Embed Size (px)

Citation preview

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 1/79

1

A

PROJECT ON

“E-BANKING ON HDFC BANK”

SUBMITTED TO

THE UNIVERSITY OF MUMBAI

IN PARTIAL FULFILLMENT FOR THE AWARD OF

THE DEGREE OF BACHELOR OF COMMERCE

(BANKING AND INSURANCE)

SEMESTER V

(SEAT NO: 12013)

BY

BHARAT R. SIRVEE

THE S.I.A COLLEGE OF HIGHER EDUCATION

2014-2015

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 2/79

2

DECLARATION BY THE RESERCH STUDENT

I hereby declare that this project titled “E-BANKING ON HDFC BANK ”.

Submitted by me is based on actual work carried out by me under the guidance andsupervision of MR.HASIT NAGARIYA.

Any reference to work done by any other person or institution or any

material obtained from other sources have been duly citied and reference.

It is in future to state that this work is not submitted anywhere else for any

examination.

S.I.A COLLEGE OF HIGHER EDUCATION

SIGNATURE OF STUDENT

(BHARAT R SIRVEE)

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 3/79

3

ACKOWLEDGEMENT

I am thankful to Professor MR. HASIT NAGARIYA for her

valuable guidance in successful completion of this project.

My overriding debt due to our Principal Dr. PADAMAJA ARVIND

and librarian MRS.BHARATI RAO.

Last but not the least I cannot forget my friends and my parents

whose constant encouragement and support made this task a happy job.

SIGNATURE

BHARAT R SIRVEE

(THIRD YEAR BACHELOR OF COMMERCE)

(BANKING AND INSURANCE)

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 4/79

4

The SIA College Of Higher Education.

P88, MIDC Residential Area Dombivli Gymkhana Road,

Near BalajiMandir, Dombivli (East).421 203.

Email: [email protected]

CERTIFICATE

This is to certify that,

Mrs. BHARAT R SIRVEE

Student of BCOM (Banking and Insurance V) 2013-2014

Seat No.12013 has successfully completed his Project

Work on E-BANKING ON HDFC BANK under the

guidance of MR. HASIT NAGARIYAas per Mumbai University

syllabus.

COURSE CO-ORDINATOR PROJECT GUIDE

EXTERNAL EXAMINER PRINCIPAL

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 5/79

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 6/79

6

PREFACE

With the rapid globalization of the Indian economy, enterprises are facing with

ever changing competitive environment. Enterprises are adopting strategies aimed

at developing competitive advantage based on enhanced customer value in terms of

product differentiation, quality, speed, service and costs. In the post liberalization

era, with the deregulation of Indian economy, the financial service sector

witnessing a complete metamorphosis and technology is playing a very significant

role in this record. Over the last decade India has been one of the fastest adopters

of information technology, particularly because of its capability to provide

software solution to organizations around the world. This capability has provided a

tremendous impetuous to the domestic banking industry in India to deploy the

latest in technology, particularly in the Internet banking and e-commerce arenas.

Banks are growing in size by mergers and acquisitions, which have been driven by

communication and technology. Technology is playing a major role in increasing

the efficiency, courtesy and speed of customer service. It is said to be the age of E-

banking.

An Online Banking user is expected to perform at least one of the following

transactions online:

1. Checking account balance and transaction history

2. Paying bills

3. Transferring funds between accounts

4. Requesting credit card advances

5. Ordering checks

6. Managing investments and stocks trading

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 7/79

7

From a bank’s perspective, using the Internet is more efficient than using other

distribution mediums because banks are looking for an increased customer base.

Using multiple distribution channels increases effective market coverage by

enabling different products to be targeted at different demographic segments. Also

Banks cannot risk loosing customers to competitors within the aggressive

competition in the banking industry around the world. Moreover Internet delivery

offers customized service to suit the needs and the likes of each user. Mass

customization happens effectively through Online Banking. It reduces cost and

replaces time spent on routine errands with spending time on business errands.

Online Banking means less staff members, smaller infrastructure demands,

compared with other banking channels. From the customers’ perspective, Online

Banking provides a convenient and effective way to manage finances that is easily

accessible 24 hours a day, seven days a week. In addition information is up to date.

Nevertheless Online Banking has disadvantages for banks like how to work the

technology, set-up cost, legal issues, and lack of personal contact with customers.

And for customers there are security and privacy issues.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 8/79

8

About the project

Title of study

The present study titled in E-BANKING. The study is made by reference to E-

BANKING services given to customer

Object of the study

To study the E-banking services in detail.

To study of awareness of E-banking services among the customer of HDFC

BANK.

To study the customer satisfaction relating to the E-banking services.

To completely study of E-banking provided by HDFC BANK

DATA AND METHODOLOGY

For the purpose of the present study, both primary as well as secondary data were

used.

Primary data is collected through questionnaire from 30 customer to understand

the awareness abut the E-banking. Sample was randomly selected.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 9/79

9

INDEX

Chapter

No.

Topic PAGE NO.

1 INTRODUCATION

2 HISTORY OF HDFC BANK

3 BUSINESS OF HDFC BANK

4 FACILITIES PROVIDED BY HDFC BANK

5 E-BANKING FACILITIES PROVIDED BY

HDFC BANK

6 IMPORTANCE OF E-BANKING FACILITY

7 E- BANKING SERVICES

8 BENEFITS/CONCERNS OF E-BANKING

9 NEWS AND ARTICLES

10 RESEARCH AND METHODLOGY

11 ANAYLISIS AND INTERPRITAION

12 CONCLUSION

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 10/79

10

Chapter 1

Introduction

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 11/79

11

INTRODUCTION

Internet banking (or E-banking) means any user with a personal computer and a browser can get connected to his bank-s website to perform any of the virtual

banking functions. In Internet banking system the bank has a centralized database

that is web-enabled.

Internet banking can be defined as a facility provided by banking and financial

institutions, that enable the user to execute bank related transactions through

Internet. The biggest advantage of Internet banking is that people can expend the

services sitting at home, to transact business.

Internet banking basically allows you to be able to do everything that you can in

your regular banking institution, only with the benefit that you can do it all right

from the convenience of your own home. You can be comfortable and have peace

of mind knowing that you can keep track yourself of all your banking issues.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 12/79

12

History

The concept of Internet banking has been simultaneously evolving with the

development of the World Wide Web. Programmers working on banking databases

came up with ideas for online banking transactions, some time during the 1980's.

The creative process of development of these services was probably sparked off

after many companies started the concept of online Shopping.

Sometime in 1980's, banking and finance organizations in Europe and United

States started suggestive researches and programming experiments on the concept

of 'home banking'.

In 1983, the Nottingham Building Society, commonly abbreviated and refereed to

as the NBS, launched the first Internet banking service in United Kingdom.

Stanford Federal Credit Union introduced the first online banking service in United

States, in October 1994, which is a financial institution.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 13/79

13

Indian scenario

As this is a time of globalization customer are getting change adapting more

upgraded technology in their life, in this busy schedule everyone is looking for a

time saving process And it’s been come in a way of ―Internet banking‖.

As Internet banking is booming now a days as a delivery of banking services and

strategic tool for business development, has gained wide acceptance internationally

and is fast catching up in India with more and more banks entering the fray.

At present, the total Internet users in the country are estimated at 1crore. Only

about 1% of Internet users did banking online in 1998. This increased to 20.7% in

March 2000.

Costs of banking service through the Internet form a fraction of costs through

conventional methods. Rough estimates assume teller cost at Re.1 per transaction,

ATM transaction cost at 45paisa, phone banking at 35paisa, debit cards at 20paise

and Internet banking at 10paise per transaction.

Some of the banks permit customers to interact with them and transact

electronically with them. Such services include request for opening of accounts,

requisition for cheque books, stop payment of cheques, viewing and printing

statements of accounts, movement of funds between accounts within the same

bank, querying on status of requests, instructions for opening of Letters of Credit

and Bank Guarantees etc. HDFC Bank Ltd. has made e shopping online and real

time with the launch of its payment gateway.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 14/79

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 15/79

15

Definition of E-BANKING

Definition:A Banking company is defined as a company, which transacts the business of

banking in India.

As per Banking Regulation Act 1949 Section 5(b)

"Banking means, accepting for the purpose of lending or investment, of deposits of

money from the public, repayable on demand or otherwise, and withdrawal by

cheque, draft, or otherwise."

According to Sir John Paget

"No person or body, corporate or otherwise can be a banker who does not, (a) take

deposits accounts, (b) take current accounts, (c) issue and pay cheques, (d) collect

cheques, crossed and uncrossed, for his customers."In simple words we can say

that bank is a financial institution which deals in money and credit by obtaining

deposits from public and giving loans and credit to trade and industrial

respectively. "

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 16/79

16

Chapter 2

INTRODUCTION

TO HDFC BANK

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 17/79

17

HDFC COMPANY PROFILE

HDFC BANK LTD

Type Private

Founded 1994

Headquarters HDFC Bank Ltd.,

Mumbai, India

Industry Banking Insurance

Capital Markets and allied industries

Products Loans, Credit Cards, Savings,

Investment vehicles Insurance etc.

