Embed Size (px)

Citation preview

Results PresentationDebenture UpdateYear ended 30 June 2020

Edward Ziff – Chairman & CEO

Mark Dilley - Group FD

Resetting the business for the future

COVID-19 and Business Review

• COVID-19 has impacted the business significantly during the year, but rent receipts have

been resilient and all covenants have been met

• Our strategy and model remains appropriate but we have accelerated asset disposals

(where mature or under-performing), further reducing our Retail & Leisure exposure

Actively managing our assets:

• Improvements completed at Ducie House and Carvers Warehouse in Manchester

Maximising available capital:

• Sales of four properties since year end generating £35m of proceeds, at or above June 20 book value

Investing in our development pipeline:

• Development pipeline continues to be improved with planning consents at Whitehall Road in Leeds

implemented

Investing in new assets:

• Significant 123 Albion Street refurbishment completed following a £4m investment

Key activity

2

Our Priorities- Strong first 9 months, followed by significant disruption

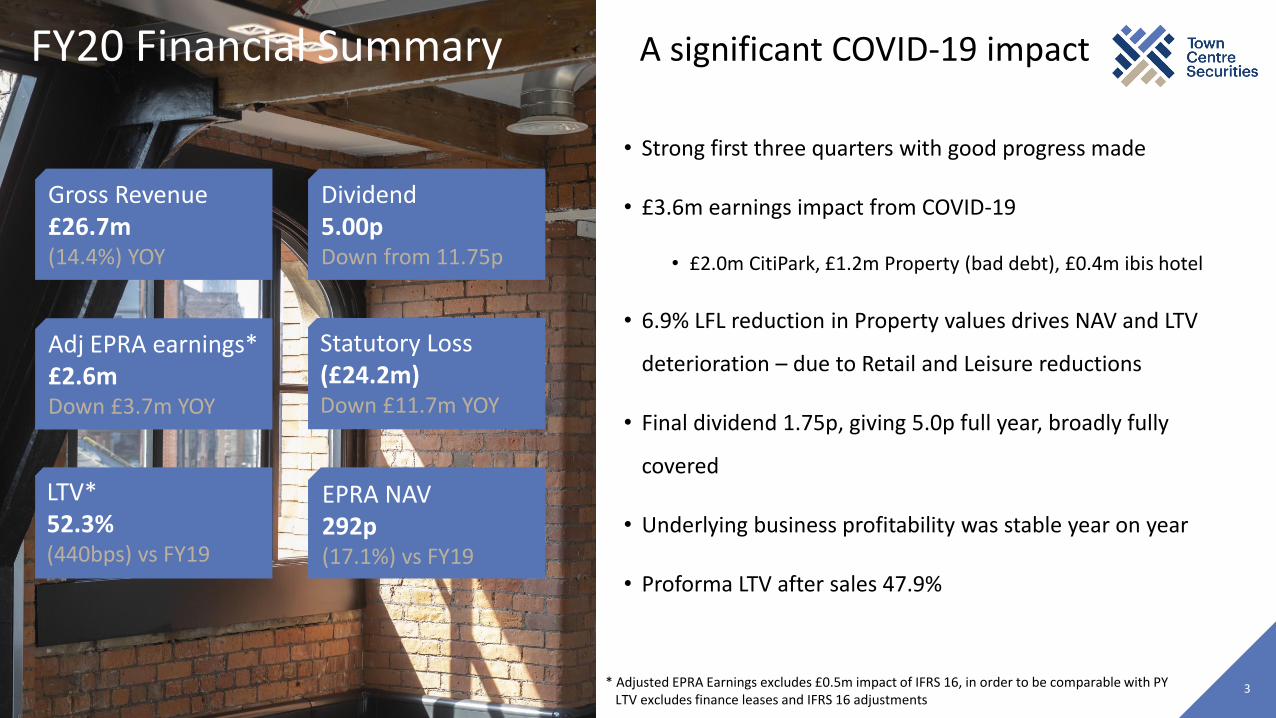

FY20 Financial Summary

3

Dividend5.00pDown from 11.75p

Statutory Loss(£24.2m)Down £11.7m YOY

Adj EPRA earnings*£2.6mDown £3.7m YOY

LTV*52.3%(440bps) vs FY19

EPRA NAV292p(17.1%) vs FY19

• Strong first three quarters with good progress made

• £3.6m earnings impact from COVID-19

• £2.0m CitiPark, £1.2m Property (bad debt), £0.4m ibis hotel

• 6.9% LFL reduction in Property values drives NAV and LTV

deterioration – due to Retail and Leisure reductions

• Final dividend 1.75p, giving 5.0p full year, broadly fully

covered

• Underlying business profitability was stable year on year

• Proforma LTV after sales 47.9%

Gross Revenue£26.7m(14.4%) YOY

* Adjusted EPRA Earnings excludes £0.5m impact of IFRS 16, in order to be comparable with PYLTV excludes finance leases and IFRS 16 adjustments

