Embed Size (px)

Citation preview

Asia’s Private Equity News Source avcj.com July 15 2014 Volume 27 Number 26

ANALYSIS DEAL OF THE WEEK

Diving into distressLPs look for stand-out strategies among Asia’s special situations GPs Page 7

Looking for liquidity2Q analysis: IPOs stay, Phillippines rise Page 10

The next Nintendo?WiL to take Japan gaming platform global Page 12

WH Group IPO: Battling perception problems

Page 3

ADIA, DeAWM, Everstone, Fidelity, GGV, Gree, Hony Capital, INCJ, JBIC, KKR, Navis, PEP, Sequoia, Standard Chartered PE, Steadview, Temasek

Page 4

EDITOR’S VIEWPOINT

NEWS

INDUSTRY Q&A

MSPEA’s post-Volcker Rule Asia fundraise

Page 13

DEAL OF THE WEEK

FUNDS

Ascendent Capital’s Liang Meng and Kevin Zhang

Page 14

VCs back selfie craze with Nice China investment

Page 12

GLOBAL PERSPECTIVE, LOCAL OPPORTUNITY avcjrealassets.com

avcjrealassets.com

1

2nd Annual Real Assets ForumAVCJ SPOTLIGHT:

Private equity investment in infrastructure, energy and real estate

28 August, 2014 • Four Seasons Hotel, Singapore

Key reasons to attend:

Registration enquiries: Carolyn Law T: +852 3411 4837 E: [email protected] Enquiry

Sponsorship enquiries: Darryl Mag T: +852 3411 4919E: [email protected]

For the latest programme and speaker line-up, visit: avcjrealassets.com

Unlocking the Real Assets Potential

1 Understandthe macroeco-

nomic forces shaping the

global real asset industry

2 Explorethe real asset

opportunities in 2015

3 Learnhow to reap the rewards of Asia’s real estate frenzy

4 Find outhow to capitalize

on a changing China

5 Discoverthe LP’s

perspective on real assets

SAVEUS$200 by 8 AUGUST 2014

BOOK NOW

Connect with over 160 PE leaders

Hear from 25+ expert speakers

Network with

40+ LPs

Asia Series Sponsor Co-Sponsors

Join your peers

Tweet #avcjrealassets

Number 26 | Volume 27 | July 15 2014 | avcj.com 3

EDITOR’S [email protected]

“I TOLD EVERYONE AT THE BEGINNING OF the year, ‘The two biggest risks for our industry are Shuanghui and Alibaba messing up.’ I knew there was going to be a pain trade but I thought it would be Alibaba, not Shuanghui.”

The China private equity investor who made the above observation added that his primary concern with Alibaba is escalating valuations – scenarios in which hedge fund sells to hedge fund and the demand for access is such that the numbers flying around bear little resemblance to the reality on the spreadsheet. And this for a company that, despite its undoubted size and success, carries numerous question marks: corporate governance, regulation, ability to respond to upstart peers and industry fluctuations…

By contrast, Shuanghui – now known as WH Group – is more of a sure thing. Wan Long, the company’s founder and chairman, famously explained his business to one Chinese newspaper as follows: “What I do is kill pigs and sell meat.” It is a historically profitable business within China too, a market in which the economic fundamentals point to rising per capita consumption of meat.

And yet it is WH Group, not Alibaba that is in the process of rebuilding its IPO. The first iteration, which launched in early April, targeted a $5.3 billion offering, enough to value the entire company at up to $21 billion and make it the second-largest IPO by a food and beverage player globally after Kraft Foods. CDH Investments, Goldman Sachs, Temasek Holdings and New Horizon Capital all planned to sell a portion of their shares.

Come the end of the month and the size of the offering had been slashed by more than half, with none of the aforementioned PE backers set for a partial exit. Soon it wasn’t happening at all, the company citing “deteriorating market conditions and recent excessive market volatility.”

WH Group is the work of many years and multiple funds for CDH. The private equity firm made its name restructuring Chinese companies

– and taking them offshore until regulations made it more difficult – in preparation for IPOs. This clean exit never seemed to happen for what was then Shuanghui, but everything changed with the acquisition of US-based Smithfield Foods for $4.7 billion. Suddenly an IPO was on the table for the world’s biggest pork company.

For all the hype about Alibaba, was WH Group undone by the fact that investors struggled to grasp what the company had become? Certainly, there were perception issues.

Questions have already been asked about the number of banks involved in the original offering and the revised prospectus issued last week has whittled them down from 29 to two. Then there were valuation concerns and the application of a typically high China consumer multiple to a company with substantial exposure to upstream US hog farming. Market conditions might also have deteriorated less rapidly with the reassuring presence of a few cornerstone investors, as is now the custom for large Hong Kong IPOs.

Beyond that, investors were perhaps rightfully wary of a business that was still in the process of digesting a major acquisition. Where was the compelling evidence of synergies? With this in mind, a $597 million payout to two senior executives for their role in a highly-leveraged transaction that has yet to bed down does not look good. And from a private equity perspective, no matter how many times WH Group emphasizes the long-term value of uniting Shuanghui and Smithfield, there may always be the perception in some quarters that assets have been glued together to facilitate a listing.

All criticisms, but none of them fatal and so WH Group’s return – with a less banked and presumably more humbly priced IPO – is no surprise. And after that, Alibaba.

Tim BurroughsManaging EditorAsian Venture Capital Journal

The pigs will flyManaging Editor

Tim Burroughs (852) 3411 4909 Staff Writers

Andrew Woodman (852) 3411 4852 Winnie Liu (852) 3411 4907

Creative Director Dicky Tang Designers

Catherine Chau, Edith Leung, Mansfield Hor, Tony Chow

Senior Research Manager Helen Lee

Research Associates Herbert Yum, Isas Chu, Jason Chong, Kaho Mak

Circulation Manager Sally Yip

Circulation Administrator Prudence Lau

Subscription Sales Executive Jade Chan

Manager, Delegate Sales Pauline Chen

Director, Business Development Darryl Mag

Manager, Business Development Anil Nathani, Samuel Lau

Sales Coordinator Debbie Koo

Conference Managers Jonathon Cohen, Sarah Doyle,

Conference Administrator Amelie Poon

Conference Coordinator Fiona Keung, Jovial Chung

Publishing Director Allen Lee

Managing Director Jonathon Whiteley

The Publisher reserves all rights herein. Reproduction in whole or in part is permitted only with the written consent of

AVCJ Group Limited. ISSN 1817-1648 Copyright © 2014

Incisive Media Unit 1401 Devon House, Taikoo Place

979 King’s Road, Quarry Bay,Hong Kong

T. (852) 3411-4900F. (852) 3411-4999E. [email protected]

URL. avcj.com

Beijing Representative OfficeNo.1-2-(2)-B-A554, 1st Building,

No.66 Nanshatan,Chaoyang District, Beijing,People’s Republic of China

T. (86) 10 5869 6203F. (86) 10 5869 6205 E. [email protected]

GLOBAL PERSPECTIVE, LOCAL OPPORTUNITY avcjrealassets.com

avcjrealassets.com

1

2nd Annual Real Assets ForumAVCJ SPOTLIGHT:

Private equity investment in infrastructure, energy and real estate

28 August, 2014 • Four Seasons Hotel, Singapore

Key reasons to attend:

Registration enquiries: Carolyn Law T: +852 3411 4837 E: [email protected] Enquiry

Sponsorship enquiries: Darryl Mag T: +852 3411 4919E: [email protected]

For the latest programme and speaker line-up, visit: avcjrealassets.com

Unlocking the Real Assets Potential

1 Understandthe macroeco-

nomic forces shaping the

global real asset industry

2 Explorethe real asset

opportunities in 2015

3 Learnhow to reap the rewards of Asia’s real estate frenzy

4 Find outhow to capitalize

on a changing China

5 Discoverthe LP’s

perspective on real assets

SAVEUS$200 by 8 AUGUST 2014

BOOK NOW

Connect with over 160 PE leaders

Hear from 25+ expert speakers

Network with

40+ LPs

Asia Series Sponsor Co-Sponsors

Join your peers

Tweet #avcjrealassets

avcj.com | July 15 2014 | Volume 27 | Number 264

ASIA PACIFIC

DeAWM hires Sambanju for Asia secondariesJason Sambanju, formerly co-head of Asia at Paul Capital Partners, has joined Deutsche Asset & Wealth Management (DeAWM) as head of Asia secondaries. In his newly created role, Sambanju will take responsibility for sourcing and executing secondary private equity opportunities across the region.

