Embed Size (px)

Citation preview

International Journal of Logistics Management, Vol. 13, No. 1, 2002 1

Developing Market Specific Supply Chain Strategies

Martin Christopher, Cranfield School of Management, Cranfield University,Bedford, MK43 0AL

Denis R. Towill, Cardiff Business School, Cardiff University, Colum Drive,Cardiff, CF10 3EU

This paper examines the issues underlying the appropriate matching of pipelines to

marketplace needs under conditions of demand volatility and price pressure. It

describes a scenario where the philosophy of “one size fits all” does not apply to

pipeline design, implementation, and control. The paper reports on research

conducted by the authors and others on how appropriate global supply chain strategies

can be developed contingent upon market characteristics and which seek

simultaneously to achieve higher levels of customer responsiveness at less total cost

to the supply chain as a whole. The selection of the right strategy within a supply

chain lends itself to a taxonomic approach. We find that three dimensions (leading to

eight possible configurations) are adequate for this purpose. These key dimensions

are product characteristics, demand characteristics and replenishment lead-time.

Over the last decade or so, there has emerged a view that recognises that the route to

competitive advantage lies through the supply chain. Indeed, it has been suggested

that “supply chains compete, not companies” (1). The idea being that the unique set

of relations that typify the web of inter-connections between organisations in a

network enable the achievement of competitive advantage through lower costs and/or

greater differentiation.

Because of the complexity of todays supply chains, due in part to out-sourcing and

globalisation, the way in which these relationships are structured and managed can

make the difference between profit and loss.

As McCullen and Towill (2) have shown, globalisation of supply chains compounds

the logistical problem along three dimensions. These are replenishment level; time;

and distance. Hence a marketplace ripple can be amplified and distorted as it passes

International Journal of Logistics Management, Vol. 13, No. 1, 2002 2

from, say, the UK to Indonesia. Furthermore, there may well be a significant delay

before any response occurs at (say) the raw material supplier. Additionally, customer

choice and the nature of the product means that in pipeline terms “one size does not fit

all” (3, 4). Hence matching the pipeline to the product is a key issue in the

engineering of global supply chains.

Many marketplaces are now highly volatile and demand is difficult to predict. The

acceleration of technological and fashion changes has additionally resulted in

extremely short product life cycles. In this new environment non-availability means

that in the event of non-supply the particular sales opportunity is lost forever (5).

Consequently the focus in supply chain management must shift from the idea of cost

as the order winner to responsiveness as the market winner. The implication is that

the emphasis in supply chain management in the future must be on agility.

Agility implies the ability of the supply chain to react quickly to changes in market

demand – be they changes in volume, variety or mix. The characteristics of the agile

supply chain have been described elsewhere (6), but it is useful to contrast agility with

the philosophy of lean operations. Lean thinking is most often associated with the car

assembly industry and Japan in particular. Agility & leanness are not opposing

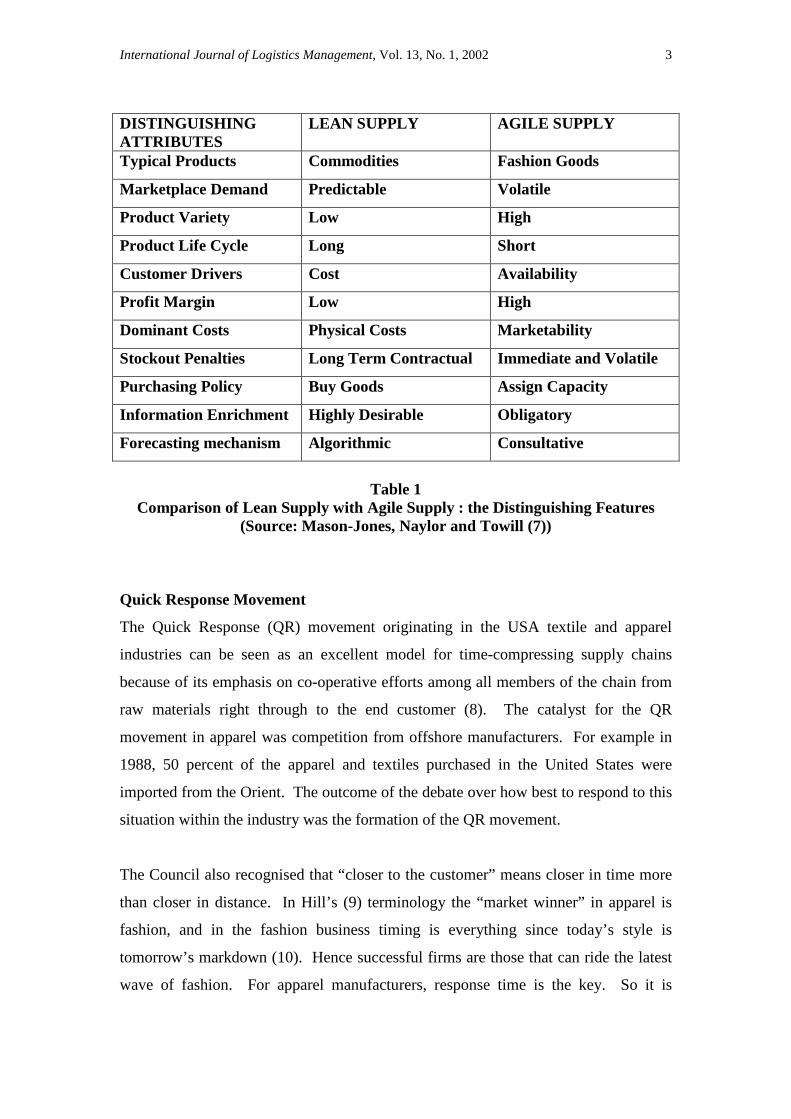

philosophies, rather they work best in certain contexts as Table 1 suggests.

International Journal of Logistics Management, Vol. 13, No. 1, 2002 3

DISTINGUISHINGATTRIBUTES

LEAN SUPPLY AGILE SUPPLY

Typical Products Commodities Fashion Goods

Marketplace Demand Predictable Volatile

Product Variety Low High

Product Life Cycle Long Short

Customer Drivers Cost Availability

Profit Margin Low High

Dominant Costs Physical Costs Marketability

Stockout Penalties Long Term Contractual Immediate and Volatile

Purchasing Policy Buy Goods Assign Capacity

Information Enrichment Highly Desirable Obligatory

Forecasting mechanism Algorithmic Consultative

Table 1Comparison of Lean Supply with Agile Supply : the Distinguishing Features

(Source: Mason-Jones, Naylor and Towill (7))

Quick Response Movement

The Quick Response (QR) movement originating in the USA textile and apparel

industries can be seen as an excellent model for time-compressing supply chains

because of its emphasis on co-operative efforts among all members of the chain from

raw materials right through to the end customer (8). The catalyst for the QR

movement in apparel was competition from offshore manufacturers. For example in

1988, 50 percent of the apparel and textiles purchased in the United States were

imported from the Orient. The outcome of the debate over how best to respond to this

situation within the industry was the formation of the QR movement.

The Council also recognised that “closer to the customer” means closer in time more

than closer in distance. In Hill’s (9) terminology the “market winner” in apparel is

fashion, and in the fashion business timing is everything since today’s style is

tomorrow’s markdown (10). Hence successful firms are those that can ride the latest

wave of fashion. For apparel manufacturers, response time is the key. So it is

International Journal of Logistics Management, Vol. 13, No. 1, 2002 4

essential to judge quickly what is selling and move it through the pipeline and onto

the racks before competitors (11).

Quick response provides a remedy to this problem by compressing the total pipeline,

thus eliminating some of those efficiency losses by moving manufacturing closer to

the consumer’s buying decision. Long pipelines also means that forecast horizons are

extended with the inevitable impact on forecast errors. As a rule of thumb the

forecast errors are as follows:

Start of Season ± 10%

Minus 16 weeks ± 20%

Minus 26 weeks ± 40%

QR has been defined at length by Lowson et al (12) as:

“A state of responsiveness and flexibility in which an organisation seeks to provide a

highly diverse range of products and services to a customer/consumer in the exact

quantity, variety and quality, and at the right time, place and price as dictated by real-

time customer/consumer demand. QR provides the ability to make demand

information driven decisions at the last possible moment in time ensuring that

diversity of offering is maximised and lead-times, expenditure, cost and inventory

minimised. QR places an emphasis upon flexibility and product velocity in order to

meet the changing requirements of a highly competitive, volatile and dynamic

marketplace. QR encompasses a strategy, structure, culture and set of operational

procedures aimed at integrating enterprises in a mutual network through rapid

information transfer and profitable exchange of activity.”

The significant conceptual breakthrough made in the QR movement was identifying

and exploiting the fact that the supply chain is a system of bi-directional flows. So

goods flow forward from the textile producer to the customer and information about

consumer demand, orders, and capacity commitments flows backward to apparel and

textile manufacturers. In control systems terminology this is a system with both

information feedforward and feedback, the advantages of which have been ably

International Journal of Logistics Management, Vol. 13, No. 1, 2002 5

demonstrated by Wikner et al (13) and Mason-Jones and Towill (14). The innovative

feature of QR is that actions are taken to increase the velocity of flows in both

directions. The QR campaign involves re-engineering the pipeline to move apparel

forward faster; that is, to shrink cycle times at each stage of manufacture and the

shipment times between stages. However the important actions were those taken to

improve the responsiveness of the system through improved, faster communication of

consumer preferences to all members of the chain.

