Embed Size (px)

Citation preview

June 17th, 2014

Deloitte and Salesforce.com

© 2014 Deloitte

Agenda

• Key challenges

• SFDC and GSI

• Our SFDC practice at Deloitte

© 2014 Deloitte

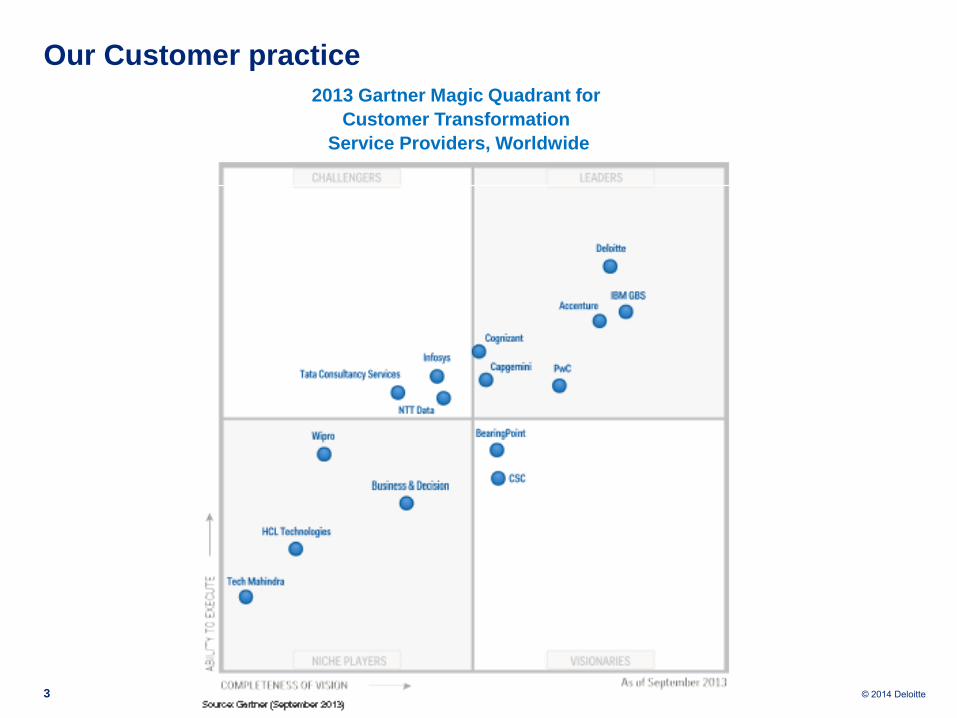

Our Customer practice

3

2013 Gartner Magic Quadrant for

Customer Transformation

Service Providers, Worldwide

© 2014 Deloitte

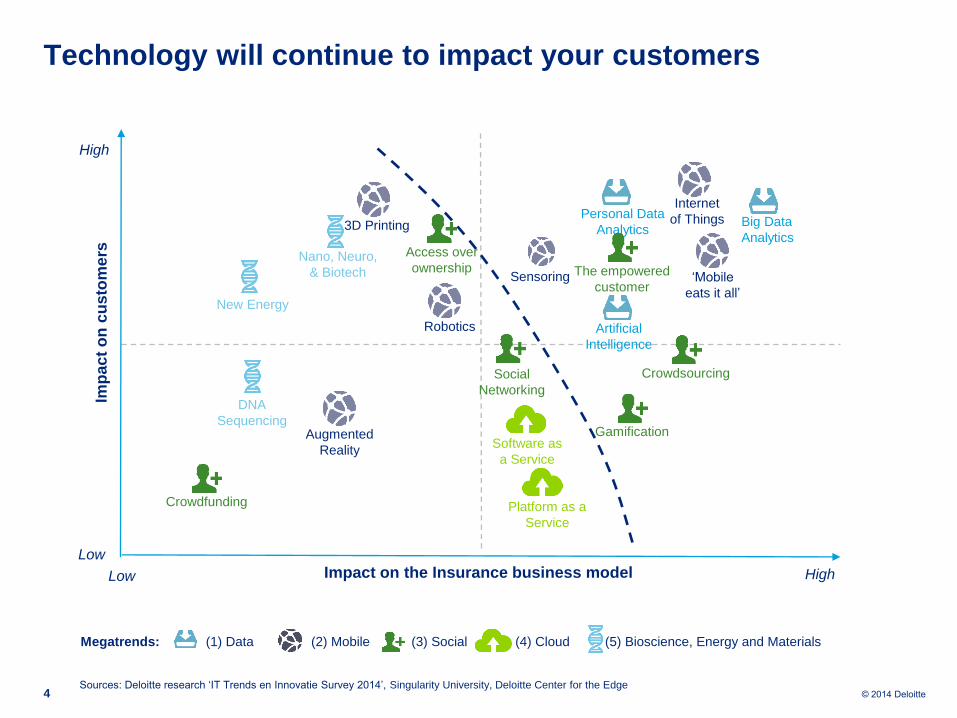

Technology will continue to impact your customers

4

(2) Mobile (3) Social (5) Bioscience, Energy and Materials (4) Cloud

Sources: Deloitte research ‘IT Trends en Innovatie Survey 2014’, Singularity University, Deloitte Center for the Edge