A significant COVID-19 impact

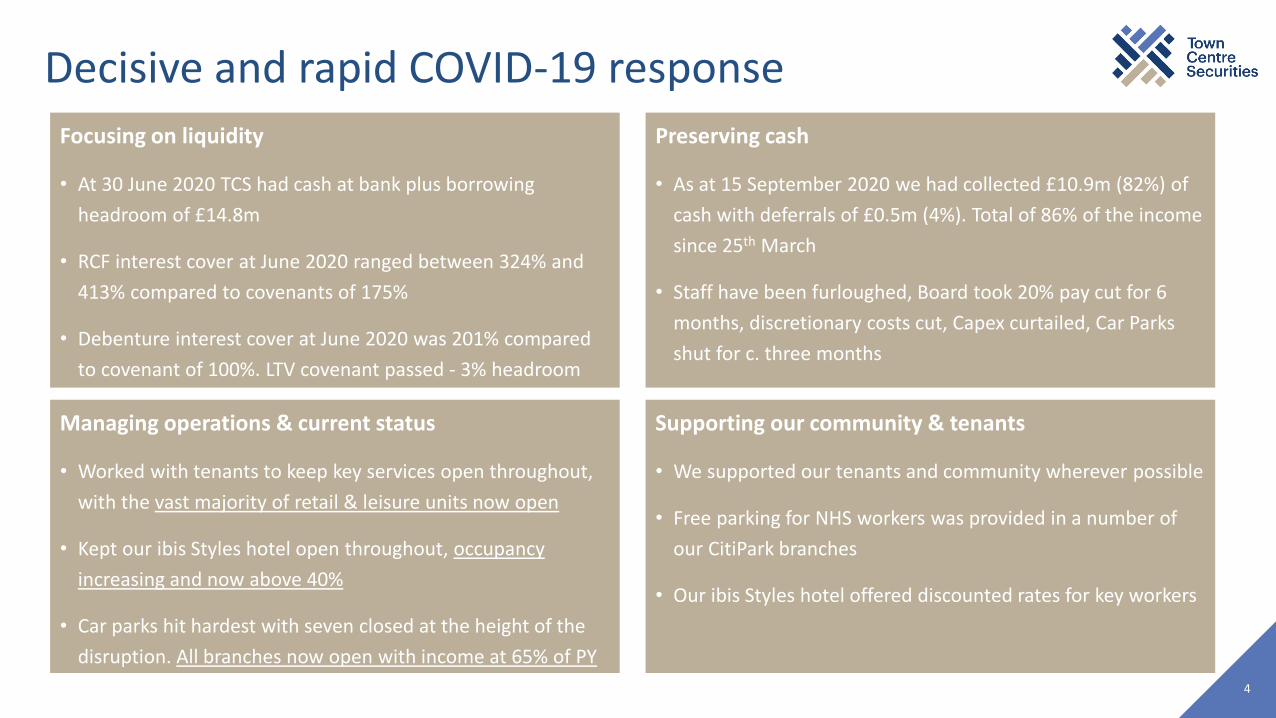

Decisive and rapid COVID-19 response

Preserving cash

• As at 15 September 2020 we had collected £10.9m (82%) of

cash with deferrals of £0.5m (4%). Total of 86% of the income

since 25th March

• Staff have been furloughed, Board took 20% pay cut for 6

months, discretionary costs cut, Capex curtailed, Car Parks

shut for c. three months

• Dividend under review

4

Supporting our community & tenants

• We supported our tenants and community wherever possible

• Free parking for NHS workers was provided in a number of

our CitiPark branches

• Our ibis Styles hotel offered discounted rates for key workers

Managing operations & current status

• Worked with tenants to keep key services open throughout,

with the vast majority of retail & leisure units now open

• Kept our ibis Styles hotel open throughout, occupancy

increasing and now above 40%

• Car parks hit hardest with seven closed at the height of the

disruption. All branches now open with income at 65% of PY

Focusing on liquidity

• At 30 June 2020 TCS had cash at bank plus borrowing

headroom of £14.8m

• RCF interest cover at June 2020 ranged between 324% and

413% compared to covenants of 175%

• Debenture interest cover at June 2020 was 201% compared

to covenant of 100%. LTV covenant passed - 3% headroom

Business Review – resetting and reinvigorating

5

• Key strategic initiatives reviewed during crisis

• Strategy and business model appropriate but needed acceleration given events

• Key elements of acceleration to include:

• Asset disposals of Retail and Leisure assets, either where they have matured following

investment, or where they are under-performing

• Continue to reduce proportion of Retail and Leisure in the portfolio

• Reduce Gearing and LTV

• Create headroom for future growth

Business Review – Asset sales

6

• Asset sales in the financial year ended 30 June 2020 were modest, however since then we have exchanged on a

number of key sales totalling £35.2m of proceeds:

• Two Waitrose stores in Scotland (Milngavie and Glasgow) sold for £23.2m. Sold in-line with June 20 valuations at a yield of 5.7%

• Recently completed retail unit in Milngavie, Scotland let to Aldi and Home Bargains sold for £10.7m at June 20 valuation level at 5.7% yield

• Retail unit in Chiswick, London for £1.4m, £0.3m above June 20 valuation at 5.9% yield

• Since FY 17 we have now sold over

£84m of assets, 95% of which were

Retail and Leisure

• Reduces % of Retail & Leisure to 42%

£m

Sales Purchases

% Retail &

Leisure in

portfolio

% Retail & Leisure % Retail & Leisure

FY17 22.3 88% 4.0 46% 61%

FY18 10.1 95% 9.0 0% 55%

FY19 14.0 100% 16.0 25% 50%

FY20 2.5 100% 1.7 100% 47%

FY21 to date 35.2 100% 42%

84.1 95% 30.6 24%

Business Review – next steps

7

• Further sales are expected to follow in the coming months

• On a proforma basis based on the FY20 financial statements the

sales will improve LTV by 530bps to circa 47.9%

• The declared sales will reduce Net Income by £1.9m pa, or

£1.0m after the reduction in borrowing costs

• Headroom will increase from £14m to £18m initially

• This will impact profits and dividend levels for the foreseeable

future whilst we execute our plan

• However, this action reduces Retail exposure, reduces absolute

borrowings and LTV, and gives headroom for future growth. The

underlying strengths of the business remain:

Business Strengths

• Strong regional portfolio diversified across sectors with a strong emphasis in Leeds & Manchester

