Embed Size (px)

Citation preview

Diffusion – The key to harnessing Intelligent Automation

Constance L. Hunter

Chief Economist, KPMG

@constancehunter

September 25, 2018

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

• The future might be farther away than you think

• Diffusion matters

• U.S. economic outlook

Outline

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

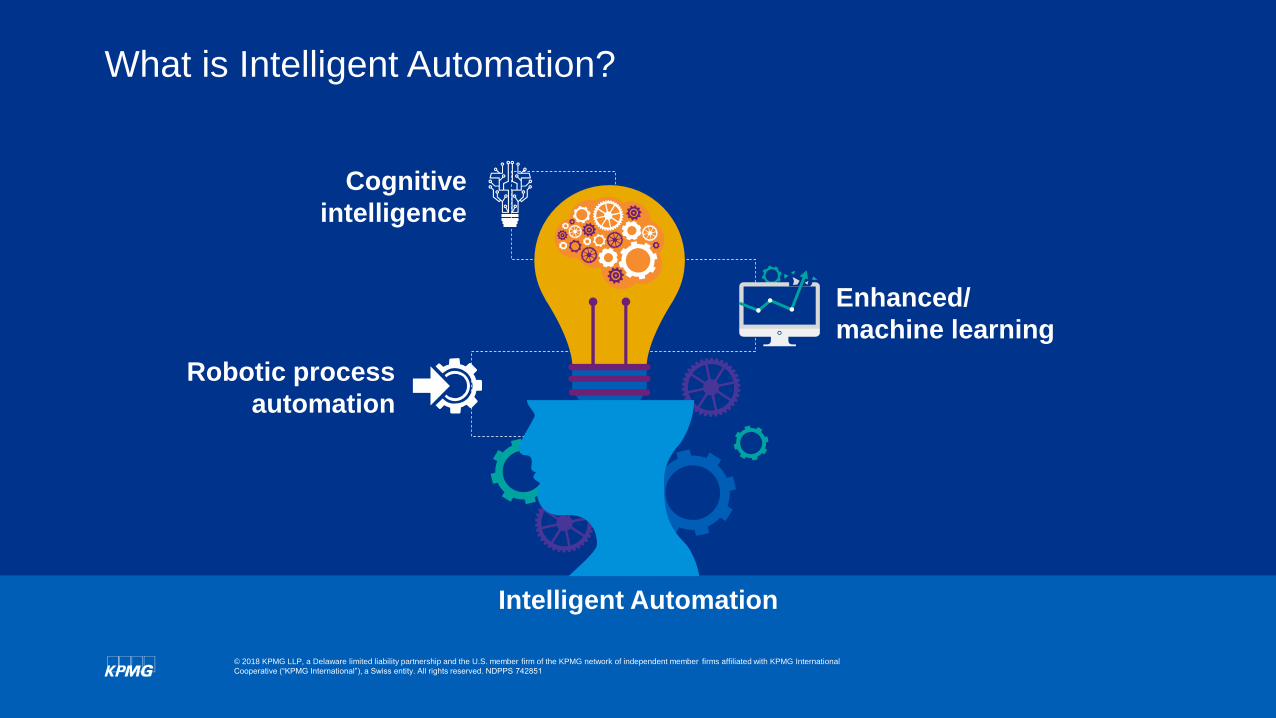

What is Intelligent Automation?

Intelligent Automation

Robotic process

automation

Enhanced/

machine learning

Cognitive

intelligence

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

Recurring phases of each technological revolution

Source: KPMG Economics, Based on Carlota Perez, “Technological Revolutions and Financial Capital: The Dynamics of

Bubbles and Golden Ages”, p. 48, (2002)

MATURITY

De

gre

e o

f d

iffu

sio

n o

f th

e te

ch

no

log

ica

l re

vo

lutio

n

IRRUPTION

Techno-economic split

FRENZY

SYNERGY

Next

Great

SurgeFinancial bubble(s) time

Golden Age

Socio-political split

Big-bang CrashInstitutional

recomposition Next big-bang

Previous

Great

Surge

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

Five successive technological revolutions

Technological

revolution

Popular name for the

periodCore country or countries

Big-bang initiating the

revolutionYear

1stThe 'Industrial

Revolution'Cromford, Britain Arkwright's mill opens 1771

2ndAge of Steam and

Railways

Britain (spreading to Europe

and USA)

