Embed Size (px)

Citation preview

Sustainable Finance: A review of the impact of Responsible Investment (RI) practices on the environment

Report to DEFRA by RiskMetrics Sustainability Solutions Group

July 2009

www.defra.gov.uk

Department for Environment, Food and Rural AffairsNobel House17 Smith SquareLondon SW1P 3JRTelephone 020 7238 6000Website: www.defra.gov.uk

© Crown copyright 2009Copyright in the typographical arrangement and design rests with the Crown.

This publication (excluding the royal arms and departmental logos) may be re-used free of charge in any format or medium provided that it is re-used accurately and not used in a misleading context. The material must be acknowledged as crown copyright and the title of the publication specified.

Information about this publication and further copies are available from:

DefraArea 5CErgon HouseHorseferry RoadLondonSW1P 2AL

Tel: 0207 238 1650

Email: [email protected]

This document is available on the Defra website:

http://defraweb/environment/business/scp/evidence/theme4/sustain-business0708.htm

Published by the Department for Environment, Food and Rural Affairs

2

Table of ContentsChapters

EXECUTIVE SUMMARY............................................................................................................................................... 5

1. INTRODUCTION....................................................................................................................................... 13

1.1 CONCEPTUAL FRAMEWORK...........................................................................................................................141.2 OBJECTIVES OF STUDY..........................................................................................................................................171.3 METHODOLOGY..................................................................................................................................................18

2. ENVIRONMENTAL INVESTING STRATEGIES...............................................................................................20

2.1 WHAT IS RESPONSIBLE INVESTING?.........................................................................................................................202.2 RI TECHNIQUES AND THEIR INFLUENCE ON CORPORATE BEHAVIOUR...............................................................................222.3 PERFORMANCE OF ENVIRONMENTAL INVESTING STRATEGIES........................................................................................32

3. LITERATURE REVIEW OF ENVIRONMENTAL EFFICACY IN INVESTMENTS....................................................36

3.1 OVERALL FINDINGS..............................................................................................................................................363.2 RI AND ENVIRONMENTAL PERFORMANCE.................................................................................................................373.3 APPROACHES TO MEASURING ENVIRONMENTAL PERFORMANCE....................................................................................423.4 CONCLUSIONS.....................................................................................................................................................44

4. SURVEY OF FUNDS WITH ENVIRONMENTAL INVESTMENT ELEMENT........................................................46

4.1 SURVEY METHODOLOGY........................................................................................................................................464.2 OVERALL FINDINGS..............................................................................................................................................474.3 CONCLUSIONS.....................................................................................................................................................57

5. BEST PRACTICES IN MEASURING ENVIRONMENTAL PERFORMANCE.........................................................60

5.1 SELECTED CASE STUDIES........................................................................................................................................61

6. TRENDS IMPACTING INVESTOR STRATEGIES............................................................................................70

6.1 GLOBAL INITIATIVES.............................................................................................................................................706.2 RI INDICES.........................................................................................................................................................766.3 COMPANY LEVEL TRENDS......................................................................................................................................77

7. CONCLUSIONS......................................................................................................................................... 79

8. REFERENCES............................................................................................................................................ 81

9. ANNEX.................................................................................................................................................... 85

A. SUMMARY OF LITERATURE REVIEW.........................................................................................................................86B. LIST OF FUNDS CONTACTED IN SURVEY....................................................................................................................93C. SURVEY QUESTIONNAIRE......................................................................................................................................96D. EcoValue 21™ Rating Methodology.............................................................................................................102

3

Figures

FIGURE 1 SUSTAINABLE ENERGY FUNDS BY TYPE AND ASSET CLASS........................................................................21

FIGURE 2 ORIGIN OF STUDIES IN LITERATURE REVIEW............................................................................................37

FIGURE 3 NUMBER OF CORRELATIONS BETWEEN RI AND ENVIRONMENTAL PERFORMANCE...................................38

FIGURE 4 BASIC FUND INFO.................................................................................................................................... 48

FIGURE 5 ENVIRONMENTAL INVESTMENT STRATEGY OF FUNDS.............................................................................49

FIGURE 6 ENVIRONMENTAL OBJECTIVES OF INVESTMENT STRATEGIES...................................................................50

FIGURE 7 ENVIRONMENTAL TARGETS..................................................................................................................... 51

FIGURE 8 RI TECHNIQUES USED IN INVESTMENT STRATEGIES..................................................................................52

FIGURE 9 SOURCES OF ENVIRONMENTAL INFORMATION ON INVESTEE COMPANIES...............................................54

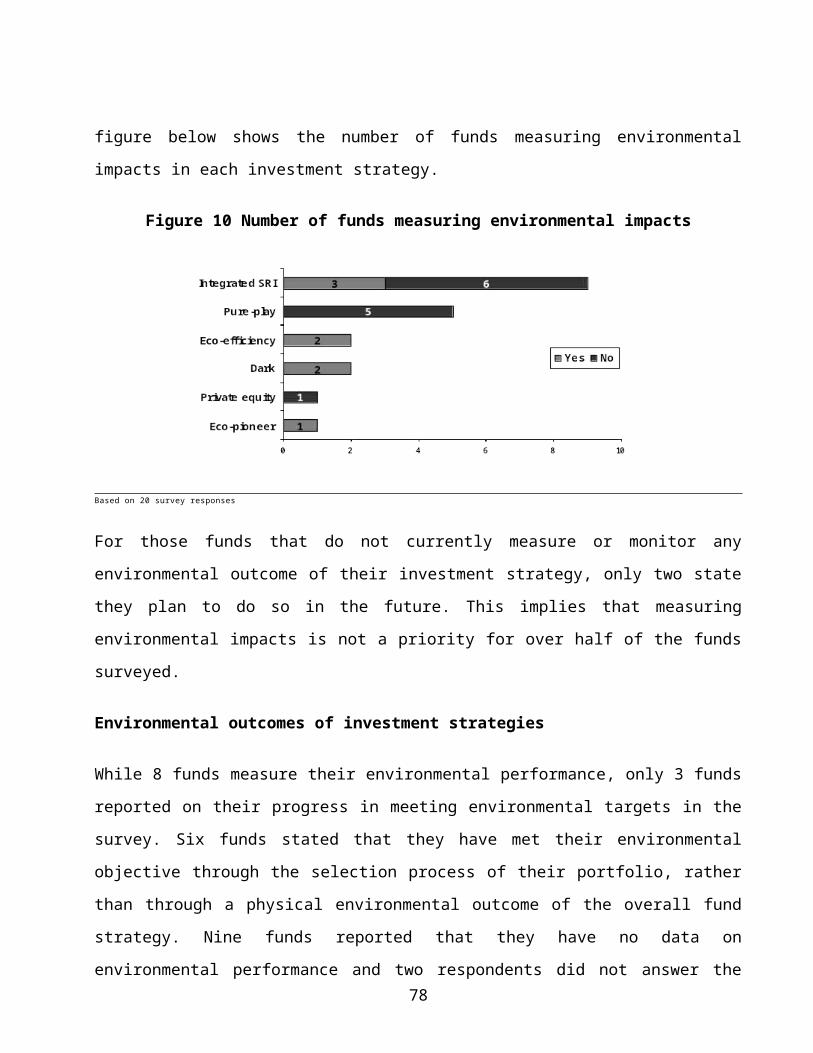

FIGURE 10 NUMBER OF FUNDS MEASURING ENVIRONMENTAL IMPACTS...........................................................55

FIGURE 11 PROGRESS OF RESPONDENTS IN MEETING ENVIRONMENTAL TARGETS.............................................56

FIGURE 12 SUMMARY OF BEST PRACTICES OF SELECTED FUNDS.........................................................................60

FIGURE 13 ANALYSIS OF EFFECTIVENESS OF RI VOTING POLICY AT MORLEY........................................................67

FIGURE 14 GLOBAL REPORTING INITIATIVE - ENVIRONMENTAL PERFORMANCE INDICATORS FOR THE FINANCIAL SERVICES SECTOR..................................................................................................................................................... 73

FIGURE 15 PERCENTAGE OF COMPANIES IN FTSE EUROTOP 300 WITH ABOVE AVERAGE ECOVALUE 21 RATINGS 78

FIGURE 16 SCHEMATIC OF MAJOR ECOVALUE 21TM ANALYSIS FACTORS..........................................................103

Figure 17 RiskMetrics’s Rating Scale...................................................................................................................... 105

4

Executive Summary

Defra commissioned RiskMetrics to look at the impact of responsible investment practices

on the environment and how the environmental performance of environmentally-focussed

investment strategies is currently assessed.