• Established relationships with our tenants proven during the COVID-19 crisis

• A resilient business with a long track record

• A development pipeline of over £600m of high-quality assets

• A secure mix of short- and long-term funding arrangements

• An experienced team with clear long-term shareholder aligned priorities

Financial performance

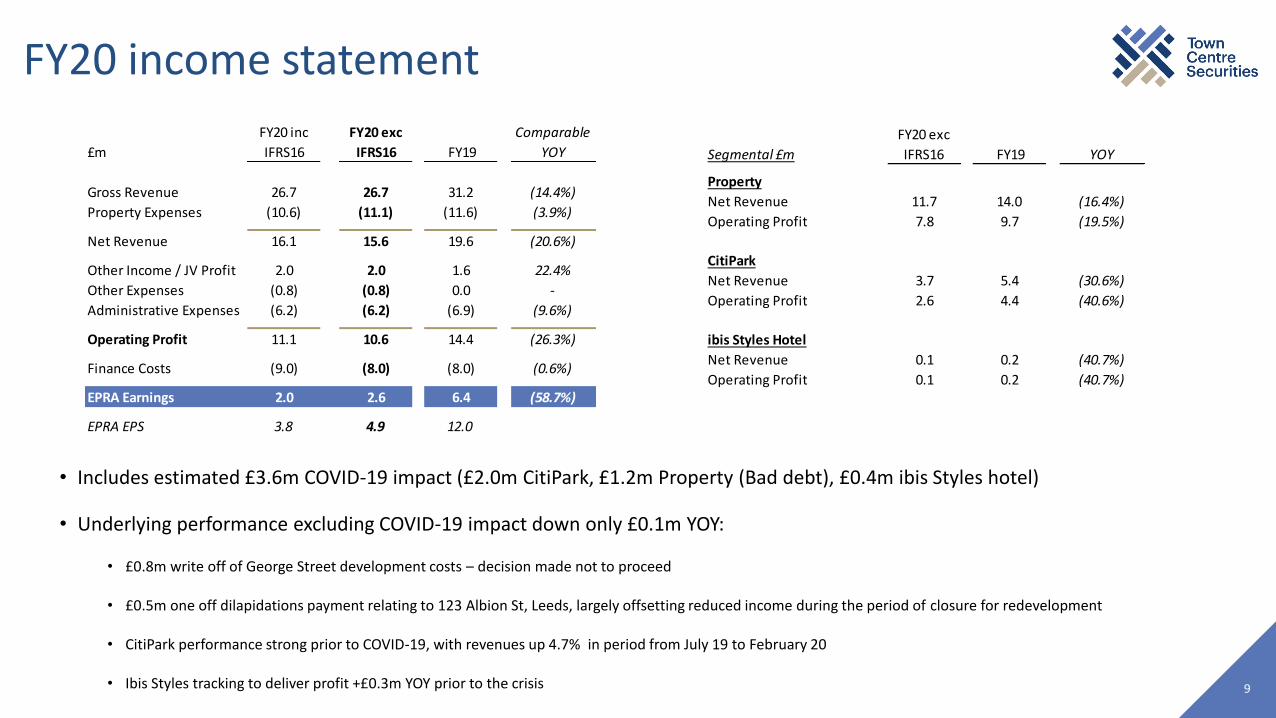

FY20 income statement

• Includes estimated £3.6m COVID-19 impact (£2.0m CitiPark, £1.2m Property (Bad debt), £0.4m ibis Styles hotel)

• Underlying performance excluding COVID-19 impact down only £0.1m YOY:

• £0.8m write off of George Street development costs – decision made not to proceed

• £0.5m one off dilapidations payment relating to 123 Albion St, Leeds, largely offsetting reduced income during the period of closure for redevelopment

• CitiPark performance strong prior to COVID-19, with revenues up 4.7% in period from July 19 to February 20

• Ibis Styles tracking to deliver profit +£0.3m YOY prior to the crisis 9

£m

FY20 inc

IFRS16

FY20 exc

IFRS16 FY19

Comparable

YOY

Gross Revenue 26.7 26.7 31.2 (14.4%)

Property Expenses (10.6) (11.1) (11.6) (3.9%)

Net Revenue 16.1 15.6 19.6 (20.6%)

Other Income / JV Profit 2.0 2.0 1.6 22.4%

Other Expenses (0.8) (0.8) 0.0 -

Administrative Expenses (6.2) (6.2) (6.9) (9.6%)

Operating Profit 11.1 10.6 14.4 (26.3%)

Finance Costs (9.0) (8.0) (8.0) (0.6%)

EPRA Earnings 2.0 2.6 6.4 (58.7%)

EPRA EPS 3.8 4.9 12.0

Segmental £m

FY20 exc

IFRS16 FY19 YOY

Property

Net Revenue 11.7 14.0 (16.4%)

Operating Profit 7.8 9.7 (19.5%)

CitiPark

Net Revenue 3.7 5.4 (30.6%)

Operating Profit 2.6 4.4 (40.6%)

ibis Styles Hotel

Net Revenue 0.1 0.2 (40.7%)

Operating Profit 0.1 0.2 (40.7%)

Rent Collections

• Throughout the crisis the strength of our tenant relationships, the diversified nature of our portfolio, and our lack of exposure to

traditional high street retail has led to a continued strong level of rent receipts

• Since the 25th March quarter day and up to 15th September 2020 we have collected or agreed deferrals for 86% of billed rent and

service charge:

10

£m

Total Billed 13.3

Total Paid 10.9 82%

Total Deferred 0.5 4%

Total Paid or Deferred 11.4 86%

To be written off as an incentive 0.8 6%

No agreement 1.1 8%

Amounts are rent and service charge combined and include VAT where relevant

• The top 10 tenants with no agreement total £0.7m of

the £1.1m reported

• These include Go Outdoors (JD Sports), The Deltic

Group, Boots, M&S, and Café Nero

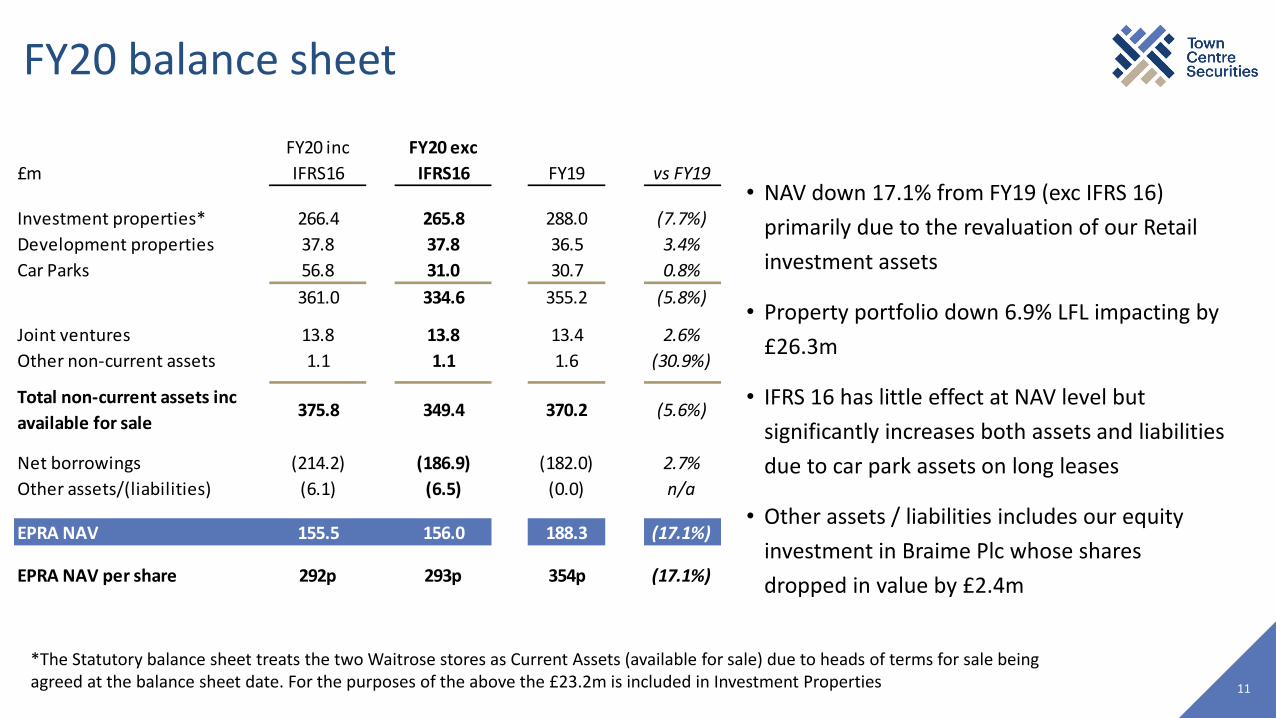

FY20 balance sheet

• NAV down 17.1% from FY19 (exc IFRS 16)

primarily due to the revaluation of our Retail

investment assets

• Property portfolio down 6.9% LFL impacting by

£26.3m

• IFRS 16 has little effect at NAV level but

significantly increases both assets and liabilities

due to car park assets on long leases

• Other assets / liabilities includes our equity

investment in Braime Plc whose shares

dropped in value by £2.4m

11

£m

FY20 inc

IFRS16

FY20 exc

IFRS16 FY19 vs FY19

Investment properties* 266.4 265.8 288.0 (7.7%)

Development properties 37.8 37.8 36.5 3.4%

Car Parks 56.8 31.0 30.7 0.8%

361.0 334.6 355.2 (5.8%)

Joint ventures 13.8 13.8 13.4 2.6%

Other non-current assets 1.1 1.1 1.6 (30.9%)

Total non-current assets inc

available for sale375.8 349.4 370.2 (5.6%)

Net borrowings (214.2) (186.9) (182.0) 2.7%

Other assets/(liabilities) (6.1) (6.5) (0.0) n/a

EPRA NAV 155.5 156.0 188.3 (17.1%)

EPRA NAV per share 292p 293p 354p (17.1%)

*The Statutory balance sheet treats the two Waitrose stores as Current Assets (available for sale) due to heads of terms for sale being agreed at the balance sheet date. For the purposes of the above the £23.2m is included in Investment Properties

At 30 June 2020:

• Retail represents only 35% of the Portfolio

- 1/3rd Merrion, 1/3rd supermarket/discount/convenience

• Retail & Leisure represents 47% of the portfolio, down

from 70% in 2016, and 80% in 2008

Following recent sales:

• Retail represents only 30% of the Portfolio

• Retail & Leisure now represents 42% of the portfolio

Repositioning the portfolio – Continuing to reduce Retail & Leisure

12

Other – predominantly Development (10% in HY20) and Residential (6% in HY20)

