Embed Size (px)

Citation preview

DUBAI PROPERTY REVIEW2016 AND BEYOND

RESIDENTIAL MARKET SUMMARY

OFFICE MARKET SUMMARY

2017 ANDBEYOND

core-me.com

32

CONTENT

This publicationThis document was published in December 2016.The data used in the charts and tables is thelatest available at the time of going to press.Sources are included for all the charts. We haveused a standard set of notes and abbreviationsthroughout the document.

RESIDENTIAL MARKET SUMMARY 2016Delivered stockTransaction analysisDubai real estate cycleRental market

RESIDENTIAL - 2017 AND BEYONDResidential supplyResidential demandRental marketOutlook

OFFICE MARKET SUMMARY 2016Market overviewCommercial real estate cycle

OFFICE - 2017 AND BEYONDOffice supply Office demandOutlook

54

Transaction distribution 2016 ready stock vs off-plan

NOTE:Affordable segment: Below AED 1 millionLow to mid segment: AED 1-2 millionMid-prime segment: AED 2-4 millionPrime: AED 4 million and above

Ready stock vs off-plan transactions

Apartment vs villa transactions -2016ready stock vs off-plan

45%

15%

10.7Thousand

units

19.4Thousand

units

10.1Thousand

units

16.4Thousand

units

Affordable

Villa

2015

Low-mid

Aparment

2016 YTD

Mid-prime Prime

29%

85%

19%

4%7%

17%

31%

90%

48%

10%

2016/17

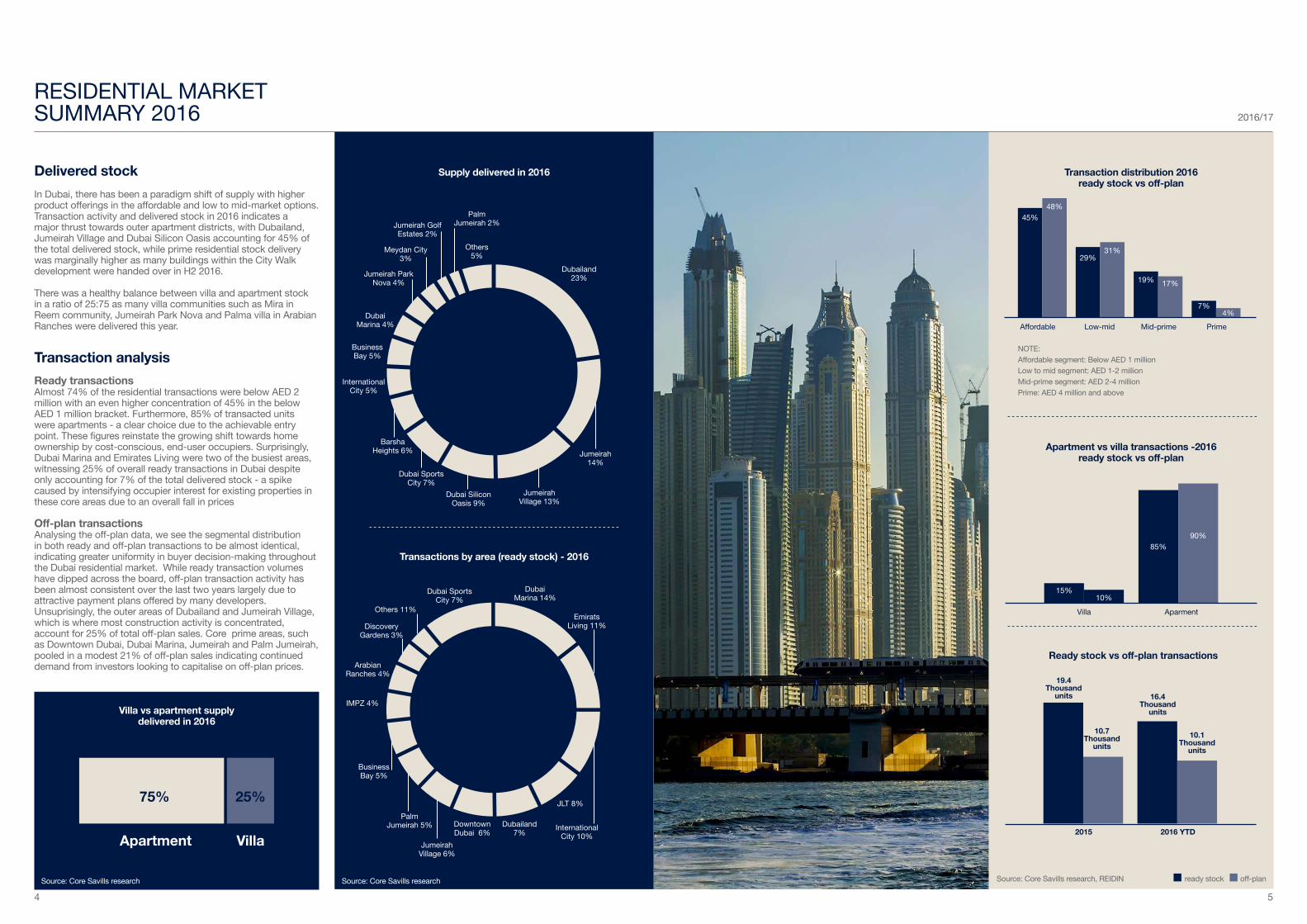

Delivered stockIn Dubai, there has been a paradigm shift of supply with higher product offerings in the affordable and low to mid-market options. Transaction activity and delivered stock in 2016 indicates a major thrust towards outer apartment districts, with Dubailand, Jumeirah Village and Dubai Silicon Oasis accounting for 45% of the total delivered stock, while prime residential stock delivery was marginally higher as many buildings within the City Walk development were handed over in H2 2016.