AUSTRALASIA

KKR, PEP to make joint bid for Australia’s Sai GlobalKKR is expected to team up with Australian private equity firm Pacific Equity Partners (PEP) to bid for risk management and standards compliance business SAI Global. In May, PEP offered to buy all outstanding shares in SAI via a scheme of arrangement, valuing the company at A$1.1 billion ($1 billion).

GREATER CHINA

Investors eye liquidity as WH Group revives HK IPOPrivate equity-backed Chinese pork processor WH Group is once again seeking to list in Hong Kong, three months after a HK$41 billion ($5.3 billion) IPO was scrapped. WH Group has filed a revised prospectus but with no further details on pricing or timing. The company is reportedly targeting $2-3 billion and will come to market in late July or early August.

PE consortium targets $1.5b China outbound fundA consortium of foreign and Chinese PE firms has begun raising a $1.5 billion fund, which aims to raise a combination of US dollars and Chinese currency to invest abroad. The fund was set up in December by Chinese GPs Bohai Industrial Investment Fund Management and Harvest Fund Management, alongside US Rosemont Seneca Partners and Thornton Group, with an original target of $1 billion.

Sequoia’s China Maple Leaf Education files for HK IPOChina Maple Leaf Education Systems, a Chinese

international school operator backed by Sequoia Capital, has filed for an IPO on the Hong Kong Stock Exchange. The company operates 33 schools of different kinds across eight cities. Sequoia invested RMB180 million ($29 million) in Maple Leaf in 2008, taking roughly a 20% stake.

Chinese regulator issues guidelines for domestic PEThe China Securities Regulatory Commission (CSRC) has issued draft rules for the domestic private equity industry, including a definition of investors qualified to participate as LPs. Investors committing more than RMB1 million to a privately-offered fund must: have at least RMB10

million ($1.6 million) in net assets; have individual financial household assets of at least RMB3 million; or have an average annual individual income of at least RMB500,000 in the last three years.

GGV leads $10m round for gamer networking platformSino-US VC firm GGV Capital has led a $10 million Series B round funding for Curse, a US-based social networking platform that targets online gamers. The new financing – which also includes $6 million in venture debt from Multiplier Capital – will be used for product development. Curse Voice adopts a similar business model to Chinese social networking service YY.

Prologis raises more capital for China logistics platformPrologis, an industrial real estate investment trust (REIT), has increased $588 million to Prologis China Logistic Venture, a platform used to acquire and manage logistics properties in China. HIP China Logistics Investment – understood to be a subsidiary of Abu Dhabi Investment Authority (ADIA) – will contribute $500 million, with Prologis putting in the remainder.

SCPE backs China property joint ventureStandard Chartered Private Equity (SCPE) has led a $124 million financing round for a mixed-used commercial property development project in China. SCPE has paid $69.4 million for a 28% interest in the joint venture, with the rest coming from an undisclosed Chinese institutional investor and an Asian family group.

Chinese stationery firm launches PE fundShenzhen Comix Stationery, a Shenzhen-listed stationery manufacturer, has won approval to launch a PE fund, which will be managed by Hejun Consulting. The vehicle, namely Comix Hejun Industry Fund, has an investment size of RMB500 million ($80 million).

Horizons Ventures joins reputation site roundHorizons Ventures, a VC business owned by Hong Kong billionaire Li Ka-Shing, has participated in a $4.7 million Series A round for shopping-based social platform Traity. The round was led by European VC firm Active Venture Partners, with participation from KRW Schindler Private

Hony buys Pizza Express from Cinven for $1.54bChinese PE firm Hony Capital has agreed to buy restaurant chain Pizza Express from UK-based private equity firm Cinven Partners for GBP900 million ($1.54 billion). The transaction is the largest seen in Europe’s casual dining industry in the past five years.

Cinven owns Gondola Group, operator of restaurant brands including Zizzi, ASK Italian and Kettner’s, as well as Pizza Express. The buyout

firm acquired the parent company in a public-to-private transaction worth EUR1.34 billion ($1.8 billion) in 2007. The sale of Pizza Express follows the sale of Byron Hamburgers, an up-market burger chain owned by the Gondola Group, to European private equity firm Hutton Collins Partners for GBP100 million last year.

Pizza Express currently has 436 shops in the UK and an additional 68 internationally, with 12 of which in Hong Kong, nine in Shanghai and one in Beijing. Richard Hodgson, Pizza Express’s CEO, will remain with the business. “We have built a strong track record in helping Chinese enterprises to expand globally,” said John Zhao, CEO of Hony. “With Pizza Express, we have the opportunity to leverage our local expertise to accelerate its growth in the Chinese market, as well as to continue to drive its business forward in the UK.”

NEWS

Number 26 | Volume 27 | July 15 2014 | avcj.com 5

Ventures, Bertelsmann Digital Media Investments, Lanta Digital Ventures, 500 startups and other individuals.

NORTH ASIA

JBIC, Mitsubishi take stake in Mid East water companyThe Japan Bank for International Cooperation (JBIC) has joined Mitsubishi Corp. and Mitsubishi Heavy Industries in acquiring a stake in Middle Eastern water treatment firm Metito. JBIC will invest up to $92 million in new preferred stock, while a special purpose vehicle will acquire 38.4% of Metito’s existing shares.

INCJ, Fidelity in cloud storage provider roundInnovation Network Corporation of Japan (INCJ and Fidelity Growth Partners have taken part in $24 million round for US-based Cloudian, a hybrid cloud storage solutions provider. Existing investors including Intel Capital also participated.

Japan’s Gree leads $4.5m round for HotelQuicklyJapanese tech giant Gree has led a $4.5 million Series A-1 round of funding for HotelQickly, a Hong Kong-headquartered last-minute hotel booking platform. This follows a $1.15 million Series A round in August last year.

SOUTH ASIA

SCPE commits $83m to Indian power businessStandard Chartered Private Equity (SCPE) will invest INR5 billion ($83 million) in the power grid subisiary of Sterlite Technologies, a listed Indian transmission solutions provider for the telecom and power industries. This is said to be the first foreign investment in India’s power transmission sector, with most overseas players having focused on power generation.

Steadview, Sequoia lead $41m Olacabs roundIndian online taxi-booking and car rental platform Olacabs has raised INR2.5 billion ($41.8 million) through a Series C round of funding led by Sequoia Capital and Hong Kong-based hedge fund Steadview Capital. Existing investors Matrix Partners India and Tiger Global also participated.

India lays ground for REIT roll-outIndia’s long-awaited real estate investments trusts (REITs) inched closer to reality as the government offered clarification on the tax status of the structures. Finance Minister Arun Jaitley said that REITs would have pass-through status - which means they are not liable for corporate tax. The move is intended to create a single layer of tax for the structures.

Everstone, Fidelity exit Transpole to Japan’s SBSEverstone Capital and Fidelity Growth Partners will exit Transpole Logisitcs as Japan’s SBS Group agreed to acquire a 66% stake in the Indian company for an undisclosed amount. Fidelity paid $13.5 million for a significant minority stake in the company in April 2011. It then made a partial exit in January last year when Everstone paid INR2.2 billion (around $40 million) for a near 25% stake.

App developer platform gets Series A roundPokkt, an Indian alternative monetization platform for mobile app developers, has secured $2.5 million in Series A funding from Singapore-based Jafco Asia and SingTel’s corporate VC arm Innov8. Existing investors Jungle Ventures and Ganesh Krishnan also participated in the round.

SOUTHEAST ASIA

Temasek ups investments, boosts unlisted exposureTemasek Holdings’ exposure to unlisted assets reached a record high as the state-controlled Singaporean fund made S$24 billion ($19.3 billion) in new investments for the year ended March 2014, the most in six years. Temasek ended the 12-month period with a portfolio worth S$223 billion, also a record high.

Navis buys Singapore oil and gas components makerNavis Capital Partners has acquired a majority stake in Tri-Star Industries, a Singapore-headquartered component manufacturer for the oil and gas sector. AVCJ understands the deal is worth $50-100 million. Key management will remain in place as shareholders and operators of the business.

DFI-backed vehicle invests in power plant developerIndonesia Infrastructure Finance, a vehicle owned by the Indonesian government and serveral development finance institutions (DFI), has committed $12.5 million for a minority stake in the Indonesian subsidiary of gas power plant developer Maxpower. International Finance Corporation (IFC), Asian Development Bank and Germany’s DEG are all involved, plus Sumitomo Mitsui Banking Corporation..

