Embed Size (px)

Citation preview

Analysts who prepared this report are registered as research analysts in Korea but not in any other jurisdiction, including the U.S.

Doosan Heavy I&C (034020 KS) Machinery

Efforts to acquire core technologies should continue

Lower TP to W85,000; Maintain Buy call

We maintain our Buy call on Doosan Heavy I&C (DHIC). Although the companyÊs

fundamentals remain intact, we are trimming our target price by 15% to W85,000

to reflect the market pullback (we have not published a report on the company for

four months, as we were the lead manager for Doosan E&CÊs rights offering).

However, the company is expected to show steady secular growth on the back of

stable order performance and earnings improvement at subsidiaries.

Worries over possible delays or cancellations in large-scale projects have grown

due to macro headwinds (e.g., the Middle Eastern turmoil, nuclear leaks in Japan,

and U.S. and European fiscal issues). However, the power plant segment·DHICÊs

key business area·seems relatively intact. Although DHIC was also affected by

negative macro issues, the companyÊs order-taking is likely to be stable on the back

of its swift responses to negative issues and its efforts to acquire core

technologies. Factoring in orders for nuclear reactors in the U.A.E. and a power

plant in Vietnam· as well as potential orders for a desalination plant in Saudi

Arabia, a coal-fueled power plant in India, and a domestic nuclear reactor·we

estimate the companyÊs full-year orders to reach W9.5tr in 2011.

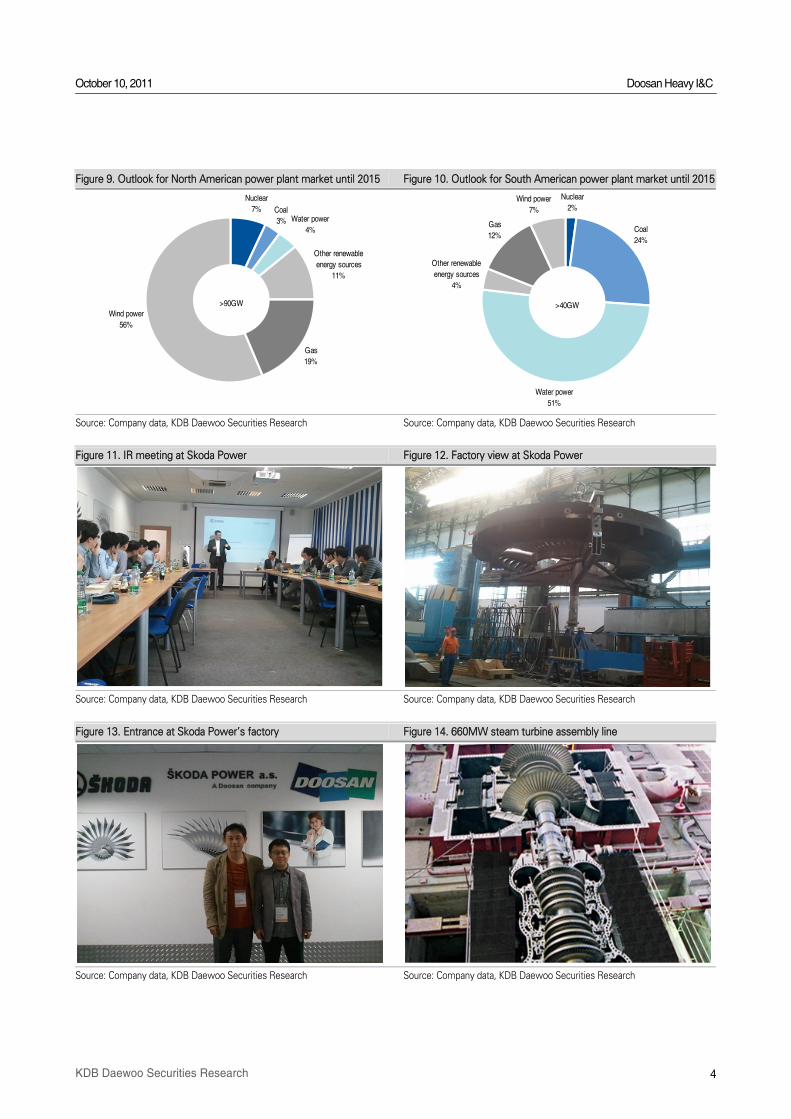

DPS (Doosan Power System: Skoda Power and Babcock) boosts DHIC

We visited DHICÊs overseas subsidiaries·Czech Republic-based Skoda Power (a

mid- to small-sized steam turbine maker; acquired in December 2009) and U.K.-

based Babcock (a boilermaker; acquired in December 2006). These overseas

subsidiaries provide key equipment for power plants. During our visits, we

confirmed DHICÊs smooth progress in acquiring core technologies (for key power

plant equipment). Core technologies hold the key to success in the power plant

business, as it is difficult to enter the segment without such technologies. Thus,

the acquisition of companies with core technologies was necessary for DHICÊs

expansion into the global market.

