Embed Size (px)

Citation preview

DOOSANHEAVY INDUSTRIES& CONSTRUCTION

ANNUAL REPORT2002

DO

OS

AN

HE

AV

YIN

DU

ST

RIE

S&

CO

NS

TR

UC

TIO

N2

00

2A

NN

UA

LR

EP

OR

T

Brought to you by Global Reports

A N E W G L O B A L P E R S P E C T I V E

It takes a world of perspective to compete and succeed in the global marketplace. At Doosan

Heavy Industries & Construction, our four decades of experience in our namesake fields

have given us the perspective to know what global customers want and the expertise and

technology to deliver quality results. And now as a fully privatized firm, we are adding

a new perspective that will help us do it more competitively and profitability for our

customers and shareholders around the globe.

>

Brought to you by Global Reports

2002 2001

Total Assets 3,094,314 3,079,318

Total Stockholders’ Equity 1,660,150 1,487,055

Net Sales 2,771,630 2,468,417

Power Plants 1,082,897 1,035,924

Industrial Plants 954,172 806,392

Castings & Forgings 199,844 179,433

Civil Engineering & Construction 534,717 446,668

Operating Income 150,056 93,136

Net Income 77,338 25,123

Per Share Performance (In Korean Won)

Net Earnings 904 257

Dividends Declared 150 150

• All figures are for the fiscal years ended December 31

In Millions of KoreanWon

F I N A N C I A L H I G H L I G H T S

NET INCOME

NET SALES

In Millions of

KoreanWon

In Millions of

KoreanWon

2,468,417

2,771,630

2001

2002

2001

2002

77,338

25,123

Brought to you by Global Reports

In many ways, 2002 saw a major turnaround for Doosan Heavy Industries and

Construction Co., Ltd., and we are now well on our way to becoming a global player.

We are currently implementing our goal attainment strategies to make last year’s vision

a reality, as we diversify to become “A comprehensive plant company that offers the best

value based on world-class technology and price competitiveness.”

C E O ’ S M E S S A G E

Brought to you by Global Reports

As the result of a far-reaching process of restructuring we have pulled out of

marginal businesses, such as chemicals and steel, to concentrate our efforts on

power and desalination. We have also laid the foundations for future businesses.

We successfully supplied main nuclear power systems to the U.S. and completed

three mega-desalination projects, including UAE Al Taweelah and Umm Al Nar, prov-

ing Doosan to be both a reliable manufacturer and an industrial plant builder.

Internally, we have improved our efficiency and profitability significantly thanks to

the launch of several “Change Programs.”

These efforts, combined with the successful completion of the Shin-Kori and Shin-

Wolsong Nuclear Power projects and the Fujairah Desalination project, have

enabled us to increase our sales by 12.3 percent over 2001 to achieve 2 trillion 771.6

billion won, despite the slow-down in global trade and the stagnant domestic

economy in 2002.

Overall, our net income nearly tripled to 77.3 billion won from 25.1 billion in 2001.

Our slogan for 2003 is “Change & Build,” signaling that we will continue to execute

innovative “Change Programs” that focus on winning domestic and overseas pro-

jects, strengthening internal management capability for efficiency innovation,

establishing a responsible management system and creating a performance-ori-

ented environment.

Brought to you by Global Reports

We shall concentrate all our efforts on developing new markets and intensifying cus-

tomer-oriented marketing activities to ensure a stable flow of orders in the diffi-

cult business environment, particularly in light of the turmoil following the Iraq War

and what appears to be a prolonged slowdown of the plant market.

In short, we aim to capture a total of 4 trillion 59.4 billion won in orders this year.

We shall deliver higher quality products at lower prices by continuing to improve

our internal management structure. We shall also strive to manufacture the

world’s best products by making key investments in the development of new

designs and technology for power and desalination systems.

Doosan Heavy Industries and Construction Co., Ltd. will remain a trustworthy part-

ner offering reliability and value to its customers.

This year, as every year, all members of the Doosan family promise to do their best

to reciprocate your support.

Thank you.

Dae-Joong KimPresident & CEO

Brought to you by Global Reports

Quality Assurance In step with the firmly held company policy thatcustomers are our teachers and quality is our pride, we see qualityimprovement as the most important management goal alongside thetwin objectives of technological capability and cost competitiveness.We are making continued quality improvement efforts for customersatisfaction, while constantly striving to listen to ‘the voice of ourcustomers.’ We are also obtaining and renewing international standardcertificates in order to meet various customer needs whilesupplementing and evaluating the validity of our quality assurancesystem.As a result of such efforts made in 2002, we recorded 4.6 Sigma with a24% improvement in quality indexes throughout the company. The COPQ(Cost of Poor Quality) has also decreased by 10%, while total customerclaims shrank by 25% compared to last year.

We have concentrated on the realization of these Major Quality Subjects in 2002:1. Development of Comprehensive Quality Information Management System2. Product Liability Prevention & Defense3. Improving High Quality Technology4. Quality Improvement of Suppliers5. Obtaining of New Global Quality Certificates

As an outstanding result of our continued efforts toward qualityimprovement, we won the Korean Grand Quality Award 2000 bestowedannually by the Korean government. As well, our management staffmembers have been recognized for their contribution to domesticindustries thanks to unstinting efforts and achievements in qualitymanagement. Indeed, the president of Doosan himself was given theSilver Tower Industrial Medal at the National Quality ManagementCompetition of 2002, after receiving the Gold Medal for 11 consecutiveyears as leader of the most excellent quality control circle in Korea.

Brought to you by Global Reports

R&D In the year 2002, all of our researchers poured their best effortsinto developing advanced technologies and differentiated, first-classproducts with a vision to build ‘a competitive research center with aninternational level of technology.’

In particular, the recent development of nuclear control rod drivemechanisms and next-generation USC (Ultra Super Critical) thermalpower plants were a chance for us to upgrade our technicalcompetitiveness.

In addition, we have concentrated all our resources and capabilities indebottlenecking and design innovation, emphasizing the aspects oftechnology development and product performance/quality improvementwith an aim to building environmentally friendly power plants. We haveregistered a total of 60 patents and published 94 technical papers inKorean and foreign journals.

In 2003 we will continue to stride forward by combining all our efforts, aswe seek to truly achieve the vision of building ‘a research center with aninternational level of competitiveness.’

Brought to you by Global Reports

Shoaiba Phase II Power & Desalination PlantFacility: Oil-fired thermal power plant and multi-stage flash distillation desalination plant Capacity: 530 MWe + 100 MIGD Location: Jeddah, Saudi Arabia Owner: Saline Water Conversion Corporation Our Role: Turnkey contractor Equipment: 10 MIGD evaporators (10), boiler islands (106 MWe x 5) Receipt: December 1993 Completion: March 2003

Taweelah A2 Power & Desalination PlantFacility: Gas-fired combined-cycle power and multi-stage flash distillation desalination plant Capacity: 720 MWe + 50 MIGD Location: Al Taweelah, UAE Owner: Abu Dhabi Water & Electricity Authority/CMS Energy Our Role: Turnkey contractor Equipment: 12.5 MIGD evaporators (4), 600 ton/hr heat recoverysteam generators (3) Receipt: December 1998 Completion: August 2001

Qinshan Nuclear Power Plant Phase IIIFacility: CANDU nuclear power plant Capacity: 700 MWe x 2 Location: Hangzhou Bay, China Owner: Atomic Energy of Canada Limited Our Role: Prime contractor Equipment: Steam generators (8), feeders (8), pressurizers (2) Receipt: January 1997 Completion: June 2001

Dangjin Thermal Power Plant Units 1~4Facility: Coal-fired supercritical thermal power plant Capacity: 500 MWe x 4 Location: Dangjin, Korea Owner: Korea East-West Power Our Role: Prime contractor, construction, equipment and installation Equipment: Boilers, turbines, generators, balance-of-plant Receipt: August 1994Completion: June 2001 Award: “Project of the Year”, Power Engineering, December 2001

When you’re working with the world’s leading companies, youhave to have a global perspective on results. For the past fourdecades, we’ve been delivering results around the globe.We’ve been making potable water in Saudi Arabia, the UAE,and Kuwait. Generating power in the US, China, Taiwan,Thailand, India, Mexico, and Korea. Building high-speedrailways in Taiwan and Korea. Casting and forging crankshaftsfor the world’s largest ships. Supplying cranes to containerterminals from Sri Lanka to Shanghai and Johor toJacksonville. And the results have made a big impression thatwe’d like to share with you.

