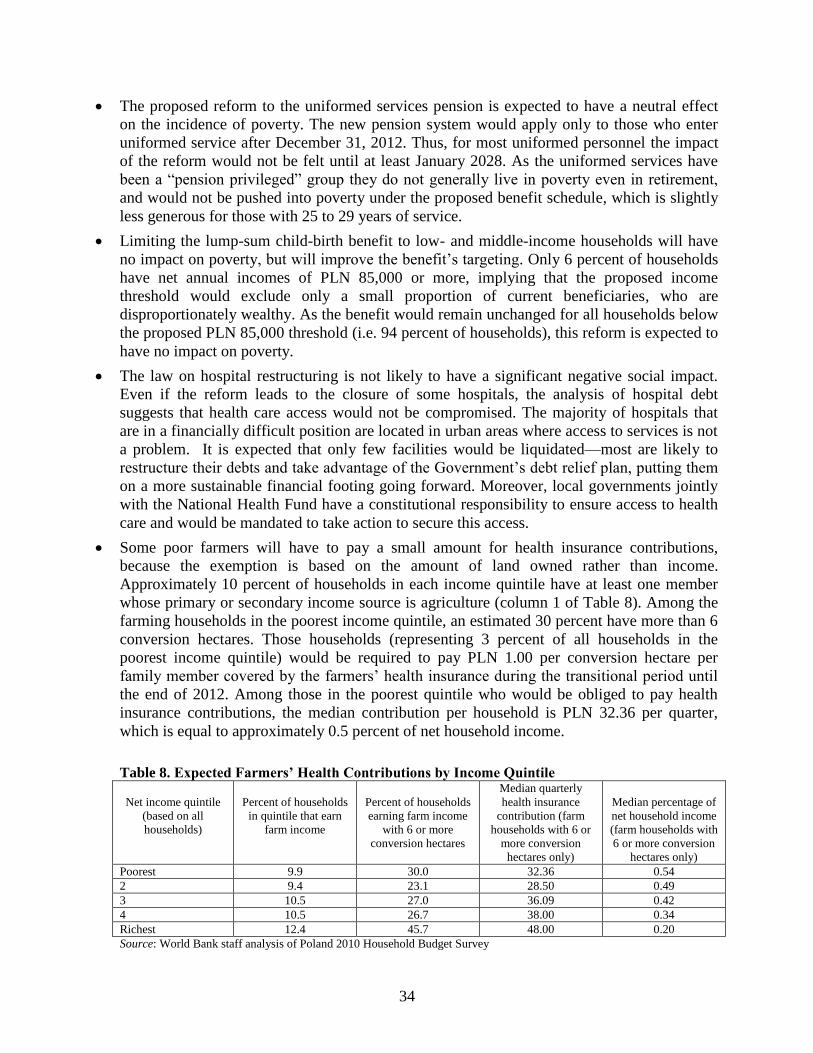

Embed Size (px)

Citation preview

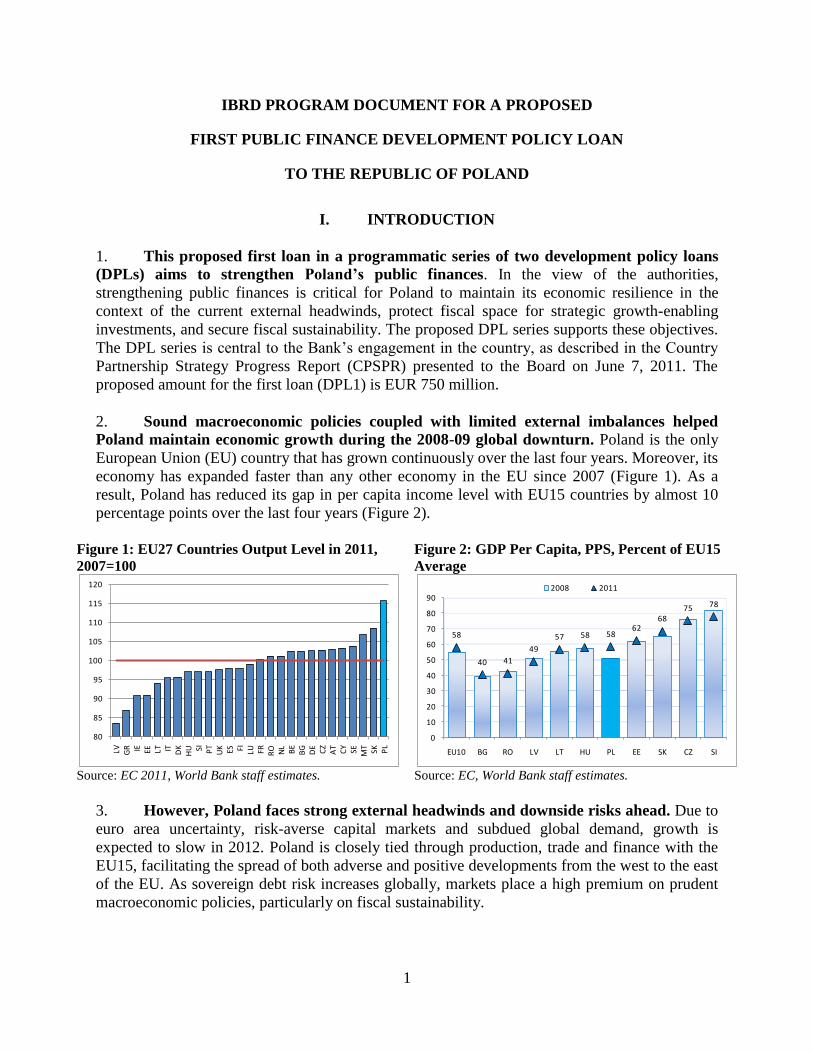

i

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 68697-PL

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

PROGRAM DOCUMENT

ON A PROPOSED LOAN

IN THE AMOUNT OF EURO 750.0 MILLION

(US$991.4 MILLION EQUIVALENT)

TO THE REPUBLIC OF POLAND

FOR THE

FIRST PUBLIC FINANCE DEVELOPMENT POLICY LOAN

May 21, 2012

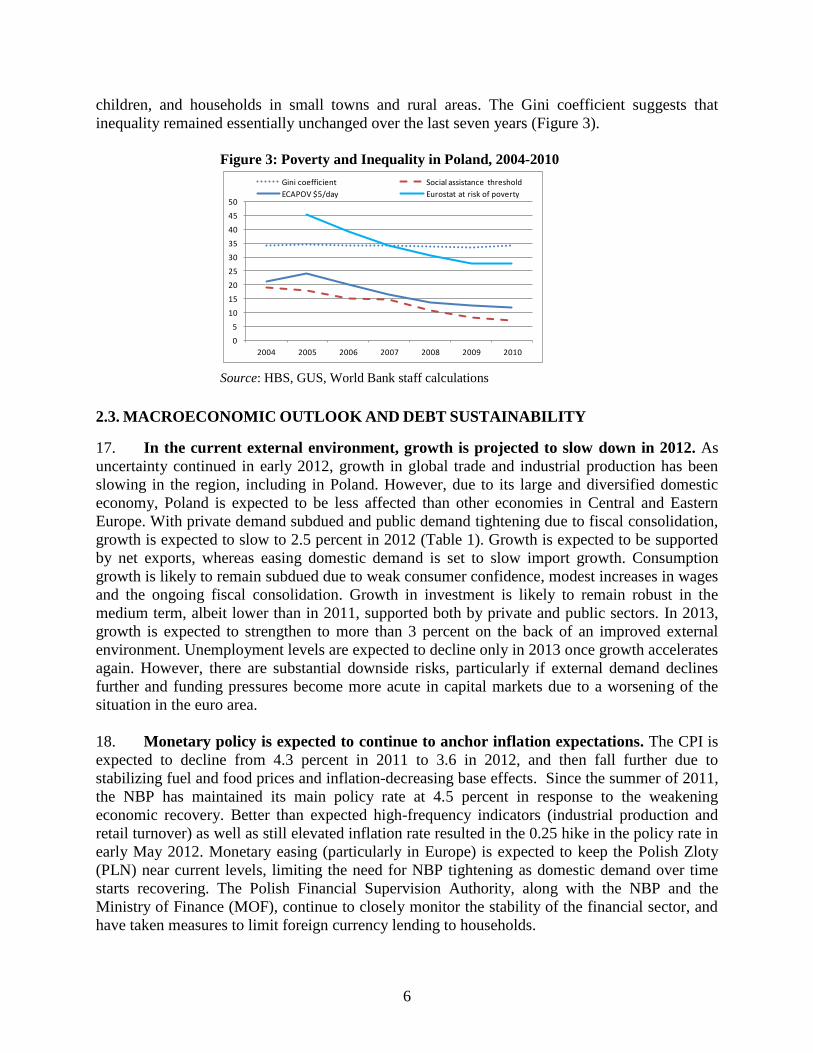

Poverty Reduction and Economic Management

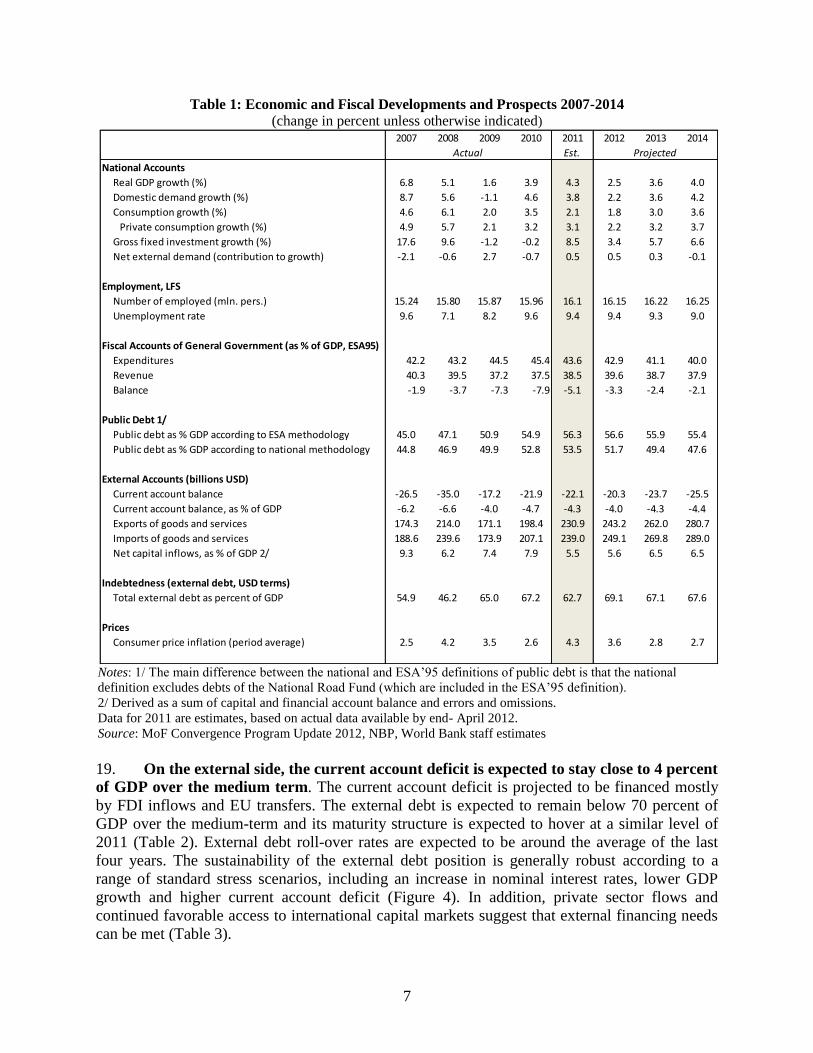

Europe and Central Asia Region

This document has a restricted distribution and may be used by recipients only in the performance

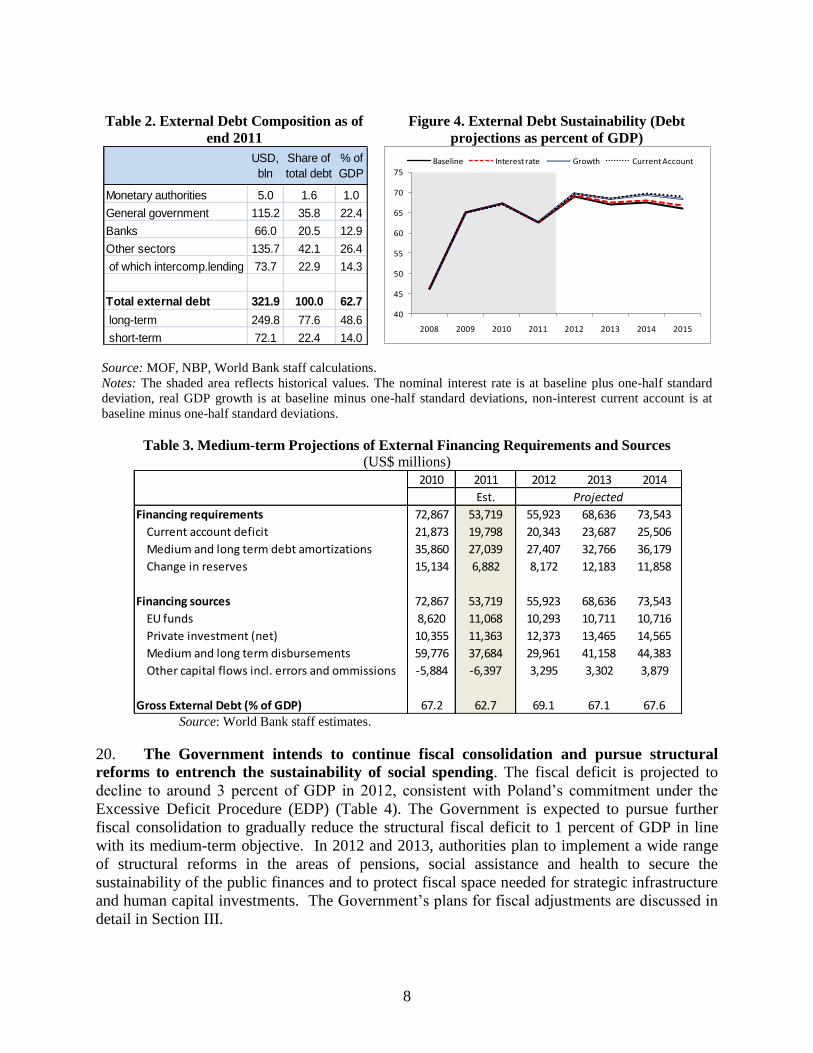

of their official duties. Its contents may not otherwise be disclosed without World Bank

