Embed Size (px)

Citation preview

3117

CHAPTER 5

DETERMINANTS OF CAPITAL STRUCTURE

This chapter explains the variation in the behavior of leverage caused by the

exogenous variables included in the study. The panel regression has been used for observing

the relationship among capital structure and other independent variables. Two measures of

leverage (endogenous variables) i.e., Total Debt to Total Assets and Debt-Equity Ratio have

been used to study the effect of exogenous variables on the capital structure decision.

Exogenous variables include size, growth, profitability, tangibility, age, earnings variability,

debt service capacity, dividend payout ratio, liquidity, non-debt tax shields, degree of

operating leverage, price-earnings ratio, promoter shareholdings, tax rate and uniqueness. The

study is conducted over a period of ten years from 2001-02 to 2010-11 to find out whether

the variations in determinants influence the capital structure in the selected industries. The

chapter intends to justify another objective that whether the factors affecting capital structure

significantly vary amongst the sample companies. For the purpose of analyzing the effect of

selected exogenous variables on the capital structure decision, the following regression

equations have been developed:

LR1 = b0 + b1SZ + b2GR + b3PROF + b4TANG + b5AG + b6EV + b7DSC + b8DPR + b9LIQ +

b10NDTS + b11DOL + b12P/E + b13PH + b14TR + b15UNIQ

LR2 = b0 + b1SZ + b2GR + b3PROF + b4TANG + b5AG + b6EV + b7DSC + b8DPR + b9LIQ +

b10NDTS + b11DOL + b12P/E + b13PH + b14TR + b15UNIQ

Where,

LR1 = Total Debt to Total Assets Ratio

LR2 = Debt-Equity Ratio

SZ = Size Measured in Terms of Assets

GR = Growth Measured in Terms of Assets

PROF = Profitability

TANG = Tangibility

AG = Age of Firm

EV = Earnings Variability

3118

DSC = Debt Service Capacity

DPR = Dividend Payout Ratio

LIQ = Liquidity

NDTS = Non-debt Tax Shield

DOL = Degree of Operating Leverage

P/E = Price-earnings Ratio

PH = Promoter Shareholdings

TR = Tax Rate

UNIQ = Uniqueness

The definition and measurements used for all variables have been explained in the

chapter on research methodology. This chapter has been divided into three sections. First

section uncovers the relationship among total debt to total assets with the regressors used in

this study. Second section establishes the relationship of debt-equity ratio with the

independent variables included in this study and the last sections summarizes and concludes

the results.

5.1 DETERMINANTS OF CAPITAL STRUCTURE (TOTAL DEBT TO TOTAL

ASSETS) (LR1)

This section deals with an examination of the empirical relationship of various

selected independent variables with leverage measured in terms of Total Debt to Total Assets.

The relationship has been studied with the help of panel regression. The analysis has been

done for Traditional, Modern and Combined Data. In order to know the effect of specific

industry on leverage, industry-wise analysis has been presented for selected industries in this

study. The panel regression has been run on selected industries for a period of ten years from

2001-02 to 2010-11. Variance Inflation Factor (VIF) test has been used to check the presence

of multi collinearity. It is observed from the results of VIF test that size measured in terms of

assets with size measured in terms of sales, growth measured in terms of assets with growth

measured in terms of sales and cash flow coverage ratio with debt service capacity have high

level of correlation, hence, to get the reliable results three variables, i.e., size measured in

terms of sales, growth measured in terms of assets and cash flow coverage have been dropped

from analysis. VIF results for the remaining variables have been found below the prescribed

level. Hausman’s Specification test has been used to check the suitability of model for

3119

analysis and then, on basis of significance of model, only appropriate models has been

presented here for analyzing the impact of exogenous variables on capital structure.

The panel regression analysis has been used to establish the relationship of all the

selected variables with total debt to total assets ratio for a period of ten years from 2001-02 to

2010-11 for Traditional, Modern and Combined Data and then specific analysis for different

industries included in study. First of all, the comparison has been made among Traditional

and Modern along with Combined Data and then results from all the industries selected for

this study have been discussed.

Table 5.1 presents the results of Random-effects regression for determinants of capital

structure in Traditional Industries. The model has been selected on the recommendation of

Hausman’s Specification test.

Table 5.1: Random-effects Regression Results for

Determinants of Capital Structure (Total Debt to Total Assets)

in Traditional Industries

R-sq: within = 0.1801between = 0.0075

overall = 0.0781

Number of observations = 930Number of groups = 93Wald chi2 (15) = 146.67Prob > chi2 = 0.0000

Variable Regression CoefficientsSize (Assets) -0.059 (4.72)*Growth (Assets) -0.078 (5.63)*Profitability 0.069 (0.56)Tangibility -0.245 (2.24)**Age -0.001 (1.61)Earnings Variability 0.001 (0.52)Debt Service Capacity -0.001 (0.65)Dividend Payout Ratio -0.001 (0.26)Liquidity -0.018 (2.05)**Non-debt Tax Shield 7.390 (8.10)*Degree of Operating Leverage -0.001 (0.50)Price-earnings Ratio 0.001 (0.32)Promoter Holdings -0.001 (2.08)**Tax Rate -0.034 (0.52)Uniqueness -0.006 (0.30)Cons 0.533 (6.68)Durbin-Watson Test= 1.307

** indicates significance at 5 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the z-values.

3120

Hausman’s Specification test has been used for checking the suitability of model for

interpretation. The value of Hausman’s Specification test has been found negative, hence,

null hypothesis of difference in coefficients not systematic cannot be rejected indicating the

suitability of Random-effects model for this data. VIF test has been applied to check the

presence of multi collinearity in the model, the value of which is below the level of 10 for all

the selected variables, therefore, model is free from the problem of multi collinearity. The

value of Durbin-Watson test is 1.307, indicating that there is no problem of auto correlation.

Wald chi-square is 146.67 and p-value of 0.0000 shows the validity and significance of

model. The value of R-square is .0781, indicates that the model has explained 7.81 per cent

variation in leverage. It is observed from the table that size, growth, tangibility, age, debt

service capacity, dividend payout ratio, liquidity, degree of operating leverage, promoter

shareholdings, tax rate and uniqueness have negative relationship with leverage but

statistically significant in respect of size and growth only with a z-value of 4.72 and 5.63

respectively, both with a p-value of 0.0000 which shows the significance at .01 level whereas

relation has been found statistically significant in case of tangibility, liquidity and promoter

shareholdings with z-value of 2.24, 2.05 and 2.08 respectively at .05 level. Profitability, non-

debt tax shield and price-earnings ratio have positive relation with leverage but statistically

significant in respect of non-debt tax shield only with a z-value of 8.10 at .01 level. The

negative significant relation of size, liquidity and tangibility with leverage has been

supporting the predictions of Pecking Order theory and negative relation of growth with

leverage has supporting Static Trade-off theory of capital structure.

Table 5.2 shows the Fixed-effects regression results for determinants of capital

structure in Modern Industries. The value of Hausman’s Specification test has recommended

the use of Fixed-effects regression model for the data from Modern Industries.

The value of Hausman’s Specification test is 93.90, which is statistically significant at

.01 level, therefore, rejecting the null hypothesis in favour of Fixed-effects regression model

for this data. The VIF test indicates the absence of multi collinearity in the model. The value

of F-test is 9.26 with a p-value of 0.0000 shows that model has been statistically significant.

The value of R-square (within) is 0.2870, means 28.70 per cent of variation in leverage has

been explained by the independent variables selected for the present study. The significant

negative relation of size and tangibility has supporting the predictions of Pecking Order

Theory. Age and non-debt tax shield has been positively related to leverage and relation has

been statistically significant with a t-value of 3.97 and 6.83 respectively at .01 level. The

3121

relation of growth, profitability, dividend payout ratio, price-earnings ratio, promoter

shareholdings, tax rate and uniqueness has been found positive with leverage but relation has

not been statistically significant. Earnings variability, debt service capacity, liquidity and

degree of operating leverage have negative insignificant relation with leverage.

Table 5.2: Fixed-effects Regression Results for

Determinants of Capital Structure (Total Debt to Total Assets)

in Modern Industries

R-sq: within = 0.2870between = 0.0595

overall = 0.0353

Number of observations = 400Number of groups = 40F (15,345) = 9.26Prob > F = 0.0000

Variable Regression CoefficientsSize (Assets) -1.222 (5.30)*Growth (Assets) 0.013 (0.21)Profitability 1.047 (1.42)Tangibility -1.878 (3.50)*Age 0.154 (3.97)*Earnings Variability -0.001 (1.31)Debt Service Capacity -0.001 (0.23)Dividend Payout Ratio 0.032 (1.12)Liquidity -0.001 (0.01)Non-debt Tax Shield 21.016 (6.83)*Degree of Operating Leverage -0.001 (0.42)Price-earnings Ratio 0.001 (0.39)Promoter Holdings 1.110 (1.58)Tax Rate 0.362 (0.68)Uniqueness 0.029 (0.17)Cons 2.136 (2.94)Durbin-Watson Test= 0.911

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the t-values.

Table 5.3 shows the Random-effects regression results for determinants of capital

structure for Combined Data. The value of Hausman’s Specification test has recommended

the use of Random-effects regression model for Combined Data from all the industries

included in the sample.

The value of Hausman’s Specification test is -2118.49, supporting the non rejection of

null hypothesis. Therefore, Random-effects model has been considered appropriate for

interpretation. The value of VIF test for all variables is less than 1.39, indicating absence of

multi collinearity in model. The value of Durbin-Watson test is 1.021, which is within the

3122

range of 1 to 3. Wald chi-square test has been used for checking the significance of model.

The value of Wald test is 138.40, which is statistically significant at .01 level. The model has

explained 8.45 per cent variation in leverage with the help of selected independent variables.

