Embed Size (px)

Citation preview

Don’t Blame the Rearview Mirror:How Actuaries Can Help Put Claims

Managers in the Driver’s Seat

John W. Rollins, FCAS, MAAAJohn W. Rollins, FCAS, MAAA

Florida Farm Bureau Insurance Cos.Florida Farm Bureau Insurance Cos.

Casualty Loss Reserve SeminarCasualty Loss Reserve Seminar

Chicago, ILChicago, IL Sept. 9, 2003Sept. 9, 2003

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 2

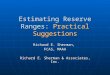

Overview of Topics

Communication between Claims and Actuary Communication between Claims and Actuary on on operatingoperating issues is key to profitability issues is key to profitability

Main Theme:Main Theme:

Three critical spheres:Three critical spheres:

Planning, staffing and incentivesPlanning, staffing and incentives

Reserving and financial reportingReserving and financial reporting

Coding and statisticsCoding and statistics

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 3

Profitability and Claims Operations Actuaries know loss costs are related to Actuaries know loss costs are related to

claim disposal rates and severityclaim disposal rates and severity

But disposal rates and severity are But disposal rates and severity are themselves related to other operating themselves related to other operating indicators in Claims:indicators in Claims: Inventory (pending files per adjuster)Inventory (pending files per adjuster) Staffing (exposures in-force per adjuster)Staffing (exposures in-force per adjuster)

Further, the strength of these “second-Further, the strength of these “second-order” relationships depends on the order” relationships depends on the planning metrics used in Claimsplanning metrics used in Claims

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 4

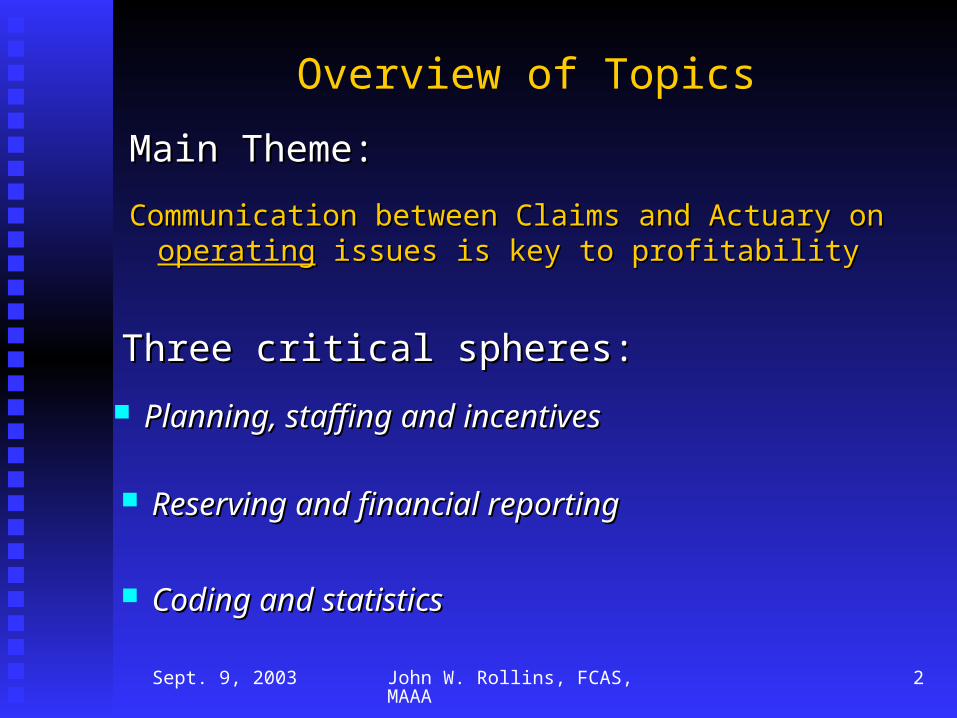

The Claims-Actuary “Feedback Loop”

Assume initial values for:Assume initial values for:

Exposure in-force, pending files, staffingExposure in-force, pending files, staffing

