Embed Size (px)

Citation preview

February 12, 2015 Industry Report

Ralph Garcea, MBA, P.Eng. [email protected] 416-849-5004

Sales/Trading —Toronto: (416) 363-5757, (866) 442-4485

See disclosure and a description of our recommendation structure at the end of this report.

Eq

uit

y R

ese

arc

h

DEALER’S CHOICE Initiating Coverage on Amaya (BUY, TP $50.00) and NYX Gaming (BUY, TP $7.00)

According to a report by Global Betting and Gaming Consultants (GBGC), global gambling revenue (GGR) was ~US$451B in 2013 (+4.4% yoy). We estimate that the market will grow at a CAGR of 3.5%, reaching ~US$540B by 2020 (assuming a US$/€ exchange rate of 1.25). In addition, GBGC estimates that online gambling reached ~US$40B in 2013 or ~9% of GGR. We estimate that the online market will grow at a CAGR of 9%, reaching ~US$65B (or ~12% of GGR) by 2020 (assuming a US$/€ exchange rate of 1.25).

Based on data from H2 Gambling Capital, we estimate that for 2014, the online gambling market by segment was: Sportsbook (42%), Casino (23%), Poker (8%), Bingo (6%) and Skills/Lotteries (21%). By 2020, Sportsbook and Casino should be ~65-70% of the global online market.

We believe investors should own AYA and NYX. Both have great management teams that have experience in doing M&A transactions. Amaya will be looking to divest of some assets to help pay down debt, and may look at a Sportsbook transaction to gain scale quickly in the largest segment of the online gambling market. NYX Gaming went public in late December 2014 with a successful IPO, has already acquired the Ongame Network assets from Amaya, and has its sights set on acquiring Amaya’s Chartwell/Cryptologic assets.

Canadian Gambling Stocks: Global, Land-Based, Mobile and Online

Source: Cantor Fitzgerald Canada, FactSet

Price Rating Target Market Cap. LTM Revenue EV/Sales EV/EBITDA P/E

Ticker (Local) (Local) (US$) (US$) 2015 2016 2015 2016 2015 2016

Amaya Inc. AYA-CA 31.25 BUY 50.00 3,281 330 5.6 5.0 13.1 10.9 16.4 11.6

NYX Gaming Group Limited NYX-CA 4.75 BUY 7.00 127 24 3.4 2.8 17.0 7.7 50.8 21.6

Technology – Online Gambling February 12, 2015

Ralph Garcea, MBA, P.Eng. 416-849-5004 2 of 36

TABLE OF CONTENTS

Global Gambling Industry Overview .......................................................................... 3 Online Gambling in the U.S. ........................................................................................ 4 Increasing Taxes On Online Gambling ...................................................................... 5 Mobile Penetration ......................................................................................................... 5 Consolidation Continues ............................................................................................... 6 How To Play This In Canada…. .................................................................................. 6 AMAYA INC. ................................................................................................................. 8 Introduction ..................................................................................................................... 9 Investment Thesis ........................................................................................................... 9

Transformational Acquisition World’s Largest Poker Business ................ 9 Divestitures to Pay Down Debt and Share Buyback ......................................... 9 Growth Includes Casino and Mobile ................................................................... 9 What about Sportsbook? ........................................................................................ 9 Strong Board Drives Compliance and Transparency ........................................ 9

Catalysts ..........................................................................................................................10 Divestitures .............................................................................................................10 Q4/14 Results ........................................................................................................10 Dual Listing ............................................................................................................10

Risks ................................................................................................................................10 Company Overview ......................................................................................................11 Products and Services...................................................................................................12

PokerStars/Full Tilt Poker ...................................................................................12 Casino ......................................................................................................................13 Sportsbook .............................................................................................................13 Mobile......................................................................................................................13

Competitors ...................................................................................................................13 Financial Forecast .........................................................................................................14 Recommendation and Valuation ................................................................................16 Appendix 1: Management and Board of Directors .................................................17 Appendix 2: Financial Statements ..............................................................................18 NYX GAMING GROUP LTD. ...............................................................................22 Introduction ...................................................................................................................23 Investment thesis ..........................................................................................................23

Full Suite of Products Built on an Open Technology Platform ....................23 Recurring Revenue Business Model ...................................................................23 Blue-Chip Customer Base ....................................................................................23 Experienced Management Team ........................................................................23

Catalysts ..........................................................................................................................24 Acquisition of Amaya’s B2B assets ....................................................................24 Leveraging the Ongame Networks Acquisition ...............................................24

Risks ................................................................................................................................24 Company Overview ......................................................................................................24 Products and Services...................................................................................................26 Competitors ...................................................................................................................27 Business Model ..............................................................................................................27 Financial Forecast .........................................................................................................29 Recommendation and Valuation ................................................................................30 Appendix 1: Management and Board of Directors .................................................31 Appendix 2: Financial Statements ..............................................................................32

Technology – Online Gambling February 12, 2015

Ralph Garcea, MBA, P.Eng. 416-849-5004 3 of 36

GLOBAL GAMBLING INDUSTRY OVERVIEW

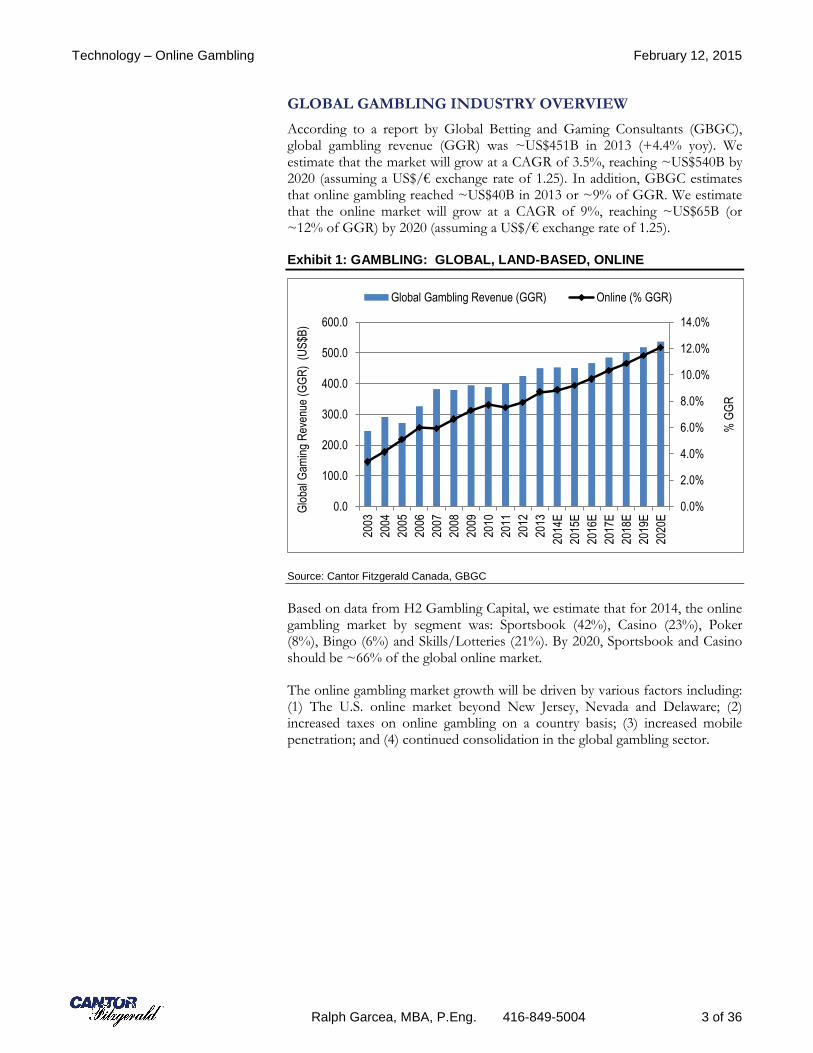

According to a report by Global Betting and Gaming Consultants (GBGC), global gambling revenue (GGR) was ~US$451B in 2013 (+4.4% yoy). We estimate that the market will grow at a CAGR of 3.5%, reaching ~US$540B by 2020 (assuming a US$/€ exchange rate of 1.25). In addition, GBGC estimates that online gambling reached ~US$40B in 2013 or ~9% of GGR. We estimate that the online market will grow at a CAGR of 9%, reaching ~US$65B (or ~12% of GGR) by 2020 (assuming a US$/€ exchange rate of 1.25).

Exhibit 1: GAMBLING: GLOBAL, LAND-BASED, ONLINE

Source: Cantor Fitzgerald Canada, GBGC

Based on data from H2 Gambling Capital, we estimate that for 2014, the online gambling market by segment was: Sportsbook (42%), Casino (23%), Poker (8%), Bingo (6%) and Skills/Lotteries (21%). By 2020, Sportsbook and Casino should be ~66% of the global online market.

The online gambling market growth will be driven by various factors including: (1) The U.S. online market beyond New Jersey, Nevada and Delaware; (2) increased taxes on online gambling on a country basis; (3) increased mobile penetration; and (4) continued consolidation in the global gambling sector.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0.0

100.0

200.0

300.0

400.0

500.0

600.0

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

E

2015

E

2016

E

2017

E

2018

E

2019

E

2020

E

% G

GR

Glo

bal G

amin

g R

even

ue (

GG

R)

(U

S$B

)Global Gambling Revenue (GGR) Online (% GGR)

Technology – Online Gambling February 12, 2015

Ralph Garcea, MBA, P.Eng. 416-849-5004 4 of 36

Exhibit 2: GLOBAL ONLINE GAMBLING – BY SEGMENT

Source: Cantor Fitzgerald Canada, H2 Gambling Capital

ONLINE GAMBLING IN THE U.S.

The U.S. online gambling market has been a disappointment to date, with New Jersey (NJ), Nevada and Delaware the only states to legalize Internet gaming. In NJ, Internet Gaming Win (IGW) for December 2014 came in at $10.7M (+23% m/m and +64% y/y). For the year, NJ’s IGW came in at ~$123M – driven by Borgata (36%), Caesars Interactive (27%), Tropicana (18%), Golden Nugget (9%) and the discontinued Trump operations (10%).

Exhibit 3: NEW JERSEY ONLINE GAMING (~$123M in 2014)

Source: Cantor Fitzgerald Canada, New Jersey Office of the Attorney General (Division of Gaming Enforcement)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Betting Casino Poker Bingo Skill, Lotteries

0

100,000

200,000

300,000

400,000

500,000

600,000

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Num

ber

of A

ccou

nts

Rev

enue

(U

S$0

00s)

Internet Gross Revenue Internet Gaming Accounts

Technology – Online Gambling February 12, 2015

Ralph Garcea, MBA, P.Eng. 416-849-5004 5 of 36

California AB-167. The real opportunity in the US online market lies in California where Assemblyman Reggie Jones-Sawyer recently reintroduced an online poker bill with significant changes to the so-called “bad actor” clause (which would allow for PokerStars participation) and the inclusion of horse racing tracks. In addition, the bill removed the language preventing agreements to pool players with other states. While Internet poker was first discussed in the California state legislature in 2008, there remains a lot of work to be done to get the bill passed.

