Embed Size (px)

Citation preview

Delticom AG: Company PresentationHanover, 19 March 2015

Company Presentation

Hanover, 19 March 20152

Agenda

3-7 | Delticom group overview

8-11 | Replacement tyre business

12-17 | Strategy

18-22 | Financials FY 2014

23-24 | Outlook 2015

Company Presentation

Hanover, 19 March 20153

Agenda

3-7 | Delticom group overview

8-11 | Replacement tyre business

12-17 | Strategy

18-22 | Financials FY 2014

23-24 | Outlook 2015

Company Presentation

Hanover, 19 March 20154

Delticom – Europe‘s leading online tyre retailer

► 163 online shops in 42 countries across the globe (Europe, North America & East Asia)

► Service partners: EU 35,344, Non-EU 5,780 + around 7,000 via Tyrepac

► More than 25,000 models from over 100 tyre brands for cars, motorcycles, commercial vehicles and buses

► Complete wheels, motor oil, replacement parts and accessories

► Multi-brand strategy

Company Presentation

Hanover, 19 March 20155

From e-commerce pioneer to European market leader

1999 – 2008:First mover and international expansion

1999

Delticom founded by a team

including Rainer Binder and

Andreas Prüfer

First mover advantage in

many European countries

2006

IPO on Frankfurt Stock

Exchange (Prime Standard)

2009 – 2011:Exceptionally goodmarkets

2012 – 2014:Challenging marketenvironment

2009 – 2011

Exceptionally good markets

due to wintery conditions and

regulations (scrapping

incentive schemes,

mandatory winter tyre

requirement)

