Embed Size (px)

Citation preview

1

CANADA’S INTERMEDIATE GOLD PRODUCER

Detour Lake Mine TourJune 4, 2015

2

Forward Looking InformationThis presentation contains certain forward-looking information and statements as defined in applicable securities law (referred to herein as“forward-looking statements”). Forward-looking statements include, but are not limited to, statements with respect to 2015 guidance forproduction, total cash costs, all-in sustaining costs, operating costs, capital costs, deferred stripping costs, exploration costs and potentialcost reductions; expected throughput, mining and recovery rates; expected future production, mining activities and long term targets forimprovements including mill consumables improvements; opportunities to optimize the mine operation and mitigate near term risks; timelinefor the life of mine plan update, second test for the processing of fines, planned shutdowns, tailings management area construction, Block Apit development and exploration program; and credit facilities, debt repayment and hedging.

Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause actual results, performanceor achievements to be materially different from any of its future results, performance or achievements expressed or implied by forward-looking statements. These risks, uncertainties and other factors include, but are not limited to, assumptions and parameters underlying thelife of mine update not being realized, a decrease in the future gold price, discrepancies between actual and estimated production, changesin costs (including labour, supplies, fuel and equipment), changes to tax rates; environmental compliance and changes in environmentallegislation and regulation, exchange rate fluctuations, general economic conditions and other risks involved in the gold exploration anddevelopment industry, as well as those risk factors discussed in the section entitled “Description of Business - Risk Factors” in DetourGold’s 2014 AIF and in the continuous disclosure documents filed by Detour Gold on and available on SEDAR at www.sedar.com.

Such forward-looking statements are also based on a number of assumptions which may prove to be incorrect, including, but not limited to,assumptions about the following: the availability of financing for exploration and development activities; operating and sustaining capitalcosts; the Company’s ability to attract and retain skilled staff; sensitivity to metal prices and other sensitivities; the supply and demand for,and the level and volatility of the price of, gold; the supply and availability of consumables and services; the exchange rates of the Canadiandollar to the U.S. dollar; energy and fuel costs; the accuracy of reserve and resource estimates and the assumptions on which the reserveand resource estimates are based; market competition; ongoing relations with employees and impacted communities and general businessand economic conditions. Accordingly, readers should not place undue reliance on forward-looking statements. The forward-lookingstatements contained herein are made as of the date hereof, or such other date or dates specified in such statements.

All forward-looking statements in this presentation are necessarily based on opinions and estimates made as of the date such statementsare made and are subject to important risk factors and uncertainties, many of which cannot be controlled or predicted. Detour Gold and theQualified Persons who authored the associated Technical Report undertake no obligation to update publicly or otherwise revise anyforward-looking statements contained herein whether as a result of new information or future events or otherwise, except as may berequired by law.

3

Notes to Investors

The scientific and technical content of this presentation was reviewed, verified and approved by Drew Anwyll, P.Eng., Senior Vice President Technical Services, and exploration results was reviewed, verified and approved by Guy MacGillivray, P.Geo., Exploration Manager , both Qualified Person as defined by Canadian Securities Administrators National Instrument 43-101 “Standards of Disclosure for Mineral Projects”.

Qualified Persons

Non-IFRS Financial Performance MeasuresThe Company has included non-IFRS measures in this presentation: total cash costs, all-in sustaining costs, adjusted net loss and adjusted net loss pershare. The Company believes that these measures, in addition to conventional measures prepared in accordance with IFRS, provide investors an improvedability to evaluate the underlying performance of the Company. The non-IFRS measures are intended to provide additional information and should not beconsidered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. These measures do not have any standardizedmeaning prescribed under IFRS, and therefore may not be comparable to other issuers. Other companies may calculate these measure differently.

Detour Gold reports total cash costs on a sales basis. Total cash costs include production costs such as mining, processing, refining and siteadministration, less non-cash share-based compensation and net of silver sales divided by gold ounces sold to arrive at total cash costs per gold ouncesold. The measure also includes other mine related costs incurred such as mine standby costs and current inventory write downs. Production costs areexclusive of depreciation and depletion. Production costs include the costs associated with providing the royalty in kind ounces.

Commencing in 2015, the Company adopted all-in sustaining costs on a prospective basis. The Company believes this measure more fully defines the totalcosts associated with producing gold. The Company calculates all-in sustaining costs as the sum of total cash costs (as described above), share-basedcompensation, corporate general and administrative expense, exploration and evaluation expenses that are sustaining in nature, reclamation costaccretion, sustaining capital including deferred stripping, and realized gains and losses on hedges due to operating and capital costs, all divided by the goldounces sold to arrive at a per ounce figure.

Costs excluded from all-in sustaining costs are non-sustaining capital expenditures and exploration costs that are expected to materially increaseproduction, financing costs and tax expense. Consequently, this measure is not representative of all of the Company’s cash expenditures. In addition, thecalculation of all-in sustaining costs does not include depreciation and depletion expense as it does not reflect the impact of expenditures incurred in priorperiods.

Adjusted net loss and adjusted basic loss per share are used by management and investors to measure the underlying operating performance of theCompany. Presenting these measures from period to period helps management and investors evaluate earnings trends more readily in comparison withresults from prior periods. Adjusted net loss is defined as net loss adjusted to exclude specific items that are significant, but not reflective of the underlyingoperations of the Company, including: fair value change of the convertible notes, the impact of foreign exchange gains and losses, including the foreignexchange on deferred income and mining taxes, non-cash unrealized gains and losses on derivative instruments, accretion on convertible notes, unwindingof discount on decommissioning and restoration provisions, impairment provisions and reversals thereof, and other non-recurring items. Adjusted basic netloss per share is calculated using the weighted average number of shares outstanding under the basic method of loss per share as determined underIFRS.

4

Morning Presentations (in the bus): Welcoming remarks – Paul Martin, President & CEO Detour Lake Operation – Pierre Beaudoin, COO Financial review – Paul Martin, President & CEO Near-term opportunities – Pierre Beaudoin, COOSite Visit Tour Plant – Andrew Nugent, Process Plant Operations Manager and Keiran Whitefield,

Business Improvement Manager (former Maintenance Manager) Mine plan – Craig Rintoul, Open Pit Manager and Josh Hurrell, Technical Services

SuperintendentLunch Time Presentations: Q&A with Mine and Processing Plant team Exploration – Jean-Francois Metail, VP Mineral Resource Management and Guy

MacGillivray, Exploration Manager Core display of Lower Detour

Agenda

5

Unique Investment OpportunityMining-friendly Jurisdiction

Large-scale, long mine life

Largest gold producing mine not controlled by a senior producer

Growing cash flow profile

Production growth opportunities

Favourable exposure to Canadian Dollar

DOMINANTGOLD PRODUCER IN CANADA

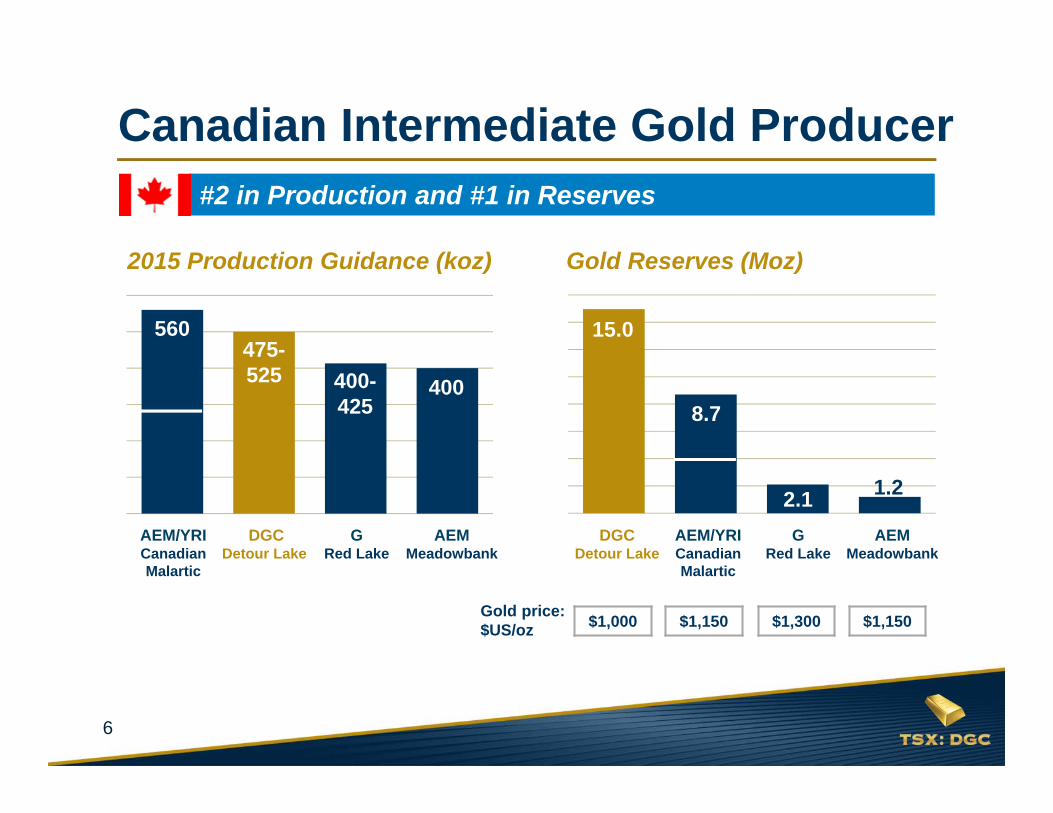

6

2015 Production Guidance (koz)

#2 in Production and #1 in Reserves

DGCDetour Lake

AEM/YRICanadian Malartic

AEMMeadowbank

GRed Lake

Canadian Intermediate Gold Producer

400-425

560475-525 400

Gold Reserves (Moz)

DGCDetour Lake

AEM/YRICanadian Malartic

AEMMeadowbank

GRed Lake

2.1

15.0

8.7

1.2

$1,000 $1,150 $1,300 $1,150Gold price: $US/oz

7

Responsible mining is more than a commitment- It’s what we do every day

Did you know? Detour Lake water balance

is at equilibrium. Thismeans no discharge overthe last 2 ½ years ofoperation

Our first CSR update has been published and is available on our website

Our Life Saving Rules help raise the visibility of safety to ensure everyone on our site goes home safely

Corporate Responsibility

MAINTENANCE

LABOUR18%

8

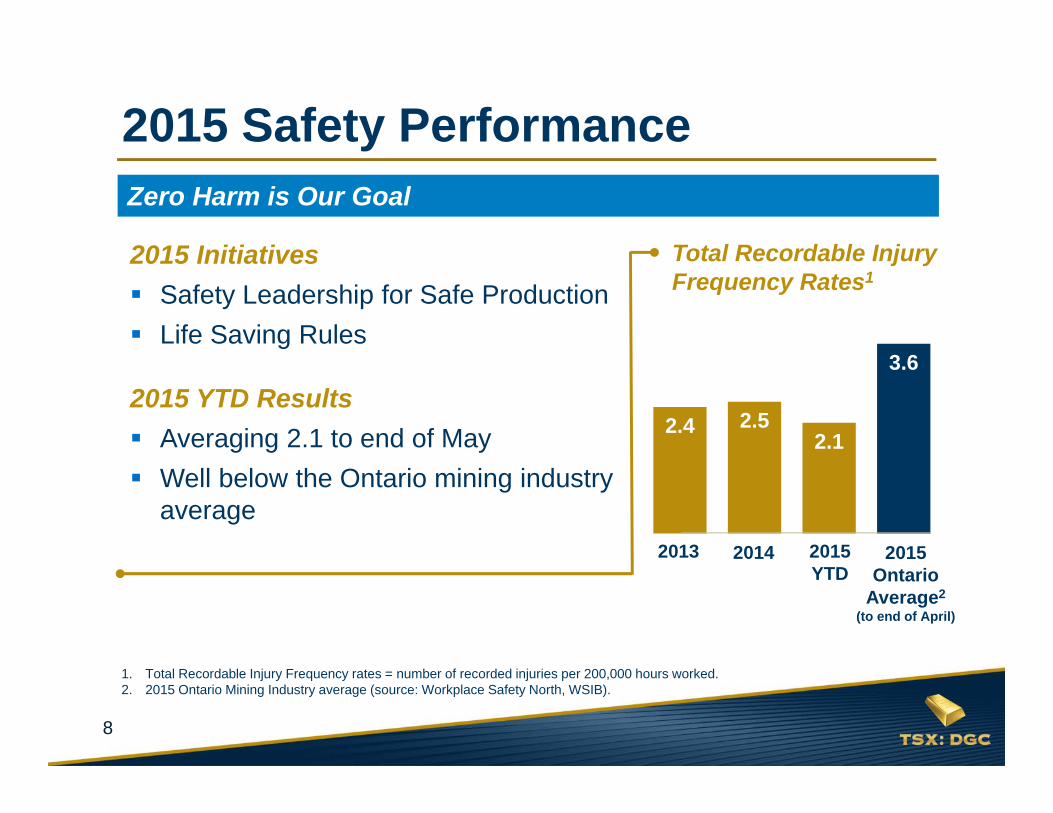

Zero Harm is Our Goal

Total Recordable Injury Frequency Rates1

2.4 2.52.1

3.6

00.5

11.5

22.5

33.5

4

2015 Safety Performance

2013 2014 2015 Ontario

Average2

(to end of April)

2015 Initiatives Safety Leadership for Safe Production Life Saving Rules

2015 YTD Results Averaging 2.1 to end of May Well below the Ontario mining industry

average

1. Total Recordable Injury Frequency rates = number of recorded injuries per 200,000 hours worked.2. 2015 Ontario Mining Industry average (source: Workplace Safety North, WSIB).