It is observed from the table that non-debt tax shield, dividend payout ratio, price-earnings

ratio, tax rate and uniqueness have positive relation with leverage whereas all other selected

variables have negative relation with leverage. But the relation has been statistically

significant in case of size, tangibility and non-debt tax shield with a z-value of 3.24, 3.64 and

9.81 respectively at .01 level and in case of liquidity with a z-value of 2.58 at .05 level. The

significant negative relation of size, tangibility and liquidity with leverage is supporting

Pecking Order Theory.

Table 5.3: Random-effects Regression Results for

Determinants of Capital Structure (Total Debt to Total Assets)

for Combined Data

R-sq: within = 0.1721between = 0.0143

overall = 0.0845

Number of observations = 1330Number of groups = 133Wald chi2 (15) = 138.40Prob > chi2 = 0.0000

Variable Regression CoefficientsSize (Assets) -0.110 (3.24)*Growth (Assets) -0.011 (0.37)Profitability -0.087 (0.42)Tangibility -0.502 (3.64)*Age -0.001 (1.26)Earnings Variability -0.001 (0.33)Debt Service Capacity -0.001 (1.24)Dividend Payout Ratio 0.001 (0.21)Liquidity -0.034 (2.58)**Non-debt Tax Shield 10.132 (9.81)*Degree of Operating Leverage -0.001 (0.30)Price-earnings Ratio 0.001 (0.85)Promoter Holdings -0.001 (1.61)Tax Rate 0.148 (1.20)Uniqueness 0.006 (0.14)Cons -0.110 (3.24)Durbin-Watson Test= 1.021

** indicates significance at 5 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the z-values.

3123

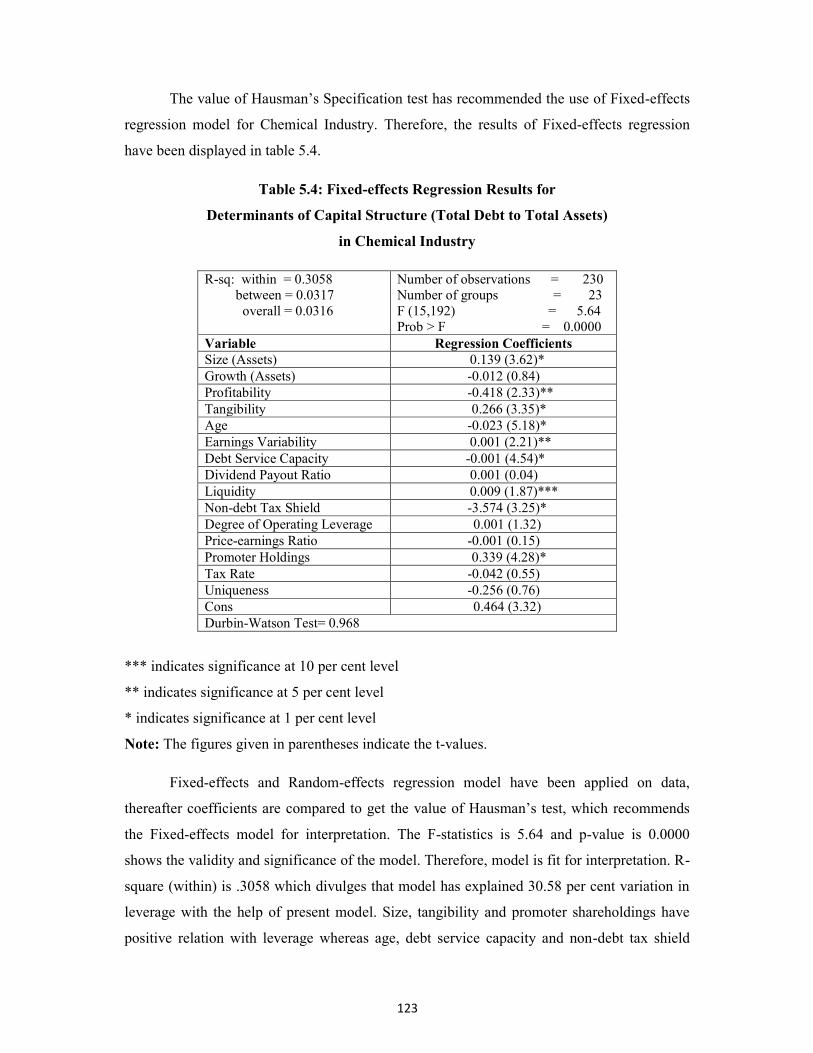

The value of Hausman’s Specification test has recommended the use of Fixed-effects

regression model for Chemical Industry. Therefore, the results of Fixed-effects regression

have been displayed in table 5.4.

Table 5.4: Fixed-effects Regression Results for

Determinants of Capital Structure (Total Debt to Total Assets)

in Chemical Industry

R-sq: within = 0.3058between = 0.0317

overall = 0.0316

Number of observations = 230Number of groups = 23F (15,192) = 5.64Prob > F = 0.0000

Variable Regression CoefficientsSize (Assets) 0.139 (3.62)*Growth (Assets) -0.012 (0.84)Profitability -0.418 (2.33)**Tangibility 0.266 (3.35)*Age -0.023 (5.18)*Earnings Variability 0.001 (2.21)**Debt Service Capacity -0.001 (4.54)*Dividend Payout Ratio 0.001 (0.04)Liquidity 0.009 (1.87)***Non-debt Tax Shield -3.574 (3.25)*Degree of Operating Leverage 0.001 (1.32)Price-earnings Ratio -0.001 (0.15)Promoter Holdings 0.339 (4.28)*Tax Rate -0.042 (0.55)Uniqueness -0.256 (0.76)Cons 0.464 (3.32)Durbin-Watson Test= 0.968

*** indicates significance at 10 per cent level

** indicates significance at 5 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the t-values.

Fixed-effects and Random-effects regression model have been applied on data,

thereafter coefficients are compared to get the value of Hausman’s test, which recommends

the Fixed-effects model for interpretation. The F-statistics is 5.64 and p-value is 0.0000

shows the validity and significance of the model. Therefore, model is fit for interpretation. R-

square (within) is .3058 which divulges that model has explained 30.58 per cent variation in

leverage with the help of present model. Size, tangibility and promoter shareholdings have

positive relation with leverage whereas age, debt service capacity and non-debt tax shield

3124

have negative relation with leverage. The p-value for all these variables is less than 0.001

which shows that all above relations has been found statistically significant at .01 level.

Earnings variability and liquidity have direct relation with leverage and relation has been

statistically significant with t-value of 2.21 and 1.87 at .05 and .10 level respectively.

Profitability has a reverse relationship with leverage. Profitability has a t-statistics of -2.33

with a p-value of 0.021 which indicates that the relationship between leverage and

profitability has been statistically significant at .05 level. All the remaining variables

included in the present study have turned out to be statistically insignificant for determining

capital structure in Chemical Industry.

Table 5.5: Fixed-effects Regression Results for

Determinants of Capital Structure (Total Debt to Total Assets)

in Drugs & Pharmaceutical Industry

R-sq: within = 0.2658between = 0.4846

overall = 0.4115

Number of observations = 310Number of groups = 31F (15,264) = 6.37Prob > F = 0.0000

Variable Regression CoefficientsSize (Assets) 0.106 (1.77)***Growth (Assets) 0.017 (0.71)Profitability -0.504 (4.70)*Tangibility 0.071 (0.86)Age -0.010 (1.94)***Earnings Variability -0.001 (0.48)Debt Service Capacity -0.001 (0.02)Dividend Payout Ratio -0.010 (0.60)Liquidity 0.017 (2.00)**Non-debt Tax Shield -1.454 (1.87)***Degree of Operating Leverage 0.001 (0.93)Price-earnings Ratio 0.001 (0.45)Promoter Holdings 0.241 (2.44)**Tax Rate 0.142 (2.39)**Uniqueness -0.773 (2.79)*Cons 0.137 (1.01)Durbin-Watson Test= 0.895

*** indicates significance at 10 per cent level

** indicates significance at 5 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the t-values.

3125

Table 5.5 shows the Fixed-effects regression results for determinants of capital

structure in Drugs & Pharmaceutical Industry. The value of Hausman’s Specification test has

recommended the use of Fixed-effects regression model for Drugs & Pharmaceutical

Industry.

The results of Hausman’s test have supported the Fixed-effects model for available

data from Drugs & Pharmaceutical Industry. The F-statistics is 6.37 and p-value is 0.0000

which shows that model is statistically significant. The model has explained 26.58 per cent of

variation in leverage by any variation in independent variables taking place within firms. The

relation of size with leverage has been found positive and statistically significant with a t-

value of 1.77 at .10 level. This relation supports the prediction of Static Trade-off theory. The

beta coefficient of profitability is -0.5044 revealing that with one unit of change in

profitability, the leverage has been decreased by 0.5044 units. Profitability has a t-statistics of

4.70 with p-value of 0.0000 which indicates that the relationship between leverage and

profitability has been found statistically significant at .01 level. The relationship of age and

non-debt tax shield has been found to be negative and statistically significant at .10 level. The

table demonstrates the relationship of uniqueness with leverage as negative and statistically

significant at .01 level. The relationship of liquidity, promoter shareholdings and tax rate has

been found to be positive with leverage and statistically significant at .05 level. All other

variables have turned out to be statistically insignificant for determining the capital structure

in Drug & Pharmaceutical Industry.

Table 5.6 gives an idea about the determinants of capital structure in Fertilizer

Industry. The Hausman’s Specification test has recommended the use of Fixed-effects

regression model in Fertilizer Industry. Therefore, the results of Fixed-effects regression for

Fertilizer Industry have been exhibited in the table.

