Embed Size (px)

Citation preview

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 101

Domestic Supply Obligation and Gas Pricing Policy

Under the DSO, every gas producer must allocate a portion of their

production to the DSO before they can allocate any gas to other

commercial obligations. Non-compliance would result in significant

penalties. Once the gas producer has satisfied its DSO quota, any amount

of gas produced in excess of that can be sold on a willing buyer/willing

seller basis. The amount each supplier must allocate is not fixed but is

determined each year based on domestic demand and the number of gas

suppliers. Allocation to each supplier is done on an equitable basis

determined by the Minister for Energy.

Before the DSO was introduced and became operational in 2010,

practically all gas produced was exported because the price the PHCN

GenCos were willing (and able) to pay was too low to make it commercially

viable to supply gas to local GenCos. The situation could not persist if the

Nigerian government wanted to attract investment not only to the power

sector but also to the gas sector. It was accepted that the age of effectively

financially and structurally subsidising the power industry had passed.

However in order to ensure, as far as possible, a smooth transition to a

free-market system in the gas industry and in other strategic industries,

price increases would have to be managed rather than left to the market to

set the level.

The regulated pricing regime for the DSO (bulk of which is for power) is

based on determining the lowest cost of supply that will allow a 15% return

to the supplier. This floor price has been set at US$0.10 per Mcf31

. The

actual price paid for gas includes an escalation for inflation and an

indexation to the real time product price and/or any other indices that the

buyer and seller agree upon. The Ministry of Energy determined that the

cost reflective baseline was c.US$1.00 per Mcf by 2012. This was later

reviewed to US$1.50 per Mcf.

The main sticking point with the DSO has been on the issue of pricing

because the baseline price paid to the producers for DSO gas to

power has been below the market price (now US$3.80-4.00 per Mcf).

On 2 August 2014 the FGN announced a revision in the DSO gas-to-power

price for 2014 to US$2.50 from US$2.00 per Mcf as part of measures to

bridge this pricing issue. This brings the DSO price closer to, but still well

short of the market spot price of US$3.50-4.00 per Mcf. The DSO price is

expected to reach “export-parity” in 2016, thereby doing away with the need

for price regulation. MYTO II factors in a gas price of US$2.19 per Mcf by

2017

31

Thousand Cubic Feet

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 102

Chart 21: DSO Gas Price to Power Profile (2010-2013), US$/Mcf

Chart 22: Old Gas Price to Power vs Annual Price of US LNG Imports from Nigeria, US$/Mcf

Source: NERC, CSL Research Source: NERC, US EIA, CSL Research

Figure 30: Operation of the Domestic Supply Obligation

Source: CSL Research

1.00

1.50 1.50

1.80 2.00

2.50

3.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

2010 2011 2012 2013 2014 2015 Est. 2016 Est.

US

$ p

er

Mcf

Current Market (Spot) Price Range

2.50

On 2 August 2014 the FGN revised the 2014 DSO gas-to-power price to

US$2.50 per Mcf Annual Price of US LNG Imports

from Nigeria Old Gas Price to Power

0

2

4

6

8

10

12

14

16

18

2000 2002 2004 2006 2008 2010 2012

US

$ p

er

Mcf

Gas Suppliers(International Oil Companies

& Independents)

Domestic Supply Obligation

(DSO)

Central Gas Processing Facility

(CGPF)

Gas for Own Export

Projects

Integrated LNG Plant

With Own CGPF

Domestic Buyers

Methanol

Plants

Fertiliser

Plants

Power

Plants

Regional

Pipelines

Pure Liquefaction

LNG Plants

Other Exports

Gas Transmission Line

Bilateral

Contracts

Excess Gas

Over DSO

Wet Gas

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 103

Gas Aggregation Company

The Gas Aggregation Company Nigeria Limited (GACN) is the aggregator

of natural gas produced for domestic use in Nigeria. It acts as an

intermediary between suppliers and buyers of natural gas in the Nigerian

domestic gas market and ensures that the Strategic Sectors are supplied

with gas under the appropriate pricing schedule. Its responsibilities also

include managing receipts of payments and disbursement of an aggregate

gas price to suppliers and facilitating the execution of necessary securities

in respect of default of gas payments.

The only three entities permitted to buy gas through the GACN are:

GenCos whose sole business is to generate power to the national grid;

companies that use gas as feedstock for their end products; and local

distribution companies which sell gas to commercial and manufacturing

companies in the domestic market. A Gas Supply and Aggregation

Agreement (GSAA) between the buyer, seller and the GACN governs terms

of gas supply and purchase.

While the GACN is not itself a regulator, it interfaces with the Department of

Petroleum Resources (DPR)32

on the due diligence process it conducts on

buyers, demand rationing criteria and DSO management. The gas market

lacks a clear regulatory hierarchy as various organisations such as the

GACN, NGC, DPR and PPPRA33

all act as pseudo regulators to a greater

or lesser degree. It is hoped that the long-awaited Petroleum Industry Bill,

should it be eventually passed by the Legislature, will clarify the situation.

Figure 31: Operations of the Gas Aggregation Company of Nigeria

Source: CSL Research, GAGN

GBI: Gas-Based Industries LDC: Local Distribution Companies. Domestic sellers of gas to commercial and manufacturing companies.

32

Part of the Ministry of Petroleum Resources. 33

Petroleum Products Pricing Regulatory Agency

GACN

Power Sector Price

GBI Sector Price

LDC Sector Price Supplier 3

Supplier 2

Supplier 1

Ag

gre

ga

te P

ric

e

Cash Flows

Gas Flows

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 104

Gas Flaring – Financial Waste & Environmental Scourge

In the current operating environment natural gas in Nigeria is essentially a

by-product of extracting crude oil. In 2011, having flared or vented 620 BCF

of natural gas, Nigeria was second only to Russia, a country that produces

over 10 times as much gas as Nigeria. There was slight improvement in

2012 when Nigeria claimed the no.3 spot, having flared 587 BCF of natural

gas. This amounted to 23% of gas extracted in 2012.

It is estimated that flaring gas costs Nigeria between US$2.5-3.0 billion a

year in lost direct revenues. Thus by reducing flaring to a minimum, the

Nigerian gas industry can be self-funding vis-à-vis the investment in

infrastructure that is required to bring the infrastructure up-to-scratch34

.

Chart 23: World’s Top Gas Flaring Countries, 2012* Chart 24: Nigeria Gas Production vs Flared, 2012

Source: US EIA, CSL Research

* Mexico, Kazakhstan, Brazil & Germany = 2011

Source: NNPC, CSL Research

Financial Loss

The real cost of gas flaring to the economy is greater if we include loss of

opportunity and production losses from the lack of gas supply to power

plants. We have used another proxy to indicate the extent of

financial/opportunity ‘waste’ resulting from flaring gas. We look at the ratio

of carbon dioxide (CO2) emissions from flaring alone to carbon dioxide

emissions from both consumption (a productive activity) and flaring. If we

compare Russia and Nigeria, both are responsible for about 14% of world

CO2 emissions from flaring gas. However, CO2 emissions from flaring

represent just 3% of Russia’s total CO2 emissions from both consumption

and flaring of natural gas. Russia at 3% compares to Nigeria at 75% (Chart

25).

34

Estimated at US$1.5-2 billion over the next five years.

646620

587

423401

256

213

157139 128 123

8865 62 55

Ru

ssia

Ira

n

Nig

eri

a

Ira

q

Ve

ne

zu

ela

An

go

la

US

Ind

on

esia

Lib

ya

Me

xic

o

Alg

eri

a

Ka

za

kh

sta

n

Ca

na

da

Bra

zil

Co

ng

o (B

rz)

Billio

n C

ubic

Fe

et (

Bcf)

42.3%

36.1%

32.6%

26.3% 27.7%

24.3%25.8%

22.7%

0%

15%

30%

45%

0

500

1,000

1,500

2,000

2,500

3,000

2005 2006 2007 2008 2009 2010 2011 2012

Billio

n C

ubic

Fe

et (

Bcf)

Gross Production Flared/Vented % Flared/Vented

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 105

Chart 25: Degree of Opportunity Loss from Flaring – ‘Productive’ CO2 Emissions (from Consumption) vs ‘Wasteful’ CO2 Emissions (from Flaring)

Source: US EIA, CSL Research

2011 Figures

3%

75%

9%

22%

91% 90%

1%

11%

5%10% 12%

6%2%

56%

90%

0%

20%

40%

60%

80%

100%

0

5

10

15

20

25

30

35

Russia

Nig

eria

Iran

Venezu

ela

Iraq

Ang

ola

US

Ind

onesia

Mexic

o

Alg

eria

Qata

r

Bra

zil

Canad

a

Co

ng

o (B

rz)

Cam

ero

on

Mill

ion M

etr

ic T

onnes

CO2 f rom f laring % CO2 f rom f laring vs. Total CO2 f rom consumption and f laringCO2 from Flaring CO2 from Flaring vs. Total CO2 from Consumption & Flaring

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 106

Environmental Cost

The financial cost to a country of flaring is one thing but the overall cost to

the country is far higher. A more holistic approach would include the

environmental cost by way of air pollution, carbon emissions etc. Without

any suitable carbon-capture technologies in place, Nigeria also ranks high

in carbon dioxide emissions from flaring (Table 20).