Test of the 'Rocket' steam

engine for the Liverpool-

Manchester railway

1829

3rdAge of Steel, Electricity

and Heavy Engineering

USA and Germany forging

ahead and overtaking Britain

The Carnegie Bessemer steel

plant opens in Pittsburgh,

Pennsylvania

1875

4th

Age of Oil, the

Automobile and Mass

Production

USA (with Germany at first

vying for world leadership),

later spreading to Europe

First Model-T comes out of

the Ford plant in Detroit,

Michigan

1908

5thAge of Information and

Telecommunications

USA (spreading to Europe

and Asia)

The Intel microprocessor is

announced in Santa Clara,

California

1971

Source: Carlota Perez, “Technological Revolutions and Techno-economic Paradigms”, p. 6, (2009)

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

Intelligent Automation needs a full ecosystem

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

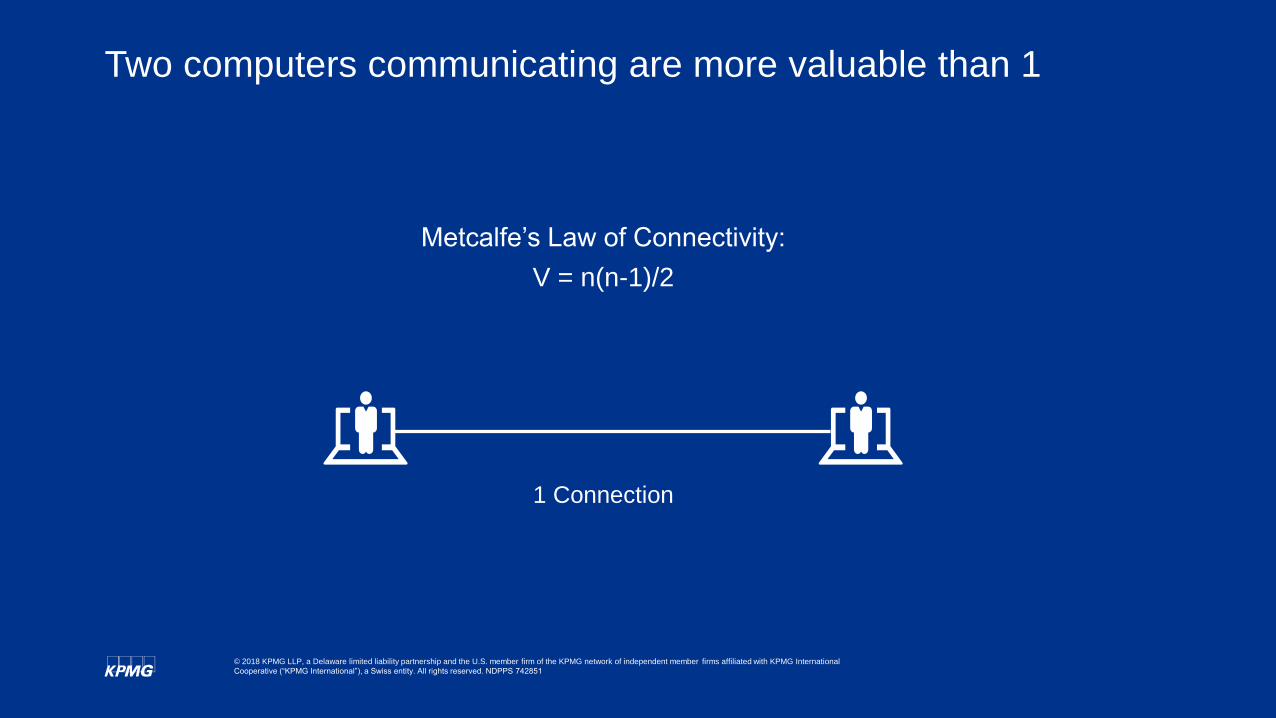

Two computers communicating are more valuable than 1

1 Connection

Metcalfe’s Law of Connectivity:

V = n(n-1)/2

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

The greater the diffusion the greater the value of the technology

45 Connections

Metcalfe’s Law of Connectivity:

V = n(n-1)/2

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

So far diffusion has been minimal

*Frontier Firms are the top 5% of firms in terms of labor productivity gains

Source: KPMG Economics, OECD, Andrews et al, “The Global Productivity Slowdown, Technology Divergence and Public Policy: A

Firm Level Perspective”, (2016)

90

100

110

120

130

140

150

90

100

110

120

130

140

150

2001 2003 2005 2007 2009 2011 2013

Manufacturing

Frontier (Top 5%) Laggards

90

100

110

120

130

140

150

90

100

110

120

130

140

150

2001 2003 2005 2007 2009 2011 2013

Services

Frontier (Top 5%) Laggards

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

The participants of the WEF survey think diffusion is on the rise

42%

29%

58%

71%

0% 20% 40% 60% 80% 100%

2022

2018

Share of Task Hours Performed

Machine Human

Source: KPMG Economics, World Economic Forum, “The Future of Jobs Report”, (September 2018)

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

Technology has historically enabled greater leisure time

0

10

20

30

40

50

60

70

0

10

20

30

40

50

60

70

1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

U.S. Average Weekly Hours1870-2017

2017: 34 Hours

Per Week

1900: 57 Hours

Per Week

Source: KPMG Economics, Haver Analytics, Huberman & Minns, “The times they are not changing’: Days and hours of work in Old and New

Worlds, 1870-2000”, (2007), BLS

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

Not all workers see same benefits from growth

0% 25% 50% 75% 100%

Doctoral degree

Professional degree

Master's degree

Bachelor's degree

Associate's degree

Some college

Only high school

Less than high school

Labor Force Share by Occupation and Educational Attainment2016

Management and professional ServiceSales and office Natural resources and constructionProduction

Source: KPMG Economics, BLS

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

Those with greater education face below 5% chance of job loss

55.0

40.0

17.5

10.0

5.01.5 1.0

0

10

20

30

40

50

60

Primary orLess

LowerSecondary

UpperSecondary

PostSecondary

Short-cycletertiary

Bachelor Master/PhD

Share

of W

ork

ers

at H

igh R

isk(>

70%

)

High Automatability by EdRiskionShare of Workers at High Risk, %

Source: OECD, “Automation and Independent Work In a Digital Economy”, (2016)

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

How do challenges and plans intersect?

Machine Learning > 75%

Information & Communication Technologies

Automotive, Aerospace, Supply Chain &

Transport

Consumer

Global Health & Healthcare

Aviation, Travel & Tourism

Energy, Utilities, & Technologies

Source: KPMG Economics, World Economic Forum, “The Future of Jobs Report”, (September 2018)

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

How do challenges and plans intersect?

Don’t Understand Opportunities> 60%

Consumer

Global Health & Healthcare

Energy, Utilities, & Technologies

Chemistry, Advanced Materials & Biotech

Mining & Metals

Oil & Gas

Source: KPMG Economics, World Economic Forum, “The Future of Jobs Report”, (September 2018)

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

How do challenges and plans intersect?

Machine Learning > 75% & Don’t Understand Opportunities> 60%

Consumer

Global Health & Healthcare

Energy, Utilities, & Technologies

Source: KPMG Economics, World Economic Forum, “The Future of Jobs Report”, (September 2018)

