Embed Size (px)

Citation preview

153

CHAPTER VII

DISCLOSURE OF INTANGIBLE ASSETS – COMPARISON

OF COMPANIES IN INDIA AND UK

While several intangible assets reporting studies have been carried out in

developed nations, there is still a dearth of comparative studies on intangible assets

disclosure between developed and developing countries. This chapter contributes to

understanding of intangible assets disclosure practices by comparing firms in India (a

developing country) and United Kingdom (a developed country).

The idea that different countries may be characterised by different reporting

behaviours is not new (Ahmed and Courtis, 1999). Recent decades have seen some

gradual convergence in accounting practice and disclosure cultures, scope still exists for

considerable variation across national boundaries (Vanstraelen et al., 2003) particularly in

the area of voluntary intangible assets disclosures. Macro or national level factors such as

business culture (Jaggi and Low, 2000), legal systems (Hope, 2003), historical

developments, government regulation, professional influence and taxation cultures

(Adhikari et al., 1998; Meek and Gray, 1989; Ball et al., 2000) influences variations in

disclosure practices across national boundaries. Abeysekera (2008) also pointed out that

different factors may intervene in determining intangible assets disclosure of firms,

whether it is a developed, moderately developed, or developing country could be one of

them.

The comparison on Indian and UK intangible assets disclosure practices has been

done on the basis attribute-wise disclosure, nature of disclosure, category-wise

disclosure and company-wise disclosure by applying the intangible assets disclosure

index to the annual reports of sample companies from both the countries.

There are four sections in this chapter. Section I discusses attribute-wise

disclosure, section II explains the nature of disclosure and section III deals with category

wise disclosure and section IV discusses the company-wise disclosure scores of sample

companies from India and UK.

154

SECTION I

7.1. ATTRIBUTE WISE DISCLOSURE IN ANNUAL REPORTS

This section explains the attribute-wise analysis for each and every category of

intangible assets disclosure index. Table 7.1 presents the attribute-wise disclosure both in

absolute figures as well as in percentages for sample companies from India and UK for

the year 2007-08. The attribute-wise disclosure score in the table has been calculated as

per methodology discussed in chapter-V1. The maximum disclosure score for attributes in

human capital, external capital, internal capital, intangible assets scoresheet and for

attribute intangible assets valuation in mandatory disclosure requirement category is 184

(92 companies multiply with maximum score of 2) in case of UK companies. The

maximum score for remaining attributes in mandatory disclosure requirement category is

92 (92 companies multiply with maximum score of 1) in case of UK companies.

For example, the number of employees attribute in human capital category in UK

has weighted disclosure score of 153 and the percentage disclosure of 83.15% (by

dividing the score attained 153 by 184 maximum disclosure score).

A brief look at the table shows that disclosure score is higher for UK companies

than Indian companies for all the attributes in external capital and mandatory disclosure

requirement category. In human capital and internal capital category, for some attributes

UK companies score higher than Indian companies and while for other attributes visa-a-

versa is true. The detailed analysis of disclosure for each attribute is given below:

1 For details refer Chapter – V, Extent of Disclosure, pp.68

155

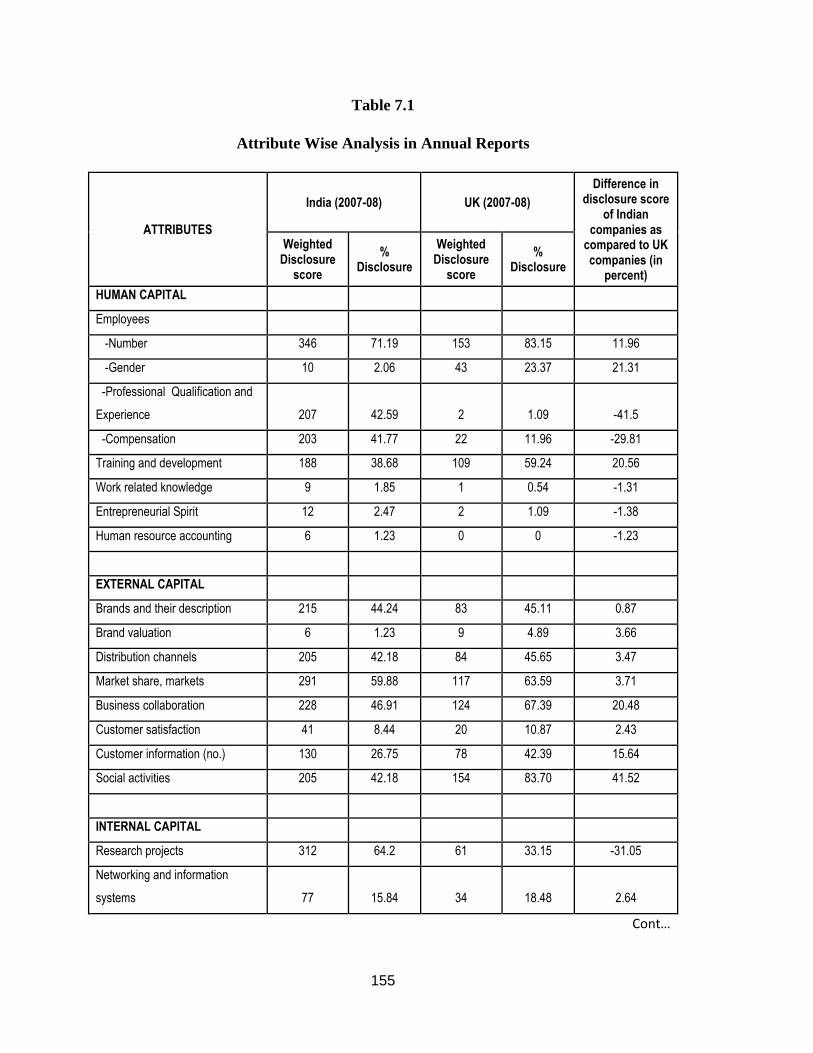

Table 7.1

Attribute Wise Analysis in Annual Reports

ATTRIBUTES

India (2007-08) UK (2007-08)

Difference in disclosure score

of Indian companies as

compared to UK companies (in

percent)