2011

Investments in warehouse

infrastructure

2012 – 2014

Little snowfall and pull-forward

effect on tyre sales from

exceptional 2009 – 2011

regulatory and weather

conditions

2013

Tirendo acquisition

2014

Full integration of Tirendo

2015:Delticom market excellence

► 01/15: 15 years RDDE

► 03/15: 14y RDCH /

13y RDSE

► 05/15: 11y RDIT

► 08/15: 14y RDUK

► 10/15: 13y RDFR /

12y RDES

Company Presentation

Hanover, 19 March 20156

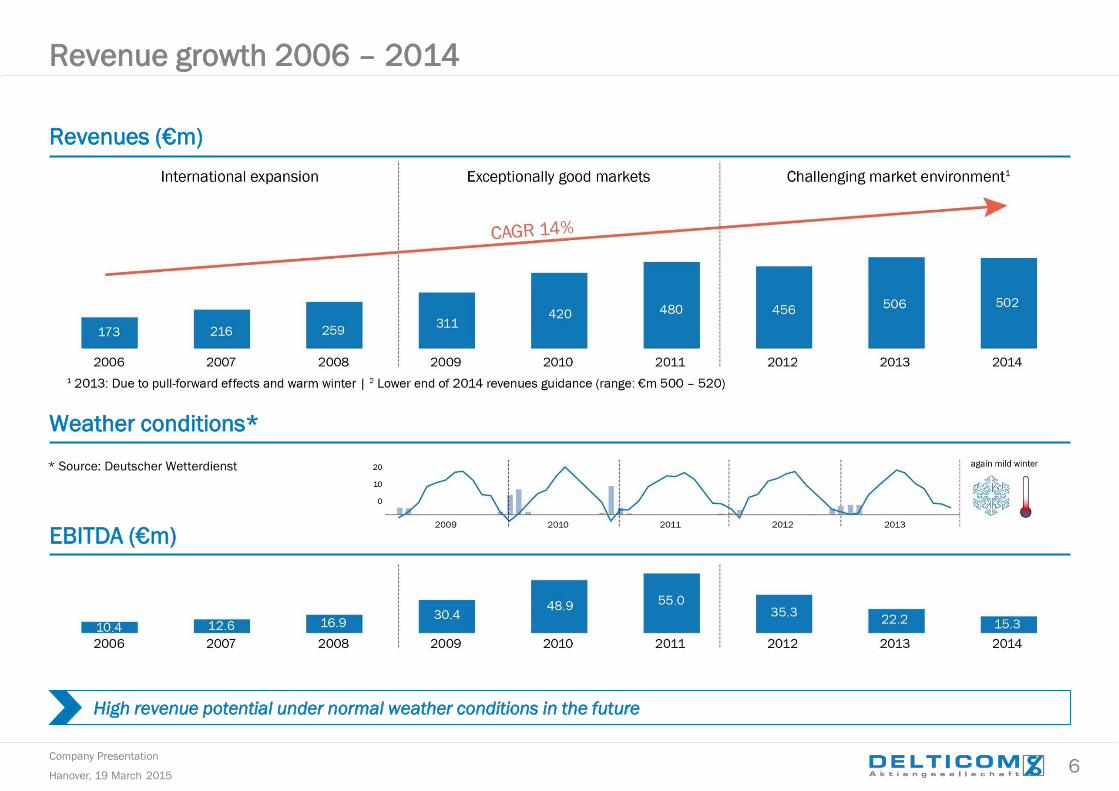

Revenue growth 2006 – 2014

Revenues (€m)

High revenue potential under normal weather conditions in the future

Weather conditions*

EBITDA (€m)

* Source: Deutscher Wetterdienst

Company Presentation

Hanover, 19 March 20157

Economies of scale

► Key player in all relevant European markets

► Margin advantages compared to smaller national players with respect to purchasing, logistics and operations

Delticom’s USPs are the basis for its market leading position

International player

► By far the largest E-Commerce tyre player in Europe► Together with Tirendo within the two top tyre online

shops in nearly every country

High cost efficiency

► Pooling of transportation► Outsourcing of support functions to low-cost countries

Logistics competence

► State-of-the-art warehousing► High delivery capacity and ability to

supply

► Loyal customer base: repeat customers bring overall acquisition costs down

► Substantial organic traffic in Delticom online shops► New Tirendo customer base has a minimal overlap

Customer base

USPs

Company Presentation

Hanover, 19 March 20158

Agenda

3-7 | Delticom group overview

8-11 | Replacement tyre business

12-17 | Strategy

18-22 | Financials FY 2014

23-24 | Outlook 2015

Company Presentation

Hanover, 19 March 20159

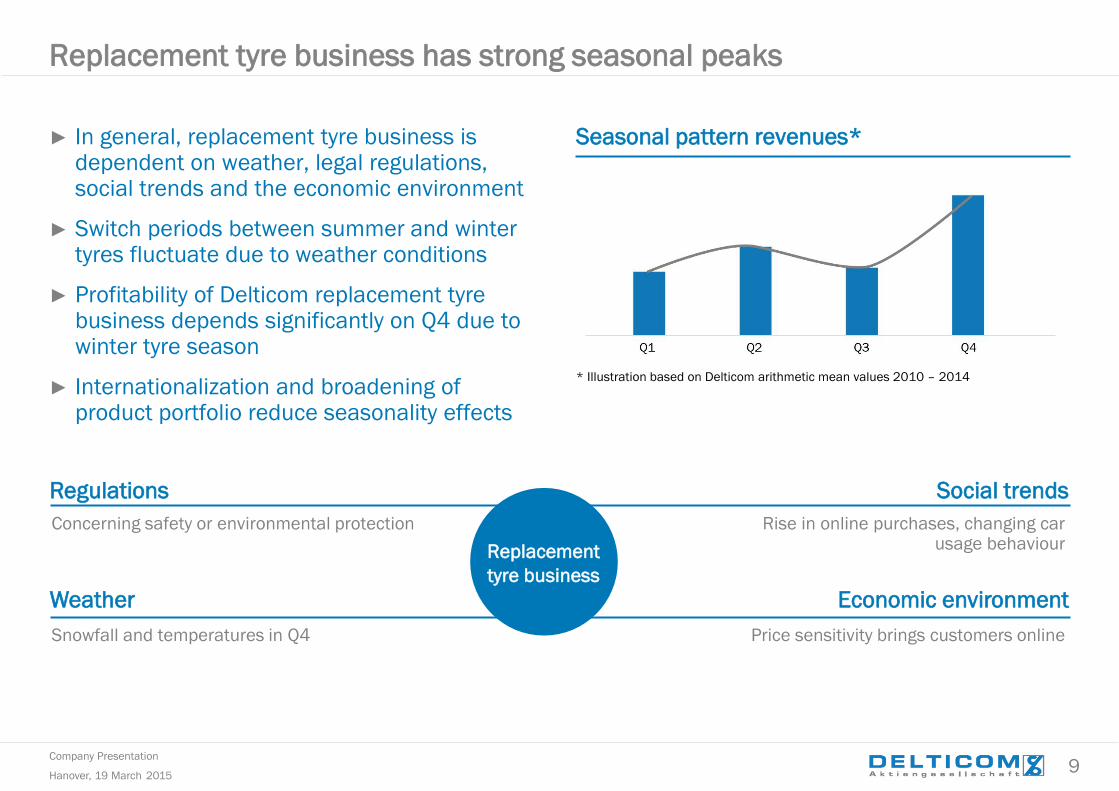

* Illustration based on Delticom arithmetic mean values 2010 – 2014

► In general, replacement tyre business is dependent on weather, legal regulations, social trends and the economic environment