Key Findings

RiskMetrics conducted a literature review which highlighted that there is limited

research into the link between Responsible Investment and the environmental

performance of portfolio companies.

The literature review concluded that there was a positive correlation between

responsible investment and improved environmental performance although the

studies provided rather weak evidence and the approaches to measuring

environmental performance differed greatly. Very few studies could provide empirical

evidence to support their conclusions and instead relied on qualitative indicators.

RiskMetrics conducted an online survey to identify the extent to which environmental

investment strategies seek to improve the environmental performance of investee

companies, and if so, how these improvements are measured. Overall, the results

indicate that RI and environment-themed funds are not measuring the environmental

performance of their investment strategies.

40% of respondents to the survey measured the environmental impact of their funds

in some manner, although this was mainly in a qualitative manner looking at process

outcomes; 25% of respondents had measurable targets to meet their environmental

objectives; and 15% of respondents reported on their progress on meeting

environmental objectives in the survey.

Reporting on environmental performance of funds is typically qualitative in nature. It

is therefore very difficult to establish an accurate and verifiable measure of a

company’s progress over time.

5

Based on a company-level analysis of environmental performance over time, more

FTSE 300 Eurotop companies had better environmental performance in 2008

(63.6%) than in 2003 (50.2%).

Introduction and objectives

Responsible Investment is understood as integration of ESG issues into investment

process in order to enhance investment assessment, while traditional socially responsible

investing (SRI) consists of “elaborated screening strategies systematically impacting

portfolio construction and often implying a values-based approach. In this report,

“Responsible Investments” or “Responsible Investing” (RI) is used throughout, as it

composed of broader investment strategies rather than screening.

In the past decade, SRI has seen tremendous growth in the UK. There are now more than

80 SRI funds available with an estimated total fund value of GBP 8.9 billion; a decade ago

there were just a dozen with a value of GBP 2.2 billion. ‘Green funds’, or RI funds with an

environmental focus, in particular have gained greater attention recently. In 2007 alone, at

least 10 funds were launched in the UK focusing on an environmental issue such as climate

change or clean technology.

Most of the focus of RI and environmental investing has been on enhancing returns or

developing new investment ideas and products. However, very little attention has been

given to the end goal of having a positive impact on the physical environment. In order to fill

this gap, Defra set out to analyse the potential for investment strategies to deliver enhanced

environmental outcomes and of the effectiveness of different environmental investing

strategies.

As a first step to answering this question, Defra has commissioned RiskMetrics to conduct

a study to understand how the environmental performance of environmentally-focused

investment strategies is currently assessed.

The research consisted of both primary and secondary research over six months.

Preliminary data collection began with a comprehensive literature review on the link

6

between RI techniques and environmental performance of investment strategies and

approaches to measuring environmental performance. This was followed by a survey of

environmental-focused funds. This was conducted to gather additional data and information

on the current practices of fund managers. Finally, the research evaluated key RI initiatives

set up by investors, intergovernmental organisations and civil society, and industry to

gather information about how they assess environmental performance.

Literature review

We have carried out a literature review of the most relevant studies published over the past

fifteen years, during the period 1993 to 2008. The literature review was global in scope, and

looked at studies published by academia, think tanks, industries and consultancies.

We identified only 23 studies that discuss environmental performance of investment

strategies in some manner. A total of 18 studies evaluated the link between RI and

environmental performance either directly or indirectly. Nine of these studies focused

explicitly on environmental outcomes, while the remaining studies discussed environmental

impacts together with social and governance issues. The studies were roughly split

between quantitative and qualitative analyses. There were 14 positive correlations, 2

neutral relationships and 2 negative correlations. This means that in 78% (14 out 18) of

cases, there is evidence from the studies to suggest that green investments are linked to

good environmental performance. These studies do not distinguish between environmental

improvement of the investee companies that are due to RI and those that are due to

adopting a stock selection approach that favours investee companies that perform better

environmentally. However the studies present rather weak evidence and the small sample

of studies makes it difficult to generalize.

While 14 out of 18 studies concluded that there was a positive link between RI and

environmental performance of portfolio companies, only three studies provided empirical

evidence that this was the case (Koellner, Holden and TruCost). In addition, the studies

differed greatly in how they measured environmental performance. Many studies looked at

7

the processes of the fund managers with very few reports explicitly citing specific

environmental outcomes.

In sum, very little research has been carried out to examine the link between RI and

environmental performance. In addition, the overwhelming majority of indicators are of a

purely qualitative nature. Consequently, coherent quantitative time series of RI data are still

scarce, and it is therefore very difficult to establish an accurate and verifiable measure of a

company’s progress over time.

Survey of funds

In order to assess actual practices in fund management, RiskMetrics conducted an on-line

survey of RI funds with an environmental component. The aim of the survey was to identify

the extent to which environmental investment practices seek to improve the environmental

performance of portfolio companies, and if so, how these improvements are measured.

Reportedly there are over 80 RI funds in the UK but the survey specifically targeted RI

funds that have environmental objectives stated in their publicly available literature. The

sample universe focused primarily on UK funds, but also included some European and US

funds. In total 55 funds were contacted to participate in the survey, and 20 funds responded

to the survey (36.4% response rate).

Nine (45%) of the respondents are RI funds with integrated environmental objectives and

11 (55%) funds are primarily focused on the environment. Most funds have multiple

environmental objectives covering a wide range of issues. The funds also employ an array

of investment strategies to achieve their environmental objectives.

Overall, the survey results indicate that RI and environment-themed funds are not

measuring the environmental impacts of their investment strategies. The environmental

outcomes of the investment strategy do not appear to be considered a priority. For

instance, only 5 funds (25%) have measurable targets for achieving their stated

environmental objectives, and only 1 of these funds has targets that are quantitative. Eight

8

(40%) respondents monitor the environmental impact of their fund in some manner, but

mainly in a qualitative manner looking at process outcomes.

Only 3 (15%) funds reported their progress on meeting environmental objectives in the

survey. No fund releases a stand-alone report discussing its environmental performance;

any environmental impact reporting is integrated into quarterly updates, annual reports or

newsletters.

The survey results provide some evidence to suggest that financial performance, not

environmental performance, is the key measure against which RI and environmentally-

focused funds benchmark their success. Moreover, while all the funds have environmental

objectives, some funds responded that they are not marketed as environmental funds, and

therefore do not have environmental targets. Some funds also cited their fiduciary

responsibility limiting the ability for them to pursue environmental targets.

Furthermore, it does not seem that particular types of funds are performing better in

environmental terms or are more likely to measure environmental impacts than others.