Weighted Disclosure

score

% Disclosure

Weighted Disclosure

score

% Disclosure

HUMAN CAPITAL

Employees

-Number 346 71.19 153 83.15 11.96

-Gender 10 2.06 43 23.37 21.31

-Professional Qualification and

Experience 207 42.59 2 1.09 -41.5

-Compensation 203 41.77 22 11.96 -29.81

Training and development 188 38.68 109 59.24 20.56

Work related knowledge 9 1.85 1 0.54 -1.31

Entrepreneurial Spirit 12 2.47 2 1.09 -1.38

Human resource accounting 6 1.23 0 0 -1.23

EXTERNAL CAPITAL

Brands and their description 215 44.24 83 45.11 0.87

Brand valuation 6 1.23 9 4.89 3.66

Distribution channels 205 42.18 84 45.65 3.47

Market share, markets 291 59.88 117 63.59 3.71

Business collaboration 228 46.91 124 67.39 20.48

Customer satisfaction 41 8.44 20 10.87 2.43

Customer information (no.) 130 26.75 78 42.39 15.64

Social activities 205 42.18 154 83.70 41.52

INTERNAL CAPITAL

Research projects 312 64.2 61 33.15 -31.05

Networking and information

systems 77 15.84 34 18.48 2.64

Cont…

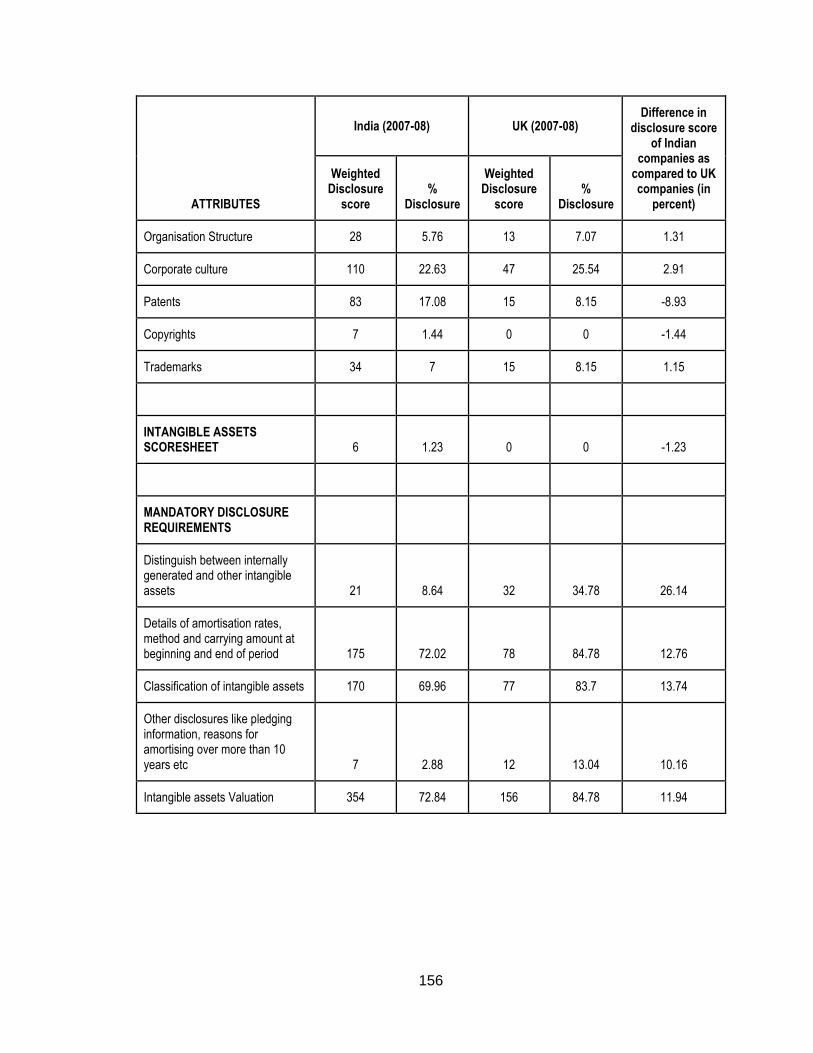

156

ATTRIBUTES

India (2007-08) UK (2007-08) Difference in

disclosure score of Indian

companies as compared to UK companies (in

percent)

Weighted Disclosure

score %

Disclosure

Weighted Disclosure

score %

Disclosure

Organisation Structure 28 5.76 13 7.07 1.31

Corporate culture 110 22.63 47 25.54 2.91

Patents 83 17.08 15 8.15 -8.93

Copyrights 7 1.44 0 0 -1.44

Trademarks 34 7 15 8.15 1.15

INTANGIBLE ASSETS SCORESHEET 6 1.23 0 0 -1.23

MANDATORY DISCLOSURE REQUIREMENTS

Distinguish between internally generated and other intangible assets 21 8.64 32 34.78 26.14

Details of amortisation rates, method and carrying amount at beginning and end of period 175 72.02 78 84.78 12.76

Classification of intangible assets 170 69.96 77 83.7 13.74

Other disclosures like pledging information, reasons for amortising over more than 10 years etc 7 2.88 12 13.04 10.16

Intangible assets Valuation 354 72.84 156 84.78 11.94

157

7.1.1. HUMAN CAPITAL

Human capital consists of basic value drivers for any firm. This category

comprises total eight attributes which are number of employees, gender, professional

qualification and experience, compensation, training and development, work-related

knowledge, entrepreneurial spirit and human resource accounting.

The first human capital attribute number of employees has weighted disclosure

score of 71.19% for Indian companies and 83.15% for UK companies. It is the most

highly disclosed intangible assets attribute in human capital category in both India and

UK (Table 7.2).High disclosure concerning this attribute ratifies its importance for

corporates in both the nations. Cobham plc a UK based company reported “At the end of

2007, Cobham employed 9,500 people on five continents with major population centres

in the UK, continental Europe, North America and Australia.” (Cobham plc, Annual

report 2007, p.30). This information is helpful for investor to understand that Cobham plc

has operations in 5 continents and information on change in number of their employees

could indicate future growth prospects of the company.

Gender of employees is the next intangible assets attribute in human capital

category which has very low disclosure score of 2.06% in case of Indian companies. The

disclosure score concerning this attribute is higher in case of UK companies (23.37%).

The emphasis on equality of men and women at workplaces in developed countries is

reflected through higher disclosure concerning this attribute for UK companies.

The weighted disclosure score for the attribute Professional qualification and

experience of employees for UK companies (1.09%) is significantly lower than Indian

companies (42.59%). Higher reporting in India could be due to the fact that Indian

companies want to publicise their high calibre management and superior hiring policies

by giving this information in their annual reports. This attribute is the second most

reported attribute for Indian companies (Table 7.2).

Similar is the case for attribute Compensation whereby a low disclosure of

11.96% has been noticed for UK companies and a much higher score of 41.77% was

attained by Indian companies.

158

The next attribute in human capital category is training and development given to

the employees of an organisation. This attribute has weighted disclosure score of 38.68%

for Indian companies and 59.24% for UK companies. This attribute is second most

disclosed attribute in case of UK companies (Table 7.2). Johnson Matthey plc a UK

based company reported that “The Management Development and Remuneration

Committee of the board takes a special interest in ensuring compliance with the Training

and Development of People Policy objectives to:

• Ensure highest standards in the recruitment of employees.

• Assess training needs in the light of job requirements.

• Ensure relevance of training and link with business goals.

• Employ and evaluate effective and efficient training methods.

• Promote from within, from high potential pools of talent.

• Understand employees’ aspirations.

• Provide development opportunities to meet employees’ potential and

aspirations”. (Johnson Matthey plc, Annual report 2007, p.30)

For both the countries the attributes work related knowledge and entrepreneurial

spirit have low weighted disclosure score. Work related knowledge has weighted

disclosure score of 1.85% for Indian companies and 0.54% for UK companies. Similarly

for the attribute entrepreneurial spirit weighted disclosure score in India is 2.47 and in

UK is 1.09. Knowledge related to the kind of job or work which an employee does and a

high spirit of innovativeness or entrepreneurship is very essential for success of any

business unit. Companies are expected to disclose such information in their annual

reports. But unfortunately the weighted disclosure score received by this category is very

low for both the countries. This implies that not many companies are investing in and

encouraging work-related knowledge and entrepreneurial spirit attribute.

The final attribute in human capital category is human resource accounting. It has

zero disclosure score in case of UK companies and a very low disclosure score of 1.23%

in case of Indian companies. The probable reason for its low or non-disclosure could be

that companies consider its calculation and presentation as unnecessary taxing on its

resources. The other reason could be that companies want to keep such information for

159

internal management purposes only and does not wish to disclose it in their annual

reports.

7.1.2 EXTERNAL CAPITAL

External capital represents relationship of a company with its customers,

suppliers, industry associates, business partners, investors, market channels, society etc.

A glance at table 7.1 shows that weighted disclosure score (percentage) for all the

attributes in this category is more in case of UK companies as compared to Indian

companies. UK’s developed accounting practices might be the motivation for the same.

Weighted disclosure score regarding this first attribute brands and their

description, in external capital category is 44.24% for Indian companies and a slightly

higher score (45.11%) for UK companies. Higher disclosure regarding this attribute

infers that companies are using their annual reports in building and promoting its brand

by informing its investors.

Brand value is a summary measure of the financial strength of the brand.

However, a low weighted disclosure score regarding the brand valuation attribute was

observed. It is 1.23% for Indian companies and 4.89% for UK companies. BT Group plc-

a UK based company in its annual report reported “Our brand values are implicit in our

advertising strap line – Bringing it all together – which captures both what we can do for

customers and our commitment to acting as a single BT team.” (BT Group plc, Annual

report 2008, p.28).

The next attribute in external capital category is the distribution channels or

suppliers who play a crucial role in ensuring maximum value to customers and company.

The weighted disclosure score regarding this attribute is 42.18% for Indian companies

and 45.65% for UK companies. ITV Plc, a UK based company reported “ITV conducts

business with a range of suppliers. As a broadcaster, ITV commissions programmes from

a number of external production companies. A number of suppliers provide ITV with

services relating to the broadcasting of ITV channels on multiple platforms, including

transmission operator Arqiva, satellite operator SES Astra and satellite platform

operator Sky.” (ITV plc, Annual report 2007, p. 41). Sage Group plc a UK based

company reported “The diversity of our distribution channels is one of our key strengths.