Hausman’s Specification test has been applied for selection of appropriate model for

available data from Fertilizer Industry. The null hypothesis of Hausman’s Specification test,

i.e., “differences in coefficients not systematic” is rejected, thus, advocating the use of Fixed-

effects model. The F-statistics is 7.35 with a p-value of 0.0000 which shows the validity and

significance of model. The value of Durbin-Watson test is 1.403 indicates that the auto

correlation is not a problem for this model. The model explains 62.56 per cent of variation in

leverage has been due to change in independent variables over time for a given company. The

table reveals that the profitability has negative beta coefficient with p-value of 0.016

3126

indicating that negative relation among leverage and profitability has been statistically

significant at .05 level. The relation of tangibility and earnings variability with leverage has

been found to be positive and statistically significant at .01 and .05 level respectively. Debt

service capacity and non-debt tax shield have negative relations with leverage and t-value of -

4.40 and -3.60 is statistically significant at .01 level. Promoter shareholding has negative

relation with leverage and relation with a t-value of -1.97 is statistically significant at .10

level. The relations of size, age, liquidity, degree of operating leverage and price-earnings

ratio with leverage have been found negative whereas growth, dividend payout ratio, tax rate

and uniqueness have positive relation with leverage but these relations has not been

statistically significant. Therefore, it can be stated that these variables has not played an

important role in determining the capital structure in Fertilizer Industry.

Table 5.6: Fixed-effects Regression Results for

Determinants of Capital Structure (Total Debt to Total Assets)

in Fertilizer Industry

R-sq: within = 0.6256between = 0.4326

overall = 0.4875

Number of observations = 90Number of groups = 9F (15,66) = 7.35Prob > F = 0.0000

Variable Regression CoefficientsSize (Assets) -0.097 (1.48)Growth (Assets) 0.018 (0.62)Profitability -0.685 (2.46)**Tangibility 0.487 (3.04)*Age -0.001 (0.42)Earnings Variability 0.001 (2.65)**Debt Service Capacity -0.004 (4.40)*Dividend Payout Ratio 0.002 (0.08)Liquidity -0.046 (1.34)Non-debt Tax Shield -7.044 (3.60)*Degree of Operating Leverage -0.001 (1.06)Price-earnings Ratio -0.001 (0.49)Promoter Holdings -0.003 (1.97)***Tax Rate 0.037 (0.40)Uniqueness 0.573 (1.16)Cons 1.122 (2.79)Durbin-Watson Test= 1.403

*** indicates significance at 10 per cent level

** indicates significance at 5 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the t-values.

3127

Table 5.7 shows the Random-effects regression results for determinants of capital

structure in Iron & Steel Industry. The value of Hausman’s Specification test has

recommended the use of Random-effects regression model in Iron & Steel Industry.

Table 5.7: Random-effects Regression Results for

Determinants of Capital Structure (Total Debt to Total Assets)

in Iron & Steel Industry

R-sq: within = 0.4259between = 0.7854

overall = 0.5616

Number of observations = 210Number of groups = 21Wald chi2 (15) = 248.54Prob > chi2 = 0.0000

Variable Regression CoefficientsSize (Assets) -0.046 (2.43)**Growth (Assets) 0.046 (1.33)Profitability -0.599 (3.04)*Tangibility -0.256 (2.06)**Age -0.002 (2.32)**Earnings Variability 0.001 (1.04)Debt Service Capacity -0.001 (2.61)*Dividend Payout Ratio -0.077 (0.79)Liquidity -0.008 (0.49)Non-debt Tax Shield 12.607 (10.55)*Degree of Operating Leverage -0.002 (3.20)*Price-earnings Ratio 0.001 (1.32)Promoter Holdings 0.084 (0.93)Tax Rate -0.007 (0.13)Uniqueness -0.151 (0.41)Cons 0.476 (4.32)Durbin-Watson Test= 0.747

** indicates significance at 5 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the z-values.

Hausman’s Specification test has been applied to check the appropriateness of model

and VIF test has been applied to check the multi collinearity among independent variables.

The value of VIF for all independent variables has been found below 5, hence, there should

not be any problem of multi collinearity in model. Hausman’s test has recommended the

Random-effects model for data from Iron & Steel Industry. It is demonstrated through R-

square (overall) in the table that 56.16 per cent of variation in capital structure has been

explained by model. The relation of size, tangibility and age with leverage has been found to

be negative and statistically significant at .05 level whereas negative relation of profitability,

3128

debt service capacity and degree of operating leverage with leverage has been statistically

significant at .01 level. All these relations are consistent with the predictions of Pecking

Order theory. The relation of non-debt tax shield with leverage has been found to be positive

and z-value of 10.55 with a p-value 0.0000 shows that relation is statistically significant at

.01 level. All other variables have been found statistically insignificant in determining the

capital structure in Iron & Steel Industry during study period.

Table 5.8 presents the Random-effects regression results for determinants of capital

structure in Computer & IT Industry. The value of Hausman’s Specification test has

recommended the use of Random-effects regression model for the data from Computer & IT

Industry.

Table 5.8: Random-effects Regression Results for

Determinants of Capital Structure (Total Debt to Total Assets)

in Computer & IT Industry

R-sq: within = 0.4482between = 0.2691

overall = 0.4057

Number of observations = 230Number of groups = 23Wald chi2 (15) = 146.09Prob > chi2 = 0.0000

Variable Regression CoefficientsSize (Assets) -0.545 (3.19)*Growth (Assets) 0.001 (0.20)Profitability 0.481 (0.55)Tangibility -7.170 (8.40)*Age 0.001 (0.19)Earnings Variability 0.001 (0.18)Debt Service Capacity -0.001 (0.81)Dividend Payout Ratio 0.144 (2.75)*Liquidity -0.052 (1.37)Non-debt Tax Shield 35.059 (8.51)*Degree of Operating Leverage -0.001 (0.75)Price-earnings Ratio 0.001 (3.54)*Promoter Holdings 0.381 (0.64)Tax Rate -0.294 (0.33)Uniqueness -1.175 (0.36)Cons 2.066 (2.68)Durbin-Watson Test= 0.997

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the z-values.

The value of Hausman’s Specification test is 9.62 with a p-value of 0.5651 which fails

to reject the null hypothesis. Therefore, Random-effects model has been considered

3129

appropriate for Computer & IT Industry. The value of Wald chi-square test has been

statistically significant at .01 level specifying the validity and robustness of model. The VIF

values are below 3 revealing absence of multi collinearity among regressors used in present

model. Durbin-Watson value is very close to 1 indicating auto correlation is within limits.

The beta coefficient for size displays negative relation with leverage and tangibility has also

been showing negative sign of relation with leverage. The relation of size and tangibility has

been found statistically significant at .01 level supporting the predictions of Pecking Order

theory. The relationship of dividend payout ratio, non-debt tax shield and price-earnings ratio

with leverage has been found to be positive and t-values of 2.75, 8.51 and 3.54 with p-values

of 0.0000 shows that these relations are statistically significant at .01 level. Growth,

profitability, age, earnings variability and promoter shareholdings has been found to be

positively related to leverage whereas debt service capacity, liquidity, degree of operating

leverage, tax rate and uniqueness has been found to be negatively related with leverage but all

these relations has not been statistically significant.

Table 5.9 shows the Random-effects regression results for determinants of capital

structure in Media & Entertainment Industry. The value of Hausman’s Specification test has

recommended the use of Random-effects regression model in Media & Entertainment

Industry.

The negative value for Hausman’s Specification test did not reject the null hypothesis,

therefore, Random-effects model has been considered appropriate for Media & Entertainment

Industry. Thus, Random-effects regression results have been exhibited in the table. VIF

values for all regressors are below 4 which points out the absence of multi collinearity in

model. The Durbin-Watson test value is 1.13 which specifies that the auto correlation is

within limits. The relation of size has been found to be positive with leverage and p-value of

0.044 shows that relation has been statistically significant at .05 level. The relation of size

with leverage has supported the expectations of Static Trade-off theory. The significant

negative relation of age with leverage has been supporting the predictions of Pecking Order

theory. Earnings variability has negative relation with leverage as expected by Static Trade-

off and Pecking Order theory. Firms with greater variability in their earnings prefer lesser

amount of debt in their capital structure, as it will be difficult for them to pay fixed amount of

interest and principal repayments with unstable earnings. The relations of dividend payout

ratio and promoter shareholdings with leverage have been found to be negative and

statistically significant at .10 level. Other regressors included in the study have not been

3130

statistically significant for determining the capital structure of Media & Entertainment

Industry.

Table 5.9: Random-effects Regression Results for

Determinants of Capital Structure (Total Debt to Total Assets)

in Media & Entertainment Industry

R-sq: within = 0.3303between = 0.1911

overall = 0.2876

Number of observations = 90Number of groups = 9Wald chi2 (15) = 29.87Prob > chi2 = 0.0124

Variable Regression CoefficientsSize (Assets) 0.093 (2.01)**Growth (Assets) 0.001 (0.35)Profitability 0.078 (0.36)Tangibility 0.159 (1.14)Age -0.005 (2.04)**Earnings Variability -0.001 (3.00)*Debt Service Capacity 0.001 (0.25)Dividend Payout Ratio -0.001 (1.71)***Liquidity -0.028 (1.33)Non-debt Tax Shield 0.529 (0.66)Degree of Operating Leverage -0.001 (0.59)Price-earnings Ratio -0.001 (0.22)Promoter Holdings -0.004 (1.96)***Tax Rate -0.194 (1.24)Uniqueness -0.012 (0.09)Cons 0.217 (1.02)Durbin-Watson Test= 1.130

*** indicates significance at 10 per cent level

** indicates significance at 5 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the z-values.

Table 5.10 throws a light on the determinants of capital structure in

Telecommunication Industry. The value of Hausman’s Specification test has recommended

the use of Fixed-effects regression model for Telecommunication Industry.