Assume constants for:Assume constants for:

Claim frequency, disposal rate per adjusterClaim frequency, disposal rate per adjuster

Assume adequate rate level is:Assume adequate rate level is:

[Loss Cost] x [Expense Multiplier][Loss Cost] x [Expense Multiplier]

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 5

The Claims-Actuary “Feedback Loop”

Then plausible model for claims operations is:Then plausible model for claims operations is:

Closed claims = [disposal rate] x [staffing]Closed claims = [disposal rate] x [staffing]

Incurred claims =Incurred claims =

[frequency] x [begin exposure][frequency] x [begin exposure]

End pending claims =End pending claims =

[Begin pending] + [incurred] - [closed][Begin pending] + [incurred] - [closed]

End staffing =End staffing =

[Begin staffing] x [adjuster hiring rate][Begin staffing] x [adjuster hiring rate]

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 6

The Claims-Actuary “Feedback Loop”

But Claims performance affects rates/growth:But Claims performance affects rates/growth:

Average Severity (above base amount) =Average Severity (above base amount) =

[K[K22] x ([Incd. claims] – [Closed claims])] x ([Incd. claims] – [Closed claims])

Exposure growth rate (above pop. base) =Exposure growth rate (above pop. base) =

[K[K11] x ([Adequate rate] – [Actual rate])] x ([Adequate rate] – [Actual rate])

Loss Cost = [frequency] x [severity]Loss Cost = [frequency] x [severity]

New exposure = [Old exposure] x [Growth rate]New exposure = [Old exposure] x [Growth rate]

New rate = [Old Loss Cost] x [Growth rate] x New rate = [Old Loss Cost] x [Growth rate] x [Expense Multiplier][Expense Multiplier]

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 7

Feedback Loop: Key Assumptions

Key model assumption is adjuster hiring rate:Key model assumption is adjuster hiring rate:

If hiring proportional to If hiring proportional to exposure exposure growthgrowth, model remains in equilibrium, model remains in equilibrium

If hiring proportional to If hiring proportional to pending inventorypending inventory, , equilibrium is uncertain – too late for equilibrium is uncertain – too late for stable results by time inventory buildsstable results by time inventory builds

Growth track depends on loss costs, which Growth track depends on loss costs, which depend on severity, which depends on growth depend on severity, which depends on growth because of staffing assumptionsbecause of staffing assumptions Negative feedback allows long-run stabilityNegative feedback allows long-run stability

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 8

Feedback Loop: Key Assumptions

Another key model assumption:Another key model assumption:

Severity depends on inventory pressureSeverity depends on inventory pressure

Claims operations may incent adjusters Claims operations may incent adjusters based on files closed and disposal rate, based on files closed and disposal rate, but but NOTNOT include financial metrics like: include financial metrics like: Paid average severity vs. settlement Paid average severity vs. settlement

lag and policy limitlag and policy limit Reserve development and initial Reserve development and initial

accuracy (discussed later)accuracy (discussed later)