However, it does not seem that the pure-play funds or private equity funds monitor

environmental performance. This may reflect the fact that these thematic funds

automatically assume that their funds will have positive environmental outcomes since they

focus exclusively on companies that contribute to environmental solutions.

The qualitative responses in the survey also highlighted several issues about measuring the

environmental performance of funds. Several respondents mentioned that it is difficult to

pinpoint what to measure and to develop an appropriate measurement methodology. Some

respondents questioned the validity of measuring environmental impact at a fund level

versus an institutional level. Some respondents also have reservations about the correlation

between environmental investment strategies and positive environmental outcomes at

companies.

Another issue that was raised in survey responses was that measuring environmental

performance was not relevant to some of the funds that are passively managed, particularly

tracker funds, or even thematic funds. This implies that any policies developed around 9

measuring environmental performance at the fund level must be nuanced enough to

encompass a variety of fund types and investment strategies.

Best practices

Based on our survey, we identified five institutions to highlight innovative practices in

measuring environmental performance and improving environmental outcomes. They are

Banco Fonder, the Environment Agency, Jupiter, Morley and Quadris Environmental

Investments. Each of the institutions incorporates environmental objectives slightly

differently in their fund management. They utilise a wide range of investment strategies and

all engage directly with portfolio companies to varying degrees on environmental issues.

Four funds review whether companies have changed their behaviour after engagement on

environmental issues over time. Other methods of measuring environmental impacts

include an independent forestry audit, review of the voting record and review of fund

management practices. The Environment Agency Pension Fund sets a quantitative target

that the environmental footprint of its combined actively managed equity portfolios is less

than the environmental footprint of the MSCI All World Index.

It is important to note that while these institutions do measure environmental performance

in some manner, none would claim that positive environmental outcomes are achieved

solely as a result of these institutions engaging with or investing in companies. In fact, all of

these institutions acknowledge that positive change with regard to environmental

performance takes time and their investment strategies are only one element in driving

change. Even so, these case studies provide good examples of innovative ways to

measure environmental impact of funds that could potentially be replicated by other funds.

Other drivers impacting investor and company behaviour

In the past decade, many global initiatives have been launched which have influenced

major financial institutions to become more socially and environmentally responsible in their

investment strategies and processes. These initiatives are currently influencing investor

thinking, policies and decision-making and will continue to do so in the future. In fact

10

several large institutional investors around the world are already referring to many of these

initiatives in their annual reports and policy documents.

These global initiatives can be divided into three categories: Investor initiatives,

Intergovernmental & civil initiatives and industry initiatives. All of these initiatives have

undoubtedly raised awareness about environmentally responsible behaviour, among both

companies and investors. However, it would be difficult to assess how much improvement

in environmental performance in companies can be attributed to these initiatives.

In addition, RI indices are also included as one of the drivers on responsible investment and

improved environmental performance of investee companies.

Collective impact of RI initiatives and investment techniques

To determine whether the growing number of RI initiatives and investment techniques

appears to be contributing to improved company environmental performance over time,

RiskMetrics analysed environmental performance at the company level. Using data from

RiskMetrics’s EcoValue 21 company ratings as a proxy for environmental performance for

the FTSE Eurotop 300 companies, we analysed changes in rating scores over a five-year

period from 2003 – 2008. The results show an improvement. This means that more

companies today have better environmental performance than five years ago.

These results, while generally positive, are inconclusive in terms of understanding the

impact either of environmental investing strategies or of the various initiatives referred to in

this report. It is difficult to say with certainty that companies that are gradually improving

their environmental ratings over time are the ones that are targeted in the environmental

investment strategies or by the initiatives.

Conclusions

The evidence from the literature review and fund manager survey reveals that very little

research has been conducted on this subject, and only a handful of institutions are actually

measuring the environmental efficacy of their funds. The majority of funds are focusing on

11

incorporating environmental targets into the portfolio selection process rather than focusing

on the environmental outcome of the investment strategy.

For those institutions measuring some aspect of environmental outcomes, conducting a

carbon audit of the portfolio at fund level or tracking engagement activities is the most

common practice. The majority of the environmental targets are thus based on improving

company behaviour in terms of environmental policies, disclosure and management

systems. Very few funds and institutions have a target to actually reduce their impact on the

physical environment.

In addition, reporting on environmental performance is typically qualitative in nature.

Consequently, coherent quantitative time series of RI data are still scarce, and it is

therefore very difficult to establish an accurate and verifiable measure of a company’s

progress over time

The metrics used by institutions also varied widely. This ranges from portfolio company

adoption of environmental management systems, to reduction and prevention of

environmental damage and increases in environmentally-focused business activities.

12

1. Introduction

Responsible Investing or Investment (RI) has evolved from the traditional socially

responsible investing (SRI) that consists of ethical exclusions as well as different types of

positive screens, to more broad integration of ESG issues to enhance investment

assessment.

In the past decade, RI has seen tremendous growth in the UK. There are now more than 80

RI funds available with an estimated total fund value of GBP 8.9 billion; a decade ago there

were just a dozen with a value of GBP 2.2 billion1. And according to a recent Mori poll, more

than two-thirds of investors say they would be interested in putting their money into

sustainable and responsible investment.

‘Green funds’, or RI funds with an environmental focus, in particular have gained greater

attention recently. In 2007 alone, at least 10 funds have been launched in the UK focusing

on an environmental issue such as climate change or clean technology. This trend is likely

to grow as consumer demands, tightening government policies and rising energy prices

drive companies to consider more environmentally friendly options. The trend for green

investments is also spreading to emerging markets.

Most of the focus of RI and environmental investing has been on enhancing returns or

developing new investment ideas and products. However, very little attention has been

given to the end goal of having a positive impact on the physical environment. As one fund

manager in Europe has noted2,

In order to fill this gap, Defra set out to analyse the potential for investment strategies to

deliver enhanced environmental outcomes and of the effectiveness of different

environmental investing strategies in delivering such outcomes. Defra has commissioned

RiskMetrics Group (RiskMetrics) to evaluate to what extent an environmental objective is

part of an environmental investing strategy, and if it is part of an environmental investing

strategy, how are these environmental goals measured, if at all?

1 EIRIS website, http://www.eiris.org/2 Butz and Pictet 2008

13

1.1 CONCEPTUAL FRAMEWORK

An attempt to understand the extent to which investor strategies have an impact on the

environment is a complex undertaking. There are many different kinds of investors, each

with different approaches. There are also many other stakeholders whose activities will

influence company behaviour, from consumers and employees to government and

regulators. Furthermore, environmental impacts themselves may be hard to define and

measure and attributing a particular type of investment strategy to a change in one

company management practice may be challenging. Below we discuss the context in which

this report needs to be read.

Process versus outcome approach

This survey seeks to ask whether environmental impacts can be evaluated or indeed simply

inferred, purely in terms of stock selection criteria and activist programmes by investors, or

whether investors are going beyond this and attempting to measure the physical

environmental outcomes of their stock selection policies and activities.

By stock selection criteria we are referring to investors choosing to allocate funds to those

companies deemed to be pursuing more environmentally friendly policies and implementing

environmental initiatives and operational performance improvements, in terms of new

environmental products, services and solutions, or eco-efficiencies. By activist programmes

we are referring primarily to engagement activities or voting policies, designed to produce

environmentally favourable results by way of changes in corporate behaviour. A number of

UK investors have adopted an engagement approach and we discuss engagement later on

in this report.

