Embed Size (px)

Citation preview

Master Programme in Finance

Does Hedging Increase Firm

Value?

An Examination of Swedish Companies

Author: Ngan Nguyen

Supervisor: Ph.D. Håkan Jankengård

ABSTRACT In an uncertain financial world, corporate risk management has become an important

element of a firm’s overall business strategy. The ability to manage risk will help

companies act more confidently on future business decisions. Their knowledge of the

risks they are facing will give them various options on how to deal with potential

problems. One of the most popular risk management programs that firm adopts is to

hedge against the future’s fluctuations of income due to the changes in currency

exchange rate or interest rate risk. Despite an increasing interest in developing theoretical

studies about the reasons why firms involved in risk management, however, only a

handful of studies that address the issue whether risk management can enhance the firm

value. The purpose of this project research is to fill this gap and investigate the impact of

hedging on firm value.

Using Tobin’s Q as an approximation for firm market value and hedging as a control

variable, I examined 90 Swedish firms listed on the Stockholm Stock Exchange, having

the total assets exceeds at least 1 billion Euros. The results of the regression analysis

show insignificant indication that the usage of hedging impacts firm value positively. The

findings of this research imply that there is no evidence that support the hypothesis that

hedging causes an increase in firm value.

Key words: corporate hedging, firm value, risk management, derivative

PREFACE

The past ten weeks writing this master thesis have been very interesting, educating and

challenging. Developing this thesis has been hard work and time- consuming nonetheless

a process of learning.

I would like to express my sincerest gratitude towards my supervisor, Ph.D., Assistant

Professor Håkan Jankengård for being a countless supportive person when developing

my thesis and for help me during the troublesome phase. Without his guidance, this thesis

would not be enabled.

Lund, May 2015

Table of Contents

1. INTRODUCTION ............................................................................................... 1 1.1 BACKGROUND ............................................................................................................................................. 1

1.2 PROBLEM DISCUSSION .............................................................................................................................. 3

1.4 AIM AND RESEARCH QUESTION .......................................................................................................... 4

1.5 LIMITATIONS .................................................................................................................................................... 5

1.6 RELEVANCE OF THE STUDY ................................................................................................................... 5

1.7 OUTLINE OF THE THESIS .......................................................................................................................... 5

2. LITERATURE REVIEW ................................................................................... 7 2.1 THE MODIGLIANI AND MILLER THEOREM ................................................................................... 7

2.2 THE THEORIES OF CAPITAL ASSET PRICING MODEL (CAPM) ........................................... 8

2.3 WHY FIRM HEDGE? .................................................................................................................................... 11

2.3.1 MINIMIZING THE UNDERINVESTMENT PROBLEM ................................................................ 11 2.3.2 MANAGERIAL RISK ADVERSION, COMPENSATION, AND HEDGING ........................... 12 2.3.3 DEBT AND HENDGING POLICIES ...................................................................................................... 13 2.3.4 TAX BENEFITS AND HEDGING POLICIES ..................................................................................... 15

2.4 SUMMARY .................................................................................................................................................. 17

3. METHODOLOGY .............................................................................................. 19 3.1 RESEARCH APPROACH AND STRATEGY ...................................................................................... 19

3.2 DATA COLLECTION ................................................................................................................................... 19

3.3 RESEARCH PROCEDURES ...................................................................................................................... 20

3.4 STATISTICAL DISTRIBUTIONS FOR DIAGNOTIC TESTS...................................................... 24

3.5 LIMITATION ................................................................................................................................................... 26

4. RESULTS AND ANALYSIS ............................................................................. 27 4.1 EMPIRICAL FINDINGS .............................................................................................................................. 27

4.1.1 STATISTICAL TEST ....................................................................................................................................... 27 4.1.2 HEDGING AND FIRM VALUE USING MULTIVARIATE TEST .......................................... 27 4.1.3 ROBUSTNESS .................................................................................................................................................. 28

4.2 ANALYSIS OF THE FINDINGS .............................................................................................................. 30

5. CONCLUSION ................................................................................................. 32

6. REFERENCES .................................................................................................... 33

7. APPENDIX ....................................................................................................... 37

1

1. INTRODUCTION

This chapter begins with a brief overview about the impact of hedging on firm value and the

reason firms hedge. The problem discussion will highlight the contradict findings related to

whether hedging impact firms value. Subsequently, I am presenting the aim and research

question at the end of the chapter.

1.1 BACKGROUND

Corporate risk management is an important element of a firm’s overall business strategy (Guay

& Kothari, 2002). In an uncertain financial world, a better understanding of the impact of risk

management on firm value is valuable to determine the firm’s long- term success. Stulz (1996)

argued that the primary goal of risk management is to eliminate the probability of costly lower-

tail outcomes- those that would cause financial distress or make a company unable to carry out

its investment strategy. In the last decades, risk management has moved from pure risk

mitigation to value creation (Ahmed, Azevedo & Guney, 2010). Despite the prevalence of

corporate risk management and the effort that has been devoted to develop theoretical studies

about the reasons why firms involved in risk management, however, only a handful of studies

that address the issue whether risk management can actually enhance the firm value (Haushalter,

2000; Allayannis & Weston, 2001).

As a definition of risk management, it is a process of thinking systematically about all possible

risks, problems or disasters before they happen and setting up procedures that will avoid risk or

at least minimize its impact1. The most popular risk management program that firms adopt is

hedging; a firm can hedge by trading in particular futures, forward or option market even though

it has no identifiable cash position in the underlying commodity (Smith & Stulz, 1985).

According to the classic Modigliani and Miller paradigm, in a perfect market, risk management

is irrelevant to firm as shareholders can do it on their own at the same cost (Yin & Jorion, 2004).

However, recent studies have shown that in the presence of realistic capital market

1 An Introduction to Risk Management, www.ourcommunity.com.au

2

imperfections, i.e. agency costs, costs of external financing, direct and indirect bankruptcy costs,

as well as taxes, corporate hedging will enhance the shareholder value (Hagelin, 2003; Aretz,

Bartram & Dufey, 2007). Those studies suggested that hedging could increase firms’ values by

reducing the expected costs of financial distress, lowering the expected cost of taxes or minimize

the underinvestment problems. Geczy, Minton and Schrand (1997) besides providing empirical

evidence and further theoretical arguments, which support the view, that hedging can create

value; they also found that firms’ use of currency derivatives is positively related to growth

opportunities by examining currency-hedging activities for a large sample of Fortune 500 firms.

Allayannis and Weston (2001) studied the relationship between hedging and firm value, with a

sample of 720 firms, the authors focus their analysis on the subsample of firms that are exposed

to exchange rate risk through sales from foreign operations and examine whether firms that have

similar exposure differ in value, depending on whether they hedge or not. The finding of their

studies indicates that firms that begin a hedging policy experience an increase in value relative to

those firms that choose to remain unhedged and that firms that quit hedging experience a

decrease in value relative to those firms that choose to remain hedged. Ahmed, Azevedo and

Guney (2010) by studying a sample of 288 nonfinancial UK firms, also found evidence that

support the value creating theory. Although the effect of hedging on firm value and performance

varies significantly across financial risks and that there are derivatives that are more effective in

hedging certain types of risks, contributing favorably to value creation and financial perform.

Similarly, Jankengard (2015) by studying the sample of 257 listed Swedish firms found

evidences consistent with the hypothesis that derivatives usage is more value creating in firms

with centralized FX exposure management than in firms with a decentralized approach.

While all of the risk management theories indicated that hedging could increase firm value, the

type of firm risk targeted by theories varies. For example, if a firm faces costly external

financing then the focus will lay on the volatility of cash flows as the risk measure to be hedged.

On the other hand, when the firms’ managers are risk adverse and under- diversified with respect

to their compensation, they are likely to reduce the firm’s risk by hedging in order to reduce the

required risk premium. In the case, the type of risk targeted for hedging is associated with cash

flows, earnings, or stock price volatility, depending on the nature of the managers’ compensation

3

contract and firm- specific wealth (Guay & Kothari, 2002). Another incentive for firms to hedge

is to reduce the expected cost of tax liability. The structure of the tax code can make it

advantageous for firms to take positions in futures, forward, or options markets. If effective

marginal tax rates are an increasing function of the corporation’s pre- tax value. If hedging

reduces the variability of pre –tax value, then the expected corporate tax liability is reduced and

the expected post- tax value of the firm is increased, as long as the cost of the hedge is not too

large (Smith & Stulz, 1985).

