Embed Size (px)

Citation preview

1

Digitalisation

The future started yesterday

Levente KOVÁCS - Secretary General Zoltán LADÁNYI - Chief Economist

Szumi, 25 October 2018

2

Introduction

• Trust is fundamental to the banking sector, therefore

innovative applications must be built on a firm, secure base.

• The adaptation of IT does not depend on technical

possibilities, but rather on how willing customers are to

apply it.

• Customers change rapidly and need a few years to adapt to

new technologies.

• Regulations and infrastructure service providers have the

ability to speed up technological change.

3

Agenda

Industrial Revolutions

Changes in Approach

Impact of Regulations

New paradox in payments

FinTech and BigTech Companies

How should banks react to new ecosystem

Instant Payment

How is the winner?

Looking into the future

Conclusion

4

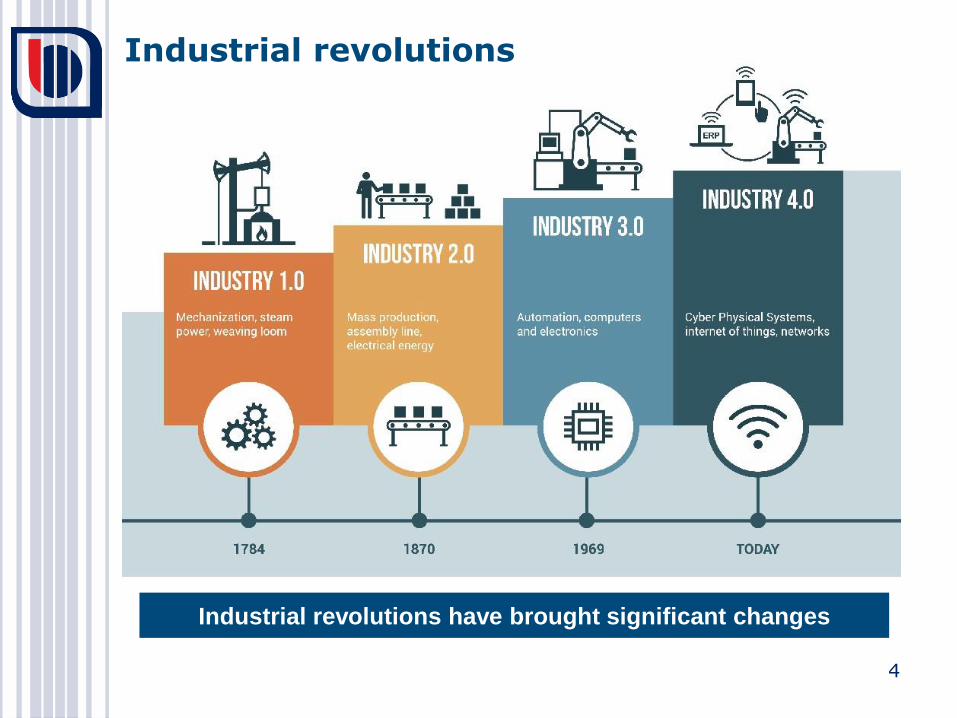

Industrial revolutions

Industrial revolutions have brought significant changes

5

What is Industry 4.0?

Industry 4.0 optimizes the computerization of Industry 3.0

6

Changes in approach

is the world’s largest taxi company. It owns no vehicles.

is the world’s most valuable retailer. It has no inventory.

is the world’s most popular media owner. It creates no content.

is the world’s largest accommodation provider. It owns no

real estate.

is the world’s biggest „bank”, with no real cash and branch.

Tech Platforms don’t Own Products

* Source: The New York Times, 16.04.2017

*

7

Payment Services Directive (PSD)

The Payment Services Directive (PSD, Directive

2007/64/EC, replaced by PSD 2, Directive (EU)

2015/2366) is an EU Directive, administered by the

European Commission (Directorate General Internal

Market) to regulate payment services and payment

service providers throughout the European Union (EU)

and European Economic Area (EEA). The Directive's

purpose was to increase pan-European

competition and participation in the payments

industry also from non-banks, and to provide for a

level playing field by harmonizing consumer

protection and the rights and obligations for

payment providers and users.

