Embed Size (px)

Citation preview

Downing Indian Solar EIS - Terms & Conditions 1Downing Renewables EIS 1

DowningIndian Solar EIS

Terms & Conditions

Downing Indian Solar EIS - Terms & Conditions2

Important notice

If you are in any doubt about the content of this terms and conditions document (the “Terms”) and/or any action that you should take, you are strongly recommended to seek advice immediately from an independent financial adviser authorised under the Financial Services and Markets Act 2000 (“FSMA”) who specialises in advising on opportunities of this type. Nothing in the Terms constitutes investment, tax, legal or other advice by Downing LLP (“Downing” or “Manager”) and your attention is drawn to the section headed “Risk factors” on page 8 to 11 of this document. An investment through Downing Indian Solar EIS (the “Service”) will not be appropriate for all recipients of these Terms.

The Indian Solar Brochure, Terms and Application Form constitute a financial promotion pursuant to Section 21 of the FSMA and are issued by Downing LLP, Ergon House, Horseferry Road, London SW1P 2AL, which is authorised and regulated by the Financial Conduct Authority in the United Kingdom.

For the purposes of the Alternative Investment Fund Managers Directive (AIFMD), we have been advised that the collection of portfolios which are managed on a collective basis constitute an alternative investment fund (AIF). Downing LLP has been appointed as the Alternative Investment Fund Manager of the Service.

Any references to tax laws or levels in the Terms are subject to change and personal circumstances. Past performance is not a guide to future performance and may not be repeated. The value of shares can go down as well as up and you may not get back the full amount invested. You should consider an investment through this Service as a medium to long term investment. Investments made by the Service are likely to be illiquid.

No person has been authorised to give any information, or to make any representation, concerning the Service other than the information contained in these Terms, the Brochure and the Application Form and, if given or made, such information or representation must not be relied upon. The Terms do not constitute a direct offer to sell or a solicitation of an offer to purchase securities and in particular does not constitute an offering in any state, country or other jurisdiction where, or to any person or entity to whom, an offer or sale would be prohibited.

Applications will only be accepted is submitted through an FCA authorised intermediary, whose details are completed in section 7 of the Application Form.

The Terms contain information relating to an investment through the Service. An investment may only be made on the basis of these Terms (in particular, the Investor Agreement), the Brochure and the Application Form. Downing has taken all reasonable care to ensure that the facts stated in the Terms are true and accurate in all material respects and that there are no other material facts whose omission would make any statement of fact or opinion in the Terms misleading. All statements of opinion or belief contained in the Terms and all views expressed and statements made regarding future events represent Downing’s own assessment and interpretation of information available to it as at the date of the Terms. No representation is made or assurances given that such statements or views are correct or that the objectives of the Service will be achieved. Prospective investors must determine for themselves what reliance (if any) they should place on such statements, views or forecasts, and no responsibility is accepted by Downing in respect thereof.

If you have any questions, please call us on 020 7416 7780. For UK investors onlyInformation correct as at 15 December 2015

Downing Indian Solar EIS - Terms & Conditions 3

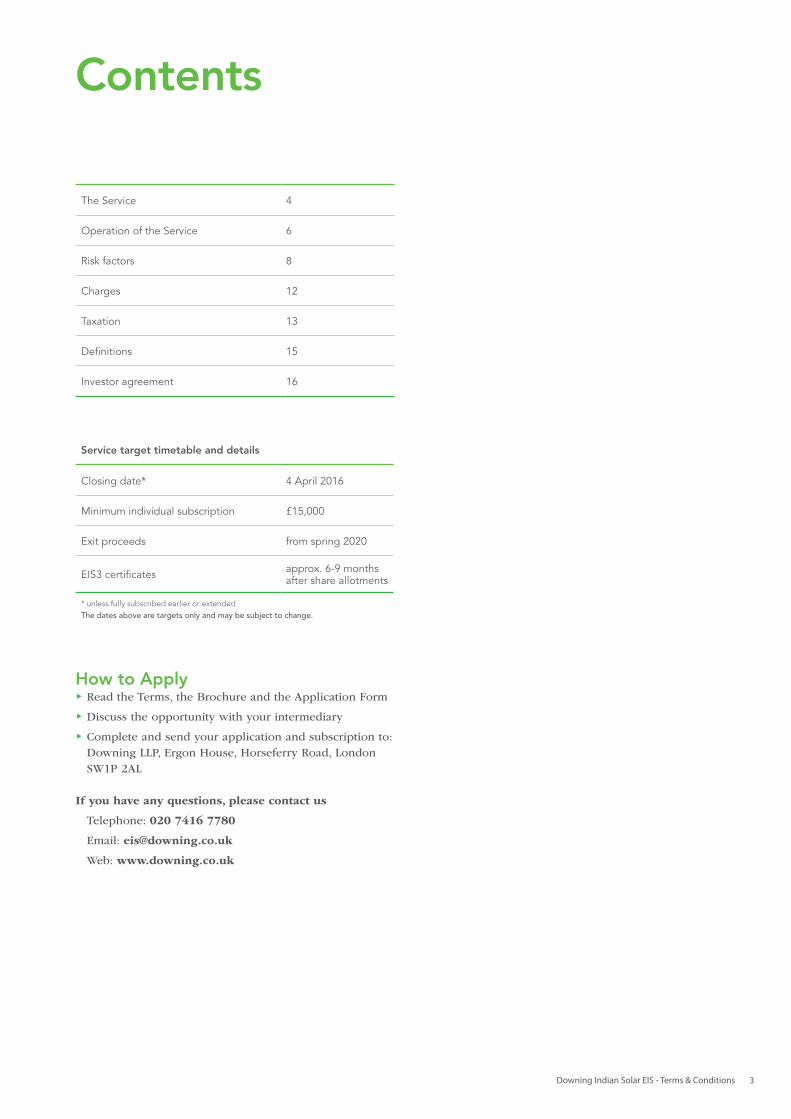

How to Applyff Read the Terms, the Brochure and the Application Form

ff Discuss the opportunity with your intermediary

ff Complete and send your application and subscription to: Downing LLP, Ergon House, Horseferry Road, London SW1P 2AL

If you have any questions, please contact us

Telephone: 020 7416 7780

Email: [email protected]

Web: www.downing.co.uk

Contents

The Service 4

Operation of the Service 6

Risk factors 8

Charges 12

Taxation 13

Definitions 15

Investor agreement 16

Service target timetable and details

Closing date* 4 April 2016

Minimum individual subscription £15,000

Exit proceeds from spring 2020

EIS3 certificates approx. 6-9 months after share allotments

* unless fully subscribed earlier or extendedThe dates above are targets only and may be subject to change.