1.2 PROBLEM DISCUSSION

There is mixed support for value creating theories; however, it could be argued that corporate

hedging has no impact on firm value (Modigliani & Miller, 1958), as investors can achieve risk

reduction at least as efficiently themselves through diversification. Dufey and Srinivasulu (1983)

argued that the hedging of risks that investors cannot diversify in financial markets might also

not increase shareholder value, as investors receive an appropriate return for holding securities of

inherently risky businesses. Therefore, corporate hedging of market risks simply shifts firms

along a line that reflect the risk/reward tradeoff in the market. Mian (1996) surveyed the effect of

hedging activities on gold mining firms and found no support for the value maximization theory

even though he found strong evidence that supported the managerial risk aversion theory:

according to which managers who hold more stock tend to undertake more hedging activities. Jin

and Jorion (2006) investigated the hedging activities of a sample of 119 U.S oil and gas

producers from 1998 to 2001. They tested for a difference in firm value between firms that hedge

and those that do not hedge their oil and gas price risk. The result of their finding indicates that

there is no general difference in firm values between firms that hedge and firms that do not

hedge. Fauver and Naranjo (2010) also studied the relationship between agency costs and

monitoring problems affect derivative usage, which in turn affects firm value. In their

investigation, the authors gathered derivative usage data on 1746 non- financial firms

headquartered in the U.S during 1991 – 2000 and used Tobin’s Q to measure the value gain or

loss from derivative usage. The findings of their study show that the usage of derivatives has a

mixed effect on firm value, suggesting that the valuation depends on the firm’s corporate

governance structure. Firms with greater agency and monitoring problems (i.e. firms that are less

transparent, face greater agency costs, have larger information asymmetry problems and so on)

4

experience negative valuation when using derivatives. Meanwhile, firms with better corporate

governance structure experience a positive firm value when using derivatives.

Those studies are contrary to the findings report in Allayannis and Weston (2001); Jankengard

(2015).

Most of the studies within the topic of risk management have mostly focused on the reasons to

why firms hedge or the relation between corporate hedging and firm characteristics (Smith &

Stulz, 1985; Hagelin, 2003; Aretz, Bartram & Dufey, 2007). Even though there are contract

findings of how hedging affect firm value, not so many studies have addressed the question

whether of there is a direct relation between hedging and firm value. The lack of attention to this

relationship creates a strong incentive for me to write this thesis.

1.4 AIM AND RESEARCH QUESTION

The purpose of this study is to shed light on the impact of hedging on firm value. Due to a mix of

results regarding the impact of hedging, this study aims to investigate if hedging can impact the

firm value positively. In this thesis, the period from 2005 to 2010 will be used and under this

period, the world has witnessed one of the most severe financial crises in the history. With this

fact in hand, I believe that hedging can create a higher value for firms since it minimizes the

financial distress that related to a slower economy. To address this issue, this research project

will explore the following question:

Does hedging impact the firm value?

There are many argument about whether hedging can increase firm value (Allayannis & Weston,

2001; Jin & Jorion, 2006; Jankengard, 2015), however, most of the empirical research did not

show any positive correlation between hedging and firm value that were performed before 2006.

None of the research (Dufey & Srinivasulu,1983; Mian, 1996; Jin & Jorion, 2006) has witnessed

the impact of our current financial crisis. Also, the time panel of the studies was relatively short,

in most cases the period varies between 1- 3 years, therefore one may not see the impact of

hedging immediately. Consequently, given that we are living in an uncertain financial world,

hedging will increase the firm value since it sends a signal to investors that the firms’ future cash

flows are secured, and the risk of financial distress will be reduced.

5

1.5 LIMITATIONS

The first limitation of this study is to focus on Swedish firms that listed on the Stockholm Stock

Exchange. Under limited resources and time, I narrow the research toward a handful mid-size

and large-size companies that have total assets exceed at least one billion Euros. I tried to find

companies that have headquarters in Stockholm but dealing with international trade. Therefore,

the result of this study is only applicable for Swedish firms.

The second limitation is the period in which firms’ hedging activities are observed.

Since there are no available suggestions about how long time is the optimal time to notice how

much hedging impacts firm value, so I choose a period of six years. The years 2005 to 2010 have

been choose, as the data is not completed after this date.

1.6 RELEVANCE OF THE STUDY

Firms use derivatives to hedge their exposure to a variety of risks. Hedging exposure attracts a

great deal of managerial and financial resources (Hagelin, 2003). Therefore, knowledge of

whether derivative hedging can add value to firms is of importance to shareholders. However,

previous research has shown contradicting findings of the impact of hedging on firm value

(Allayannis & Weston, 2001; Jin & Jorion, 2006; Jankengard, 2015). Until now, we still cannot

draw a firm conclusion about whether hedging can add a positive value to firms or not.

Therefore, the demand for a better understanding of risk management shows the importance of

this research project to deal with the uncertainties in today’s financial world.

With this knowledge of firm value, companies will be able to enhance their future success.

Furthermore, in a macro perspective, this study could contribute to creating a more stable

economic development.

1.7 OUTLINE OF THE THESIS

The thesis consists of 7 chapters: Chapter 1 introduces the background to the study, the problem

discussion, followed by the aim and objectives of the research question. Chapter 2 presents the

Literature and Theoretical Review, which discusses previous research relevant to the study,

followed by a theoretical underpinning in this study. Chapter 3 describes the methodology in

which the data was collected and how it was analyzed. Chapter 4 presents the data findings along

6

with the discussion. The thesis ends with chapter 5 that presents the conclusions are drawn from

the findings along with implications and suggestions for further research.

7

2. LITERATURE REVIEW

The previous chapter provides a basic overview about the contradiction in theories regarding

the impact of hedging on firm value, followed by the problem discussion and purpose of the

study. This chapter will bring up relevant studies related to areas connect to my thesis topic,

starting with the classic Modigliani& Miller theorem and CAPM theories followed by a deep

review of the reasons why firms hedge.

2.1 THE MODIGLIANI AND MILLER THEOREM

The basic idea of the Modigliani and Miller (M&M) theorem is that under certain assumptions

such as if the CAPM holds, then it does not matter how the firm chooses to finance its

investment: either by issuing shares, borrowing debts or spending its cash. The financing method

will not affect the value of a firm since firm value is determined by its earning power and by the

risk of its underlying assets. For the theorem to hold, there are some criteria must be satisfied

such as there are no taxes, no transaction costs and no bankruptcy cost (Ogden, Jen & O’Connor,

2003). The theorem is consisted by two propositions; below I will describe the content of each

proposition in details based on the work of M&M (1958).

Proposition I

Consider any company j and let 𝑋𝐽 stand as before for the expected return on assets owned by the

company. Denote 𝐷𝑗 as the market value of the debt of the company and 𝑆𝑗, the market value of

the company’s common shares. In Equilibrium we have:

𝑉𝑗, ≡ (𝑆𝑗 + 𝐷𝑗) = 𝑋𝐽/ 𝜌𝑘 for any firm j, in class k.

“That is the market value of the any firm is independent of its capital structure

and is given by capitalizing its expected return at the rate 𝜌𝑘 appropriate to its

class (M&M, 1958 pp. 268)”.

This proposition can be stated in an equivalent way in terms of firm average cost of capital 𝑋𝑗/𝑉𝑗,

we can then express the proposition as:

8

𝑋𝑗

( 𝑆𝑗 + 𝐷𝑗 ) ≡

𝑋𝑗

𝑉𝑗 =𝜌𝑘 for any firm j, in class k.

“That is, the average cost of capital to any firm is completely independent of its

capital structure and is equal to the capitalization rate of pure equity stream of its

class (M&M, 1958 pp. 268-269)”.

Proposition II

Proposition II is a situation when the rate of return on common stock in companies whose capital

structure includes some debt: The expected rate of return, i on the stock of any company j

belonging to kth class is a linear function of leverage as follow:

𝑖𝑗 = 𝜌𝑘 + (𝜌𝑘 − 𝑟) ∗ 𝐷𝑗/𝑆𝑗

“That is, the expected rate of return of a share of stock is equal to the appropriate

capitalization rate, 𝜌𝑘 , for a pure equity stream in the class, plus a premium

related to financial risk equal to the debt to equity ratio times the spread between

𝜌𝑘 𝑎𝑛𝑑 𝑟 (M&M, 1958)”.

The conclusion, which can be derived from proposition I & II, is that in an efficient market when

a firm value is not affected by the taxes, bankruptcy costs, agency costs and information

asymmetry. It will not matter how a firm choose to invest in some projects, the 𝜌𝑘 will be

completely unaffected by the type of security firm used to finance the investment. In other word,

regardless of the financing used, the marginal cost of capital to a firm equal to the average cost

of capital, which is in turn equal to the capitalization rate for an unlevered stream in the class to

which the firm belongs (M&M, 1958).