Website www.hdfcbank.com

HDFC Bank (NYSE: HDB), one amongst the firsts of the new generation, tech-

savvy commercial banks of India, was incorporated in August 1994, after the

Reserve Bank of India allowed setting up of Banks in the private sector. The Bank

was promoted by the Housing Development Finance Corporation Limited, a

premier housing finance company (set up in 1977) of India..

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 18/79

18

COMPANY PROFILE

History

The Housing Development Finance Corporation Limited (HDFC) was amongst the

first to receive an 'in principle' approval from the Reserve Bank of India (RBI) to

set up a bank in the private sector, as part of the RBI's liberalization of the Indian

Banking Industry in 1994. The bank was incorporated in August 1994 in the name

of 'HDFC Bank Limited', with its registered office in Mumbai, India. HDFC Bank

commenced operations as a Scheduled Commercial Bank in January 1995.

HDFC Bank was incorporated in 1994 by Housing Development Finance

Corporation Limited (HDFC), India's largest housing finance company. It was

among the first companies to receive an 'in principle' approval from the ReserveBank of India (RBI) to set up a bank in the private sector. The Bank started

operations as a scheduled commercial bank in January 1995 under the RBI's

liberalization policies.

Times Bank Limited (owned by Bennett, Coleman & Co. / Times Group) was

merged with HDFC Bank Ltd., in 2000. This was the first merger of two private

banks in India. Shareholders of Times Bank received 1 share of HDFC Bank for

every 5.75 shares of Times Bank.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 19/79

19

In 2008 HDFC Bank acquired Centurion Bank of Punjab taking its total branches

to more than 1,000. The amalgamated bank emerged with a base of about Rs.

1,22,000crore and net

advances of about Rs.89,000 crores. The balance sheet size of the combined entity

is more than Rs. 1,63,000crores.

Distribution network

HDFC Bank is

headquartered in Mumbai. The Bank has an nationwide network of 2000 branches

spread in 996 towns and cities across India. All branches are linked on an online

real-time basis. Customers in over 500 locations are also serviced through

Telephone Banking. The Bank has a presence in all major industrial and

commercial centers across the country. Being a clearing/settlement bank to various

leading stock exchanges, the Bank has branches in the centres’ where the

NSE/BSE have a member base.

The Bank also has 5,998 networked ATMs across these towns and cities.

Moreover, HDFC Bank's ATM network can be accessed by all domestic and

international Visa/MasterCard, Visa Electron/Maestro, Plus/Cirrus and American

Express Credit/Charge cardholders.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 20/79

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 21/79

21

Chapter 3

Business of HDFC bankBusiness of HDFC bank

HDFC Bank deals with three key business segments. - Wholesale Banking

Services, Retail Banking Services, Treasury. It has entered the banking consortia

of over 50 corporates for providing working capital finance, trade services,

corporate finance, and merchant banking. It is also providing sophisticated

product structures in areas of foreign exchange and derivatives, money markets

and debt trading and equity research.

Wholesale banking services

Blue-chip manufacturing companies in the Indian corp. to small & mid-sized

corporates and agri-based businesses. For these customers, the Bank provides a

wide range of commercial and transactional banking services, including working

capital finance, trade services, transactional services, cash management, etc. The

bank is also a leading provider for its to corporate customers, mutual funds, stock

exchange members and banks.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 22/79

22

Retail banki ng services

HDFC Bank was the first bank in India to launch an International Debit Card in

association with VISA (VISA Electron) and issues the MasterCard Maestro debit

card as well. The Bank launched its credit card business in late 2001. By March

2009, the bank had a total card base (debit and credit cards) of over 13 million.

The Bank is also one of the leading players in the “merchant acquiring” business

with over 70,000 Point-of-sale (POS)

terminals for debit / credit cards acceptance at merchant establishments. The Bank

is positioned in various net based B2C opportunities including a wide range of

internet banking services for Fixed Deposits, Loans, Bill Payments, etc.

Treasury

Within this business, the bank has three main product areas - Foreign Exchange

and Derivatives, Local Currency Money Market & Debt Securities, and Equities.

These services are provided through the bank's Treasury team. To comply with

statutory reserve requirements, the bank is required to hold 25% of its deposits in

government securities. The Treasury business is responsible for managing the

returns and market risk on this

investment portfolio.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 23/79

23

Chapter 4

Facilities provided by HDFC bank

Facilities provided by HDFC bank

Personal Banking

Accounts & Deposits

Loans

Cards

Forex

Investments & Insurance

NRI Banking

Accounts & Deposits

Remittances

Investments & Insurance Loans Payment Services

Wholesale Banking

Corporate

Small & Medium Enterprises

Financial Institutions & Trusts

Government Sector

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 24/79

24

Chapter 4

E-banking facilities provided by HDFC bank

E-banking facilities provided by HDFC bank

Net Banking

InstaAlerts

Branch Network

ATM

Email Statements

PhoneBanking

Mobile Banking

P.O.Boxes

Net Banking

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 25/79

25

HDFC Bank offers you a comprehensive range of transactions across

multiple products through its NetBanking channel. So just log in to

NetBanking and conduct 135 + transactions from the comfort of your

home or office.

You can check your Account Balance, book Fixed and Recurring Deposits,

Download A/c Statement up to 5 years, pay your Bills, Recharge your Mobile/

DTH connection, and much more in a secure environment.

You can log in to NetBanking using your Customer ID and IPIN (password).

Experience Convenience ... Choose NetBanking!

Are you tired of heading down to a Bank branch? Of waiting in queues? Of notknowing how to manage your account at your convenience? We have the answer!

NetBanking is an incredibly convenient and powerful tool, letting you do

everything you want with your accounts at the click of a mouse.

It is Real Time, giving you up-to-the-second details on your account.

All you need to do is Log in using your Customer ID and IPIN (NetBanking

password).

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 26/79

26

Your Customer ID is mentioned on your account statement/ account welcome

letter/ chequebook. (Current account / HUF customers can obtain this from the

branch). You can re-generate your IPIN online in 3 easy steps.

Some of the transactions you can do through NetBanking are:

Check your account balances and download 5 year account statement in 5

formats, instantly

Book Fixed Deposit / Recurring Deposit

Pay Utility Bills

View your Credit Card details and pay your Credit Card Bills Recharge your Prepaid Mobile & DTH Connections

Invest in Mutual Funds Online

Book IRCTC Tickets online

Purchase a Gift Card

Pay your Taxes online

Update your PAN Details online

Request Stop Payment of a Cheque/ Hotlist you Debit Card/ Credit Card

View your Loan details

Transfer funds between accounts within HDFC Bank and other Bank

Accounts

InstaAlerts

Now you can get regular updates on your bank account on your mobilephone or

email ID. Just register for our Insta Alert service and receive updates on

youraccount as and when the select transaction happens - all this without visiting

the branch or ATM.You can register for any or all of the following alerts:

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 27/79

27

Debit transactions greater than Rs. 5,000/ Rs.10, 000/ Rs. 20,000/Rs. 50,000

Credit in account greater than Rs. 5,000/ Rs.10, 000/ Rs. 20,000/Rs. 50,000

Account Balance below Rs. 5,000/ Rs.10, 000/ Rs. 20,000/Rs. 50,000-

Weekly account balance

Salary Credits

Utility bill payment due Alert

Fees and charges

The service is FREE for you.

Branch Network

Welcome to the networked world of HDFC Bank. You can open an account

and access it from any branch nearest to your residence or office, anywhere

in the country.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 28/79

28

The sophisticated, computerized network gives you the flexibility of

accessing your Savings or Current Account from any of over 3,488 branches

and over 11,426 ATMs across India.

ATM

Our wide range of ATMs across the country ensures that you are never too

far away from money. You can cater to your diverse banking needs, right

from just withdrawing cash to a whole host of other transactions to help you

manage your account with complete security and convenience, whenever

you want.

Welcome to 24 hour banking!

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 29/79

29

Features and benefits

Enjoy various features using our Bank ATMs. Here is a look at what you can do at

our ATMs:

24 hour access to cash : You can withdraw up to Rs. 10,000 per day on your

ATM Card and up to Rs. 25,000 or more on your Debit Card (depending on the

type of card held).

Personalized cash withdrawals : Save time on your cash withdrawal

transactions by pre-setting your preferred language / account / amount.

View account balances and mini-statements : Get a mini-statement with the

last 9 transactions on your account, with your account balance.

Change ATM PIN :Change your ATM PIN whenever you want.

Order a cheque book or account statement : You can order a cheque book or

an account statement from our ATMs.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 30/79

30

HDFC Bank Credit Card Payment : Pay your HDFC Bank Credit Card bill at

any of our ATMs. The primary account of your Debit / ATM card will be

debited.

Deposit cash or cheques : Deposit cheques or cash into your account at our

selected non-branch ATMs.

Transfer funds between accounts : You can transfer funds between the

accounts. A maximum of 16 accounts (Savings / Current) can be linked to a

card.

Refill your Prepaid mobile : Refill your prepaid mobile using the Prepaid

Mobile Refill service instantly.

Pay your utility bills : Pay your mobile, telephone and electricity bills through

our ATMs using BillPay, a comprehensive bill payment solution.

Cheque Status Enquiry : Get information about the status of a cheque issued

from your account.