Brought to you by Global Reports

TAW

EELA

H A

2 P

OW

ER &

DES

ALI

NAT

ION

PLA

NT

SHO

AIB

A P

HA

SE II

PO

WER

& D

ESA

LIN

ATIO

N P

LAN

TQ

INSH

AN

NU

CLEA

R P

OW

ER P

LAN

T P

HA

SE II

I

DA

NG

JIN

TH

ERM

AL

PO

WER

PLA

NT

UN

ITS

1~4

NUCLEAR POWER PLANTS_20

THERMAL POWER PLANTS_28

TURBINES & GENERATORS_36

DESALINATION PLANTS_42

CASTINGS & FORGINGS_50

MATERIAL HANDLING EQUIPMENT_54

PLANT CONSTRUCTION_58

CIVIL CONSTRUCTION_62

A GLOBAL PERSPECTIVE ON TOMORROW’S HEAVY INDUSTRIES

>

Brought to you by Global Reports

The world has a “love-hate” relationship with nuclear

power. On one hand, it loves the clean, cost-effective

energy it produces. On the other, the devastating 1986

Chernobyl accident in the Ukraine and the ongoing

legal and political wrangling over permanent waste

storage sites have raised safety and environmental

issues that must be addressed. Ultimately, we believe

that these concerns will be satisfied and that demand

for nuclear power will rebound in the absence of a

trulyviable alternative energy source. And when it does,

we intend to be ready to serve the industry as a

world-class total solution provider that rivals the

best in the business.

SHIN-KORI 3 AND 4

Slated for completion in 2010 and 2011,

Shin-Kori 3 and 4 will be the first units built

in Korea using the 1400 MWe nuclear

plant PWR design. This new approach

reflects our construction and operating

experience while integrating the cutting-

edge technology of advanced foreign

nuclear power plants. We will be sup-

plying and installing total nuclear steam

supply systems -including the reactor and

steam generators -while also providing

the turbine generator and balance - of -

plant.

2002 HIGHLIGHTS July 5Ulchin 6 reactor vessel delivery

PROJECT CLIENT COUNTRY

KEDO LWR 1 and 2 KEPCO North Korea

Qinshan Phase III AECL China

Sequoyah #1 TVA USA

Shin-Kori 1 and 2 KHNP Korea

Shin-Wolsong 1 and 2 KHNP Korea

Ulchin 5 and 6 KHNP Korea

Watts Bar #1 RSG TVA USA

Yonggwang 5 and 6 KHNP Korea

Brought to you by Global Reports

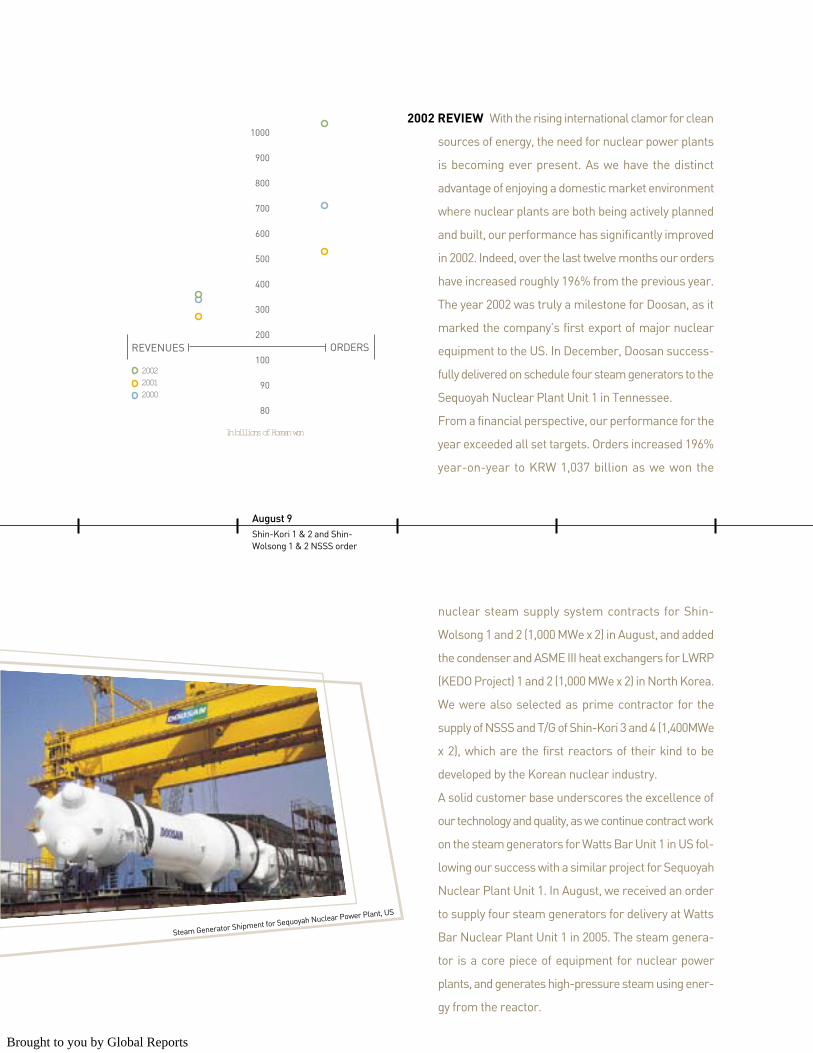

With the rising international clamor for clean

sources of energy, the need for nuclear power plants

is becoming ever present. As we have the distinct

advantage of enjoying a domestic market environment

where nuclear plants are both being actively planned

and built, our performance has significantly improved

in 2002. Indeed, over the last twelve months our orders

have increased roughly 196% from the previous year.

The year 2002 was truly a milestone for Doosan, as it

marked the company’s first export of major nuclear

equipment to the US. In December, Doosan success-

fully delivered on schedule four steam generators to the

Sequoyah Nuclear Plant Unit 1 in Tennessee.

From a financial perspective, our performance for the

year exceeded all set targets. Orders increased 196%

year-on-year to KRW 1,037 billion as we won the

REVENUES ORDERS

1000

900

800

700

600

500

400

300

200

100

90

80

In billions of Korean won

200220012000

August 9 Shin-Kori 1 & 2 and Shin-Wolsong 1 & 2 NSSS order

nuclear steam supply system contracts for Shin-

Wolsong 1 and 2 (1,000 MWe x 2) in August, and added

the condenser and ASME III heat exchangers for LWRP

(KEDO Project) 1 and 2 (1,000 MWe x 2) in North Korea.

We were also selected as prime contractor for the

supply of NSSS and T/G of Shin-Kori 3 and 4 (1,400MWe

x 2), which are the first reactors of their kind to be

developed by the Korean nuclear industry.

A solid customer base underscores the excellence of

our technology and quality, as we continue contract work

on the steam generators for Watts Bar Unit 1 in US fol-

lowing our success with a similar project for Sequoyah

Nuclear Plant Unit 1. In August, we received an order

to supply four steam generators for delivery at Watts

Bar Nuclear Plant Unit 1 in 2005. The steam genera-

tor is a core piece of equipment for nuclear power

plants, and generates high-pressure steam using ener-

gy from the reactor.

2002 REVIEW

Steam Generator Shipment for Sequoyah Nuclear Power Plant, US

Brought to you by Global Reports

Gen

erat

or R

otor

Domestic and overseas nuclear markets will

be fairly sluggish in 2003 in step with the worldwide eco-

nomic depression. Thus we expect to win slightly few-

er orders than we were awarded in 2002. At the same

time, however, we intend to intensify our position as

a prominent supplier in the domestic arena.

Life extension projects are being steadily continued in

the nuclear power plant business, and our experi-

ence in supplying steam generators to the US will

make prospects for an advance into overseas markets

even brighter. Customers around the world have tak-

en note of the guaranteed quality and delivery of our

products, and are now requesting for us to make bids

on major international projects. We are promoting

the supply of not only steam generators but also the

reactor closure head, control rod drive mechanism, and

pressurizer for the life extension of nuclear power

plants. We also hope to enter overseas markets with

the spent fuel transportation cask and canister mod-

els. At the same time we are driving hard to participate

in new nuclear power constructions in East Asia,

Europe and North America. The establishment of

strategic alliances with major partners will provide more

opportunities for Doosan.

We supplied major CANDU equipment to Qinshan

Phase III Units 1 and 2 in China, including the steam

generators, feeder and header assembly and major heat

October 18 Sequoyah Plant steam generatorshipment (4 units)

KRW420billion

KRW 260billion

2002

PROJECTED 2003 REVENUES

PROJECTED 2003 ORDERS

2003 PREVIEW

2003

2002

August 14 Watts Bar Unit 1 RSG order

2003

Brought to you by Global Reports

exchangers. In December 2002, Unit 1 started com-

mercial operation successfully and well before sched-

ule. Unit 2 will commence commercial operation some

time in 2003. Building on two decades of experience

and technology in the nuclear power industry, we can

supply virtually every piece of major equipment for both

PWR and PHWR plants.

Many utilities are considering the cost competitiveness

of their nuclear power plants in comparison to other

energy sources. As an equipment supplier and service

provider, Doosan is making every effort to meet cus-

tomer demand by developing cost-reduced designs and

organizing optimum production processes. New tech-

nology is being continuously developed and adapted to

our product specifications, as we strive to improve

the efficiency of our customers’ nuclear power plants.