Washington and Mississippi Say No to Online Poker. The Washington State online poker bill (HB 1114) which was presented to the state legislature in early January 2015, did not get enough support to move forward in the current session. Note that Washington is the only state in the U.S. where playing online

poker is actually illegal! For a third consecutive year, Mississippi’s “Lawful Internet Gaming Act” failed to gather enough support to make it into the legislature session.

INCREASING TAXES ON ONLINE GAMBLING

U.K. POC Tax. According to GBGC, several markets (U.K., Italy, Spain, France, Denmark) have begun regulating online gambling and offering domestic licences to private companies to prevent offshore leakage of tax revenues. The U.K. introduced a new bill on December 1, 2014 which brought into play a 15% Point of Consumption (POC) tax on offshore gambling operators vs the previous tax on Point of Supply (POS) where offshore operators benefitted from low tax rates in such jurisdictions as Gibraltar, Isle of Man and Malta. According to GBGC, the higher gambling taxes may increase GGR as operators have to increase margins or rake percentages to cover the higher taxes.

New EU VAT Directive. On January 1, 2015, the European Union (EU) imposed new rules regarding the application of a value-added tax (VAT) to businesses providing telecommunications, broadcasting or electronically supplied services to customers in EU Member States (another POC-type tax, with VAT’s varying by country). Online gambling had traditionally been exempt from VAT but that decision has now been left to individual markets – Germany does not provide this exemption. According to a KPMG report, the changes will not affect businesses supplying services on a business-to-business (B2B) basis. Bwin.party is one of the first publically-traded online gambling operators to report an impact from the new EU VAT directive. BWIN has warned that the new law could cost the company an extra €15M in 2015 as Germany (~25% of revs) is charging a 19% VAT on BWIN’s casino and poker revenue from the country vs a 0% VAT previously as BWIN is based in Gibraltar and the VAT was POS-based previously.

MOBILE PENETRATION

The increase in mobile penetration for online gambling has been driven by the continued expansion of high-speed wireless broadband (3G/4G) and the growth in smartphone/tablet shipments. According to a GBGC report, gross gaming revenue (GGR) from mobile devices is expected to grow from US$1B (<5% of online total) in 2006 to ~US$21B (~32% of online total) in 2020.

Technology – Online Gambling February 12, 2015

Ralph Garcea, MBA, P.Eng. 416-849-5004 6 of 36

CONSOLIDATION CONTINUES

There were some large acquisitions in 2014, led by the GTECH/IGT (Pending), Amaya/Rational Group and Scientific Games/Bally Technologies transactions. The land-based vendors were consolidating amongst themselves (Bally/SHFL, GTECH/IGT) to gain scale and cut costs, and to move into other physical markets (Aristocrat/VGT, GCA/MGAM). Intertain Group closed two acquisitions (Mandalay Media/Vera&John) that delivered immediate scale in the Bingo and Casino markets. We expect the consolidation to continue, and for Amaya, Intertain and NYX to be active participants.

Exhibit 4: RECENT TRANSACTIONS IN THE GAMBLING SECTOR

Source: Cantor Fitzgerald Canada, FactSet, Bloomberg

HOW TO PLAY THIS IN CANADA….

We believe investors should own AYA and NYX. Both have great management teams that have experience in doing M&A transactions. Amaya will be looking to divest of some assets to help pay down debt, and may look at a Sportsbook transaction to gain scale quickly in the largest segment of the online gambling market. NYX Gaming went public in late December 2014 with a successful IPO, has already acquired the Ongame Network assets from Amaya, and has its sights set on acquiring Amaya’s Chartwell/Cryptologic assets.

Closing Date Acquirer Target Ent. Value (US$M) EV/REV EV/EBITDA

Pending Intertain Group Gamesys (Jackpotjoy) $682.5 3.4x 6.4x

Pending GTECH S.p.A. International Game Technology $6,385.9 2.8x 12.6x

12/23/2014 Intertain Group Dumarca / Vera&John $118.7 3.2x 11.0x

12/19/2014 Global Cash Access Multimedia Games $1,112.1 5.1x 10.2x

11/21/2014 Scientific Games Bally $4,978.1 4.4x 14.5x

10/21/2014 Aristocrat Video Gaming Tech $1,283.0 5.4x 8.2x

08/01/2014 Amaya Gaming Rational Group $4,900.0 4.9x 11.7x

07/14/2014 Intertain Group Mandalay Media $100.4 3.4x 6.9x

06/05/2014 Bally Dragonplay $100.0

11/25/2013 Bally SHFL $1,283.5 4.7x 15.4x

03/20/2013 William Hill Sporting Bet $656.40 2.2x

01/31/2013 Scientific Games WMS $1,549.7 2.3x 7.1x

11/20/2012 Boyd Gaming Peninsula Gaming $1,444.0 4.1x 13.2x

11/05/2012 Amaya Gaming Cadillac Jack $167.0 2.1x 4.2x

11/01/2012 Amaya Gaming Ongame Network $19.3

02/23/2012 Bally Chiligaming

01/12/2012 International Game Technology DoubleDown $420.0 4.2x 16.8x

05/05/2011 International Game Technology Entraction $90.6 1.7x 17.0x

04/26/2011 Scientific Games Barcrest $54.0

07/29/2010 PartyGaming Bwin $1,055.2 2.6x 10.6x

AVERAGES: 3.5x 11.0x

Technology – Online Gambling February 12, 2015

Ralph Garcea, MBA, P.Eng. 416-849-5004 7 of 36

Exhibit 5. Global Gambling Comparables

Source: Cantor Fitzgerald Canada, FactSet

Price Rating Target Market Cap. LTM Revenue EV/Sales EV/EBITDA P/E

Ticker (Local) (Local) (US$) (US$) 2015 2016 2015 2016 2015 2016

Amaya Inc. AYA-CA 31.25 BUY 50.00 3,281 330 5.6 5.0 13.1 10.9 16.4 11.6

NYX Gaming Group Limited NYX-CA 4.75 BUY 7.00 127 24 3.4 2.8 17.0 7.7 50.8 21.6

Great Canadian Gaming Corporation GC-CA 19.40 1,055 399 3.4 3.3 8.4 8.1 17.7 16.7

Pollard Banknote Limited PBL-CA 6.00 112 184 9.7 12.1 9.1 7.9 18.8 15.0

Imperus Technologies Corp. LAB-CA 0.58 34 - - - - - - -

DEQ Systems Corp. DEQ-CA 0.15 8 7 - - - - - -

Poydras Gaming Finance Corp PYD-CA 0.08 4 - - - - - - -

Contagious Gaming Inc. CNS-CA 0.41 11 - - - - - - -

Las Vegas From Home.com Entertainment Inc.LVH-CA 0.04 4 0 - - - - - -

International Game Technology IGT 17.15 4,265 1,968 2.9 2.7 9.3 7.7 15.2 13.3

Scientific Games Corporation Class A SGMS 12.79 1,085 1,622 1.4 1.4 3.7 3.4 -4.1 -5.8

Global Cash Access Holdings, Inc. GCA 6.67 437 581 0.6 0.6 3.0 2.2 6.6 5.7

William Hill PLC WMH-GB 3.85 5,148 2,508 2.4 2.3 10.7 10.0 15.3 14.0

Paddy Power Plc PAP-GB 68.57 3,794 1,034 3.0 2.7 14.5 12.8 24.2 21.4

Ladbrokes plc LAD-GB 1.19 1,677 1,857 1.3 1.3 8.6 8.0 14.5 12.6

Playtech plc PTEC-GB 7.19 3,219 549 5.0 4.7 11.5 10.7 16.2 15.1

bwin.party digital entertainment Plc BPTY-GB 1.01 1,267 851 1.6 1.5 9.8 9.1 21.4 19.3

Betfair Group plc BET-GB 15.88 2,242 732 2.5 2.4 13.0 11.4 26.0 21.5

Rank Group Plc RNK-GB 1.84 1,098 1,127 1.1 1.1 6.4 6.2 12.7 11.9

888 Holdings Plc 888-GB 1.72 931 425 1.7 1.7 11.6 10.5 20.4 17.7

32Red Plc TTR-GB 0.49 55 36 0.9 - 6.9 - 9.2 -

GVC Holdings PLC GVC-GB 4.54 424 273 1.8 1.7 8.0 7.6 9.0 8.8

Sportech PLC SPO-GB 0.64 200 172 1.0 1.0 4.5 4.4 13.8 13.2

GTECH S.p.A. GTK-IT 16.90 3,343 4,118 1.9 1.9 4.9 4.5 10.4 9.7

Unibet GRoup Plc Shs Swedish Depository ReceiptsUNIB-SE 473.00 1,608 510 2.6 2.4 11.3 11.1 14.9 16.0

Kambi Group plc Class B KAMBI-SE 72.50 257 42 3.6 NM 9.2 NM 19.6 NM

Net Entertainment NE AB Class B NET.B-SE 272.50 1,296 119 10.1 8.6 21.6 18.0 34.6 28.0

Mr Green & Co. AB MRG-SE 37.40 160 94 1.4 1.0 6.4 4.7 10.4 7.9

Aristocrat Leisure Limited ALL-AU 7.10 3,471 708 2.6 2.4 7.4 6.6 17.5 16.4

Ainsworth Game Technology Limited AGI-AU 2.75 683 224 2.8 2.6 7.6 6.8 12.5 11.5

AVERAGES: 2.5 2.3 9.0 8.2 15.2 13.6

February 12, 2015 Research Update

Ralph Garcea, MBA, P.Eng. [email protected] (416) 849-5004

Sales/Trading — Toronto: (416) 363-5757, (866) 442-4485

See disclosure and a description of our recommendation structure at the end of this report. 8 of 36

Company profile: Amaya is the owner of Rational Group (PokerStars/Full Tilt Poker) which runs the largest poker business in the world. Amaya also provides B2B interactive and physical gaming solutions to the regulated gaming industry.

Eq

uit

y R

ese

arc

h

AMAYA INC. What’s Next after the PokerStars/Full Tilt Poker Acquisition?

EVENT

We are initiating coverage of Amaya with a BUY recommendation, and a DCF-based one-year target price of $50.00 per share.