There was a healthy balance between villa and apartment stock in a ratio of 25:75 as many villa communities such as Mira in Reem community, Jumeirah Park Nova and Palma villa in Arabian Ranches were delivered this year.

Transaction analysisReady transactionsAlmost 74% of the residential transactions were below AED 2 million with an even higher concentration of 45% in the below AED 1 million bracket. Furthermore, 85% of transacted units were apartments - a clear choice due to the achievable entry point. These figures reinstate the growing shift towards home ownership by cost-conscious, end-user occupiers. Surprisingly, Dubai Marina and Emirates Living were two of the busiest areas, witnessing 25% of overall ready transactions in Dubai despite only accounting for 7% of the total delivered stock - a spike caused by intensifying occupier interest for existing properties in these core areas due to an overall fall in prices

Off-plan transactionsAnalysing the off-plan data, we see the segmental distribution in both ready and off-plan transactions to be almost identical, indicating greater uniformity in buyer decision-making throughout the Dubai residential market. While ready transaction volumes have dipped across the board, off-plan transaction activity has been almost consistent over the last two years largely due to attractive payment plans offered by many developers.Unsuprisingly, the outer areas of Dubailand and Jumeirah Village, which is where most construction activity is concentrated, account for 25% of total off-plan sales. Core prime areas, such as Downtown Dubai, Dubai Marina, Jumeirah and Palm Jumeirah, pooled in a modest 21% of off-plan sales indicating continued demand from investors looking to capitalise on off-plan prices.