Megatrends: (1) Data

Impact on the Insurance business model

Imp

ac

t o

n c

usto

me

rs

High

Low

High Low

Crowdfunding

Augmented

Reality Software as

a Service

DNA

Sequencing

New Energy

Personal Data

Analytics

Platform as a

Service

Nano, Neuro,

& Biotech

Social

Networking

Crowdsourcing

3D Printing

Sensoring

Internet

of Things

Artificial

Intelligence

Robotics

Big Data

Analytics Access over

ownership ‘Mobile

eats it all’

Gamification

The empowered

customer

© 2014 Deloitte

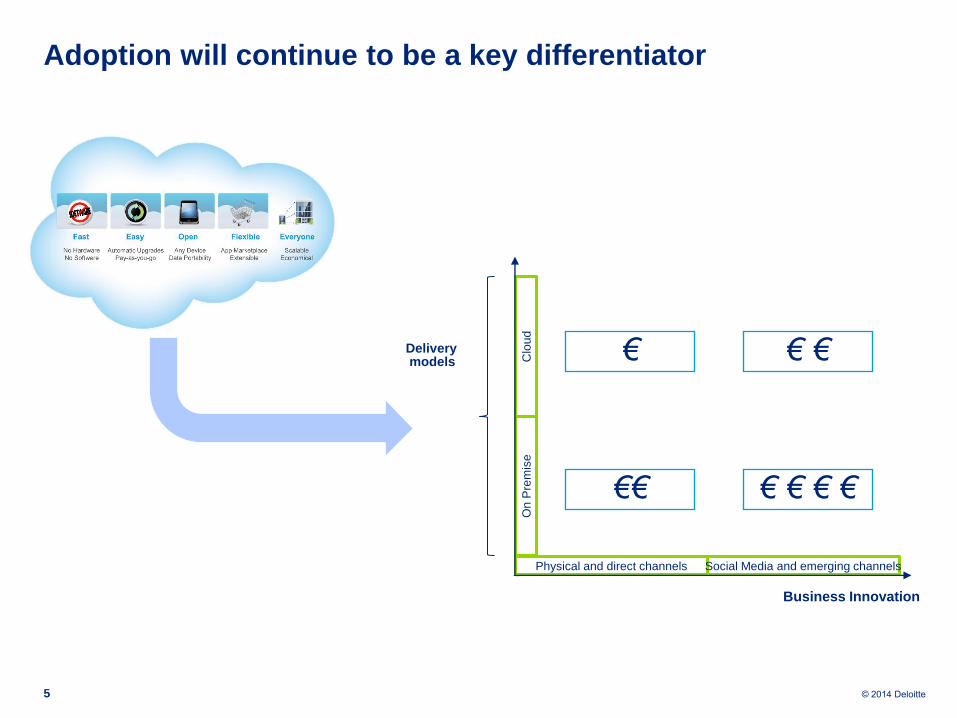

Adoption will continue to be a key differentiator

5

Business Innovation

Delivery models € €

Physical and direct channels Social Media and emerging channels

On

Pre

mis

e

Clo

ud

€ € € € €€

€

© 2014 Deloitte

Agenda

• Key challenges

• SFDC and GSI

• Our SFDC practice at Deloitte

© 2014 Deloitte

Salesforce.com continue to grow ahead of competition

Salesforce.com Update:

• Current Market Cap: $33.35B

• FY15 Q1 Revenue Growth of 37% (42% in EMEA)

