Embed Size (px)

Citation preview

1 November 27, 2017 | ©2017 Kaiser Foundation Health Plan, Inc.

Demonstration of Math and Actuarial Principles in Health InsuranceUCLA BAS – November 27th, 2017

Lorenz Glaza, FSA, MAAA

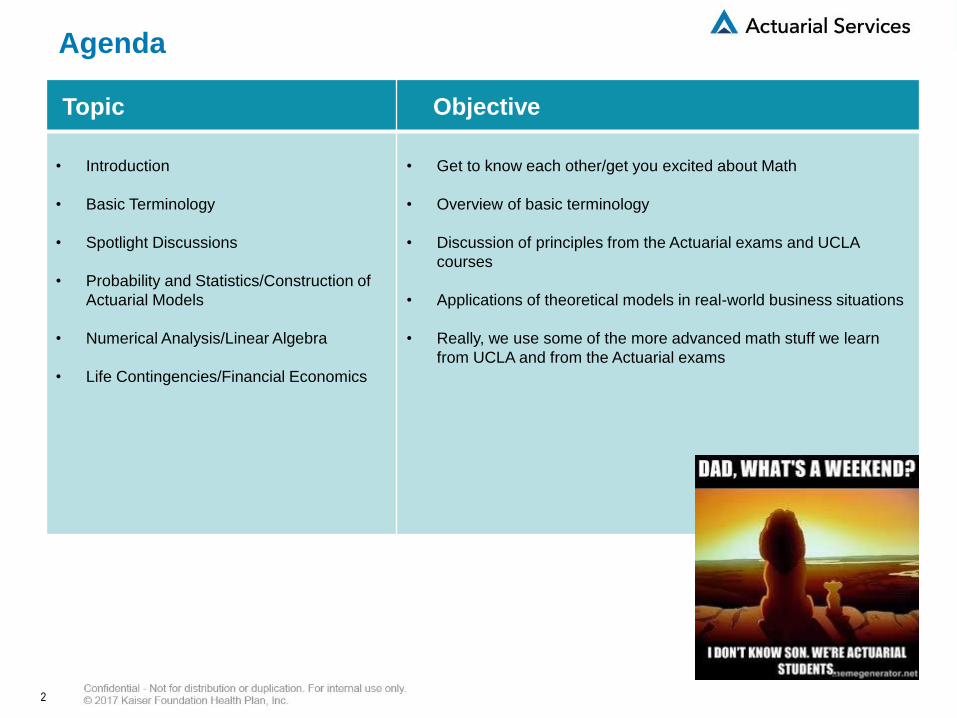

Agenda

2

Topic Objective

• Introduction

• Basic Terminology

• Spotlight Discussions

• Probability and Statistics/Construction of

Actuarial Models

• Numerical Analysis/Linear Algebra

• Life Contingencies/Financial Economics

• Get to know each other/get you excited about Math

• Overview of basic terminology

• Discussion of principles from the Actuarial exams and UCLA

courses

• Applications of theoretical models in real-world business situations

• Really, we use some of the more advanced math stuff we learn

from UCLA and from the Actuarial exams

Introduction

Basic Terminology

Deductible - A specified amount of money that the insured must pay before an

insurance company will begin providing benefits (i.e. paying of medical claims).

Embedded Deductible – Under a family contract, it is the individual deductible that

each member is responsible for.

Aggregate Deductible – Under a family contract, the common deductible that

applies to all insureds. The deductible can be paid by one or several members.

Out of Pocket Maximum - The most an insured has to out of pocket during a policy

period (usually a year) for health care services.

Coinsurance – A percent share of the claim an insured must pay.

Lapse Rate - The rate at which an insurance policy terminates usually because of

failure to pay the premiums or death.

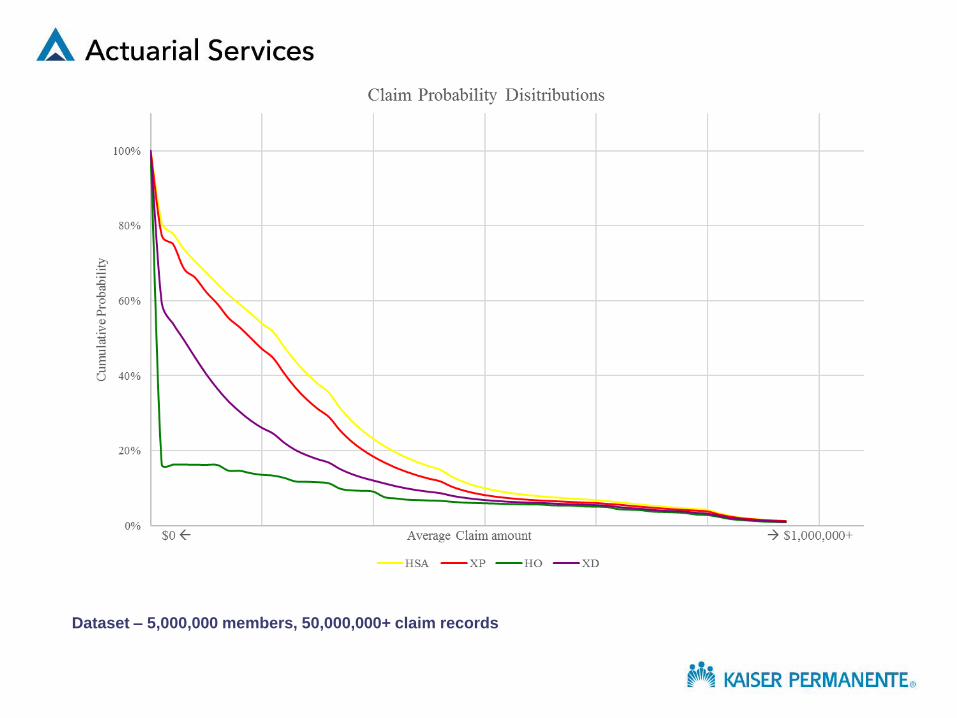

Spotlight Discussions

Probability and StatisticsExam P

Construction of Actuarial ModelsExam C

Building a Claims Probability Distribution (CPD):

1. Need data

Use experience data which is discrete

2. What to consider so we can summarize the data

What are we trying to do? Value deductibles, benefit maximums, per script maximums?