Downing Indian Solar EIS - Terms & Conditions4

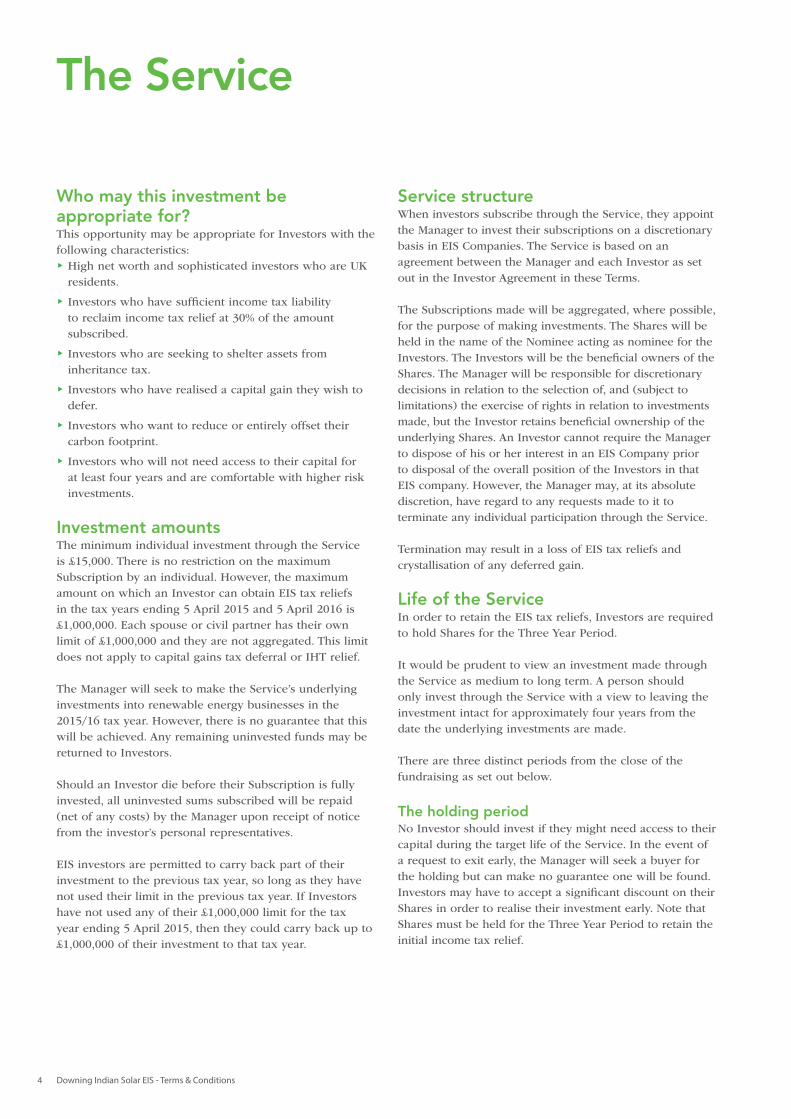

The Service

Who may this investment be appropriate for?This opportunity may be appropriate for Investors with the following characteristics:ff High net worth and sophisticated investors who are UK residents.

ff Investors who have sufficient income tax liability to reclaim income tax relief at 30% of the amount subscribed.

ff Investors who are seeking to shelter assets from inheritance tax.

ff Investors who have realised a capital gain they wish to defer.

ff Investors who want to reduce or entirely offset their carbon footprint.

ff Investors who will not need access to their capital for at least four years and are comfortable with higher risk investments.

Investment amountsThe minimum individual investment through the Service is £15,000. There is no restriction on the maximum Subscription by an individual. However, the maximum amount on which an Investor can obtain EIS tax reliefs in the tax years ending 5 April 2015 and 5 April 2016 is £1,000,000. Each spouse or civil partner has their own limit of £1,000,000 and they are not aggregated. This limit does not apply to capital gains tax deferral or IHT relief.

The Manager will seek to make the Service’s underlying investments into renewable energy businesses in the 2015/16 tax year. However, there is no guarantee that this will be achieved. Any remaining uninvested funds may be returned to Investors.

Should an Investor die before their Subscription is fully invested, all uninvested sums subscribed will be repaid (net of any costs) by the Manager upon receipt of notice from the investor’s personal representatives.

EIS investors are permitted to carry back part of their investment to the previous tax year, so long as they have not used their limit in the previous tax year. If Investors have not used any of their £1,000,000 limit for the tax year ending 5 April 2015, then they could carry back up to £1,000,000 of their investment to that tax year.

Service structureWhen investors subscribe through the Service, they appoint the Manager to invest their subscriptions on a discretionary basis in EIS Companies. The Service is based on an agreement between the Manager and each Investor as set out in the Investor Agreement in these Terms.

The Subscriptions made will be aggregated, where possible, for the purpose of making investments. The Shares will be held in the name of the Nominee acting as nominee for the Investors. The Investors will be the beneficial owners of the Shares. The Manager will be responsible for discretionary decisions in relation to the selection of, and (subject to limitations) the exercise of rights in relation to investments made, but the Investor retains beneficial ownership of the underlying Shares. An Investor cannot require the Manager to dispose of his or her interest in an EIS Company prior to disposal of the overall position of the Investors in that EIS company. However, the Manager may, at its absolute discretion, have regard to any requests made to it to terminate any individual participation through the Service.

Termination may result in a loss of EIS tax reliefs and crystallisation of any deferred gain.

Life of the ServiceIn order to retain the EIS tax reliefs, Investors are required to hold Shares for the Three Year Period.

It would be prudent to view an investment made through the Service as medium to long term. A person should only invest through the Service with a view to leaving the investment intact for approximately four years from the date the underlying investments are made.

There are three distinct periods from the close of the fundraising as set out below.

The holding periodNo Investor should invest if they might need access to their capital during the target life of the Service. In the event of a request to exit early, the Manager will seek a buyer for the holding but can make no guarantee one will be found. Investors may have to accept a significant discount on their Shares in order to realise their investment early. Note that Shares must be held for the Three Year Period to retain the initial income tax relief.

Downing Indian Solar EIS - Terms & Conditions 5

The exit period It is the Manager’s intention to offer Investors an opportunity to exit the Service after approximately four years. There are no arrangements for this, and no guarantee that it will be achieved. Possible exit routes include a Share buyback at net asset value, which might be funded by:

i. Selling renewable energy installations; and/or

ii. Raising new equity or debt.

Retaining the investment As an alternative to exiting after four years, it is intended that Investors will be offered the opportunity to remain in the Service, with annual exit opportunities thereafter, subject to liquidity. Details of the terms of “rolling over” will be provided prior to the exit opportunity.

In the event that an insufficient number of Investors wish to remain in the Service to make it economically viable, then the Service’s businesses will be sold, the Service closed, and the proceeds returned to Investors.

WithdrawalsPartial withdrawals from the Service are not permitted. However, Investors may terminate their Investor Agreement and make an early withdrawal from the Service by transferring their shareholdings in the EIS Companies into their own names. Please note that if a disposal of Shares to a third party occurs before the end of the Three Year Period, Investors will have to repay the initial income tax relief (if it has been claimed). Any deferred gains will crystallise on a disposal of Shares at any time.

The Manager will have a lien on all assets being withdrawn by an Investor and shall be entitled to dispose of some or all of the same and apply the proceeds in discharging that Investor’s liability to the Manager in respect of damages or accrued but unpaid fees including any Performance Incentive accrued until the time of withdrawal. The balance of any sale proceeds and control of any remaining investments will then be passed to the Investor.

Downing Indian Solar EIS - Terms & Conditions6

Operation of the Service

Client accountInvestors’ Subscriptions will be held in the Custodian’s aggregated client account prior to investment in EIS Companies and, following the realisation of investments in EIS Companies, prior to the distribution of proceeds to Investors. The interest arising therefrom will be paid to the Manager and Custodian as a contribution towards the costs of establishing the Service.

All documents of title will be held by the Nominee and will be registered in the name of the Nominee.

AllocationsThe Manager will maintain accounts which will be open to inspection by each Investor showing the amount contributed by that Investor and the amounts invested and yet to be invested on that Investor’s behalf.

The number of shares in each EIS Company allocated to a particular Investor shall, where possible, be calculated by reference to the proportion which the Investor’s Subscription bears to the total Subscriptions by all Investors at the time the investment is made. However, this may not always be possible where investments are made from funds received from early Investors. It is intended that monies received from each Investor will be invested on a pro-rata basis to his or her Subscription, as investment opportunities arise. Variations to this standard procedure will occur to avoid issuing fractions of shares, or, for example, where the Manager has received special instructions from an Investor or if an Investor is subject to professional rules preventing him or her from making an investment in a particular EIS Company.

Investment in selected companiesWhen the Manager has selected an appropriate EIS Company, and appropriate terms and conditions have been negotiated, it will subscribe for new shares in the EIS Company on behalf of Investors.

Share certificates will be issued in the name of the Nominee. Any dividends received by the Custodian or the Nominee from EIS Companies will be forwarded directly to Investors according to the instructions of the Manager. The Manager does not anticipate any dividends being paid by the EIS Companies during at least the first four years from investment.

Investment agreementAs a precondition of investment, each EIS Company will normally be required to enter into an investment monitoring agreement regulating, to the extent possible, the conduct of its business. This agreement will normally remain in place until the investment is realised. The agreement will normally give the Manager the right to nominate a director to the board of the EIS Company and will require the supply of regular management accounts and other information to the Manager to enable it to monitor the EIS Company.