• FY 2014 revenue growth of 41% in Europe

• Plans to open new data centres in UK, France and Germany

• Cloud Ecosystem: ~2k Apps, Over Two million installs

• Significant expansion into ‘Non Core’ markets

#1 Salesforce: World’s #1 CRM

Enterprise Cloud Computing Market Share

#1 World’s Most Innovative Company

2011, 2012, 2013

#1 Market Leader: Enterprise, MidMarket, SMB & Sales Force Automation

#1

© 2014 Deloitte

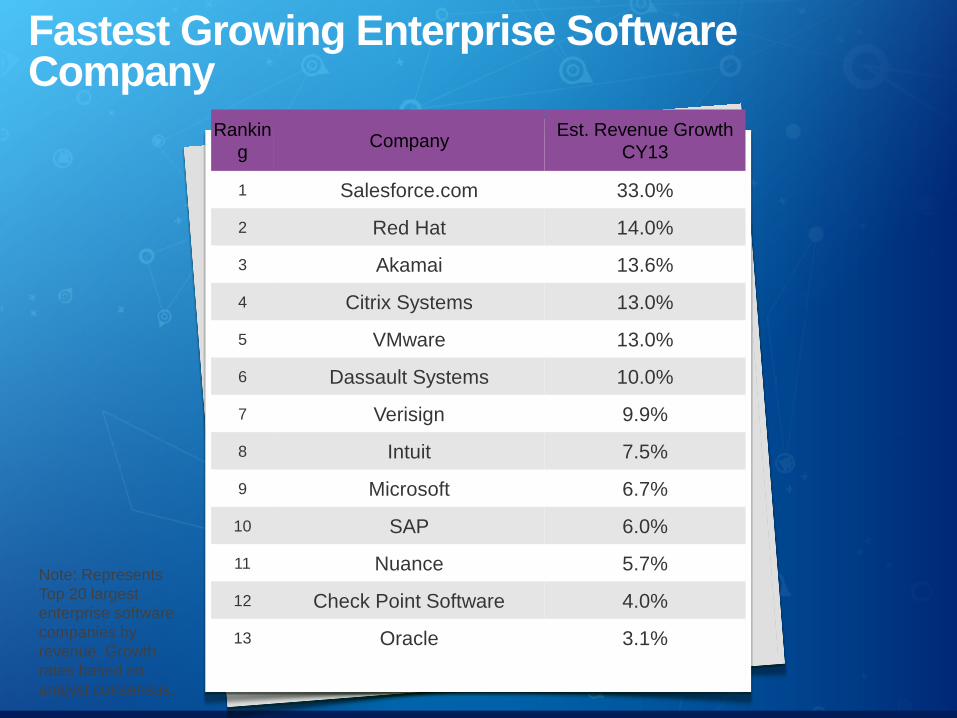

Fastest Growing Enterprise Software Company

Note: Represents

Top 20 largest

enterprise software

companies by

revenue. Growth

rates based on

analyst consensus.

Rankin

g Company

Est. Revenue Growth

CY13

1 Salesforce.com 33.0%

2 Red Hat 14.0%

3 Akamai 13.6%

4 Citrix Systems 13.0%

5 VMware 13.0%

6 Dassault Systems 10.0%

7 Verisign 9.9%

8 Intuit 7.5%

9 Microsoft 6.7%

10 SAP 6.0%

11 Nuance 5.7%

12 Check Point Software 4.0%

13 Oracle 3.1%

© 2014 Deloitte

Deep Commitment to Working with Partners

Subscription model guarantees that Salesforce always “has

skin in the game” • We support customer success long after the deal is signed

• We ensure long term customer success with excellent partner

implementations

• We train, certify, build solutions and collaborate with the right

partner for your unique situation

Salesforce Product

and

Support Excellence

Partner

Implementation

Excellence

Customer

Success

Partner Selection + Implementation Excellence =

Customer Success

© 2014 Deloitte

Our Partners Share Our Commitment to Your Success

Our Partners:

• Have 20,500+ advanced Salesforce

certifications held by 16,000+ individuals

• Are evaluated for 100% of $200K+ deals

for implementation qualifications

• Over 350 SI Partners across EMEA

Our Partner Program Measures:

• Technical Certifications

• Customer Satisfaction

• Success Stories

• Industry and Product Expertise

• Partner Influenced growth

Customer

Success

The right partner is key to customer success

© 2014 Deloitte

Cloud Alliance Partner Tiers

Demonstrated success in global

implementations

SFDC presence and across multiple regions

Demonstrated proficiency in SFDC niche

implementations

Certified individuals and minimum project

requirements

Regional Partners with either:

A discovery and analysis focus OR a delivery and

operations focus

Qualifications and

Sample Partners

Platinum

Gold

Silver

Global

Strategic

Demonstrated success in complex implementations

Certifications and presence in country

Customer Satisfaction Required Across All Tiers

© 2014 Deloitte

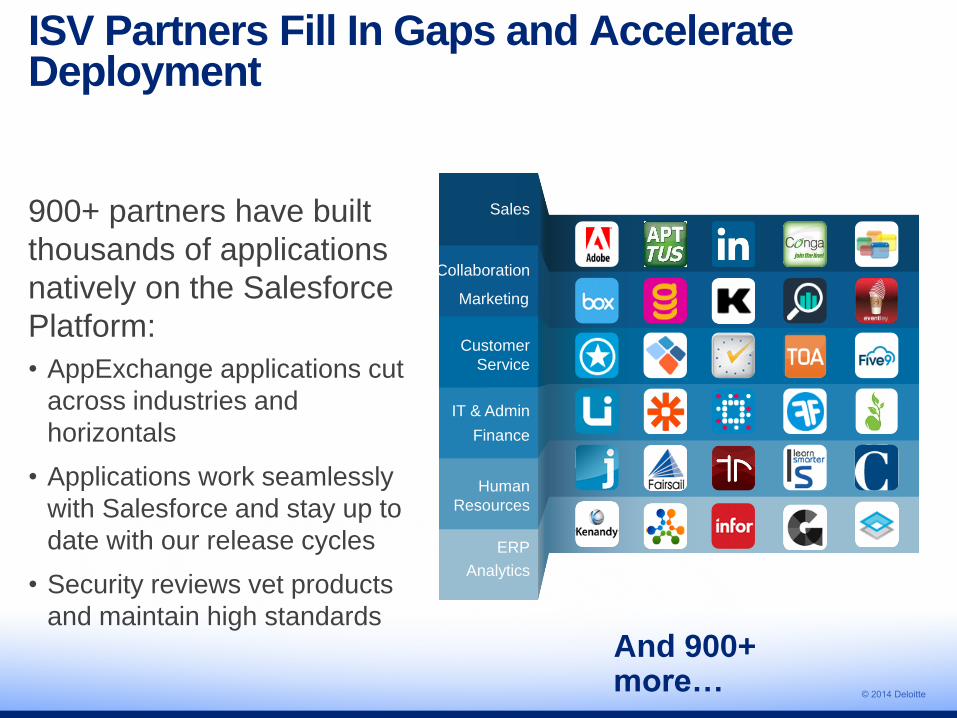

ISV Partners Fill In Gaps and Accelerate Deployment

900+ partners have built

thousands of applications

natively on the Salesforce

Platform:

• AppExchange applications cut

across industries and

horizontals

• Applications work seamlessly

with Salesforce and stay up to

date with our release cycles

• Security reviews vet products

and maintain high standards

And 900+ more…

Sales

Customer

Service

Marketing

IT & Admin

Human

Resources

Finance

ERP

Collaboration

Analytics

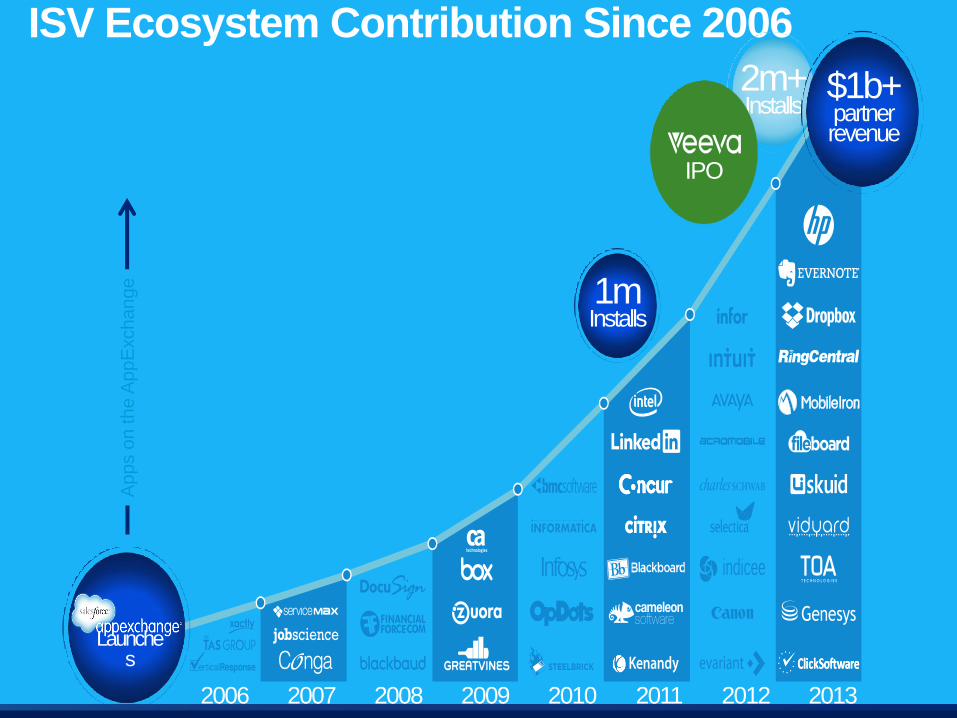

ISV Ecosystem Contribution Since 2006

2m+ Installs

2010 2013 2012 2011 2009 2008 2007 2006

Ap

ps o

n th

e A

pp

Exch

an

ge

Launches

1m Installs

$1b+ partner revenue

IPO

© 2014 Deloitte

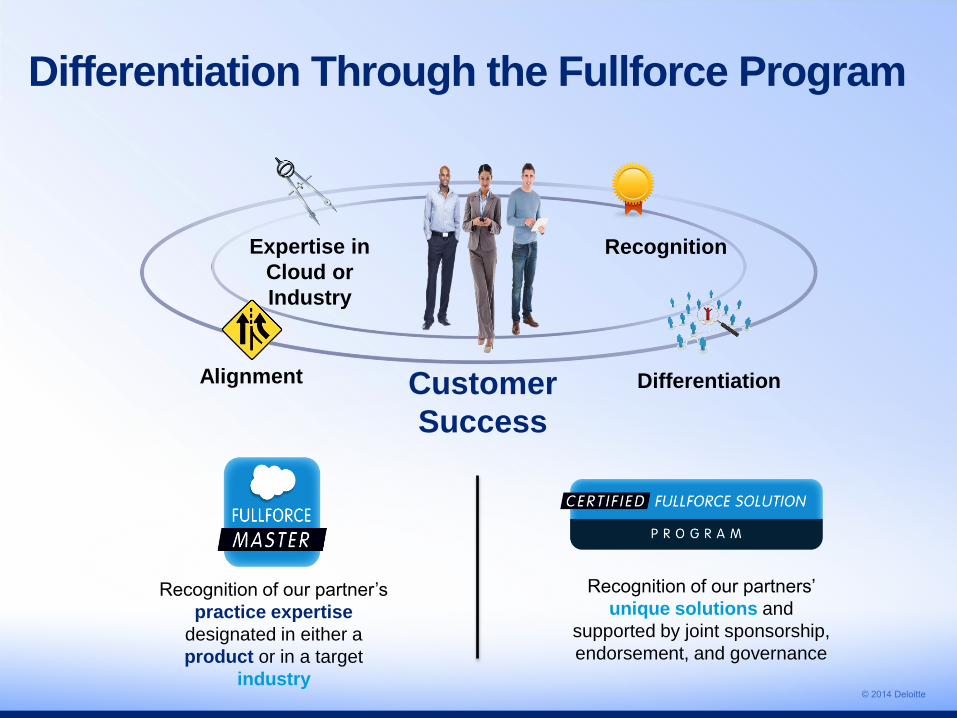

Differentiation Through the Fullforce Program

Recognition

Alignment Differentiation Customer

Success

Expertise in

Cloud or

Industry

Recognition of our partner’s

practice expertise

designated in either a

product or in a target

industry

Recognition of our partners’

unique solutions and

supported by joint sponsorship,

endorsement, and governance

© 2014 Deloitte

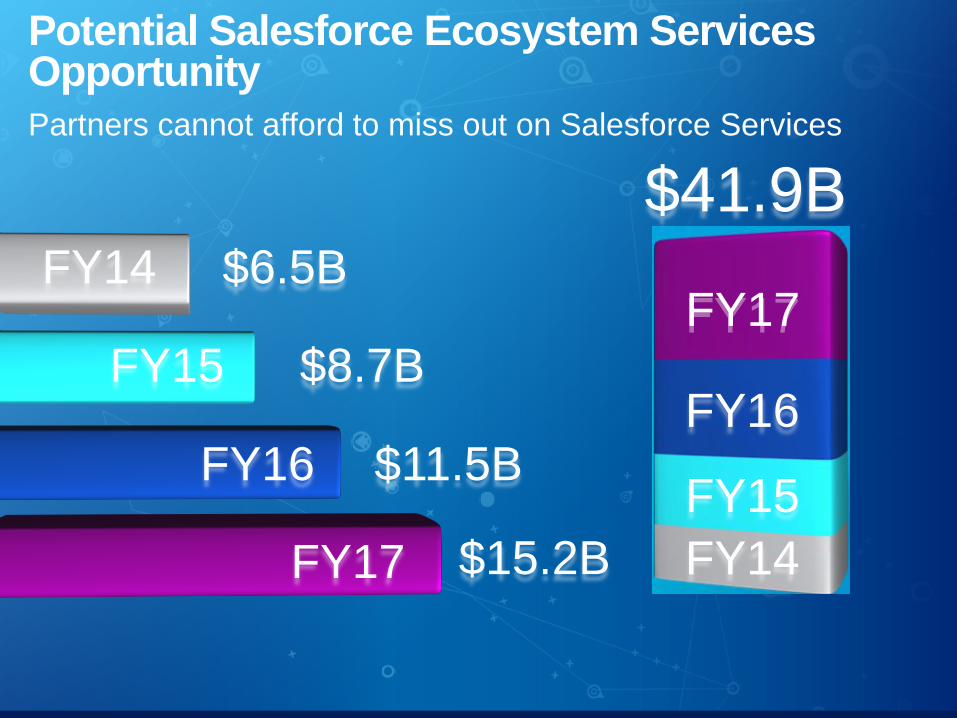

Potential Salesforce Ecosystem Services Opportunity Partners cannot afford to miss out on Salesforce Services

$8.7B

$11.5B

$41.9B

FY15

FY16

FY17

FY14

$6.5B

$15.2B

FY15

FY16

FY17

FY14

© 2014 Deloitte

Top Partners Have Expertise

Industry Expertise

‒ Understand your business

‒ Experience in your country / region / language

‒ In depth knowledge of systems to be migrated

Salesforce Expertise & Assets

‒ Cloud-specific certifications

‒ Technical & Solution Architects

‒ Methodologies, Accelerators, Apps, etc.