At what level of data do we need our data? Member level, claim level?

How do we want to express our data?

What variables do we need? Claim allowed amounts, types of services, dates of service, etc.?

How large is the dataset we are using? How can we be efficient in how we summarize our data?

3. Let’s summarize the data

4. How do we know if the distribution is credible/usable?

Statistical analysis can be performed

Work experience/common sense helps to know if the results are reasonable

Dataset – 5,000,000+ members, 50,000,000+ claim records

Roughly 1 in 8 Californians

CLAIM PROBABILITY DISTRIBUTION

(1) (2) (3) (4) (5)

Probability Annual Cost

Claims are of Claims

Total Annual Greater Than Greater Than

Annual Annual Cost of or Equal to or Equal to

Frequency Claim Claim Column 2 Column 2

0.8359830 $0.00 $0.00 1.0000000 $2,515.22

0.0002127 $28.47 $0.01 0.1640170 $2,515.22

0.0003144 $75.18 $0.02 0.1638043 $2,515.21

0.0003980 $124.16 $0.05 0.1634899 $2,515.19

0.0003421 $173.98 $0.06 0.1630919 $2,515.14

0.0003103 $224.81 $0.07 0.1627498 $2,515.08

0.0151644 $274.74 $4.17 0.1624395 $2,515.01

0.0002242 $324.89 $0.07 0.1472751 $2,510.84

0.0065839 $355.82 $2.34 0.1470509 $2,510.77

0.0043014 $443.91 $1.91 0.1404670 $2,508.43

0.0018799 $484.50 $0.91 0.1361656 $2,506.52

0.0062227 $541.71 $3.37 0.1342857 $2,505.61

0.0094493 $646.20 $6.11 0.1280630 $2,502.24

0.0008870 $752.00 $0.67 0.1186137 $2,496.13

0.0013524 $851.94 $1.15 0.1177267 $2,495.46

0.0027165 $930.15 $2.53 0.1163743 $2,494.31

0.0142911 $1,129.83 $16.15 0.1136578 $2,491.78

0.0045062 $1,328.49 $5.99 0.0993667 $2,475.63

0.0014211 $1,491.12 $2.12 0.0948605 $2,469.64

0.0020347 $1,720.09 $3.50 0.0934394 $2,467.52

0.0148140 $1,907.31 $28.25 0.0914047 $2,464.02

0.0033126 $2,080.23 $6.89 0.0765907 $2,435.77

0.0032845 $2,273.10 $7.47 0.0732781 $2,428.88

0.0011410 $2,489.57 $2.84 0.0699936 $2,421.41

0.0010695 $2,682.69 $2.87 0.0688526 $2,418.57

1A HSA 1B XP 2A HO 5A XD

Pr(Claim) Avg Claim Amt Pr(Claim) Avg Claim Amt Pr(Claim) Avg Claim Amt Pr(Claim) Avg Claim Amt