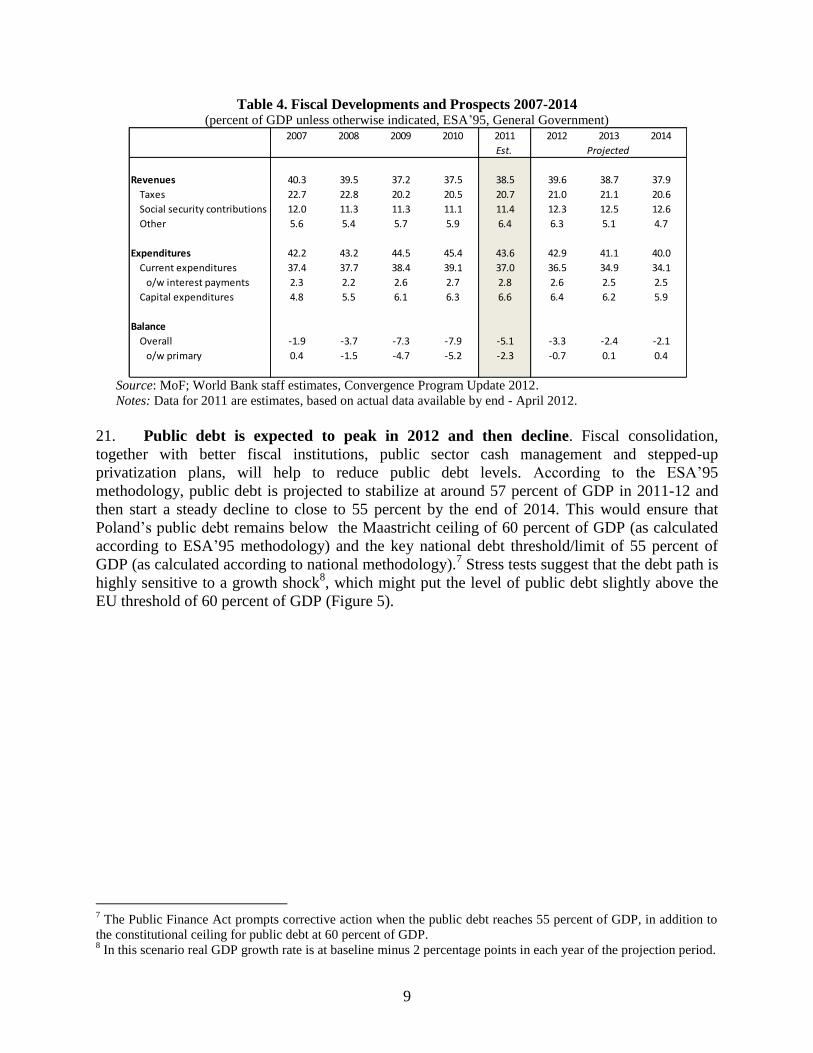

authorization.