2015 YTD

9

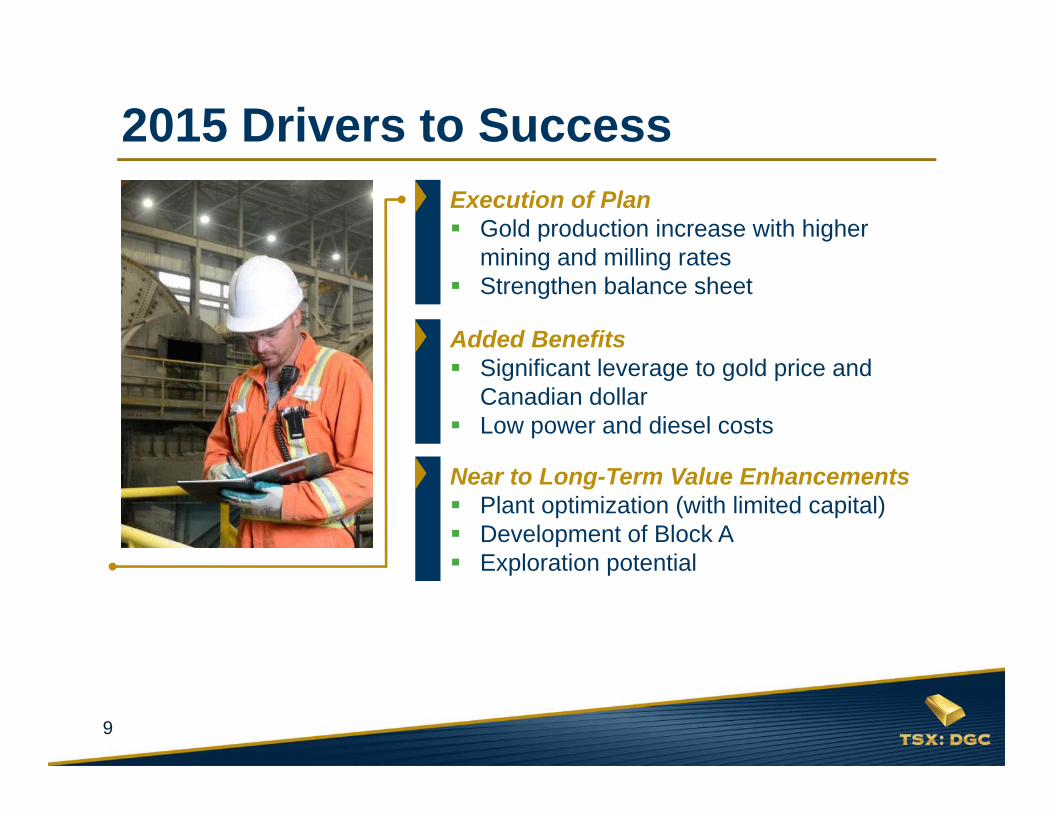

2015 Drivers to SuccessExecution of Plan Gold production increase with higher

mining and milling rates Strengthen balance sheet

Added Benefits Significant leverage to gold price and

Canadian dollar Low power and diesel costs

Near to Long-Term Value Enhancements Plant optimization (with limited capital) Development of Block A Exploration potential

10

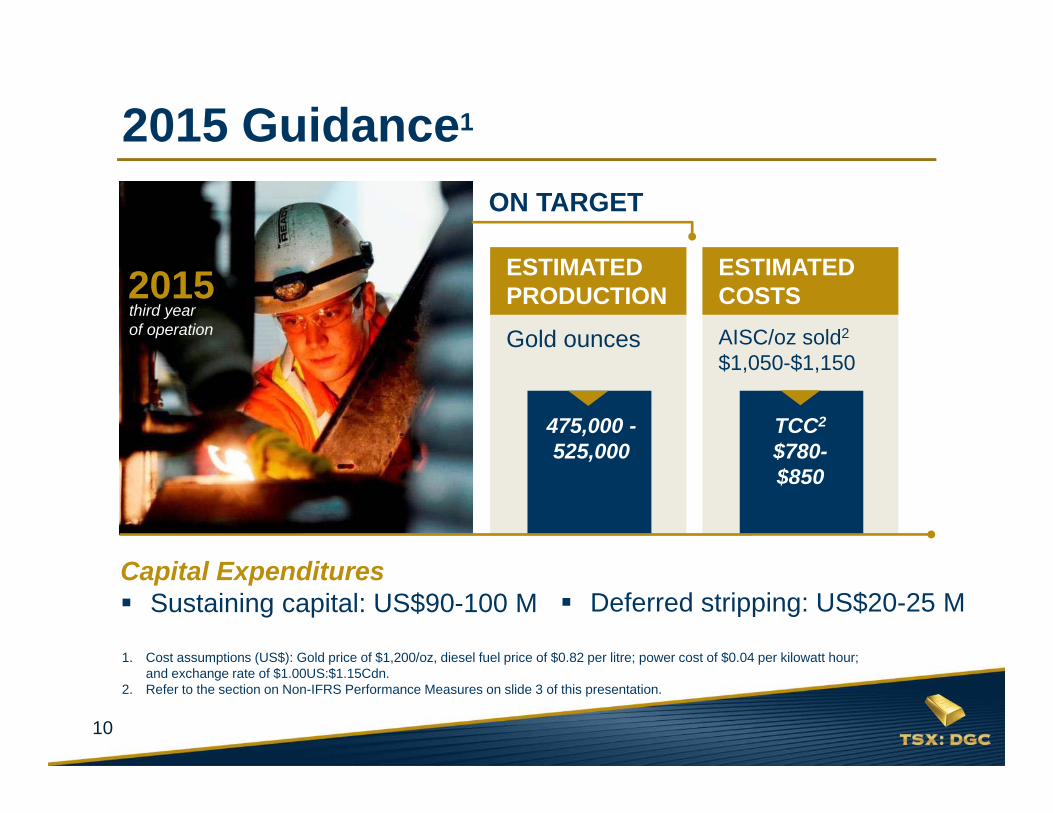

third year of operation

2015

2015 Guidance1

TCC2

$780-$850

AISC/oz sold2

$1,050-$1,150

Capital Expenditures Sustaining capital: US$90-100 M

ON TARGET

475,000 -525,000

Gold ounces

ESTIMATED COSTS

ESTIMATED PRODUCTION

Deferred stripping: US$20-25 M

1. Cost assumptions (US$): Gold price of $1,200/oz, diesel fuel price of $0.82 per litre; power cost of $0.04 per kilowatt hour; and exchange rate of $1.00US:$1.15Cdn.

2. Refer to the section on Non-IFRS Performance Measures on slide 3 of this presentation.

11

DETOUR LAKE OPERATIONPierre Beaudoin, COO 2015

12

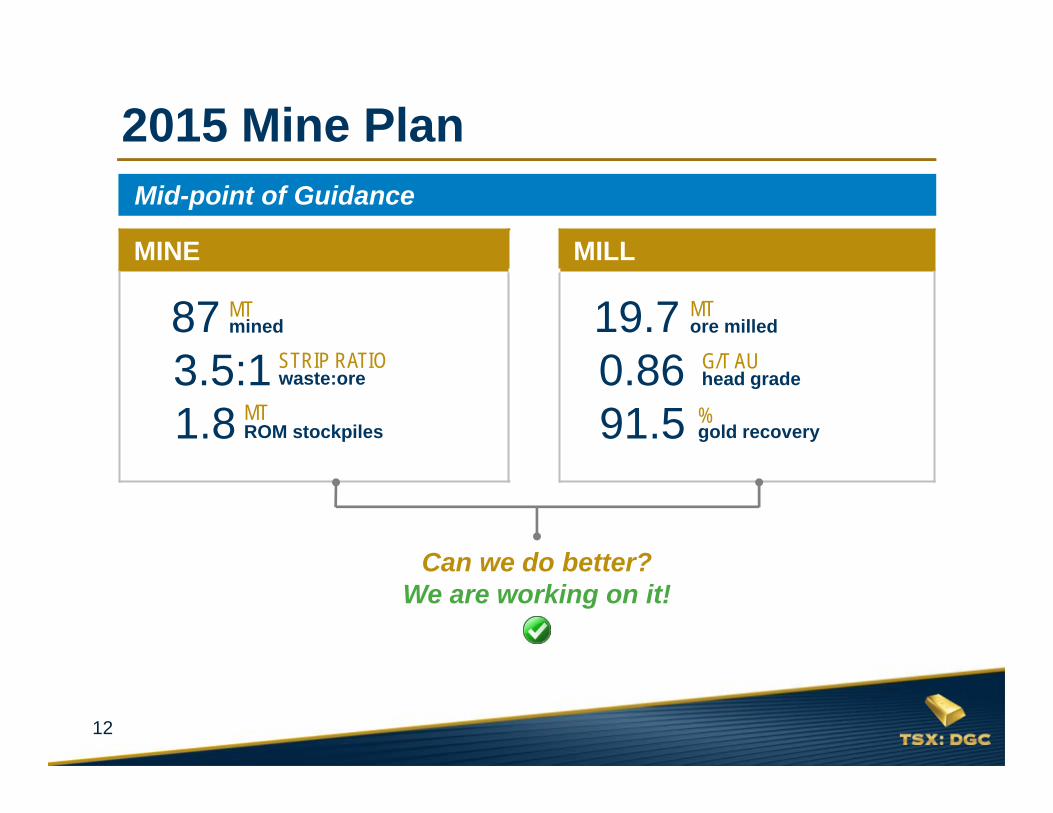

MINE MILL

2015 Mine PlanMid-point of Guidance

MTmined

3.5:1 STRIP RATIOwaste:ore

MTROM stockpiles

87

1.8

MTore milled

0.86 G/T AUhead grade

%gold recovery

19.7

91.5

Can we do better?We are working on it!

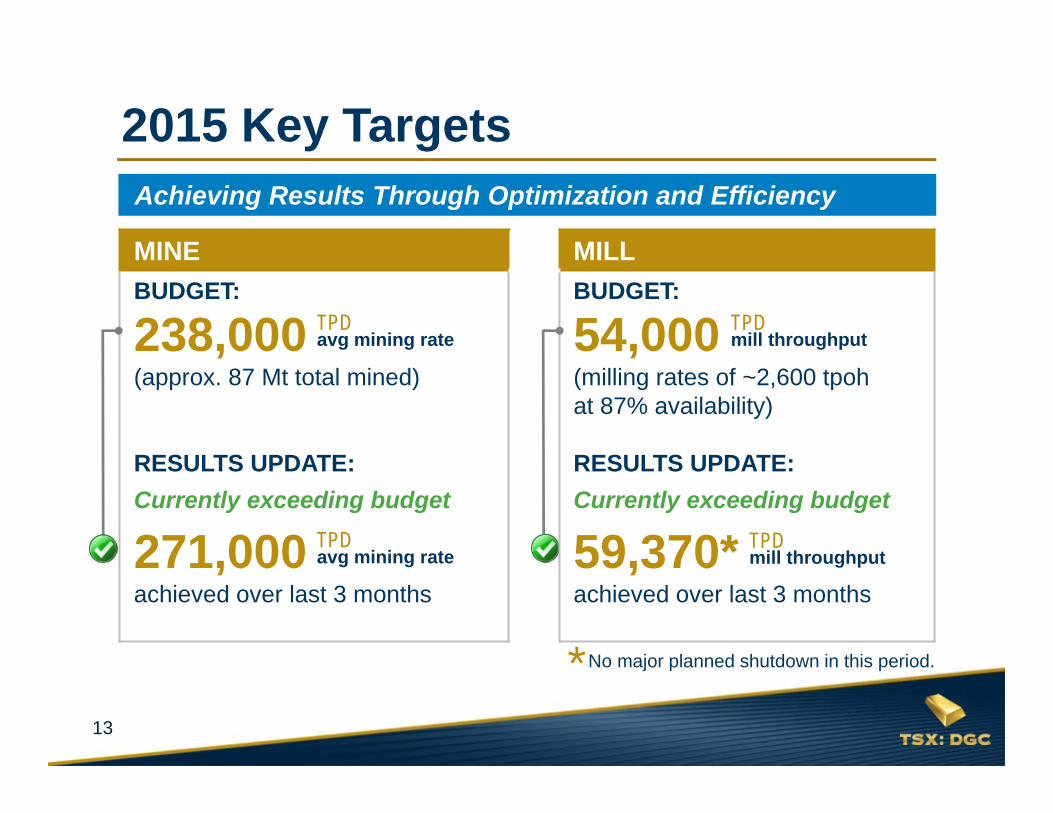

13

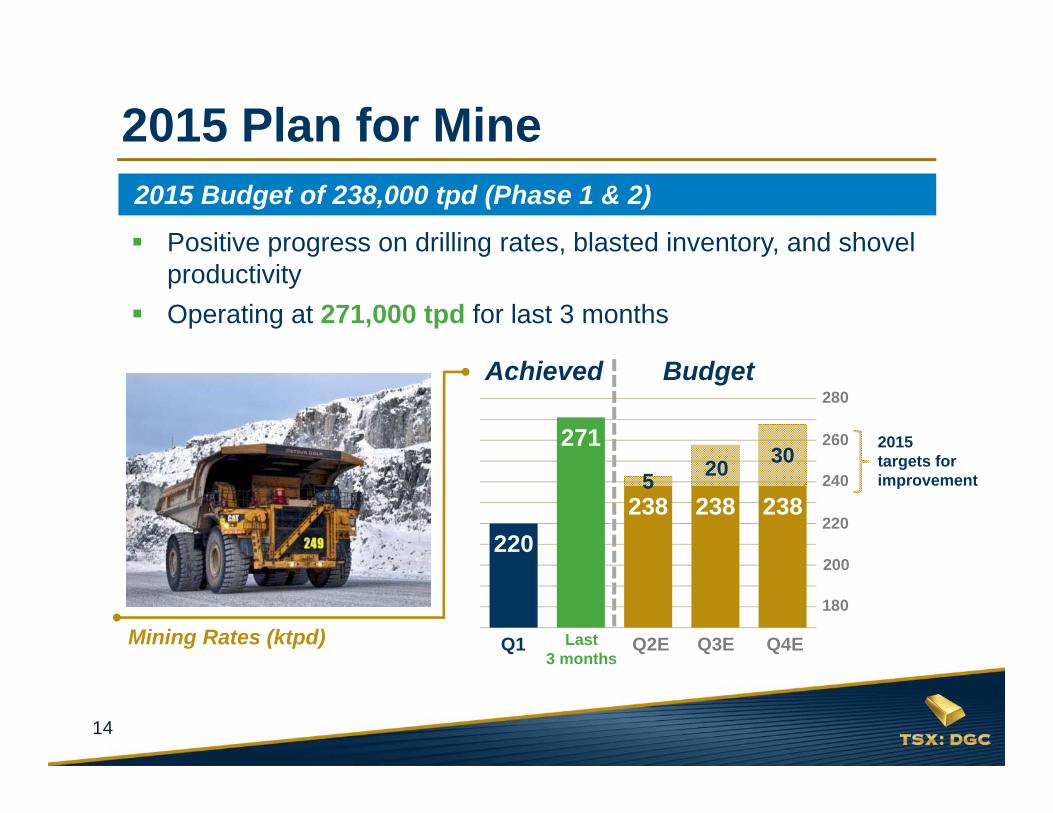

MINE MILLBUDGET:

238,000(approx. 87 Mt total mined)

RESULTS UPDATE:Currently exceeding budget

271,000achieved over last 3 months

BUDGET:

54,000(milling rates of ~2,600 tpohat 87% availability)

