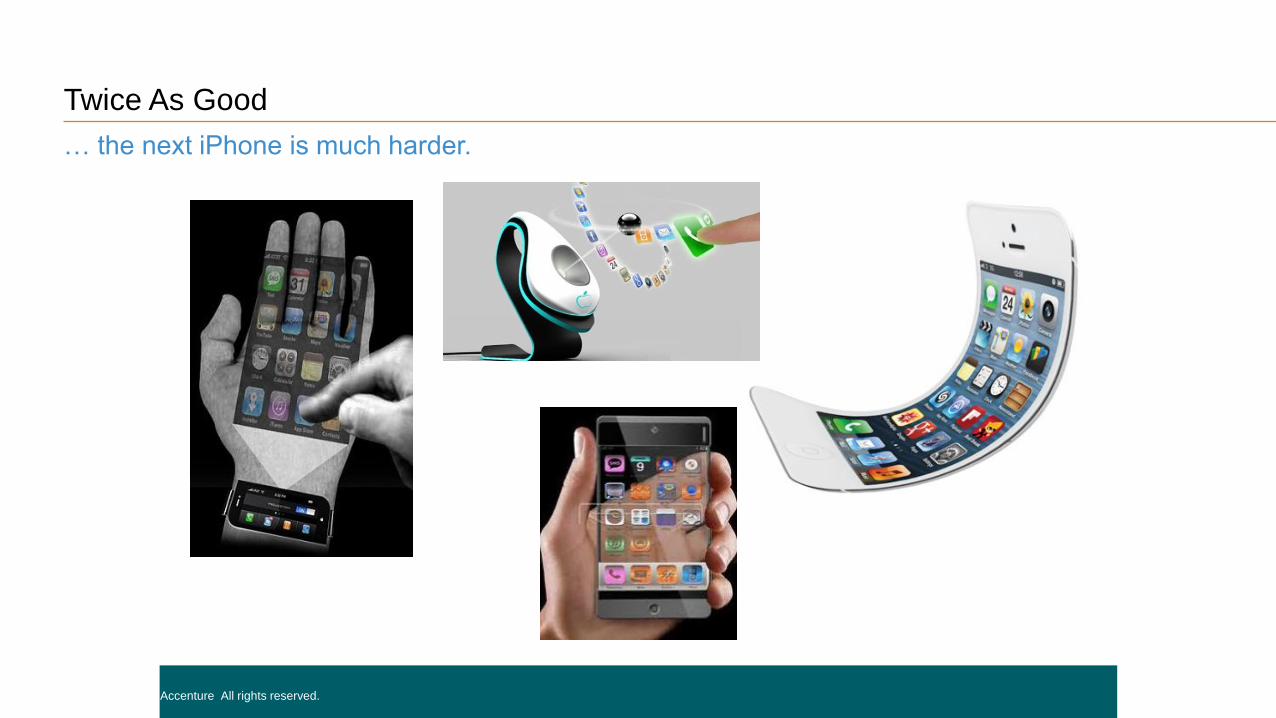

Twice As Good

… the next iPhone is much harder.

Copyright © 2015 Accenture All rights reserved.

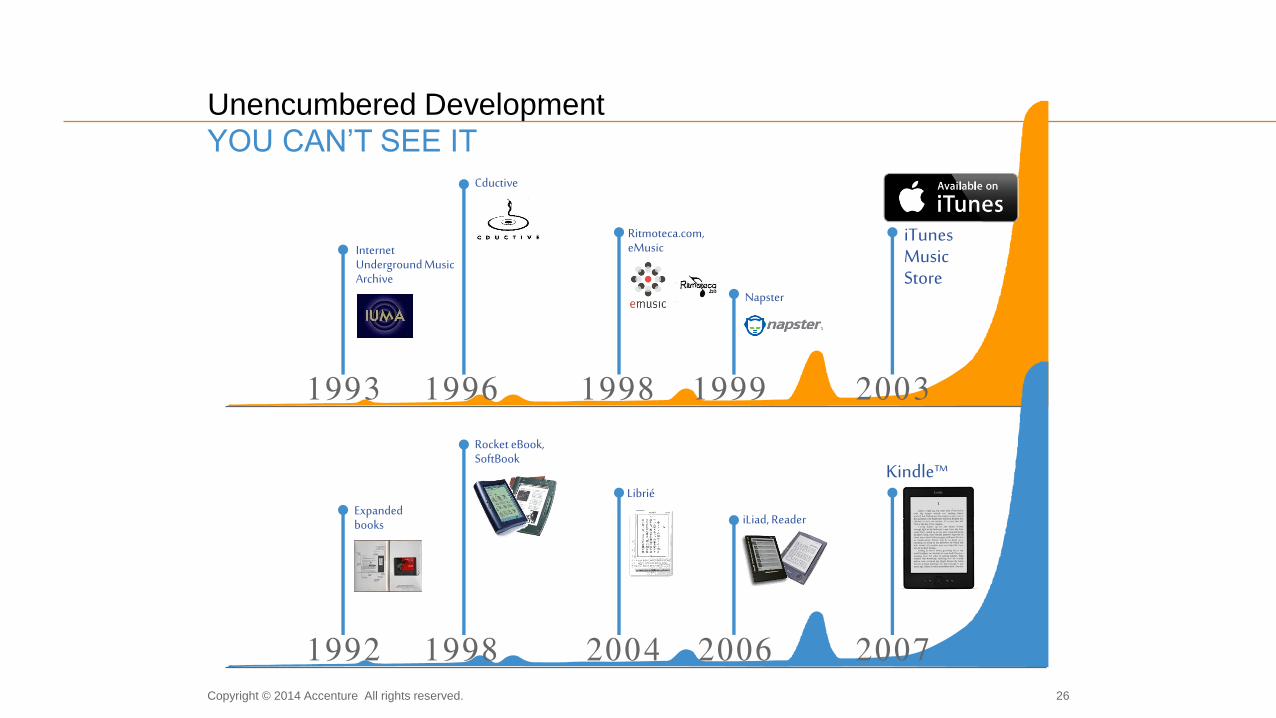

1993 1996 1998 1999 2003

Unencumbered Development

YOU CAN’T SEE IT

Napster

iTunes Music Store

Internet Underground Music Archive

Ritmoteca.com, eMusic

Cductive

Kindle™

Expanded books

Rocket eBook, SoftBook

Librié

iLiad, Reader

1992 1998 2004 2006 2007Copyright © 2014 Accenture All rights reserved. 26

27

Moore’s Law Applied

Three technologies have come together to forever radically change the consumer landscape.

Copyright © 2015 Accenture All rights reserved.

Smartphone

+ Network

+ Cloud

Infinite Processing Capacity

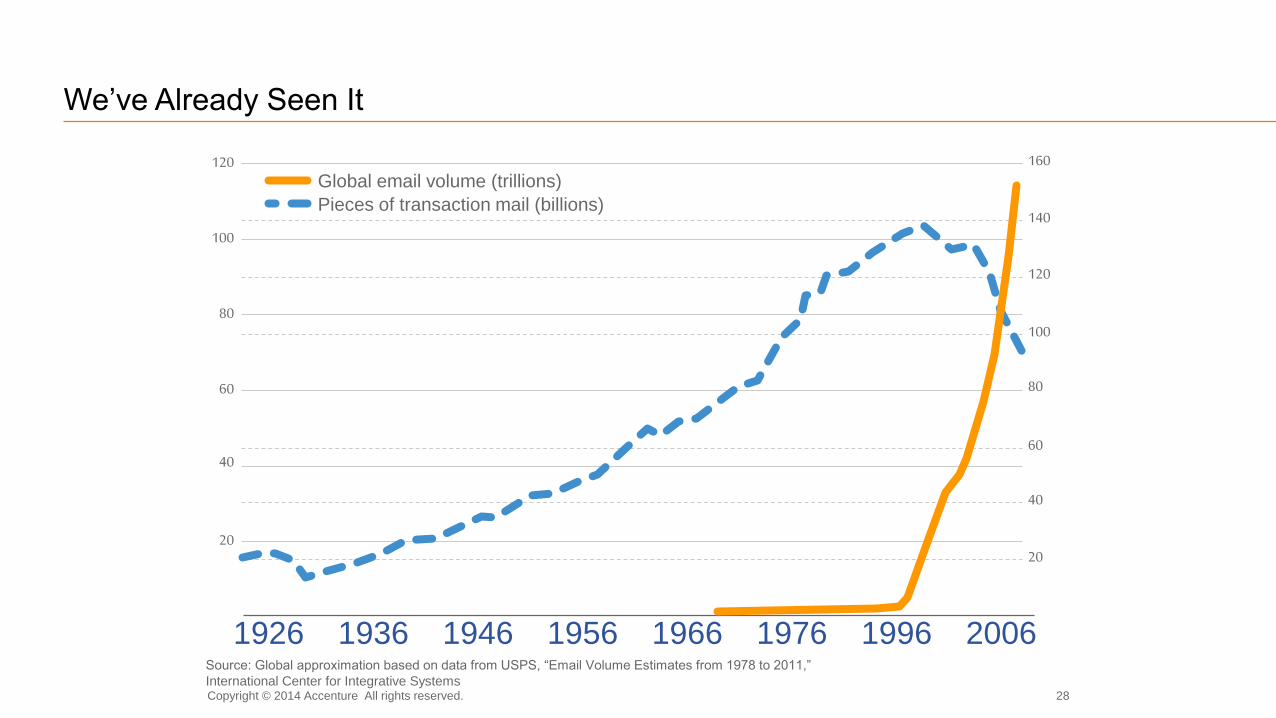

We’ve Already Seen It

Source: Global approximation based on data from USPS, “Email Volume Estimates from 1978 to 2011,”

International Center for Integrative Systems

1926 1936 1946 1956

Pieces of transaction mail (billions)