Source: Core Savills research Source: Core Savills research

RESIDENTIAL MARKETSUMMARY 2016

Others 5%

Palm Jumeirah 2%Jumeirah Golf

Estates 2%

Meydan City 3%

Jumeirah Park Nova 4%

Dubai Marina 4%

Business Bay 5%

International City 5%

Barsha Heights 6%

Dubai Sports City 7%

Dubai Silicon Oasis 9%

Jumeirah Village 13%

Jumeirah 14%

Dubailand 23%

Dubai Marina 14%

Dubai Sports City 7%

EmiratsLiving 11%

International City 10%

JLT 8%

Dubailand 7%

Downtown Dubai 6%

Jumeirah Village 6%

Palm Jumeirah 5%

Business Bay 5%

Arabian Ranches 4%

Discovery Gardens 3%

Others 11%

IMPZ 4%

VillaApartment

Supply delivered in 2016

Transactions by area (ready stock) - 2016

Villa vs apartment supply delivered in 2016

25%75%

Source: Core Savills research, REIDIN ready stock off-plan

76

Jumeriah Village

JLTJumeirah Village

The Lakes

DubailandThe Springs

& The MeadowsAlBarari

Emirates Hills

ArabianRanches Palm

Jumeirah

Palm Jumeirah

DIFC

DowntownDubai

The Views

Dubai Marina

Discovery Gardens

The Greens

Business Bay

JBR

1 0

0.5 0.5 1 1.5 2 2 2.5 2.5 31

1 3.5 3.5 4 4 4.5 5

Change in apartment rents percentage Q1 2016 vs Q4 2016

Change in villa rents percentageQ1 2016 vs Q4 2016

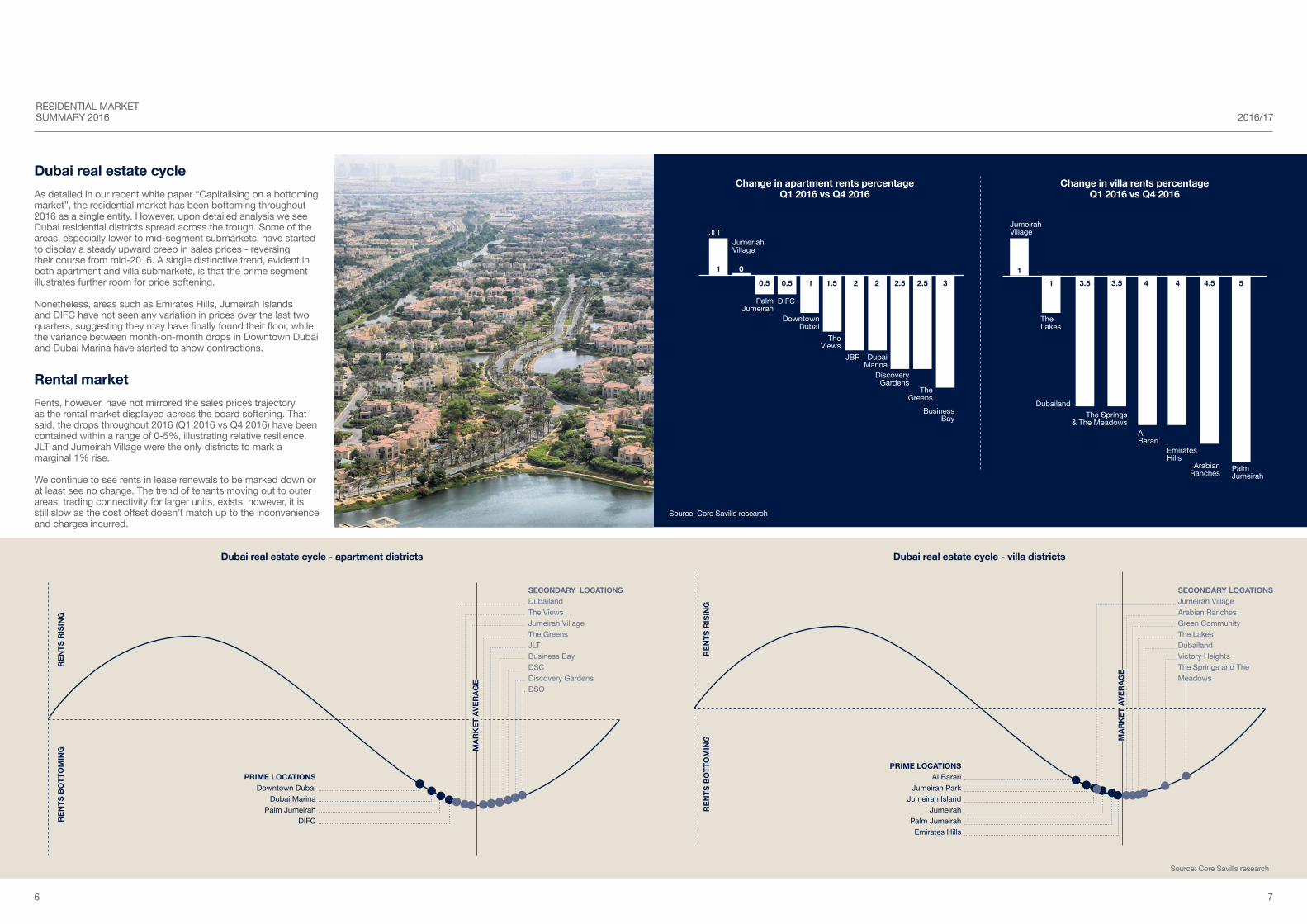

Dubai real estate cycleAs detailed in our recent white paper “Capitalising on a bottoming market”, the residential market has been bottoming throughout 2016 as a single entity. However, upon detailed analysis we see Dubai residential districts spread across the trough. Some of the areas, especially lower to mid-segment submarkets, have started to display a steady upward creep in sales prices - reversing their course from mid-2016. A single distinctive trend, evident in both apartment and villa submarkets, is that the prime segment illustrates further room for price softening.

Nonetheless, areas such as Emirates Hills, Jumeirah Islands and DIFC have not seen any variation in prices over the last two quarters, suggesting they may have finally found their floor, while the variance between month-on-month drops in Downtown Dubai and Dubai Marina have started to show contractions.

Rental marketRents, however, have not mirrored the sales prices trajectory as the rental market displayed across the board softening. That said, the drops throughout 2016 (Q1 2016 vs Q4 2016) have been contained within a range of 0-5%, illustrating relative resilience. JLT and Jumeirah Village were the only districts to mark a marginal 1% rise.

We continue to see rents in lease renewals to be marked down or at least see no change. The trend of tenants moving out to outer areas, trading connectivity for larger units, exists, however, it is still slow as the cost offset doesn’t match up to the inconvenience and charges incurred.

PRIME LOCATIONSDowntown Dubai

Dubai MarinaPalm Jumeirah

DIFC

SECONDARY LOCATIONSDubailandThe ViewsJumeirah VillageThe GreensJLTBusiness BayDSCDiscovery GardensDSO

MAR

KET

AVE

RAG

E

REN

TS R

ISIN

GR

ENTS

BO

TTO

MIN

G

Dubai real estate cycle - apartment districts

PRIME LOCATIONSAl Barari

Jumeirah ParkJumeirah Island

JumeirahPalm Jumeirah

Emirates Hills

SECONDARY LOCATIONSJumeirah VillageArabian RanchesGreen CommunityThe LakesDubailandVictory HeightsThe Springs and The Meadows