RESULTS UPDATE:Currently exceeding budget

59,370*achieved over last 3 months

2015 Key TargetsAchieving Results Through Optimization and Efficiency

TPDavg mining rate

TPDavg mining rate

TPDmill throughput

TPDmill throughput

No major planned shutdown in this period.*

14

220

271

238 238 2385 20 30

Q1

280

Positive progress on drilling rates, blasted inventory, and shovel productivity

Operating at 271,000 tpd for last 3 months

Q2E Q4EQ3EMining Rates (ktpd)

2015 targets for improvement

260

220

180

2015 Plan for Mine2015 Budget of 238,000 tpd (Phase 1 & 2)

200

240

Last 3 months

Achieved Budget

15

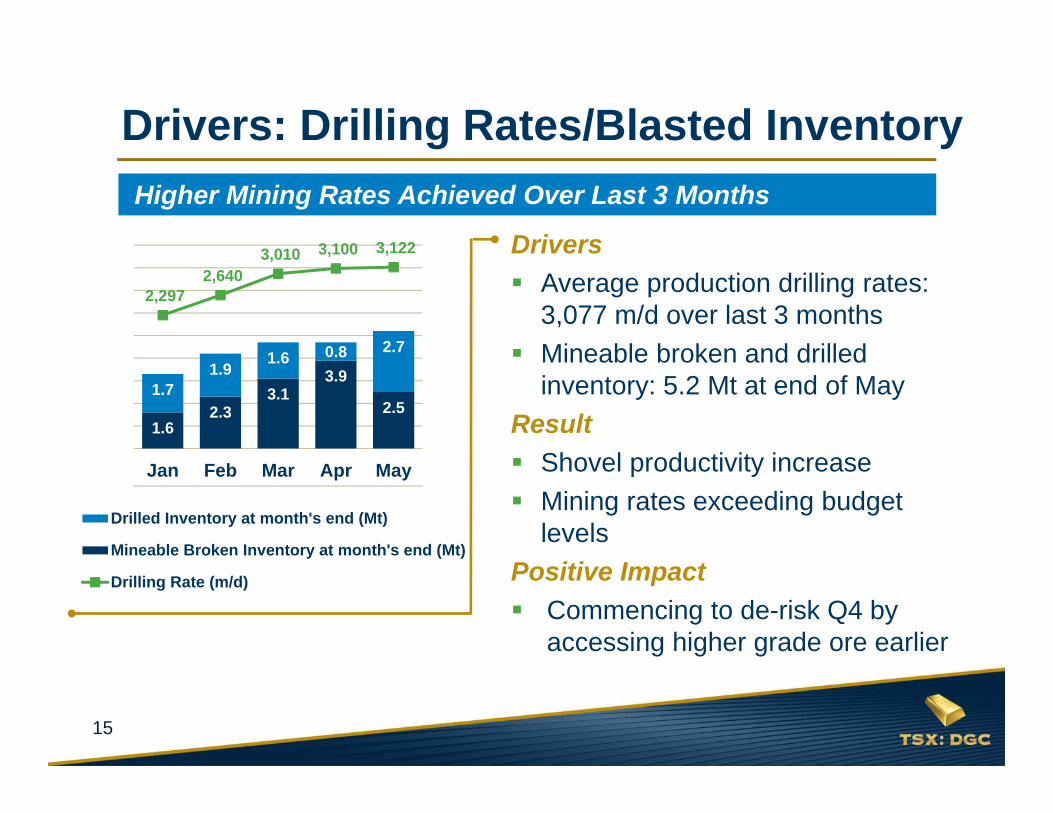

Drivers Average production drilling rates:

3,077 m/d over last 3 months Mineable broken and drilled

inventory: 5.2 Mt at end of MayResult Shovel productivity increase Mining rates exceeding budget

levelsPositive Impact Commencing to de-risk Q4 by

accessing higher grade ore earlier

Drivers: Drilling Rates/Blasted Inventory

1.62.3

3.13.9

2.51.7

1.91.6 0.8 2.7

2,297 2,640

3,010 3,100 3,122

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0.01.02.03.04.05.06.07.08.09.0

Jan Feb Mar Apr May

Drilled Inventory at month's end (Mt)

Mineable Broken Inventory at month's end (Mt)

Drilling Rate (m/d)

Higher Mining Rates Achieved Over Last 3 Months

16

4,465 4,739

5,048 5,137 4,914

4,400.04,600.04,800.05,000.05,200.0

69 69

81

73

87 74 74

77

78

78

50.060.070.080.090.0

100.0

Jan Feb Mar Apr May

Availability (%)Utilization (%)2,423 2,407

2,583 2,602 2,748

2,350.02,450.02,550.02,650.02,750.02,850.0

Jan Feb Mar Apr May

78 76

54

83 83

75 75

77

78 7950.060.070.080.090.0

100.0

Jan Feb Mar Apr May

Availability (%)Utilization (%)

Shovel Productivity

Availability & Utilization (%):Shovel Productivity (tpoh):CAT 7495

CAT 6060CAT 6060

CAT 7495

Significant Shovel Productivity Improvements

Improving trend:

Productivity Availability Utilization

*Started mining with CAT7495 trucks south of Campbell pit.

*

17

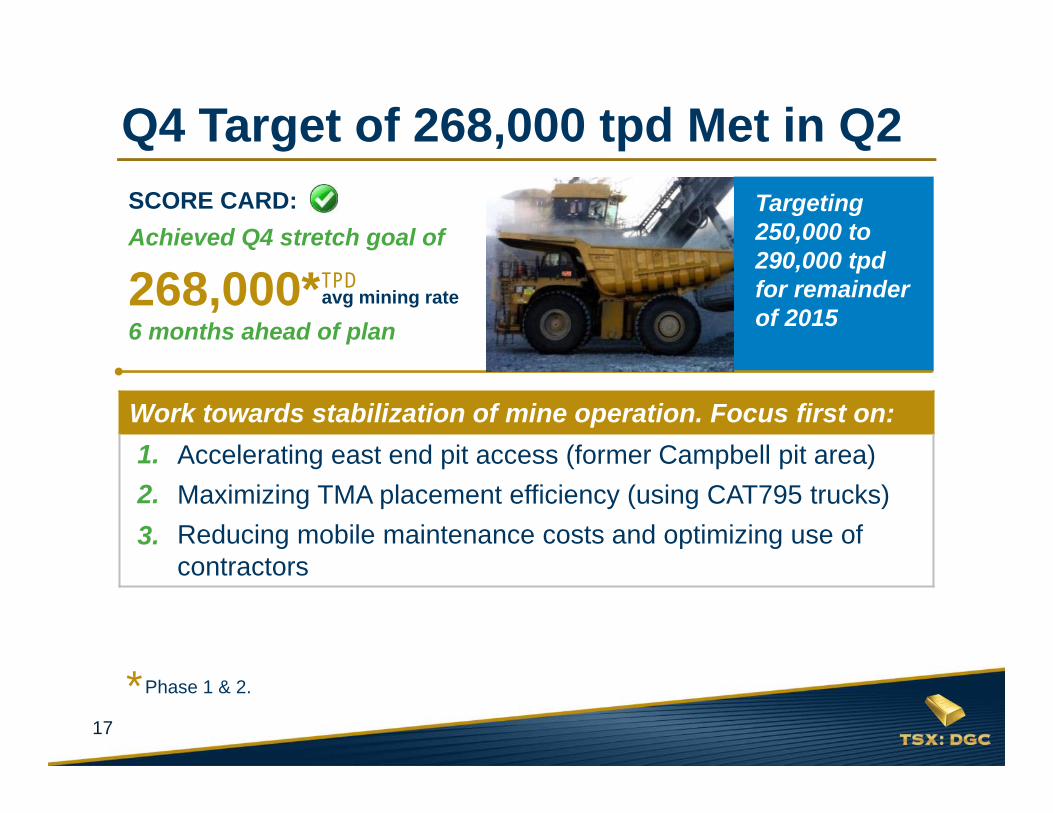

Q4 Target of 268,000 tpd Met in Q2SCORE CARD:Achieved Q4 stretch goal of

268,000*6 months ahead of plan

TPDavg mining rate

Phase 1 & 2.*

Targeting 250,000 to 290,000 tpdfor remainder of 2015

Work towards stabilization of mine operation. Focus first on:1. Accelerating east end pit access (former Campbell pit area)2. Maximizing TMA placement efficiency (using CAT795 trucks)3. Reducing mobile maintenance costs and optimizing use of

contractors

1.2.3.

18

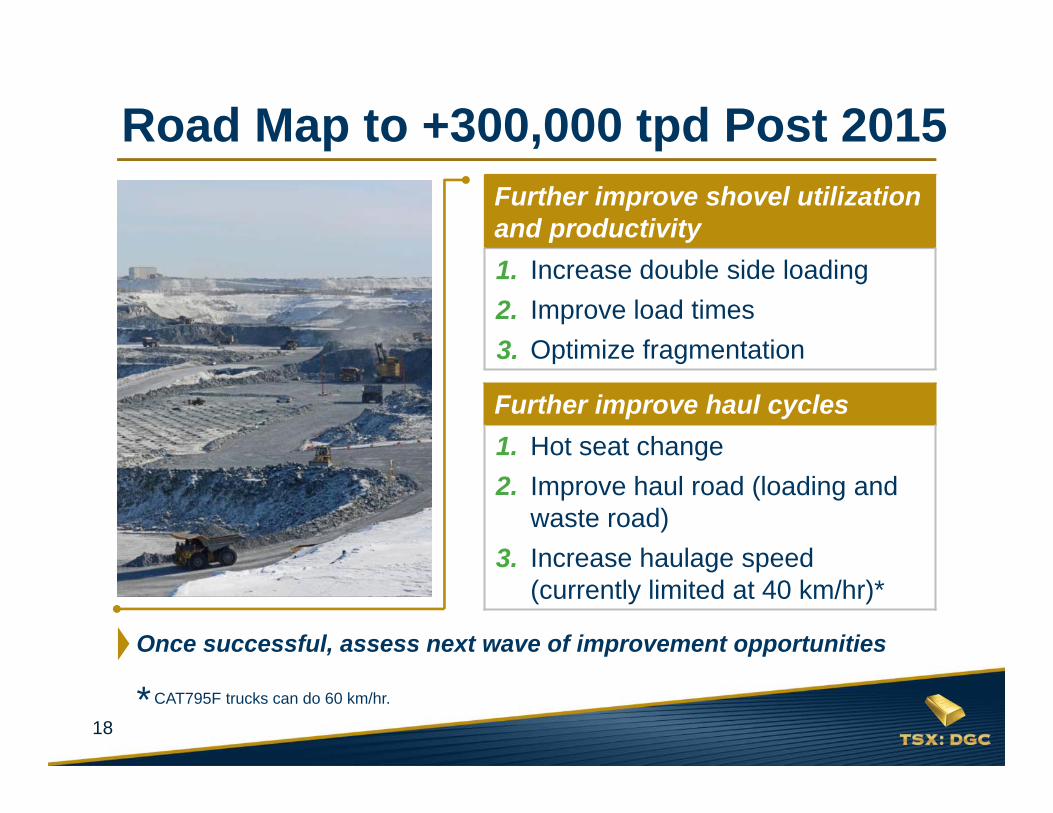

Road Map to +300,000 tpd Post 2015Further improve shovel utilization and productivity Increase double side loading Improve load times Optimize fragmentation

Further improve haul cycles Hot seat change Improve haul road (loading and

waste road) Increase haulage speed

(currently limited at 40 km/hr)*

1.2.

3.

1.2.3.

Once successful, assess next wave of improvement opportunities

*CAT795F trucks can do 60 km/hr.

19

020406080

100120140160180200

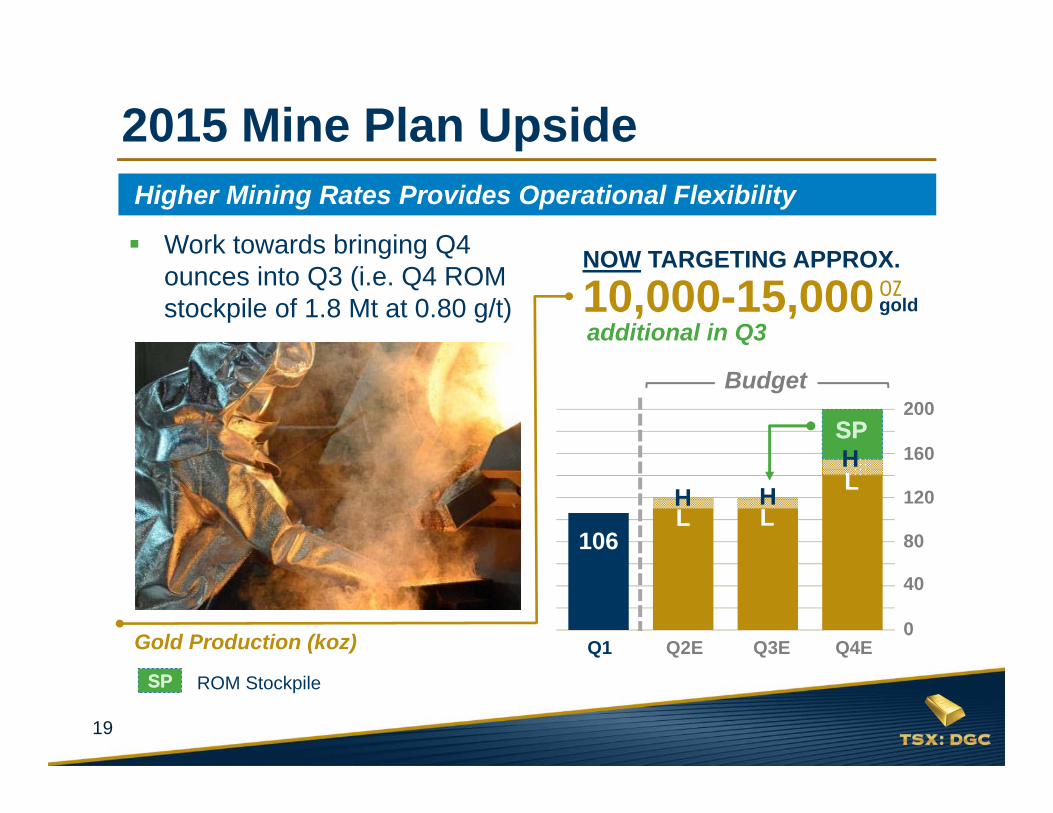

Work towards bringing Q4 ounces into Q3 (i.e. Q4 ROM stockpile of 1.8 Mt at 0.80 g/t)

200

160

120

80

40

0

Higher Mining Rates Provides Operational Flexibility

2015 Mine Plan Upside

H HHL

L L

SPSP

106

Q2E Q4EQ3EQ1Gold Production (koz)

ROM Stockpile

10,000-15,000additional in Q3

OZgold

NOW TARGETING APPROX.