0.1920810 $0.00 0.2258301 $0.00 0.8359827 $0.00 0.4056799 $0.00

0.0283029 29.56 0.0225886 34.11 0.0002127 28.47 0.0550497 36.21

0.0424781 85.93 0.0665892 88.58 0.0003144 75.18 0.0445185 78.56

0.0322477 122.96 0.0239146 126.11 0.0003980 124.16 0.0468316 121.59

0.0300715 176.64 0.0386297 177.16 0.0003421 173.98 0.0443365 174.81

0.0299126 222.23 0.0314649 220.50 0.0003103 224.81 0.0388783 222.52

0.0294778 275.73 0.0377795 275.40 0.0151644 274.74 0.0338326 274.35

0.0245889 324.77 0.0244346 325.17 0.0002242 324.89 0.0272280 323.45

0.0249513 374.21 0.0290306 372.65 0.0065839 355.82 0.0239903 371.74

0.0267688 423.53 0.0289123 423.08 0.0043014 443.91 0.0191783 425.30

0.0219945 474.77 0.0239112 474.37 0.0018799 484.50 0.0151545 474.05

0.0406693 548.24 0.0415431 547.74 0.0062227 541.71 0.0245550 545.92

0.0379326 647.23 0.0379698 646.29 0.0094493 646.20 0.0194220 646.57

0.0321368 747.91 0.0308174 747.14 0.0008870 752.00 0.0136808 748.86

0.0272855 848.91 0.0256398 848.20 0.0013524 851.94 0.0108113 848.14

0.0239394 948.82 0.0215171 948.34 0.0027165 930.15 0.0091097 948.92

0.0408286 1,096.54 0.0358569 1,095.43 0.0142911 1,129.83 0.0170319 1,099.27

0.0334127 1,296.15 0.0288626 1,294.93 0.0045062 1,328.49 0.0128534 1,295.40

0.0267005 1,496.65 0.0225108 1,495.32 0.0014211 1,491.12 0.0099590 1,494.88

0.0227243 1,697.76 0.0188113 1,697.13 0.0020347 1,720.09 0.0078685 1,695.98

0.0192855 1,897.06 0.0158268 1,896.76 0.0148140 1,907.31 0.0077990 1,901.65

0.0165371 2,096.84 0.0136593 2,095.09 0.0033126 2,080.23 0.0073811 2,092.82

0.0141144 2,297.70 0.0113897 2,296.94 0.0032845 2,273.10 0.0060126 2,295.09

0.0122113 2,497.69 0.0097671 2,497.64 0.0011410 2,489.57 0.0049034 2,495.90

0.0105659 2,697.81 0.0081796 2,696.91 0.0010695 2,682.69 0.0039746 2,694.94

0.0090844 2,897.46 0.0071234 2,896.49 0.0008448 2,899.72 0.0035592 2,895.07

0.0180807 3,236.53 0.0137421 3,235.72 0.0024116 3,186.38 0.0068276 3,235.32

Dataset – 5,000,000 members, 50,000,000+ claim records

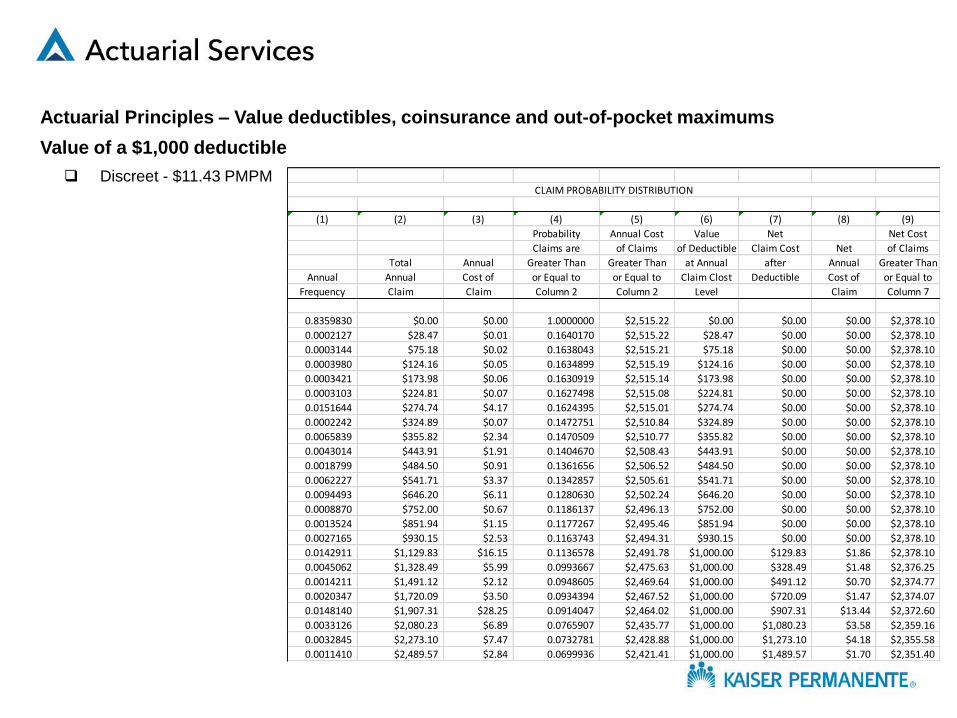

Actuarial Principles – Value deductibles, coinsurance and out-of-pocket maximums

Value of a $1,000 deductible

Discreet - $11.43 PMPMCLAIM PROBABILITY DISTRIBUTION

(1) (2) (3) (4) (5) (6) (7) (8) (9)

Probability Annual Cost Value Net Net Cost

Claims are of Claims of Deductible Claim Cost Net of Claims

Total Annual Greater Than Greater Than at Annual after Annual Greater Than

Annual Annual Cost of or Equal to or Equal to Claim Clost Deductible Cost of or Equal to

Frequency Claim Claim Column 2 Column 2 Level Claim Column 7

0.8359830 $0.00 $0.00 1.0000000 $2,515.22 $0.00 $0.00 $0.00 $2,378.10

0.0002127 $28.47 $0.01 0.1640170 $2,515.22 $28.47 $0.00 $0.00 $2,378.10

0.0003144 $75.18 $0.02 0.1638043 $2,515.21 $75.18 $0.00 $0.00 $2,378.10

0.0003980 $124.16 $0.05 0.1634899 $2,515.19 $124.16 $0.00 $0.00 $2,378.10

0.0003421 $173.98 $0.06 0.1630919 $2,515.14 $173.98 $0.00 $0.00 $2,378.10

0.0003103 $224.81 $0.07 0.1627498 $2,515.08 $224.81 $0.00 $0.00 $2,378.10

0.0151644 $274.74 $4.17 0.1624395 $2,515.01 $274.74 $0.00 $0.00 $2,378.10

0.0002242 $324.89 $0.07 0.1472751 $2,510.84 $324.89 $0.00 $0.00 $2,378.10

0.0065839 $355.82 $2.34 0.1470509 $2,510.77 $355.82 $0.00 $0.00 $2,378.10

0.0043014 $443.91 $1.91 0.1404670 $2,508.43 $443.91 $0.00 $0.00 $2,378.10

0.0018799 $484.50 $0.91 0.1361656 $2,506.52 $484.50 $0.00 $0.00 $2,378.10

0.0062227 $541.71 $3.37 0.1342857 $2,505.61 $541.71 $0.00 $0.00 $2,378.10

0.0094493 $646.20 $6.11 0.1280630 $2,502.24 $646.20 $0.00 $0.00 $2,378.10

0.0008870 $752.00 $0.67 0.1186137 $2,496.13 $752.00 $0.00 $0.00 $2,378.10

0.0013524 $851.94 $1.15 0.1177267 $2,495.46 $851.94 $0.00 $0.00 $2,378.10

0.0027165 $930.15 $2.53 0.1163743 $2,494.31 $930.15 $0.00 $0.00 $2,378.10

0.0142911 $1,129.83 $16.15 0.1136578 $2,491.78 $1,000.00 $129.83 $1.86 $2,378.10

0.0045062 $1,328.49 $5.99 0.0993667 $2,475.63 $1,000.00 $328.49 $1.48 $2,376.25

0.0014211 $1,491.12 $2.12 0.0948605 $2,469.64 $1,000.00 $491.12 $0.70 $2,374.77

0.0020347 $1,720.09 $3.50 0.0934394 $2,467.52 $1,000.00 $720.09 $1.47 $2,374.07

0.0148140 $1,907.31 $28.25 0.0914047 $2,464.02 $1,000.00 $907.31 $13.44 $2,372.60

0.0033126 $2,080.23 $6.89 0.0765907 $2,435.77 $1,000.00 $1,080.23 $3.58 $2,359.16

0.0032845 $2,273.10 $7.47 0.0732781 $2,428.88 $1,000.00 $1,273.10 $4.18 $2,355.58

0.0011410 $2,489.57 $2.84 0.0699936 $2,421.41 $1,000.00 $1,489.57 $1.70 $2,351.40

Actuarial Principles – Value deductibles, coinsurance and out-of-pocket maximums

Value of a $1,000 deductible

2 ways to value the deductible

Short-hand:

((Total Gross Annual Claims) – ((Claims in Excess of the Deductible – (Deductible) * (Probability of Member

Exceeding the Deductible)))/12

In Excel: =E22/12-(VLOOKUP(F6,$B$22:$E$121,4)-F6*VLOOKUP(F6,$B$22:$D$121,3))/12

What value did you get?