Until a realisation is achieved, the Manager will seek to ensure that EIS Companies comply with the EIS rules and are appraised of the consequences should the relief be withdrawn. Tax relief may be withdrawn in certain circumstances and neither the Manager nor the Custodian accepts any liability for any loss or damage suffered by any Investor or other person in consequence of such relief being withdrawn or reduced. In this regard, Investors are strongly advised to read the risk factors set out on page 8 in this document.

Documentation and communicationEach Investor will receive from the Manager a contract note detailing each new investment made on their behalf as these occur.

The Manager will also send each Investor half-yearly reports, containing details of all investments made by the Service, together with a commentary on the progress of each of those investments.

Following HMRC clearance for each EIS Company, Investors will be provided with an EIS3 certificate, in the form required by HMRC, which may be used to claim tax reliefs, subject to each Investor’s personal circumstances.

The Custodian and NomineeBy completing the Application Form, prospective Investors will, inter alia, be deemed to have agreed to the Custodian being appointed by the Manager to exercise the powers, and to carry out duties, on behalf of the Manager in accordance with the provisions of this paragraph, which are as follows:

(a) Function

The function of the Custodian will be to exercise the powers and duties which are conferred upon it by the terms of these Terms (including this paragraph).

Downing Indian Solar EIS - Terms & Conditions 7

(b) Restrictions on transfer

(i) The Custodian shall not be obliged to recognise the title of any person in whom an interest in shares in any EIS Company shall have become vested unless a properly validated notice or evidence of that person’s entitlement shall have been produced to the Custodian.

(ii) The Custodian shall not be obliged to recognise any transfer or assignment of an interest in the Shares to any person unless such person shall have first agreed to enter into a transfer or assignment in a form approved by the Manager which shall incorporate an undertaking that such person will be bound by the terms of this paragraph.

(c) Custodian’s and Nominee’s obligations and powers

(i) The Manager will bank cheques on behalf of the Custodian into one or more of its FCA approved designated client money bank accounts held by the Custodian on behalf of the Investor, where the Custodian will securely hold the aggregated cleared funds.

(ii) The Custodian will make payments from these client money accounts in accordance with proper instructions received from the Manager as relied upon under the FCA rules upon the purchase and delivery of securities providing the instructions comply with FCA rules. It is the responsibility of the Manager, not the Custodian or the Nominee, to ensure that appropriate investments are made.

(iii) All appropriate securities will be registered in the name of the Nominee and will be physically delivered to the Custodian.

(iv) The Custodian will hold the securities for safe keeping in its safe, or may at its discretion place them in the vault of an FCA authorised UK bank, held to the order of the Nominee.

(v) The Custodian will upon receipt of instructions from the Manager together with simultaneous or advanced receipt of sale proceeds, deliver securities as directed by the Manager.

(vi) In order to safeguard Investors’ assets the Custodian will not deliver cash without receipt of securities or securities without receipt of cash to any third party including the Manager, unless such securities are held in a solicitors’ client account to be released to the Custodian on receipt of the share certificate by the solicitors. The Custodian may at its sole discretion agree to place the securities with an approved firm of solicitors in England, held to the order of the Nominee, pending receipt of funds by the Custodian.

(vii) Following the sale of the Shares, the Manager will instruct the Custodian to distribute the monies held to the Investors. The Custodian will transfer funds to the Investors’ bank accounts in accordance with proper instructions from the Manager.

(viii) The Custodian will be authorised, on the instruction of the Manager, to exercise voting, pre-emption or similar rights in relation to the Shares in accordance with the Articles of Association of the EIS Companies or any agreement entered into in connection with the subscription for the Shares, and to deal with any rights relating to any share issue made or proposed by an EIS Company; and

(ix) The Custodian will seek to ensure that any dividends shall be paid direct to the Investors. In the event that any money in relation to the Shares is received by the Custodian it shall pay such money or monies’ worth to the Investors subject to any legal obligations on the Custodian to make retentions for payment of tax and/or fees and expenses payable to the Manager.

(d) Appointment of new Custodian

The Manager may at any time accept the resignation of, or remove, the Custodian, subject to the terms of the agreement between the Manager and the Custodian, and appoint a new Custodian in its place, on behalf of the Investors.

(e) Investment

The Custodian may place any monies for the time being held by it on deposit with any bank or building society.

(f) Indemnity

By completing the Application Form, each Investor indemnifies Downing (in proportion to each Investor’s respective interest in the Shares at the date of the indemnity claim) against any claim made against it by the Custodian and/or Nominee resulting from any and all direct liabilities, obligations, losses, damages, penalties, actions against the Custodian, proper costs and expenses or disbursements of the Custodian (other than those resulting from the fraud, negligence, wilful default or breach of contract on the part of the Custodian) which may be imposed on, incurred by or asserted against the Custodian in properly performing its obligations or duties as a custodian of the Investor’s Shares (under such custody agreement in force from time to time between Downing and the Custodian).

Downing Indian Solar EIS - Terms & Conditions8

Risk factors

Prospective Investors should be aware that the value of Shares in an EIS Company can fluctuate. In addition, there is no guarantee that the valuation of the Shares will fully reflect their underlying net asset value, or that Investors will be able to buy and sell at that valuation or at all.

An investment made through the Service is subject to a number of risks. Before making any investment decision, prospective Investors should consider carefully the risks attached to investing through the Service together with all other information contained in these Terms, including, in particular, the risk factors described below. This information does not purport to be exhaustive and the risks below are not set out in order of priority. Additional risks and uncertainties not presently known to the Manager, or that the Manager currently deems to be immaterial, may also have an adverse effect on the business of the EIS Companies. Investors should consider carefully whether an investment made through the Service is appropriate for them in light of the information in the Brochure and their personal circumstances.

ff Valuations of unquoted companies are determined by the Manager. However, as the Investor’s portfolio will be holdings in small unquoted companies with very limited or no historical performance track record, such valuations will include a high degree of judgement, and the actual proceeds generated from the disposal of the Investor’s interest in any EIS Company may materially differ from the Investor’s carrying value prior to the disposal.

ff The value of the Shares may go up or down. Investors may not get back the full amount invested. There is no market, nor is there intended to be a market, in the Shares. As such, the Shares will not be readily realisable. It is not intended that any income or capital will be returned to Investors during the Three Year Period. After holding the Shares in the EIS Companies for the Three Year Period, it may still be difficult to realise the Shares or to obtain reliable information about their value.

ff The performance of investments made through the Service is dependent on the Manager’s ability to identify appropriate EIS Companies undertaking appropriate EIS Trades. In addition, the investment timetable may not be achieved, which would delay the availability of EIS tax reliefs, or, in some cases, result in the loss of EIS tax reliefs. In some circumstances a delay could cause certain Investors to lose the opportunity to defer gains which occurred more than three years prior to investment in EIS Companies.

ff Past performance is not a guide to the future performance of an investment made through the Service.

ff There are circumstances in which an Investor could cease to qualify for the taxation advantages offered by the EIS Company. If an EIS Company ceases to carry on an EIS Trade during the Three Year Period, this could prejudice its qualifying status under the EIS. In addition, if an EIS Company does not employ the funds made available to it within the deadlines set out in the EIS rules, it would be in breach of these rules and tax reliefs would be withdrawn. The situation will be closely monitored with a view to preserving each EIS Company’s EIS status, but this cannot be guaranteed.

ff A failure of an EIS Company to meet the qualifying requirements for the EIS could result in:

(i) Investors being required to repay the 30% income tax relief received on Subscription and interest on the same;

(ii) a liability to capital gains tax on a disposal of Shares; and

(iii) any deferred gain crystallising.

ff Where practicable, provisional approval that each EIS Company’s activities should qualify under the EIS will be sought from HMRC prior to investment. However, there can be no guarantee that the EIS tax reliefs will be available. In such circumstances, subscription monies will not be returned to investors.

ff A sale of Shares in any EIS Company within the Three Year Period will result in the 30% income tax relief available upon investment in those Shares becoming repayable and a liability to CGT on the disposal may arise.

ff It is possible for Investors to lose their EIS tax reliefs and/or CGT deferral relief and/or IHT relief by taking or not taking certain steps; Investors are advised to take appropriate independent professional advice on the tax aspects of their investment.

ff The investments will be limited to a very small number of EIS Companies (1-2), all investments are intended to be in renewable opportunities located in the same geographical area. Therefore, there will be limited diversification (if any) which could increase concentration risk for Investors.

ff The information in these Terms is based upon current taxation, other legislation and HMRC practice, and any changes in the legislation or HMRC practice may affect the value of an investment. In particular, if CGT rates increase then those Investors who choose to defer a gain may face a higher CGT liability when the deferred gain comes back in to charge following an exit. The value of the tax reliefs will depend on the individual circumstances of Investors.