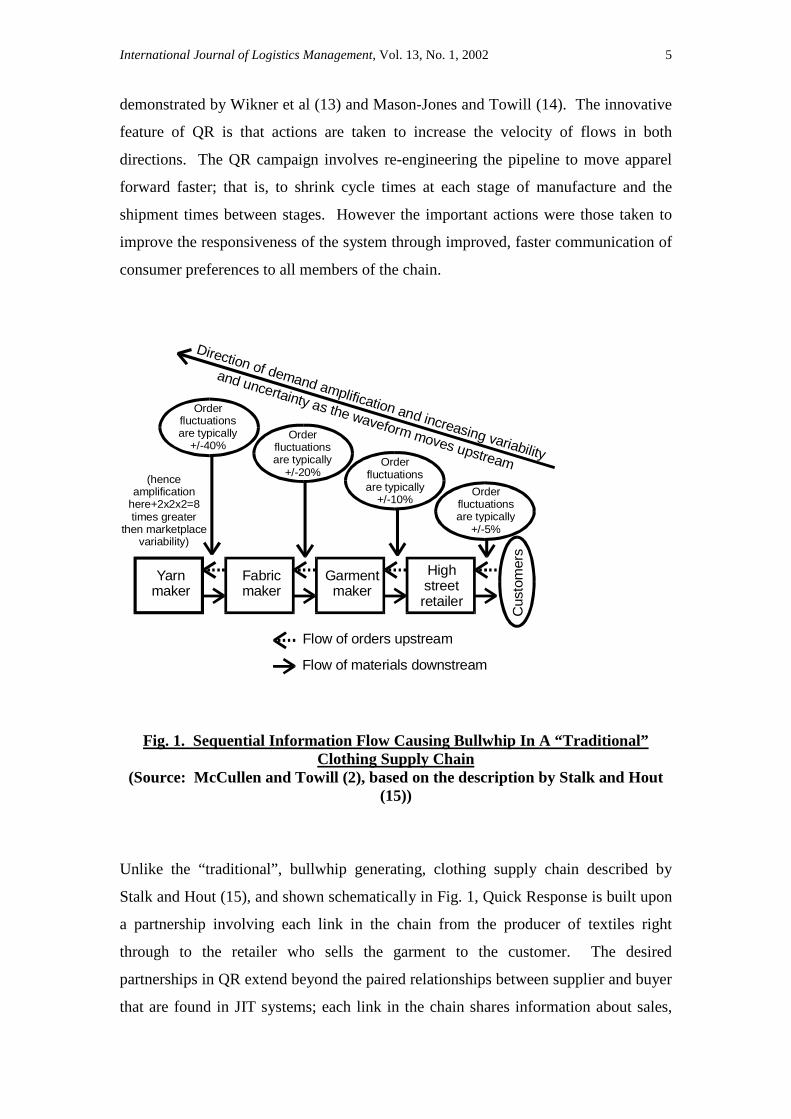

Fig. 1. Sequential Information Flow Causing Bullwhip In A “Traditional”Clothing Supply Chain

(Source: McCullen and Towill (2), based on the description by Stalk and Hout(15))

Unlike the “traditional”, bullwhip generating, clothing supply chain described by

Stalk and Hout (15), and shown schematically in Fig. 1, Quick Response is built upon

a partnership involving each link in the chain from the producer of textiles right

through to the retailer who sells the garment to the customer. The desired

partnerships in QR extend beyond the paired relationships between supplier and buyer

that are found in JIT systems; each link in the chain shares information about sales,

Fabricmaker

Yarnmaker

Garmentmaker

Highstreetretailer

Flow of orders upstream

Flow of materials downstream

Cus

tom

ers

Orderfluctuationsare typically

+/-5%

Orderfluctuationsare typically

+/-10%

Orderfluctuationsare typically

+/-20%

Orderfluctuationsare typically

+/-40%

(henceamplification

here+2x2x2=8times greater

then marketplacevariability)

Direction of demand amplification and increasing variability

and uncertainty as the waveform moves upstream

International Journal of Logistics Management, Vol. 13, No. 1, 2002 6

orders, and inventories with the others. Retailers communicate information about

sales, not only to the apparel manufacturer, but also back to the textile producer.

Mutual co-operation among all partners is required if the system is to succeed in its

goal of increasing sales with less inventory in the total system. A successful

partnership means higher inventory turns and improved return on investment for each

link in the chain.

A trend to off-shore sourcing

As we have previously noted, offshore sourcing and manufacturing has been an

increasing trend across much of Western industry for several decades. The

motivation for this tendency to offshore sourcing has been primarily cost. However,

it could be argued that the concept of cost that has been employed in those decisions

is narrow in the extreme because the cost criteria employed is essentially the unit cost

of manufacture or purchase. Costs such as those associated with today’s wider view

of the supply chain are often ignored. Thus rarely is a realistic charge placed upon the

additional inventory that inevitably will be created as pipelines lengthen, neither is a

cost placed upon the risk that this might generate in terms of obsolescence, equally

the impact on the firm’s agility is not factored into the equation.

Whole sectors of industry – particularly in electronics and clothing – have migrated to

the Far East as the search for lower labour cost intensifies. Strangely, even industries

where labour costs represent only a small part of total value-added such as semi-

conductor fabrication have been seduced by this general trend.

A study by Lowson (16) of fifty European Union retailers found that 70% of their

total purchases came from outside the EU at purchase prices up to 35% lower than

could be obtained locally. Companies such as Marks & Spencer who as recently as

1990 sourced almost 100% of their garments in the British Isles (UK and Republic of

Ireland) had reduced this by half by 2000. A shirt sourced in Indonesia could be

purchased by Marks & Spencer buyers for £2.69 compared to £6.01 in Northern

Ireland (17).

Lowson also highlighted the fact that the retailers in his study were typically working

on order to delivery lead-times of between 48 and 60 weeks when ordering from

International Journal of Logistics Management, Vol. 13, No. 1, 2002 7

Asian sources. This clearly inhibits their agility and has the potential to place

themselves at some risk if demand for those products does not come up to

expectations.

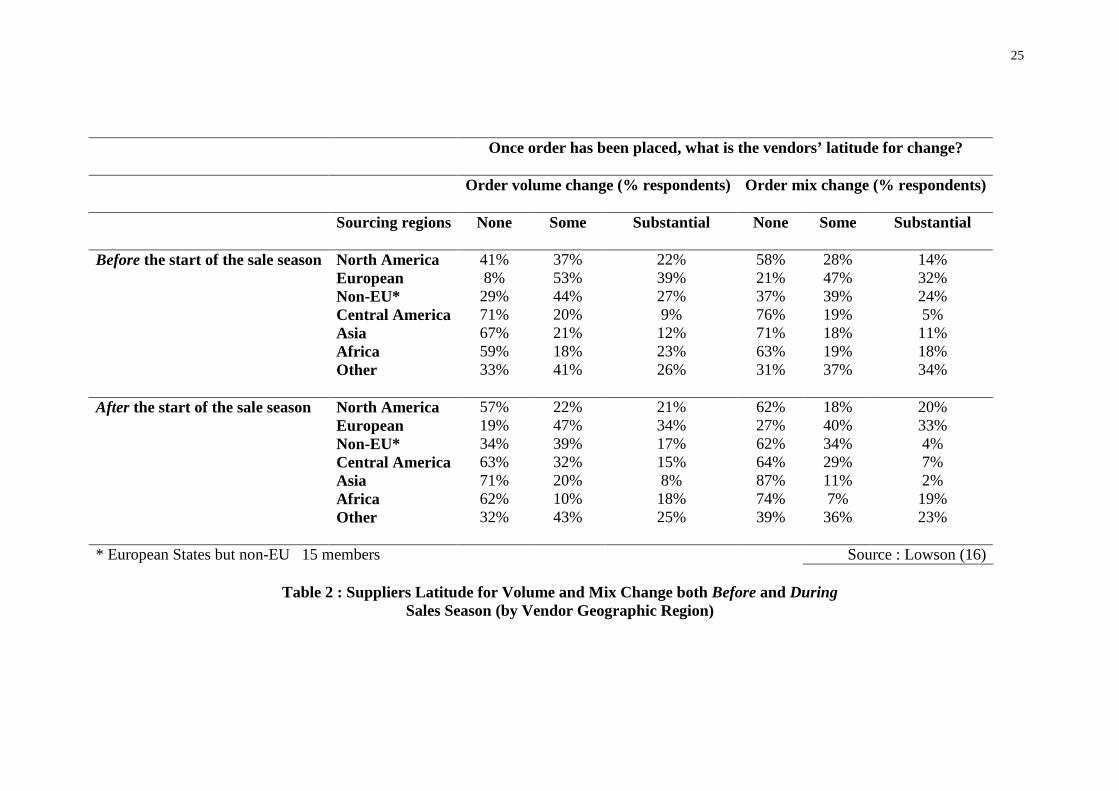

The same survey also examined the extent to which retailers’ flexibility was affected

by their choice of sourcing location. The findings are summarised in Table 2 below.

Take in table 2

To highlight the differences in flexibility and responsiveness by source location we

have applied a numerical weight to each column as follows:-

None x 0

Some x 1

Substantial x 3

The three resulting scores are then summed and divided by 300% (the maximum

possible score) to produce a metric highlighting volume and mix responsiveness

before and after the sales season commences. It seeks to provide a single aggregate

“score” which sheds insight into sourcing decisions, especially when coupled with

vendor lead times.