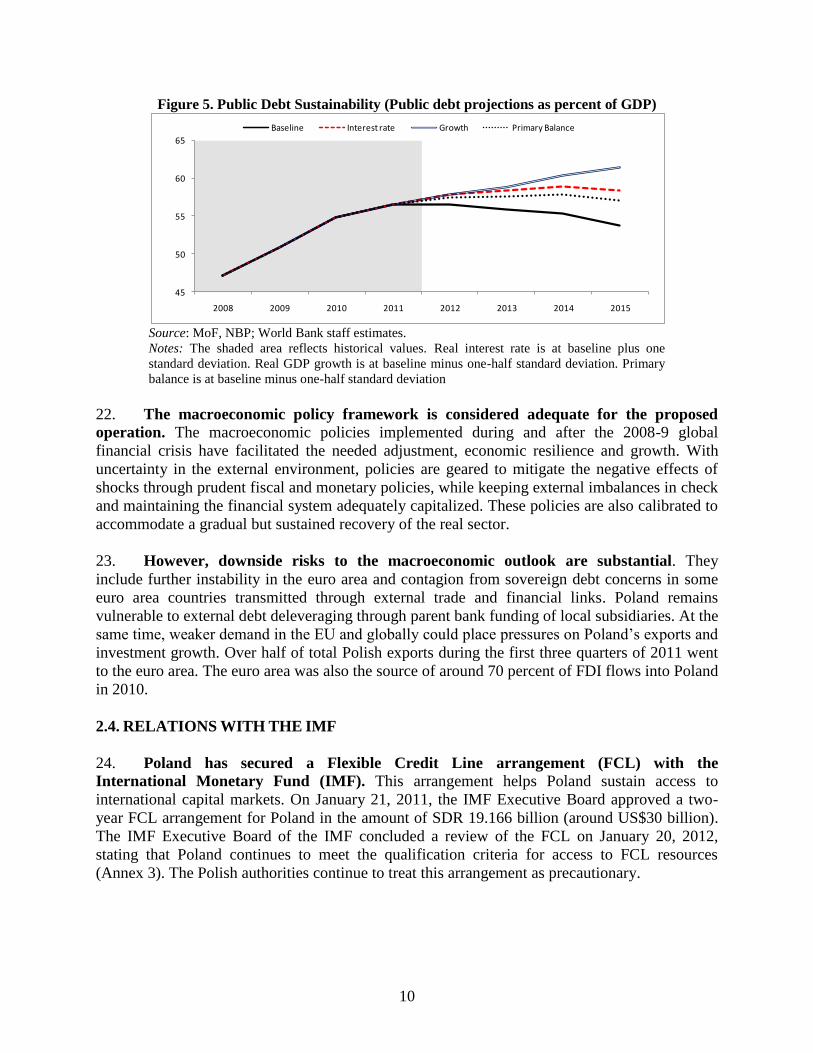

Pub

lic D

iscl

osur

e A

utho

rized

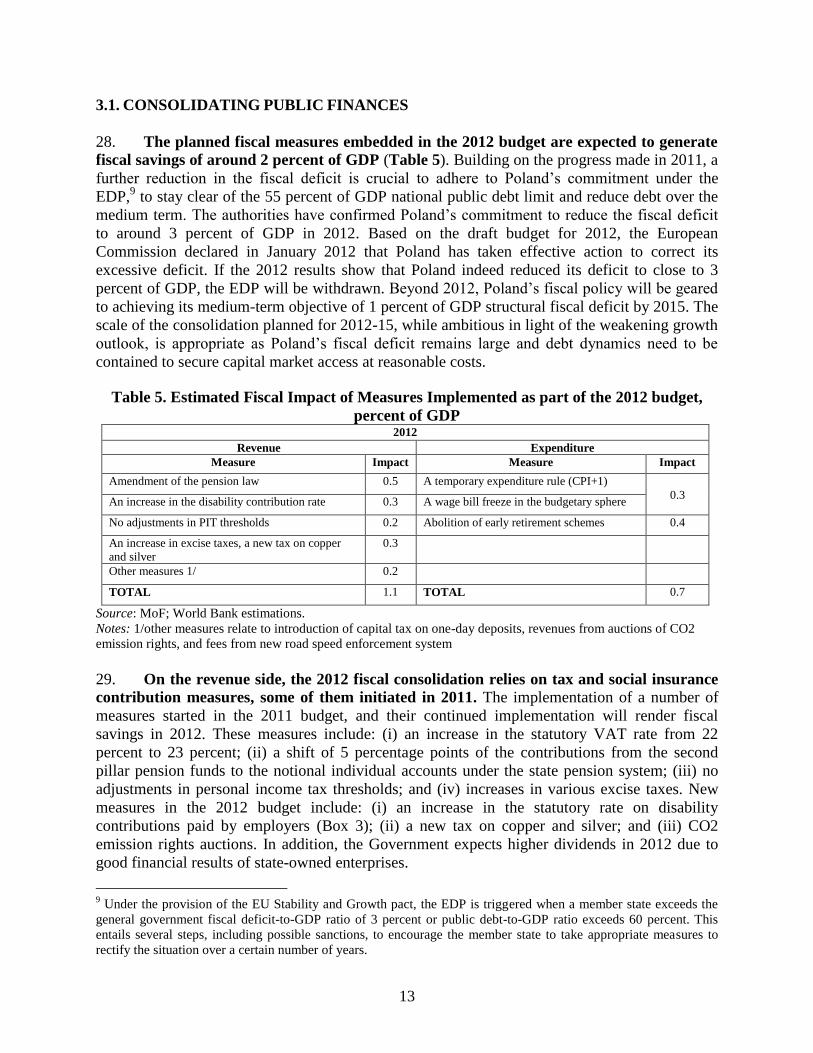

Pub

lic D

iscl

osur

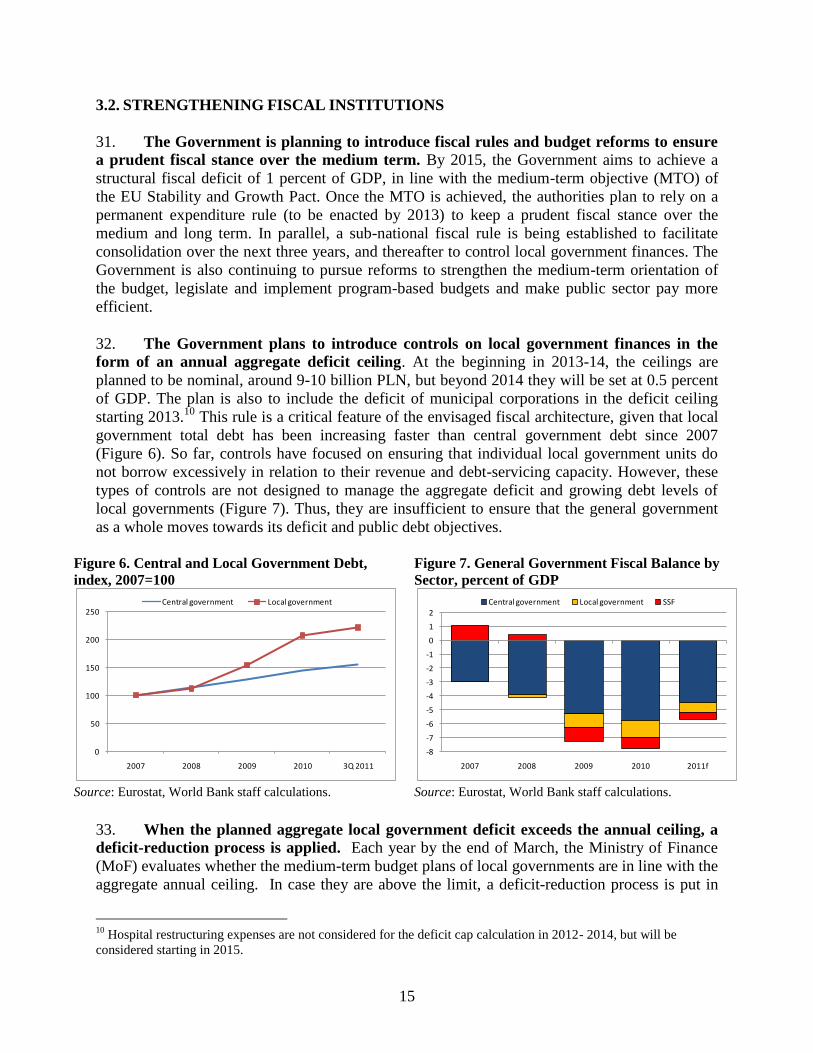

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

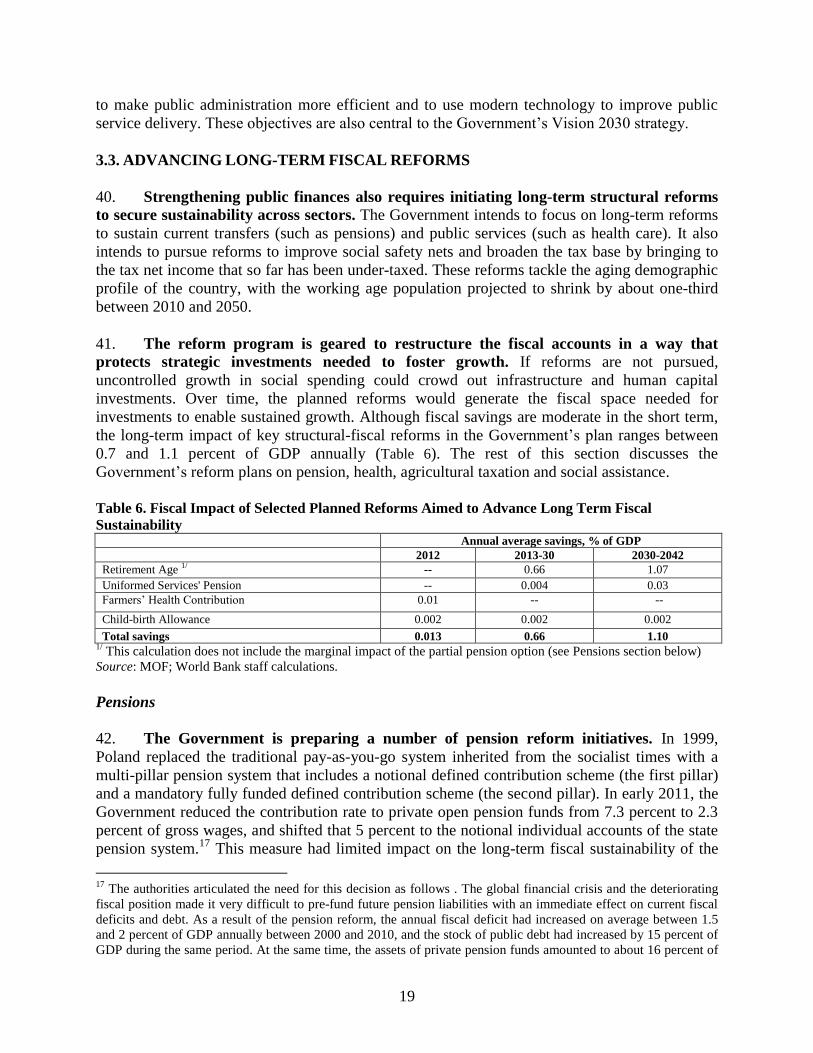

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

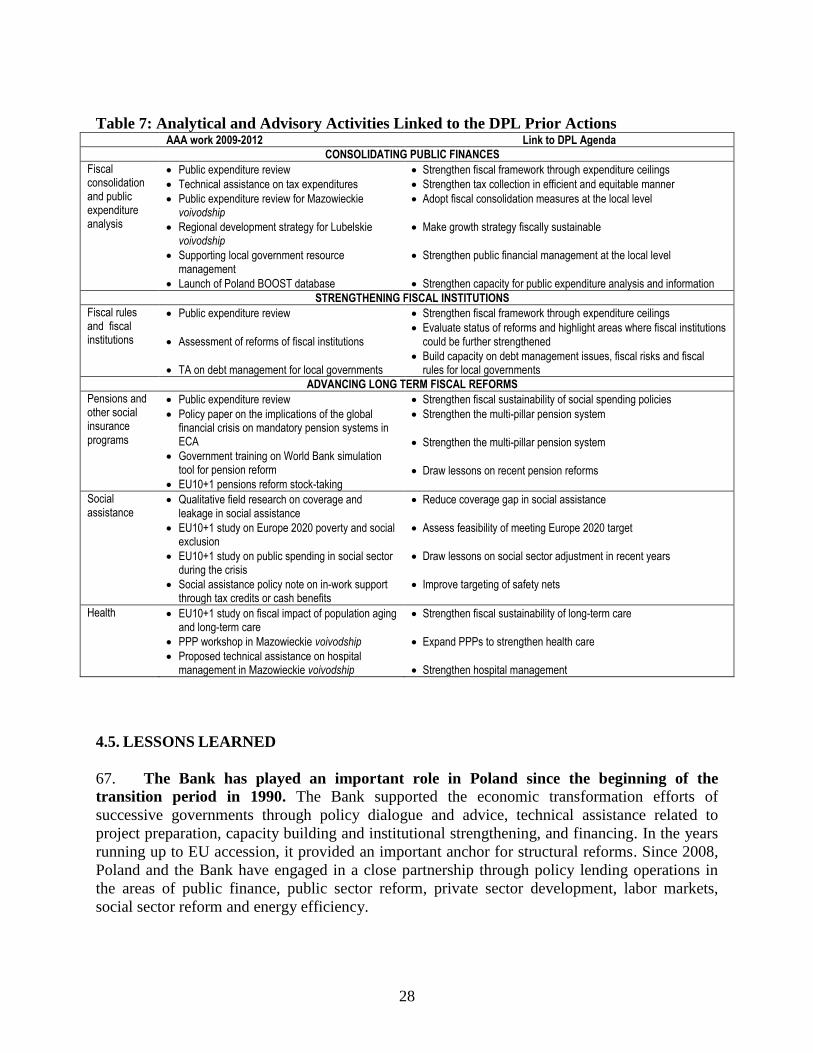

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

ii

REPUBLIC OF POLAND

CURRENCY EQUIVALENTS

(Exchange Rate Effective as of March 28, 2012)

EUR 1.00: USD 1.332: PLN 3.1867

ABBREVIATIONS, ACRONYMS & TERMS

AAA Analytic and Advisory Activities

CP Convergence Program

CPI Consumer Price Index

CPS Country Partnership Strategy

CTC Child Tax Credit

DC Defined Contribution

DPL Development Policy Loan

EC European Commission

ECA Europe and Central Asia Region

ECB European Central Bank

ERM2 Exchange Rate Mechanism (2nd

phase)

ESA European System of Accounts

ESF European Social Fund

EU European Union

FCL Flexible Credit Line

FDI Foreign Direct Investments

GDP Gross Domestic Product

Gmina Municipality/commune administrative

unit (2,478)

GNI Gross National Income

GUS National Statistical Office

HBS Household Budget Survey

IBRD International Bank for Reconstruction

and Development

IFIs International Financial Institutions

IMF International Monetary Fund

KNF Financial Supervision Authority

KRUS Farmers’ Insurance Fund

LFS Labor Force Survey

LM Labor Market

MIC Middle-Income Country

MLSP Ministry of Labor and Social Policy

MOF Ministry of Finance

MOH Ministry of Health

MTEF Medium-Term Expenditure

Framework

MTO Medium Term Objective

MYSFP Multi-Year State Financial Plan

NBP National Bank of Poland

NDC Notional Defined Contribution

NHF National Health Fund

NUTS Nomenclature of Territorial Units for

Statistics

OECD Organization for Economic

Cooperation and Development

OPF Open Pension Fund

PARSP Post-Accession Rural Support Project

PBB Performance-Based Budgeting

PER Public Expenditure Review

PFA Public Finance Act

PFM Public Finance Management

PIT Personal Income Tax

Powiat County administrative unit (379)

PLN Polish Zloty

PPP Public Private Partnerships

PTE Pension Fund Association

RER Regular Economic Report

SGP Stability and Growth Pact

SME Small and Medium Enterprises

TA Technical Assistance

VAT Value-Added Tax

Voivodeships Province administrative unit (16)

ZUS Social Insurance Institution

Vice President:

Country Director:

Sector Director:

Sector Manager:

Task Team Leaders:

Co-Task Team Leader:

Philippe Le Houerou

Peter Harrold

Yvonne Tsikata

Satu Kahkonen

Gallina A. Vincelette, Pablo Saavedra, Kaspar Richter

Emilia Skrok

iii

FOR OFFICIAL USE ONLY

REPUBLIC OF POLAND

FIRST PUBLIC FINANCE DEVELOPMENT POLICY LOAN (DPL1)

TABLE OF CONTENTS

LOAN AND PROGRAM SUMMARY .......................................................................... iv I. INTRODUCTION..................................................................................................... 1

II. COUNTRY CONTEXT............................................................................................ 2 2.1. POLITICAL DEVELOPMENTS ........................................................................................ 2 2.2. RECENT ECONOMIC DEVELOPMENTS ....................................................................... 3 2.3. MACROECONOMIC OUTLOOK AND DEBT SUSTAINABILITY ............................... 6 2.4. RELATIONS WITH THE IMF ......................................................................................... 10

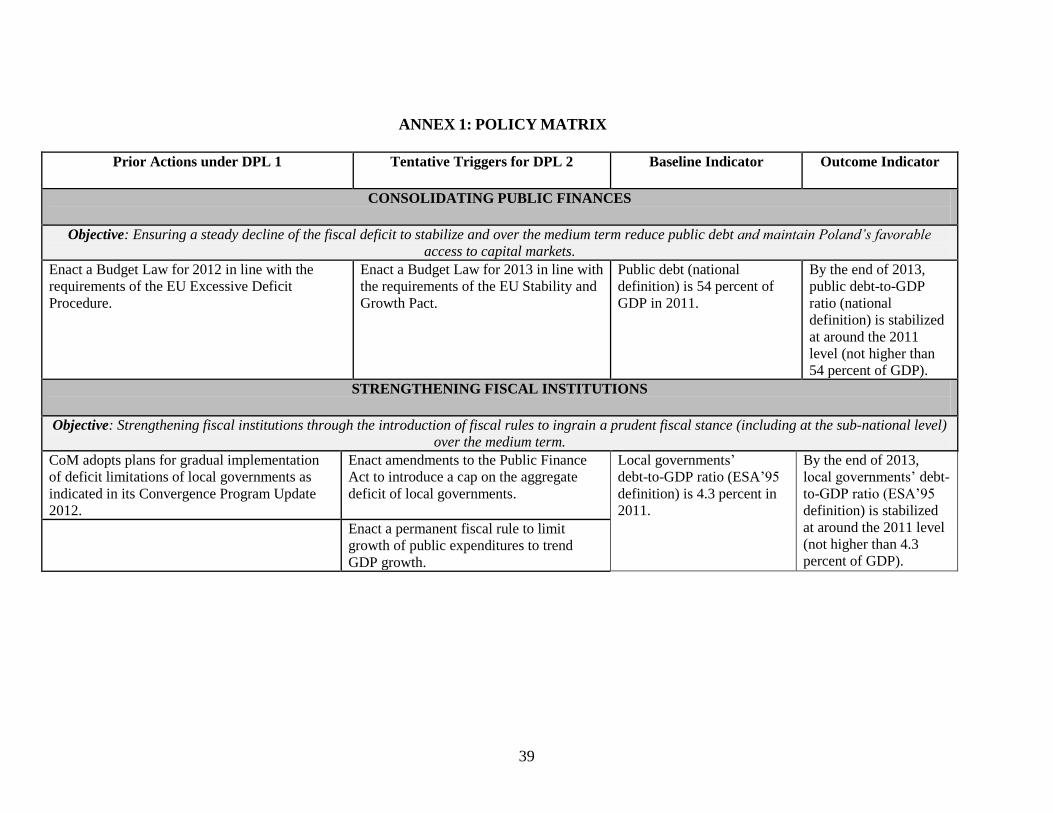

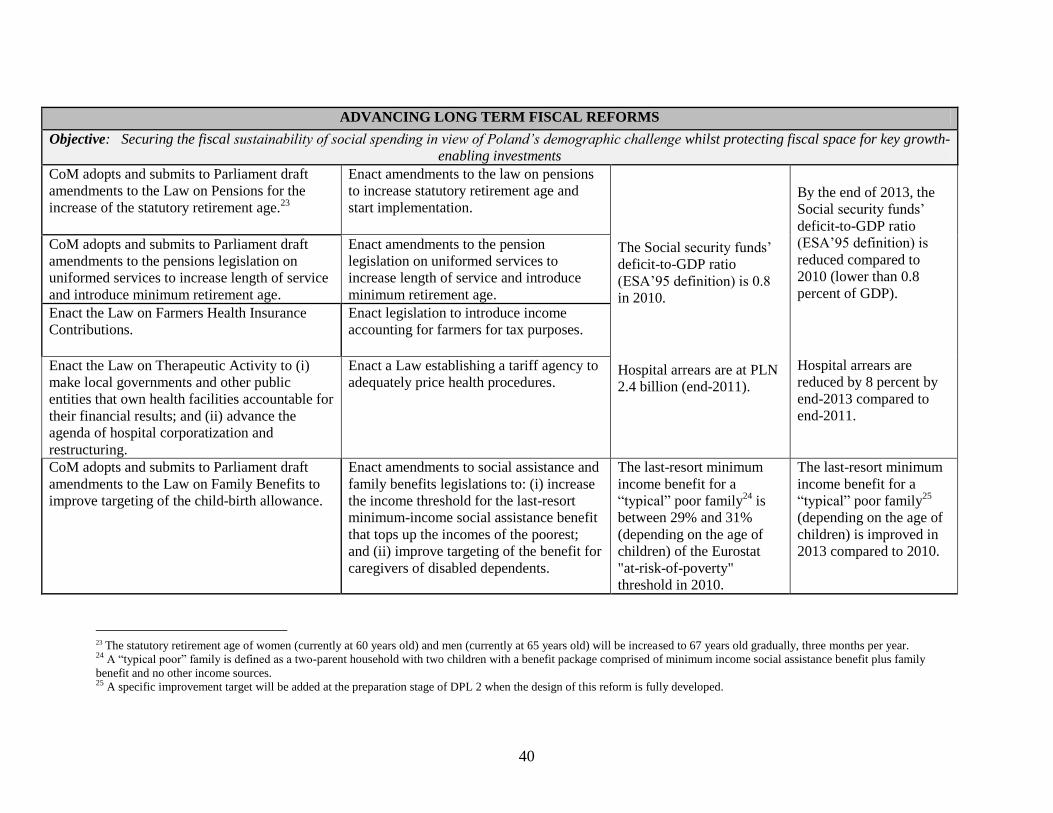

III. THE GOVERNMENT’S REFORM PROGRAM ............................................ 11 3.1. CONSOLIDATING PUBLIC FINANCES ....................................................................... 13 3.2. STRENGTHENING FISCAL INSTITUTIONS ............................................................... 15 3.3. ADVANCING LONG-TERM FISCAL REFORMS ......................................................... 19 3.4. CONSULTATIONS ........................................................................................................... 25