Global email volume (trillions)120

100

80

60

40

20

160

140

100

80

40

20

120

60

1966 20061976 1996

Copyright © 2014 Accenture All rights reserved. 28

29

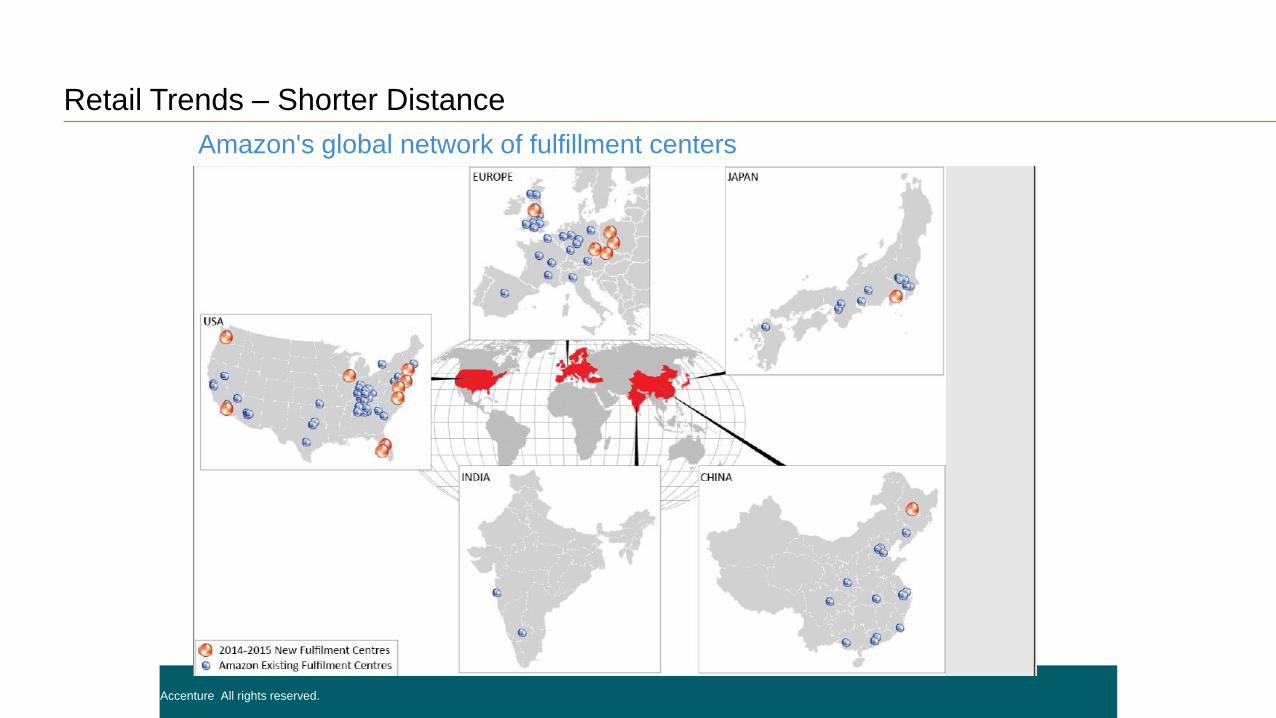

Retail Trends – Shorter Distance

Copyright © 2015 Accenture All rights reserved.

Amazon's global network of fulfillment centers

30

Retail Trends – Free Shipping

Free shipping is the number one decision factor for online purchases.

Copyright © 2015 Accenture All rights reserved.

31

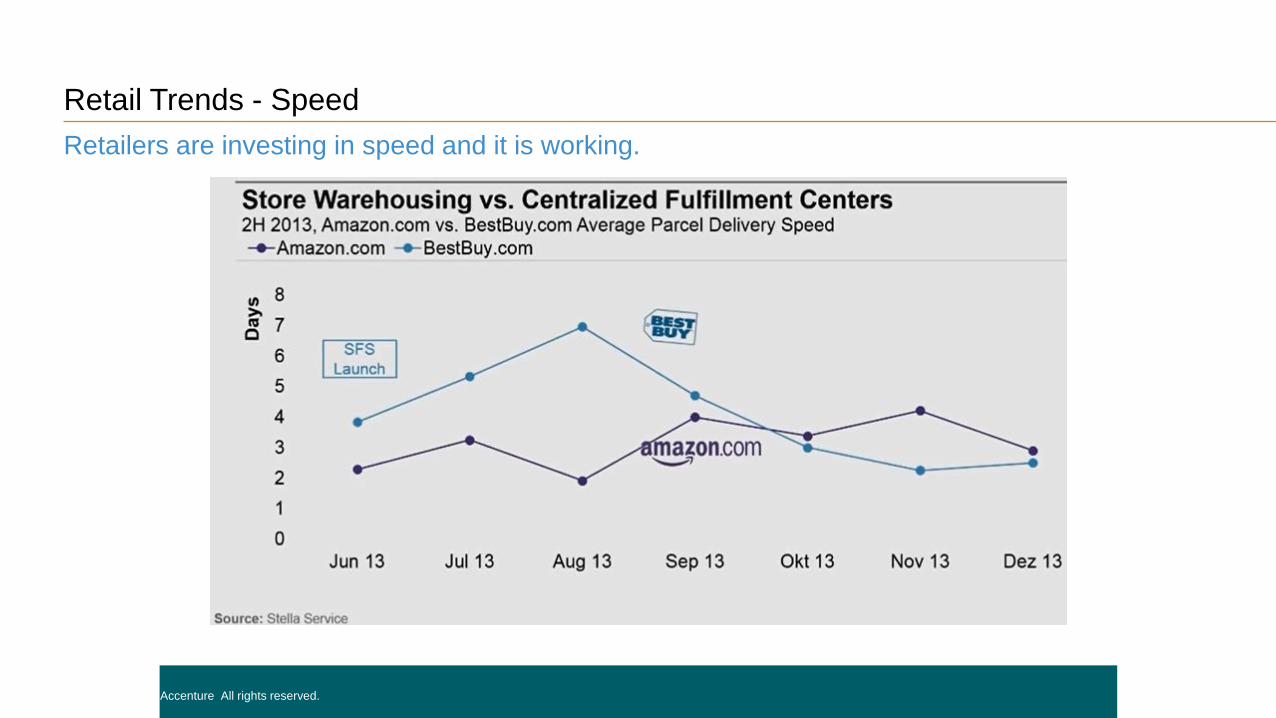

Retail Trends - Speed

Retailers are investing in speed and it is working.

Copyright © 2015 Accenture All rights reserved.

32

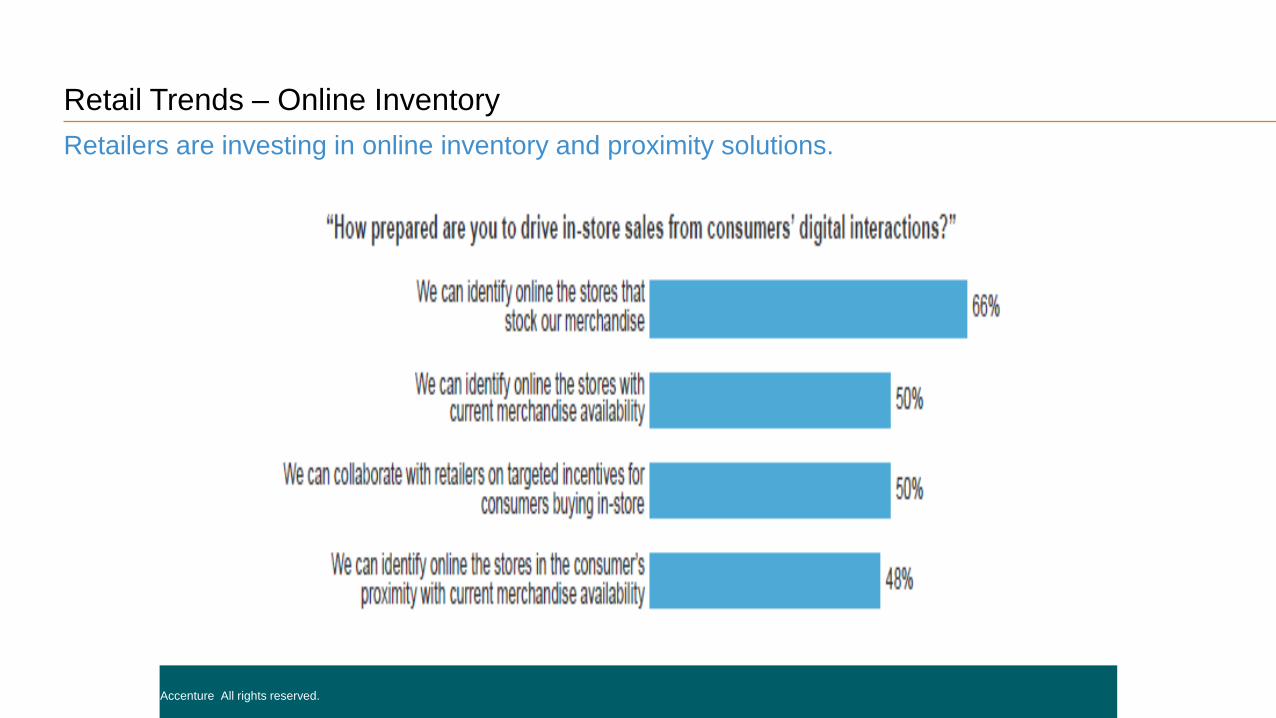

Retail Trends – Online Inventory

Retailers are investing in online inventory and proximity solutions.

Copyright © 2015 Accenture All rights reserved.

33

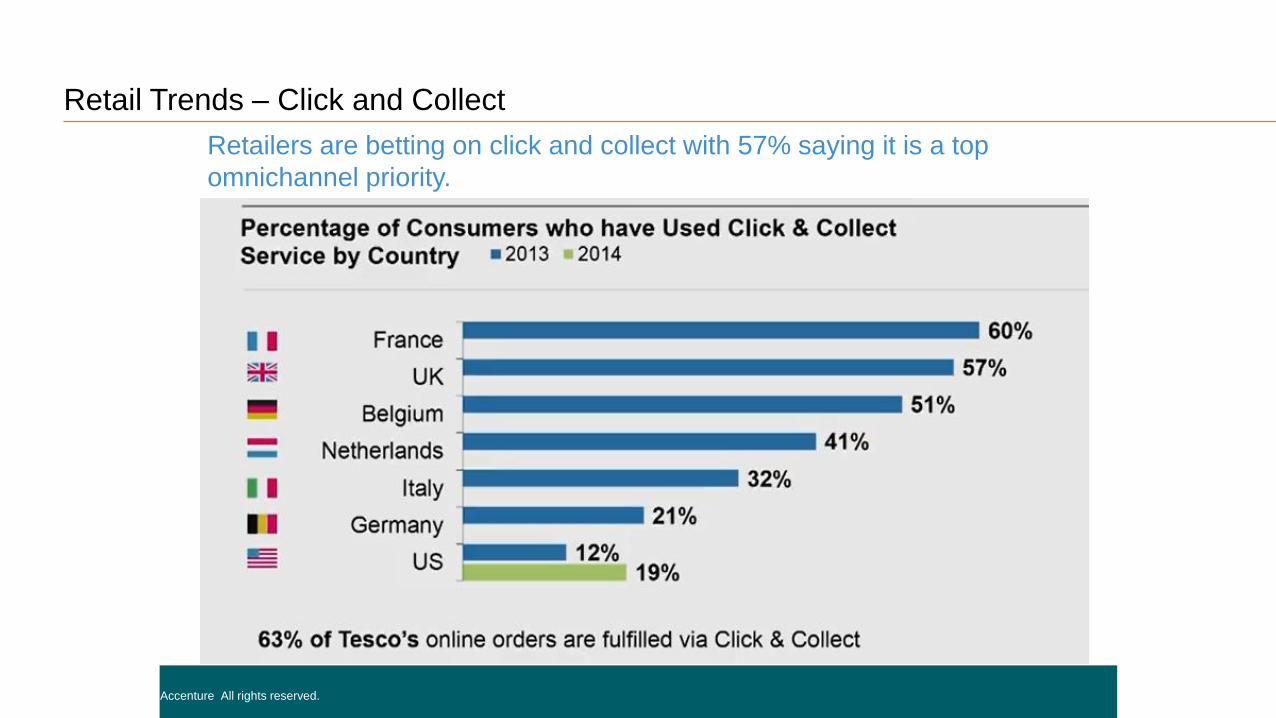

Retail Trends – Click and Collect

Retailers are betting on click and collect with 57% saying it is a top

omnichannel priority.