The global turbine market is dominated by seven companies, including GE,

Siemens, and Alstom. Skoda Power is one of the leaders in the small- and mid-

sized steam turbine market. As it has been a while since DHIC acquired Skoda

Power, synergies between the two companies are expected to occur full swing

soon. The two companies jointly won the IEC (Israel) and Sabarmati (India) projects.

They should continue to engage in joint marketing campaigns. We believe that

DHIC, which has enhanced its cost and technological competitiveness, will be able

to further strengthen its global marketing capability.

October 10, 2011Company Report

Daewoo Securities Co., Ltd.

Ki-jong Sung +822-768-3263

Rachael Lee +822-768-3266

Buy (Maintain)

Target Price (12M, W) 85,000

Share Price (10/07/11,W) 56,300

Expected Return (%) 51.0

EPS Growth (11F, %) 400.2

Market EPS Growth (11F, %) 5.7

P/E(11F, x) 10.1

Market P/E(11F, x) 9.4

KOSPI 1,759.77

Market Cap (Wbn) 5,959

Shares Outstanding (mn) 106

Avg Trading Volume (60D, '000) 568

Avg Trading Value (60D, Wbn) 33

Dividend Yield (11F, %) 0.0

Free Float (%) 43.4

52-Week Low 49,550

52-Week High 96,200

Beta (12M, Daily Rate of Return) 1.0

Price Return Volatility (12M Daily, %,SD) 2.5

Foreign Ownership (%) 12.6

Major Shareholder(s)

Doosan Corp. et al. (41.3)

Treasury shares (15.26)

Price Performance

(%) 1M 6M 12M

Absolute 4.1 -17.8 -36.2

Relative 8.1 -0.7 -28.8

40

5060

7080

90100

110120

130

9/10 1/11 5/11 9/11

Share price

KOSPI§ Earnings & Valuation Metrics

FY Revenues OP OP Margin NP EPS EBITDA FCF ROE P/E P/B EV/EBITDA

(Wbn) (Wbn) (%) (Wbn) (Won) (Wbn) (Wbn) (%) (x) (x) (x)

12/09 18,070 356 2.0 -335 -3,190 1,176 1,141 -10.1 -25.4 5.5 18.5

12/10 20,411 1,353 6.6 118 1,116 2,174 1,246 3.5 76.9 4.9 9.8

12/11F 8,601 684 8.0 587 5,583 209 2,357 12.7 9.7 1.1 42.7

12/12F 9,688 794 8.2 1,583 15,003 885 409 24.1 3.6 0.8 10.2

12/13F 10,874 949 8.7 2,020 19,129 1,046 711 24.4 2.8 0.7 8.4

Note: All figures are based on consolidated K-IFRS; NP refers to net profit attributable to controlling interests

Source: Company data, KDB Daewoo Securities Research estimates

October 10, 2011 Doosan Heavy I&C

2 KDB Daewoo Securities Research

The coal-fired thermal power generation market is considered stagnant in advanced

countries, as coal-fired thermal power generation is being switched to renewable energy,

nuclear power and gas-fired power generation due to environmental concerns. However,

DHIC is expanding into rapidly growing markets, including India, Latin America, and East

Europe, in cooperation with Skoda Power and Babcock. In addition, the company is also

targeting advanced markets through advanced technologies, such as carbon capture and

storage (CCS) and circulating fluidized bed (CFB). Furthermore, the company is seeking long-

term growth by jointly engaging in U.K.-led offshore wind power and nuclear power projects.

Efforts to acquire core technologies should continue

DHIC has acquired two core technologies related to small- and mid-sized steam turbines and

boilers. Still, the company lacks the core technologies to produce gas turbines, large-sized

boilers, and generators. However, going forward, the company should be able to find new

opportunities to acquire core technologies. In addition, with the business environment

rapidly changing, DHIC should obtain new technologies, including CFB combustion

technology, which enables coal-fired thermal power plants to use low-quality coal (60% of

the worldÊs coal production). On April 14th, DHIC announced that it is considering the

acquisition of German-based AE&E Lentjes, which holds CFB combustion technology.