► Switch periods between summer and winter tyres fluctuate due to weather conditions

► Profitability of Delticom replacement tyrebusiness depends significantly on Q4 due towinter tyre season

► Internationalization and broadening ofproduct portfolio reduce seasonality effects

Seasonal pattern revenues*

Replacement

tyre business

Social trends

Rise in online purchases, changing car usage behaviour

Regulations

Concerning safety or environmental protection

Economic environment

Price sensitivity brings customers online

Weather

Snowfall and temperatures in Q4

Replacement tyre business has strong seasonal peaks

Company Presentation

Hanover, 19 March 201510

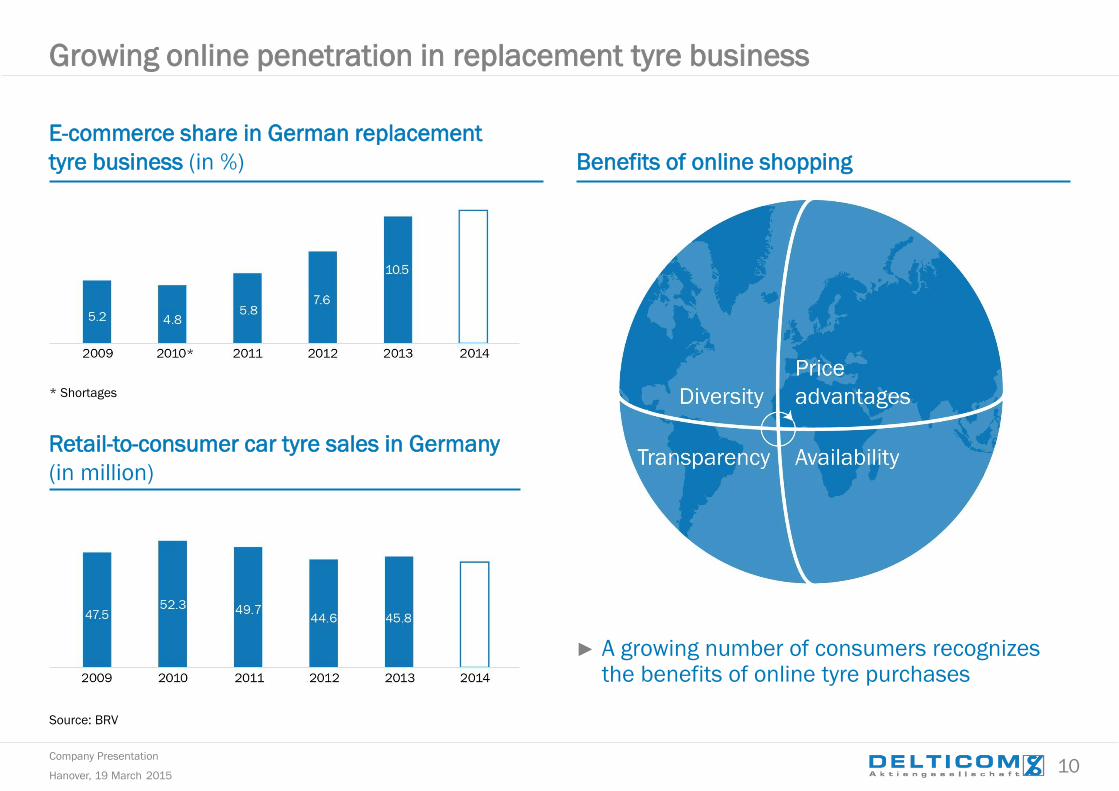

► A growing number of consumers recognizes the benefits of online tyre purchases

Growing online penetration in replacement tyre business

E-commerce share in German replacement

tyre business (in %)

Retail-to-consumer car tyre sales in Germany

(in million)

Benefits of online shopping

Source: BRV

* Shortages

Company Presentation

Hanover, 19 March 201511

* Sources: BRV, BMI, Statista, Eurostat, Euromonitor, IFH Köln, OECD, Roland Berger