Copyright © 2015 Accenture All rights reserved.

34

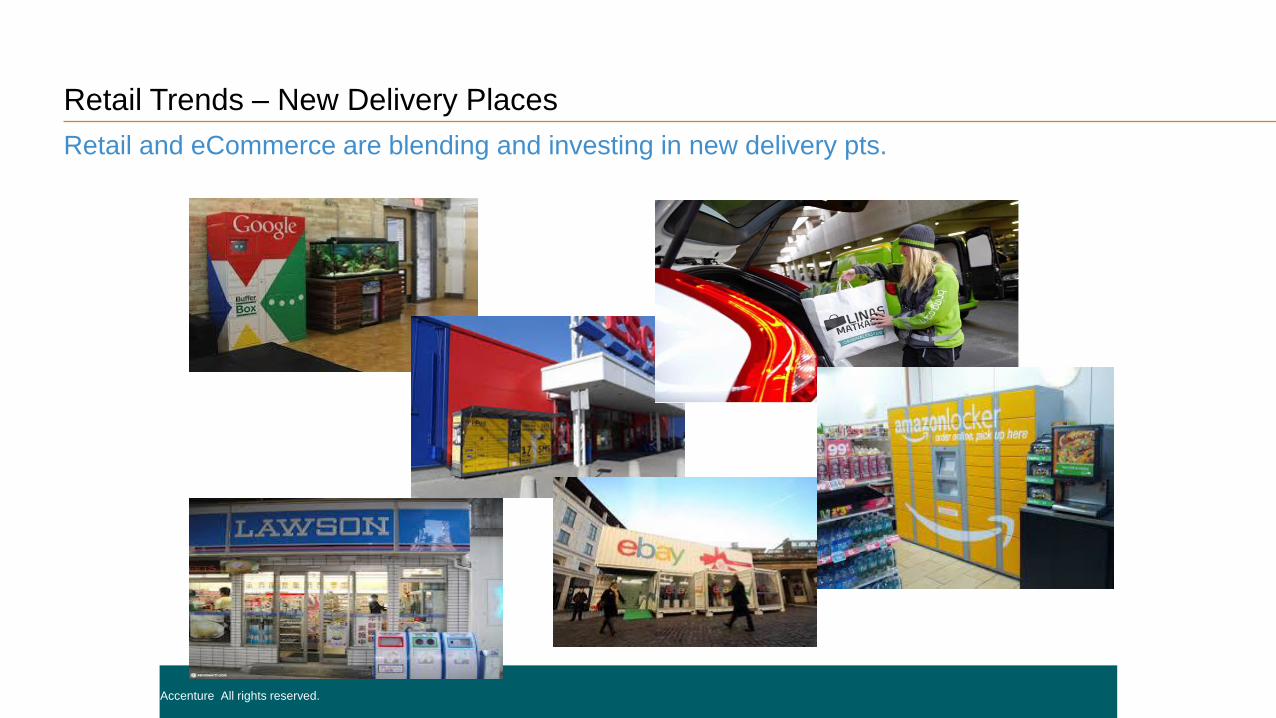

Retail Trends – New Delivery Places

Retail and eCommerce are blending and investing in new delivery pts.

Copyright © 2015 Accenture All rights reserved.

35

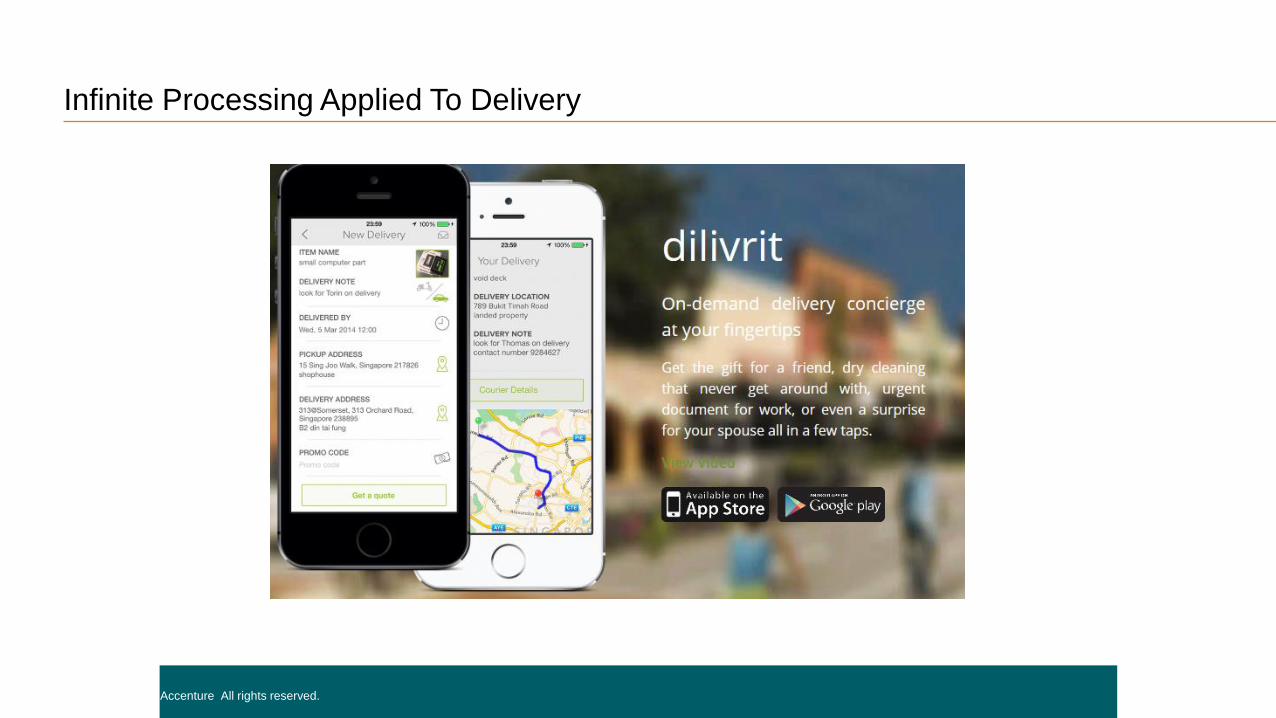

Infinite Processing Applied To Delivery

Copyright © 2015 Accenture All rights reserved.

36

New Models Now Possible

New entrants have an entirely different cost structure.

Copyright © 2015 Accenture All rights reserved.

Sourcing Spare Capacity

Rapid Scale (Up and Down)

Technology Enabled

Focused On Last Mile (For Now)

37

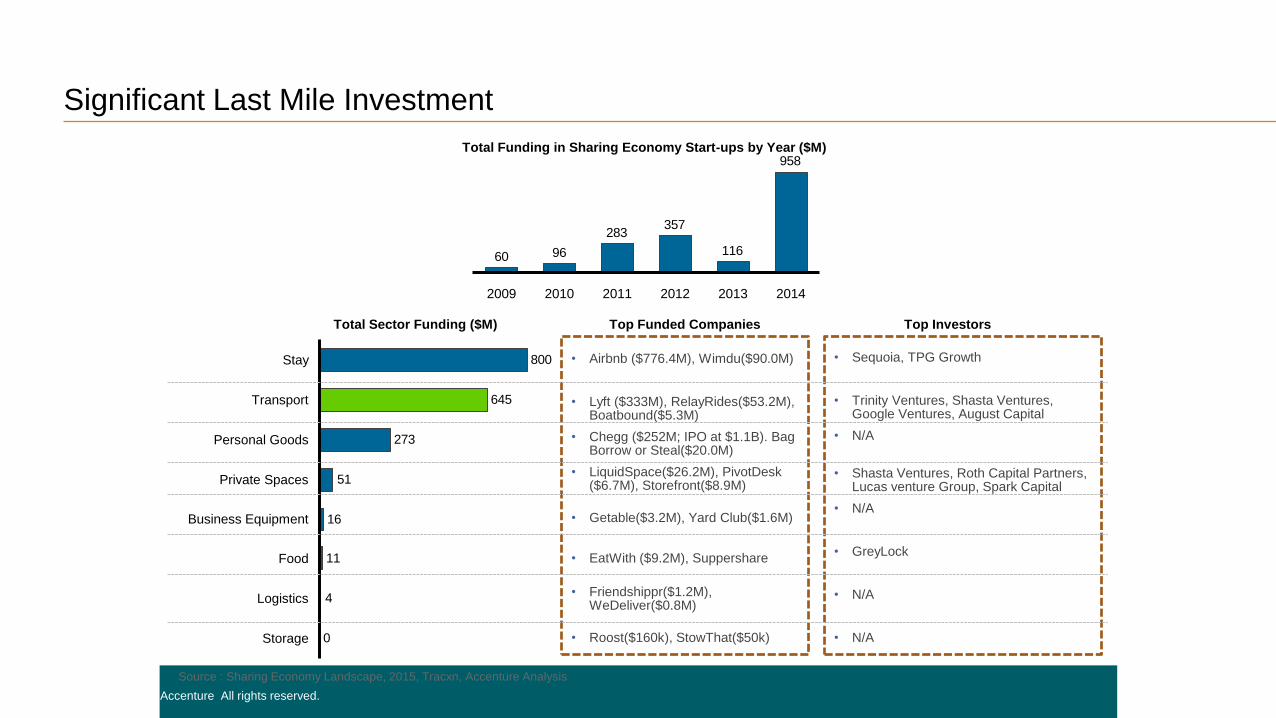

Significant Last Mile Investment

Copyright © 2015 Accenture All rights reserved.

Source : Sharing Economy Landscape, 2015, Tracxn, Accenture Analysis

958

116

357283

9660

2013 20142009 2010 2011 2012

Total Funding in Sharing Economy Start-ups by Year ($M)

0

4

11

16

51

273

645

800

Storage

Logistics

Stay

Transport

Personal Goods

Private Spaces

Food

Business Equipment

Total Sector Funding ($M)

• Airbnb ($776.4M), Wimdu($90.0M)

• Lyft ($333M), RelayRides($53.2M), Boatbound($5.3M)

• Chegg ($252M; IPO at $1.1B). Bag Borrow or Steal($20.0M)

• LiquidSpace($26.2M), PivotDesk($6.7M), Storefront($8.9M)

• Getable($3.2M), Yard Club($1.6M)

• EatWith ($9.2M), Suppershare

• Friendshippr($1.2M), WeDeliver($0.8M)

• Roost($160k), StowThat($50k)

• Sequoia, TPG Growth

• Trinity Ventures, Shasta Ventures, Google Ventures, August Capital

• N/A

• Shasta Ventures, Roth Capital Partners, Lucas venture Group, Spark Capital

• N/A

• GreyLock

• N/A

• N/A

Top Funded Companies Top Investors

38

Significant Last Mile Investment

Copyright © 2015 Accenture All rights reserved.