MAR

KET

AVE

RAG

E

REN

TS R

ISIN

GR

ENTS

BO

TTO

MIN

G

Dubai real estate cycle - villa districts

2016/17RESIDENTIAL MARKETSUMMARY 2016

Source: Core Savills research

Source: Core Savills research

98

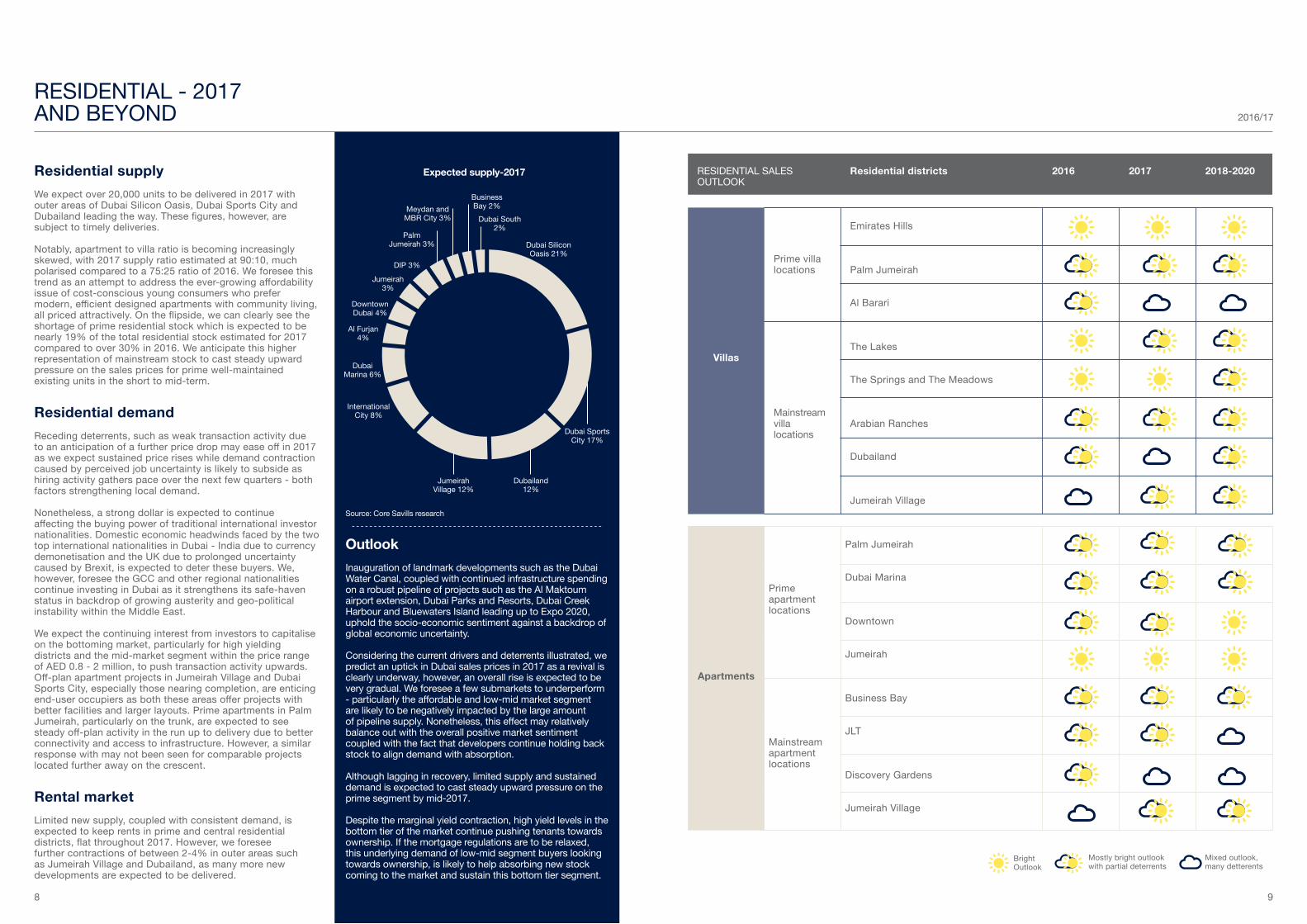

Residential supplyWe expect over 20,000 units to be delivered in 2017 with outer areas of Dubai Silicon Oasis, Dubai Sports City and Dubailand leading the way. These figures, however, are subject to timely deliveries.

Notably, apartment to villa ratio is becoming increasingly skewed, with 2017 supply ratio estimated at 90:10, much polarised compared to a 75:25 ratio of 2016. We foresee this trend as an attempt to address the ever-growing affordability issue of cost-conscious young consumers who prefer modern, efficient designed apartments with community living, all priced attractively. On the flipside, we can clearly see the shortage of prime residential stock which is expected to be nearly 19% of the total residential stock estimated for 2017 compared to over 30% in 2016. We anticipate this higher representation of mainstream stock to cast steady upward pressure on the sales prices for prime well-maintained existing units in the short to mid-term.

Residential demandReceding deterrents, such as weak transaction activity due to an anticipation of a further price drop may ease off in 2017 as we expect sustained price rises while demand contraction caused by perceived job uncertainty is likely to subside as hiring activity gathers pace over the next few quarters - both factors strengthening local demand.

Nonetheless, a strong dollar is expected to continue affecting the buying power of traditional international investor nationalities. Domestic economic headwinds faced by the two top international nationalities in Dubai - India due to currency demonetisation and the UK due to prolonged uncertainty caused by Brexit, is expected to deter these buyers. We, however, foresee the GCC and other regional nationalities continue investing in Dubai as it strengthens its safe-haven status in backdrop of growing austerity and geo-political instability within the Middle East.

We expect the continuing interest from investors to capitalise on the bottoming market, particularly for high yielding districts and the mid-market segment within the price range of AED 0.8 - 2 million, to push transaction activity upwards. Off-plan apartment projects in Jumeirah Village and Dubai Sports City, especially those nearing completion, are enticing end-user occupiers as both these areas offer projects with better facilities and larger layouts. Prime apartments in Palm Jumeirah, particularly on the trunk, are expected to see steady off-plan activity in the run up to delivery due to better connectivity and access to infrastructure. However, a similar response with may not been seen for comparable projects located further away on the crescent.

Rental marketLimited new supply, coupled with consistent demand, is expected to keep rents in prime and central residential districts, flat throughout 2017. However, we foresee further contractions of between 2-4% in outer areas such as Jumeirah Village and Dubailand, as many more new developments are expected to be delivered.

Expected supply-2017

Outlook Inauguration of landmark developments such as the Dubai Water Canal, coupled with continued infrastructure spending on a robust pipeline of projects such as the Al Maktoum airport extension, Dubai Parks and Resorts, Dubai Creek Harbour and Bluewaters Island leading up to Expo 2020, uphold the socio-economic sentiment against a backdrop of global economic uncertainty. Considering the current drivers and deterrents illustrated, we predict an uptick in Dubai sales prices in 2017 as a revival is clearly underway, however, an overall rise is expected to be very gradual. We foresee a few submarkets to underperform - particularly the affordable and low-mid market segment are likely to be negatively impacted by the large amount of pipeline supply. Nonetheless, this effect may relatively balance out with the overall positive market sentiment coupled with the fact that developers continue holding back stock to align demand with absorption. Although lagging in recovery, limited supply and sustained demand is expected to cast steady upward pressure on the prime segment by mid-2017.