IV. BANK SUPPORT TO THE GOVERNMENT’S PROGRAM ........................ 26 4.1. LINK TO THE COUNTRY PARTNERSHIP STRATEGY ............................................. 26 4.2. COLLABORATION WITH THE IMF AND THE EUROPEAN COMMISSION .......... 26 4.3. RELATIONSHIP TO OTHER BANK OPERATIONS .................................................... 26 4.4. ANALYTICAL UNDERPINNINGS ................................................................................. 27 4.5. LESSONS LEARNED ....................................................................................................... 28

V. THE PROPOSED POLICY LOAN ......................................................................... 29 5.1. OPERATION DESCRIPTION .......................................................................................... 29 5.2. CONSOLIDATING PUBLIC FINANCES ....................................................................... 30 5.3. STRENGTHENING FISCAL INSTITUTIONS ............................................................... 30 5.4. ADVANCING LONG-TERM FISCAL REFORMS ......................................................... 31

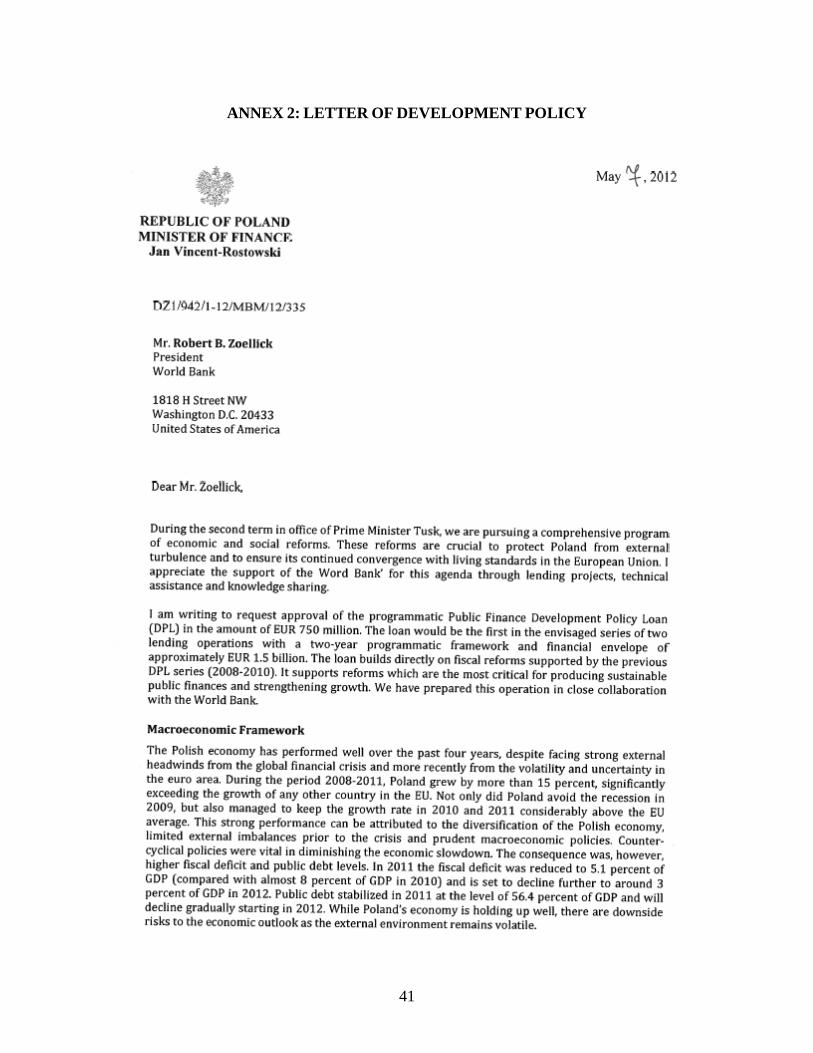

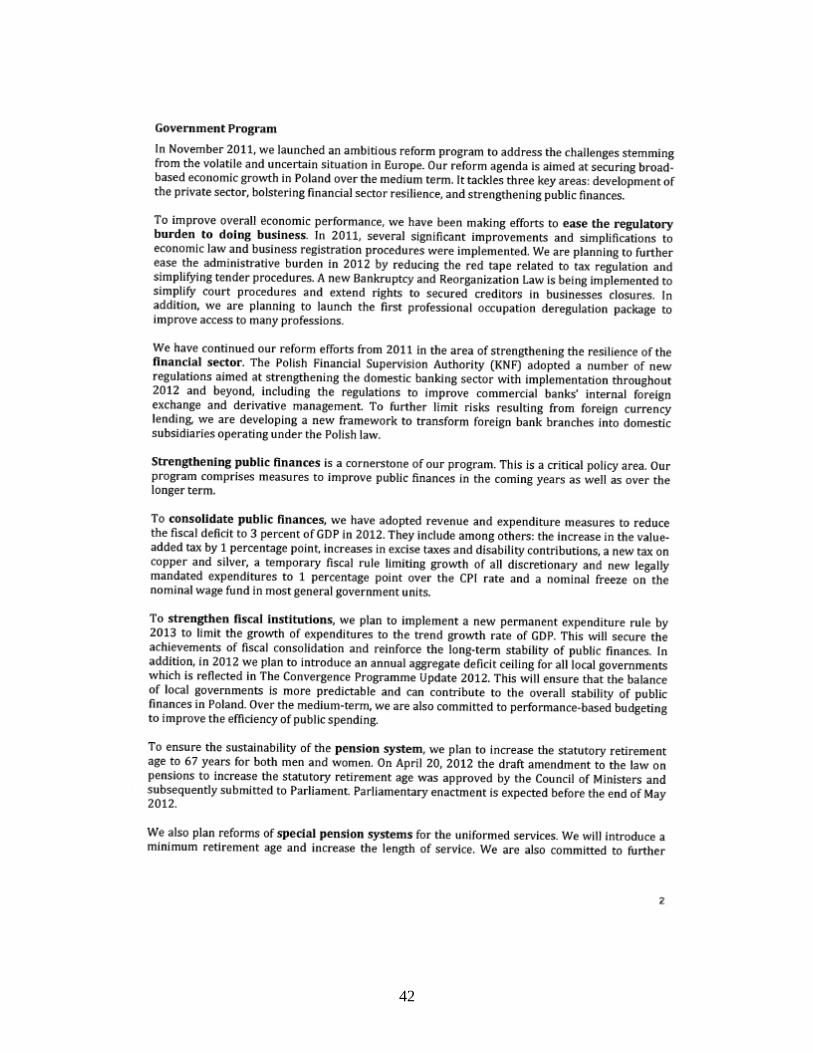

VI. OPERATION IMPLEMENTATION ................................................................ 33 6.1. POVERTY AND SOCIAL IMPACT ................................................................................ 33 6.2. ENVIRONMENTAL ASPECTS ....................................................................................... 35 6.3. IMPLEMENTATION MONITORING AND EVALUATION ......................................... 35 6.4. FIDUCIARY ASPECTS AND PROCUREMENT............................................................ 35 6.5. DISBURSEMENT AND AUDITING ............................................................................... 37 6.6. RISKS AND MITIGATION .............................................................................................. 37 ANNEX 1: POLICY MATRIX ................................................................................................ 39 ANNEX 2: LETTER OF DEVELOPMENT POLICY ............................................................. 41 ANNEX 3: IMF ASSESSMENT .............................................................................................. 44 ANNEX 4: POLAND AT A GLANCE .................................................................................... 45 ANNEX 5: MAP OF POLAND ................................................................................................ 48

This loan was prepared by an IBRD team comprising John Balafoutis, Mukesh Chawla, Agnès Couffinhal, Joseph

Formoso, Herwig Immervoll, Ewa Korczyc, Kirsten Burghardt Propst, Kaspar Richter (former TTL), Marc

Robinson, Pablo Saavedra (former TTL), Emilia Skrok (co-TTL), Kenneth Simler, Emily Sinnott, Victoria

Strokova, Anita Schwarz, Gallina A. Vincelette (TTL) and Iwona Warzecha. Malgorzata Michnowska provided

essential support.

iv

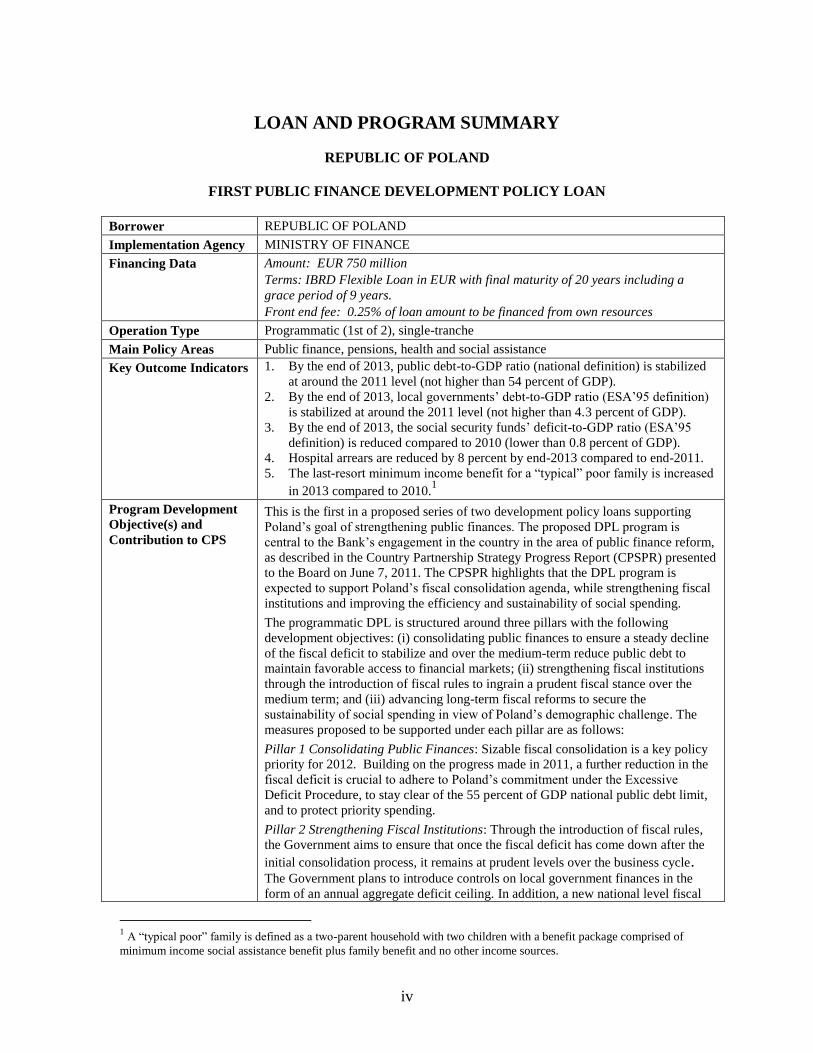

LOAN AND PROGRAM SUMMARY

REPUBLIC OF POLAND

FIRST PUBLIC FINANCE DEVELOPMENT POLICY LOAN

Borrower REPUBLIC OF POLAND

Implementation Agency MINISTRY OF FINANCE

Financing Data Amount: EUR 750 million

Terms: IBRD Flexible Loan in EUR with final maturity of 20 years including a

grace period of 9 years.

Front end fee: 0.25% of loan amount to be financed from own resources

Operation Type Programmatic (1st of 2), single-tranche

Main Policy Areas Public finance, pensions, health and social assistance

Key Outcome Indicators 1. By the end of 2013, public debt-to-GDP ratio (national definition) is stabilized

at around the 2011 level (not higher than 54 percent of GDP).

2. By the end of 2013, local governments’ debt-to-GDP ratio (ESA’95 definition)

is stabilized at around the 2011 level (not higher than 4.3 percent of GDP).

3. By the end of 2013, the social security funds’ deficit-to-GDP ratio (ESA’95

definition) is reduced compared to 2010 (lower than 0.8 percent of GDP).

4. Hospital arrears are reduced by 8 percent by end-2013 compared to end-2011.

5. The last-resort minimum income benefit for a ―typical‖ poor family is increased

in 2013 compared to 2010.1

Program Development

Objective(s) and

Contribution to CPS

This is the first in a proposed series of two development policy loans supporting

Poland’s goal of strengthening public finances. The proposed DPL program is

central to the Bank’s engagement in the country in the area of public finance reform,

as described in the Country Partnership Strategy Progress Report (CPSPR) presented

to the Board on June 7, 2011. The CPSPR highlights that the DPL program is

expected to support Poland’s fiscal consolidation agenda, while strengthening fiscal

institutions and improving the efficiency and sustainability of social spending.

The programmatic DPL is structured around three pillars with the following

development objectives: (i) consolidating public finances to ensure a steady decline

of the fiscal deficit to stabilize and over the medium-term reduce public debt to

maintain favorable access to financial markets; (ii) strengthening fiscal institutions

through the introduction of fiscal rules to ingrain a prudent fiscal stance over the

medium term; and (iii) advancing long-term fiscal reforms to secure the

sustainability of social spending in view of Poland’s demographic challenge. The

measures proposed to be supported under each pillar are as follows:

Pillar 1 Consolidating Public Finances: Sizable fiscal consolidation is a key policy

priority for 2012. Building on the progress made in 2011, a further reduction in the

fiscal deficit is crucial to adhere to Poland’s commitment under the Excessive

Deficit Procedure, to stay clear of the 55 percent of GDP national public debt limit,

and to protect priority spending.