2007 – PSD

2018 – PSD2 The new rules aim to better protect consumers when

they pay online, promote the development and use of

innovative online and mobile payments such as

through open banking, and make cross-border

European payment services safer.

8

How banks should react to new ecosystem

Growing Complexity Needs

Cost effectiveness

Simplicity

Service Quality

Answers

Innovation

Value-added

Services

Digitalisation

Payment Market has to keep up with the increased needs of

customers

9

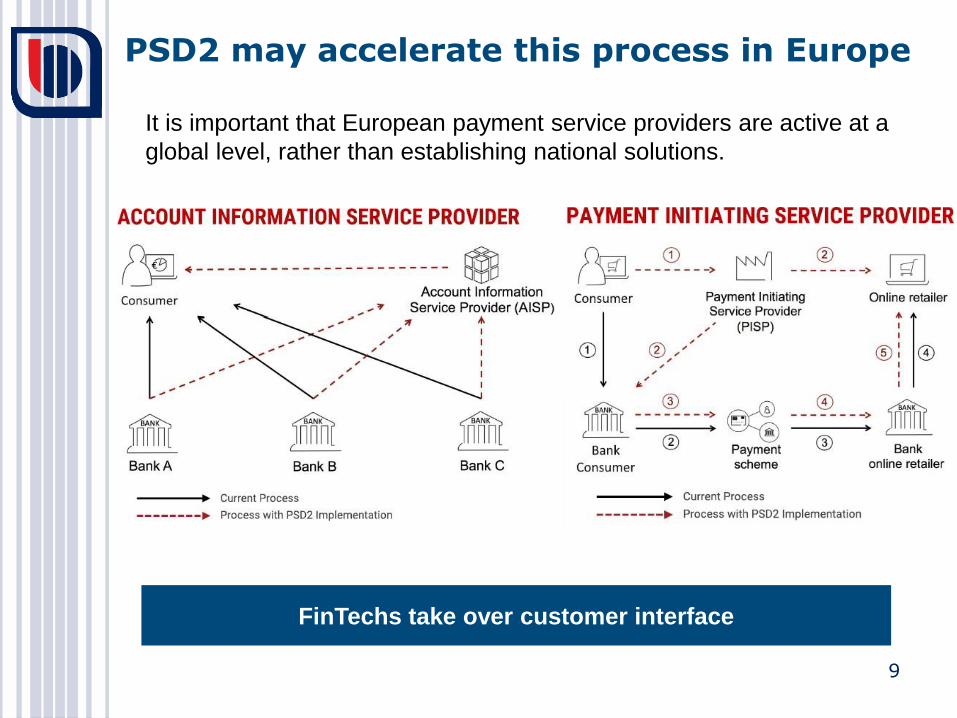

PSD2 may accelerate this process in Europe

FinTechs take over customer interface

It is important that European payment service providers are active at a

global level, rather than establishing national solutions.

10

Fierce competition

*Source: VISA

Profitability concerns 3

1

Customer expectations, requirement and behaviour

2

Key drivers inducing changes in business models

Due to mobile phone and other improved access methods the barriers

to entry in the financial services industry are being reduced.