DHIC is attempting to become a global power plant player by acquiring overseas technology

holders (e.g., AE&E Lentjes, Babcock, and Skoda Power). Such efforts are likely to continue. U.S.

and European issues should be negative in the short term. However, over the long term, these

crises are expected to lead to the diversification of project financing sources and provide

companies in emerging nations with opportunities to acquire core technologies. In this market

environment, we believe that the companyÊs power plant business should show secular growth.

Figure 1. Order trend and forecasts at DPS Figure 2. Earnings trend and forecasts at DPS

Source: Company data, KDB Daewoo Securities Research Source: Company data, KDB Daewoo Securities Research

0

200

400

600

800

1,000

1,200

1,400

1,600

06 07 08 09 10 11F 12F 13F 14F 15F

New orders

( £mn)

0

200

400

600

800

1,000

1,200

1,400

06 07 08 09 10 11F 12F 13F 14F 15F

(£mn)

0

3

6

9

12

15

18Revenues (L)

OP margin (R)

(%)

October 10, 2011 Doosan Heavy I&C

3 KDB Daewoo Securities Research

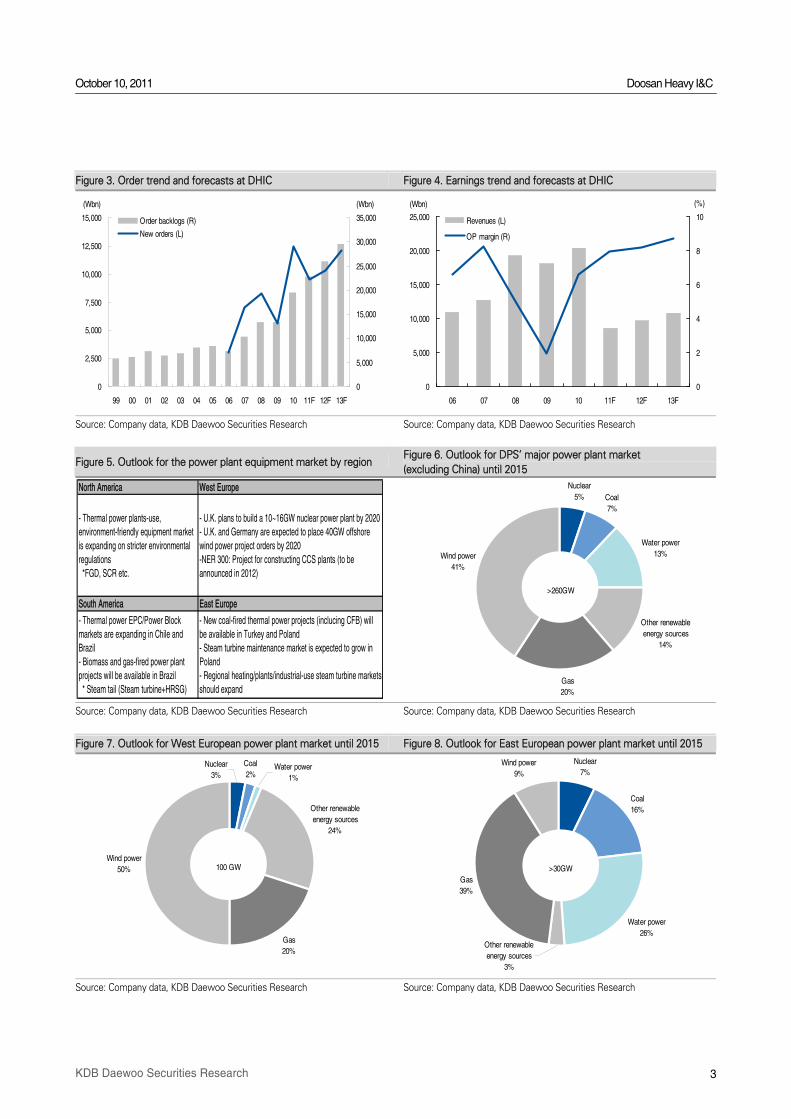

Figure 3. Order trend and forecasts at DHIC Figure 4. Earnings trend and forecasts at DHIC

Source: Company data, KDB Daewoo Securities Research Source: Company data, KDB Daewoo Securities Research