Actuarial Principles – Value deductibles, coinsurance and out-of-pocket maximums

Value of a $6,000 Out-Of-Pocket (OOP) Credit

We need to know the deductible and coinsurance amount – Let’s assume a $1,000 deductible and 20% coinsurance

Need to calculate the trigger amount – The gross claim amount where a member would hit their OOP

(OOP – Deductible)/(Coinsurance) + Deductible

If we did not have any out-of-pocket protection, the member could pay over $200,000 in out-of-pocket costs!

Value of Gross Claims $2,515.22

Value of Member Cost Share Before OOP Adjustment $612.71

Value of OOP Adjustment $250.60

Net Adjustment for Member OOP $362.11

Estimated Net Health Plan Paid Claims $2,153.11

Benefit Plan Value 85.6%

Actuarial Principles – Value deductibles, coinsurance and out-of-pocket maximums

CLAIM PROBABILITY DISTRIBUTION CLAIM COST SUMMARY

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

Probability Annual Cost

Claims are of Claims Value of Annual Adjustment

Total Annual Greater Than Greater Than OOP Value of for Value with Credit

Annual Annual Cost of or Equal to or Equal to Before OOP Member $6,000 OOP $6,000 for

Frequency Claim Claim Column 2 Column 2 Adjustment Cost Share Adjustment OOP $6,000 OOP

0.8359830 $0.00 $0.00 1.0000000 $2,515.22 $0.00 $0.00 $0.00 $0.00 $0.00

0.0002127 28.47 0.01 0.1640170 2,515.22 28.47 $0.01 28.47 $0.01 $0.00

0.0003144 75.18 0.02 0.1638043 2,515.21 75.18 $0.02 75.18 $0.02 $0.00

0.0018084 17,535.55 31.71 0.0362035 2,121.81 4,307.11 $7.79 4,307.11 $7.79 $0.00

0.0039754 18,418.42 73.22 0.0343951 2,090.10 4,483.68 $17.82 4,483.68 $17.82 $0.00

0.0013475 19,445.74 26.20 0.0304197 2,016.88 4,689.15 $6.32 4,689.15 $6.32 $0.00

0.0048922 22,274.10 108.97 0.0290722 1,990.68 5,254.82 $25.71 5,254.82 $25.71 $0.00

0.0056290 26,998.55 151.97 0.0241800 1,881.71 6,199.71 $34.90 6,000.00 $33.77 $1.12

0.0028679 32,213.40 92.38 0.0185510 1,729.74 7,242.68 $20.77 6,000.00 $17.21 $3.56

0.0020359 37,376.83 76.10 0.0156831 1,637.36 8,275.37 $16.85 6,000.00 $12.22 $4.63

0.0019474 42,300.38 82.38 0.0136472 1,561.26 9,260.08 $18.03 6,000.00 $11.68 $6.35

0.0011634 47,413.98 55.16 0.0116998 1,478.88 10,282.80 $11.96 6,000.00 $6.98 $4.98

0.0009892 52,447.19 51.88 0.0105364 1,423.72 11,289.44 $11.17 6,000.00 $5.94 $5.23

0.0014451 57,914.31 83.69 0.0095472 1,371.84 12,382.86 $17.89 6,000.00 $8.67 $9.22

0.0007468 62,355.14 46.57 0.0081021 1,288.15 13,271.03 $9.91 6,000.00 $4.48 $5.43

0.0006210 67,381.73 41.84 0.0073553 1,241.58 14,276.35 $8.87 6,000.00 $3.73 $5.14

0.0005440 72,480.87 39.43 0.0067343 1,199.74 15,296.17 $8.32 6,000.00 $3.26 $5.06

0.0006102 77,066.29 47.03 0.0061903 1,160.31 16,213.26 $9.89 6,000.00 $3.66 $6.23

0.0004390 82,491.27 36.21 0.0055801 1,113.28 17,298.25 $7.59 6,000.00 $2.63 $4.96

0.0003897 87,313.43 34.03 0.0051411 1,077.07 18,262.69 $7.12 6,000.00 $2.34 $4.78

0.0003198 92,260.85 29.51 0.0047514 1,043.04 19,252.17 $6.16 6,000.00 $1.92 $4.24

0.0001299 373,665.17 48.54 0.0005788 380.60 75,533.03 $9.81 6,000.00 $0.78 $9.03

0.0000881 425,432.03 37.48 0.0004489 332.06 85,886.41 $7.57 6,000.00 $0.53 $7.04

0.0000616 473,920.84 29.19 0.0003608 294.58 95,584.17 $5.89 6,000.00 $0.37 $5.52

0.0000517 524,757.01 27.13 0.0002992 265.39 105,751.40 $5.47 6,000.00 $0.31 $5.16

0.0000393 573,394.12 22.53 0.0002475 238.26 115,478.82 $4.54 6,000.00 $0.24 $4.30

0.0000290 624,706.63 18.12 0.0002082 215.73 125,741.33 $3.65 6,000.00 $0.17 $3.47

0.0000236 677,900.80 16.00 0.0001792 197.61 136,380.16 $3.22 6,000.00 $0.14 $3.08

0.0001556 1,167,134.51 181.61 0.0001556 181.61 234,226.90 $36.45 6,000.00 $0.93 $35.51