77% of Europeans use their phones to bank and make everyday payments*

Regulatory changes

4

11

New paradox in payments

More players (FinTechs, BigTechs)

More technology

More solution

Payments part of a “bigger game”

Globalisation

More regulation • Harmonisation (Single Market – e.g. SEPA)

• Consumer protection

• Price regulation

• Integrity and continuity

• Security (SCA)

Existing payments vs. “new payments” methods

More complex ecosystem expected to produce simpler, faster

and cheaper payments

12

Key trends in reacting to FinTech

Employing new technologies to

transform internal and external

processes

“digital transformation” component

Rethinking interaction with

customers experience through the

use of innovative technologies

“digital disruption” component

Technological change calls established business models into question

13

Institutions

Issue with existing IT infrastructure / IT legacy systems

Need to develop internal “innovative” culture and mindset / organisational transformation

Need to attract and maintain talent and skills

Customers trust banks compared to new entrants (mainly due to data protection concerns)

Strong on customer relationship providing the full value chain to customers with respective customer expectations and behaviour

Partnering

New entrant FinTech firms

• Agile, flexible and familiar with technologies

• Learn and grow through partnerships with banks

• Through their interaction with banks, they receive funding, access to customers and distribution channels, visibility, and banking expertise (including legal, compliance and regulatory knowledge)

• Do not currently provide the full value chain to customers

Partnerships with FinTech firms

Technology is opening the door to competition from non-banks in core

areas such as payments

14

Proactive/ Front-runners

• Ambitious or aggressive innovation strategies, high-targeted transformation projects accompanied by unclear impact and risk assessments (aiming for first-mover advantage)

• Well-thought and comprehensive strategies and targets with strong research orientation and focus on governance, organisational aspects, operations and risk management

PROACTIVE

Reactive

• ‘Followers’ of technological developments, taking a ‘wait and see’ approach, with carefully defined strategies and steady-pace on internal changes

• Institutions reacting to peer pressure, taking a ‘go with the flow’ approach in combination with the concern of staying behind.

Passive

• Lagging behind technological developments due to other significant priorities, slowly trying to catch up following customers’ changing expectations

• Conservative/more traditional institutions reluctant to change

In terms of the level of adoption of innovative technologies, working together with FinTechs, current digitalisation, innovation strategies, along with the respective stage of development, incumbent institutions seem to fall into three groups:

REACTIVE

PASSIVE

Status of FinTech adoption

15

Where FinTech startups are most active

FinTechs are everywhere, especially in payments

16

Overview of the Fintech Sector

Categories Product Areas Examples

Blockchain Cryptocurrencies Smart Contracts

Coinbase, Bitcoin, Ethereum ChainThat

Analytics Artificial Intelligence Machine Leaning Deep Learning Big Data

Kensho Avant Shift Technology

Deposit and Lending P2P Marketplaces Crowdfunding (both investing and lending)

Lending Club, Zopa, SoFi. CreditKarma KickStarter ZestFinance

Payment Money Transfer Online Payment Mobile Payment

Transferwise Stripe, Adyen M-Pesa, One97

Banking Infrastructure Self-service banking Identity and security issues Open bank (API) Personal financial management

