Embed Size (px)

Citation preview

DISTRIBUTION

2

Market Update and Strategy Overview

The marketplace has evolved past traditional delivery platforms(1). Now, emerging platforms(2) and non-traditional competition(3) are buying content and rights, forcing the established platforms to step-up their game to diversify the ways they deliver programming, causing them to buy more rights. More companies are buying content and rights than ever before, and we are selling to all of them.

This marketplace evolution affords SPT the ability to capitalize on our unique “all rights under one roof” (4) capabilities of a coordinated strategic approach(5) to customers multi-faceted business objectives.

We are distributing shows from more sources now than ever before:

• Off broadcast (Rules of Engagement, Power of 10)

• Off cable (Rescue Me, Damages)

• 1st run (Judge David Young)

• Internet developed shows (The 9)

• 3rd party acquisitions (G.B.B., Just for Laughs) (6)

• New library strategies (Minisode network)

We are licensing more rights and creating innovative deal structures to best position our content to be relevant to viewers and advertisers. This enables all of our customers to develop new ways to deliver content to survive/thrive in a fiercely competitive marketplace.

1.Cable networks, TV shows, MSO’s, satellite companies.2.VOD, internet, mobile.3.Comcast, Google, mobile.4.SPT houses all rights – broadcast, cable, satellite.5.Next cycle Seinfeld offering.6.We have acquired rights for 3rd party distribution for shows from broadcast, cable, and foreign at no financial risk to SPT.

3

Distribution Sales – Total Revenues

$216

$285

$264$318

$164

$113

$113 $122

$110

$867

$695

$754$728

$190

$377$286

$210

$78$91

$107

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

FY07 FY08 FY09 FY10

($ in MM) Free/Basic TV PayTV Syndication Pay Per View/VOD

Budget/ Prior MRP

$846 $663

Variance $21 $32

$631

$123

SPT will generate over $867 million in total current and library sales for SPE

[Last Year’s Numbers]

4

Free / Basic TV

Market Dynamic MRP Initiatives

Cable networks growing appetite for original programming is coming at the direct expense of acquisition budgets.[1]

For movies and TV shows, we are employing new strategic initiatives and licensing new rights to make the most money and become vital partners with our clients:

New internal ratings systems;Shorter and dual windowing;Inclusion of barter;Repurposing;Network VOD/SVOD;Network branded MSO VOD;EST.

[1] The question asked is “should we buy 50 runs of Spider-Man or launch 2 original series.” In spite of the answer, we sold Spider-Man 3 (35 million) for the biggest movie deal of any kind in 2 years, and Seinfeld’s last cycle (65 million) for a record price.

•Increase revenue by 2 to 3% by increasing sales of

non-linear digital rights and monetizing them across

non-traditional and traditional platforms

•Increase library film sales by 5% by utilizing newly

developed ratings and competitive database to

analyze genre performance by network and target

presentations to highlight top performing movies by

genre to the appropriate networks

•Increase library film sales by 2-3% by converting

“event” movie buyers into ongoing buyers (e.g.,

Hallmark, G4, and E!)

•Increase library sales by 1-2% by converting non-

buyers (e.g., TV Land, Nick @ Nite, and SoapNet)

into at least occasional buyers

5

Free / Basic TV – Revenues

$377

$190

$286

$210

$370

$171$152

$0

$50

$100

$150

$200

$250

$300

$350

$400

FY07 FY08 FY09 FY10

Q2/MRP Budget/Prior MRP

[Last Year’s Numbers]

6

Syndication

Market Dynamic MRP Initiatives

The consolidation of buyers has created the need for SPT to partner and co-develop programs for 1st run programming. This vests the client in our mutual success.

Off net programming continues to be a highly desired product that premiums are paid for.

For library sales, we are creating new clients (GTN) and developing smaller buyers into big volume buyers (ION).

•Continue aggressive sales efforts of all library, movie packages and all current and new product

–Sell King of Queens 2nd cycle increasing US coverage from 82% to 95% while maintaining our double runs and strong time period exposure

–Lay the ground work in support of upcoming 4th cycle renewal of Seinfeld while maintaining our strong time period exposure

–Continue to push our court shows – upgrades and renewals for Judge Maria Lopez (moving from CW+ to mkt by mkt sale in bottom 100 in Fall 2008) and Judge David Young and coming up with potential alternatives for Judge Hatchett (if needed) in 2008

–Increase product offering in first run syndication: The 9, Power of 10, Judge Karen, etc.