India announces $1.6b fund to support start-upsThe Indian government has pledged to support local start-ups by launching a INR100 billion ($1.6 billion) fund-of-funds. The fund is one of a raft of proposals put forward by Finance Minister Arun Jaitley on Thursday with a view to boosting entrepreneurship and encouraging small enterprises, as part of the Union Budget for 2014-2015. It will serve as a catalyst for attracting private capital by providing equity, mezzanine capital, soft loans and other risk capital to start-ups. However, as of yet, there is no more detail on how the fund will be allocated.

Plans were also unveiled to establish a technology center to promote innovation, entrepreneurship and agro-industry accompanied by a fund with a corpus of INR2 billion. The government added that it will put

aside other smaller pools of capital for early-stage investment, including a INR1 billion for a “Start Up Village Entrepreneurship Program” for rural youths.

Jaitley said there was a need to “examine the financial architecture” of the micro, small and medium enterprises (MSME) sector. He proposed appointing a committee of representatives from the Finance Ministry, the Ministry of MSMEs and the Reserve Bank of India to make recommendations on how the sector can be better financed. He also proposed that the definition of MSME be reviewed to provide for a higher capital ceiling, which will give companies easier access to credit.

NEWS

Book Now and

Save BIG!Register online at

www.avcjforum.com or email

Asia series sponsor

Co-sponsors

Lead sponsors

Legal sponsor

LP summit sponsor Awards sponsors Exhibitor

VC summit sponsorsLP Breakfast sponsor VC summit legal sponsor

PE leaders’ summit sponsors

Early Bird Expires on 10 October

Customer Enquiries:Email us at [email protected]

Registration Enquiries:CALL Carolyn Law on +852 3411 4837

Sponsorship Enquiries: Darryl Mag T: +852 3411 4919 E: [email protected]

11-13 November 2014 Four Seasons Hotel, Hong Kong

AVCJ PRIVATE EQUITY & VENTURE FORUM 2014

27th Annual

Meet 1,000+ global PE professionals

Network with 280+ LPs

Hear from 170+ expert speakers

Join attendees from 35+ countries

Join your peers

Tweet #avcjforum

Scan this QR code to register to

this event NOW

Number 26 | Volume 27 | July 15 2014 | avcj.com 7

COVER [email protected]

IF FURTHER CONVINCING WERE REQUIRED that Asian distress funds have become a major draw for LPs, perhaps May saw the last doubts laid to rest. Within days of each another, two GPs – one focused on India distress opportunities, the other a pan-regional special situations fund – revealed they had raised $1.73 billion between them, both far exceeding their original targets.

The first was Aion Capital Partners, a joint venture formed by Apollo Global Management and ICICI Ventures. It received commitments of $825 million for its maiden special situations fund, having set out to raise a more modest $500 million just over a year ago. The fund will pursue opportunities such as financial restructurings, recapitalizations and promoter financings.

Then second was SSG Capital Partners, which closed its third Asia special situations fund at the hard cap of $915 million after only five months in the market. The fund – backed by mixture of large family offices, pension funds and insurance companies, among others, from Europe and the US – targets numerous proprietary transactions but specializes in restructuring.

The two GPs’ strategies differ but both speak of a broader trend of growing acceptance in the investor community. Already part of the furniture in developed markets, distress and private debt are now more widely recognized as an asset class in Asia and LPs are looking to increase allocations. Strategies and track records are being scrutinized, but will these niche managers receive enough backing to enter the mainstream?

“I think, from an Asian perspective, it is a factor of the maturation of the Asian private equity market, where investors have built significant exposure to the region during the mid-to-late 2000s and now they are seeking further diversification and yield,” says Jonathan English, managing director with Portfolio Advisors.

According to Preqin, three Asia-focused distress funds have raised $1.9 billion so far this year compared to $1.7 billion, across 11 funds, in 2013. This is less than the 2012 tally of $6.5 billion, but it could be argued that Mount Kellett Capital Management, which raised $4 billion for a global fund with a substantial Asia allocation, should be discounted. Meanwhile, there are around seven Asia-focused funds currently in the market looking to raise a collective $5.8 billion.

Given the Asian market still lacks depth, the numbers offer only a partial insight. On a global basis, while distress fundraising has been slow so far in 2014 – with $13 billion committed to 16 funds – managers have proliferated in recent years. In 2013, $35 billion raised by 45 funds compared to $26 billion by 39 funds in 2010. An estimated 63 managers are currently seeking to raise $33 billion.

Growing appetites There are number of factors driving increased LP interest in debt-related assets, particularly in Asia. First and foremost, many investors say returns coming out of the region have been disappointing. This leads LPs to look for alternatives and private debt is an option.

Barry Lau, managing partner as Adamas

Assest Management, observes that LPs had historically overlooked private debt in favor of seeking 2-3x returns by investing traditional growth capital and buyouts. But as the reality is changing, so is investor appetite. “LPs are sort of having this awakening and realizing that actually it is not bad to generate a quick cash return and therefore private debt has become more of an interesting topic,” he says.

Rob Petty, managing partner and co-founder of Clearwater Capital Partners, contends that the absolute yield for Asian credit relative to the US and Europe is simply more compelling. “If you compare growth capital or buyout return history and cash distribution timetables versus

the credit and special situations track record, the opportunity set looks increasingly interesting,” he says.

To better understand where LPs are looking for with regards to distressed debt one must examine the areas that have seen the most activity to date.

Across the region, slower growth and increasing corporate debt are putting more pressure on company balance sheets. Add to this the number of Asian companies that have run into trouble due to overexpansion or mismanagement and there are a number of opportunities for distress investors. In many cases, these companies might be good businesses with bad balance sheets that – as a result of unwise strategic moves – are unable to service their debt under current operations.

“The broader trend is that banks are not lending for their own reasons and there is a gap in funding in Asia,” says Sharon Hartline, a fund formation lawyer and partner with White & Case in Hong Kong. “In particular, Asian debt-related strategies are popular among US pension plans and college endowments where they are looking for steady returns instead of home-runs.”

Within Asia, three jurisdictions have typically been the focus of distress investors: India, China and Australia. The first two account for the bulk of opportunities in the region.

While the election of a new government has been a cause for optimism in India recently, over the past year economic growth has deteriorated

In credit?Whether disillusioned by the returns from conventional private equity or seeking to diversify their exposure, LPs are more open to Asia credit strategies. The returns are there, provided you pick the right strategy

Funds closed

Fundraising for Asia-focused distressed PE funds

Source: Preqin * Includes distressed debt, special situations and turnaround strategies

8

6

4

2

0

12

10

8

6

4

2

US$

billi

on

Fund

s

Aggregate capital raised (US$ billion)

2010 2011 2012 2013 2014 YTD

Book Now and

Save BIG!Register online at

www.avcjforum.com or email

Asia series sponsor

Co-sponsors

Lead sponsors

Legal sponsor

LP summit sponsor Awards sponsors Exhibitor

VC summit sponsorsLP Breakfast sponsor VC summit legal sponsor

PE leaders’ summit sponsors

Early Bird Expires on 10 October

Customer Enquiries:Email us at [email protected]

Registration Enquiries:CALL Carolyn Law on +852 3411 4837

Sponsorship Enquiries: Darryl Mag T: +852 3411 4919 E: [email protected]

11-13 November 2014 Four Seasons Hotel, Hong Kong

AVCJ PRIVATE EQUITY & VENTURE FORUM 2014

27th Annual

Meet 1,000+ global PE professionals

Network with 280+ LPs

Hear from 170+ expert speakers

Join attendees from 35+ countries

Join your peers

Tweet #avcjforum

Scan this QR code to register to

this event NOW

avcj.com | July 15 2014 | Volume 27 | Number 268

to its slowest pace in a decade, leaving companies struggling to raise capital. Aion is just one of a number of GPs looking at the country.

Data from the Reserve Bank of India indicate that stressed assets, including bad debts and restructured loans, rose to 10.2% of total debt held by Indian banks last year, the highest in a decade. In this context, the government has also sought to encourage private-equity funds and asset reconstruction companies to play an active role in stressed assets markets.

“Two years ago when we sat on the conference panels and said India was interesting, people rolled their eyes,” says Petty. “Today, if you look at realized returns, India has performed very nicely over the past 18 months.”

Specifically, more GPs are looking to target debt opportunities in the country. KKR has

been providing local currency debt products via its own non-banking finance company for several years. In January, the firm reached a final close of $2 billion on a global special situations fund. A month later, during a visit to India, KKR co-founder Henry Kravis said the firm was keen to capitalize on corporate indebtedness by investing in companies with distressed balance sheets that have difficulty raising capital through conventional channels.