The value of Hausman’s Specification test is 131.23 and p-value is 0.0000 which

rejects the null hypothesis in favour of Fixed-effects model as appropriate for

Telecommunication Industry. Therefore, results of Fixed-effects regression model have been

displayed in the table for interpretation. The F-statistics is 5.39 and p-value is 0.0000 which

3131

Table 5.10: Fixed-effects Regression Results for

Determinants of Capital Structure (Total Debt to Total Assets)

in Telecommunication Industry

R-sq: within = 0.6274between = 0.0133

overall = 0.0813

Number of observations = 70Number of groups = 7F (15,48) = 5.39Prob > F = 0.0000

Variable Regression CoefficientsSize (Assets) 0.271 (4.20)*Growth (Assets) 0.055 (1.43)Profitability 0.532 (1.57)Tangibility -0.216 (1.40)Age -0.017 (1.96)***Earnings Variability -0.001 (4.67)*Debt Service Capacity -0.001 (0.73)Dividend Payout Ratio 0.014 (0.42)Liquidity -0.021 (1.85)***Non-debt Tax Shield 2.692 (2.87)*Degree of Operating Leverage -0.001 (0.44)Price-earnings Ratio -0.001 (1.51)Promoter Holdings 1.153 (3.91)*Tax Rate -0.108 (0.64)Uniqueness 0.026 (1.36)Cons -1.430 (5.48)Durbin-Watson Test= 1.526

*** indicates significance at 10 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the t-values.

shows that the model is statistically significant at .01 level. VIF values for all regressors has

been found less than 10, thus, multi collinearity is not a problem for this model. The value of

Durbin-Watson is 1.52 which points out that the model is not suffering from auto correlation.

The relation of size with leverage has been consistent with Static Trade-off theory which

indicates that size of the firm has been positively related to debt financing because the direct

bankruptcy cost is well diversified in large firms. The negative relation of age with debt

financing has been found consistent with the Pecking Order theory. Earnings variability has

been found to be negatively related to leverage as per the expectations of Static Trade-off and

Pecking Order theory. The relationship among liquidity and leverage has been found to be

negative and statistically significant at .10 level. The table reveals positive relation of non-

debt tax shield and promoter shareholdings with leverage and relation has been statistically

3132

significant at .01 level. All the remaining regressors have turned out to be statistically

insignificant in determining capital structure in Telecommunication Industry.

Table 5.11 shows the Fixed-effects regression results for determinants of capital

structure in Transport Industry. The value of Hausman’s Specification test has recommended

this model.

Table 5.11: Fixed-effects Regression Results for

Determinants of Capital Structure (Total Debt to Total Assets)

in Transport Industry

R-sq: within = 0.4273between = 0.2670

overall = 0.2864

Number of observations = 100Number of groups = 10F (15,75) = 3.73Prob > F = 0.0001

Variable Regression CoefficientsSize (Assets) 0.135 (3.12)*Growth (Assets) -0.003 (0.44)Profitability -0.325 (1.85)***Tangibility 0.206 (1.31)Age -0.032 (3.60)*Earnings Variability -0.001 (2.07)**Debt Service Capacity 0.001 (0.25)Dividend Payout Ratio 0.003 (0.59)Liquidity -0.008 (0.73)Non-debt Tax Shield 0.347 (0.44)Degree of Operating Leverage 0.001 (0.67)Price-earnings Ratio -0.001 (0.94)Promoter Holdings -0.023 (0.17)Tax Rate -0.108 (0.92)Uniqueness -0.002 (0.26)Cons 0.301 (1.73)Durbin-Watson Test= 1.292

*** indicates significance at 10 per cent level

** indicates significance at 5 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the t-values.

The Fixed-effects model has been selected on the basis of output produced by

Hausman’s Specification test. Therefore, results of Fixed-effects regression model have been

presented in table for interpretation. VIF test results indicate absence of multi collinearity in

model and Durbin-Watson test discloses that model is free from auto correlation. The F-

statistics is 3.73 and p-value is 0.0001 which shows the validity and significance of model.

3133

The model has explained 42.73 per cent of variation in leverage due to variation in

independent variables within the firms over the period of study. The relation of size has been

found to be positive with leverage and statistically significant at .01 level. The relation of

size with leverage has been found consistent with expectations of Static Trade-off theory. The

beta coefficient for profitability discloses that with a unit change in profitability, leverage will

decline by 0.3250 units. The t-value for profitability is -1.85 with a p-value of 0.068 specifies

that relation has been statistically significant at .10 level. Negative relation of profitability

with leverage has supported the predictions of Pecking Order theory. According to this

theory, highly profitable firms use internal funds for financing and use debt if need arises.

Hence, Pecking Order theory expects negative relation of profitability with leverage. Age has

negative relation with leverage and relation has been found statistically significant at .01

level. Mature firms have sufficient funds to meet their financial requirements, hence, negative

relation has been expected between age and leverage as per Pecking Order theory. Earnings

variability also has negative relation with leverage and p-value of 0.042 indicating that

relation has been statistically significant at .05 level. All other regressors have turned out to

be statistically insignificant for determining the capital structure in Transport Industry.

5.2 DETERMINANTS OF CAPITAL STRUCTURE (DEBT-EQUITY RATIO)

(LR2)

This section explains the empirical relationship of various selected independent

variables with leverage measured in terms of debt-equity ratio. The Fixed-effects and

Random-effects regression for panel data has been used for establishing relationship among

leverage and regressors. The analysis has been done for Traditional, Modern and Combined

Data, thereafter, industry-wise analysis has been presented for industries selected in this

study. The panel regression has been run on selected industries for a period of ten years from

2001-02 to 2010-11. Variance Inflation Factor (VIF) test has been used to check the presence

of multi collinearity. VIF results for the regressors used in this model have been found below

the prescribed level. Hausman’s Specification test has been used to check the suitability of

model for analysis and then on basis of significance of model, only appropriate models have

been presented here for analyzing the impact of exogenous variables on capital structure.

Hausman’s Specification test has been applied to check the suitability of model for

Traditional Industries. The results of Hausman’s test favours the use of Fixed-effects

3134

regression model, therefore, the Fixed-effects regression results for Traditional Industries has

been exhibited in table 5.12.

Table 5.12: Fixed-effects Regression Results for

Determinants of Capital Structure (Debt-equity Ratio)

in Traditional Industries

R-sq: within = 0.0440Between = 0.0075overall = 0.0002

Number of observations = 930Number of groups = 93F (15,822) = 2.52Prob > F = 0.0012

Variable Regression CoefficientsSize (Assets) -0.158 (2.68)*Growth (Assets) 0.067 (0.66)Profitability 0.534 (0.94)Tangibility 0.214 (0.40)Age -0.002 (0.75)Earnings Variability -0.001 (3.79)*Debt Service Capacity -0.001 (0.23)Dividend Payout Ratio -0.001 (1.19)Liquidity 0.024 (0.63)Non-debt Tax Shield -3.198 (0.76)Degree of Operating Leverage -0.001 (0.06)Price-earnings Ratio 0.001 (1.82)***Promoter Holdings 0.023 (1.48)Tax Rate -0.128 (0.47)Uniqueness -0.148 (1.80)***Cons 0.666 (1.51)Durbin-Watson Test= 1.558

*** indicates significance at 10 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the t-values.

The F-statistics is 2.52 and p-value is 0.0012 which signifies that model is statistically

significant at .01 level. The table shows that the Durbin-Watson test value is 1.55 which is

within permissible range of 1 to 3, therefore, auto correlation can not be a problem for this

model. VIF test indicates that multi collinearity is not causing any problem. The value of R-

square (within) displays that 4.40 per cent of variation in leverage has been explained due to

variation in independent variables within the firms during time period covered in present

study. The relation of size with leverage has been found to be negative and t-value is 2.68

with p-value 0.008 signify that the relation has been statistically significant at .01 level

supporting the Pecking Order theory. The negative relation of earnings variability with

leverage has been found statistically significant and as per the expectations of Static Trade-

3135

off and Pecking Order theory. The relation of price-earnings ratio with leverage has been

found positive and statistically significant at .10 level. The negative relation of uniqueness

with leverage has been found negative and statistically significant at .10 level and consistent

with the expectations of Static Trade-off theory. The relation of all other independent

variables included in this study with leverage has not been statistically significant.

Hausman’s Specification test has been applied to check the suitability of model and

the value of Hausman’s Specification test has recommended the use of Fixed-effects

regression model for the data from Modern Industries. Therefore, Fixed-effects regression

results for determinants of capital structure in Modern Industries have been exhibited in table

5.13.

Table 5.13: Fixed-effects Regression Results for

Determinants of Capital Structure (Debt-equity Ratio)

in Modern Industries

R-sq: within = 0.1641between = 0.0789

overall = 0.0040

Number of observations = 400Number of groups = 40F (15,345) = 4.51Prob > F = 0.0000

Variable Regression CoefficientsSize (Assets) -2.848 (4.57)*Growth (Assets) -0.115 (0.65)Profitability -1.849 (0.93)Tangibility 2.583 (1.78)***Age 0.374 (3.55)*Earnings Variability -0.001 (2.11)**Debt Service Capacity 0.001 (0.18)Dividend Payout Ratio 0.167 (2.11)**Liquidity -0.068 (0.61)Non-debt Tax Shield 20.629 (2.48)**Degree of Operating Leverage -0.001 (0.70)Price-earnings Ratio -0.001 (1.22)Promoter Holdings 3.399 (1.79)***Tax Rate -1.828 (1.26)Uniqueness -0.085 (0.19)Cons 4.797 (2.43)Durbin-Watson Test= 0.925

*** indicates significance at 10 per cent level

** indicates significance at 5 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the t-values.

3136

The value of Hausman’s test is 39.99 with a p-value of 0.0000 which supports the

rejection of null hypothesis in favour of Fixed-effects regression model. The F-statistics is

4.51 with a p-value of 0.0000 which signifies the validity of model. The model has explained

16.41 per cent of variation in leverage due to change in independent variables within a

company over time. The relation of size with leverage has been found to be negative and

statistically significant at .01 level as consistent with Pecking Order theory. The tangibility

has a positive sign of polarity with leverage and relation has been found statistically

significant at .10 level as consistent with the expectations of Static Trade-off theory. The beta

coefficient for tangibility is 2.58 which shows that with a unit change in tangibility, the

leverage has been increased by 2.58 units. The relation of earnings variability with leverage

has been found negative and p-value 0.036 indicates that the relation has been statistically

significant at .05 level. This negative relation between earnings variability and leverage has

been expected by most of researcher and consistent with Pecking Order and Static Trade-off

theory. Dividend payout ratio and non-debt tax shield have been found to be positively

related with leverage and relation has been statistically significant at .05 level. Promoter

shareholdings have positive relation with leverage and relation has been statistically

significant at .10 level. The relation of all other independent variables with leverage has not

been statistically significant, therefore, these variables have not been considered important in

determining the capital structure in Modern Industries.