Numerical AnalysisUCLA Math Course 151

Linear AlgebraUCLA Math Course 33/115

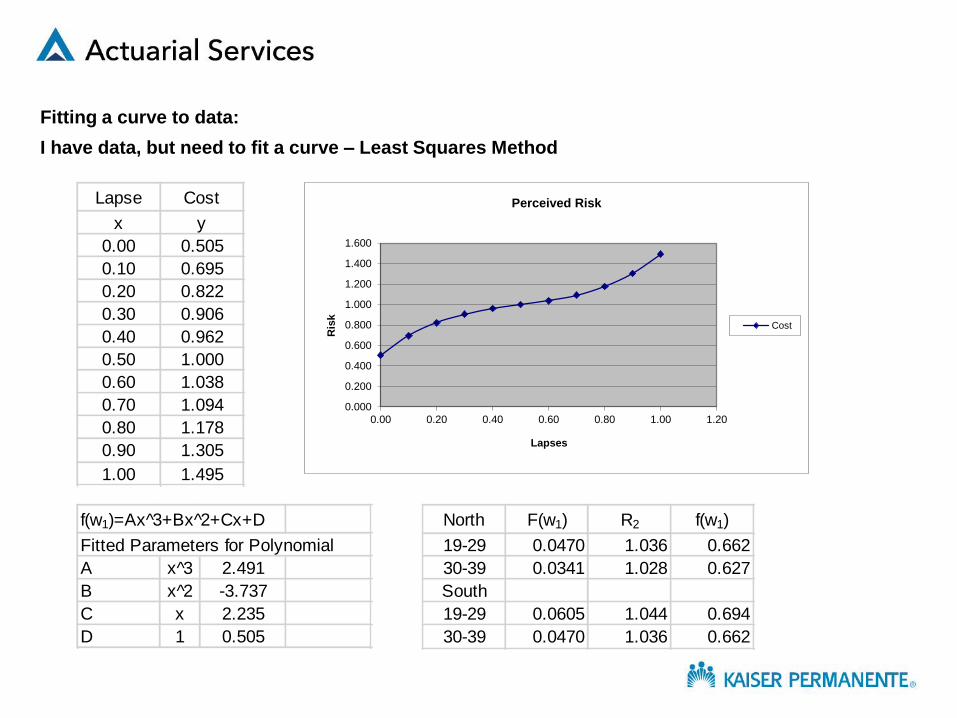

Fitting a curve to data:

I have data, but need to fit a curve – Least Squares Method

Lapse Cost

x y

0.00 0.505

0.10 0.695

0.20 0.822

0.30 0.906

0.40 0.962

0.50 1.000

0.60 1.038

0.70 1.094

0.80 1.178

0.90 1.305

1.00 1.495

0.000

0.200

0.400

0.600

0.800

1.000

1.200

1.400

1.600

0.00 0.20 0.40 0.60 0.80 1.00 1.20

Ris

k

Lapses

Perceived Risk

Cost

North F(w1) R2 f(w1)

19-29 0.0470 1.036 0.662

30-39 0.0341 1.028 0.627

South

19-29 0.0605 1.044 0.694

30-39 0.0470 1.036 0.662

f(w1)=Ax 3̂+Bx 2̂+Cx+D

Fitted Parameters for Polynomial

A x 3̂ 2.491

B x 2̂ -3.737

C x 2.235

D 1 0.505

Northern CA Age/Step Adjustments Southern CA Age/Step Adjustments

North South

Lapse Rate for 19-29 year olds 8.00% Lapse Rate for 19-29 year olds 10.00%

Lapse Rate for 30-39 year olds 6.00% Lapse Rate for 30-39 year olds 8.00%

Additional Rate Increase to 19-29 year olds 3.6% Additional Rate Increase to 19-29 year olds 4.4%

Additional Rate Increase to 30-39 year olds 2.8% Additional Rate Increase to 30-39 year olds 3.6%

Risk Factor for remaining 19-29 year olds 1.036 Risk Factor for remaining 19-29 year olds 1.044

Risk Factor for remaining 30-39 year olds 1.028 Risk Factor for remaining 30-39 year olds 1.036

North Results South Results

Expected Change in Margin 0.16% Expected % Change in Margin 0.19%

Age/Step Factors Age/Step Factors

Age SUB ONLYSUB+SP SUB+CH SUB+CHNFAMILY Age SUB ONLYSUB+SP SUB+CH SUB+CHNFAMILY

<1 0.889 1.778 1.778 2.667 2.667 <1 0.889 1.778 1.778 2.667 2.667

1-18 0.683 1.367 1.367 2.050 2.050 1-18 0.683 1.367 1.367 2.050 2.050

19-29 0.867 1.926 1.762 2.521 2.913 19-29 0.867 1.926 1.762 2.521 2.913

30-39 1.000 2.189 2.050 2.744 3.300 30-39 1.000 2.189 2.050 2.744 3.300

40-49 1.233 2.402 2.050 2.744 3.351 40-49 1.233 2.402 2.050 2.744 3.351

50-59 1.629 3.174 2.515 2.982 3.705 50-59 1.629 3.174 2.515 2.982 3.705

60-64 1.941 3.762 2.883 3.542 4.187 60-64 1.941 3.762 2.883 3.542 4.187

New Age/Step Factors with Revenue Neutrality New Age/Step Factors with Revenue Neutrality

Age SUB ONLYSUB+SP SUB+CH SUB+CHNFAMILY Age SUB ONLYSUB+SP SUB+CH SUB+CHNFAMILY

<1 0.903 1.806 1.806 2.708 2.708 <1 0.908 1.816 1.816 2.724 2.724

1-18 0.675 1.351 1.351 2.026 2.026 1-18 0.674 1.348 1.348 2.022 2.022

19-29 0.887 1.972 1.804 2.581 2.983 19-29 0.892 1.983 1.814 2.596 2.999

30-39 1.016 2.223 2.082 2.787 3.352 30-39 1.022 2.236 2.094 2.804 3.371

40-49 1.218 2.374 2.026 2.713 3.312 40-49 1.216 2.369 2.022 2.707 3.305

50-59 1.610 3.137 2.486 2.948 3.662 50-59 1.607 3.130 2.480 2.941 3.654

60-64 1.919 3.718 2.850 3.501 4.138 60-64 1.914 3.710 2.844 3.493 4.129

Final Impact including Revenue Neutrality Final Impact including Revenue Neutrality