NetBanking password request : Request for your NetBanking password (IPIN) at

an ATM and it will be sent to your recorder mailing address.

Registration for Mobile Banking : Register for MobileBanking and use our

Banking services through your mobile.

There are no charges levied for use of other bank’s cards on HDFC Bank ATMs

for cash withdrawals and balance enquires.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 31/79

31

Fees and charges

There is no charge for using the card at HDFC Bank ATMs

Charges on Other Bank's

ATM Networks in India Charges

For Current Account Debit

Card Holders

Balance enquiry - Free

Cash withdrawal - Rs. 20/-* per transaction

For Salary & Saving

Account Debit Card Holders

Total of 5 ATM Financial and Non-Financial

transactions per month at other Bank ATMs free of

cost.

Charges from the 6th Transaction onwards:

– Rs. 20.00/-* per Financial transaction - i.e Cash

Withdrawals

– Rs. 8.50/-** per Non-Financial transaction - e.g.

Balance Inquiry, Pin Change & Mini Statement

You will be allowed to withdraw a maximum of Rs. 10,000 per transaction from

another bank’s ATM, w.e.f. from 15th October 2009.

You will not be charged any fee when you use your ATM / Debit Card at any

merchant location.

However, at petrol pumps and railway stations you will be charged a fee as per

Industry practice.

Transaction Cash Balance

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 32/79

32

Withdrawal Inquiry

International Visa/ Plus ATMs and Cirrus

ATMsRs. 110/- Rs. 15/-***

Email Statements

Receive your account statements via email without any delays for your Savings

and Current Accounts. You also have the option to maintain the statement on

email, print it or save it on a CD. Your account info is now available to you at the

click of a button with email statements.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 33/79

33

Features and benefits

Email statements are FREE

Monthly email statements for your Savings Account

Opt for daily / weekly / monthly email statements for your Current Account

Physical statements will be discontinued if you opt for email statements

Based on the date of account opening, it follows a staggered cycle

Even if you are registered for hold mails, you can opt for email statements

Get information on our new products and mandatory information online.

Email statements will be non-combined statements.

PhoneBanking

PhoneBanking services are a combination of IVR and Agent offering,

depending on the type of transaction. For all transactions that cannot be

completed on the IVR such as reporting loss of cards, logging complaints,

requests & queries, PhoneBanker-assisted services are available

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 34/79

34

Features and benefits

Get up-to-the-second details of your Savings or Current Accounts and Fixed

Deposits

Get the details of the last 5 transactions on your account.

Enquire on the status of cheques issued or deposited anywhere in India#

Order a Cheque Book / Account statement to be delivered to your mailing

address.

Open a Fixed Deposit or enquire about your Fixed Deposits / TDS#

Transfer funds between Accounts linked to your Customer ID

Pay your cellular, telephone & electricity bills using BillPay

Call PhoneBanking to report Loss of your ATM / Debit / Prepaid Card.

This service is available 24 hours on all days

Get details on HDFC Bank products and services by talking to our

PhoneBanker

Enquire about latest interest / exchange rates by talking to our PhoneBanker

SMS BANKING

With SMSBanking you can access your account on your mobile wherever you are.

Access your bank account, make banking transactions, monitor your accounts and

fixed deposits on your mobile.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 35/79

35

SMSBanking, a great way to have your bank account at your fingertips!

What features does SMSBanking have?

Take a look at the features of SMSBanking:

View balance details

Get last 3 transaction details

Request for cheque book

Stop cheque payment

Enquire cheque status Request for account statement

Get Fixed Deposit details

Request for IPIN generation

NRI SERVICE DESK / OVERSEAS P.O. BOXES:

At HDFC Bank, we make it easier for you to reach us from across the world.

Keeping in mind the global reach of our esteemed NRI customers like you,

our PO Box facility is available for you in USA, UK, UAE, Australia,

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 36/79

36

Canada, Saudi Arabia, Singapore, Germany.

So go ahead and mail us your account related* requests to the below listed

local PO Box addresses in your country.

You no longer have to incur expensive courier charges to send us account

instructions. All you need to do is simply mail your instruction to a local PO

Box in your country overseas. What's more, this facility is available to you

free of charge.

Chapter 6

Importance of E-banking facility

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 37/79

37

Importance of E-banking facility

Businesses rely on efficient and rapid access to banking information for cash flow

reviews, auditing and daily financial transaction processing. E-banking offers ease

of access, secure transactions and 24-hour banking options. From small start-up

companies to more established entities, small businesses rely on e-banking to

eliminate runs to the bank and to make financial decisions with updated

information. In an information-driven business climate, companies who do not use

e-banking are at a competitive disadvantage.

Activity Review

Business owners, accounting staff and other approved employees can access

routine banking activity such as deposits, cleared checks and wired funds quickly

through an online banking interface. This ease of review helps ensure the smooth

processing of all banking transactions on a daily basis, rather than waiting for

monthly statements. Errors or delays can be noted and resolved quicker, potentially

before any business impact is felt.

Productivity

E-banking leads to productivity gains. Automating routine bill payments,

minimizing the need to physically visit the bank and the ability to work as needed

rather than on banking hours may decrease the time involved in performing routine

banking activities. Additionally, online search tools, banking actions and other

programs can allow staff members to research transactions and resolve banking

problems on their own, without interacting with bank employees. In some cases,

month-end reconciliations for credit card transactions and bank accounts can be

automated by using e-banking files.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 38/79

38

Lower Banking Costs

Banking relationships and costs are often based on resource requirements.

Businesses that place more demands on banking employees and need more

physical assistance with wire transfers, deposits, research requests and other

banking activities often incur higher banking fees. Opting for e-banking minimizes

business overhead and banking expenses.

Reduced Errors

Utilizing e-banking reduces banking errors. Automation of payments, wires or

other consistent financial activities ensures payments are made on time and may

prevent errors caused by keyboard slips or user error. Additionally, opting for

electronic banking eliminates errors due to poor handwriting or mistaken

information. In many cases, electronic files and daily reviews of banking data can

be used to double or triple check vital accounting data, which increases the

accuracy of financial statements.

Reduced Fraud

Increased scrutiny of corporate finances through audits and anti-fraud measures

requires a high level of visibility for all financial transactions. Relying on e-

banking provides an electronic footprint for all accounting personnel, managers

and business owners who modify banking activities. E-banking offers visibility

into banking activities, which makes it harder for under-the-table or fraudulent

activities to occur.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 39/79

39

Chapter 7

E- BANKING SERVICES:

E- BANKING SERVICES

1. Bill payment service

Each bank has tie-ups with various utility companies, service providers and

insurance companies, across the country. It facilitates the payment of electricity

and telephone bills, mobile phone, credit card and insurance premium bills.

To pay bills, a simple one-time registration for each biller is to be completed.Standing instructions can be set, online to pay recurring bills, automatically. One-

time standing instruction will ensure that bill payments do not get delayed due to

lack of time. Most interestingly, the bank does not charge customers for online bill

payment.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 40/79

40

2. Fund transfer

Any amount can be transferred from one account to another of the same or any

another bank. Customers can send money anywhere in India. Payee’s account

number, his bank and the branch is needed to be mentioned after logging in the

account. The transfer will take place in a day or so, whereas in a traditional

method, it takes about three working days. ICICI Bank says that online bill

payment service and fund transfer facility have been their most popular online

services.

3. Credit card customers

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 41/79

41

Credit card users have a lot in store. With Internet banking, customers can not only

pay their credit card bills online but also get a loan on their cards. Not just this,

they can also apply for an additional card, request a credit line increase and God

forbid if you lose your credit card, you can report lost card online.

4. Railway pass

This is something that would interest all the adamant. Indian Railways has tied up

with ICICI bank and you can now make your railway pass for local trains online.

The pass will be delivered to you at your doorstep. But the facility is limited to

Mumbai, Thane, Nasik, Surat and Pune. The bank would just charge Rs 10 + 12.24

percent of service tax.

5. Investing through Internet banking

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 42/79

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 43/79

43

Now there is no need to rush to the vendor to recharge the prepaid phone, every

time the talk time runs out. Just top-up the prepaid mobile cards by logging in to

Internet banking. By just selecting the operator's name, entering the mobile number

and the amount for recharge, the phone is again back in action within few minutes.

7. Shopping at your fingertips

Leading banks have tie ups with various shopping websites. With a range of all

kind of products, one can shop online and the payment is also made conveniently

through the account. One can also buy railway and air tickets through Internet

banking.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 44/79

44

Chapter 8

BENEFITS/CONCERNS OF E-

BANKING

BENEFITS OF E-BANKING

For Banks

• Price- In the long run a bank can save on money by not paying for tellers or

for managing branches. Plus, it's cheaper to make transactions over the

Internet.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 45/79

45

• Customer Base- the Internet allows banks to reach a whole new market-

and a well off one too, because there are no geographic boundaries with the

Internet. The Internet also provides a level playing field for small banks who

want to add to their customer base.

• Efficiency- Banks can become more efficient than they already are by

providing Internet access for their customers. The Internet provides the bank

with an almost paper less system.