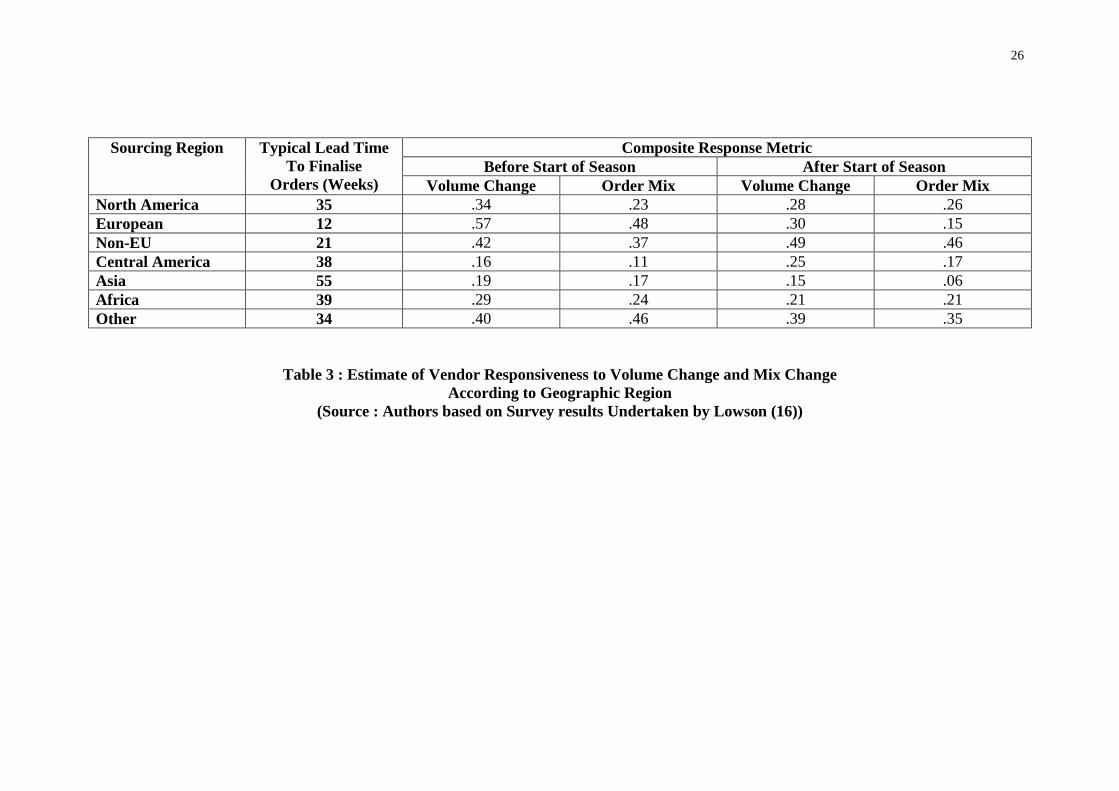

Table 3 shows the resulting scores along with the average lead-time that the

respondents associated with each sourcing location.

Take in table 3

These results suggest that the loss of flexibility that results from sourcing offshore can

be significant. The paradox is that these data are derived from retailers themselves

but dramatic though they may be, they seem not to influence the manufacturing cost-

based sourcing decisions. Whilst these findings result from a survey of retailers they

are not dissimilar to the experience of companies in industries such as electronics or

high technology generally.

International Journal of Logistics Management, Vol. 13, No. 1, 2002 8

What is called for is a wider definition of costs which is based upon total supply chain

costs. The limited definition of cost that is still the main driver in sourcing decisions

(i.e. unit manufacturing or purchase cost) is clearly inadequate and will not reflect the

true total costs of ownership. True supply chain costs need to incorporate such

elements as:-

Inventory carrying costs

cost of mark-downs

cost of loss sales

transaction costs (including letters of credit, customs clearance)

transportation (including emergency airfreight)

warehousing

duties

There will be many occasions where, even taking all the above costs into account, it

will still make sense to source in low-cost, offshore locations. For example, standard

products with limited variation in demand. However for other products where

demand is much more volatile and harder to predict, local sourcing may be preferable.

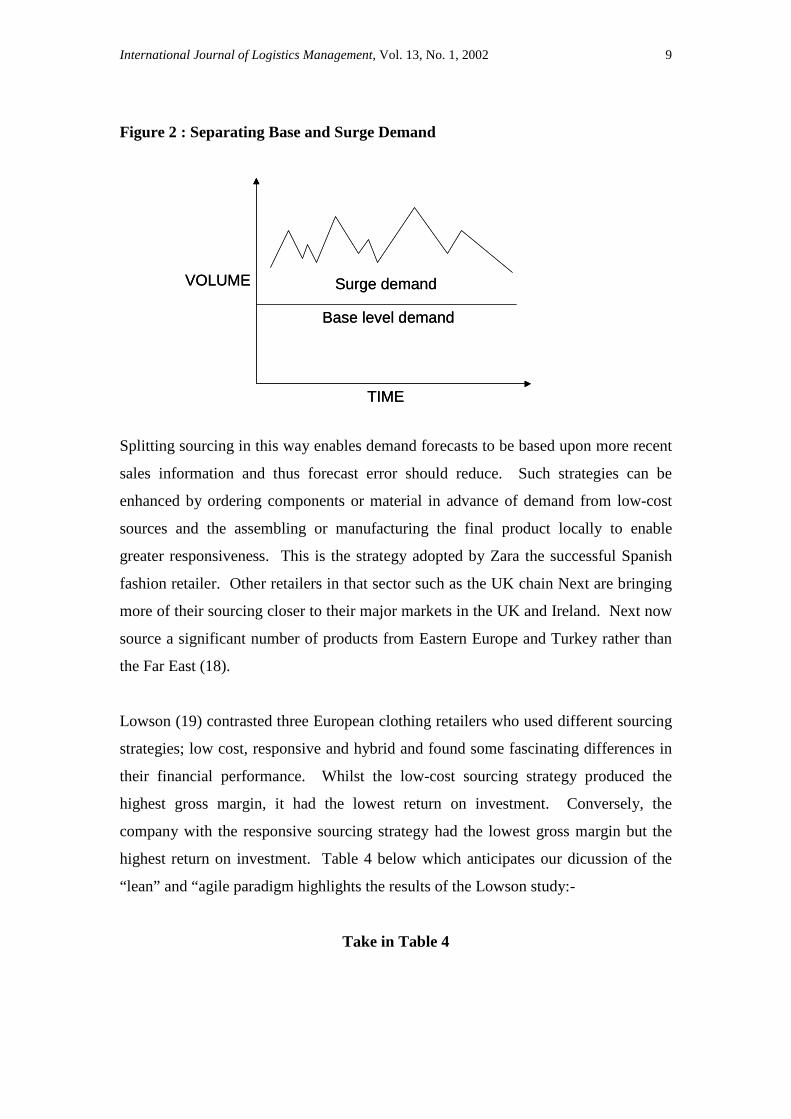

The Concept of Separating Baseline and Surge DemandsA further option exists for

a hybrid strategy where low-cost sourcing is adopted for the ‘base’ level demand (i.e.

a minimum level of potential demand based upon past experience) with more

responsive sourcing to cope with demand above that level. See Figure 2 below:-

International Journal of Logistics Management, Vol. 13, No. 1, 2002 9

Figure 2 : Separating Base and Surge Demand

Splitting sourcing in this way enables demand forecasts to be based upon more recent

sales information and thus forecast error should reduce. Such strategies can be

enhanced by ordering components or material in advance of demand from low-cost

sources and the assembling or manufacturing the final product locally to enable

greater responsiveness. This is the strategy adopted by Zara the successful Spanish

fashion retailer. Other retailers in that sector such as the UK chain Next are bringing

more of their sourcing closer to their major markets in the UK and Ireland. Next now

source a significant number of products from Eastern Europe and Turkey rather than

the Far East (18).