Brought to you by Global Reports

RESEARCH & DEVELOPMENT Accelerated development of next-generation technologies is a key element

in our strategy to become a world-class total solution provider in the nuclear power field. Over the years, we’ve

acquired state-of-the-art engineering and manufacturing expertise through real-world project experience

as well as licensing agreements with industry leaders. But rather than simply operating as an OEM manu-

facturer, we’ve continued to incrementally improve on our technologies and capabilities to enhance the

reliability and safety of the 1,000 MWe Korean standard nuclear plant design. Ulchin 3 and 4, the most recent

units to adopt this design, have compiled a remarkable capacity and availability record since their completions

in 1998 and 1999, respectively. We’re also a key partner in the development of Korea’s next-generation 1,400

MWe reference design—Advanced Power Reactor 1400—slated to enter commercial service by 2010. With

basic design work now complete, we’re optimistic that development will be wrapped up in time to be adopted

for the Shin-Kori 3 and 4 project we won in April 2002.

Steam Generator

Reactor Coolant Pump

Reactor

Pressurizer

REACTOR COOLANT SYSTEM

The Korean standard nuclear plant design is a 1,000 MWe pressurized water reactor system that uses two discrete coolant loops

to supply steam to the turbine generator. The primary coolant loop—the reactor coolant system—consists of one reactor vessel, two

steam generators, one pressurizer, and four reactor coolant pumps.

Brought to you by Global Reports

PROJECT EQUIPMENT CLIENT COUNTRY

Altamira CCPP HRSG x 4 GE Power Systems Mexico

Dangjin TPP Units 3/4 Turnkey Project Korea East-West Power Korea

Dangjin TPP Units 5/6 Boiler & BOP Korea East-West Power Korea

Gezer & Haifa HRSG x 3 Siemens Israel

Gibraltar & Palos HRSG x 5 Siemens Spain

Hadong TPP Units 5/6 Turnkey Project Korea Southern Power Korea

Ho-Ping TPP Boiler Package x 2 Alstom Power Taiwan

Panglima CCPP HRSG x 2 Siemens Malaysia

Pohang Sintering Plants 3/4 FGCS x 2 POSCO Korea

Ras Laffan LNG Plant HRSG x 4 Enelpower Qatar

Taean TPP Units 5/6 Boiler & De-Sox System Korea West Power Korea

Yongheung TPP Units 1/2 De-SOx Systems Korea South-East Power Korea

The technology and expertise we’ve accumulated

over the years in engineering, manufacturing, and

installing major equipment for thermal power plants

has given us a high degree of engineering and technical

independence in the field. In 1998, we formed a strate-

gic technical alliance with US-based Parsons in the

architecture engineering field that’s enabling us to

holistically synthesize operational, technical, and

efficiency requirements. We’re also collaborating with

UK-based Mott MacDonald on the architecture engi-

neering work for the 660 MWe power portion of the

Fujairah Power & Desalination Plant project in the UAE

as we continue to expand the scope of our project capa-

bilities to bring greater value to our clients.

DANGJIN THERMAL POWER PLANT

In March 2002, we won an order to pro-

vide boilers and installation works for

Dangjin Thermal Power Plant 5 & 6

(500MW x 2 units). This was the first

international contract bidding ever in

the history of the Korean thermal pow-

er plant industry, and we were award-

ed the project after a fierce competi-

tion with major Japanese companies.

February 53 Gezer & Haifa HRSG Units(Contract awarded by Siemens)

TAEA

N T

HER

MAL

PO

WER

PLA

NT

UN

ITS

1~4

2002 HIGHLIGHTS

Brought to you by Global Reports

our technology and price competitiveness are now rec-

ognized throughout the world.

We won HRSG orders for a total of 157.3 billion won,

which is nearly as good as last year’s sales figures.

Substituting for the US power market, which has

been stagnant since the 9/11 terrorist attack, we

shifted our focus to Europe and Central Asia so that

our major clients are now Spain and Israel. Particularly,

since we successfully completed the Gezer Project -

the first HRSG project in Israel - and were highly

praised by IEC (Israel Electric Corp.), we have secured

an advantageous position for upcoming coal thermal

plant projects.

With a decreasing number of new projects

and fierce competition in overseas markets, 2002

was a tough year for domestic power plant companies.

Even so, we were successful in achieving 727.5 billion

won in orders, 439.2 billion won in sales and 17.2 bil-

lion won in operating profit.

Amid a stagnant global economy, many power plant

projects were either cancelled or dominated by a few

major companies. Despite the reduction in thermal pow-

er plants and HRSG markets that resulted from this

trend, we were able to win the Dangjin Thermal Power

Plant 5 and 6 project after a heated competition

against MHI, IHI and other Japanese companies that

participated in the international bid. This means that

REVENUES ORDERS

900

800

700

600

500

400

300

200

100

90

80

20022001

March 132 Gibraltar HRSG Units (Contractawarded by Siemens)

March 29Dangjin Units 5 and 6 boiler package order

2002 REVIEW

In billions of Korean won

HADONG THERMAL POWER PLANT DE-NOx/DE-SOx FACILITY

Brought to you by Global Reports

SAM

CH

EON

PO T

HER

MAL

PO

WER

PLA

NT

UN

ITS

1~4

As for technology development, we were able to com-

pletely assemble the boiler unit, steel structure, pipes

and electric systems in our factory before shipping the

five 1,100-ton steam boilers to the 62.5MIGD Umm Al

Nar Project. The one-module boilers greatly shortened

the usual 18-month process by nine months, while the

boiler efficiency rate exceeded 92% in reliability and

performance tests. With outstanding performance

and quality, our technology competitiveness in the

design and manufacturing of one-module boilers is now

at an international level.

Our goal for this year is 926.1 billion won

in orders, 565 billion won in sales and 11.6 billion won

in operating profit. We will bolster our cost competi-

tiveness and quality to win more domestic coal ther-

mal plant projects, while sharpening our business

edge through local outsourcing and sustaining our

market share in foreign markets. To this end, we aim

to strengthen business alliances with our major clients

like Siemens, GE and Alstom. As for HRSG projects, we

are planning to win more orders from major buyers like

Simens and major companies in China and Iran through

package deals by regions and products.

September 4Grand Opening of Taean ThermalPower Plant 5 & 6 (Contract award-ed by Korea Western Power Co.)

2003 PREVIEW

KRW565billion

KRW926billion

2002

2002

PROJECTED 2003 REVENUES

PROJECTED 2003 ORDERS

2003

2003

May 20 2 Amorebieta HRSG Units(Contract awarded by GE)

Brought to you by Global Reports

Based on technology and experience accumulated

over the supply of nearly 20 supercritical pressure

boilers, we are currently developing a mode of next-

generation ‘ultrasupercritical’ boilers to keep pace

with the global trend of building higher tempera-

ture/pressure/capacity power plants. Also, to improve

and differentiate our technology in the area of Circulating

Fluidized Bed (CFB), we are carrying out R&D activi-

ties to come up with more environmentally friendly and

superior CFB combustion technology. This will be

accomplished by developing new and improved com-

ponents for CFB combustion, such as fluidizing noz-

zles and solid recycling systems. All of this is aimed

at establishing a basis that will enable convenient

supply to the increasingly popular low-pollution coal

thermal and combined cycle power plants using low

quality fuels.

Other detailed plans of action include cost reduction

activities, the development of design and core technology,

project risk management and an establishment of

comprehensive management systems in accordance

with our “Change program.”

Brought to you by Global Reports

RESEARCH & DEVELOPMENT Driven by intense competition in combustion technology and increasingly strict

international environmental regulations, R&D in the thermal power plant industry today is largely focused

on advanced firing systems designed to maximize efficiency and minimize emissions. Our efforts have

focused on optimizing combustion efficiency by combining low-NOx burners with air staging and reburning

to create firing systems that are significantly more cost-effective to build, operate, and maintain. In

addition to new and retrofit coal-fired power plant installations, our research has applications in fossil fuel

combustion equipment design. It will also serve as the basis for future development projects involving

emissions reduction and other clean coal technologies.

Boiler technology for next-generation ultrasupercritical power plants is another area we’re actively invest-

ing in. Backed by technology and expertise acquired through our delivery of over twenty 500 MWe coal-fired

supercritical boilers to date, we’re now working on boiler designs for future plants that will operate at steam

temperatures exceeding 600°C to generate upwards of 1,000 MWe. In short, our firing system

and ultrasupercritical boiler R&D projects are helping position us as an emerging player in the fastest-

growing segment of the power generation industry.

500 MWe KOREAN STANDARD COAL-FIRED POWER PLANTSince our first boiler order for Poryong Thermal Power Plant Units 3 and 4 in 1989, we’ve installed a total of twenty-two 500 MWe supercritica

fired plants across Korea. We’re proud that three of the plants we’ve helped build have won international recognition in recent years. In 1996, Power Engineering Internatio

honored Taean Thermal Power Plant Units 1 and 2 with its “Project of the Year” award. That same year, Electric Power International recognized Poryong Thermal Power

Plant Units 3 and 4 with its “1996 Power Plant Award.” Most recently, Power Engineering named Dangjin Thermal Power Plant the “Project of the Year” in its December

2001 edition. And we expect the accolades to keep coming.

