Embed Size (px)

Citation preview

Objective Findings Comments

Discussion on “Stagnation Traps”

Jang-Ting Guo

Department of EconomicsUniversity of California, Riverside

May 15, 2015

Jang-Ting Guo Discussion on “Stagnation Traps” 1 / 12

Objective Findings Comments

Existence and Persistence of Stagnation Trap in a MonetaryEndogenous Growth Model with Quality Ladders

⇒ Coexistence of Positive Unemployment, Low Growth, andLiquidity Trap

The Key Mechanism

(1) Unemployment and Weak Aggregate Demand ⇒ ReducesFirms’ Investment in Innovation ⇒ Low Growth

(2) Low Growth ⇒ Reduces Real Interest Rate ⇒ PushesNominal Interest Rate to Zero

Jang-Ting Guo Discussion on “Stagnation Traps” 2 / 12

Objective Findings Comments

Existence and Persistence of Stagnation Trap in a MonetaryEndogenous Growth Model with Quality Ladders

⇒ Coexistence of Positive Unemployment, Low Growth, andLiquidity Trap

The Key Mechanism

(1) Unemployment and Weak Aggregate Demand ⇒ ReducesFirms’ Investment in Innovation ⇒ Low Growth

(2) Low Growth ⇒ Reduces Real Interest Rate ⇒ PushesNominal Interest Rate to Zero

Jang-Ting Guo Discussion on “Stagnation Traps” 2 / 12

Objective Findings Comments

Two Steady States in Baseline Model

(1) Full Employment y f = 1, High Growth g f , PositiveNominal Interest Rate i f > 0, and Positive/Negative InflationRate πf ≷ 1

(2) Unemployment yu < 1, Low Growth gu < g f , ZeroNominal Interest Rate iu = 0, and Negative Inflation Rateπu < 1

Two Extensions: Precautionary Savings and Time-VaryingInflation Rate

Constant or Countercyclical Subsidy to Firms’ Investment inInnovation ⇒ Removal of Low-Growth Steady State

Jang-Ting Guo Discussion on “Stagnation Traps” 3 / 12

Objective Findings Comments

Two Steady States in Baseline Model

(1) Full Employment y f = 1, High Growth g f , PositiveNominal Interest Rate i f > 0, and Positive/Negative InflationRate πf ≷ 1

(2) Unemployment yu < 1, Low Growth gu < g f , ZeroNominal Interest Rate iu = 0, and Negative Inflation Rateπu < 1

Two Extensions: Precautionary Savings and Time-VaryingInflation Rate

Constant or Countercyclical Subsidy to Firms’ Investment inInnovation ⇒ Removal of Low-Growth Steady State

Jang-Ting Guo Discussion on “Stagnation Traps” 3 / 12

Objective Findings Comments

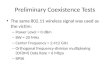

Two Steady States: y f = 1 and yu < 1

⇒ y Denotes the Level of Actual Output

⇒ 1− y = Output Gap

Figure 1 ⇒ Local Stability Property of Each Steady State:Saddle, Sink or Source

Possibility of Global Indeterminacy ⇒ Various Forms ofBifurcations

Jang-Ting Guo Discussion on “Stagnation Traps” 4 / 12

Objective Findings Comments

Two Steady States: y f = 1 and yu < 1

⇒ y Denotes the Level of Actual Output

⇒ 1− y = Output Gap

Figure 1 ⇒ Local Stability Property of Each Steady State:Saddle, Sink or Source

Possibility of Global Indeterminacy ⇒ Various Forms ofBifurcations

Jang-Ting Guo Discussion on “Stagnation Traps” 4 / 12

(yu, gu)

(1, gf )

AD

GG

gro

wth

g

output gap y

Objective Findings Comments

This Paper

max∞∑t=0

βtC 1−σt − 1

1− σ, 0 < β < 1

Ct = exp

(∫ 1

0ln qjtcjtdj

)and Qt = exp

(∫ 1

0lnqjtdj

)(ct+1

ct

)σ

= β (1 + rt) g1−σt+1 , where gt+1 =

Qt+1

Qt

Need σ > 1 such that

(1) Positive Relationship between Present Consumption andInnovation Growth

(2) Existence of Unemployment Steady State

(3) i f > 0 at Full-Employment Steady State

Jang-Ting Guo Discussion on “Stagnation Traps” 5 / 12

Objective Findings Comments

This Paper

max∞∑t=0

βtC 1−σt − 1

1− σ, 0 < β < 1

Ct = exp

(∫ 1

0ln qjtcjtdj

)and Qt = exp

(∫ 1

0lnqjtdj

)(ct+1

ct

)σ

= β (1 + rt) g1−σt+1 , where gt+1 =

Qt+1

Qt

Need σ > 1 such that

(1) Positive Relationship between Present Consumption andInnovation Growth

(2) Existence of Unemployment Steady State

(3) i f > 0 at Full-Employment Steady State

Jang-Ting Guo Discussion on “Stagnation Traps” 5 / 12

Objective Findings Comments

Alternative Specification (Footnote 14)

max∞∑t=0

βtc1−σt − 1

1− σ, 0 < β < 1

yt = f

(∫ 1

0qjtXjtdj

)= f (Qt)