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

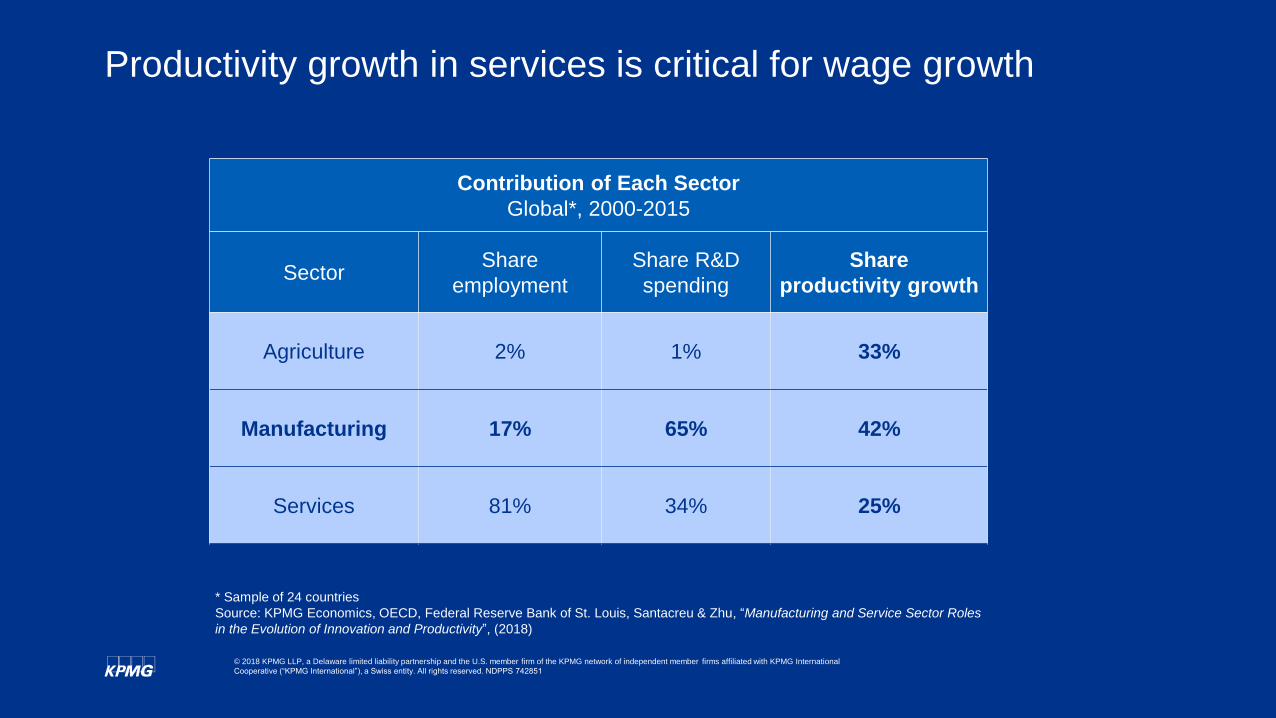

Productivity growth in services is critical for wage growth

Contribution of Each Sector

Global*, 2000-2015

SectorShare

employment

Share R&D

spending

Share

productivity growth

Agriculture 2% 1% 33%

Manufacturing 17% 65% 42%

Services 81% 34% 25%

* Sample of 24 countries

Source: KPMG Economics, OECD, Federal Reserve Bank of St. Louis, Santacreu & Zhu, “Manufacturing and Service Sector Roles

in the Evolution of Innovation and Productivity”, (2018)

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

Productivity growth in services is critical for wage growth

Contribution of Each Sector

Global*, 2000-2015

SectorShare

employment

Share R&D

spending

Share

productivity growth

Agriculture 2% 1% 33%

Manufacturing 17% 65% 42%

Services 81% 34% 25%

* Sample of 24 countries

Source: KPMG Economics, OECD, Federal Reserve Bank of St. Louis, Santacreu & Zhu, “Manufacturing and Service Sector Roles

in the Evolution of Innovation and Productivity”, (2018)

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

The case for capital substitution is well established

r = 0.81

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

U.S. growth is solid and rates are normalizing

Source: KPMG Economics, Natixis, BEA, BLS, Federal Reserve Board, Haver Analytics

`

-4%

-2%

0%

2%

4%

6%

8%

Determinants of the Natural Rate of Interest

Inflation GDP 10 Year Yield Fed Funds Rate

ForecastRecession

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

The outlook is becoming bifurcated

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Dec 2018 June 2019 Dec 2019 June 2020 Dec 2020

August WSJ Survey: Fed Funds to 10-Year Bond Spread

1st 2nd 3rd 4th

Source: KPMG Economics, WSJ Economic Forecasting Survey, August 2018

Quartile:

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 742851

• Diffusion of a variety of technologies is

required to fully realize intelligent

automation’s potential

• The time horizon to the Golden

Age/Synergy phase is peppered with

challenges for diffusion

• Advancements in productivity, especially

in the services sector is key to maintaining

healthy growth rates

• The current U.S. economic backdrop

is steady with low inflation and low

interest rates

• However, the long expansion may only have

1-2 more years to run given growth dynamics

Conclusion

Thank you

© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity.

All rights reserved.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we

endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue

to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

kpmg.com/socialmedia

Some or all of the services described herein may not be permissible for KPMG audit

clients and their affiliates and related entities.