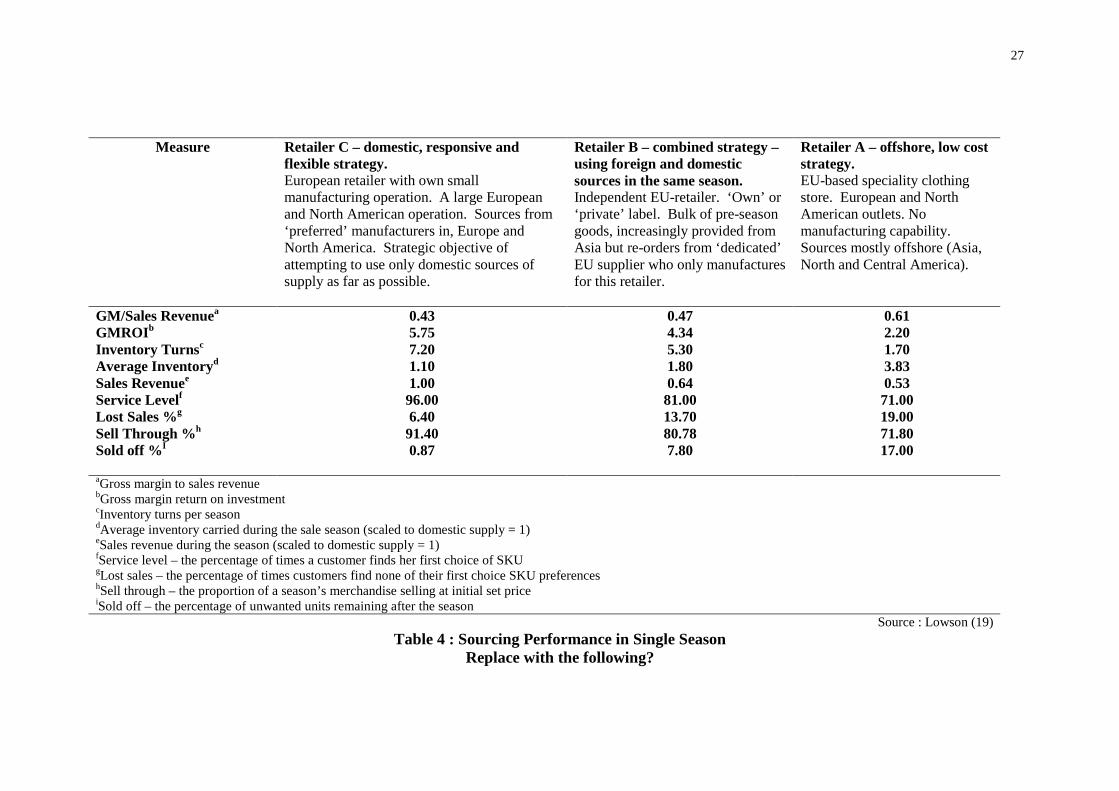

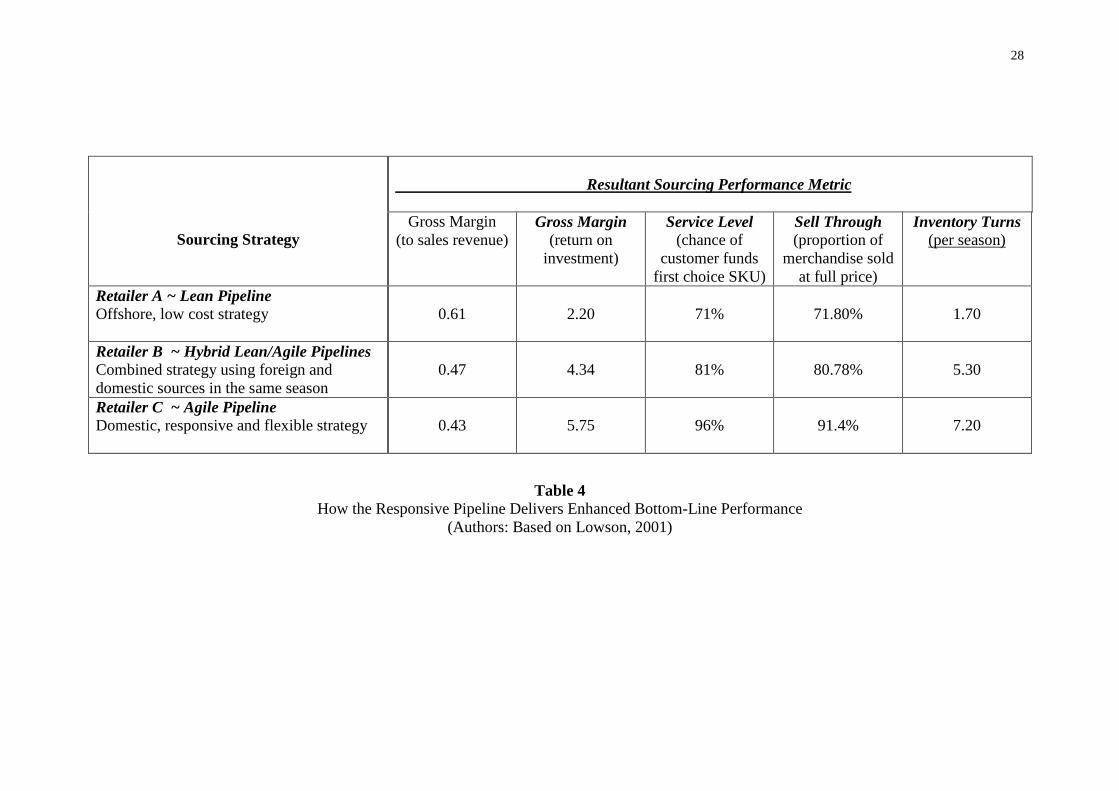

Lowson (19) contrasted three European clothing retailers who used different sourcing

strategies; low cost, responsive and hybrid and found some fascinating differences in

their financial performance. Whilst the low-cost sourcing strategy produced the

highest gross margin, it had the lowest return on investment. Conversely, the

company with the responsive sourcing strategy had the lowest gross margin but the

highest return on investment. Table 4 below which anticipates our dicussion of the

“lean” and “agile paradigm highlights the results of the Lowson study:-

Take in Table 4

TIME

Base level demand

VOLUME Surge demand

TIME

Base level demand

VOLUME Surge demand

International Journal of Logistics Management, Vol. 13, No. 1, 2002 10

The Decline of an Icon

As an example of a business which has faced challenges in managing a global

pipeline in a volatile market, we need look no further than Marks and Spencer (M&S),

a well-known UK retailer. As summarised by Christopher and Peck (20) the company

had had a century of unbridled success, prior to their fall from grace. In the 1920s the

business adopted the then revolutionary policy of buying direct from manufacturers,

instead of through wholesalers. These unique supplier relationships gave the business

an advantage that few of its rivals could match. By 1930 it was already recognisable

as an established and effective practitioner of keiritsu with its supply base (21).

Historically M&S has designed most of its clothes in-house before putting the designs

forward to favoured manufacturers with notoriously strict specifications regarding the

finished product. These manufacturers provided dedicated facilities for M&S who

required suppliers to refrain from bidding for work from other clients. The close

partnerships arrangements also relieved M&S of the need to allocate resources of its

own to technological research and development activities. The outcome of servicing

such a demanding client was a culture of continuous improvement within the

suppliers organisations and the loyalty of M&S through both good times and bad.

But this UK based supply strategy was inhibiting the development of the retail

business in Asia and the Pacific. Also M&S still officially encouraged its suppliers to

source in the UK, enabling it to maintain its ‘buy-British’ marketing stance. But their

suppliers were now struggling to remain price-competitive. Hence some had

therefore opted to supply at least a proportion of M&S’s orders from overseas

facilities or buy-in virtually finished goods produced in low-cost manufacturing

centres such as China. So in order to comply with “home” sourcing requirements, the

garments were then shipped to the UK for finishing. Some of the consignment would

then need to be returned to the region of origin for sale! This round-trip lengthened

the time delay before goods appeared in the shops, and in some instances distribution

charges added as much as £14 to an item that cost only £4 to make.

In 1998/99 failure to match supply with demand resulted in too much winter stock

costing M&S £150 million, of which £90 million was lost from pre-Christmas sales,

the remaining £60 million being the cost of clearing the excess stock. Some critics

International Journal of Logistics Management, Vol. 13, No. 1, 2002 11

pointed to overpricing and poor service as the reasons behind these falling sales.

Others claimed that customers were unhappy about a drop in quality of some

products. Retail analysts were also talking of a decline in product quality, putting it

down to an increase in overseas sourcing. In 1983 the company had sourced 90% of

its clothing in the UK, by 1994 this had slipped to 75% and then further downwards to

an estimated 65% in 1998. To become price competitive, M&S was then urging its

largest suppliers to relocate production to low-wage economies. By January 2000

M&S was indeed achieving its stated target by sourcing roughly 50% of its clothing

and general merchandise outside the UK.

When Price Deflation Impacts Demand

Historically M&S bought stock to cover over 100% of budgeted sales. Even now

they still make a forward commitment to 90% of the season’s merchandise. So the

10% uncommitted means there is far too little scope to respond when real demand is

known.

Wheatcroft (22) further infers that the company’s problems result largely from a

failure by M&S to remedy core problems relating to supply chain design and

operation. The symptoms are clearly visible via product-mix mismatch and non-

availability of key goods, especially in shoes and clothing. Disastrous performance in

these two product ranges dragged down comparable sales for M&S as a whole by

8.4% for the five weeks to November 4, 2000. Typically, poor availability cost the

knitwear division around £M6 in lost sales, and similar problems in the footwear

division cost around £M5. Even more surprising and worrying to the company is the

availability problem continuing to surround lingerie supply, which has a relatively

stable and predictable demand pattern.

In contrast the year 2000 performance of their UK competitor Next was outstanding.

Next share price rose 42p to 650p following pre-tax rise in profits of 18%.

Furthermore the Next CEO disputed claims that M&S were suffering from the

polarisation of the high street clothing market into branded goods at one end and

discounted goods at the other. His view was that “Peoples’ shopping habits are not

changing. You just have to be good at what you do.” The Next strategy is to be

aspirational and affordable. Shopping on price deflation has come to an end.

International Journal of Logistics Management, Vol. 13, No. 1, 2002 12

Shoppers are opting for higher-priced items as consumers become more interested in

quality and design.” (22). The Next sales growth continues to be maintained.

Designing and managing the supply chain to deliver just what the customer wants yet

again appears to be the key to business success.

As noted by Perry et al (23) in Australia there is now a clear trend for suppliers to the

domestic market to focus on high value-added local-demand products that can

compete with offshore imports. Also the evolution of the information economy has

had a clear impact on the Australian textile, clothing and footwear industry, providing

a potential means of control over emerging global supply chains. Communication

with overseas supply chain partners was a challenge, calling for high levels of use of

secure Extranets, EDI transaction platforms, CAD/CAM design and specification

transfer, email, facsimiles and the telephone. Perry et al (23) concluded that there is a

need for new organisational paradigms to cater for the increasingly complex supply

chain. In leadership terms they found that the close-knit retail-to-upstream supplier

partnerships that had been originally encouraged through government workshops and

assistance programmes had been eroded somewhat through the retreat of the retailers

back to their traditional power-based role of setting terms and standards for suppliers.

Role of “Lean” and “Agile” Paradigms in Modern Supply Chains

There has recently been some significant debate about the relative merits of the so-

called “lean” and “agile” approaches to supply chain management. There has been a

tendency to suggest that these approaches are mutually exclusive and represent

conflicting paradigms. In reality the two approaches can complement each other, and

in many cases there is a requirement for a “hybrid” lean/agile strategy to be adopted,

(24). Hence it is our contention that the issue is not “Lean versus Agile” rather it is

the judicious selection and integration of appropriate aspects of these paradigms

appropriate to the particular supply chain strategy.

The idea of “lean manufacturing” was popularised by Womack, Jones and Roos, (25),

together with the wider concepts of the “lean enterprise” (26). The focus of the lean

approach has essentially been on the elimination of waste or muda. The upsurge of

interest in lean manufacturing can be traced to the Toyota Production System (TPS)

with its focus on the reduction and elimination of waste. However, the origins of lean

International Journal of Logistics Management, Vol. 13, No. 1, 2002 13

manufacture are certainly visible in Spitfire aircraft production in the UK in World

War II, and Keiretsu date back to the USA automotive industry in 1915.