• Customer Service and Satisfaction- Banking on the Internet not only

allow the customer to have a full range of services available to them but it

also allows them some services not offered at any of the branches. The

person does not have to go to a branch where that service may or may not be

offer. A person can print of information, forms, and applications via the

Internet and be able to search for information efficiently instead of waiting

in line and asking a teller. With more better and faster options a bank will

surely be able to create better customer relations and satisfaction.

• Image- A bank seems more state of the art to a customer if they offer

Internet access. A person may not want to use Internet banking but having

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 46/79

46

the service available gives a person the feeling that their bank is on the

cutting image.

For Customers

• Bill Pay- Bill Pay is a service offered through Internet banking that allows

the customer to set up bill payments to just about anyone. Customer can

select the person or company whom he wants to make a payment and Bill

Pay will withdraw the money from his account and send the payee a paper

check or an electronic payment

• Other Important Facilities- E- banking gives customer the control over

nearly every aspect of managing his bank accounts. Besides the Customers

can, Buy and Sell Securities, Check Stock Market Information, Check

Currency Rates, Check Balances, See which checks are cleared, Transfer

Money, View Transaction History and avoid going to an actual bank. The

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 47/79

47

best benefit is that Internet banking is free. At many banks the customer

doesn't have to maintain a required minimum balance. The second big

benefit is better interest rates for the customer.

CONCERNS WITH E-BANKING

As with any new technology new problems are faced.

• Customer support - Banks will have to create a whole new customer

relations department to help customers. Banks have to make sure that the

customers receive assistance quickly if they need help. Any major problems

or disastrous can destroy the banks reputation quickly an easily. By showing

the customer that the Internet is reliable you are able to get the customer to

trust online banking more and more.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 48/79

48

• Laws - While Internet banking does not have national or state boundaries,

the law does. Companies will have to make sure that they have software in

place software market, creating a monopoly.

• Security - Customer always worries about their protection and security or

accuracy. There are always questions whether or not something took place.

• Other challenges - Lack of knowledge from customers end, sit changes by

the banks, etc.

Chapter 9

SWOT ANALYSIS

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 49/79

49

SWOT ANALYSIS

Strengths

- It has an extensive distribution network comprising of 535

branches in 312 cities & one international office in Dubai this

provides a competitive edge over the competitors.

- The Bank has a strong retail depository base & has more than

million customers.

- Bank has strong brand equity.

- ISO 9001 certification for its depository & custody operations &

for its backend processing of retail operations & direct banking

operation.

- The bank is a market leader in cash settlement service for the

major stock exchanges in its country.

- HDFC Bank is one of the largest private sector banks working

in India.

- It has a highly automated environment in terms of information

technology & communication system.

- Infrastructure is one of the best in the country.- It has many innovative products like kids Advantage scheme,

NRI services.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 50/79

50

Weaknesses

- Account opening and delivery of cheque book take more time. Lackof availability of different credit products like CC Limit, Bill discounting

facilities.

- Complicated terms and conditions of products, which is not easily

Understandable by the layman.

Opportunities

- Branch expansion

- Door step services

- Greater liberalization is foreign ownership via FDI in Indian Pvt.

Sector banks.

- Infrastructure movements & better systems for trading & settlement

in the Govt. securities & foreign exchange markets.

Threats

The bank has started facing competition from players like SBI, PNB inthe finance market itself. This may reduce the profit margins in the

future.

Some Pvt. Banks have 7 days banking.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 51/79

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 52/79

52

Chapter 10

News and articles

News and articles

1. Any time money, no more: How frequent transactions at ATMs become

expensive

New Delhi | Updated: Aug 19 2014, 09:31 IST

SUMMARY

Come Nov 1, frequent usage of

ATMs will become expensive, with

RBI imposing limit of transactions

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 53/79

53

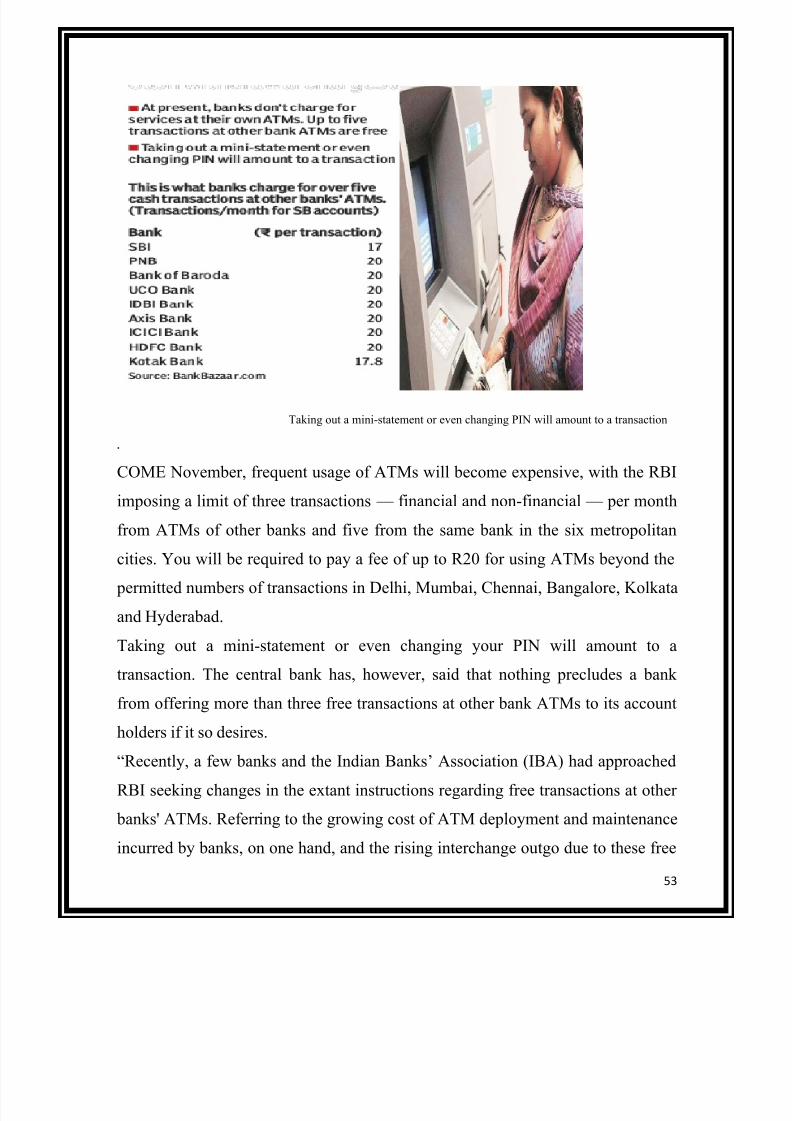

Taking out a mini-statement or even changing PIN will amount to a transaction

.

COME November, frequent usage of ATMs will become expensive, with the RBI

imposing a limit of three transactions — financial and non-financial — per month

from ATMs of other banks and five from the same bank in the six metropolitan

cities. You will be required to pay a fee of up to R20 for using ATMs beyond the

permitted numbers of transactions in Delhi, Mumbai, Chennai, Bangalore, Kolkata

and Hyderabad.

Taking out a mini-statement or even changing your PIN will amount to a

transaction. The central bank has, however, said that nothing precludes a bank

from offering more than three free transactions at other bank ATMs to its account

holders if it so desires.

―Recently, a few banks and the Indian Banks’ Association (IBA) had approached

RBI seeking changes in the extant instructions regarding free transactions at other

banks' ATMs. Referring to the growing cost of ATM deployment and maintenance

incurred by banks, on one hand, and the rising interchange outgo due to these free

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 54/79

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 55/79

55

Alarmed by the recent Bangalore incident, banks are gearing up to enhance

security at ATMs after a review of threat perception at various locations.

"Though our ATMs have adequate security, the bank will review it and beef up

where required," a senior official of Bank told PTI.

As per the usual practice, banks deploy full-time security guards at the off-site

ATMs (Automated Teller Machines), while at the on-site ATM i.e. at the bank

branch, guards are placed only at night.

According to a Corporation Bank official, in the light of the incident in Bangalore,

the bank will further strengthen the security and take appropriate steps.

In a shocking incident on Tuesday, a women employee of Corporation Bank was

attacked brutally at the on-site ATM of the bank.

The assailant had attacked her after entering the ATM booth closely following her

and downing the rolling shutter when she refused to draw money and hand it over

to him.

The private security industry, which manages the cash logistics and security of

bank ATMs, has been raising the security issue of ATM operations time and again

with the government and banks.

"Its the long wait for the gun licences that will cost the ATM security. The

situation could worsen further as the government has announced one lakh more

ATMs in next 2 years.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 56/79

56

"Imagine what could be state then considering the slow progress on the armed

security front," said Rituraj Sinha managing director of cash management company

SIS Prosegur.

As of August, there were 1,26,950 ATMs of banks across the country. Of this, the

number of onsite ATMs are 63,380 while there 63,570 cash dispensing machines

off-site.

Public sector banks had a combined 72,340 branches, of which 37,672 had onsite

ATMs at the end of March 2013.

3. Soon, you can withdraw cash from ATM even without bank account:

Raghuram Rajan

Summary:

RBI in talks with markets to set up trade receivables exchange to facilitate credit to

MSMEs.