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 9

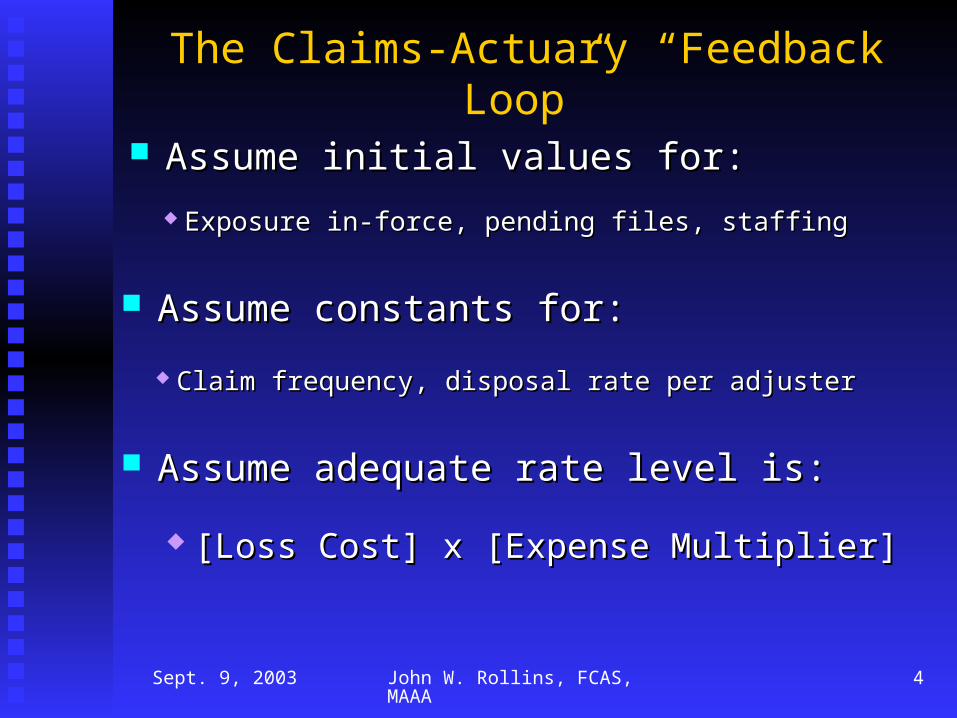

Profitability and Feedback: Actions

Actuary can provide user-friendly data Actuary can provide user-friendly data to Claims management for planning:to Claims management for planning:

Earned and in-force exposure per adjusterEarned and in-force exposure per adjuster

Lagged severity vs. past inventoryLagged severity vs. past inventory

Lagged inventory vs. past exposure growthLagged inventory vs. past exposure growth

Claims must commit to operational usage:Claims must commit to operational usage:

Budgeting with actuarial growth projectionsBudgeting with actuarial growth projections

Rewarding adjusters for financial goalsRewarding adjusters for financial goals

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 10

Reserving Issues

Actuaries can assist Claims in setting:Actuaries can assist Claims in setting:

Factor (formula) reserves for new claimsFactor (formula) reserves for new claims

Case reserves for pending claimsCase reserves for pending claims

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 11

Reserving Issues: Factor Reserves

Using feedback loop discussed above, factor Using feedback loop discussed above, factor reserve formula can be adjusted for inventory reserve formula can be adjusted for inventory pressure and growth expectations as well!pressure and growth expectations as well!

Basic factor reserve formula should reflect:Basic factor reserve formula should reflect: Historical average paid severityHistorical average paid severity

ProbabilityProbability of payment (no-pay ratio) of payment (no-pay ratio)

Latter often ignored by Claims due to:Latter often ignored by Claims due to:

Lack of mathematical perspectiveLack of mathematical perspective

Poor data on no-pay claim countsPoor data on no-pay claim counts

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 12

Reserving Issues: Case Reserves

Evaluate and help implement Claims Evaluate and help implement Claims benchmarking tools and use in projectionsbenchmarking tools and use in projections

Though province of adjusters, affected Though province of adjusters, affected by actuarial issues:by actuarial issues: Current reserving practices always affected Current reserving practices always affected

by prior years’ runoff (despite protests)by prior years’ runoff (despite protests)

Actuaries can help smooth cycle by:Actuaries can help smooth cycle by: Report runoff projections regularlyReport runoff projections regularly

Educate Claims and stress consistencyEducate Claims and stress consistency

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 13

Coding Issues: Garbage In, Garbage Out

Accurate statistical coding not typically a high Accurate statistical coding not typically a high priority for Claims; no performance incentivespriority for Claims; no performance incentives

But critical to Actuary for rates and reserves:But critical to Actuary for rates and reserves:

Categorical (cause of loss, coverage)Categorical (cause of loss, coverage)

Catastrophic event and “bad faith” codesCatastrophic event and “bad faith” codes

Dates of loss, report, settlementDates of loss, report, settlement

““Count” transactions (no-pay, closure)Count” transactions (no-pay, closure)