Brought to you by Global Reports

REVENUES ORDERS

900

800

700

600

500

400

300

200

100

90

80

In billions of Korean won

200220012000

Our experience in the nuclear power generation

equipment industry dates back to the mid-1980s

when we delivered the steam turbine-generator sets

for Yonggwang Nuclear Power Plant Units 3 and 4

(1,000 MWe x 2). Since then, we’ve made inroads

into virtually every area of turbine and generator

manufacturing, building mutually profitable rela-

tionships with major clients that provide a large

majority of our overall orders as well as access to the

most advanced technology in the industry. And now

we’re applying our extensive experience and exper-

tise in design, manufacturing, service, and mainte-

nance to offer clients around the world total solutions

to their turbine and generator needs.

SHIN-KORI NUCLEAR POWER PLANT

In August 2002, we booked orders for two

1,000 MWe turbine-generator sets for

Units 1 and 2 of Shin-Kori Nuclear Power

Plant. We’re currently developing a 1,400

MWe set that will power Korea’s next-gen-

eration Advanced Power Reactor 1400

reference design slated to enter com-

mercial service by 2010.

March 29

Dangjin Thermal Power PlantUnits 5 & 6 Turbine/Generatorsets order

2002 HIGHLIGHTS

GENERATOR STATOR BARS UNDERGOING ASSEMBLY

Brought to you by Global Reports

With a momentous awarding of two 500MWe

turbine-generator sets of Dangjin Thermal Power

Plant Units 5 and 6, which was the first international

open bid ever in the Korean power generation mar-

ket, Doosan secured orders of six 1,000MWe Turbine-

generator sets in Nuclear Power Plants.

Orders amount to KRW 400.9 billion, continuing the

growth trend that accelerated with orders from GE

Power Systems and Harbine Turbine Company in

China. Revenues reached to KRW 296.3 billion.

2002 REVIEW

May 1

Light Water Reactor Projects Units 1& 2 Turbine/Generator sets order

PROJECT EQUIPMENT CLIENT COUNTRY

Andong HPP Units 1/2 Excitation System Korea Water Resources Korea

Dangjin TPP Units 5/6 Turbine-Generator Sets Korea East-West Power Co. Korea

GE Sourcing Agreement Turbine-Generator Sets GE Power Systems USA

Laem Chabang CCPP Gas Turbine Generator LCP/Fortum Power Engineering Thailand

Light Water Reactor Units 1/2 Turbine-Generator Sets Korea Electric Power Corp. Korea

Shin-Kori NPP Units 1/2 Turbine-Generator Sets Korea Hydro & Nuclear Power Korea

Shin-Wolsong NPP Units 1/2 Turbine-Generator Sets Korea Hydro & Nuclear Power Korea

Ulchin NPP Units 1/2 Moisture Separator Reheater Korea Hydro & Nuclear Power Korea

Brought to you by Global Reports

As the downturn in the global power gen-

eration industry continues to redefine the competitive

landscape, we’re confident that we have the critical mass

of technical, manufacturing, and real-world experi-

ence necessary to compete with the world’s best.

We’re now well positioned to win orders at home and

around the globe for new equipment, replacement,

upgrade, and repair projects and will take on a business

opportunity through long-term cooperation with steam

turbine manufactures in China. Our advanced capabilities,

especially in respect to service and repair projects,

were demonstrated in mid-2001 when we serviced

and repaired the generator rotor of Unit 3 at Ulsan

Combined-Cycle Power Plant in a record time of 30 days,

and our selection as preferred bidder of generator,

excitor and IPB replacement of Kori Nuclear Power Plant

Unit 1.

From a financial perspective, we expect orders to lev-

el out in 2003, holding at just under KRW 328 billion as

domestic and overseas orders for steam turbines,

generators, and other equipment begin to recover. At

the same time, we expect revenues of KRW 287 billion

as we continue to optimize our manufacturing process-

es and accelerate our ability to fulfill the order back-

log in a timely way.

2003 PREVIEW

KRW287billion

KRW 328billion

2002

2002

PROJECTED 2003 REVENUES

PROJECTED 2003 ORDERS

August 9

Shin-Wolsong Nuclear Power PlantUnits 1 & 2 Turbine/Generator setsorder

2003

2003

Brought to you by Global Reports

RESEARCH & DEVELOPMENT As with any industrial facility project, limited space and environmental consid-

erations are becoming increasingly important issues for power plant owners. We currently have two main pro-

jects underway that are focusing on improving plant efficiency and capacity. The first is a 1,000 MWe ultrasupercritical

turbine generator for thermal power plants that promises to achieve higher efficiency and reliability as well as

lower operating costs and emissions than the supercritical 800 MWe design we’re currently developing for

Yongheung Thermal Power Plant Units 1 and 2. The second is a 1,400 MWe turbine-generator set for the next-

generation Korean nuclear power plant reference design—Advanced Power Reactor 1400—that’s expected to be

adopted for the eight nuclear units scheduled for tender over the remainder of the decade.

August 9 Shin-Kori Nuclear Power PlantUnits 1 & 2 Turbine/Generatorsets order

Located between the high-pressure and low-pressure sections of the turbine, the MSR plays a key role in optimizing the efficiency

of the nuclear steam cycle. We design and manufacture compact, high-efficiency MSRs with either two- or four-pass tube bun-

dles for both horizontal and vertical installations.MOISTURE SEPARATOR REHEATERS

Brought to you by Global Reports

Back in 1999, desalination was a small but growing

part of our business portfolio, supplying just over

8% of overall revenues. In the two years that have

passed, it’s become our top business field, providing

28% of the total in 2002. With a number of projects

either underway or fully completed in Kuwait, Saudi

Arabia and the UAE, we are today the undisputed

world leader in thermal desalination plant con-

struction. And with our unique ability to deliver seam-

lessly integrated turnkey water and power solutions

as well as next-generation hybrid desalination sys-

tems, we expect to be an even more dominant play-

er in the Middle East and markets around the world

in the years to come.

2002 HIGHLIGHTS

IDA PRESIDENTIAL AWARD

In March 2002, we won the IDA Presidential

Award as the first company in the world

to apply the hybrid method of plant tech-

nology, which we applied at the UAE

Fujairah Project.

January 24Completion of Az-Zour South Phase 3

PROJECT CAPACITY CLIENT COUNTRY

Az-Zour Phase 3 28.8 MIGD MEW Kuwait

Fujairah 660 MWe + 100 MIGD UOG UAE

Shoaiba Phase II 530 MWe + 100 MIGD SWCC Saudi Arabia

Taweelah A2 720 MWe + 50 MIGD ADWEA/CMS Energy UAE

Umm Al Nar B 62.5 MIGD ADWEA UAE

Brought to you by Global Reports

REVENUES ORDERS

1000

900

800

700

600

500

400

300

200

100

90

80

In billions of Korean won

200220012000

March 12IDA (International DesalinationAssociation) Presidential Award

In the last two years, we have proven our

uncontested status as a leading company in the

world desalination market by completing the Middle

East’s first IWPP project Al Taweelah A2 in 2001, Az-

Zour South Phase 3 in Kuwait and Umm Al Nar B

Station in the UAE, as well as the Al-Shoaiba Phase

2 project of Saudi Arabia in 2002.

In March of 2002 we applied a groundbreaking new

hybrid method at the 100MIGD Fujairah Water and

Power Plant project, which began in June 2001 and

is currently under construction. In recognition of this

accomplishment and our continued efforts toward

technology development, we won the Presidential

Award from IDA (International Desalination

Association). The hybrid method is a combination

of Reverse Osmosis Process and Multi-Stage Flash

2002 REVIEW

AERIAL VIEW OF TAWEELAH A2 POWER & DESALINATION PLANT

Brought to you by Global Reports

FUJA

IRAH

DES

ALIN

ATIO

N P

LAN

T EV

APOR

ATOR

SHI

PMEN

T

Distillation, and our project was the

world’s first case of applying this

method to a 100MIGD desalination

plant.

As a result, we have achieved 799.7 bil-

lion won in sales (30% increase from

2001) and an operating profit of 79.4 bil-

lion won, which is significantly higher

than the year before.

The global desalination market has been

showing steady growth, and is expected to reach a total

size of 27 trillion won by the year 2010. Such unprece-

dented market expansion is largely due to a serious

water shortage in the Middle East and Africa caused

by industrialization and climate change, as well as

the increasing number of independent water and pow-

er projects underway in Middle Eastern countries.

We have set a goal of achieving a total of 1 trillion 255

billion won of orders in 2003.

2003 PREVIEW

KRW895billion

KRW700billion

2002

2002

PROJECTED 2003 REVENUES

PROJECTED 2003 ORDERS

2003

2003

June 1Completion of Umm Al Nar B Station

Brought to you by Global Reports

In order to achieve this goal, we intend to maximize the

number of orders through the Attractive Value

Proposition plan and world-class marketing. Our main

goal for this year is to ensure price competitiveness over

our competitors by positioning sales teams further into

Middle Eastern regions, establishing strategic ties

with Saudi Arabia in the area of IWPP, establishing our

value proposition and winning combined package con-

tracts.