BOTTOM LINE

PokerStars was Transformative – What’s Next? With some of the gambling world’s biggest brands (including PokerStars and Full Tilt Poker), Amaya has amassed the largest poker business in the world (land-based, online and mobile). We expect growth to include the leveraging of the Casino assets on the PokerStars platform, as well as the move to mobile. At the end of Q3/14, PokerStars registered user base had grown to 95M from 90M in the previous quarter – Amaya is now a customer acquisition and cross-selling of products story.

FOCUS POINTS

▪ Divestitures to help pay back debt. Amaya has announced its intentions to divest of B2B assets including Cadillac Jack, Diamond Game Enterprises (DGE) and the Chartwell/ Cryptologic software development group.

▪ What about Sportsbook? Sportsbook represents ~40% of the global online gambling market. Amaya announced it will roll out its own solution in Q1/15, ahead of schedule. What if another acquisition is in the works to accelerate its move?

▪ Blue Sky Scenario. With a growing PokerStars base, a Casino roll out and a nascent Sportsbook, we could see 2016 revs of $2B and EBITDA of $900M+.

Recommendation: BUY

Symbol/Exchange: AYA/TSX

Sector: Technology - Online Gambling

All dollar values in C$ unless otherwise noted.

Current price: C$31.25

One-year target: C$50.00

Dividend / Yield ---/---

Target return 60%

Financial summary

Source: Cantor Fitzgerald Canada

Shares O/S (M) 132.56 52-Week Range $5.61 - $39.25

Market Cap ($M) 4,142.5 Avg. Weekly Volume (M) 3.15

Net Cash ($M) (2,854.2) Fiscal Year End 31-Dec

C$M 2013 2014E 2015E 2016E

Revenue 154.5 712.7 1,644.0 1,890.6

Revenue (YoY % ) 102.2% 361.2% 130.7% 15.0%

EBITDA 57.9 281.5 682.3 841.3

EBITDA margin 37.4% 39.5% 41.5% 44.5%

GAAP EPS (Diluted) (0.22) 0.85 1.35 2.77

Adjusted EPS (Diluted) (0.22) 1.04 1.99 2.85

Shares O/S 89.5 121.6 132.6 132.6

EV / Revenue 45.3x 9.8x 4.3x 3.7x

EV / EBITDA 120.9x 24.9x 10.3x 8.3x

P/E (adj. EPS) NMF 29.9x 15.7x 11.0x

0

1

2

3

4

5

$0

$10

$20

$30

$40

$50

Feb/14 Apr/14 Jun/14 Aug/14 Oct/14 Dec/14 Feb/15

Vol

ume

(M)

Pric

e ($

)

Amaya Inc. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 9 of 36

INTRODUCTION

With some of the gambling world’s biggest brands (including PokerStars, Full Tilt Poker, the European Poker Tour (EPT), PokerStars Caribbean Adventure, Latin American Poker Tour and the Asia Pacific Poker Tour), Amaya has amassed the largest poker business in the world (land-based, online and mobile). In addition, Amaya provides B2B interactive and physical gaming solutions to the regulated global gaming industry; and holds minority positions in Intertain Group (7%) and NYX Gaming (8%).

We are initiating coverage of Amaya with a BUY recommendation and a DCF-based one-year price target of $50.00 per share. On our estimates, Amaya currently trades at a C2016 EV/Sales of 3.7x and EV/EBITDA of 8.3x vs its Global Gaming comparables at an average of 2.3x and 8.2x, respectively.

INVESTMENT THESIS

Transformational Acquisition World’s Largest Poker Business

Amaya acquired the Rational Group in August 2014. PokerStars is a leading brand in online poker, which has led to the development of the world’s largest poker business (online, live tournaments/tours, poker rooms, TV, etc).

Divestitures to Pay Down Debt and Share Buyback

Amaya has announced its intentions to divest of B2B assets including Cadillac Jack (CJ), Diamond Game Enterprises (DGE) and the Chartwell/Cryptologic software development group. These could generate $600M to $800M in cash to pay down debt and support a share buyback.

Growth Includes Casino and Mobile

We expect growth to include the leveraging of the Casino assets on the PokerStars platform, as well as the move to mobile. At the end of Q3/14, PokerStars registered user base had grown to 95M from 90M in the previous quarter – Amaya is now a customer acquisition and cross-selling of products story.

What about Sportsbook?

Sportsbook represents 40% of the online gambling market. Amaya announced that it anticipates PokerStars' planned launch of sports betting will launch in Q1/15 - ahead of schedule. The sports betting product will launch within the PokerStars poker client in certain markets, and PokerStars will gradually add more markets as well as web and mobile versions throughout the year. What if another acquisition is in the works to accelerate its move into sports betting?

Strong Board Drives Compliance and Transparency

Amaya has a strong board of directors that has served it well through its recent acquisitions, and we expect the board to play a crucial roll going forward. Principles of social responsibility, transparency and good business practice are central to Amaya’s corporate approach

Amaya Inc. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 10 of 36

CATALYSTS

The following are three catalysts that could move the stock over the next 3 to 12 months.

Divestitures

As mentioned previously, the divestitures of CJ, DGE and the remaining Chartwell/Cryptologic assets could generate $600M to $800M in cash to pay down debt and support a share buyback. The strategic review of these assets is well underway and we could see some positive outcomes in the near-term.

Q4/14 Results

Amaya is set to report Q4/14 results by the end of March 2015. Guided to high end of the range. On the Q3/14 call, the Company guided to F2014 revenue of $669M to $715M and adj. EBITDA of $265M to $285M. Subsequent to that call, they guided that results were expected at the high end of the ranges.

Dual Listing

A dual listing is expected by the Fall 2015 on either the NYSE or London stock exchange. This event should help raise more capital to pay down debt or fund further M&A.

RISKS

Tax Increases in Regulated Countries

The recent tax increases in the U.K. and VAT taxes in the EU could impact the growth in online gambling if the operators decide to increase rakes or pass on the increased costs to players via alternate means. VIP rewards reductions and potential rake/fee increases in taxed areas are expected to counter up to 50% of the tax increases. Growth in business, including through recently introduced income streams such as currency conversion fees, expected to offset the remainder.

Pushback from PokerStars Customer Base

The PokerStars customer base has been very vocal on some of the early changes made by Amaya, and has forced Amaya to reverse some of the changes (introducing Casino games) or allow players the option to opt out.

Move into Sportsbook Disappoints

With Sportsbook such a major share of the online gambling market, a disappointing move into this segment may impact the stock adversely.

Amaya Inc. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 11 of 36

COMPANY OVERVIEW

Company Description

Amaya was founded in 2004, and is headquartered in Montreal with a global presence across North America, Latin America, Europe, and Asia. Since its IPO in July 2010, the Company has raised over $5B in capital to execute on its “build and buy” strategy – culminating in the acquisition of the Rational Group (PokerStars) in August 2014.

Exhibit 1. How Did We Get Here?

Source: Cantor Fitzgerald Canada, Company Documents

Recent Corporate Events

Amaya recently provided a corporate update focusing on three main initiatives: (1) Exploring the divestiture of its B2B businesses to facilitate debt repayment and/or a share buyback (includes Cadillac Jack (CJ), Diamond Game Enterprises (DGE) and its online casino games supplier Amaya Online (CryptoLogic/Chartwell); (2) announcement of a normal course issuer bid (NCIB) to purchase and cancel up to 5,399,631 common shares over a one-year period, representing up to approximately 5% of the public float of Amaya's common shares as of January 9, 2015; and (3) pursue a dual listing for 2015 on either the New York or London stock exchanges. Other announcements include the following:

Date Target Announcement

July 2011 Acquired for C$22.4M.

Chartwell developed and licensed gaming software and online casino game content to leading online firms such as Partygaming and 888

April 2012

Acquired for C$35.8M.

CryptoLogic offered internet-based gaming content and electronic software products to licensees to create virtual casinos, and operated InterCasino

Nov 2012 Acquired for $177M.

Privately-owned Cadillac Jack is a leading supplier of electronic games and game systems for the global gaming market with gaming machine placements in more than 200 venues in the United States and Mexico.

Nov 2012

Acquired for up to €25M.

Ongame Network is a leading B2B online poker network provider.

Divested to games supplier partner NYX Gaming Group in Dec. 2014.

Feb 2014 Acquired for $25M.

Diamond Game was a designer and manufacturer of gaming related products for the global casino gaming and lottery industries with gaming machine placements in approximately 100 venues in the United States and Canada.

Feb 2014 Divested for C$70M less a closing working capital adjustment of C$7.5M to Intertain Group.

WagerLogic is an online casino operator that was a subsidiary of CryptoLogic.

Aug 2014

Acquired Oldford Group, parent of Rational Group, for $4.9B, including certain deferred payment subject to adjustment.

Rational Group is the owner and operator of PokerStars and Full Tilt, collectively majority market share leader in online poker.

Largest poker business in the world including largest producer of live poker events and poker programming.

Amaya Inc. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 12 of 36

Exhibit 2. Recent Announcements

Date Announcement

Jan 21/2015 Appointed former Commissioner of the Ontario Provincial Police (OPP) Chris D. Lewis, as an advisor to its board of directors. It has also named George Sweny, a member of the Board of Directors of the Responsible Gambling Council of Canada and a gaming industry executive, as its Vice President of Strategic Ventures.

Mr. Lewis joins Ben Soave as an advisor to Amaya's board of directors. Mr. Soave, appointed in 2012, is a retired Chief Superintendent of the RCMP and internationally recognized innovator in the field of law enforcement, decorated by Canadian and foreign governments for his achievements combating organized crime and terrorism. Mr. Soave is also a member of Amaya's compliance committee.

Jan 15/2015 In December 2014 PokerStars completed the rollout of casino table games to players in eligible markets on PokerStars.com and certain domains sharing liquidity on the global network. The table games are available through the new PokerStars 7 platform, which is currently an optional download to players but which will become the sole poker client in the future. PokerStars will also launch web and mobile versions of its casino in 2015, supported by an aggressive consumer marketing campaign. Amaya announced that it anticipates PokerStars' planned launch of sports betting will launch in the first quarter of 2015, ahead of schedule. The sports betting product will launch within the PokerStars poker client in certain markets and PokerStars will gradually add more markets as well as web and mobile versions throughout the year.

Jan 12/2015 Amaya announced it intends to make a normal course issuer bid ("NCIB") to purchase and cancel up to 5,399,631 common shares over a one-year period, representing up to approximately 5% of the public float of Amaya's common shares as of January 9, 2015. The Corporation intends to fund such purchases through proceeds of certain divestments and cash on hand.

Further to Amaya's previously announced strategic review of its B2B land-based gaming solutions business, Cadillac Jack Inc., Amaya has received and is evaluating non-binding proposals from certain persons.