Despite the marginal yield contraction, high yield levels in the bottom tier of the market continue pushing tenants towards ownership. If the mortgage regulations are to be relaxed, this underlying demand of low-mid segment buyers looking towards ownership, is likely to help absorbing new stock coming to the market and sustain this bottom tier segment.

Dubai South 2%

Business Bay 2%Meydan and

MBR City 3%

Palm Jumeirah 3%

DIP 3%

Jumeirah 3%

Downtown Dubai 4%

Al Furjan 4%

Dubai Marina 6%

International City 8%

Jumeirah Village 12%

Dubailand 12%

Dubai Silicon Oasis 21%

Dubai Sports City 17%

Bright Outlook

Mostly bright outlook with partial deterrents

Mixed outlook, many detterents

RESIDENTIAL SALES OUTLOOK

Residential districts 2016 2017 2018-2020

Villas

Prime villa locations

Emirates Hills

Palm Jumeirah

Al Barari

Mainstream villa locations

The Lakes

The Springs and The Meadows

Arabian Ranches

Dubailand

Jumeirah Village

Apartments

Prime apartment locations

Palm Jumeirah

Dubai Marina

Downtown

Jumeirah

Mainstream apartment locations

Business Bay

JLT

Discovery Gardens

Jumeirah Village

2016/17

RESIDENTIAL - 2017 AND BEYOND

Source: Core Savills research

1110

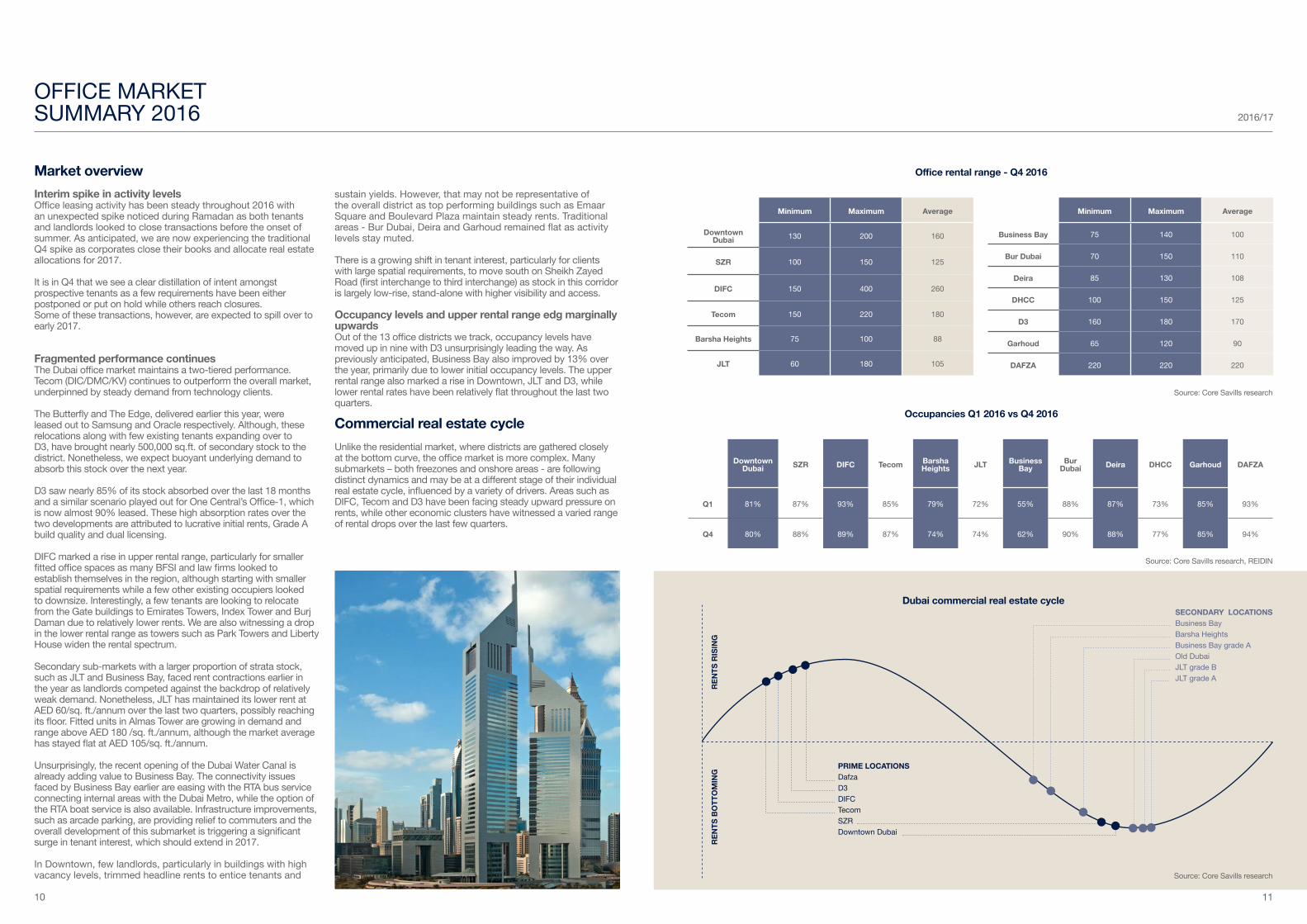

Market overviewInterim spike in activity levelsOffice leasing activity has been steady throughout 2016 with an unexpected spike noticed during Ramadan as both tenants and landlords looked to close transactions before the onset of summer. As anticipated, we are now experiencing the traditional Q4 spike as corporates close their books and allocate real estate allocations for 2017.