► Internet usage is changing: increasing relevance as point of sale instead of just price and product comparison tool

► Combination of high basket value and low return rate for tyres

► Further offline to online shift expected

Growing online penetration in replacement tyre business

Online penetration (Germany)* (in %) Average basket value (Germany)* (in €)

Very low goods return rates (Germany)* (in %)

Company Presentation

Hanover, 19 March 201512

Agenda

3-7 | Delticom group overview

8-11 | Replacement tyre business

12-17 | Strategy

18-22 | Financials FY 2014

23-24 | Outlook 2015

Company Presentation

Hanover, 19 March 201513

Tirendo integration into Delticom – on track

Phase 1After acquisition 2013

Know-how exchange:

Existing IT infrastructure

complemented by modern

webshop technologies and new

analytical tools for online

marketing

Realizing synergy potential:

Integration of transport, storage

and finance operations

A house of strong B2C brands:

Integration of Tirendo business

under Delticom management

starting in H1/2014

Efficieny improvement process

started:

► Reducing Berlin headcount to

far below 50 (core team of

~20 employees in 2015)

► Less and more targeted TV

advertising

Reduced cost base implemented:

Reduced personnel expenses

Reduced rent and operating costs

Marketing costs with lower

cost/revenue ratio

Optimized TV advertising

spending

Using Tirendo strengths:

Tap into new customer group

Phase 2Start of full integrationH2/2014

Phase 3New organizational setupfrom 2015 onwards

Full integration of Tirendo completed

Quick wins realizedEfficiency improvement measures implemented

Way paved for break-even in 2015

Company Presentation

Hanover, 19 March 201514

► Increasing market share and drive penetration

► Focus on profitable growth and efficiency improvement

Strategic roadmap

Geographic expansion

Further developing of US business

Product portfolio expansion

Complete wheels, motorcycle tyres, specialty tyres

E-commerce tools

Conversion rate improvement with state-of-the-art tools

B2B

Broadening of B2B services

Cross-promotions

Cross-promoting between shops to keep customers in the group

Marketing

More targeted advertising

Spare parts and accessories

Tap market potential; one-stop shop for all parts

Price comparison

Using Toroleo to increase traffic on generic tyre-related domains

Logistics

Efficiency improvement measures

Purchasing

Data-driven purchasing organisation

Relaunch of online shops

Increase functionality

Mobile shops

Company Presentation

Hanover, 19 March 201515

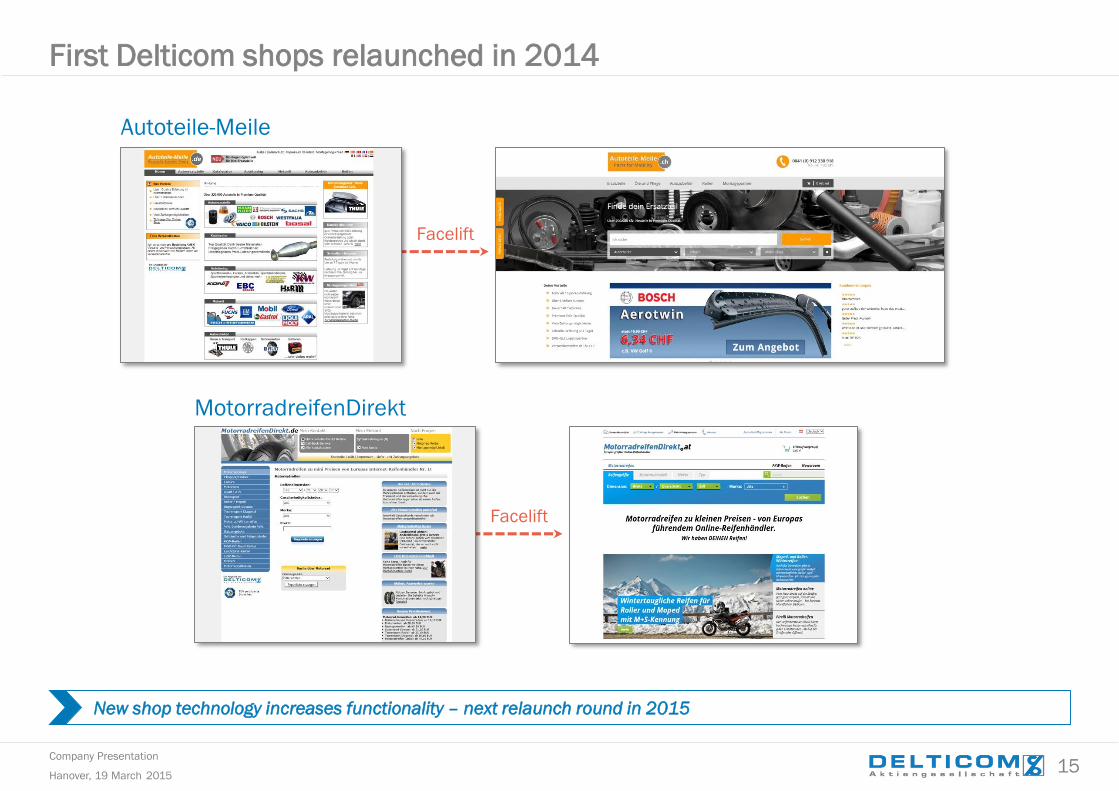

First Delticom shops relaunched in 2014

New shop technology increases functionality – next relaunch round in 2015

Facelift

Autoteile-Meile

Facelift

MotorradreifenDirekt

Company Presentation

Hanover, 19 March 201516

Complete Wheels

► Highly sophisticated own wheel assembly lines

► Professional assembly team for TPMS

► Wheel assembly of 13 up to 23 inch for passenger cars, SUVs, Vans, and Offroad cars

► Highest order flexibility and IT-based processes

► High availability of tires and rims through connected inventory > 100,000 rims

► Supplier for B2C, B2B, fleets, car dealers and industry

► Delticom wheels configurator for a quick and safe product advice – high quality pictures for a perfect impression of the selected wheel/tire combination on the customer's vehicle

► Easy ordering via the shops of Delticom

Company Presentation

Hanover, 19 March 201517

B2B services

B2B Retail

► 26 Onlineshops in 26 countries► More than 100K customers

► Car Dealer Business► Fastfitters► Garages► Fuel Stations► Franchise

Fleets

► 6 OnlineshopsDACH/FR/NL/UK

Fitting partner

► More than 40,000 fitting partners► > 9K in Germany► > 5K in France► > 4K in Italy► > 3K in Spain► > 2K in UK

► Tyre hotel

Mobile fitting

► Test in Germany (own branded)

Service

Company Presentation

Hanover, 19 March 201518

Agenda

3-7 | Delticom group overview

8-11 | Replacement tyre business

12-17 | Strategy

18-22 | Financials FY 2014

23-24 | Outlook 2015

Company Presentation

Hanover, 19 March 201519

Business FY 2014: Transition year

Macroeconomy

► Recovery in the Euro zone increasingly stumbled during the year

► Economic performance of the Euro countries remains divergent

► Consumption propensity of householdsin Germany remains high

Tirendo

► Reduced marketing spend in Q3+Q4 – higher efficiency► Reduced workforce: end of 01/15 <20 headcounts► EBITDA Q4/14 improved by € 1.3m

Tyre market

► Warm temperatures in March prompted early switch to summer tyres

► Q3: delayed start of winter season► Q4: mild winter in Europe► FY 2014: German winter tyre sales -13.3 %

(first BRV estimate)

Customer base FY

► 1,106 thousand new customers (including Tirendo)

► 774 thousand repeat customers► Customer base > 8 million

Revenues

► e-commerce revenues of 163 online shops flat yoy► Q4: volume growth > revenues growth

Toroleo acquisition in September

► tyre price comparison website Toroleo (toroleo.de, toroleo.at) will help increase traffic on up to 34 generic tyre-related domains owned by Delticom and not fully exploited yet