Investors may believe that their stock selection policies and engagement or voting activities

will in themselves be likely to influence corporate behaviour and thus yield environmental

benefits. But we are also putting forward the idea that investors could, in addition, develop

mechanisms that would go beyond stock selection criteria and engagement / voting

activities, in order to ascertain whether or not such approaches deliver tangible

14

environmental impacts, for example by way of reduced resource use by the companies in

which they have invested.

In short, the report will therefore need to examine whether the investor focus is currently on

looking at the processes or the outcomes of their environmental investment strategies, or

both.

A process-oriented approach can look at the research methodology and selection rules for

building a fund portfolio as well as efforts to influence corporate management. Some

questions to be considered in this report are:

How might the allocation of capital influence company behaviour?

What role can engagement play in changing company behaviour?

Do voting and the lodging of specific shareholder resolutions lead to improved

environmental performance? What is the relative importance of a fund or fund

manager and how might the power of the investor determine the extent to

which companies respond to investor action?

Our working hypothesis is that in most cases, institutional investors have focused on

relating their environmental performance in terms of processes in their portfolio selection or

on dialogue with corporate management. The survey results in Chapter 4 indicate that this

is the case, and the reasons for a focus on process impacts rather than outcomes may be

the result of a number of potentially constraining factors, discussed in more detail below.

An outcome-oriented approach looks at the impact that the companies in the fund portfolio

have on the environment and attempts to attribute that impact to the activities of the fund

itself – a difficult task in itself. There are many influences on corporate behaviour, for

example, customer or consumer buying trends or government policies on the environment.

Therefore the impact of investor actions on corporate behaviour and subsequent

environmental impacts should be viewed within the context of a whole range of drivers of

change.

15

It should also be borne in mind that the RI market represents a relatively small part of the

overall investment arena when viewed in terms of assets under management. So

responsible investors may be limited when it comes to changing corporate behaviour and

helping to create new paradigm shifts, whereby companies pay heed to more sustainable

business models and take a longer term view of their markets than the current short term

focus advocated historically by many ‘mainstream’ investors.

There is a further difficulty in assessing environmental outcomes. It is hard to point to

particular steps companies may have undertaken to improve environmental performance,

and their corresponding environmental outcomes. A fundamental question that can be

asked is what is the relationship between corporate management practices (e.g. ISO14001

certification, corporate environmental reporting) and environmental performance (as

measured in terms of emissions, resource consumption, etc), i.e. does one particular

process improvement lead to a known and measurable environmental performance

outcome?

Given the range of actors that may influence company behaviour, and the imprecise

linkages between one type of company management practice and a corresponding

environmental outcome, it may only be possible for investors to make some very general

assumptions about the effectiveness of their actions.

Demonstrating causality

Accepting, then, that there are real challenges in demonstrating causality, it would be useful

to systematically distinguish between those investor activities where such a link is made

with relative confidence (e.g. pure-play investments, offsetting activities) and those with

more uncertainty to them (e.g. stakeholder activism, engagement). This might be a

sensitive issue for some in the industry, but equally it may help to explain why many

investors may not yet have developed fully fledged measurement systems.

It does seem to be true that the subject of environmental performance of RI and

environmental investment strategies have received much less attention. Looking at publicly

available information from fund managers, there is very little reported on what impact their

16

funds have on the environment. In their report ‘Responsible Investment 2008’, RImetrics

evaluated fund managers from around the world managers with over USD 12 trillion (GBP

6.1 trillion) of assets under management, comparing each manager to a series of Best

Practice Principles that measured 22 aspects of RI competency. They found that even for

the managers who engage with companies, a "large proportion" of them do so to get ESG

information, with many less engaging to change companies' behaviours. Importantly, a

majority of managers do not monitor or track the costs of engagements with companies,

with 30% not keeping any record of engagement activities at all.

One reason for this lack of data on environmental performance is the ambiguity in the

process of measuring environmental performance of funds. At the most basic level, there is

a debate as to whether performance should be measured at the institutional level or the

fund level. Often, institutional investors have environmental policies that span their fund

range and it becomes difficult to attribute institution-wide outcomes to specific funds. On

the other hand, particular funds may use a targeted investment strategy with environmental

objectives which would elicit a potentially different environmental outcome from the rest of

the funds.

The following chapter provides a background on environmental investing strategies.

Chapter 3 presents the results of a literature review on the environmental efficacy of

investment strategies. Chapter 4 presents the results of a survey to fund managers about

their approaches to measuring environmental impacts, and Chapter 5 highlights the best

practices of fund managers in the survey. Chapter 6 evaluates trends impacting

environmental outcomes of investor strategies and Chapter 7 is the conclusion of the

overall report.

1.2 Objectives of study

While the financial performance of socially responsible investing has been discussed

widely, there has been little discussion on the actual social and environmental impact these

investment funds can bring. In other words: Do environmental investment strategies have

positive indirect impacts on the environment?

17

As a first step to answering this question, Defra has commissioned a study to understand

how the environmental performance of environmentally-focused investment strategies is

currently assessed. The results of this study will help inform a broader programme to

determine the role that investors can play in promoting sustainable development.

This study seeks to answer:

How do environmental investment strategies measure environmental efficacy?

In order to answer the research question, this study will include the following:

An analysis of how the environmental performance of investment strategies is

currently assessed

An analysis of the investment techniques available, where and how these are

applied, and what approaches, methodologies and metrics are used to assess these

techniques

An analysis of how the environmental performance of current initiatives set up

by industry or civil society is assessed

A review of existing evidence and any newly available empirical data about

how effective these environmental strategies are in driving social and environmental

improvement

The scope of the analysis includes institutional and retail investments across a wide range

of investment categories.

1.3 Methodology

The research consisted of both primary and secondary research over six months.

Preliminary data collection began with a comprehensive literature review on the link

between RI techniques and environmental performance of investment strategies and

approaches to measuring environmental performance. The research reviewed academic

papers, industry reports and civil society reports.

18

Since an initial literature review yielded limited evidence, a survey of environmental-focused

funds was conducted to gather additional data and information on the current practices of

fund managers. The survey consisted of an online questionnaire carried out over a two

month period in June and July 2008. The survey targeted primarily UK funds that have

stated elements of environmental objectives in their investment policies, but also included