Jointly work with Salesforce

‒ Develop the market with us

‒ Build solutions on our Platform

‒ Work in conjunction with our Customer

Success teams

© 2014 Deloitte

Agenda

• Key challenges

• SFDC and GSI

• Our SFDC practice at Deloitte

© 2014 Deloitte

+ =

18

• First projects in 2006 and a global alliance in 2011

• #1 or #2 in all key alliance metrics with Salesforce.com

• Active practices 20 countries

• Very mature practices in US, UK, Belgium, The Netherlands and Japan

• Known for our capabilities in Service Cloud, Social Business, and

Industry Sector expertise (Technology, Insurance, Banking, Life

Sciences, Media) with 2 global awards in 2014

• Significant joint marketing through PR and 20+ major event

sponsorships in 11 countries

© 2014 Deloitte

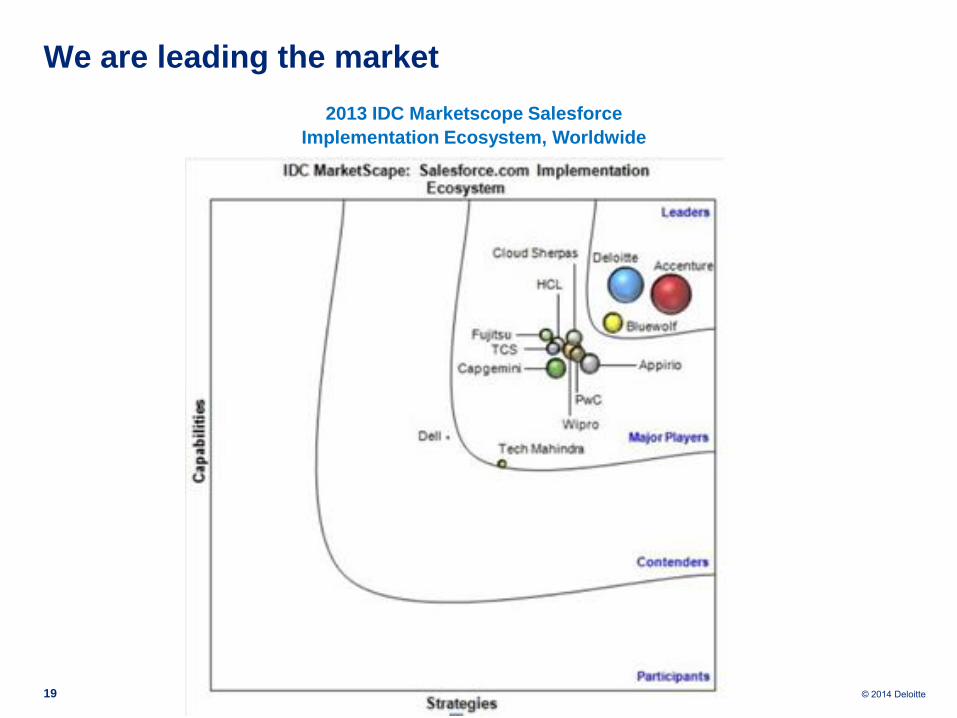

We are leading the market

19

2013 IDC Marketscope Salesforce

Implementation Ecosystem, Worldwide

© 2014 Deloitte

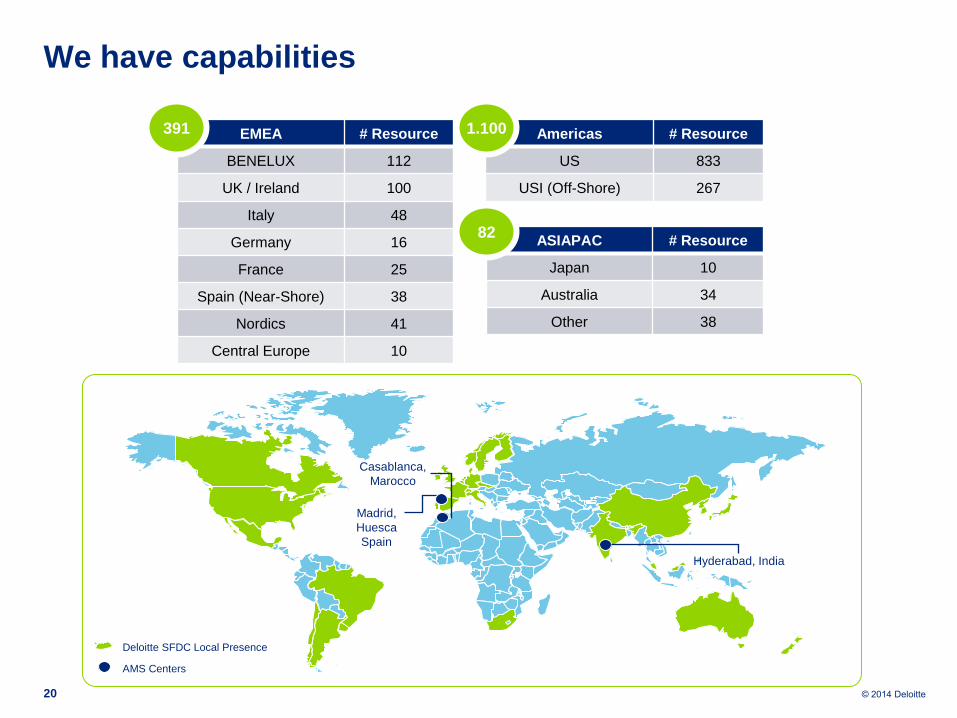

We have capabilities

20

EMEA # Resource

BENELUX 112

UK / Ireland 100

Italy 48

Germany 16

