Embed Size (px)

Citation preview

DRIVERS OF THE MARKET

1

About us

.

2

Incorporated in 1982, Raine & Horne International Zaki + Partners Sdn.

Bhd. is a firm of Chartered Surveyors and Registered Valuers. Our practice

covers a wide range of services including property valuation, investment and

project management, property management, real estate agency and

property consultancy.

The firm currently operates twelve (12) offices in Malaysia: Kuala Lumpur,

Petaling Jaya, Subang Jaya, Kelang, Johor Bahru, Melaka, Ipoh, Seremban,

Kuantan, Penang, Kota Kinabalu and Kuching.

Since its inception and establishment, Raine & Horne International Zaki +

Partners Sdn. Bhd. has enjoyed an outstanding and enviable reputation and

success. The firm has received wide recognition from all quarters, nationally

and internationally.

Founded in 1883, Raine & Horne is one of the world’s largest real estate

organisations with offices and affiliates all over the world, including in the

major cities of South East Asia, Europe, Canada, USA, Fiji, Australia, New

Zealand, Japan and Africa.

Raine & Horne International Zaki + Partners Sdn. Bhd. aims to provide our

clients with quality professional service. Raine & Horne International Zaki +

Partners Sdn. Bhd. is committed to the Quality Management System required by

ISO 9001:2008 Standards.

Our team comprises of highly qualified partners in various expertise which

authorize us to offer broad ranges of services in:

Professional Valuation Services

Corporate Advisory Services

Project Management

Property Management & Maintenance

Real Estate Agency

Auctioning

Market Research & Feasibility Studies

Property Investment Consultancy

Building Auditing

Bio Asset Valuation

Forensic Valuation

CYF.A5/07.14

Contents

3

Summary………………..........…...........4

Drivers of the Market…………………6

Mortgage Rates………………………...7

Housing costs relative to Income........15

Speculative Activity..............................16

Demographic Factors………………...19

Micro Factors.......................................26

References………………………….....27

Contact us…………………………….29

International Affiliations…………….30

CYF.A5/07.14

Summary

.

4

Classified under the broad category of alternative investments; the real estate

market is inevitably tied to the performance of various economic factors. Such

factors are further refined into macro and micro drivers, which serve as the

determinants of the level of activity in the property market.

Macro Drivers

Some of the more important determinants of the housing sector include:

Mortgage rates

In general, mortgage rates have an inverse relationship with housing activities.

As one rises, the other is expected to fall. Historically, mortgage rate is widely

anticipated to rise in the near future due to various reasons. Such reasons

include the upswing in leading indicators such as US mortgage rates, yield of

10-year MGS, and ticking up of inflation rate.

Contrary, there were arguments against a hike in local interest rates such as the

existence of high level of household debts, elevated debt service ratios, ever

increasing bankruptcy cases, and weakening GDP growth rate. Recent

improvement of the GDP in Q1 2014 backed by strong exports has provided the

perfect opportunity for Bank Negara to raise interest rates.

The degree of the hike will be closely monitored, should the central bank

decides to do so. Since, an increase in interest rates will translate into a stronger

Ringgit and thus putting pressure on exports which currently supports the better

performance of the GDP.

Housing costs relative to Income

Housing price was increasing faster than income for most of the time. This was

more pronounced in recent years. This does not bode well for the property

market in the long run, since affordability of the housing market will be out of

reach for most of the population. Recent cooling policies were necessary to

avoid such radical incident.

Speculative Activity

During the 10-year period being examined, the property market was noticed to

be constantly under speculative influence whether it was positive or negative.

An exception was witnessed in 2013 due to various cooling measures applied.

CYF.A5/07.14

Summary

.

5

A quick view on the KLSE Property Index has provided the affirmation in

which the property market was and still is on an uptrend; with higher support

and higher resistance levels. Trading volumes were strong and supportive of any

surge. Thus, developers were still speculated to perform well over the short and

long-term.

Demographic Factors

Malaysia’s population is aging slowly but still in its early stages. Median age

has increased from 23.6 (2000) to 26.2 (2010); which is still a relatively young

population. Annualized average growth rate has declined slowly throughout the

years. The highest percentage of working adults are in the 20 – 29 age group,

followed by 30 – 39. These 2 groups are ages of greatest household formations.

Malaysia has a low population density ratio coming in at just 86 person/km2.

The nation’s population is not evenly distributed with concentrations in a few

selective states. The degree of density usually dictates the type of houses offered

by developers.

On the other hand, the nation recorded a fairly moderate urbanization rate of

71.0% in 2010. The household size of 4.31 person/household is considered

fairly large on an international standard. It is anticipated that there could be a

high possibility of smaller household size in the future. Such a reduction in the

number of person per household would directly increase the demand for new

living quarters and strain the existing housing stock in the market. In addition,

smaller household size would translate into demand for smaller residential units

as well.

Micro Drivers

As revealed earlier, macro drivers affect the property market at a national scale,

while micro drivers emphasize on local conditions of the subject property.

The price of house is a function of several local variables such as location

characteristics, house characteristics, plot size, surrounding view and

neighbourhood characteristics. These factors usually adhere to a general

guideline but in some instances, may subject to personal preference.