Budget

SPSP

20

48

5955 55 55

30

35

40

45

50

55

60

Q1'15 Last 3months

Q2'15 Q3'15 Q4'15

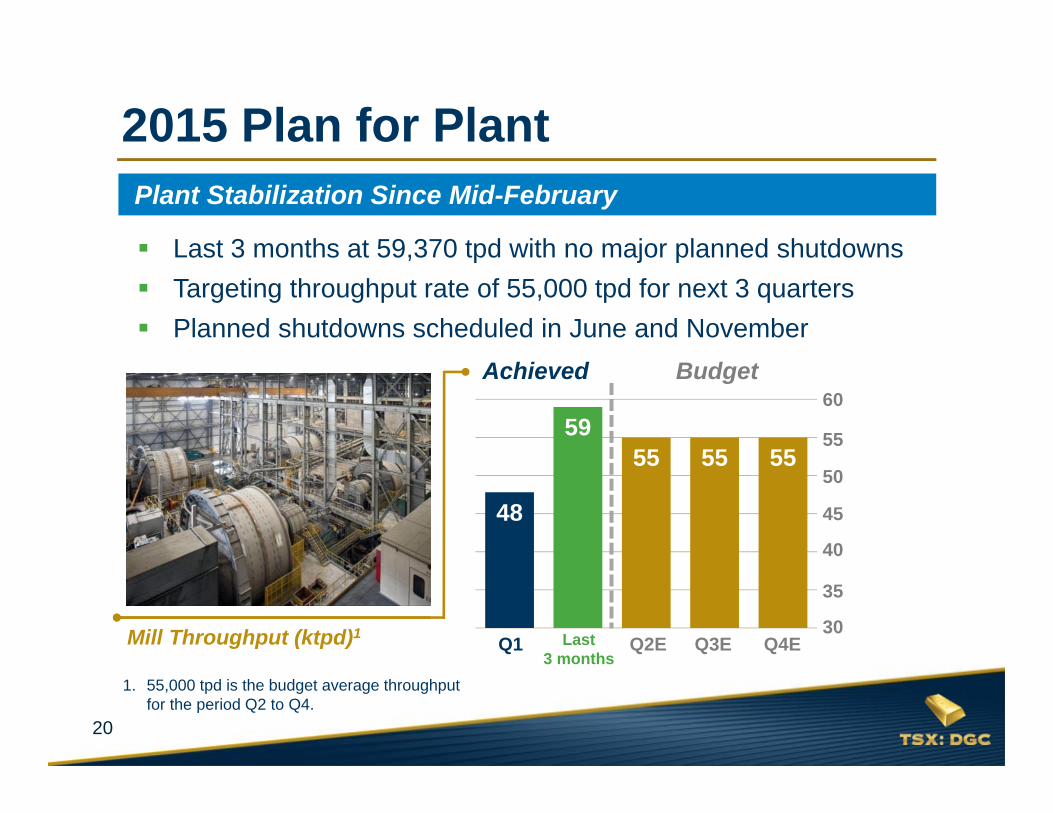

Last 3 months at 59,370 tpd with no major planned shutdowns Targeting throughput rate of 55,000 tpd for next 3 quarters Planned shutdowns scheduled in June and November

Plant Stabilization Since Mid-February

2015 Plan for Plant

Mill Throughput (ktpd)1

1. 55,000 tpd is the budget average throughput for the period Q2 to Q4.

60

50

40

30Q2E Q4EQ3EQ1 Last

3 months

Achieved Budget

35

55

45

21

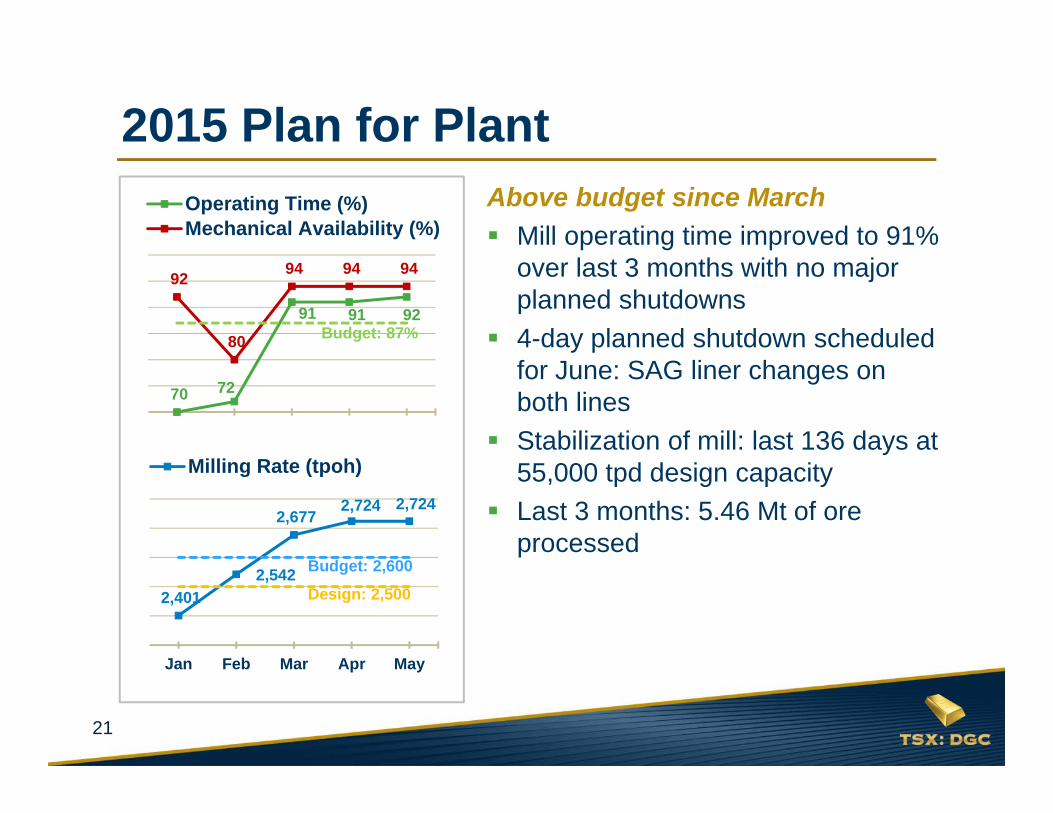

70 72

91 91 92

92

80

94 94 94

70.0

75.0

80.0

85.0

90.0

95.0

100.0

Jan Feb Mar Apr May

Operating Time (%)Mechanical Availability (%)

Above budget since March Mill operating time improved to 91%

over last 3 months with no major planned shutdowns

4-day planned shutdown scheduled for June: SAG liner changes on both lines

Stabilization of mill: last 136 days at 55,000 tpd design capacity

Last 3 months: 5.46 Mt of ore processed

2,401 2,542

2,677 2,724 2,724

2,300.0

2,400.0

2,500.0

2,600.0

2,700.0

2,800.0

Jan Feb Mar Apr May

Milling Rate (tpoh)

2015 Plan for Plant

Budget: 2,600

Budget: 87%

Design: 2,500

22

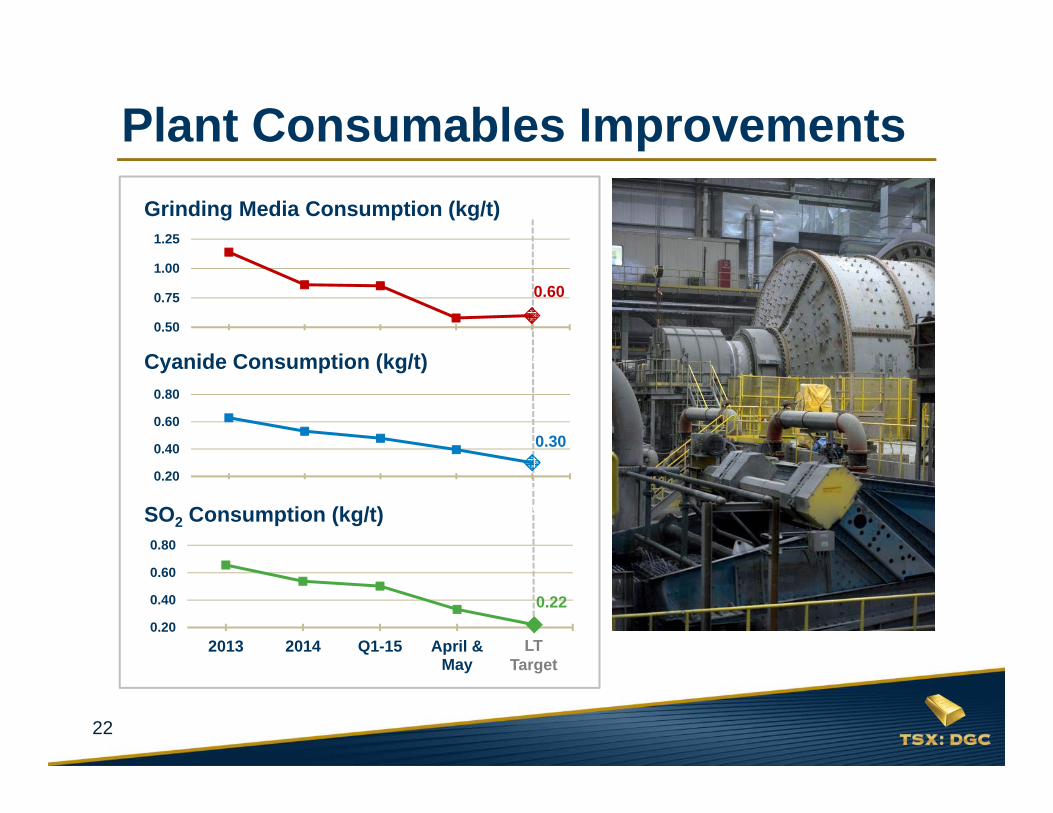

0.60

0.50

0.75

1.00

1.25

2013 2014 Q1-15 Q2-15to May 21

LTTarget

0.30

0.20

0.40

0.60

0.80

2013 2014 Q1-15 Q2-15to May 21

LTTarget

0.220.20

0.40

0.60

0.80

2013 2014 Q1-15 April &May

LTTarget

Grinding Media Consumption (kg/t)

SO2 Consumption (kg/t)

Cyanide Consumption (kg/t)

LT Target

Plant Consumables Improvements

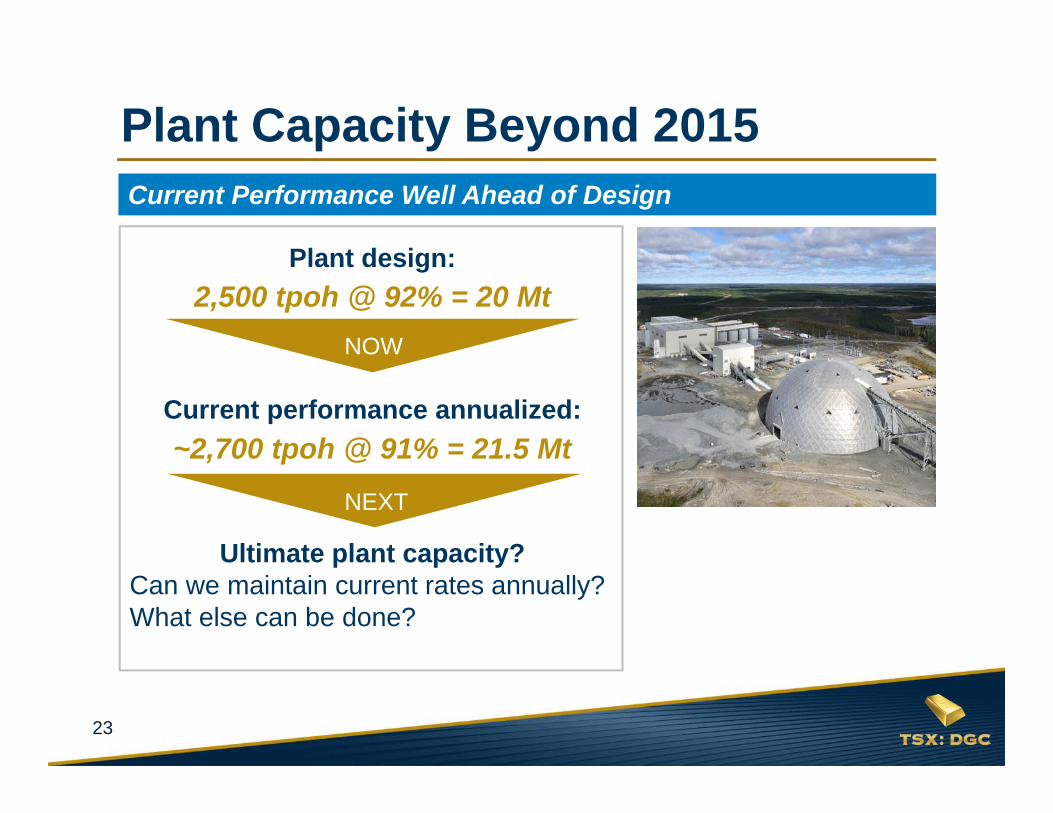

23

Plant design:

Current performance annualized:

Ultimate plant capacity?Can we maintain current rates annually?What else can be done?