160

Worldwide, we have over 40,000 advisers and 25,000 business partners and certified

consultants.” (Sage Group plc, Annual report 2007, p. 5)

Another attribute in external capital category is market or market share of a

company. Weighted disclosure score for this attribute is 59.88% for Indian companies

and 63.59% for UK companies. Within the external capital category, this attribute is the

most frequently reported attribute in case of Indian companies (Table 7.2). Anglo

American plc, a UK based company disclosed about its markets as “In Australia, 2007

opened with a strengthened market for thermal coal on the back of strong Asia Pacific

demand, particularly from China, which experienced a reduction in export tonnage and a

rise in domestic prices. Continued port congestion at Newcastle throughout the year, and

storm and flood events kept supply tight and further strengthened the export thermal

market. Prices steadily increased throughout the year and are likely to remain high into

2008. Export performance from South Africa and from Colombia was steady.” (Anglo

American plc, Annual report 2007, p.48)

The information regarding business collaborations has also received moderately

high disclosures for both the sample sets. The weighted disclosure score is 46.91% for

Indian companies and 67.39% for UK companies. This attribute is the second most

reported attribute in both Indian and UK context (Table 7.2). For instance GSK plc in its

annual report mentions “GSK has a very active external partnering strategy. In 2007 we

entered into nine external product licensing collaborations, together with a number of

other partnerships to develop further and utilise novel science and technologies in

pharmaceutical and biological R&D.” (GSK, Annual report 2007, p.7)

Satisfied Customers are challenging yet important intangible assets for an

organisation. But companies make meagre disclosure regarding this attribute in their

annual reports. Only 8.44% of maximum weighted disclosure score in India and 10.87%

in the UK relates to this attribute. This non-disclosure pattern may be taken to indicate

that only companies with good customer feedbacks want to mention this fact in their

annual report. Centrica Plc, a UK based company reported its customer satisfaction by

calculating NPS “ NPS is 3.1%- British Gas and 6.1%- Direct energy. Net promoter

score (NPS) is a measure of customer advocacy. It shows the percentage of customers

who would recommend us, minus the percentage who would not.” (Centrica Plc, Annual

report 2007, p. 15)

161

In addition to the above the Customers themselves also constitute to be important

intangible assets for an organisation. But its disclosure is not very high in India as

compared to UK. Weighted disclosure score is 26.75% in Indian context. It is almost

double at 42.39% for UK companies. Illustrating disclosure about this attribute from the

annual report of Admiral Group plc “Gladiator increased its customer base significantly

during the year and now boasts over 62,000 customers up from 43,000 last year (+44%),

which bodes well for the future.” (Admiral Group plc, Annual report 2007, p.12)

Disclosure about the attribute Social Activities is 42.18% in India and

comparatively higher (83.70%) for UK companies. Greater emphasis on societal needs

and its disclosure in annual reports of developed country (UK) is very encouraging for

companies in developing nation (India). For example Antofagasta plc, a UK based

company reported its social activities as “The Group supports local communities in many

ways, including providing education and training, fostering enterprises and encouraging

small businesses, job creation, the arts, health, sport, recreational activities and general

issues facing local communities.” (Antofagasta plc, Annual report 2007, p.55)

7.1.3 INTERNAL CAPITAL

In internal capital category, the disclosure regarding the first attributes Research

activities is 64.2% and 33.15% in India and UK respectively. This attribute is the most

reported attribute in case of both Indian and UK companies (Table 7.2). Johnson

Matthey, a UK based company reported “We maintain a high level of R&D expenditure

to ensure the continuous flow of new products and technologies to provide our customers

with cost effective solutions to meet legislated and technical requirements. In 2006/07 the

continuing operations spent £66.5 million gross on research and development.” (Johnson

Matthey, Annual report 2007, p.14).

Disclosure regarding Networking and information systems which is another

internal capital attribute is15.84% in case of Indian companies whereas it is slightly high

at 18.48% in case of UK companies.

Another important intangible assets attribute in internal capital category is

organisation structure of a company. Low disclosure of 5.76% for Indian companies and

7.07% for UK was noticed with regard to this attribute. Sage Group plc reported on this

attribute that “Sage operates a decentralised organisational structure with four regions

162

managing day-to-day business activities. Each region – UK & Ireland, Mainland Europe,

North America and Rest of World – is run by a regional management team headed by a

regional CEO. The regions all report into the parent Company.” (Sage Group plc,

Annual report 2007, p. 4)

Corporate culture attribute has mostly been reported in qualitative form in the

annual reports. It has 22.63% disclosure in India and 25.54% disclosure in the UK. This

is the second most reported attribute in internal capital category for both the datasets

(Table 5.4). A UK based company BAE Systems reported on this attribute “We seek to

nurture a culture within the Group of continuous improvement – in all aspects of business

performance. This includes ethical awareness as we work to achieve the highest

standards of governance in the conduct of our day-to-day business.” (BAE Systems,

Annual report 2007, p.2)

Intellectual capital assets like patents, trademarks and copyrights are other

attributes in internal capital category. Disclosure regarding patents is 17.08% in India and

8.15% in UK. In case of copyrights it is 1.44% in India and negligible in UK. For

trademarks disclosure is 7% in India and 8.15% in UK.

7.1.4 INTANGIBLE ASSETS SCORESHEET

Intangible assets Scoresheet is usually presented as additional information to the

investors. Only 1.23% companies in India (and none of the company in UK) are

disclosing this scoresheet in the annual reports.

7.1.5 MANDATORY DISCLSOURE REQUIREMENT

UK’s Financial Reporting Standard 10 on Goodwill and Intangible assets issued

in 1997 and Accounting Standard 26 on Intangible assets issued by the Institute of

Chartered Accountants of India in 2002 specifies some disclosure requirements for

companies having intangible assets in their balance sheets. These requirements have been

categorised into four sub-heads which are:

(a) Distinguish between internally generated and other intangible assets;

(b) Details of amortisation rates, method and carrying amount at beginning and end

of period;

163

(c) Classification of intangible assets; and

(d) Other disclosures like pledging information, reasons for amortising over more

than 10 years etc.

The sub-head (a) above which is distinguishing between internally generated and

other intangible assets, has a disclosure score of 8.64% in India and 34.78% in UK.

Lower disclosure score in case of Indian companies implies that not many Indian

companies, which have intangible assets in their books, are differentiating between

internally generated and acquired intangible assets.

Accounting Standard also requires that companies should give details of

amortisation rates, method and carrying amount at beginning and end of period. This

requirement has been fulfilled by all the companies which had intangible assets as a part

of their balance sheet. Disclosure score for this sub-head is 72.02% in India and 84.78%

in UK.

Another requisite of Accounting Standards is Classification of intangible assets

into separate classes. In case of Indian companies, out of 72.84% companies having

intangible assets in their balance sheet, 69.96% companies are categorising them into

classes like software, brand, licences etc. Similarly in case of UK companies, 83.70%

companies are categorising their intangible assets, out of a total of 84.78% of sample

companies which recognise intangible assets in their books of accounts.

Other disclosures like pledging information, reasons for amortising over more

than 10 years etc. have achieved a score of 2.88% in India and 13.04% in UK. Low

disclosure for this sub-head could be due to limited applicability of this disclosure

requirement.

Intangible assets Valuation

The category Intangible assets Valuation have received a disclosure score of

72.84% in India and 84.78% in UK.

164

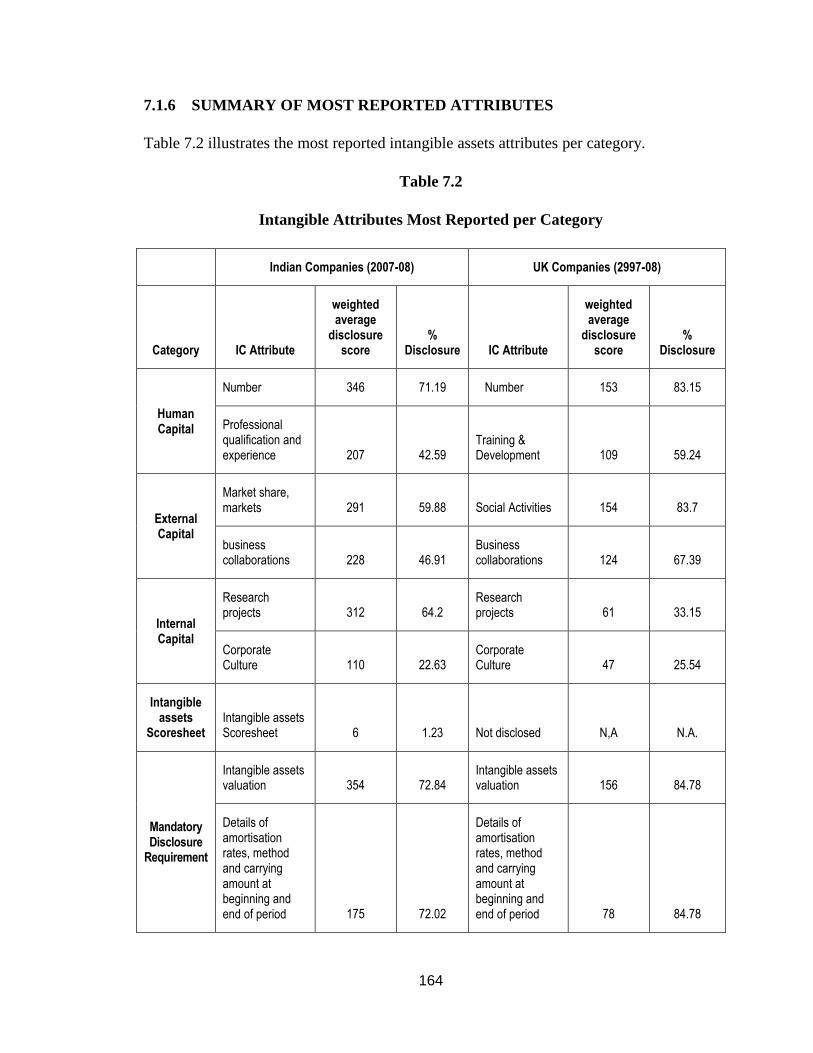

7.1.6 SUMMARY OF MOST REPORTED ATTRIBUTES

Table 7.2 illustrates the most reported intangible assets attributes per category.