► Websites include e.g. reifen.de and pneus.fr

Transition

year 2014

Company Presentation

Hanover, 19 March 201520

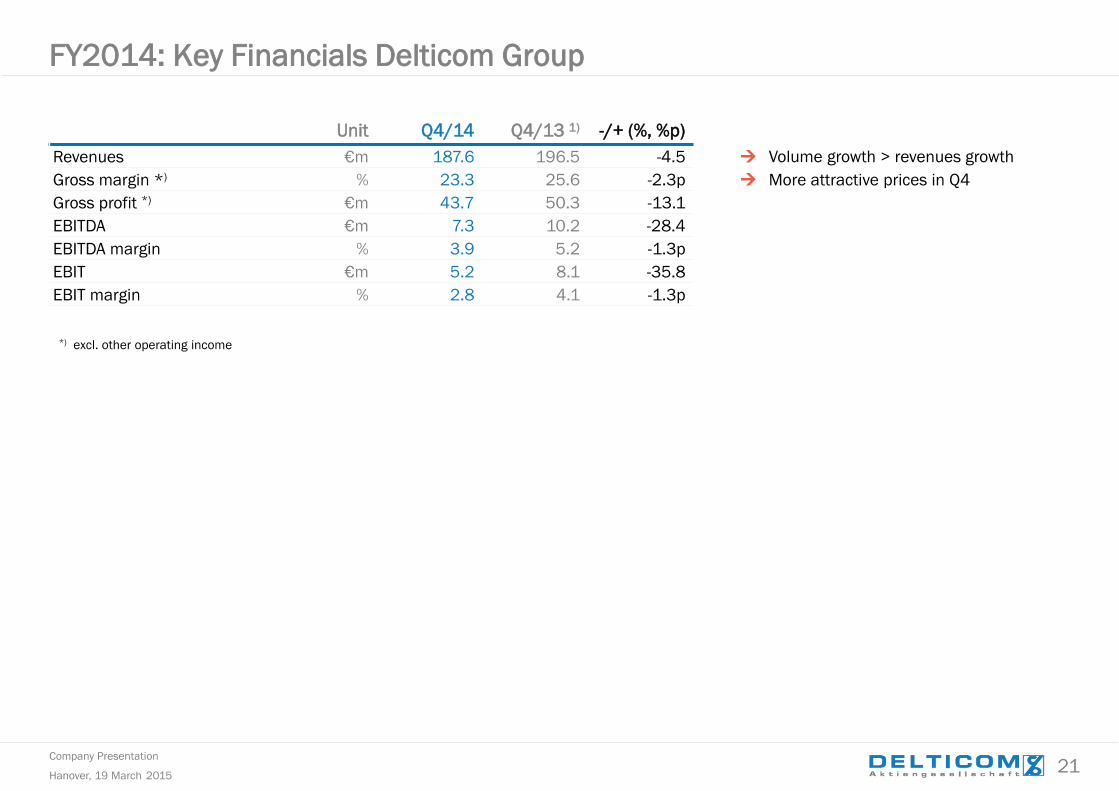

FY2014: Key Financials Delticom Group

Unit FY 2014 FY 2013 -/+ (%, %p)

New customers k 1,016 1,037 -2.0 New methodology

Revenues €m 501.7 505.5 -0.8 76.3 % of revenues in EU countries

Gross margin *) % 24.5 24.8 -0.3p

Gross profit *) €m 122.8 125.2 -1.9

EBITDA €m 15.3 22.2 -31.1

EBITDA margin % 3.0 4.4 -1.4p

PPA effect of €m 5.2EBIT €m 7.0 17.8 -60.6

EBIT margin % 1.4 3.5 -2.1

Net income €m 2.9 11.6 -75.3

Earnings per share (undiluted) € 0.24 0.97 -75.3

Liquidity position €m 30.0 11.3 164.7 Swing back after Tirendo acquisition

Operating cash flow €m 36.7 8.1

Free cash flow €m 35.0 -35.2

Unit 31.12.14 31.12.13 -/+ (%, %p)

Inventories €m 56.2 72.8 -22.9 According to plan

Equity €m 50.3 51.7 -2.7

Equity ratio % 30.7 29.2 +1.5p

*) excl. other operating income

Company Presentation

Hanover, 19 March 201521

FY2014: Key Financials Delticom Group

Unit Q4/14 Q4/13 1) -/+ (%, %p)