Secure funding

• Loan to Value increases to 53.2% as a result of COVID-19

impact on cashflows and capex primarily at 123 Albion St

• Following recent sales the LTV drops to 47.8%

• £106m debenture at 5.375% maturing in 2031

• £103m RCFs with RBS, Lloyds and Handelsbanken, plus

£5m overdraft facility 13

• Headroom stood at £14.8m at year end

• At September 20 it stood at £13.7m

• Following the recent asset sales headroom increases to

£18.2m

• Further sales and restructuring of the security pool will

give the opportunity for further increases in headroom

FY20 FY19

Net Debt £183.6m £177.5m

Loan to value 53.2% 48.8%

Interest cover (underlying) 2.1 1.8

Weighted average cost of debt 4.1% 4.2%

Bank facilities £108m £108m

Debenture £106m £106m

Weighted average maturity 6.7 7.6

Note excludes IFRS 16 accounting, f inance leases, and JVs on a net basis

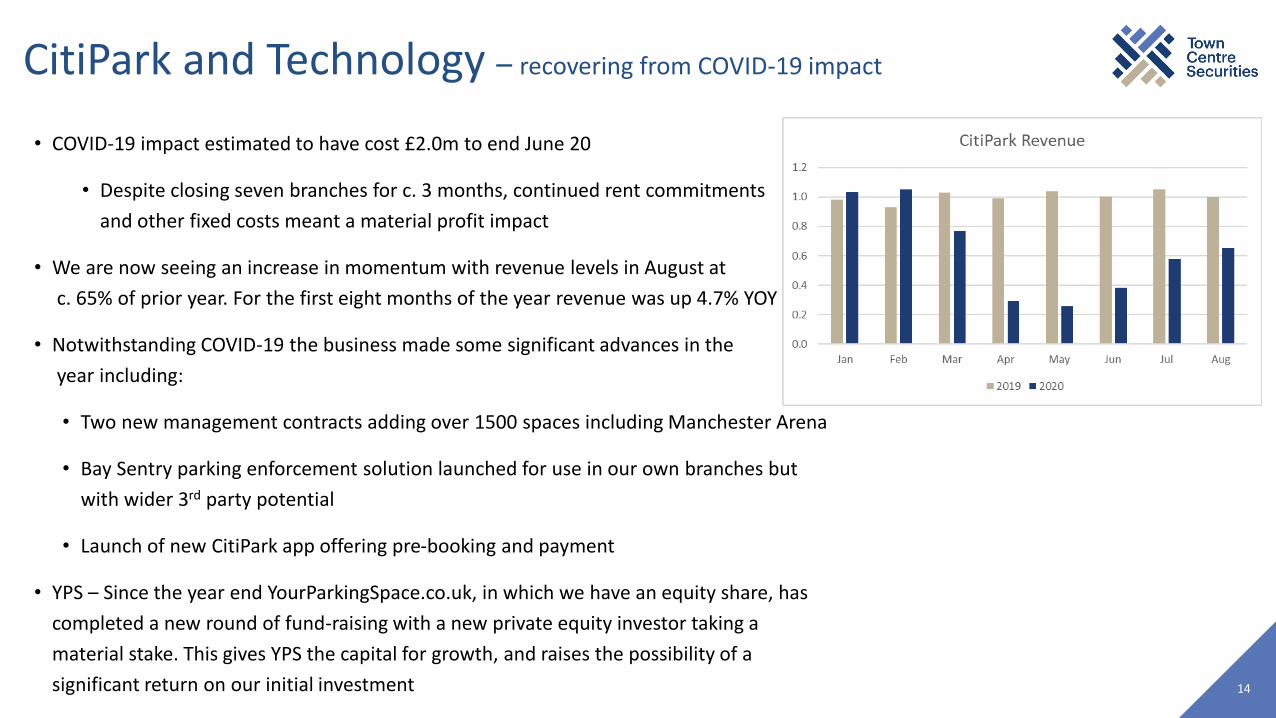

CitiPark and Technology – recovering from COVID-19 impact

• COVID-19 impact estimated to have cost £2.0m to end June 20

• Despite closing seven branches for c. 3 months, continued rent commitments

and other fixed costs meant a material profit impact

• We are now seeing an increase in momentum with revenue levels in August at

c. 65% of prior year. For the first eight months of the year revenue was up 4.7% YOY

• Notwithstanding COVID-19 the business made some significant advances in the

year including:

• Two new management contracts adding over 1500 spaces including Manchester Arena

• Bay Sentry parking enforcement solution launched for use in our own branches but

with wider 3rd party potential

• Launch of new CitiPark app offering pre-booking and payment

• YPS – Since the year end YourParkingSpace.co.uk, in which we have an equity share, has

completed a new round of fund-raising with a new private equity investor taking a

material stake. This gives YPS the capital for growth, and raises the possibility of a

significant return on our initial investment 14

Debenture SpecificPerformance

Amount outstanding £106m

Coupon 5.375%

Maturity 2031

ICR at last reporting date 2.014x cover as at 30 June 2020

Asset Cover at last reporting date 1.546x cover as at 30 June 2020

Top up levels 1.5x asset cover; 1x income cover

Withdrawal levels 1 2/3s asset cover; 1.15x Income cover

Substitution Equal value asset cover; 1.15x income cover or equal

Valuation Every 5 years (for information, provided every 12 months)

Key Terms of the Mortgage Debenture Stock

16

Debenture Specific Performance

17

2016 – 3 properties removed with no additions

2017 – Empire House sold and removed, Premier Inn and Clements Rd MSCP added

Reversionary Covenant represents the cover that we would have to return to following any breach

Jun-16 Jun-17 Jun-18 Jun-19 Jun-20

Valuation

Actual £m 176.9 180.5 184.5 176.7 163.9

Cover (times) 1.67 1.70 1.74 1.67 1.55

Minimum Covenant 1.50 1.50 1.50 1.50 1.50

Reversionary Covenant 1.67 1.67 1.67 1.67 1.67

Income

Actual £m 11.1 10.2 12.0 12.0 11.5

Cover (times) 1.95 1.79 2.10 2.10 2.01

Covenant 1.00 1.00 1.00 1.00 1.00

Properties within the Debenture

18

Valuation £m Income £m NIY

Jun-20 Jun-20

Merrion Centre LEEDS Mixed Use 104.6 8.49 8.1%

Urban Exchange, MANCHESTER Retail 14.8 1.08 7.3%

Premier Inn, Whitehall Road LEEDS Hotel 14.5 0.68 4.7%

Merrion Hotel LEEDS Hotel 8.6 0.14 1.6%

CitiPark Clarence Dock LEEDS Car Park 10.5 0.53 5.0%

8/10 West Park HARROGATE Retail 2.7 0.22 8.2%

CitiPark 30 Tariff Street MANCHESTER Car Park 3.8 0.17 4.4%

CitiPark Clements Road, ILFORD Car Park 3.0 0.03 1.1%

6/24 Abingdon Street BLACKPOOL Retail 1.2 0.14 11.2%

75 Dale Street MANCHESTER Offices 0.3 0.00 0.0%

163.9 11.5 7.0%

Property

Type

Valuation since Jun-14

Abingdon Road market in process of being sold for £1.2m, with the proceeds from the sale being substituted in as security for the time being