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 14

Coding Issues: Categories & Allocations

Categorical accuracy a challenge with modern Categorical accuracy a challenge with modern bulk-billed cost containment devices:bulk-billed cost containment devices:

Medical/Legal invoice reviewMedical/Legal invoice review

Auto Glass claimsAuto Glass claims

Difficulty of allocating back to file # leads to:Difficulty of allocating back to file # leads to: Establishment of fake file “dumpsters” with Establishment of fake file “dumpsters” with

bogus accident/report dates and statsbogus accident/report dates and stats

Misallocation of D&CC expense to A&OEMisallocation of D&CC expense to A&OE

Effect on rates and reserves obvious – to Effect on rates and reserves obvious – to usus

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 15

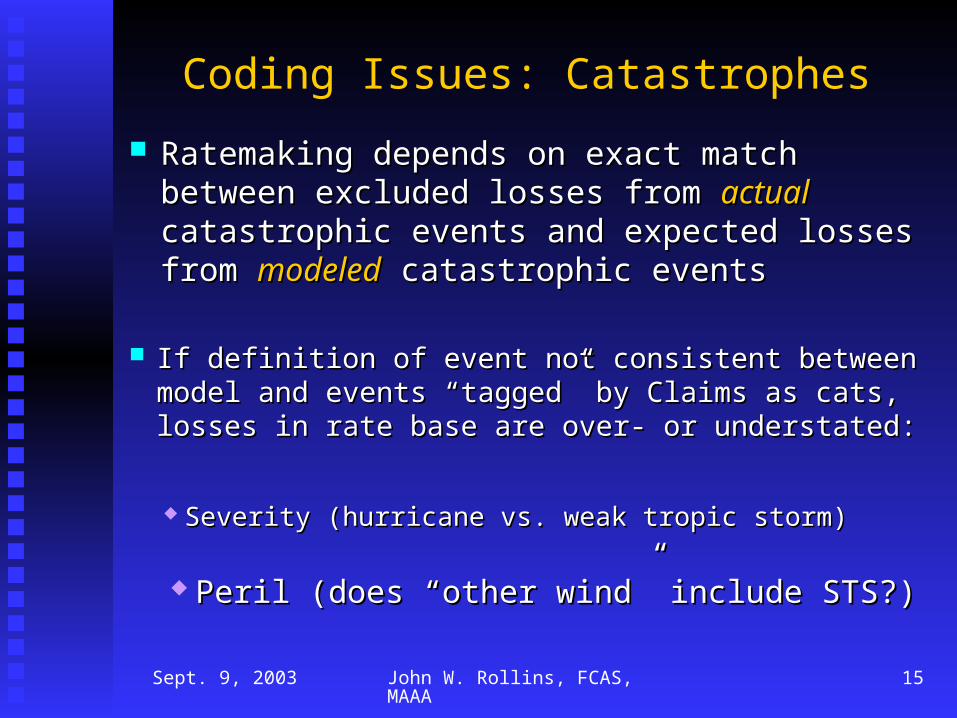

Coding Issues: Catastrophes

Ratemaking depends on exact match Ratemaking depends on exact match between excluded losses from between excluded losses from actualactual catastrophic events and expected losses catastrophic events and expected losses from from modeledmodeled catastrophic events catastrophic events

If definition of event not consistent between If definition of event not consistent between model and events “tagged” by Claims as cats, model and events “tagged” by Claims as cats, losses in rate base are over- or understated:losses in rate base are over- or understated:

Severity (hurricane vs. weak tropic storm)Severity (hurricane vs. weak tropic storm)

Peril (does “other wind” include STS?)Peril (does “other wind” include STS?)