Table 20: Carbon Dioxide Emissions from Gas Flaring, 2011 (MMT)

World Rank

CO2 Emissions from Flaring

1 Russia 31.2

2 Nigeria 31.1

3 Iran 30.6

4 Venezuela 17.3

5 Iraq 17.0

6 Angola 12.7

7 United States 11.7

8 Indonesia 9.6

9 Mexico 8.1

10 Algeria 7.1

11 Qatar 5.4

12 Brazil 3.2

13 Canada 3.0

14 Congo (Brazzaville) 2.7

15 Cameroon 2.7

WORLD 224.9

AFRICA 64.0

Source: US EIA

MMT – Million Metric Tonnes

Pragmatism on Green Electricity and the Environment

Having consideration of the environmental impact of any industrial activity

has become as critical as the evaluation of the economics. So much so that

major finance institutions such as the World Bank, the IMF and the African

Development Bank will not support a project without an environmental

impact assessment report. Nigeria, in looking to make more constructive

use of its gas reserves and reduce flaring, improves its environmental

awareness credentials significantly.

We acknowledge that thermal power generation is far from being carbon-

neutral, however it causes less environmental damage than flaring gas.

The thermal generating plants in situ and those planned are open-cycle gas

turbine (OCGT) plants rather than combined-cycle gas turbine (CCGT)

plants largely due to the fact that CCGTs have higher construction costs35

.

However it is anticipated that over time many will be converted to CCGT

plants as these are more energy efficient and have less impact on the

35

See Appendix 5: OCGT and CCGT Power Plants, page 189.

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 107

environment. The advantage of having efficient electrical power supply to

households is easy to appreciate as it would alleviate the need to burn

biomass for light and heat. There are also benefits to industry by making it

more energy-efficient.

It is still early days and there are more ground-level activities to address

regarding power generation. Notwithstanding we consider it commendable

that the FGN’s plans have integral yet pragmatic considerations for

reducing the carbon footprint of the power industry. Renewable energy

such as solar power, wind and small hydro have dedicated resources at the

federal level to support and encourage the expansion of this sub-sector

under the aegis of the Federal Ministry of the Environment. We believe that

the incorporation into MYTO II of a specific tariff schedule for electricity

generation from renewables is a firm indication of the FGN/NERC’s long-

term commitment to green electricity.

Figure 32: Gas Processing and Transport in Nigeria

Source: CSL Research

LPG – Liquefied Petroleum GasNGL – Natural Gas Liquids

Central Gas

Processing Facility

Gas processed and treated to remove

impurities

Gas

Compressor

Station

Gas

Compressor

Station

Gas, other hydrocarbons and impurities

extracted

LPG

&

NGL

Wet Gas

Ships

Trucks

Power Plants

Domestic

Buyers

LPG Storage

Gas Transmission Line

Dry Gas

Lean

Gas

Gas

Wells

Wet Gas

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 108

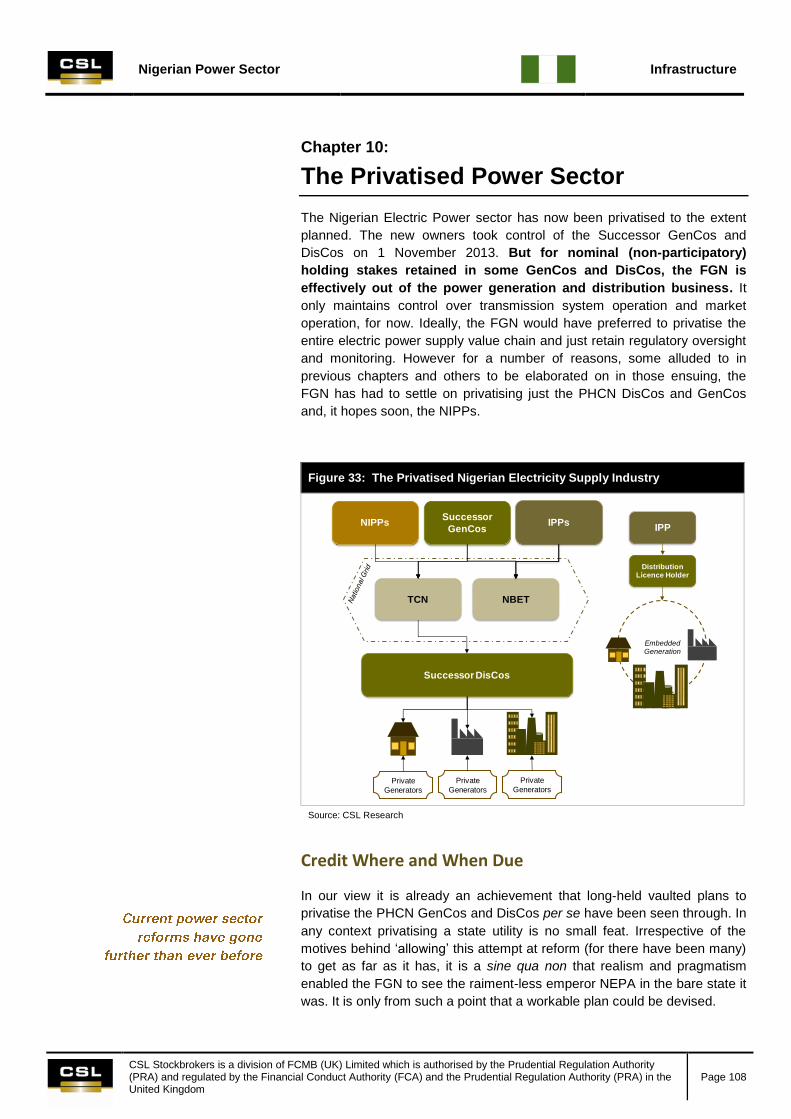

Chapter 10:

The Privatised Power Sector

The Nigerian Electric Power sector has now been privatised to the extent

planned. The new owners took control of the Successor GenCos and

DisCos on 1 November 2013. But for nominal (non-participatory)

holding stakes retained in some GenCos and DisCos, the FGN is

effectively out of the power generation and distribution business. It

only maintains control over transmission system operation and market

operation, for now. Ideally, the FGN would have preferred to privatise the

entire electric power supply value chain and just retain regulatory oversight

and monitoring. However for a number of reasons, some alluded to in

previous chapters and others to be elaborated on in those ensuing, the

FGN has had to settle on privatising just the PHCN DisCos and GenCos

and, it hopes soon, the NIPPs.

Figure 33: The Privatised Nigerian Electricity Supply Industry

Source: CSL Research

Credit Where and When Due

In our view it is already an achievement that long-held vaulted plans to

privatise the PHCN GenCos and DisCos per se have been seen through. In

any context privatising a state utility is no small feat. Irrespective of the

motives behind ‘allowing’ this attempt at reform (for there have been many)

to get as far as it has, it is a sine qua non that realism and pragmatism

enabled the FGN to see the raiment-less emperor NEPA in the bare state it

was. It is only from such a point that a workable plan could be devised.

NIPPsSuccessor

GenCos IPPs

Successor DisCos

TCN NBET

Private

Generators

Private

GeneratorsPrivate

Generators

EmbeddedGeneration

IPP

Distribution Licence Holder

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 109

Leadership and Intellectual Capital Responsibility

Unlike the case of mobile telephony, it was impractical to start the entire

electricity system of the country from scratch. Transforming a moribund

industry into one with the culture, systems and technology fit for the twenty-

first century was going to require unwavering commitment and intellectual

brawn. Any hope of success in privatising the electricity sector was/is

dependent on getting the right professionals in to oversee the process and

to lead the new institutions. In our estimation, and gauging by the opinions

of numerous industry stakeholders we have canvassed, the FGN has done

well in this regard.

The intellectual and professional capital of key institutions like the regulator

NERC, NBET and TCN has been bolstered by recruiting skilled leaders

from within the domestic power industry and also from outside the domestic

market. However we have reservations about the amount of political

interference that could come from the country’s Executive and Legislative

arms going forward. Our concerns particularly relate to NERC and TCN.

The degree to which these two institutions are left to carry out their

statutory roles independently and for the benefit of all the

stakeholders in the electricity market and they actually do so, is the

degree to which the privatised industry will endure, will be efficient

and will be profitable.