Figure 5. Outlook for the power plant equipment market by region Figure 6. Outlook for DPSÊ major power plant market

(excluding China) until 2015

Source: Company data, KDB Daewoo Securities Research Source: Company data, KDB Daewoo Securities Research

Figure 7. Outlook for West European power plant market until 2015 Figure 8. Outlook for East European power plant market until 2015

Source: Company data, KDB Daewoo Securities Research Source: Company data, KDB Daewoo Securities Research

(Wbn)

0

2,500

5,000

7,500

10,000

12,500

15,000

99 00 01 02 03 04 05 06 07 08 09 10 11F 12F 13F

(Wbn)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000Order backlogs (R)

New orders (L)

0

5,000

10,000

15,000

20,000

25,000

06 07 08 09 10 11F 12F 13F

(Wbn)

0

2

4

6

8

10Revenues (L)

OP margin (R)

(%)

Nuclear

5% Coal

7%

Water power

13%

Other renewable

energy sources

14%

Gas

20%

Wind power

41%

>260GW

Other renewable

energy sources

24%

Gas

20%

Wind power

50%

Coal

2%Water power

1%

Nuclear

3%

100 GW

Nuclear

7%

Coal

16%

Water power

26%

Gas

39%

Wind power

9%

Other renewable

energy sources

3%

>30GW

North America West Europe

- Thermal power plants-use,

environment-friendly equipment market

is expanding on stricter environmental

regulations

*FGD, SCR etc.

- U.K. plans to build a 10~16GW nuclear power plant by 2020

- U.K. and Germany are expected to place 40GW offshore

wind power project orders by 2020

-NER 300: Project for constructing CCS plants (to be

announced in 2012)

South America East Europe

- Thermal power EPC/Power Block

markets are expanding in Chile and

Brazil

- Biomass and gas-fired power plant

projects will be available in Brazil

* Steam tail (Steam turbine+HRSG)

- New coal-fired thermal power projects (inclucing CFB) will

be available in Turkey and Poland

- Steam turbine maintenance market is expected to grow in

Poland

- Regional heating/plants/industrial-use steam turbine markets

should expand

October 10, 2011 Doosan Heavy I&C

4 KDB Daewoo Securities Research

Figure 9. Outlook for North American power plant market until 2015 Figure 10. Outlook for South American power plant market until 2015

Source: Company data, KDB Daewoo Securities Research Source: Company data, KDB Daewoo Securities Research

Figure 11. IR meeting at Skoda Power Figure 12. Factory view at Skoda Power

Source: Company data, KDB Daewoo Securities Research Source: Company data, KDB Daewoo Securities Research

Figure 13. Entrance at Skoda PowerÊs factory Figure 14. 660MW steam turbine assembly line

Source: Company data, KDB Daewoo Securities Research Source: Company data, KDB Daewoo Securities Research

Nuclear

7%Water power

4%

Other renewable

energy sources

11%

Gas

19%

Wind power

56%

Coal

3%

>90GW

Nuclear

2%

Coal

24%

Water power

51%

Other renewable

energy sources

4%

Gas

12%

Wind power

7%

>40GW

October 10, 2011 Doosan Heavy I&C

5 KDB Daewoo Securities Research

Figure 15. Steam turbine module assembling process Figure 16. Steam turbine blade and core

Source: Company data, KDB Daewoo Securities Research Source: Company data, KDB Daewoo Securities Research

Figure 17. Boiler test design by Babcock Figure 18. Burner used for Babcock boiler

Source: Company data, KDB Daewoo Securities Research Source: Company data, KDB Daewoo Securities Research

October 10, 2011 Doosan Heavy I&C

6 KDB Daewoo Securities Research

Figure 19. Boiler test facility at Babcock (1) Figure 20. Boiler test facility at Babcock (2)

Source: Company data, KDB Daewoo Securities Research Source: Company data, KDB Daewoo Securities Research

Figure 21. Ventilation of a boiler test facility Figure 22. Boiler monitoring system at Babcock

Source: Company data, KDB Daewoo Securities Research Source: Company data, KDB Daewoo Securities Research