In terms of business management, we will establish

an EPC basis by creating a comprehensive manage-

ment system and drafting standard procedures.

As for technology development, we plan to seize new

market share through the realization of MED/RO

development. The objective is to gain world-class

leadership in terms of cost dimension through continued

operational improvement. We will concentrate on

heightening the operation of DTC/PSM and work on

developing made-in-Korea package items.

Brought to you by Global Reports

RESEARCH & DEVELOPMENT Over the past 20 years, we’ve emerged as the world’s leading builder of thermal

distillation plants using the multi-stage flash (MSF) distillation process—the most common desalination tech-

nology for large-scale facilities. Today, we’re expanding our thermal technology portfolio with multi-effect (ME)

and vapor compression (VC) distillation technologies for installations with water production requirements of under

5 MIGD and 1 MIGD per evaporator, respectively. We’re also moving into the membrane separation field with reverse

osmosis—the second most common desalination technology in terms of installed capacity—through the Fujairah

project. The world’s largest hybrid facility to date combining multi-stage flash distillation and reverse osmosis sys-

tems, Fujairah promises to deliver greater operational flexibility, optimal water quality, and lower costs, making

it a model for future projects in the region and around the world.

SeawaterBrineSteam

DistillateNon-Condensible Gas

Anti-Scale Chemical

Anti-Foam ChemicalSodium Sulphite

Deaerator

Distillate Pump

Blow-Down Pump

Adjustable Orifice

Flash Chamber

Distillate Tray

Condensate Pump

Brine Heater

LP Steam

To Outfall

After Condenser

To ATM

3rd StageEjector

2nd StageEjector

1st StageEjector

MP Steam

Precondenser

From Stage 10

From Stages 1~4

Brine RecirculationPump

To Outfall

Mak

e-Up

Wat

er

From Seawater

Widely used in large-scale desalination facilities, the MSF distillation process begins with the boiling of seawater in a brine heater. The

brine is then fed through a succession of 15 to 25 “flash chambers” where the air pressure is progressively reduced, causing the brine

to “flash” or instantly boil as it enters each new stage. The water vapor released is then condensed and collected for use.MULTI-STAGE FLASH DISTILLATION

Brought to you by Global Reports

January 31Forge shop sets a world record ofmonthly production of forged mate-rials

While it generated only 8% of total rev-

enues in 2002, our casting and forging operation

plays a key supporting role virtually in all our busi-

nesses; it is what keeps our steel foundry and forge

shop operating 24 hours a day. In terms of industries

served, turbine runners, rotors, and other power

plant equipment lead with 37% of the total, while

marine engine components like crankshafts and

connecting rods stepped in with 23%. Special steels

for plastic molds, tools and dies came next with 17%,

followed by shipbuilding components like rudder

horn and propeller shaft at 10%. Rounding out the list,

rolls and mill housings for steel mills provided 7%,

and others added the final 6%.

Although orders and revenues for this business have

enjoyed solid growth in recent years, we’ve recorded

operating losses since 1998. We set out to rectify this

problem in 2002 with a focus on qualitative growth that

targeted the most profitable industries. In our home

market, we identified the shipbuilding, marine engine,

tool and die, and steel plant industries as strategic fields.

In our largest international market - China - the short-

list consisted of only three central elements: ship-

building, marine engines, and power generation.

Armed with this perspective, we then determined an

optimal product mix based on our sales and production

capabilities and set out on the road to profitability.

WORLD’S LARGEST CRANKSHAFT

PRODUCTION CAPACITY

Ten years after it first opened its doors

in December 1992, the Doosan Crankshaft

Factory has grown to be the world’s

largest crankshaft factory with a pro-

duction capacity of 150 units per year.

Based on synergy effects achieved through

a decade of applied know-how, advanced

manufacturing technology and system

capabilities, it is now the most compet-

itive factory in the world.

2002 HIGHLIGHTS

Plastic Mold & Tool Steels Runner Crowns, Blades & Bands Rotors & Casings

2002 REVIEW

Roll & Mill Housings

Brought to you by Global Reports

As our select-and-focus strategy took effect, orders

increased nearly 15% to KRW 247.4 billion for the year,

roughly 8% short of our 2002 target. Revenues continued

to outpace projections to reach KRW 206.6 billion as we

made significant progress in reducing our order back-

log. But the most remarkable accomplishment of the

year was our return to profitability as our focus and hard

work helped us rebound from a KRW 3.8 billion gain in

2001 to post a KRW 20.8 billion profit.REVENUES ORDERS

In billions of Korean won

200220012000

240

230

220

210

200

190

180

170

160

150

140

March 21Shaft forging order for BharatHeavy Electricals Ltd. (India)

May 31Casting component order forpress from Canton Drop Forge(USA)

POURING 350 TONS OF CAST STEEL AT FOUNDRY SHOP

PROJECT EQUIPMENT CLIENT COUNTRY

Azumi Dam Crown and Band Toshiba Corp. Japan

General Order Shield Shells Precision Components Corp. USA

Gwangan Bridge Various Components Dongah Construction Korea

Indra Sargar Dam Runner Bharat Heavy Electricals Ltd. India

Ongoing Order Crankshafts and Components HSD Engine Korea

Ongoing Order Rudder Horn Daewoo Shipbuilding Korea

Three Gorges Dam Crown and Band Harbin Electrical Machinery China

Brought to you by Global Reports

With a basic foundation for profitability

now in place, our next challenge is to keep building on

that success. In 2003, we’ll continue to expand our

international marketing efforts as we move ahead

with a business-wide initiative to sharpen our competitive

edge. We’ll be cutting manufacturing costs through

process improvements as well as pursuing incre-

mental cost reductions across the board. We’ll also be

reducing lead-time as we trim inventories and fine-tune

processes to cut reworking time and costs. Taken

together, we expect this strategic focus on profitabil-

ity to boost orders more than 2% to over KRW 252.5 bil-

lion in 2003 as it keeps revenues growing, pushing them

upwards of 13% to KRW 233.2 billion.

TECHNICAL CAPABILITIES It takes state-of-the-art facilities and experience to produce quality castings

and forgings. Our steel foundry is capable of producing 216,000 tons of melting iron and 20,000 tons of steel

castings annually, including individual castings of up to 350 tons. Our forge shop is equipped with a 10,000-

ton forging press and vertical heat-treatment furnace that enable us to produce 100,000 tons of steel forg-

ings annually, including individual forgings of up to 270 tons. Finally, our ISO 9001 quality management sys-

tem and full range of ASME certificates covering nuclear fabrication, boiler piping and vessels, and casting

and forging materials are backed up by a comprehensive start-to-finish inspection and testing regime to ensure

top quality, performance, and client satisfaction.

2003 PREVIEW

KRW 233billion

KRW 253billion

2002

2002

PROJECTED 2003 REVENUES

PROJECTED 2003 ORDERS

June 27Crown and band order forWujiangdu project from TianjinAlstom (China)

September 31Long-term contract for roll withPOSCO (Korea)

2003

2003

Brought to you by Global Reports

SAGT RTGC DELIVERY

In February of 2001 and 2002, we shipped

9 RTGCs (first shipment) and then anoth-

er 9 RTGCs (second shipment) to the

South Asia Gateway Terminals in Sri

Lanka. We’ve now delivered a total of 28

RTGCs to that port, including the last

shipment of 10 RTGCs shipped in February

2003.

2002 HIGHLIGHTS February 7Busan/Gwangyang Port RMQCand RTGC order

As part of our efforts to keep pace with the international

trend of informationalization, we also provide COMIS

(Crane Operation Maintenance Information System)

apparatus to our clients to enable the more effective

maintenance of equipment we have supplied.

Besides our Doosan Changwon Plant, we also have fac-

tories in Haiphong, Vietnam and Lampung, Indonesia

to support the success of our marketing activities.

Engineers and quality management staff from our home

offices are assigned to these factories, ensuring that

all products manufactured in these factories are as

good as the ones manufactured in Changwon Plant,

by applying the most strict production and quality

management procedures.

Our BU (Business Unit) is engaged in the business of

designing, manufacturing and installing all kinds of

material handling equipment for ports, power plants, steel

mills and other industrial plants on a turnkey basis. The

business unit is particularly noted for its manufacture of

products that satisfy various aspects of customer demand

based on its own engineering capability.

Through continued technology development and strict

quality management procedures, we at Doosan are

always trying to supply the high-quality material han-

dling equipment that will best meet the demands of

our customers. As a result, our clients are well sat-

isfied with our equipment and the fact that it records

a lower ‘break-down time’ in commercial operation

compared to those supplied by other companies.