(ct+1

ct

)σ

= β (1 + rt)

(ct+1

ct

)σ

= β (1 + rt) g1−σt+1 , where gt+1 =

Qt+1

Qt

⇒ Isomorphic Formulations Only When σ = 1

Jang-Ting Guo Discussion on “Stagnation Traps” 6 / 12

Objective Findings Comments

Alternative Specification (Footnote 14)

max∞∑t=0

βtc1−σt − 1

1− σ, 0 < β < 1

yt = f

(∫ 1

0qjtXjtdj

)= f (Qt)

(ct+1

ct

)σ

= β (1 + rt)

(ct+1

ct

)σ

= β (1 + rt) g1−σt+1 , where gt+1 =

Qt+1

Qt

⇒ Isomorphic Formulations Only When σ = 1

Jang-Ting Guo Discussion on “Stagnation Traps” 6 / 12

Objective Findings Comments

This Paper

Euler:

(ct+1

ct

)σ

= β(1 + it)

πg1−σt+1

Growth : 1 = β

[(ctct+1

)σ

g1−σt+1 (χ

γ − 1

γyt+1 + 1− ln gt+2

ln γ)

]When σ > 1⇒ Positive Relationship between yt+1 and gt+1

Market Clearing: ct +ln gt+1

χ ln γ= yt

Monetary Policy: 1 + it = max{

(1 + ı) yφt , 1}

Jang-Ting Guo Discussion on “Stagnation Traps” 7 / 12

Objective Findings Comments

This Paper

Euler:

(ct+1

ct

)σ

= β(1 + it)

πg1−σt+1

Growth : 1 = β

[(ctct+1

)σ

g1−σt+1 (χ

γ − 1

γyt+1 + 1− ln gt+2

ln γ)

]When σ > 1⇒ Positive Relationship between yt+1 and gt+1

Market Clearing: ct +ln gt+1

χ ln γ= yt

Monetary Policy: 1 + it = max{

(1 + ı) yφt , 1}

Jang-Ting Guo Discussion on “Stagnation Traps” 7 / 12

Objective Findings Comments

Alternative Specification

Period Utility:c1−σt − 1

1− σ

Final Good: Yt = A

∫ 1

0(qjtXjt)

αdj , A > 0, 0 < α < 1

Demand for Xjt : Xjt =

(AαqαjtPjt

) 11−α

Supply for Xjt : Xjt = Ljt , where

∫ 1

0Ljtdj + LRDt + Ut = L

R&D Firms’ Profits: πjt = (Pjt −Wt)Xjt ,Wt

Wt−1= π

Jang-Ting Guo Discussion on “Stagnation Traps” 8 / 12

Objective Findings Comments

Alternative Specification

Period Utility:c1−σt − 1

1− σ

Final Good: Yt = A

∫ 1

0(qjtXjt)

αdj , A > 0, 0 < α < 1

Demand for Xjt : Xjt =

(AαqαjtPjt

) 11−α

Supply for Xjt : Xjt = Ljt , where

∫ 1

0Ljtdj + LRDt + Ut = L

R&D Firms’ Profits: πjt = (Pjt −Wt)Xjt ,Wt

Wt−1= π

Jang-Ting Guo Discussion on “Stagnation Traps” 8 / 12

Objective Findings Comments

Alternative Specification

Period Utility:c1−σt − 1

1− σ

Final Good: Yt = A

∫ 1

0(qjtXjt)

αdj , A > 0, 0 < α < 1

Demand for Xjt : Xjt =

(AαqαjtPjt

) 11−α

Supply for Xjt : Xjt = Ljt , where

∫ 1

0Ljtdj + LRDt + Ut = L

R&D Firms’ Profits: πjt = (Pjt −Wt)Xjt ,Wt

Wt−1= π

Jang-Ting Guo Discussion on “Stagnation Traps” 8 / 12

Objective Findings Comments

Monopoly Pricing: Pjt =Wt

α

Equilibrium Quantity: Xjt =

(Aα2qαjtWt

) 11−α

Aggregate Output: Yt = A1

1−αα2α1−αW

−α1−αt Qt ,

where Qt =

∫ 1

0q

α1−α

jt dj

Equilibrium Profit: πjt = α(1− α)qα

1−α

jt

Yt

Qt

Jang-Ting Guo Discussion on “Stagnation Traps” 9 / 12

Objective Findings Comments

Monopoly Pricing: Pjt =Wt

α

Equilibrium Quantity: Xjt =

(Aα2qαjtWt

) 11−α

Aggregate Output: Yt = A1

1−αα2α1−αW

−α1−αt Qt ,

where Qt =

∫ 1

0q

α1−α

jt dj

Equilibrium Profit: πjt = α(1− α)qα

1−α

jt

Yt

Qt

Jang-Ting Guo Discussion on “Stagnation Traps” 9 / 12

Objective Findings Comments

Probability of Innovating =χLRDtL

= χµt

Value Function: Vt = β

(ct+1

ct

)−σ[πjt+1 + (1− χµt+1)Vt+1]