Table 7.2

Intangible Attributes Most Reported per Category

Indian Companies (2007-08) UK Companies (2997-08)

Category IC Attribute

weighted average

disclosure score

% Disclosure IC Attribute

weighted average

disclosure score

% Disclosure

Human Capital

Number 346 71.19 Number 153 83.15

Professional qualification and experience 207 42.59

Training & Development 109 59.24

External Capital

Market share, markets 291 59.88 Social Activities 154 83.7

business collaborations 228 46.91

Business collaborations 124 67.39

Internal Capital

Research projects 312 64.2

Research projects 61 33.15

Corporate Culture 110 22.63

Corporate Culture 47 25.54

Intangible assets

Scoresheet Intangible assets Scoresheet 6 1.23 Not disclosed N,A N.A.

Mandatory Disclosure

Requirement

Intangible assets valuation 354 72.84

Intangible assets valuation 156 84.78

Details of amortisation rates, method and carrying amount at beginning and end of period 175 72.02

Details of amortisation rates, method and carrying amount at beginning and end of period 78 84.78

165

The attribute “Number of employees” and “Professional qualification and

experience” in case of Indian companies whereas attribute “Number of employees” and

“Training and development” in case of UK companies are the most reported attributes

from the human capital category.

“Market share, markets” and “Business collaboration” in Indian context and

“Social Activities” and “Business collaboration” in UK context are most highly

disclosed attributes in external capital category.

Focussing on internal capital category, ranking profiles are broadly similar for

both the countries. “Research projects” and “Corporate culture” are the most reported

intangible assets attributes.

Similarly for mandatory disclosure requirement category, “Intangible assets

valuation” and “Details of amortisation rates, method and carrying amount at beginning

and end of period” are most disclosed attributes in the annual reports of both India and

UK.

SECTION II

7.2 NATURE OF INTANGIBLE ASSETS DISCLOSURE

After explaining in detail the extent of disclosure it is very essential to discuss

about the nature of reporting of intangible assets. Nature of intangible assets disclosure

involves distinguishing between qualitative and quantitative nature of reporting.

Table 7.3 depicts the nature of intangible assets disclosure in annual reports of

both Indian and UK based companies. The percentage number of companies as

mentioned in the table has been calculated by dividing the total number of companies

disclosing an attribute in qualitative or quantitative form by total number of sample

companies (which is 243 in India and 92 in UK). For example number of employees

attribute has been disclosed by 2.47% companies in qualitative form and 69.96% in

quantitative form in case of Indian companies.

166

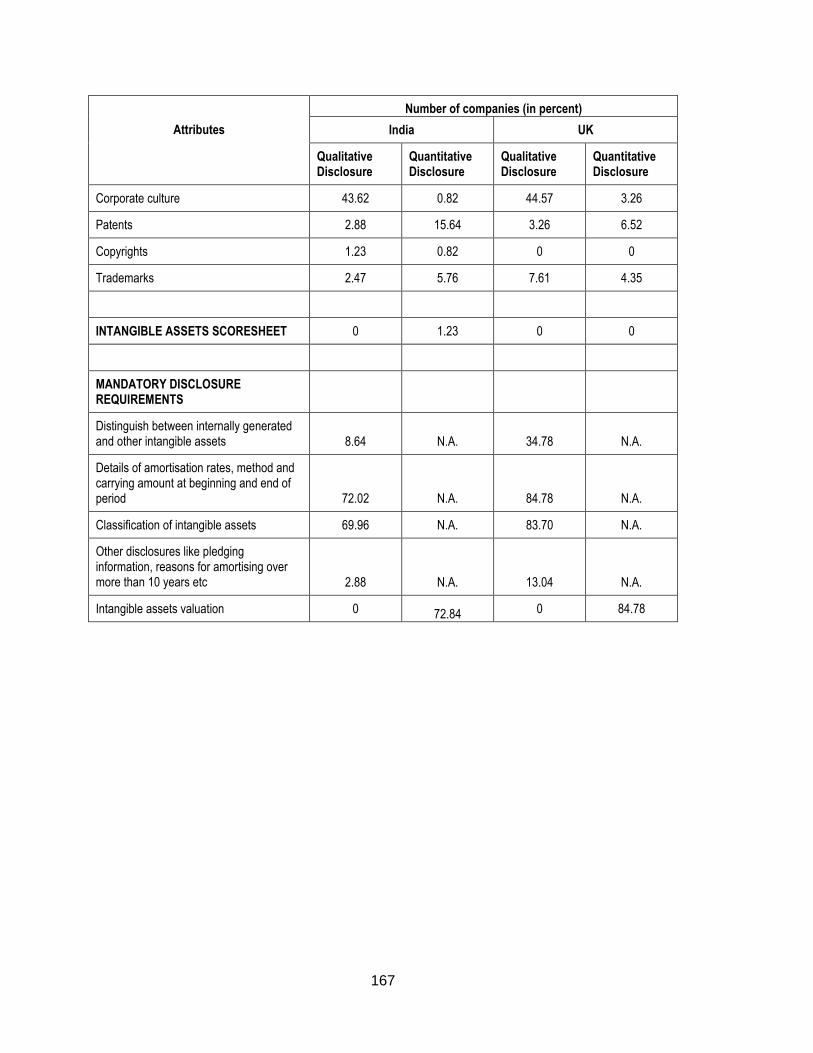

Table 7.3

Nature of intangible assets disclosure (in percentage)

Attributes

Number of companies (in percent)

India UK

Qualitative Disclosure

Quantitative Disclosure

Qualitative Disclosure

Quantitative Disclosure

HUMAN CAPITAL

Employees

-Number 2.47 69.96 1.09 82.61

-Gender 1.65 1.23 3.26 21.74

-Professional qualification and Experience 7 39.09 0 1.09

-Compensation 8.64 37.45 10.87 6.52

Training & Development 39.51 18.93 35.87 41.30

Work related knowledge 2.88 0.41 1.09 0

Entrepreneurial Spirit 4.12 0.41 2.17 0

Human resource accounting 0 1.23 0 0

EXTERNAL CAPITAL

Brands and their specification 26.75 30.86 22.83 33.70

brand valuation 0 1.23 7.61 1.09

Distribution channels 29.22 27.57 26.09 32.61

Market share, markets 34.16 42.80 40.22 43.48

Business collaboration 19.75 37.04 13.04 60.87

Customer satisfaction 10.29 3.29 6.52 7.61

Customer information (no.) 7.41 23.05 8.70 38.04

Social activities 23.46 30.45 10.87 78.26

INTERNAL CAPITAL

Research projects 12.35 58.02 18.48 23.91

Networking and information systems 20.99 5.35 26.09 5.43

Organisation Structure 4.12 3.70 5.43 4.35

Cont…

167

Attributes

Number of companies (in percent)

India UK

Qualitative Disclosure

Quantitative Disclosure

Qualitative Disclosure

Quantitative Disclosure

Corporate culture 43.62 0.82 44.57 3.26

Patents 2.88 15.64 3.26 6.52

Copyrights 1.23 0.82 0 0

Trademarks 2.47 5.76 7.61 4.35

INTANGIBLE ASSETS SCORESHEET 0 1.23 0 0

MANDATORY DISCLOSURE REQUIREMENTS

Distinguish between internally generated and other intangible assets 8.64 N.A. 34.78 N.A.

Details of amortisation rates, method and carrying amount at beginning and end of period 72.02 N.A. 84.78 N.A.

Classification of intangible assets 69.96 N.A. 83.70 N.A.

Other disclosures like pledging information, reasons for amortising over more than 10 years etc 2.88 N.A. 13.04 N.A.

Intangible assets valuation 0 72.84 0 84.78

168

Table 7.3 brings out that nature of intangible assets reporting is more or less the

same in case of both the countries. Disclosure is more in discursive (Qualitative) form

rather than numerical (Quantitative) form. This finding is not unexpected with the

difficulty involved in quantifying what is, in many instances, essentially a qualitative

item. The detailed attribute-wise nature of intangible assets reporting is discussed below.

