Embed Size (px)

Citation preview

VARIABLE ANNUITY (“VA”) PRODUCTS PRICING CHALLENGES AND ISSUES

10th Annual Equity Based Insurance Guarantee Conference (Chicago)

Session 1B: November 17, 2014 (1045 – 1215 hours)

Amit Ayer

Executive Summary Tactical challenges and issues with VA pricing

Elements of VA Pricing Framework - Tactical

Principle Description Impact Rider

Charge

Reserves

/ Capital Profitability Hedging

A Presence of

living benefit

Presence of living benefit rider places increased pressure on

adequate pricing framework

B Risk-neutral

and real-world

frameworks

VA pricing framework is cumbersome because it must be

performed using risk-neutral and real world frameworks

C Multiple risk

management

incentives

Heterogeneity in risk management incentives necessitates VA

pricing functions to be agile and flexible

D Accounting

asymmetries

on capital

Heterogeneity in accounting frameworks necessitates VA

pricing functions to be agile and flexible

E Projection of

hedging in

pricing

Reflecting hedging in pricing remains an arduous process with

a range of practices

F Pricing and

capital

markets

Even robust pricing of VAs cannot withstand prolonged

markets with high realized volatility

2 Significant impact to pricing Insignificant impact to pricing

Executive Summary Strategic challenges and issues with VA pricing

Elements of VA Pricing Framework - Strategic

Principle Description Impact Rider

Charge

Reserves

/ Capital Profitability Hedging

G Pricing

Metrics

Lack of convergence around pricing metrics makes VA pricing

process more difficult

H Scrutiny on

pricing

targets

VA writers are able to meet pricing targets, but greater scrutiny

on pricing targets is warranted

I VA

disclosures

The deficiencies in VA disclosures should be further

investigated and improved

J Volatility

managed

funds

Pricing of target volatility funds requires care and impact on

statutory requirements should be further analyzed

K VA Exchange

offers

Exchange offers have demonstrated success across VA

markets to eliminate liabilities from balance sheet through

various offers

L VA

reinsurance

market

Rejuvenated VA reinsurance market offers more flexibility with

regard to VA pricing frameworks

3 Significant impact to pricing Insignificant impact to pricing

Agenda

Interdependencies between VA pricing components

Challenges and Issues with VA pricing

Lack of convergence around VA pricing metrics and anomalous

pricing results

Shortcomings with GAAP/IFRS ROE profitability metrics

Reactions to VA pricing difficulties

Questions and answers

4

INTERDEPENDENCIES BETWEEN VA PRICING COMPONENTS

Interdependencies between VA pricing components require an optimal risk-return balance

Background Traditional product pricing exercise searches for premium rate that meets desired profit target

Despite same fundamental objective for variable annuities, VA pricing exercise is much more

complicated because of presence of living benefit rider

Four elements of VA pricing process are intertwined and influence each other

• Hedging implemented to reduce

economic risk, and directly affects

the reserve / capital requirements

and profitability

• Warrants analysis of not just

expected value but also tail events

• Economic, GAAP and statutory

considerations

• Sensitive to market conditions and

policyholder behavior

• Warrants analysis of not just

expected value but also tail events

• Profitability affected by interest

earned on reserves / capital and

changes in reserves / capital levels

• Many companies opt for stochastic

projections of reserves / capital

• Rider charge set with long-term view

• Industry unlikely to factor to re-

setting GLB rider charge on

frequent basis

Reserves / Capital Hedging

Rider charge

Profitability

6

CHALLENGES AND ISSUES WITH VA PRICING

Presence of living benefit rider places increased pressure on adequate pricing framework

Living benefit rider materially changes risk profile of base VA contract

Dimension VA Base Contract Living Benefit Rider

Contribution

to risk of

rider

1 Profitability • Without the living benefit rider, profitability

relates to accruing fees that are adequate

to cover expenses and death claims

• Driven primarily by performance of underlying

investments

2 Risk profile

• Roughly equivlavalent probability of upside

loss and gain since base product passes

most of investment risk to policyholders

• No embedded derivatives

• Increases risk of making large guaranteed payments,

with low upside gain

• Embedded derivatives

3 Drag on separate

account value

• M&E fee only, with no volatility in separate

accounts

• Increased drag on account value from rider fees and

potential downward movements in separate

accounts

4 Policyholder

behavior • Minimal

• Living benefit rider contributes higher degree of

uncertainty around policyholder behavior

5 Reserve and

capital

requirements

• Dependent on equity long term expected

volatilities for reserve and capital charges

• AG43 and C3 Phase-II requirements (while

principles based) are higher in presence of living

benefit rider

6 Risk

Management • Typically not hedged

• Cost of hedging (economic, GAAP, statutory, or

combination)