October 10, 2011 Doosan Heavy I&C

7 KDB Daewoo Securities Research

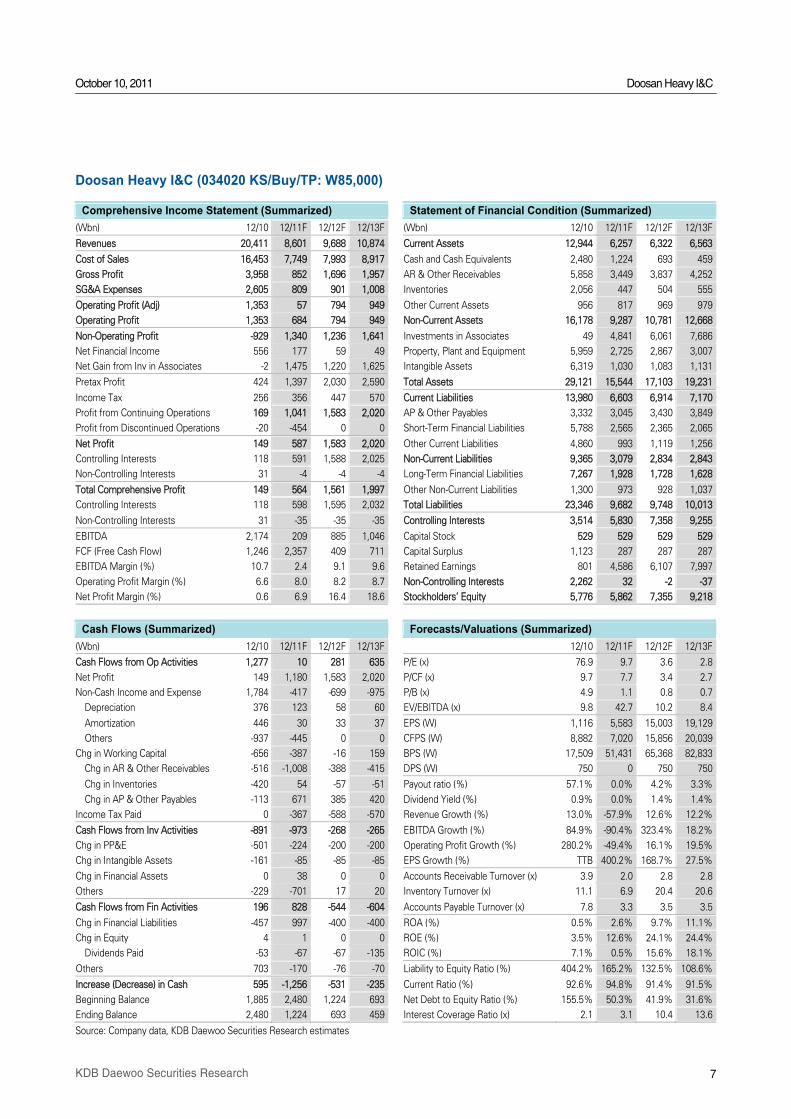

Doosan Heavy I&C (034020 KS/Buy/TP: W85,000)

Comprehensive Income Statement (Summarized) Statement of Financial Condition (Summarized)

(Wbn) 12/10 12/11F 12/12F 12/13F (Wbn) 12/10 12/11F 12/12F 12/13F

Revenues 20,411 8,601 9,688 10,874 Current Assets 12,944 6,257 6,322 6,563

Cost of Sales 16,453 7,749 7,993 8,917 Cash and Cash Equivalents 2,480 1,224 693 459

Gross Profit 3,958 852 1,696 1,957 AR & Other Receivables 5,858 3,449 3,837 4,252

SG&A Expenses 2,605 809 901 1,008 Inventories 2,056 447 504 555

Operating Profit (Adj) 1,353 57 794 949 Other Current Assets 956 817 969 979

Operating Profit 1,353 684 794 949 Non-Current Assets 16,178 9,287 10,781 12,668

Non-Operating Profit -929 1,340 1,236 1,641 Investments in Associates 49 4,841 6,061 7,686

Net Financial Income 556 177 59 49 Property, Plant and Equipment 5,959 2,725 2,867 3,007

Net Gain from Inv in Associates -2 1,475 1,220 1,625 Intangible Assets 6,319 1,030 1,083 1,131

Pretax Profit 424 1,397 2,030 2,590 Total Assets 29,121 15,544 17,103 19,231

Income Tax 256 356 447 570 Current Liabilities 13,980 6,603 6,914 7,170

Profit from Continuing Operations 169 1,041 1,583 2,020 AP & Other Payables 3,332 3,045 3,430 3,849

Profit from Discontinued Operations -20 -454 0 0 Short-Term Financial Liabilities 5,788 2,565 2,365 2,065