In another effort towards financial inclusion, the RBI has given in-principle

approval to setting up of a new payment system that will facilitate fund transfers

from bank account holders to those without accounts through automated teller

machines (ATMs).

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 57/79

57

―Essentially, the sender can have the money withdrawn from his account through

an ATM transaction. The intermediary processes the payment, and sends a code to

the recipient on his mobile that allows him to withdraw the money from any

nearby bank’s ATM,‖ said RBI governor Raghuram Rajan on Wednesday at the

Nasscom summit, and highlighted how technologies can be used to deepen

financial inclusion. Rajan also said the RBI is in talks with market players to set up

a trade receivables exchange to better facilitate credit to micro, small and medium

enterprises (MSMEs). Rajan explained that MSMEs get squeezed all the time by

their large buyers, who pay after long delays.

The governor also said that the RBI will ―accelerate dialogue with key players‖ in

the telecom industry in the next few months to better facilitate mobile banking

through the SMS and unstructured supplementary service data channels.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 58/79

58

Chapter 11

RESEARCH AND METHODLOGY

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 59/79

59

OBJECTIVES OF THE STUDY

The main objectives of the study are:

To study the awareness level of service class people regarding E-Banking.

To find out the frequency and the factors that influences the adoption of E-

Banking services.

To measure the satisfaction level of people.

To understand the problems encountered in by service class people while

using E-Banking services(ATM, Phone banking, etc)

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 60/79

60

RESEARCH METHODOLOGY

Research is a careful investigation or inquiry especially through search for new

facts in branch of knowledge: market research specifies the information. Required

to address these issues: designs the method for collecting information: manage and

implements the data collection process analyses the results and communicates the

finding and their implications.

Research problem is the one which requires a researcher to find out the best

solution for the given problem that is to find out the course of action, the action the

objectives can be obtained optimally in the context of a given environment.

RESEARCH DESIGN

A framework or blueprint for conducting the research project. It specifies the

details of the procedures necessary for obtaining the information needed to

structure and/or solve research problems. A good research design lays the

foundation for conducting the project. A good research design will ensure that the

research project is conducted effectively and efficiently. Typically, a research

design involves the following components, or tasks:

Define the information needed.

Design the research.

Specify the measurement and scaling procedures.

Construct and present a questionnaire or an appropriate form for data

collection.

Specify the sampling process and sampling size.

Develop a plan of data analysis.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 61/79

61

Data Collection:

The objectives of the project are such that both primary and secondary data is

required to achieve them. So both primary and secondary data was used for the

project. The mode of collecting primary data is questionnaire mode and sources of

secondary data are various magazines, books, newspapers, & websites etc.

1. Primary Data: The primary data was collected to measure the customer

satisfaction and their perception regarding HDFC Bank. The primary data was

collected by means of questionnaire and analysis was done on the basis of response

received from the 30 customers. The questionnaire has been designed in such a

manner that the consumer’s satisfaction level can be measured and consumer can

enter his responses easily.

2. Secondary Data: The purpose of collecting secondary data was to achieve the

objective of studying the recent trends and developments taking place in banking.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 62/79

62

Sample size –

30 customers were selected.

Sampling Unit –

Dombivli (Mumbai)

Sampling Technique –

Convenient sampling.

Analysis and Interpretation

After the data collection, it was compiled, classified and tabulated manually and

with help of computer. Then the task of drawing inferences was accomplished with

the help of percentage and graphic method.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 63/79

63

Chapter 12

ANAYLISIS AND INTERPRITAION

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 64/79

64

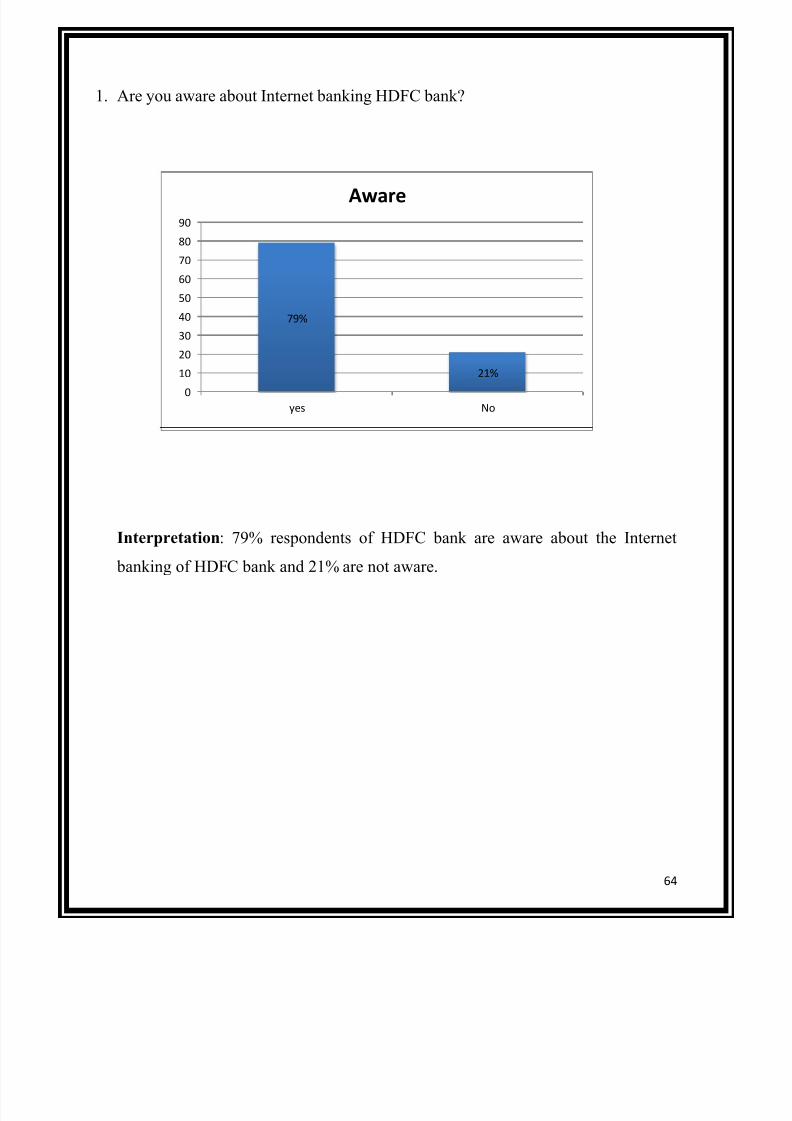

1. Are you aware about Internet banking HDFC bank?

Interpretation: 79% respondents of HDFC bank are aware about the Internet

banking of HDFC bank and 21% are not aware.

79%

21%

0

10

20

30

40

50

60

70

80

90

yes No

Aware

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 65/79

65

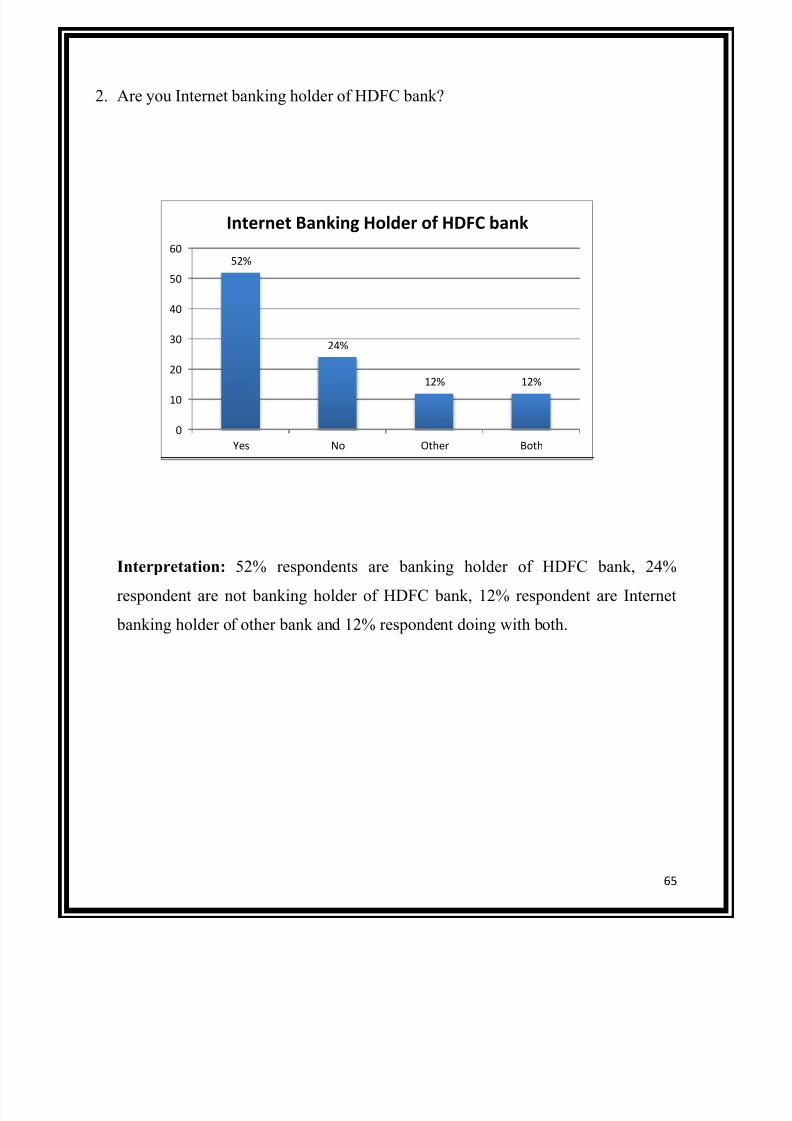

2. Are you Internet banking holder of HDFC bank?

Interpretation: 52% respondents are banking holder of HDFC bank, 24%

respondent are not banking holder of HDFC bank, 12% respondent are Internet

banking holder of other bank and 12% respondent doing with both.