Local

Deliveries

Storage

Crowd

Shipping

39

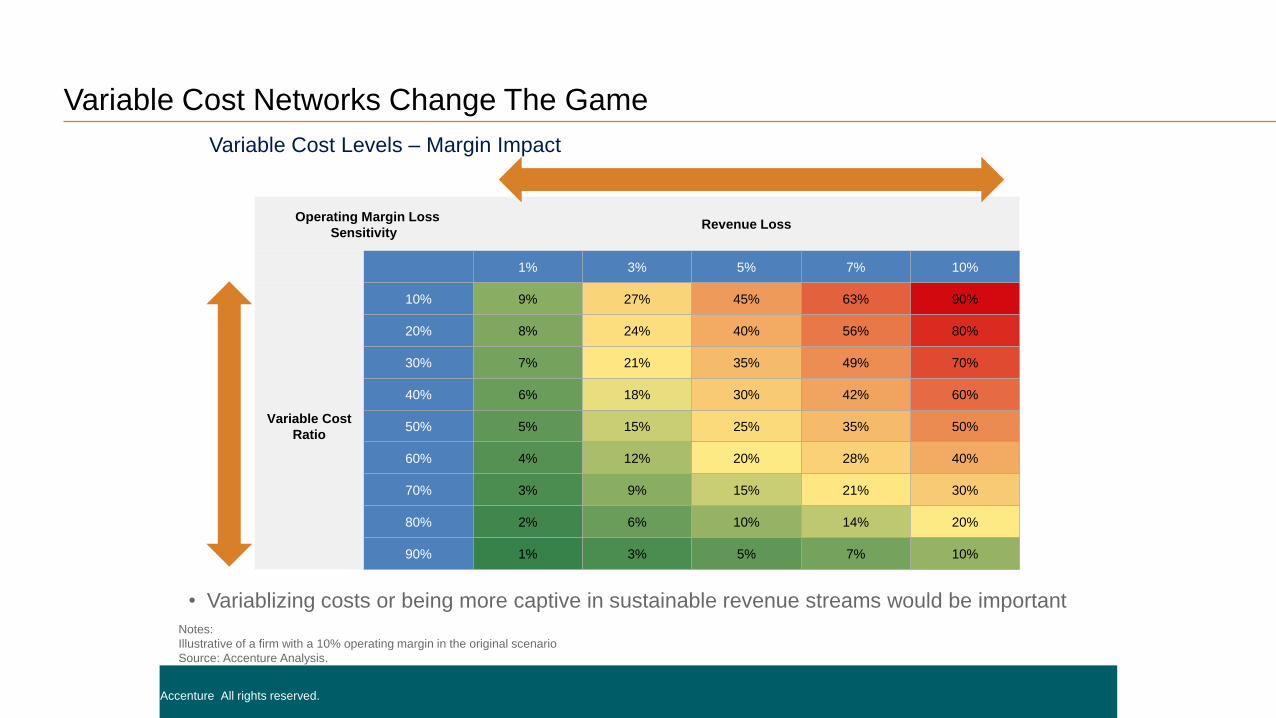

Variable Cost Networks Change The Game

Copyright © 2015 Accenture All rights reserved.

Variable Cost Levels – Margin Impact

Notes:

Illustrative of a firm with a 10% operating margin in the original scenario

Source: Accenture Analysis.

• Variablizing costs or being more captive in sustainable revenue streams would be important

Operating Margin Loss

SensitivityRevenue Loss

1% 3% 5% 7% 10%

Variable Cost

Ratio

10% 9% 27% 45% 63% 90%

20% 8% 24% 40% 56% 80%

30% 7% 21% 35% 49% 70%

40% 6% 18% 30% 42% 60%

50% 5% 15% 25% 35% 50%

60% 4% 12% 20% 28% 40%

70% 3% 9% 15% 21% 30%

80% 2% 6% 10% 14% 20%

90% 1% 3% 5% 7% 10%

We Are In The Singularity

Copyright © 2014 Accenture All rights reserved. 40

The Singularity The BigBang

The BigCrunch

Entropy

41

What Is Better?

Copyright © 2015 Accenture All rights reserved.

Faster Delivery

New Value Added Services

Convenience Is King

42

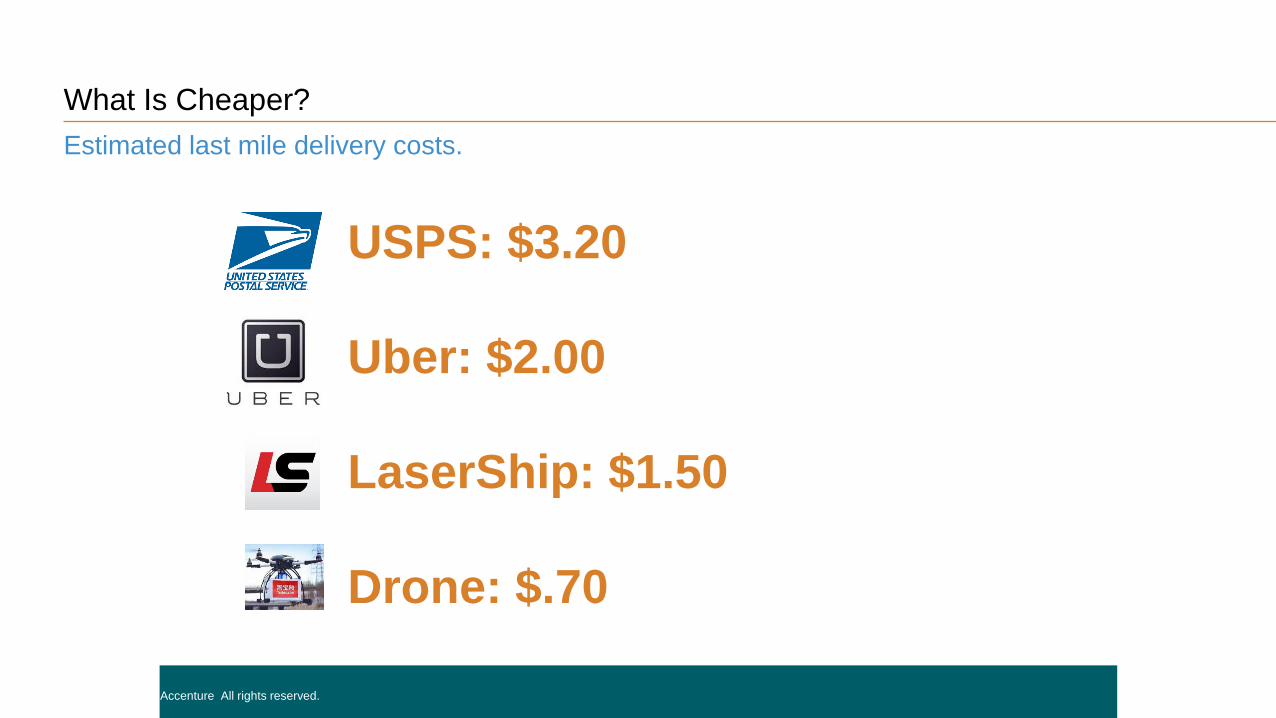

What Is Cheaper?

Copyright © 2015 Accenture All rights reserved.

USPS: $3.20

Uber: $2.00

LaserShip: $1.50

Drone: $.70

Estimated last mile delivery costs.

43

What Is More Personal?

Copyright © 2015 Accenture All rights reserved.

When I Want It

Where I Want It

Completely Transparent

Fully Within My Control

44

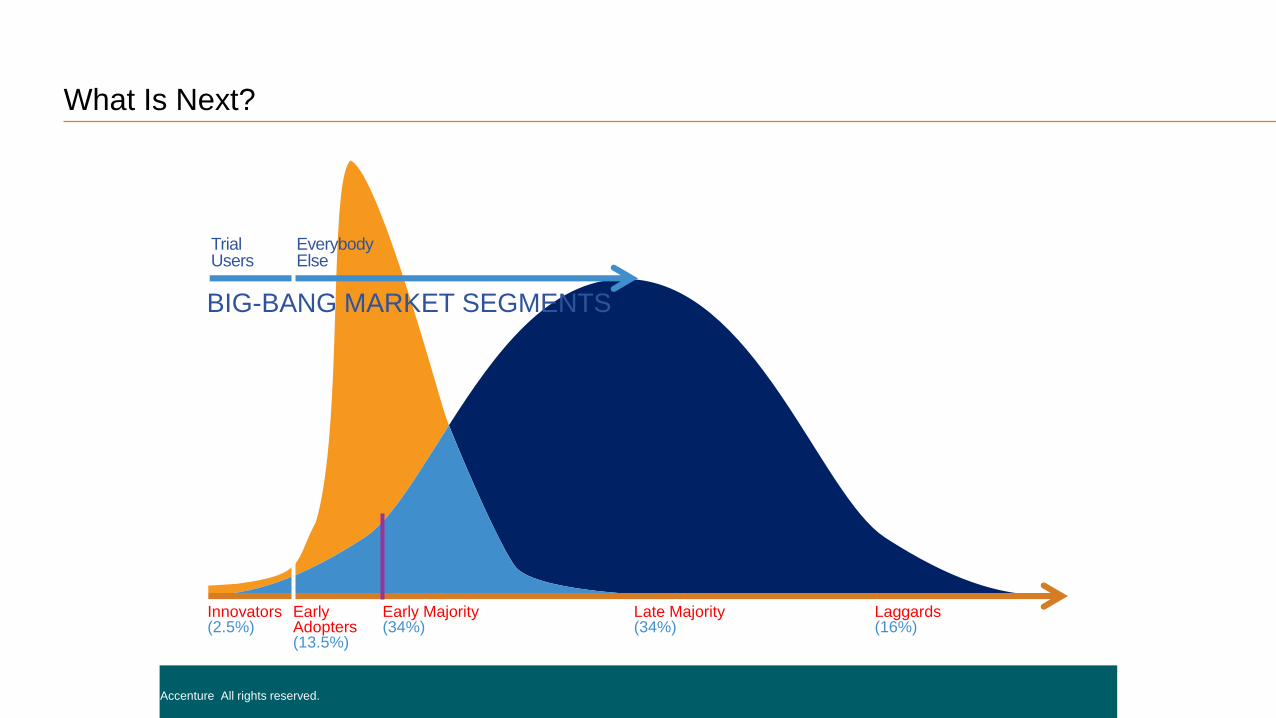

What Is Next?