Net Profit 149 587 1,583 2,020 Other Current Liabilities 4,860 993 1,119 1,256

Controlling Interests 118 591 1,588 2,025 Non-Current Liabilities 9,365 3,079 2,834 2,843

Non-Controlling Interests 31 -4 -4 -4 Long-Term Financial Liabilities 7,267 1,928 1,728 1,628

Total Comprehensive Profit 149 564 1,561 1,997 Other Non-Current Liabilities 1,300 973 928 1,037

Controlling Interests 118 598 1,595 2,032 Total Liabilities 23,346 9,682 9,748 10,013

Non-Controlling Interests 31 -35 -35 -35 Controlling Interests 3,514 5,830 7,358 9,255

EBITDA 2,174 209 885 1,046 Capital Stock 529 529 529 529

FCF (Free Cash Flow) 1,246 2,357 409 711 Capital Surplus 1,123 287 287 287

EBITDA Margin (%) 10.7 2.4 9.1 9.6 Retained Earnings 801 4,586 6,107 7,997

Operating Profit Margin (%) 6.6 8.0 8.2 8.7 Non-Controlling Interests 2,262 32 -2 -37

Net Profit Margin (%) 0.6 6.9 16.4 18.6 Stockholders' Equity 5,776 5,862 7,355 9,218

Cash Flows (Summarized) Forecasts/Valuations (Summarized)

(Wbn) 12/10 12/11F 12/12F 12/13F 12/10 12/11F 12/12F 12/13F

Cash Flows from Op Activities 1,277 10 281 635 P/E (x) 76.9 9.7 3.6 2.8

Net Profit 149 1,180 1,583 2,020 P/CF (x) 9.7 7.7 3.4 2.7

Non-Cash Income and Expense 1,784 -417 -699 -975 P/B (x) 4.9 1.1 0.8 0.7

Depreciation 376 123 58 60 EV/EBITDA (x) 9.8 42.7 10.2 8.4

Amortization 446 30 33 37 EPS (W) 1,116 5,583 15,003 19,129

Others -937 -445 0 0 CFPS (W) 8,882 7,020 15,856 20,039

Chg in Working Capital -656 -387 -16 159 BPS (W) 17,509 51,431 65,368 82,833

Chg in AR & Other Receivables -516 -1,008 -388 -415 DPS (W) 750 0 750 750

Chg in Inventories -420 54 -57 -51 Payout ratio (%) 57.1% 0.0% 4.2% 3.3%

Chg in AP & Other Payables -113 671 385 420 Dividend Yield (%) 0.9% 0.0% 1.4% 1.4%

Income Tax Paid 0 -367 -588 -570 Revenue Growth (%) 13.0% -57.9% 12.6% 12.2%

Cash Flows from Inv Activities -891 -973 -268 -265 EBITDA Growth (%) 84.9% -90.4% 323.4% 18.2%

Chg in PP&E -501 -224 -200 -200 Operating Profit Growth (%) 280.2% -49.4% 16.1% 19.5%

Chg in Intangible Assets -161 -85 -85 -85 EPS Growth (%) TTB 400.2% 168.7% 27.5%

Chg in Financial Assets 0 38 0 0 Accounts Receivable Turnover (x) 3.9 2.0 2.8 2.8

Others -229 -701 17 20 Inventory Turnover (x) 11.1 6.9 20.4 20.6

Cash Flows from Fin Activities 196 828 -544 -604 Accounts Payable Turnover (x) 7.8 3.3 3.5 3.5

Chg in Financial Liabilities -457 997 -400 -400 ROA (%) 0.5% 2.6% 9.7% 11.1%

Chg in Equity 4 1 0 0 ROE (%) 3.5% 12.6% 24.1% 24.4%

Dividends Paid -53 -67 -67 -135 ROIC (%) 7.1% 0.5% 15.6% 18.1%

Others 703 -170 -76 -70 Liability to Equity Ratio (%) 404.2% 165.2% 132.5% 108.6%

Increase (Decrease) in Cash 595 -1,256 -531 -235 Current Ratio (%) 92.6% 94.8% 91.4% 91.5%

Beginning Balance 1,885 2,480 1,224 693 Net Debt to Equity Ratio (%) 155.5% 50.3% 41.9% 31.6%

Ending Balance 2,480 1,224 693 459 Interest Coverage Ratio (x) 2.1 3.1 10.4 13.6

Source: Company data, KDB Daewoo Securities Research estimates

October 10, 2011 Doosan Heavy I&C

8 KDB Daewoo Securities Research

Disclosures

As of the publication date, Daewoo Securities Co., Ltd. has acted as a liquidity provider for equity-linked warrants backed by shares of DHICO as an underlying asset, and

other than this, Daewoo Securities has no other special interests in the covered companies.