Table 5.14 shows the Fixed-effects regression results for determinants of capital

structure in Combined Data from all the industries included in sample. The value of

Hausman’s Specification test has recommended the use of Fixed-effects regression model for

this particular data.

The value of Hausman’s Specification test is 37.99 and p-value of 0.0001 signifies the

rejection of null hypothesis in favour of Fixed-effects model for Combined Data of industries

included in the present study. Therefore, results of Fixed-effects regression model have been

presented for interpretation. The value of Durbin-Watson test is 2.44 which reveal that model

is not sufferings from auto correlation. The value of VIF for all regressors is below 10

indicating that multi collinearity is within control. It is revealed from the table that debt

service capacity, non-debt tax shield, price-earnings ratio and promoter shareholdings have

positive relation with leverage whereas all other variables have shown negative relation. The

negative relation of growth with leverage has been statistically significant at .10 level and

consistent with the Static Trade-off theory and complex version of Pecking Order theory. The

3137

non-debt tax shield has been found to be positively related to leverage contradicting the

predictions of Static Trade-off theory. Except these two variables no other variable has been

found to be statistically significant to determine the capital structure for Combined Data from

all the industries included in sample.

Table 5.14: Fixed-effects Regression Results for

Determinants of Capital Structure (Debt-equity Ratio)

in Combined Industries

R-sq: within = 0.0343between = 0.0102

overall = 0.0057

Number of observations = 1330Number of groups = 133F (15,1182) = 2.80Prob > F = 0.0003

Variable Regression CoefficientsSize (Assets) -0.364 (1.19)Growth (Assets) -0.346 (1.90)***Profitability -0.311 (0.21)Tangibility -0.309 (0.26)Age -0.001 (0.01)Earnings Variability -0.001 (0.84)Debt Service Capacity 0.001 (0.19)Dividend Payout Ratio -0.001 (0.05)Liquidity -0.028 (0.30)Non-debt Tax Shield 34.695 (4.25)*Degree of Operating Leverage -0.001 (0.51)Price-earnings Ratio 0.001 (0.74)Promoter Holdings 0.011 (0.32)Tax Rate -0.625 (0.80)Uniqueness -0.216 (0.89)Cons 1.576 (1.02)Durbin-Watson Test= 2.449

*** indicates significance at 10 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the t-values.

Table 5.15 shows the Fixed-effects regression results for determinants of capital

structure in Chemical Industry. The value of Hausman’s Specification test has recommended

the use of Fixed-effects regression model for the data from Chemical Industry.

The Fixed-effects regression model has been selected on the basis of Hausman’s

Specification test, whose value is 51.37 and p-value is small enough to reject the null

hypothesis. The r ejection of null hypothesis favours Fixed-effects model over Random-

3138

Table 5.15: Fixed-effects Regression Results for

Determinants of Capital Structure (Debt-equity Ratio)

in Chemical Industry

R-sq: within = 0.2918between = 0.0245

overall = 0.0257

Number of observations = 230Number of groups = 23F (15,192) = 5.27Prob > F = 0.0000

Variable Regression CoefficientsSize (Assets) 0.368 (1.67)***Growth (Assets) 0.031 (0.36)Profitability -2.497 (2.44)**Tangibility 1.696 (3.74)*Age -0.104 (3.97)*Earnings Variability 0.001 (1.47)Debt Service Capacity -0.003 (3.17)*Dividend Payout Ratio -0.028 (0.58)Liquidity 0.050 (1.71)***Non-debt Tax Shield -24.546 (3.91)*Degree of Operating Leverage 0.001 (0.85)Price-earnings Ratio 0.001 (0.46)Promoter Holdings 2.179 (4.81)*Tax Rate 0.160 (0.36)Uniqueness -1.011 (0.53)Cons 2.205 (2.77)Durbin-Watson Test= 0.947

*** indicates significance at 10 per cent level

** indicates significance at 5 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the t-values.

effects model. Therefore, Fixed-effects model has been exhibited in the table for

interpretation. The F-statistics is 5.27 and p-value of 0.0000 which discloses that model is

significant and fit for interpretation. The model explains 29.18 per cent of variation in

leverage due to change in independent variables within companies over the time period

selected for present study. The relation of size has been found to be positive with leverage

and t-value is 1.67 with a p-value 0.096 which shows that relation has been statistically

significant at .10 level. Profitability has been negatively related to leverage and relation has

been statistically significant at .05 level. Age, debt service capacity and non-debt tax shield

have been found to be negatively related to leverage and relations have been statistically

significant at .01 level. The relation of tangibility and promoter shareholdings with leverage

has been found to be positive and statistically significant at .01 level. The study has observed

3139

positive sign of coefficient for liquidity and p-value of 0.089 shows that relation has been

statistically significant at .10 level. All other regressors included in model have been found to

be statistically insignificant for determining the capital structure in Chemical Industry.

The value of Hausman’s Specification test is 11.39 and p-value is .4962 which is not

small enough to reject the null hypothesis. Therefore, Random-effects model has been

considered appropriate for Drugs & Pharmaceutical Industry and presented for interpretation

in table 5.16.

Table 5.16 Random-effects Regression Results for

Determinants of Capital Structure (Debt-equity Ratio)

in Drugs & Pharmaceutical Industry

R-sq: within = 0.2024between = 0.6479

overall = 0.4654

Number of observations = 310Number of groups = 31Wald chi2 (15) = 115.13Prob > chi2 = 0.0000

Variable Regression CoefficientsSize (Assets) 0.031 (0.28)Growth (Assets) 0.175 (1.50)Profitability -3.149 (6.16)*Tangibility 0.233 (0.65)Age -0.011 (3.44)*Earnings Variability 0.001 (0.86)Debt Service Capacity -0.001 (0.18)Dividend Payout Ratio -0.088 (1.01)Liquidity -0.015 (0.36)Non-debt Tax Shield -4.726 (1.29)Degree of Operating Leverage 0.001 (1.09)Price-earnings Ratio -0.001 (0.63)Promoter Holdings 0.136 (0.43)Tax Rate 0.507 (1.74)***Uniqueness -3.291 (3.01)*Cons 1.588 (2.72)Durbin-Watson Test= 0.964

*** indicates significance at 10 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the z-values.

The value of Wald chi square test is significant at .01 level, which advocates the

validity and significance of model. It is observed from the table that 46.54 per cent of

variation has been explained by this model. The relation of profitability and age has been

found to be negatively related to leverage and statistically significant at .01 level. These

3140

relations are consistent with expectations of Pecking Order theory. Tax rate has been found to

be positively related to leverage whereas uniqueness has been negatively related to leverage

and statistically significant at .10 and .01 level respectively. These results have been

consistent with predictions of Static Trade-off theory. All other independent variables

included in the study turn out to be insignificant for determining the capital structure in Drugs

& Pharmaceutical Industry.

The value of Hausman’s Specification test has recommended the use of Random-

effects regression model for Fertilizer Industry. Therefore, Random-effects regression results

for determinants of capital structure in Fertilizer Industry have been exhibited in Table 5.17.

Table 5.17: Random-effects Regression Results for

Determinants of Capital Structure (Debt-equity Ratio)

in Fertilizer Industry

R-sq: within = 0.5185between = 0.8312

overall = 0.5855

Number of observations = 90Number of groups = 9Wald chi2 (15) = 104.54Prob > chi2 = 0.0000

Variable Regression CoefficientsSize (Assets) -1.420 (4.60)*Growth (Assets) -0.084 (0.28)Profitability -13.485 (5.12)*Tangibility 2.079 (1.88)***Age -0.001 (0.29)Earnings Variability 0.002 (3.01)*Debt Service Capacity -0.023 (2.81)*Dividend Payout Ratio 0.402 (1.19)Liquidity 0.188 (0.66)Non-debt Tax Shield -24.460 (1.96)***Degree of Operating Leverage -0.001 (0.08)Price-earnings Ratio -0.011 (2.11)**Promoter Holdings -0.017 (3.89)*Tax Rate 0.372 (0.43)Uniqueness -11.230 (3.54)*Cons 10.594 (6.74)Durbin-Watson Test= 1.587

*** indicates significance at 10 per cent level

** indicates significance at 5 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the z-values.

3141

The Random-effects regression model has been selected on the recommendation of

Hausman’s Specification test. The value of Hausman’s test is 12.49 and p-value is 0.3283

which shows that null hypothesis of difference in coefficients not systematic can not be

rejected. Therefore, Random-effects model has been considered appropriate for the data from

this particular industry. All the values of VIF test are below 10, therefore, multi colloinearity

is not a problem for this model. The Wald chi square value is 104.54 and p-value of 0.0000

supports the validity and significance of model. The R-square reveals that 58.55 per cent of

variation has been explained by the model. The impact of size, profitability and debt service

capacity on leverage has been found to be negative and statistically significant at .01 level.