2.2 THE THEORIES OF CAPITAL ASSET PRICING MODEL (CAPM)

The Capital Asset Pricing Model is probably one of the most famous models in the financial

history. The model builds on the Markowitz mean-variance- efficiency model in which risk

adverse investors with a one period horizon care only about expected returns and the variance of

returns (Fama & French, 2004). The basic idea of this model is that the investors are price takers

and have homogenous expectations will choose only efficient portfolio, meaning that given the

9

same expected returns they will choose the portfolio with minimum variance and with given

variance they will choose the portfolio with maximum returns.

Figure 1: The Capital Asset Pricing Model

Source: Fama & French (2004)

The equation for the expected return for a given asset 𝐸 (𝑅𝑖) is:

𝐸(𝑅𝑖) = 𝑟𝑓 + 𝛽𝑖 [E (𝑟𝑚) − 𝑟𝑓]

The equation above describes the relationship between the expected return of the asset 𝐸 (𝑅𝑖)

and risk where 𝐸 (𝑅𝑖 ) is the sum of the risk- free rate and the risk premium of the market

multiplied by 𝛽𝑖. In other word, 𝐸 (𝑅𝑖) is the compensation that the investors require for taking

additional risk.

According to Rothschild (1985), the CAPM captures the notion that an asset’s risk premium is

determined by its diversifiable risk. In the CAPM, an asset’s diversifiable risk is measured by its

covariance with the market and is called Beta, 𝛽𝑖 is the systematic risk and it measures the

sensitivity of the expected excess asset return to the expected excess market return and can be

expressed mathematically:

10

𝛽𝑖= 𝐶𝑜𝑣 (𝑟𝑖,𝑟𝑚)

𝑉𝑎𝑟 (𝑟𝑚)

The market portfolio presents the market and is consisted of all the assets. The β of the market

portfolio is equal to one.

The reason I include CAPM in the Literature Review Chapter is to highlight the contradict

theories regarding how risk management impact firm value. From the shareholder’s perspective,

risk management should contribute to the firm value. However, it is not entirely obvious why

risk management can increase firm value. The demonstration below proving the so- called risk

management irrelevance proposition is based on the Lecture note one (pp. 2-3) from the course

Risk Management, spring semester, 20142.

From above, the mathematical expression for beta is:

𝛽𝑖= 𝐶𝑜𝑣 (𝑟𝑖,𝑟𝑚)

𝑉𝑎𝑟 (𝑟𝑚)

Now we want to value a firm with systematic risk (β> 0), in one year the firm will earn an

uncertain cash flow (CF) and then liquidate. Under the assumptions that if CAPM hold, then the

expected return of the investment is:

𝐸 [𝐶𝐹]−𝑉

𝑉 = 𝑟𝑓+ β (E [𝑟𝑚] − 𝑟𝑓)

Where V is the value of the firm, and the value of the firm today according to the CAPM is:

V = 𝐸 [𝐶𝐹]

1+ 𝑟𝑓+ β (E [𝑟𝑚] − 𝑟𝑓)

The value of the firm today is the discounted expected value of the cash flow and the discounted

rate is equal to 1 + 𝑟𝑓+ β (E [𝑟𝑚] − 𝑟𝑓), which is higher than the risk free rate, reflecting the

systematic risk.

If CAPM holds, we can decompose the actual return R of the firm as:

R = 𝑟𝑓+ β [𝑟𝑚 − 𝑟𝑓] + u

2 Course: Risk Management, Instructor: Birger Nilsson

11

Where 𝑟𝑓+ β [𝑟𝑚 − 𝑟𝑓] is the systematic component of the return and u is the unsystematic

component of the return (which is uncorrelated with the systematic return and has zero mean.

Taking the variance of R we obtain:

var (R)= var (𝑟𝑓+ β [𝑟𝑚 − 𝑟𝑓] + 𝑢 )= β2𝜎𝑚2 + 𝜎𝑢

2

Where 𝜎𝑚2 is the variance of the market, and 𝜎𝑢

2 is the variance of the unsystematic firm return.

From here we can see that conclude that risk management will not impact firm value since only

the systematic risk (β) enters the formula to calculate firm value V when the unsystematic risk 𝜎𝑢2

not. Even if the firm wants to hedge the market risk β, this act doesn’t help the firm either, since

the cost of hedging will offset the lower discounted rate (through lower β) on an efficient market.

2.3 WHY FIRM HEDGE?

2.3.1 MINIMIZING THE UNDERINVESTMENT PROBLEM

The neoclassical investment models (Hayashi, 1982) suggest that the firm faces frictionless

capital markets and the Modigliani and Miller (1958) theorem holds. In reality, however, firms

often face important external financing cost due to asymmetric information and managerial

incentive problems (Gay & Nam, 1998; Bolton, Chen & Wang, 2011). This happens because the

decline in in a firm’s stock price depends on the fact that the demand curve for shares is

downward sloping, meaning that when the firm increases the amount of its shares will have to be

sold at discount from existing market prices in order to attract new buyers. The magnitude of the

discount is an increasing function of the size of the issue (Scholes, 1972). There are a number of

previous researches that try to measure these external financing costs. For instance, Asquith and

Mullins (1986) find that the average stock price reaction to the announcement of a common

stock issue is -3% and the loss in equity value is -31 %.

One of the reasons why firms choose to hedge depends on the fact that they want to avoid

underinvestment problem. That’s to be said, firms might have some promising future’s

investments, but those investments require significant funding and firms need plenty of cash.

Froot, Scharfstein and Stein (1993) argue that if external financing is more costly than internal

financing, hedging can be a value increasing activity if it more costly matches fund inflows with

12

outflows, thereby lowering the probability that a firm needs faces costs of external funds, it can

reduce future financing costs by holding cash to finance its future investments i.e. lowering the

probability that a firm needs to access to the capital market. In other word, hedging creates a

positive association between potential underinvestment costs and the benefits of hedging.

The question here is: How much value does hedging add to the firm? Bolton, Chen and Wang

(2011) answer this question by computing the Net Present Value (NPV) of optimal hedging to

the firm with costly margin requirements (the percentage of marginal securities that an investor

must pay for with his/her own cash). The NPV of hedging is calculated as follows. First the

author computes the cost of external financing as the difference in Tobin’s q under the case of

hedging and under the case of not hedging. Second, they compute the loss in adjusted present

value (APV), which is the difference in Tobin’s q under the case of hedging and the case of

hedging with a costly margin. Then the difference between costs of external financing and the

loss in APV is simply the value created through hedging. The authors find out that, on average,

when measured relative to Tobin’ q under hedging with a costly margin, the cost of external

financing is about 6% and the loss in APV is about 5%, so that the NPV of costly hedging is on

the order of 1%.

2.3.2 MANAGERIAL RISK ADVERSION, COMPENSATION, AND HEDGING

In corporate finance theory, the principal- agency problem is explained by for example there are

two individuals who operate in an uncertain environment and for whom risk sharing is desirable.

Suppose that one of the individuals known as the agent is to take an action which the other

individual known as the principal cannot observe. The problem arises when the principal cannot

monitor the agent’s behavior, leading to the agent acts in his self- interest at the expense of the

principal (Grossman & Hart, 1983). In general, the action, which is optimal for the agent will

depend on the extent of risk sharing between the principal and the agent. The question is: In the

present of information asymmetry, what is the optimal action the principal needs to take in order

to protect his interest? Smith and Stulz (1985) took this question into consideration and argued

that in a corporate environment, under a constraint budget, the amount of risk that can be

allocated to the stockholders is restricted by the company’s capital stock. However, the firm can

reduce the risk imposed on other claim holders by hedging. To see this, let assume that

shareholders hire managers for their specialized resources, but in the absence of monitoring

13

shareholders will not know if the mangers really do their best in order to maximize the

shareholders’ value. One solution to the principal and agent problem is that the compensation

contract must be designed so that when managers increase the value of the firm, they also

increase their expected utility.

When the compensation ties to the manager’s performance i.e. in term of the stock price

movements, for the most part, stock price- related compensation schemes might consist of

company stock or stock option programs. If the future’s stock price can affect management’s

compensation, then the potential decline in stock price will intensify the risk aversion if

undiversified managers. As a result, strong incentives are created for managers to reduce their

risk aversion and to boost the stock price (Bartram, 2000).

Nonetheless, the stock price movement doesn’t depend only on the managers’ performance but

other determinants as well for example exchange rate or interest rate risks are clearly beyond the

managers’ control. As a result, due to the external influences unrelated to managers’

performance on share price, management compensation plans are less effective (Aretz, Bartram

& Dufey, 2007). If managers and shareholders have different risk preferences, the firm may not

be able to achieve its maximum value since the managers will be less like take risky investments.