As of the publication date, Daewoo Securities Co., Ltd. has been acting as a financial advisor to DHICO for its treasury share buyback program, and other than this, Daewoo

Securities has no other special interests in the companies covered in this report.

As of the publication date, Daewoo Securities Co., Ltd. issued equity-linked warrants with DHICO as an underlying asset, and other than this, Daewoo Securities has no other

special interests in the covered companies.

Daewoo Securities Co., Ltd.`s analyst attended the IR meeting held by DHICO within recent one month. Expenses related to the meeting were covered by DHICO.

Buy Relative performance of 20% or greater

Trading Buy Relative performance of 10% or greater, but with volatility

Hold Relative performance of -10% and 10%

Stock Ratings

Sell Relative performance of -10%

Overweight Fundamentals are favorable or improving

Neutral Fundamentals are steady without any material changes Industry

Ratings Underweight Fundamentals are unfavorable or worsening

* Ratings and Target Price History (Share price (----), Target price (----), Not covered (■), Buy (▲), Trading Buy (■), Hold (●), Sell (◆))

* Our investment rating is a guide to the relative return of the stock versus the market over the next 12 months.

* Although it is not part of the official ratings at Daewoo Securities, we may call a trading opportunity in case there is a technical or short-term material development.

* A target price was determined by the research analyst through valuation methods discussed in this report, in part based on the analystÊs estimate of future earnings.

The achievement of the target price may be impeded by risks related to the subject securities and companies, as well as general market and economic conditions.

Analyst Certification

The research analysts who prepared this report (the „Analysts‰) are registered with the Korea Financial Investment Association and are subject to Korean securities

regulations. They are neither registered as research analysts in any other jurisdiction nor subject to the laws and regulations thereof. Opinions expressed in this publication

about the subject securities and companies accurately reflect the personal views of the Analysts primarily responsible for this report. Daewoo Securities Co., Ltd. policy

prohibits its Analysts and members of their households from owning securities of any company in the AnalystÊs area of coverage, and the Analysts do not serve as an officer,

director or advisory board member of the subject companies. Except as otherwise specified herein, the Analysts have not received any compensation or any other benefits

from the subject companies in the past 12 months and have not been promised the same in connection with this report. No part of the compensation of the Analysts was, is,

or will be directly or indirectly related to the specific recommendations or views contained in this report but, like all employees of Daewoo Securities, the Analysts receive

compensation that is impacted by overall firm profitability, which includes revenues from, among other business units, the institutional equities, investment banking,

proprietary trading and private client division. At the time of publication of this report, the Analysts do not know or have reason to know of any actual, material conflict of

interest of the Analyst or Daewoo Securities Co., Ltd. except as otherwise stated herein.

Disclaimers

This report is published by Daewoo Securities Co., Ltd. („Daewoo‰), a broker-dealer registered in the Republic of Korea and a member of the Korea Exchange. Information

and opinions contained herein have been compiled from sources believed to be reliable and in good faith, but such information has not been independently verified and

Daewoo makes no guarantee, representation or warranty, express or implied, as to the fairness, accuracy, completeness or correctness of the information and opinions

contained herein or of any translation into English from the Korean language. If this report is an English translation of a report prepared in the Korean language, the original

Korean language report may have been made available to investors in advance of this report. Daewoo, its affiliates and their directors, officers, employees and agents do not

accept any liability for any loss arising from the use hereof. This report is for general information purposes only and it is not and should not be construed as an offer or a

solicitation of an offer to effect transactions in any securities or other financial instruments. The intended recipients of this report are sophisticated institutional investors who

have substantial knowledge of the local business environment, its common practices, laws and accounting principles and no person whose receipt or use of this report would

violate any laws and regulations or subject Daewoo and its affiliates to registration or licensing requirements in any jurisdiction should receive or make any use hereof.