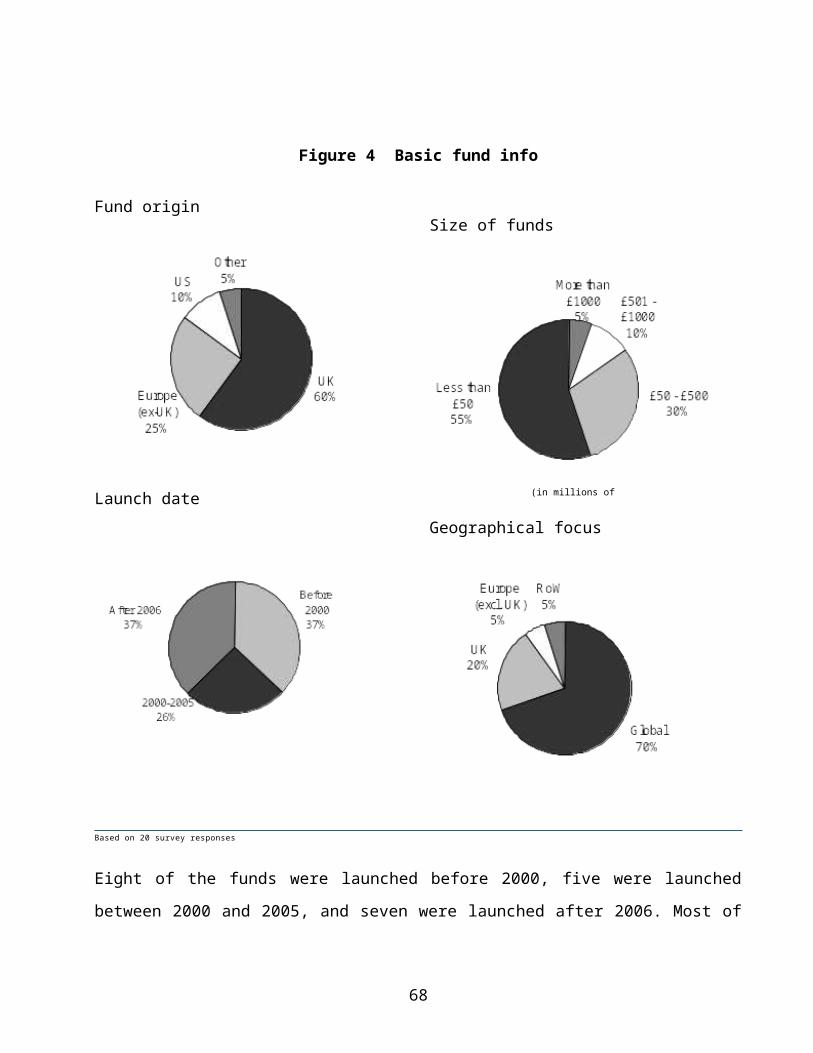

some European and US funds. The sample consisted of 55 funds and a total of 20 funds

participated in the survey (36.4% response rate).

Finally, the research evaluated key initiatives set up by investors, industry and civil society

to gather information about how they assess environmental performance. This consisted of

desk-based research and was supplemented by a company-level analysis of environmental

performance over time. This analysis was based on RiskMetrics’s EcoValue 21 ratings of

companies in the FTSE Eurotop 300 from 2003 to 2008.

19

2. Environmental Investing StrategiesThis section provides a description of socially responsible investing and environmental

investment strategies. It also introduces the key issues around the environmental

performance debate.

2.1 What is responsible investing?

Traditionally, environmental criteria were incorporated into broader RI strategies along with

social, ethical and governance issues. Investment managers with RI funds and mandates

overlay a qualitative, and increasingly a quantitative analysis, of corporate environmental

and social policies, practices, and performance onto traditional financial analysis of profit

potential. It is a process of identifying and investing in companies that meet certain

standards of corporate social responsibility.

During the past decade there has been a significant increase in the number of investors

who have adopted RI strategies and are holding companies more and more accountable for

their social and environmental practices. Investors in mutual funds, pension funds, and

other portfolios are also becoming active in shareholder advocacy and engagement in

record numbers, by filing resolutions or engaging in dialogue to pressure companies to

become more responsible on a particular social, environmental, or corporate governance

issue.

There are now more than 80 RI funds available in the UK with an estimated total fund value

of GBP 8.9 billion representing approximately 2% of all assets under management in the

UK3; a decade ago there were just a dozen with a value of GBP 2.2 billion4.

In recent years, the public's broader awareness of environmental issues such as global

warming and its impacts have supported demand for the creation of new RI investment

products with a specific environmental focus. Such environmental funds differ from RI funds

in that they apply only an environmental screen to the companies in which they invest.

Several mainstream financial institutions - Deutsche Bank, F&C, HSBC, Schroders and 3 As of December 2007; Total UK assets under management = GBP 468 billion (source: UK Investment Management Association)4 UKSIF

20

Virgin Money launched climate funds within the past year. In addition, funds that invest

solely in companies involved in developing environmental solutions such as renewable

energy sources and clean technology are on the rise.

In 2008, the number of funds seeking sustainable energy opportunities has risen to 441,

with an estimated total of USD 67.4 billion (GBP 42.2 billion) under management, with 62%

of these funds aimed at buying shares in publicly listed companies5. This is a four-fold

increase over the same period in the previous year. This rapid capital build up was due to a

record number of new clean energy public equity fund launches in 2007 – 17, compared to

just five in 2006. Several of these were from mainstream fund managers launching ‘climate

change’ funds as mentioned above.

FIGURE 1Sustainable energy funds by type and asset class

Source: New Energy Finance; Values in brackets refer to number of funds; Figures as of March 2008 from UNEP Report: Global Trends In Sustainable Energy Investment

2008; Average exchange rate for March 2008: 1 USD = 0.49992 GBP

Investment capital flowing into renewable energy will only continue to increase as more

investors recognise the scale of the climate change problem and future energy investment

needs. The International Energy Agency estimates that USD 17 trillion (GBP 10.5 trillion) of

investment6 will be required in the energy sector from now until 2030 which should prompt

investors to move more capital into this area.

5 As of March 2008; based on figures from UNEP Report: Global Trends In Sustainable Energy Investment 20086 UNEPFI 2008

21

2.2 RI techniques and their influence on corporate behaviour

These techniques are growing exponentially in terms of the numbers of individual and

institutional investors participating, in the amount of invested money involved, and, most

importantly, in the movement's ability to persuade corporations to develop a sense of

corporate social responsibility in the conduct of their businesses.

RI techniques

In the past, negative screening was the most basic and the most popular strategy of social

investing. Today, values-based avoidance screening continues to play an important role in

RI, but new screening issues have also emerged, and RI strategies continue to evolve.

There is growth in the number of RI funds, as well as in the diversity of screening

techniques. Shareholder advocates are also increasingly entering into direct dialogues with

companies, rather than filing resolutions. The following section describes the main

strategies used in RI today.

Screening

Screening is the practice of evaluating investment portfolios or mutual funds using social

and / or environmental criteria. Negative screening, sometimes called exclusion, consists of

barring investment in certain companies, economic sectors or even countries for ESG-

related reasons. There are limitations to using negative screening as a strategy on its own.

Negative screening, especially extensive screening, can potentially increase risk by altering

sector and geographic allocations within an investment universe. This could in turn affect a

portfolio's performance relative to its benchmark index. Nevertheless, negative screening

remains the most common initial strategy employed by investors entering into RI. Following

the definition, environmental funds that utilise negative screening techniques are

sometimes referred to as “Dark Green” funds and have strict ethical criteria to exclude

companies that challenge the environment, such as oil and gas companies. For example,

Friends Provident's Stewardship Fund, managed by F&C, does not invest in airlines

because it believes that the industry as a whole is not doing enough to tackle carbon

22

emissions. Many dark green funds also automatically exclude all companies involved in

tobacco, armaments, gambling, the fur trade and pornography.

RI investors also employ positive screening to select companies with positive attributes for

investment. The most popular form of positive screening is called ‘best-in-class’, where

stocks are selected within each sector of a given index, thereby retaining sector balance

within the investment universe. A less often used, but equally interesting form is pioneer

screening, where funds specialise in the best-performing companies against a specific

criterion, such as management of natural resources. Motivated by a desire to set standards

for, and improve, corporate social and environmental performance, social investors use

such positive screening techniques to identify companies with competitive advantages over

their peers, many of which may be intangible in nature. In contrast to “Dark Green” funds,

“Light Green” funds concentrate on selecting companies with positive environmental

attributes. These funds may invest in industries such as aviation and oil that would be

shunned by many of the stricter dark green funds. Within this category, funds can be

classified as an eco-efficiency or eco-pioneer fund7. An eco-efficiency fund utilises a ‘best-

in-class’ approach to invest in the companies within each sector that score highest when

rated on various environmental criteria. An eco-pioneer fund invests in innovative

companies that have business activities focused on environmental technologies and

services.

When either screening out heavy polluted companies or selecting environmentally friendly

ones, one should ask the question of how screening can influence corporate behaviour and

thus contribute to the goal of making a difference in terms of environmental improvement.