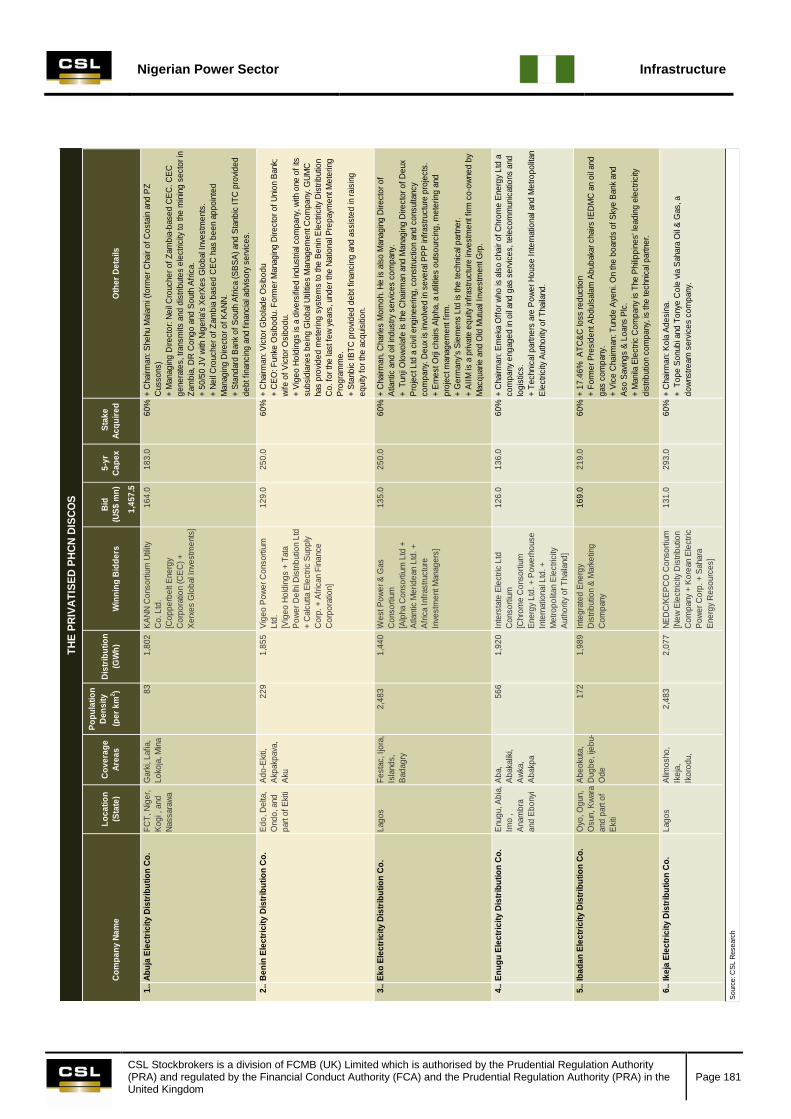

The Privatisation Process – What, When & How?

The FGN sold 60% stakes in 11 successor DisCos to the private sector

raising US$1.46 billion. It also sold between 51-100% stakes in 5 successor

thermal GenCos and awarded 15-year concessions for 2 successor

hydroelectric power plants, raising US$1.65 billion.

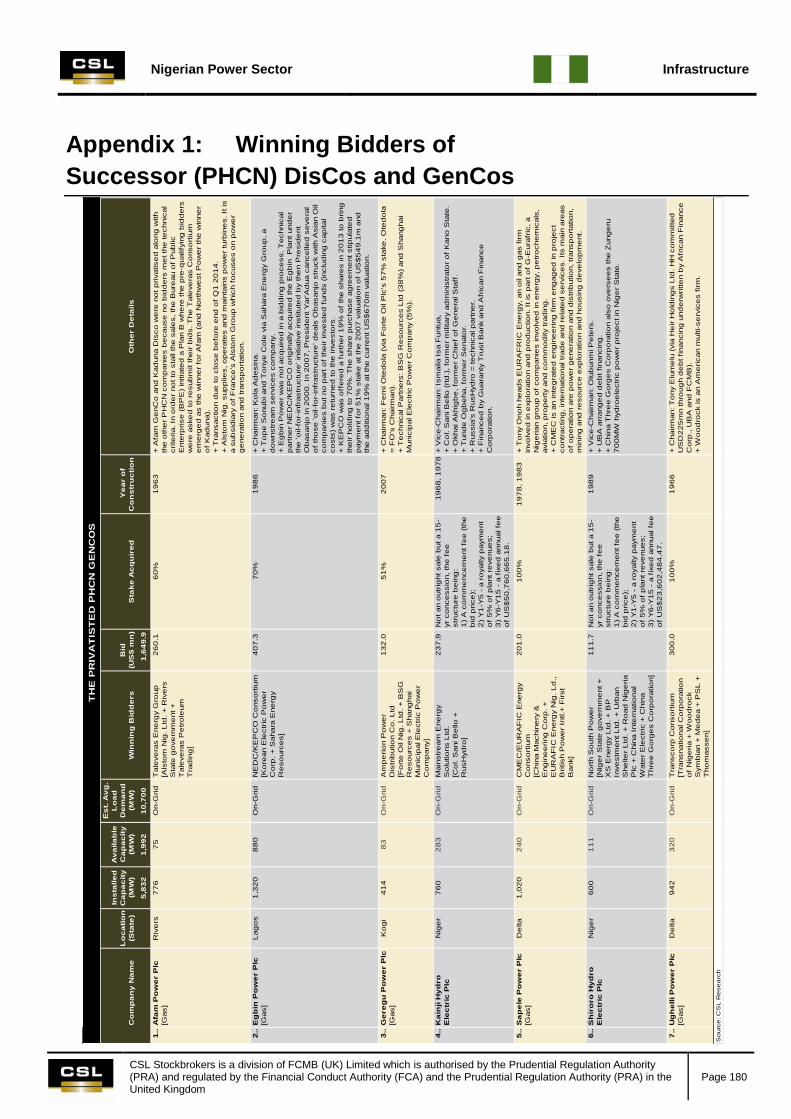

Purchasers of Successor GenCos and DisCos

Table 21 and Table 22 below give the names of the winning bidders for the

successor GenCos and DisCos respectively. We expand these tables with

the salient details of the privatisation in Table 21 and in Table 22 at the end

of this chapter. In the tables we include the parties within the winning

consortia and have sought to identify, as far as possible, key individual(s)

connected with each of the winners.

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 110

Table 21: Purchasers of Successor DisCos

Successor DisCo Purchaser Bid

(US$ mn) Stake

Acquired Distribution

(GWh)

Abuja Electricity DisCo KANN Consortium Utility Co. Ltd. 164.0 60% 1,802

Benin Electricity DisCo Vigeo Power Consortium 129.0 60% 1,855

Eko Electricity DisCo West Power & Gas Consortium 135.0 60% 1,440

Enugu Electricity DisCo Interstate Electric Consortium 126.0 60% 1,920

Ibadan Electricity DisCo Integrated Energy Distribution & Marketing 169.0 60% 1,989

Ikeja Electricity DisCo NEDC/KEPCO Consortium 131.0 60% 2,077

Jos Electricity DisCo Aura Energy Ltd 82.0 60% 714

Kaduna Electricity DisCo Northwest Power Ltd. 201.0 60% 1,233

Kano Electricity DisCo Sahelian Power SPV Consortium 137.0 60% 788

Port Harcourt Electricity DisCo 4Power Consortium 124.2 60% 1,164

Yola Electricity DisCo Integrated Energy Distribution & Marketing 59.3 60% 265

Source: BPE

Table 22: Purchasers of Successor GenCos

Successor GenCo Purchaser Bid

(US$ mn) Stake

Acquired Installed

Capacity (MW)

Afam Power Taleveras Energy Group 260.1 60% 776

Egbin Power NEDC/KEPCO Consortium 407.3 70% 1,320

Geregu Power Amperion Power Distribution Co. Ltd 132.0 51% 414

Kainji Hydro Electric Mainstream Energy Solutions Ltd. 237.9

A 15-yr concession, the fee structure being: 1) A commencement fee

(the bid price); 2) Yr1-Yr5 – a royalty

payment of 5% of plant annual revenues;

3) Yr6-Yr15 – a fixed annual fee US$50.8mn. 760

Sapele Power CMEC/EURAFIC Energy Consortium 201.0 100% 1,020

Shiroro Hydro Electric North South Power Consortium 111.7

A 15-yr concession, the fee structure being:

1) A commencement fee (the bid price);

2) Yr1-Yr5 – a royalty payment of 5% of plant annual revenues;

3) Yr6-Yr15 - a fixed annual fee US$23.6mn. 600

Ugheli Power Transcorp Consortium 300.0 100% 942

Source: BPE

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 111

Industry Agreements

In February 2013 the preferred bidders and the BPE signed Shareholders

Agreements and Share Sale Agreements. They also executed Industry

Agreements which serve as the framework for the fully-commercialised

power sector. The following have emerged as some of the key documents

which will need to be in place and bankable for power sector financings:

Share Sale Agreements (DisCos and thermal GenCos)

Concession Agreements (Hydro GenCos)

Gas Supply and Aggregation Agreements

Gas Transportation Agreements

Power Purchase Agreements (GenCos; 15 year duration): capacity

and energy payments are broken into Naira and US Dollar

components. The foreign components are payable in naira at the

prevailing exchange rate.

Vesting Contracts (DisCos; 15 year duration)

Transmission Use of Network System Agreements

Grid Connection Agreements

Ancillary Services Agreements

Bulk Trader Credit Support

Deed of Assignment of Pre-Completion Receivables

Operations and Maintenance Agreement

Pre-Completion Liabilities Transfer Agreement

Future Performance Evaluation and Monitoring

The Nigerian Electricity Supply Industry (NESI) is now fully regulated.

NERC is charged with overall regulation and issuing of licences for

participants in the sector. The BPE is the FGN’s signatory to the

agreements with the new owners of GenCos and DisCos. The documents

that govern the monitoring and regulatory frame work are in Table 23.

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 112

Table 23: NESI Monitoring and Performance Evaluation Documents

Governing Document Scope

Share Sale and Purchase Agreement (SSPA)

Terms and conditions of sale of shares to investors

Performance Agreements (PA) Contains terms of payment and Post-Acquisition Plans (PAP) implementation

BPE's Post Privatisation Monitoring Template

NERC's Reporting compliance Regulation

Outlines the level of compliance and standards expected of utilities

NERC's Terms and Conditions of Licensing

Sets out mandatory requirements for acquiring a licence and penalties for breach of terms.