Revenues €m 187.6 196.5 -4.5 Volume growth > revenues growth

Gross margin *) % 23.3 25.6 -2.3p More attractive prices in Q4

Gross profit *) €m 43.7 50.3 -13.1

EBITDA €m 7.3 10.2 -28.4

EBITDA margin % 3.9 5.2 -1.3p

EBIT €m 5.2 8.1 -35.8

EBIT margin % 2.8 4.1 -1.3p

*) excl. other operating income

Company Presentation

Hanover, 19 March 201522

in €m 31.12.14 % '-/+ (%) 31.12.13 %

Assets

Non-current assets 58.1 35.4 -12.8 66.7 30.2

Current assets 105.9 64.6 -4.0 110.3 69.8

Inventories 56.2 34.2 -22.9 72.8 51.8

Receivables 19.8 12.0 -24.4 26.2 14.1

Liquidity 30.0 18.3 +164.7 11.3 3.9

Assets 164.0 100.0 -7.4 177.0 100.0

Equity and Liabilities

Long-term funds 66.9 41.0 +3.6 64.6 23.2

Equity 50.3 31.0 -2.7 51.7 19.9

Long-term debt 16.7 10.2 +28.5 13.0 3.3

Provisions 0.4 0.2 +39.2 0.3 0.1

Liabilities 16.3 9.9 +25.4 13.0 3.2

Short-term debt 97.1 59.2 -13.6 112.4 76.8

Provisions 2.4 1.4 +26.4 2.0 0.8

Liabilities 94.7 57.7 -46.5 110.4 76.0

thereof accounts payable 75.9 46.3 +1.6 74.7 42.2

Equity and Liabilities 164.0 100.0 -7.4 177.0 100.0

FY2014: Abridged balance sheet

Company Presentation

Hanover, 19 March 201523

Agenda

3-6 | Delticom group overview

7-11 | Replacement tyre business

12-17 | Strategy

18-22 | Financials FY 2014

23-24 | Outlook 2015

Company Presentation

Hanover, 19 March 201524

Market

At present significant uncertaintities regarding

market and price trends in European

replacement tyres business (low visibility)

Excess inventory for winter goods in the supply

chain possible

US import duties for tyres made in China –

import to Europe?

BVR not expecting a far-reaching business

improvement for 2015

Outlook 2015

Investor Relations

Melanie GerekeDelticom AGBrühlstr. 1130169 Hanover, Germany

eMail: [email protected]: +49-511-93634-8903

Delticom

Turnover + EBITDA (abs.) at least flat yoy

Increase in volume vs. 2014

2015: Tirendo break-even

Over 1m new customers in 2015

Expand market leadership

Company Presentation

Hanover, 19 March 201525

Q&A

Company Presentation

Hanover, 19 March 201526

in €m FY 2014 FY 2013 -/+ (%, %p)