One of the mechanisms is based on the “Cost of Capital” argument. By channelling capital

away from “bad” companies (negative screening), it is said to lead to a decrease in the

share prices and an increase in the cost of capital; the opposite is true for positive

screening. However, if a fund owns only a small proportion of the shares in a company, a

divestment or investment is unlikely to have a significant price impact on the shares and

thus influence corporate behaviour change on the environment. Currently it is estimated

that responsible investment only represents 2% of global market values, which is

7 Adapted from Koellner 2005

23

considered negligible. Heinkel et al (2001) studied the effect of exclusion on a firm’s cost of

capital. It was concluded that the increase in cost will only be significant enough to force

change when the investor owns more than 20% of the market. Therefore the number of

investors that use screening methodologies would have to increase dramatically in order to

have an overall impact on the cost of capital of these companies and ultimately impose

changes on the way companies tackle environmental issues.

In addition, screening can influence corporate behaviour indirectly by impacting a

company’s reputation, awareness raising and identifying management quality. It is believed

that there are reputational impacts attached to being included or excluded from

sustainability standards, indices and benchmarks. For instance, in September 2008

Norwegian Government Pension Fund Global (NGPFG) whose current market value was

NOK 2,076 billion (approximately GBP 200.5 billion) as of 2009 Q1, sold all its Rio Tinto

stock that was worth more than NOK 4.8 billion (GBP 463.6 million) at the end of 2007. This

high profile divestment and exclusion by one of the largest sovereign wealth funds attracted

media attention and thus reputational damage to the company. In response to the

divestment, Rio Tinto wrote to The Norwegian Ministry of Finance outlining Rio Tinto's

Group wide approach to environmental performance, and providing specifics of the

environmental management processes at the Grasberg mine, which was the main subject

of the Norwegian fund’s decision8. Tesco, initially excluded from the FTSE4Good index in

2001, rectified its environmental policies to gain inclusion in the benchmark that tracks

performance of companies with “globally recognized corporate social responsibility

standards”. In 2004, research conducted by the University of Dundee found the Tesco case

"is not an isolated example" and that FTSE4Good's “Best-in-class” approach has "had a

clear impact on a significant subset of companies and their stakeholders"9.

The existence of screening raises the profile of the environmental agenda and supports

communities and regulators in their effort to foster corporate change to a more sustainable

business model.

8 http://www.riotinto.com/media/news_12469.asp9 http://www.guardian.co.uk/business/2008/feb/21/greenbusiness.ethicalliving

24

Management quality is arguably the most intangible asset to a company’s value10 and

company managers are rewarded if their companies are judged to have high quality

management. Considering sustainability issues within business risk and opportunity

assessment is seen as an indicator of high quality management, which incentivises

company managers to improve their corporate environmental performance.

Integrated Analysis

Integrated analysis is an investment style in which analysis of ESG issues contributes to

traditional financial analysis by identifying additional sources of risk and opportunity,

thereby contributing to better overall investment decision-making. It is based on the premise

that non-financial criteria can have an impact on the financial bottom line in the long-term.

Arguably there is a market failure within the traditional financial analyst community, that the

long-term value drivers of companies and sectors are often overlooked. Fund managers

that take on this approach see ESG issues as drivers of long term value, and therefore as a

way to outperform. This is based on their greater understanding of the long-term strategic

value drivers of firms, sectors and the economy.

Desirable environmental impacts by using ESG Integration can be achieved through

signalling. The signal can be from investors, ESG specialists or mainstream analysts and

fund managers. The key mechanism is that by integrating sustainability issues such as

environment issues across the board, it will send a signal to companies that the markets

take into account the financial and environmental materiality of these “non-traditional”

factors. By collecting, evaluating and monitoring the risks and opportunities of

environmental issues that companies face in conjunction to traditional financial valuation,

investors, ESG specialists, research analysts and fund managers create an effective

dialogue with companies on how companies should go about reducing their environmental

impacts and fostering positive change. In addition, the focus on company’s environmental

performance at mainstream level in turn forces companies to disclose and improve.

10 Pricewaterhouse Coopers (2005) “Reporting the Value of Acquired Intangible Assets.”

25

Fund managers that adopt the integration approach include Generation Investment

Management and Cazenove Capital Management. Colin le Duc, head of Research at

Generation, believes that “full integration of sustainability research into equity analysis

enables firms to consider such issues within the context of a company’s business

fundamentals. This integration increases the flow of material information into the investment

process and ensures that both financial and sustainability research is incorporated to more

accurately analyse the effect of sustainability issues on a company’s ability to generate

shareholder value”11.

Shareholder Advocacy and Engagement

Shareholder advocacy and engagement relate to responsible investors taking an active role

as owners of corporate stock. These efforts include dialoguing with companies on issues of

environmental concern, public campaigns as well as filing, co-filing, voting on shareholder

resolutions, and ultimately divestment. Proxy resolutions on environmental issues are

aimed at improving company policies and practices, addressing perceived shortcomings

and encouraging management to exercise good corporate citizenship towards the

environment while promoting long-term shareholder value and financial performance.

There are a number of rationales why responsible investors seek improvements in the

environmental performance of investee companies. Generally speaking, investors claim to

engage on ESG issues in order to increase the value of the companies with which they

engage, resulting in increased returns to their portfolios over the longer term. This is

because they justify their activities on the basis that these ESG issues are connected with

material risks or opportunities that may affect the portfolio, particularly over the longer term.

Another reason for shareholder engagement is that company managers are simply not fully

aware of all the risks and their incentives often are not in line with shareholders’ value. It is

believed that responsible investors can add value by enhancing ESG information flows to

company managers and raising awareness about issues of importance to a company’s long

term value.

11 http://www.generationim.com/media/pdf-environmental-finance-12-04.pdf

26

The term “Universal Ownership” provides a strong argument for investor involvement in

influencing corporate behaviour. A universal owner is often regarded as a large financial

institution such as a pension fund, which owns securities in a broad cross- section across

the economy. As they become larger and more diversified, a universal owner’s returns are

more closely linked to those of the economy as a whole rather than the returns of the

individual companies in its portfolio. As such, universal investors should adopt measures

that enhance the overall market performance by providing incentives for companies to

internalize all the externalities. Ultimately the universal investors have direct benefits in

improvements in corporate ESG performance.

Engagement with companies must be assertive and persistent to have effective results in

sending the message across to the company’s management and board. In 2008, F&C (full

name needed) raised ESG issues at over 900 companies (2007: 762) in 49 countries in

2008, including over 70 face-to-face meetings with board members. 30% of ESG issues

engaged with companies were environmental related including climate change, ecosystems

services and environmental management, while 40% of these engagements were

conducted in Europe. F&C recorded 429 cases (2007: 224) that a company improves its

policies, procedures or practices following engagement, 45% of which were on

environmental issues. For example, Royal Bank of Scotland established a Group

Environment Board with senior management representation to focus on product and service

innovation, environmental risk, employee engagement and group footprint management.

Following active engagement, Tesco adopted a new strategy to make “low-carbon” product

choices easier and more affordable for customers, including promotions and clear labelling.