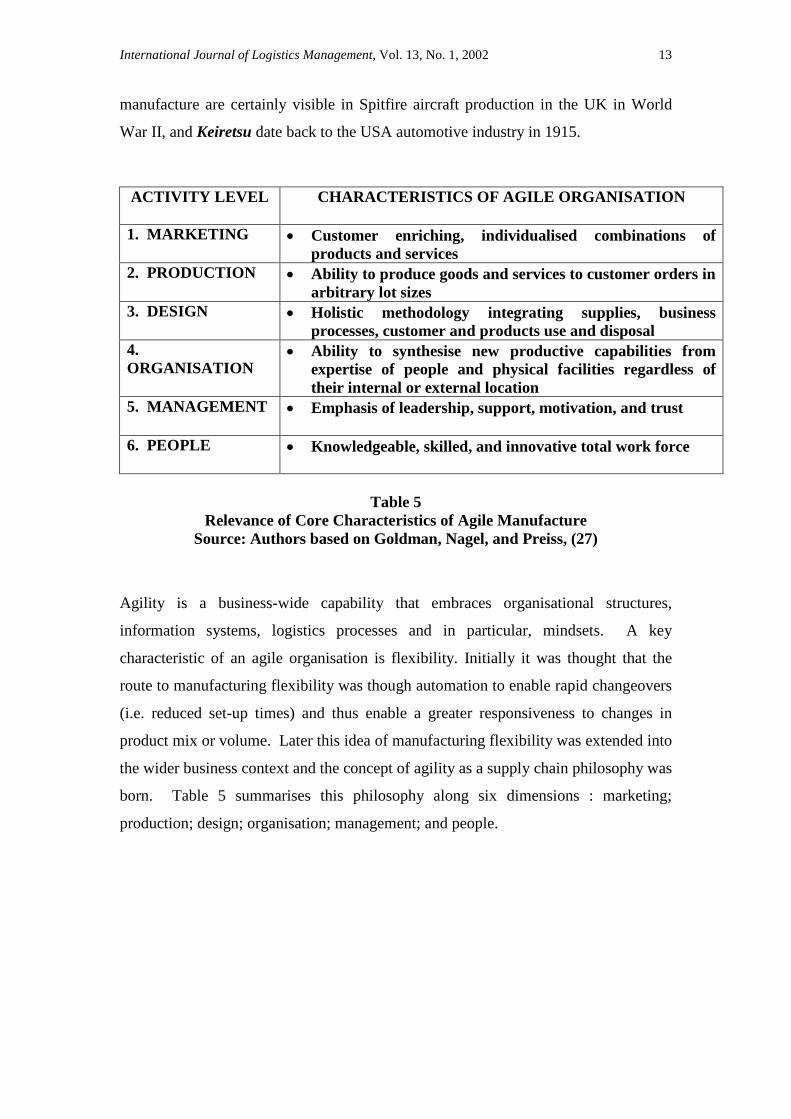

ACTIVITY LEVEL CHARACTERISTICS OF AGILE ORGANISATION

1. MARKETING Customer enriching, individualised combinations ofproducts and services

2. PRODUCTION Ability to produce goods and services to customer orders inarbitrary lot sizes

3. DESIGN Holistic methodology integrating supplies, businessprocesses, customer and products use and disposal

4.ORGANISATION

Ability to synthesise new productive capabilities fromexpertise of people and physical facilities regardless oftheir internal or external location

5. MANAGEMENT Emphasis of leadership, support, motivation, and trust

6. PEOPLE Knowledgeable, skilled, and innovative total work force

Table 5Relevance of Core Characteristics of Agile Manufacture

Source: Authors based on Goldman, Nagel, and Preiss, (27)

Agility is a business-wide capability that embraces organisational structures,

information systems, logistics processes and in particular, mindsets. A key

characteristic of an agile organisation is flexibility. Initially it was thought that the

route to manufacturing flexibility was though automation to enable rapid changeovers

(i.e. reduced set-up times) and thus enable a greater responsiveness to changes in

product mix or volume. Later this idea of manufacturing flexibility was extended into

the wider business context and the concept of agility as a supply chain philosophy was

born. Table 5 summarises this philosophy along six dimensions : marketing;

production; design; organisation; management; and people.

International Journal of Logistics Management, Vol. 13, No. 1, 2002 14

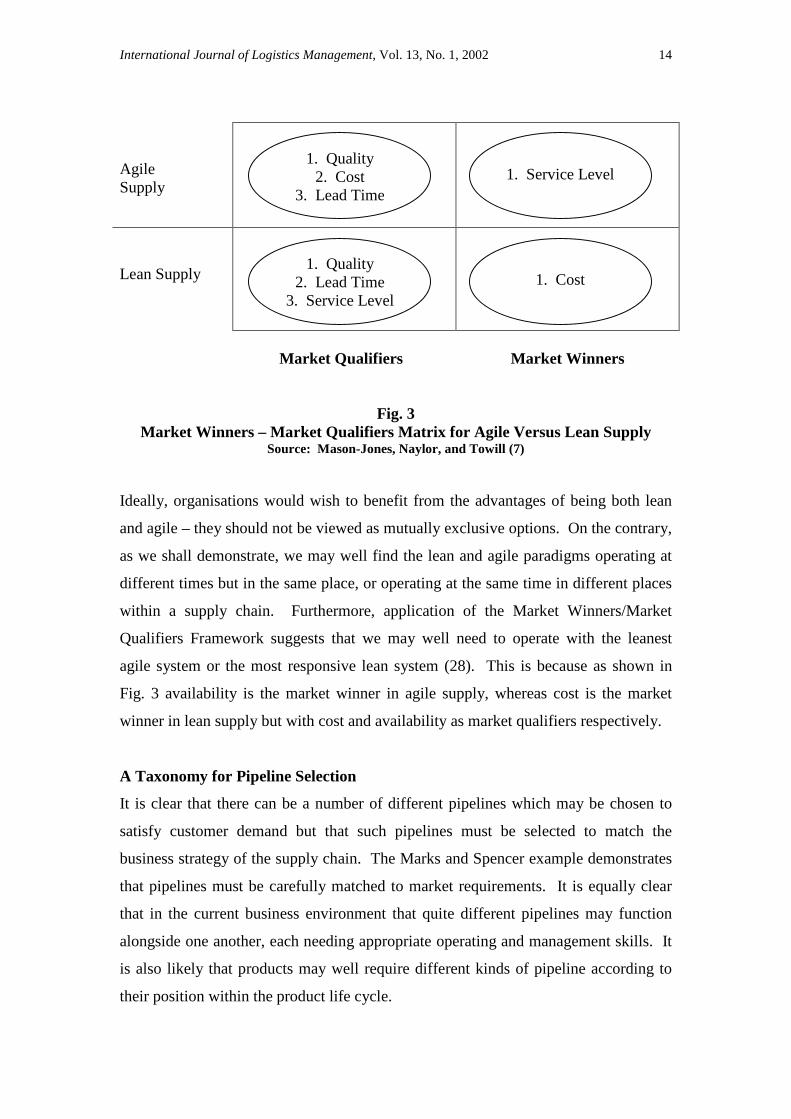

AgileSupply

Lean Supply

Market Qualifiers Market Winners

Fig. 3Market Winners – Market Qualifiers Matrix for Agile Versus Lean Supply

Source: Mason-Jones, Naylor, and Towill (7)

Ideally, organisations would wish to benefit from the advantages of being both lean

and agile – they should not be viewed as mutually exclusive options. On the contrary,

as we shall demonstrate, we may well find the lean and agile paradigms operating at

different times but in the same place, or operating at the same time in different places

within a supply chain. Furthermore, application of the Market Winners/Market

Qualifiers Framework suggests that we may well need to operate with the leanest

agile system or the most responsive lean system (28). This is because as shown in

Fig. 3 availability is the market winner in agile supply, whereas cost is the market

winner in lean supply but with cost and availability as market qualifiers respectively.

A Taxonomy for Pipeline Selection

It is clear that there can be a number of different pipelines which may be chosen to

satisfy customer demand but that such pipelines must be selected to match the

business strategy of the supply chain. The Marks and Spencer example demonstrates

that pipelines must be carefully matched to market requirements. It is equally clear

that in the current business environment that quite different pipelines may function

alongside one another, each needing appropriate operating and management skills. It

is also likely that products may well require different kinds of pipeline according to

their position within the product life cycle.

1. Quality2. Cost

3. Lead Time1. Service Level

1. Cost1. Quality

2. Lead Time3. Service Level

International Journal of Logistics Management, Vol. 13, No. 1, 2002 15

So pipelines are not fixed for all times. What is needed is continuous assessment of

the product range and market characteristics so that changing scenarios may be

identified. Against these product/market characteristics will be a number of

alternative options for pipeline design, dependent upon supply lead-times.

A number of classification schemes have been proposed in the literature (see for

example Childerhouse (29) to guide the choice of supply chain strategy. We are

suggesting a simple three dimensional classification appropriate for global supply

chains. The variables and their binary gradation are:

Products (either standard or special)

Demand (either stable or volatile)

Lead Times (either short or long)

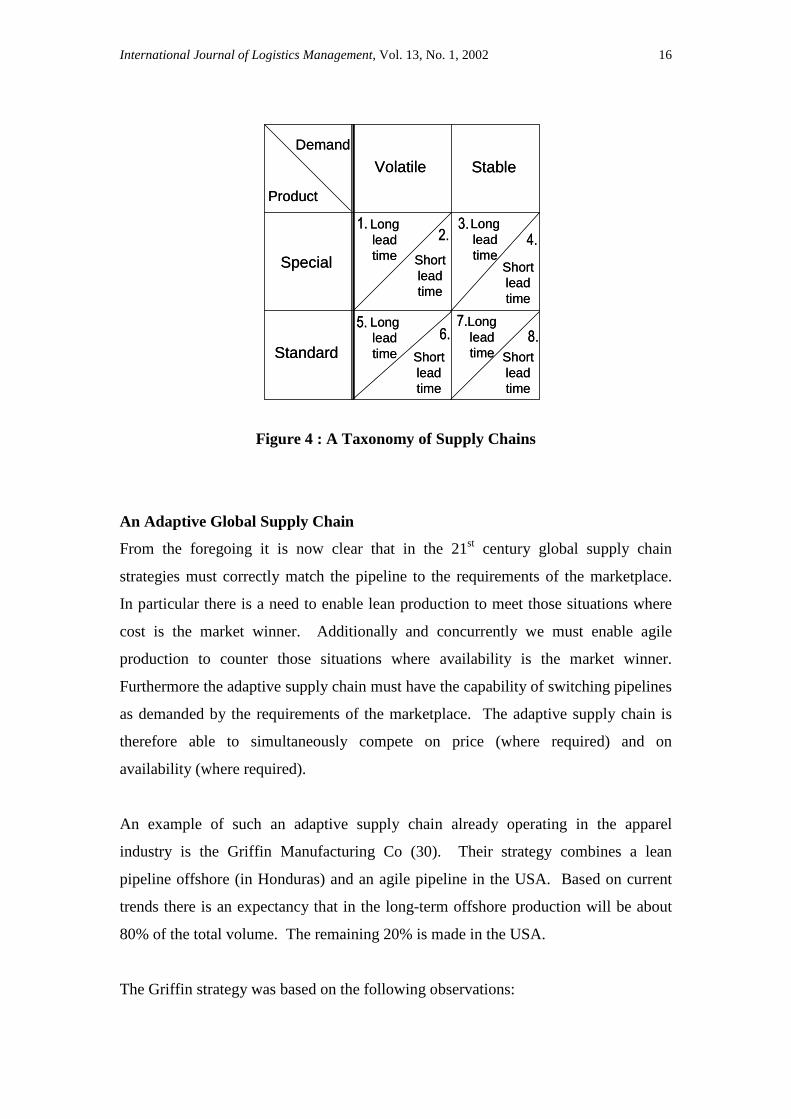

Figure 4 shows the theoretical combinations of product, demand and lead-times. In