China’s economic expansion has yet to slow to Indian pace, but for companies with business models predicated on the hyper-growth rates of recent of years the financial pressure is very real. According to the China Banking Regulatory Commission, non-performing loans (NPLs) rose by RMB28.5 billion ($4.7 billion) in the last quarter of 2013 to reach RMB592.1 billion, the highest level seen since September 2008.

These debts represent a complex patchwork of state and private interests, making it difficult to quantify the size of the opportunity, but Shoreline Capital is the forefront of those looking to take advantage of it. The China-focused GP, which raised $303 million for its second fund and

is said to be targeting $500 million for Fund III, buys NPLs and looks for ways to force payment or extract value from related assets.

Adamas’ strategy is to provide credit alternatives to companies that can’t access financing through conventional channels – certainly not the capital markets and increasingly not the banking system either. Lau explains that with bank balance sheets shrinking so often, his firm is often one of few options remaining, which translates into creditor-friendly terms. “We are looking at an emerging market risk but we are getting paid for taking that risk,” he adds. “For example, we are getting returns of 25% and you can’t get that from anywhere else in Asia.”

However, not all of Asian distress opportunities are limited to the region’s emerging economies. Until recently, Australia

tended to be seen in the context of highly-leveraged companies struggling to unwind positions that became untenable in the wake of the global financial crisis. Now most of this low-hanging fruit has been picked, investors are looking at smaller mid-market deals.

The challenge is generating attractive returns in a market that is far more mature than China and India and doesn’t offer the same risk-return profile. Allegro Private Equity is an example of an investor with a strategy closer to traditional private equity. It focuses on control positions in distressed business where operational improvements are used to drive returns.

“The large restructurings have been done so I don’t think that space is as rich in targets,” says Adrian Loader, managing director at Allegro. “But businesses below $150 million dollars are in need of solutions that involve more than just money because we you have to fix the board and solve operational issues.”

The combination of strong a rule of law supported by predictable creditor laws and strict director laws means Australia is can be attractive to more risk-averse LPs. But Loader cautions

that making the system work requires a local presence and a highly specific skill set. “I honestly believe that the whole game is about providing capital and solutions, and a lot of the solutions involve being on the ground,” he says.

Region vs. countryThe diversity of the distress opportunity in Asia begs the question as to whether LPs are best served backing managers in individual markets rather as opposed to pan-regional players. It should come as no surprise where the different GPs stand on this. Much like Loader, Lau of Adamas – which focuses exclusively on China – emphasizes the advantages of a country specific approach and an on-the-ground presence.

“Private debt is a localized business because credit protection is different from country to country and it is difficult to be experts in almost every single geography and jurisdiction,” he says. “You need a local team for everything you do and our vision was that we would focus on China because from a risk-return standpoint, it makes perfect sense.”

On the other hand, Petty of Asia-focused Clearwater argues that debating the respective merits of a regional versus a country-specific strategy somewhat miss the point.

“It is not just about geography, but people always chart Asia by geography. We emphasize again and again that it is about sectors,” he says. “For example, if you look at the commodities and natural resources space, whether it is in India, Indonesia, Australia or China – coal is getting crushed. Shipping is also creating opportunities across a number of jurisdictions.”

Indeed, the market has seen a number of deals in these areas. Clearwater previously bought and sold both Griffin Coal Mining and Carpenter Mine Management to Lanco Resources Australia. Meanwhile, GPs like Denham Capital and Helmsman Capital are targeted distressed mining opportunities.

However, regardless of strategy, convincing some LPs of the Asian distress opportunity is still a challenge. “For the nascent LPs in this space, there always tends to be an issue with return multiples, as the multiples are typically going to be lower than with a pure PE play,” says Portfolio Advisors’ English. “That is an issue for some LPs – getting comfortable with the return profile and where it fits into their broader portfolio construction.”

He is not alone in this view. While an increasing number of LPs are focused on private debt and building out their absolute returns coverage, education remains an issue. Speaking to AVCJ after announcing the final close of Fund III, Edwin Wong, managing partner of SSG, observed that receptiveness to credit

COVER [email protected]

Funds closed

Fundraising for distressed PE funds globally

Source: Preqin

40

30

20

10

0

50

40

30

20

10

US$

billi

on

Fund

s

Aggregate capital raised (US$ billion)

2010 2011 2012 2013 2014 YTD

COVER [email protected]

strategies had improved since the firm’s previous fundraising cycle, but defining the opportunity set can be challenging.

Needless to say, explaining a portfolio of 25 credit or special situations investments relating to companies with varying levels of financial health is more complicated than 10-12 buyout or growth capital deals that may follow coherent sector patterns. “It is just more complex, especially when you layer in structures, cash- flow characteristics, and multiple scenario analysis of different exit routes,” notes Clearwater’s Petty.

The other difficulty facing GPs is the lack of track records in Asian distress. One LP observes that pan-regional funds have served investors well these past few years, providing liquidity even when markets are tough. But at the same time, few data points are available for a fully-realized, liquidated portfolio in Asia.

“In some cases, the returns are locked-in from a current yield perspective,” the LP explains. “You can try to goose the IRR with an equity kicker, and the upside can drive the multiple, but there are very few data points from a fully realized track record that demonstrate that outcome.”

Chicken and eggDespite the recent fundraising success stories, question marks over strategy and track record still present obstacles for distress-focused GPs as they make the transition from niche to mainstream. It is arguably the same for many managers in Asia, but particularly the more specialist players, as they deal with investor inquiries. Certainly, the phenomenon of capital being concentrated in fewer hands is common to all.

“We have had people coming in to talk to us for the last years two years on these strategies, but in the past six months we have noticed more people in the market are having trouble raising even their third or fourth fund,” says White &

Case’s Hartline. She adds that LPs remain cautious about stepping in too soon, especially in China where some expect the economy to deteriorate.

If distress is to sustain the broader interest it has been receiving, a larger manager universe is essential. But are there sufficient people with experience and expertise in executing transactions across the capital structure? Clearwater’s Petty says no.

“It is a pretty small group of GPs that run institutional capital of $1 billion plus and have a team across multiple geographies that can do deals of $25-100 million,” he explains. “There are perhaps 10 of us – that is not many for a $30 trillion market. Because of the complexity of the deals, it takes larger teams, generally more systems and analytical firepower to play across the capital structure.”

The more managers, the easier it becomes to fill the gaps in investor education. The caveat is LPs have to be comfortable enough to support new GPs as they emerge. Adamas’ Lau understands the need to tread carefully when an industry is in its nascent stages, but stresses that early movers might have the most to gain.

“So long as investors are willing to consider the space and willing to take a leap of faith in this emerging sector I think they will be handsomely rewarded,” he says.

“If you compare growth capital or buyout return history and cash distribution timetables versus the credit and special situations track record, the opportunity set looks increasingly interesting” – Rob Petty

The most authoritative and comprehensive guide to private equity investors in Asia

The Asian Private Equity Online Directory is the most comprehensive online directory on private equity and venture capital in Asia. It is easy to navigate, enabling access to a listing of around 3,900 Asian private equity firms and over 9,600 professionals.

For a free trial, please visit asianfn.com/VCDemo.

Asian Private Equity Online Directory

To subscribe, call Sally Yip at +(852) 3411 4921 or email [email protected]