Age SUB ONLYSUB+SP SUB+CH SUB+CHNFAMILY Age SUB ONLYSUB+SP SUB+CH SUB+CHNFAMILY

<1 1.56% 1.56% 1.56% 1.56% 1.56% <1 2.16% 2.16% 2.16% 2.16% 2.16%

1-18 -1.16% -1.16% -1.16% -1.16% -1.16% 1-18 -1.38% -1.38% -1.38% -1.38% -1.38%

19-29 2.39% 2.39% 2.39% 2.39% 2.39% 19-29 2.95% 2.95% 2.95% 2.95% 2.95%

30-39 1.56% 1.56% 1.56% 1.56% 1.56% 30-39 2.16% 2.16% 2.16% 2.16% 2.16%

40-49 -1.16% -1.16% -1.16% -1.16% -1.16% 40-49 -1.38% -1.38% -1.38% -1.38% -1.38%

50-59 -1.16% -1.16% -1.16% -1.16% -1.16% 50-59 -1.38% -1.38% -1.38% -1.38% -1.38%

60-64 -1.16% -1.16% -1.16% -1.16% -1.16% 60-64 -1.38% -1.38% -1.38% -1.38% -1.38%

Current Pricing Units Current Pricing Change

Age SUB ONLY SUB+SP SUB+CH SUB+CHN FAMILY Age SUB ONLY SUB+SP SUB+CH SUB+CHN FAMILY Age SUB ONLYSUB+SP SUB+CH SUB+CHN FAMILY

<1 0.8889 1.7778 1.7778 2.6667 2.6667 <1 158.00 317.00 317.00 475.00 475.00 <1 0.00% 0.00% 0.00% 0.00% 0.00%

1-18 0.6834 1.3669 1.3669 2.0503 2.0503 1-18 122.00 244.00 244.00 365.00 365.00 1-18 -3.47% -3.47% -3.47% -3.47% -3.47%

19-29 0.8668 1.9262 1.7617 2.5213 2.9130 19-29 154.00 343.00 314.00 449.00 519.00 19-29 0.77% 0.77% 0.77% 0.77% 0.77%

30-39 1.0000 2.1889 2.0500 2.7444 3.3000 30-39 178.00 390.00 365.00 489.00 588.00 30-39 0.00% 0.00% 0.00% 0.00% 0.00%

40-49 1.2327 2.4016 2.0500 2.7444 3.3509 40-49 220.00 428.00 365.00 489.00 597.00 40-49 -3.47% -3.47% -3.47% -3.47% -3.47%

50-59 1.6294 3.1738 2.5149 2.9825 3.7051 50-59 290.00 565.00 448.00 531.00 660.00 50-59 -3.47% -3.47% -3.47% -3.47% -3.47%

60-64 1.9411 3.7617 2.8833 3.5421 4.1868 60-64 346.00 670.00 514.00 631.00 746.00 60-64 -3.47% -3.47% -3.47% -3.47% -3.47%

Current PSPM Cost Current Subscirbership Final Impact including Rev Neu, Trend and Ben Adj

Age SUB ONLY SUB+SP SUB+CH SUB+CHN FAMILY Age SUB ONLY SUB+SP SUB+CH SUB+CHN FAMILY Age SUB ONLYSUB+SP SUB+CH SUB+CHN FAMILY

<1 172.89 0.00 607.96 260.40 0.00 <1 623 - 22 1 - <1 2.16% 2.16% 2.16% 2.16% 2.16%

1-18 105.43 427.02 181.01 233.93 253.00 1-18 7,899 2 781 60 1 1-18 -1.38% -1.38% -1.38% -1.38% -1.38%

19-29 131.07 397.61 338.26 443.49 504.54 19-29 20,835 808 1,007 291 905 19-29 2.95% 2.95% 2.95% 2.95% 2.95%

30-39 179.58 391.21 352.68 332.13 483.85 30-39 14,400 1,864 1,126 673 3,803 30-39 2.16% 2.16% 2.16% 2.16% 2.16%

40-49 190.83 337.68 249.15 373.88 428.26 40-49 13,186 2,381 1,010 597 3,991 40-49 -1.38% -1.38% -1.38% -1.38% -1.38%

50-59 218.97 378.61 295.59 305.12 504.50 50-59 14,752 3,318 297 87 961 50-59 -1.38% -1.38% -1.38% -1.38% -1.38%

60-64 259.78 481.32 312.59 565.25 526.57 60-64 9,442 1,524 20 7 85 60-64 -1.38% -1.38% -1.38% -1.38% -1.38%

Experience Proposed Pricing Units Current Margin per cell by Units

Age SUB ONLY SUB+SP SUB+CH SUB+CHN FAMILY Age SUB ONLY SUB+SP SUB+CH SUB+CHN FAMILY Age SUB ONLYSUB+SP SUB+CH SUB+CHN FAMILY

<1 0.9627 0.0000 3.3855 1.4500 0.0000 <1 0.8889 1.7778 1.7778 2.6667 2.6667 <1 -8.31% 100.00% -90.43% 45.62% 100.00%

1-18 0.5871 2.3779 1.0080 1.3027 1.4089 1-18 0.6598 1.3195 1.3195 1.9793 1.9793 1-18 14.09% -73.96% 26.26% 36.46% 31.29%

19-29 0.7299 2.2141 1.8836 2.4696 2.8096 19-29 0.8734 1.9410 1.7753 2.5406 2.9354 19-29 15.79% -14.95% -6.92% 2.05% 3.55%

30-39 1.0000 2.1785 1.9639 1.8495 2.6944 30-39 1.0000 2.1889 2.0500 2.7444 3.3000 30-39 0.00% 0.48% 4.20% 32.61% 18.35%

40-49 1.0627 1.8804 1.3874 2.0820 2.3848 40-49 1.1899 2.3183 1.9789 2.6493 3.2347 40-49 13.79% 21.70% 32.32% 24.14% 28.83%

50-59 1.2194 2.1083 1.6460 1.6991 2.8093 50-59 1.5729 3.0638 2.4277 2.8791 3.5767 50-59 25.16% 33.57% 34.55% 43.03% 24.18%

60-64 1.4466 2.6803 1.7407 3.1476 2.9322 60-64 1.8738 3.6314 2.7834 3.4194 4.0417 60-64 25.47% 28.75% 39.63% 11.14% 29.96%