Downing Indian Solar EIS - Terms & Conditions 9

considers this to be appropriate to seek to mitigate any financial loss to the EIS Company. However, in the event of the capital equipment being damaged the insurance may not cover the EIS Company’s total financial loss, resulting in a material adverse effect on the return from an investment.

ff Development partners: The projects developed by the EIS Companies are likely to be constructed and operated in co-operation with one or more development partners. Such development partners may be involved in sourcing opportunities, in submitting planning applications, or in the supply, operation and maintenance of equipment. The ability of the Manager to maintain existing partnerships and develop new partnerships will be key to the performance of an investment. If disputes were to occur between the EIS Companies and one or more of its partners, or if one or more partnerships were to terminate, this could have a material adverse effect on the return from an investment.

ff Permits and authorisation: Renewable energy businesses require various permits and authorisations. It is not intended that any EIS Company will take any development risk prior to construction. However, certain issues may arise after construction has commenced and the Service has committed funds. This could have a material adverse effect on the return from an investment. Having received the required permits, the EIS Company may fail to comply with the necessary conditions of the permits and a permit could be revoked, suspended or delayed. The loss or suspension of a permit in any of the EIS Companies could have a material adverse effect on the return from an investment.

ff Environmental claims and liabilities: Although the Manager will expect all the EIS Companies to make provisions to meet all known and anticipated environmental claims and liabilities, if any, there can be no assurance that additional costs and liabilities will not be incurred in the future, or that injunctions by environmental regulators will not result in business interruptions, and that these factors, either in isolation or together, may have a material adverse effect on the return from an investment. More generally, environmental laws and regulations will have an impact on the activities of the EIS Companies. It is not possible to accurately predict the effects of future changes in such laws and regulations on the financial condition and results of the EIS Companies. There can be no assurance that material costs and liabilities will not be incurred.

Specific industry risksff Availability of supply of equipment: EIS Companies

may be unable to secure the timely supply of equipment. This could delay the installation of projects and increase the capital cost of the projects and, therefore, delay or reduce financial returns from the EIS Companies.

ff Reliability of equipment: Mechanical failure or other defects or accidents which result in non-performance or under-performance of equipment will have a negative impact on the revenue and profitability of an EIS Company.

ff Warranties: An EIS Company may be the beneficiary of warranties or guarantees given by an equipment supplier, but warranties and guarantees typically only apply for a limited duration and can exclude some causes of project non-availability, such as scheduled and unscheduled grid outages. Component suppliers may be unable to meet their warranty obligations in respect of components, in whole or in part, because of production, economic or financial difficulties, or other reasons. Such circumstances could cause the EIS Companies to experience increased costs which could have a material adverse effect on the return from an Investment. Many of the suppliers of small scale renewable technologies are relatively small companies, which may be unable to provide spare parts or meet warranty claims if their technology fails. The Manager will seek to mitigate this risk by focusing on EIS Companies seeking to use market leading suppliers where this risk is considered to be lower.

ff Construction: Prior to the construction and operating phase of a project the Manager expects that EIS Companies will enter into agreements with third-party professionals and independent contractors and other companies to provide the required construction, installation and maintenance services. If such contracted parties are not able to fulfil their contractual obligations, EIS Companies may be forced to provide additional resources to complete their work, or to engage other companies to complete the work, which may be on different terms. Any financial difficulty, breach of contract or delay in services by these third-party professionals and independent contractors could have a material adverse effect on the return from an investment.

ff Insurance: The capital equipment owned by the EIS Companies may be damaged as a result of, inter alia, natural disasters (e.g. lightning strikes), accidents (e.g. fire), or vandalism. The Manager will seek to ensure that the EIS Company insures these risks where it

Downing Indian Solar EIS - Terms & Conditions10

ff Illiquid shares: The Manager believes that by investing in a portfolio of broadly similar renewable energy generating assets, the EIS Companies can be packaged up and sold as an entire portfolio to either a financial investor or an energy company. Despite its best efforts, the Manager may not be able to find a purchaser for the investment portfolio.

ff Electricity price inflation: Investee Companies are unable to fix the sales price of the electricity generated for the entire operating life of the power plant. In the event that electricity prices rise more slowly than forecast in the financial model used by Investee Companies, or even fall, there may be a financial loss to Investors. There is a risk that one or more of the Investee Companies’ Power Purchase Agreement (‘PPA’) customers could fail which would invalidate the relevant PPA. In this case, the Investee Companies would look to terminate the PPA and sell the power to a new third party.

ff Insolvency of the Engineering, Procurement and Construction (‘EPC’) contractor during installation: The Investee Companies will be paying their EPC contractors against milestones. At times during the construction period Investee Companies may have paid more in milestone payments than the value of the works installed. Further, the EPC contractor may use the funds paid to it by Investee Companies for purposes other than, for example, making deposits on the equipment required for the construction of the relevant farm. Where this is the case, and the EPC contractor were then to go into insolvency, Investee Companies could suffer financial loss. Additional risks also include poor quality installations, which could result in warranties from the manufacturer of the equipment being invalidated. Investee Companies will seek to address these risks by appointing experienced EPC contractors, with a range of financial support mechanisms, including strong balance sheets, and/or parent company guarantees, and/or letters of credit from a bank. Investee Companies would also consider paying a premium for sites on a turnkey basis, so that the payment for the solar farm is only made to the EPC contractor when it is fully installed.

ff Failure of system to deliver expected outputs: Under the terms of the EPC contract, the EPC contractor will be required to deliver the system to a certain level of performance. Failure to do this will result in the EPC contractor being penalised. There is a risk that the EPC contractor could fail. In this case the performance warranties in the EPC contract are likely to have little or no value, and this could result in Investors suffering financial loss.

ff Failure of system to be maintained: There are a number of parties that could provide the maintenance of the site, and in the event that the appointed maintenance contractor fails to meet the required standard, this role will be given to a third party. The technology for solar panels and inverters is well established, and they have very few moving parts, reducing the risk of unexpected failures and maintenance spend. However, the risk of mechanical failure cannot be avoided.

ff Failure of panels and inverters: The solar panels are likely to be warranted for circa 20 years and inverters for circa five years. However, it is possible that the manufacturer may fail during the warranty period, thereby invalidating the warranty. The solar industry is highly competitive and a number of manufacturers have failed over recent years. It may be possible for Investee Companies to obtain warranty insurance to cover the cost of the panels.

ff Variations in irradiation: Variation in the amount of irradiation from year to year is modest, though extreme circumstances such as a volcanic eruption, could reduce output for a period, and possibly for an extended period.

ff Theft or damage of panels: The systems will be protected by fencing and 24-hour on-site security, making it more difficult to access the site and steal or damage equipment. However, in the event of theft or damage of the system, the system will be insured. It should also be noted that it is possible the insurer may fail during this period.

ff Access to the grid: Investee Companies’ business models are based on being able to export the electricity generated to one or more customers. In the event that Investee Companies are denied the ability to export electricity in the future (e.g. as a result of regulatory change or corruption), then Investee Companies would suffer financial loss for the period for which it could not export electricity. In the event that the ability to export electricity is permanent, then the loss suffered could be total on the relevant solar farm.

ff Grid stability: Investee Companies will analyse the stability of the electricity grid in the areas where projects are to be installed and to ensure that they are reasonably stable.

Downing Indian Solar EIS - Terms & Conditions 11

ff However, electricity grids are dynamic networks, and it is possible that, if not well managed by the grid operator, Investee Companies’ ability to export in the future could be constrained (e.g. if another power plant was installed on the grid at the same points of connection without the necessary upgrade works).

