Embed Size (px)

Citation preview

Mohammed Farhad Miah

Head of Marketing and Sales

Eusof Group

Fundamentals of Cotton Demand and Supply.

To Develop an effective Hedging Strategy

A Critical economic issue for end –user.

Unforeseen natural and man-made events raise the economic stakes.

Ever- present price risk , Depend on Coarse – Premium

Security of locking in a price

Risk Manager assess business goals

Good faith

Other hedging Transactions-EFP,EFS,OFS

HISTORY OF USE COTTON IN BANGLADESH

Year Event

Pre-1947 11 Composite Mill, Having 1.1Mn Spindles and 2700 loom for weaving and Handloom Cottage inds.

1956 Capacity Increases to 3.20 Mn Spindles

1972 Capacity Declines to 0.8 Mn Spindles. All Textile Mill are nationalized and put under BTMC

1982 Privatization of Textile Mills starts when Government Adopts open Market Policy.

1999 Capacity reaches 2.4 Mn Spindles in the Private Sector and 0.40Mn spindles in Public Sector.

2007 Capacity grows to 6.30 Mn Spindles in290 Private Mills and where 0.40 Mn spindles public Mills.

2008 Capacity grows to 7.20Mn Spindles in 341 Mills

2009 Capacity grows to 7.60Mn Spindles in 350 Mills

2011 Capacity grows to 8.70Mn Spindles in 385 Mills

2015 Capacity grows to 11.05 Mn Spindles in 413 Mills and Rotor 0.257 Mn

Up tread Scenario of Bangladesh.

0

2

4

6

8

10

12

1947 1956 1972 1999 2007 2009 2011 2015

No.s of

Spindles in mn

setup

No.s Rotor

Nos of

Loom

Source:BTMA

Spindle Nos-

.80 Millions

Bangladesh

1971 After 44 Yrs

Blooming in PTS

Exporting

Countries

India CIS Africa

Australia

USA

Consumption

5.85 Million

Bales yrly

Reasons For Higher Demand of Cotton

seek sustainable worth in Textile- sector where

product is almost 95% imports substitute.

2. By adopting denationalization policy since 1983 ‘s emerge private sector spinning and mostly double production

capacity.

3. Backed by Gov. Spinning sub-sector demand high

Cotton consumption in Domestic and gradual feeding in

RMG of Bangladesh.

Reasons For Higher Demand of Cotton

4 .RMG export began in 1980 and Start new Era .

Increases Cotton import but 1990 shows another amazing

turning opportunities.

5.More attraction for Blooming demand of cotton due to GSP of EU.

6.To meet huge demand of millions of peoples (160 mn) .

Why Cotton Traders/Suppliers Over Bangladesh

(Investment Over $4.50 Billions )

No of Unit Installed Machine

Capacity

Production

Capacity (mn)

Cotton Consumption

Spinning Mills 413 Spindles -11.05 mn 2250 Mn Kg Approx-2520 mn kg

Rotor-0.257 mn

Fabrics Weaving 792 Shuttleless

Denim-30,H.Tex-22 Shuttle both-48000

Dying –Printing

Finishing

240 2720 mn (m)

Ba

ng

lad

esh

is

the

Se

con

d la

rge

st g

arm

en

t e

xp

ort

er

an

d s

eco

nd

big

ge

st c

ott

on

im

po

rte

r w

orl

dw

ide

.J L

ea

Tremendous Growth of RMG Sector

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

900.00

2003-2005 2005-2007 2007-2009 2009-2011 2011-2013 2013-2015

Knitwear

Woven Wear

RMG

Source:BKMEA

Qty in Mn

doz pcs

Why Cotton Traders/Suppliers Cotton over Bangladesh

Vision

-2021

• R

MG

E

arn

ing

sh

ares

in

G

DP

0

20

40

60

80

100

120

140

160

2003-2005 2005-2007 2007-2009 2009-2011 2011-2013 2013-2015

Share in GDP(%)

Share in National Export(%)

Knitwear Share in National

Export

Why Cotton Traders/Suppliers Over Bangladesh (Vision-2021)