avcj.com

avcj.com | July 15 2014 | Volume 27 | Number 2610

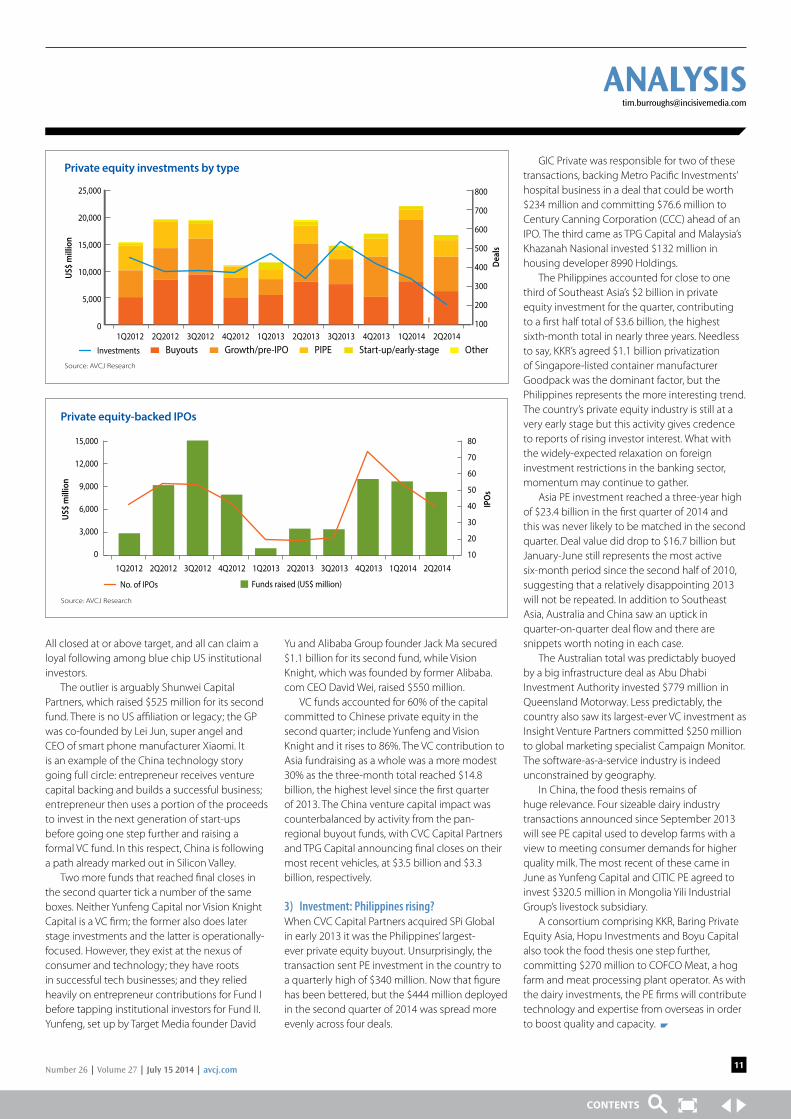

1) Exits: The roll continuesThree months ago, the question was whether bumper first-quarter trade sale and IPO numbers could be sustained. It appears they can – at least for the time being.

According to provisional data from AVCJ Research, trade sales for May-June generated $7.3 billion, just short of the first quarter’s $7.5 billion, while overall exits came in at $13.2 billion, compared to $13.3 billion for the previous three months. As with the previous quarter, one large-ticket item moved the needle: Australia’s QIC scooped $6.2 billion by selling Queensland Motorways to Transurban Group, AustralianSuper and Abu Dhabi Investment Authority. Without it, the total looks far more ordinary.

As is usually the case, trade sales account for the bulk of the top 25 exits for the quarter. More notable is that seven of the entries were IPOs (i.e. full or partial exits from companies on listing). Australia figures prominently, confounding observations that sparse first-quarter activity was evidence of the public markets window closing. Having abandoned its IPO in the first quarter, CVC Capital Partners-owned Mantra is now listed. This was one of eight PE-backed IPOs in Australia that between them raised $2.7 billion between April and June, the highest quarterly total on record.

More than half of these proceeds were generated by two offerings: catering and cleaning contractor Spotless Group (A$994.6 million, $931 million) and hygiene and paper products manufacturer Asaleo Care (A$655.7 million). Pacific Equity Partners and its co-investors retain a minority interest in the former and fully exited the latter, taking approximately A$537 million from both IPOs. Ironbridge Capital also received proceeds of A$168.4 million through the exit of all but a 5% holding in in vitro fertilization specialist Monash IVF. Meanwhile, Quadrant Private Equity secured A$241.5 million from the IPOs of media monitoring business iSentia and Burson Auto Parts.

Asia-wide PE-backed IPOs generated $8.3 billion for the quarter from 40 offerings, down from $9.7 billion for the previous three months. A large portion of this came from Chinese online retailer JD.com, which raised $1.78 billion – pricing its offering above the indicative range due to investor demand and whetting the appetite for what may follow when Alibaba

Group also goes public in the US.Tiger Global Management, DST Advisors,

Hillhouse Capital Management and Capital Today all made partial exits, sharing approximately $674 million. But what they retain is far more valuable. Six disclosed PE and VC investors – the aforementioned four plus Bull Capital Partners and Sequoia Capital – have between them an economic interest of more than 40% in a business with a market capitalization of $38 billion and net revenues that increased threefold to $11.5 billion in the two years to 2013.

Capital Today invested $18 million in JD.com between 2007 and 2009, and held 6.8% of the company immediately after the IPO and is said to be sitting on an unrealized return of more than 100x.

2) Fundraising: A China VC storyThe rich seam of China VC fundraising continued into the second quarter of 2014, with an astonishing $3.7 billion raised across 16 vehicles. This is more than double the total for January-March and takes VC fundraising for the first half to $5.6 billion. To put that in context, it is 79% of all capital entering Asian VC funds during the period.

With six months left to run, 2014 is already the second-biggest year on record for China VC fundraising, trailing only 2011, which represented not only the peak of the pre-IPO investment boom but also the last time a lot of the established firms were in the market. This phenomenon also explains

the uptick in activity in 2008. There are other factors – fundraising is always going to be easier on the back of a string of IPO exits, for example – but historically the big names in China tend to seek new capital around the same time. It begs the question of what happens from the third quarter onwards and the reality is the headline number will drop off, perhaps dramatically.

Of the 20 largest funds in Asia to reach a final close in the second quarter, eight were China venture capital vehicles. GGV Capital led the way with $621.9 million for its fifth Sino-US fund, followed by IDG Capital Partners, Legend Capital, Matrix Partners and Lightspeed China.

Still open for businessThe IPO window remains open, especially in Australia; VCs continue to dominate China fundraising, but probably not for much longer; the Philippines stakes its claim as Southeast Asia’s emerging PE star

Private equity exits by type

Source: AVCJ Research

1Q2012 2Q2012 3Q2012 4Q2012 1Q2013 2Q2013 3Q2013 4Q2013 1Q2014 2Q2014

US$

mill

ion

25,000

20,000

15,000

10,000

5,000

0

Trade salePublic market sale Share buybackSeconadry buyoutNo. of exits

200

150

100

Exits

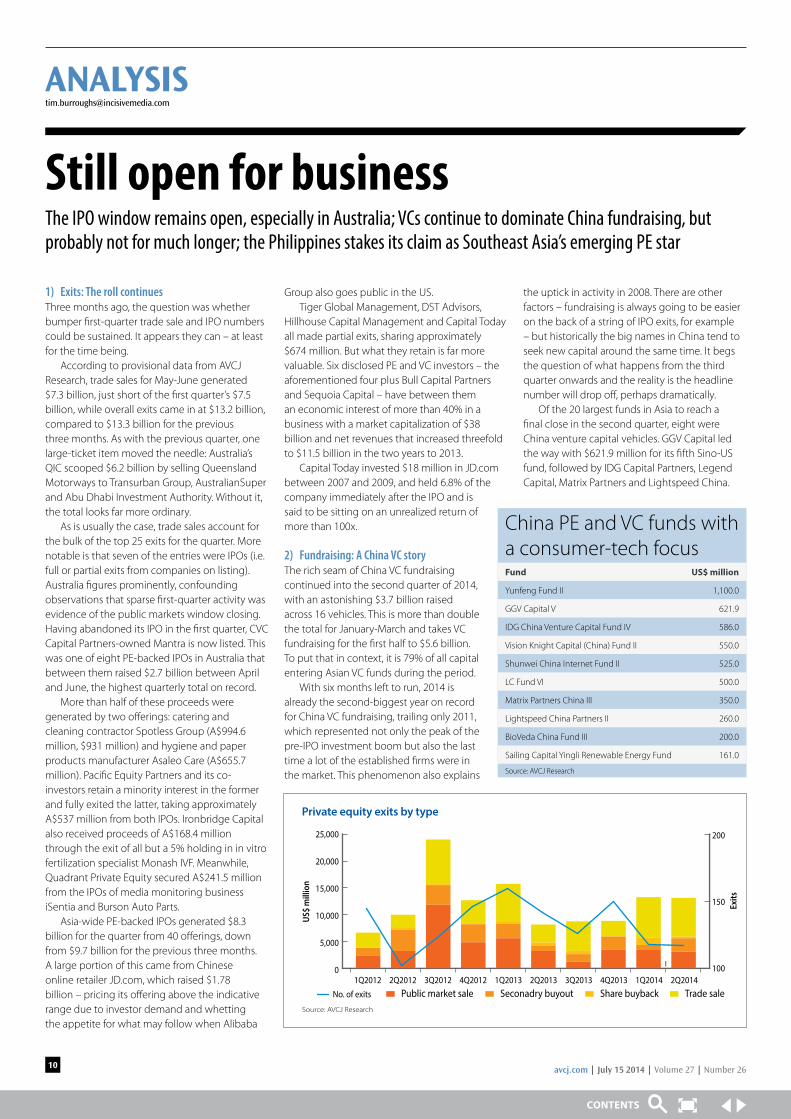

China PE and VC funds with a consumer-tech focusFund US$ million

Yunfeng Fund II 1,100.0

GGV Capital V 621.9

IDG China Venture Capital Fund IV 586.0

Vision Knight Capital (China) Fund II 550.0

Shunwei China Internet Fund II 525.0

LC Fund VI 500.0

Matrix Partners China III 350.0

Lightspeed China Partners II 260.0

BioVeda China Fund III 200.0

Sailing Capital Yingli Renewable Energy Fund 161.0

Source: AVCJ Research

Number 26 | Volume 27 | July 15 2014 | avcj.com 11

All closed at or above target, and all can claim a loyal following among blue chip US institutional investors.

