Embed Size (px)

Citation preview

A global long only equity TMT fundSeptember 2015

DNB Technology

Sverre Bergland, Portfolio Manager

DNB Technology

• Long-only UCITS global equity fund which invests in technology, media and telecom sectors

• Strong and consistent performance record

• Dedicated and experienced investment team

• Compliant with DNB Asset Managements SRI policy

2

Agenda

3

1 DNB Asset Management

3 Investment Process

2 Portfolio Management Team & Track Record

4 Risk Management

5 Fund Facts

DNB Asset Management

DNB is among the largest Asset Manager in the Nordic Region

• Specialist approach to investing

• 76 portfolio managers and analysts

• € 61 billion under management

• Offices in Oslo, Bergen, Stockholm, Luxembourg, and Hong Kong

• 100% owned by Oslo-listed DNB Group

The DNB Group

• DNB is Norway's largest financial services group and one of the largest in the Nordic region in terms of market capitalization, represented in 21 countries worldwide

• The Group is among the world’s leading banks within shipping, energy and seafood

• The Group offers a full range of financial services, including loans, savings, advisory services, insurance and pension products for retail and corporate customers and the public sector

4

Agenda

5

1 DNB Asset Management

3 Investment Process

2 Portfolio Management Team & Track Record

4 Risk Management

5 Fund Facts

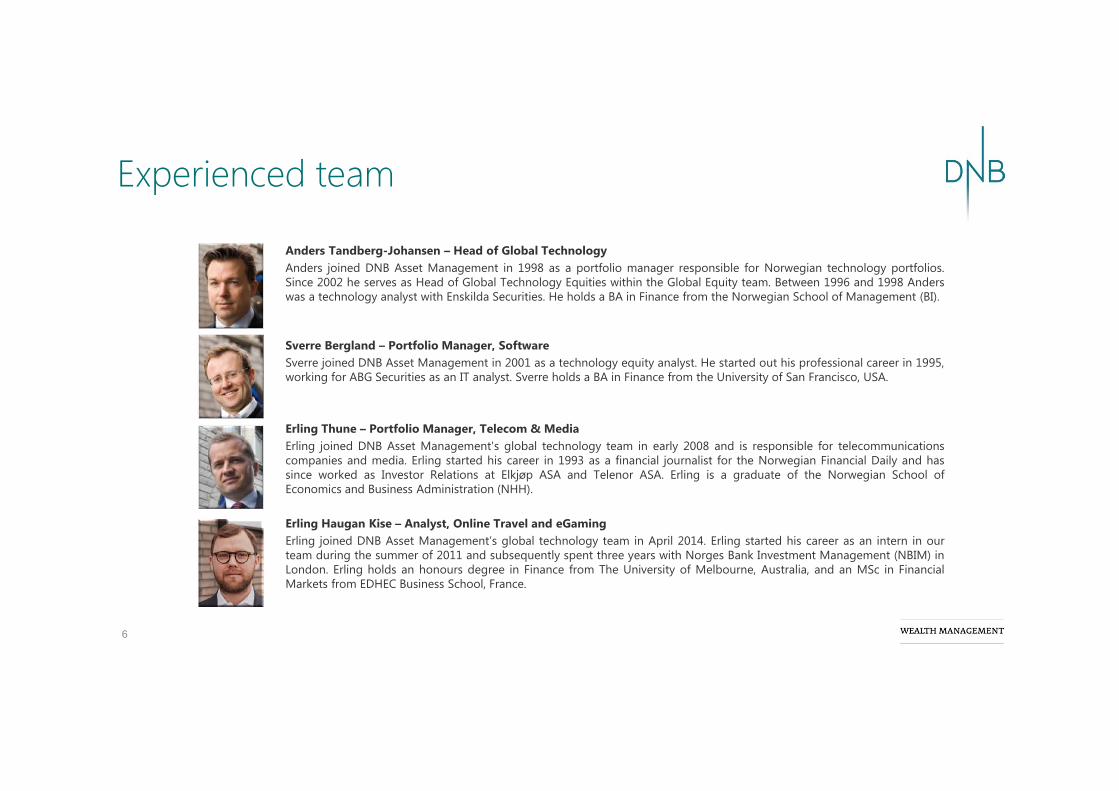

Experienced team

Anders Tandberg-Johansen – Head of Global TechnologyAnders joined DNB Asset Management in 1998 as a portfolio manager responsible for Norwegian technology portfolios.Since 2002 he serves as Head of Global Technology Equities within the Global Equity team. Between 1996 and 1998 Anderswas a technology analyst with Enskilda Securities. He holds a BA in Finance from the Norwegian School of Management (BI).

