Embed Size (px)

Citation preview

Customer RelationshipManagement (CRM)stream

Dublin, 21 june 2000

Customer RelationshipManagement (CRM)stream

Dublin, 21 june 2000

Deutsche Bank:On-line banking for profit

Resi CuypersPricewaterhouseCoopers

Deutsche Bank:On-line banking for profit

Resi CuypersPricewaterhouseCoopers

Who is Resi Cuypers?

! Since March 1998:"Data Mining expert at Analytical Intelligence Services (AIS)"AIS, experts quantitative methods and techniques inAmsterdam, NL"Responsible development I-CRM (Apply Data Mining)

! Prior:"SAS Consultant ELC"Statistical Process Engineer at ‘Heidelberger Zement’ concern

! Master degree Mathematics

Agenda

! Deutsche Bank’s business drivers forces the need for CRM

! On-line Banking Segmentation Project Objectives and Approach

! Process and Methodology Segmentation and Modelling

! Process and Methodology Customer proposition

! Key Results and Experiences

Deutsche Bank’s business driversforcing the need for CRM

On-line Banking Service offering

! Successfully developed range of On-line Banking services(1998).On-line banking:= the delivery of banking and financial servicesthrough electronic devices such as PC’s, Mobile Phone andInteractive TV.

! Services used by > 300,000 Retail and Private customers(at beginning 1999).

! Services based on existing customer segmentation model:classification four groups based on a combination of transactionvolume, income and net wealth.

Deutsche Bank’s business drivers forcing the need for CRM

! Question: Is existing customer segmentation modelsophisticated enough for On-line Banking?

Headquarters

Telephone Infrastructure

WebInfrastructure

Retailers

Database and Data Mining

Overnight Delivery

Manufacturer

Distributors

Transportation

Direct Marketing

Suppliersand Vendors

StrategicPartners

CustomersInfomediary andOutsourced Service Products

But, Profitable Growth is More Difficult to Achieve as Businesses Face Significant Change

! New entrants(competitorsfrom 8 to 180)

! New channels

! Newtechnologies

! New markets

! Disintermediation

! Globalisation

! Deregulation

! Consolidation

! Convergence

! Market saturation

! Eroding customerloyalty

! E-mania

Deutsche Bank’s business drivers forcing the need for CRM

Deutsche Bank’s business drivers forcing the need for CRM

In the Face of these Changes, Deutsche Bank realised the Importance of Customer Centricity

! Gained competitive advantage in key area Customers & Product:

# Proactively manage customer information and relationships tomaximise lifetime customer value (incl. Recruiting)

# Differentiated management of various customer segments

# Using strength On-line Banking

CustomersProactive management of

customer information & relationships

ChannelsDevelopment & integrationof multiple sales & service

channels

CustomersProactive management of

customer information & relationships

Products/ServicesManagement of innovation

& time-to-market

CustomerRelationshipManagement

On-line Banking SegmentationProject Objectives and Approach

Knowing On-line Banking Customers, Market, Penetration, Competitors and taking Action

1 Development robust (static) segmentation model within:

# The German retail and private banking market# Deutsche Bank’s existing On-line Banking customer Base(map)# Deutsche Bank’s current Retail and Private Client customer base

2 Design of On-line Banking consumer propositions for the definedtarget customer segments

3 Development of high level marketing and communication plans insupport of defined consumer propositions

On-line Banking Segmentation Project Objectives and Approach

⇓⇓⇓⇓ Ultimate objective: dynamic segmentation

Project organisation PwC: November 1998 - February 1999

On-line Banking Segmentation Project Objectives and Approach

ProjectManager

Segmentationand Modeling

CustomerProposition

DynamicSegmentation

Model

Team1 Team3Team2

! Market andCustomerSegmentationexpert

! Statistician/dataminer

! Databasebuilder/modeler

! Internet Bankingmarketingexpert

! Market analyst(full time)

! MarketResearchanalyst

! 1 PwC technicalarchitect

! 1 PwC technicalanalyst

! 2 PwC databasebuilder/modellers

Example: Route map Segmentation Development Existing On- line Banking Customer Base