Brought to you by Global Reports

PROJECT EQUIPMENT/FACILITY CLIENT COUNTRY

Busan/ Gwangyang Container Terminal Ship-to-Shore Gantry Cranes Korea Express Co., Ltd. Korea/Rubber-Tyred Gantry Cranes

Busan Port Container Terminal Ship-to-Shore Gantry Cranes Korea Container Terminal Authority KoreaDangjin TPP Coal Handling System Korea East-West Power Co., Ltd. KoreaJakarta Int. Container Terminal Ship-to-Shore Gantry Cranes Huchison Port Holdings JakartaKEDO Polar Crane Korea Electric Power Corp. KoreaKoja Container Terminal Ship-to-Shore Gantry Cranes Huchison Port Holdings Ltd. IndonesiaPOSCO CSU Continuous Ship Unloader POSCO KoreaPort of Tanjung Pelepas Rubber-Tyred Gantry Cranes Port of Tanjung Pelepas MalaysiaSouth Asia Gateway Terminals Rubber-Tyred Gantry Cranes P&O Group Sri Lanka

MaterialHandlingEquipment

September 24Koja Container Terminal RMQCorder

July 15 Dangjin coal handling systemorder

For the past few years, a great number of

projects have been postponed or cancelled due to

stagnant economies at home and abroad. However,

with the recent resumption of projects and new invest-

ment plans, our orders and sales have increased by

a respective 90% and 75% compared to last year.

Particularly in the domestic market, we have won a

number of new projects including the coal handling

system for Dangjin Thermal Power Plant continuous

ship unloader for POSCO and container cranes for

Busan and Gwangyang Ports. Of particular note is the

rail mounted quayside gantry cranes for Korea Express

Co., Ltd., which are capable of handling 22 rows of con-

tainer vessels and are nearly complete.

We are also continuously paring down manufactur-

ing costs through our “Change program” and process

innovation, with which we aim to establish an improved

project management system.

2002 REVIEW

Brought to you by Global Reports

The domestic economy has been showing

signs of recovery since 2002, and although there may

be a number of unexpected turns it is highly proba-

ble that continuous investment will be made in pow-

er plants and social overhead capital. In line with the

Government’s plan to build Korea into a logistics cen-

ter for Northeast Asia, scheduled investment will be

made in the Busan New Port project and other port

construction projects.

Also, a worldwide trend for shipping cargo in containers

and the supply of large containerships are expected

to bring increased port investment and a demand for

equipment replacement.

Accordingly, our goal in 2003 is to focus all efforts on

increasing our orders by 40% and sales by 20% com-

pared to last year.

SUPER POST-PANAMAX CRANES, BUSAN PORT, KOREA

October 25POSCO continuous ship unloaderorder

December 19Jawaharlal Nehru Port Trust RMQCshipment

2003 PREVIEW

Brought to you by Global Reports

In 2002, the power plant construction market in

Korea withered by 1.9 trillion won as the Shin-Kori and Shin-

Wolsong Nuclear Power Plant projects, biddings and con-

tracts expected for issuance in 2002 were deferred until 2003.

Furthermore, the privatization of KEPCO and decreasing

electricity prices forced clients to squeeze their budgets

for power plant construction, while the need for price com-

petitiveness and more efficient management systems

impacted all construction companies.

Likewise in the overseas plant construction market, the

construction plans for many projects have been delayed

or cancelled due to a stagnant economy in Asia and the

sluggish growth of plant markets in South and Central

America.

However, under such restrictive and adverse circum-

stances, Doosan managed to win the construction con-

tract for Dangjin Thermal Power Plant Units 5 and 6 - the

only project in the domestic power plant market this year

- thanks to our continuous endeavors to improve com-

petitiveness through PRM (Project Risk Management), PSM

(Purchasing & Supply Management) and PI (Process

Innovation). Our victory was an exemplary case of prov-

ing our unsurpassed experience and price competitive-

ness, and confirmed that we still occupy an unchallenged

position in the Korean industry.

At the same time, our business in 2002 demonstrated sig-

nificant growth by recording a nearly 300% increase with

222.3 billion won in orders. Our sales also increased by

4% to record 158.1 billion won while operating profit

reached 19.7 billion won, which is nearly 97% of the oper-

ating profit recorded in 2001. All of this proved indis-

putably that we are the plant construction company

leader in all areas of system manufacturing, installa-

tion, construction and testing.

September 14Hoping Thermal Power PlantCompletion

DANGJIN THERMAL POWER PLANT 5 & 6

In April 2002, we won an order to build two

coal thermal plants using 500MW super-

critical boilers. The project is slated for

completion by June 2006, and we are

the first domestic company ever to build

a 500MW thermal power plant single-

handedly.

2002 HIGHLIGHTS

2002 REVIEW

Combined-Cycle Power Plants Pumped-Storage Power Plants Transmission Facilities

Brought to you by Global Reports

Since KEPCO subsidiaries have been plan-

ning to build additional power plants in accordance

with their Power Supply Milestone, a number of bidding

opportunities for new power plant projects are expect-

ed to be issued in the next three to four years. At least

four nuclear and thermal power projects are to take place

in the year 2003, and competition between a number of

plant companies - including firms that have newly

launched into the power plant market -will be greater

than ever.

To lead the power plant construction market and max-

imize profitability, we have established new management

policy, detailed strategies, established bidding com-

petitiveness and cost competitiveness, while at the

September 27Renewed KEPIC (MN,EN,SN)Mark and Obtained DN Certificate

November 7Completion of Wolsong CanisterInstallation

REVENUES ORDERS

In billions of Korean won

200220012000

350

300

250

200

150

100

50

0

-50

-100

-200

2003 PREVIEW

YON

GH

EUN

G T

HER

MAL

PO

WER

PLA

NT

UN

ITS

1 AN

D 2

KRW 216billion

KRW 528billion

2002

2002

PROJECTED 2003 REVENUES

PROJECTED 2003 ORDERS

2003

2003

Brought to you by Global Reports

Econ

omic

dev

elop

men

t and

con

stru

ctio

n go

han

d-in

-han

d in

our

indu

stri

aliz

ed w

orld

. Ove

r ttw

o de

cade

s, w

e’ve

hel

ped

build

Kor

ea’s

mod

ern

infr

astr

uctu

re th

roug

h a

long

list

of c

ivil

wo

ject

s th

at to

day

keep

peo

ple

and

good

s flo

win

g sm

ooth

ly a

cros

s th

e pe

nins

ula

by ro

ad a

nd r

we’

re d

edic

ated

to d

oing

mor

e of

the

sam

e ar

ound

Asi

a an

d th

e w

orld

in th

e 21

st c

entu

ry.

CIVI

L CO

NST

RUCT

ION

EXPRESSWAY PAVING WORK

FACILITIES Expressways Railways & Subways Bridges & Tunnels

Brought to you by Global Reports

Sports Complexes Apartment Complexes

CENTRAL EXPRESSWAY, KOREA

Brought to you by Global Reports

SEOSUWON-OSAN-PYEONGTAEK

EXPRESSWAY

In 2002, we won the SeoSuwon-Osan-

Pyeongtaek Expressway construction

project on an SOC basis. The 39.54km long

expressway is to be completed by

November 2007.

2002 HIGHLIGHTS

Following our licensing in 1980, our first project was

to build the infrastructure that has helped our affili-

ated heavy industries businesses collectively emerge

as Korea’s leading power and industrial plant solution

provider—our Changwon plant. Our civil construction

business has continued to grow over the past 23 years

as we’ve expanded our portfolio beyond transporta-

tion infrastructure to include apartment complexes,

distribution centers, and sports stadiums. Today, we

are an ISO 9001- and ISO 14001-certified general

construction firm capable of project planning, engi-

neering, construction, and supervision duties for pro-

jects of all types and sizes.

FebruaryCompletion of HSD EnginePlant Expansion

KOREA TRAIN EXPRESS HIGH-SPEED RAILWAY PROJECT

Brought to you by Global Reports

In 2002, backed by government policy/sup-

port and economic recovery, the number of con-

struction projects in the civil construction industry

was nearly 90% of the total projects awarded in 1997

before the economic crisis struck at the end of that year.

However despite the increasing number of projects, win-

ning contracts became increasingly difficult due to

the excessive number of construction companies and

an expansion of the Lowest Price Bid policy. The con-

ditions in the industry were further worsened due to

a declining economy and the Housing Stabilization

Program.

REVENUES ORDERS

900

800

700

600

500

400

300

200

100

90

80

In billions of Korean won

20022001

MarchCompletion of Hanaro Building

JuneCompletion of HwigyeongApartment Complex

2002 REVIEW

PROJECT CLIENT COUNTRY

Agro-Fisheries Distribution Center City of Seongnam Korea

Busan Container Port Expansion Busan New Port Korea

Busan Subway Busan Urban Transit Authority Korea

Central Expressway Korea Highway Corp. Korea

Daegu-Busan Expressway Korea Highway Corp. Korea

East Coast Expressway Expansion Korea Highway Corp. Korea

High-Speed Railway Korea Train Express Korea

High-Speed Railway Viaduct Taiwan High Speed Rail Corp. Taiwan

HSD Engine Plant Expansion HSD Engine Korea

Hwigyeong Apartment Complex Korea National Housing Corp. Korea

Jeju World Cup Stadium City of Seogwipo Korea

Sangam World Cup Stadium City of Seoul Korea

Woomyun Tunnel Woomyun San Development Korea

Brought to you by Global Reports

Although the number of public and civil

engineering construction projects has increased, the

total project amount is expected to decrease by about

1% to 76 trillion 200 billion won compared to last year.