Sverre Bergland – Portfolio Manager, SoftwareSverre joined DNB Asset Management in 2001 as a technology equity analyst. He started out his professional career in 1995,working for ABG Securities as an IT analyst. Sverre holds a BA in Finance from the University of San Francisco, USA.

Erling Thune – Portfolio Manager, Telecom & MediaErling joined DNB Asset Management's global technology team in early 2008 and is responsible for telecommunicationscompanies and media. Erling started his career in 1993 as a financial journalist for the Norwegian Financial Daily and hassince worked as Investor Relations at Elkjøp ASA and Telenor ASA. Erling is a graduate of the Norwegian School ofEconomics and Business Administration (NHH).

Erling Haugan Kise – Analyst, Online Travel and eGamingErling joined DNB Asset Management’s global technology team in April 2014. Erling started his career as an intern in ourteam during the summer of 2011 and subsequently spent three years with Norges Bank Investment Management (NBIM) inLondon. Erling holds an honours degree in Finance from The University of Melbourne, Australia, and an MSc in FinancialMarkets from EDHEC Business School, France.

6

The best Global TMT fund last 5 years

7

18.0 % 17.6 %16.9 %

16.0 % 16.0 % 16.0 % 15.5 % 15.5 % 15.5 % 15.4 % 15.3 % 15.0 % 14.7 % 14.7 % 14.7 % 14.6 %14.1 %

Note: Returns as of August 26, 2015, source Morningstar Direct out of 178 Global Technology funds available for sale in Germany. Index is "MSCI World TMT" (66% MSCI Global IT, 22% MSCI Global Telecom Services, 12% MSCI Global Media). Inception of fund is August 16th 2007. Historical performance is no guarantee of future returns. Future returns will depend on market development, manager skill, portfolio / fund's risk exposure and the costs associated with the management / investment. The return can at times be negative.

Long only fund awarded best Global Technology Fund 5 year performance

DNB Nordic Technology Massively beating peers over more than 10 years

8

Global TMT funds – last 10 years (annual) Acc. net return of 732% since inception in 2001

Note: Inception of DNB Nordic Technology is August 8th 2001. Performance data as of July 31, 2015 (NOK). Peers comparison from Morningstar last 10 years as of August 8th,2015. Historical performance is no guarantee of future returns. Future returns will depend on market development, manager skill, portfolio / fund's risk exposure and the costs associated with the management / investment. The return can at times be negative.

17.3 %

12.0 % 11.6 % 11.3 % 10.8 % 10.2 % 9.7 % 9.4 %8.7 % 8.4 %

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-100%

0%

100%

200%

300%

400%

500%

600%

700%

800%DNB Nordic Technology BM ABGTMT (PI) Linked

Successful Absolute Return strategy

Period MSCI TMT Net return*

sep.07 +12.0% 3.0%

2008 -57.8% 21.3%

2009 +54.8% 22.7%

2010 +22.6% -1.6%

2011 +2.1% +10.2%

2012 +12.5% -10.9%

2013 +25.8% +13.2%

2014 +26.8% -2.0%

YTD +15.1% +3.0%

9Source: Performance is net of fees for TMT with gross swap performance only for Global Hedge. Table shows annual Global Hedge performance untli inception of TMT from 2011 until July31, 2015. Historical performance is no guarantee of future returns. Future returns will depend on market development, manager skill, portfolio / fund's risk exposure and the costs associated with the management / investment. The return can at times be negative.