Start-up,Mobilisation

andRequirementsConfirmation

and

Interviews

Systems andDatabaseAnalysis

DataEvaluation

Validateexisting

Segments

BuildData

Sample

ApplyProfitability

Model2Data

MergeData

Enhancement

MarketResearch

SegmentTest

Map Segments toDBank Database

Confirm BridgingVariables for

Mapping againstexternal Market

Requires flags onDBank Database

Input of initialConsumer

Propositions

Iterative

Map against Data Models and External Data

Design and buildDynamic Segments

DesignStatic

Segments

Analysis andDesign Build and Test Implement

On-line Banking Segmentation Project Objectives and Approach

Process and MethodologySegmentation and Modelling

Interviews with Deutsche Bank resulted in initialising and prioritising high-level customer focus groups...

GermanResidentBanking

populationGerman ISPSubscribers

Deutsche BankCustomer Base

German InternetBanking Customers

!7: Non-Deutsche Bankcustomers in Germany withInternet banking and ISP.!8: Non-Deutsche Bankcustomers in Germany withInternet banking.!10: Non-Deutsche Bankcustomers in Germany withISP.!11: Non-Deutsche Bankcustomers in Germany.

1

2

3

46

5 7

8

9

10

11

Process and Methodology Segmentation and Modelling

! How easy is it for the individuals to be identified?i.e. is data available (internally or externally), would enable on-going identification of people within each segment?

! How attractive are the individual segments toDeutsche Bank?Segment of strategic importance i.e. is a specific segment likelyto grow or is it likely to contain people who aredisproportionately profitable?

! Can we identify cost effective methods ofcommunicating with the segments?i.e. through either highly targeted or broadcast media.

according to set criteria

Process and Methodology Segmentation and Modelling

Technical Environment was established for data analysis and modelling (data required not all available in DwH)

Deutsche BankLAN

Data from MainframeData Warehouse

HardwareA Client Server environment utilising existingnetwork infrastructure (40 GB), linking:! Sun Solaris 2.4 server, with

Sun OS UNIX 4.2 operating system,! Client PC, operating Microsoft NT4.

SoftwareUsed for analysis and file manipulation:! Server

SAS System license DB v6.12Enterprise Miner ™ v2.01

! ClientSAS System license DB v6.12Enterprise Miner ™ v2.01Labtam X-WinPro for X-Windows emulation and ftp

Project Client

UNIX Server

Process and Methodology Segmentation and Modelling

Our methodology comprised a number of sequential tasks

! Data Identification, Collection and Collation - INTERNAL: DwH vast and complex, knowledge very vast apart; usedDatabase Marketing data till Nov 1998 (8.21mio unique clientnumber), logfiles on-line Banking service (June-Nov 1998), Tel. banking service (Oct-Nov1998), file flag interest (June 1998)EXTERNAL: Market ‘Lifestyle’ database last 2 years, Stat. Repr. Adults, ownsegmentation system (survey quarterly: 1.1 Mio individual records, 900 var.)

! Data Preparation, Enhancement and Analysis - Eliminate poorlypopulated variables, Remove variables unlikely to influence analysis (e.g.:favourite Cigarette brand), Enhance by combining variables into scores(e.g.: score on PC Ownership sophistication - equipment and peripherals).Using Crosstabs and Descriptive Statistics.

! Data Modelling - iterative process for discriminating personnelcharacteristics; using clustering (least squares), decision trees

! Model Validation - checking with data not used in modelling phase(exclude data problems)