Rocketbank iDGate FidorOS3 PostFinance, Qontis

* Source: SWIFT Institute Swift Institute Working Paper No. 2017-002

17

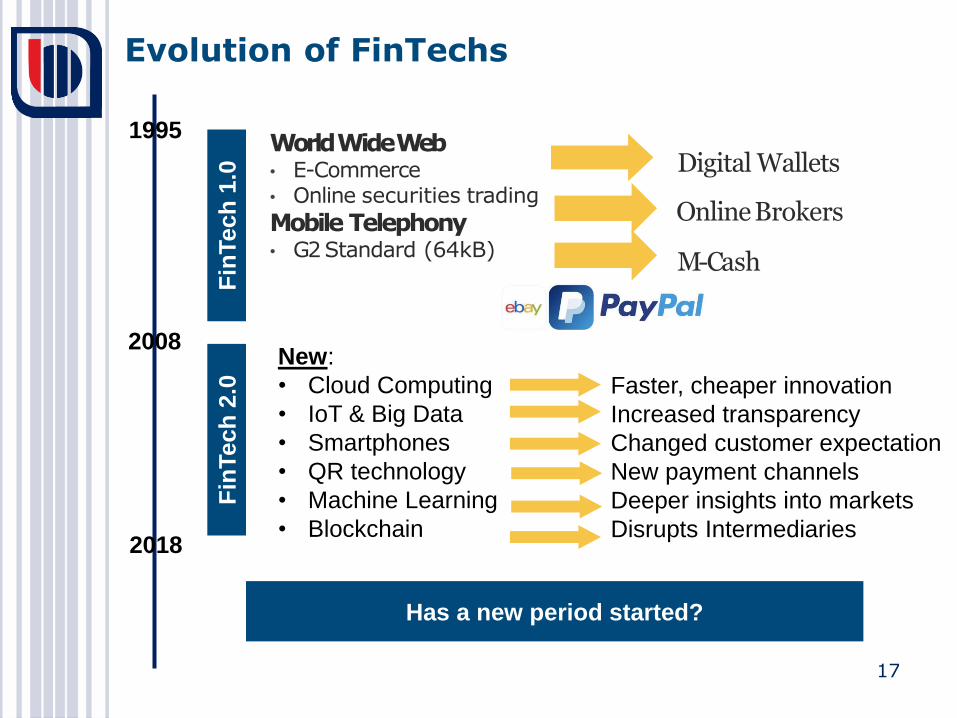

Evolution of FinTechs

1995

2008

2018

Fin

Tech

1.0

F

inTech

2.0

Digital Wallets

Online Brokers

M-Cash

World Wide Web • E-Commerce • Online securities trading

Mobile Telephony • G2 Standard (64kB)

New:

• Cloud Computing

• IoT & Big Data

• Smartphones

• QR technology

• Machine Learning

• Blockchain

Faster, cheaper innovation

Increased transparency

Changed customer expectation

New payment channels

Deeper insights into markets

Disrupts Intermediaries

Has a new period started?

18

BigTech companies

Source: Medici’s Global Fintech Report 2018

Large companies with digital knowledge and experience

19

Advantage and Challenges of Players

Fintech

Startups

Banks

BigTechs

Advantage

• Quick

• Focused

• Specialist

Challenges

• Customer Acquisition

• Competition

• Trust

• $$$

• Customer relationships

• Experience

• Trust

• Customer relationships

• Data

• $$$

• Legacy Systems

• Regulators

• Need to manage risk

• Trust

• Motivation

Trust is very important to customers

20

The required time for digital adaptation is different in each country

Branch dominance

Online users

Strong online presence

Online dominance

Online dominance: more than 95% of transactions and more than 30%

of sales are completed on an online channel

Hungary

21

Key features of SEPA Instant Credit Transfer (SCT Inst)

National Instant Payment Solutions are in progress, but we

should seek to develop global solutions.

22

Instant Payment in Hungary

24 hours a day, 365 days a year (24/7/365)

payments will happen immediate (5 sec)

low value domestic payments via Electronic channel (10.000.000HUF ≈ 32.000EUR)

usage of proxy

maintenance (24 hours in year ≈ 99,7% availability)

Request for payment

These are in line with the Definition on Instant Payment

23

Development of Payment System in Hungary

1984

2012.07.02 2019.07.01 00:00:00

debit : D D D

credit: D+1 D + 4 hours D + 5 sec

Over 25 national instant payment systems already live today around the world

and many others are in the planning or development phase. Instant payments

are rapidly becoming the “new norm” for electronic payments.

24

Impact of Instant Payment on Payment System

40%

60%

NON-Cash

Cash

20%

80%

Volume of Payment Transactions

* Source: G4S Cash Report (2016)

** Source: National Bank of Hungary (2017)

HU**

We have to find the way to Cashless Society!

PSD2 Instant Payment New Technology

Mobile payments are the new key to success

EU28*

25

Who is the winner?

Regulators believe that

New Payment methodes

• will expand access to banking

services,

• support economic growth,

• provide alternatives to bank cards and

cash,

• are opening the real-time payment

markets to new agents and stimulate

competition,

• provide a basis for launching new and

innovative products.