40

60

80

100

120

140

160

180

200

220

240

260

DNB TMT Absolute Return NOK ST1X MSCI World (NOK) OSE Global Hedge TMT

DNB Technology - Largest Holdings

10

Stock Holdings

Samsung Electronics 7.29 %

APPLE 6.84 %

ORACLE 6.78 %

GOOGLE 6.01 %

Playtech Plc 5.21 %

PRICELINE 4.97 %

CISCO SYSTEMS 3.57 %

Ctrip.Com 3.37 %

Mellanox Technologies 3.19 %

King Digital 3.08 %

INTEL CORP 3.00 %

YAHOO 2.89 %

Canadian Solar Inc 2.85 %

Adva Optical 2.62 %

As of August 28. 2015

Stock Overweight

Samsung Electronics 7.29 %

Playtech 5.21 %

PRICELINE 4.97 %

ORACLE CORP 4.69 %

Ctrip.Com 3.37 %

Mellanox 3.19 %

King Digital 3.08 %

Canadian Solar 2.85 %

Adva Optical 2.62 %

YAHOO 2.42 %

AVG Technologies 1.96 %

Lenovo Group 1.57 %

Finisar 1.57 %

Oclaro 1.47 %

Stock Underweight

MICROSOFT CORP -3.67 %

APPLE -3.46 %

AT&T -3.24 %

VERIZON -3.02 %

FACEBOOK -2.83 %

DISNEY -2.58 %

VISA A -2.24 %

COMCAST -1.90 %

MASTERCARD -1.48 %

IBM -1.25 %

TELEFONICA -1.01 %

ACCENTURE -0.96 %

TIME WARNER -0.96 %

BT GROUP -0.89 %

11

DNB Technology

Relative Performance YTD: 5.9%

Pr Sept 12, 2015. Relative performance before fees

Contributors AttributionAdva Optical Networking 3.53 %

Playtech 1.78 %

Google A Shares 0.98 %

Activision Blizzard 0.97 %

Oclaro 0.82 %

AVG Technologies 0.81 %

The Priceline Group 0.79 %

Cyan 0.72 %

Quindell 0.70 %

Intel 0.58 %

Detractors Attribution

Samsung Electronics -1.24 %

Oracle -1.01 %

Finisar -0.67 %

Yahoo -0.64 %

Netgear -0.61 %

Facebook -0.56 %

Yingli Green Holding -0.49 %

Toshiba -0.49 %

Google C Shares -0.48 %

Qlogic -0.40 %

12

Source: Bloomberg (cash adjusted with 15% effective tax rate)

Trailing 12 mth forward PE – EPS CAGR Industry group

Trailing 12 mth forward PE – sales growth10 largest positions

12

15 15 15 15 15 16 1617

1921

5%

1%

11%

4%

6% 7% 7%

9%7%

5%

11%

0%

5%

10%

15%

20%

25%

30%

0

5

10

15

20

25

Tech stocks are not expensive

6 78 9

12 1215

1720

43

7% -10%5%

9%23%

0%

44%

17%

18%

53%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

0

5

10

15

20

25

30

35

40

45

Agenda

13

1 DNB Asset Management

3 Investment Process

2 Portfolio Management Team & Track Record

4 Risk Management

5 Fund Facts

Four key elements of stock selection

14

ValuationValuation Earnings rev/momentum

Earnings rev/momentum

Continously monitoring approx. 500 stocks Continously monitoring approx. 500 stocks

ValueCreation

ValueCreationThemesThemes

15

Themes - Six Important Megatrends

Internet for all Services moving to the cloud

Payments go mobileFragmentation of video

Internet of things

0

2,000

4,000

6,000

8,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Internet Population

Big Data

Global Population

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

GamingGaming GamblingGambling AdvertisingAdvertising

PaymentsPayments Taxi centrals Taxi centrals Travel bookingTravel booking

Scalable business models that take share of wallet

Source: ITU (International Telecommunication Union)

16

Only 40% of the world population is online

Global Population

Internet Population

17

The shift to cloud is real – but extreme valuations

Incumbents Market Cap(USD bn)

EV/SALES –15e

Sales growth- 15e

Oracle 194 4.7 1%

SAP 85 4.6 9%

Microsoft 348 3.0 8%

Challengers Market Cap(USD Bn)

EV/SALES - 15e

Sales growth– 15e

Salesforce 44 7 21%

Workday 16 13 45%

ServiceNow 12 12 44%

NetSuite 7 10 30%

Services moving to the cloud

Challengers grow with little or no profits- with high option costs…

…and depressing the multiples of the incumbents

18

“IoT” and “Big data” – from buzzword to reality

1,928 2,2922,712

3,1803,782

4,592

5,649

7,065

2013 2014 2015 2016 2017 2018 2019 2020

Global IoT Revenue (USD Bn)