In the fourth calendar quarter of 2014, Amaya completed the divestiture of Ongame Network Limited, its B2B poker and platform provider, to NYX Gaming Group Ltd. ("NYX Gaming Group"), as discussed in the Corporation's November 14, 2014 earnings release. In connection with the divestiture, Amaya made a strategic investment in NYX Gaming Group via a subscription of an unsecured convertible debenture, which matures two years after the date of issuance and bears interest at 6.00% per annum, payable at maturity.

Source: Cantor Fitzgerald Canada, Company Documents

PRODUCTS AND SERVICES

PokerStars/Full Tilt Poker

For 2015, we estimate that PokerStars could generate ~$1.4B in revs and ~$600M in EBITDA. On average, the company deals 700 poker hands every second of every day with as many as 20,000 hands being played concurrently. It also runs 3,500 daily scheduled tournaments, which award more than $25 million of guaranteed prizes into the online accounts of hundreds of thousands of players each week. The company has had 481,488 players seated at the site at the same time.

Amaya Inc. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 13 of 36

Casino

Amaya launched its Casino offering on Full Tilt Poker with table games, slots and Live Dealer. More than 30% of active poker players were playing casino games (where permitted) showing the cross-selling leverage of the strategy. In addition, 50% of Full Tilt casino players do not leave to play on other casino sites. On the PokerStars platform, table games were launched in Spain in Q3/14 achieving double-digit market share. Other casino games will be launched in Spain in 2015. According to management, the casino launches have been successful in reactivating dormant users and increasing net player deposits, with a negligible impact on poker spend. Management expects Casino customer yields to be 1.5-2.5x poker yields.

Sportsbook

Sportsbook represents 40% of the online gambling market. Amaya announced that it anticipates PokerStars' planned launch of sports betting will launch in Q1/15 - ahead of schedule. The sports betting product will launch within the PokerStars poker client in certain markets, and PokerStars will gradually add more markets as well as web and mobile versions throughout the year. What if another acquisition is in the works to accelerate its move into sports betting? From Exhibit 3 below, we see that 888, Unibet, Betsson and Betfair would all fit nicely within the Amaya fold.

Mobile

In Q3/14, mobile represented >50% of new worldwide registrations vs ~40% yoy. In the U.K., mobile represented ~66% of new registrations. The fast-paced Spin & Go application has added boost to mobile growth. We note that Casino and Sportsbook verticals respond well to a mobile offering.

COMPETITORS

In the poker market, it’s liquidity that matters most and PokerStars has the highest liquidity and tournament payouts in the world. Greater liquidity attracts more players, which translates to bigger tournaments, larger payouts and lower probability of player collusion.

Exhibit 3. Competitive Landscape – Who Has the Greatest Liquidity is Key for Poker

Source: Cantor Fitzgerald Canada, Company documents, www.PokerScout.com (as of Feb 5/2015)

Site Cash Game 7-day Average Liquidity

PokerStars.com 21,000

888poker 2,700

iPoker 2,100

Bodog 1,800

PokerStars.it 1,600

Full Tilt 1,600

PartyPoker 1,500

PokerStars.es 1,200

Winamax.fr 1,150

PokerStars.fr 950

Poker Casino Bingo Sportsbook

Amaya 100% --- --- ---

BWIN 18% 35% 9% 38%

888 29% 58% 13% ---

Unibet 5% 53% --- 42%

Betsson 5% 67% --- 38%

Betfair --- 20% --- 80%

Playtech 4% 52% 5% 8%

Amaya Inc. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 14 of 36

FINANCIAL FORECAST

Amaya is expected to report Q4/14 results by the end of March 2015. The company has provided FY2014 guidance for revenue of $669M - $715M, and adj EBITDA of $265M - $285M, with results expected at the high end of the range.

Exhibit 4. Summary of Estimates

Source: Cantor Fitzgerald Canada, Company Documents

Exhibit 5. CFCC Estimates vs Consensus

Source: Cantor Fitzgerald Canada, Company Documents

Longer term we are looking for rev growth of 10%-15% and EBITDA to approach 45% margins.

Exhibit 6. Revenue and EBITDA margins

Source: Cantor Fitzgerald Canada, Company Documents

Forecasts Q214 Q314 Q414E Q414 %Diff. 2014E 2015E

Revenue ($M) $42.45 $238.96 $390.09 - - $712.70 $1,644.04

Adj. EBITDA $14.34 $108.39 $143.94 - - $281.54 $682.28

Adj. EPS (FD) $0.13 $0.43 $0.45 - - $1.04 $1.99

Adj. EPS (basic) $0.13 $0.59 $0.65 - - $1.40 $2.85

CFPS ($0.02) $0.85 ($1.07) - - ($0.41) $4.15

2014E 2015E 2016E

CFCC Consensus CFCC Consensus CFCC Consensus

Revenue $ 712.7 $ 716.3 $ 1,644.0 $ 1,631.0 $ 1,890.6 $ 1,831.6

Revenue (YoY %) 361.2% 363.5% 130.7% 127.7% 15.0% 12.3%

EBITDA $ 281.5 $ 286.0 $ 682.3 $ 699.4 $ 841.3 $ 840.4

EBITDA (%) 39.5% 39.9% 41.5% 42.9% 44.5% 45.9%

EPS, diluted $ 0.85 $ 0.52 $ 1.35 $ 1.43 $ 2.77 $ 2.18

Adj. EPS, diluted $ 1.04 $ 0.95 $ 1.99 $ 1.89 $ 2.85 $ 2.65

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

0.0

100.0

200.0

300.0

400.0

500.0

600.0

Q113 Q213 Q313 Q413 Q114 Q214 Q314 Q414E Q115E Q215E Q315E Q415E Q116E Q216E Q316E Q416E

Rev

enue

($M

)

Revenue Adj EBITDA %

Amaya Inc. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 15 of 36

CFOPS should grow to ~$700M per year, providing enough support to pay down debt, execute on the share buyback, and pursue further M&A.

Exhibit 7. CFOPS supports Debt repayment and M&A

Source: Cantor Fitzgerald Canada, Company Documents

-50

0

50

100

150

200

250

300

350

400

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Q113 Q213 Q313 Q413 Q114 Q214 Q314 Q414E Q115E Q215E Q315E Q415E Q116E Q216E Q316E Q416E

Css

h fr

om O

pera

tions

($M

)

Tot

al D

ebt (

$M)

Total Debt Total Cash Provided By Operating Activities

Amaya Inc. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 16 of 36

RECOMMENDATION AND VALUATION

We are initiating coverage of Amaya with a BUY recommendation and a DCF-based one-year price target of $50.00 per share. On our estimates, Amaya currently trades at a C2016 EV/Sales of 3.7x and EV/EBITDA of 8.3x vs its Global Gaming comparables at an average of 2.3x and 8.2x, respectively.

Exhibit 8. Discounted Cash Flow Analysis

Source: Cantor Fitzgerald Canada, Company Documents

Exhibit 9. Sensitivity Analysis

Source: Cantor Fitzgerald Canada, Company Documents

AMAYA GAMING (AYA-V) CAGR

Discounted Cash Flow Analysis 2011 2012 2013 2014E 2015E 2016E 2017E 12 - 16

Revenue 18,375,249 76,435,009 154,529,443 712,698,137 1,644,042,160 1,890,648,484 2,174,245,756 123.0%

Revenue Growth 203.8% 316.0% 102.2% 361.2% 130.7% 15.0% 15.0%

EBITDA (adj.) (1,726,140) 18,870,426 57,857,871 169,785,272 682,277,496 841,338,575 1,076,251,649 158.4%

EBITDA Growth (258.3% ) (1193.2%) 206.6% 193.5% 301.8% 23.3% 27.9%

Adj. EBITDA Margin -9.4% 24.7% 37.4% 23.8% 41.5% 44.5% 49.5%

Depreciation and Amortization 2,160,005 9,958,778 33,819,451 64,221,822 52,042,628 66,620,254 82,734,227

EBIT ($) -3,886,145 8,911,648 24,038,420 105,563,450 630,234,869 774,718,322 993,517,422

NOPAT 1,907,333 (12,671,603) (926,718,702) 135,481,499 553,105,579 682,319,770 879,659,729

Unlevered Free Cash Flow ($) (1,216,547) (31,503,775) (916,617,126) (73,082,360) 854,525,568 669,576,219 953,175,715

PV of Unlevered FCFs ($) (1,590,414) (37,775,880) (1,008,355,011) (73,758,413) 791,220,552 568,647,956 742,659,827

Valuation Assumptions:

Discount Rate 9.0%

Terminal Multiple 11.00

Valuation Analysis: 1-Yr Target

Total PV of FCFs ($) 1,904,723,197

Terminal Value ($) 11,838,768,142

PV of Terminal Value ($) 10,054,256,870

Net (debt) cash position (2,305,852,026)

Total Value ($) 9,653,128,042

DCF Value/Share $50.84

FD Shares O/S 189,881,171

Terminal EV/EBITDA Multiple

$50.85 7.00 8.00 9.00 10.00 11.00 12.00 13.00

5.0% 34.84 40.01 45.17 50.34 55.51 60.68 65.85

7.0% 33.17 38.16 43.14 48.13 53.12 58.10 63.09

Discount Rate 9.0% 31.59 36.41 41.22 46.04 50.85 55.67 60.48

11.0% 30.10 34.75 39.40 44.06 48.71 53.36 58.01

13.0% 28.69 33.18 37.68 42.18 46.68 51.17 55.67

15.0% 27.35 31.70 36.05 40.40 44.75 49.10 53.45

Amaya Inc. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 17 of 36

APPENDIX 1: MANAGEMENT AND BOARD OF DIRECTORS

Exhibit 10. Board of Directors

Name Office Principal occupation

David Baazov Director See management bio below.

Daniel Sebag Director See management bio below.

General Wesley Clark Sr. Director Retired a four-star General after 38 years in the US Army. Former Supreme Allied Commander Europe of NATO. He graduated first in his class at West Point and completed degrees in Philosophy, Politics and Economics at Oxford University (B.A. and M.A.) as a Rhodes Scholar.

David (Divyesh) Gadhia, C.A.

Director Former CEO and Executive Vice-Chairman of Gateway Casinos & Entertainment Limited, responsible for strategic initiatives, regulatory matters, and government relations of Gateway Casinos. Mr. Gadhia was with Gateway Casinos since its inception in 1992 until 2010. Mr. Gadhia was a director of the Canadian Gaming Association.