! Constraints - European and German Data Protection Legislation

Process and Methodology Segmentation and Modelling

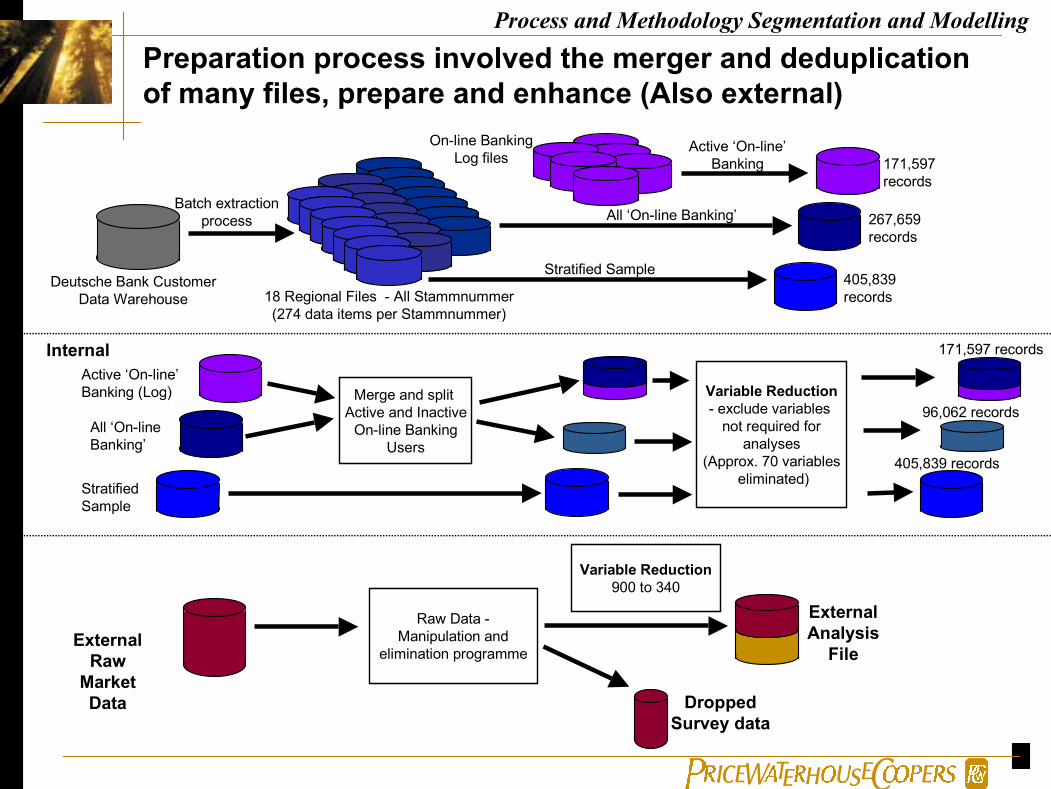

Preparation process involved the merger and deduplicationof many files, prepare and enhance (Also external)

Deutsche Bank CustomerData Warehouse 18 Regional Files - All Stammnummer

(274 data items per Stammnummer)

Batch extractionprocess

On-line BankingLog files

Stratified Sample

All ‘On-line Banking’

Active ‘On-line’Banking 171,597

records

267,659records

405,839records

Process and Methodology Segmentation and Modelling

Merge and split Active and Inactive

On-line BankingUsers

Variable Reduction- exclude variables

not required foranalyses

(Approx. 70 variables eliminated)

171,597 records

96,062 records

StratifiedSample

All ‘On-lineBanking’

Active ‘On-line’Banking (Log)

405,839 records

Raw Data -Manipulation and

elimination programme External

RawMarketData

ExternalAnalysis

File

DroppedSurvey data

Variable Reduction900 to 340

Internal

Preparation Final External Market Data Files

External Market Base File

On-line Bankingnon-users

Non- PC Owners

Not PotentialPC Owners

‘Internet not importantin future’

On-line Bankingusers

PC Owners

Potential PCOwners

‘Internet importantin future’

Satisfied andDissatisfied users

Process and Methodology Segmentation and Modelling

The modelling activity was aligned with the original high-level customer groups finished for analysing

1

2

3

46

5 7

8

9

10

11

On-line Bankingusers

‘Internet importantin future’

PC Owners

Potential PCOwners

Technologically lessadvanced

Unlikely Remainder

Within each analysissegment it waspossible to split the‘populations’ into:

! Those whoconsideredDeutsche Bank tobe theirmain Bank.

! Those whoconsideredanother bank to betheir main bank.Primary Targets

Secondary Targets

Process and Methodology Segmentation and Modelling

Process and MethodologyCustomer Proposition

The Output from our Process and Methodology...