7.2.1 HUMAN CAPITAL

In human capital category, the attribute Number of Employees has been disclosed

by 69.96% companies in quantitative form and 2.47% companies in qualitative form in

India. Similarly in UK large number of companies (82.61%) is reporting this attribute in

quantitative form and only few companies (1.09%) are disclosing it in qualitative form.

The attribute Gender is more widely reported in the UK. In India only 1.23%

companies are disclosing this attribute in quantitative manner whereas the percentage of

companies disclosing it quantitatively is 21.74% in UK.

Contrary to the above results, for attributes Professional qualification &

experience and Compensation quantitative disclosure is more in case of Indian

companies. Further, the attribute Training and development has been reported by 39.51%

companies in qualitative form and 18.93% in quantitative manner in case of Indian

sample. It has been reported by 35.87% companies in qualitative form and 41.30% in

quantitative form in the UK.

As discussed in Section-I the disclosure on attributes Work-related knowledge and

Entrepreneurial spirit is minimal in case of both the countries. Regarding the nature of

reporting while none of the company is disclosing it in quantitative form in UK, 0.41%

companies are reporting this attributes in quantitative form in India. Further the attribute

Human resource accounting has been reported only by 1.23% Indian companies in

quantitative form.

7.2.2 EXTERNAL CAPITAL

For most companies the attributes in external capital category are reported in

quantitative rather than qualitative form. The nature of reporting seems similar in case of

both the sample sets.

169

For instance the attribute Brands and their descriptions have been reported by

26.75% companies in discursive form and 30.86% in numerical form in case of Indian

companies. Similarly for UK based companies this attribute has been reported by 22.83%

companies in qualitative form and 33.70% companies in quantitative form.

In India the attribute Brand valuation has been reported by only 1.23% companies

in quantitative form. While it has been disclosed by 7.61% companies in qualitative form

and 1.09% companies in quantitative form by UK companies

Further the attribute Distribution channels has been disclosed qualitatively by

29.22% companies in India and 26.09% companies in UK. This attribute has been

reported quantitatively by 27.57% companies in India and 32.61% companies in UK.

The attribute Markets and market share has been disclosed by 34.16% and 42.8%

Indian companies in qualitative and quantitative form respectively. The disclosure in

both forms is 40.22% and 43.48% in case of UK companies.

The nature of reporting appears to be more in quantitative form in case of attribute

Business collaborations in case of both the countries. 37.04% companies in India and

60.87% companies in UK are disclosing this attribute in quantitative form.

Disclosure for the attribute Customer satisfaction is in discursive manner

(10.29%) rather than quantitative form (3.29%) in India. The disclosure for this attribute

in UK is 6.52% in qualitative form and 7.61% in quantitative form.

The attribute Social has been disclosed by 23.46% Indian companies and 10.87%

UK companies in discursive form. It has been reported by 30.45% companies in India

and more than double (78.26%) UK companies in quantitative form

In nutshell there is similarity in the nature of reporting of attributes in external

capital category. The quantitative nature of disclosure is more in case of UK based

companies.

7.2.3 INTERNAL CAPITAL

As referred in section-I that the extent of disclosure on attributes in internal

capital category has not been very high in case of both the countries. The nature of

reporting on attributes of this category is also similar for both the countries.

170

The attribute Research activities has been reported by 12.35% companies in India

and 18.98% companies in UK in qualitative form. The number of companies reporting

this attribute in quantitative form is 58.02% in India and 23.91% in UK.

The reporting on attribute Networking and information systems is identical in

India and UK. This attribute has been disclosed in qualitative manner by 20.99% and

26.09% companies in India and UK respectively.

The reporting on the attribute Organisation structure is low in both the countries.

The manner of reporting is also similar. 4.12% and 3.7% companies in India are

disclosing this attribute in discursive and numerical form respectively. Similarly, 5.43%

and 4.35% companies in UK are reporting on this attribute in qualitative and quantitative

form respectively.

The attribute Corporate culture has been disclosed by both Indian and UK

companies in qualitative form. The number of countries disclosing this attribute in

quantitative form is 0.82% and 3.26% in India and UK.

Finally, as shown in table 7.3 the nature of reporting for attributes Patents,

Copyrights and Trademarks is also similar in case of both the countries.

7.2.4 INTANGIBLE ASSETS SCORESHEET

This attribute has been disclosed by very few (1.23%) companies in India. None

of the company in UK is disclosing this attribute in qualitative or quantitative form

7.2.5 MANDATORY DISCLOSURE REQUIREMENT

Intangible assets valuation attribute in this category has been disclosed by all companies

in quantitative form.2

SECTION-III

7.3 CATEGORY-WISE ANALYSIS

In this section, aggregated disclosure scores of intangible assets for each of the

five categories i.e. human capital, external capital and internal capital, intangible assets

2 Disclosure relating to remaining attributes in this category is of qualitative nature only

171

scoresheet and mandatory disclosure requirements has been calculated. This is to

determine the highest reported intangible assets category out of the five categories

mentioned above, for India and the UK. Table 7.4 and figure 7.1 & 7.2 shows the

different categories of intangible assets index and total score (in percent) for each

category for both the countries.

Table 7.3

Category-wise Disclosure

Categories India (2007-08)

UK

(2007-08)

Human Capital 27% 22%

External Capital 36% 43%

Internal Capital 18% 12%

Intangible assets scoresheet 0% 0%

Mandatory Disclosure Requirements 20% 23%

Note: Disclosure percentages have been calculated using the weighted means

172

Figure 7.1

Category-wise intangible assets disclosure (India)

27%

36%

18%

0%

20%

Human Capital External Capital

Internal Capital Intangible assets scoresheet

Mandatory Disclosure Requirements

Figure 7.2

Category-wise intangible assets disclosure (UK)

22%

43%

12%

0%

23%

Human Capital External Capital

Internal Capital Intangible assets scoresheet

Mandatory Disclosure Requirements

173

The category-wise analysis of intangible assets disclosure in the above Table 7.3,

Figure 7.1 & 7.2 shows external capital as the highest reported intangible assets category for

both the countries. It has disclosure score of 36% in India and 43% in UK. In the present

competitive world the dominance of external capital can be justified by increased role played

by customers, brands, suppliers, business partners and society in the business.

In India, human capital is the second most reported category with a disclosure score

of 27%. It is followed by mandatory disclosure requirement category with a score of 20%.

Internal capital category is the second least reported category with 18% disclosure. The

reporting for the category intangible assets scoresheet is negligible.

For UK, mandatory disclosure requirement category is the second most reported

category with a disclosure score of 23%. It is followed by human capital category with a

disclosure score of 22%. Like India, internal capital category is the second least reported

category with a total disclosure score of 12%. The reporting for the category intangible assets

scoresheet is almost negligible (which is also similar to India).

The above analysis brings out that the pattern of intangible assets reporting is broadly

consistent in both the countries.

SECTION IV

7.4 COMPANY-WISE DISCLOSURE

The company-wise disclosure score has been calculated by dividing the total

weighted disclosure index score obtained by a company during a particular year by the

maximum score for the company (which is 54). The companies have been ranked in the

descending order of their disclosure score.

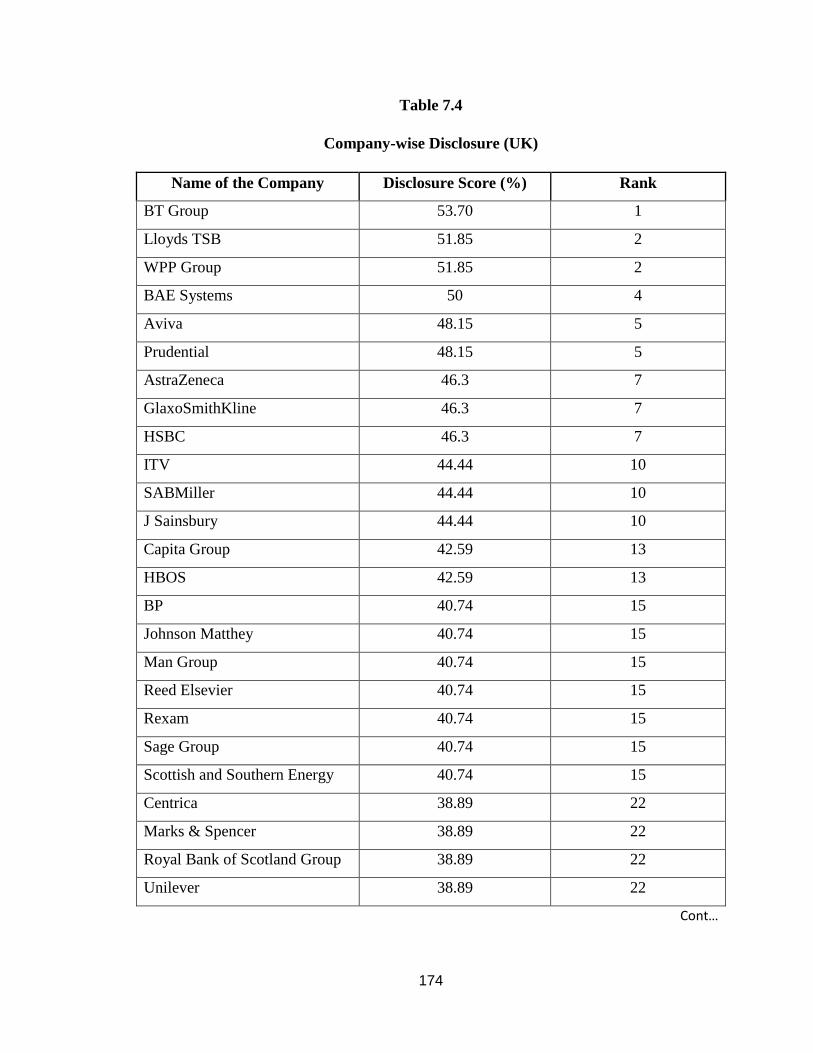

Table 7.4 explains the company-wise disclosure score for UK companies3. The

highest disclosure score has been achieved by BT Group (54%). It is closely followed by