CAGR ~ 20%

Source IDC

Internet of things

Big Data

Will be powered by Google and Apple

19

The next couple of years will be transformational for TV

Source: Statstics Norway

0

20

40

60

80

100

120

140

160

180

Newspaper

TV

TV (16-25)

Radio

Books

Internet

Daily time spent (mins)

Fragmentation of video

5%

12%

38%

25%20%19%

10%

45%

22%

4%

0%

10%

20%

30%

40%

50%

Print Radio TV Internet Mobile

Time spent Ad share

Time spent on media - Norway

Ad spend on media - Norway

WinnersWinners

LosersLosers

20

Mobile payments – The jury is out… and confused

Payments go mobile

…. Banks most likely losers…. Banks most likely losers

…. PayPal’s position underestimated…. PayPal’s position underestimated

…. Mastercard & Visa networks look safe…. Mastercard & Visa networks look safe

…. Tech most likely winners…. Tech most likely winners

GoogleWell positioned in most megatrends

YouTube Google Maps Online advertising

Google mobile search Android Google TVMarket share

Android

iOS

Windows

Blackberry

80%

0%

5%

10%

15%

20%

25%

30%

35%

Google Facebook Microsoft Yahoo

2012

2014

Source: eMarketer

GoogleStrong positions and reasonable valuation

22

Totally dominating search Strong and visionary management teamEconomies of scale – "The winner takes it all"

Net cash adjusted P/E of 16 in 2016 EPS growing by appr 16%Above 70% gross marginUSD 70 billion in net cash

Inflection point mobile advertisingReorganisation will reveal hidden value

Winner in transition from Offline to onlineWell positioned in most TMT megatrends

Revenues (USD Bn) EPS (USD)

ValueCreation

Valuation

Earnings rev/momentum

Theme

0

10

20

30

40

50

60

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Q4

Q3

Q2

Q1

0

5

10

15

20

25

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Q4

Q3

Q2

Q1

Ctrip.com InternationalChinese #1 in online travel booking

…but lagging in booking travel online

Travel spend is growing 6x that of US As the hotel mix improve, so will margins

China is leading the world in eCommerce…

85%63%

41%25%

-80%

-60%

-40%

-20%

0%

20%

40%

0%

20%

40%

60%

80%

100%

Priceline Expedia Ctrip Qunar

Hotel Air Other EBIT margin

$323 $358 $386 $408 $428

$5 $7

$10 $13 $17

11%8% 6% 5%

40%43%

30% 31%

0%5%10%15%20%25%30%35%40%45%50%

$1

$10

$100

$1,000

2010 2011 2012 2013 2014

US Bookings per capita China bookings per capita

US growth China growth

48% 45%

30%25% 26%

15%0%5%10%15%20%25%30%35%40%45%50%

-

50

100

150

200

250

300

350

400

Europe US EastEur LatAm MEA China

Bill

ion

USD

Online Total Online share (%)

15%

5% 5%4% 4%

3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

China Japan UK Korea Taiwan US

Online spending per capita as % of GDP (2013)

Ctrip.com InternationalMarket not appreciating the scope for margin acceleration

24

Toll booth to internet visibility in a fragmented hotel marketReviews verify accuracy of information and hotel ratingsDetailed understand of the Chinese traveller

Chinese online travel booking at 10-20% vs 50% in westCtrip growing ~50% organically vs. 25% for Priceline5.5x EV/Sales vs. 6.7x for Priceline

Earnings revision positive following strong Q1 and Q2Market not pricing in the operating leverage as the model scalei) Priceline went from 5% EBIT margin in 2002 to 34% 2010ii) eLong purchase consolidates the high-end of the marketiii) Market #2 Qunar is running -60% EBIT margin and losing $500m year vs $450m

gross cash in a marketing push to gain scale in hotels

At current trajectory CTRIP is trading at <30x ’16 P/E growing sales 40-50% organically

China leading the world in transacting onlineLagging the world in booking travel online, but catching up