These results are consistent as per the expectations of Pecking Order theory. Whereas the

negative significant relation of uniqueness and non-debt tax shield has supporting the

predictions of Static Trade-off theory. The coefficient for tangibility shows the positive

relationship with leverage and supporting the predictions of Static Trade-off theory. The

relation of price earnings and promoter shareholdings with leverage has been found to be

negative and statistically significant at .05 and .01 level respectively.

The value of Hausman’s Specification test has recommended the use of Fixed-effects

regression model for Iron & Steel Industry. Therefore, Random-effects regression results for

determinants of capital structure in Iron & Steel Industry have been exhibited in table 5.18.

From the results of Hausman’s Specification test, it has been discovered that Fixed-effects

model should be appropriate for interpretation in case of Iron & Steel Industry. The F-

statistics is 5.45 and p-value of 0.0000 confirms the validity of model for interpretation. The

VIF values for all regressors are below 5, indicating that there is no severe collinearity in

model. The R-square (within) discloses that 31.95 per cent of variation in leverage of a

particular company over time has been explained by model. The relation of size with leverage

has been found to be positive and statistically significant at .05 level and consistent as per

Static Trade-off theory. The table reveals that the coefficients for age, earnings variability

and uniqueness have been found to be negative and their respective p-values confirm the

statistical significance of these variables at .01 level. The degree of operating leverage and

promoter shareholdings has been found to be positively related with leverage and statistically

significant at .10 and .01 level respectively. Other variables considered for this study has

been found to be statistically insignificant in determining capital structure in Iron & Steel

Industry during the study period.

3142

Table 5.18: Fixed-effects Regression Results for

Determinants of Capital Structure (Debt-equity Ratio)

in Iron & Steel Industry

R-sq: within = 0.3195between = 0.1964

overall = 0.1273

Number of observations = 210Number of groups = 21F (15,174) = 5.45Prob > F = 0.0000

Variable Regression CoefficientsSize (Assets) 0.955 (2.60)**Growth (Assets) -0.389 (1.01)Profitability -3.488 (1.62)Tangibility 0.544 (0.30)Age -0.204 (2.93)*Earnings Variability -0.001 (3.56)*Debt Service Capacity -0.001 (0.09)Dividend Payout Ratio 0.653 (0.61)Liquidity -0.176 (0.84)Non-debt Tax Shield -24.062 (1.64)Degree of Operating Leverage 0.012 (1.88)***Price-earnings Ratio -0.001 (0.64)Promoter Holdings 7.377 (3.94)*Tax Rate -1.042 (1.63)Uniqueness -29.813 (2.92)*Cons 3.274 (1.33)Durbin-Watson Test= 0.899

*** indicates significance at 10 per cent level

** indicates significance at 5 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the t-values.

Table 5.19 shows the Fixed-effects regression results for determinants of capital

structure in Computer & IT Industry. The value of Hausman’s Specification test has

recommended the use of Fixed-effects regression model in Computer & IT Industry.

The value of Hausman’s Specification test is 47.78 and p-value is small enough to

reject the null hypothesis in favour of Fixed-effects regression model for Computer & IT

Industry. The value of R-square (within) discloses that 54.86 per cent of variation in leverage

over time within a company has been explained by model. The table displays that size and

tangibility have negative sign of relationship with leverage and statistically significant at .01

level. These relations are consistent with the predictions of Pecking Order theory. Age has

positive sign of relationship with leverage and statistically significant at .01 level

3143

contradicting the expectations of Pecking Order theory. The relationship among earnings

variability and leverage has been found to be negative and statistically significant at .10 level

consistent with Static Trade-off and Pecking Order theory. Dividend payout ratio and non-

debt tax shield have positive relations with leverage and statistically significant at .01 level.

The promoter shareholdings have positive relation with leverage whereas tax rate have

negative relations and both these relations has been statistically significant at .10 level.

Higher tax rate motivates the firms to use higher level of debt in their capital structure to

avail maximum amount of tax benefit and increase the amount available for equity

shareholders. Static Trade-off theory has also been expecting positive relation between tax

rate and leverage. Other variables included in this study have been found to be statistically

insignificant in determining the capital structure in Computer & IT Industry.

Table 5.19: Fixed-effects Regression Results for

Determinants of Capital Structure (Debt-equity Ratio)

in Computer & IT Industry

R-sq: within = 0.5486between = 0.0128

overall = 0.0920

Number of observations = 230Number of groups = 23F (15,192) = 15.56Prob > F = 0.0000

Variable Regression CoefficientsSize (Assets) -2.787 (4.81)*Growth (Assets) -0.009 (0.68)Profitability -0.276 (0.18)Tangibility -12.912 (7.00)*Age 0.392 (4.18)*Earnings Variability -0.001 (1.85)***Debt Service Capacity -0.001 (0.74)Dividend Payout Ratio 0.733 (7.63)*Liquidity 0.027 (0.34)Non-debt Tax Shield 47.627 (5.73)*Degree of Operating Leverage 0.001 (1.08)Price-earnings Ratio 0.001 (1.45)Promoter Holdings -3.365 (1.88)***Tax Rate 3.663 (1.95)***Uniqueness 4.006 (0.49)Cons 5.022 (2.25)Durbin-Watson Test= 1.161

*** indicates significance at 10 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the t-values.

3144

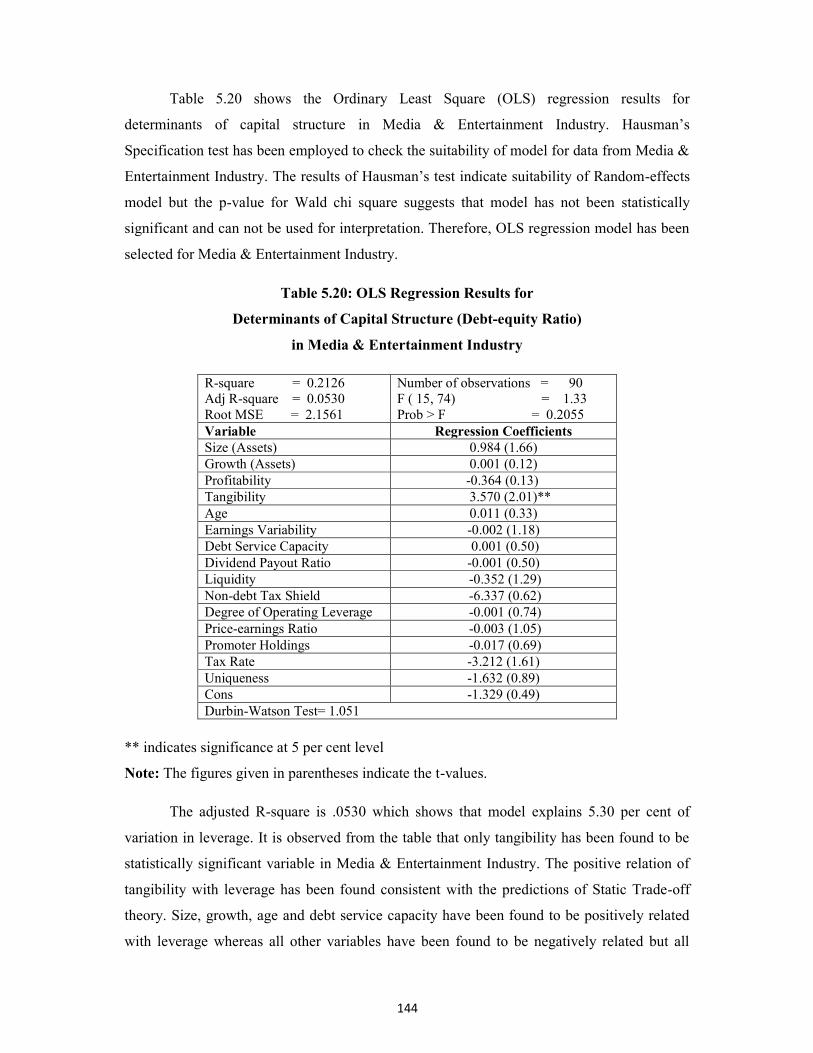

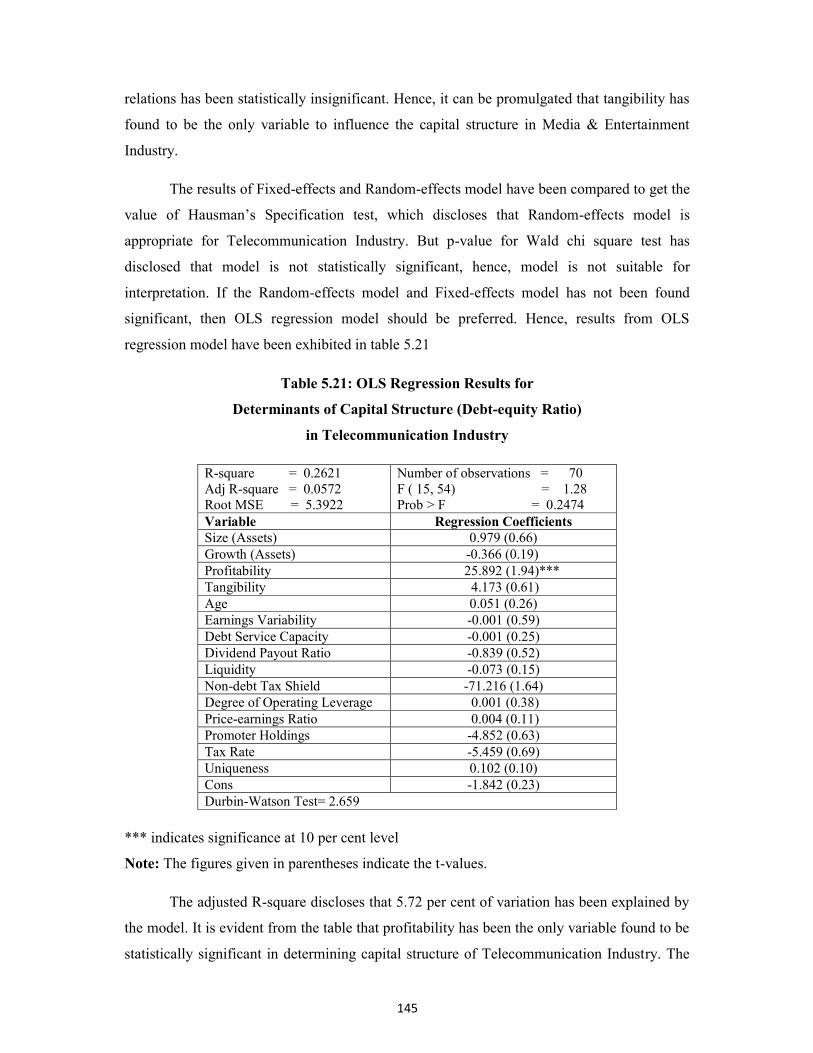

Table 5.20 shows the Ordinary Least Square (OLS) regression results for

determinants of capital structure in Media & Entertainment Industry. Hausman’s

Specification test has been employed to check the suitability of model for data from Media &