Facts about Bangladesh Knitwear untill or in FY-2014-2015

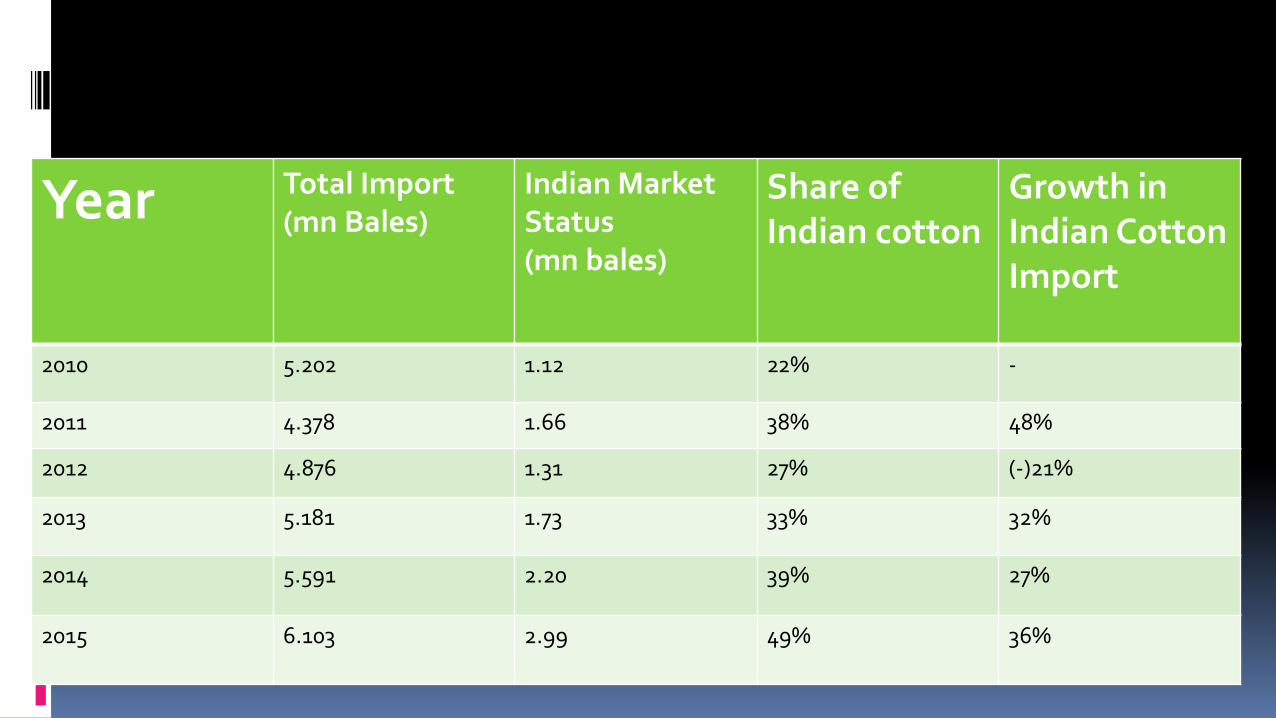

Import scenario of Cotton Last few Yrs

(Source : BTMA)

Year Total Import

(mn Bales)

Indian Market

Status

(mn bales)

Share of

Indian cotton

Growth in

Indian Cotton

Import

2010 5.202 1.12 22% -

2011 4.378 1.66 38% 48%

2012 4.876 1.31 27% (-)21%

2013 5.181 1.73 33% 32%

2014 5.591 2.20 39% 27%

2015 6.103 2.99 49% 36%

Country Import Own Production Stock Available USED Export

Bangladesh 5.80 -- -- 5.90 -

Vietnam 5.20 5.20

China 5.00 23.80 64.50 32.00 -

Turkey 3.80 - 3.80 6.40

Indonesia 3.10 3.10

India -- 26.80 11.20 24.50 5.50

United States 12.90 3.60 - 9.50

Brazil 6.70 6.90 - 4.20

Pakistan 7.20 2.30 9.80

Rest of World 12.20 22.90 14.80 31.00 10.07

World 34.90 100.20 103.30 109.20 34.90

Cotton statement for the Month of March, 2016

So

urc

e:U

SD

A

Statistics of World Cotton Producing Country

World Cotton USE in Domestic Consumption

0 5000 10000 15000 20000 25000 30000 35000 40000

China

India

Pakistan

Bangladesh

Vietnam2015-16

2014-15

2013-14

2012-13

1000 480 Ib . Bales

Countrywise Statistics of Cotton Cons.in Million Bales

World Cotton Stock And Domestic Cons.