52%

24%

12% 12%

0

10

20

30

40

50

60

Yes No Other Both

Internet Banking Holder of HDFC bank

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 66/79

66

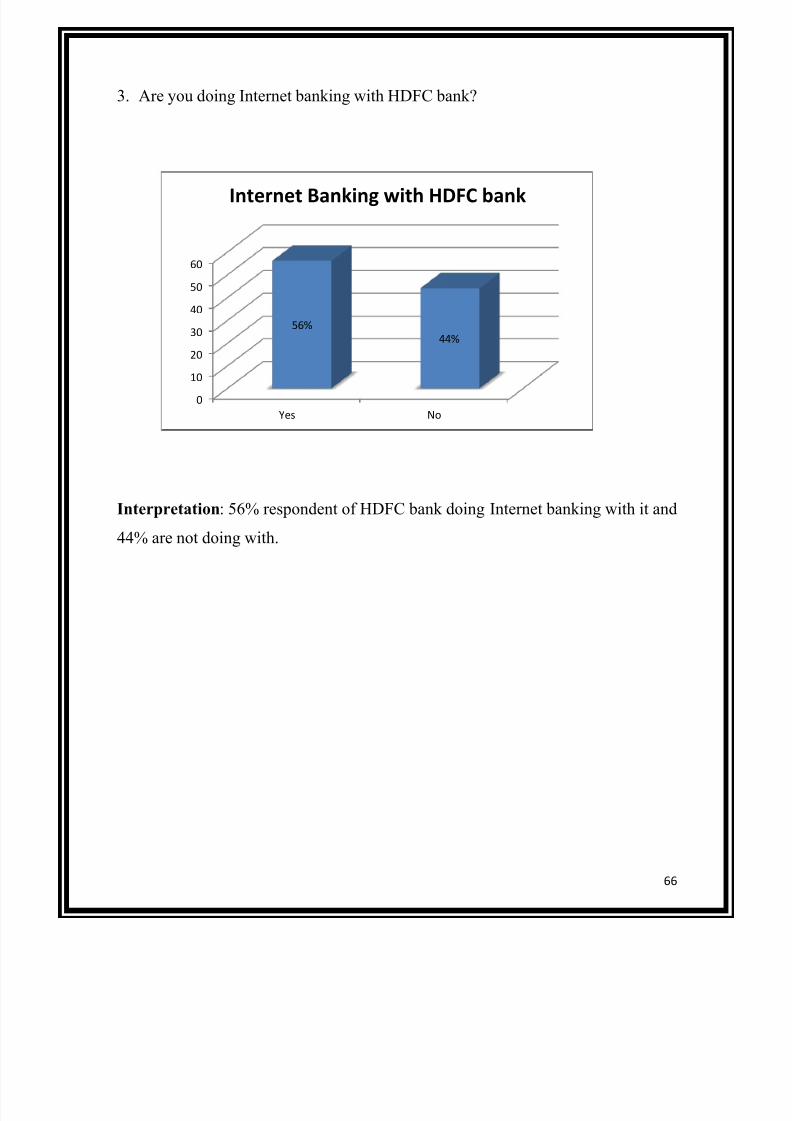

3. Are you doing Internet banking with HDFC bank?

Interpretation: 56% respondent of HDFC bank doing Internet banking with it and

44% are not doing with.

0

10

20

30

40

50

60

Yes No

56%

44%

Internet Banking with HDFC bank

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 67/79

67

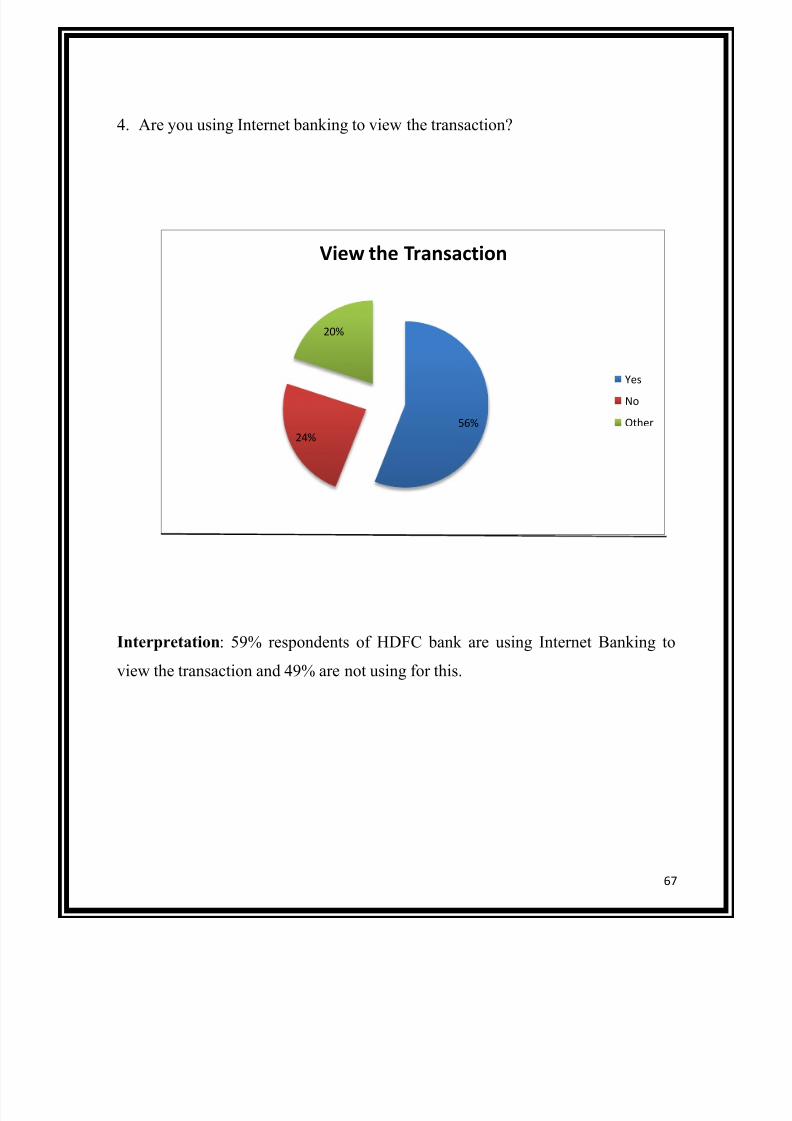

4. Are you using Internet banking to view the transaction?

Interpretation: 59% respondents of HDFC bank are using Internet Banking to

view the transaction and 49% are not using for this.

56%

24%

20%

View the Transaction

Yes

No

Other

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 68/79

68

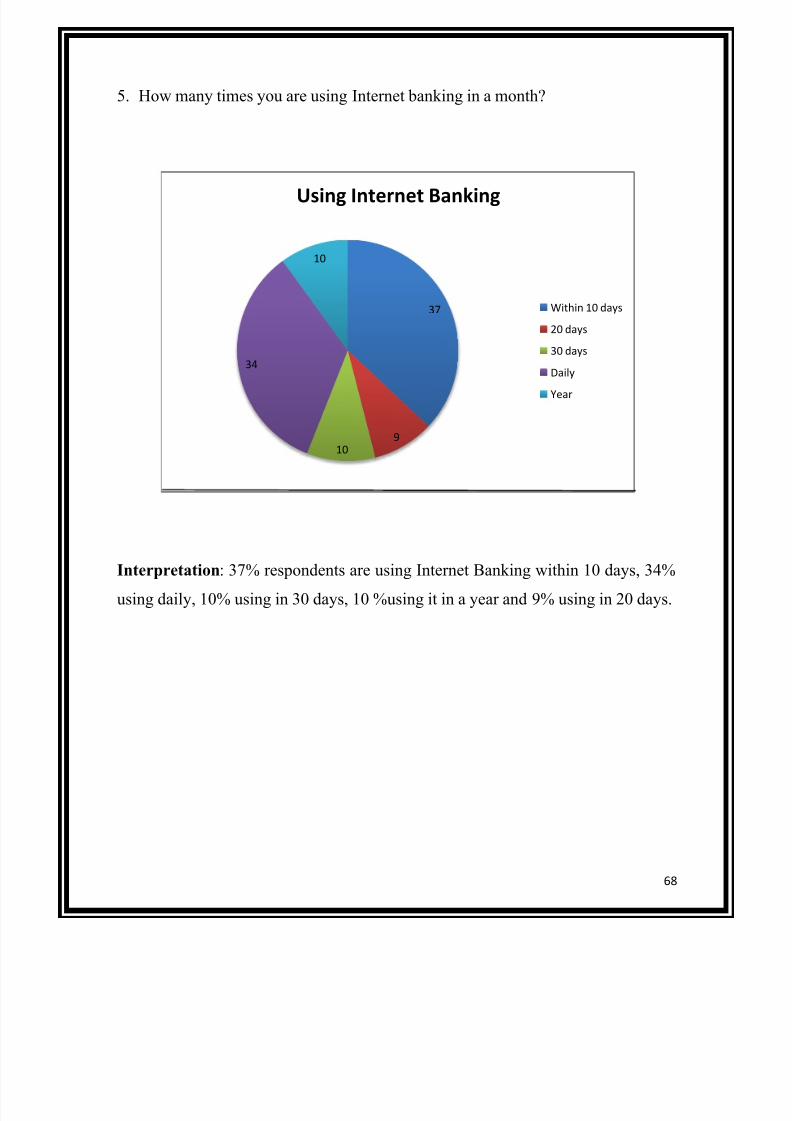

5. How many times you are using Internet banking in a month?

Interpretation: 37% respondents are using Internet Banking within 10 days, 34%

using daily, 10% using in 30 days, 10 %using it in a year and 9% using in 20 days.