Information and opinions contained herein are subject to change without notice and no part of this document may be copied or reproduced in any manner or form or

redistributed or published, in whole or in part, without the prior written consent of Daewoo. Daewoo, its affiliates and their directors, officers, employees and agents may

have long or short positions in any of the subject securities at any time and may make a purchase or sale, or offer to make a purchase or sale, of any such securities or other

financial instruments from time to time in the open market or otherwise, in each case either as principals or agents. Daewoo and its affiliates may have had, or may be

expecting to enter into, business relationships with the subject companies to provide investment banking, market-making or other financial services as are permitted under

applicable laws and regulations. The price and value of the investments referred to in this report and the income from them may go down as well as up, and investors may

realize losses on any investments. Past performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital may occur.

Important Disclosures & Disclaimers

DHICO

0

20,000

40,000

60,000

80,000

100,000

120,000

10/09 4/10 10/10 4/11 10/11

(W)

October 10, 2011 Doosan Heavy I&C

KDB Daewoo Securities Research 9

Distribution

United Kingdom: This report is being distributed by Daewoo Securities (Europe) Ltd. in the United Kingdom only to (i) investment professionals falling within Article 19(5) of

the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the „Order‰), and (ii) high net worth companies and other persons to whom it may lawfully be

communicated, falling within Article 49(2)(A) to (E) of the Order (all such persons together being referred to as „Relevant Persons‰). This report is directed only at Relevant

Persons. Any person who is not a Relevant Person should not act or rely on this report or any of its contents.

United States: This report is distributed in the U.S. by Daewoo Securities (America) Inc., a member of FINRA/SIPC, and is only intended for major institutional investors as

defined in Rule 15a-6(b)(4) under the U.S. Securities Exchange Act of 1934. All U.S. persons that receive this document by their acceptance thereof represent and warrant

that they are a major institutional investor and have not received this report under any express or implied understanding that they will direct commission income to Daewoo

or its affiliates. Any U.S. recipient of this document wishing to effect a transaction in any securities discussed herein should contact and place orders with Daewoo Securities

(America) Inc., which accepts responsibility for the contents of this report in the U.S. The securities described in this report may not have been registered under the U.S.

Securities Act of 1933, as amended, and, in such case, may not be offered or sold in the U.S. or to U.S. persons absent registration or an applicable exemption from the

registration requirements.

Hong Kong: This document has been approved for distribution in Hong Kong by Daewoo Securities (Hong Kong) Ltd., which is regulated by the Hong Kong Securities and

Futures Commission. The contents of this report have not been reviewed by any regulatory authority in Hong Kong. This report is for distribution only to professional

investors within the meaning of Part I of Schedule 1 to the Securities and Futures Ordinance of Hong Kong (Cap. 571, Laws of Hong Kong) and any rules made thereunder

and may not be redistributed in whole or in part in Hong Kong to any person.

All Other Jurisdictions: Customers in all other countries who wish to effect a transaction in any securities referenced in this report should contact Daewoo or its affiliates only

if distribution to or use by such customer of this report would not violate applicable laws and regulations and not subject Daewoo and its affiliates to any registration or

licensing requirement within such jurisdiction.

Daewoo Securities Co. Ltd. (Seoul) Daewoo Securities (Hong Kong) Ltd. Daewoo Securities (America) Inc. Head Office 31-3 Yeouido-dong, Yeengdeungpo-gu

Seoul 150-716

Korea

Two International Finance Centre Suites 2005-2012

8 Finance Street, Central

Hong Kong

600 Lexington Avenue Suite 301

New York, NY 10022

United States

Tel: 82-2-768-3026 Tel: 85-2-2514-1304 Tel: 1-212-407-1022

Daewoo Securities (Europe) Ltd. Tokyo Representative Office Beijing Representative Office Tower 42, Level 41 25 Old Broad Street

London EC2N 1HQ

United Kingdom

7th Floor, Yusen Building 2-3-2 Marunouchi, Chiyoda-ku

Tokyo 100-0005

Japan

Suite 2602, Twin Towers (East) B-12 Jianguomenwai Avenue

Chaoyang District, Beijing 100022

China

Tel: 44-20-7982-8016 Tel: 81-3- 3211-5511 Tel: 86-10-6567-9699

Shanghai Representative Office Ho Chi Minh Representative Office

Unit 13, 28th Floor, Hang Seng Bank Tower 1000 Lujiazui Ring Road

Pudong New Area, Shanghai 200120

China

Centec Tower 72-74 Nguyen Thi Minh Khai Street

Ward 6, District 3, Ho Chi Minh City

Vietnam

Tel: 86-21-5013-6392 Tel: 84-8-3910-6000

KDB Daewoo Securities International Network