Collaborative engagement is often considered an effective way to draw management’s

attention. Established in late 2006, the Principles for Responsible Investment (PRI)

Engagement Clearinghouse has been an important factor in facilitating collaborative

engagement. It is a forum where PRI signatories can post ideas and proposals for

collaboration with peers to seek changes in company behaviour and policies. In 2007

Morley Fund Management (now Aviva Investors) led a PRI collaborative engagement

focused on the reporting requirements of the UN Global Compact. A coalition of 20

investors representing approximately USD 2.13 trillion in assets wrote to the CEOs of 103

27

companies in more than 30 different countries to either congratulate them on their good

practice or ask them to improve their engagement with the Global Compact and their

reporting on progress. In total, 78 companies were identified as ‘laggards’ for not producing

a ‘Communication on Progress’ – an annual report on how the company is implementing

the ten principles of the UN Global Compact, and which is a requirement of participation.

The engagement resulted in over 32% of the companies identified as laggards

subsequently submitting a Communication on Progress and improving their engagement

with the UN Global Compact. Another example is a joint engagement by The Carbon Trust

and Hermes through the Clearinghouse to encourage UK publicly listed companies to

reduce their carbon emissions. The engagement programme began in Q3 of 2007 and is

still ongoing. In total six UK companies including International Power, Associated British

Foods, FKI, WM Morrison Supermarkets, Arriva, and TDG were selected based on specific

criteria by Carbon Trust. PRI claims that the engagement is ongoing and so no formal

results have been processed. However, WM Morrisons supermarket is one organisation

that has shown particular improvements after active engagement. In June 2008 Morrisons

became the first company to win an award from the Carbon Trust, called the ‘Carbon Trust

Standard’ for cutting its carbon footprint. Reportedly Morrisons reduced its carbon

emissions by 12.8% in the past three years.

Filing resolutions is considered a good way to warn management that the investor strongly

disagrees with some of the company’s policies. A downside is that the focus of engagement

is intrinsically limited by human factors such as size of engagement teams and time

allotment, thus potentially covering less ground than positive screening strategies.

RiskMetrics research found that 410 ESG related resolutions were filed and 202 came to

votes in the US in 2008.

In addition to the above RI approaches, there are two types of environmental investing that

are often used.

28

Thematic investment funds

These funds focus on a range of themes emerging from the shift to a more sustainable

economy, such as clean technology, energy efficiency, renewable energy, waste

management, and water treatment. The idea is that a portfolio which is over-weight in these

long-term themes will out-perform because the change to a more sustainable economy is

necessary and unavoidable. These funds generally invest exclusively in companies which

provide environmental solutions, often called pure-play environmental companies because

they dedicate a majority of their business activities to environmental issues. Thematic

investment funds provide investors with some of the purest environmental investment

options.

Venture capital and private equity funds

An increasing number of venture capital (VC) and private equity (PE) funds are investing in

private companies that develop new environmental products and services. These funds are

relatively illiquid and represent a higher risk investment than many of the funds above which

invest in public companies. These investments generally go directly to the investee

companies and enable them to expand and develop their businesses. Some of these funds

specialise in specific types of environmental companies whereas others take a more

generalist approach to portfolio selection. For example the Low Carbon Accelerator, an AIM

listed fund, invests in sustainable building, energy efficiency and clean energy. It is

important to note that environmental funds may not fit neatly into each category. For

example, on the surface the Virgin Climate Change Fund could be considered a thematic

investment fund; however, it is not investing only in environmental pure-play companies. It

is using an ‘eco-efficient’ approach to identify those with the best environmental credentials

in each industry and select companies considered to deliver the highest returns. Often,

funds will use a mixture of strategies to achieve their environmental objectives.

We believe that the indirect environmental impacts of pure-play, venture capital and private

equity funds (VC/PE) are similar. By providing funding to these companies that tend to be

29

start ups, these environmental investing strategies help deliver significant and scalable

positive environmental outputs indirectly.

Currently there is a large gap between the capital needed and the capital currently

deployed to create solutions to environmental problems such as climate change, energy

scarcity, water shortage and pollution, and waste disposal. According to New Energy

Finance, new investments by VC/PE players grew significantly by 37% from USD 9.8 billion

(GBP 6.1 billion) to USD 13.5 billion (GBP 8.4 billion) in 2008 globally. During the year,

USD 5.6 billion (GBP 3.5 billion) was invested in Solar equally as in Wind, and USD 2 billion

(GBP 1.2 billion) was deployed into the Biofuels sector. There are a number of VC/PE funds

in the UK such as WHEB Ventures, Impax Group Plc and Low Carbon Accelerator (LCA).

Low Carbon Accelerator (LCA), launched in 2006 by Low Carbon Investors (LCI), is an

investment vehicle that has holdings in a diverse portfolio of unquoted private companies

that provide low carbon products and services. Examples of LCA’s portfolio companies

include: Responsive Load Technology, which has developed technology allowing

household electrical appliances to respond to grid pressure and better match supply and

demand; Helio Dynamics, a solar energy technology company, currently reporting to be

achieving 15 times greater generation capacity in photovoltaic cells whilst reducing the

usage of silicon; and Saddlehorn, an 800 acre sustainable housing development in the

U.S.A. The pure-play nature of these investments means that there will be indirect

environmental benefits from the investments made by LCA, particularly if LCA can aid these

companies to expand their market share more rapidly through their engagement activities.

RI investment products

RI Indices and Funds

Since KLD Research & Analytics introduced the Domini 400 Index back in 1990, social

indices and mutual funds that track them have proliferated. An RI index is a stock index of

publicly traded companies that have met certain standards of social and environmental

excellence. Potential candidates for the index will have positive records on issues such as

employee and human relations, product safety, environmental safety, and corporate

30

governance. Companies engaged in the business of alcohol, tobacco, firearms, gambling,

nuclear power and military weapons are often excluded. An RI index fund is a mutual fund

made up of companies from a particular RI index. For example, the Calvert Social Index

Fund seeks to match the performance of the Calvert Social Index™, a benchmark for

measuring the performance of large- and mid-sized US-based socially responsible

companies.

The future for RI index products is likely to be one where investment universes are

progressively more customised so that the needs of all RI practitioners are met. While

mainstream investors have in excess of 50,000 indices in which to invest and RI investors

have only around 10012, there is enough room within which index creators can provide new

products for the environmentally-conscious investor. In the past three to four years, some

indices have already been developed that focus on a particular environmental theme,

examples include the JPMorgan Environmental Index – Carbon Beta.

Exchange Traded Funds (ETFs)

ETFs are mutual funds that are traded on exchanges just like stocks and have become

popular due to the growth in demand for index linked products, their tax efficiency, low cost,

and ease of trading. Socially responsible investors have a handful of ETF products to

choose from, with a growing number of environmentally focused ones. Both FTSE and Dow

Jones have created RI- focused ETFs to develop a niche in the U.S. and Europe.

The number and the complexity of the strategies used in RI have grown considerably and

often involve a combination of screening and shareholder influencing techniques.

Environmental investing can use any of these strategies as part of an integrated RI fund or

a fund with an environmental focus. The following section provides a general overview of

the different types of environmental investing today.

12 http://www.sriadviser.com/commentary.html?id=1331

2.3 Performance of environmental investing strategies

Financial performance of environmental investing strategies

The biggest debate regarding RI relates to whether considering environmental, social and

governance (ESG) factors can have a material impact on investment performance. As more

academic and practitioner research in this field emerges, there is a solid and growing body

of evidence that good management of ESG factors can potentially increase long-term

performance and reduce certain types of portfolio risks.

For instance, in 2007 RiskMetrics carried out a literature review of the most relevant studies

published from 1996 to 2006 that explore the linkages between ESG factors and financial

performance. A review of 88 studies revealed strong evidence for the existence of a

positive relationship between ESG management and performance and financial

performance. In 90% of the total number of relationships that were assessed, a positive

correlation between ESG factors and financial performance was identified; in only 10% of

cases could a negative relationship be said to exist. The implementation of a

comprehensive environmental management strategy in particular can be linked to good

financial performance, as can development of good governance structures.