ValueCreation

ValueCreation

ValuationValuation

Earnings rev/momentum

Earnings rev/momentum

ThemeTheme

145 153187 177 187 203

252 238 254278

347308

373408

517

450

553

601

766

662

19% 17% 16%11%

14% 16%19%

13%

4% 5% 4%

-21%

-8%

2%

12%

-2%

12%

20%26%

14%

-30%

-10%

10%

30%

50%

70%

90%

-

100

200

300

400

500

600

700

800

900

The Priceline GroupGlobal leader in online travel agency duopoly

40% of online bookings goes through OTAs

#1 position gives scale on marketing… …and superior margins

50% of bookings done online

62%

62%

59%

50%

65%

65%

61%

38%

38%

41%

50%

35%

35%

39%

0% 20% 40% 60% 80% 100% 120%

Overall

Middle East

LatAm

Easter Europe

APAC

US

Europe

% online booking from airline/hotel %of online booking through OTAs

48%

31%

45%

30%

25% 26%

0%5%10%15%20%25%30%35%40%45%50%

-

50

100

150

200

250

300

350

400

Europe APAC US EastEur LatAm MEA

Bill

ion

USD

Online Total Online share (%)

7.6

17.0

-

5

10

15

20

25

30

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

PCLN ad spend per room night Expedia

Growth ratesTravel market: 5%Online travel: 10%OTAs: 25%

30%

4%

-10%

0%

10%

20%

30%

40%

50%

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

PCLN Ebit margin Expedia EBIT margin

The Priceline GroupLeading position in growing market not reflected in share price

26

Toll booth to internet visibility in a fragmented hotel marketStrong and very competent management

Travel market growing 5%, online 10%, OTAs 25%Opportunities in developing regions and vacation rentals25% organic growth in ‘1520x ‘15 PE for the market leader in a global duopoly

Lapping an investment phase in H2, scope for operating leverageReduced currency headwinds in H2Earnings revisions turned positive in July

Travel booking shifting from offline to onlineOnline Travel Agencies (OTAs) taking share from hotels directOTA market growing at 5x travel market

ValueCreation

ValueCreation

ValuationValuation

Earnings rev/momentum

Earnings rev/momentum

ThemeTheme

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0%

10%

20%

30%

40%

50%

60%

FQ12012

FQ22012

FQ32012

FQ42012

FQ12013

FQ22013

FQ32013

FQ42013

FQ12014

FQ22014

FQ32014

FQ42014

FQ12015

FQ22015

Organic booking growth EBIT margin

PlaytechLeader in digital gambling technology

Mobile driving market growth

Online taking share from offline …providing long-term opportunities

Turnkey provider of eGaming Software

PlaytechLeading position in growing markets

28

Turnkey product for eGamingTechnology leader across all channels, #1 in mobileConsolidator of the online CFD and spread betting market

Online penetration of gambling less than 10%Physical gaming growing 4%, desktop 8%, mobile 30-40%Acquired presence in online CFD market at single digit PE’s12x ‘16 PE for years of organic growth

Positive earnings revisions in gaming as the company lap exits from some Asian markets in Q4 Further upside as acquisitions of TradeFX (9x), Avatrade (9x) and Plus500 (8x) conservatively reflected in estimates

Secular shift from physical to online casinos (eGaming)Convergence of gameplay across all channelsOpportunities in betting on financial markets (CFDs)

Revenues (€mn)Revenues (€mn) EBITDA(€mn)EBITDA(€mn)

ValueCreation

ValueCreation

ValuationValuation

Earnings rev/momentum

Earnings rev/momentum

ThemeTheme

0

50

100

150

200

250

300

350

2010 2011 2012 2013 2014

Q4

Q3

Q2

Q1

0

100

200

300

400

500

600

700

800

900

2011 2012 2013 2014 2015

Q4

Q3

Q2

Q1

7%

0%

5%

10%

15%

20%

0

5,000

10,000

15,000

20,000

2011 2012 2013 2014 2015e

FCF/yield%

ORACLE/SAPWell positioned in the Cloud – low valuation

29

Global domination in database and ERPVery profitable and huge R&D Successfully maneuvered technological shifts in the past