The outlier is arguably Shunwei Capital Partners, which raised $525 million for its second fund. There is no US affiliation or legacy; the GP was co-founded by Lei Jun, super angel and CEO of smart phone manufacturer Xiaomi. It is an example of the China technology story going full circle: entrepreneur receives venture capital backing and builds a successful business; entrepreneur then uses a portion of the proceeds to invest in the next generation of start-ups before going one step further and raising a formal VC fund. In this respect, China is following a path already marked out in Silicon Valley.

Two more funds that reached final closes in the second quarter tick a number of the same boxes. Neither Yunfeng Capital nor Vision Knight Capital is a VC firm; the former also does later stage investments and the latter is operationally-focused. However, they exist at the nexus of consumer and technology; they have roots in successful tech businesses; and they relied heavily on entrepreneur contributions for Fund I before tapping institutional investors for Fund II. Yunfeng, set up by Target Media founder David

Yu and Alibaba Group founder Jack Ma secured $1.1 billion for its second fund, while Vision Knight, which was founded by former Alibaba.com CEO David Wei, raised $550 million.

VC funds accounted for 60% of the capital committed to Chinese private equity in the second quarter; include Yunfeng and Vision Knight and it rises to 86%. The VC contribution to Asia fundraising as a whole was a more modest 30% as the three-month total reached $14.8 billion, the highest level since the first quarter of 2013. The China venture capital impact was counterbalanced by activity from the pan-regional buyout funds, with CVC Capital Partners and TPG Capital announcing final closes on their most recent vehicles, at $3.5 billion and $3.3 billion, respectively.

3) Investment: Philippines rising?When CVC Capital Partners acquired SPi Global in early 2013 it was the Philippines’ largest-ever private equity buyout. Unsurprisingly, the transaction sent PE investment in the country to a quarterly high of $340 million. Now that figure has been bettered, but the $444 million deployed in the second quarter of 2014 was spread more evenly across four deals.

GIC Private was responsible for two of these transactions, backing Metro Pacific Investments’ hospital business in a deal that could be worth $234 million and committing $76.6 million to Century Canning Corporation (CCC) ahead of an IPO. The third came as TPG Capital and Malaysia’s Khazanah Nasional invested $132 million in housing developer 8990 Holdings.

The Philippines accounted for close to one third of Southeast Asia’s $2 billion in private equity investment for the quarter, contributing to a first half total of $3.6 billion, the highest sixth-month total in nearly three years. Needless to say, KKR’s agreed $1.1 billion privatization of Singapore-listed container manufacturer Goodpack was the dominant factor, but the Philippines represents the more interesting trend. The country’s private equity industry is still at a very early stage but this activity gives credence to reports of rising investor interest. What with the widely-expected relaxation on foreign investment restrictions in the banking sector, momentum may continue to gather.

Asia PE investment reached a three-year high of $23.4 billion in the first quarter of 2014 and this was never likely to be matched in the second quarter. Deal value did drop to $16.7 billion but January-June still represents the most active six-month period since the second half of 2010, suggesting that a relatively disappointing 2013 will not be repeated. In addition to Southeast Asia, Australia and China saw an uptick in quarter-on-quarter deal flow and there are snippets worth noting in each case.

The Australian total was predictably buoyed by a big infrastructure deal as Abu Dhabi Investment Authority invested $779 million in Queensland Motorway. Less predictably, the country also saw its largest-ever VC investment as Insight Venture Partners committed $250 million to global marketing specialist Campaign Monitor. The software-as-a-service industry is indeed unconstrained by geography.

In China, the food thesis remains of huge relevance. Four sizeable dairy industry transactions announced since September 2013 will see PE capital used to develop farms with a view to meeting consumer demands for higher quality milk. The most recent of these came in June as Yunfeng Capital and CITIC PE agreed to invest $320.5 million in Mongolia Yili Industrial Group’s livestock subsidiary.

A consortium comprising KKR, Baring Private Equity Asia, Hopu Investments and Boyu Capital also took the food thesis one step further, committing $270 million to COFCO Meat, a hog farm and meat processing plant operator. As with the dairy investments, the PE firms will contribute technology and expertise from overseas in order to boost quality and capacity.

Private equity investments by type

Source: AVCJ Research

1Q2012 2Q2012 3Q2012 4Q2012 1Q2013 2Q2013 3Q2013 4Q2013 1Q2014 2Q2014

US$

mill

ion

25,000

20,000

15,000

10,000

5,000

0

Start-up/early-stage OtherBuyouts PIPEGrowth/pre-IPO Investments

800

700

600

500

400

300

200

100

Dea

ls

No. of IPOs

Private equity-backed IPOs

Source: AVCJ Research

15,000

12,000

9,000

6,000

3,000

0

80

70

60

50

40

30

20

10

US$

mill

ion

IPO

s

Funds raised (US$ million)

1Q2012 2Q2012 3Q2012 4Q2012 1Q2013 2Q2013 3Q2013 4Q2013 1Q2014 2Q2014

avcj.com | July 15 2014 | Volume 27 | Number 2612

FROM NINTENDO’S SUPER MARIO BROS. all the way through to Sony PlayStation’s Final Fantasy, there was a time when Japan ruled the gaming industry. Microsoft’s Xbox and recent Western successes such as Call of Duty and Grand Theft Auto have dented this dominance, but now developers are looking to new platforms.

Fast-growing mobile app maker Gumi is latest great hope of a resurgent Japan – or at least that’s the hope of Gen Isayama, founder of WiL (World Innovation Lab), which led a $50 million funding round for the company. The round – which included Sega Networks – brings Gumi’s total capital raised to $94 million. The investor roster also features Incubate Fund, East Ventures, DBJ Capital, Nissei Capital, B Dash Ventures, Shinsei Bank and Jafco Ventures.

“I have come across so many Japanese game developers over the past 10 years but Gumi has a unique profile,” says Isayama, who was a partner with DCM in Japan before founding WiL in Silicon Valley last year. “To my mind they have the potential to become the next Nintendo.”

Isayama’s confidence is arguably justified. Gumi is in the process of achieving what so many Japanese mobile game start-ups have failed to do – a breakthrough in the US market. One title in particular, role-playing game (RPG) Brave Frontier, has been a big hit across the Pacific, becoming one of the top 15 bestselling RPGs on the App Store. It previously topped the charts in Japan and Korea.

Gumi was set up in 2007 and has about 10 games under its belt. With an office in Singapore and plans to expand further, it is one the few Japan mobile start-ups – along with Gree and DeNA – to make significant headway overseas.

“If you look at most Japanese mobile start-ups, each one is doing something interesting but I would say around 99% have a very domestic-focused business,” says Isayama.

Despite competition from other investors in Asia and the US, Isayama says that WiL, which

has strong ties to the founding team, was best-placed to support Gumi’s US expansion alongside Sega. “The fact we speak the same language also made things easier,” he adds.

This is not Gumi’s first attempt at international expansion. In 2012, the company ranked top

of a Deloitte list of Japan’s fastest-growing tech start-ups, with revenues expanding 3,950%. An office opened in the US but then Gumi scaled back. “This was before Brave Frontier,” Isayama says. “If you think about future growth, they will inevitably need a presence in Silicon Valley

and that is our mission.”Now Gumi has the traction – and user base

– it previously lacked, there appears to be little standing between the company and an IPO on first section of the Tokyo Stock Exchange later this year. According to rumors, the offering could be worth as much as JPY100 billion ($1 billion).