Buyers would be more willing to pay a higher price for the house if these related

characteristics matched their individual expectations and preferencesCYF.A5/07.14

Drivers of the Market

Classified under the broad category of alternative investments; the real estate

market is inevitably tied to the performance of various economic factors. Such

factors are further refined into macro and micro drivers, which serve as the

determinants of the level of activity in the property market.

Macro Drivers

According to Kaplan University (2013), some of the more important

determinants of the housing sector include:

1. Mortgage rates

2. Housing costs relative to income

3. Speculative activity

4. Demographic factors

They are quite similar and do overlap with some of the factors listed under the

expanded equation of hedonic regression by Wheatley (2012):

Ps = W (S, Y, Z)

Ps: price of house

W: willingness to pay

S: size of house

Y: household income

Z: vector (individual preferences; based on age, race, social background, family

size etc.)

In this equation, the price of house is determined by the factors of S, Y, and Z

as stated above.

Micro Drivers

Besides addressing the macro drivers which affect the property market at a

national scale, micro drivers emphasize on local conditions of the subject

property. The main equation of hedonic regression by Wheatley (2012) are as

follow:

P = f (L, T, S, V, N)

P: price of house

f: function of

L: location characteristics

T: house characteristics

S: plot size

V: surrounding view

N: neighbourhood characteristics6CYF.A5/07.14

Mortgage Rates

7

ALR = Malaysia Average Lending Rate

US MR = United States 30-years Mortgage Rate

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

INTE

RST

RA

TE (

%)

10 YRS MEAN (ALR) 10 YRS MEAN (US MR)

Poly. (MALAYSIA ALR) Poly. (US 30-YR MORTGAGE RATE)

The ALR (average lending rate) of Malaysian banks were decreasingthroughout the 10-year period being studied and currently at an all-time low.Low mortgage rate has fuelled the boom of the property market and at the sametime encouraged households to rack in more debts.

When compared to the US 30-year mortgage rate, interest rates were almostcomparable between 2005 to 2009. Divergence begun in the aftermath of thesubprime mortgage crisis. In order to stimulate growth, interest rates in US wasartificially suppressed to historical low in order to promote growth.

Recent improvements in the US labour and housing market have promptedspeculation that interest rates will be raise sooner than expected. This wasreflected in rising mortgage rates and 10-year treasury bonds back in 2013 andcontinuing into 2014. Thus the spread between the Malaysia ALR and US 30-year mortgage rate has narrowed to a small margin. If the long-term trend holds,interest rates in Malaysia will be under pressure to rise.

Figure 1: Mortgage rates in Malaysia and US (BNM, 2014; Freddie Mac, 2014).

CYF.A5/07.14

Mortgage Rates

8

OPR = Overnight policy rate, IBR = Interbank rate

BLR = Base lending rate, ALR = Average lending rate

MGS = Malaysian government securities, FDR = Fixed-deposit rate

The OPR was quite stable in last 10 years, with the exception in 2009 due to the

subprime mortgage crisis. The 3-month IBR and 1-month FDR generally tracks the

OPR set by Bank Negara. Savings rate is currently at an all-time low at 0.25%. This

has boosted the margin of banks and the incentive to lend.

Due to lower payout for savings, banks could lend at a lower rate, this was reflected in

the decreasing ALR compared to the proposed BLR. However, the spread between

ALR and FDR are narrowing, thus squeezing the margin of banks, and their

willingness to lend. If OPR is to rise, FDR will follow suit hence putting pressure on

banks to raise mortgage rates.

Based on the chart above, 10-year MGS is usually a leading indicator of OPR. This

was displayed in 2007, where the 10-year MGS dipped before the drop of OPR in

2009. The 10-year MGS is seen rising again in 2014, pricing in a hike in OPR.

Back in the old days before the subprime mortgage crisis, it makes sense that the

general public withdraw money from the pension fund to pay for mortgage down

payments; due to the reason that the yield of EPF is lower than the ALR. However,

this is no longer true after 2009, where rise in asset prices has caused EPF yields to

overtake mortgage rates. A substantial rise in mortgage rates might just reverse the

current condition.

Figure 2: Interest rates in Malaysia

(BNM, 2014, EPF, 2014; Trading Economics, 2014).

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

INTE

RES

T R

ATE

(%

)

OPR 3-MONTH IBR BLR ALR

10-YR MGS 1-M FDR SAVINGS RATE EPF YIELD

CYF.A5/07.14

Mortgage Rates

9

Inflation rate

Another reason for the central bank to raise OPR is the ticking up of inflation

rate due to subsidy reduction by government. Anticipation of further subsidy

removal and the implementation of GST in 2015 has fuelled expectations that

the local inflation rate may build up to the 4% level thus causing a negative rate

of return at the current interest level.

However, there are some important considerations before deciding for a hike in

OPR. Under current circumstance, inflation is caused mainly by the removal of

subsidies and not by high growth rate. As such, an excessive hike in OPR might

put downward pressure on the already weakening domestic economy.

Argument against an excessive hike in interest rate will be delivered in the

subsequent pages.