It is in Q4 that we see a clear distillation of intent amongst prospective tenants as a few requirements have been either postponed or put on hold while others reach closures. Some of these transactions, however, are expected to spill over to early 2017.

Fragmented performance continuesThe Dubai office market maintains a two-tiered performance.Tecom (DIC/DMC/KV) continues to outperform the overall market, underpinned by steady demand from technology clients.

The Butterfly and The Edge, delivered earlier this year, were leased out to Samsung and Oracle respectively. Although, these relocations along with few existing tenants expanding over to D3, have brought nearly 500,000 sq.ft. of secondary stock to the district. Nonetheless, we expect buoyant underlying demand to absorb this stock over the next year.

D3 saw nearly 85% of its stock absorbed over the last 18 months and a similar scenario played out for One Central’s Office-1, which is now almost 90% leased. These high absorption rates over the two developments are attributed to lucrative initial rents, Grade A build quality and dual licensing.

DIFC marked a rise in upper rental range, particularly for smaller fitted office spaces as many BFSI and law firms looked to establish themselves in the region, although starting with smaller spatial requirements while a few other existing occupiers looked to downsize. Interestingly, a few tenants are looking to relocate from the Gate buildings to Emirates Towers, Index Tower and Burj Daman due to relatively lower rents. We are also witnessing a drop in the lower rental range as towers such as Park Towers and Liberty House widen the rental spectrum.

Secondary sub-markets with a larger proportion of strata stock, such as JLT and Business Bay, faced rent contractions earlier in the year as landlords competed against the backdrop of relatively weak demand. Nonetheless, JLT has maintained its lower rent at AED 60/sq. ft./annum over the last two quarters, possibly reaching its floor. Fitted units in Almas Tower are growing in demand and range above AED 180 /sq. ft./annum, although the market average has stayed flat at AED 105/sq. ft./annum.

Unsurprisingly, the recent opening of the Dubai Water Canal is already adding value to Business Bay. The connectivity issues faced by Business Bay earlier are easing with the RTA bus service connecting internal areas with the Dubai Metro, while the option of the RTA boat service is also available. Infrastructure improvements, such as arcade parking, are providing relief to commuters and the overall development of this submarket is triggering a significant surge in tenant interest, which should extend in 2017.

In Downtown, few landlords, particularly in buildings with high vacancy levels, trimmed headline rents to entice tenants and

sustain yields. However, that may not be representative of the overall district as top performing buildings such as Emaar Square and Boulevard Plaza maintain steady rents. Traditional areas - Bur Dubai, Deira and Garhoud remained flat as activity levels stay muted.

There is a growing shift in tenant interest, particularly for clients with large spatial requirements, to move south on Sheikh Zayed Road (first interchange to third interchange) as stock in this corridor is largely low-rise, stand-alone with higher visibility and access.

Occupancy levels and upper rental range edg marginally upwardsOut of the 13 office districts we track, occupancy levels have moved up in nine with D3 unsurprisingly leading the way. As previously anticipated, Business Bay also improved by 13% over the year, primarily due to lower initial occupancy levels. The upper rental range also marked a rise in Downtown, JLT and D3, while lower rental rates have been relatively flat throughout the last two quarters.

Commercial real estate cycleUnlike the residential market, where districts are gathered closely at the bottom curve, the office market is more complex. Many submarkets – both freezones and onshore areas - are following distinct dynamics and may be at a different stage of their individual real estate cycle, influenced by a variety of drivers. Areas such as DIFC, Tecom and D3 have been facing steady upward pressure on rents, while other economic clusters have witnessed a varied range of rental drops over the last few quarters.

Minimum Maximum Average

Downtown Dubai 130 200 160

SZR 100 150 125

DIFC 150 400 260

Tecom 150 220 180

Barsha Heights 75 100 88

JLT 60 180 105

Minimum Maximum Average

Business Bay 75 140 100

Bur Dubai 70 150 110

Deira 85 130 108

DHCC 100 150 125

D3 160 180 170

Garhoud 65 120 90

DAFZA 220 220 220

DowntownDubai SZR DIFC Tecom Barsha

Heights JLT Business Bay

Bur Dubai Deira DHCC Garhoud DAFZA

Q1 81% 87% 93% 85% 79% 72% 55% 88% 87% 73% 85% 93%

Q4 80% 88% 89% 87% 74% 74% 62% 90% 88% 77% 85% 94%

PRIME LOCATIONSDafzaD3DIFCTecomSZRDowntown Dubai

SECONDARY LOCATIONSBusiness BayBarsha HeightsBusiness Bay grade AOld DubaiJLT grade BJLT grade A