Lloyds TSB (52%), WPP Group, BAE Systems (50%), Aviva (48%), Prudential, Astra

Zeneca (46%), Glaxosmithkline, HSBC, ITV (44%), SABMiller, J Sainsbury, Capita Group

(43%), and HBOS.

Companies with least disclosure score in UK are Bunzl (11%), Liberty International

(13%), Hammerson, Drax group, Carnival, United utilities (15%), Enterprise Inns (15%),

Cairn energy, Lonmin (17%), Enterprise Natural Resources Corporation, and Allaince

Trust etc.

3 For company –wise disclosure score of Indian companies, refer table 5.8 in chapter V, Extent of Disclosure, pp.98

174

Table 7.4

Company-wise Disclosure (UK)

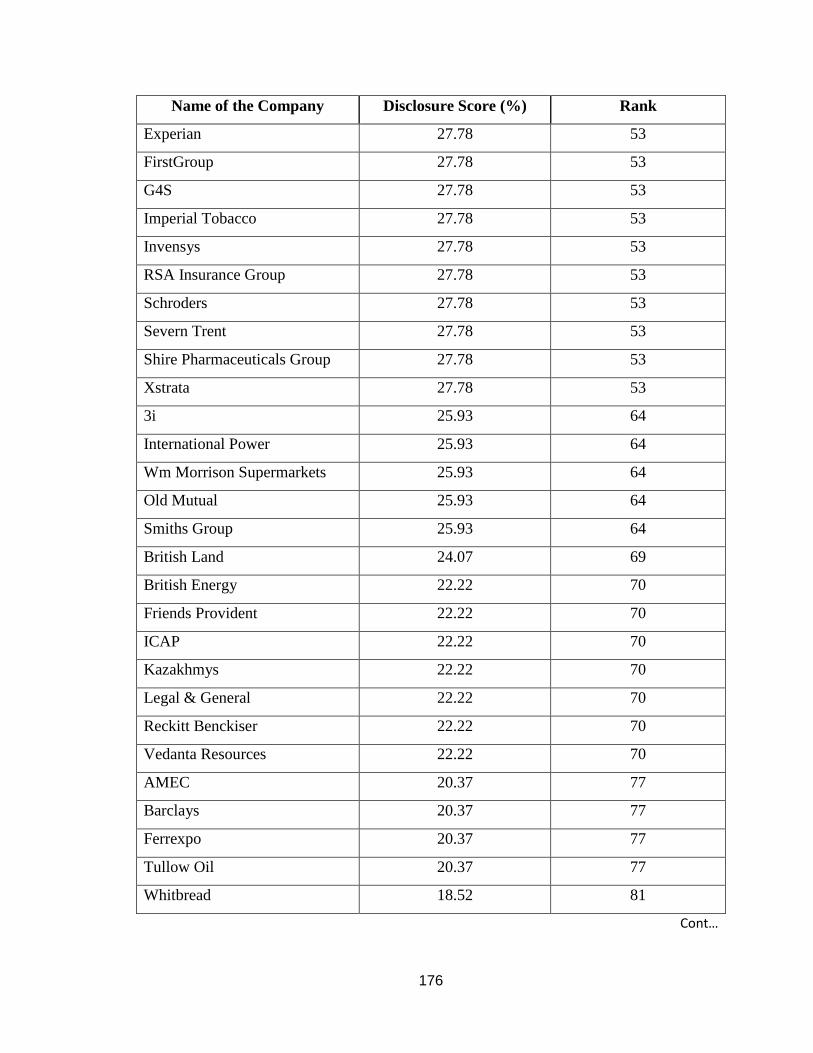

Name of the Company Disclosure Score (%) Rank

BT Group 53.70 1

Lloyds TSB 51.85 2

WPP Group 51.85 2

BAE Systems 50 4

Aviva 48.15 5

Prudential 48.15 5

AstraZeneca 46.3 7

GlaxoSmithKline 46.3 7

HSBC 46.3 7

ITV 44.44 10

SABMiller 44.44 10

J Sainsbury 44.44 10

Capita Group 42.59 13

HBOS 42.59 13

BP 40.74 15

Johnson Matthey 40.74 15

Man Group 40.74 15

Reed Elsevier 40.74 15

Rexam 40.74 15

Sage Group 40.74 15

Scottish and Southern Energy 40.74 15

Centrica 38.89 22

Marks & Spencer 38.89 22

Royal Bank of Scotland Group 38.89 22

Unilever 38.89 22

Cont…

175

Name of the Company Disclosure Score (%) Rank

Associated British Foods 37.04 26

British American Tobacco 37.04 26

National Grid 37.04 26

Rolls-Royce Group 37.04 26

TUI Travel 37.04 26

BG Group 35.19 31

British Airways 35.19 31

Cable & Wireless 35.19 31

Tesco 35.19 31

Admiral Group 33.33 35

Cadbury 33.33 35

Compass Group 33.33 35

InterContinental Hotels Group 33.33 35

Kingfisher 33.33 35

London Stock Exchange Group 31.48 40

Antofagasta 29.63 41

Carphone Warehouse 29.63 41

Cobham 29.63 41

Diageo 29.63 41

Next 29.63 41

Petrofac 29.63 41

Rio Tinto Group 29.63 41

Royal Dutch Shell 29.63 41

Standard Chartered Bank 29.63 41

Thomas Cook Group 29.63 41

Wolseley 29.63 41

Wood Group 29.63 41

Anglo American 27.78 53

Cont…

176

Name of the Company Disclosure Score (%) Rank

Experian 27.78 53

FirstGroup 27.78 53

G4S 27.78 53

Imperial Tobacco 27.78 53

Invensys 27.78 53

RSA Insurance Group 27.78 53

Schroders 27.78 53

Severn Trent 27.78 53

Shire Pharmaceuticals Group 27.78 53

Xstrata 27.78 53

3i 25.93 64

International Power 25.93 64

Wm Morrison Supermarkets 25.93 64

Old Mutual 25.93 64

Smiths Group 25.93 64

British Land 24.07 69

British Energy 22.22 70

Friends Provident 22.22 70

ICAP 22.22 70

Kazakhmys 22.22 70

Legal & General 22.22 70