Additional Indian solar risksListed below are potential risks of investing in solar projects in India faced by an Investor, along with mitigations to them. The list is not exhaustive, and there may be other material risks not listed below. There are a number of infrastructure, political and other risks of transacting business in India, some of which are unknown. Any of these risks could result in financial loss to investors.

ff Exchange controls: India could introduce exchange controls that would prevent subsidiary companies being able to distribute profits to the Investee Companies. In this case the investors could be faced with suffering financial loss, even where the underlying projects are profitable. The Investee Companies may be able to find alternative solutions to address this risk at such time (e.g. through a sale of the shares in the subsidiary companies to an Indian company), but such options would need to be considered at such time.

ff Change in taxation rates: Investee Companies are always exposed to changing tax rules. Indeed, over the life of Investee Companies’ projects it can be reasonably expected that the tax rules which affect Investee Companies will change in one way or another, either in India or the UK. A particular risk to foreign investors in India – and an alternative to the imposition of exchange controls discussed above – could be the introduction of much higher withholding taxes on the distribution of dividends and/or interest payments to foreign investors. Again, this could result in Investors suffering financial loss even if the underlying projects are performing as expected, but Investee Companies may be able to find alternative solutions as set out above.

ff Land ownership: The Investee Companies’ subsidiaries are intending to own the land on which their solar power plants are installed. However, there are stories in general circulation relating to land disputes in India. We anticipate that this risk would be particularly high where the land is unoccupied and the landowner is absent. This will not be the case for our Investee Companies, where the land will be occupied, will be surrounded by security fencing, and will have constant manned security. Our Investee Companies’ Indian legal advisers will be performing title due diligence prior to purchasing any land, and land will only be purchased where land can be transferred with clear, good title. However, ultimately the cost of the land is not the most material part of Investee Companies’ solar projects, and if Investee Companies did lose a land dispute then it is likely that the installed equipment would be moved to an alternative site. Such circumstances would likely result in some financial loss to Investors.

ff Currency devaluation: The Investee Companies will be operating in Indian Rupees. Downing uses an assumed annual rate of currency devaluation in its forecasts based on the Pound Sterling/Indian Rupee exchange rate over the last 10 years. In the event that actual devaluation is higher than the rate assumed by Downing, Investor returns would be adversely affected, and could result in Investors losing some of their capital. If the rate of devaluation is less than assumed, Investor returns should be positively affected.

ff Political Risk Insurance: The EIS Companies will put in place political risk insurance through Lloyds of London Underwriters. The policy covers political acts by the Indian government such as expropriating Investee Company assets and preventing the transfer or conversion of currency (exchange controls). It also covers loss from damage to assets caused by war or political violence. As with any insurance policy there are a number of conditions and exclusions and there are no guarantees that losses from political acts will be covered in full or at all.

The Service described in these Terms may not be appropriate for all Investors. Investors are accordingly advised to consult an investment adviser authorised under the FSMA, and an appropriately qualified taxation adviser, prior to investing.

Downing Indian Solar EIS - Terms & Conditions12

Charges - how Downing’s charges are applied

Initial chargesAn initial charge of 2% of the Subscription will be payable by EIS Companies at the time of investment. If you are investing through an intermediary who doesn’t give advice the 2% balance of the initial charge of 4% will be deducted from the exit proceeds realised from four years’ time onwards.

Annual feeAn annual fee of 2% of the Subscription will be payable on a quarterly basis by EIS Companies. If you are investing through an intermediary who doesn’t give advice the balance of the annual fee of 0.5% of the Subscription per annum will be deducted from the exit proceeds when realised.

Out of its fee, Downing will be responsible for all the usual running costs of the Service, namely custodian and nominee fees, bank charges, administration and reporting to investors.

Adviser chargesAdviser charges are costs that you have agreed with your adviser, in payment for the advice they have provided to you. If agreed between you and your adviser, Downing can facilitate adviser charges from your investment. For ongoing adviser fees, four years’ worth of charges will be deducted from your Subscription and set aside in a client cash account with ongoing adviser charges charged annually and paid from this account. No interest will be paid or accrued to the Investor on these sums. If the funds in this account become exhausted, any further ongoing adviser charges will accrue against your portfolio until liquidity is available for these charges to be taken.

Performance IncentiveIn order to align interests between Downing and Investors, no performance incentive is payable until Investors receive cash proceeds at least equal to the target return of £1.20 per net 70p invested (including income tax relief). The performance fee will then be payable at a rate of 20% of the exit proceeds over £1.00 (in respect of each £1.00 invested). If Investors elect to continue holding their Shares after the first opportunity to exit, the Performance Incentive will be payable based on the amount that would have been received had the Investor elected to exit.

Charges to EIS companiesAn arrangement fee of up to 2% plus VAT of the amount invested will be charged to each EIS Company. Downing does not charge any other fees such as monitoring, service or exit fees. The cost of all deals that do not proceed to completion will be borne by Downing.

Although most fees and costs are payable by the EIS Companies to increase tax efficiency, and not by the Service directly, they will, in effect, reduce the returns generated by the EIS Companies for Investors. Any unpaid fees due to the Manager will be recouped from the proceeds of the sale of investments.

If you are investing through an adviser

Downing’s initial charge 2%

Initial charge to your adviser agreed with your adviser

Downing’s annual fee 2% plus VAT per annum

Ongoing fee to your adviser agreed with your adviser

If you are investing through an intermediary who doesn’t give you advice (execution only)

Downing’s initial charge

4% (2% of which will usually be paid to your intermediary unless indicated otherwise on your application form)

Downing’s annual fee

2.5% plus VAT per annum (0.5% of which will usually be paid to your intermediary for 4 years)

All percentages above are applied to the Subscription

Downing Indian Solar EIS - Terms & Conditions 13

Taxation

This summary is based upon current UK tax law and published practice and is intended as a guide only. The summary considers the position of individuals who are both UK resident and domiciled. It is not intended to constitute legal or tax advice and prospective Applicants are recommended to consult their own professional advisers concerning the possible tax consequences of investing through the Service.

EIS CompaniesEach EIS Company in which the Investor invests through the Service must initially (i.e. at the time of issue of the Shares) not be listed on a recognised stock exchange (as defined for the purposes of EIS relief) and there must be no “arrangements” in place for it to become listed. In addition, throughout the Three Year Period, it must not be a subsidiary of, or be controlled by, another company; it must either exist to carry on an EIS Trade or else be the parent company of a trading group; and there must be no “arrangements” in existence for the company to become a subsidiary of, or be controlled by, another company.

The qualifying business activity for which the money is raised by the share subscription must be a trade carried on by a company or certain of its subsidiaries and the trade must be conducted on a commercial basis and with a view to the realisation of profit.

The maximum fundraising per EIS Company is restricted to £5 million per year and the maximum number of full-time employees in the EIS Company at the time of fundraising is restricted to a maximum of 249.

Most types of trades are EIS Trades but the following are excluded:

a. Dealing in land, commodities or futures, or in shares, securities or other financial instruments;

b. Dealing in goods otherwise than in the course of an ordinary trade of wholesale or retail distribution, or acting as a wholesaler or retailer of goods of a kind which are collected or held as investments if stock is not actively sold;

c. Banking, insurance, money lending, debt factoring, hire purchase financing or other financial activities;

d. Leasing, except certain lettings of ships, or receiving royalties or licence fees (subject to certain exceptional cases);

e. Providing legal or accountancy services;

f. Farming, market gardening, forestry, timber production, shipbuilding, coal and steel production;

g. Property development;

h. Operating or managing hotels (or similar establishments), nursing homes and residential care homes;

i. Electricity generation or export from which FITs, ROCs or RHI are derived, except electricity generated from anaerobic digestion and hydro power; and

j. Providing services to a trade consisting of any of the above carried on by a “connected person”.

Investment fund statusThe Service has not been approved by HMRC under Section 251 of the ITA 2007. The effect of this is that the Investor can only obtain EIS income tax relief in the tax year in which each underlying investment is made, or the previous tax year, rather than in the tax year in which an approved fund closes.

The Manager reserves the right to return a surplus of cash if it concludes that it cannot be properly invested.