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 16

Coding Issues: Catastrophes

Just using Property Claim Services definitions Just using Property Claim Services definitions no guarantee of proper match (models based no guarantee of proper match (models based on phenomena, not industry loss)on phenomena, not industry loss)

Also, cat codes should be “statistically Also, cat codes should be “statistically isolated” as much as possible:isolated” as much as possible: Line of business (i.e. no liability cat losses)Line of business (i.e. no liability cat losses)

Geographic area (agree on affected Geographic area (agree on affected territories/states)territories/states)

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 17

Coding Issues: Bad Faith (ECO/XPL)

Claims managers tend to be hostile to Claims managers tend to be hostile to segregating such losses in stat systems segregating such losses in stat systems due to easy discoverydue to easy discovery

Unfortunately, actuaries must have systematic Unfortunately, actuaries must have systematic way to identify and exclude excess amounts way to identify and exclude excess amounts from rate base in some statesfrom rate base in some states

F.S. 627.0651(12) prohibits use in ratesF.S. 627.0651(12) prohibits use in rates

Compromises on how data is stored and Compromises on how data is stored and coded may be necessarycoded may be necessary

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 18

Counting Claims – is it that simple?

Transaction coding rules deep in bowels Transaction coding rules deep in bowels of claims systems affect definitions of of claims systems affect definitions of “closed”, “no pay”, and date logic“closed”, “no pay”, and date logic

Unpublished systems changes distort Unpublished systems changes distort claim counts, affecting Actuary:claim counts, affecting Actuary: Data reporting (Sch. P part 5)Data reporting (Sch. P part 5)

Bulk reserve estimate (structural methods)Bulk reserve estimate (structural methods)

Ratemaking (severity/frequency trends)Ratemaking (severity/frequency trends)

Coverage partitions also affect claim countsCoverage partitions also affect claim counts

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 19

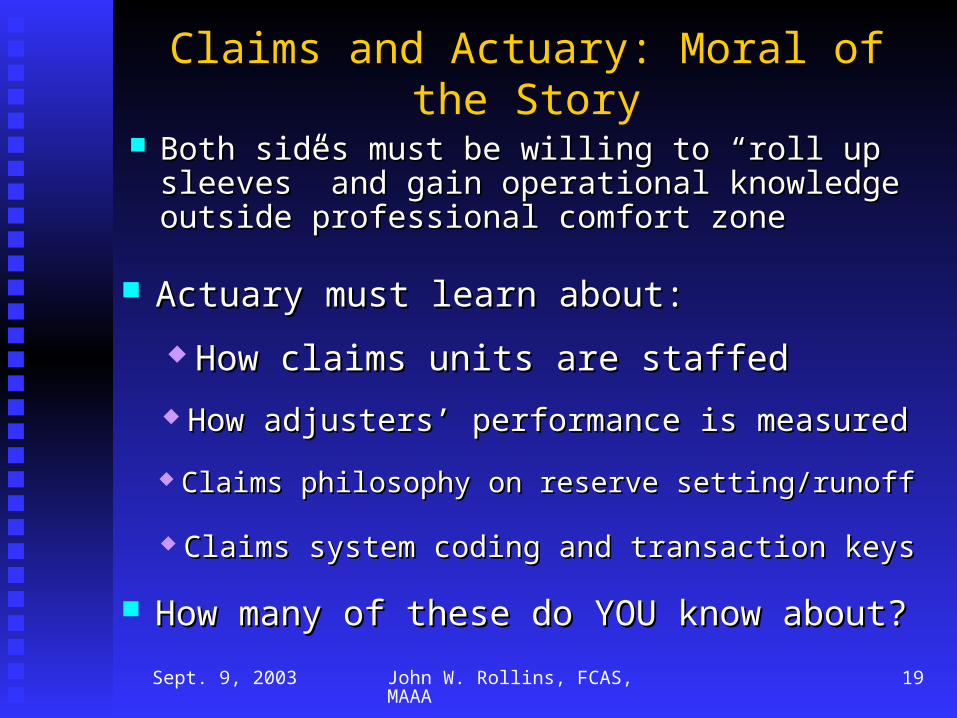

Claims and Actuary: Moral of the Story

Both sides must be willing to “roll up Both sides must be willing to “roll up sleeves” and gain operational knowledge sleeves” and gain operational knowledge outside professional comfort zoneoutside professional comfort zone

Actuary must learn about:Actuary must learn about:

How claims units are staffedHow claims units are staffed

How adjusters’ performance is measuredHow adjusters’ performance is measured

Claims philosophy on reserve setting/runoffClaims philosophy on reserve setting/runoff

Claims system coding and transaction keysClaims system coding and transaction keys

How many of these do YOU know about?How many of these do YOU know about?