In general, RI products have maintained competitive performance in comparison to

mainstream and traditional funds. Established indices around the world also show that

companies that incorporate social and environmental standards historically deliver

competitive returns. For example, the HSBC Global RI Life fund, a globally-diverse pension

fund managed by SINOPIA which combines a best-in-class positive screening approach

and quantitative stock selection process has outperformed mainstream equities since its

launch. Over the three-years to end of August 2007, the HSBC Global RI Life fund has

posted a 52.5% gain, net of fees13. This represents a significant outperformance when

compared to the 44.7% return in the MSCI World Index over the same period. The three-

year net annualised performance of the fund equates to 15.1%, compared to 13.1% from

the MSCI World Index.

13 According to figures from HSBC Investments (UK) Ltd. (Figures are quoted total return, in sterling, cumulative over 36 months to 30 August 2007. Time period for performance calculation is based on first full 36 months of available performance data).

32

Environmental performance

The subject of environmental performance of RI strategies has received much less

attention. Environmental performance of RI strategies can have a range of indirect impacts.

As discussed in previous section, indirect environmental impacts can be achieved through

various environmental investing strategies such as screening, integration and shareholder

engagement. Alternatively, fund managers may simply offset the carbon emissions

associated with their portfolio. Looking at publicly available information from fund

managers, there is very little reported on what impact their funds could have on the

environment. In their report ‘Responsible Investment 2008’, RImetrics evaluated fund

managers from around the world managers with over USD 12 trillion (GBP 7.4 trillion) of

assets under management, comparing each manager to a series of Best Practice Principles

that measured 22 aspects of RI competency. They found that even for the managers who

engage with companies, a "large proportion" of them do so to get ESG information, with

many less engaging to change companies' behaviours. Importantly, a majority of managers

do not monitor or track the costs of engagements with companies, with 30% not keeping

any trail of engagement activities at all.

One reason for this lack of data on environmental performance is the ambiguity in the

process of measuring environmental performance of funds. At the most basic level, there is

a debate as to whether performance should be measured at the institutional level or the

fund level. Often, institutional investors have environmental policies that span their fund

range and it becomes difficult to attribute institution-wide outcomes to specific funds. On the

other hand, particular funds may use a targeted investment strategy with environmental

objectives which would elicit a potentially different environmental outcome from the rest of

the funds.

Another core debate is whether to look at the processes or outcomes of environmental

investment strategies. A process-oriented approach can look at the research methodology

and selection rules for building a fund portfolio as well as corporate management. An

outcome-oriented approach looks at the impact that the companies in the fund’s portfolio

have on the environment and correspondingly that impact to the fund itself. In most cases,

33

institutional investors have focused on relating their environmental performance in terms of

processes in their portfolio selection or corporate management.

Beyond these core issues, there are several additional factors to consider in developing a

methodology to measure the environmental outcomes of different investment strategies14:

Standardisation and functional unit – In order to compare the sustainability

outcomes of different investment funds, it is necessary to standardise the measures

of the assessment based on a common functional unit. At a company level, a

common indicator is CO2 equivalent emissions per sale (i.e. pound, dollar or euro of

revenues), but the functional unit for investment funds is harder to define. A study by

Dr. Thomas Koellner and his colleagues at the Swiss Federal Institute of Technology

recommends using percentage of financial performance per year as a functional unit

to measure sustainability performance.

Aggregation – Another issue to consider is whether all the criteria can be

condensed into a single score result. Some of the criteria may not be quantitative

and difficult to add up to a single score.

Time perspective – The outcomes of an assessment of a fund’s

sustainability performance depend very much on the time perspective chosen. Thus,

a methodology must consider whether to assess the current sustainability

performance or its projected future performance because sustainability funds either

build on a strong potential for improvements in the future (e.g. eco-pioneers funds) or

on a powerful sustainability performance (e.g. pure-play thematic funds).

System border – In order to assess these impacts practically, however, it is

necessary to specify the system borders of the environment and society. It is not

possible to investigate the social and ecological impact without narrowing the system

down.

Peer group and benchmark – It is more relevant to compare the fund’s

performance (both financial and non-financial) with the performance of other funds

and relative to a benchmark. Such a comparison allows the analysis to distinguish

14 Koellner 2005

34

the general trends in performance, which affect most funds similarly, from the

individual performance of a specific fund.

35

3. Literature Review of Environmental Efficacy in Investments

This section is a review of the most recent academic research that examines whether

environmentally-focused investment strategies have positive impacts on the environment.

In order to address this question, we explore literature that addresses the following two

themes:

Relationships between socially responsible investing and their impacts on the

environment

Approaches to measuring environmental performance in investment

strategies

We have carried out a literature review of the most relevant studies published over the past

fifteen years, during the period 1993 to 2008. The literature review was global in scope, and

looked at studies published by academia, think tanks, industries and consultancies.

A full list of all the studies reviewed in this paper can be found in the Annex. This list

contains full details of each study including title, year of publication, author(s) and country of

publication, as well as a brief abstract of each study’s methodology and conclusions.

3.1 Overall findings

We identified only 23 studies that discuss environmental performance of investment

strategies in some manner. Approximately half of these studies discuss RI broadly, and

only 11 studies have an exclusive environmental focus. In addition, studies tended to

examine social or environmental performance of the RI industry as a whole, with only 6

studies looking at the performance of specific funds or investment portfolios.

Over two-thirds of the studies have been published in the past five years, indicating a

growing concern for the efficacy of investment strategies in meeting their stated social or

environmental objectives. However, this type of research remains primarily within the

36

academic sphere, with only seven studies conducted outside of academia. Of the 23

studies included in our analysis, 14 originated in Europe (6 of these from the UK)

suggesting that Europe is leading the field in terms of research into the ESG outcomes of

investments. Figure 2 shows the origin of the different studies.

Figure 2 Origin of studies in literature review

By GeographyBy Publisher

3.2 RI and environmental performance

A total of 18 studies evaluated the link between RI and environmental performance either

directly or indirectly. Nine of these studies focused explicitly on environmental outcomes,

while the remaining studies discussed environmental impacts together with social and

governance issues. The studies were roughly split between quantitative and qualitative

analyses.

Some of the studies examined a specific RI technique such as negative screening or

shareholder engagement, but the majority of the studies had a broad focus and looked at RI

as an overall investment strategy.

37

The overall results showing the link between RI and environmental performance, including

the types of strategies featured in the studies, are shown in the chart below. The linkages

are classified as being:

Positive correlationRI strategies influence corporate behaviour on ESG issues

which leads to positive environmental outcomes

Neutral correlation

RI strategies may influence corporate behaviour on ESG

issues but no conclusion was reached regarding effect on

environmental outcomes

Negative correlationRI strategies do not influence corporate behaviour on ESG

issues and do not lead to positive environmental outcomes

There were 14 positive correlations, 2 neutral relationships and 2 negative correlations.

These 14 studies provide rather weak evidence from the studies to suggest that green

investments can be linked to good environmental performance.

Figure 3 Number of correlations between RI and environmental performance

In terms of environmental impacts, the studies considered the influence of RI on changing

corporate behaviour related to the environment in three main areas:

Adoption of an environmental strategy or management system

Reduction and prevention of environmental damage (primarily through cutting

greenhouse gas emissions and curbing pollution)

Increase in an environmentally-focused business activity

38

The indicators used to measure environmental impacts varied widely from measuring fund-

level performance to company level performance. For example one study measured the

percentage of a portfolio invested in pure play environmental companies while several