In order to solve this problem, the firm can employ a hedging program since it will reduce the

impact of unrelated financial risks on firm value and help to secure the manager’s compensation.

However, we need to take into account that the managers’ risk aversion can give them the

incentive to hedge, but it not necessary happen in that way. Smith and Stulz (1985) explained

that if the compensation package of the manager is such that his income is a convex function of

the value of the firm, it leads to that manager is better off if he choose not to hedge. Hence, the

more option- like features in a firm’ compensation plan, the less the firm is expected to hedge. In

other hand, if the manager owns a significant fraction of the form, he will likely to hedge, as his

income is now more a linear function of the firm’s value.

2.3.3 DEBT AND HENDGING POLICIES

The transaction costs related to bankruptcy can be a deal breaker when it comes to hedging.

Recent empirical studies of hedging theories have paid significant attention to the impact of high

14

leverage on firm’ decision to hedge. Classic corporate finance theory tells us that while high

leverage increase firm’s value through the tax advantage of debt (Modigliani & Miller, 1958)

since it also puts pressure on the firm i.e. a risk- averse investor will think twice before he puts

money on a high leverage firm. Furthermore, in case firm doesn’t meet its obligations to debt

holders promptly, the firm may encounter financial distress and ultimately, bankruptcy (Aretz,

Bartram & Dufey, 2007).

Financial distress costs consist of two forms: direct and indirect costs. Direct costs refer to a

situation when in the case of bankruptcy; firms need to pay fees for lawyers, expert witnesses

and administrative and accounting fees. While indirect costs relate to the situation when firms

lose valuable contact with customers, suppliers or skillful employees. To demonstrate how

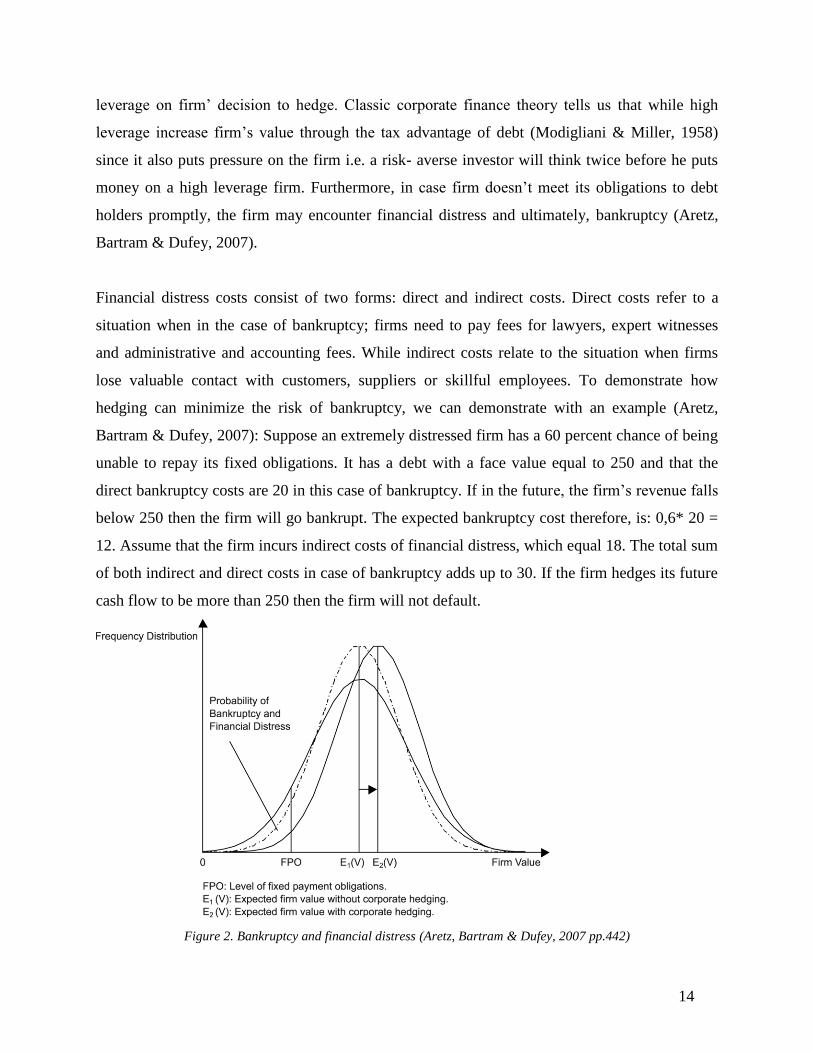

hedging can minimize the risk of bankruptcy, we can demonstrate with an example (Aretz,

Bartram & Dufey, 2007): Suppose an extremely distressed firm has a 60 percent chance of being

unable to repay its fixed obligations. It has a debt with a face value equal to 250 and that the

direct bankruptcy costs are 20 in this case of bankruptcy. If in the future, the firm’s revenue falls

below 250 then the firm will go bankrupt. The expected bankruptcy cost therefore, is: 0,6* 20 =

12. Assume that the firm incurs indirect costs of financial distress, which equal 18. The total sum

of both indirect and direct costs in case of bankruptcy adds up to 30. If the firm hedges its future

cash flow to be more than 250 then the firm will not default.

Figure 2. Bankruptcy and financial distress (Aretz, Bartram & Dufey, 2007 pp.442)

15

Figure 1 above shows the distribution of cash flows of a firm, which is unable to pay off the debt

to its debt holders when the cash flow drops under FPO. As the probability of falling below this

point is positive, the firm may go bankrupt with a positive bankruptcy costs. If corporate risk

management ensures that firm’s future cash flow will be above FPO, firm value increases from

𝐸1(𝑉) to 𝐸2(𝑉).

So far, we have discussed the benefit of hedging to potential bankruptcy, but we still do not take

into consideration the size of hedging costs. One question remains if hedging still increases the

firm value if the costs of hedging are significant? Warner (1977) pointed out that in case if the

transaction costs of bankruptcy costs are a small fraction of large firms’ assets and they are less

likely the reason for firms to hedge. However, if the reduction on expected bankruptcy costs

exceeds the costs of hedging then large firms will likely to hedge. The same argument applies for

small firms as well; since the expected bankruptcy costs are a significant fraction of the small

firm’ assets, then the reduction in expected bankruptcy costs is greater for the small firms.

Therefore, they will be more likely to hedge.

Smith and Stulz (1985) explored the fact that hedging still give benefits to the firm give the fact

that the hedge decreases the present value of bankruptcy costs and increases the present value of

the tax shield of debt. To maximize the firm value, one thing managers can do is choosing the

hedging alternative that has lower cost.

2.3.4 TAX BENEFITS AND HEDGING POLICIES

The structure of the tax code can make it advantageous for firm to take positions in futures,

forward, or options markets. To analyze the effect of hedging on the present value of the firm’s

after- tax cash flow, I will use the demonstration taken from (Smith & Stulz, 1985). We can

assume that there are s states of the world, with 𝑉𝑖 defined as the pre- tax value of the firm in

state of the world i. States of the world are numbered so that 𝑉𝑖 < 𝑉𝑗 if i < j. Let 𝑃𝑖 be the price

today of one dollar to be delivered in state of the world i and T (𝑉𝑖) be the tax rate if the before-

tax value of the firm is 𝑉𝑖. In the absence of leverage, the value of the firm after taxes, V (0), is

given by:

(1) V (0) = ∑ 𝑃𝑖 (𝑉𝑖 − T (𝑉𝑖)𝑉𝑖)𝑆𝑖=1

16

Hedging can increase the value of the firm if there two states in the world, j and k, such that T

(𝑉𝑖) < T (𝑉𝑘). To demonstrate it, suppose that the firm holds a hedge portfolio such that 𝑉𝑗 + 𝐻𝑗 =

𝑉𝑘 + 𝐻𝑘, and that the hedge portfolio is self- financing in the sense that 𝑃𝑗 𝐻𝑗 + 𝑃𝑘 𝐻𝑘 = 0. Let

𝑉𝐻(0) be the value of the hedged firm. Then we have:

(2) 𝑉𝐻(0) – V (0) = 𝑃𝑗 (T (𝑉𝑗)𝑉𝑗 − T (𝑉𝑗 + 𝐻𝑗) (𝑉𝑗 + 𝐻𝑗))

+ 𝑃𝑘 (T (𝑉𝑘)𝑉𝑘 − T (𝑉𝑘 + 𝐻𝑘) (𝑉𝑘 + 𝐻𝑘)) > 0

The inequality implies that (2) is a concave function. Therefore, costless hedging increases the

value of the firm.