Expected PSPM Cost Expected Margin per cell

Age SUB ONLY SUB+SP SUB+CH SUB+CHN FAMILY Age SUB ONLY SUB+SP SUB+CH SUB+CHN FAMILY Current margin 19.02%

<1 172.89 0.00 607.96 260.40 0.00 <1 -4.55% 100.00% -83.83% 47.51% 100.00% Expected Margin 19.21%

1-18 105.43 427.02 181.01 233.93 253.00 1-18 14.09% -73.96% 26.26% 36.46% 31.29%

19-29 136.82 415.05 353.10 462.94 526.67 19-29 15.79% -14.95% -6.92% 2.05% 3.55%

30-39 186.03 405.25 365.34 344.05 501.23 30-39 0.00% 0.48% 4.20% 32.61% 18.35%

40-49 190.83 337.68 249.15 373.88 428.26 40-49 13.79% 21.70% 32.32% 24.14% 28.83%

50-59 218.97 378.61 295.59 305.12 504.50 50-59 25.16% 33.57% 34.55% 43.03% 24.18%

60-64 259.78 481.32 312.59 565.25 526.57 60-64 25.47% 28.75% 39.63% 11.14% 29.96%

Expected Experience Expected Subscirbership

Age SUB ONLY SUB+SP SUB+CH SUB+CHN FAMILY Age SUB ONLY SUB+SP SUB+CH SUB+CHN FAMILY

<1 0.9294 0.0000 3.2681 1.3998 0.0000 <1 623 - 22 1 -

1-18 0.5668 2.2955 0.9730 1.2575 1.3600 1-18 7,899 2 781 60 1

19-29 0.7355 2.2311 1.8981 2.4886 2.8311 19-29 18,751 727 907 262 814

30-39 1.0000 2.1785 1.9639 1.8495 2.6944 30-39 13,248 1,715 1,036 619 3,499

40-49 1.0258 1.8152 1.3393 2.0098 2.3022 40-49 13,186 2,381 1,010 597 3,991

50-59 1.1771 2.0353 1.5890 1.6402 2.7120 50-59 14,752 3,318 297 87 961

60-64 1.3965 2.5874 1.6803 3.0385 2.8306 60-64 9,442 1,524 20 7 85

Multidimension Matrix Calculations:

1. Want to value deductibles and out-of-pocket maximums for multiple party contracts

2. Need to make Actuarial assumptions

Ex., Members act independently of each other and distribution of claims are independent

3. Need to represent vectors and matrices in Excel

2-dimensional: u=(u1,u2,u3, …,um) and v=(v1,v2,v3,…,vn), each representing a vector of probabilities of claims

Multidimension Matrix Calculations:

Represent dimensional vectors and matrices in Excel

3-dimensional

Let’s take a look at a model in Excel…

Life ContingenciesExam MLC

Financial EconomicsFM

Lapse Study: Create lapse rates by cohort

CohortMonth 1/1/1999 2/1/1999 3/1/1999 4/1/1999 5/1/1999 6/1/1999 7/1/1999 8/1/1999 9/1/1999 10/1/1999 11/1/1999 12/1/1999