France 25

Spain (Near-Shore) 38

Nordics 41

Central Europe 10

Americas # Resource

US 833

USI (Off-Shore) 267

ASIAPAC # Resource

Japan 10

Australia 34

Other 38

Deloitte SFDC Local Presence

AMS Centers

Hyderabad, India

Madrid,

Huesca

Spain

Casablanca,

Marocco

391 1.100

82

© 2014 Deloitte

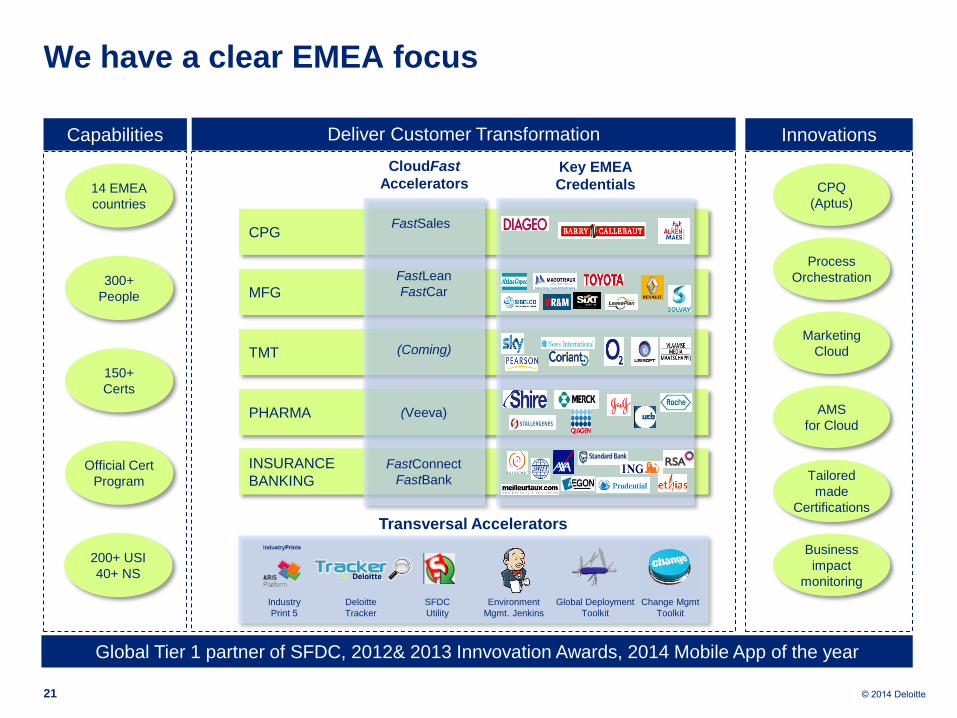

We have a clear EMEA focus

21

14 EMEA

countries

300+

People

150+

Certs

Official Cert

Program

CPG

MFG

TMT

PHARMA

INSURANCE

BANKING

FastSales

200+ USI

40+ NS

Process

Orchestration

Marketing

Cloud

FastLean

FastCar

(Veeva)

FastConnect

FastBank

CloudFast

Accelerators Key EMEA

Credentials

Capabilities Deliver Customer Transformation Innovations

Transversal Accelerators

Change Mgmt

Toolkit

Global Deployment

Toolkit

Environment

Mgmt. Jenkins

Deloitte

Tracker

Industry

Print 5

SFDC

Utility

CPQ

(Aptus)

AMS

for Cloud

Business

impact

monitoring

Tailored

made

Certifications

Global Tier 1 partner of SFDC, 2012& 2013 Innvovation Awards, 2014 Mobile App of the year

(Coming)