REN

TS R

ISIN

GR

ENTS

BO

TTO

MIN

G

Office rental range - Q4 2016

Occupancies Q1 2016 vs Q4 2016

Dubai commercial real estate cycle

2016/17

OFFICE MARKETSUMMARY 2016

Source: Core Savills research, REIDIN

Source: Core Savills research

Source: Core Savills research

1312

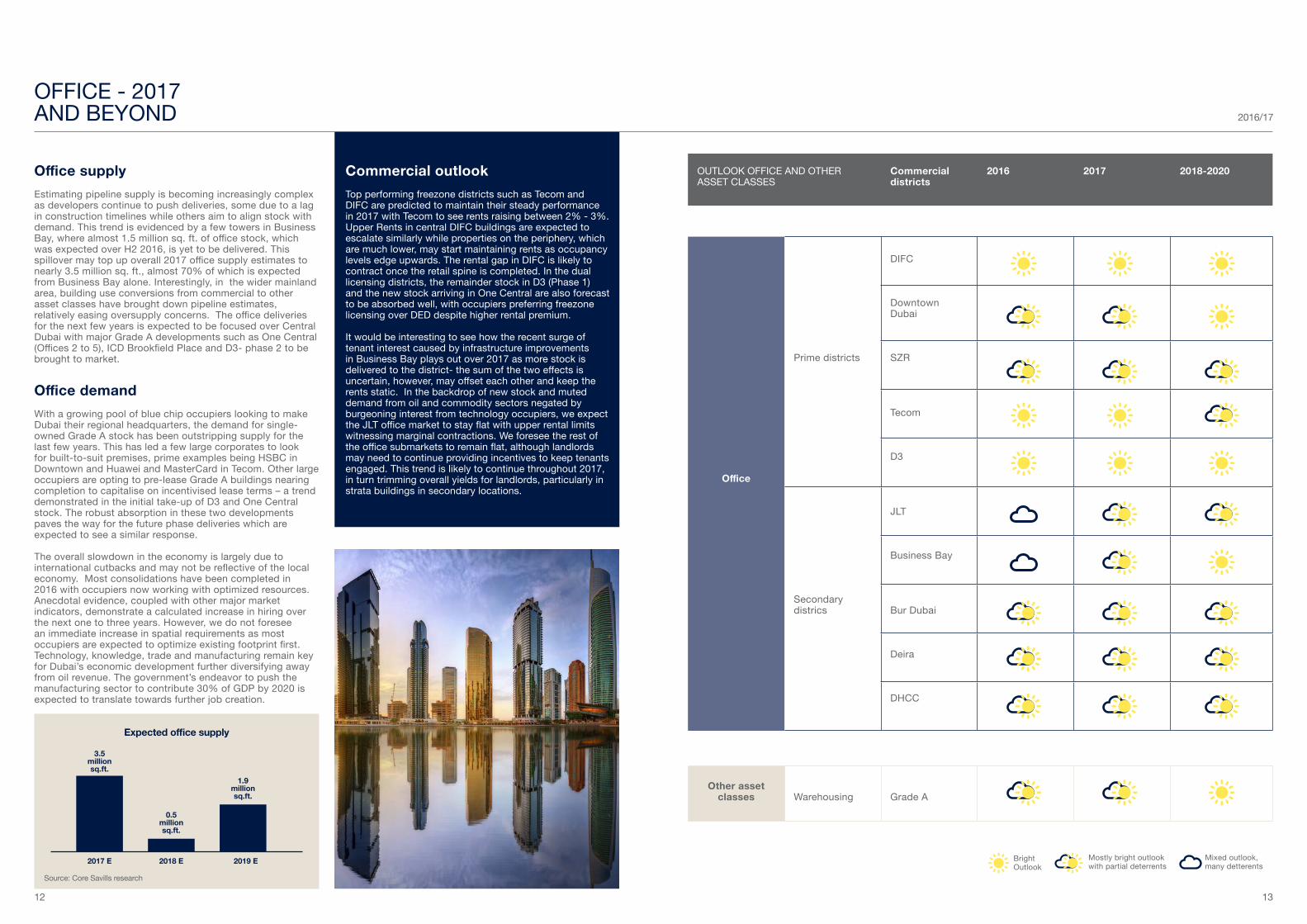

Office supply Estimating pipeline supply is becoming increasingly complex as developers continue to push deliveries, some due to a lag in construction timelines while others aim to align stock with demand. This trend is evidenced by a few towers in Business Bay, where almost 1.5 million sq. ft. of office stock, which was expected over H2 2016, is yet to be delivered. This spillover may top up overall 2017 office supply estimates to nearly 3.5 million sq. ft., almost 70% of which is expected from Business Bay alone. Interestingly, in the wider mainland area, building use conversions from commercial to other asset classes have brought down pipeline estimates, relatively easing oversupply concerns. The office deliveries for the next few years is expected to be focused over Central Dubai with major Grade A developments such as One Central (Offices 2 to 5), ICD Brookfield Place and D3- phase 2 to be brought to market.

Office demand With a growing pool of blue chip occupiers looking to make Dubai their regional headquarters, the demand for single-owned Grade A stock has been outstripping supply for the last few years. This has led a few large corporates to look for built-to-suit premises, prime examples being HSBC in Downtown and Huawei and MasterCard in Tecom. Other large occupiers are opting to pre-lease Grade A buildings nearing completion to capitalise on incentivised lease terms – a trend demonstrated in the initial take-up of D3 and One Central stock. The robust absorption in these two developments paves the way for the future phase deliveries which are expected to see a similar response.

The overall slowdown in the economy is largely due to international cutbacks and may not be reflective of the local economy. Most consolidations have been completed in 2016 with occupiers now working with optimized resources. Anecdotal evidence, coupled with other major market indicators, demonstrate a calculated increase in hiring over the next one to three years. However, we do not foresee an immediate increase in spatial requirements as most occupiers are expected to optimize existing footprint first. Technology, knowledge, trade and manufacturing remain key for Dubai’s economic development further diversifying away from oil revenue. The government’s endeavor to push the manufacturing sector to contribute 30% of GDP by 2020 is expected to translate towards further job creation.