Plant Capacity Beyond 2015Current Performance Well Ahead of Design

~2,700 tpoh @ 91% = 21.5 Mt

2,500 tpoh @ 92% = 20 MtNOW

NEXT

24

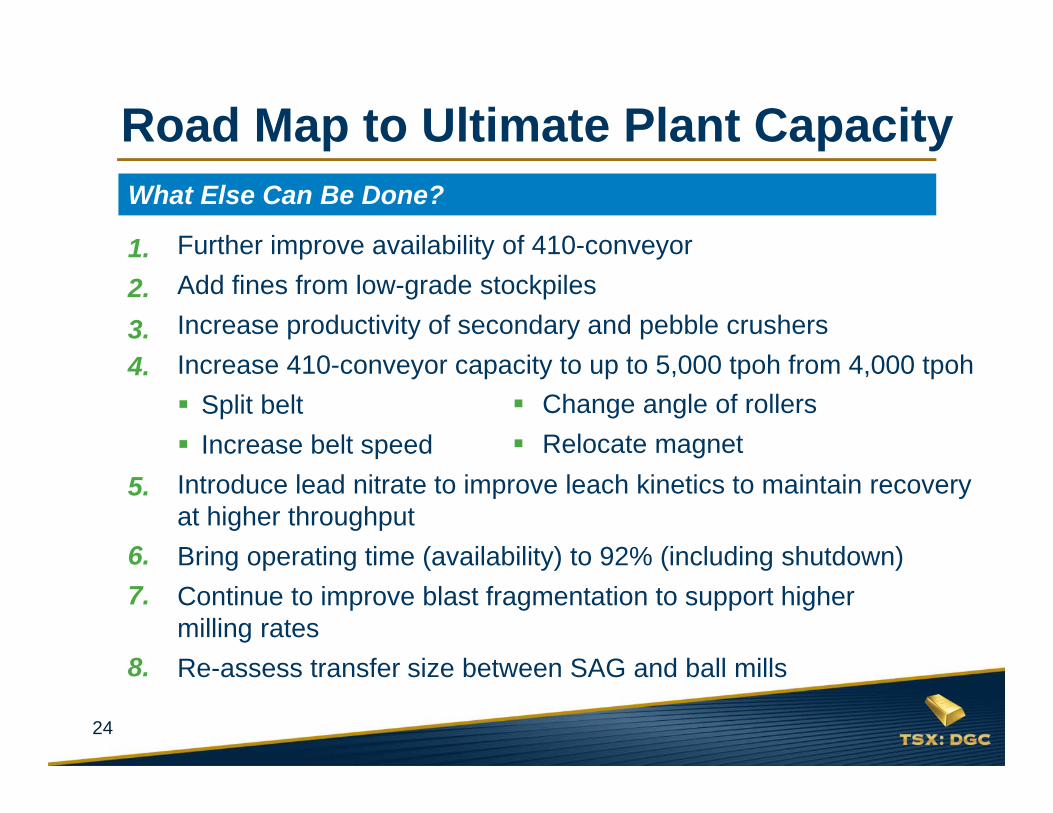

Road Map to Ultimate Plant Capacity

1. Further improve availability of 410-conveyor1. Add fines from low-grade stockpiles2. Increase productivity of secondary and pebble crushers3. Increase 410-conveyor capacity to up to 5,000 tpoh from 4,000 tpoh

Split belt Increase belt speed

4. Introduce lead nitrate to improve leach kinetics to maintain recovery at higher throughput

5. Bring operating time (availability) to 92% (including shutdown)6. Continue to improve blast fragmentation to support higher

milling rates7. Re-assess transfer size between SAG and ball mills

1.2.3.4.

5.

What Else Can Be Done?

6.7.

8.

Change angle of rollers Relocate magnet

25

Near-term Risks to be Mitigated

MINE MILL1. Water management

program2. Mine equipment

winterization (for extreme cold weather)

3. UG workings4. Campbell Pit bottom

clean up

1. 410-conveyor reliability2. Plant winterization

(for extreme cold weather), including stockpile management

1.

2.

3.

1.2.

4.

26

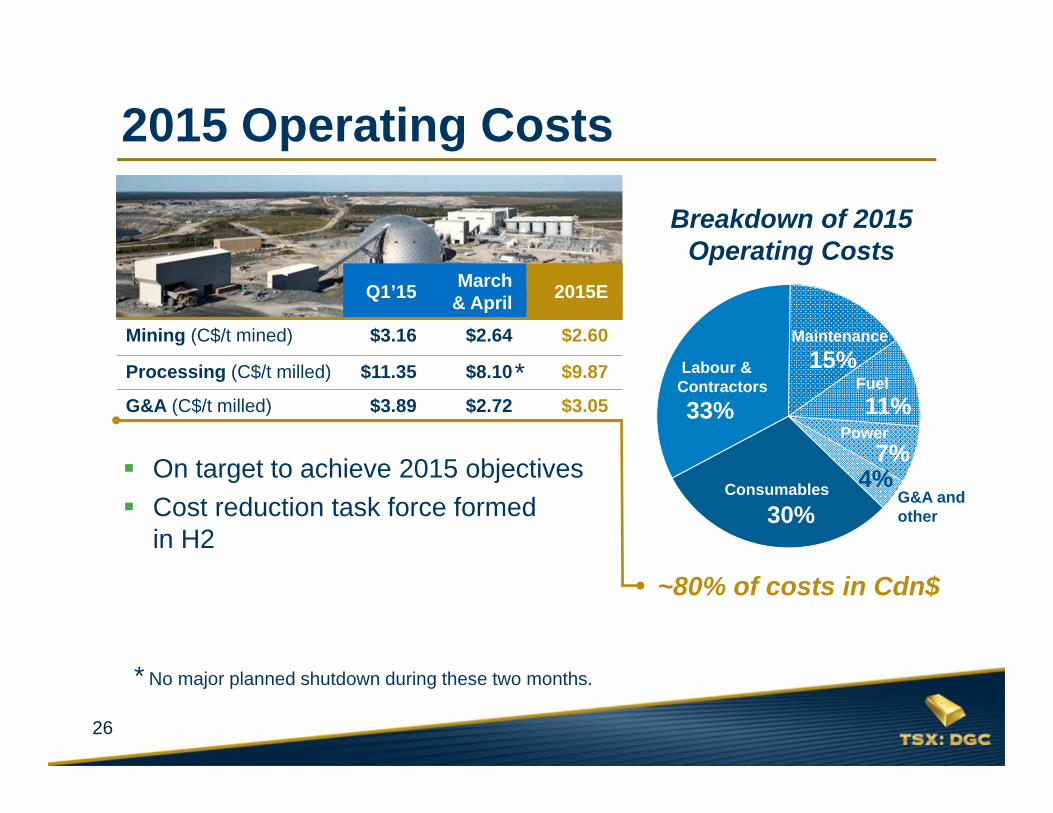

~80% of costs in Cdn$

2015 Operating Costs

Maintenance

Labour & Contractors

Power

Fuel

G&A and other

Consumables

30%

15%

33%

7%

11%

4% On target to achieve 2015 objectives Cost reduction task force formed

in H2

Breakdown of 2015 Operating Costs

Q1’15 March & April 2015E

Mining (C$/t mined) $3.16 $2.64 $2.60

Processing (C$/t milled) $11.35 $8.10 $9.87

G&A (C$/t milled) $3.89 $2.72 $3.05

* No major planned shutdown during these two months.

*

27

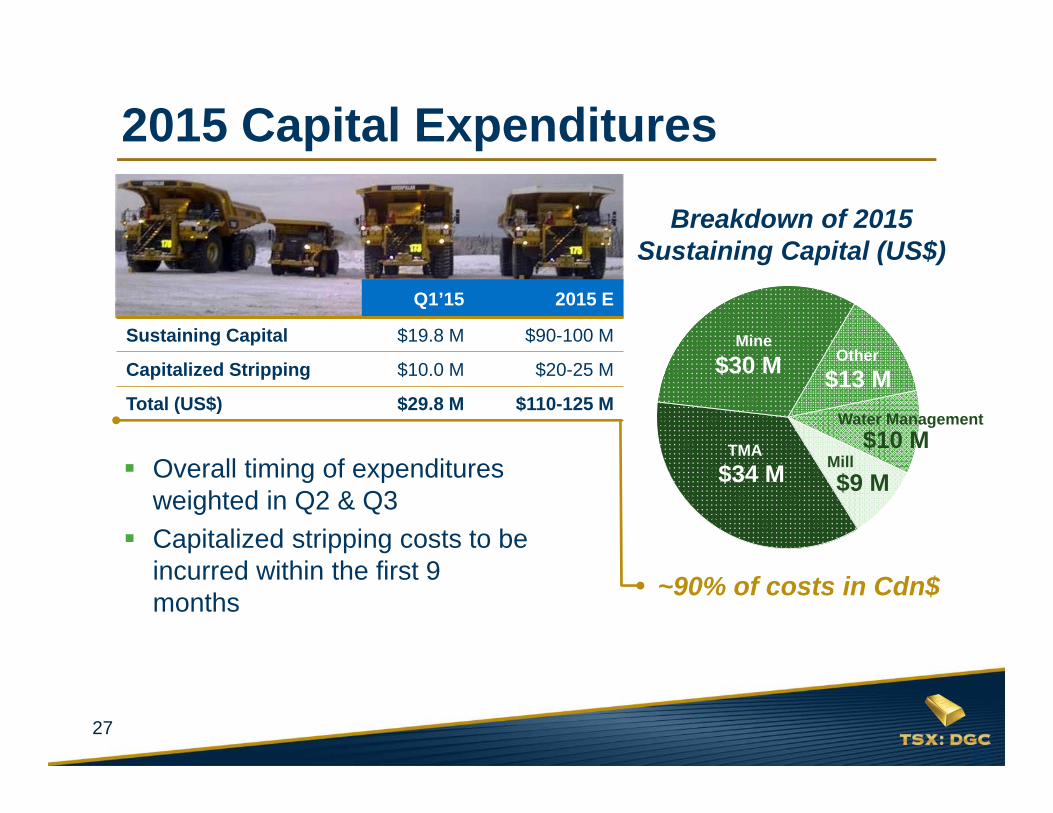

Overall timing of expenditures weighted in Q2 & Q3

Capitalized stripping costs to be incurred within the first 9 months

Mine$30 M

TMA$34 M

Other$13 M

Mill$9 M

Water Management$10 M

Breakdown of 2015 Sustaining Capital (US$)

~90% of costs in Cdn$

27

2015 Capital Expenditures

Q1’15 2015 E

Sustaining Capital $19.8 M $90-100 M

Capitalized Stripping $10.0 M $20-25 M

Total (US$) $29.8 M $110-125 M

28

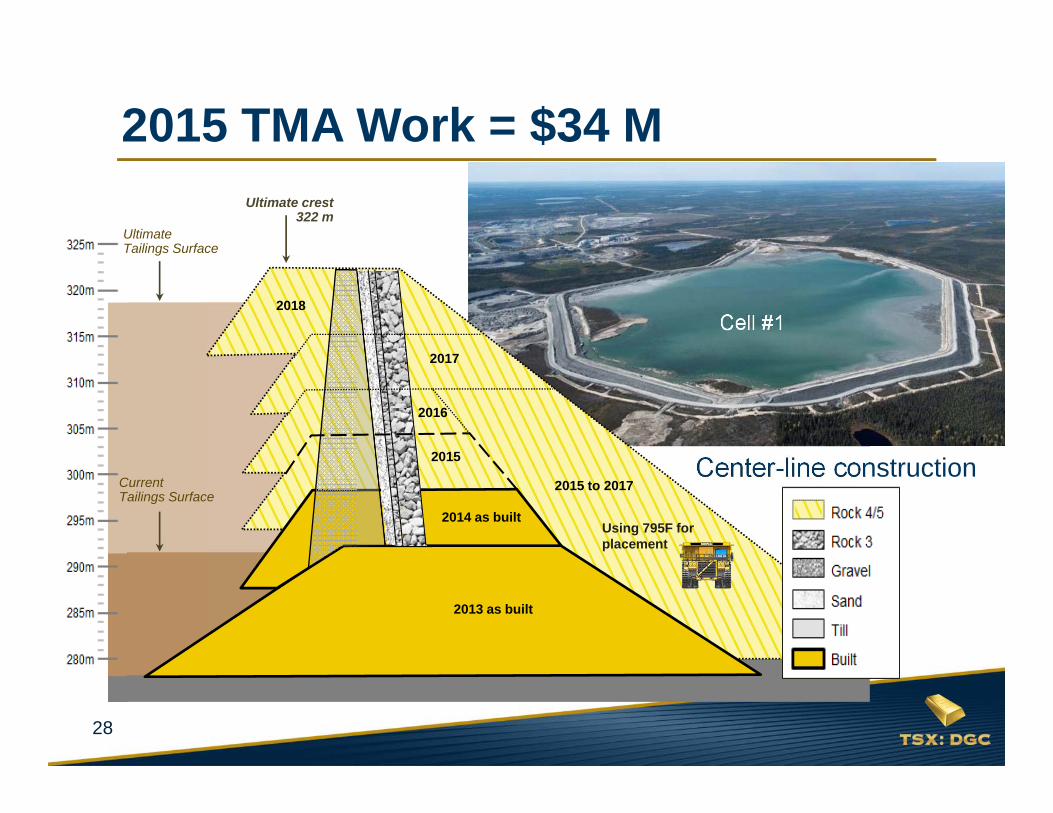

Cell #1

2015 TMA Work = $34 M

Center-line constructionCurrent Tailings Surface

Ultimate Tailings Surface

2014 as built

2013 as built

2016

2017

2015

2018

2015 to 2017

Ultimate crest322 m

Using 795F for placement

29

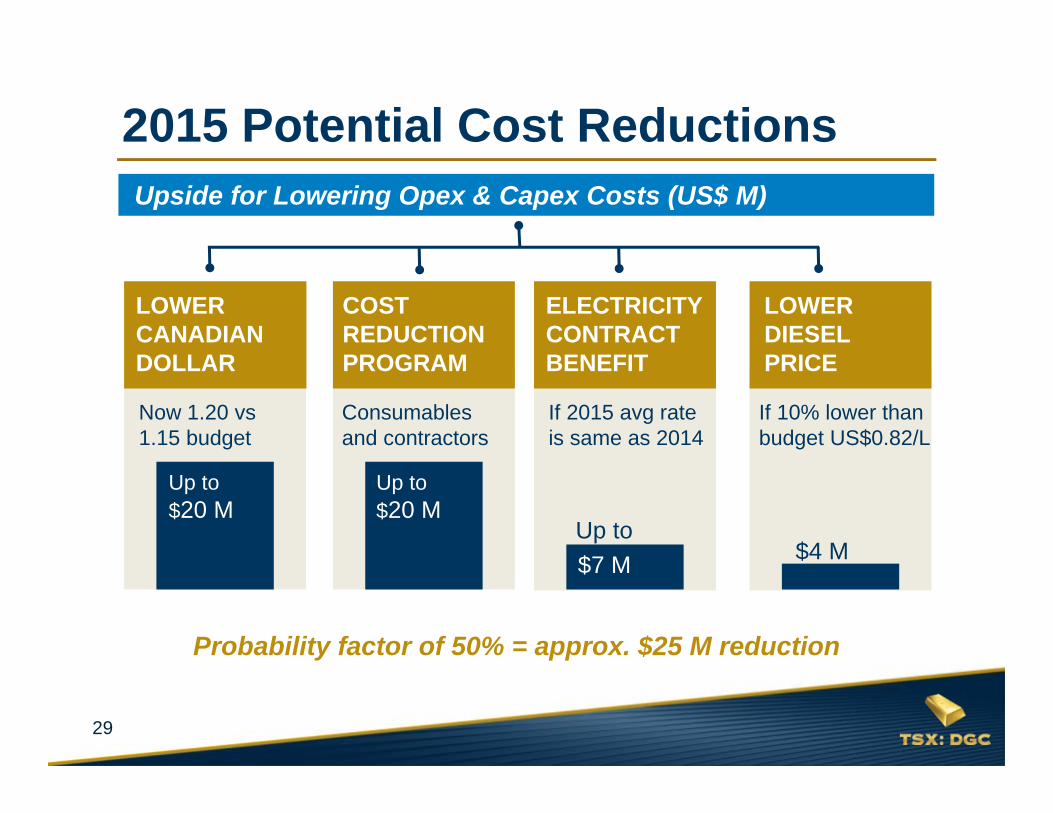

Upside for Lowering Opex & Capex Costs (US$ M)