Figure 3: Tax and Hedging policies (Aretz, Bartram & Dufey, 2007 pp.443)

Figure 2 above show illustrated the fact if the firm tax schedule is a convexity, and then the firm

faces a higher expected tax burden in the case of high volatile pre- tax income than in case of

stable income. Therefore, the value of hedging will increase firm value compare with when the

tax schedule is linear.

However, there are contradict about corporate tax shields can induce value maximizing

corporation to hedge their operating cash flows. Kale and Noe (1990) point out that corporate

17

debt tax shields can prevent firms from hedging. The intuition behind this statement is that value-

maximizing firm will set its hedging policy with the objective of minimizing the sum of financial

distress costs. If the corporate tax code exhibits convexity and personal tax rates are linear, then

the act of hedging can actually lower the value of the firm. As mentioned earlier in the Debt and

Hedging policies part, firm will choose to hedge if the benefit of hedging exceeds the financial

distress costs then firm will be better off to hedge. Nonetheless, if the effective corporate tax rate

is low and the costs of bankruptcy are low, and then the effect of hedging will be to lower the

value of the firm.

2.4 SUMMARY

There are two contradicting theories about whether firms should hedge or not. According to the

neoclassical investment theories (Modigliani& Miller, 1958; Hayashi, 1982), in an efficient

market (assuming CAPM hold) hedging is fruitless since investors with access to perfect

information can manage to reduce the risk in their portfolios by themselves. In other word,

hedging creates no value to the firm.

Nonetheless, in the presence of realistic capital market imperfections, i.e. agency costs, costs of

external financing, direct and indirect bankruptcy costs, as well as taxes, corporate hedging will

enhance the shareholder value. The theories about why firms choose to hedge can be divided into

two categories: (1) Shareholder value maximization theory and (2) The structure of financial

structure and tax code. The shareholder value maximization theory highlights the fact that when

the compensation ties to the manager’s performance in term of the stock price movements i.e. if

the future’s stock price can affect management’s compensation, then the potential decline in

stock price will intensify the risk aversion if undiversified managers. Hence, a risk adverse

manager will stay away from risky projects, leading to underinvestment problem. One solution to

this underinvestment problem is to hedge against the fluctuation of the stock price movement

(Smith & Stulz, 1985; Froot, Scharfstein& Stein, 1993; Aretz, Bartram& Dufey, 2007).

Regarding the financial structure and tax code of the company, the motivations behind firm’s

decision to hedge are to (1) minimize the risk of bankruptcy and (2) reduce the corporate tax

burden if the firm tax schedule is a convexity, then the firm faces a higher expected tax burden in

the case of high volatile pre- tax income than in case of stable income. Therefore, the value of

18

hedging will increase firm value compare with when the tax schedule is linear (Smith & Stulz,

1985; Aretz, Bartram& Dufey, 2007).

19

3. METHODOLOGY

This chapter will describe the methodology used when developing this thesis and how the data

was collected, followed by different diagnostics tests. In the end of this chapter, I present the

OLS equation for estimating the firm value.

3.1 RESEARCH APPROACH AND STRATEGY

The research approach is used in this study has a quantitative nature, which is “explaining

phenomena by collecting numerical data that are analyzed using mathematically based methods”

(Aliaga & Gunderson, 2000). In order to find out if hedging can affect firm value or not, all the

data need to be tested by using Eviews- a software program for time- series oriented econometric

analysis.

Two empirical studies are used extensively in this thesis as benchmarks. The first one is

Allayannis and Weston (2001) and the second one is Jankengard (2015), both studies provide

great analysis and data about the subject. Nonetheless, I pay most attention to Jankengard’s study

by following reasons:

The methodology in which the author used is very well described and easy to replicate.

The author was one of few researchers that study Swedish firms’ derivatives usage at a

very deep level and his research provides great guidance to my own study.

3.2 DATA COLLECTION

The data used consisted of 90 Swedish firms listed on the Stockholm Stock Exchange, having the

total assets exceeds at least 1 billion Euros. Initially 353 firms were extracted from DataStream,

thereafter I excluded all the financial service firms, because most of them are also market makers

in Foreign Currencies derivatives, hence their motivations for using derivatives may be different

from the motivations of nonfinancial firms. I also excluded public organizations because they are

heavily regulated. The next step is to delete all the firms that don’t have complete data. This is an

easy task since most of the data was extracted from the Data Stream. After the selection, I was

left with 90 firms.

The choice of sample selection is very critical to the accuracy of results. Firstly, the sample is

limited to the Swedish large and mid-cap firms in different industries with different growth rates.

Comparison of the value may be affected by other variables not included in the analysis.

20

Secondly, I am aware that firms in different industries with different growth rates can make the

comparison bias since the firm value can be affected by other variables not include in the

analysis.

3.3 RESEARCH PROCEDURES

The purpose of this study is to document the impact of hedging on firm value. However, there

are other variables that may affect the firm value as well, such as: profitability, leverage,

dividend, industrial diversification, firm size, CAPEX (Allayannis & Weston, 2001; Jankengard,

2015). To take those variables into account, a multivariate setting will be used to test the

hypothesis that hedgers have higher values than non-hedgers.

Firm value: To estimate the firm value, I use Tobin’s Q. Tobin’s Q is defined as the ratio of the

market value of the firm to replacement cost of assets, evaluated at the end of the fiscal year. I

compute Tobin’s Q for a total of 540 firm- year observations (Total 90 firms * 6 years).

According to Allayannis and Weston (2001), one more advantage of using Tobin’s Q is that it

makes the comparisons across firms easier than comparisons based on stock returns or

accounting measures where a risk adjustment or normalization is required.

Hedging: The information about whether the selected firms hedge or not can be collected manual

from the annual reports. I go through the reports for each firm and take note about their risk

management. In most cases, this information was easy to obtain since most companies disclosure

about their risk management program and also are clearly about why they choose to hedge. They

declare that the purpose of hedging is not for speculative activities but rather to minimize the

volatility of future cash flows and exposure to currency exchange rates. I use derivatives as a

dummy variable that take the value one if the firm hedge and zero otherwise. Using dummy

variable is appropriate for my regression analysis because it is hard to measure the size of

hedging costs since most companies only disclosure the fact that they are involving in risk

management program but do not articulate the magnitude of hedging costs in their financial

reports.

Similarly to Jankengard (2015), besides the test variable hedging, I also choose other control

variables that can affect the firm value such as: Dividend, firm size, profitability, leverage,

diversification and CAPEX. I also want to include the variable foreign sales ratio as a control

21

variable. However, due to the severe lack of relevant data, this variable needs to be excluded

from the analysis.

Dividend: is a dummy variable and takes the value of one if the firms pay dividends and zero

otherwise. The reason to why I take dividend payment into my study is there are previous

research providing the evidence that dividend payout announcement can impact firm value due

to higher dividend payout rate, the higher is the tax cost of the dividend, which dampens the

increase in firm value (Kane, Lee & Marcus, 1984; Murdoch, 1992). Nonetheless, there is also

evidence that supports the hypothesis that dividend payout enhances firm value since it signals to

the market that the firm in question is in a good financial shape, and in turn the investors reward

the firm with higher valuation (Jin & Jorison, 2006).

Firm size: There is ambiguous evidence for U.S firms that the size of the firm leads to higher

accounting profitability (Allayannis & Weston, 2001), due to the existence of large fixed start-

up costs of hedging, the firm size is determined by taking the logarithm of Total Assets.

Profitability: A profitable firm is likely to trade at a premium relative to a less profitable one.

This variable is equal to Net Income/ Total asset (Jankengard, 2015).

Leverage: A firm’s capital structure can affect its value. In Modigliani and Miller (1958)

demonstrated that in a frictionless world, financial leverage is unrelated to firm value. However,

in a world with tax- deductible interest payments, firm value and capital structure are positively

related (Antwi, Mills & Zhao, 2012). A firm’s capital structure may affect its value. To control

for leverage, I take Total Debt/Total Assets.

Industrial Diversification: This data was collected manually; I go through annual reports of all

firms and take note if the companies operate in two or more product segments. This control

variable is a dummy variable and takes the value one of the companies have more than two

segments and zero otherwise. The reason, I want to include this variable in my regression

analysis is that there are several theoretical suggest that industrial diversification increases value

(Williamson, 1970; Jensen, 1986).

22

CAPEX: is defined as additions to Fixed Assets/Total Sales.

Table 1: Summary of variables and data sources

Definition

Source

Tobin' Q The log of (total book Datastream

value of assets less book

value of equity plus market

value of equity) / Total assets

Hedging A dummy variable that has value 1 Annual reports

if the firm hedges and 0 otherwise

Leverage Total debt/ Total Assets Datastream-

CAPEX Additional fixed assets Datastream

Profitability Net income/ Total assets Datastream

Firm size Logarithm of total assets Datastream

Dividend A dummy variable that takes value 1 Datastream

if firm pays dividend and 0 otherwise

Diversified A dummy variable that takes value 1 if the Annual reports

firm has more than 2 product segments and

0 otherwise

Since I have different companies and a six- year period, I organize the collected data into panel

data in order to use the software program Eviews. The advantages of panel method comparing to

other methods are those that a panel of data will embody information across both time and space.