Source: BPE

Post-privatisation monitoring by the BPE was expected to start in May

2014. But as TEM has not yet been declared, it is not likely that the full

scope of performance monitoring under the regulatory powers given to the

BPE and NERC will be in effect.

The Performance Agreement (PA) is the main document empowering the

BPE in its monitoring function. Compliance monitoring gives the BPE the

right to enter and monitor the privatised companies every six months upon

giving five days notice of such action. It also gives it the right to audit or

review the businesses every six months.

Performance Obligations Under the PA

General

The intent of these general provisions in the PA is to ensure that the

investor is held to the spending plans. The BPE retains these rights to

ensure that the development of the NESI remains on target. From a public

policy perspective, we consider this to be a shrewd arrangement by the

BPE/NERC given the FGN will no longer have direct control of the GenCos

or DisCos and will not be contributing any capital pro rata to its retained

stakes36

. Some general provisions of note include:

The investor must ensure the purchased DisCo or GenCo achieves the

Minimum Performance Targets;

The investor is liable to pay liquidated damages for performance falling

below the stipulated standard;

36

Thus in the case of any further capital raising by the GenCo or DisCo in which the FGN has retained a stake, the FGN’s holding with be diluted.

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 113

The investor must comply with the initial budget and Post-Acquisition

Plans (PAP) set out in the Performance Agreement, to which they

agreed to enter when they signed the SSPA.

For the first 5 years, annual revisions to budgets and plans require the

consent of the BPE and thereafter the BPE reserves the power of veto

over certain expenditures;

The investor is not allowed to take on senior debt without the prior

consent of the BPE, which shall not delay or unreasonably withhold

consent. This provision is included to safe-guard against the Successor

Companies being laden down with debt;

The Debt to Equity ratio of the successor company cannot exceed

70:30 for the first 5-years. Thereafter it may only rise to 75:25;

Insurance cover must be maintained on the companies at all times;

Performance obligations are to be secured by Parent Company

Guarantee. In the case of a consortium, the parent company of the lead

investor is to provide the guarantee, subject to BPE approval in relation

to the technical and financial standing of the parent company.

Successor GenCos-Specific:

Successor GenCos’ capacities are expected to be increased from current

low available capacity levels to meet minimum target generation capacities

set out in the Industry Agreements.

Successor DisCos-Specific:

The performance of the business operations of the new owners of the

successor DisCos will be measured on the basis of their abilities to reduce

distribution losses to loss targets specified in their business plans. They will

also have targets for expanding their distribution networks and in

connecting new customers.

ATC&C Losses

The Successor GenCos were sold to the highest bidder for the specific

GenCos. Bidders for the Successor DisCos, on the other hand, were given

the figure the FGN was going to sell the DisCo for and the evaluation of

bids was on the basis of the projected reduction in Aggregate Technical,

Commercial and Collection Loss (ATC&C Loss) over the first five years of

acquisition. The DisCo was sold to the bidder with the highest reduction in

ATC&C Loss.

The ATC&C loss figure is a key performance indicator for power distribution

companies. It enables operators to monitor efficiency and profitability in

delivery of power to customers. ATC&C Loss is the difference between the

amount (in MWh) of electricity received by the DisCo and the amounts

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 114

billed and received from customers (in ₦). The difference in electricity

received by the DisCo and electricity it bills the customer gives the

technical and commercial loss, while the difference in the amount billed and

the amount received/collected from the customer gives the collections loss.

Thus reduction in these losses improves profitability.

Each bid contained a 5-year ATC&C Loss reduction schedule based on a

starting loss figure provided by PHCN. The winning bidder had the lowest

end loss level for that particular successor DisCo. The purchasers ATC&C

Loss figure is very important because the purchaser’s end level figure is

then incorporated into the MYTO model, as each DisCo has its own MYTO-

determined tariff plan. If the purchaser does not achieve the loss target, it

will be less profitable than it has planned, and vice-versa should the target

be exceeded (i.e. the end ATC&C Loss figure achieved turns out lower than

targeted). If the purchaser consistently fails to meet its loss-reduction

targets, NERC may decide to revise the purchaser’s capex allowance

amount under its DisCo tariff.

The ATC&C Loss targets of the winning bidders are shown in Table 24.

Table 24: Distribution (ATC&C) Losses and Loss Reductions

Successor DisCo

Winning Bidder

Opening Loss

Bidder's Yr 5 Loss

Bidder's Yr 5 ATC&C Loss

Relative to Opening Loss

Abuja DisCo

KANN

35.00%

12.78%

-36.51%

Benin DisCo

Vigeo Power

40.00%

12.19%

-30.48%

Eko DisCo

West Power & Gas

35.00%

12.76%

-36.46%

Enugu DisCo

Interstate Electric

35.00%

6.70%

-19.14%

Ibadan DisCo

Integrated Energy

35.00%

12.71%

-36.31%

Ikeja DisCo

NEDC/KEPCO

35.00%

9.99%

-28.54%

Jos DisCo

Aura Energy

40.00%

18.09%

-45.23%

Kaduna DisCo

Northwest Power

40.00%

11.70%

-29.26%

Kano DisCo

Sahelian Power

40.00%

13.02%

-32.55%

Port Harcourt DisCo

4Power

40.00%

14.90%

-37.25%

Yola DisCo

Integrated Energy

40.00%

17.34%

-43.35%

Source: BPE

India’s Tata Power Delhi Distribution Limited (TPDDL) is a joint venture between Tata Power and

the Government of the National Capital Territory of Delhi, with the majority stake being held by

Tata Power (51%). Tata Power acquired its stake following the unbundling of the Delhi Vidyut

Board (DVB) in 2002. As is the case for investors in Nigeria’s DisCos, Tata also had five-year

ATC&C Loss reduction targets. Its opening ATC&C Loss was 53% and its target was 31%. TPDDL’s

ATC&C Losses stood at 11% at the end of the 2012/13 financial year. This compares to a world

average of about 15%.

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 115

Table 25: Successor DisCo 5-Year Capex*

(US$ million)

2014-18 Capex

Abuja DisCo

180

Benin DisCo

119

Eko DisCo

134

Enugu DisCo

215

Ibadan DisCo

112

Ikeja DisCo

147

Jos DisCo

149

Kaduna DisCo

222

Kano DisCo

288

Port Harcourt DisCo

125

Yola DisCo

64

Total

1,755

Source: NERC

* MYTO II Model assumptions.

NGN:USD rate of ₦160

Table 26: CSL Estimated* Successor GenCo Capex

Installed Capacity

(MW)

2011 Available Capacity

(MW)

Estimated Capex

(US$ mn)

Afam Power 776 45 796

Egbin Power^ 1,320 880 430

Geregu Power 414 361 37

Kainji Hydro 760 359 653

Sapele Power 1,020 135 959

Shiroro Hydro 600 393 319

Ughelli Power 900 228 721

Total 5,790 2,401 3,915

Source: BPE, CSL estimates

* Please note boxed commentary within the main body of the report. ^ Not included in 2011 BPE presentation. Figures from market sources.

- NOTE - There have been varying reports over the last few months of the level of Available Capacity (AC) of these successor power plants and it continues to be difficult to get precise figures. Now that the GenCos are under private ownership, for the time being at least, we expect the precise figures to be considered privilege between the operators and NERC/BPE. This is especially so given the sensitivities surrounding the delay in the declaration of TEM and the operation of the Interim Rules Period.

Notwithstanding, we wanted to have a rough sense of how much capex could be required to get each GenCo's Available Capacity close to its Installed Capacity, as this is a key performance requirement of the new owners set out in the Performance Agreements signed with the BPE.

At the 2011 Bankers’ Conference Workshop for the PHCN privatisation, the BPE provided the AC of each PHCN GenCo. We have based our calculations on this figure and used the MYTO II model’s level for AC of 95% as our target. Given the 2011 AC date, we caveat our calculated figures because the reality on the handover date may have been higher or lower for any of the GenCos.

We have assumed that each MW added for the gas-fired plants costs US$1.15 million based on the industry

yardstick of US$1-1.3 million of capex per MW. We have used the MYTO II estimate of US$1.8m per MW for

the hydro plants.

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 116

Current Market Stage – Interim Rules Period

Figure 34: Key Characteristics of the Market Stages in the Evolution of the Nigerian Electricity Supply Industry

Source: CSL Research

Interim Rules

Period

(IRP)

Pre-TEM

Stage

Transitional

Electricity Market

(TEM)

Medium Term

Market

Long Term

Market

Unbundling of NEPA/PHCN;

Privatisation of PHCN GenCos and

DisCos;

Review and

subsequent application of the

Market Rules and procedures;

Establishment of performance incentives and

performance standards for the

distribution and generation companies;

Payments and

settlements based on Shadow Trading and Transfer Pricing;

NBET, TCN and

PRGs not yet operational;

TEM was expected to start at the end of January 2014. However a number of factors

made NERC deem it necessary to delay the start of TEM and

introduce a set of Interim Rules.

Notable points on the IRP:

i. As contracts of the

privatisation such as PPAs and VCs only become fully enforceable once TEM is

declared, Successor GenCos and DisCos are expected to

continue with their Pre-TEM trading arrangements during the IRP.

ii.GenCos bill the Market Operator (MO) for electricity

generated and available capacity based on MYTO II

tariffs. However as Pre-TEM contracts apply, Transfer Pricing and Estimated Billing

is in operation.

iii.The MO continues to bill the DisCos for electricity.

iv.The MO determines the allowable amount of funding

(the Minimum Funding Requirement) for the Successor DisCos, Successor

GenCos and for the Service Providers including NERC, the

Transmission Service Provider (TSP) and the System Operator (SO).