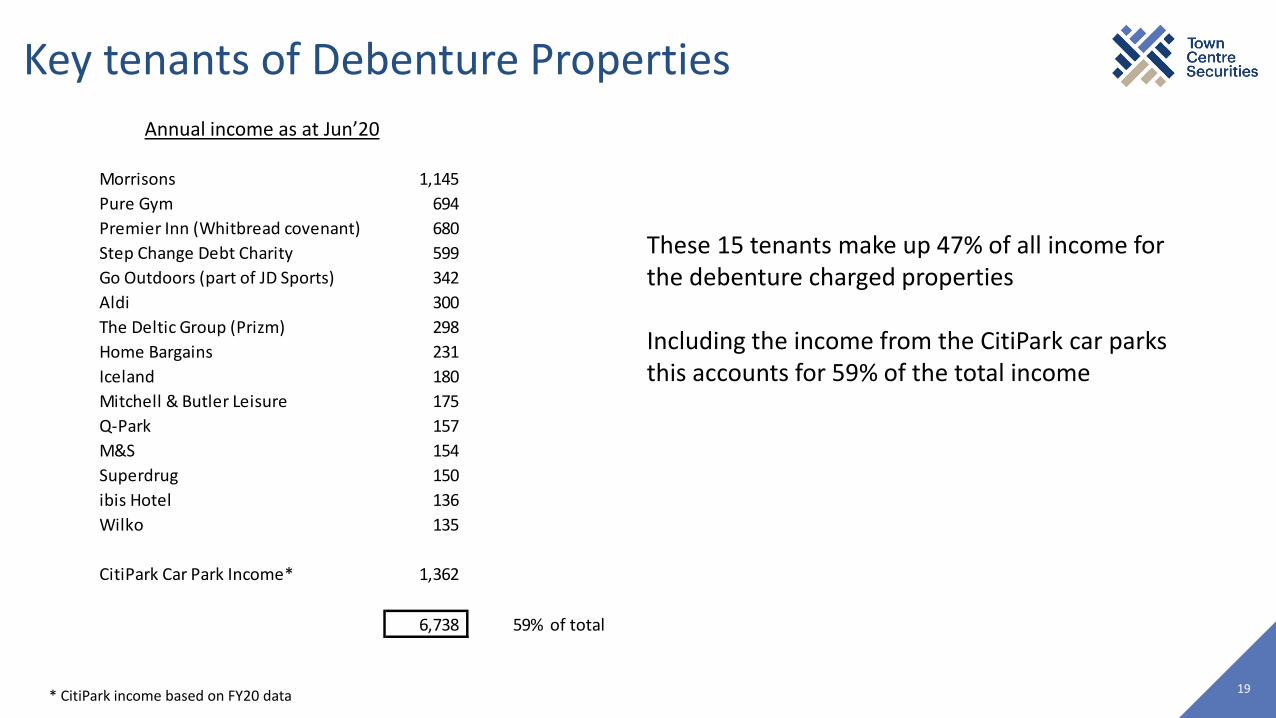

Key tenants of Debenture Properties

19

Annual income as at Jun’20

* CitiPark income based on FY20 data

• These 15 tenants make up 47% of all income for the debenture charged properties

• Including the income from the CitiPark car parks this accounts for 59% of the total income

Morrisons 1,145

Pure Gym 694

Premier Inn (Whitbread covenant) 680

Step Change Debt Charity 599

Go Outdoors (part of JD Sports) 342

Aldi 300

The Deltic Group (Prizm) 298

Home Bargains 231

Iceland 180

Mitchell & Butler Leisure 175

Q-Park 157

M&S 154

Superdrug 150

ibis Hotel 136

Wilko 135

CitiPark Car Park Income* 1,362

6,738 59% of total

Strengthening the portfolio

Adding value to new acquisitions – 123 Albion St, Leeds

21

• Purchased in 2018 for £12m – 50k sqft office space and 22k sqft leisure on ground floor

• £4m net capex scheme now complete

• Estimated total running yield on cost of 8.5%

• Since acquisition we have renewed the lease with the Secretary of State for 10k sqft, and agreed Dilapidations payment with

departing tenant

• We have seen significant interest in the redeveloped space and are working with a number of potential tenants

The Cube

Merrion Estate

Actively managing assets – Ducie House, Manchester

22

• TCS has commenced a significant refurbishment of Ducie House, a 33k sqft historic flexible office conversion

• £2m improvement halted during COVID-19, now recommenced, completing this autumn

• Work will reconfigure the office space, create common amenity and break-out spaces, an improved reception, shower facilities and new lifts

• Expected to increase net income by c. £0.3m per annum and deliver a post investment return on investment of 8.5%

• Car park continues to present a development opportunity for a 60,000 sqft 7 storey office

22

Maximising Available Capital – CitiPark Manchester arena

23

• In order to drive growth in the CitiPark business whilst minimising capital requirements we continue to seek car park management contracts

• In the year we secured two new contracts; 546 spaces at Victoria Mills, Shipley, and the 978 spaces at the Manchester Arena car park

• Manchester Arena normally attracts over 1.2m visitors each year being the largest indoor arena in Europe

• Car park also well placed for the main retail and visitor attractions

• Agreed an initial two-year contract delivering a fixed management fee and the opportunity to share in profits over an agreed level

• Using our local knowledge, operational expertise and technological solutions we expect this new addition to be a keystone in our future growth strategy