Banks know that

Banks

• are facing a very challenging „new

norm”,

• want to and will remain the key player

within the payment ecosystem,

• want to and can stay a key actor in

payments,

• remain a key trusted partner of billions

of customers.

Real-Time Economy

The Winner is the Customer

Encouraging the use of real-time

electronic payment methods Development & New Solutions

26

Profitability in the Age of Digitalisation

Banks (should) shift priorities toward digitalisation and innovation for

future growth

• Customer needs changing

• New competitors entering

• New technology

• How should banks innovate?

• What will the current account

of the future look like?

• Aggressive innovation

strategies and quick response

• New business model,

partnering with Fintechs and

BigTechs

• Trust as advantage

• New technology to increase

income and cut cost

27

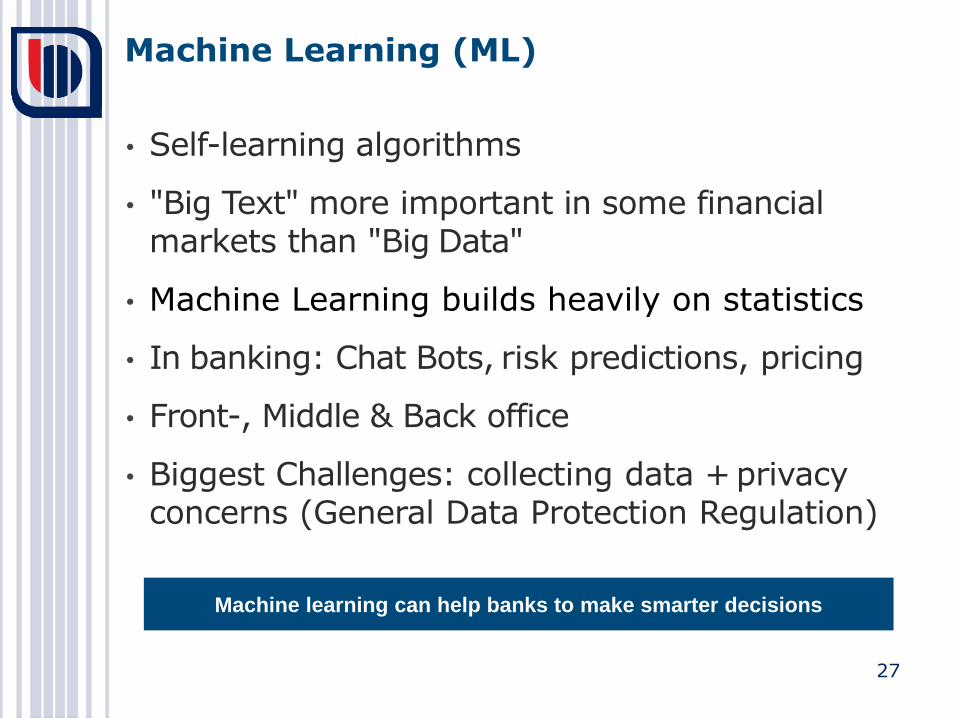

Machine Learning (ML)

• Self-learning algorithms

• "Big Text" more important in some financial markets than "Big Data"

• Machine Learning builds heavily on statistics

• In banking: Chat Bots, risk predictions, pricing

• Front-, Middle & Back office

• Biggest Challenges: collecting data + privacy concerns (General Data Protection Regulation)

Machine learning can help banks to make smarter decisions

28

Artificial Intelligence (AI)

• AI: “ability to learn, understand and think”. • AI is the study of how to make computers make

things which at the moment people do better. • Weak A.I. - Machines with weak Artificial

Intelligence are made to respond to specific situations, but can not think for themselves

• Strong A.I. is able to think and act just like a human. It is able to learn from experiences.