Significant impact to risk profile Insignificant impact to risk profile

A B C D E F

VA pricing framework is cumbersome because it must be performed using risk-neutral and real world frameworks (1/2)

Common approach to risk neutral pricing in VA pricing (illustrative)

9

0

20

40

60

80

100

120

140

160

180

Ba

sis

Po

ints

(b

ps

)

Real world pricing

(reserves / capital)

Cost of Hedging

PAD / Profit

VA

pro

du

ct

(rid

er

fee

an

d b

as

e c

on

tra

ct)

1

2

3

4

Risk neutral valuation

• Almost all companies make a provision for the risk

neutral cost of the rider in pricing

• Business can be priced at today’s market conditions, the

product could be sold for up to two years

– Profitability results for business priced today are

by definition already stale tomorrow

1

Note – reflection of hedging in VA pricing is covered in Issue #5

A B C D E F

Risk Neutral Pricing /

“Economic Hedge

Cost”

Observations

• Two primary approaches in generating risk-neutral

scenarios

– Use current market conditions to develop risk-

neutral scenarios to calculate rider cost

– Use long-term estimates to generate risk-neutral

scenarios to calculate the rider cost

• Three methods used to set implied volatility for later

tenors

– Grade from longest-credible market-observable

tenor to target value

– Hold level at longest-credible market-observable

tenor

– Use level volatility throughout (e.g., long term

estimates)

VA pricing framework is cumbersome because it must be performed using risk-neutral and real world frameworks (2/2)

Common approach to real-world pricing in VA pricing (illustrative)

10

0

20

40

60

80

100

120

140

160

180

Ba

sis

Po

ints

(b

ps

)

Real world pricing

(reserves / capital)

Cost of Hedging

PAD / Profit

VA

pro

du

ct

(rid

er

fee

an

d b

as

e c

on

tra

ct)

1

2

3

4

Real-world pricing

Cost of hedging is calculated using a variety of methods,

implemented as en expense throughout base product

pricing (cannot lock in hedging costs today)

PADs are an additional buffer for deviations away from

expected loss (i.e., unexpected losses, which is

consistent with definition of capital)

Reserves / Capital Description

1 Less refined • Develop set of factors that may vary on product

feature, duration, ITM

2 More refined

• Real-world scenarios to project reserve / capital

requirements

• Open considerations: number of scenarios, time

steps

3

Note – reflection of hedging in VA pricing is covered in Issue #5

4

A B C D E F

Risk Neutral Pricing /

“Economic Hedge

Cost”

“Expense”