When each underlying investment is made, pursuant to this procedure, the Manager will send Investors in that fund an EIS3 Form, once the EIS Company has been trading for four months. The EIS3 Form will show the Investor’s entitlement to EIS tax relief.

EIS tax reliefsTo obtain the tax reliefs described in this section it is necessary for the Service to subscribe for new shares in an EIS Company. The summary below gives only a brief outline of the tax reliefs and assumes that the Investor is a 40% taxpayer. It does not set out all the rules which must be met during the Three Year Period by the EIS Company and the Investor. The tax reliefs will only be relevant to Investors who pay UK income tax and/or wish to defer a capital gain.

The summary is not a substitute for the Investor obtaining professional advice before applying to subscribe for Shares.

1. Income tax relief

Individuals can obtain income tax relief on the amount subscribed for Shares in EIS Companies provided they are not connected with the issuing company. This is subject to the limit of £1 million across all EIS investments in any tax year. Husbands and wives, and civil partners, can each subscribe up to these limits.

Downing Indian Solar EIS - Terms & Conditions14

To calculate the relief, 30% is multiplied by the amount subscribed. The relief is given against the individual’s income tax liability for the tax year in which the Shares are issued, unless the individual makes a carryback claim to the previous tax year. The relief cannot exceed the amount which reduces the Investor’s income tax liability to nil.

Income tax relief

£

Gross investment in Shares 100,000

Less income tax relief at 30% (30,000)

Net cost of investment 70,000

In respect of EIS investments made, tax relief on the subscription may be carried back to the previous tax year (subject to the annual limit across all EIS investments in that tax year having not yet been claimed).

2. Exemption from capital gains tax

Any capital gains realised on a disposal of Shares in the EIS Companies after the Three Year Period, and on which EIS income tax relief has been given and not withdrawn, will be capital gains tax-free.

Any capital gains realised on a disposal within the Three Year Period will be subject to CGT.

3. Loss relief against income or gains

Tax relief is available upon any loss realised upon a disposal of Shares on which EIS income tax relief (see 1 above) has been given and not withdrawn. The amount of the loss (after taking account of any income tax relief retained) can be set against the individual’s gains in the tax year in which the disposal occurs, or, if not so used, against gains of a subsequent year, or against the individual’s taxable income in either the tax year in which the disposal occurs, or the previous tax year if carried back.

CGT exemption

£

Realisation after 3 years 105,000

Less original cost (100,000)

Tax-free gain 5,000

The table above is based on a 40% taxpayer.

4. CGT deferral relief

To the extent to which a UK resident Investor (including certain trustees) subscribes for qualifying shares, he or she can claim to defer paying tax on all or part of a chargeable gain. The gain may have arisen on the disposal of any asset or a previously deferred gain may have been brought back into charge. Although there is a limit of £1 million for both income tax relief and for the exemption from capital gains tax upon a disposal (see 1 and 2 above), there is no limit on the amount of EIS investments which can be used to defer a gain. The Shares must be issued within one year before and three years after the date of the disposal which gives rise to the gain or the date upon which a previously deferred gain crystallises. The gain is deferred until there is a chargeable event, such as a disposal of Shares or an earlier breach of the EIS rules.

5. IHT – business property relief

Provided an investor has owned Shares in an IHT qualifying company for at least two years, and certain conditions are met at the time of the transfer, 100% business property relief is available, which reduces the IHT liability on the transfer to nil. The examples in this document are set out for illustrative purposes only. They are not, and should not be construed as, forecasts or projections of the likely performance of the Service. Please note that this is only a condensed summary of the taxation legislation and should not be construed as constituting advice which a potential Investor should obtain from his or her own investment or taxation adviser before subscribing through the Service. The value of any tax reliefs will depend on the individual circumstances of Investors and may be subject to change in the future.

Loss relief

£

Realised value of Shares Nil

Less gross investments in Shares (100,000)

Income tax relief at 30% 30,000

Loss before loss relief (70,000)

Loss relief at 40% 28,000

Net loss (42,000)

Downing Indian Solar EIS - Terms & Conditions 15

Definitions

“Adviser Charge” fee agreed between an FCA authorised and regulated adviser, for advice and related services

“AIFMD” Alternative Investment Fund Managers Directive (2011/61/EU)

“Applicable Rules” FSMA, the FCA Rules and all other relevant laws and regulations

“Application Form” application form and notes on application for investment under the Service

“Approved Investment Fund” investment fund approved by HMRC under Section 251 of ITA 2007

“Brochure” document dated 4 December 2015 describing the Service

“CGT” capital gains tax

“Closing Date” final date upon which applications will be accepted by the Manager

“Custodian” Thompson Taraz Depository Limited, of 47 Park Lane, London W1K 1PR (FCA No: 465415), or such organisation as the Manager may appoint to provide, and with whom it has agreed terms for, safe custody and custodial and nominee services in respect of the Service

“Downing” or “Manager” Downing LLP, which is authorised and regulated by the Financial Conduct Authority in the United Kingdom (whose business was transferred from Downing Corporate Finance Limited)

“EIS” Enterprise Investment Scheme

“EIS Companies” companies which are qualifying EIS companies

“EIS Investments” investments made in EIS Companies

“EIS Trade” business which qualifies for EIS tax reliefs

“FCA” Financial Conduct Authority and any successor body

“FIT” or “FITs” Feed-in Tariff(s)

“FSMA” Financial Services and Markets Act 2000

“HMRC” HM Revenue & Customs

“IHT” inheritance tax

“IHTA 1984” Inheritance Tax Act 1984

“Intermediary” authorised intermediary who signs the Application Form and whose details are set out in section 7 of the Application Form

“Investor” individual (and certain trustees) who completes an Application Form which is accepted by the Manager and so enters into the Investor Agreement and invests in EIS Companies through the Service

“Investor Agreement” agreement to be entered into between each Investor and the Manager, in the terms set out in this document

“ITA 2007” Income Tax Act 2007

“ML Regulations” Money Laundering Regulations 2007

“NAV” Net Asset Value

“Nominee” TT Nominees Limited or such nominee as the Custodian may appoint to act as the Investor’s nominee from time to time

“Performance Incentive” performance-related incentive payable to the Manager and/or its executives as described on page 13 of these Terms

“RHI” Renewable Heat Incentive

“ROCs” Renewable Obligation Certificates

“Service” Downing Indian Solar EIS, a service set up to enable Investors to invest in EIS Companies by way of the Investor Agreement with the Manager

“Shares” shares in an EIS Company purchased through the Service on behalf of Investors

“Subscription” amount subscribed through the Service net of any Adviser Charges

“Terms” this document

“Three Year Period” period beginning on the date the Shares in the EIS Company are issued and ending three years after that date, or three years after the commencement of the EIS Company’s trade, whichever is later

Downing Indian Solar EIS - Terms & Conditions16

Investor agreement

This Investor Agreement (the “Agreement”) sets out the agreement between the Manager and the Investor in relation to the making of investments, by the Manager on behalf of Investors as described in these Terms. The investments will together constitute a “Portfolio”. Upon acceptance of a signed Application Form, this Agreement will constitute a binding agreement between the Investor and the Manager.

1. Definitions, construction and interpretation

1.1 The following terms shall have the following meanings in this Agreement:

“Applicable Rules” all relevant UK laws, regulations and rules, including those of the FCA;

“Application Form” an application form to invest through the Service completed by the Investor and (where applicable) the adviser in the form provided by the Manager;

“Closing Date” in respect of the Service, the date on which the final Subscription may be made by the Investor through the Service, which shall be a date determined by the Manager and notified to the Investor;

“EIS” the Enterprise Investment Scheme set out in ITA Sections 156-257, and in TCGA Sections 150A-150D and Schedule 5B;

“EIS Relief” the tax reliefs available under the EIS, including income tax relief, capital gains tax exemption, share loss relief and capital gains tax deferral relief;

“FCA Rules” the rules of the FCA as set out in the FCA’s Handbook of Rules and Guidance and any other rules and guidance issued by the FCA from time to time;

“Initial Period” the period of twelve months commencing on the Closing Date;

“Investment” an investment acquired at the discretion of the Manager for the Investor through the Service;

“Investment Objective” the investment objective for the Investments made through the Service as set out in the Brochure and/or these Terms;

“Investment Restrictions” the investment restrictions for the Investments made through the Service as set out in the Brochure and/or these Terms

“Investment Services” the investment services provided under Clause 4 of this Agreement;

“Regulated Collective Investment Scheme” an authorised open-ended investment company as defined in Section 237(3) of the Act; or an authorised unit trust scheme as defined in Section 237(3) of the Act; or a recognised scheme under Sections 264, 270 or 272 of the Act.