Most importantly, a panel keeps the same individuals or objects and measures some quantity

about them over time (Brooks, 2008).

23

Table 2: Descriptive Statistics

Number Min Max Median Mean St. Dev

Tobin' Q 85 0,24 6,26 1,21 1,55 1,09

Hedging 60 1,00 1,00 0,77 0,42

Leverage 72 0,69 0,17 0,19 0,16

CAPEX 85 0,80 0,02 0,05 0,10

Profitability 85 -0,17 0,57 0,01 0,01 0,04

Firm size 85

3,30 8,56 6,46 6,58 0,95

Dividend 80 1,00 1,00 0,69 0,46

Diversified 85 1,00 0,00 0,32 0,47

The table above describes the descriptive statistic for all the control variables. Using the

descriptive statistic is a good way to spot possible problems with the data (outliners and so on)

and it also gives an idea about the distribution of the variables while interpreting the regression.

As we can see from the descriptive statistic table, the median of Tobin’s Q is 1, 21, which is

smaller than the mean Tobin’s Q (1, 55) indicates that the distribution of Tobin’s Q is skewed.

To control for the skewness, the natural log of Tobin’s Q will be used in the multivariate test so

that the distribution of Tobin’s Q will be more symmetric.

The equation for the regression is:

Log(Tobin’s Q) = c+ 𝛽1*capex + 𝛽2 *diver + 𝛽3*dividend + 𝛽4*hedge

+ 𝛽5*leverage + 𝛽6*profit +𝛽7*size

Since I used panel data for my study, the remained question is to choose Fixed or Random

effects? According to Brooks (2008, pp. 500) the random effects model is more appropriate

when the entities in the sample can be thought of as having been randomly selected from the

population, but a fixed effect model is more plausible when the entities in the sample effectively

constitute the entire population. Furthermore, the fixed effects model also allows cross- sectional

heterogeneity. In my data sample, there are 90 firms in different industries and it is unlikely to

assume that there is no heterogeneity. One more advantage of using fixed effects model is that all

24

the unobservable firm characteristics that may affect firm value can be controlled since each firm

is assigned a unique intercept (Hausman & Taylor, 1981).

In Eviews, I still perform both of the tests in order to find the most suitable one. (1) I select the

fixed effects on the cross section after that I run the Redundant Fixed Effect- Likelihood Ratio,

the P- value is 0,000 indicating that the effects are significant. (2) Select the random effect and

perform the Correlated Random Effects- Hausman test. In this test, I am testing the random

effects model against the fixed effects model. The null hypothesis in that case is that both tests

are consistent estimators and the random effects model is efficient. Under the alternative

hypothesis, only the fixed effect is consistent. Since the p- value is 0.000, I reject the null and,

therefore, the fixed effects model is to be preferred.

3.4 STATISTICAL DISTRIBUTIONS FOR DIAGNOTIC TESTS

In order to run an OLS regression with the highest accuracy as possible, I need at first run

various regression diagnostic tests that are based on the calculation of the test statistic.

For the classical OLS to work well, there are three basic assumptions that need to be satisfied in

order to have an unbiased OLS estimation.

(1) E(𝑢𝑡) = 0

(2) Var(𝑢𝑡)= 𝜎2

(3) Cov(𝑢𝑖, 𝑢𝑡) = 0

The first assumption (1) required that the average value of the errors is zero. However, when I

estimate OLS, a constant term is included in the regression equation so this assumption will not

be violated.

For the second assumption (2), it has been assumed so far that the variance of the errors is

constant. This is known as the assumption of homoscedasticity. If the errors do not have a

constant variance, they are said to be heteroscedastic. The consequence of not having a constant

variance is that estimation of OLS will be biased. In order to detect if there is some evidence of

heteroscedasticity, I run the Goldfeld Quandt test.

25

Assumption (3) requires that the covariance between the error terms over time is zero. In other

word, it is assumed that errors are uncorrelated with one another. Because the population

disturbances cannot be observed, so a test for this is necessary. I will use the Watson- Durbin test

for this purpose.

One more potential problem that may occur is the relationship between the dependent variable

and independent variables. For example, Froot et al. (1993) pointed out that the more valuable

the firm’s investment opportunities, the more attractive risk management becomes because

disruptions to the investment program are more costly, this lead to the endogeneity problem. To

test for this possibility, I will carry out the procedure recommend by Hausman, which involves

using the residuals with hedging as dependent and other variables such as: Firm’s size,

profitability, leverage, CAPEX, dividends, diversified as exogenous variables. However, since

fixed effects test allows for heterogeneity then Hausman test for endogeneity will not be

performed.

Detection of heteroscedasticity

The Goldfeld Quandt is based on splitting the total sample of length T into two sub- samples of

length 𝑇1and 𝑇2 . The regression model is estimated on each sub-sample and the two

residual variances are calculated as 𝑠12= �̂�1

´ �̂�1 / (𝑇1-k) and

𝑠22= �̂�2

´ �̂�2 / (𝑇2-k) respectively. The null hypothesis is that the variances of the disturbances are

equal, which can be written as 𝐻0: 𝜎12 = 𝜎2

2, against a two- sided alternative. If we reject the null

hypothesis then we can conclude that our model contain heteroscedasticity problem i.e. the

variances of the error terms are not constant.

Detecting autocorrelation

As mentioned earlier the Durbin- Watson (DW) is a useful test for detecting the first order

autocorrelation i.e. it tests only for a relationship between an error and its immediately previous

value. The test equation is:

𝑢𝑡= 𝜌𝑢𝑡−1+ 𝑣𝑡

Where 𝑣𝑡~ N (0, 𝜎𝑣2), the DW test statistic has as its null and alternative hypotheses are:

26

𝐻0: 𝜌= 0 and 𝐻1= 𝜌≠ 0

If 𝜌≠ 0, we can reject the null and conclude that there is evidence of a relationship between

residuals i.e. correlation.

After I run Goldfeld Quandt test for heteroscedasticity and Durbin-Watson for autocorrelation to

make sure that there are no errors in the collected data. The next step is to estimate an OLS

model for testing hedging premium based on the following equation:

Log(Tobin’s Q) = c+ 𝛽1*hedging + 𝛽2*leverage + 𝛽3*CAPEX + 𝛽4*profitability + 𝛽5*size +

𝛽6*dividend +𝛽7*diversifie

3.5 LIMITATION

The first limitation in methodology is due to the time constraint and difficulties in gathering

complete data set, I will exclude some variables that can affect firm value such as:

NETPOSITION and FOREIGN, though two variables may have significant impact on firm

value. The variable NET Position is defined as the sum of absolute of the net position in each

currency (expressed in units of home currency scaled by total assets. FOREIGN is the ratio of

Foreign Sales to Total Sales. Previous studies showed that these variables impact firm value

since they connect directly to the currency risks (Jankengard, 2015).

The second limitation is the univariate tests will be excluded from this study since even if

univariate tests show hedging variable significant when the multivariate tests do not then a

conclusion cannot be drawn based on univariate tests. Hence, because of the time shortage, only

multivariate tests are performed.

27

4. RESULTS AND ANALYSIS

This chapter will present the results of the statistical tests and the OLS regression analysis. Since

there may be another alternative explanation for the ordinary OLS, I also consider the

robustness of the result and the re-estimation of the model is also presented at the end of the

chapter.

4.1 EMPIRICAL FINDINGS

4.1.1 STATISTICAL TEST

For Goldfeld Quandt test: The t- statistic is 2, 72 and the P- value is 0,000, we can conclude that

there is no evidence for the presence of heteroscedasticity. For Durbin- Watson (DW) Test: the

Test- statistic is 1, 46 indicating that there is no autocorrelation between the residuals since

theoretically speaking, if DW is close to 2, we can assume that there is no evidence of

autocorrelation (Brooks, 2008). The results of the diagnostic tests signal that I can go ahead to

run OLS regression analysis.

4.1.2 HEDGING AND FIRM VALUE USING MULTIVARIATE TEST

The explanatory variables for the equilibrium test regression are CAPEX, diver, dividend, hedge,

leverage, profit and size. The dependent variable is the log of Tobin’s Q. The null hypothesis for

fixed effects is jointly zero (𝐻0 : ƞ𝑖 = 0). Since the P- value of fixed effects is 0.000 so I

reject 𝐻0 , meaning that the firm value is affected differently by the same variables

(heterogeneity).