Sept. 9, 2003 John W. Rollins, FCAS, MAAA 20

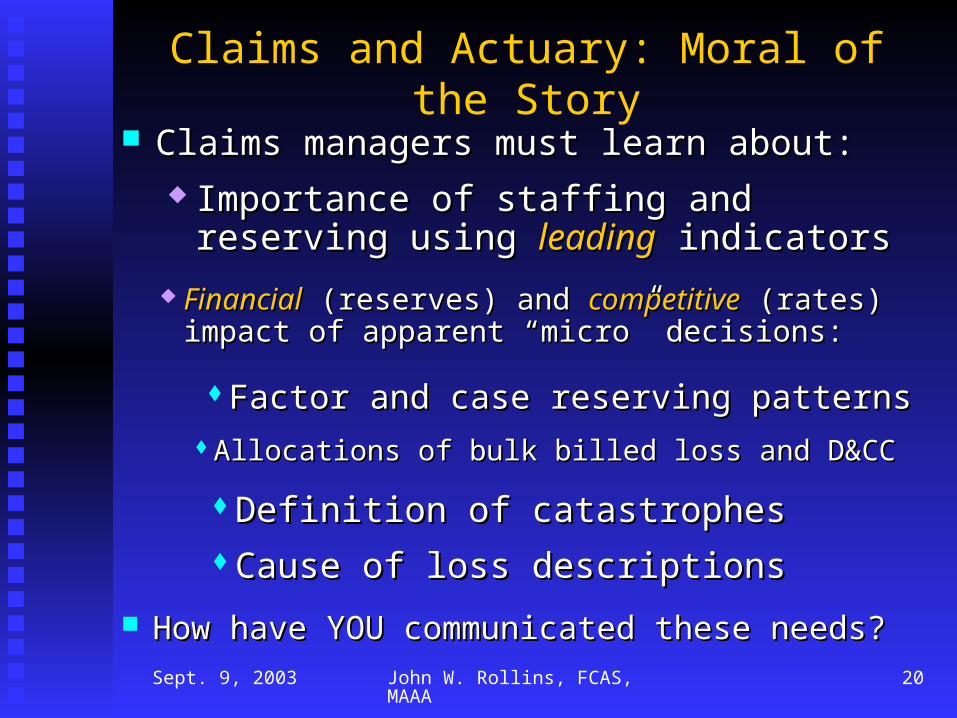

Claims and Actuary: Moral of the Story

Claims managers must learn about:Claims managers must learn about: Importance of staffing and reserving Importance of staffing and reserving

using using leadingleading indicators indicators

Factor and case reserving patternsFactor and case reserving patternsAllocations of bulk billed loss and D&CCAllocations of bulk billed loss and D&CC

How have YOU communicated these needs?How have YOU communicated these needs?

FinancialFinancial (reserves) and (reserves) and competitivecompetitive (rates) (rates) impact of apparent “micro” decisions:impact of apparent “micro” decisions:

Definition of catastrophesDefinition of catastrophesCause of loss descriptionsCause of loss descriptions

Speaker Contact Information

John W. Rollins, FCAS, MAAAJohn W. Rollins, FCAS, MAAA

Chief ActuaryChief Actuary

Florida Farm Bureau Insurance Cos.Florida Farm Bureau Insurance Cos.

5700 SW 34 St., Gainesville, FL 326085700 SW 34 St., Gainesville, FL 32608

(352) 374-1566(352) 374-1566 Fax: (352) 374-1514Fax: (352) 374-1514

[email protected]@sfbcic.com