© 2014 Deloitte

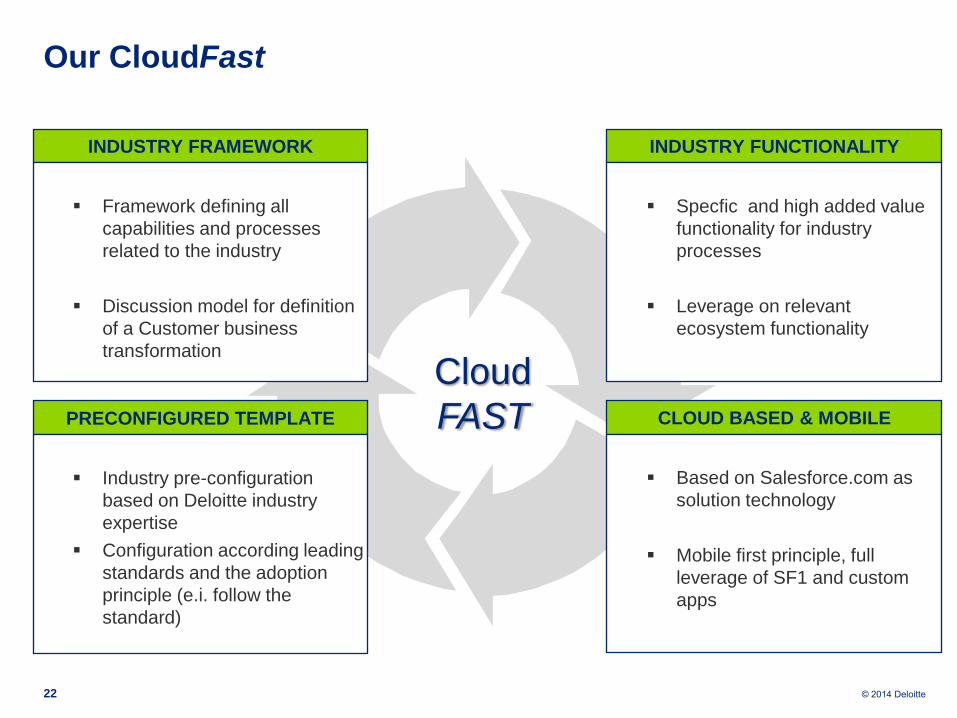

Our CloudFast

22

INDUSTRY FRAMEWORK

Framework defining all

capabilities and processes

related to the industry

Discussion model for definition

of a Customer business

transformation

PRECONFIGURED TEMPLATE

Industry pre-configuration

based on Deloitte industry

expertise

Configuration according leading

standards and the adoption

principle (e.i. follow the

standard)

CLOUD BASED & MOBILE

Based on Salesforce.com as

solution technology

Mobile first principle, full

leverage of SF1 and custom

apps

Cloud

FAST

INDUSTRY FUNCTIONALITY

Specfic and high added value

functionality for industry

processes

Leverage on relevant

ecosystem functionality

© 2014 Deloitte

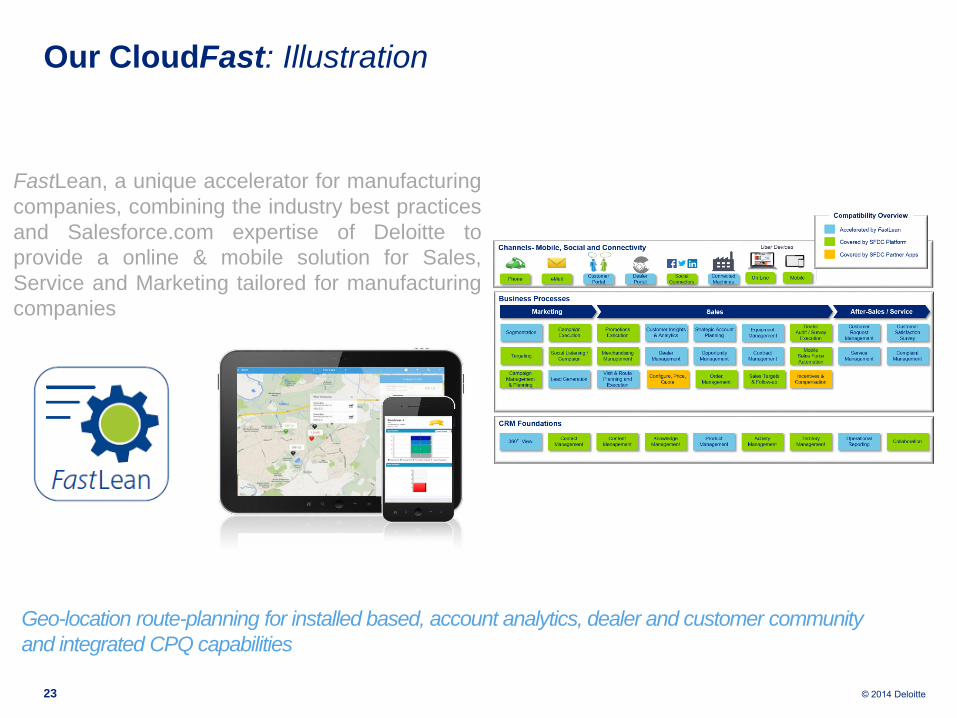

Our CloudFast: Illustration

23

FastLean, a unique accelerator for manufacturing

companies, combining the industry best practices

and Salesforce.com expertise of Deloitte to

provide a online & mobile solution for Sales,

Service and Marketing tailored for manufacturing

companies

Geo-location route-planning for installed based, account analytics, dealer and customer community

and integrated CPQ capabilities

© 2014 Deloitte

We have the flexibility to support your ambitions

24

Tra

nsfo

rma

tio

n A

dvis

ory

Business Advisory

Limited Multiple

Needs a

re d

escribed

S

cop

e is d

efine

d

Your requirements

Business

interactions