Now 1.20 vs 1.15 budget

If 2015 avg rateis same as 2014

If 10% lower than budget US$0.82/L

Up to $20 M

LOWER CANADIAN DOLLAR

COST REDUCTION PROGRAM

ELECTRICITY CONTRACT BENEFIT

LOWER DIESEL PRICE

Consumables and contractors

$4 M

Probability factor of 50% = approx. $25 M reduction

$7 M

2015 Potential Cost Reductions

Up to $20 M

Up to

30

FINANCIAL REVIEWPaul Martin, President & CEO2015

31

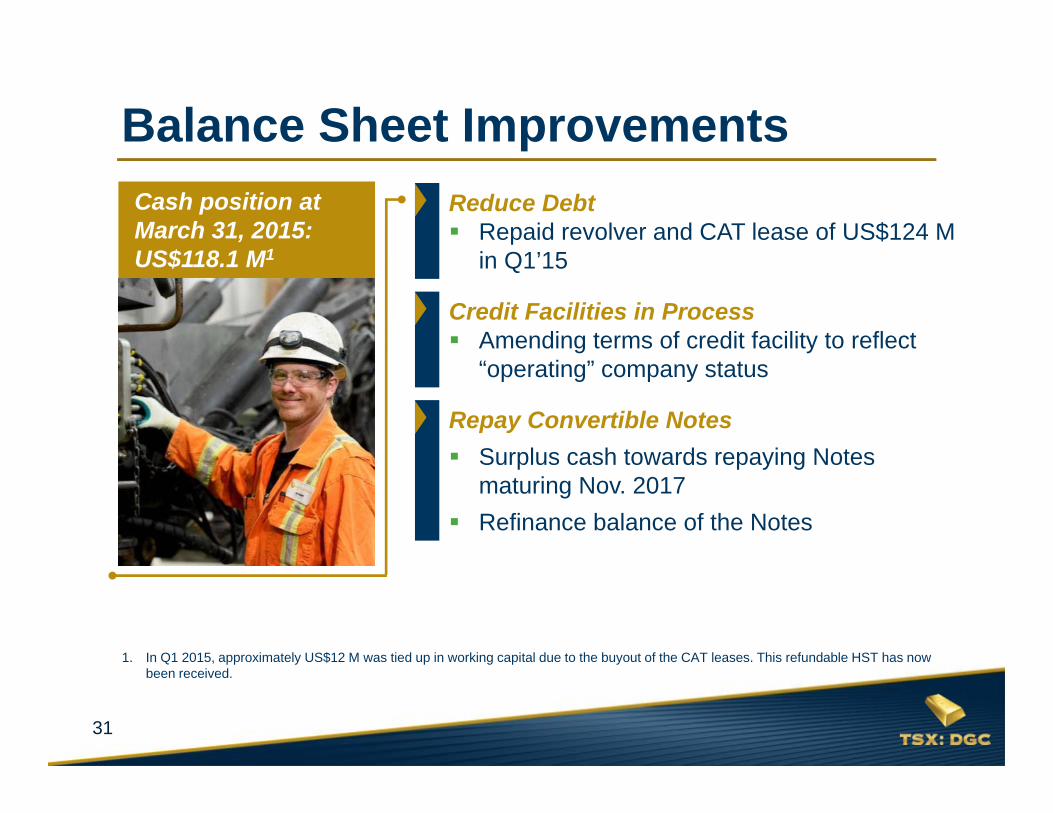

Cash position at March 31, 2015: US$118.1 M1

Balance Sheet ImprovementsReduce Debt Repaid revolver and CAT lease of US$124 M

in Q1’15

Credit Facilities in Process Amending terms of credit facility to reflect

“operating” company status

Repay Convertible Notes Surplus cash towards repaying Notes

maturing Nov. 2017 Refinance balance of the Notes

1. In Q1 2015, approximately US$12 M was tied up in working capital due to the buyout of the CAT leases. This refundable HST has now been received.

32

Credit Facility of US$50-70 M Amend prior facility to eliminate Completion Test and improve

covenant structure Good banking relationships with 5 banks (BMO, CIBC, CBA,

RBC, and TD) Finalize by mid-2015Equipment Lease Facility Re-establish a US$50 M equipment lease facility

Available Credit Facilities in Place

33

Convertible Notes (US$500 M, unsecured) Maturity November 2017 Target to repay a minimum of US$200 M from cash flow Management comfortable with long-term debt of US$300 M

› Based on US$1,200/oz and typical debt/EBITDA ratios Re-finance options:

1. Larger secured bank facility2. High yield note3. Convertible note

Repay Convertible Notes

or a blend of these options

1.2.3.

34

Prudent Financial ManagementHedge up to 50% of 2015 Gold ProductionForward sales on 85,000 oz @ US$1,255/oz

Currency Exchange ContractsZero-cost collars for US$90 M with a ceiling of 1.20; Forward contracts for US$50 M at average 1.26

Hedge ~50% of Q2-Q3 Diesel UsePurchasing diesel product (~12 M litres) at effective hedge price of C$0.80/litre

As at March 31, 2015

35

OPPORTUNITIESPierre Beaudoin, COONEAR-TERM

36

Realizing on Near-Term Opportunities LOM Plan Update in Q45 options being reviewed that include Block A

Assessing Ultimate Plant Capacity* Improve 410-conveyor availability short-

term Modify 410-conveyor long-term Increase productivity of secondary and

pebble crushers

Low-grade Stockpiles (not in reserves)Second test in H2: 4,000 tpd of enriched material to be processed

Increase Exploration ActivitiesStart 30,000 metre drilling program at Lower Detour this summer

* Refer to list on slide 24.

37

Pit shells based on US$1,000/oz Maximize returns for next 5-10 years and optimize NAV Optimize capital allocation of the mining fleet Add only valuable incremental ounces Mining rates and pit sequences will establish plant feed grades

Block A included in scenario development for LOM plan

LOM Plan UpdateTechnical Report to be Issued With 2016 Guidance

38

Key evaluations focusing on: Evaluate production ranging from 105 to 140 Mt annually

(equivalent to mining rates of 288,000 to 385,000 tpd) Mining rates and timing of ongoing production increases year to

year:1. No new shovels2. Incremental shovel(s):

CAT6030 and/or CAT6060

Timing of Block A (at earliest 2018) TMA options and potential co-disposal in Block A pit

LOM Plan UpdateEvaluating 5 Scenarios

Options being considered

1.2.

39

Exploration Focus: Lower Detour Q1 Drilling Program5,700 m completed at Lower Detour: extended high-grade mineralization of Zone 58N

Q2-Q3 Drilling Program30,000 m additional drilling: 50-metre infill totaling 50 holes to assess UG potential(budget of US$5 M)

Regional PotentialTarget identification following airborne magnetics and IP ground surveys