Figure 3: Inflation rate in Malaysia (Trading Economics, 2014).

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

INFL

ATI

ON

RA

TE (

%)

INFLATION RATE 10 YRS AVERAGE 3 YRS AVERAGE

CYF.A5/07.14

Mortgage Rates

10

Household debt & Savings rate

The easy monetary policy back in 2009 has seen its effect on interest rates

where ALR and savings rate dropped to record low. This in turn affect the

household debt and savings rate in Malaysia directly.

Due to historical low interest rates, households were tempted to borrow more

and save less. A boom in household debt was witnessed since 2009 and

increasing steadily throughout the years. While gross domestic savings were

below the 40% mark since 2009. This translates into a debt/savings ratio from

around 1.5 (pre-crisis) to 2.0 (after 2009).

An excessive hike in interest rates will therefore weigh on the high level of

existing debts, causing more defaults if the situation runs out of hand.

Figure 4: Household debt and Gross domestic savings in Malaysia (BNM, 2014).

2003.5 2004.5 2005.5 2006.5 2007.5 2008.5 2009.5 2010.5 2011.5 2012.5

0.00

0.50

1.00

1.50

2.00

2.50

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

2004 2005 2006 2007 2008 2009 2010 2011 2012

% O

F G

DP

HOUSEHOLD DEBT/GDPGROSS DOMESTIC SAVINGS/GDPHOUSEHOLD DEBT/GROSS DOMESTIC SAVINGS

CYF.A5/07.14

Mortgage Rates

11

Debt servicing

Figure 5 depicts that a lion’s share of the household debts were dedicated

towards the repayment of property loans. Thus, an excessive hike in interest

rates will affect the property market negatively.

Whereas the debt to service ratio was above the 30% proposed guideline; which

is not really healthy. A raise in interest rates will definitely increase the debt to

service ratio above the current level.

Figure 5: Composition of household debt in Malaysia (The Star Online, 2014).

2007 2008 2009 2010 2011 2012

-2.00

-1.00

0.00

1.00

2.00

3.00

4.00

36.00

37.00

38.00

39.00

40.00

41.00

42.00

43.00

44.00

45.00

46.00

2007 2008 2009 2010 2011 2012

YO

Y %

CH

AN

GE

DEB

T SE

RV

ICE

RA

TIO

(%

)

DEBT SERVICE RATIO YOY % CHANGE

Figure 6: Debt to service ratio in Malaysia (BNM, 2014).

CYF.A5/07.14

Mortgage Rates

12

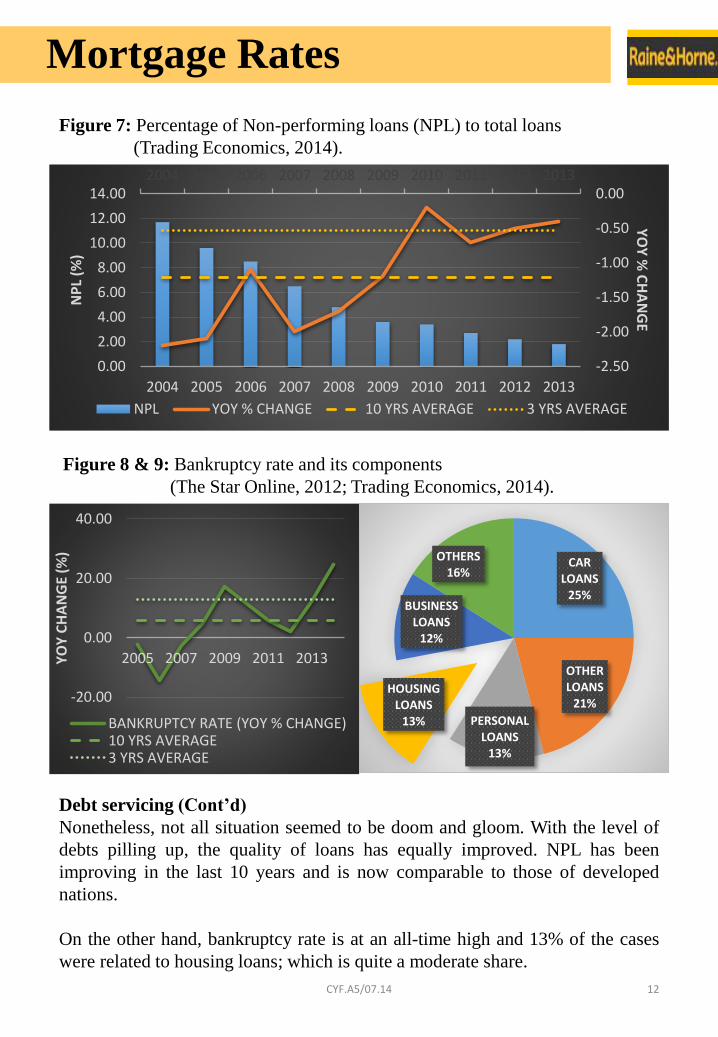

Debt servicing (Cont’d)

Nonetheless, not all situation seemed to be doom and gloom. With the level of

debts pilling up, the quality of loans has equally improved. NPL has been

improving in the last 10 years and is now comparable to those of developed

nations.