Oracle at 2016 P/E of 12x – ex cashSAP at 2016 P/E of 14x – ex cash

Improving trends in the cloudContinued FCF growth in the 5-10% range

Cloud threat exaggerated

Oracle

SAP

5%

0%

5%

10%

15%

20%

0

1,000

2,000

3,000

4,000

2011 2012 2013 2014 2015e

FCF/yield%

ValueCreation

ValueCreation

ValuationValuation

Earnings rev/momentum

Earnings rev/momentum

ThemeTheme

SamsungQuality company at a big discount

30

• Strong management • Scale leader in handset and memory

• Uniquely cheap vs own industry and universe

• Estimates slipping (like the industry), but minor compared to valuation

• Tailwinds from mobility growth and increased storage

Dominant in mobile memoryHistorical P/B

51%

25%

22%1%

Samsung Hynix Micron Other

ValueCreation

Valuation

Earnings rev/momentum

Theme

Agenda

31

1 DNB Asset Management

3 Investment Process

2 Portfolio Management Team & Track Record

4 Risk Management

5 Fund Facts

Risk management

• Standard deviation combined with stress tests and common sense

• Low concentration of portfolio - 5/10/40 - rule apply

• Structured process for "Approved Counterparty List"

• Low exposure to counterparties (according to UCITS)

- Maximum 10 % exposure towards "large European Financial institutions"

- 5 % towards others

• Low credit risk in interest bearing instruments

• Robust infrastructure for risk management and control called Worldport32

Controlling Liquidity Risks

33 "Worldport" extracts are examples only

Understanding Portfolio Sensitivities

• Risk system based on GRAM (Citi)

• Challenges the manager's fundamental bias

34

Agenda

35

1 DNB Asset Management

3 Investment Process

2 Portfolio Management Team & Track Record

4 Risk Management

5 Fund Facts

DNB Technology - Fund Profile

Fund managers: Anders Tandberg-Johansen, Sverre Bergland, Erling Thune

Strategy: Long only equity fund

Fund type UCITS: FCP - Long only equity fund

Benchmark: "MSCI World TMT" (66% MSCI Global IT, 22% MSCI Global Telecom Services, 12% MSCI Global Media)

Risk target: 6-10% TE

Number of holdings: 30-60

Country range: Flexible

Inception date: August 16, 2007

36

DNB Technology - Terms

37

ISIN: LU0302296495

Liquidity: Daily

Management fee: 1.5% p.a.

Performance fee: 20% (based on accumulated relative performance, no reset)

Front end fee: Up to 5%

Currency: EUR

Minimum investment: EUR 1000

Domiciled: Luxembourg

As portfolio managers our ambitions are clear

38

Identify winners and losers in changing landscape

Creating uncorrelated absolute returns for investors

Always keeping tight risk management

OsloDNB Asset Management ASDronning Eufemias gate 30N-0021 Oslo, Norway

StockholmDNB Asset Management ABRegeringsgatan 59SE-105 88 Stockholm, Sweden

LuxembourgDNB Asset Management S.A.13, rue GoetheL-1637 Luxembourg

Hong KongDNB Asset Management (Asia) Ltd.99 Queen's Road Central3305-3306, The Center, Hong Kong

The presentation has been prepared in accordance with DNB Asset Management’s General Business Terms. The presentation was prepared for internal use as information for our clients and is not intended for public use or distribution. The information contained herein may not be reproduced without DNB Asset Management’s prior consent.

This presentation was prepared on the basis of publicly available information. DNB Asset Management does not warrant that the information in the presentation is exact, correct or complete. The opinions expressed herein reflect the views of DNB Asset Management at the time. DNB Asset Management reserves the right to change its opinion without notice. Any written material distributed must be seen in the context of the oral presentation. DNB Asset Management will not accept responsibility for direct or indirect losses incurred as a result of the interpretation and/or use of information in this presentation.

This presentation is not an offer or recommendation to purchase or sell financial instruments. Investments in financial instruments are associated with risk, including the possibility that all or part of invested funds may be lost. Historical returns are no guarantee of future returns.

DNB Bank ASA and/or other entities in the DNB Group or employees and/or representatives of the DNB Group may trade in or hold positions in the presented or related financial instruments and may give financial advice or provide banking services linked to such financial instruments. Rules regarding confidentiality and other internal rules limit the exchange of information between different units and group companies in the DNB group. The employees in DNB who prepared this presentation may thus be prevented from using, or be unaware of, information held in other units/companies in the DNB Group that may be relevant to this presentation.

DNB Asset Management AS, a division within DNB Wealth Management, is an entity within the DNB Group registered in the Registry of Business Enterprises under Enterprise Number 880 109 162.