Harlan Goodson Director Former Director of California’s Division of Gambling Control where he was instrumental in the implementation of California’s Tribal-State Class III gaming compacts. Prior to forming his own law practice, he was with the national law firm of Holland and Knight, LLP, where he focused on Gaming Law and Gaming Regulation and Governmental Affairs.

Dr. Aubrey Zidenberg Director President and Chief Executive Officer of Casino Amusements Canada, which offers commercial gaming industry experience to both the private sector and government. Gaming industry specialist with extensive experience in the development, implementation and operation of international gaming, tourism and entertainment projects since 1974. Pioneer in the development of Responsible Gambling policies, practices and procedures.

Tom Auriemma Chair, Compliance Committee

Former chair of the NJ Division of Gaming Enforcement. Recently retired Chief Compliance Officer of Penn National Gaming.

Amaya’s Compliance Committee consists of Ben Soave, Harlan Goodson, Marlon Goldstein and Daniel Sebag.

Source: Cantor Fitzgerald Canada, Company Documents

Exhibit 11. Management Team

Name Office Previous positions

David Baazov President & CEO

Mr. David Baazov is a director and has been President and CEO of Amaya since 2006. He is responsible for devising and implementing the Company’s general business strategies.

He served as Vice President of Sales at Vortek Systems Inc. from 2000 to 2006. Mr. Baazov acquired extensive experience in sales and marketing in the consumer electronics industry, particularly computer hardware. He saw tremendous potential in online gaming, particularly poker and more so in the P2P gaming market, envisioning it as a new niche and the future of the gaming industry.

Daniel Sebag CFO Mr. Daniel Sebag is a Chartered Accountant and specialist in the areas of cost management and financial reporting systems. Mr. Sebag joined Amaya in July 2007 as Chief Financial Officer. He has a 10-year background as a faculty lecturer at McGill University. In addition, he has acted as a consultant to several multinational companies including Bombardier, Ericsson, Transat AT and Air Liquide.

Marlon Goldstein EVP, Corporate Development & General Counsel

Mr. Goldstein represented Amaya in the company's two acquisitions of Diamond Game Enterprise and Cadillac Jack (helping secure a $110m senior secured credit facility to finance that deal). Mr. Goldstein was previously a principal shareholder in the corporate and securities practice of law firm Greenberg Traurig, where he worked on M&A, financing transactions and securities offering. Goldstein also served as co-chair of Greenberg Traurig’s gaming practice, working with financial institutions funding gambling businesses, land-based operators, technology suppliers and Indian Tribes involved in the sector, as well as iGaming companies. In the past, he represented hospitality and gaming operator Hard Rock International, worked on the sale of Maine’s Oxford Casino to Churchill Downs, as well as handling cases for the Seminole Tribe of Florida. He has a Bachelor’s Degree from Emory University, and a JD from the University of Florida.

Source: Cantor Fitzgerald Canada, Company Documents

Amaya Inc. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 18 of 36

APPENDIX 2: FINANCIAL STATEMENTS

Exhibit 12. Income Statement

Source: Cantor Fitzgerald Canada, Company Documents

Income Statement (in C$000) (YE Dec 31) 2013 2014E 2015E 2016E 2017E

Total Revenue 154,529 712,698 1,644,042 1,890,648 2,174,246

Total Cost of Goods Sold 5,980 14,249 24,661 28,360 32,614

Total Gross Profit 148,549 698,449 1,619,382 1,862,289 2,141,632

Selling Expenses 14,590 80,304 115,083 113,439 130,455

G&A 132,585 437,256 854,902 945,324 978,411

Financial 19,569 25,794 0 0 0

Acquisition related costs 1,332 21,934 0 0 0

Amortization of Property & Equipment 12,734 8,876 52,043 66,620 82,734

Amortization of Intangibles 19,361 0 0 0 0

Amortization of deferred development costs 1,725 0 0 0 0

Total Operating Expenses 168,076 574,163 1,022,028 1,125,383 1,191,600

Operating Income (19,527) 124,286 597,354 736,905 950,033

Interest Expense 0 (33,940) (186,378) (148,615) (111,221)

Total Other Income 9,673 11,280 (186,378) (148,615) (111,221)

EBT (9,854) 135,566 410,976 588,291 838,812

Income Taxes (9,646) 11,203 (32,878) (47,063) (67,105)

Total Comprehensive Income (Loss) to Company (19,500) 102,739 378,098 541,227 771,707

Minority Interest 0 0 0 0 0

Net Income to Common Shareholder (19,500) 102,739 378,098 541,227 771,707

EPS - Excluding Non-Recurring Items

Basic EPS - GAAP 0.08 1.40 2.85 4.08 5.82

Basic EPS - ex-non-recurring items 0.08 1.04 1.99 2.85 4.06

Shares Outstanding

Basic 89,491 121,559 132,559 132,559 132,559

Diluted 89,838 164,021 189,881 189,881 189,881

Operating Metrics

Gross Profit 148,549 698,449 1,619,382 1,862,289 2,141,632

Adj EBITDA 57,858 281,536 682,277 841,339 1,076,252

EBITDA 37,394 169,785 682,277 841,339 1,076,252

EBIT (19,527) 124,286 597,354 736,905 950,033

EBT (9,854) 135,566 410,976 588,291 838,812

Net Income (ex-non-recurring items) (19,500) 146,768 378,098 541,227 771,707

Amaya Inc. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 19 of 36

Exhibit 13. Balance Sheet

Source: Cantor Fitzgerald Canada, Company Documents

Balance Sheet (in C$000) (YE Dec 31) 2013 2014E 2015E 2016E 2017E

Current Assets

Cash 93,640 210,169 308,234 249,642 420,428

Trade & Other Receivables 47,460 387,777 199,929 229,918 264,406

Oldford acq. Receivables & Other current assets 0 0 0 0

Investment tax credit - current 112 176 176 176 176

Capital Assets 38,369 0 0 0 0

Investment in marketable securities 0 368,910 368,910 368,910 368,910

Current maturity of rec. under finance lease 4,865 4,095 4,095 4,095 4,095

Inventories 7,595 61,517 55,365 63,670 73,220

Income taxes recoverable 520 8,687 8,687 8,687 8,687

Prepaid Expenses 4,173 13,873 12,486 14,359 16,513

Total Current Assets 196,735 1,055,204 957,882 939,457 1,156,435

Non-Current Assets

Restricted Cash 131 42,945 42,945 42,945 42,945

Investments 10,582 38,646 38,646 38,646 38,646

Vendor Takeback 0 29,805 29,805 29,805 29,805

Property & Equipment 40,521 104,460 127,891 157,391 199,961

Deferred Tax Assets 13,330 60,969 60,969 60,969 60,969

Deferred development costs 3,818 8,722 8,722 8,722 8,722

Receivable under finance lease 10,004 6,960 6,960 6,960 6,960

Investment tax credit receivable long-term 2,673 12,881 12,881 12,881 12,881

Goodwill 79,975 5,555,588 5,555,588 5,555,588 5,555,588

Intangible Assets 83,062 0 0 0 0

Total Assets 440,831 6,916,180 6,842,289 6,853,363 7,112,913

Current Liabilities

Trade & Other Payables 27,477 247,775 376,789 433,308 498,304

Oldford acq. Accounts payable and accrued liabilities 0

FX contracts 0 0 0 0 0

Provisions 3,685 41,967 41,967 41,967 41,967

Income taxes payable 1,763 19,059 19,059 19,059 19,059

Short-Term Debt 0 0 0 0 0

Held for Sale 4,638 0 0 0 0

Customer Deposits 4,453 676,111 676,111 676,111 676,111

Unearned Revenue 0 2,248 2,697 3,102 3,567

Promissory Notes 0 0 0 0 0

Current Portion of Long-Term Debt 2,388 86,295 114,397 121,997 131,914

Current Portion of Ob. Under Capital Lease 1,133 1,395 1,395 1,395 1,395

Total Current Liabilities 45,537 1,074,850 1,232,416 1,296,939 1,372,318

Non-Current Liabilities

Deferred Revenue 249 1,985 1,985 1,985 1,985

Other payable 0 14,466 14,466 14,466 14,466

Holdback 0 7,840 7,840 7,840 7,840

Employee future benefits 0 0 0 0 0

Provisions 1,547 392,081 392,081 392,081 392,081

Income taxes payable 0 0 0 0 0

Deferred Income Tax Liabilities 5,802 33,432 33,432 33,432 33,432

Convertible debentures 0 0 0 0 0

Long-Term Debt 192,799 3,239,801 2,597,365 1,964,876 1,333,855

Deferred Purchase Price 0 0 0 0

Obligations Under Capital Lease 551 0 0 0 0

Total Liabilities 246,484 4,764,456 4,279,585 3,711,619 3,155,977

Shareholders' Equity

Capital Stock 220,683 1,640,562 1,640,562 1,640,562 1,640,562

Contributed Surplus 4,214 383,211 416,092 453,905 497,389

Deficit (39,388) 0 0 0 0

Non-controlling interest 0 (133) (133) (133) (133)

Other comprehensive loss 8,838 62,345 62,345 62,345 62,345

Retained Earnings 0 65,740 443,838 985,065 1,756,772

Total Shareholders Equity 194,347 2,151,724 2,562,704 3,141,744 3,956,935

Total Liabilities & Shareholders Equity 440,831 6,916,180 6,842,289 6,853,363 7,112,913

Amaya Inc. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 20 of 36

Exhibit 14. Cash Flow Statement

Source: Cantor Fitzgerald Canada, Company Documents

Cash Flow Statement (in C$000) (YE Dec 31) 2013 2014E 2015E 2016E 2017E

Cash Provided By Operating Activities

Net Income (29,173) 104,994 378,098 541,227 771,707

Depreciation 33,819 64,222 52,043 66,620 82,734

Deferred Income Tax (553) (26,611) 0 0 0

Interest Accretion on Special Warrants 1,493 3,657 0 0 0

R&D tax credits 256 0 0 0 0

Interest Paid 0 2,954 0 0 0

Stock-Based Compensation 2,030 10,829 32,881 37,813 43,485

Investment in lease (9,303) 2,286 0 0 0

Unrealized Loss (Gain) on FX (2,542) (6,915) 0 0 0

Change in Non-Cash Working Capital

Trade & Other Receivables 6,129 (220,556) 187,848 (29,989) (34,488)

Work in Process 0 0 0 0 0

Income Taxes Receivable 4,270 3,222 0 0 0

Inventories 1,812 (50,188) 6,152 (8,305) (9,550)

Trade & Other Payables (6,967) 20,290 129,014 56,518 64,996

Unrealised Exchange (Gain) Loss 0 0 0 0 0

Unearned Revenue 77 1,523 450 405 465

Total Cash Provided By Operating Activities (60) (66,521) 787,873 662,417 917,195