items Description

1 Economic

Hedge Cost

• Incorporated as an “expense” in base product pricing

through real-world scenarios

2 Hedge

Effectiveness

• Provision for hedge ineffectiveness by allowing portion

of real-world claims to flow through their integrated base

product and rider pricing

2a

2b

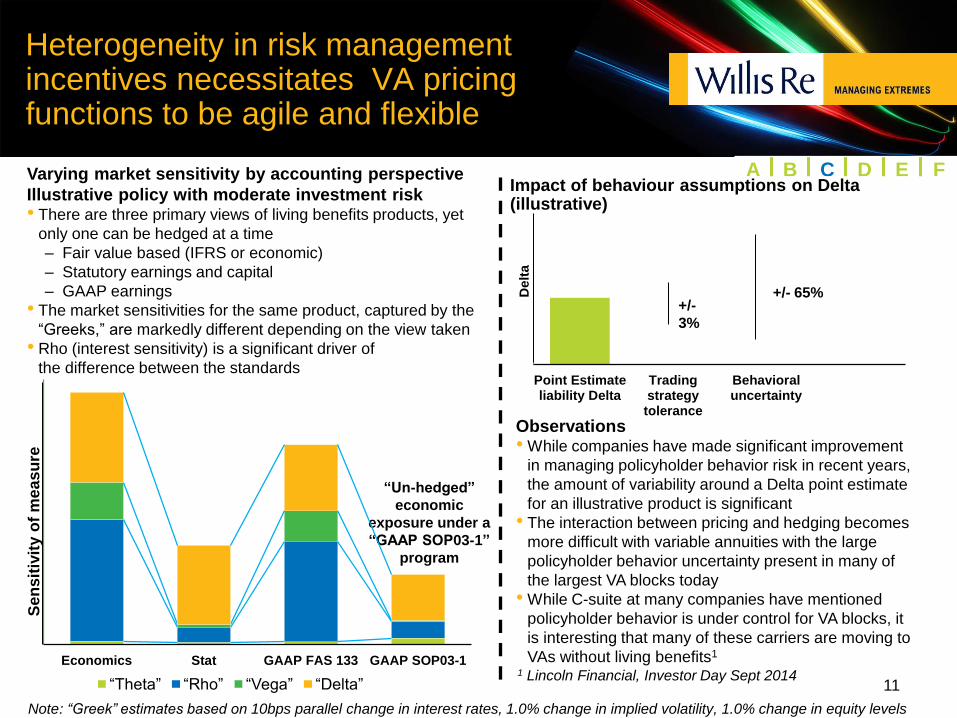

Varying market sensitivity by accounting perspective

Illustrative policy with moderate investment risk • There are three primary views of living benefits products, yet

only one can be hedged at a time

– Fair value based (IFRS or economic)

– Statutory earnings and capital

– GAAP earnings

• The market sensitivities for the same product, captured by the

“Greeks,” are markedly different depending on the view taken

• Rho (interest sensitivity) is a significant driver of

the difference between the standards

Heterogeneity in risk management incentives necessitates VA pricing functions to be agile and flexible

11

A B C D E F

Note: “Greek” estimates based on 10bps parallel change in interest rates, 1.0% change in implied volatility, 1.0% change in equity levels

“Un-hedged”

economic

exposure under a

“GAAP SOP03-1”

program

Point Estimateliability Delta

Tradingstrategytolerance

Behavioraluncertainty

Delt

a

+/-

3%

+/- 65%

Observations • While companies have made significant improvement

in managing policyholder behavior risk in recent years,

the amount of variability around a Delta point estimate

for an illustrative product is significant

• The interaction between pricing and hedging becomes

more difficult with variable annuities with the large

policyholder behavior uncertainty present in many of

the largest VA blocks today

• While C-suite at many companies have mentioned

policyholder behavior is under control for VA blocks, it

is interesting that many of these carriers are moving to

VAs without living benefits1

1 Lincoln Financial, Investor Day Sept 2014 Economics Stat GAAP FAS 133 GAAP SOP03-1

Se

nsit

ivit

y o

f m

ea

su

re

“Theta” “Rho” “Vega” “Delta”

Impact of behaviour assumptions on Delta (illustrative)

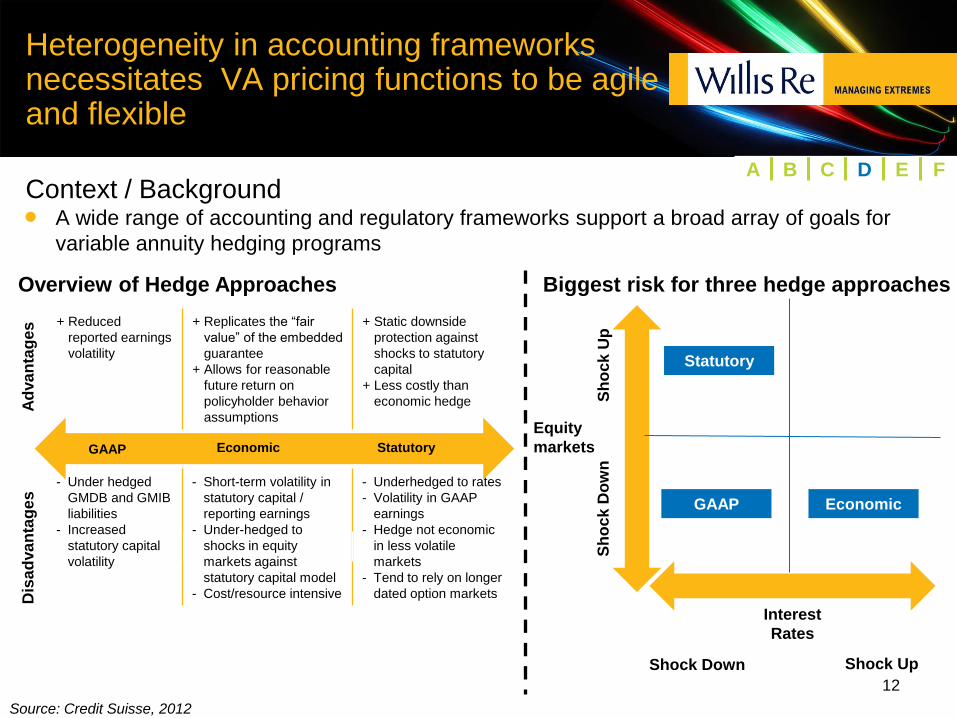

Heterogeneity in accounting frameworks necessitates VA pricing functions to be agile and flexible