40

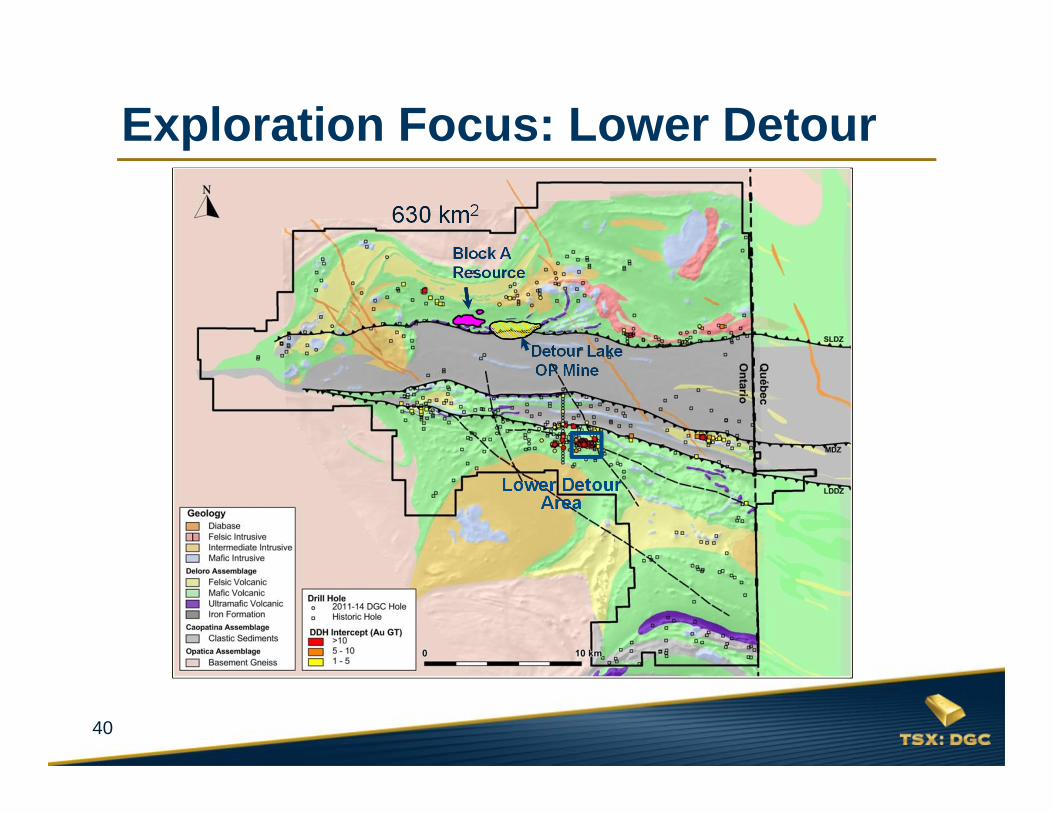

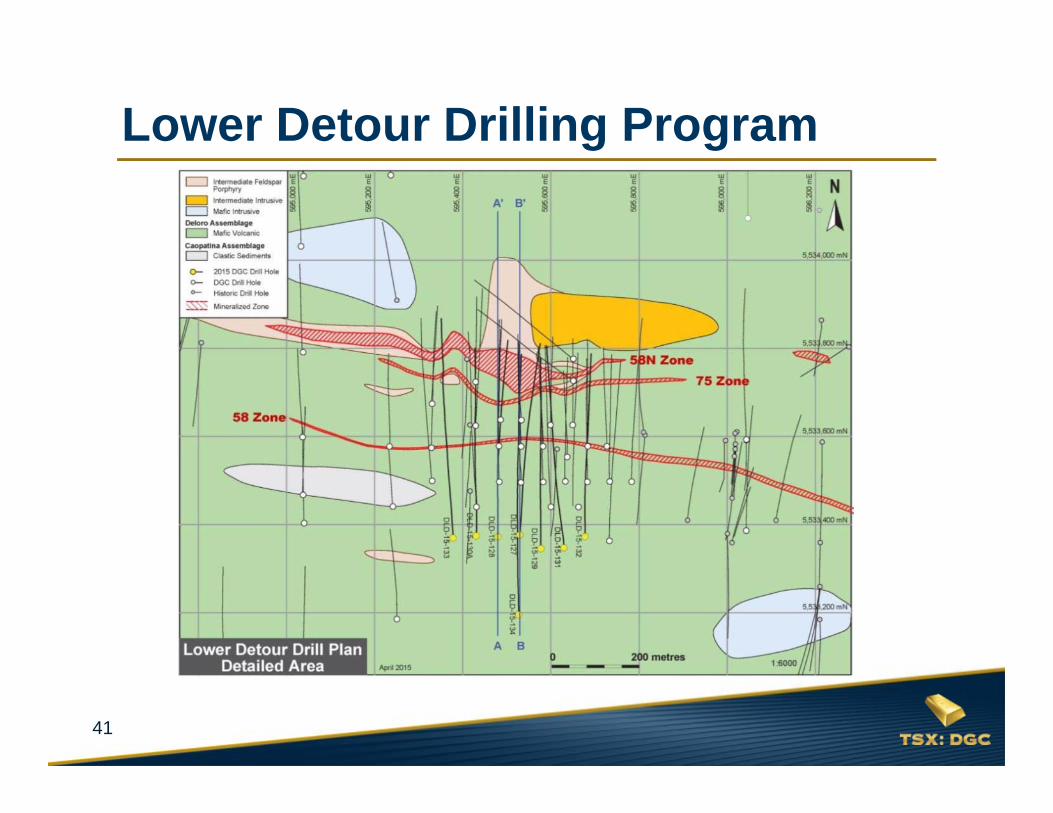

Lower Detour Area

630 km2

Exploration Focus: Lower Detour

Block A Resource

Detour LakeOP Mine

41

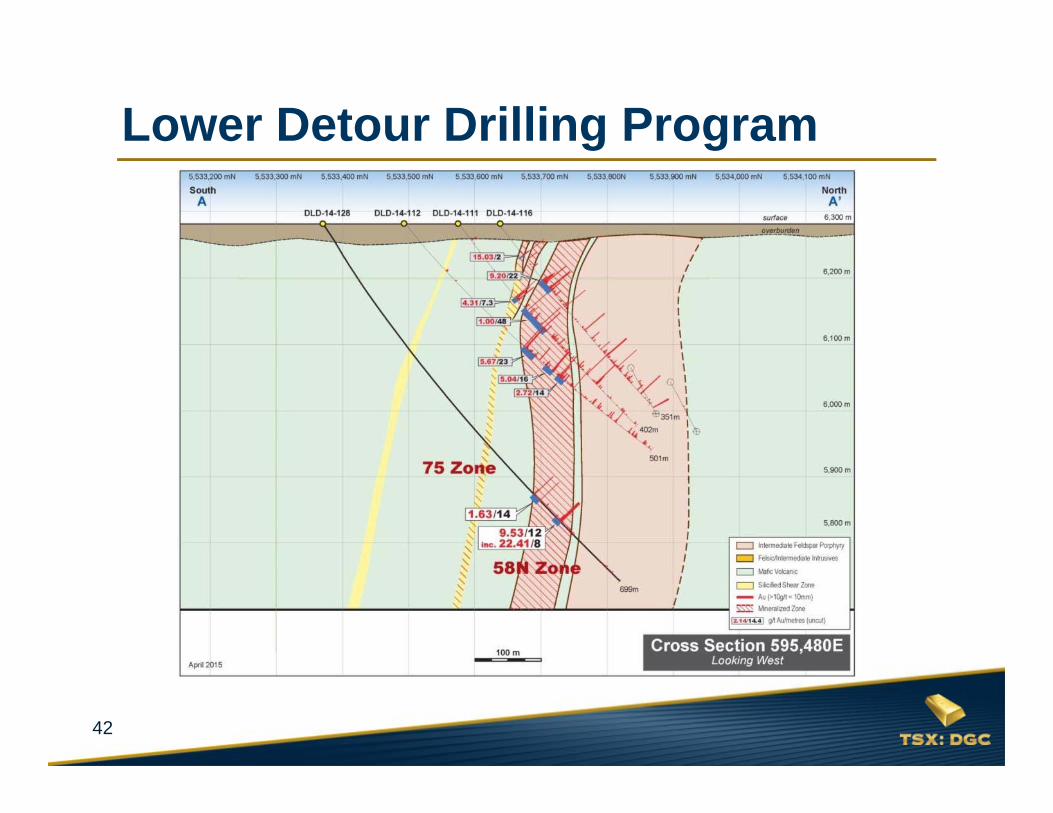

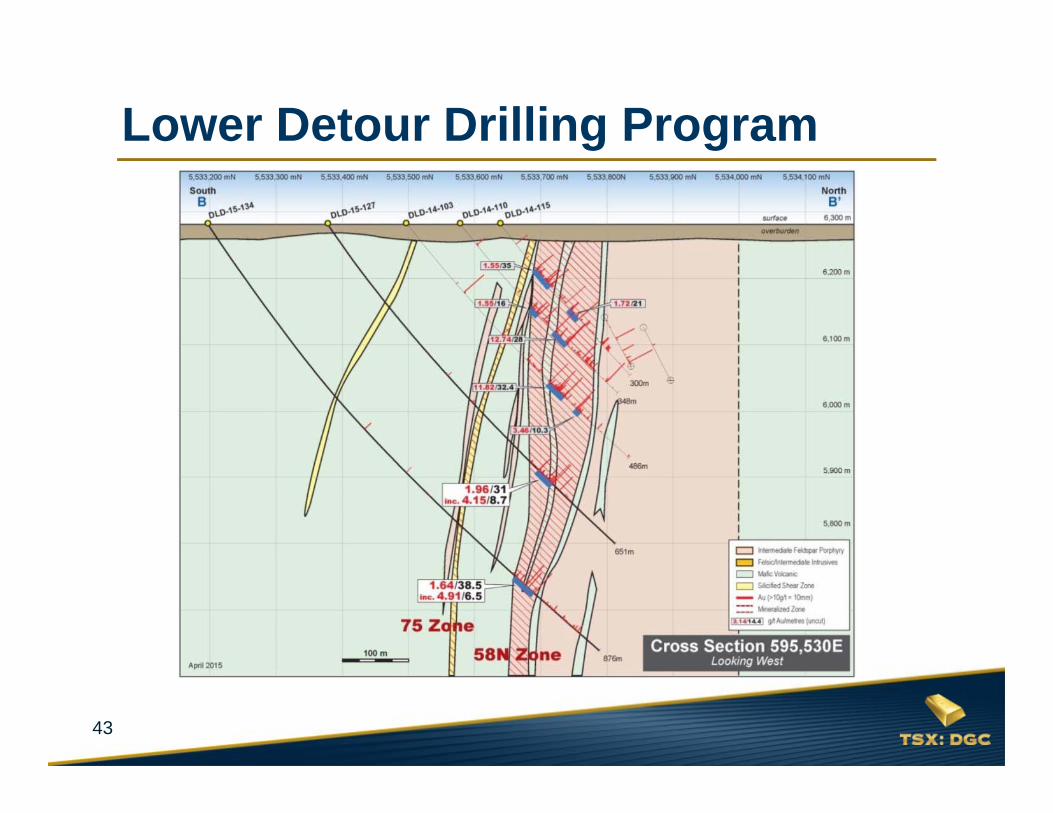

Lower Detour Drilling Program

42

Lower Detour Drilling Program

43

Lower Detour Drilling Program

44

PRODUCTION GROWTH / DECLINING UNIT COSTS

REALIZE VALUE-ENHANCINGOPPORTUNITIES

MATERIAL INPUTS TRENDINGFAVOURABLY

GROWING CASH FLOW

A GREAT TIME TO BE A GOLD PRODUCER!

45

ADDITIONALinformation Operations Team Block Model Reconciliation Detour Gold Reserves &

Resources Detour Lake & Block A Q1 2015 Operational Statistics Q1 2015 Financial Results Contact Information

46

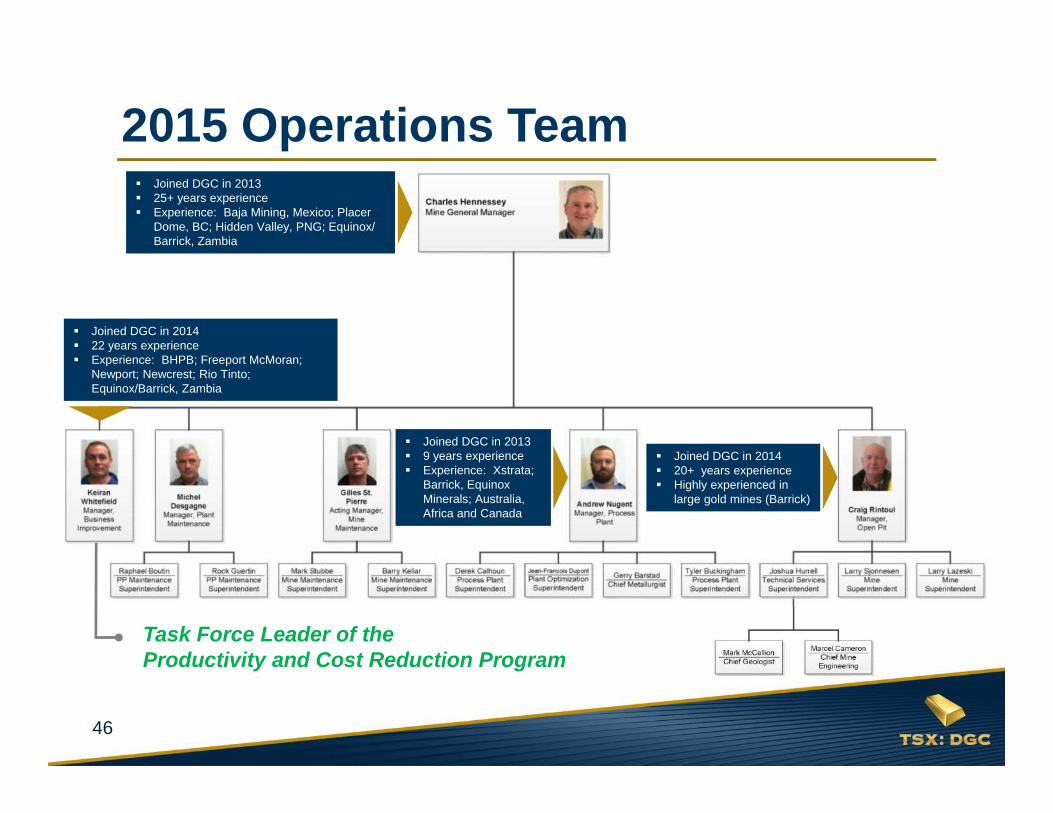

2015 Operations Team Joined DGC in 2013 25+ years experience Experience: Baja Mining, Mexico; Placer

Dome, BC; Hidden Valley, PNG; Equinox/ Barrick, Zambia

Joined DGC in 2013 9 years experience Experience: Xstrata;

Barrick, Equinox Minerals; Australia, Africa and Canada

Joined DGC in 2014 20+ years experience Highly experienced in

large gold mines (Barrick)

Joined DGC in 2014 22 years experience Experience: BHPB; Freeport McMoran;

Newport; Newcrest; Rio Tinto; Equinox/Barrick, Zambia

Task Force Leader of theProductivity and Cost Reduction Program

47

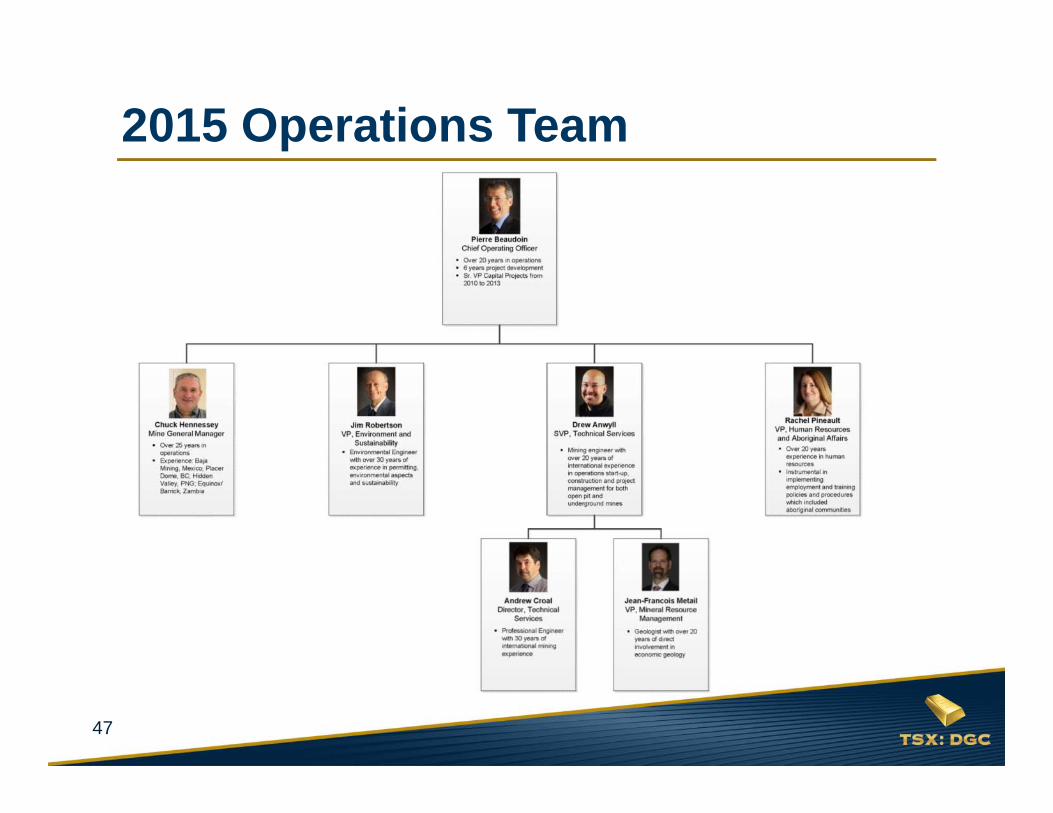

2015 Operations Team

48

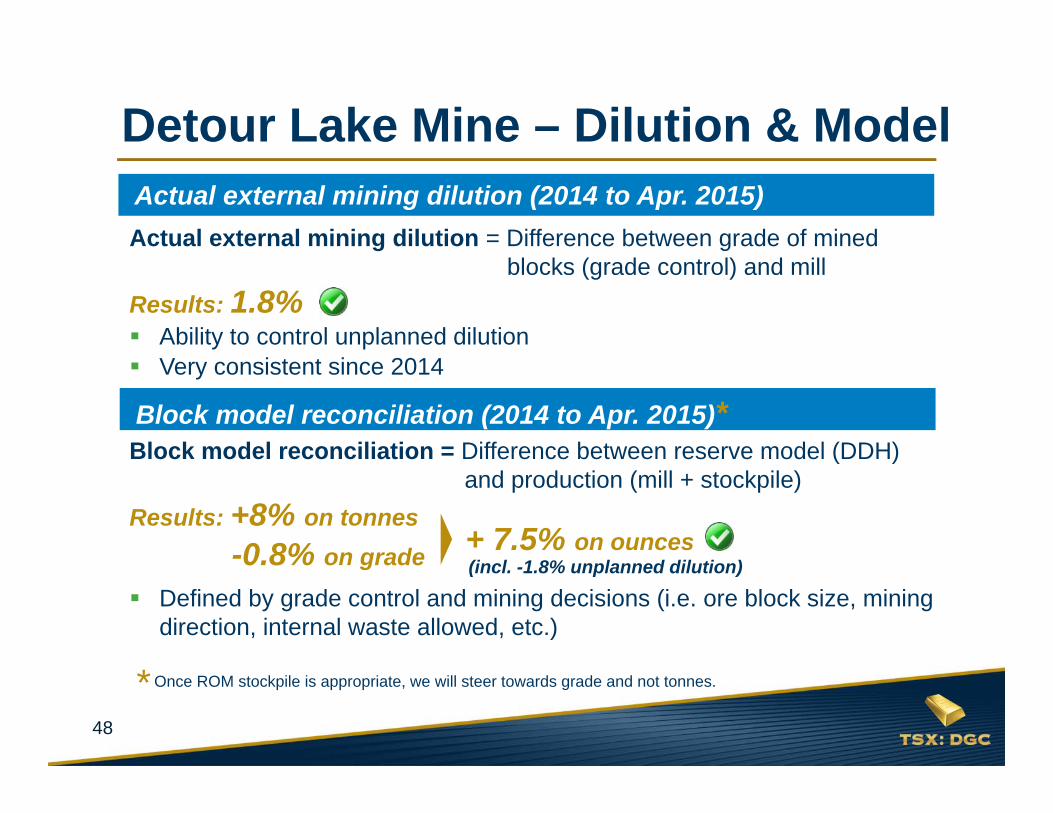

Detour Lake Mine – Dilution & Model

Actual external mining dilution = Difference between grade of mined blocks (grade control) and mill

Results: 1.8% Ability to control unplanned dilution Very consistent since 2014

Actual external mining dilution (2014 to Apr. 2015)

Block model reconciliation (2014 to Apr. 2015)*Block model reconciliation = Difference between reserve model (DDH)

and production (mill + stockpile)Results: +8% on tonnes

-0.8% on grade Defined by grade control and mining decisions (i.e. ore block size, mining

direction, internal waste allowed, etc.)

+ 7.5% on ounces(incl. -1.8% unplanned dilution)

*Once ROM stockpile is appropriate, we will steer towards grade and not tonnes.