“Regulated Market” any market included on the list maintained by the FCA in accordance with the provisions of Article 47 of MiFID and included as such on the FCA Register, or any equivalent market similarly regulated in another member state of the EEA.

“Tax Advantages” the various tax advantages, including EIS Relief, arising from subscriptions for shares in EIS Companies.

“US Person” (1) individuals who are United States of America (US) citizens (including dual citizens) or resident, US passport holders, green card holders, individuals born in the US who have not renounced their citizenship, permanent residents of the US and those with a “substantial presence” in the US as defined in US tax law; (2) a partnership or corporation organised in the US or under the laws of the US; (3) certain trusts with a US nexus; and (4) a non-US entity which is controlled by US Persons (if you are in any doubt as to whether you are a US Person you should consult an adviser).

1.2 Words and expressions defined in either these Terms or the FCA Rules which are not otherwise defined in this Agreement shall, unless the context otherwise requires, have the same meaning in this Agreement.

1.3 Any reference to a statute, statutory instrument or to rules or regulations shall be references to such statute, statutory instrument or rules and regulations as from time to time amended, re-enacted or replaced and to any codification, consolidation, re-enactment or substitution thereof as from time to time in force.

1.4 References to the singular only shall include the plural and vice versa.

1.5 Unless otherwise indicated, references to Clauses and Schedules shall be to clauses and schedules in this Agreement.

1.6 Headings to Clauses are for convenience only and shall not affect the interpretation of this Agreement.

2. Investing through the Service

2.1 This Agreement comes into force on the date that the Manager accepts the Investor’s Application Form. An Application Form is accepted when recorded on the register of applications maintained by the Manager.

2.2 This Agreement enables the Investor to invest through the Service.

2.3 Investors should be aware that the right to cancel a distance contract within 14 days does not apply to this agreement as it falls within the exemption contained in FCA rule COBS 15 Annex 1. Please speak to your adviser or us if you require further information.

Downing Indian Solar EIS - Terms & Conditions 17

2.4 Where the Investor submits an Application Form which is accepted, and then the Investor makes Subscriptions, the Investor hereby appoints the Manager to fulfil its role in managing the Portfolio for the Investor on the terms set out in this Agreement. The Manager agrees to accept its appointment and obligations on the terms set out in this Agreement.

2.5 The Manager is Downing LLP, and is authorised and regulated by the Financial Conduct Authority, with Firm Reference Number 545025. The Manager is a Limited Liability Partnership registered in England and Wales under company number OC341575 and with a registered address at Ergon House, Horseferry Road, London SW1P 2AL. The FCA’s registered address is 25 The North Colonnade, London E14 5HS. This Agreement is supplied to you in English and we will continue to communicate with you in English for the duration of this Agreement. The Investor is classified as a Retail Client. The Investor has the right to request a different client categorisation. However, if the Investor does so and if the Manager agrees to such categorisation the Investor will lose protections afforded by certain FCA Rules. This may include, but may not be limited to:

(a) the Investor will not be given any of the additional disclosures required to be provided to Retail Clients (for example on costs, commissions, fees and charges, foreign exchange conversion rates and information on managing investments);

(b) the Manager is entitled to assume that the Investor has the requisite knowledge and experience to understand the risks involved and that they are financially able to bear any investment risk consistent with their investment objectives;

(c) the Manager is entitled to assume that the Investor has the necessary level of experience and knowledge to understand the risks involved in relation to any investment, service, product or transaction contemplated by the Terms, the Brochure and the Application Form;

(d) the FCA Rules imposes detailed requirements on financial promotions directed at Retail Clients. Promotions directed at Professional Clients are simply subject to the high level requirement that they are fair, clear and not misleading;

(e) if the Manager were to hold money on behalf of a Retail Client the Manager would have to notify the client of whether interest is payable (which is not required for Professional Clients); and the Manager would not be able to transfer the money to a third party without notifying a Retail Client and without explaining who is responsible for that third party’s actions or omissions, and the consequences where that third party becomes insolvent;

(f) if the Manager were to manage client assets, the Manager would be obliged to provide Retail Clients with more detailed information periodically. A Retail Client has a right to a periodic statement every three months, rather than every six months for a Professional Client;

(g) where the Manager places Investors’ orders with third parties for execution, the factors taken into account in obtaining the best possible execution result for a Professional Client will differ to those for a Retail Client. It should be noted that Professional Clients can no longer opt out of best execution; and

(h) entitlement to claim compensation under the Financial Services Compensation Scheme.

2.6 The Investor confirms that he/she is suitably knowledgeable of the risks associated with Non-Readily Realisable Investments and/or has been suitably advised of these risks.

2.7 The Investor confirms that he/she is not seeking advice from the Manager on the merits of any investment made through the Service.

2.8 The Investor agrees that the Manager may hold information about them and their affairs in order to verify their identity and financial standing (among other things the Manager may consult a credit or mutual reference agency, which may retain a record of the enquiry).

2.9 Anti-money laundering regulations aim to prevent criminal property being used or disguised as legitimate wealth. To satisfy these regulations the Investor may have to produce satisfactory evidence of their identity before the Manager can do business with them, and from time to time thereafter. This identification process is designed to assist in the prevention of crime within the financial services industry. If the Investor does not provide the information when requested, the Manager may be unable to accept any instructions from them or provide them with any services.

3. Subscription

3.1 In respect of the Investor‘s Subscription:

(a) the Investor shall make a Subscription of not less than £15,000 for each tax year invested into, through the Service at the same time as submitting his/her Application Form to invest;

(b) the Investor may make further Subscriptions through the Service up to and including the Closing Date. The total subscriptions made through the Service by the Investor shall be the initial value of the Investor’s Portfolio in that Service; and

(c) the Investor may not make any Subscription after the Closing Date.

Downing Indian Solar EIS - Terms & Conditions18

3.2 The Investor may make a withdrawal of his/her Portfolio, or terminate the Agreement, pursuant to Clause 14 below. In the case of there being excess Subscriptions through the Service which are not, in the Manager’s view, capable of being invested appropriately in accordance with the Investment Objective and the Investment Restrictions within the Initial Period, the Investor shall be deemed to have instructed the Manager to make a partial withdrawal from that Service immediately prior to the end of the Initial Period, such that the Service thereafter has at least 100% of the Subscriptions through the Service invested as at the end of the Initial Period and (unless the Manager, at its discretion, determines to return such excess subscriptions) to have instructed the Manager to treat such sums withdrawn as new Subscriptions to a subsequent fund as determined by the Manager and notified by the Manager to the Investor (such instructions shall be subject to any such further instructions as are set out in the Investor’s Application Form or as agreed with the Investor). The Investor’s Application Form to subscribe through the Service shall be deemed to be an Application Form, repeated in similar terms, for any subsequent fund to which excess Subscriptions are diverted pursuant to the terms of this clause.

3.3 Prior to investment in Investee Companies, and following the realisation of Investments in Investee Companies but prior to the distribution of proceeds, Investors’ funds will be held by the Custodian in cash in a designated client money account with trust status. Funds may be held on overnight deposit or, where realisation for investment is not required immediately, in a term deposit not exceeding the lesser of the expected realisation date and three calendar months. All client money will be held in a Prudential Regulatory Authority approved UK bank, typically the Royal Bank of Scotland or another institution with equivalent standing and credit rating. Qualifying Shares will be issued in the name of the Nominee (and, for EIS purposes, the Shares in the EIS Companies will be treated as if they were subscribed for and issued to the Investor who will retain beneficial ownership of them for the life of the Investment). Any dividends received by the Nominee from Investee Companies will be forwarded directly to the Investor pro rata to the Investor’s respective shareholding in such Investee Companies. These will be batched and paid out in dividend runs periodically. De minimis sums will apply as the cost of processing trivial dividends can outweigh the value of the dividend. However, the Manager does not anticipate that any dividends will be paid by the Investee Companies during the Relevant Period. All documents of title will be held by the Nominee on behalf of the Investors.