Copyright © 2015 Accenture All rights reserved.

Trial Users

Everybody Else

Innovators(2.5%)

Early Adopters (13.5%)

Early Majority (34%)

Late Majority (34%)

Laggards(16%)

BIG-BANG MARKET SEGMENTS

45© 2015 InfoTrends www.infotrends.com© 2015 InfoTrends

The Future of DeliveryPrepared for PostalVision 2020/5.0

Matt SwainDirectorMarch 10, 2015

46© 2015 InfoTrends www.infotrends.com

47© 2015 InfoTrends www.infotrends.com

Focus Group Locations

48© 2015 InfoTrends www.infotrends.com

Focus Group Participants(A Sample)

49© 2015 InfoTrends www.infotrends.com

Residential delivery location and the number of delivery days represented the most

likely areas for compromise.

Seven Key Research Highlights

5

4

3

2

1

7

6

The majority of participants did not realize that the Postal Service is self-funded.

Most participants valued the Postal Service as a community asset.

Reducing hours of operations should not be a primary focus for cost saving efforts.

Some participants saw value in the Postal Service introducing new products

or services at post offices.

Most participants were hesitant about the Postal Service providing digital services.

Nearly every participants cited that they would be negatively affected if the Postal

Service ceased to exist, but had trouble articulating how they would be affected.

50© 2015 InfoTrends www.infotrends.com

Residential delivery location and the number of delivery days represented the most likely areas for compromise.

51© 2015 InfoTrends www.infotrends.com

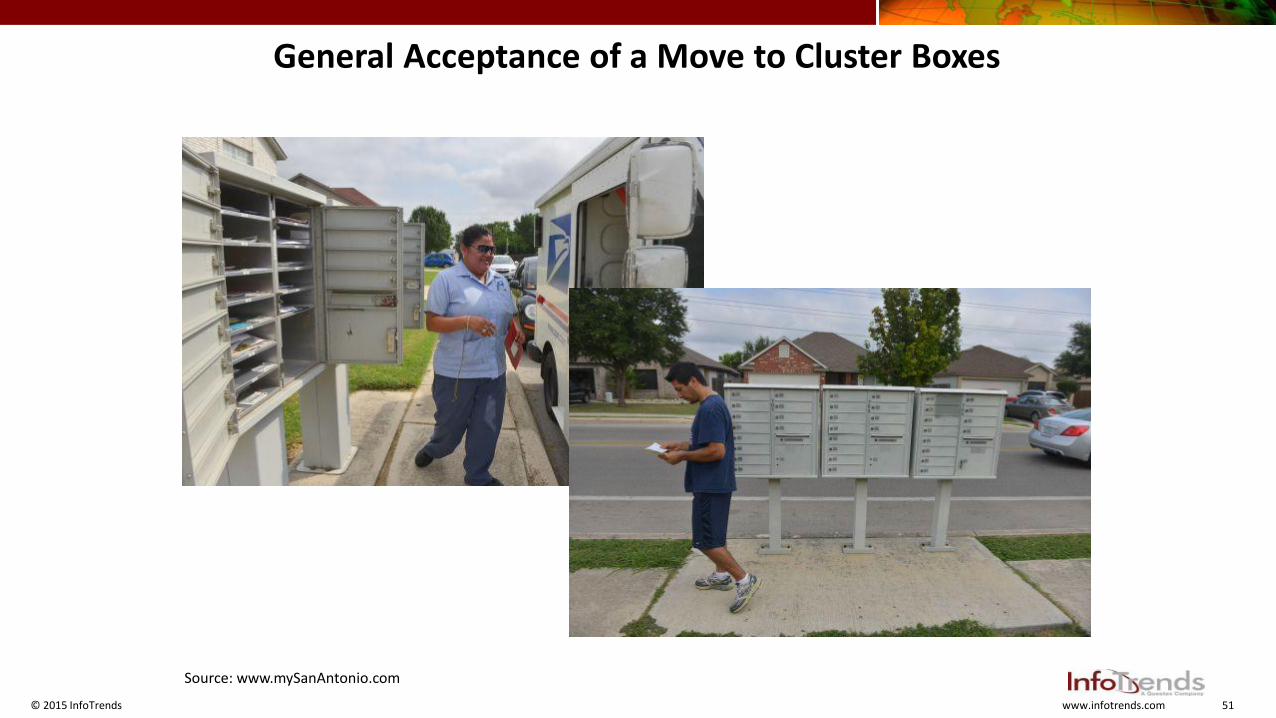

General Acceptance of a Move to Cluster Boxes

Source: www.mySanAntonio.com

52© 2015 InfoTrends www.infotrends.com

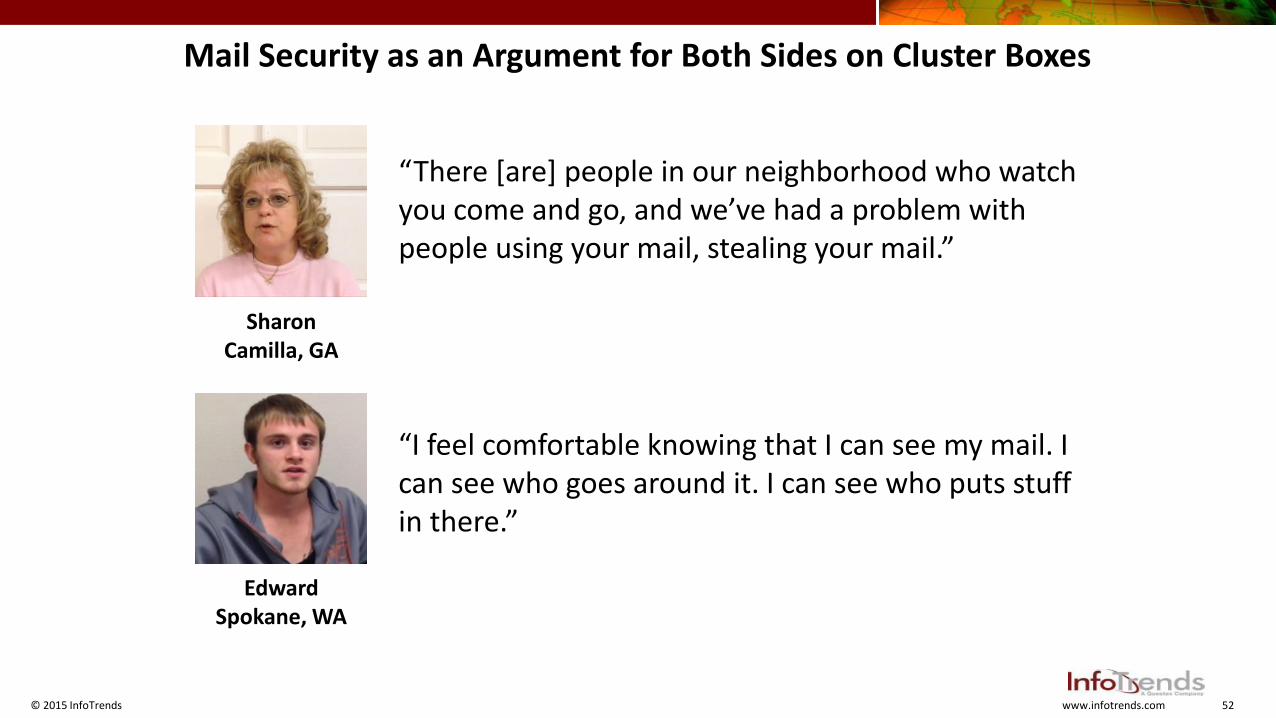

“There [are] people in our neighborhood who watch you come and go, and we’ve had a problem with people using your mail, stealing your mail.”

“I feel comfortable knowing that I can see my mail. I can see who goes around it. I can see who puts stuff in there.”

SharonCamilla, GA

EdwardSpokane, WA

Mail Security as an Argument for Both Sides on Cluster Boxes

53© 2015 InfoTrends www.infotrends.com

New Consumer Research, Including Insight on Cluster box

• InfoTrends conducted research on behalf of the USPS OIG

• Research timeline was August 2014 – September 2014

• 5,000 respondents in the United States

− Aligned age, gender, and geography by U.S. Census data

− 4,500 from web surveys, 500 from phone surveys

• 88% had Internet access at home

• This is a preview of a subset of the data, which will publish in a USPS OIG report later this year

54© 2015 InfoTrends www.infotrends.com

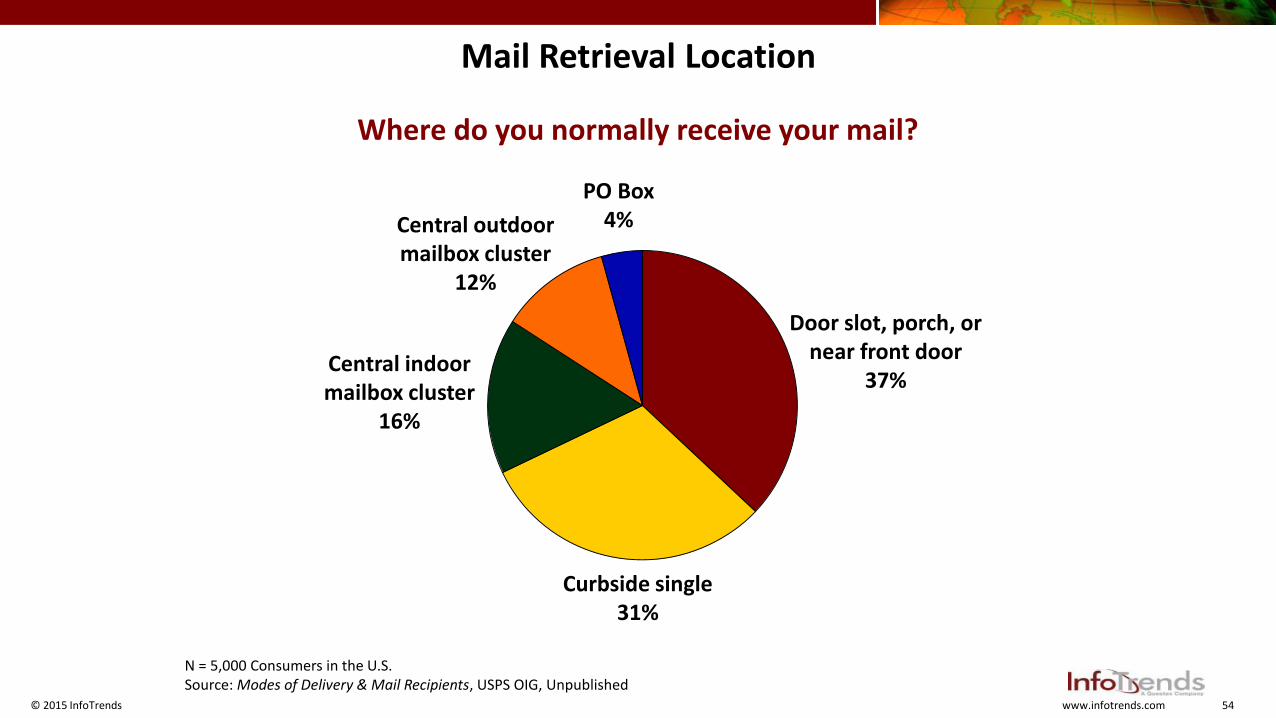

Mail Retrieval Location

Where do you normally receive your mail?