Reckitt Benckiser 22.22 70

Vedanta Resources 22.22 70

AMEC 20.37 77

Barclays 20.37 77

Ferrexpo 20.37 77

Tullow Oil 20.37 77

Whitbread 18.52 81

Cont…

177

Name of the Company Disclosure Score (%) Rank

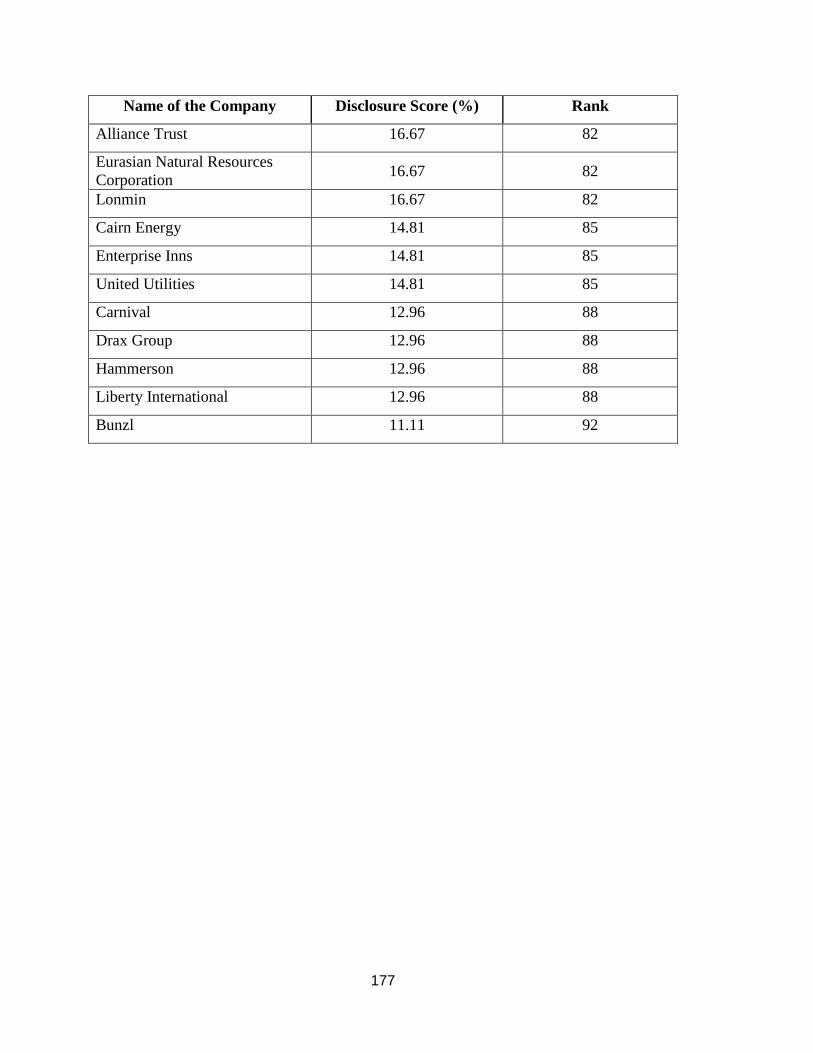

Alliance Trust 16.67 82

Eurasian Natural Resources

Corporation 16.67 82

Lonmin 16.67 82

Cairn Energy 14.81 85

Enterprise Inns 14.81 85

United Utilities 14.81 85

Carnival 12.96 88

Drax Group 12.96 88

Hammerson 12.96 88

Liberty International 12.96 88

Bunzl 11.11 92

178

The above table reveals that the range of disclosure score of the UK companies

varies from 11.11 to 53.70. It is 1.85% to 57.41% for Indian companies (after excluding

two outperforming companies i.e. Infosys Technologies Ltd. and Satyam Computer

Services Ltd.).

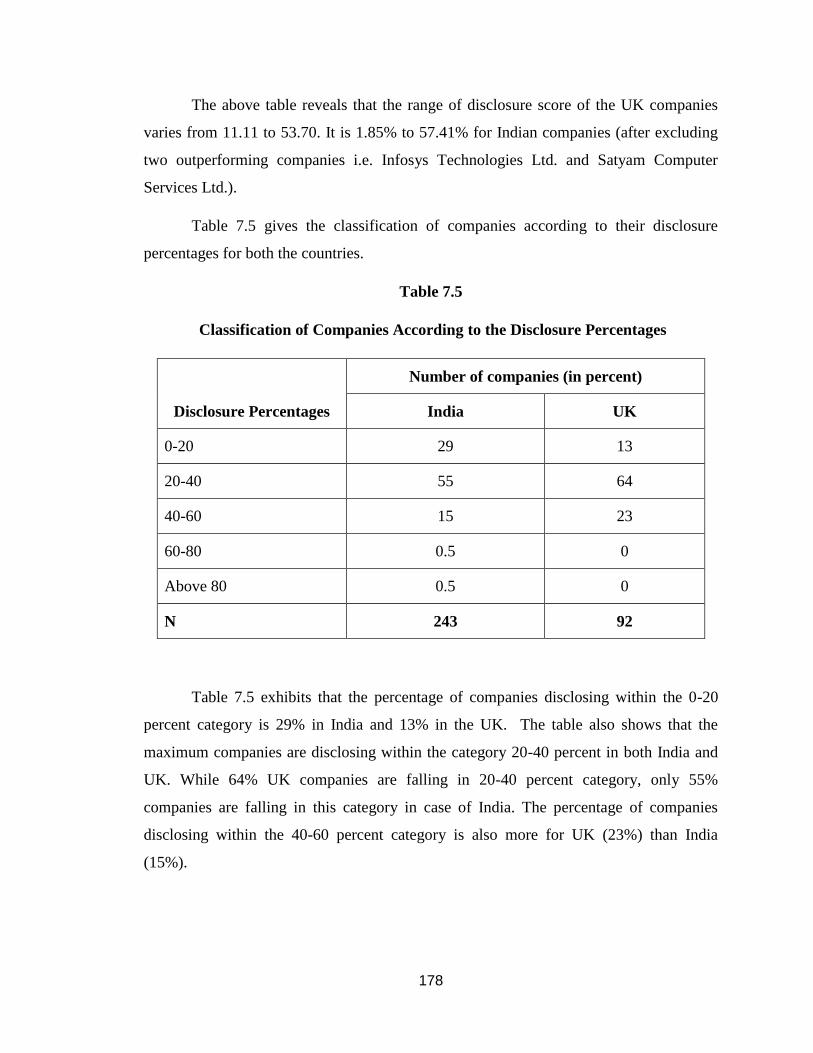

Table 7.5 gives the classification of companies according to their disclosure

percentages for both the countries.

Table 7.5

Classification of Companies According to the Disclosure Percentages

Disclosure Percentages

Number of companies (in percent)

India UK

0-20 29 13

20-40 55 64

40-60 15 23

60-80 0.5 0

Above 80 0.5 0

N 243 92

Table 7.5 exhibits that the percentage of companies disclosing within the 0-20

percent category is 29% in India and 13% in the UK. The table also shows that the

maximum companies are disclosing within the category 20-40 percent in both India and

UK. While 64% UK companies are falling in 20-40 percent category, only 55%

companies are falling in this category in case of India. The percentage of companies

disclosing within the 40-60 percent category is also more for UK (23%) than India

(15%).

179

Further only 0.5% Indian companies are within the disclosure range of 60-80

percent and Above 80 percent. None of the UK based company is in this disclosure

range.

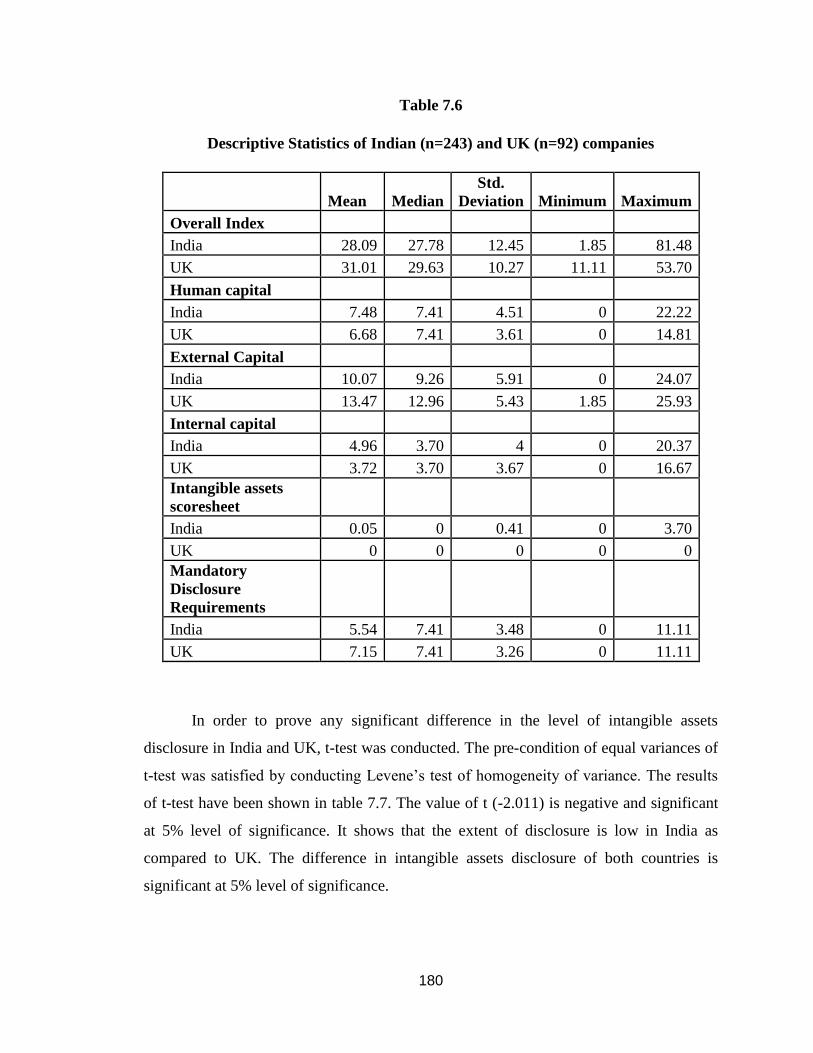

7.3.1 Descriptive Statistics

Table 7.6 displays the descriptive statistics with respect to intangible assets

disclosure for both the countries. The overall mean disclosure score is 28.09% in India

and is slightly higher for UK (31.02). The variation and range of disclosure is higher in

India as compared to UK. Range of intangible asset disclosure is 11.11% to 53.70% in

the UK and 1.85% to 81.48% in India. Range of disclosure for Indian companies

descends to 1.85% to 57.41% if two Indian companies (i.e. Infosys Technologies Ltd. and

Satyam Computer Services Ltd.) are excluded from the list of all companies for the

purpose of its calculation.