37

910

34

10

Using Internet Banking

Within 10 days

20 days

30 days

Daily

Year

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 69/79

69

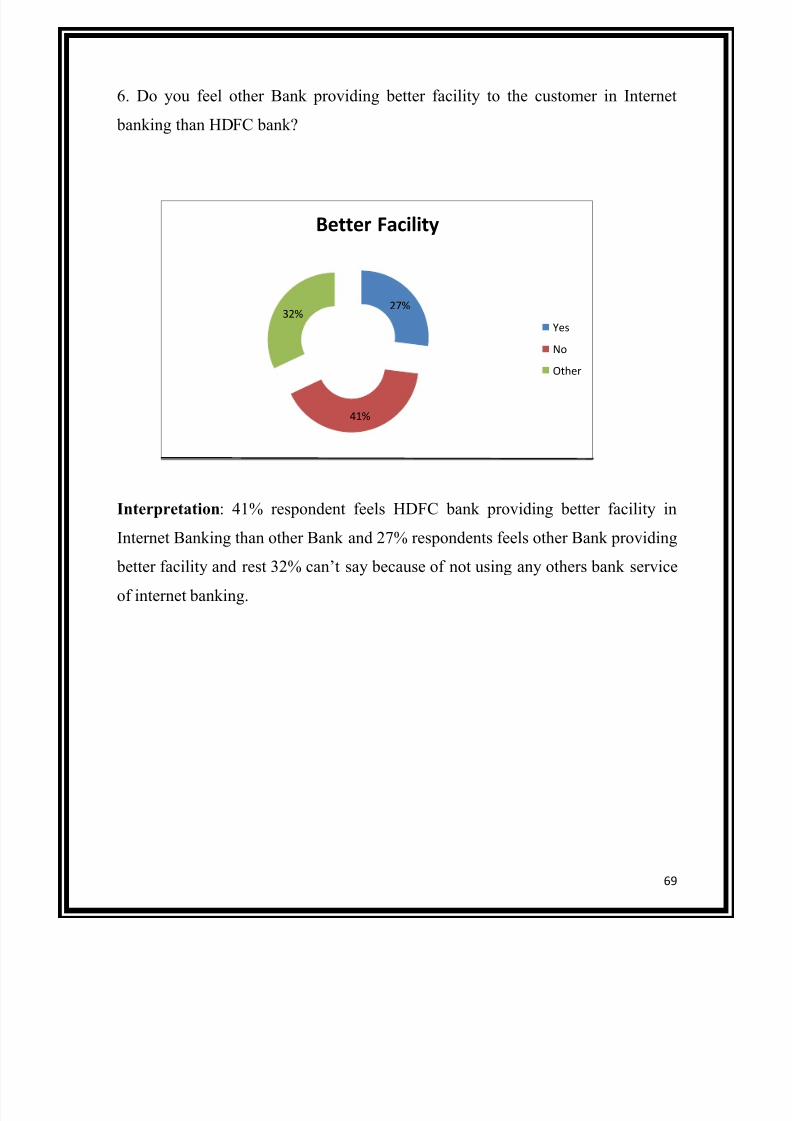

6. Do you feel other Bank providing better facility to the customer in Internet

banking than HDFC bank?

Interpretation: 41% respondent feels HDFC bank providing better facility in

Internet Banking than other Bank and 27% respondents feels other Bank providing

better facility and rest 32% can’t say because of not using any others bank service

of internet banking.

27%

41%

32%

Better Facility

Yes

No

Other

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 70/79

70

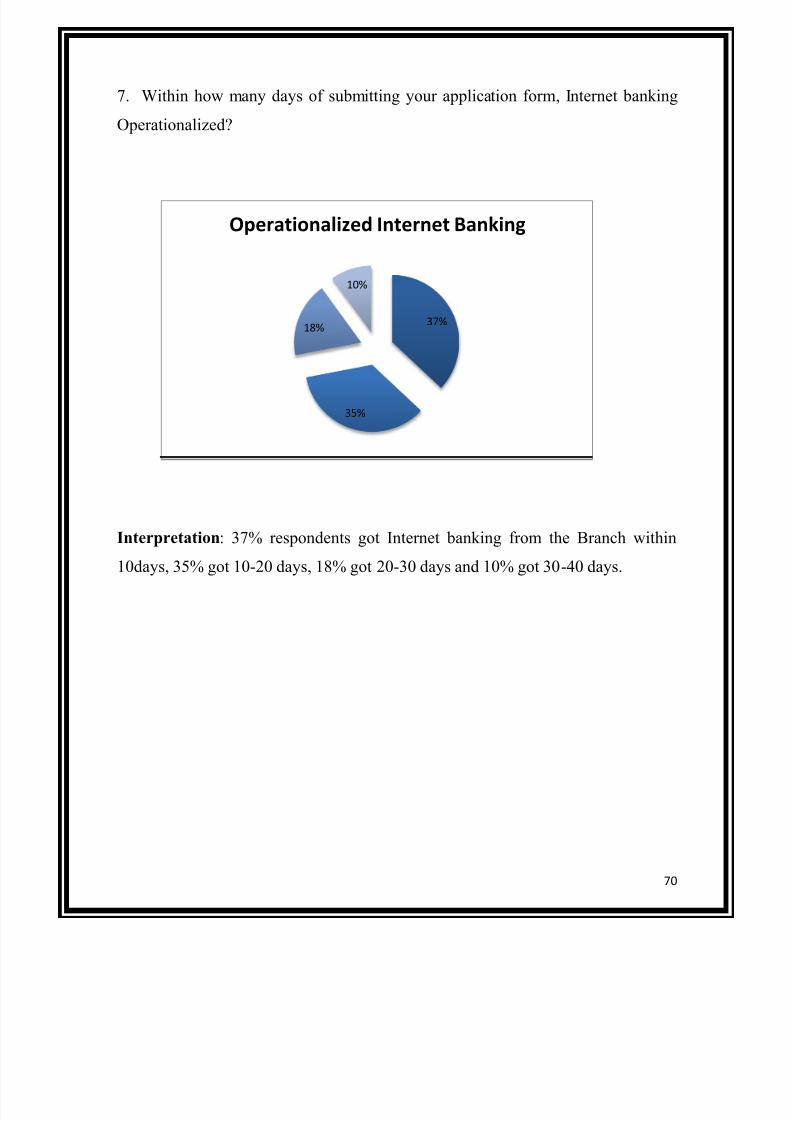

7. Within how many days of submitting your application form, Internet banking

Operationalized?

Interpretation: 37% respondents got Internet banking from the Branch within

10days, 35% got 10-20 days, 18% got 20-30 days and 10% got 30-40 days.