This situation is largely due to the housing stabiliza-

tion policy and unstable economic conditions at home

and abroad. It is also forecast that from early this year,

national construction laws and policy environments

will undergo major changes following the inaugura-

tion of a new federal government.

2003 PREVIEW

July Completion of Incheon DistrictPublic Prosecutor’s Office

NovemberCompletion of Sri Lanka WalaweLeft Bank Irrigation

Even amongst difficult business conditions in 2002, with

excessive competition for contracts and an increasing

number of construction companies, we recorded 405

billion won in orders and 394.7 billion won in sales, show-

ing a 3.2% and 33.8% respective increase compared

to 2001.

Particularly by winning construcition projects for the

SeoSuwon-Osan-Pyeongtaek Expressway following

the two SOC projects of Mt. Woomyun Tunnel and

Daegu-Busan Expressway awarded earlier, we have

secured our position as the market leader in the area

of SOC businesses.

KRW345billion

KRW 450billion

PROJECTED 2003 REVENUES

PROJECTED 2003 ORDERS

2002

2002

2003

2003

Brought to you by Global Reports

As a survival strategy to cope with changes in the con-

struction industry, we proposed a new vision for 2003:

“Transition into a Strategic Plan Oriented for High

Added Values.” We established the four major strate-

gies of: 1) Expansion of strategic plan-oriented busi-

nesses, 2) Winning contracts in the order of prof-

itability through the improvement of public construc-

tion bid competitiveness, 3) Improvement of cost com-

petitiveness through Operational Excellence and 4)

Maximization of company value by KMS establish-

ment and manpower training.

Based on these four strategies for the year 2003, we plan

to achieve 450 billion won in orders, 345 billion won in

sales and 42.9 billion won in operating profit.

We will combine all our efforts to achieve these goals

and maximize shareholder value by employing skilled

and experienced manpower, ensuring market com-

petitiveness, and strengthening our internal capabili-

ties as we benchmark other construction companies in

a similar situation to us.

DecemberCompletion of Jangyu TelephoneOffice

DecemberCompletion of Gyeongbu High-Speed Railway section 2-1

GYEONGBU HIGH-SPEED RAILWAY

Brought to you by Global Reports

DOOSAN AFFILIATES

A WORD ABOUT DOOSAN... Doosan Heavy Industries & Construction is proud to be a core member of

Korea’s oldest business group. Starting out in August 1896 as a small textiles store in Seoul, Doosan is

today a healthy 107-year-old group of 16 multinational companies involved in the industrial, consumer

goods, and service sectors. We build everything from power plants to apartments. We make high-tech

materials and machines. We brew beer and serve food. We sell fashion and publish books. We build

brands and invest in dreams. We educate and entertain. We consult and incubate. And we do all these

things with professionalism, passion, positivity, and pride. Visit us soon at www.doosan.com to find out

more about who we are and what we do.

Doosan Corporation

Liquor BGFood BGFashion BGTrading BGPublishing BGElectro-Materials BGTechpack BGMagazine BUInformation &Communication BU Doosan Tower BUBiotech BU

Oricom

Doosan Enterprise

Doosan Bears

Neoplux Capital

Korea Book Promotion

Wilus

Novos

Dentsu, Young & Rubicom Korea

HSD Engine

Doosan Mecatec

Doosan TMS

Samhwa Crown & Closure

Semicontech

Doosan Construction & Engineering

Doosan Heavy Industries & Construction

Brought to you by Global Reports

OVERSEAS BRANCHES

Doosan Heavy Industries America Corp.140 Sylvan Avenue, Suite 3BEnglewood Cliffs, NJ 07632, USAPhone: 1-201-944-4554 Fax: 1-201-944-5022/5053

Doosan Heavy Industries Japan Corp.Room 2410, Mita Kokusai Bldg. 1-4-28Mita, Minato-ku, Tokyo 108-0073, JapanPhone: 81-3-3452-5451~3Fax: 81-3-3452-5624

Doosan Malaysia Sdn. Bhd.(Kuala Lumpur Office)Letter Box No. 86, 22nd FloorUBN Tower, 10, Jalan P. RamleeKuala Lumpur 50250, MalaysiaPhone: 60-3-2026-8890/60-10-513-3708 Fax: 60-3-2026-8891

Inkor Engineering Private Ltd.1508, Maker Chambers-VINariman Point, Mumbai 400 021, IndiaPhone: 91-22-202-6504/6516, 287-0674Fax: 91-22-202-6557

Beijing OfficeRoom 1904, Landmark Bldg.8 North Dongsanhuan RoadChaoyang Dist., Beijing 100004, ChinaPhone: 86-10-6590-0924/0109Fax: 86-10-6590-0991

Dubai OfficeOffice #1002, Al Moosa Tower IISheikh Zayed Road, P.O. Box 11859Dubai, UAEPhone: 971-4-332-2703Fax: 971-4-332-2714

Frankfurt Office4th Floor, Arabella CenterLyoner Strasse 44-4860528 Frankfurt am Main, GermanyPhone: 49-69-69-5004 0Fax: 49-69-69-5004 10

Riyadh OfficeP.O. Box 9656, Riyadh 11423Saudi ArabiaPhone: 966-1-419-1920/1696/0397Fax: 966-1-419-1995

Taipei Office704, No. 51, Keelung Road Sec. 2Taipei, TaiwanPhone: 886-2-2739-2255Fax: 886-2-2739-2266

Schenectady OfficeRoom 33-202A, General Electric Bldg.One River Road, SchenectadyNY 12345, USAPhone: 1-518-385-5218/2629Fax: 1-518-385-4984

Windsor Office2000 Day Hill Road, P.O. Box 500Windsor, CT 06095, USAPhone: 1-860-731-6482/6479Fax: 1-860-731-6478

OVERSEAS SUBSIDIARIES

Ceylon Heavy Industries & Construction Co., Ltd. (CHICO)Oruwala Athurugiriya, Sri LankaPhone: 94-1-561310/561448Fax: 94-74-440030

Han-Viet Heavy Industry & ConstructionCorp. (HANVICO)933 Ton Duc Thang StreetHong Bang Dist., Hai Phong, VietnamPhone: 84-31-712-708~711Fax: 84-31-712-714~5

HF Controls Corporation16650 Westgrove Drive, #500Addison, TX 75001, USAPhone: 1-972-367-4600Fax: 1-972-367-4689

Hanjung Power Ltd. (HPL)P.O. Box 2803, Boroko, NCDPort Moresby, Papua New GuineaPhone: 675-320-0529/321-2932Fax: 675-321-2984

Perak-Hanjoong Simen Sdn. Bhd. (PHS)Batu 14, 33700 Padang Rengas State of Perak, MalaysiaPhone: 605-758-5648/758-4002-202Fax: 605-758-4052

PT. Doosan IndonesiaJl. Raya Soekarno-Hatta Km. 115 Srengsem, PanjangBandar Lampung, IndonesiaPhone: 62-721-32288/32292Fax: 62-721-33216

Shada Industrial Construction Services Co., Ltd.P.O. Box 9656, Riyadh 11423, Saudi ArabiaPhone: 966-1-460-0665~7Fax: 966-1-460-0682

DOMESTIC AFFILIATES

Doosan Mecatec Co., Ltd.64, Sincheon-dong, ChangwonGyeongsangnam-do, KoreaPhone: 82-55-279-5600/5700Fax: 82-55-279-5777

HSD Engine Co., Ltd.69-3, Sincheon-dong, ChangwonGyeongsangnam-do, KoreaPhone: 82-55-260-6001Fax: 82-55-260-6983

Brought to you by Global Reports

CHANGWON PLANT, DOOSAN HEAVY INDUSTRIES & CONSTRUCTION

Brought to you by Global Reports

Financial Statements

72 74 76 77 78

Inde

pend

ent A

udito

rs’ R

epor

t

Bal

ance

She

ets

Stat

emen

ts o

f Inc

ome

Stat

emen

ts o

f Cas

h Fl

ows

Stat

emen

tsof

App

ropr

iatio

ns o

f Ret

aine

d Ea

rnin

gs

Brought to you by Global Reports

I N D E P E N D E N T A U D I T O R S ’ R E P O R T

To the Stockholders and Board of Directors of Doosan Heavy Industries and Construction Co., Ltd.

We have audited the accompanying non-consolidated balance sheets of Doosan Heavy Industries and Construction Co.,Ltd. (the "Company") as of December 31, 2002 and 2001, and the related non-consolidated statements of income,appropriations of retained earnings and cash flows for the years then ended (all expressed in Korean won). Thesefinancial statements are the responsibility of the Company's management. Our responsibility is to express an opinionon these financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the Republic of Korea. Thosestandards require that we plan and perform the audit to obtain reasonable assurance about whether the financialstatements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting theamounts and disclosures in the financial statements. An audit also includes assessing the accounting principles usedand significant estimates made by management, as well as evaluating the overall financial statement presentation. Webelieve that our audits provide a reasonable basis for our opinion.