practice some of these combinations are either unlikely to be encountered or are non-

viable situations. Where demand is stable it will generally be easier to forecast and

hence inventory-based solutions may be appropriate, particularly where lead-times are

long. However, by definition when demand is volatile, forecast-based management

becomes untenable. Hence the need in those situations for agile supply chain

strategies. Agility implies end-to-end time compression or postponement of final

product configuration.

A further element to influence the choice of supply chain strategy is the specific

‘market winner’ criterion. Where cost is the primary market winner, then the

emphasis must be upon efficiency which will imply lean strategies. However, the

reality is that lean strategies will only be viable where demand is stable and the

products are standard. Where availability is the market winner then the emphasis will

inevitably veer towards agile strategies.

International Journal of Logistics Management, Vol. 13, No. 1, 2002 16

Figure 4 : A Taxonomy of Supply Chains

An Adaptive Global Supply Chain

From the foregoing it is now clear that in the 21st century global supply chain

strategies must correctly match the pipeline to the requirements of the marketplace.

In particular there is a need to enable lean production to meet those situations where

cost is the market winner. Additionally and concurrently we must enable agile

production to counter those situations where availability is the market winner.

Furthermore the adaptive supply chain must have the capability of switching pipelines

as demanded by the requirements of the marketplace. The adaptive supply chain is

therefore able to simultaneously compete on price (where required) and on

availability (where required).

An example of such an adaptive supply chain already operating in the apparel

industry is the Griffin Manufacturing Co (30). Their strategy combines a lean

pipeline offshore (in Honduras) and an agile pipeline in the USA. Based on current

trends there is an expectancy that in the long-term offshore production will be about

80% of the total volume. The remaining 20% is made in the USA.

The Griffin strategy was based on the following observations:

Volatile Stable

Special

Standard

Demand

Product

Longleadtime

1.2.

Shortleadtime

3.4.

5.6.

7.8.

Longleadtime

Longleadtime

LongleadtimeShort

leadtime

Shortleadtime

Shortleadtime

Volatile Stable

Special

Standard

Demand

Product

Longleadtime

1.2.

Shortleadtime

3.4.

5.6.

7.8.

Longleadtime

Longleadtime

LongleadtimeShort

leadtime

Shortleadtime

Shortleadtime

International Journal of Logistics Management, Vol. 13, No. 1, 2002 17

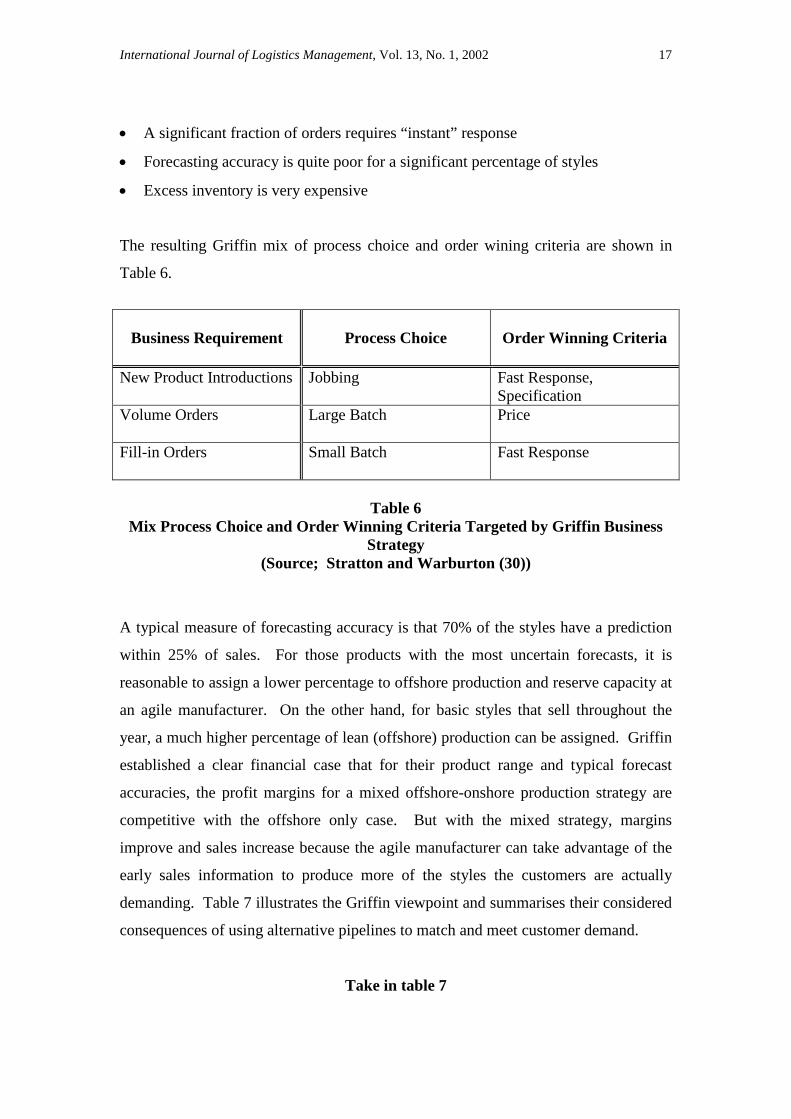

A significant fraction of orders requires “instant” response

Forecasting accuracy is quite poor for a significant percentage of styles

Excess inventory is very expensive

The resulting Griffin mix of process choice and order wining criteria are shown in

Table 6.

Business Requirement Process Choice Order Winning Criteria

New Product Introductions Jobbing Fast Response,Specification

Volume Orders Large Batch Price

Fill-in Orders Small Batch Fast Response

Table 6Mix Process Choice and Order Winning Criteria Targeted by Griffin Business

Strategy(Source; Stratton and Warburton (30))

A typical measure of forecasting accuracy is that 70% of the styles have a prediction

within 25% of sales. For those products with the most uncertain forecasts, it is

reasonable to assign a lower percentage to offshore production and reserve capacity at

an agile manufacturer. On the other hand, for basic styles that sell throughout the

year, a much higher percentage of lean (offshore) production can be assigned. Griffin

established a clear financial case that for their product range and typical forecast

accuracies, the profit margins for a mixed offshore-onshore production strategy are

competitive with the offshore only case. But with the mixed strategy, margins

improve and sales increase because the agile manufacturer can take advantage of the

early sales information to produce more of the styles the customers are actually

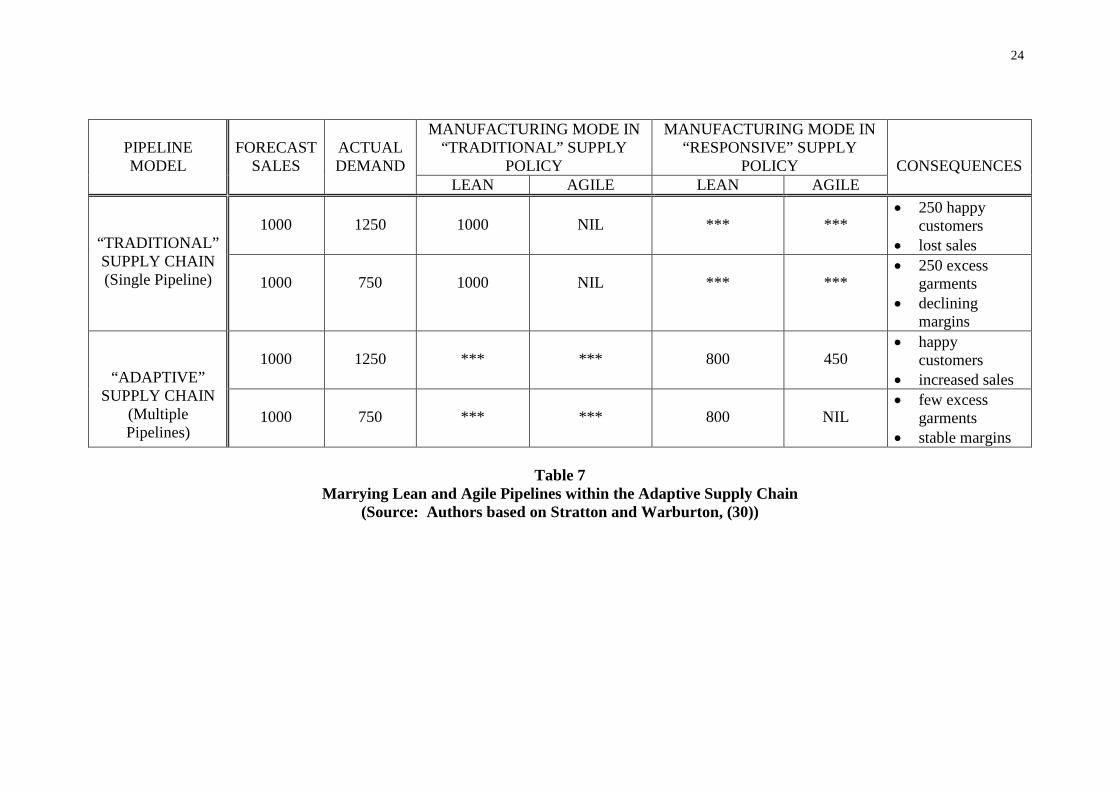

demanding. Table 7 illustrates the Griffin viewpoint and summarises their considered

consequences of using alternative pipelines to match and meet customer demand.