Free Entry: LRDt Wt = χµtVt ⇒ LWt = χVt

Innovation Growth: gt+1 =Qt+1

Qt= χµtγ

α1−α ⇒ Yt+1

Yt= gt+1π

−α1−α

Growth: 1 =(βπ

σα1−α

)g−σt+1

[α(1− α)q

α1−α

j(t+1)

χYt+1

LWtQt+1+ π(1− gt+2

γα

1−α

)]

When σ > 0⇒ Positive Relationship betweenYt+1

Qt+1and gt+1

Jang-Ting Guo Discussion on “Stagnation Traps” 10 / 12

Objective Findings Comments

Probability of Innovating =χLRDtL

= χµt

Value Function: Vt = β

(ct+1

ct

)−σ[πjt+1 + (1− χµt+1)Vt+1]

Free Entry: LRDt Wt = χµtVt ⇒ LWt = χVt

Innovation Growth: gt+1 =Qt+1

Qt= χµtγ

α1−α ⇒ Yt+1

Yt= gt+1π

−α1−α

Growth: 1 =(βπ

σα1−α

)g−σt+1

[α(1− α)q

α1−α

j(t+1)

χYt+1

LWtQt+1+ π(1− gt+2

γα

1−α

)]

When σ > 0⇒ Positive Relationship betweenYt+1

Qt+1and gt+1

Jang-Ting Guo Discussion on “Stagnation Traps” 10 / 12

Objective Findings Comments

Probability of Innovating =χLRDtL

= χµt

Value Function: Vt = β

(ct+1

ct

)−σ[πjt+1 + (1− χµt+1)Vt+1]

Free Entry: LRDt Wt = χµtVt ⇒ LWt = χVt

Innovation Growth: gt+1 =Qt+1

Qt= χµtγ

α1−α ⇒ Yt+1

Yt= gt+1π

−α1−α

Growth: 1 =(βπ

σα1−α

)g−σt+1

[α(1− α)q

α1−α

j(t+1)

χYt+1

LWtQt+1+ π(1− gt+2

γα

1−α

)]

When σ > 0⇒ Positive Relationship betweenYt+1

Qt+1and gt+1

Jang-Ting Guo Discussion on “Stagnation Traps” 10 / 12

Objective Findings Comments

Alternative Specification

Euler:

(ct+1

ct

)σ

= β(1 + it)

π

Growth: 1 =(βπ

σα1−α

)g−σt+1

[α(1− α)q

α1−α

j(t+1)

χYt+1

LWtQt+1+ π(1− gt+2

γα

1−α

)]

When σ > 0⇒ Positive Relationship betweenYt+1

Qt+1and gt+1

Market Clearing: ct = Yt ⇒ct+1

ct=

Yt+1

Yt= gt+1π

−α1−α

Monetary Policy: 1 + it = max{(1 + i)Yt

Qt, 1}

Jang-Ting Guo Discussion on “Stagnation Traps” 11 / 12

Objective Findings Comments

Alternative Specification

Euler:

(ct+1

ct

)σ

= β(1 + it)

π

Growth: 1 =(βπ

σα1−α

)g−σt+1

[α(1− α)q

α1−α

j(t+1)

χYt+1

LWtQt+1+ π(1− gt+2

γα

1−α

)]

When σ > 0⇒ Positive Relationship betweenYt+1

Qt+1and gt+1

Market Clearing: ct = Yt ⇒ct+1

ct=

Yt+1

Yt= gt+1π

−α1−α

Monetary Policy: 1 + it = max{(1 + i)Yt

Qt, 1}

Jang-Ting Guo Discussion on “Stagnation Traps” 11 / 12

(yu, gu)

(1, gf )

AD

GG

gro

wth

g

output gap y

Objective Findings Comments

At Unemployment Steady State

(1) Baseline π < 1⇒ Deflation

Extension with Precautionary Savings, but UnemployedHouseholds Cannot Borrow or Trade Firms’ Shares

(2) Zero Nominal Interest Rate iu = 0

Negative Nominal Interest Rates Observed in Europe: ECB’sDeposit Rate of −0.2%, and Swiss National Bank’s DepositRate of −0.75%

⇒ 1 + it = max{

(1 + ı) yφt , i}

, where i¯< 1

Jang-Ting Guo Discussion on “Stagnation Traps” 12 / 12

Objective Findings Comments

At Unemployment Steady State

(1) Baseline π < 1⇒ Deflation

Extension with Precautionary Savings, but UnemployedHouseholds Cannot Borrow or Trade Firms’ Shares

(2) Zero Nominal Interest Rate iu = 0

Negative Nominal Interest Rates Observed in Europe: ECB’sDeposit Rate of −0.2%, and Swiss National Bank’s DepositRate of −0.75%

⇒ 1 + it = max{

(1 + ı) yφt , i}

, where i¯< 1

Jang-Ting Guo Discussion on “Stagnation Traps” 12 / 12

(1, gf )

AD

GG

gro

wth

g

output gap y