N = 5,000 Consumers in the U.S.Source: Modes of Delivery & Mail Recipients, USPS OIG, Unpublished

Central indoor mailbox cluster

16%

Central outdoor mailbox cluster

12%

PO Box4%

Door slot, porch, or near front door

37%

Curbside single31%

55© 2015 InfoTrends www.infotrends.com

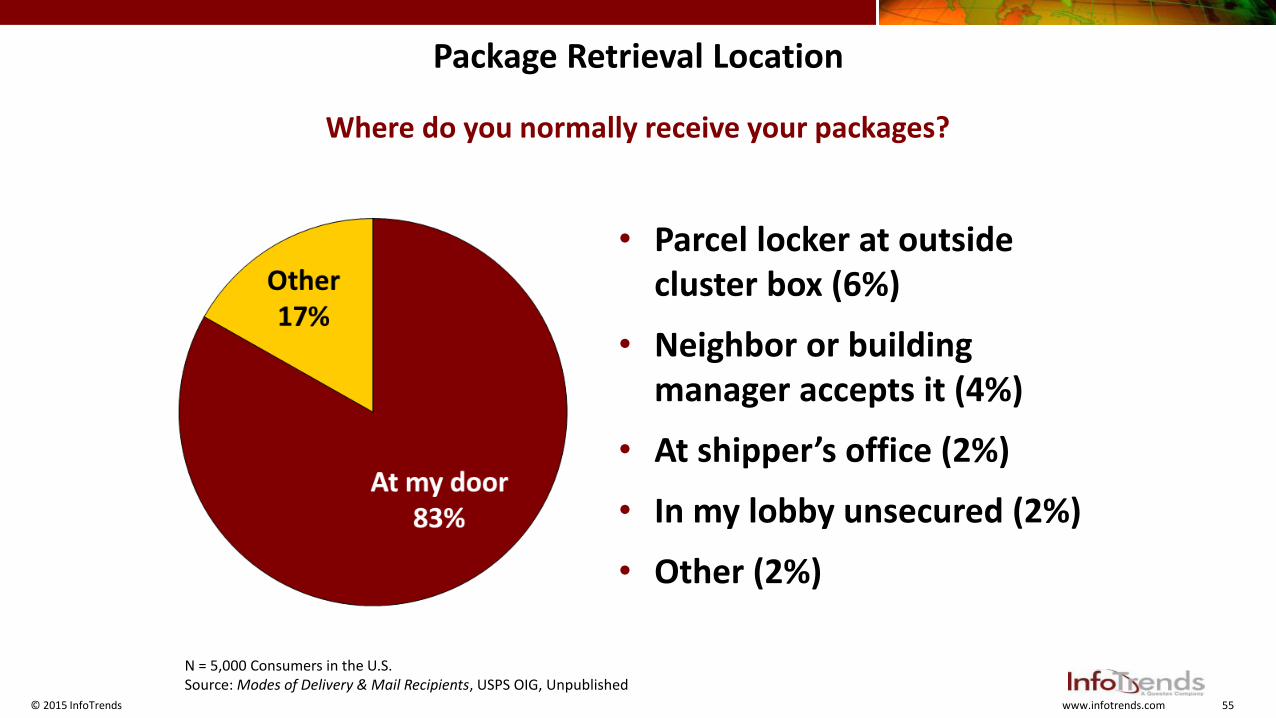

Package Retrieval Location

Where do you normally receive your packages?

• Parcel locker at outside cluster box (6%)

• Neighbor or building manager accepts it (4%)

• At shipper’s office (2%)

• In my lobby unsecured (2%)

• Other (2%)

N = 5,000 Consumers in the U.S.Source: Modes of Delivery & Mail Recipients, USPS OIG, Unpublished

56© 2015 InfoTrends www.infotrends.com

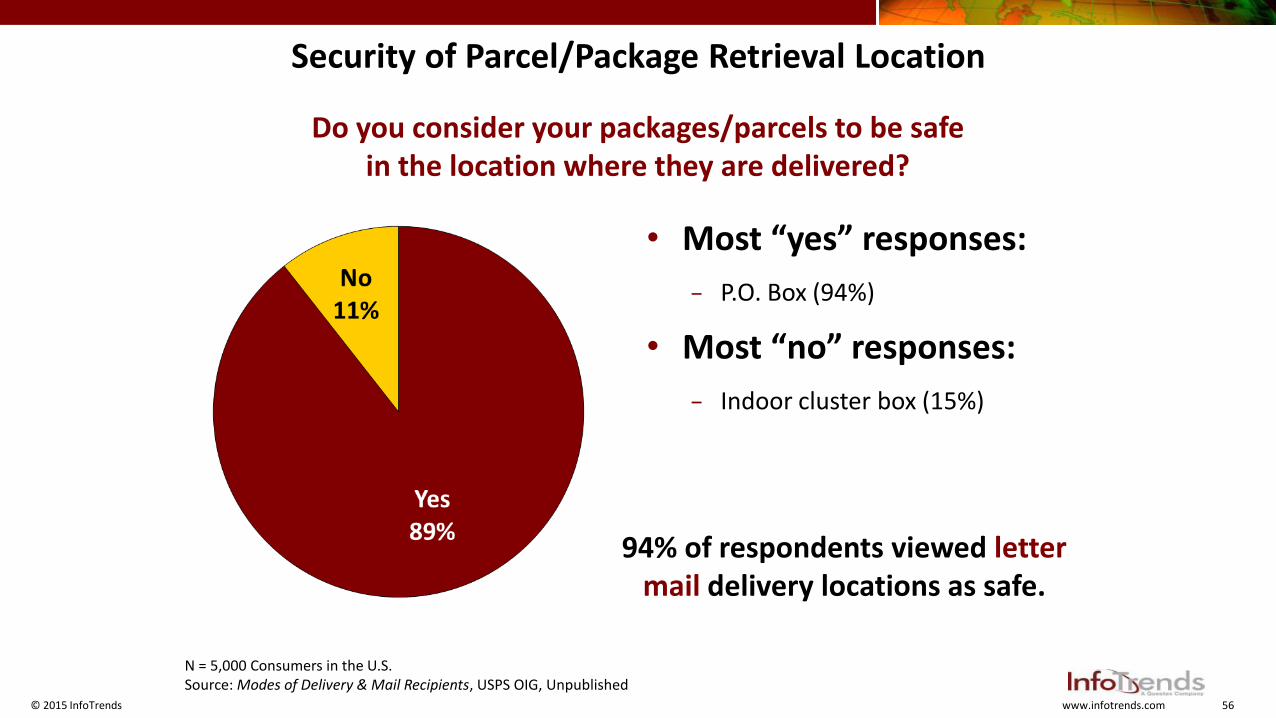

Security of Parcel/Package Retrieval Location

Do you consider your packages/parcels to be safe in the location where they are delivered?

• Most “yes” responses:

− P.O. Box (94%)

• Most “no” responses:

− Indoor cluster box (15%)

94% of respondents viewed letter mail delivery locations as safe.

N = 5,000 Consumers in the U.S.Source: Modes of Delivery & Mail Recipients, USPS OIG, Unpublished

57© 2015 InfoTrends www.infotrends.com

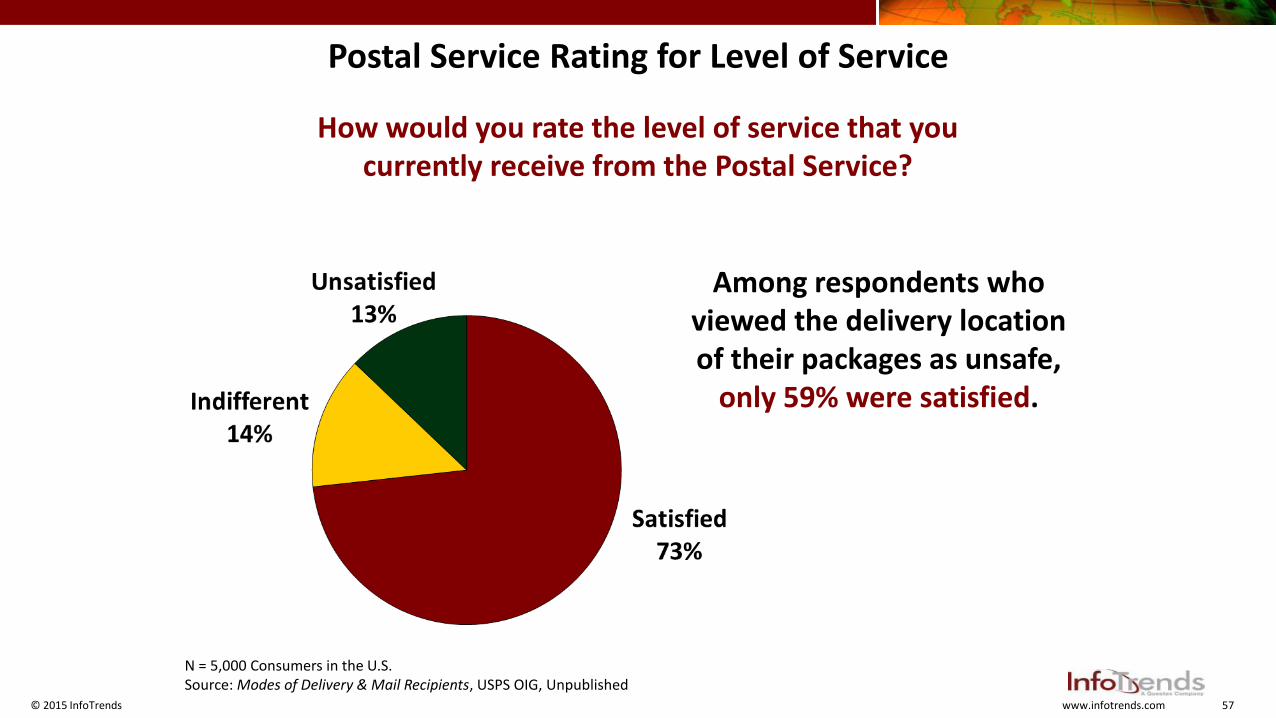

Postal Service Rating for Level of Service

How would you rate the level of service that you currently receive from the Postal Service?

Among respondents who viewed the delivery location of their packages as unsafe,

only 59% were satisfied.