3.4 The Investor acknowledges that any monies held on deposit by the Manager or the Custodian are held at the Investor’s risk and that neither the Manager, nor any Custodian, nor any director or officer of any of them, will be liable to the Investor in the event of any loss in value of such Investments or the insolvency of any bank with which Investor’s funds are deposited, nor will they be so liable in the event of any restriction on their ability to withdraw funds from such bank for reasons beyond the reasonable control of any of them.

4. Investment Services

4.1 The Manager will provide investment services to the Investor as from the receipt of each Application on the terms set out in this Agreement. The Manager will exercise all discretionary powers in relation to the selection of, or exercising rights relating to, Investments on the terms set out in this Agreement. The Manager will also arrange for the Custodian to provide safe custody services in relation to Portfolio investments and cash.

4.2 The Manager shall not, except as expressly provided in this Agreement or unless otherwise authorised, have any authority to act on behalf of, or in respect of, the Investor or to act as the agent of the Investor. The Investor acknowledges and agrees that the Custodian is not obliged to seek or accept any instruction or direction directly from the Investor in respect of the Custodian’s execution of instructions from the Manager relating to the exercise of the Investor’s rights relating to Investments.

5. Investment objectives and restrictions

5.1 In performing its Services, the Manager shall have regard to, and shall comply with, the Investment Objective and the Investment Restrictions.

5.2 In performing its Services, the Manager shall at all times have regard to:

(a) the need for the Investments to attract the Tax Advantages; and

(b) all Applicable Rules.

5.3 The Manager reserves the right to return a small surplus of cash if it concludes that it cannot be properly invested for the Investor and it considers this to be in the best interests of the Investor having regard to availability of EIS Relief for the Investor.

5.4 In the event of a gradual realisation of Investments, prior to termination of the Service under Clause 14.1, the cash proceeds of realised EIS Investments may be placed on deposit (in an interest bearing client account) or invested in UK Government securities or in other investments of a similar risk profile. Any interest paid on such deposits will be payable to the Manager.

Downing Indian Solar EIS - Terms & Conditions 19

6. Terms applicable to dealing

6.1 The Investor should be aware that the Portfolio will be invested in a range of unlisted securities and that there is generally no relevant market or exchange, and consequent rules and customs and there will be varying practices for different securities. Transactions in shares of such securities will be effected on the best commercial terms which can be secured.

6.2 Where deals are aggregated with other Investors investing through the Service, the number of shares in an EIS Company allocated to the Investor shall be calculated by the Manager, taking into account the timing of subscriptions and with reference to the proportion which the Investor’s Subscription of the Service applied to such share purchase bears to the total Subscriptions by all Investors through that Service at that similar time to the Investor’s Subscriptions, provided that Investors shall not have fractions of shares or if the Manager is acting on specific instructions from an Investor (if one or more of the Investors is an accountant, lawyer or other professional person who is subject to professional rules preventing him/her from making an investment in a particular EIS Company, then the number of shares so allocated to that Investor or Investors shall not be taken up and the cash value of such shares shall be returned to such Investor, such that the number of shares so allocated to other Investors in that Service shall not be increased). Investments may be made by the Service prior to the Closing Date.

6.3 Subject to both the Applicable Rules and the Manager’s conflicts of interest policy (a summary of which is included at Schedule 2 of this Agreement) the Manager may make use of dealing commission arrangements in respect of deals undertaken for the Service as may be disclosed to the Investor from time to time.

6.4 Subject to both the Applicable Rules and the Manager’s portfolio management policy (at Schedule 1 of this Agreement) the Manager will act in good faith and with due diligence in its choice and use of counterparties but, subject to this obligation, shall have no responsibility for the performance by any counterparty of its obligations in respect of transactions effected under this Agreement.

6.5 The Manager may aggregate your transactions with those of other customers and of its employees in accordance with the Applicable Rules. It is likely that the effect of such an allocation will not work to the Investor’s disadvantage; however, occasionally this may not be the case. The Manager will allocate aggregated transactions promptly on a fair basis in accordance with the requirements of the Applicable Rules.

6.6 As an FCA authorised firm the Manager is required to take all reasonable steps to obtain the best possible result on behalf of clients when placing orders for execution that result from decisions by the Manager. Set out in Schedule 3 is the Manager’s summary of its policy in respect of this requirement. Where applicable, the Manager’s decisions will normally be executed by itself or the Custodian in accordance with its Execution Policy.

7. Reports and information

7.1 The Manager and where applicable the Custodian shall supply such further information which is in its possession or under its control as the Investor may reasonably request as soon as reasonably practicable after receipt of such request.

7.2 The Manager shall provide the Investor with half yearly valuations in respect of the Portfolio. The Investor may request in writing that the Manager provide a periodic statement every three months.

7.3 Reports will include a measure of performance in the later stages of the Service once valuations are available. Any statements, reports or information so provided by the Manager will state the basis of any valuations of investments provided.

8. Fees and expenses

The Manager shall receive fees for its Services, and reimbursements of its costs and expenses, as set out in the Brochure. The Manager will pay the costs of the Custodian.

9. Management and custodian obligations9.1 The Manager shall devote such time and attention and have all necessary competent personnel and equipment as may be required to enable it to provide the services properly and efficiently, and in compliance with the FCA Rules.

9.2 Except as disclosed in any Terms issued in relation to the Service and as otherwise provided in this Agreement (for example on early termination), the Manager shall not take any action which may prejudice the tax position of the Investor insofar as it is aware of the relevant circumstances, and in particular which may prejudice obtaining the Tax Advantages for the Investments.

9.3 The Custodian will act as custodian of the cash and other assets of the Service.

9.4 The Custodian will use reasonable care and skill in providing the services under the custodian agreement.

9.5 The Investors indemnify the Custodian and the Nominee (in proportion to each Investor’s respective interest in the Shares at the date of the indemnity claim) from and against any and all direct liabilities, obligations, losses, damages, penalties, actions against

Downing Indian Solar EIS - Terms & Conditions20

the Custodian, judgements, suits against the Custodian, proper costs and expenses or disbursements (other than those resulting from the fraud, negligence, wilful default or breach of contract on the part of the Custodian) which may be imposed on, incurred by or asserted against the Custodian in properly performing its obligations or duties to the Service under the Custodian Agreement.

9.6 The Investors or the Manager shall pay or reimburse the Custodian from time to time on demand for any transfer taxes payable upon transfers, exchanges or deliveries of securities made under the Custodian Agreement in accordance with the Terms.

9.7 The Custodian is authorised to deduct from any cash received or credited to the Investor’s account, any amount of taxes or levies required by any revenue or UK Governmental authority for whatever reason in respect of the Investor’s accounts.

9.8 The Custodian and the Nominee shall register all securities in respect of which registration shall be necessary in order to perfect the transfer thereof or title thereto as soon as reasonably practicable after receipt of the necessary documents by or to the order of the Custodian in any name permitted by the FCA Rules. Where securities are subject to the law or market practice outside of the United Kingdom and it is, in the Custodian’s opinion, in the Investors’ best interests to do so (and only after the Custodian has received written consent from retail clients), the Custodian may register or record or arrange the registration or recording of securities in the Custodian’s name or the name of a third party. If legal title to securities is held by the Custodian, a nominee or a third party, securities may not be segregated or separately identifiable from the Custodian’s assets, or the assets of a nominee or third party in accordance with FCA regulation, and, in the event of the Custodian’s default or the default or insolvency of a nominee or third party (as the case may be), securities may not be as well protected from the claims of the Custodian’s creditors or the creditors of a nominee or third party (as the case may be).

9.9 The Custodian and the Nominee shall hold the certificates and other documents from time to time, representing or evidencing title to the securities by physical possession of the certificates or other instruments representing the securities in registered or bearer form, including, inter alia, brokers’ receipts or confirmations for future contracts, options or similar investments.