• All delivered with minimal capital expenditure, and no exposure to fixed costs

23

Development pipeline of +£600m – delivering future growth

• GDV pipeline value of over £600m

• Land currently in TCS ownership with detailed planning or

strategic frameworks in place for the majority

• Opportunity to reconfigure Whitehall Road plans

• Exploring options to unlock Piccadilly Basin developments24

100MC, Merrion, Leeds CGI

Whitehall Road developments, Leeds CGI

Eider House PRS, Manchester CGI

Development Type Status

Estimated

GDV

Estimated

Income

Yield on

Cost

Manchester - Eider House Residential Detailed planning £41m £1.6m 5.2%

Leeds - Car Park Car Park Detailed planning £14m £1.2m 9.1%

Leeds - Whitehall Road No2 Offices Detailed planning £92m £5.3m 7.0%

Leeds - Whitehall Road No3 Offices Strategic Framework £40m £2.8m 9.3%

Leeds - Whitehall Road No7 Offices / Leisure Strategic Framework £28m £2m 9.2%

Leeds - 100MC Merrion Office Offices Detailed planning £62m £4m 7.1%

Manchester - Residential Tower A Residential Strategic Framework £82m £3.5m 5.2%

Manchester - Residential Tower B Residential Strategic Framework £55m £2.4m 5.2%

Manchester - Residential D Residential Strategic Framework £28m £1.1m 4.9%

Manchester - Ducie House Offices Unscoped £21m £1.3m 7.8%

Manchester - Commercial Mixed Use Strategic Framework £76m £5m 7.9%

Manchester - Car Park Car Park Strategic Framework £12m £0.8m 7.2%

Leeds - Merrion Corner Tower Residential / Mixed Use Unscoped £50m £3m 6.4%

£601m £34m

Outlook

Outlook

26

Resetting and reinvigorating the business for the future

• The strength of the business has ensured continued

operation during the disruption

• Footfall is improving, our Car Parks are open and getting

busier, and occupancy at our hotel is strengthening

• Our strategy remains appropriate but its delivery needed to

be accelerated

• Property sales will enable the resetting of the business but

will impact profits and dividend levels whilst we execute it

• Our unique strengths remain intact, namely our knowledge

of the Leeds and Manchester markets, our long-term

approach, and our large high-quality development pipeline

Appendices:

- Our portfolio- Our Leeds assets- Piccadilly Basin, Manchester

Our diversified portfolio

• LFL reduction of 6.9% driving a £26.3m revaluation charge

• Total Retail and Leisure overall reduced by 11.8%

28Note the above table includes Merrion House within Offices and Burlington House within Residential, and therefore differs from the notes in the accounts