Pillar 2 Strengthening Fiscal Institutions: Through the introduction of fiscal rules,

the Government aims to ensure that once the fiscal deficit has come down after the

initial consolidation process, it remains at prudent levels over the business cycle. The Government plans to introduce controls on local government finances in the

form of an annual aggregate deficit ceiling. In addition, a new national level fiscal

1 A ―typical poor‖ family is defined as a two-parent household with two children with a benefit package comprised of

minimum income social assistance benefit plus family benefit and no other income sources.

v

rule would limit the growth of national government expenditures to a rate not

exceeding the trend growth rate of GDP. These rules would safeguard against the re-

emergence of excessive structural budget deficits in the medium and long term.

Pillar 3 Advancing Long-Term Fiscal Reforms: Strengthening public finances also

requires Poland to initiate structural reforms across various sectors. These reforms

are focused on helping to secure the sustainability of pension transfers and public

health care services, while improving the coverage and generosity of social

assistance for the most vulnerable. In addition, introducing a regular income

accounting for farmers will enable moving to a system of regular taxation of the

agriculture sector based on income, including for the payment all social insurance

contributions over the medium term.

These policies aim to enhance Poland’s economic resilience in the face of adverse

times. These policies also aim at protecting fiscal space for key growth-enhancing

investments.

Risks This operation faces three risks: macroeconomic, financial sector and reform

implementation risks:

Macroeconomic risks stem from potential further instability in the euro area. A

severe event affecting the core and/or the periphery of the euro area could

undermine economic growth in Poland and jeopardize fiscal outcomes. The euro

area is Poland’s largest market and source for foreign investment, and as such euro

area problems could be transmitted to Poland through weaker export demand and

investment.

Financial sector risks stem from Poland’s vulnerabilities to external debt

deleveraging through parent bank funding of local subsidiaries and tighter access to

capital for firms and households. A deterioration of macroeconomic conditions

could also lead to an increase in non-performing loans.

The key mitigating factors against macroeconomic and financial sector risks include

a stepped-up utilization of EU funds and the flexibility of the exchange rate as a

shock absorber. In addition, Poland’s financial sector has demonstrated strong

fundamentals, benefitting from continued strengthening of regulation and

supervision and access to liquidity support from the European Central Bank (ECB)

and the National Bank of Poland (NBP). Lastly, the authorities could draw on the

Flexible Credit Line with the IMF, which has so far been treated as strictly

precautionary.

Reform implementation risks stem from potential public discontent with reforms.

This could reduce the Government’s political ability to implement and sustain the

needed fiscal and structural reforms. Ensuring support for the proposed reform

agenda within the coalition government will continue to be key for successful

implementation of the reforms.

Mitigating factors against this risk include: the Government’s strong electoral

mandate in recent parliamentary elections and thus the window of opportunity to

proceed with reforms prior to next general elections in 2015; the Government’s

strong commitment to strengthening public finances as articulated in the Prime

Minister’s opening speech to Parliament in November 2011; and the broadly

recognized need for fiscal reform in view of the national and EU public debt limits

and market pressures to improve fiscal balances.

Operation ID Number P127433

1

IBRD PROGRAM DOCUMENT FOR A PROPOSED

FIRST PUBLIC FINANCE DEVELOPMENT POLICY LOAN

TO THE REPUBLIC OF POLAND

I. INTRODUCTION

1. This proposed first loan in a programmatic series of two development policy loans

(DPLs) aims to strengthen Poland’s public finances. In the view of the authorities,

strengthening public finances is critical for Poland to maintain its economic resilience in the

context of the current external headwinds, protect fiscal space for strategic growth-enabling

investments, and secure fiscal sustainability. The proposed DPL series supports these objectives.

The DPL series is central to the Bank’s engagement in the country, as described in the Country

Partnership Strategy Progress Report (CPSPR) presented to the Board on June 7, 2011. The

proposed amount for the first loan (DPL1) is EUR 750 million.

2. Sound macroeconomic policies coupled with limited external imbalances helped

Poland maintain economic growth during the 2008-09 global downturn. Poland is the only

European Union (EU) country that has grown continuously over the last four years. Moreover, its

economy has expanded faster than any other economy in the EU since 2007 (Figure 1). As a

result, Poland has reduced its gap in per capita income level with EU15 countries by almost 10

percentage points over the last four years (Figure 2).

Figure 1: EU27 Countries Output Level in 2011,

2007=100

Figure 2: GDP Per Capita, PPS, Percent of EU15

Average

Source: EC 2011, World Bank staff estimates. Source: EC, World Bank staff estimates.

3. However, Poland faces strong external headwinds and downside risks ahead. Due to

euro area uncertainty, risk-averse capital markets and subdued global demand, growth is

expected to slow in 2012. Poland is closely tied through production, trade and finance with the

EU15, facilitating the spread of both adverse and positive developments from the west to the east

of the EU. As sovereign debt risk increases globally, markets place a high premium on prudent

macroeconomic policies, particularly on fiscal sustainability.

80

85

90

95

100

105

110

115

120

LV GR IE EE LT IT DK

HU SI PT

UK ES FI LU FR RO NL

BE

BG

DE CZ

AT

CY

SE MT

SK PL

58

40 41

49

57 58 5862

6875 78

0

10

20

30

40

50

60

70

80

90

EU10 BG RO LV LT HU PL EE SK CZ SI

2008 2011

2

4. To further safeguard access to capital markets and sustain the economic recovery,

authorities have made strengthening public finances a central policy objective. During

2008-10, the authorities adopted counter-cyclical fiscal and monetary policies to cushion the

impact of the slowdown and support the recovery. The general government deficit increased

from 3.7 percent of GDP in 2008 to 7.9 percent of GDP in 2010. As the recovery took hold in

2011, and in the context of a limited macroeconomic space, the Government shifted away from

supporting growth through fiscal policy and launched a fiscal consolidation strategy. A set of

expenditure and revenue measures brought the fiscal deficit down to around 5 percent of GDP in

2011. The authorities plan to continue a gradual path of deficit reduction that does not hamper

the recovery. Policies and reforms are geared to reduce the structural fiscal deficit to 1 percent of

GDP by 2015 to stabilize and (over the medium term) reduce public debt, build strong fiscal

institutions, and establish a foundation for long-run fiscal sustainability and growth.

5. At the request of the Polish authorities, the DPL series is designed to support this

Government’s objective. The DPL support is focused on three critical policy areas. First, fiscal

consolidation is needed to rein in public debt and enhance the country’s resilience to external

shocks. Second, stronger fiscal institutions are essential to ensure that once the fiscal deficit has

come down, it remains at prudent levels over the business cycle. And third, structural and fiscal

reforms are required to secure long-term sustainability of social spending, particularly in the face

of the country’s aging population.2 The measures under these three areas are also geared to

protect fiscal space for growth-enabling investments. The authorities value the support of the

Bank through policy lending for several reasons: it embeds technical advice for reform design; it

signals the Government’s commitment to key structural reforms; it establishes a time table to

anchor the reform process; and it comes with lower transactions costs and longer maturity than

investment lending. The proposed series of two DPLs is part of the Government’s medium-term

public debt strategy.

II. COUNTRY CONTEXT

2.1. POLITICAL DEVELOPMENTS

6. Prime Minister Tusk began a second term in office in November 2011, with the next

general election scheduled for late 2015. The new coalition government, comprised of the

center-right Civic Platform (PO) party and the agrarian Polish Peasants’ Party (PSL). The ruling

coalition has a small majority in the Parliament, but faces a divided opposition. The Government

was elected with a strong mandate for reform, particularly in the areas of public finance,

financial sector stability and business climate. Prime Minister Tusk's Government is taking the

beginning of his second term in office as a window of opportunity to launch necessary, but

politically difficult reforms. In his speech to the lower house on November 18, 2011, he

announced plans to strengthen public finances as a cornerstone of the reform agenda. The

coalition has thus far remained cohesive and effective in reaching agreements among political

partners on policy reforms.

2 Poland’s working age population will decline from 27 million in 2007 to 16 million in 2060 (European

Commission 2009).

3

2.2. RECENT ECONOMIC DEVELOPMENTS

7. Poland was the only economy in the EU to avoid recession during the 2008-09 global

financial crisis. The country’s deep economic integration with Europe and other global markets

made it vulnerable to the collapse in capital flows and trade. Yet in 2009, Poland’s GDP grew by

1.6 percent, while the EU’s output declined by 4.2 percent. This performance stemmed from a

number of factors. First, Poland’s relatively large and diversified domestic economy mitigated

the negative effect of the sharp decline in global demand. Second, the country had limited

external imbalances in the years prior to the crisis. Third, adequate macroeconomic policies both

prior to and during the crisis helped to support output growth and protect the financial sector.

Monetary policy was accommodative in the context of the downturn, and automatic fiscal

stabilizers were allowed to operate. Solid banking regulation and supervision and relatively

moderate credit growth in the pre-crisis period (compared to the rest of Central and Eastern

Europe) strengthened the resilience of the financial sector.

8. Poland’s economy rebounded in 2010 and 2011, but growth is expected to slow in

2012. Real GDP growth accelerated to close to 4 percent in 2010 on the back of strong domestic

demand, improved labor market conditions and credit growth. At the same time, fiscal policy

continued to support the economy as public demand compensated for faltering private demand.

In 2011, despite a worsening external environment, financial market volatility and the launch of

fiscal consolidation, GDP growth remained strong at 4.3 percent. Good performance in industry

and construction, the absorption of EU funds and spending for the Euro 2012 soccer

championships contributed to this outcome. Growth also became more balanced in 2011, with

domestic fixed investments recovering from moderate declines in 2009 and 2010, and positive

net exports contributing in the second half of the year. The unemployment rate declined from a

peak of 10.6 percent in the first quarter of 2010 to 9.8 percent in the fourth quarter of 2011. In

late 2011, the unfavorable external environment started to weigh down Poland’s growth. Growth

in retail sales turnover eased from 16.3 percent in October 2010 to 2.1 percent in December

2011, and new orders for industry slid from 16.6 percent to 5.5 percent in the same period (year-

on-year, 3-month moving average). While this did not translate into weaker GDP growth in the

third and fourth quarters, reduced consumer and business confidence suggest that consumption,

investment and exports will be impacted by weak EU and global demand and increased risk

aversion in capital markets in 2012.

9. The current account deficit narrowed in 2011 and was financed mostly by FDI

inflows and capital transfers from the EU. The current account deficit is estimated to have

declined from 4.7 percent of GDP in 2010 to 4.3 percent of GDP in 2011, mainly due to

improvements in services and current transfers. The trade deficit is projected to have widened

somewhat in 2011 due to strong import demand—fuelled by investment and consumption—as

well as moderating export demand. Net FDI (around 1.8 percent of GDP in 2011) and EU capital

transfers (around 2.2 of GDP in 2011) covered over 90 percent of the current account deficit. As

a result of exchange rate depreciation in late 2011, the external debt-to-GDP ratio dropped to

around 63 percent of GDP (calculated in USD terms) by the end of 2011. The share of external

debt-to-GDP calculated in Polish zloty terms was around 70 percent of GDP. The share of short-

term debt in total debt dropped to around 22 percent in 2011 from around 25 percent in 2007-

2010. The level of international reserves remained broadly adequate. Although the ratio of forex

4

reserves to short-term debt plus current account deficit was around 70 percent, reserves covered

5.2 months of imports in 2011.

10. Monetary and exchange rate policies helped the adjustment in 2008-09 and

anchored inflation expectations in 2010-11. During the global financial crisis, the flexible

exchange rate facilitated the economy’s adjustment to external shocks. Monetary policy was

accommodative with cuts in policy rates and liquidity provision. Inflation pressures increased in

early 2011, fueled by higher international commodity prices, stronger domestic demand and the

increase in the statutory value-added tax (VAT) rate. In response, the Monetary Council

increased the key policy rate four times between January and June 2011, each time by 0.25

percentage points. Subsequently, the policy rate was maintained at 4.5 percent as inflationary

pressures eased. Headline inflation has already decreased from its peak of 5.0 percent in May

2011 to 4.1 percent in January 2012, but still slightly above the National Bank of Poland’s (NBP)

tolerance band of 1.5 percent to 3.5 percent.

11. The financial sector has been resilient to the shocks of the global crisis. The banking

sector has not required public support and remains well capitalized, liquid and profitable. The

solid position of the financial sector reflects: (i) strong fundamentals, such as low leverage and

high profitability of the corporate sector; (ii) lack of significant exposure to ―toxic‖ assets in both

the US and in the euro area and well-managed credit growth in the years prior the crisis; (iii)

continued improvements in regulation and supervision; (iv) continued capital and liquidity

support from international parent banks to domestic subsidiaries; and (v) the decision of several

banks to retain the majority of profits during 2008-2011 to improve capital adequacy ratios.

12. But vulnerabilities have increased and deleveraging and other risks remain. The

capital adequacy ratio at the end of 2011 was 13.1 percent, and the level of non-performing loans

(NPLs) was around 8.3 percent of assets, down from 8.8 percent in 2010. However, Poland

remains exposed to European banks. Foreign banks and branches (most of which are European)

account for about two-thirds of Poland’s banking system. In addition, the NPL nominal stock

continued growing. Further, there is still a large stock of FX-denominated loans among

unhedged borrowers, including in the construction industry. This highlights the existing

vulnerabilities of the banking sector. Thus, the authorities will need to remain vigilant about

financial sector policies to cope with these risks and those of deleveraging of local subsidiaries

of euro area banks.