Investing Activities

Purchase of Property & Equipment (17,430) (28,442) (75,474) (96,120) (125,305)

Proceeds from Sale of Property & Equipment 352 (2,147) 0 0 0

Purchase of Intangibles (18,736) (6,554) 0 0 0

Invest. in marketable sec./business acqs. 0 7,850 0 0 0

Asset acquisition 14,418 (4,577,054) 0 0 0

Deferred Development costs (11,025) (9,294) 0 0 0

Total Cash From Investing Activities (57,422) (4,615,641) (75,474) (96,120) (125,305)

Financing Activities

Proceeds from Common Shares/Units/Bonds 43,711 1,846,169 0 0 0

Repayment of Bal. of Payable to Former Shlders 0 0 0 0 0

Trans. costs related to capital stock issuance (4,846) (99,502) 0 0 0

Issuance of capital stock 43,711 7,132 0 0 0

Net Variation in Bank Advances 0 0 0 0 0

Proceeds from Promissory Notes 0 0 0 0 0

Repayment of Obligations Under Promisory Notes 0 0 0 0 0

Addition of Long-Term Debt 193,337 3,150,238 0 0 0

Repayment of Long-Term Debt (114,114) (70,110) (614,334) (624,889) (621,104)

Total Cash From Financing Activities 114,844 4,826,795 (614,334) (624,889) (621,104)

Effect of exchange rates on cash 4,950 14,712 0 0 0

Net Increase in cash 62,313 159,345 98,065 (58,592) 170,786

Beginning Cash 31,328 93,640 253,114 351,179 292,587

Ending Cash 93,640 253,114 351,179 292,587 463,373

Amaya Inc. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 21 of 36

This page is intentionally left blank.

February 12, 2015 Research Update

Ralph Garcea, MBA, P.Eng. [email protected] 416-849-5004

Sales/Trading — Toronto: (416) 363-5757, (866) 442-4485

See disclosure and a description of our recommendation structure at the end of this report. 22 of 36

Eq

uit

y R

ese

arc

h

Company profile: NYX Gaming Group provides flexible

gaming solutions to some of the largest lotteries, casinos, poker rooms and I-gaming operators across the globe.

NYX GAMING GROUP LTD. The New Kid on the Block

EVENT

We are initiating coverage of NYX Gaming with a BUY recommendation, and a DCF-based one-year target price of $7.00 per share.

BOTTOM LINE

Content is King. NYX Gaming is a digital gaming software supplier engaged in the design, development, manufacture, and distribution of digital gaming solutions for interactive, social, land-based and mobile gaming worldwide. With an exclusive focus on content and technology development, thus reducing potential conflicts with its customers, NYX’s platform has 350+ proprietary, and 550+ third-party supplied, lottery, bingo, and casino products developed to address the multi-channel content and distribution strategies of its customers. In addition, NYX is creating 25-50 new games annually.

FOCUS POINTS

▪ Recurring Revenue Model. With over 90% of revs recurring in nature, NYX provides good visibility into its long term forecasts.

▪ Blue chip customer base, with low concentration. NYX has 100+ customers such as Amaya, 888, bwin.party and many more global players. Top 10 represent only ~55% of revs, with only 2 customers above 10%.

▪ Experienced M&A Team. NYX has completed three acquisitions to date: NYX Interactive AB, Zen Entertainment, and Ongame Networks. We expect NYX to continue on the M&A trail.

Recommendation: BUY

Symbol/Exchange: NYX/TSX-V

Sector: Technology - Online Gambling

All dollar values in C$ unless otherwise noted.

Current price: C$4.75

One-year target: C$7.00

Dividend / Yield ---/---

Target return: 47.4%

Financial summary

Source: Company documents, Cantor Fitzgerald Canada

Shares O/S (M) 33.8 52-Week Range $3.25 - $5

Market Cap ($M) 160.5 Avg. Weekly Volume (M) 2.82

Net Cash ($M) (33.4) Fiscal Year End 31-Dec

C$M 2013 2014E 2015E 2016E

Revenue 18.7 26.6 36.7 47.4

Revenue (YoY % ) 39.5% 42.0% 38.1% 29.1%

Adj. EBITDA 2.7 7.6 8.5 13.3

Adj. EBITDA margin 14.6% 28.6% 23.2% 28.0%

GAAP EPS (Diluted) (0.07) 0.05 0.12 0.25

Adjusted EPS (Diluted) (0.07) 0.05 0.12 0.25

Shares O/S 25.7 29.5 33.8 33.8

EV / Revenue 6.8x 4.8x 3.5x 2.7x

EV / EBITDA NMF 16.7x 15.0x 9.6x

P/E (adj. EPS) NMF 87.1x 40.9x 19.0x

0

1

2

3

4

5

$0

$1

$2

$3

$4

$5

$6

Dec/14 Jan/15 Jan/15 Jan/15 Jan/15 Feb/15

Vol

ume

(M)

Pric

e ($

)

NYX Gaming Group Ltd. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 23 of 36

INTRODUCTION

NYX Gaming is a digital gaming software supplier engaged in the design, development, manufacture, and distribution of digital gaming solutions for interactive, social and mobile gaming worldwide. With 270+ employees (including over 24 contract employees) and 100+ B2B customers, NYX has a registered office in Guernsey and principal offices in the U.S., Sweden, and Australia. With an exclusive focus on content and technology development, thus reducing potential conflicts with its customers, NYX’s platform has more than 350 proprietary, and over 550 third-party supplied, lottery, bingo, and casino products developed to address the multi-channel content and distribution strategies of its customers.

We are initiating coverage of NYX Gaming with a BUY recommendation and a DCF-based one-year price target of $7.00 per share. On our estimates, NYX currently trades at a C2016 EV/Sales of 2.7x and EV/EBITDA of 9.6x vs its Global Gaming comparables at an average of 2.3x and 8.2x, respectively.

INVESTMENT THESIS

Full Suite of Products Built on an Open Technology Platform

NYX has developed a proprietary content library of 350+ gaming titles within a portfolio of slots, bingo, lottery, poker and other casino games. Through NYX Open Gaming System (“OGS”), NYX provides access to 550+ games through its integrated third-party content suppliers. NYX’s open technology platform and partnerships with leading content providers and 30+ payment processors, provides flexibility in game content delivery, payment processing, geolocation technology, fraud prevention, affiliate management, and business analytical tools, allowing its customers to respond to market changes and select products and services that directly address their evolving needs.

Recurring Revenue Business Model

With over 90% of revs recurring in nature, NYX provides good visibility into its long term forecasts.

Blue-Chip Customer Base

NYX has 100+ customers, including Amaya, Intertain, 888, bwin.party, Mr. Green, William Hill and many more on and off-line gaming operators, state-regulated lotteries, media and entertainment firms, and land-based casinos. Most customers sign long-term deals, and the average relationship with its top ten customers is five years. NYX has a low customer concentration as its top ten customers represent only 55% of revenues and no single customer represented more than 12% of revenues for the nine months ended September 30, 2014.

Experienced Management Team

The Company has completed two acquisitions since its inception – NYX Interactive AB and Zen Entertainment. In addition, NYX recently acquired Ongame Networks from Amaya. We expect NYX to continue doing acquisitions to supplement its growth strategy. Note that management owns ~35% of the company.

NYX Gaming Group Ltd. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 24 of 36

CATALYSTS

Acquisition of Amaya’s B2B assets

NYX has the right of first offer for the remainder of the Chartwell/Cryptologic assets within Amaya. We expect the company to exercise this right in the H1/15.

Leveraging the Ongame Networks Acquisition

Amaya had essentially put the Ongame assets on hold by the end of Q4/13, and we believe as part of NYX the Ongame business will be revitalized.

RISKS

Social Gaming Integration

The integration of Zen Entertainment is proceeding as planned. However, any delays in leveraging the growth in social gaming could impact Zen’s profitability.

Ongame Networks’ Integration

Integrating Ongame’s European operations could take longer than expected, impacting margins.

Increased Taxation

Increasing taxes in various jurisdictions could impact the growth of online gambling.

COMPANY OVERVIEW

Company Description

NYX Gaming Group is headquartered in Las Vegas with development out of Stockholm and Sydney. The group provides flexible gaming solutions to some of the largest lotteries, casinos, poker rooms and i-gaming operators across the globe. NYX Poker Network (previously Ongame Networks acquired from Amaya), is a leading internet poker network delivering poker solutions for online poker operators world-wide. The Las Vegas office provides social Poker & Casino solutions out of the group headquarters. NYX has over 270 employees across 10 regions.

NYX Gaming Group Ltd. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 25 of 36

Exhibit 1. A Global Footprint Supports Further Acquisitions

Source: Cantor Fitzgerald Canada, Company Documents

Exhibit 2. How Did We Get Here?

Source: Cantor Fitzgerald Canada, Company Documents

Date Event

1999

NextGen Gaming was founded in Sydney, Australia

2006

NYX Interactive launched in Stockholm, Sweden

Launched the NYX Open Platform System (OPS)

2008

Nordic Ventures (now known as Verdane Capital) made initial equity investment, with subsequent investments totalling €10M.

2009

Launched Game Development Module (GDM)

2010 NextGen Gaming was reorganized as RNG Holdings Guernsey

2011 NYX Gaming Group formed through the merger of RNG Holdings Guernsey and NYX Interactive.

2012

Expanded into the U.S. through the formation of NextGen Gaming (USA) in Nevada

Launched NYX Open Gaming System (OGS)

Launched NYX Move, a mobile gaming and social application providing a portfolio of games for social networks

2013

Entered B2C Social Gaming industry through the acquisition of Zen Entertainment.

Expanded presence in the U.S. online gaming market through a joint venture with Sportech Plc and formed SNG Interactive.

2014

Signed first partner in U.S. market – Resorts Casino

Completed successful IPO on the TSX-V; started trading on Dec 30/14

Acquired Ongame Network for a consideration equal to 8.0x 2015 EBITDA; rebranded as NYX Poker

Raised an additional $10M through a convertible debenture issued to Amaya

NYX Gaming Group Ltd. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 26 of 36

Recent corporate events

NYX completed its initial public offering, and started trading on the Toronto Venture Exchange, on December 30, 2014 at an initial price of $3.50. As part of the IPO process, NYX acquired Ongame Network from Amaya. Post the IPO, we have seen several announcements from the Company.

Exhibit 3. Recent Announcements from NYX

Date Announcement

Feb 6/15 NextGen Gaming announced a partnership with Lightning Box Games (LBG) to create and distribute online LBG’s traditionally land based slot games.

Feb 5/15 NYX entered new regulated markets with the launch of NYX OGS and the signing of its NYX Poker product with Iveriabet.