N = 5,000 Consumers in the U.S.Source: Modes of Delivery & Mail Recipients, USPS OIG, Unpublished

58© 2015 InfoTrends www.infotrends.com

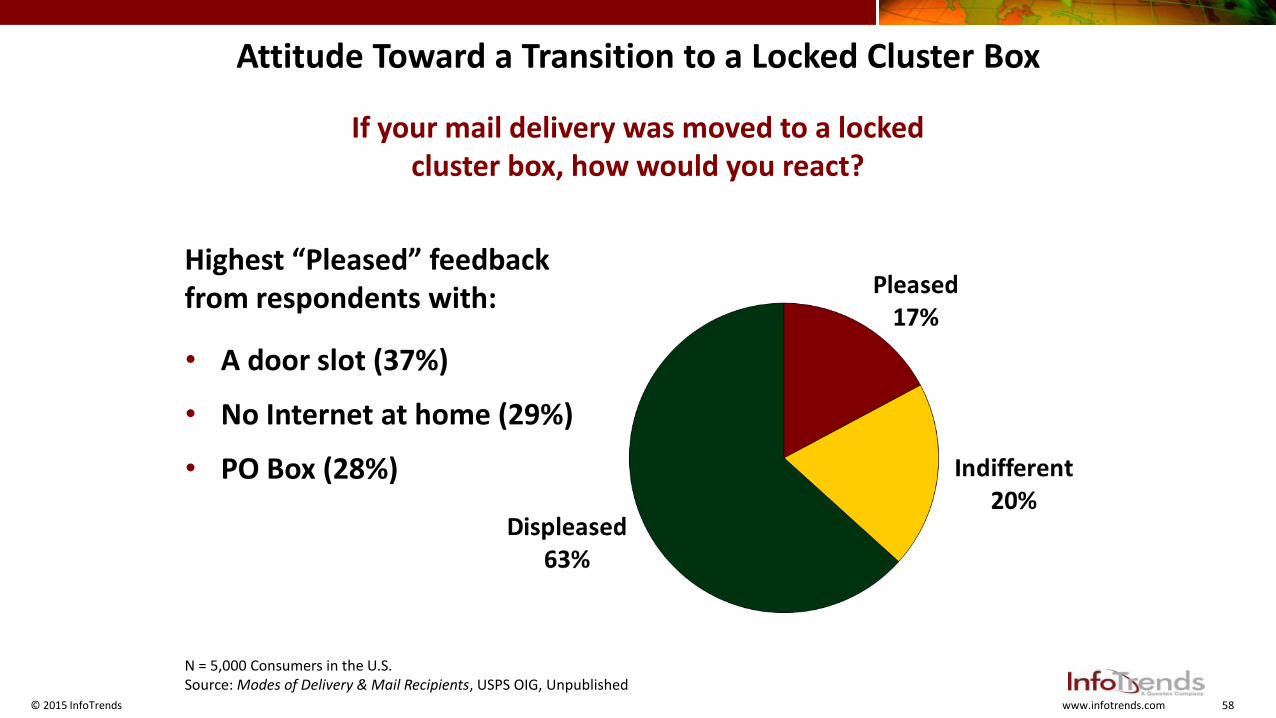

Attitude Toward a Transition to a Locked Cluster Box

If your mail delivery was moved to a locked cluster box, how would you react?

Highest “Pleased” feedback from respondents with:

• A door slot (37%)

• No Internet at home (29%)

• PO Box (28%)

N = 5,000 Consumers in the U.S.Source: Modes of Delivery & Mail Recipients, USPS OIG, Unpublished

59© 2015 InfoTrends www.infotrends.com

Sample of Attending Organizations

• Association of Magazine Media

• Canada Post

• Greeting Card Association

• National Association of Letter Carriers

• National Association of Presort Mailers

• National Postal Policy Council

• Parcel Shippers Association

• U.S. Postal Service

• Valassis

• American Catalog Mailers Association

• Publishers Clearing House

• Posti

• WIK

60© 2015 InfoTrends www.infotrends.com

Key Themes from the Round Table Discussion

• We can learn from international implementations for cluster box delivery (e.g., what worked and where messaging/approach needed to be adjusted)

• Some people raised concerns about reducing Postal employee interaction with consumers and thus reducing the USPS competitive advantage

• Community cluster boxes will need to be designed to accommodate for the age of eCommerce, with an expectation for more (larger) parcels being delivered

Gary Reblin

VP, New Products & Innovation

Unite States Postal Service

United States Postal Service

Evolving now to meet tomorrow’s needs

20

4

37

0

What will e-Commerce be like in the year 2020?

• Ecommerce Forecast to Keep Growing

- $200 billion market today

- Growing at five times the rate of traditional retailing

- Projected to be 15% of total retail sales1

(Today 8%)

• More nimble warehousing

- Smaller warehouses

- Ship from store

- Distribution capable

• Same-Day Delivery will be more common

• New entrants in market place affect consumer expectations

- Leisure and Regional ShippersSource: Quora.com

20

4

37

0

What will shopping be like in the year 2020?

• Shopping evolves to offer more stores that take advantage show rooming trend

- Blend of Brick and Mortar and e-Commerce

Source: 1WSJ

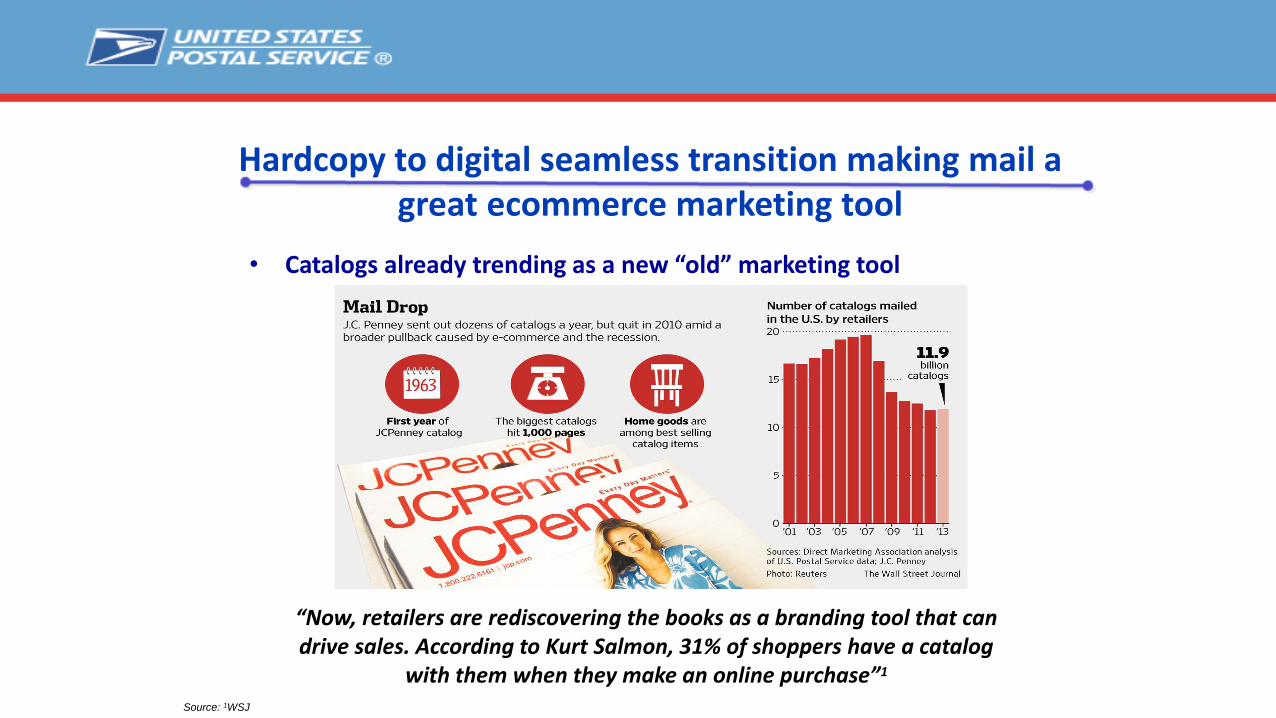

Hardcopy to digital seamless transition making mail a great ecommerce marketing tool

• Catalogs already trending as a new “old” marketing tool

“Now, retailers are rediscovering the books as a branding tool that can drive sales. According to Kurt Salmon, 31% of shoppers have a catalog

with them when they make an online purchase”1

Growing Consumer

Expectations

Consumers’ busy lifestyles demand more delivery convenience

New businesses take notice of these demands and offer more expedient deliveries

Existing players improve their offerings to meet

demand

These changes set new

consumer expectations

Changing Shipping Environment

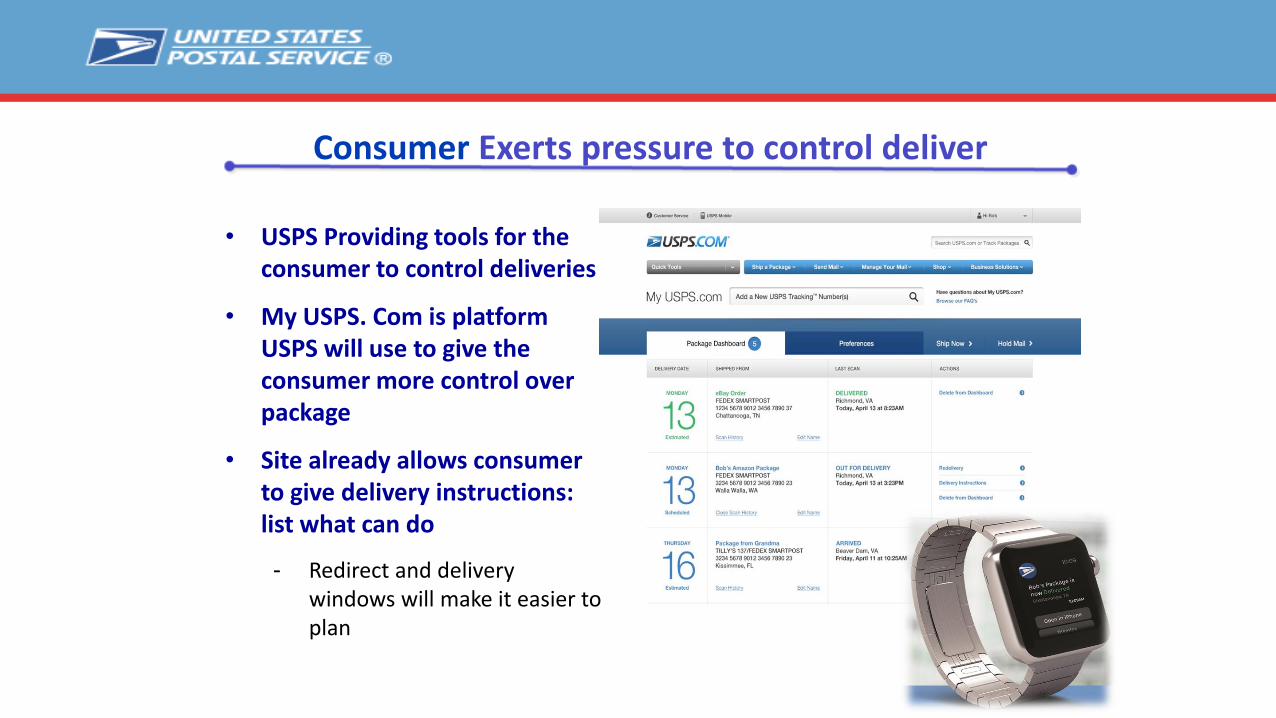

• USPS Providing tools for the consumer to control deliveries

• My USPS. Com is platform USPS will use to give the consumer more control over package