Context / Background A wide range of accounting and regulatory frameworks support a broad array of goals for

variable annuity hedging programs

12

Overview of Hedge Approaches

GAAP Economic Statutory

+ Reduced

reported earnings

volatility

+ Replicates the “fair

value” of the embedded

guarantee

+ Allows for reasonable

future return on

policyholder behavior

assumptions

+ Static downside

protection against

shocks to statutory

capital

+ Less costly than

economic hedge

Ad

va

nta

ges

- Under hedged

GMDB and GMIB

liabilities

- Increased

statutory capital

volatility

- Short-term volatility in

statutory capital /

reporting earnings

- Under-hedged to

shocks in equity

markets against

statutory capital model

- Cost/resource intensive

- Underhedged to rates

- Volatility in GAAP

earnings

- Hedge not economic

in less volatile

markets

- Tend to rely on longer

dated option markets Dis

ad

va

nta

ge

s

Source: Credit Suisse, 2012

Biggest risk for three hedge approaches

Equity

markets

Sh

ock

Up

S

ho

ck

Do

wn

Shock Down Shock Up

Statutory

GAAP Economic

A B C D E F

Interest

Rates

FAS

SOP

Insurer A Insurer B

Additional

capital

Accounting differences for same product can create pricing pressures due to distortions in capital outcomes

Context Two variable annuity contracts with same liabilities

One is accounted for using FAS 133

Other is accounted for using SOP 03-1

13

Hypothetical GAAP liability under

interest rate stress scenario

GAAP Liability value

FAS 133: carrying at fair value

SOP 03-1: carrying at “least present value” of

cash flows

FAS 133: market interest rate assumption

SOP 03-1: “real world” interest rate

assumptions

SOP 03-1 improves capital position SOP 03-1 reduces interest rate sensitivity

FAS

SOP

Insurer A Insurer B

Additional

liabilities in

stress scenario

A B C D E F

Reflecting hedging in pricing remains an arduous process with a range of practices

Reflection of hedging in pricing models is not uniform across

insurers Hedging approach generally impacted by a number of factors, including:

– Accuracy of results

– Complexity of implementation, validation, inputs and analysis

– Computational demands (software and hardware)

14

Range of

practices Description Sophistication Accuracy

1 Reinsurance • Assume that portion of claims along real world projection is reinsured

2 Change in

Liabilities • Hedge payoff is some assumed percentage of change in liability

3 Proxy of hedge

transactions

• Make Black-Scholes approximation on value of hedge assets along

real world scenario

4 Explicit projection

of hedging

Transactions

• Full nested stochastic projection

A B C D E F

Even robust pricing of VAs cannot withstand prolonged markets with high realized volatility

Disconnect exists between real world scenarios used to project

statutory balance sheet items and risk neutral scenarios used to project

change in market value of hedges

Higher implied volatility levels will increase the cost of hedging

associated with Delta hedging

15

A B C D E F

Statutory requirements for GMAB policy – impact of dynamic hedging with index futures

0

20

40

60

80

100

120

140

Unhedged 10% vol 15% vol 20% vol 25% vol 30% vol 35% vol

Sta

tuto

ry r

eq

uir

em

en

t

AG43 Reserves Required Capital

Observations • AG43 requirement increases

with Delta hedging strategy, requiring no required capital.

• AG43 requirement with a Delta hedging strategy displays high sensitivity to implied volatilities, as Delta positions are sensitive to changes in implied volatility.

LACK OF CONVERGENCE AROUND VA PRICING METRICS AND

ANOMALOUS PRICING RESULTS

Lack of convergence around pricing metrics makes VA pricing process more difficult

General observations Rider cost coverage, statutory IRR, and statutory VNB margins are the most prevalent

primary metrics

Statutory earning / capital strain and return on assets (ROA) are other significant metrics

While there is not one “correct” VA pricing metric, the variability of metrics across the industry

is expansive

17

Source: Towers Watson 2013 Pricing Survey

0

2

4

6

8

10

12

Rider costcoverage

Statutory IRRon capital

Statutory VNBmargins

Statutoryearnings/capital

strain

Marketconsistent VNB

ROA ROE Statutorycapital/EAR

GAAP ROE typically

promulgated in

investor disclosures

Rider charge /

hedge cost

G H I J K L

VA writers are able to meet pricing targets, but greater scrutiny on pricing targets is warranted