Feb 3/15 NYX announced the signing of White Hat Gaming for its NYX Poker product, formerly Ongame Network.

Jan 30/15 NYX announced the appointment of Mr. Hamish Brown as Group Chief Operating Officer (COO). Mr. Brown has 18 years of experience in the gaming industry in various operational and commercial roles at IGT (Australia), Aristocrat and Tabcorp, before transitioning to iGaming in 2008 as NextGen Gaming's COO and General Manager in Sydney, Australia.

Jan 22/15 NextGen Gaming announced the debut of its slot games on paddypower.com, with the dual mobile and desktop launch of smash hit Merlin's Millions Superbet™.

Jan 12/15 NextGen Gaming to release Psycho under agreement with Universal Partnerships & Licensing. The online slot is due to be released in Q1/15.

Source: Cantor Fitzgerald Canada, Company Documents

PRODUCTS AND SERVICES

NYX has developed a modular open architecture that is flexible to adapt to both regulatory and operational requirements.

Exhibit 4. Open Architecture Platform and Technology

Source: Cantor Fitzgerald Canada, Company Documents

NYX Gaming is a digital gaming software supplier engaged in the design, development, manufacture, and distribution of digital gaming solutions for

NYX Gaming Group Ltd. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 27 of 36

interactive, social, land-based and mobile gaming worldwide. NYX also offers a fully-hosted Social casino, GDM integration and free-to-play poker platform.

Exhibit 5. Content is King

Multi-platform products

Source: Cantor Fitzgerald Canada, Company Documents

COMPETITORS

NYX’s competitors range from small private software studios to large publicly listed companies and vary significantly depending on the jurisdiction and customer base. NYX’s open platform allows it to aggregate its own proprietary content (350+ games) as well as 550+ games from best-of-breed third party content including Amaya, GTECH, Scientific Games, Aristrocrat and Net Entertainment.

BUSINESS MODEL

NYX generates revenue from many streams, with the many segments being Content Development (51% of revs), Platform/Technology (39%) and Social Gaming (10%).

Exhibit 6. NYX Business Model

Source: Cantor Fitzgerald Canada, Company Documents

NYX Gaming Group Ltd. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 28 of 36

On a more granular level, the splits are roughly as follows:

Exhibit 7. Revenue by Segment

Segment % of Revs Recurring

Royalties/Licensing Fees ~80% Yes

Advertising/Virtual Currency ~10% Yes

Maintenance/Support Fees <5% Yes

Upfront Development Fees ~5% No

Professional Services Fees <5% No

Source: Cantor Fitzgerald Canada, Company Documents

NYX Gaming Group Ltd. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 29 of 36

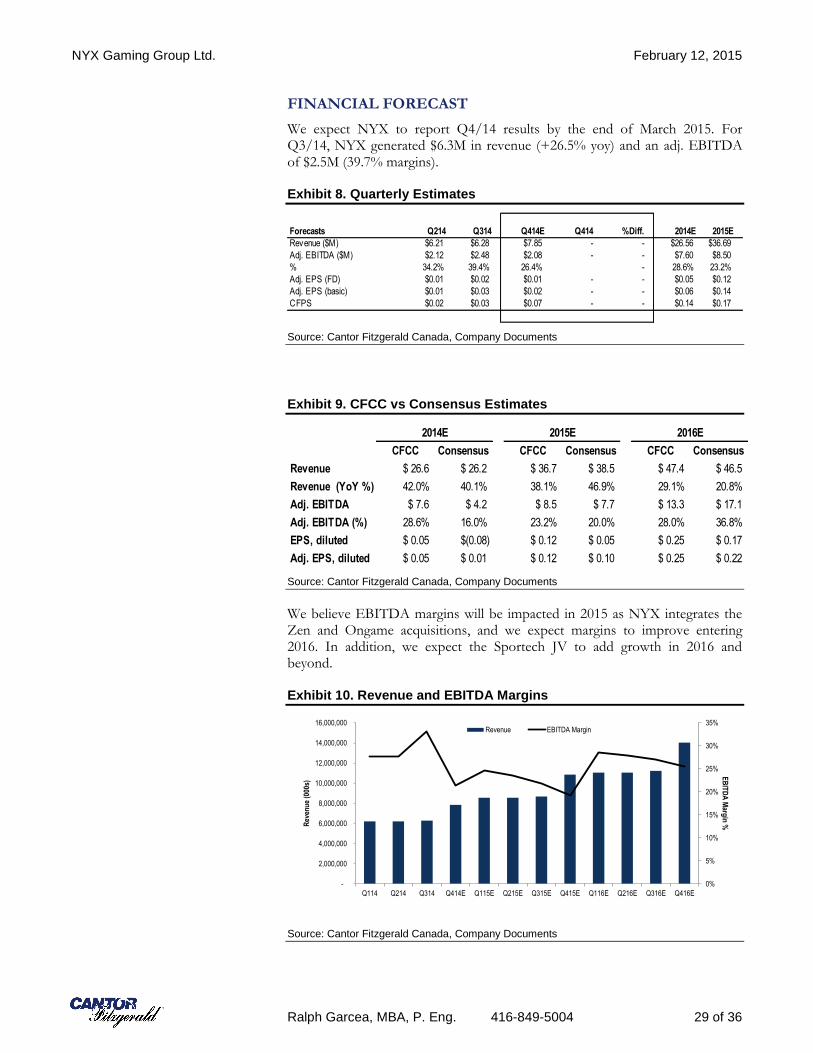

FINANCIAL FORECAST

We expect NYX to report Q4/14 results by the end of March 2015. For Q3/14, NYX generated $6.3M in revenue (+26.5% yoy) and an adj. EBITDA of $2.5M (39.7% margins).

Exhibit 8. Quarterly Estimates

Source: Cantor Fitzgerald Canada, Company Documents

Exhibit 9. CFCC vs Consensus Estimates

Source: Cantor Fitzgerald Canada, Company Documents

We believe EBITDA margins will be impacted in 2015 as NYX integrates the Zen and Ongame acquisitions, and we expect margins to improve entering 2016. In addition, we expect the Sportech JV to add growth in 2016 and beyond.

Exhibit 10. Revenue and EBITDA Margins

Source: Cantor Fitzgerald Canada, Company Documents

Forecasts Q214 Q314 Q414E Q414 %Diff. 2014E 2015E

Revenue ($M) $6.21 $6.28 $7.85 - - $26.56 $36.69

Adj. EBITDA ($M) $2.12 $2.48 $2.08 - - $7.60 $8.50

% 34.2% 39.4% 26.4% - 28.6% 23.2%

Adj. EPS (FD) $0.01 $0.02 $0.01 - - $0.05 $0.12

Adj. EPS (basic) $0.01 $0.03 $0.02 - - $0.06 $0.14

CFPS $0.02 $0.03 $0.07 - - $0.14 $0.17

2014E 2015E 2016E

CFCC Consensus CFCC Consensus CFCC Consensus

Revenue $ 26.6 $ 26.2 $ 36.7 $ 38.5 $ 47.4 $ 46.5

Revenue (YoY %) 42.0% 40.1% 38.1% 46.9% 29.1% 20.8%

Adj. EBITDA $ 7.6 $ 4.2 $ 8.5 $ 7.7 $ 13.3 $ 17.1

Adj. EBITDA (%) 28.6% 16.0% 23.2% 20.0% 28.0% 36.8%

EPS, diluted $ 0.05 $(0.08) $ 0.12 $ 0.05 $ 0.25 $ 0.17

Adj. EPS, diluted $ 0.05 $ 0.01 $ 0.12 $ 0.10 $ 0.25 $ 0.22

0%

5%

10%

15%

20%

25%

30%

35%

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

Q114 Q214 Q314 Q414E Q115E Q215E Q315E Q415E Q116E Q216E Q316E Q416E

EB

ITD

A M

argin

% R

even

ue

(000

s)

Revenue EBITDA Margin

NYX Gaming Group Ltd. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 30 of 36

RECOMMENDATION AND VALUATION

We are initiating coverage of NYX Gaming with a BUY recommendation and a DCF-based one-year price target of $7.00 per share. On our estimates, NYX currently trades at a C2016 EV/Sales of 2.7x and EV/EBITDA of 9.6x vs its Global Gaming comparables at an average of 2.3x and 8.2x, respectively.

Exhibit 11. Discounted Cash Flow Analysis

Source: Cantor Fitzgerald Canada, Company Documents

Exhibit 12. Sensitivity Analysis

Source: Cantor Fitzgerald Canada, Company Documents

NYX GAMING GROUP LIMITED CAGR

Discounted Cash Flow Analysis F2011 F2012 F2013 F2014E F2015E F2016E F2017E F12 - F17

Revenue 7,407,727 12,238,301 18,704,946 26,563,326 36,687,202 47,367,418 56,840,902 36.0%

Revenue Growth #DIV/0! 65.2% 52.8% 42.0% 38.1% 29.1% 20.0%

EBITDA -1,755,116 -2,699,743 -2,237,393 7,199,120 8,098,458 12,857,935 19,348,862

EBITDA Growth #DIV/0! 53.8% (17.1% ) (421.8% ) 12.5% 58.8% 50.5%

EBITDA Margin -23.7% -22.1% -12.0% 27.1% 22.1% 27.1% 34.0%

Depreciation and Amortization 1,583,118 3,814,627 4,275,960 4,558,385 3,700,529 2,577,211 1,798,529

EBIT ($) -3,338,234 -6,514,370 -6,513,353 2,640,735 4,397,930 10,280,724 17,550,333

NOPAT -1,634,530 -2,298,209 -1,833,767 4,351,969 5,484,566 10,280,724 13,500,257

Plus Amortization ($) 1,583,118 3,814,627 4,275,960 4,558,385 3,700,529 2,577,211 1,798,529

Less Capital Expenditures ($) -1,353,114 -308,189 -149,370 -129,872 -39,610 -41,416 -40,596

Capital Intensity 18.3% 2.5% 0.8% 0.5% 0.1% 0.1% 0.1%

Net Working Capital Changes -1,029,438 688,111 -825,239 -1,236,376 -1,522,680 -3,264,907 -1,029,641

EPS (ex-non-recurring items) (0.07) (0.08) (0.07) 0.05 0.12 0.25 0.31

Unlevered Free Cash Flow ($) -2,433,964 1,896,340 1,467,584 7,544,107 7,622,805 9,551,613 14,228,548 49.6%

PV of Unlevered FCFs ($) -3,276,186 2,319,875 1,632,145 7,627,300 7,006,242 7,978,861 10,805,183 36.0%

Valuation Assumptions:

Discount Rate 10.0%

Terminal Multiple 11.00x

Valuation Analysis: 1-Yr Target

Total PV of FCFs ($) 22,287,165

Terminal Value ($) 212,837,482

PV of Terminal Value ($) 195,622,327

Net (debt) cash position 51,767,219

Total Value ($) 269,676,711

DCF Value/Share $6.78

FD Shares O/S 39,753,537

Terminal EV/EBITDA Multiplier

$6.78 8.00 9.00 10.00 11.00 12.00 13.00 14.00

6.0% 5.61 6.07 6.53 7.00 7.46 7.92 8.38

8.0% 5.52 5.98 6.43 6.89 7.34 7.80 8.25

Discount Rate 10.0% 5.44 5.89 6.34 6.78 7.23 7.68 8.13

12.0% 5.36 5.80 6.24 6.68 7.12 7.56 8.00

14.0% 5.29 5.72 6.15 6.59 7.02 7.46 7.89

16.0% 5.22 5.64 6.07 6.50 6.92 7.35 7.78

NYX Gaming Group Ltd. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 31 of 36

APPENDIX 1: MANAGEMENT AND BOARD OF DIRECTORS

Exhibit 13. Board of Directors

Name Office Principal occupation

James Lanthier Toronto,Ontario

Chairman CEO of RAM Equity Former COO, CFO and Vice Chairman of Mood Media

Matt Davey Las Vegas, NV

Director See management bio below.