0

20000

40000

60000

80000

100000

120000

2012-13 2013-14 2014-15 2015-16 2016-17

Beginng Stock

Total Dom.Cons

Ending Stock

Source:

USDA,March,

2016

At a Glance Forex Earning in Bangladesh.

(Value in Million USD)

0

10000

20000

30000

40000

50000

60000

2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2020-2021

Knitwear only

Total RMG

BD Total Export

Projected

Source : EXPORT PROMOTION BUREAU

(EPB) ,

The Vision - 0 is significant (GDP Expected doubled )

Democracy and effective Parliament

Political framework ,Decetralisation of power & Peoples Participation.

Good governance and avoiding political partisanship.

Transformation of Political Culture.

A Society Free from corruption.

Empowerment equal rights for woven.

Economic Development & Initiatives-Environment,Housing,energy Security,Industry,Education,Food& Nutrition,Alleviation of proverty,Population and Labour Force

Cotton Supply Chain Management(SCM)

Demand forecasting

• Purchasing-Requirements Planning-Inventory.

Logistics

• Distribution Planning-Order Processing-Transportation-Customer Service. Physical

Distribution

• Strategic Planning-Information Services- Marketing/Sales- Finance. SCM

• Warehousing-Material Handing-Packaging-Finish Raw Goods Inventory.

World Cotton

Depo Textiles

Sub-Sector

Cotton

Farmer’s/Ginner’s

USER

Human

Being Cotton By Product

End user

Demand Creator of

Raw Cotton

Cotton is white , Peace of Life

Supply of Raw

Cotton

Financial Institute, Insurance, Freight

Forwarder, Logistics supporter

Cloth for Wear

Cycle for Cotton USE

SWOT ANALYSIS in Demand & Supply of Cotton

STRENGTH:

•To have good relation with Sellers- Buyers.

•To positive responses from government to

mitigate issues •Strong Field For COTTON USE

•USDA Marked-UP as a 2ND Biggest Importer in

World.

•Assurance of Payment against Supplied Goods under UCPDC-600

THREATS:

•At 90-95% import based infrastructural

Establishment from national Banks.

•In quality of goods in delivery Doubtful by Suppliers .

•Intime Shipment is required in Factory .

OPERTUNITIES:

•To ensure manufacturing garments with quality of

Men's/women's Wear to treat as a Market Leader.

•Chance to focus Bangladesh in the global World in

Fashion Arena.

•Skilled nursering School to proof to shine national

dignity.

•To Circulate Huge Money in this Textile Sub-Sector.

WEAKNESSES:

•To chance Monetary stuck-up.

•Not available arbitration to solve any dispute

arises in contract/LC. •No ready Controller to check Financial Loss.

•Still Not any Recovery body to Protect Fund.

•To Find One stop Services

21

Recommendations:

To Increase the EDF for facilitating adequate Import as per requirements.

To adjustment period may extend up to 1(One) Year instead of 6 (six) Months.

To Ensure Cotton Quality before Shipment ,Inspection must be done by Pre-Qualified enlisted Inspection Firms.

At Present this Sub-Sector contribution to GDP is 12%. This may be increased to 24% within Vision 2021.

Fabrics Import may be reduced by increasing Textile manufacturing Quality fabrics Production for backward linked Support to Woven Garments Export.

Key Reference

EPB-Export Promotion Bureau.

BTMA- Bangladesh Textile Mills Association

BKMEA- Bangladesh Knitwear Manufacturers and Exporters Association

BGMEA- Bangladesh Garments Manufacturers and Exporter s Association

BCA- Bangladesh Cotton Association, CDB-Cotton Development Board Bangladesh.

USDA- United States Department of Agriculture

NCC- National Cotton Council of America

ITC- International Trade Center

GDP- Gross Domestic Product

MN-Million

CCI- Cotton corporation of India ,EICA-East India Cotton Association

EFP-Exchange of futures for Physicals,EFS-Ex for Swaps,OFS-Opations on Spreads

PTS- Primary Textile Sector

Q/A

Thanks to All