Skdjfkasjdf;jks

Skdjfkasjdf;jks

Skdjfkasjdf;jks

Product1

2

12

3

46

5 7

89

10

11

Personalised Internet Banking, incl:personalised web siteson-line advicepersonalised product offers and pricing

Broking, incl:preselected portfolio optionsstock warning systemanalysis and scenario systemslinks to other stock exchanges

Potentialsubject areasof proposition

Group 1: Online heavy users

! 20-45 years old! 6 men & 3 women! 50% high earners

Recruitment criteria

Face to facefocus groups

Targetmarket andcompetitor

analysis Developnew

propositionideas Assess

Internalscoring &

prioritisation Research

customerevaluationand ideas Evaluate

analysis and

refinement

1

2

3

4

5

Brainstorms,

workshops,

revised product

frameworks

Customer research

Score matrix

Narrower

customer group

characteristics

Macro market

Review and development

"Worked up

propositions

(Not repeated)

Process and Methodology Customer proposition

In detail...

! Estimating market opportunity and Dynamics (possible growth)

! Key Characteristics within each group were identified (resultsegmentation analysis).

! Activities, penetration Deutsche Bank’s main competitorsreviewed (result segmentation analysis).

! Created a wide range of initial propositions for existing Internetusers, starters, retention, migrate T-Online and AOL customersto the Internet - (1) based on our expertise and market knowledge (fromdocumentation, interview panels etc.) (2) based on insights of InfratestBurke (3) The categories were based upon the need to, and appetite for,Deutsche Bank to enter into partnerships with other organisations.

! Create a shortlist proposition - 46 propositions were scored throughteam Bank and score matrix decreased to 5. No conjoint analysis used.

! Qualitative Market research and Test - feedback of (pot.) custo-mers and test against published data (ICON) and Infratest Burke

Process and Methodology Customer proposition

Key Results and Experiences

Key Results and Experiences

We have estimated the market opportunity for On-lineBanking based on our initial customer groups...

1

2*

3*

46

5* 7**8**

9**

10

11

Red circle - 6.9m Internet users inGermany (14-59 years old).Growth 80%Growth possible?

Green circle - 2.4m on-line banking users inthe German Market. 3,5% total population[growth 49%]

Blue circle - 69m people inGermany aged over 15 years(46.4m people aged 14-59 yearsold).[growth 0,2%]

Yellow circle - 6.6mDeutsche Bank Retail andPrivate customers, of whichapproximately 67% are agedbetween 14-59 years old.9,5% total population.[growth past 3 years 2%]

* customer groups 2, 3and 5 (existing DeutscheBank on-line bankingcustomers) add up to310k retail and privatecustomers.0,4%total, 12,9% on-line bankers.[growth 42%]

** customer groups 7, 8 and 9 addup to approximately 2.1m people.

Approximately 15% of the Germanpopulation (aged 14-59 years) areinternet users. Assuming that theDeutsche Bank retail and private clientcustomer base is statistically representativeof the German population, then customergroups 5 and 6 include 990k people (agedbetween 14-59 years old).

¹ It should be noted that data relating to the German on-line banking market variesconsiderably depending upon the source.

!The respective size of key customer groups have been estimatedon the basis of available market data¹.

German ResidentBanking Population.Existing German Internet Users

Deutsche BankCustomer Base

Existing German On-lineBanking Customers

1

2

3

46

5 78

9

10

11

Deutsche Bank customers:1: ‘Satisfied Early Users’

2: ‘Dissatisfied Adopters’

3: ‘Potential Experimenters’

4: ‘Following the TechnologyTrend’

5: ‘Passing Interest’

Non-Deutsche Bank customers:1: ‘Satisfied Early Users’

2: ‘Dissatisfied Adopters’

3: ‘Potential Experimenters’

4: ‘Following the TechnologyTrend’

5: ‘Passing Interest’

Segmentation analysis: Six main target customer groupswere identified and ten established

Key Results and Experiences

The key characteristics of the customers within eachgroup were identified by segmentation analysis (Twoexamples)

1

2*3*

46

5* 78

9

10

11

Existing Internet Users (not DB customers)

! 31% of households with PCs are on the Internet.