Entertainment Industry. The results of Hausman’s test indicate suitability of Random-effects

model but the p-value for Wald chi square suggests that model has not been statistically

significant and can not be used for interpretation. Therefore, OLS regression model has been

selected for Media & Entertainment Industry.

Table 5.20: OLS Regression Results for

Determinants of Capital Structure (Debt-equity Ratio)

in Media & Entertainment Industry

R-square = 0.2126Adj R-square = 0.0530Root MSE = 2.1561

Number of observations = 90F ( 15, 74) = 1.33Prob > F = 0.2055

Variable Regression CoefficientsSize (Assets) 0.984 (1.66)Growth (Assets) 0.001 (0.12)Profitability -0.364 (0.13)Tangibility 3.570 (2.01)**Age 0.011 (0.33)Earnings Variability -0.002 (1.18)Debt Service Capacity 0.001 (0.50)Dividend Payout Ratio -0.001 (0.50)Liquidity -0.352 (1.29)Non-debt Tax Shield -6.337 (0.62)Degree of Operating Leverage -0.001 (0.74)Price-earnings Ratio -0.003 (1.05)Promoter Holdings -0.017 (0.69)Tax Rate -3.212 (1.61)Uniqueness -1.632 (0.89)Cons -1.329 (0.49)Durbin-Watson Test= 1.051

** indicates significance at 5 per cent level

Note: The figures given in parentheses indicate the t-values.

The adjusted R-square is .0530 which shows that model explains 5.30 per cent of

variation in leverage. It is observed from the table that only tangibility has been found to be

statistically significant variable in Media & Entertainment Industry. The positive relation of

tangibility with leverage has been found consistent with the predictions of Static Trade-off

theory. Size, growth, age and debt service capacity have been found to be positively related

with leverage whereas all other variables have been found to be negatively related but all

3145

relations has been statistically insignificant. Hence, it can be promulgated that tangibility has

found to be the only variable to influence the capital structure in Media & Entertainment

Industry.

The results of Fixed-effects and Random-effects model have been compared to get the

value of Hausman’s Specification test, which discloses that Random-effects model is

appropriate for Telecommunication Industry. But p-value for Wald chi square test has

disclosed that model is not statistically significant, hence, model is not suitable for

interpretation. If the Random-effects model and Fixed-effects model has not been found

significant, then OLS regression model should be preferred. Hence, results from OLS

regression model have been exhibited in table 5.21

Table 5.21: OLS Regression Results for

Determinants of Capital Structure (Debt-equity Ratio)

in Telecommunication Industry

R-square = 0.2621Adj R-square = 0.0572Root MSE = 5.3922

Number of observations = 70F ( 15, 54) = 1.28Prob > F = 0.2474

Variable Regression CoefficientsSize (Assets) 0.979 (0.66)Growth (Assets) -0.366 (0.19)Profitability 25.892 (1.94)***Tangibility 4.173 (0.61)Age 0.051 (0.26)Earnings Variability -0.001 (0.59)Debt Service Capacity -0.001 (0.25)Dividend Payout Ratio -0.839 (0.52)Liquidity -0.073 (0.15)Non-debt Tax Shield -71.216 (1.64)Degree of Operating Leverage 0.001 (0.38)Price-earnings Ratio 0.004 (0.11)Promoter Holdings -4.852 (0.63)Tax Rate -5.459 (0.69)Uniqueness 0.102 (0.10)Cons -1.842 (0.23)Durbin-Watson Test= 2.659

*** indicates significance at 10 per cent level

Note: The figures given in parentheses indicate the t-values.

The adjusted R-square discloses that 5.72 per cent of variation has been explained by

the model. It is evident from the table that profitability has been the only variable found to be

statistically significant in determining capital structure of Telecommunication Industry. The

3146

positive significant relationship among profitability and leverage has been consistent with

Static Trade-off theory. The relation of size, tangibility, age, degree of operating leverage and

price-earnings ratio has been found to be positive with leverage whereas other independent

variables included in study have negative sign of relationship with leverage. But none of the

variables except profitability has been found to be statistically significant to influence capital

structure in Telecommunication Industry.

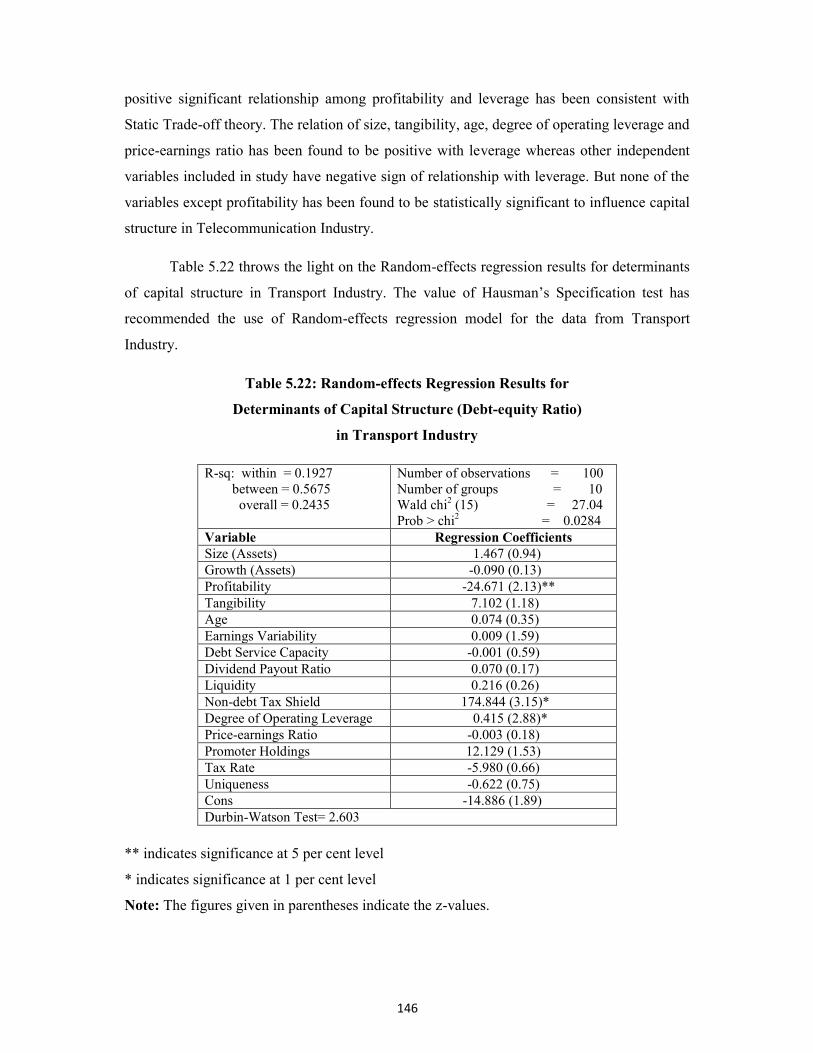

Table 5.22 throws the light on the Random-effects regression results for determinants

of capital structure in Transport Industry. The value of Hausman’s Specification test has

recommended the use of Random-effects regression model for the data from Transport

Industry.

Table 5.22: Random-effects Regression Results for

Determinants of Capital Structure (Debt-equity Ratio)

in Transport Industry

R-sq: within = 0.1927between = 0.5675

overall = 0.2435

Number of observations = 100Number of groups = 10Wald chi2 (15) = 27.04Prob > chi2 = 0.0284

Variable Regression CoefficientsSize (Assets) 1.467 (0.94)Growth (Assets) -0.090 (0.13)Profitability -24.671 (2.13)**Tangibility 7.102 (1.18)Age 0.074 (0.35)Earnings Variability 0.009 (1.59)Debt Service Capacity -0.001 (0.59)Dividend Payout Ratio 0.070 (0.17)Liquidity 0.216 (0.26)Non-debt Tax Shield 174.844 (3.15)*Degree of Operating Leverage 0.415 (2.88)*Price-earnings Ratio -0.003 (0.18)Promoter Holdings 12.129 (1.53)Tax Rate -5.980 (0.66)Uniqueness -0.622 (0.75)Cons -14.886 (1.89)Durbin-Watson Test= 2.603

** indicates significance at 5 per cent level

* indicates significance at 1 per cent level

Note: The figures given in parentheses indicate the z-values.