–In response to a request from Ad Sales for ethnic sitcoms with barter, bring Steve Harvey back as a ad-supported strip in 2008

•Expand our streaming of products onto local TV station, cable network and portal websites

•Secure additional 3rd party products (e.g., Bananas deal)

•Expand distribution of library product and features through digital second channel owners, including GTN

•Exploit the relationship with WGN+ for new library sales

•Continue to exploit the opportunities with ION Television and Spanish Language channels (Telemundo, Univision, TeleFutura, etc)

•Pursue co-development deals with NBC, Tribune and other station groups to guarantee key time periods when launching new 1st run programs

7

Syndication – Revenues

$164

$113 $113$122

$149

$103 $106

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

FY07 FY08 FY09 FY10

Q2/MRP Budget/Prior MRP

[Last Year’s Numbers]

8

Pay Per View / VOD

Cable Market MRP Initiatives

Satellite Market MRP Initiatives

•Cable companies continue to be focused on the triple play. They are committed to being the single provider of distribution/pipes into the home: TV, voice, data.

•Clients are eager to improve the traditional PPV/VOD offerings and are seeking earlier windows and HD rights.

•Cable MSOs continue to focus on sales of their high-speed offerings

•Provide a full bouquet of Sony content across all the MSO distributed products

•Our primary product is traditional PPV/VOD rights. SPT has locked a 3 year extension output deal for PPV/VOD rights (expires Dec 31, 2010).

•SPT is leveraging such interest in PPV / VOD to bring more value to Sony product, (e.g. better placement, higher pricepoints, higher take to Sony)

•SPT is expanding our licensing discussions to on-line rental VOD and EST based on MSO focus on high-speed services

•Satellite companies are desperately trying to catch up to cable with respect to VOD and broadband. As satellite companies continue to be threatened by the triple play, satellite companies are also creating new products for their home customers.

•DIRECTV and EchoStar are building out a closed IP delivered products to the home

•Provide a full bouquet of Sony content across all the satellite distributed products.

•Our primary product is traditional PPV rights. Leveraging satellite's need to provide VOD, SPT is in negotiations for PPV/VOD output deals with both DIRECTV and EchoStar.

•Securing commitment from DIRECTV SPT FOD product.

•Securing commitment from EchoStar to carry The Minisode Network.

9

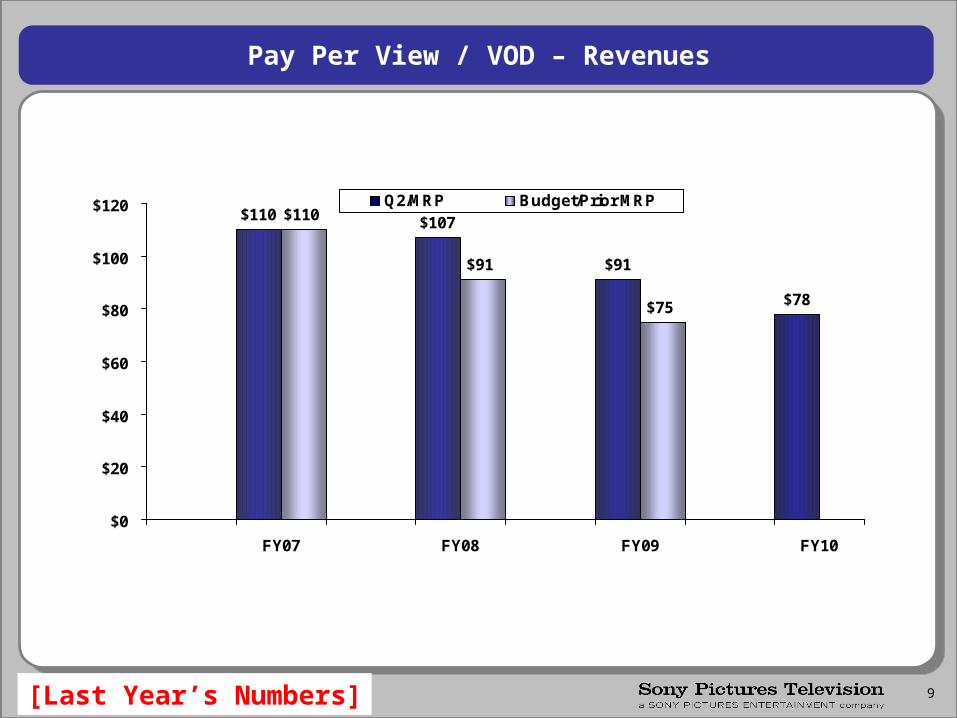

Pay Per View / VOD – Revenues

$110 $107

$91

$78

$110

$91

$75

$0

$20

$40

$60

$80

$100

$120

FY07 FY08 FY09 FY10

Q2/MRP Budget/Prior MRP

[Last Year’s Numbers]

10

Pay TV – Strategy

• Exercise the Starz option. Once exercised, the deal will expire December 31, 2013.