On the other hand, bankruptcy rate is at an all-time high and 13% of the cases

were related to housing loans; which is quite a moderate share.

Figure 7: Percentage of Non-performing loans (NPL) to total loans

(Trading Economics, 2014).

Figure 8 & 9: Bankruptcy rate and its components

(The Star Online, 2012; Trading Economics, 2014).

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

-2.50

-2.00

-1.50

-1.00

-0.50

0.00

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

YO

Y %

CH

AN

GE

NP

L (%

)

NPL YOY % CHANGE 10 YRS AVERAGE 3 YRS AVERAGE

-20.00

0.00

20.00

40.00

2005 2007 2009 2011 2013YO

Y C

HA

NG

E (%

)

BANKRUPTCY RATE (YOY % CHANGE)10 YRS AVERAGE3 YRS AVERAGE

CAR LOANS

25%

OTHER LOANS

21%

PERSONAL LOANS

13%

HOUSING LOANS

13%

BUSINESS LOANS

12%

OTHERS16%

CYF.A5/07.14

Mortgage Rates

13

GDP & Property valueBased on Figure 10, it is noticed that the GDP growth rate of Malaysianeconomy was slowing down. Whereas the growth rate for the construction sub-sector (residential and non-residential) is becoming an important factor tosupport the economy of the country as a whole. Even though the portion of thisconstruction sub-sector is small compared to overall GDP; nonetheless theimmense spillover and multiplication effect of it is important to boost othersectors of the economy.

Whereas the growth rate for total value of property transactions hasoverextended in 2010 and 2011, causing it to revert closer to the nominal GDPgrowth rate. An excessive hike in interest rates will inevitably dent the growthrate of the local economy and definitely is an issue to be concerned over by thecentral bank. Recent improvement of the GDP in Q1 2014 backed by strongexports has provided the perfect opportunity for Bank Negara to raise interestrates.

The degree of the hike will be closely monitored, should the central bankdecides to do so. Since, an increase in interest rates will translate into a strongerRinggit and thus putting pressure on exports which currently supports the betterperformance of the GDP.

Figure 10: YOY changes for GDP, construction sub-sector (residential & non-

residential), and total value of property transactions

(Department of Statistics Malaysia, 2014; JPPH, 2014).

-20.00

-10.00

0.00

10.00

20.00

30.00

40.00

2006 2007 2008 2009 2010 2011 2012 2013

YO

Y %

CH

AN

GE

GDP AT CURRENT PRICES

GDP FOR SUB-SECTOR OF CONSTRUCTION (R & NR)

VALUE OF PROPERTY TRANSACTION

CYF.A5/07.14

Mortgage Rates

14

Construction sector

As mentioned in the previous section, the growth rate of construction sector was

faster than the pace of the overall economy. Further analysis of this sector has

provided the evidence that the growth rate of residential sector has overtaken

non-residential since 2011. Nevertheless, their direct contribution towards the

GDP was insignificant (slightly over 2% of the overall GDP).

An excessive hike in interest rates will most certain hold back this sector due to

the increment in financing cost and reduction in demand appetite for properties.

The current strength witnessed in the construction sector implied that

developers were confident in the outlook of the property market.

Figure 11: GDP of construction sub-sector (residential & non-residential).

(Department of Statistics Malaysia, 2014).2006 2007 2008 2009 2010 2011 2012 2013

-10.00

0.00

10.00

20.00

30.00

40.00

50.00

0.00

0.50

1.00

1.50

2.00

2.50

2006 2007 2008 2009 2010 2011 2012 2013

YOY %

CH

AN

GE

% O

F G

DP

% OF TOTAL GDP (RESIDENTIAL) % OF TOTAL GDP (NON-RESIDENTIAL)

YOY % CHANGE (RESIDENTIAL) YOY % CHANGE (NON-RESIDENTIAL)

CYF.A5/07.14

Housing costs relative to Income

15

GDP per capita versus Housing price

Housing costs were tracked using 2 different methods; which include the house

price index and average price per transaction. Basically, they moved in the same

direction but the latter is more volatile than the former.

A ratio was devised using the rate of change for GDP per capita to the rate of

change for housing price. A threshold line of 1.00 was drawn on the chart to

illustrate this relationship. Any value above 1.00 suggests that income is

growing faster than housing price and vice versa.

A quick view at Figure 11 implied that both ratios spent most of their time

below the threshold line. Hence, housing price was increasing faster than

income for most of the time. This was more pronounced in recent years. This

does not bode well for the property market in the long run if the ratio is

persistently below 1.00, since affordability of the housing market will be out of

reach for most of the population. Recent cooling policies were necessary to

avoid such radical incident.

Figure 12: Ratio of changes in GDP per capita to changes in housing price

(Trading Economics, 2014).

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013RA

TIO

OF

YOY

% C

HA

NG

E

GDP PER CAPITA/HOUSE PRICE INDEXGDP PER CAPITA/AVERAGE PRICE PER TRANSACTIONTHRESHOLD LINE (RATIO = 1)

CYF.A5/07.14

Speculative Activity

16

Figure 13: Volume and Average price

per transaction of the

Malaysian property market

(JPPH, 2014, NAPIC, 2014).