! 33% of mobile phone users are on the Internet

! 44% of households with laptops at home have Internet access

! Almost 32% of Internet users are between 20 and 29 years old - withthe strongest growth rate

! More than 50% have a net household income over 5,000DM permonth

! Only 8% use an OSP for on-line services only (down from 13%)

! The slowest growth sector is those who use it for professionalreasons with ‘News’ surfers the fastest growing. Typically the ‘News’surfers are using it mainly externally (only 27% using it only at home).

! Students and Abiturienten are the fastest growing group.

! Access from work or university is increasing faster than access athome.

! Up to 53% of business heads and directors are on the Internet,suggesting a potentially high hit rate for targeted marketing.

! Self employed and freelance comprise 13% of the Internet users - anincreasing percentage.

! 79% of banking customers with Internet access could imagine usingthe Internet for part of their banking in future.

! There is strong dissatisfaction amongst Internet users who bank withother banks - over 50% of customers of the Sparkasse, Postbank andRaiffeisenbank are unhappy with their bank’s Internet offer and 20%would start a new banking relationship and use the Internet.

! 71% of T-online users use the Internet

! 47% of Internet users who also do stock and share transactionswould use the Internet to do their banking

! 53% of Internet users who also do options transactions transactionswould use the Internet to do their banking

Existing DB customers either using theInternet or Online

! Deutsche Bank already has a relationshipwith 13% of the total Internet users - but only6.8% view Deutsche Bank as their mainbank

! Internet access varied by depth ofrelationship with Deutsche Bank -24% ofthose with any relationship, 32% of thosewho regard Deutsche Bank as their mainbank, 49% of current account holders and50% of those who do wertpapiertrasnactions. Readiness to do all theirbanking by Internet does not appear to showany significant differences by productholding.

Source: PwC analysis; Claritas;GfK

Key Results and Experiences

Competitors and Proposition

! Competitors:

" Target customers of the direct banks are clearly have a muchhigher potential for On-line Banking, both in terms of PCownership at home and willingness to bank only via theInternet.

" The direct banks show a higher penetration (than Universalbanks) of key customers who will be buying new (or replacingold) PCs - potentially a driver of On-line Banking access.

! Proposition:

" Merger another bank started to have influence in the generalselection process.

" Young, well-educated women were not being targeted, in somecases neglected with respect to their banking needs andrepresented a good recruitment opportunity. It will be the nextwave of Internet users.