In human capital category the mean disclosure score is 7.48% in India and 6.68%

in UK. Both variation and range are higher in case of Indian companies.

Further for external capital category mean disclosure score is higher in case of

UK companies. It is 10.06% for India and 13.47% for UK. While variation is slightly

more in India as compared to UK, the range of disclosure is similar in India and UK.

For internal capital category the mean disclosure is higher in India (4.96%) in

comparison to UK (3.72%). Variation is also more in India (4%) as compared to UK

(3.66%).

Further for intangible assets scoresheet category the mean is 0.05% in India. It is

zero in case of UK.

The mean of mandatory disclosure requirement category is higher in case of UK

companies. It is 7.15% for UK and 5.54% for India. Variation is slightly more in India

but range of score is same for both the countries.

In nutshell, the level of intangible assets reporting is low for both the countries.

However the overall reporting on intangible assets is slightly better in UK.

180

Table 7.6

Descriptive Statistics of Indian (n=243) and UK (n=92) companies

Mean Median

Std.

Deviation Minimum Maximum

Overall Index

India 28.09 27.78 12.45 1.85 81.48

UK 31.01 29.63 10.27 11.11 53.70

Human capital

India 7.48 7.41 4.51 0 22.22

UK 6.68 7.41 3.61 0 14.81

External Capital

India 10.07 9.26 5.91 0 24.07

UK 13.47 12.96 5.43 1.85 25.93

Internal capital

India 4.96 3.70 4 0 20.37

UK 3.72 3.70 3.67 0 16.67

Intangible assets

scoresheet

India 0.05 0 0.41 0 3.70

UK 0 0 0 0 0

Mandatory

Disclosure

Requirements

India 5.54 7.41 3.48 0 11.11

UK 7.15 7.41 3.26 0 11.11

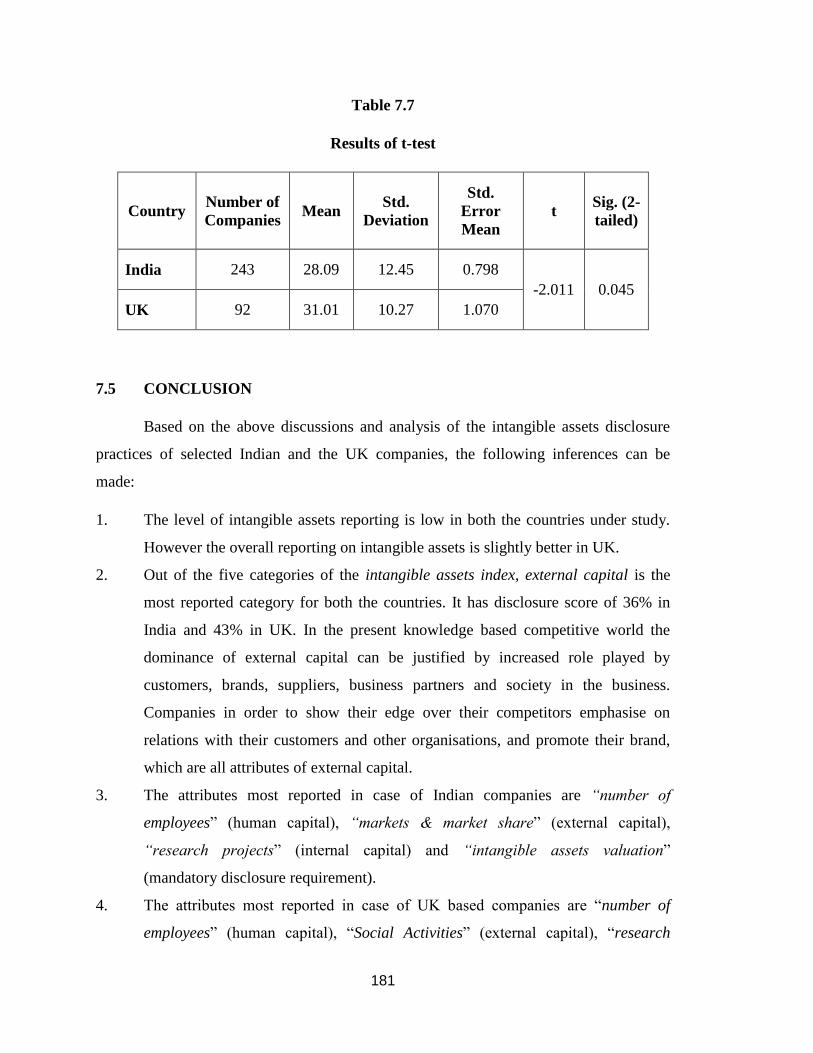

In order to prove any significant difference in the level of intangible assets

disclosure in India and UK, t-test was conducted. The pre-condition of equal variances of

t-test was satisfied by conducting Levene’s test of homogeneity of variance. The results

of t-test have been shown in table 7.7. The value of t (-2.011) is negative and significant

at 5% level of significance. It shows that the extent of disclosure is low in India as

compared to UK. The difference in intangible assets disclosure of both countries is

significant at 5% level of significance.

181

Table 7.7

Results of t-test

Country Number of

Companies Mean

Std.

Deviation

Std.

Error

Mean

t Sig. (2-

tailed)

India 243 28.09 12.45 0.798

-2.011 0.045

UK 92 31.01 10.27 1.070

7.5 CONCLUSION

Based on the above discussions and analysis of the intangible assets disclosure

practices of selected Indian and the UK companies, the following inferences can be

made:

1. The level of intangible assets reporting is low in both the countries under study.

However the overall reporting on intangible assets is slightly better in UK.

2. Out of the five categories of the intangible assets index, external capital is the

most reported category for both the countries. It has disclosure score of 36% in

India and 43% in UK. In the present knowledge based competitive world the

dominance of external capital can be justified by increased role played by

customers, brands, suppliers, business partners and society in the business.

Companies in order to show their edge over their competitors emphasise on

relations with their customers and other organisations, and promote their brand,

which are all attributes of external capital.

3. The attributes most reported in case of Indian companies are “number of

employees” (human capital), “markets & market share” (external capital),

“research projects” (internal capital) and “intangible assets valuation”

(mandatory disclosure requirement).

4. The attributes most reported in case of UK based companies are “number of

employees” (human capital), “Social Activities” (external capital), “research

182

projects” (internal capital) and “intangible assets valuation” (mandatory

disclosure requirement).

5. The nature of intangible assets reporting is more or less the same for UK and

India. Disclosure is more in discursive (Qualitative) form rather than numerical

(Quantitative) form for both the countries. Lack of consensus about the need of

the disclosure and the manner of disclosing it in the annual report might be a

cause for low level of quantification.

6. In India Infosys Technologies Ltd. has the highest intangible assets disclosure

score. BT Group has highest intangible assets disclosure score in the UK.

7. Overall mean disclosure score is 28.09% for Indian companies and 31.01% for

UK companies. The result of T-test showed that these differences are significant.

8. The range of mean disclosure score is higher for Indian companies (1.85% to

81.48%) than UK companies (11.11% to 53.70%). The range of disclosure score

descends to 1.85% to 57.41% for Indian companies, if mean scores of two

outperforming companies (namely Infosys Technologies Ltd. and Satyam

Computer Services Ltd.) are excluded from the data for the purpose of its

calculation.

9. Reporting of intangible assets is very unorganised and unsystematic in both the

countries. The lack of established and generally accepted intangible assets

reporting framework could have contributed to it.

![INTANGIBLE VALUE –FACT OR FICTION - AI Home | … · [IAS 38.8] 3. INTANGIBLE VALUE –FACT OR FICTION ... 2.36 INTANGIBLE PROPERTY (INTANGIBLE ASSETS): Non-physical assets, …](https://img.pdfslide.us/doc/110x75/5af0812f7f8b9ac2468e1bc2/intangible-value-fact-or-fiction-ai-home-ias-388-3-intangible-value.jpg)