• Secure an additional long-term Pay TV extension with Starz.

• Anticipate and analyze the issues that will be raised in such discussions, including but not limited to:

– Caps on Sony's theatrically released product– Expansion of on demand rights– Reductions in overall license fees– Earlier windows to Pay TV

• Starz is committed to establishing an on-line presence through VONGO. SPT's strategy is to provide a full bouquet of Sony content across all Starz distributed products.

• SPT has closed a rental on-line VOD deal. SPT is negotiating EST, The Minisode Network and SPT on-line channels.

• Close library deals with Showtime and HBO

11

Pay TV – Revenues

$216

$285$264

$318

$217

$298 $298

$0

$50

$100

$150

$200

$250

$300

$350

FY07 FY08 FY09 FY10

Q2/MRP Budget/Prior MRP

[Last Year’s Numbers]

12

Title PPV Pay TV Free TV Title PPV Pay TV Free TV Title PPV Pay TV Free TV

SPIDER-MAN 3 $8,500 $22,500 $50,000 VACANCY $2,500 $9,510 $6,500 PERFECT STRANGER $3,000 $0 $0SUPERBAD $3,000 $10,350 $6,500 RESIDENT EVIL 3 $2,160 $9,510 $4,000 ARE WE DONE YET? $4,880 $0 $0VANTAGE POINT $2,950 $13,450 $11,380 BONE DEEP $2,380 $7,830 $4,880 BROTHERS SOLOMON $1,130 $0 $030 DAYS OF NIGHT $2,160 $9,290 $4,000 UNTRACEABLE $2,500 $9,510 $6,500 NEXT $3,025 $0 $0THE OTHER BOLEYN GIRL $2,500 $9,510 $6,500 THIS CHRISTMAS $1,890 $8,850 $3,060 ACROSS THE UNIVERSE $3,000 $0 $0WALK HARD $3,750 $11,130 $8,130 UNDERWORLD 3 $2,250 $10,460 $7,310 WATERHORSE $3,750 $0 $0

STEP FATHER $2,350 $7,830 $4,880

TOTAL $22,860 $76,230 $86,510 TOTAL $16,030 $63,500 $37,130 TOTAL $18,785 $0 $0

Title PPV Pay TV Free TV Title PPV Pay TV Free TV Title PPV Pay TV Free TV

SURF'S UP $5,000 $18,890 $19,500 TBD#1-2008 $10 $90 $300 A HOPE $700 $2,830 $780TBD#2-2008 $800 $2,560 $300 LUST, CAUTION $300 $1,300 $500

TOTAL $5,000 $18,890 $19,500 TBD#3-2008 $10 $290 $170TBD#4-2008 $5 $190 $80 TOTAL $1,000 $4,130 $1,280

TBD#5-2008 $10 $380 $150TBD#6-2008 $20 $440 $220TBD#7-2008 $800 $2,560 $300TBD#8-2008 $10 $580 $150TBD#9-2008 $10 $90 $190 Title PPV Pay TV Free TV

TBD#10-2008 $10 $290 $170 TBDTBD#11-2008 $5 $190 $80TBD#12-2008 $10 $380 $180TBD#14-2008 $455 $2,340 $250TBD#15-2008 $10 $380 $450TBD#16-2008 $10 $380 $150TBD#17-2008 $10 $180 $190TBD#18-2008 $10 $750 $290TBD#19-2008 $5 $190 $80

TOTAL $2,200 $12,260 $3,700

SPT will generate over $389 million in sales from the FY08 slate

[Updated / Reformat]

Distribution Sales – FY08 Slate

13

Library Sales – Market Trends

The consistent licensing of our library product is evolving with new business models and applications

• Dual windowing (Just Shoot Me – cable and broadcast)

• 3rd party distribution (RTN – premium guarantees)

• Repacking library products (Minisodes)

14

$73 $77$66

$77

$20

$17

$8

$90

$77

$102

$5

$5

$60

$5

$6

Forecast $150 +

$0

$20

$40

$60

$80

$100

$120

$140

$160

FY07 FY08 FY09 FY10

($ in MM) Free/Basic Pay TV PPV/VOD

Library Sales Targets by Market

• 3 year annual average of $106MM in FY07-FY09, and $90MM in FY08-FY10

• 4 year annual average of $105MM

In-House $103MM

Budget $65MM

Last Year’s Numbers]