37%

35%

18%

10%

Operationalized Internet Banking

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 71/79

71

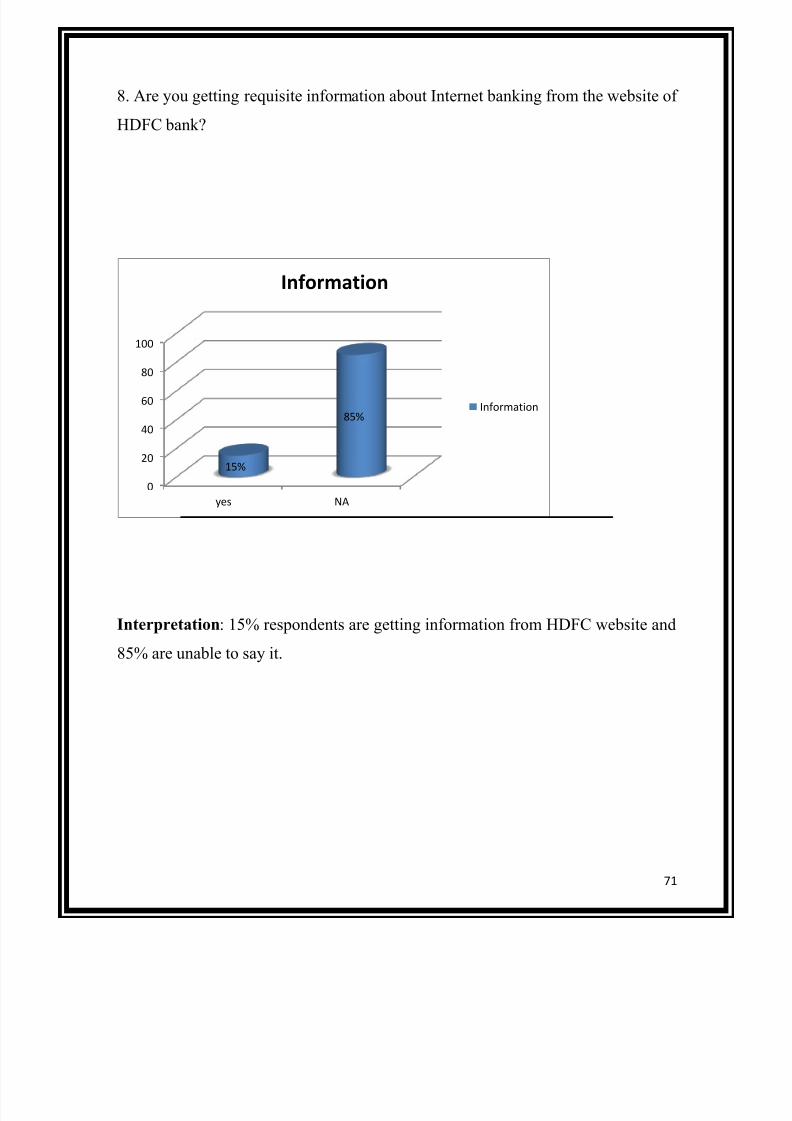

8. Are you getting requisite information about Internet banking from the website of

HDFC bank?

Interpretation: 15% respondents are getting information from HDFC website and

85% are unable to say it.

0

20

40

60

80

100

yes NA

15%

85%

Information

Information

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 72/79

72

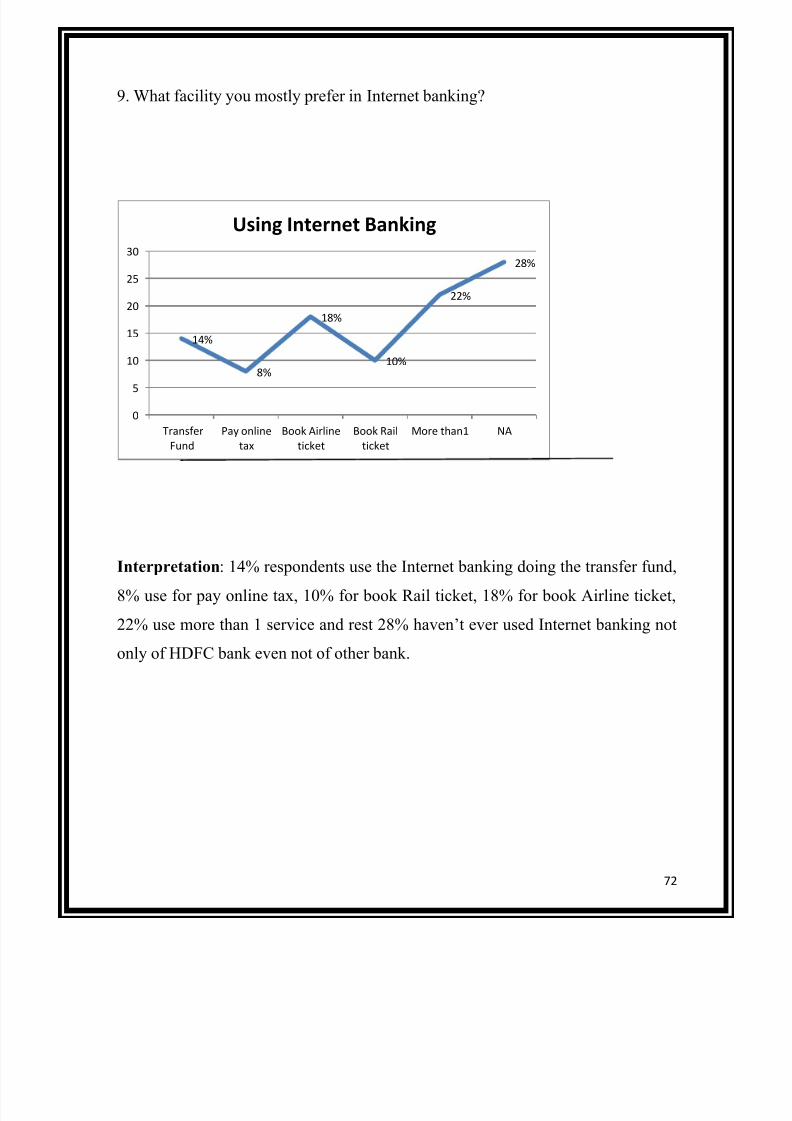

9. What facility you mostly prefer in Internet banking?

Interpretation: 14% respondents use the Internet banking doing the transfer fund,

8% use for pay online tax, 10% for book Rail ticket, 18% for book Airline ticket,

22% use more than 1 service and rest 28% haven’t ever used Internet banking not

only of HDFC bank even not of other bank.

14%

8%

18%

10%

22%

28%

0

5

10

15

20

25

30

Transfer

Fund

Pay online

tax

Book Airline

ticket

Book Rail

ticket

More than1 NA

Using Internet Banking

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 73/79

73

LIMITATIONS

Every research is conducted under some constraints and this research is not an

exception. Limitations of this study are as follows:-

1. There were several time constraints.

2. The study is limited to areas of dombivli only.

3. The sample size of only 30 was taken from the large population for the purpose

of study, so there can be difference between results of sample from total

population.

4. The study is related to service class people only.

5. People were reluctant to go in to details because of their busy schedules.

6. Merely asking questions and recording answers may not always elicit the actual

Information sought.

7. Due to continuous change in environment, what is relevant today may beIrrelevant tomorrow.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 74/79

74

Chapter 12

CONCLUSION

CONCLUSION

The usage of E-banking is all set to increase among the service class. The service class

at the moment is not using the services thoroughly due to various hurdling factors like

insecurity and fear of hidden costs etc. So banks should come forward with measures to

reduce the apprehensions of their customers through awareness campaigns and more

meaningful advertisements to make E-banking popular among all the age and income

groups. Further, with increasing consumer demands, banks have to constantly think of

innovative customized services to remain competitive. E-Banking is an innovative tool

that is fast becoming a necessity. It is a successful strategic weapon for banks to

remain profitable in a volatile and competitive marketplace of today.

In future, the availability of technology to ensure safety and privacy of e-transactions

and the RBI guidelines on various aspects of internet banking will definitely help in rapid

growth of internet banking in India.

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 75/79

75

BIBLIOGRAPHYBOOKS

Malhotra, T. D., “Electronic Banking and Information Technology in Banks”

Sultan Chand and Sons, New Delhi,2008.

S.S Kaptan & N.S. Choubey. “Indian Banking in Electronic Era”

Internet Banking in India-Part I- Dr A. K. Mishra

WEBSITES

www.banknetindia.com

www.bharatbook.com

www.hdfcbank.com

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 76/79

76

Annexure

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 77/79

77

QUESTIONAIRE

Dear Respondent,

We are conducting a research study of “E-banking Preferences among people in

Dombivli”. We will appreciate your cooperation in this regard by filling up the

questionnaire carefully. All the information provided by you will be kept confidential.

Respondent’s Profile

Name : ________________ Income level per month

Age: ________________ Less than Rs. 10,000

Gender (M/F) : ________________ Rs.10,000 to Rs.20,000

Profession: ________________ Rs.20,000 to Rs.30,000

Organization: ________________ More than Rs.30,000

1. In which banks do you have your account?

a. State Bank of India

b. HDFC Bank

c. Punjab National Bankd. ICICI Bank

e. State Bank of Patiala

f. Canara Bank

g. Bank of India

2. While opening up the account, were you aware of E-banking services provided by

your bank?

a. Fully aware

b. Had an idea

c. No

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 78/79

78

3. How did you get to know about E-banking services of your bank?

a. Personal visit

b. Executive from the bank

c. Advertisements

d. Friends/ Relatives

4. Which of the following E-banking services are you aware of?

e. ATM

f. Debit Card

g. Credit Card

h. Phone banking

i. Mobile banking

j. Internet banking

5. Do you use E-banking services?

a. Yes

b. No

6. Which of the following benefits accrue to you, while using E-banking services?

a. Time saving

b. Inexpensive

c. Easy processing

d. Easy fund transfer

e. Any other, please specify

8/10/2019 E-banking Final Proojet 12013 - Copy (2)

http://slidepdf.com/reader/full/e-banking-final-proojet-12013-copy-2 79/79

7. To what extent are you satisfied with your Banks’ E-banking services?

a. Highly Satisfied ___________

b. Satisfied _________

c. Neutral ___________

d. Dissatisfied ___________

e. Highly dissatisfied___________

8. What other services you would like to have through E-banking?

____________________________________________________________

____________________________________________________________