Revenues 501.7 505.5 -0.8

Other operating income 12.1 5.4 +123.4

Total operating income 513.8 511.0 +0.6

Cost of goods sold -379.0 -380.3 -0.4

Gross profit 134.9 130.6 +3.3

Personnel expenses -15.6 -11.3 +38.1

Other operating expenses -104.0 -97.2 +7.1

EBITDA 15.3 22.2 -31.1

Depreciation -8.3 -4.3 +90.2

EBIT 7.0 17.8 -60.6

Financial expense -0.8 -0.2 +350.0

Financial income 0.03 0.05 -30.6

Net financial result -0.8 -0.1 +492.6

EBT 6.3 17.7 -64.6

Income taxes -3.4 -6.2 -44.6

Consolidated net Income 2.9 11.6 -75.3

FY2014: P+L statement

Company Presentation

Hanover, 19 March 201527

in €m FY 2014 FY 2013

Earnings before interest and taxes (EBIT) 7.0 17.8

Cash flow from operating activities 36.7 8.1

Cash flow from investing activities -1.6 -43.3

Cash flow from financing activities -16.9 +0.5

Changes in cash and cash equivalents 18.4 -34.9

Cash and cash equivalents at the start of the period 11.3 46.2

Changes in the scope of consolidation 0.2 0

Cash and cash equivalents - end of period 30.0 11.3

FY2014: Abridged cash flow statement

Company Presentation

Hanover, 19 March 201528

in €m 31.12.14 % '-/+ (%) 31.12.13 %

Assets

Non-current assets 58.1 35.4 -12.8 66.7 37.7

Intangible assets 47.9 29.2 -9.2 52.8 29.8

Property, plant and equipment 9.0 5.5 -16.1 10.7 6.0

Financial assets 0.0 0.0 -97.0 0.8 0.5

Deferres taxes 0.7 0.4 -62.2 1.9 1.1

Other receivables 0.5 0.3 -3.2 0.5 0.3

Current assets 105.9 64.6 -4.0 110.3 62.3

Inventories 56.2 34.2 -22.9 72.8 41.1

Accounts receivable 14.5 8.8 -28.7 11.3 6.4

Other current assets 4.7 2.9 -62.6 12.6 7.1

Income tax receivables 0.5 0.3 -76.2 2.3 1.3

Cash and cash equivalents 30.0 18.3 +164.7 11.3 6.4

Assets 164.0 100.0 -7.4 177.0 100.0

FY2014: Balance sheet – Assets

Company Presentation

Hanover, 19 March 201529

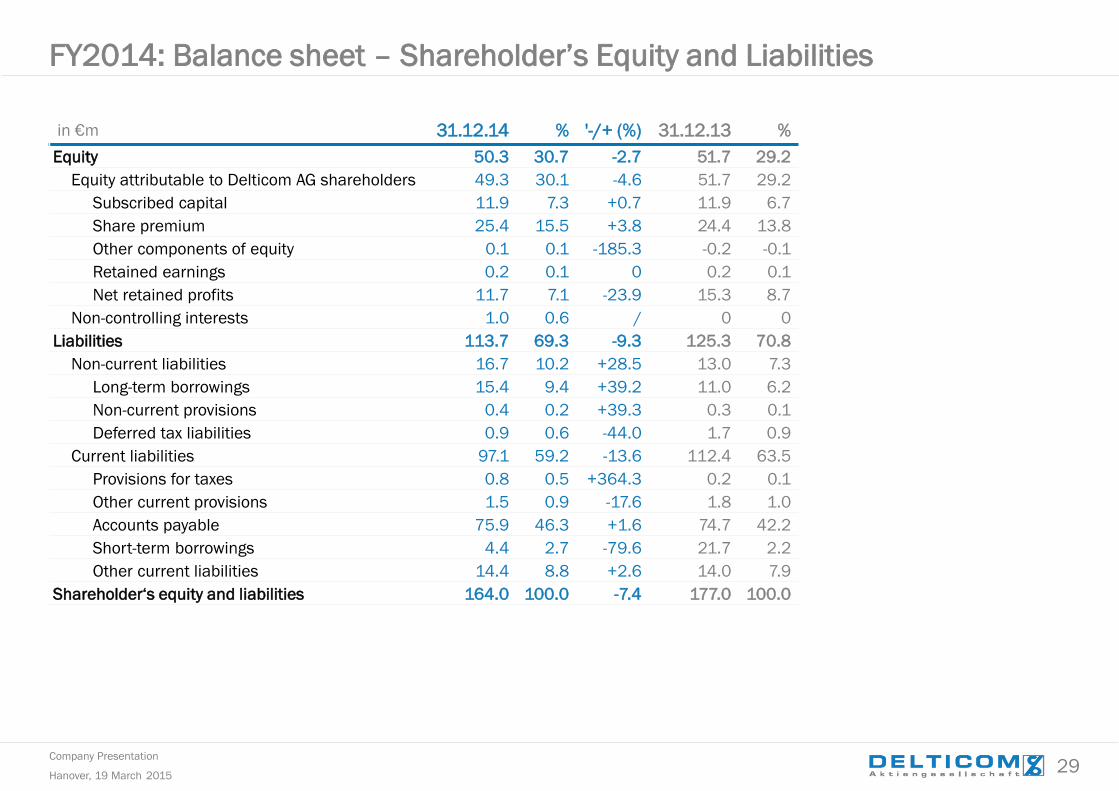

in €m 31.12.14 % '-/+ (%) 31.12.13 %

Equity 50.3 30.7 -2.7 51.7 29.2

Equity attributable to Delticom AG shareholders 49.3 30.1 -4.6 51.7 29.2

Subscribed capital 11.9 7.3 +0.7 11.9 6.7

Share premium 25.4 15.5 +3.8 24.4 13.8

Other components of equity 0.1 0.1 -185.3 -0.2 -0.1

Retained earnings 0.2 0.1 0 0.2 0.1

Net retained profits 11.7 7.1 -23.9 15.3 8.7

Non-controlling interests 1.0 0.6 / 0 0

Liabilities 113.7 69.3 -9.3 125.3 70.8

Non-current liabilities 16.7 10.2 +28.5 13.0 7.3

Long-term borrowings 15.4 9.4 +39.2 11.0 6.2

Non-current provisions 0.4 0.2 +39.3 0.3 0.1

Deferred tax liabilities 0.9 0.6 -44.0 1.7 0.9

Current liabilities 97.1 59.2 -13.6 112.4 63.5

Provisions for taxes 0.8 0.5 +364.3 0.2 0.1

Other current provisions 1.5 0.9 -17.6 1.8 1.0

Accounts payable 75.9 46.3 +1.6 74.7 42.2

Short-term borrowings 4.4 2.7 -79.6 21.7 2.2

Other current liabilities 14.4 8.8 +2.6 14.0 7.9

Shareholder‘s equity and liabilities 164.0 100.0 -7.4 177.0 100.0

FY2014: Balance sheet – Shareholder’s Equity and Liabilities