NBET and TCN roles within NESI become effective/operational;

Contracts of privatisation

signed between Successor Companies and State institutions including Power

Purchase Agreements (PPAs), Vesting Contracts (VCs) and

Partial Risk Guarantees (PRGs) become effective;

Payments and settlements based on prices and terms

contained in PPAs and in VCs.

No centrally-administered

balancing mechanism for the market;

Development of procedures for the management of inadequate

supply and shortage in the system;

Open access to the transmission network to

GenCos and DisCos.

Wholesale Electricity Market will be the balancing market for trading electricity in the

industry. It will be characterisedby a spot market where

electricity prices are set daily.

DisCos and GenCos will be

permitted to enter bilateral contracts for the purchase

and/or sale of electricity.

Open entry to the transmission

network to GenCos, DisCos and large power consumers. All

subject to technical and environmental obligations, and overseen and licensed by the

regulator NERC.

Retail competition - all consumers choose their suppliers;

Clear differentiation between

distribution (delivery) and retail activities;

Open access to the transmission and distribution

networks.

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 117

Table 27: Pre-TEM and TEM Characteristics Compared

PRE-TEM TEM

Transmission, Distribution and System Operations retain their monopoly and regulated status during Pre-TEM and TEM.

Market Structure

Sellers:- Sellers:-

- Successor GenCos - Successor GenCos

- IPPs with PPAs - IPPs with PPAs

Buyers:- Buyers:-

- Successor DisCos - Successor DisCos (also licensed as marketers)

- International connections - International connections/customers

- Local large power consumers - Local large power consumers

Service Providers:- Service Providers

- TSP - TSP

- ONEM Market Operator - NBET

- System Operator - TCN System Operator

- Central (Headquarter) Services - TCN Market Operator

Pricing Regime

Transfer Pricing Vesting Contract and PPA Prices

Successor GenCos and IPPs sell to Successor DisCos

- Successor GenCos sell at Transfer Prices calculated every 3 months

- IPPs sell at their PPA prices

Buyers:-

- Successor DisCos buy at Transfer Prices

- International connections buy at prices in their Connection Agreements.

- Local large power consumers buy at regulated end-user tariffs

Service Provision

TSP TSP

- Provides transmission access to both GenCos and DisCos - Provides transmission access to both GenCos and DisCos

- Recognises and accounts for transmission losses - Recognises and accounts for transmission losses

ONEM Market Operator NBET

- Commercial administration of the market including settlements and payments using Market Rules

- Commercial administration of the market including settlements and payments using Market Rules

System Operator TCN System Operator

- Technical administration of the market using the Grid Code and provision of other services for grid stability.

- Technical administration of the market using the Grid Code and provision of other services for grid stability.

Central (Headquarter) Services - Pricing of transmission access

- Provides common services such as funding of special projects, emergency funding

Payment &

Settlement System

Market does not always balance Market in equilibrium - a debit by a DisCo has a

corresponding credit to a GenCo therefore NBET maintains a zero balance.

Shadow Trading Wholesale Electricity Market Trading

- MO receives payments into its market clearing account from DisCos and eligible customers

- NBET receives and transfers payments between GenCos and Successor DisCos

- Existing IPPs sell through PPAs with NBET

- MO transfers payments to GenCos and service providers - New IPPs may contract to sell either to NBET or with the DisCos directly

Settlement Settlement

- Per individual settlement calendar - Market settlement each month (M) for each DisCo

- DisCos sell at uniform prices and use estimated billing - Monthly payment (M+1 month)

- IPPs sell at PPA prices; Successor GenCos at various Transfer Prices .

Payment Payment

- Payment made into escrowed settlement accounts

- DisCos submit a Letter of Credit covering three months of payments to be drawn down (plus interest) in the event of non-payment by the DisCo.

- Based on Minimum Funding Requirement determined by the MO - Incomes in line with MYTO II Revenue Requirement provisions

- The Transfer Price is expected to cover the budget for operating costs only.

- Per MYTO II, capital costs and return on investments can also be recovered.

Source: CSL Research

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 118

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 119

PART III – The Investment Case

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 120

Chapter 11:

Pitfalls and Opportunities

It is an indisputable fact that the supply/demand gap for power in a

country with a population of almost 170 million generating less than

4GW presents a prima facie investment opportunity. How the theory

(of the new regime) works in practice is the crux of the investment

case for the Nigerian power sector.

As with any such sector-wide endeavour, stakeholders (investors,

customers etc) and other commentators need to make allowances for the

journey not going entirely smoothly. This is not a Nigerian phenomenon

but is to be expected in the implementation of corporate or industry-wide

strategy the world over. The concern and hope is that these bumps

amount to minor, surmountable hiccoughs.

We ultimately want to identify where the equity is in the new sector and

assess how much funding is available to make the required investments.

This involves an initial evaluation of the main risks in the Nigerian

Electricity Supply Industry. We have grouped the risks methodologies

adopted and operating procedures in the NESI Financial and Systemic

Risks. The latter not least highlighted by and revealed in the Interim

Market and the delay in the declaration of the Transitional Electricity

Market (TEM). We then analyse the Structural Risks of the industry.

NERC

END-USERS

GAS

SUPPLIERSGENCOS

FGN

FINANCE

MARKETSTCN /

NBET

DISCOS

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 121

Chapter 12:

Financial Risks

We will address two core financial risks in this chapter:

1. The skewness of risk allocation amongst counterparties;

2. Critical problems with MYTO II, which in practice results in a

tariff structure that is not commercially sustainable as it

currently stands.

Network Risk Allocation Skewed Against Discos

NERC insists that the pricing structure is set so that it spreads the risks

equitably among the users of the transmission network. It is intended to

assign the costs or charges to “the user or group of users incurring those

costs”37

. At the same it states that the rationale on risk allocation is that

the “pricing arrangements should allocate risks efficiently [which implies]

generally to those who are best placed to manage them.”38

These two phrases may strike one as incompatible because they both

claim to be the premise on which the transmission tariffs are set and load

allocated, yet on interpretation they could lead to different results. One

purports to allocate costs to the user(s) incurring the cost and yet for the

second to also hold true, it implies that costs are incurred by those best

placed to manage them. This is not necessarily the case.

If we then look at how this has worked in practice, in MYTO II the bulk of

the cost of the transmission network (build, management and

maintenance) is charged to the DisCos – 80% of the TUOS charge is

borne by the DisCos. It is not immediately apparent why:

(a) 80% of the cost of getting the energy from the generator to the

distributor/retailer should be incurred by the DisCo and/or

(b) the DisCo is considered to be better placed and more efficient than

the GenCo to manage transmission costs.

All these costs are ultimately passed onto the end-user, so it could be

said that neither GenCo nor DisCo are disadvantaged. However from a

cash management and capital structure perspective, to say the least, it

does matter. It has implication for the risk exposure of the businesses

hence their cost of capital and returns profiles.

37

NERC Multi Year Tariff Order for the Determination of the Cost of Electricity Transmission and the Payment of Institutional Charges for the Period 1 June 2012 to 31 May 2017 (herein after ‘MYTO II – Transmission’); p.19. 38

MYTO II – Transmission, p. 17.

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 122

According to NERC, if GenCos were to be exposed to connection

charges, they would be more likely to choose locations that minimise

these charges. NERC contends that this could be detrimental to the even

distribution of access to electricity across the country.

GenCos Not Let Off in Entirety

NERC asserts that GenCos have an incentive to reduce the losses

associated with transmitting their generated energy. GenCos have limited

ability to effect improvements in transmission losses (and by equivalence

Marginal Loss Factors, MLFs). We believe the incentive to improve this is

limited since they do not bear the cost of system transmission loss. They

can minimise the losses associated with transmission up to their network

node connection point, however it is on a de minimis scale when

considering the vast bulk of transmission occurs after title/responsibility

passes from them at their node connection.

DisCos essentially pay for transmission losses however they too have no

means of reducing these losses. They are not in control of the spending

to improve and extend the transmission network even though they

provide the financing (through the TUOS charge).

Under the terms of the PRG, NBET/TCN bears the risk of Availability

Events. It essentially guarantees transmission. We understand the full

implication of this, in light of the realities of the market post handover,

might be weighing heavy on the FGN. Current negotiations,

renegotiations and discussions during the Interim Rules Period may well

be seized upon to adjust the blanket guarantee. However we believe this

would send a very negative signal to the market as it smarts of an

inclination of the FGN shifting the goal posts after the fact.

The MYTO II Powder Keg

We have analysed the methodology and assumptions used in the MYTO

II models for generation, transmission and distribution. In Chapter 5: we

talked about the theoretical soundness of the methodologies used and

pointed to similar examples in other electricity markets.