13. The Government pursued counter-cyclical fiscal policies that cushioned the

slowdown in 2008-09 and supported the recovery in 2010. The general government deficit

increased from 3.7 percent of GDP in 2008 to 7.3 percent of GDP in 2009 and 7.9 percent of GDP

in 2010. The increase in fiscal imbalances resulted in a rise of public debt from 47.1 percent of

GDP in 2008 to 54.9 percent of GDP in 2010—a more moderate increase than in other EU

countries. The rise was contained by strong public debt and liquidity management, stable interest

rates due to Poland’s macroeconomic policies and stepped up privatization.

14. With the growth rebound in 2011, the Government embarked on a fiscal adjustment

path and initiated a process of fiscal consolidation. The general government deficit declined to

around 5.1 percent of GDP in 2011 (fiscal outturn proved to be better than expected by 0.5

5

percent of GDP) through a combination of revenue and expenditure measures. On the revenue

side, the main measures were: (i) a change in the pension system that shifted 5 percentage points

of the contribution from the funded second pillar to the first pillar; (ii) a 1 percentage point

increase in the VAT statutory rate; (iii) a 4 percentage point increase in excise duties on tobacco;

(iv) the abolition of VAT exemptions on company cars and fuel as well as exemptions on excise

duties on bio-fuels; and (v) no change in personal income tax thresholds. In parallel, faster GDP

growth and improved corporate income tax annual settlements3 aided revenue growth. On the

expenditure side, the growth in government spending was contained by: (i) a temporary fiscal

rule4 limiting increases in all newly enacted and existing discretionary expenditure items to 1

percentage point over the rate of inflation (CPI); and (ii) a nominal freeze of the budgetary

sphere wage bill.5

15. The structural reforms initiated by the Government are critical to ensure long-term

fiscal sustainability in Poland. Spending on pensions, health, education and other services

remains large relative to other emerging economies. At the same time, Poland’s aging population

presents significant challenges for long-term growth potential and fiscal sustainability.

According to EC projections, Poland’s working age population will decline from close to 27

million in 2010 to only 16 million in 2060. The pension reform of 1999 has a positive effect on

fiscal sustainability, but further reforms are needed, such as increasing retirement age for both

men and women and dealing with special pension schemes. The drop in the working age

population will also have an effect on fiscal sustainability through lower GDP growth and lower

revenues—including social insurance contributions. Further, the aging population will place

fiscal pressures on public services and programs, especially burdening the public health care

system (including long-term care) and social assistance. In education, quality needs to be

improved to build up skills demanded by the changing economy, but without spending additional

resources. Instead, existing inefficiencies need to be weeded out (see PER 20106). If action is not

taken, social spending will crowd out fiscal space for critical infrastructure and other capital

investments needed to sustain growth. On the revenue side, a main challenge is to continue

expanding the tax base, including bringing in sectors that are currently outside the tax net. Over

time, this will generate space to consider fiscally responsible reductions in marginal tax rates.

16. Despite the 2008-09 global financial crisis, poverty has remained low. Taking the

minimum social assistance threshold as a poverty line, poverty was halved from 14.6 percent in

2007 to 7.3 percent in 2010. Alternative measures of poverty confirm this trend (Figure 3). The

rate of poverty reduction (percentage points per year) has slowed down only slightly since 2008

and 2009. The poverty profile remained broadly unchanged. The incidence of poverty is high

among the unemployed, families with household heads with low education, families with many

3 The revenue from the corporate income tax rebounded in 2011 as companies ceased to deduct losses incurred as a

result of the global financial crisis in 2008-09. The loss carry-over provisions in Poland apply for a period of

maximum five years. Since companies are allowed to deduct at most 50 percent of their losses in a given year, in

practice, most companies deduct all the losses within two years. 4 The temporary fiscal rule was introduced as an amendment to the Public Finance Act in December 2010. The rule

is automatically enforced when Poland is under the Excessive Deficit Procedure (EDP). 5 The 475,000 employees of the state budgetary sphere are public sector employees directly under the control of the

central government. 6 Public Expenditure Review, Analysis of Social Sectors and Public Wages, World Bank 2010.

6

children, and households in small towns and rural areas. The Gini coefficient suggests that

inequality remained essentially unchanged over the last seven years (Figure 3).

Figure 3: Poverty and Inequality in Poland, 2004-2010

Source: HBS, GUS, World Bank staff calculations

2.3. MACROECONOMIC OUTLOOK AND DEBT SUSTAINABILITY

17. In the current external environment, growth is projected to slow down in 2012. As

uncertainty continued in early 2012, growth in global trade and industrial production has been

slowing in the region, including in Poland. However, due to its large and diversified domestic

economy, Poland is expected to be less affected than other economies in Central and Eastern

Europe. With private demand subdued and public demand tightening due to fiscal consolidation,

growth is expected to slow to 2.5 percent in 2012 (Table 1). Growth is expected to be supported

by net exports, whereas easing domestic demand is set to slow import growth. Consumption

growth is likely to remain subdued due to weak consumer confidence, modest increases in wages

and the ongoing fiscal consolidation. Growth in investment is likely to remain robust in the

medium term, albeit lower than in 2011, supported both by private and public sectors. In 2013,

growth is expected to strengthen to more than 3 percent on the back of an improved external

environment. Unemployment levels are expected to decline only in 2013 once growth accelerates

again. However, there are substantial downside risks, particularly if external demand declines

further and funding pressures become more acute in capital markets due to a worsening of the

situation in the euro area.

18. Monetary policy is expected to continue to anchor inflation expectations. The CPI is

expected to decline from 4.3 percent in 2011 to 3.6 in 2012, and then fall further due to

stabilizing fuel and food prices and inflation-decreasing base effects. Since the summer of 2011,

the NBP has maintained its main policy rate at 4.5 percent in response to the weakening

economic recovery. Better than expected high-frequency indicators (industrial production and

retail turnover) as well as still elevated inflation rate resulted in the 0.25 hike in the policy rate in

early May 2012. Monetary easing (particularly in Europe) is expected to keep the Polish Zloty

(PLN) near current levels, limiting the need for NBP tightening as domestic demand over time

starts recovering. The Polish Financial Supervision Authority, along with the NBP and the

Ministry of Finance (MOF), continue to closely monitor the stability of the financial sector, and

have taken measures to limit foreign currency lending to households.

0

5

10

15

20

25

30

35

40

45

50

2004 2005 2006 2007 2008 2009 2010

Gini coefficient Social assistance threshold

ECAPOV $5/day Eurostat at risk of poverty

7

Table 1: Economic and Fiscal Developments and Prospects 2007-2014

(change in percent unless otherwise indicated)

Notes: 1/ The main difference between the national and ESA’95 definitions of public debt is that the national

definition excludes debts of the National Road Fund (which are included in the ESA’95 definition).

2/ Derived as a sum of capital and financial account balance and errors and omissions.

Data for 2011 are estimates, based on actual data available by end- April 2012.

Source: MoF Convergence Program Update 2012, NBP, World Bank staff estimates

19. On the external side, the current account deficit is expected to stay close to 4 percent

of GDP over the medium term. The current account deficit is projected to be financed mostly

by FDI inflows and EU transfers. The external debt is expected to remain below 70 percent of

GDP over the medium-term and its maturity structure is expected to hover at a similar level of

2011 (Table 2). External debt roll-over rates are expected to be around the average of the last

four years. The sustainability of the external debt position is generally robust according to a

range of standard stress scenarios, including an increase in nominal interest rates, lower GDP

growth and higher current account deficit (Figure 4). In addition, private sector flows and

continued favorable access to international capital markets suggest that external financing needs

can be met (Table 3).

2007 2008 2009 2010 2011 2012 2013 2014

Est.

National Accounts

Real GDP growth (%) 6.8 5.1 1.6 3.9 4.3 2.5 3.6 4.0

Domestic demand growth (%) 8.7 5.6 -1.1 4.6 3.8 2.2 3.6 4.2

Consumption growth (%) 4.6 6.1 2.0 3.5 2.1 1.8 3.0 3.6

Private consumption growth (%) 4.9 5.7 2.1 3.2 3.1 2.2 3.2 3.7

Gross fixed investment growth (%) 17.6 9.6 -1.2 -0.2 8.5 3.4 5.7 6.6

Net external demand (contribution to growth) -2.1 -0.6 2.7 -0.7 0.5 0.5 0.3 -0.1

Employment, LFS

Number of employed (mln. pers.) 15.24 15.80 15.87 15.96 16.1 16.15 16.22 16.25

Unemployment rate 9.6 7.1 8.2 9.6 9.4 9.4 9.3 9.0

Fiscal Accounts of General Government (as % of GDP, ESA95)

Expenditures 42.2 43.2 44.5 45.4 43.6 42.9 41.1 40.0

Revenue 40.3 39.5 37.2 37.5 38.5 39.6 38.7 37.9

Balance -1.9 -3.7 -7.3 -7.9 -5.1 -3.3 -2.4 -2.1

Public Debt 1/

Public debt as % GDP according to ESA methodology 45.0 47.1 50.9 54.9 56.3 56.6 55.9 55.4

Public debt as % GDP according to national methodology 44.8 46.9 49.9 52.8 53.5 51.7 49.4 47.6

External Accounts (billions USD)

Current account balance -26.5 -35.0 -17.2 -21.9 -22.1 -20.3 -23.7 -25.5

Current account balance, as % of GDP -6.2 -6.6 -4.0 -4.7 -4.3 -4.0 -4.3 -4.4

Exports of goods and services 174.3 214.0 171.1 198.4 230.9 243.2 262.0 280.7

Imports of goods and services 188.6 239.6 173.9 207.1 239.0 249.1 269.8 289.0

Net capital inflows, as % of GDP 2/ 9.3 6.2 7.4 7.9 5.5 5.6 6.5 6.5

Indebtedness (external debt, USD terms)

Total external debt as percent of GDP 54.9 46.2 65.0 67.2 62.7 69.1 67.1 67.6

Prices

Consumer price inflation (period average) 2.5 4.2 3.5 2.6 4.3 3.6 2.8 2.7

Actual Projected

8

Table 2. External Debt Composition as of

end 2011

Figure 4. External Debt Sustainability (Debt

projections as percent of GDP)

Source: MOF, NBP, World Bank staff calculations. Notes: The shaded area reflects historical values. The nominal interest rate is at baseline plus one-half standard

deviation, real GDP growth is at baseline minus one-half standard deviations, non-interest current account is at

baseline minus one-half standard deviations.

Table 3. Medium-term Projections of External Financing Requirements and Sources

(US$ millions)

Source: World Bank staff estimates.

20. The Government intends to continue fiscal consolidation and pursue structural

reforms to entrench the sustainability of social spending. The fiscal deficit is projected to

decline to around 3 percent of GDP in 2012, consistent with Poland’s commitment under the

Excessive Deficit Procedure (EDP) (Table 4). The Government is expected to pursue further

fiscal consolidation to gradually reduce the structural fiscal deficit to 1 percent of GDP in line

with its medium-term objective. In 2012 and 2013, authorities plan to implement a wide range

of structural reforms in the areas of pensions, social assistance and health to secure the

sustainability of the public finances and to protect fiscal space needed for strategic infrastructure

and human capital investments. The Government’s plans for fiscal adjustments are discussed in

detail in Section III.

USD,

bln

Share of

total debt

% of

GDP

Monetary authorities 5.0 1.6 1.0

General government 115.2 35.8 22.4

Banks 66.0 20.5 12.9

Other sectors 135.7 42.1 26.4

of which intercomp.lending 73.7 22.9 14.3

Total external debt 321.9 100.0 62.7

long-term 249.8 77.6 48.6

short-term 72.1 22.4 14.0

40

45

50

55

60

65

70

75

2008 2009 2010 2011 2012 2013 2014 2015

Baseline Interest rate Growth Current Account

2010 2011 2012 2013 2014

Est.

Financing requirements 72,867 53,719 55,923 68,636 73,543

Current account deficit 21,873 19,798 20,343 23,687 25,506

Medium and long term debt amortizations 35,860 27,039 27,407 32,766 36,179

Change in reserves 15,134 6,882 8,172 12,183 11,858

Financing sources 72,867 53,719 55,923 68,636 73,543

EU funds 8,620 11,068 10,293 10,711 10,716

Private investment (net) 10,355 11,363 12,373 13,465 14,565

Medium and long term disbursements 59,776 37,684 29,961 41,158 44,383

Other capital flows incl. errors and ommissions -5,884 -6,397 3,295 3,302 3,879

Gross External Debt (% of GDP) 67.2 62.7 69.1 67.1 67.6

Projected

9

Table 4. Fiscal Developments and Prospects 2007-2014 (percent of GDP unless otherwise indicated, ESA’95, General Government)

Source: MoF; World Bank staff estimates, Convergence Program Update 2012.

Notes: Data for 2011 are estimates, based on actual data available by end - April 2012.

21. Public debt is expected to peak in 2012 and then decline. Fiscal consolidation,

together with better fiscal institutions, public sector cash management and stepped-up

privatization plans, will help to reduce public debt levels. According to the ESA’95

methodology, public debt is projected to stabilize at around 57 percent of GDP in 2011-12 and

then start a steady decline to close to 55 percent by the end of 2014. This would ensure that

Poland’s public debt remains below the Maastricht ceiling of 60 percent of GDP (as calculated

according to ESA’95 methodology) and the key national debt threshold/limit of 55 percent of

GDP (as calculated according to national methodology).7 Stress tests suggest that the debt path is

highly sensitive to a growth shock8, which might put the level of public debt slightly above the

EU threshold of 60 percent of GDP (Figure 5).