Roger Buckeridge

Australia

Director Former owner of venture capital fund manager

Involved in 50+ start-up technology-based companies

Eric Matejevich

United States

Director Former COO of Atlantic Club Casino (formerly Atlantic City Hilton)

Former CFO for entities of Resorts International Holdings

Staffan Lindgren

Stockholm, Sweden

Director Founder and former CEO of NYX Interactive with 20+ years

of experience in technology and finance sectors

Source: Cantor Fitzgerald Canada, Company Documents

Exhibit 14. Senior Management

Name Office Previous positions

Matt Davey CEO Mr. Davey joined NextGen in 2000 as the VP of Technology, was appointed to Executive Director in 2003, and was named CEO in 2005. Mr. Davey has over 20 years of experience in the gaming industry, having worked in both the private and public sectors as a gaming regulator as well as a consultant and gaming industry executive. Mr. Davey’s core competencies include regulatory compliance, sales and marketing, international relations, and corporate strategy and governance. Mr. Davey received a Bachelor of Engineering from Northern Territory University, Australia.

Staffan Lindgren Sales Director of Lotteries, NYX Interactive AB

Mr. Lindgren has been in the technology and finance sector for more than 20 years. Mr. Lindgren was one of the founders of NYX Interactive AB in 2006 and was the Chief Executive Officer of NYX Interactive AB from 2006 through 2010, until he joined the Board of Directors in 2011. Following the acquisition of NYX Interactive AB by the Company, Mr. Lindgren was appointed to his current position as Sales Director, Lotteries. Prior to his tenure with NYX Interactive AB, Mr. Lindgren co-founded TSG AB, a company focused on solutions for high intensive transaction environments.

Matthew J. Stafford

General Counsel

From 2009 until July 2014, Mr. Stafford was with Aruze Gaming America Inc., where he most recently served as Assistant General Counsel. During his tenure at Aruze, one of the fastest growing slot machine and video table game companies in the world, Mr. Stafford secured over 150 gaming licenses in North America and other major global gaming jurisdictions, and negotiated gaming contracts with some of the major land-based operators around the world. Mr. Stafford received a Bachelor of Arts in Political Science from the University of New Mexico and a Juris Doctor from the William S. Boyd School of Law, University of Nevada, Las Vegas, and was admitted to practice by the State Bar of Nevada and the United States District Court, District of Nevada.

Arthur Elliott Hamilton IV

CFO Prior to joining the company in July 2014, Mr. Hamilton served as Chief Accounting Officer and Executive Vice President for Spectrum Group International. Mr. Hamilton served as Senior Manager, Internal Audit, for Franklin Templeton Investments from 2009 to May 2010, and as Internal Audit Manager from 2003 to 2006. Mr. Hamilton also served as Director of Internal Audit for MGM Resorts International from 2006 to 2008, and as Director of Compliance and Treasury for Fontainebleau Resorts, LLC. during 2008 and 2009. Mr. Hamilton received a Bachelor of Science in Accounting and Business from the University of Baltimore and a Masters of Business Administration from Northwestern University Kellogg School of Management, and is a Certified Public Accountant in Maryland.

Vladislav Aizenstadt

CTO Prior to joining the Company in May 2013, Mr. Aizenstadt briefly served as Director of Poker Development at Caesars Interactive, overseeing online poker. In 2012, Mr. Aizenstadt served as Vice President of Software Development of Amaya Gaming Group Inc. From 2001 to 2012, Mr. Aizenstadt served multiple roles with CryptoLogic Inc., with his most recent position as Director of Platform and Games Development. Mr. Aizenstadt has over 25 years of technology experience, over 14 years of experience in the gaming industry, and over three years of experience in the retail gaming industry. Mr. Aizenstadt received a Bachelor of Science in Applied Mathematics from Kiev Technology University.

Hamish Brown COO Mr. Brown has 18 years of experience in the gaming industry in various operational and commercial roles at IGT (Australia), Aristocrat and Tabcorp, before transitioning to iGaming in 2008 as NextGen Gaming's COO and General Manager in Sydney, Australia.

Source: Cantor Fitzgerald Canada, Company Documents

NYX Gaming Group Ltd. February 12, 2015

Ralph Garcea, MBA, P. Eng. 416-849-5004 32 of 36

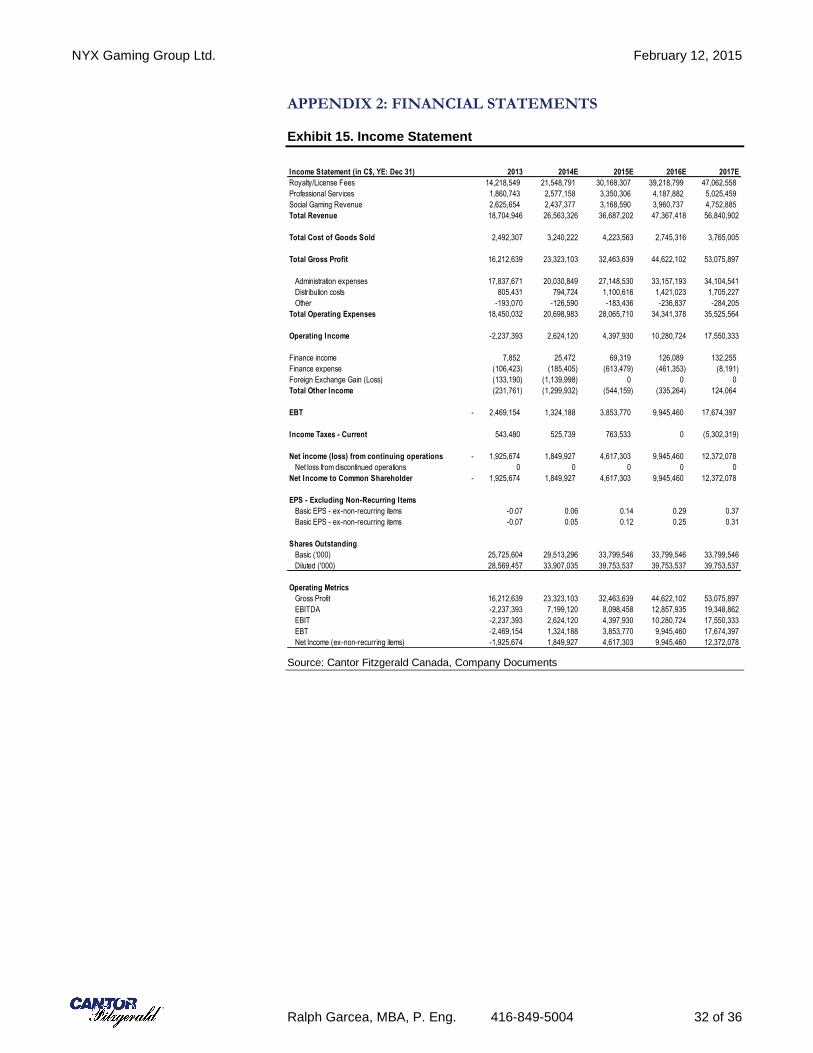

APPENDIX 2: FINANCIAL STATEMENTS

Exhibit 15. Income Statement

Source: Cantor Fitzgerald Canada, Company Documents

Income Statement (in C$, YE: Dec 31) 2013 2014E 2015E 2016E 2017E

Royalty/License Fees 14,218,549 21,548,791 30,168,307 39,218,799 47,062,558

Professional Services 1,860,743 2,577,158 3,350,306 4,187,882 5,025,459

Social Gaming Revenue 2,625,654 2,437,377 3,168,590 3,960,737 4,752,885

Total Revenue 18,704,946 26,563,326 36,687,202 47,367,418 56,840,902

Total Cost of Goods Sold 2,492,307 3,240,222 4,223,563 2,745,316 3,765,005

Total Gross Profit 16,212,639 23,323,103 32,463,639 44,622,102 53,075,897

Administration expenses 17,837,671 20,030,849 27,148,530 33,157,193 34,104,541

Distribution costs 805,431 794,724 1,100,616 1,421,023 1,705,227

Other -193,070 -126,590 -183,436 -236,837 -284,205

Total Operating Expenses 18,450,032 20,698,983 28,065,710 34,341,378 35,525,564

Operating Income -2,237,393 2,624,120 4,397,930 10,280,724 17,550,333

Finance income 7,852 25,472 69,319 126,089 132,255

Finance expense (106,423) (185,405) (613,479) (461,353) (8,191)

Foreign Exchange Gain (Loss) (133,190) (1,139,998) 0 0 0

Total Other Income (231,761) (1,299,932) (544,159) (335,264) 124,064

EBT 2,469,154- 1,324,188 3,853,770 9,945,460 17,674,397

Income Taxes - Current 543,480 525,739 763,533 0 (5,302,319)

Net income (loss) from continuing operations 1,925,674- 1,849,927 4,617,303 9,945,460 12,372,078

Net loss from discontinued operations 0 0 0 0 0

Net Income to Common Shareholder 1,925,674- 1,849,927 4,617,303 9,945,460 12,372,078

EPS - Excluding Non-Recurring Items

Basic EPS - ex-non-recurring items -0.07 0.06 0.14 0.29 0.37

Basic EPS - ex-non-recurring items -0.07 0.05 0.12 0.25 0.31

Shares Outstanding

Basic ('000) 25,725,604 29,513,296 33,799,546 33,799,546 33,799,546