CYF.A5/07.14

Speculative Activity

17

There was a high correlation between volume and average price per transaction

as proposed in the previous article of ‘Significance of volume & value’.

According to the law of demand, this inferred that the property market was

constantly under speculative influence whether it was positive or negative. An

exception was witnessed in 2013.

D1: 2005

Consumer sentiment was negative in 2005, thus the demand curve shifted to the

left, resulting in a new equilibrium of lower quantity and price.

D2: 2011

Buyer outlook was positive in 2011, hence the demand curve shifted to the right,

ensuing in a new equilibrium of higher volume and price.

D3: 2013

A great divergence was seen in 2013, where volume and price moved in

opposite directions; suggesting that the once influential speculative activity was

departing from the market due to various cooling measures employed by the

regulators.

Therefore it was proposed that the demand curve did not shift but move along it.

As prices of houses increased, volume decreased; which was the case in 2013.

However, the movement along the curve can be both ways, in which the fall in

prices will result in higher volume.

Looking forward, developers (which are the supply providers) could easily sway

the supply curve to the left or right depending on the type, price and quantity of

houses they will be providing. Developers could act as a speculative force in the

market.

CYF.A5/07.14

Speculative Activity

18

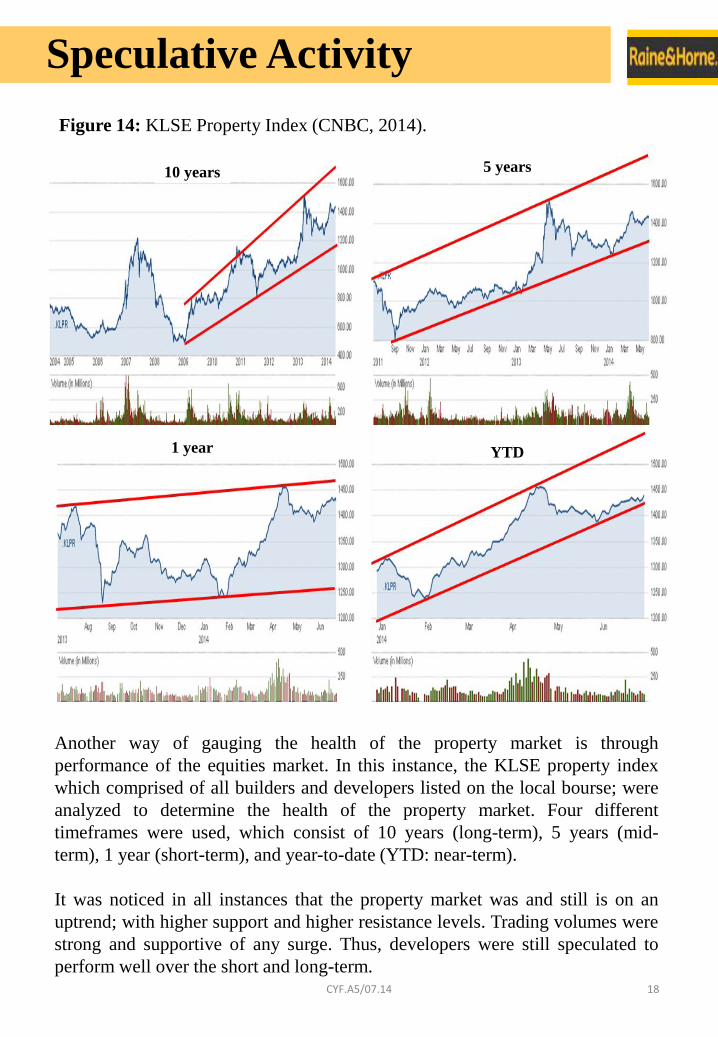

Figure 14: KLSE Property Index (CNBC, 2014).

10 years 5 years

1 year YTD

Another way of gauging the health of the property market is through

performance of the equities market. In this instance, the KLSE property index

which comprised of all builders and developers listed on the local bourse; were

analyzed to determine the health of the property market. Four different

timeframes were used, which consist of 10 years (long-term), 5 years (mid-

term), 1 year (short-term), and year-to-date (YTD: near-term).