39

Disclaimer

41

Since inceptionDNB TechnologyBenchmark

Fund Market ValueReport Currency USDReturn Type Gross of Management FeeReport Period 2007-08-17 - 2015-08-25

Potential investors should carefully study the various risks associated with investing in the fund as detailed in the prospectus beforeinvesting. The most recent prospectus and the periodical reports may be obtained free of charge from the management company.Past performance is no guarantee for future performance.

MSCI World Global Information Technology / MSCI World Telecom / MSCI World Media (66/22/12)133 434 986

0

50

100

150

200

250

300

Aug.07

Jan.08

Jun.08

Nov.08

Apr.09

Sep.09

Feb.10

Jul.10

Dec.10

May.11

Oct.11

Mar.12

Aug.12

Jan.13

Jun.13

Nov.13

Apr.14

Sep.14

Feb.15

Jul.15

Fund Index

Yearly Returns, %Fund Index Relative

YTD -3,47 -6,26 2,802014 7,90 11,36 -3,46 2013 47,65 31,43 16,232012 9,56 14,27 -4,71 2011 -1,63 -1,23 -0,40 2010 23,28 14,63 8,642009 105,26 59,76 45,492008 -47,78 -59,86 12,08

Accumulated Returns, %Fund Index Relative

3 Years 54,48 35,44 19,045 Years 112,28 91,33 20,95

Report Period 140,56 35,45 105,11

Annualized Returns, %Fund Index Relative

3 Years 15,60 10,64 4,965 Years 16,25 13,86 2,39

Report Period 11,56 3,85 7,71

Annualized Risk Measures 3 Yrs, %Fund Index

Volatility 14,52 11,42Tracking Error 8,36

42

Last 7 yearsDNB TechnologyBenchmark

Fund Market ValueReport Currency USDReturn Type Gross of Management FeeReport Period 2008-08-25 - 2015-08-25

Potential investors should carefully study the various risks associated with investing in the fund as detailed in the prospectus beforeinvesting. The most recent prospectus and the periodical reports may be obtained free of charge from the management company.Past performance is no guarantee for future performance.

MSCI World Global Information Technology / MSCI World Telecom / MSCI World Media (66/22/12)133 434 986

0

50

100

150

200

250

300

Aug.08

Jan.09

Jun.09

Nov.09

Apr.10

Sep.10

Feb.11

Jul. 11 Dec.11

May.12

Oct.12

Mar.13

Aug.13

Jan.14

Jun.14

Nov.14

Apr.15

Fund Index

Yearly Returns, %Fund Index Relative

YTD -3,47 -6,26 2,802014 7,90 11,36 -3,46 2013 47,65 31,43 16,232012 9,56 14,27 -4,71 2011 -1,63 -1,23 -0,40 2010 23,28 14,63 8,642009 105,26 59,76 45,492008 -47,78 -59,86 12,08

Accumulated Returns, %Fund Index Relative

3 Years 54,48 35,44 19,045 Years 112,28 91,33 20,95

Report Period 129,73 55,73 74,00

Annualized Returns, %Fund Index Relative

3 Years 15,60 10,64 4,965 Years 16,25 13,86 2,39

Report Period 12,62 6,53 6,08

Annualized Risk Measures 3 Yrs, %Fund Index

Volatility 14,52 11,42Tracking Error 8,36

43

Last 5 yearsDNB TechnologyBenchmark

Fund Market ValueReport Currency USDReturn Type Gross of Management FeeReport Period 2010-08-25 - 2015-08-25

Potential investors should carefully study the various risks associated with investing in the fund as detailed in the prospectus beforeinvesting. The most recent prospectus and the periodical reports may be obtained free of charge from the management company.Past performance is no guarantee for future performance.

MSCI World Global Information Technology / MSCI World Telecom / MSCI World Media (66/22/12)133 434 986

0

50

100

150

200

250

300

Aug.10

Dec.10

Apr.11

Aug.11

Dec.11

Apr.12

Aug.12

Dec.12

Apr.13

Aug.13

Dec.13

Apr.14

Aug.14

Dec.14

Apr.15

Aug.15

Fund Index

Yearly Returns, %Fund Index Relative

YTD -3,47 -6,26 2,802014 7,90 11,36 -3,46 2013 47,65 31,43 16,232012 9,56 14,27 -4,71 2011 -1,63 -1,23 -0,40 2010 23,28 14,63 8,64