• Examples: Self Driving Cars, Boston Dynamics, Navigation Systems, Chatbots

30

Is this really the future?!

31

Looking into the future

• Real time economy needs new and innovativ Real time payment solution

• How fast and how far will Instant payment develop?

• PSD2 + Instant payment = (R)EVOLUTION?

• Customer experience is the key and Customer must be put at the centre

• Battle for data and customer relationship

• Now Mobile is the key, but future developments in technology remain uncertain.

• (Cyber)security as a key priority

• Will there be banks in the near future as we know them today?

32

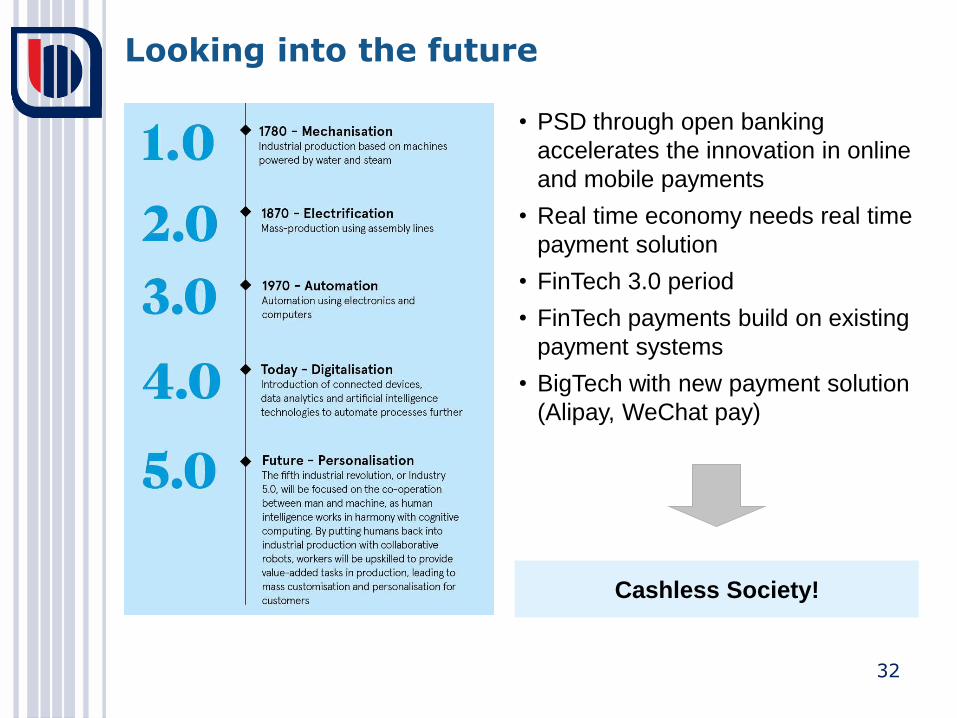

Looking into the future

• PSD through open banking

accelerates the innovation in online

and mobile payments

• Real time economy needs real time

payment solution

• FinTech 3.0 period

• FinTech payments build on existing

payment systems

• BigTech with new payment solution

(Alipay, WeChat pay)

Cashless Society!

33

Conclusion

• New streams (Instant Payment, PSD2, SCT Inst) will change

the payments landscape forever and are rapidly becoming the

“new norm” for electronic payments.

• FinTech 2.0 (3.0) is an evolution, not a revolution.

• Banks are and will be the key players within the renewing

payment ecosystem.

• The shift towards a Real-Time Economy and a Cashless

Society is accelerating the PAYMENTS (R)EVOLUTION.

• Instant payment is the future of payment.

• Consumers are moving to online payment channels, with

retail payments increasingly being carried out via mobile phones.

Mobile payments will be a new key to success.

• BigTechs are offering innovative, consumer-friendly solutions.

• Innovation may start at domestic level, but it should not face

barriers preventing pan-European expansion.

34

Q A &

35

Thank you for your attention!