Note excludes IFRS16 adjustments to Car Park valuations

Passing rent ERV Value

% of

portfolio

Valuation

incr/(decr) Initial yield

Reversionary

yield

Retail & Leisure 3.6 4.1 51.1 14% -19.2% 6.6% 7.5%

Merrion Centre (ex offices) 7.0 7.4 85.7 23% -7.9% 7.7% 8.1%

Offices 3.8 6.2 82.5 22% -2.9% 4.4% 7.1%

Hotels 1.2 1.6 23.1 6% -10.5% 4.8% 6.7%

Out of town retail 2.5 2.5 38.0 10% -9.5% 6.3% 6.2%

Distribution 0.4 0.4 6.0 2% -2.1% 6.5% 6.7%

Residential 1.1 0.6 21.5 6% -1.3% 5.0% 2.8%

19.7 22.8 307.9 83% -8.6% 6.0% 7.0%

Development property 1.6 1.6 37.8 10% 2.6%

Other Car parks 0.9 0.9 26.9 7% 1.3%

Portfolio 22.2 25.3 372.5 100% -6.9%

• Part of the 4th largest conurbation in the

UK

• City alone has a workforce of over 2m

• Significant growth in employment and city

living forecast

• >3,500 student rooms under construction

around Merrion alone

• 60% of our portfolio with the Merrion

Estate being our largest single asset

• £148m asset, £42m invested since 2012

• Creation of a true mixed-use asset

• Significant student developments around

the centre will continue to drive footfall

Leeds – a city of opportunity

29Merrion House Premier Inn, Whitehall Roadibis Styles hotel, Merrion

Leeds– TCS Assets

30

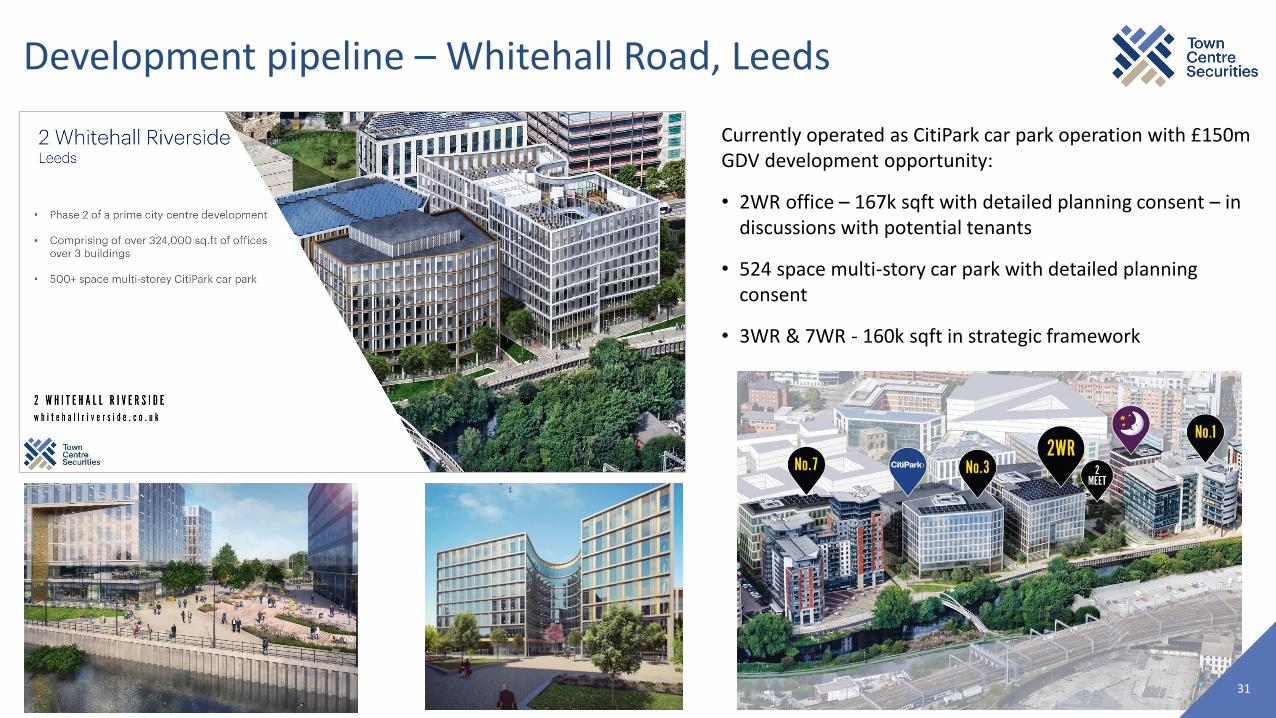

Development pipeline – Whitehall Road, Leeds

31

Currently operated as CitiPark car park operation with £150m GDV development opportunity:

• 2WR office – 167k sqft with detailed planning consent – in discussions with potential tenants

• 524 space multi-story car park with detailed planning consent

• 3WR & 7WR - 160k sqft in strategic framework

• Part of the 2nd largest conurbation in the UK

• 7m people within 1hr drive

• Significant growth in employment and city living forecast

• 18% of our portfolio based in the city with Piccadilly Basin providing our largest

development opportunity – over £300m GDV

• 12.5-acre mixed use development site in the heart of Manchester

• Mixed-use scheme with Offices, Residential, Retail, Leisure and Car Parking

• Framework includes another 638 residential units, a multi-storey car park and

c.177,000 sq ft of commercial development

• Opened first bespoke PRS building in Sept’19, with second building having detailed

planning consent

Manchester – significant opportunity for growth

32

33

As is Piccadilly Basin Manchester

10

11

7

9

8

5

6

4

1

2

3

1

Car park and Development

Burlington House

Car park and Development

2 Urban Exchange

3

AVRO (Urban Splash dev)

Car park and Development

5

Multistorey car park

4

6

7

8

9

10

11

Ducie House

Development – Eider House

Carvers Warehouse

Car park and Development

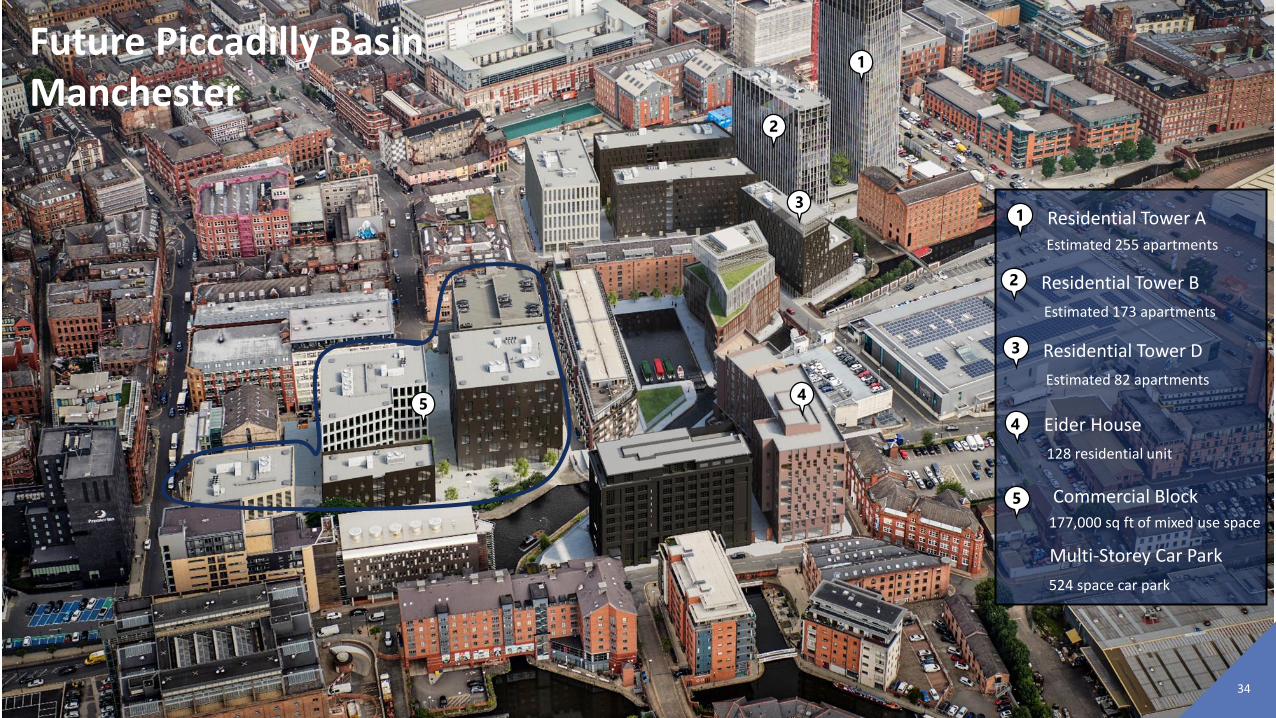

34

Future Piccadilly Basin Manchester

1

2

3

45

1 Residential Tower A

Commercial Block

Estimated 255 apartments

2 Residential Tower B

Estimated 173 apartments

3 Residential Tower D

Estimated 82 apartments

177,000 sq ft of mixed use space

Multi-Storey Car Park

524 space car park

5

Eider House

128 residential unit

4

35

Town Centre House

The Merrion Centre

Leeds, LS2 8LY

+44 (0)113 222 1234

6 Duke Street

Marylebone

London, W1U 3EN

+44 (0)20 3370 0080

Town Centre Securities Plc

www.tcs-plc.co.uk