Accumulated Returns, %Fund Index Relative

3 Years 54,48 35,44 19,045 Years 112,28 91,33 20,95

Report Period 112,28 91,33 20,95

Annualized Returns, %Fund Index Relative

3 Years 15,60 10,64 4,965 Years 16,25 13,86 2,39

Report Period 16,25 13,86 2,39

Annualized Risk Measures 3 Yrs, %Fund Index

Volatility 14,52 11,42Tracking Error 8,36

44

Last 3 yearsDNB TechnologyBenchmark

Fund Market ValueReport Currency USDReturn Type Gross of Management FeeReport Period 2012-08-25 - 2015-08-25

Potential investors should carefully study the various risks associated with investing in the fund as detailed in the prospectus beforeinvesting. The most recent prospectus and the periodical reports may be obtained free of charge from the management company.Past performance is no guarantee for future performance.

MSCI World Global Information Technology / MSCI World Telecom / MSCI World Media (66/22/12)133 434 986

0

20

40

60

80

100

120

140

160

180

200

Aug.12

Oct.12

Dec.12

Feb.13

Apr.13

Jun.13

Aug.13

Oct.13

Dec.13

Feb.14

Apr.14

Jun.14

Aug.14

Oct.14

Dec.14

Feb.15

Apr.15

Jun.15

Aug.15

Fund Index

Yearly Returns, %Fund Index Relative

YTD -3,47 -6,26 2,802014 7,90 11,36 -3,46 2013 47,65 31,43 16,232012 9,56 14,27 -4,71

Accumulated Returns, %Fund Index Relative

3 Years 54,48 35,44 19,045 Years

Report Period 54,48 35,44 19,04

Annualized Returns, %Fund Index Relative

3 Years 15,60 10,64 4,965 Years

Report Period 15,62 10,65 4,96

Annualized Risk Measures 3 Yrs, %Fund Index

Volatility 14,52 11,42Tracking Error 8,36

45

Last 12 monthsDNB TechnologyBenchmark

Fund Market ValueReport Currency USDReturn Type Gross of Management FeeReport Period 2014-08-25 - 2015-08-25

Potential investors should carefully study the various risks associated with investing in the fund as detailed in the prospectus beforeinvesting. The most recent prospectus and the periodical reports may be obtained free of charge from the management company.Past performance is no guarantee for future performance.

MSCI World Global Information Technology / MSCI World Telecom / MSCI World Media (66/22/12)133 434 986

0

20

40

60

80

100

120

140

Aug. 14 Sep. 14 Oct. 14 Nov. 14 Dec. 14 Jan. 15 Feb. 15 Mar. 15 Apr. 15 May. 15 Jun. 15 Jul. 15 Aug. 15

Fund Index

Yearly Returns, %Fund Index Relative

YTD -3,47 -6,26 2,802014 7,90 11,36 -3,46

Accumulated Returns, %Fund Index Relative

3 Years5 Years

Report Period -2,18 -4,13 1,95

Annualized Returns, %Fund Index Relative

3 Years5 Years

Report Period -2,18 -4,13 1,95

Annualized Risk Measures 3 Yrs, %Fund Index

VolatilityTracking Error

46

YTDDNB TechnologyBenchmark

Fund Market ValueReport Currency USDReturn Type Gross of Management FeeReport Period 2014-12-31 - 2015-08-25

Potential investors should carefully study the various risks associated with investing in the fund as detailed in the prospectus beforeinvesting. The most recent prospectus and the periodical reports may be obtained free of charge from the management company.Past performance is no guarantee for future performance.

MSCI World Global Information Technology / MSCI World Telecom / MSCI World Media (66/22/12)133 434 986

0

20

40

60

80

100

120

Dec.14

Jan.15

Jan.15

Feb.15

Feb.15

Mar.15

Mar.15

Apr.15

Apr.15

May.15

May.15

Jun.15

Jun.15

Jul. 15Jul. 15Jul. 15 Aug.15

Fund Index

Yearly Returns, %Fund Index Relative

YTD -3,47 -6,26 2,80

Accumulated Returns, %Fund Index Relative

3 Years5 Years

Report Period -3,47 -6,26 2,80

Annualized Returns, %Fund Index Relative

3 Years5 Years

Report Period

Annualized Risk Measures 3 Yrs, %Fund Index

VolatilityTracking Error