Take in table 7

International Journal of Logistics Management, Vol. 13, No. 1, 2002 18

There are a number of challenges associated with the mixed (adaptive pipeline)

strategy such as sharing the pain between retailer and manufacturer. In one sense

what is required of the retailer using the adaptive supply chain is a much more

challenging approach. Rather than ordering to forecast, the retailer has to analyse

forecasts. It is their remit to decide on offshore (lean) production commitments, and

USA (agile) capacity reservation. Hence retailers must share their sales data and

work continuously with manufacturers to get the exact inventory they need. When

sales increase, everyone will be satisfied. The retailer sells more products with fewer

markdowns, resulting in less excess inventory. Also, the manufacturer can make

minor adjustments (e.g. fill in sizes) to further tailor the inventory to the actual

demand. Finally, there is less profit leakage via “cannibalisation” due to sales

markdowns. Cannibalisation is the phenomenon whereby the customer buys two

cheaper garments now, thus avoiding a full price purchase in the future.

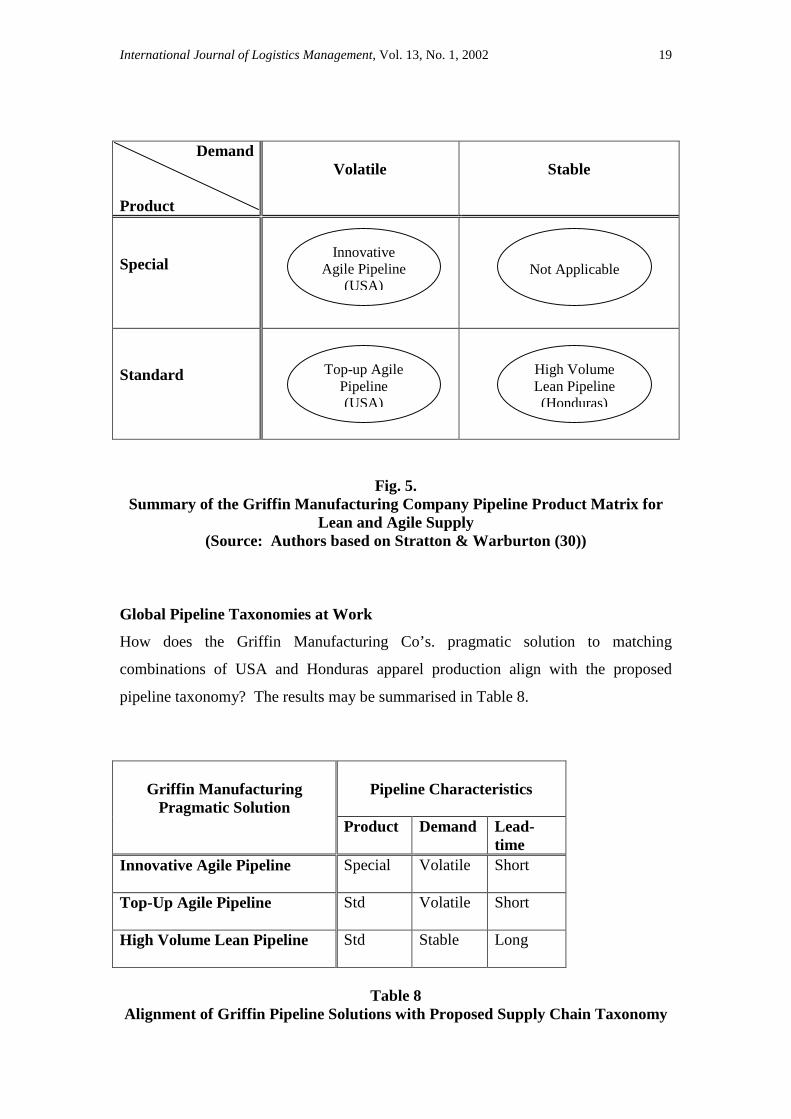

The way that Griffin Manufacturing Co. have engineered and exploited the adaptive

supply chain is shown in matrix format in Fig. 5. Along with the implied changes in

operations a significant evolution in Griffin’s management philosophy also occurred.

Initially the USA factory used to view themselves as in competition with the

Honduras factory, and resented every unit that went abroad as lost internal business.

Eventually they came to realise that they could never compete on price alone, but did

have an essential legitimate and complimentary cost-effective role in supplying the

retailer. The days of large, stable production runs for the US plant have disappeared.

But the reality is that the plant can survive by making small runs of complex styles,

and producing them quickly. As shown in Fig. 5, the USA facility also “tops-up”

high volume products as required to meet extreme demands. These two agile

pipelines account for some 20% of the total volume. The Griffin strategy has thus

protected US jobs by identifying the right agile home-based niches to complement

lean Honduras manufacture.

International Journal of Logistics Management, Vol. 13, No. 1, 2002 19

Demand

Product

Volatile Stable

Special

Standard

Fig. 5.Summary of the Griffin Manufacturing Company Pipeline Product Matrix for

Lean and Agile Supply(Source: Authors based on Stratton & Warburton (30))

Global Pipeline Taxonomies at Work

How does the Griffin Manufacturing Co’s. pragmatic solution to matching

combinations of USA and Honduras apparel production align with the proposed

pipeline taxonomy? The results may be summarised in Table 8.

Pipeline CharacteristicsGriffin ManufacturingPragmatic Solution

Product Demand Lead-time

Innovative Agile Pipeline Special Volatile Short

Top-Up Agile Pipeline Std Volatile Short

High Volume Lean Pipeline Std Stable Long

Table 8Alignment of Griffin Pipeline Solutions with Proposed Supply Chain Taxonomy

InnovativeAgile Pipeline

(USA)

High VolumeLean Pipeline(Honduras)

Top-up AgilePipeline(USA)

Not Applicable

International Journal of Logistics Management, Vol. 13, No. 1, 2002 20

How many significantly different pipelines do we really need? The biggest need is

undoubtedly to move away from the “One Size Fits All” scenario. At the same time

there is little point in selecting a taxonomy yielding multiple possible pipelines if the

end result means that only a handful of solutions are eventually selected. This

“filtering” may be on the basis of management preference for specific pipelines, or on

the base of a cost-effectiveness model. We think a binary classification system has a

number of advantages. Firstly, analysts have to make a firm judgement in such a

situation – they cannot sit on the fence. Secondly, the use of binary codes tends to

avoid regression to the mean ~ “seeking to satisfy everyone, but pleasing no one”.

There is little point in using a taxonomy which does not lead to supply chain

managers being offered real choices in a language they understand. Our proposed

classification system based on Lead Times (Short/Long); Demand Predictability

(Stable/Volatile) and Product Type (Standard/Special) meets this requirement.

Conclusions

Present day marketplaces are volatile and at the same time extremely price sensitive.

Achieving success in this environment requires a good knowledge of pipeline

requirements from marketing back to materials manufacturers. Within supply chains

it is possible to identify some operations which are “lean” (without fat) and some

operations which are “agile” (nimble). The aim is to select and marry together the

particular combinations of lean/agile operations so as to match individual pipelines to

market needs.

In the paper we have developed a taxonomy suitable for this purpose. It is based on

demand (predictable/volatile), product (standard/special) and supply lead times

(long/short). This is seen to generate three feasible pipeline designs, all of which are

applicable within the global apparel supply chain framework. Generally the preferred

solution will be that predictable demand for standard items will be met via a lean

pipeline probably fed from overseas manufacturers. Volatile demand for special

items will then be met via an agile pipeline probably fed from home manufacturers.

A third pipeline design is for quick response to top-up standard products for which

there is an unexpected demand for specific colours, sizes, volume etc.

International Journal of Logistics Management, Vol. 13, No. 1, 2002 21

References

(1) Christopher, Martin, “Logistics and Supply Chain Management : Strategiesfor Reducing Costs and Improving Services” Pitman Publishing, London,1992.

(2) McCullen, Peter and Denis R. Towill, “Practical Ways of Reducing Bullwhip:the case of the Glosuch global supply chain”, International Journal ofOperations Management, Vol 26, No. 10, 2000, pp 24-30.

(3) Shewchuck, John. P., “Agile Manufacturing : One Size Does Not Fit All”,Proc. Int. Conf. on Manufacturing Value Chains, Troon, 1998, pp 143-150.

(4) Fuller, Joseph B., James O’Connor and Richard Rawlinson, “TailoredLogistics : the Next Advantage”, Harvard Business Review, May-June, 1993,pp 87-98.

(5) Fisher, Marshall L., Janice H. Hammond, Walter R Obermeyer, AnanathRaman, “Configuring a Supply Chain to Reduce the Cost of DemandUncertainty”, Production and Operations Management, Vol 6, No. 3, Fall,1997, pp 211-225.

(6) Towill, Denis R. and Martin Christopher, “The Supply Chain StrategyConundrum ~ to be Lean or Agile or to be Lean and Agile”, Proceedings ofthe International Logistics Symposium, Salzburg, 2001, pp 3-12.

(7) Mason-Jones, Rachel, James B. Naylor, and Denis R. Towill, “Lean, Agile orLeagile? Matching Your Supply Chain to the Marketplace”, InternationalJournal of Production Research, Vol 38(1`7), 2000, pp 4061-4070.

(8) Blackburn, Joseph D., “The Quick-Response Movement in the ApparelIndustry: a Case Study in Time Compressing Supply Chains”, in J.D.Blackburn (Ed) “Time Based Competition”, Business One Irwin, Homewood,1991, pp 246-269.

(9) Hill, Terry, Manufacturing Strategy : Text and Cases, Second Edition,MacMillan Press, London, 1993.