3147

The value of Hausman’s Specification test is 17.68 and p-value is .1702 that do not

reject the null hypothesis regarding differences in coefficients not systematic. So, Random-

effects model has been favoured over Fixed-effects model. Therefore, Random-effects

regression results have been presented in the table. VIF values for all independent variables

are below 3, hence, collinearity can not cause any problem for this model. The R-square

discloses that 24.35 percent of variation in leverage has been explained by the model. The p-

value for Wald chi square is .0284 which is small enough to signify the model for

interpretation. It is observed from the table that profitability has been found to be negatively

related to leverage and statistically significant at .05 level. The Pecking Order theory is also

expecting negative relation of profitability and leverage. The relations of non-debt tax shield

and degree of operating leverage with leverage have been found positive and statistically

significant at .01 level. Among the other regressors, the variables, growth, debt service

capacity, price-earnings ratio, tax rate and uniqueness have been found to be negatively

related with leverage whereas all other have shown positive relations. But these relations

have not been statistically significant for determining the capital structure in Transport

Industry.

5.3 SUMMARY AND FINDINGS

Two different measures of leverage have been used in this study. The impact of

different determinants on these two measures has been discussed in previous two sections. In

this section, the researcher provides the summary of results for different industries included

in sample.

It is observed from the empirical analysis that relation of size has been found to be

positive in Traditional Industries and Modern Industries as well as for Combined Data. The

relation of size has been significant at .01 level in all three models. The relation of size with

leverage has been found to be negative in Fertilizer Industry, Iron & Steel Industry and

Computer & IT Industry but statistically significant in Iron & Steel and Computer & IT

Industry only at .05 and .01 level respectively. The negative sign of this effect supports the

Pecking Order theory and various empirical researches viz., Titman and Wessels (1988),

Rajan and Zingales (1975), Booth, et al. (2001) and Datta and Agarwal (2009). It is worth to

make note that in Chemical, Drugs & Pharmaceutical, Media & Entertainment,

Telecommunication and Transport Industry, the relationship between size and leverage has

positive sign. The results illustrate that the bigger the company in terms of assets, the larger

3148

amount of debt it has in its capital structure. The findings has been consistent with Static

Trade-off theory and empirical findings by Baral (2004), Bevan and Danbolt (2002), Gaud, et

al. (2003), Pandey (2000), Taub (1975) etc. The risk of bankruptcy for a bigger company is

less than a smaller company. The reason behind this could be that the large companies being

‘too big to fail’, since they operate in large scales and more diversified (Akdal, 2011).

Therefore, smaller companies tend to borrow less than larger ones.

The relation of growth with leverage has been negative and significant in Traditional

Industries whereas in Modern Industries, relation has been positive and insignificant. The

growth has been found to be negatively related to leverage in Chemical and Transport

Industry whereas positive in remaining industries. Negative relationship of growth and

leverage has been consistent with previous empirical studies i.e., Bevan and Danbolt (2002),

Gaud, et al. (2003) and Jong, et al. (2007). It is observed from the regression results that six

of the selected industries have positive sign but none of the relations has been statistically

significant which shows that growth has no significant effect on leverage.

Profitability has been measured by the ratio of Earnings before Interest and Taxes

(EBIT) to total assets. The regression results of different models have shown that profitability

has been positively related with leverage in Traditional and Modern Industries but the

relation is negative for Combined Data. The relation has not been statistically significant in

either case. From different industries, the relation of profitability with leverage has been

found to be negative and statistically significant in Chemical, Drugs & Pharmaceutical,

Fertilizer, Iron & Steel and Transport Industry whereas positive insignificant in other three

industries. The negative relation of profitability with leverage has been supporting the

expectations of Pecking Order theory. According to Pecking Order theory, companies with

high profits prefer retained earnings as a primary source of financing new investments. These

findings imply that profitable firms prefer internal financing rather than external financing.

The results are in line with the findings of past studies of Harris and Raviv (1991), Rajan and

Zingales (1995), Booth, et al. (2001), Bevan and Danbolt (2002), Gaud, et al. (2003), Jong, et

al. (2007) and Pandey (2001).

The results from different regression models indicate that there exists mix type of

relations among tangibility and leverage in different models. The relationship among

tangibility and leverage has been found to be negative and statistically significant at .05 level

for Traditional Industries and at .01 level for Modern and Combined data. The relation of

3149

tangibility with leverage has been found to be negative for Iron & Steel, Computer & IT and

Telecommunication Industries and positive in remaining five industries selected for the

present study. But the relation has been statistically significant for Chemical, Fertilizer, Iron

& Steel and Computer & IT Industries only. The positive relations between tangibility and

leverage are consistent with Static Trade-off theory which suggests that companies having

higher collateral assets are more likely to have high level of debt ratios. The views in favour

of this are that tangible assets are easy to collateralize and therefore, it decreases the agency

cost of debt (Rajan and Zingales, 1995). Also studies of Titman and Wessels (1988), Gaud, et

al. (2003), Pandey, et al. (2000), Oztekin (2008) and Pathak (2011) have found evidences in

support of this relation. The negative sign of relationship among tangibility and leverage

implies that firms with larger tangibility of assets will have lower financial leverage. This

view is as per the expectations of Pecking Order theory and several research studies i.e.,

Cuong and Canh (2012), Eldomiaty (2007), Jong, et al. (2007) and Pandey (2001) have also

supported this relation.

Age has negative relation with leverage in Traditional Industries whereas positive and

significant in Modern Industries. Regression results for Combined Data also disclosing

negative sign of relationship of age with leverage. From the specific analysis of industries,

Computer & IT Industry has positive relation with leverage whereas all remaining industries

have negative relation. A large number of empirical studies such as Cuong and Canh (2012)

and Frydenberg (2004) have found negative relation among age and leverage as consistent

with Pecking Order theory. It implies that debt levels should decrease with the increase in

the age of enterprise. Conversely, several researchers suggest that lower information

imbalances will result in higher debt levels. The debt owners will be more likely to lend

capital to enterprises that they have better understanding rather than enterprises they have

little knowledge about. The positive relation of age and leverage has been consistent with

previous empirical studies i.e., Garg and Shekhar (2002), Mojtahedzadeh and Nejati (2009),

Rafiq (2008) and Zaheer, et al. (2011).

The expected sign of relationship among earnings variability and leverage has been

found to be negative because high risk companies are supposed to have higher chances of

bankruptcy risk. The relation of earnings variability with leverage has been found positive in

Traditional Industries as against the expected relation whereas negative in Modern Industries

and Combined Data. These results are consistent with the Pecking Order and Static Trade-off

theory. The relation of earnings variability with leverage has been negative and statistically

3150

significant in Media & Entertainment, Telecommunication and Transport Industries as in line

with empirical studies of Bhatt (1980), Titman and Wessels (1988), Kumar, et al. (2012), Qiu

and La (2008) and Eldomiaty (2007). The positive sign of relationship has been observed in

Chemical and Fertilizer Industry as in line with Sarvanam (2006) and Lakshmi (2010).

The relation of debt service capacity with leverage has been observed as negative for

Traditional, Modern and Combined Data. The relation has also been negative for industry

specific analysis in all industries except Media & Entertainment and Transport Industry. But

the relation has been statistically significant in respect of Chemical, Fertilizer and Iron &

Steel Industry only. Negative relation of debt service capacity with leverage confirms to the

prediction of Pecking Order theory and consistent with the views of Bhatt (1980),

Mojtahedzadeh and Nejati (2009) and Pandey, et al. (2000). The positive relation of debt

service capacity with leverage has been consistent with Static Trade-off theory and in line

with the views of Kumar, et al. (2012), Barol (2004) and Garg and Shekhar (2002).

The relation of dividend payout ratio with leverage has been found to be negative in

Traditional Industries and positive in case of Modern Industries and Combined Data. But no

relation has been statistically significant means dividend payout has not been an important

determinant of capital structure in either case. From the specific analysis of industries

included in sample, the relation of dividend payout ratio with leverage has been negative in

case of Drugs & Pharmaceutical Industry, Iron & Steel Industry and Media & Entertainment

Industry whereas positive in all remaining industries included in study. The relation has been

statistically significant in Computer & IT and Media & Entertainment Industry at .01 and .10

level respectively.

The ratio of current assets to current liabilities has been used as a proxy of liquidity.

The companies with high level of liquidity have more liquid assets and hence, less amount of

debt is required which results in lower leverage. Therefore, negative relation is expected

between liquidity and leverage. The negative relation between liquidity and leverage has been

observed in Traditional, Modern and Combined Data. But relation has been statistically

significant in Traditional and Combined Data at .05 level which implies that liquidity has

been a significant factor in determining the capital structure in Traditional Industries whereas

insignificant in Modern Industries. The relation between liquidity and leverage is supporting

the views of Pecking Order theory and in line with Akdal (2011), Waliullah and Nishant

(2008), Oztekin (2008) and Myers (1977). From industry wise analysis, all industries except

3151

Chemical and Drugs & Pharmaceutical Industries have negative sign of relations among

liquidity and leverage. The positive sign of relation has been consistent with Static Trade-off

theory and in line with Jong, et al. (2007).

Static Trade-off theory points out that the companies with higher non-debt tax shield

tend to have lesser amount of debt rather than other companies. Therefore, reverse relation is

expected between non-debt tax shield and leverage. From the regression results, it has been

observed that non-debt tax shield has been found to be positively related with leverage in

Traditional, Modern and Combined Data. The findings are contradicting the expectations of

Static Trade-off theory but positive relation among them has been supported by

Mojtahedzadeh and Nejati (2009), Rafiq, et al. (2008), Kakani and Reddy (1998) and Salawu

and Agboola (2008). From the regression results of different industries, Chemical, Drugs &

Pharmaceutical and Fertilizer Industries have negative sign of relationship with leverage and

consistent with Static Trade-off theory. In addition, these findings are consistent with past

empirical studies such as, Oztekin (2008), Rao and Lukose (2001), Qian, et al. (2007) and

Shah and Khan (2007). Positive sign of relationship has been observed in Iron & Steel,

Computer & IT, Media & Entertainment, Telecommunication and Transport Industries as