49

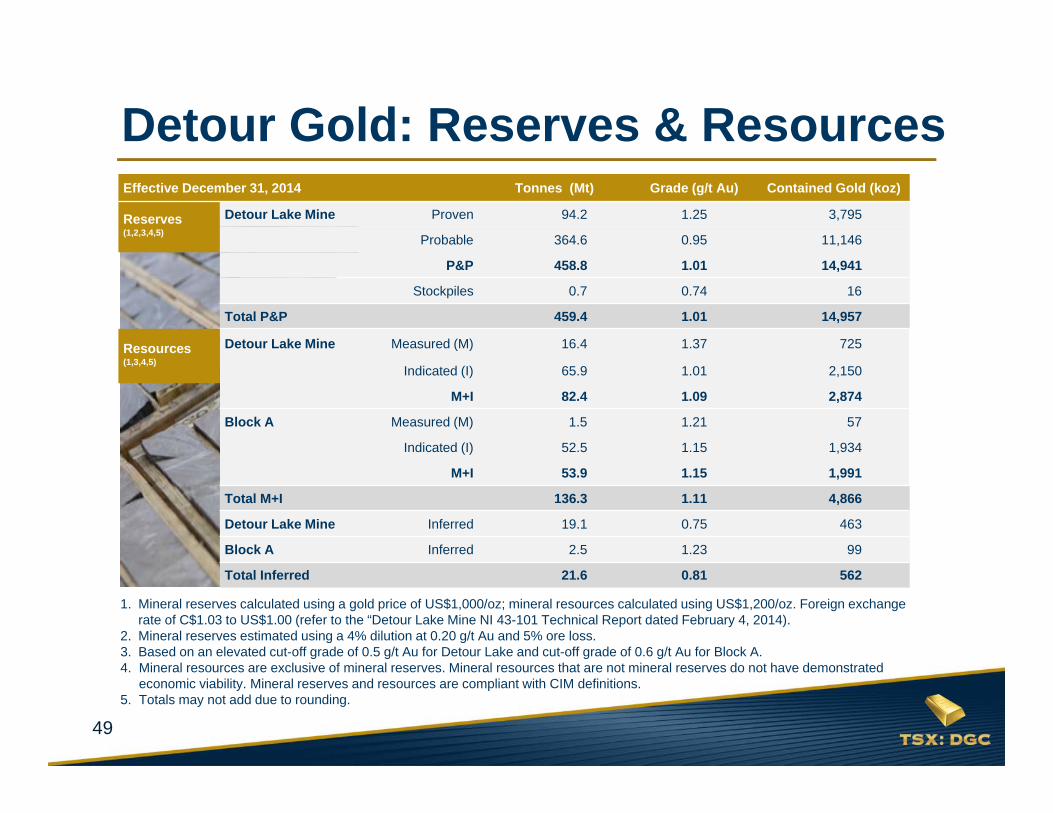

Effective December 31, 2014 Tonnes (Mt) Grade (g/t Au) Contained Gold (koz)

Reserves(1,2,3,4,5)

Detour Lake Mine Proven 94.2 1.25 3,795

Probable 364.6 0.95 11,146

P&P 458.8 1.01 14,941

Stockpiles 0.7 0.74 16

Total P&P 459.4 1.01 14,957

Resources (1,3,4,5)

Detour Lake Mine Measured (M) 16.4 1.37 725

Indicated (I) 65.9 1.01 2,150

M+I 82.4 1.09 2,874

Block A Measured (M) 1.5 1.21 57

Indicated (I) 52.5 1.15 1,934

M+I 53.9 1.15 1,991

Total M+I 136.3 1.11 4,866

Detour Lake Mine Inferred 19.1 0.75 463

Block A Inferred 2.5 1.23 99

Total Inferred 21.6 0.81 562

Detour Gold: Reserves & Resources

1. Mineral reserves calculated using a gold price of US$1,000/oz; mineral resources calculated using US$1,200/oz. Foreign exchange rate of C$1.03 to US$1.00 (refer to the “Detour Lake Mine NI 43-101 Technical Report dated February 4, 2014).

2. Mineral reserves estimated using a 4% dilution at 0.20 g/t Au and 5% ore loss.3. Based on an elevated cut-off grade of 0.5 g/t Au for Detour Lake and cut-off grade of 0.6 g/t Au for Block A.4. Mineral resources are exclusive of mineral reserves. Mineral resources that are not mineral reserves do not have demonstrated

economic viability. Mineral reserves and resources are compliant with CIM definitions.5. Totals may not add due to rounding.

50

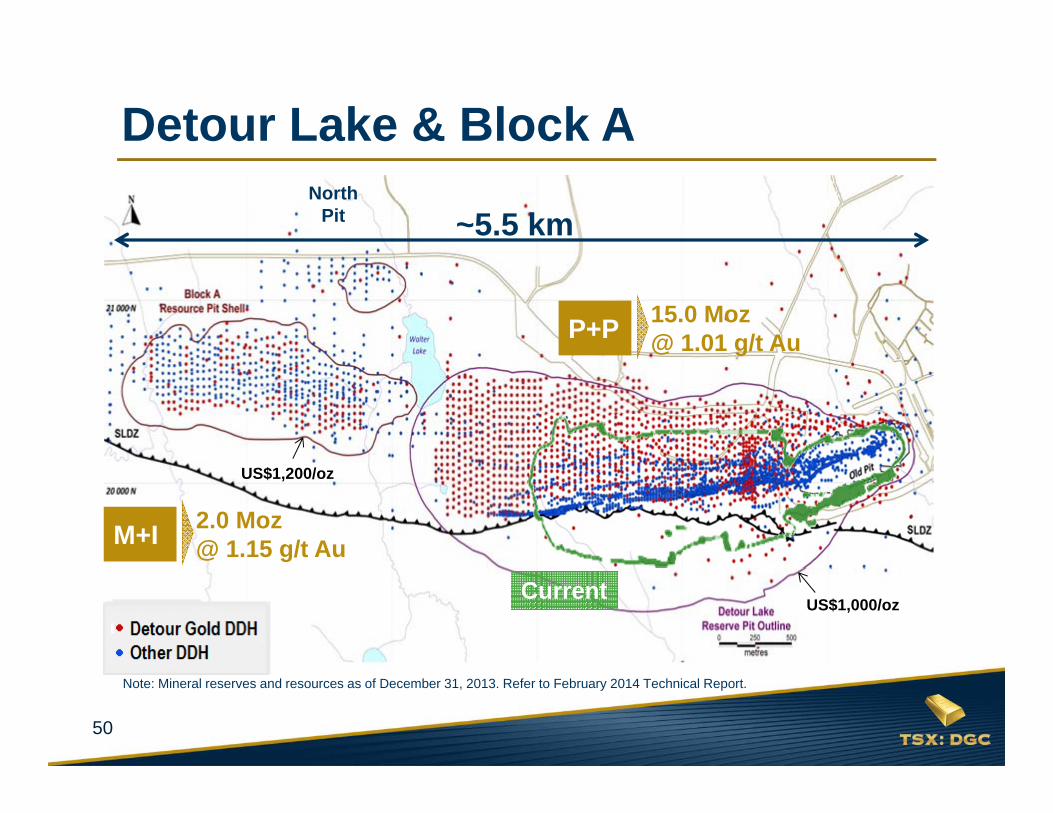

Detour Lake & Block A

US$1,000/oz

US$1,200/oz

15.0 Moz@ 1.01 g/t AuP+P

2.0 Moz@ 1.15 g/t AuM+I

~5.5 km

Current

North Pit

Note: Mineral reserves and resources as of December 31, 2013. Refer to February 2014 Technical Report.

51

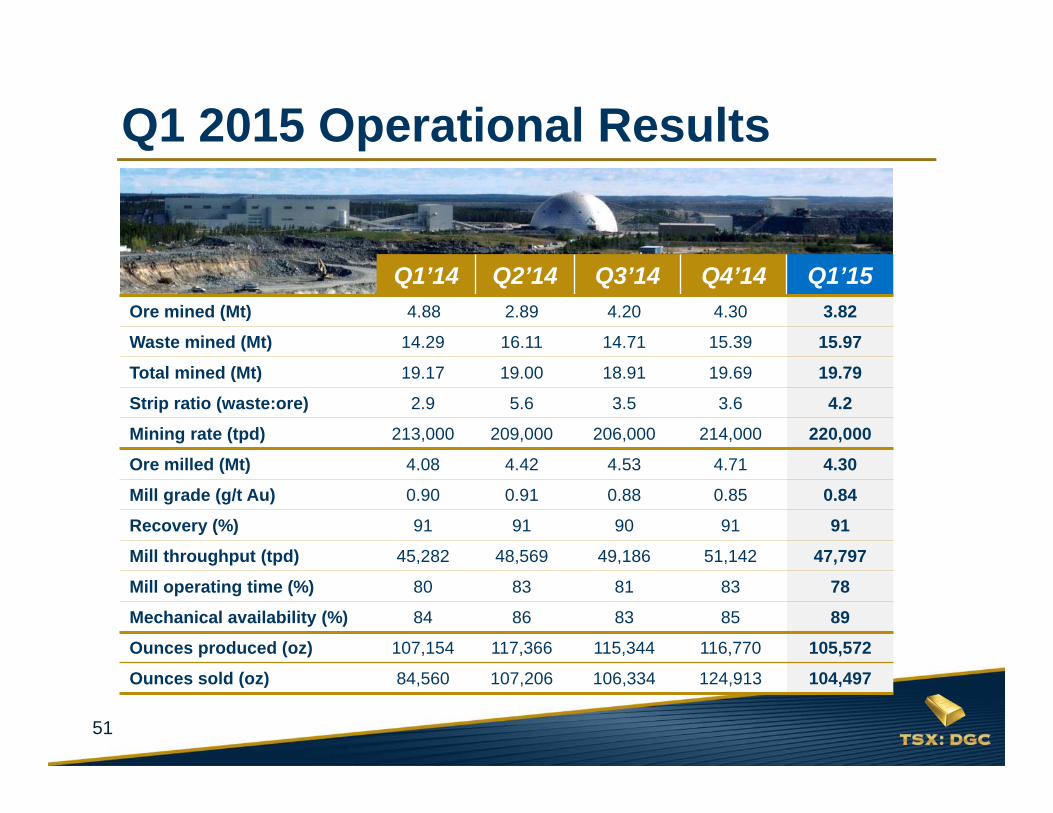

Q1 2015 Operational Results

Q1’14 Q2’14 Q3’14 Q4’14 Q1’15Ore mined (Mt) 4.88 2.89 4.20 4.30 3.82

Waste mined (Mt) 14.29 16.11 14.71 15.39 15.97

Total mined (Mt) 19.17 19.00 18.91 19.69 19.79

Strip ratio (waste:ore) 2.9 5.6 3.5 3.6 4.2

Mining rate (tpd) 213,000 209,000 206,000 214,000 220,000

Ore milled (Mt) 4.08 4.42 4.53 4.71 4.30

Mill grade (g/t Au) 0.90 0.91 0.88 0.85 0.84

Recovery (%) 91 91 90 91 91

Mill throughput (tpd) 45,282 48,569 49,186 51,142 47,797

Mill operating time (%) 80 83 81 83 78

Mechanical availability (%) 84 86 83 85 89

Ounces produced (oz) 107,154 117,366 115,344 116,770 105,572

Ounces sold (oz) 84,560 107,206 106,334 124,913 104,497

52

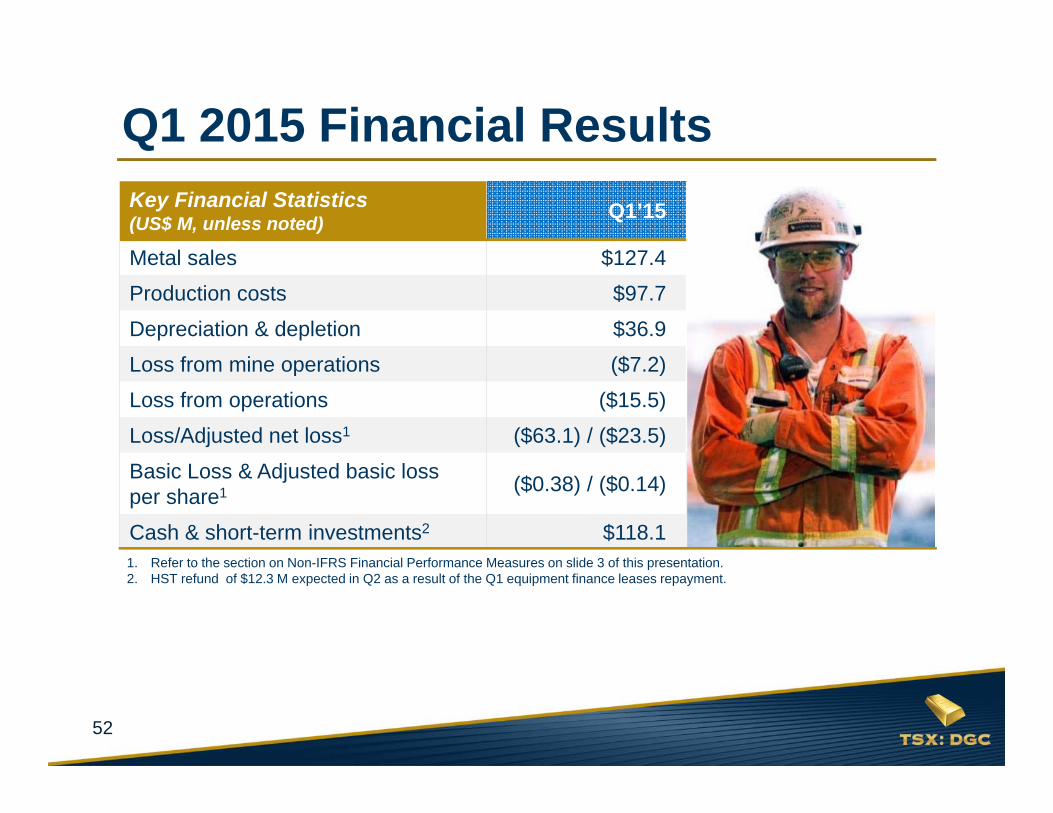

Q1 2015 Financial ResultsKey Financial Statistics (US$ M, unless noted) Q1’15

Metal sales $127.4

Production costs $97.7

Depreciation & depletion $36.9

Loss from mine operations ($7.2)

Loss from operations ($15.5)

Loss/Adjusted net loss1 ($63.1) / ($23.5)

Basic Loss & Adjusted basic loss per share1 ($0.38) / ($0.14)

Cash & short-term investments2 $118.11. Refer to the section on Non-IFRS Financial Performance Measures on slide 3 of this presentation.2. HST refund of $12.3 M expected in Q2 as a result of the Q1 equipment finance leases repayment.

53

Laurie GaboritDirector Investor RelationsEmail: [email protected]: 416.304.0581

Paul MartinPresident and Chief Executive OfficerEmail: [email protected]: 416.304.0800

www.detourgold.com

Contact Information

Pierre BeaudoinChief Operating OfficerEmail: [email protected]: 416.304.0800