1 3,860 2,848 3,972 2,836 2,760 2,695 3,012 2,743 5,454 3,007 38 2,808

2 3,619 2,504 3,777 2,655 2,588 2,519 2,838 2,395 5,098 2,888 36 2,445

3 3,454 2,417 3,593 2,525 2,414 2,395 2,536 2,254 5,058 2,727 27 2,333

4 3,273 2,295 3,431 2,394 2,296 2,153 2,403 2,246 4,812 2,524 27 2,185

5 3,081 2,215 3,282 2,289 2,067 2,037 2,388 2,137 4,425 2,379 23 1,978

6 2,953 2,124 3,142 2,073 1,976 2,017 2,257 1,961 4,260 2,275 22 1,968

7 2,851 2,024 2,898 1,979 1,965 1,926 2,088 1,889 4,080 2,086 22 1,890

8 2,739 1,854 2,778 1,969 1,880 1,784 1,999 1,814 3,804 2,081 21 1,864

9 2,544 1,791 2,762 1,889 1,748 1,712 1,921 1,690 3,787 1,998 20 1,738

10 2,458 1,786 2,660 1,771 1,682 1,645 1,785 1,688 3,653 1,974 17 1,668

11 2,451 1,713 2,495 1,719 1,620 1,531 1,782 1,632 3,619 1,822 15 1,608

12 2,359 1,590 2,409 1,668 1,493 1,527 1,715 1,621 3,384 1,734 15 1,528

13 2,265 1,535 2,328 1,570 1,488 1,473 1,689 1,522 3,241 1,652 14 1,468

14 2,195 1,491 2,195 1,569 1,446 1,463 1,587 1,477 3,125 1,594 14 1,372

15 2,137 1,420 2,190 1,520 1,431 1,372 1,530 1,436 3,014 1,536 14 1,330

16 2,017 1,417 2,119 1,504 1,351 1,320 1,475 1,393 2,918 1,460 14 1,286

17 2,015 1,390 2,097 1,413 1,292 1,277 1,431 1,350 2,767 1,422 14 1,234

18 1,968 1,375 1,994 1,373 1,244 1,241 1,390 1,279 2,683 1,378 14 1,193

19 1,952 1,317 1,923 1,342 1,202 1,212 1,319 1,247 2,599 1,330 12 1,160

20 1,864 1,280 1,879 1,314 1,157 1,147 1,290 1,221 2,532 1,288 10 1,124

21 1,797 1,233 1,818 1,269 1,102 1,108 1,261 1,193 2,453 1,258 10 1,100

22 1,757 1,202 1,774 1,217 1,074 1,089 1,238 1,167 2,401 1,237 10 1,076

23 1,731 1,174 1,694 1,179 1,036 1,070 1,219 1,133 2,338 1,202 10 1,039

24 1,682 1,123 1,642 1,142 1,015 1,046 1,182 1,098 2,275 1,169 10 1,008

25 1,614 1,097 1,604 1,120 989 1,013 1,149 1,078 2,210 1,133 10 991

26 1,575 1,068 1,558 1,096 968 994 1,113 1,049 2,147 1,106 10 949

27 1,528 1,047 1,523 1,069 944 958 1,077 1,033 2,097 1,079 10 921

28 1,504 1,026 1,493 1,047 930 936 1,058 1,011 2,039 1,035 10 906

29 1,480 1,007 1,461 1,027 913 921 1,037 984 1,961 1,013 9 880

30 1,462 980 1,433 1,009 875 897 1,005 948 1,905 1,000 9 872

31 1,433 958 1,405 979 857 877 962 927 1,861 981 9 854

32 1,408 943 1,371 956 838 831 933 906 1,818 967 9 841

Smoothing of Lapse Rates

Average Policy Life 25.92 Months

2.16 Years

Population Total Lapse

Month 10,000 Average Survival Cumulative Survival

1 9,386 -6.14% 93.86% 93.86%

2 8,852 -5.69% 94.31% 88.52%

3 8,386 -5.26% 94.74% 83.86%

4 7,939 -5.33% 94.67% 79.39%

5 7,563 -4.73% 95.27% 75.63%

6 7,213 -4.63% 95.37% 72.13%

7 6,897 -4.38% 95.62% 68.97%

8 6,614 -4.11% 95.89% 66.14%

9 6,352 -3.96% 96.04% 63.52%

10 6,113 -3.76% 96.24% 61.13%

11 5,873 -3.93% 96.07% 58.73%

12 5,655 -3.72% 96.28% 56.55%

13 5,456 -3.52% 96.48% 54.56%

14 5,276 -3.31% 96.69% 52.76%

15 5,100 -3.33% 96.67% 51.00%

16 4,933 -3.26% 96.74% 49.33%

17 4,774 -3.22% 96.78% 47.74%

18 4,630 -3.03% 96.97% 46.30%

19 4,497 -2.87% 97.13% 44.97%

20 4,371 -2.81% 97.19% 43.71%

21 4,248 -2.80% 97.20% 42.48%

22 4,127 -2.86% 97.14% 41.27%

23 4,004 -2.97% 97.03% 40.04%

24 3,901 -2.59% 97.41% 39.01%

25 3,792 -2.79% 97.21% 37.92%

26 3,695 -2.55% 97.45% 36.95%

27 3,603 -2.48% 97.52% 36.03%

28 3,520 -2.32% 97.68% 35.20%

29 3,434 -2.44% 97.56% 34.34%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57 59 61 63 65 67 69 71 73

Cu

mu

lati

ve P

erce

nt

of

Po

loci

es In

-Fo

rce

Duration - Months

Cumulative Policy Survival

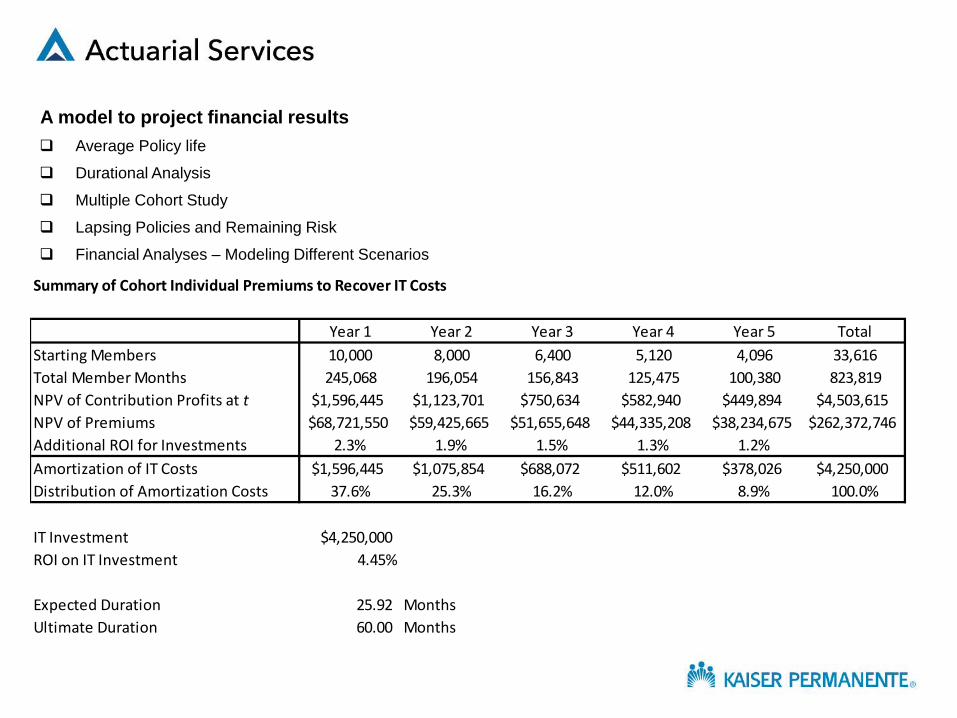

A model to project financial results

Average Policy life

Durational Analysis

Multiple Cohort Study

Lapsing Policies and Remaining Risk

Financial Analyses – Modeling Different Scenarios

Summary of Cohort Individual Premiums to Recover IT Costs

Year 1 Year 2 Year 3 Year 4 Year 5 Total

Starting Members 10,000 8,000 6,400 5,120 4,096 33,616

Total Member Months 245,068 196,054 156,843 125,475 100,380 823,819

NPV of Contribution Profits at t $1,596,445 $1,123,701 $750,634 $582,940 $449,894 $4,503,615

NPV of Premiums $68,721,550 $59,425,665 $51,655,648 $44,335,208 $38,234,675 $262,372,746

Additional ROI for Investments 2.3% 1.9% 1.5% 1.3% 1.2%

Amortization of IT Costs $1,596,445 $1,075,854 $688,072 $511,602 $378,026 $4,250,000

Distribution of Amortization Costs 37.6% 25.3% 16.2% 12.0% 8.9% 100.0%

IT Investment $4,250,000

ROI on IT Investment 4.45%

Expected Duration 25.92 Months

Ultimate Duration 60.00 Months