7 The Public Finance Act prompts corrective action when the public debt reaches 55 percent of GDP, in addition to

the constitutional ceiling for public debt at 60 percent of GDP. 8 In this scenario real GDP growth rate is at baseline minus 2 percentage points in each year of the projection period.

2007 2008 2009 2010 2011 2012 2013 2014

Est.

Revenues 40.3 39.5 37.2 37.5 38.5 39.6 38.7 37.9

Taxes 22.7 22.8 20.2 20.5 20.7 21.0 21.1 20.6

Social security contributions 12.0 11.3 11.3 11.1 11.4 12.3 12.5 12.6

Other 5.6 5.4 5.7 5.9 6.4 6.3 5.1 4.7

Expenditures 42.2 43.2 44.5 45.4 43.6 42.9 41.1 40.0

Current expenditures 37.4 37.7 38.4 39.1 37.0 36.5 34.9 34.1

o/w interest payments 2.3 2.2 2.6 2.7 2.8 2.6 2.5 2.5

Capital expenditures 4.8 5.5 6.1 6.3 6.6 6.4 6.2 5.9

Balance

Overall -1.9 -3.7 -7.3 -7.9 -5.1 -3.3 -2.4 -2.1

o/w primary 0.4 -1.5 -4.7 -5.2 -2.3 -0.7 0.1 0.4

Projected

10

Figure 5. Public Debt Sustainability (Public debt projections as percent of GDP)

Source: MoF, NBP; World Bank staff estimates.

Notes: The shaded area reflects historical values. Real interest rate is at baseline plus one

standard deviation. Real GDP growth is at baseline minus one-half standard deviation. Primary

balance is at baseline minus one-half standard deviation

22. The macroeconomic policy framework is considered adequate for the proposed

operation. The macroeconomic policies implemented during and after the 2008-9 global

financial crisis have facilitated the needed adjustment, economic resilience and growth. With

uncertainty in the external environment, policies are geared to mitigate the negative effects of

shocks through prudent fiscal and monetary policies, while keeping external imbalances in check

and maintaining the financial system adequately capitalized. These policies are also calibrated to

accommodate a gradual but sustained recovery of the real sector.

23. However, downside risks to the macroeconomic outlook are substantial. They

include further instability in the euro area and contagion from sovereign debt concerns in some

euro area countries transmitted through external trade and financial links. Poland remains

vulnerable to external debt deleveraging through parent bank funding of local subsidiaries. At the

same time, weaker demand in the EU and globally could place pressures on Poland’s exports and

investment growth. Over half of total Polish exports during the first three quarters of 2011 went

to the euro area. The euro area was also the source of around 70 percent of FDI flows into Poland

in 2010.

2.4. RELATIONS WITH THE IMF

24. Poland has secured a Flexible Credit Line arrangement (FCL) with the

International Monetary Fund (IMF). This arrangement helps Poland sustain access to

international capital markets. On January 21, 2011, the IMF Executive Board approved a two-

year FCL arrangement for Poland in the amount of SDR 19.166 billion (around US$30 billion).

The IMF Executive Board of the IMF concluded a review of the FCL on January 20, 2012,

stating that Poland continues to meet the qualification criteria for access to FCL resources

(Annex 3). The Polish authorities continue to treat this arrangement as precautionary.

45

50

55

60

65

2008 2009 2010 2011 2012 2013 2014 2015

Baseline Interest rate Growth Primary Balance

11

III. THE GOVERNMENT’S REFORM PROGRAM

25. The Government has presented a package of reforms to strengthen public finances

as a core priority. On November 18, 2011 Prime Minister Tusk launched the Government

program for his second four-year term. The program rests on three complementary pillars aiming

to sustain medium-term economic growth and accelerate Poland’s EU convergence prospects:

strengthening public finances, safeguarding the financial sector stability, and boosting private

sector development. In the view of the authorities, strengthening public finances is vital for

Poland to maintain its economic resilience and help secure fiscal sustainability, while continuing

to protect the most vulnerable. Therefore, the public finance pillar includes reforms with deep

structural impact in social sectors. Policy reforms in the financial sector (Box 1) are geared

towards safeguarding the stability of the Polish banking sector in the medium term. The

tightening of regulatory rules aims to alleviate potential systemic risks stemming from the

exposure of Polish banks to the euro area. Further, to crowd in the private sector, the

Government has adopted a comprehensive ―Deregulation Package‖ aimed at improving the ease

of doing business in Poland (Box 2). All these reforms are part of structural changes envisioned

in the long-term Government’s strategy 2010-2030.

Box 1. Policies to Safeguard Financial Sector Stability

The Polish Financial Supervision Authority (KNF) has adopted a number of new regulations aimed at strengthening

the domestic banking sector with implementation in 2012 and beyond, including:

A regulation to improve commercial banks’ internal FX and derivative management.

The EU Markets in Financial Instruments Directive, raising requirements for banks to properly assess clients’

eligibility to engage in derivative transactions.

A regulation to further limit risks resulting from foreign currency lending. Foreign currency mortgage loan

repayments cannot exceed 42 percent of a client’s monthly income, calculated for a maximum 25-year maturity

of the loan. Capital weights on FX mortgage lending increased from 75 percent to 100 percent.

A periodic bottom-up stress test of banks is being implemented.

More frequent onsite inspections are being conducted.

A new framework to transform foreign bank branches into domestic subsidiaries operating under the Polish law.

A regulation mandating that capital adequacy ratios of banks should not fall below 12 percent following 2012

dividend payments.

A working group to design improvements to the bank resolution framework.

A tax on financial transactions to be introduced in 2012, with proceeds used to establish a special Stability Fund

for bank recapitalization managed by the Bank Guarantee Fund (BFG).

12

Box 2. Policies to Strengthen Private Sector Development

A comprehensive ―Deregulation Package‖ has been adopted by the Government aimed at improving the business

climate, with implementation in 2012 and beyond, including:

A new Bankruptcy and Reorganization Law to simplify court procedures and extend increasing rights to secured

creditors in businesses closures.

A second deregulation package, which entered into force in early 2012. Among other measures it: (i) abolishes

the costly requirement for companies to publish their financial reports; (ii) reduces the frequency with which

companies must inform their employees in writing about mandatory health and social insurance payments; (iii)

eases health and safety requirements accompanying the construction or adaptation of buildings; (iv) extends the

deadline for the submission of real estate tax declarations; (v) gives taxpayers the power to request general tax

interpretations from the MOF; and (vi) shortens the required period for storing past social insurance declarations

and notices from 10 to 5 years.

A 24-hour online registration of new limited liability companies, based on standard agreements and with no need

for notary authorization.

26. Reigning in the fiscal deficit and stabilizing debt dynamics through fiscal-structural

reforms are key priorities in the Government’s strategy. The authorities are focusing their

reform efforts on fiscal-structural agenda for at least three reasons:

Following the global financial crisis of 2008-09, markets pay increasing attention to fiscal

vulnerabilities, particularly as regards to sovereign debt. While government bond spreads in

the EU had a limited correlation with public debt prior to the crisis, bond spreads are now

closely tied with growth and pressures in sovereign debt. The public debt level in 2011 is

estimated to be at 53.5 percent of GDP (according to national methodology), that is, close to

Poland’s Public Finance Act threshold of 55 percent of GDP. Stabilizing and later reducing

public debt to maintain its favorable capital market access remains critical to Poland’s

medium-term growth. Moreover, public debt has to be reduced to keep public finances on a

solid footing to withstand future shocks.

Poland needs fiscal space to continue investments in infrastructure and human capital to

support growth while making social transfers sustainable for future generations. Post-crisis

growth is likely to remain weaker than before the global crisis. Moreover, in the coming

decade, the decline in the labor force due to population aging will drag growth and place

added fiscal pressure in pensions and social services. If deep reforms are not implemented,

these expenditures will reduce the fiscal space for investments critical to spur growth.

Public spending reached almost 44 percent of GDP in 2011. Reducing gradually the public

sector footprint in the economy would help to crowd in private sector growth.

27. The authorities have developed a plan to consolidate public finances and undertake

fiscal-structural reforms. The measures are structured around three broad objectives: (i) to

ensure a steady decline in the fiscal deficits and public debt; (ii) to strengthen fiscal institutions;

and (iii) to secure the sustainability of social spending in view of Poland’s demographic

challenge. The measures under these three areas would also help protecting fiscal space for

growth-enabling expenditures. The Government views these policies as not only a way to keep

Poland resilient in the face of adverse times, but also to improve the ability of the budget to

facilitate growth over the medium and long term.

13

3.1. CONSOLIDATING PUBLIC FINANCES

28. The planned fiscal measures embedded in the 2012 budget are expected to generate

fiscal savings of around 2 percent of GDP (Table 5). Building on the progress made in 2011, a

further reduction in the fiscal deficit is crucial to adhere to Poland’s commitment under the

EDP,9 to stay clear of the 55 percent of GDP national public debt limit and reduce debt over the

medium term. The authorities have confirmed Poland’s commitment to reduce the fiscal deficit

to around 3 percent of GDP in 2012. Based on the draft budget for 2012, the European

Commission declared in January 2012 that Poland has taken effective action to correct its

excessive deficit. If the 2012 results show that Poland indeed reduced its deficit to close to 3

percent of GDP, the EDP will be withdrawn. Beyond 2012, Poland’s fiscal policy will be geared

to achieving its medium-term objective of 1 percent of GDP structural fiscal deficit by 2015. The

scale of the consolidation planned for 2012-15, while ambitious in light of the weakening growth

outlook, is appropriate as Poland’s fiscal deficit remains large and debt dynamics need to be

contained to secure capital market access at reasonable costs.

Table 5. Estimated Fiscal Impact of Measures Implemented as part of the 2012 budget,

percent of GDP 2012

Revenue Expenditure

Measure Impact Measure Impact

Amendment of the pension law 0.5 A temporary expenditure rule (CPI+1)

0.3 An increase in the disability contribution rate 0.3 A wage bill freeze in the budgetary sphere

No adjustments in PIT thresholds 0.2 Abolition of early retirement schemes 0.4

An increase in excise taxes, a new tax on copper

and silver

0.3

Other measures 1/ 0.2

TOTAL 1.1 TOTAL 0.7

Source: MoF; World Bank estimations.

Notes: 1/other measures relate to introduction of capital tax on one-day deposits, revenues from auctions of CO2

emission rights, and fees from new road speed enforcement system

29. On the revenue side, the 2012 fiscal consolidation relies on tax and social insurance

contribution measures, some of them initiated in 2011. The implementation of a number of

measures started in the 2011 budget, and their continued implementation will render fiscal

savings in 2012. These measures include: (i) an increase in the statutory VAT rate from 22

percent to 23 percent; (ii) a shift of 5 percentage points of the contributions from the second

pillar pension funds to the notional individual accounts under the state pension system; (iii) no

adjustments in personal income tax thresholds; and (iv) increases in various excise taxes. New

measures in the 2012 budget include: (i) an increase in the statutory rate on disability

contributions paid by employers (Box 3); (ii) a new tax on copper and silver; and (iii) CO2

emission rights auctions. In addition, the Government expects higher dividends in 2012 due to

good financial results of state-owned enterprises.

9 Under the provision of the EU Stability and Growth pact, the EDP is triggered when a member state exceeds the

general government fiscal deficit-to-GDP ratio of 3 percent or public debt-to-GDP ratio exceeds 60 percent. This

entails several steps, including possible sanctions, to encourage the member state to take appropriate measures to

rectify the situation over a certain number of years.

14

Box 3. Disability Contribution Rates

Starting in 2012, the disability contribution rate has been increased by 2 percentage points—from 6 percent to 8

percent of gross wage. This fiscal measure is a partial correction of the large reduction in the disability contribution

rate that started in 2007, lowering that statutory rate from 13 percent to 6 percent. That initial reduction had the

objective of reducing the tax wedge in the country. However, while that reduction was a move in the right direction

and supported by the World Bank, the size of the reduction was too large, in particular in the context of the global

economic crisis and resulting fiscal pressures. The rate reduction moved the disability system from a close to

balanced position in 2007 to a deficit of 1.1 percent of GDP in 2011. With the increase in the contribution rate in

2012, the disability contributions will cover over 90 percent of paid benefits, compared to only 73 percent before

(prior to the reduction in the disability contribution rate in 2007, contributions covered 115 percent of paid benefits).

With this upward correction, Poland’s tax wedge (at 35 percent) will still remain below the EU average (39 percent)

and be the lowest among the EU10 countries, along with Bulgaria and Slovakia.

The authorities believe that the rate increase to 8 percent—still significantly below the pre-2007 level of 13

percent—would have a negligible effect on labor market outcomes. An important objective of the earlier disability

contributions rate reduction was the potential positive effect on labor markets. However, recent data suggests that

these rate reductions were not behind improvements in some labor market outcomes. For example, higher

employment participation rates among the elderly, which is driving improvements in aggregate labor participation,

increased from 29 percent in 2007 to 37 percent in 3Q 2011, mostly on the back of the phasing-out of early

retirement pensions schemes rather than on the reduction in tax wedge.