The result of the regression analysis shows that out of seven control variables, only size and

profit are statistically significant at 5% level, telling us that size and profit affect the firm value

positively. If firm increases its profit then the value of the firm will also be rewarded with higher

value. The variable size is significant at 5% level indicating that larger firms have a stronger

tendency to have higher value than smaller firms.

28

Table 3: An OLS model of firm value

Note: t- ratios in parentheses, * and ** denote significance at the 1% and 5% levels respectively

4.1.3 ROBUSTNESS

To check the robustness of the results, the model is re-estimated using different subsamples. This

method is used to address outliner concern. One way to do this is using the Descriptive Statistics

to find out if there are many too large numbers that deviate significantly from the mean value,

then I will delete them and then re-estimate the model. There are also other concerns that need to

be taken into account. In my data sample, some of the companies such as H& M and Fingerprint

Cards AB don’t have any debts at all, so those companies should not be included in the

estimation since the t- stat for leverage may be affected. Furthermore, since the time period for

the data is from 2005- 2010, due to the severe down turn in the economy because of the financial

crisis; some of the companies in the data sample do not have dividend payments continuously.

Some of them cut the dividends between years 2008 and 2009. Therefore, I also exclude those

companies in order to avoid robustness in the dividend variable.

C 0,47

(0,22)

CAPEX 0,05

(1,51)

DIVER – 0,06

(2,14)

DIVIDEND 0,04

(0,116)

HEDGE 0,04

(0,93)

LEVERAGE – 0,54

(3,73)

PROFIT 0,29

(2,12)**

SIZE 0,04

(2,27)**

29

Below is the re- estimated OLS model:

Table 4: Robustness check for the impact of hedging on firm value

Note: t- ratios in parentheses, *, ** and *** denote significance at the 1%, 5% and 10% levels

respectively.

After re-estimate the model I get a slightly different result. The coefficients for the seven control

variables have different signs, suggesting a different effect on the dependent variable. For

instance: the control variables for diversified (diver) and leverage have the negative sign (though

diver is not statistically significant) meanwhile leverage is statistically significant at the 5%

level.

One more difference that can be observed here is that the variable dividend is significant at 10 %

level.

The control variables CAPEX, hedge and diver are not statically significant.

C 0,6

(1,31)

CAPEX 0,45

(1,59)

DIVER – 0,04

(2,07)

DIVIDEND 0,013

(0,42)***

HEDGE 0,58

6,9

LEVERAGE – 0,4

(1,9)**

PROFIT 1,79

(2,56)**

SIZE 0,36

(2,19)**

30

4.2 ANALYSIS OF THE FINDINGS

The finding indicates that there is no relationship exists between hedging and firm value since

the variable hedging is insignificant, although the coefficient of this test variable is positive. This

finding is in contrast to some studies in the literature (Allayannis & Weston, 2001; Jankengard,

2015). The time panel, which this study cover is from 2005 to 2010 and intuitively one might

expect that the risk management program would be considered more valuable during the crisis.

As a well known fact that, since Sweden is an export dependency country and the fact that the

macro condition is quite favorable for Sweden in term of a weakened Krona against major

currencies such as USD and EUR. For instance, in 2009 the averages for these exchange rates

versus SEK were 11% and 13% above their average for 2006- 2008, respectively (Jankengard,

2015). Previous research (Smith & Stulz, 1985; Bartram, 2000; Aretz, Bartram & Dufey, 2007)

supports the value maximization theory, in which managers engage in risk management in order

to secure the future cash flows, especially when the managers’ compensation is tied to the

performance of the firms. As a consequence of the financial crisis, we should not rule out the

probability that the profits Swedish firms gained from net- export due to a weakened Krona can

impair the effect of derivatives usage (the coefficient of test variable hedging is positive, we can

assume that hedging impacts firm value positively but nonetheless, we can not prove a

significant relationship). This theory is also consistent with the findings of Geczy, Minton and

Schrand (1997), suggesting that the potential benefits of using currency derivatives depend on

the firm’s exposure to foreign exchange- rate risk. They find that firm characteristics related to

these costs and benefits are related to how firm forecast its future cash flows. If the forecast is

accuracy, indicating higher profitability then firm has less incentive to hedge.

The variable leverage is significant at 5% level, and the negative sign of variable indicates that if

a firm has less debt (leverage) its value will increase more. This result is expected since an

increase in debts leads to higher distress costs (Aretz, Bartram & Dufey, 2007). Previous studies

have shown that highly leveraged firm lose substantial market share to more conservatively

financial competitors in industry down turns. A similar decline also takes place in the market

value of equity (Opler & Titman, 1994; Ogden, Jen & O’Connor, 2003). Smith and Stulz (1985)

31

also pointed that a firm’s high level of debt is one of the main reasons mangers choose to hedge

if corporate risk management ensures that firm’s future cash flow will be secured.

Dividend variable is statistically significant at 10% level, and it tells us that whether the firm

pays dividend or not will affect its value. This result is consistent with what is found in Jin and

Jorison (2006), that dividend payouts may be viewed as a positive signal from management since

it signals to the market that the firm in question is in a good financial shape, and in turn the

investors reward the firm with higher valuation.

Size is statistically significant at 5% level, indicating that larger firms tend to have higher value.

This result is consistent with what is found in Allayannis and Weston (2001), which states that

the size of the firm leads to higher accounting profitability. However, the positive correlation

between size and firm value is inconsistent with that of Bodnar, Tang and Wientrop (1999),

according to the findings of this study, bigger firms are, the more multinational they are and

when they do business in more than country, efficient and effectiveness are likely to become low

due to the lack of corporate governance. This problem has been mentioned many times in

corporate finance theory as principal and agency problem (Grossman & Hart, 1983). This is to be

said, the shareholders’ value maximization goal may differ from the managers’ objectives

leading to less firm value.

The variable profit is significant at 5 %, indicates a positive correlation between profit and firm

value. The influence of profitability on firm value has long been discussed in the literature

(Modigliani & Miller, 1958; Myer, 1984). An increased firm value due to a higher profitability is

related to the pecking order theory (Myer, 1984) which states that when a firm has a need for

capital to invest in some attractive projects, the optimal choice for firm is to fund the project with

its internal fund (cash) since external financing (issuing debt or equity) can be costly due to

information asymmetry. Therefore, higher profitability makes firm less vulnerable for external

funds. Haugen and Baker (1996); Yang et al. (2010); Chen and Chen (2011) also proved that the

greater is the firm’s profit, the more distributable earnings there are for shareholders, and hence

the expected firm value will be higher.

32

5. CONCLUSION

This project research studies the impact of hedging on firm value using a sample of 90 Swedish

companies listed on the Stockholm Stock Exchange from 2005 through 2010. I examine whether

the act of hedging is rewarded by investors with a higher market valuation.

Using Tobin’s Q as an approximation for firm market value and hedging as a control variable, I

found insignificant evidence that the usage of hedging impacts firm value positively. However, I

found evidence about other factors such as: dividend, leverage, firm size and profitability affect

the firm value differently. Leverage has a negative impact (the coefficient is negative), indicates

that the higher the debt level in the firm’ capital structure the less valuable firm is, while other

variables such as: firm size, profitability, and dividend affect firm value positively.

Recently, the relationship between hedging and firm value has been studied extensively, and this

research report is supposedly contribute to a better understanding of the risk management

program. There an important implication from these findings that is the link between hedging

and firm value does not support the notion that hedging increase firm value. Consequently,

managers need to evaluate and consider whether to participate in the corporate risk management

program. However, due to the mixed result of whether hedging can impact firm value positively,

more research in this area is necessary before we can draw a firm conclusion about the impact of

hedging on firm value.