Key Results and Experiences

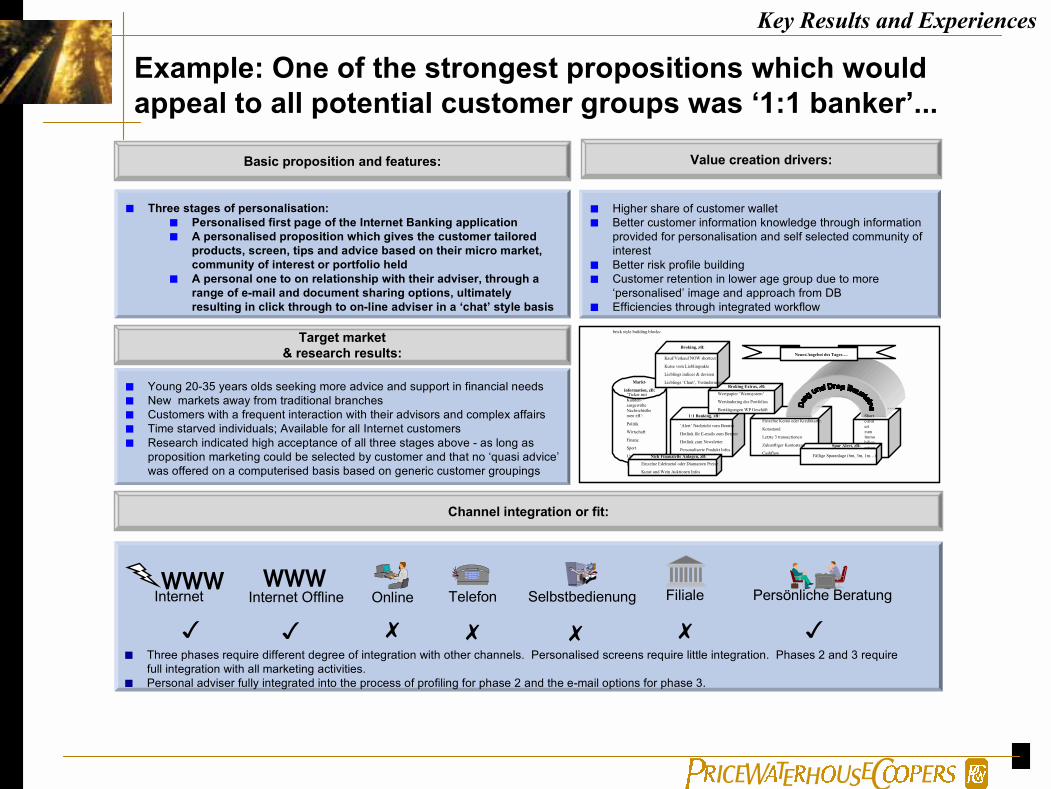

Example: One of the strongest propositions which wouldappeal to all potential customer groups was ‘1:1 banker’...

Basic proposition and features:

! Three stages of personalisation:! Personalised first page of the Internet Banking application! A personalised proposition which gives the customer tailored

products, screen, tips and advice based on their micro market,community of interest or portfolio held

! A personal one to on relationship with their adviser, through arange of e-mail and document sharing options, ultimatelyresulting in click through to on-line adviser in a ‘chat’ style basis

Value creation drivers:

! Higher share of customer wallet! Better customer information knowledge through information

provided for personalisation and self selected community ofinterest

! Better risk profile building! Customer retention in lower age group due to more

‘personalised’ image and approach from DB! Efficiencies through integrated workflow

Target market& research results:

! Young 20-35 years olds seeking more advice and support in financial needs! New markets away from traditional branches! Customers with a frequent interaction with their advisors and complex affairs! Time starved individuals; Available for all Internet customers! Research indicated high acceptance of all three stages above - as long as

proposition marketing could be selected by customer and that no ‘quasi advice’was offered on a computerised basis based on generic customer groupings

Channel integration or fit:

Internet Offline WWW

Internet WWW

Online Telefon Selbstbedienung Filiale Persönliche Beratung

! Three phases require different degree of integration with other channels. Personalised screens require little integration. Phases 2 and 3 requirefull integration with all marketing activities.

! Personal adviser fully integrated into the process of profiling for phase 2 and the e-mail options for phase 3.

$%

Kauf/Verkauf NOW shortcut

Kurse vom Lieblingsakte

Lieblings indices & devisen

Lieblings ‘Chart’, Veränderungen

Broking, zB:

Markt-

information, zB:‘Ticker mitKunden-ausgewälteNachrichtsthemen zB’:

Politik

Wirtschaft

Finanz

Sport

Unterhaltung

IT

1:1 Banking, zB:

‘Alert’ Nachricht vom Berater

Hotlink für E-mails zum Berater

Hotlink zum Newsletter

Personaliserte Produkt Infos

Wertpapier ‘Warnsystem’

Wertändering des Portfolios

Bestätigungen WP Geschäft

Broking Extras, zB:

Fällige Sparanlage (6m, 3m, 1m…)

Einzelne Konto oder Kreditkarte:

Kotostand

Letzte 3 transactionen

Zukunftiger Kontostand

Cashflow

Neues/Angebot des Tages….

Shortcut/alertzumImmobilienseitenSpar Alert, zB:

brick style building blocks:

Nich Finanzielle Anlagen, zB:Einzelne Edelmetal oder Diamanten Preise

Kunst und Wein Auktionen Infos

%$$ $%

Key Results and Experiences

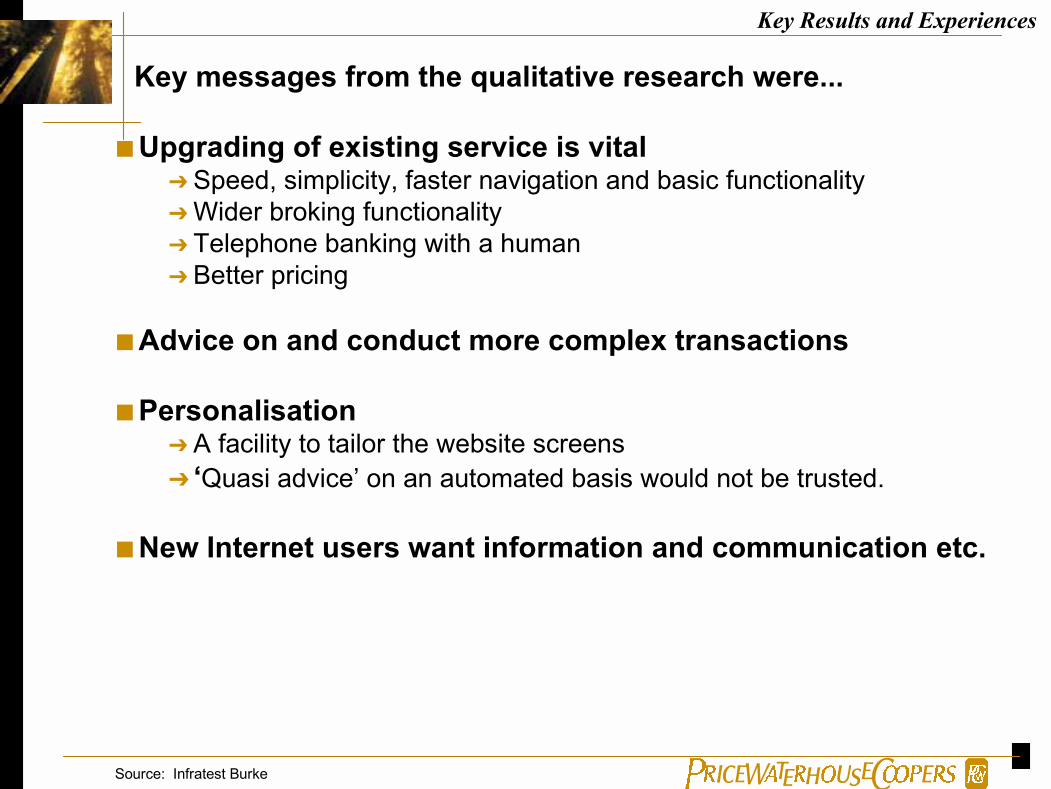

Key messages from the qualitative research were...

!Upgrading of existing service is vital# Speed, simplicity, faster navigation and basic functionality# Wider broking functionality# Telephone banking with a human# Better pricing

!Advice on and conduct more complex transactions

!Personalisation# A facility to tailor the website screens# ‘Quasi advice’ on an automated basis would not be trusted.

!New Internet users want information and communication etc.

Source: Infratest Burke

Key Results and Experiences

Key Results and Experiences

Experience

! Data Collection and Preparation costs 90% of time.

! Comment Internal Data - AGING: (1) Majority Customer details anddemographics was collected when account were opened (2) Much datanot relevant for purpose.

! Comment External Data - AGING: (1) For this subject outdated, i.e.Most records from 1997, Internet usage related questions were notcollected in the Q1/Q2 surveys in 1998 (2) Enhancement needed forgenerating Key measurement.

! Benefit Enterprise Miner - (1) for the database marketingdepartment of Deutsche Bank lies in the extensive potential for trying outdifferent models in the shortest possible time (2) and to do this atsubstantially lower programming expense than before.

Key Results and Experiences

What is finally used from this Pilot Project?

! Some results from the static segmentation - definitions like‘satisfied early users’ etc.

! Update customer data more frequently

! Target customers changed

! Personalisation website

! No implementation segmentation model, because of merger

! Possibility Enterprise Miner

Contact Information

Resi Cuypers or Harmen Ettemamob. +31 (0)6 22 46 81 80 mob. +31 (0)6 53 56 35 50email: resi.cuypers@ email: harmen.ettema@

nl.pwcglobal.com nl.pwcglobal.com

PricewaterhouseCoopers Strawinskylaan 3127 P.O. Box 7067 1007 JB Amsterdam The Netherlands fax. +31 (0)20 568 41 54

Key Results and Experiences