THE WORLD HAS SEEN PLENTY OF SELFIES. From dining tables to football matches, there is always someone, arm outstretched and phone in hand, keen to capture a photo of themselves for posterity. It was only a matter of time before mobile apps enabling people to beautify these images emerged.

Nice is a Chinese mobile app that has taken the process one logical step further. It allows users to tag photos of themselves in order to showcase the brands they are wearing. In addition to being uploaded to Facebook and Instagram, selfies find their way to the Nice platform with the Gucci or Starbucks logo also logged for posterity.

A brand-tagging function has been available on Instagram for some time without really taking off. China is a completely different proposition, though. Nice launched last October and has built up a following of more than 2 million registered users who share about 100,000 images each day. One

in 10 of these users are based outside of China. Matrix Partners and Morningside Technologies were suitably convinced and put up $8 million in Series A funding two months ago.

“Our company was set up earlier last year and we wanted to launch a mobile product to address the young demographic. But it has taken time for us to find our market position,” explains

Alex Zhou, co-founder of Nice. Zhou’s previous online ventures

include streetwear magazine Kidulty and e-commerce site Kongdao. He then teamed up with Dapeng Cao, formerly Sina and Baidu, and they created male-focused app KK Shopping – which failed to gain traction – before conceiving Nice. Matrix and Morningside have both provided

assistance since then, notably helping the company create an online community for users to share lifestyle information rather than a pure e-commerce platform selling products.

“China has been seen as a copycat of apps

developed in the US, while Chinese-made products haven’t gained a following overseas. But we think Nice can develop domestically and internationally,” Zhou says.

VY Capital and H Capital recently joined the existing investors in a Series B round worth $20 million. Both are newly-established funds. VY was set up by Xiaohong Chen, ex-China managing partner at Tiger Global, while H is led by Alexander Tamas, previously of DST Advisors.

“We weren’t really looking for capital in this round, rather expansion strategies offered by global VC firms. Chen has invested in almost every leading technology firm in China and Tamas has seen all cutting edge technologies developed in Silicon Valley,” Zhou says.

Nice now supports Facebook and Instagram as well as Chinese platforms Weibo and WeChat as it seeks to broaden its user base. An online chatting function, which groups users who like similar brands, has also been introduced, and new users have increased tenfold since January.

“For us, developing a strong data base is the most important task right now,” Zhou adds.

DEAL OF THE [email protected] / [email protected]

WiL aims high with Japan’s ‘next Nintendo’

Nice targets selfies with style

Japan’s Gumi: Levelling up

Nice: Self-aware

FOR MOST ASIA-FOCUSED GPS THAT WERE once captive units of investment banks, the shadow of their former parent has long since faded. Restrictions on financial institutions as LPs is a problem, but they are already accustomed to life without balance sheet capital.

Morgan Stanley Private Equity Asia (MSPEA) is in a different place; it is still affiliated to a bank. Raising $1.49 billion for its third fund in 2007, MSPEA received $400 million from Morgan Stanley and employees of the bank. The firm launched Fund IV in 2012 knowing that – under the Volcker Rule – the bank share was capped at 3%, or $50 million out of a $1.5 billion target.

Filling the balance sheet hole represents as significant challenge in an already difficult fundraising environment. However, MSPEA announced last week announced a final close of approximately $1.7 billion. Capital from institutional third parties is about 50% higher in dollar terms compared to Fund III.

Having reached a first close in late 2012, MSPEA went into the second phase of the fundraising with a number of deals in the

pipeline. Two investments have already been completed from Fund IV – Korean tissue paper manufacturer Monalisa and India’s Janalakshmi Financial Services – and at least five more are contracted. These include take-private deals for US-listed Sino Gas Holdings and Noah Education.

Chin Chou, CEO of MSPEA, sees take-privates as the most significant development in the firm’s China business in the last 4-5 years. While he expects growth capital deals to remain dominant in the country, he sees privatizations as part of a broader opportunity set. Control transactions are part of this.

“In the past a number of the control deals in the market have been for export-oriented businesses and our preference has been on businesses catering to the domestic market,” Chou tells AVCJ. “Eighteen months ago we acquired control of Hi-24, Beijing’s largest convenience store chain, and there will be more control-oriented deals in China in the new fund.”

Fund IV follows a similar strategy to that of its predecessor, pursing minority and control investments across the consumer, financial services, industrial products sectors, as well as service-related businesses in general. China and Korea will account for 80% of the corpus with the rest deployed mainly in India and Taiwan.

There have been two disclosed investments in Korea in the past two years – Monalisa and restaurant chain Nolboo – while the

acquisition of a construction materials business from a local conglomerate Hanwha Group has been reported but not announced.

“We have done two buyouts in Korea in the last two years of companies facing succession planning issues and we expect these to continue,” Chou says.

“The large conglomerates in Korea also continue to streamline and focus their business objectives and that leads to deal flow involving non-core businesses.”

MSPEA rides out Volcker impact

MSPEA: Life after Volcker

Wider reach to everyone in your organisation

avcj.com site licence allows everyone in your organisation to have instant access to in-depth analysis, real-time news and information on private equity in Asia and beyond. Sign up for an avcj.com site licence now and empower your team with critical information and data to soar above your competitors in Asian private equity.

How does it work?

We will arrange online access for your employees to avcj.com, either with individual passwords or by general access through IP address recognition.

How much does it cost

That depends on how much access you want, but we can customise cost-effective packages to all firms, regardless of size. For more information, contact Sally Yip at +(852) 3411 4921 or email [email protected].

avcj.com

avcj.com | July 15 2014 | Volume 27 | Number 2614

Q: What led to the creation of Ascendent in 2011?

MENG: Chinese private equity has changed significantly since 2004-2005. At that time there were fewer players, and therefore investment banks were key to introducing and brokering deals. However, most international banks didn’t really have much in terms of advisory, as they were mostly focused on IPOs. My M&A team at J.P. Morgan served as sell-side advisors for some of the earliest PE deals. When I moved on to D.E. Shaw in 2007 to start and lead the firm’s Greater China investment business, it was a similar approach. We helped companies think about their issues and opportunities, and then provided capital in combination with advice and solutions. Kevin and I first met when we were both advising CNOOC on the attempted acquisition of Unocal in 2005 – he was at Goldman on the capital markets side and I was on the M&A side. Between 2007 and 2011, we co-invested around $600 million in China PE deals, so we knew each other’s style. Spinning out from D.E. Shaw in 2011, I decided to partner with him.

Q: And the advisory approach still prevails?

MENG: Today’s environment is even more uncertain than a few years ago, so the combination of capital and advice is very powerful. Our strategy is all about having a lot of influence, thinking about what companies want to do and in a lot of cases helping them do it.

ZHANG: The market is maturing and entrepreneurs are becoming more sophisticated. They are

more open to interesting transactions that they wouldn’t have been open to 10 years ago. And then the Chinese economy is slowing. If a company is growing at 40%, all it needs is the cheapest cost of capital; there is not much interested in other opportunities. But as growth slows, even industry leaders must deal with challenges such as rising costs, increasing capital intensity and consolidation. At this juncture, if you show them not only capital but also opportunities such as M&A that offer synergistic combinations and change the competitive landscape, it is very interesting to them.

Q: So you would describe your strategy as different to conventional private equity?

ZHANG: Chinese private equity has seen its good days when everyone was making money, driven mostly by beta plays – GDP growth and multiple expansion. In a slower growth environment and with a lot of dry powder chasing those opportunities, you really have to deliver alpha. Our objective is to deliver attractive risk-adjusted returns. We do that by generating our own ideas and advising Chinese companies on how to accelerate growth. Through that process we develop a trusting relationship with entrepreneurs, which means we get in at reasonable valuations and can structure deals not only towards meeting a company’s capital needs but optimizing our risk-return profile. We stay very involved post-investment, actively managing the portfolio.

MENG: Our approach also differs

from conventional private equity because we look at things from a credit angle and an equity angle. We protect our downside using structured mechanisms but without sacrificing too much of the equity upside. Everyone talks about downside protection but how many of them have really gone through the exercise of loan-to-value, credit, analytics, asset and equity pledges, and enforcements? We are one of few with knowledge and experience in this area.

Q: What are the challenges involved with downside protection in China?