It was noticed in all instances that the property market was and still is on an

uptrend; with higher support and higher resistance levels. Trading volumes were

strong and supportive of any surge. Thus, developers were still speculated to

perform well over the short and long-term.CYF.A5/07.14

Demographic Factors

19

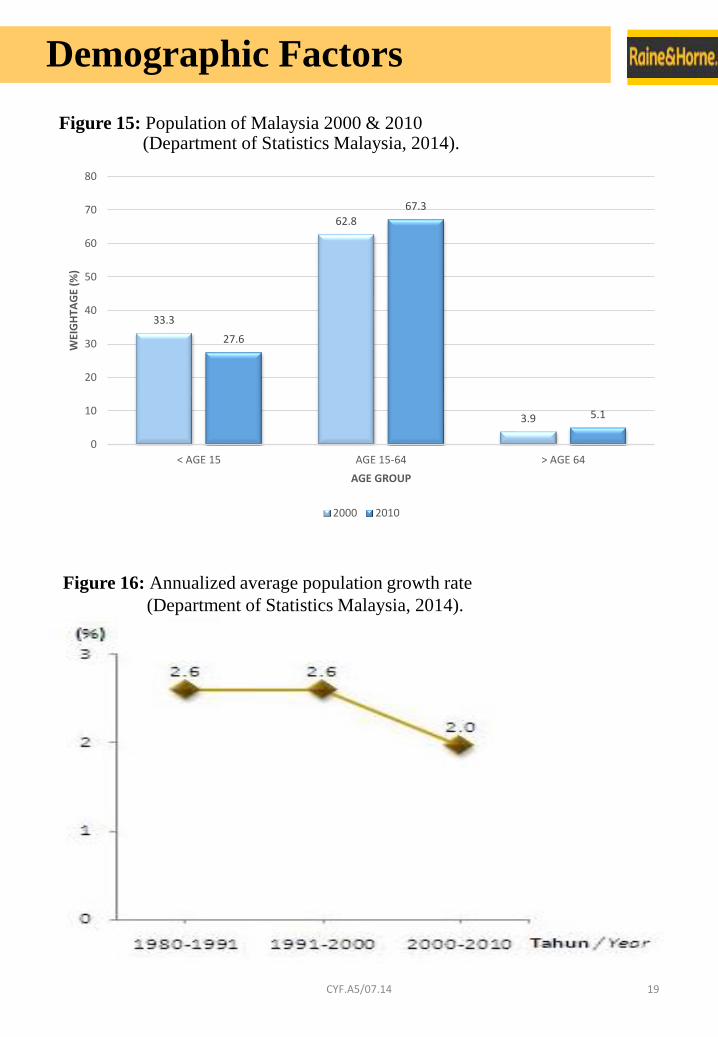

Figure 15: Population of Malaysia 2000 & 2010 (Department of Statistics Malaysia, 2014).

33.3

62.8

3.9

27.6

67.3

5.1

0

10

20

30

40

50

60

70

80

< AGE 15 AGE 15-64 > AGE 64

WEI

GH

TAG

E (%

)

AGE GROUP

2000 2010

Figure 16: Annualized average population growth rate

(Department of Statistics Malaysia, 2014).

CYF.A5/07.14

Demographic Factors

20

Population Growth Rate

Malaysia’s population is aging slowly (early stages); with lower portion of

children age group (< age 15) in 2010 compared to 2000. Working age adults

and retirement segments have increased by 4.5% and 1.2% respectively. Median

age has increased from 23.6 (2000) to 26.2 (2010); which is still a relatively

young population. Annualized average growth rate was stable at 2.6% from

1980 to 2000. A decline was observed from the subsequent period (2000 to

2010); to 2.0%.

The country’s dependency ratio has dropped from 0.59 (2000) to 0.49 (2010),

reinforcing the fact that:

1. population growth is slowing

2. children age group is diminishing (entering the age of workforce)

3. working age group is increasing

4. more working adults are supporting the non-working classes (children and

elders).

Refined grouping

Classification of the population in Malaysia was further refined to selective age

groups; to provide a better appraisal of the domestic workforce.

37.53

54.61

7.86

< AGE 20 AGE 20-59 > AGE 59

WEI

GH

TAG

E (%

)

AGE GROUP

2010

Figure 17: Refined population grouping 2010

(Department of Statistics Malaysia, 2014).

CYF.A5/07.14

Demographic Factors

21

Figure 18: Demographics by age group 2010

(Department of Statistics Malaysia, 2014).

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

0-19 20-29 30-39 40-49 50-59 60-75+

PO

PU

LATI

ON

AGE GROUP

POPULATION COUNT

KELANTAN, 1.16

TERENGGANU, 1.07

PERLIS, 1.01

KEDAH, 0.96

PAHANG, 0.96

SABAH, 0.93

PERAK, 0.93

SARAWAK, 0.91

MELAKA, 0.90

NEGERI SEMBILAN, 0.84

MALAYSIA, 0.83

JOHOR, 0.78

LABUAN, 0.74

PULAU PINANG, 0.73

SELANGOR, 0.65

KUALA LUMPUR, 0.62

PUTRAJAYA, 0.59

0.00 0.20 0.40 0.60 0.80 1.00 1.20 1.40

Figure 19: Dependency ratio by state 2010 (using refined grouping)

(Department of Statistics Malaysia, 2014).

CYF.A5/07.14

Demographic Factors

22

Refined grouping (Cont’d)

The refined grouping has increased the interval range for both children

(< 20 age) and retirees (> 59 age) by 5 years each. Hence, the number and range

of working adults (20 – 59 age) decreased by 10 years in total. As depicted in

Figure 17, the share of working adults was reduced to 54.6% of the total

population from the previous unrefined reading of 67.3%.

Further dissection of the working age group has reinforced the point that the

Malaysian workforce is indeed very young; with the highest percentage in the

20 – 29 age group, followed by 30 – 39. These 2 groups are ages of greatest

household formations.