It goes without saying that the utility of a financial model is only as

good as the assumptions plugged into it. We have found the MYTO

II model does not stand up to scrutiny in this regard. The

components of the gun powder we have identified which we discuss in

detail next are:

A. Generation Technical Assumptions

(i) Available Capacity Factor assumptions need to be more conservative

(ii) Construction period for Large Hydro is too ambitious

(iii) Plant Availability needs to be lowered

(iv) Fuel cost assumption is too low

B. Miscalculation of Wholesale Prices leaves GenCos short

C. Transmission Capex is insufficient for actual requirements

D. Distribution ATC&C Losses assumptions are too low

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 123

MYTO II Generation Technical Assumptions

The technical assumptions of GenCos are set out in ‘Table 1: Technical

Characteristics of New Entrant Plants – 2012’ of the MYTO document on

the determination of the generation tariff published by NERC on 1 June

2012. We have reproduced it below and discuss our findings:

Figure 35: MYTO II Generation – Technical Characteristics of New Entrants

Source: NERC, Multi-Year Tariff Order for the Determination of the Cost of Electricity Generation for the Period 1 June 2012 to 31 May 2017, ‘Table 1: Technical Characteristics of New Entrant Plants – 2012’, p.20.

The industry rule of thumb for construction costs of an OCGT plant is approximately US$ 1 million per megawatt (i.e.

US$1,000 per kilowatt). Hence this Unit should be per kW and not per kWh (kilowatt hour). Otherwise it would mean

NERC assumes that a 250 MW OCGT plant costs over US$ 2 trillion! (250 MW = 2.19 billion kWh)

As far as the calculations in the MYTO financial model is concerned, after analysing the calculations in the MYTO

financial model, we can confirm that the effect of this particular typographical error turns out to be merely cosmetic.

However, as we illustrate in Table 29 page 126 and Table 30 on page 127, other typographical errors led to a significant

miscalculation of the Revenue Requirement. This is notable because it is the (purported cost-reflective) Revenue

Requirement from which tariffs are set.

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 124

(i) Available Capacity Factor Assumptions Need To Be More

Conservative

We have compared MYTO II plant Available Capacity Factors (ACF) with

those from more established and efficient markets (see Table 28 below).

As a result, we believe those in MYTO II need to be more conservative.

ACF is sometimes referred to as ‘Available Capacity’ or ‘Capacity Factor’

(as in the MYTO II financial model; item #5 in the MYTO table shown in

Figure 35). There is an inverse relationship between the ACF and the end

tariff. So MYTO assumes that as the ACF of plants increases, the end-

user tariff should decrease. This is not a one-for-one proportional

relationship as there are several other technical variables that also affect

the end-tariff and/or also affect each other.

Table 28: Comparison of Capacity Factors (Available Capacity)

Natural Gas Hydro Coal Comments

US 43% 40% 64% ‘Best In Class’ gas thermal plants have ACFs over 90%.

The inference from the MYTO II Capacity Factor assumptions for the gas plants is that they are akin to base load plants running at or very near full capacity (i.e. nameplate capacity). While this might not be such a stretch in situations where demand far exceeds supply, it is not a reasonable or realistic assumption in a situation like Nigeria’s where lack of maintenance, equipment inefficiencies and gas and transmission infrastructure issues result in a lot of downtime.

The world average for Hydro is 44% but the spectrum is wide (10-99%) due the variations in plant design. A small hydro plant in a small river, or one with a sufficiently large dam reservoir will always have enough water so won’t suffer downtime from fuel supply issues.

UK 57% 34% 45%

MYTO II Successor GenCos

65% New Entrants

85% 65% 70%

Source: NERC, US EIA (2009), UK Dept. Of Energy & Climate (2007-2012 Averages)

The seemingly low ACFs for UK and US gas plants are due to the number and variation of participants selling electricity in their open-traded wholesale markets. Electricity is offered for sale from power generating installations that use various fuels – nuclear, gas, coal, wind, solar, etc. The running costs of these generators vary and at a particular time it might not be economical for a particular plant to produce electricity at its optimal (possible) ACF level. Typically, those with the lowest running costs can offer the best prices but the major determinants of price are ultimately supply and demand and any regulatory price controls that might exist.

Available Capacity Factor = Actual Plant Output (in MWh)

Theoretical Nameplate Output (MWh)

Hence the ACF of a 1,000 MW plant generating 648,000 MWh of

electricity in 30 days, for example:

= 648,000 MWh

1,000 MW × 24hrs ×30 days

= 0.9 = 90%

Available Capacity Factor is the

ratio of the actual output of a

power plant over a period of time

versus the theoretical power

output were it possible to run the

plant at nameplate/installed

capacity indefinitely. Equipment

availability characterises the

operating reliability of the plant.

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 125

(ii) Construction Period for Large Hydro Plants Is Too Ambitious

The construction period for Large Hydro plants is set at 4 years, just a

year longer than the construction period assumed for small hydro plants

under the feed-in tariff plan. The norm in most markets is a construction

period of 5-7 years.

(iii) Plant Availability Needs To Be Lowered

Plant Availability is the percentage of time the plant is available to

generate electricity over a period of time. It is affected by a plant’s

Available Capacity (AC)/Available Capacity Factor (ACF).

The MYTO II model sets Plant Availability at 95% of AC for both

successor and new entrant thermal plants. Most gas thermal plants have

high Plant Availability, about 80-99%. The new plants are more likely to

have such a high figure, but this is very unlikely for the Successor

GenCos. Furthermore the figure assumes that plants will not suffer fuel

supply or transmission issues that would effectively make them

unavailable even though technically they might be able to produce

electricity (at their ACF level), as is currently being faced by Successor

GenCos.

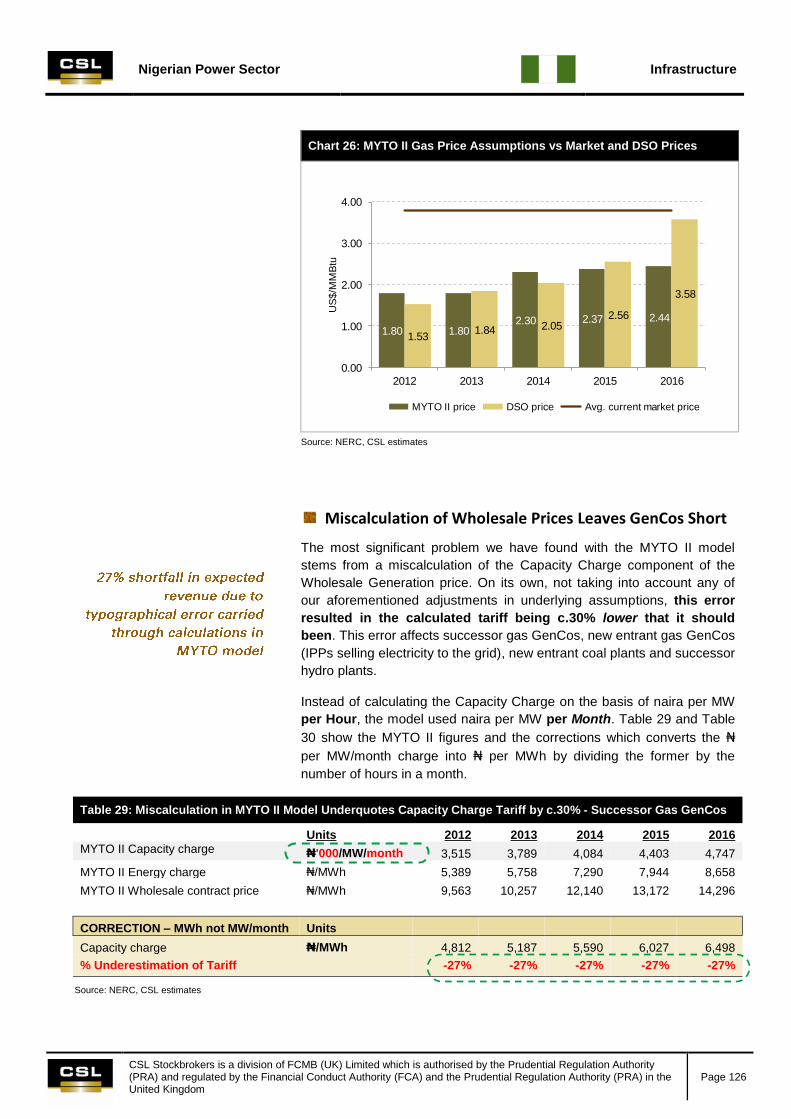

(iv) Fuel Cost Assumptions Are Too Low

The gas price is based on the regulated price for both the successor

GenCos and new entrant GenCos (Chart 26). In our view this is not a

plausible assumption for a number of reasons starting with the fact that

the current market price of gas is about US$3 per MMBtu39

:

The DSO price as incorporated in the successor GenCos’

privatisation GSA’s only applies to the Available Capacity at the

time of sale. There was a wide variation in ACs but the average

for the gas-fired plants was c.40%. Thus using MYTO II’s ACFs

of 65% the successor GenCos will need to buy gas for 35% of

their output at the market price.

The IPPs/new entrants do not benefit from the DSO price but buy

at the market price.

39

Million British Thermal Units.

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 126

Chart 26: MYTO II Gas Price Assumptions vs Market and DSO Prices

Source: NERC, CSL estimates

Miscalculation of Wholesale Prices Leaves GenCos Short

The most significant problem we have found with the MYTO II model

stems from a miscalculation of the Capacity Charge component of the

Wholesale Generation price. On its own, not taking into account any of

our aforementioned adjustments in underlying assumptions, this error

resulted in the calculated tariff being c.30% lower that it should

been. This error affects successor gas GenCos, new entrant gas GenCos

(IPPs selling electricity to the grid), new entrant coal plants and successor

hydro plants.