33

6. REFERENCES

Ahmed, H., Azevedo, A. & Guney, Y. (2010) “The effect of Hedging on Firm Value and Performance:

Evidence from the Nonfinancial UK Firms”, Working Paper, Hull University Business School

Aliaga, M. & Gunderson, B. (2000) “Interactive Statistics”, Saddle River

Allayannis, G. & Weston, P. J. (2001) “The Use of Foreign Currency Derivatives and Firm Market

Value”, The Review of Financial Studies, Vol.14 No.1 243- 276

Antwi, S., Mills, E. & Zhao, X. (2012) “Capital Structure and Firm Value: Empirical Evidence from

Ghana”, International Journal of Business and Social Science, Vol. 3, No. 22

Aretz, Bartram & Dufey. (2007) “Why hedge? Rationales for corporate hedging and value

implications”, The Journal of Risk Finance, Vol.8 No.5 pp. 434-449

Asquith, P. & David, M. (1986) “Equity issues and offering dilution”, Journal of Financial Economics

15, 61–89

Bartram, S. M. (2000) “Corporate risk management as a lever for shareholder value creation”,

Financial Markets, Institutions and Instrument, Vol.9 No.5 pp. 279- 324

Bodnar, G.M, Tang, C. & Weintrop, J. (1999) “Both Side of Corporate Diversification: The

Value Impact of Geographic and Industrial Diversification”, Working Paper, John Hopkin

University

Bolton, M., Chen, H. & Wang, N. (2001) “A Unified Theory of Tobin’s q, Corporate Investment,

Financing, and Risk Management”, The Journal of Finance Vol. LXVI, No 5

Brooks, C. (2008) “Introductory Econometrics for Finance”, Cambridge University Press,

Cambridge, UK

Chen, J. & Chen, Y. (2011) “The Influence of Profitability on Firm Value with Capital Structure

as the mediator and Firm Size and Industry as Moderators”, Investment Management and

Financial Innovations, Vol. 8, No. 3

34

Dufey, G. & Srinivasulu, S.L. (1983) “The case for corporate management of foreign exchange

risk”, Financial Management, Vol. 12 No. 4, pp. 54-62.

Fama, F.E. & French, R.K. (2004) “The Capital Asset Pricing Model: Theory and Evidence”,

Journal of Economic Perspective Vol. 18, no. 13

Fauver, L. & Naranjo, A. (2010) “Derivative usage and firm value: The influence of agency

costs and monitoring problems”, Journal of Corporate Finance, Vol. 16, pp. 719- 735

Gay, D. G. & Nam, J. (1998) “The Underinvestment Problem and Corporate Derivatives Use”,

Financial Management, Vol. 27, No. 4, pp. 53- 69

Geczy, C., Minton, B. & Schrand, C. (1995) “Why Firms Use Derivatives Distinguishing among

Existing Theories”, working paper, Wharton Business School, University of Pennsylvania

Grossman, S. & Hart, O. (1983) “An Analysis of the Principal- Agent Problem”, Journal of The

Econometric Society, Vol. 51, No. 1 pp.7-45

Guay, W. & Kothari, S. P. (2002) “How much do Firms Hedge with Derivatives?”

Hagelin, N. (2003) “Why firms hedge with currency derivatives: An examination of transaction

and translation exposure”, Applied Financial Economics, Vol. 13 pp. 55-69

Haugen, R. A. & Baker, N. L. (1996) “Commonality in the determinants of expected stock

returns”, Journal of Financial Economics, Vol. 41, pp. 401- 439

Haushalter, D. (2000) “Financing Policy, Basic Risk, and Corporate Hedging: Evidence from Oil

and Gas Producers”, Journal of Finance¸ Vol. LV, No.1

Hausman, J. & Taylor, W. (1981) “Panel Data and Unobservable Individual Effects”,

Econometrica, 49, pp.1377- 1398

Hayashi, F. (1982) “Tobin’s Marginal q and Average q: A Neoclassical Interpretation”,

Econometrica, Vol.50, No.1, pp. 213-224

Jankengård, H. (2015) “Does Centralisation of FX Derivative Usage Impact Firm Value?”,

35

European Financial Management Vol.21, No.2 pp. 309-332

Jensen, M. (1896) “Agency Costs of Free Cash Flow, Corporate Finance and Takeovers”,

American Economic review, Vol. 76 pp. 323-329

Jin, Y. & Jorion, P. (2006) “Firm Value and Hedging: Evidence from U.S Oil and Gas

Producers”, The Journal of Finance, Vol. LXI

Kale, J.R. & Noe, T.H. (1990) “Corporate hedging under personal and corporate taxation”,

Managerial and Decision Economics, Vol.11, No.3, pp.199- 205

Kane, A, Lee, Y. & Marcus, A. (1984) “Earnings and Dividend Announcements: Is there a

Corroboration Effect?”, The Journal of Finance, Vol. 39, No.4 pp. 1091-1099

Modigliani, F. & Miller, M. (1958) “The cost of Capital, Corporation Finance and The Theory of

Investment”, The American Economic Review, Vol. XLVIII, No. 3

Murdoch, A. (1992) “Dividends and earnings: Their effect on firm value”, working paper,

University of Washington

Myers, S. C. (1984) “The Capital Structure Puzzle”, Journal of Finance, Vol. 39, pp. 575- 592

Ogden, J.P., Jen, F.C. & O’Connor, P. F. (2003) “Advanced Corporate Finance: Policies and

Strategies”, Prentice Hall

Opler, T. & Titman, S. (1994) “Financial Distress and Corporate Performance”, The Journal of

Finance, Vol. 49, No. 3 pp. 1015- 104

Rothschild, M. (1985) “Asset Pricing Theories”, Technical Working Paper, No.44

Scholes, M. (1972) “The marker for securities: Substitution versus price and the effects of

information of share prices”, Journal of Business, Vol. 45 pp.179-211

Smith, W.C., & Stulz (1985) “The Determinants of Firms’ Hedging Policies”, Journal of

Financial and Quantitative Analysis, Vol.20, No.4

36

Stulz, R. (1996) “Rethinking Risk Management”, Journal of Applied Corporate Finance, Vol. 9,

No.3 pp. 8-25

Warner, J. (1977) “Bankruptcy costs: Some Evidence”, Journal of Finance, Vol.32 pp.337- 348

Williamson, O. (1970) “Corporate Control and Business Behavior: An Inquiry into the Effects of

Organizational Form on Enterprise Behavior”, Prentice Hall, Englewood Cliffs, N.J.

Yang, C.C., Lee, C.F., Gu, Y.X. & Lee, Y. W., (2010) “Co-determination of Capital structure

and Stock Returns- A LISREL approach: An Empirical Test of Taiwan Stock Market”, The

Quarterly Review Of Economics and Finance, Vol. 50, pp. 222- 233

Website: www.ourcommunity.com.au (n.d)

37

7. APPENDIX

1, Heteroskedasticity Test: Breusch-Pagan-Godfrey

F-statistic 2.722032 Prob. F(7,424) 0.0000

Obs*R-squared 31.24230 Prob. Chi-Square(7) 0.0001

Scaled explained SS 33.13285 Prob. Chi-Square(7) 0.0000

Test Equation:

Dependent Variable: RESID^2

Method: Least Squares

Date: 05/07/15 Time: 17:39

Sample: 1 432

Included observations: 432

Variable Coefficient Std. Error t-Statistic Prob.

C -0.001152 0.048089 -0.023950 0.9809

CAPEX -0.006146 0.014176 -0.433550 0.6648

DIVER 0.015551 0.011865 1.310685 0.1907

DIVIDEND 0.022842 0.012749 1.791653 0.0739

HEDGE 0.023055 0.015709 1.467665 0.1429

LEVERAGE -0.162921 0.037059 -4.396251 0.0000

PROFIT -0.312874 0.123396 -2.535526 0.0116

SIZE 0.010867 0.006537 1.662204 0.0972

R-squared 0.072320 Mean dependent var 0.078686

Adjusted R-squared 0.057005 S.D. dependent var 0.116893

S.E. of regression 0.113512 Akaike info criterion -1.495463

Sum squared resid 5.463274 Schwarz criterion -1.420122

Log likelihood 331.0201 Hannan-Quinn criter. -1.465719

F-statistic 4.722032 Durbin-Watson stat 1.459300

Prob(F-statistic) 0.000040

2, Fixed effects

Redundant Fixed Effects Tests

Equation: Untitled

38

Test period fixed effects

Effects Test Statistic d.f. Prob.

Period F 12.498058 (5,497) 0.0000

Period Chi-square 60.402435 5 0.0000

Period fixed effects test equation:

Dependent Variable: TOBQ_LOG

Method: Panel Least Squares

Date: 05/07/15 Time: 15:43

Sample: 2005 2010

Periods included: 6

Cross-sections included: 90

Total panel (balanced) observations: 540

Variable Coefficient Std. Error t-Statistic Prob.

C 0.471898 0.094883 0.215400 0.0003

HEDGE 0.039482 0.032605 0.930910 0.2265

SIZE 0.036493 0.013542 2.274756 0.0043

PROFIT 0.293954 0.309939 2.121648 0.0407

LEVERAGE -0.537268 0.084558 3.725165 0.0000

CAPEX 0.046357 0.035421 1.511065 0.1122

DIVIDEND 0.042698 0.029954 0.115906 0.6718

DIVER -0.056292 0.027103 2.136967 0.5383

Redundant Fixed Effects Tests

Equation: Untitled

Test period fixed effects

Effects Test Statistic d.f. Prob.

Period F 12.498058 (5,497) 0.0000