15

$10 $10 $10 $10

$10

$10 $10

10 10 10 10

$40 $40 $40

$10$10$10

$10$10

Forecast $100+

$0

$10

$20

$30

$40

$50

$60

FY07 FY08 FY09 FY10

($ in MM) Free/Basic Pay TV PPV/VOD Digital

Library Revenue Targets by Market

• 3 year annual average of $xxMM in FY07-FY09, and $xxMM in FY08-FY10

• 4 year annual average of $xxMM

[Placeholder Numbers]

16

Library Revenue by Division

$76

$33

$52

$27

$44

$46

$48

$28

$34

$26

$26

$18

$11

$36$33

$75

$42 $40

$32 $30

$16

$0

$20

$40

$60

$80

$100

$120

$140

$160

FY07 FY08 FY09 FY10

$133

$111

$81

$124

$77

$101

$146

Q2/BDGT. MRP/PRIOR MRP/PRIOR MRP

TV SPHEMPG

In-House

$103MM

In-House $62MM

In-House $77MM

In-House $31MM

NOTE: Assumes a consistent volume and quality of SPHE acquired product.

($ in MM)

[Placeholder Numbers]

17

Digital Distribution Landscape: Growing Demand

1,170

1,691

2,191

2,629

447

651

846

1,3502,100

3,100

4,300

775

774

2007 2008 2009 2010 2011

Ads TV Downloads* MovieDownloads*

U.S. Consumer /Advertiser Spending ($M)

$1,663$1,663

$2,765$2,765

$7,775$7,775

$4,238$4,238

$5,942$5,942

Source: eMarketer; *includes DST and rental

• Spending on paid and ad-supported content is forecasted to grow at double-digit rates well into the next decade

• Studios are continuing to make an increasing amount of premium content available for digital distribution

– Primetime TV, movies, and original content

• Content owners are leveraging wide distribution networks, rather than exclusivity, to drive demand

– NBCU and Fox to launch JV “Hulu” in Q4 as well as distributing through Yahoo! and MSN

• TV and movie content is fully cross platform utilizing a variety of business models

– Ad supported streams on ABC.com and DST on iTunes

– DST and VOD on XBox360– Ad supported and subscription TV and movies on

Verizon Wireless and Sprint

18

Digital Distribution

SPT Strategy & Financials

Total Revenue

• Aggressively build the distribution network– Strike partnerships across the complete spectrum of traditional and on-line players

• Continue to expand the overall content offering– Broaden selection of film and TV product– Introduce the most compelling short-form/original content into the offering

• Continue to lead the market in innovating the digital product offering and usage models– Focus on Digital Sell-Through as foundational/core product

• Build a strong, retail-focused organization – Create innovative marketing and promotional programs – Continue to lead the industry with respect to asset delivery and digital operations

19

Case Study: Digital Marketing

Digital has provided new opportunities and SPT has enhanced marketing efforts to support the distribution and promotion of all content across platforms

MaterialsMaterials

Partner Promos

Partner Promos

• Creating materials to market both offline and online content

– Developed HD promotional packages for Seinfeld

– Designing collateral for to support DST partners (iTunes, Amazon) and mobile games (Wheel and Jeopardy)

• Developing digital experiences with partners to promote core assets

– Built-out Seinfeld and Boondocks MySpace pages

– Planning multiple Seinfeld UGC contests on Yahoo!

– Working on Y&R and Days Tivocasts

• Developing digital experiences of our own

– Designing direct-to-consumer sites for Minisodes and Buried Alive

– Developing Y&R websites in support of 35th anniversary

– Managing on-going Rescue Me campaign on Crackle’s Firehouse channel

“Owned” Initiatives

“Owned” Initiatives

[Revised]

20

Mobile Overview

• Taken responsibility for game development from SPDE and coordinating greenlights with SPTI– Slating 8 games per year

• Now directly responsible for personalization products focusing on– Tones/graphics based on film/TV properties– Packages based on compelling brands/themes

• Market approach– Close carrier relationships and marketing support– Consistent product development– Reinvigorate the library

SPT Strategy & Financials

$2.0

$6.0

$8.0

$2.0

$4.0

$6.0

$8.0

$4.0

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

Q2/ BGT FY08 FY09 FY10

($ in MM)

$15.0

$25.0

$30.0

$15.0

$20.0

$25.0

$30.0

$20.0

$0

$5

$10

$15

$20

$25

$30

$35

FY07 FY08 FY09 FY10

($ in MM)EBIT Total Revenue

[Placeholder Numbers]

Budget/Prior MRPQ2/MRP