Instead of calculating the Capacity Charge on the basis of naira per MW

per Hour, the model used naira per MW per Month. Table 29 and Table

30 show the MYTO II figures and the corrections which converts the ₦

per MW/month charge into ₦ per MWh by dividing the former by the

number of hours in a month.

Table 29: Miscalculation in MYTO II Model Underquotes Capacity Charge Tariff by c.30% - Successor Gas GenCos

Units 2012 2013 2014 2015 2016

MYTO II Capacity charge ₦'000/MW/month 3,515 3,789 4,084 4,403 4,747

MYTO II Energy charge ₦/MWh 5,389 5,758 7,290 7,944 8,658

MYTO II Wholesale contract price ₦/MWh 9,563 10,257 12,140 13,172 14,296

CORRECTION – MWh not MW/month Units

Capacity charge ₦/MWh 4,812 5,187 5,590 6,027 6,498

% Underestimation of Tariff -27% -27% -27% -27% -27%

Source: NERC, CSL estimates

1.80 1.802.30 2.37 2.44

1.531.84 2.05

2.56

3.58

0.00

1.00

2.00

3.00

4.00

2012 2013 2014 2015 2016

US

$/M

MB

tu

MYTO II price DSO price Avg. current market price

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 127

Table 30: Miscalculation in MYTO II Model Underquotes Capacity Charge Tariff by c.30% - New Entrant Gas GenCos

Units 2012 2013 2014 2015 2016

MYTO II Capacity charge ₦'000/MW/month 4,359 4,701 5,071 5,470 5,902

MYTO II Energy charge ₦/MWh 5,568 5,951 7,499 8,169 8,902

MYTO II Wholesale contract price ₦/MWh 10,743 11,534 1,350 14,665 15,910

CORRECTION – MWh not MW/month Units

Capacity charge ₦/MWh 5,967 6,435 6,942 7,488 8,079

% Underestimation of Tariff

-27% -27% -27% -27% -27%

Source: NERC, CSL estimates

Allocation for Ancillary Services is Grossly Inadequate

The MYTO Model only allocates 1.5% of revenues of the system to

Ancillary Services. In an electrical system at the stage of development

that Nigeria’s is, at a bare minimum 10% of revenue needs to be put

towards Ancillary Services. Thus the under-provision understates the

Revenue Requirement of the sector.

Ancillary Services consist of system capacity allowances vital to the

stability of the entire electrical network. They include:

Spinning Reserves: This is back-up energy production capacity which

can be made available to the system operator (for transmission) within

ten minutes of a power system failure and can operate continuously for at

least two hours once brought online. It is done by increasing the power

generation output of power plants already connected to the system.

Voltage Support: This is used to maintain the voltages in the

transmission system within a secure, stable range. It is an essential

service for the security of equipment and people. Its proper management

ensures cost and operational efficiency of the transmission system.

Black Start Capability: It is the process of restoring a power plant to

operation without relying on power from the grid in the event of a major

system collapse or system wide blackout. In the event of a power

blackout, black start system capability is critical.

Transmission Capex Insufficient for Actual Requirements

Capital expenditure on transmission feeds into the TUOS charge

component of the tariff however MYTO II only assumes ₦56 billion

(US$350 million) per year for the capital which is less than a quarter of

The Roadmap’s (and the industry’s) estimate of US$1.5 billion per

year over the next five years.

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 128

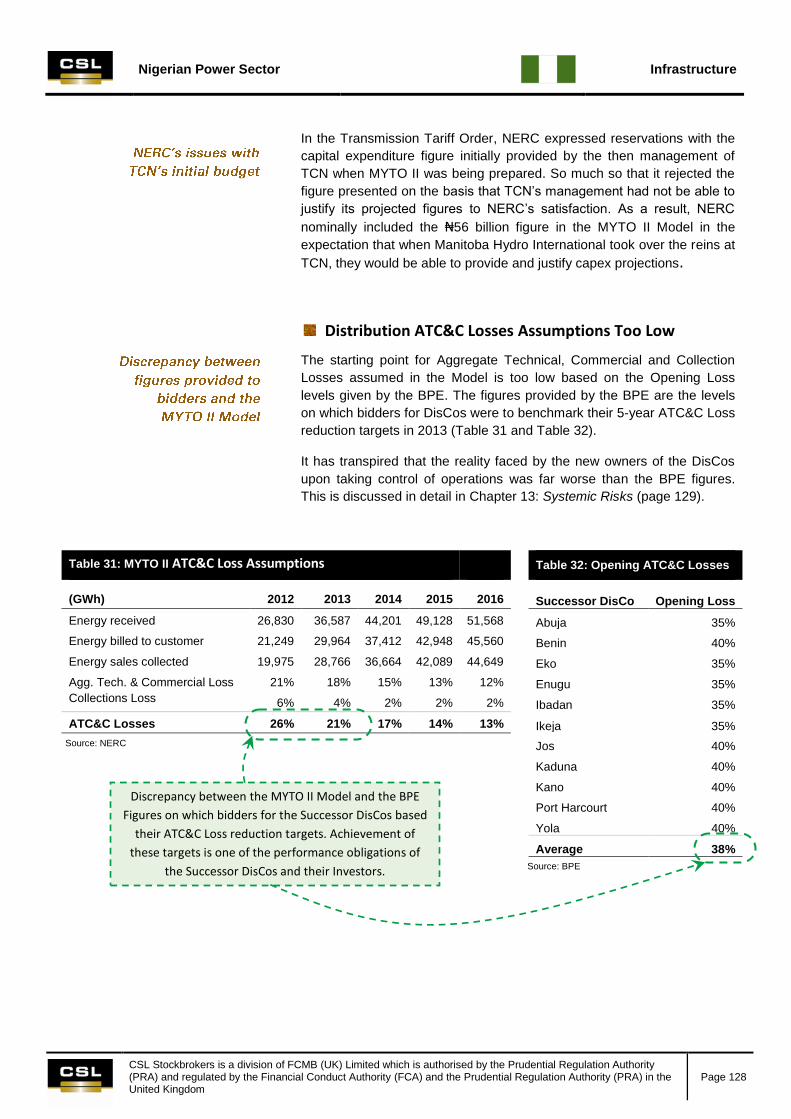

In the Transmission Tariff Order, NERC expressed reservations with the

capital expenditure figure initially provided by the then management of

TCN when MYTO II was being prepared. So much so that it rejected the

figure presented on the basis that TCN’s management had not be able to

justify its projected figures to NERC’s satisfaction. As a result, NERC

nominally included the ₦56 billion figure in the MYTO II Model in the

expectation that when Manitoba Hydro International took over the reins at

TCN, they would be able to provide and justify capex projections.

Distribution ATC&C Losses Assumptions Too Low

The starting point for Aggregate Technical, Commercial and Collection

Losses assumed in the Model is too low based on the Opening Loss

levels given by the BPE. The figures provided by the BPE are the levels

on which bidders for DisCos were to benchmark their 5-year ATC&C Loss

reduction targets in 2013 (Table 31 and Table 32).

It has transpired that the reality faced by the new owners of the DisCos

upon taking control of operations was far worse than the BPE figures.

This is discussed in detail in Chapter 13: Systemic Risks (page 129).

Table 31: MYTO II ATC&C Loss Assumptions Table 32: Opening ATC&C Losses

(GWh) 2012 2013 2014 2015 2016

Successor DisCo Opening Loss

Energy received 26,830 36,587 44,201 49,128 51,568

Abuja 35%

Energy billed to customer 21,249 29,964 37,412 42,948 45,560

Benin 40%

Energy sales collected 19,975 28,766 36,664 42,089 44,649

Eko 35%

Agg. Tech. & Commercial Loss 21% 18% 15% 13% 12%

Enugu 35%

Collections Loss 6% 4% 2% 2% 2%

Ibadan 35%

ATC&C Losses 26% 21% 17% 14% 13%

Ikeja 35%

Source: NERC

Jos 40%

Kaduna 40%

Kano 40%

Port Harcourt 40%

Yola 40%

Average 38%

Source: BPE

Discrepancy between the MYTO II Model and the BPE

Figures on which bidders for the Successor DisCos based

their ATC&C Loss reduction targets. Achievement of

these targets is one of the performance obligations of

the Successor DisCos and their Investors.

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 129

Chapter 13:

Systemic Risks

We have identified three main systemic risks relating to:

1. Load allocation between the DisCos by the System Operator;

2. Implications of the delay in declaring the Transactional

Electricity Market (TEM) and operation of the Interim Rules

Period (IRP);

3. Legacy issues of the monitoring and reporting standards of

the old system; notably the discovery that the state of the

newly-acquired assets was worse than investors expected,

based on information provided to bidders in the Data Room.

Load Allocation Mechanism

Load allocation of the first 3,200 MW among the 11 DisCos is based on a

number of factors including projected demand. The limited amount of

energy available has necessitated the System Operator (SO) having a

system to ration between the DisCos. The DisCos will be evaluated and

scored on achievement of minimum customer service performance

standards and NESI Key Performance Indicators (KPIs). The criteria used

and their respective weightings are depicted in Chart 27.

While some of the criteria have more objective parameters than others,

there is still a significant degree of subjectivity in the evaluation criteria.

This is an area of concern, in our view, due to the potential for political and

other vested interests to use this an opportunity to create a bias in favour of

one or other DisCo. The political in-fighting that already has been

demonstrated over the Manitoba Hydro International matter and the

machinations surrounding the composition of the TCN board does not bode

well in our view.