• Site already allows consumer to give delivery instructions: list what can do

- Redirect and delivery windows will make it easier to plan

Consumer Exerts pressure to control deliver

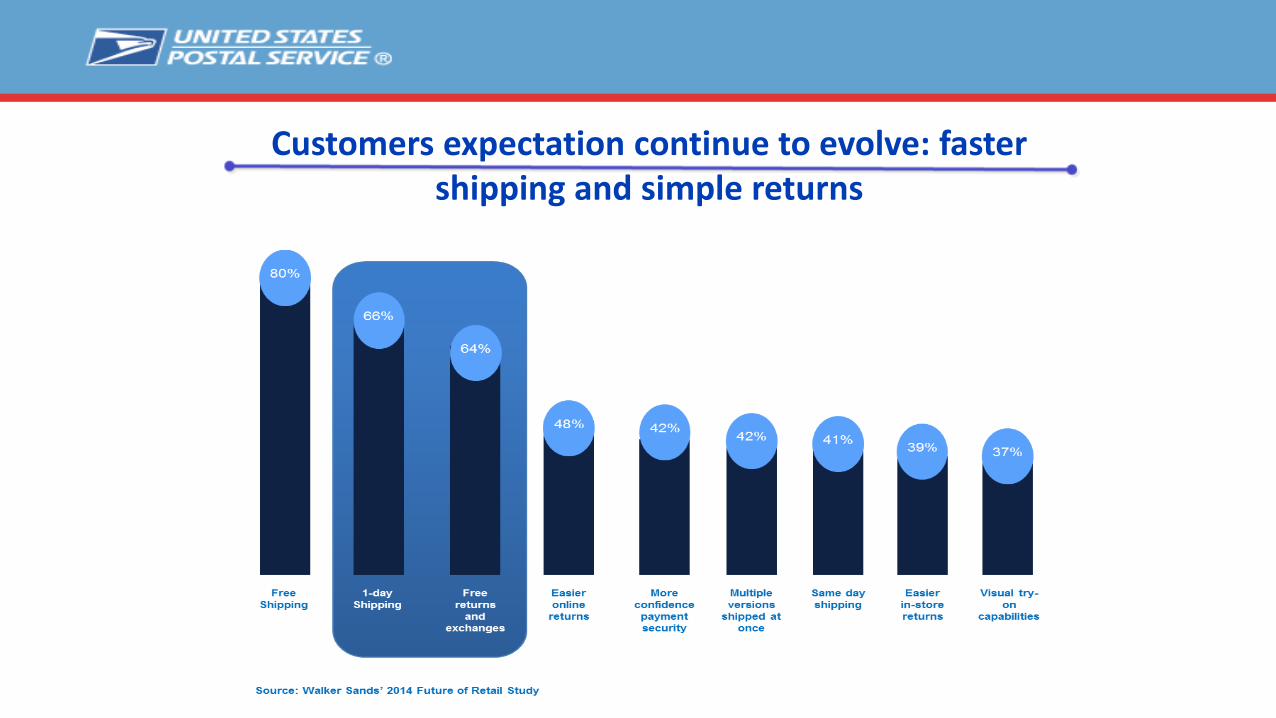

Customers expectation continue to evolve: faster shipping and simple returns

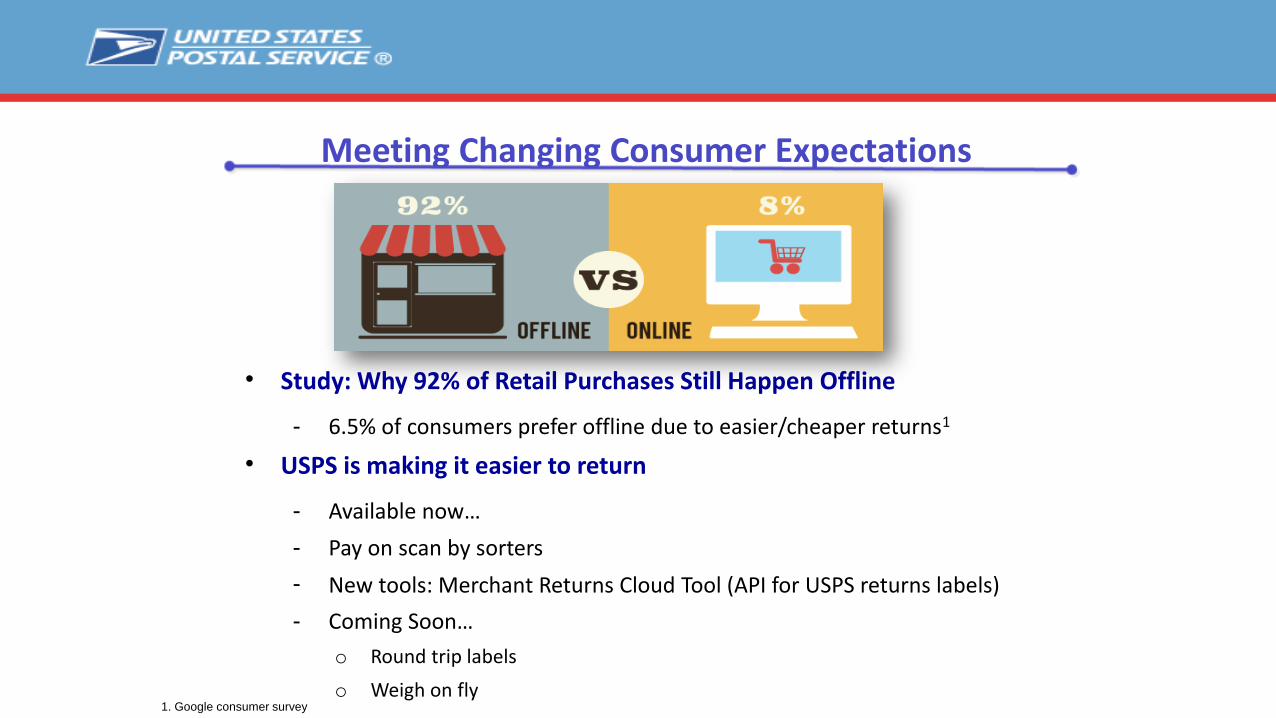

• Study: Why 92% of Retail Purchases Still Happen Offline

- 6.5% of consumers prefer offline due to easier/cheaper returns1

• USPS is making it easier to return

- Available now…

- Pay on scan by sorters

- New tools: Merchant Returns Cloud Tool (API for USPS returns labels)

- Coming Soon…

o Round trip labels

o Weigh on fly

Meeting Changing Consumer Expectations

1. Google consumer survey

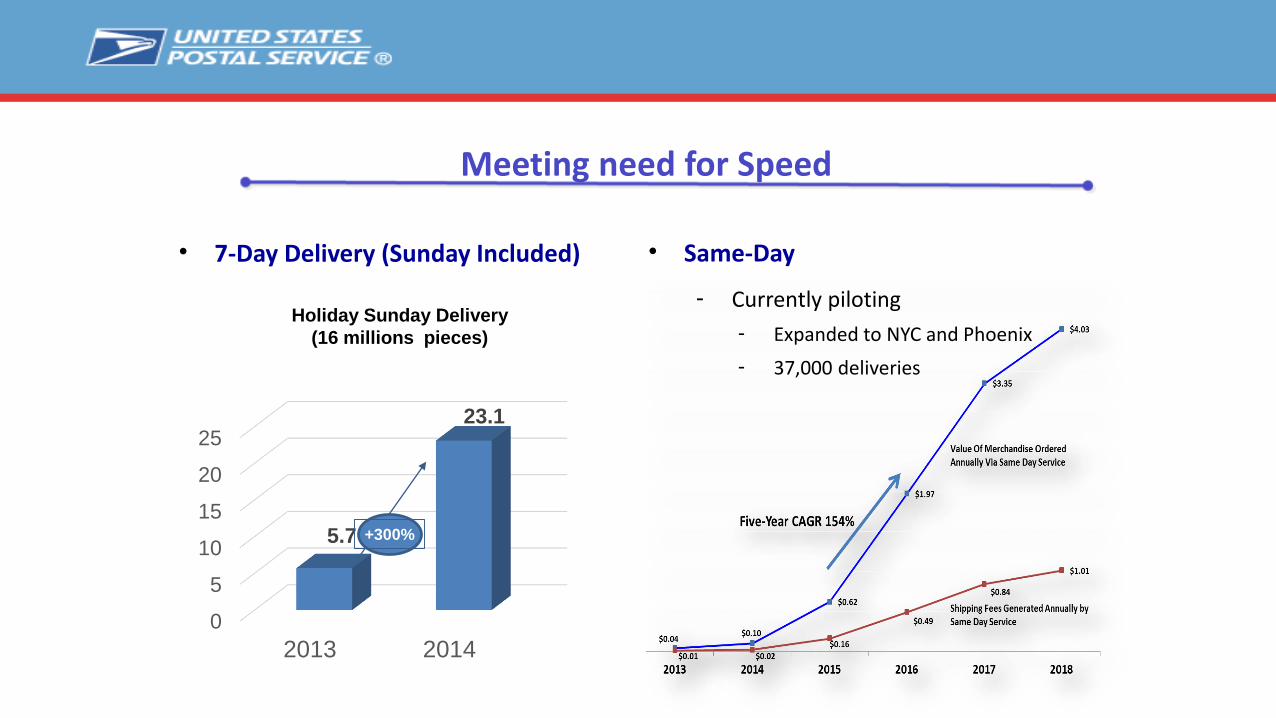

• 7-Day Delivery (Sunday Included)

Meeting need for Speed

0

5

10

15

20

25

2013 2014

5.7

23.1

+300%

Holiday Sunday Delivery

(16 millions pieces)

• Same-Day

- Currently piloting

- Expanded to NYC and Phoenix

- 37,000 deliveries

• Opening New Markets

- Expanding delivery around our core

o Pre-dawn grocery deliveryo Pilot Location:

- San Francisco

- San Diego (March 4)

- Los Angeles (March 9)

o Dynamic routing

- Scan and sort totes to

route/sequence order

What’s on the horizon for Delivery

Q & A