In our opinion, such non-consolidated financial statements present fairly, in all material respects, the financial positionof the Company as of December 31, 2002 and 2001, and the results of its operations, the appropriations of its retainedearnings and its cash flows for the years then ended in conformity with financial accounting standards generallyaccepted in the Republic of Korea.

Without qualifying our opinion, we draw attention to the following:

Through 2001, the Company recognized the dividends in the year when they were proposed as a liability at the balancesheet date. Effective January 1, 2002, the Company early adopted the Statement of Korea Accounting Standard(“SKAS”) No. 6, “Events Occurring after the Balance Sheet Date,” which requires recognition when dividends aredeclared which, for the Company, is after the balance sheet date. The Company's financial statements for the yearended December 31, 2001, which are presented herein for comparative purposes, are restated. This change resulted inan increase in the Company’s stockholders’ equity as of December 31, 2002 and 2001 by 12,829 million and 12,857million, respectively, and a decrease in liabilities as December 31, 2002 and 2001 by the same amounts. Suchaccounting change did not affect ordinary income, net income, ordinary income per share and net income per share forthe years ended December 31, 2002 and 2001.

Brought to you by Global Reports

A major portion of the Company’s sales are made to related parties, including HSD Engine Co., Ltd. The Company hadsales to its related parties, totaling 217 billion and 191 billion, and made purchases from its related parties,totaling 166 billion and 195 billion, during the years ended December 31, 2002 and 2001, respectively. The relatedreceivables were 26 billion and 57 billion, and the related payables were 39 billion and 29 billion as ofDecember 31, 2002 and 2001, respectively.

Effective March 23, 2001, the Company changed its name from Korea Heavy Industries and Construction Co., Ltd. toDoosan Heavy Industries and Construction Co., Ltd.

Accounting principles and auditing standards and their application in practice vary among countries. Theaccompanying non-consolidated financial statements are not intended to present the financial position, results ofoperations and cash flows in accordance with accounting principles and practices generally accepted in countries otherthan Korea. In addition, the procedures and practices utilized in Korea to audit such financial statements may differfrom those generally accepted and applied in other countries. Accordingly, this report and the accompanying financialstatements are for use by those knowledgeable about Korean accounting procedures and auditing standards and theirapplication in practice.

March 5, 2003

Deloitte ToucheTohmatsu

Brought to you by Global Reports

ASSETSIn thousands of Korean won

ASSETS 2002 2001

CURRENT ASSETSCash and cash equivalents 211,975,507 148,909,087Short-term financial instruments 113,676,934 157,065,642Marketable securities 9,664,775 16,508,534Accounts and notes receivable - net

Trade 724,212,236 627,452,321Other 109,419,117 91,023,040

Accrued income 514,145 5,515,747Short-term loans 1,094,428 938,565Inventories 81,915,171 171,161,159Advance payments - net 31,141,346 67,134,488Prepaid expenses 7,640,346 5,586,099Prepaid taxes and other 1,184,888 1,276,481Total current assets 1,292,438,893 1,292,571,163

NON-CURRENT ASSETSInvestments and other assets

Long-term financial instruments 80,065 6,596,065Investment securities 417,093,569 281,932,142Long-term loans 6,221,787 6,909,713Long-term receivables - net 32,656,833 37,778,365Guarantee deposits 113,614,113 154,414,393Deferred income tax assets 92,087,115 107,103,334Other 7,526,083 3,347,748Total investments and other assets 669,279,565 598,081,760

Property, plant and equipmentCost 1,535,704,951 1,521,091,876Less accumulated depreciation (451,306,809) (389,393,817)Property, plant and equipment - net 1,084,398,142 1,131,698,059

Intangible assets 48,197,477 56,966,532Total non - current assets 1,801,875,184 1,786,746,351

TOTAL ASSETS 3,094,314,077 3,079,317,514

Brought to you by Global Reports

AS OF DECEMBER 31, 2002 AND 2001

LIABILITIES AND STOCKHOLDERS’ EQUITY 2002 2001

CURRENT LIABILITIESAccounts and notes payable

Trade 281,280,977 189,646,330Other 97,662,290 201,116,903

Short-term borrowings 108,915,990 105,432,522Advance receipts 15,557,854 25,199,822Withholdings 10,023,081 6,608,530Accrued expenses 10,753,181 24,974,780Income taxes payable 11,978,414 —Billings in excess of costs and recognized profit 141,128,403 260,275,427Current portion of debentures - net of discounts — 299,111,563Current portion of conversion bonds - plus accrued interest

and net of discounts 34,534,321 —

Current portion of long-term debt 153,631,459 117,528,364Total current liabilities 865,465,970 1,229,894,241

LONG-TERM LIABILITIESConvertible bonds - plus long-term accrued interest and

net of discounts — 34,233,999

Long-term debt - net of current portion 338,331,249 52,813,792Long-term accounts payable - other 31,338,003 42,312,801Guarantee deposits received 5,363,619 20,123,419Accrued severance indemnities

- net of transfers to the National Pension Fund 96,664,066 103,628,797and deposits for severance indemnities

Reserve for loss on construction contracts 10,088,603 12,785,363Reserve for warranty costs 28,875,012 30,447,692Reserve for penalties for delays 6,175,487 10,642,241Retention for warranty 51,861,738 44,701,157Other — 10,678,789Total long-term liabilities 568,697,777 362,368,050Total liabilities 1,434,163,747 1,592,262,291

STOCKHOLDERS’ EQUITYCommon stock 521,000,000 521,000,000Capital surplus

Asset revaluation reserve 594,261,662 594,261,662Other capital surplus 2,618,558 33,609,107Total capital surplus 596,880,220 627,870,769

Retained earningsLegal reserve 58,383,000 57,083,000Reserve for corporate rationalization 36,407,000 35,407,000Other reserves 467,398,028 458,898,026Unappropriated retained earnings

(Net income of 77,338,111 in 2002 and 25,123,063 in 2001) 77,165,667 23,667,672Total retained earnings 639,353,695 575,055,698

Capital adjustment accountsTreasury stock (151,490,602) (180,659,519)Loss on valuation of investment securities (10,653,331) (2,260,533)Overseas operations translation credit (debit) (13,550,790) 12,328,254Gain (loss) on valuation of forward contracts 78,201,243 (66,279,446)Stock options 409,895 —Total capital adjustment accounts (97,083,585) (236,871,244)

Total stockholders' equity 1,660,150,330 1,487,055,223

TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY 3,094,314,077 3,079,317,514

In thousands of Korean won

Brought to you by Global Reports

2002 2001

NET SALES 2,771,630,264 2,468,417,290

COST OF SALES (2,452,849,495) (2,184,765,745)

GROSS PROFIT 318,780,769 283,651,545

SELLING AND ADMINISTRATIVE EXPENSES (168,724,921) (190,515,783)

OPERATING INCOME 150,055,848 93,135,762

OTHER INCOME (EXPENSES)Interest income 20,745,669 29,608,976Interest expense (42,923,880) (61,051,857)Dividend income 1,181,286 —Guarantee expense — (1,297,436)Gain (loss) on foreign currency exchange - net 10,275,185 (1,856,212)Gain (loss) on foreign currency translation - net 14,644,225 (3,255,911)Loss from strikes (28,430,732) (6,438,243)Gain (loss) on valuation of marketable securities - net (5,014,748) 8,289,700Bad debts — (563,299)Reversal of allowance for doubtful accounts 1,591,306 11,693,068Loss on valuation of inventories (94,085) (211,178)Loss on disposal of investment securities — (1,271,109)Impairment losses on investment securities (10,935,935) —Gain (loss) on valuation of investment securities

using the equity method of accounting - net (9,457,743) 7,374,499

Gain (loss) on disposal of property, plant and equipment - net (5,287,520) 8,331,904Impairment losses on development costs (7,268,075) (1,762,023)Gain (loss) on valuation of forward contracts 334,178 (1,768,255)Gain (loss) on forward contract transactions - net 28,480,012 (3,769,394)Other - net (13,562,247) 4,627,189Other expenses - net (45,723,104) (13,319,581)

ORDINARY INCOME 104,332,744 79,816,181

EXTRAORDINARY GAIN (LOSS)Other special losses - net — (37,909,310)

INCOME BEFORE INCOME TAXES 104,332,744 41,906,871

INCOME TAX EXPENSE (26,994,633) (16,783,808)

NET INCOME 77,338,111 25,123,063

ORDINARY INCOME PER SHARE 904 526

NET INCOME PER SHARE 904 257

DILUTED ORDINARY INCOME PER SHARE 879 521DILUTED INCOME PER SHARE 879 263

In thousands of Korean won, except for share data

Brought to you by Global Reports

FOR THE YEARS ENDED DECEMBER 31, 2002 AND 2001

In thousands of Korean won

2002 2001

RETAINED EARNINGS BEFORE APPROPRIATIONSBeginning of the year 10,811 11,709 Loss on valuation of investments

using the equity method of accounting (183,255) (1,467,100)Net income for the year 77,338,111 25,123,063End of the year 77,165,667 23,667,672