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 130

Chart 27: Weighting of Energy Allocation Evaluation Criteria

Source: NERC, CSL Research

IRP and Delay in Declaration of TEM

The winning bidders of the successor GenCos and DisCos were

announced in February 2013. These new owners were due to be handed

full control of the purchased assets on 1 November 2013 after which there

was to be a 4 month shadow-management period. In the months leading to

the handover, some stipulated conditions-precedent to declaration of TEM

(originally planned for October 1 2013) were still outstanding. So as not to

stall the handover of the Successor Companies to the new owners on

November 1, NERC developed a set of Interim Rules to govern the market

in the pre-TEM, post-handover market. The Interim Rule Order (IRO)

committed to a maximum duration of the IRP of 3 months. The IRO was

issued in December with retroactivity to November 1.

The 3-month deadline has come and gone and the market continues to

operate under Interim Rules with no firm indication on when it will end and

TEM will begin. The prolongation of the IRP creates several problems for

the new owners of the Successor Companies because:

1. The expected, unbundled market with NBET and TCN as the link

between GenCos and DisCos is yet to become effective. There is little

difference operationally between the previous vertically-integrated

PHCN market and the status quo. A no-man’s land post-handover is

not what investors and the market subscribed to;

2. The no-man’s land situation has been compounded by discoveries

made by the new owners relating to the state of the assets themselves

and concerns raised over the validity of certain agreements central to

the privatisation.

35%

30%

15%

15%

5% — Reduction of losses

— Attainment of metering targets

— Customer service ratings based onbiannual customer surveys

— Achievement of distribution networkexpansion targets

— Distribution Capacity

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 131

No-Man’s Land Suffocates Cash Flow Management

While the bidders of the Successor Companies were not permitted to use

the target company’s assets as surety to raise funds for the bid process,

they were permitted to secure contingent finance against the cash flows.

The anniversary for repaying these loans is in August 2014.

Operation of the Interim Rules

At the heart of the matter, the operation of the IRO itself can negatively

impact the sustainability of the NESI. Clause 3 of the IRO states that:

During the Interim Period, PPAs and Vesting Contracts executed by

the Successor Companies shall not be effective.

This has profound implications for cash flows expected by the owners of

the Successor Companies, not least:

i. Ultimately it means that the Successor Companies cannot raise the

project or corporate finance to fund capex and their operations as

expected because banks will only lend to them if they have

bankable PPAs, Vesting Contracts, GSAs, etc which underpin

their respective business plans.

ii. The MO handles settlements as before. The MO invoices and receives

payments from Successor DisCo on behalf of Successor GenCos and

IPPs. In the event that DisCos do not pay invoices in full, GenCos do

not get full payment but are settled based on an ‘Allowable Revenue’

formula to arrive at a ‘Minimum Funding Requirement’.

Table 33: Allowable Revenue During the Interim Rules Period

The adjustments made to the Revenue Requirement (RR) that underpins MYTO II for the MO to arrive at the allowable amount of funding are as follows:

DisCos

Fixed and variable costs 20% of MYTO II revenue requirement

Admin costs 100% of MYTO II revenue requirement

Return on Capital 50% of MYTO II revenue requirement

Depreciation 10% of MYTO II revenue requirement

GenCos

Energy charge 100% of energy generated and supplied to grid

Capacity charge 45% of Available Capacity

Those that have existing PPAs which would have been operational during the IRP will have any difference reimbursed once TEM is declared.

Other Service Providers

TSP 70% of MYTO II market revenue

NERC 70% of MYTO II market revenue

MO 60% of MYTO II market revenue

SO 60% of MYTO II market revenue

NBET 20% of MYTO II market revenue

Source: NERC

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 132

iii. NBET, purportedly, is meant to make up for any shortfalls in PPA

amounts for GenCos (IPPs and Successor GenCos) “that have

effective PPAs during the Interim Period”. We believe this to be at best

an ambiguous provision because ‘Effective Contracts’ for the purpose

of the IRO are those that for which all conditions-precedent have been

met. Furthermore, it is unclear where NBET is going to get these funds

from as not only are there concerns over if and how the FGN subsidy

will be disbursed during the IRP, the other purported sources of funds

appear less than certain at this stage, in our opinion.

Power Shortfall – the Gas Supply Red Herring

During the IRP GenCos are now expected to pay for their gas supplies

directly. This contrasts with the former practice where the MO deducts gas

costs from the GenCos’ receivables. Gas is supplied on a take-or-pay basis

so come what may, the GenCos must pay for their gas offtake obligations

under their GSAs. Other than the take-or-pay arrangement, the gas

suppliers have willing buyers for any gas not taken up by the GenCos.

Furthermore, those willing buyers will purchase the gas at market prices as

opposed to the GenCos which pay the DSO price for gas.

An operating fact of the IRP (and one of the main reasons that necessitated

an IRP in the first place) is that NBET and the MO are not functioning (or

funded) as they should and were expected to be at that time. In particular,

as previously stated, they are not paying for all the capacity generated by

the GenCos nor making up shortfalls in the PPAs. Caught between a

proverbial rock and a hard place, the GenCos’ cash flows are strained.

Shortfalls in settlements meant gas suppliers weren’t being paid,

“everybody owes everybody money”. This eventually resulted in the gas

suppliers turning off/limiting flow from their taps to the GenCos, hence the

recent decline in generation.

In Chapter 9: Gas Supply – Fuel-to-Power (on page 101), we talked about

the 2 August 2014 announcement made by the FGN via the Ministries of

Power and Petroleum and NERC on the upward revision of the DSO gas-

to-power price. In the same announcement it was stated that in conjunction

with the Central Bank of Nigeria (CBN), they would be setting up a facility to

settling outstanding gas-to-power debts owed to the gas suppliers,

estimated at ₦25 billion (US$156.3 million). These developments are

certainly welcome; however it is very early-days. Moreover, the precise

mechanism for managing this process is yet to be finalised as the CBN

plans to engage the banking sector in the bid to settle these accounts.

Nigerian Power Sector

Infrastructure

CSL Stockbrokers is a division of FCMB (UK) Limited which is authorised by the Prudential Regulation Authority (PRA) and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) in the United Kingdom

Page 133

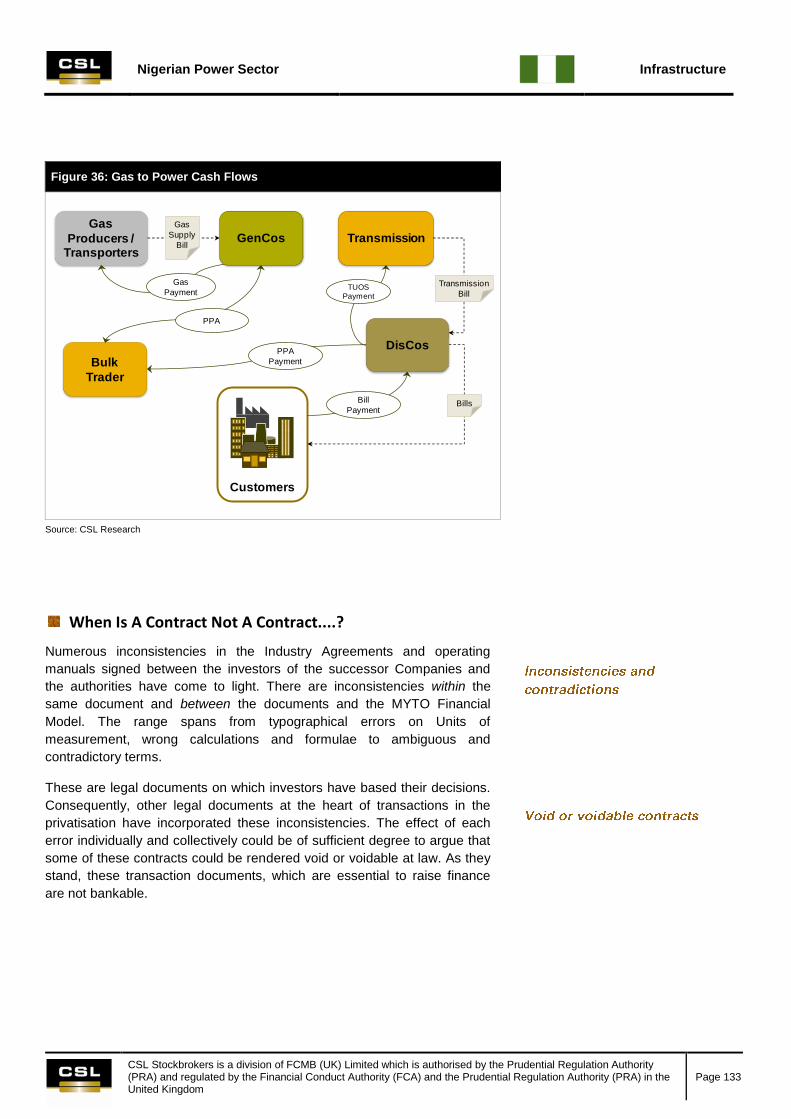

Figure 36: Gas to Power Cash Flows

Source: CSL Research

When Is A Contract Not A Contract....?

Numerous inconsistencies in the Industry Agreements and operating

manuals signed between the investors of the successor Companies and

the authorities have come to light. There are inconsistencies within the

same document and between the documents and the MYTO Financial