MENG: Downside protection could be as simple as a put option, but then you have to ask if it’s really protected. Is your counterpart a special purpose vehicle or

a person? Is there a personal guarantee next to it and, if so, does the person have sufficient assets? Is the enforcement mechanism strong enough. We take precautionary measures to protect equity pledges – we get pre-signed instruments of transfer with full power-of-attorney allowing us to date and effect the transfer upon a default. But in most cases we have known the company for a long time through the advisory angle. We understand them, we know they are creditworthy, and we are comfortable working with them. A lot of conversations run along the lines of us saying, “Let’s develop this idea together and we will put in money to show we believe in the idea. If things go well, we get some equity upside. If things go really badly, just treat it as a loan and return the money plus some interest.”

Q: So you wouldn’t use protection mechanisms such as ratcheting?

MENG: We don’t like those situations because there is a misalignment of interest – some founders might fudge the accounts rather than face losing 30% of their equity. We do it the other way around. We tell the founder that we think the business is capable of 10-15% growth, and our valuation reflects this assumption. But if we together manage to achieve higher growth we will return equity to him. Downside protection is not a zero-sum game. There is often some kind of trade-off, incentives to get them to return cash sooner rather than later. For example, we might own 40% of a company with a 2x put option after four

INDUSTRY Q&A | LIANG MENG & KEVIN [email protected]

Corporate consiglioreM&A advisors turned PE investors, Liang Meng and Kevin Zhang pooled their experiences at J.P. Morgan, D.E. Shaw and Goldman Sachs to create Ascendent Capital Partners, and pursue a different kind of China strategy

“Downside protection could be as simple as a put option, but then you have to ask if it’s really protected” – Liang Meng

Liang Meng

years and a preferred dividend stream that guarantees us a certain payout until we have covered 1x cost. If capital can be returned earlier we don’t mind reducing the 40% ownership to 37.5%. It is less challenging when interests are aligned and you are giving them money not just to pursue organic growth but do something strategic to maximize shareholder value.

Q: What sort of strategic benefits have you achieved with your portfolio companies?

ZHANG: We have been involved in one take-private of a Chinese company on the Korean Stock Exchange. It is a complicated process and few people have done it before – our deal was announced last May and completed in October and it wasn’t until last week that the remaining minority shareholders finally exited. We invested $54 million in the form of a convertible bond with a

4% coupon and an 18% put option. Our entry valuation is very competitive. But from the entrepreneur’s perspective, he owned 45% and post-privatization his stake has risen to 70% without putting in any additional capital. We have invested and also helped the company make some small acquisitions to enter new areas. We have been working with a bank on an offshore syndicated loan that will extend financing from one-and-a-half years to three years, lowering the risk.

And we are in the process of bringing in one of the company’s largest customers as a strategic investor.

Q: Most private equity firms emphasize the operational side of value creation…

ZHANG: We work with industry leaders and established companies. A food packaging business doesn’t need us to come in and explain how to make a metal can at lower cost. But they might need us to advise on how the company can reposition itself as a multi-product food and beverage packaging company. They might have identified an acquisition target and need help on the transaction, or they might want us to look at their capital structure, not only to lower financing costs but also to match assets and liabilities in order to reduce potential risks. We want to add value in areas where companies most need support

and right now it is not operations.

Q: Doesn’t your strategy – building relationships with the possibility of investing later – limit the number of deals you can look at?

MENG: We can probably do no more than two or three deals each year, but that’s okay. When we launched Fund I we said there would be 7-9 investments in total with a $30-70 million sweet spot. Three years on, we have made five investments and are currently working on a sixth. If you see us doing one deal a month then we have deviated from our strategy. The deals will probably become larger in size but overall number won’t increase much. And you won’t see us opening four offices in China either. It doesn’t make any sense. We don’t need a lot of people but it is an advice- and intelligence-intensive strategy – there is a lot of dialogue with companies.

LIANG MENG & KEVIN ZHANG | INDUSTRY Q&A [email protected]

Kevin Zhang

The AVCJ Private Equity and Venture Capital Reports provide key information about the fast changing Asian private equity industry. Researched and compiled by AVCJ’s industry leading research team, the reports offer an in-depth view of private equity and venture capital activity in Asia Pacific, as well as in major countries and regions including Australasia, China, India, North Asia and Southeast Asia. Each AVCJ Report includes the latest statistics and analysis, delivering insights on investments, capital raising, sector-specific activity. The reports also feature information on leading companies and business transactions. For more information, please contact Sally Yip at +(852) 3411 4921 or email [email protected].

AVCJ, your Asian private equity information source.

avcj.com

Market intelligence on Asian private equity? AVCJ is the solution

Scan to find out more about the regional reports

REPOSITIONING ASIAN PRIVATE EQUITY TO THE WORLD

Singapore 2014 4th Annual Private Equity & Venture Forum

17-18 July • Four Seasons Hotel, Singapore

SIGN UP NOW and meet 250+ senior representatives from the following leading institutions:

Registration: Pauline Chen T: +852 3411 4936 E: [email protected]: Darryl Mag T: +852 3411 4919 E: [email protected]

Contact us

Asia Series Sponsor Co-Sponsors Scan the QR code with your

mobile phone to register now!

Join your peers

Tweet #avcjsingapore

avcjsingapore.com

1337 Ventures 57 Stars LLC Aberdeen Asset Management Asia Advantage Partners, LLP Adveq Management Allen & Gledhill Allianz Capital Partners Allianz Private Equity Alpinvest Partners Ancora Capital Management Anthem Asia Ascendas Land Avista Advisory Partners Axiom Asia Private Capital Bain Capital Asia, LLC Bank of Singapore Baring Private Equity Partners India Beluga Capital BlackRock Private Equity Partners Bloomberg LP BNP Paribas Wealth Management BPI Capital Corporation Campbell Lutyens CapAsia Catcha Group Celadon Capital CHAMP Private Equity Citi CITIC Capital Clifford Chance Collas Crill Coller Capital Cooley LLP Cornerstone Family Office CPPIB Asia Inc Credit Agricole Creador CS Partners DBJ (Development Bank of Japan) DBS Bank

Debtwire DEG Representative Office Singapore DFDL Dragon Pearl Partners Eagle Asia Partners Eagle Asia Partners Eastspring Investments EFG Fund Services EMIS Ernst & Young Solutions LLP Everstone Capital Fedesa Asia Advisory Fenox Venture Capital Garage Technology Ventures LLC GIC GIC Special Investments Golden Gate Ventures HarbourVest Partners Headland Capital Partners Hermes GPE Hogan Lovells Lee & Lee ICICI Investment Management IIML Fund Managers Infocomm Development Authority of Singapore (IDA) Infocomm Investments IPP Financial Advisers iSEACO investment JP Morgan Asset Management Jungle Ventures KKR Asia KKR Singapore Private KPMG Kroll KV Asia Capital L.E.K. LGT Capital Partners Lunar Capital Management Maples and Calder

Marsh Marsh Insurance Brokers Mergermarket Ministry of Economy and Finance Mitsui Global Investment Monetary Authority of Singapore Morgan Creek Capital Management NABARD National Research Foundation National University of Singapore Navis Capital Partners New Forests Asset Management NewQuest Capital Partners Norinchukin Bank Northstar Northstar Group Northstar Silicon Island NTUC Income Insurance Co-operative Ogier Fiduciary Services (Hong Kong) Oman India Joint Investment Fund Ontario Teachers’ Pension Plan (Asia) Orangefield Group ORIX Investment and Management Private Pacific Equity Partners PineBridge Investments PNB-SBI Asean Gateway Investment Management Primavera Capital Group Principle Partners Proskauer Rose PT. Nusantara Infrastructure Pyramid Private Equity Partners Red Dot Ventures RHTLaw Taylor Wessing LLP Risk Capital Advisors Riverside Asia Partners S&P Capital IQ Samsung C&T SanTeh Philanthropy Foundation

Saratoga Capital SBI Islamic Fund Brunei Sequoia Capital Singapore Institute of Technology Singapore Management University Singapore Venture Capital & Private Equity Association SK China Southern Capital Group Standard Chartered Bank StepStone Sumitomo Mitsui Banking Corporation Suzhou Chenghe Venture Capital Company TATA Capital Markets Temasek Temasek International The Blackstone Group The Carlyle Group The Citi Private Bank The Norinchukin Bank Thomson Reuters Tiger Healthcare Private Equity Tricor IAG Fund Administration Tricor Singapore UBS Investment Bank United Overseas Bank (UBO) Usaha Tega Sdn Bhd Venture Capital Trust Fund VI Group Vickers Venture Partners Vistra Fund Services Webbe International Asia Wendel Singapore White & Case Wilshire Private Markets Woori Investment & Securities Asia

… and many more!

For the latest programme and speaker line-up, please visit avcjsingapore.com

7,843

THE EVENT STARTS ON THURSDAY!