Commercial outlookTop performing freezone districts such as Tecom and DIFC are predicted to maintain their steady performance in 2017 with Tecom to see rents raising between 2% - 3%. Upper Rents in central DIFC buildings are expected to escalate similarly while properties on the periphery, which are much lower, may start maintaining rents as occupancy levels edge upwards. The rental gap in DIFC is likely to contract once the retail spine is completed. In the dual licensing districts, the remainder stock in D3 (Phase 1) and the new stock arriving in One Central are also forecast to be absorbed well, with occupiers preferring freezone licensing over DED despite higher rental premium. It would be interesting to see how the recent surge of tenant interest caused by infrastructure improvements in Business Bay plays out over 2017 as more stock is delivered to the district- the sum of the two effects is uncertain, however, may offset each other and keep the rents static. In the backdrop of new stock and muted demand from oil and commodity sectors negated by burgeoning interest from technology occupiers, we expect the JLT office market to stay flat with upper rental limits witnessing marginal contractions. We foresee the rest of the office submarkets to remain flat, although landlords may need to continue providing incentives to keep tenants engaged. This trend is likely to continue throughout 2017, in turn trimming overall yields for landlords, particularly in strata buildings in secondary locations.

3.5 millionsq.ft.

0.5 million sq.ft.

1.9 million sq.ft.

2017 E 2018 E 2019 E

Expected office supply

OUTLOOK OFFICE AND OTHER ASSET CLASSES

Commercial districts

2016 2017 2018-2020

Office

Prime districts

DIFC

Downtown Dubai

SZR

Tecom

D3

Secondary districs

JLT

Business Bay

Bur Dubai

Deira

DHCC

Other asset classes Warehousing Grade A

Bright Outlook

Mostly bright outlook with partial deterrents

Mixed outlook, many detterents

2016/17

OFFICE - 2017 AND BEYOND

Source: Core Savills research

1514

DMCC Office

7H, Seventh Floor, Almas Tower,Jumeirah Lake Towers, Dubai, UAE

Tel: +971 4 423 9933Fax: +971 4 425 0099Mail: [email protected]

Head Office

Ground Floor, Building 6,Emaar Square, Downtown Dubai, Dubai, UAE

Tel: +971 4 388 3339Fax: +971 4 388 3308Mail: [email protected]

Abu Dhabi Office

Of�ce No. RU 04, Abu Dhabi National Exhibition Centre (ADNEC)Al Khaleej Al Arabi Street, Abu Dhabi, UAE

Tel: +971 2 556 7778Fax: +971 2 659 4165 Mail: [email protected]

Recent market-leading research publications

Established Prime ResidentialMarket in DubaiQ2 2016

Dubai InvestmentOutlookH1 2016

Market in MinutesDubai Commercial MarketQ2 2016

In Focus:Affordable Housingin Dubai - 2016

Market in MinutesDubai Residential MarketQ1 2016

Market in MinutesDubai Office MarketQ1 2016

Market in MinutesDubai Industrial MarketQ1 2016

In Focus:Start-up Environment in Dubai - 2016

Dubai Residential Market UpdateSummer 2016

Dubai OfficeMarket UpdateQ3 2016

Dubai Residential Market Sentiment Survey2016

62 OFFICESAMERICAS & CARIBBEAN

135 OFFICESUK, IRELAND & CHANNEL ISLANDS

103 OFFICESEUROPE

272 OFFICESMIDDLE EAST &AFRICA

134 OFFICESASIA PACIFIC

GLOBAL PRESENCEOVER 700 OFFICES AND ASSOCIATES WORLDWIDE

RECENT MARKETLEADING RESEARCH PUBLICATIONS

Core - UAE Associate of SavillsAs one of the largest UAE property services rms, Core, UAE Associate of Savills, combines expert local market insight with the international strength provided by 700 ofces globally.

Core’s multi-lingual advisers share an entrepreneurial spirit with a commitment to cultivating long-term, collaborative client relationships. Our local roots, commitment, and attention to detail are backed by the global standards of Savills’ 150-year-old brand, giving our clients direct access to 30,000 experienced practitioners, with a deep understanding of specialist real estate services in over 60 countries.Our bespoke residential and commercial property advice enables our clients to make informed real estate decisions both locally and abroad, through a single point of contact in any of the 15 languages spoken by our consultants, in one of our 3 ofces, in Downtown Dubai, Jumeirah Lake Towers and Abu Dhabi.

This report is for general informative purposes only. It may not be published, reproduced or quoted in part or in whole, nor may it be used as a basis for any contract, prospectus, agreement or other document without prior consent. Whilst every effort has been made to ensure its accuracy, Core, UAE Associate of Savills, accepts no liability whatsoever for any direct or consequential loss arising from its use. The content is strictly copyright and reproduction of the whole or part of it in any form is prohibited without written permission from Core’s research team. © Core Real Estate Brokers.

Prathyusha GurrapuSenior Manager- Researchand [email protected]

Capitilising On A Bottoming MarketYear end 2016

David AboodPartner - Head of [email protected]

Katherine RevettDirector - [email protected]

IN FOCUS:Capitalising on a bottoming marketAn investment guide Year end 2016

Core ResearchDubai Property

core-me.com

Lyndsey RedstoneHead of Sales and Leasing - [email protected]

Head Office

Ground Floor, Building 6,Emaar Square, Downtown Dubai,Dubai, UAE

Tel: +971 4 388 3339Fax: +971 4 388 3308Mail: [email protected]

DMCC Office

7H, Seventh Floor, Almas Tower,Jumeirah Lake Towers,Dubai, UAE

Tel: +971 4 423 9933Fax: +971 4 425 0099Mail: [email protected]

Abu Dhabi Office

Office No. RU 04, Abu Dhabi National Exhibition Centre (ADNEC), Al Khaleej Al Arabi Street, Abu Dhabi, UAE

Tel: +971 2 556 7778Fax: +971 2 659 4165Mail: [email protected]