(10) Fisher, Marshall L., “What is the Right Supply Chain for your Product?”,Harvard Business Review, March/April, 1997, pp105-116.

(11) Fisher, Marshall L., Janice H. Hammond, Walter R. Obermeyer, AnanathRaman, “Making Supply Meet Demand in an Uncertain World”, HarvardBusiness Review, May-June, 1994, pp 83-93.

International Journal of Logistics Management, Vol. 13, No. 1, 2002 22

(12) Lowson, Robert, Russell King and Alan Hunter (1999), Quick Response:Managing the Supply Chain to Meet Customer Demand, John Wiley and SonsLtd., Chichester.

(13) Wikner, Joakim, Denis R. Towill, and Mohamed M. Naim, “SmoothingSupply Chain Dynamics”, International Journal of Production Economics,Vol 22, No. 3, 1991, pp 231-248.

(14) Mason-Jones, Rachel and Denis R. Towill (1997) “Information enrichment:designing the supply chain for competitive advantage”, International Journalof Supply Chain Management, Vol. 2, No. 4, pp 137-148.

(15) Stalk, Jnr. George H. and Hout, Thomas M., Competing Against Time, FreePress, New York, 1990.

(16) Lowson, Robert, “Analysing the Effectiveness of European Retail SourcingStrategies”, European Management Journal, Vol. 19, No. 5, 2001, pp 543-551.

(17) Christopher, Martin, and Helen Peck, “Moving Mountains at Marks andSpencer”, Case Study, Council of Logistics Management, USA, 2001.

(18) Shamoon, Stella, “The Next Big Thing”, The Times, London, U.K., 30 March2002.

(19) Lowson, Robert, “Analysing the Effectiveness of European Retail SourcingStrategies”, European Management Journal, Vol. 19, No. 5, 2001, pp 543-551

(20) Christopher, Martin & Helen Peck, “Moving Mountains at Marks & Spencer”,Case Study, Council of Logistics Management, USA, 2001.

(21) Drucker, Peter, “The Information that Executives Truly Need”, HarvardBusiness Review, Jan-Feb, 1995, pp 55-63.

(22) Wheatcroft, Patience, Business Commentary, The Times, London, 13September and 8 November 2000

(23) Perry, Marcia, Amrik S. Sohal and Richard Laney, “An Australian QuickResponse Supply Chain Model” Proceedings ISL - Logistics and the DigitalEconomy Conference, Salzburg, 2001.

(24) Christopher, Martin and Denis R. Towill, “Marrying the Lean and AgileParadigms”, Proc. EUROMA Conference, Ghent, 2000, pp 114-121.

(25) Womack, James P., David T. Jones & Daniel Roos, The Machine the Changedthe World, Macmillan, USA, 1990.

(26) Womack, James P.& David T. Jones, Lean Thinking, Simon & Schuster, USA,1996

International Journal of Logistics Management, Vol. 13, No. 1, 2002 23

(27) Goldman, Steven N., Roger N. Nagel & Kenneth Preiss, Agile Competitorsand Virtual Corporations, 1995

(28) McCullen, Peter, and Denis R. Towill, “Manufacturing Agility and the LeanSupply Chain”, Proc. MIM 2000 Conf, Aston, 2000, pp 424-431.

(29) Childerhouse, P., Enabling Seamless Market-Oriented Supply Chains, PhDThesis, Cardiff University, 2001

(30) Warburton, Roger & Roy Stratton, “Questioning the Relentness Shift toOffshore Manufacturing”, Supply Chain Management, Vol. 7, No. 2, 2002, pp101-108.

24

MANUFACTURING MODE IN“TRADITIONAL” SUPPLY

POLICY

MANUFACTURING MODE IN“RESPONSIVE” SUPPLY

POLICYPIPELINEMODEL

FORECASTSALES

ACTUALDEMAND

LEAN AGILE LEAN AGILECONSEQUENCES

1000 1250 1000 NIL *** *** 250 happy

customers lost sales“TRADITIONAL”

SUPPLY CHAIN(Single Pipeline) 1000 750 1000 NIL *** ***

250 excessgarments

decliningmargins

1000 1250 *** *** 800 450 happy

customers increased sales“ADAPTIVE”

SUPPLY CHAIN(MultiplePipelines)

1000 750 *** *** 800 NIL few excess

garments stable margins

Table 7Marrying Lean and Agile Pipelines within the Adaptive Supply Chain

(Source: Authors based on Stratton and Warburton, (30))

25

Once order has been placed, what is the vendors’ latitude for change?

Order volume change (% respondents) Order mix change (% respondents)

Sourcing regions None Some Substantial None Some Substantial

Before the start of the sale season North AmericaEuropeanNon-EU*Central AmericaAsiaAfricaOther

41%8%29%71%67%59%33%

37%53%44%20%21%18%41%

22%39%27%9%12%23%26%

58%21%37%76%71%63%31%

28%47%39%19%18%19%37%

14%32%24%5%11%18%34%

After the start of the sale season North AmericaEuropeanNon-EU*Central AmericaAsiaAfricaOther

57%19%34%63%71%62%32%

22%47%39%32%20%10%43%

21%34%17%15%8%18%25%

62%27%62%64%87%74%39%

18%40%34%29%11%7%36%

20%33%4%7%2%19%23%

* European States but non-EU 15 members Source : Lowson (16)

Table 2 : Suppliers Latitude for Volume and Mix Change both Before and DuringSales Season (by Vendor Geographic Region)

26

Composite Response MetricBefore Start of Season After Start of Season

Sourcing Region Typical Lead TimeTo Finalise

Orders (Weeks) Volume Change Order Mix Volume Change Order MixNorth America 35 .34 .23 .28 .26European 12 .57 .48 .30 .15Non-EU 21 .42 .37 .49 .46Central America 38 .16 .11 .25 .17Asia 55 .19 .17 .15 .06Africa 39 .29 .24 .21 .21Other 34 .40 .46 .39 .35

Table 3 : Estimate of Vendor Responsiveness to Volume Change and Mix ChangeAccording to Geographic Region

(Source : Authors based on Survey results Undertaken by Lowson (16))

27

Measure Retailer C – domestic, responsive andflexible strategy.European retailer with own smallmanufacturing operation. A large Europeanand North American operation. Sources from‘preferred’ manufacturers in, Europe andNorth America. Strategic objective ofattempting to use only domestic sources ofsupply as far as possible.

Retailer B – combined strategy –using foreign and domesticsources in the same season.Independent EU-retailer. ‘Own’ or‘private’ label. Bulk of pre-seasongoods, increasingly provided fromAsia but re-orders from ‘dedicated’EU supplier who only manufacturesfor this retailer.

Retailer A – offshore, low coststrategy.EU-based speciality clothingstore. European and NorthAmerican outlets. Nomanufacturing capability.Sources mostly offshore (Asia,North and Central America).

GM/Sales Revenuea

GMROIb

Inventory Turnsc

Average Inventoryd

Sales Revenuee

Service Levelf

Lost Sales %g

Sell Through %h

Sold off %I

0.435.757.201.101.00

96.006.40

91.400.87

0.474.345.301.800.64

81.0013.7080.787.80

0.612.201.703.830.53

71.0019.0071.8017.00

aGross margin to sales revenuebGross margin return on investmentcInventory turns per seasondAverage inventory carried during the sale season (scaled to domestic supply = 1)eSales revenue during the season (scaled to domestic supply = 1)fService level – the percentage of times a customer finds her first choice of SKUgLost sales – the percentage of times customers find none of their first choice SKU preferenceshSell through – the proportion of a season’s merchandise selling at initial set priceiSold off – the percentage of unwanted units remaining after the season

Source : Lowson (19)Table 4 : Sourcing Performance in Single Season

Replace with the following?

28

Resultant Sourcing Performance Metric

Sourcing StrategyGross Margin

(to sales revenue)Gross Margin

(return oninvestment)

Service Level(chance of

customer fundsfirst choice SKU)

Sell Through(proportion of

merchandise soldat full price)

Inventory Turns(per season)

Retailer A ~ Lean PipelineOffshore, low cost strategy 0.61 2.20 71% 71.80% 1.70

Retailer B ~ Hybrid Lean/Agile PipelinesCombined strategy using foreign anddomestic sources in the same season

0.47 4.34 81% 80.78% 5.30

Retailer C ~ Agile PipelineDomestic, responsive and flexible strategy 0.43 5.75 96% 91.4% 7.20

Table 4How the Responsive Pipeline Delivers Enhanced Bottom-Line Performance

(Authors: Based on Lowson, 2001)

29

Denis R. Towill is a University of Wales Research Professor and is presently Co-Director of the Logistics Systems Dynamics Group at CardiffUniversity. In 2000 he was awarded the Lord Hirst Premium by the Council of the Institution of Electrical Engineers for the paper“Management Theory – is it of any practical use?” Professor Towill has worked with many industries, including automotive, aerospace,mechanical, construction, electronic, steel supplies, and healthcare supply chains. He holds the degree of D.Sc from the University ofBirmingham. In 1988 he was elected a Fellow of the Royal Academy of Engineering in recognition of his contributions on the theory andapplication of systems engineering to a range of European industries. He can be reached at Cardiff University, Cardiff Business School,Aberconway Building, Colum Drive Cardiff, CF10 3EU, Wales, UK, Phone : 44 (0)29 20 876083, Fax : 44 (0)29 20 874301.

Martin G Christopher is Professor of Marketing and Logistics at Cranfield School of Management, Cranfield University, UK. He is alsoChairman of the Cranfield Centre for Logistics and Transportation, Europe’s leading centre for teaching and research in logistics and supplychain management. Dr Christopher is an Emeritus Fellow of the Institute of Logistics and Transport in the UK who in 1988 awarded him the SirRobert Lawrence Gold Medal for his contribution to logistics education. In 1997 he was jointly awarded the Council of Logistics Management’sFounder’s Award. He can be reached at Cranfield School of Management, Cranfield University, Cranfield, Bedford, England, MK43 0AL.Phone : 44 1234 751122, Fax : 44 1234 752691.