Such refined grouping has increased the country’s dependency ratio to 0.83

from the initial calculation of 0.49. According to Figure 19, it was noted that a

total of 6 states in the country had better dependency ratio compared to the

national average. As expected, they include the more developed states; led by

Putrajaya (0.59), Kuala Lumpur (0.62), Selangor (0.65), Pulau Pinang (0.73),

Labuan (0.74), and Johor (0.78). Almost all of these states had received the

deserving attention from developers and buyers alike.

Whereas those with dependency ratio slightly below the national reading such

as Negeri Sembilan (0.84) and Melaka (0.90); was starting to command interest

from developers due to overcrowding of the respective markets as stated above.

CYF.A5/07.14

Demographic Factors

23

Figure 20: Distribution of Malaysian population by state 2010.

Figure 21: Urbanization rate by state 2010

(Department of Statistics Malaysia, 2014).

SELANGOR21%

SABAH12%

JOHOR9%

SARAWAK9%

PERAK7%

KEDAH7%

KUALA LUMPUR6%

PULAU PINANG6%

PAHANG5%

KELANTAN5%

TERENGGANU4%

NEGERI SEMBILAN3%

MELAKA3%

PERLIS1%

LABUAN0%

PUTRAJAYA0%

KELANTAN, 42.4

PAHANG, 50.5

PERLIS, 51.4

SARAWAK, 53.8

SABAH, 54.0

TERENGGANU, 59.1

KEDAH, 64.6

NEGERI SEMBILAN, 66.5

PERAK, 69.7

MALAYSIA, 71.0

JOHOR, 71.9

LABUAN, 82.3

MELAKA, 86.5

PULAU PINANG, 90.8

SELANGOR, 91.4

KUALA LUMPUR, 100.0

PUTRAJAYA, 100.0

0.0 20.0 40.0 60.0 80.0 100.0 120.0

CYF.A5/07.14

Demographic Factors

24

Figure 22: Population density (person/km2) 2010

(Department of Statistics Malaysia, 2014).

Figure 23: Household size 2010 (Department of Statistics Malaysia, 2014).

SARAWAK, 19

PAHANG, 40

SABAH, 42

TERENGGANU, 78

MALAYSIA, 86

KELANTAN, 97

PERAK, 110

NEGERI SEMBILAN, 150

JOHOR, 174

KEDAH, 199

PERLIS, 280

MELAKA, 470

SELANGOR, 674

LABUAN, 950

PUTRAJAYA, 1,478

PULAU PINANG, 1,500

KUALA LUMPUR, 6,891

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000

SABAH, 5.88

KELANTAN, 4.86

TERENGGANU, 4.78

LABUAN, 4.72

PAHANG, 4.59

SARAWAK, 4.47

MALAYSIA, 4.31

KEDAH, 4.29

PERLIS, 4.26

NEGERI SEMBILAN, 4.20

JOHOR, 4.17

MELAKA, 4.05

PERAK, 4.04

PULAU PINANG, 3.94

SELANGOR, 3.93

KUALA LUMPUR, 3.72

PUTRAJAYA, 3.45

0.00 1.00 2.00 3.00 4.00 5.00 6.00 7.00

CYF.A5/07.14

Demographic Factors

25

Distribution

The top 5 states in Malaysia in regards to number of inhabitants were Selangor

(21%), Sabah (12%), Johor (9%), Sarawak (9%), and Perak (7%). Some of the

reasons as to why Sabah, Sarawak, and Perak were less favored by developers

include the vast land size compared to the number of population; resulting in

low population density, relatively poor infrastructures, low rate of urbanization,

and unfavorable dependency ratio.

Urbanization

Malaysia recorded a fairly moderate urbanization rate of 71.0% in 2010.

Mimicking the chart of dependency ratio; with both the Federal Territories in

Peninsular Malaysia posted 100.0% urbanization rate. Other usual members

above the national average were Selangor (91.4%), Pulau Pinang (90.8%),

Labuan (82.3%) , and Johor (71.9%). The only surprise was Melaka which

came in 86.5%.

Density

Malaysia has a low population density ratio coming in at just 86 person/km2.

This suggests that the nation’s population is not evenly distributed with

concentrations in a few selective states. The most dense state is Kuala Lumpur

(6,891 person/km2: comparable to Singapore and Hong Kong), followed by

Pulau Pinang (1,500 person/km2), Putrajaya (1,478 person/km2), Labuan

(950 person/km2), Selangor (674 person/km2), and Melaka (470 person/km2).

The degree of density usually dictates the type of houses offered by developers.

Household Size

Malaysia has a fairly large household size of 4.31 person/household. It is

anticipated that there could be a high possibility of smaller household size in the

future. Such a reduction in the number of person per household would directly

increase the demand for new living quarters and strain the existing housing

stock in the market. In addition, smaller household size would translate into

demand for smaller residential units as well.

CYF.A5/07.14

Micro Factors

26

As revealed earlier, macro drivers affect the property market at a national scale,

while micro drivers emphasize on local conditions of the subject property. The

main equation of hedonic regression by Wheatley (2012) are as follow:

P = f (L, T, S, V, N)

P: price of house

f: function of

L: location characteristics

T: house characteristics

S: plot size

V: surrounding view

N: neighbourhood characteristics

The above equation proposed that the price of house is a function of several

local variables such as location characteristics, house characteristics, plot size,

surrounding view and neighbourhood characteristics. These factors usually

adhere to a general guideline but in some instances, may subject to personal

preference.