However, several structural and parametric issues of the disability insurance need to be addressed over the medium

term. Total expenditures of the disability fund are exceptionally high relative to other countries, where disability and

survivors can be covered by wage contributions of 2-3 percent. The relatively high disability contribution rate in

Poland can be explained by the following reasons. First, there is a very large stock of disabled pensioners. While

there have been significant improvements in the screening system and eligibility criteria for disability have been

tightened, the number of beneficiaries remains high. In addition, the current disability benefit formula (if

maintained) may create incentives for people to opt for disability rather than old-aged pensions, especially as old-

aged pension levels are expected to decline under the notional accounts formula. Second, there is hardly any outflow

from disability into the labor market. While 64.2 percent of beneficiaries have partial incapacity to work, they have

limited options for retraining and tend to stay in disability until they reach retirement age. Third, the generous

survivors’ pensions (at the level of 85 percent of spouses’ old-age pension compared to 60-70 percent in other

OECD countries) and the relatively low eligibility age (50 years, 10 years below the current statutory retirement age

for woman) tend to raise the expenditures of the disability fund.

30. On the expenditure side, the fiscal consolidation in 2012 is based on containment

measures. Overall, the plan envisages a gradual decline of the overall expenditure envelope in

2012-14. Similar to the revenue side, a number of measures were legislated and their

implementation started in the context of the 2011 budget, but their continued implementation

will render fiscal savings in 2012 (Table 5). They include: (i) the temporary ―CPI +1‖ rule that

limits the growth rate of discretionary expenditures to 1 percentage point over the CPI rate; (ii)

the phasing-out of early retirement schemes; and (iii) the nominal freeze of the wage bill in the

state budget, extended for the first time to include judges and prosecutors. The composition of

expenditure measures ensures that social safety nets remain adequate to protect the most

vulnerable.

15

3.2. STRENGTHENING FISCAL INSTITUTIONS

31. The Government is planning to introduce fiscal rules and budget reforms to ensure

a prudent fiscal stance over the medium term. By 2015, the Government aims to achieve a

structural fiscal deficit of 1 percent of GDP, in line with the medium-term objective (MTO) of

the EU Stability and Growth Pact. Once the MTO is achieved, the authorities plan to rely on a

permanent expenditure rule (to be enacted by 2013) to keep a prudent fiscal stance over the

medium and long term. In parallel, a sub-national fiscal rule is being established to facilitate

consolidation over the next three years, and thereafter to control local government finances. The

Government is also continuing to pursue reforms to strengthen the medium-term orientation of

the budget, legislate and implement program-based budgets and make public sector pay more

efficient.

32. The Government plans to introduce controls on local government finances in the

form of an annual aggregate deficit ceiling. At the beginning in 2013-14, the ceilings are

planned to be nominal, around 9-10 billion PLN, but beyond 2014 they will be set at 0.5 percent

of GDP. The plan is also to include the deficit of municipal corporations in the deficit ceiling

starting 2013.10

This rule is a critical feature of the envisaged fiscal architecture, given that local

government total debt has been increasing faster than central government debt since 2007

(Figure 6). So far, controls have focused on ensuring that individual local government units do

not borrow excessively in relation to their revenue and debt-servicing capacity. However, these

types of controls are not designed to manage the aggregate deficit and growing debt levels of

local governments (Figure 7). Thus, they are insufficient to ensure that the general government

as a whole moves towards its deficit and public debt objectives.

Figure 6. Central and Local Government Debt,

index, 2007=100

Figure 7. General Government Fiscal Balance by

Sector, percent of GDP

Source: Eurostat, World Bank staff calculations. Source: Eurostat, World Bank staff calculations.

33. When the planned aggregate local government deficit exceeds the annual ceiling, a

deficit-reduction process is applied. Each year by the end of March, the Ministry of Finance

(MoF) evaluates whether the medium-term budget plans of local governments are in line with the

aggregate annual ceiling. In case they are above the limit, a deficit-reduction process is put in

10

Hospital restructuring expenses are not considered for the deficit cap calculation in 2012- 2014, but will be

considered starting in 2015.

0

50

100

150

200

250

2007 2008 2009 2010 3Q 2011

Central government Local government

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

2007 2008 2009 2010 2011f

Central government Local government SSF

16

place. In the first stage of this process, the local governments are allowed to negotiate among

themselves the size of the reduction of the deficit.11

If the aggregate deficit remains above the

annual ceiling, the MoF steps in and imposes a proportional cut in deficits affecting all local

governments. To ensure compliance with the aggregate ceiling, the local governments are

obliged to report any changes to their budget execution and plans on quarterly basis.

34. In parallel, the Government is preparing legislation to create a permanent

expenditure rule for the central government (national) budget. The rule would limit the

growth of national government expenditure to a rate not exceeding the trend growth rate of GDP.

Existing national fiscal rules are focused on debt and do not address the pro-cyclicality of

expenditures. The aim of this rule is to safeguard against the re-emergence of excessive

structural budget deficits in the medium and long term, following the completion of the present

fiscal consolidation program. The tentative target date for reaching the MTO structural fiscal

deficit of 1 percent of GDP is 2015, and this rule would come into force the following year (i.e.,

for the 2016 Budget Law). With revenue projected to grow (holding tax policies constant) at the

same trend rate as GDP, the expenditure rule would help to maintain the budget balance on

average over the business cycle at the level required by the MTO.

35. The planned expenditure rule is adequate to Poland’s needs. It directly addresses the

main causal factor behind excessive deficits in Poland—the excessive rate of growth of

expenditure. Also, an expenditure rule is more relevant at this time than a rule that applies to the

budget balance itself, due to the complexities of measuring the structural fiscal balances. At the

same time, an expenditure rule would allow for the unrestricted operation of automatic stabilizers

on the revenue side in case of a downturn. The successful implementation of this measure would

assure a prudent fiscal stance over the medium- and long-term. This rule is similar to an

expenditure rule recently introduced by the European Commission as part of the preventative

arm of the Stability and Growth Pact (one of the so-called "six pack" measures).12

11

The deficit reduction process does not apply to those local governments, which generate deficit due to co-

financing of EU-financed capital projects, the implementation of national investment programs, and to those that

cover their own deficits with the sale of assets. 12

The most important difference between the two is that the EC ceiling applies only when a country has not yet

achieved its MTO.

17

Box 4. Fiscal Rules in Poland

International experience with fiscal rules implementation has been mixed. In many cases fiscal rules have

had a positive impact on fiscal outcomes, particularly in countries with effective fiscal institutions and the

political will for successful implementation.13

However, some rules have resulted in pro-cyclical

tendencies. For example, strong revenues in cyclical upturns have enabled expenditures to grow more

rapidly within a nominal deficit limit. Nonetheless, numerical fiscal rules have generally played an

important role in containing spending and deficit biases by guiding or imposing constraints on

policymakers’ discretion. They are particularly effective when established by laws and higher level

legislation such as the Constitution.

Poland has had a positive experience with fiscal rules: fiscal rules, enshrined in the Constitution and the

Public Finance Act (PFA), have been effective in preventing the breach of debt limits. Poland's

Constitution sets an upper limit for public sector debt (based on a national definition) at 60 percent of

GDP. It prohibits both borrowing and the provision of guarantees that would exceed this limit. In

addition, the PFA sets two lower debt thresholds for national public sector debt, at 50 and 55 percent of

GDP. If the 50 percent threshold is exceeded in year (t – 1), the Parliament may not in year t approve a

budget for the following year (t + 1) with a central government budget deficit/revenue ratio that is higher

than the deficit/revenue ratio in the approved budget for year t. If the 55 percent threshold is exceeded, the

budget for year (t + 1) must be balanced or provide for a reduction of the central government debt to GDP

ratio as compared to t-1. The PFA also mandates deficit-reducing actions to be taken by local

governments. If the 55 percent limit for general government debt is exceeded, local governments may

generate a deficit only due to co-financing of EU funded projects. If the debt ratio exceeds 60 percent of

GDP, they are required to balance their budgets. The PFA sets also a temporary expenditure-based fiscal

rule (effective since 2010) that limits the annual growth rate of discretionary expenditure and newly

enacted mandatory spending to 1 percent above inflation. This temporary measure is planned to be in

force until the EDP procedure is abrogated.

As regards to local governments, the PFA lays out the following rules: (i) the debt of individual local

government units may not exceed 60 percent of its revenue (it does not cover debt issued for pre-

financing–bridge financing— projects co-financed from EU funds); (ii) the debt service (which includes

debt repayment plus interest paid and guarantees due in a current year) may not exceed 15 percent of the

local government revenue; (iii) local government units may not run current budget deficits; (iv) in

addition, starting in 2014, new borrowing will be regulated by the local governments’ capacity to service

debt (a debt-servicing ratio).

In addition to its own national rules, Poland is subject to the European Union's 60 percent of GDP debt

limit and 3 percent of GDP deficit limits, as according to ESA’95 methodology. The European Council

Regulation of 2011 allows to take into account the cost of systemic pension reform (in Poland’s case it

was above 0.6 percent of GDP in 2012) when assessing compliance with the Stability and Growth Pact.

36. The new permanent rule will also include a correction mechanism to reinforce the

link between the expenditure ceiling and the MTO.14

Under the correction mechanism, when

the actual budget balance differs from the MTO, the difference between the two will be added to

a "notional account", which will record the cumulative value of such deviations. If the amounts

added to the notional account exceed a defined threshold, equivalent automatic expenditure cuts

will be required. Similar to the new EU expenditure rule, the Polish permanent expenditure rule

13

For a recent review of international experience with fiscal rules, see IMF. 2009. ―Fiscal Rules—Anchoring

Expectations for Sustainable Public Finances‖, at http://www.imf.org/external/np/pp/eng/2009/121609.pdf 14

This correction mechanism is similar to the Swiss "debt brake" and to a mechanism that operates under the

German balanced budget rule.

18

is intended to apply to expenditures net of discretionary measures on the revenue side.15

Unlike

the EU rule, the Polish fiscal rule will cover essentially all national government expenditure

(including spending on unemployment benefits and interest payments), other than EU-funded

capital expenditure.16

Because the rule is to be enshrined in legislation it can be expected to raise

the political and market access costs of non-compliance.

37. Beyond fiscal rules, Poland is committed to developing program-based budgeting.

An indicative performance budget—including a programmatic breakdown of expenditures,

program objectives and key performance indicators—has been presented to the Parliament for

information alongside the traditional annual budget since 2008. The coverage and details of this

indicative program budget have been gradually increased. The 2012 indicative budget covers the

whole central government. The aim of this has been to eliminate pure input and process

indicators and focus on output and outcome indicators. The Government’s plan over the medium

term is the implementation of a program-based budget where appropriations are also approved

by the Parliament, in parallel to the traditional budget. If the move to a program-based budget is

accompanied by appropriate supporting measures and information infrastructure (including

continued development of performance information, strengthening of budget preparation

processes and integrated information systems for policy making), it would help to improve the

efficiency of public expenditure in Poland.

38. Poland has also been taking steps towards medium-term budgeting. The

development of the Multi-Year State Financial Plan (MYSFP) is the most recent example. The

MYSFP is a four-year rolling fiscal plan presented to the Parliament that includes fiscal policy

goals, revenue and expenditure projections as well as deficit and debt projections. The

expenditure projections contained in the MYSFP represent indicative (as opposed to fixed)

ceilings for the ministries and other entities. The authorities plan to further strengthen this

process in tandem with the implementation of the fiscal rules.

39. Finally, the Government plans to proceed in the coming years with pay reforms in

the public sector. While Poland’s public sector is not large in regional comparison from a fiscal

or employment perspective, the system has a number of structural problems. The Government

has difficulties recruiting and retaining staff with adequate skills. The civil service population is

aging (which is raising salaries due to seniority payments), the pay is rigid, fragmented, non-

transparent and likely to be inequitable, and payroll administration is expensive and marked by

weak financial controls. In November 2011, the Government announced the creation of a new

Ministry of Public Administration and Digitalization. This ministry will be in charge of reforms

15

Thus if, for example, new tax measures were introduced that permanently increased government revenues by 1

percent of GDP, the maximum level of expenditure permitted by the expenditure rule would also increase by 1

percent of GDP. The same principle would apply in the opposite direction in the event of permanent tax cuts, which

is of particular importance in Poland given that in the longer term governments need to act to reduce Poland's

unduly high tax rates. 16

The inclusion of unemployment benefits is justified in the Polish case by the relatively short duration of benefit

eligibility, which is a key reason why expenditure-side automatic stabilizers are very small in Poland. The exclusion

of EU-funded capital expenditure reflects the fact that such capital expenditure adds neither to deficits nor debt, and

therefore has no bearing on the achievement of the MTO. Poland's own financial contribution ("co-financing") to

these projects—which does contribute to deficits and debt—will, appropriately, be covered by the expenditure rule.

19

to make public administration more efficient and to use modern technology to improve public

service delivery. These objectives are also central to the Government’s Vision 2030 strategy.

3.3. ADVANCING LONG-TERM FISCAL REFORMS

40. Strengthening public finances also requires initiating long-term structural reforms

to secure sustainability across sectors. The Government intends to focus on long-term reforms

to sustain current transfers (such as pensions) and public services (such as health care). It also

intends to pursue reforms to improve social safety nets and broaden the tax base by bringing to

the tax net income that so far has been under-taxed. These reforms tackle the aging demographic

profile of the country, with the working age population projected to shrink by about one-third

between 2010 and 2050.

41. The reform program is geared to restructure the fiscal accounts in a way that

protects strategic investments needed to foster growth. If reforms are not pursued,

uncontrolled growth in social spending could crowd out infrastructure and human capital

investments. Over time, the planned reforms would generate the fiscal space needed for

investments to enable sustained growth. Although fiscal savings are moderate in the short term,

the long-term impact of key structural-fiscal reforms in the Government’s plan ranges between

0.7 and 1.1 percent of GDP annually (Table 6). The rest of this section discusses the