In common, a house could usually command a higher price by locating in close

proximity to commercial and recreational areas, possessing superior building

quality and design, built on a larger land size, surrounded by ideal view such as

lush sceneries or unobstructed view of the city, and enclosed in a clean and safe

neighbourhood.

Buyers would be more willing to pay a higher price for the house if these

related characteristics matched their individual expectations and preferences.

CYF.A5/07.14

References

Bank Negara Malaysia (BNM). (2014) Rates & Statistics, Kuala Lumpur: BNM

Publications, [Online], Available:

http://www.bnm.gov.my/index.php?ch=statistic&lang=en [18 Jun 2014].

CNBC. (2014) KLSE Property Index, [Online], Available:

http://data.cnbc.com/quotes/PROPERTIES/tab/2 [1 July 2014].

Department of Statistics Malaysia. (2014) Gross domestic product at current

prices, [Online], Available:

http://www.statistics.gov.my/portal/index.php?option=com_content&view=artic

le&id=2261 [18 Jun 2014].

Department of Statistics Malaysia. (2014) Statistical Releases, [Online],

Available: http://www.statistics.gov.my/portal/index.php?option=

com_content&view=article&id=472&Itemid=111&lang=en&negeri=Malaysia

[15 Jun 2014].

EPF. (2014) Dividend Rates, [Online], Available:

http://www.kwsp.gov.my/portal/about-epf/investment-highlights/dividend-

rates/dividend-rates [18 Jun 2014].

Freddie Mac. (2014) 30-Year Fixed-Rate Mortgages, [Online], Available:

http://www.freddiemac.com/pmms/pmms30.htm [18 Jun 2014].

JPPH. (2014) Property Market Report 2013, Putrajaya: Valuation and Property

Services Department.

Kaplan University. (2013) Schwesernotestm 2014 CFA Level I Book 2:

Economics, United States of America: Kaplan Inc.

NAPIC. (2014) Key Statistics, [Online], Available:

http://napic.jpph.gov.my/portal [15 Jun 2014].

The Star Online. (2012). ‘A second chance for bankrupts’, The Star Online, 9

December, [Online], Available:

http://www.thestar.com.my/story.aspx/?file=%2f2012%2f12%2f9%2fnation%2f

12434811&sec=nation [18 Jun 2014].

27CYF.A5/07.14

References

The Star Online. (2014). ‘Malaysia's rising household debt hits new record of

86.8% of GDP’, The Star Online, 20 March, [Online], Available:

http://www.thestar.com.my/business/business-news/2014/03/20/rising-

household-debt-it-hits-new-record-of-868-of-gdp-on-loans-for-properties-and-

motor-vehicles/ [18 Jun 2014].

Trading Economics. (2014) Malaysia Economic Indicators, [Online], Available:

http://www.tradingeconomics.com/malaysia/indicators [18 Jun 2014].

Wheatley D. (2012) Hedonic Pricing Method, [Online], Available:

http://www.cbabuilder.co.uk/Quant5.html [18 Jun 2014].

28CYF.A5/07.14

Contact us

29

OFFICE EMAIL TELEPHONE

HQ (KL) [email protected] 603 26980911

Petaling Jaya [email protected] 603 78806542

Subang Jaya [email protected] 603 56319668

Klang [email protected] 603 33420193603 33420182

Ipoh [email protected] 605 2532804605 2413888

Seremban [email protected] 606 6333211

Melaka [email protected] 606 2860017606 2840017

Penang [email protected] 604 2638093604 2612032

Johor Bahru [email protected] 607 3863791607 3863795

Kuantan [email protected] 609 5157100

Kuching [email protected] 6082 235236

Kota Kinabalu [email protected] 6088 266520

CYF.A5/07.14

International Affiliations

30

Country Affiliates

Australia

Corporate Office – SydneyNew South Wales – Sydney

Queensland –BrisbaneVictoria - Melbourne

South Australia – Kent TownTasmania – Hobart

Western Australia – South PerthNorthern Territory – Parap

Austria DMH Vienna

Belgium Activia Belgium SA

Czech Republic Huber Holdings Prag s.r.o

Fiji Raine & Horne Fiji

Hong Kong Raine & Horne Projects Hong Kong

Hungary Dr. Max Huber Kft.

India Arora & Associates Realty Ltd.

Italy GC International S.R.L.

JapanKiuchi Property Counselors & Valuers

Inc

United Kingdom Raine & Horne Crossgates

UAE Raine & Horne Dubai

Vanuatu Raine & Horne Vanuatu

CYF.A5/07.14

Raine & Horne International Zaki + Partnerswww.raineandhorne.com.my

Perpetual 99, Jalan Raja Muda Abdul Aziz, 50300 Kuala Lumpur

Tel: 03-2698 0911 Fax: 03-2691 1959 Email: [email protected]

Company No. 99440-T, VE (1) 0067

31