General observations Companies reported significant

differences between pricing targets and

minimum tolerable levels

Companies pricing on a GAAP/IRFS

basis tended to have higher target ROEs

than overall industry statutory IRR figures

Companies are more apt to accept lower

hedge cost minimum due to low interest

rate environment

GAAP/IFRS ROEs are often inflated

(discussed during next section)

18

Source: Towers Watson 2013 Pricing Survey

GAAP/IFRS Pricing Targets and Minimums

Statutory Pricing Targets and Minimums

G H I J K L

0.0%

5.0%

10.0%

15.0%

20.0%

15th Mean 85th

US GAAP/IFRS ROE - Target

US GAAP/IFRS ROE - minimum tolerable

0.00%

5.00%

10.00%

15.00%

20.00%

15th Mean 85th

Statutory IRR on Capital - target

Statutory IRR on Capital - minimum tolerable

SHORTCOMINGS WITH GAAP/IFRS ROE PROFITABILITY METRICS

Disconnected

from liability

valuation

Issues with GAAP VA general account balance sheet

GAAP variable annuity general

account balance sheet

20

Commentary • Inconsistent accounting treatment for

identical economic cash flows

• GMIB/GMDB vs. GMWB

• Rider vs. base contract

• Inconsistent assumptions across different

companies

• DAC mean reversion assumptions

• Different assumptions around

application of FAS 157

• Lack of transparency as to value and in

some cases the performance of the hedge

position

• Little transparency around “sources of

earnings”

• Inconsistent definition of where results

appear (Net Income vs OCI)

FAS 133 guarantees

0

200

400

600

800

1000

1200

Assets Liabilities

DAC

GAAP

value of

guarantee

fees

Net MV

hedge

assets

SOP 03-01

guarantees

Valuation

based on

non-market

assumption

is at odds

with an

economic

viewpoint

Assumptions

locked in at

issue; relies

on mean

reversion

G H I J K L

Background on VA “opaqueness” around variable annuity writers

21

The Insured Retirement Institute's study found a lack of disclosure

among annuity manufacturers around their investment hedging

strategies is depressing stock valuations

UBS Securities Managing Director Andrew Kligerman

– “Investors want to know more about the effectiveness and cost of hedging, the

sensitivity of VA products to equity markets and interest rates, and where excess

capital is going”

– “Clearly greater transparency is needed in the industry, which will improve investors’

perception as to the sectors’ strength and unlock capacity for growth”

Failing to meet investor expectations around transparency is largely due

to companies viewing their strategies as proprietary, thus providing full

transparency may place companies at competitive disadvantage

G H I J K L

Articulation of “Opaqueness” Discount

• U.S. life insurers continue to trade at material discounts to

reported GAAP book value and exhibit low price / book ratios

compared to rest of the financial services industry

22

Source: Factset, company reports, UBS (6/30/12)

G H I J K L

Major deficiencies in current VA disclosures

Deficiency Description Impact

1 Little transparency

into the value of

new business

• Provide little visibility into new business profitability

• Insurers do not communicate the underlying capital markets

assumptions behind these stated ROEs

• Full disclosures could help investors

understand that they have cheaper, and

certainly more transparent, vehicles to take

these types of capital markets positions

2 Performance of the

business over time

cannot be tracked

• In an attempt to foster greater understanding of their financial results,

many insurers have introduced modified earnings definitions that

leverage existing GAAP calculations

• Modified definitions are still rooted in GAAP concepts with all

attendant shortcomings.

• Adjusted performance measures have

often left investors even more confused

and skeptical of companies’ assertions of

satisfactory VA performance

3 Lack of credibility

of true tail risk

protection

• During the financial crisis, some insurers with large VA exposures

suffered substantial capital calls forcing them to raise capital when

valuations were at a trough.

• Current disclosures do not provide

investors adequate assessment of whether

a given business is well protected against

such ill-timed capital calls going forward.

4

Disconnect between

economic

valuations and

GAAP and Statutory

frameworks

• Price to GAAP Book multiples for valuation benchmarks have

limitations

– Inconsistent valuation of liabilities

– Asset valuations geared to capital markets (not all DAC assets

are created equal)

• The framework can leads to instances

where risk management decisions can

inappropriately influence reserve levels,

with the effect that reserves can increase

as a result of more hedging

G H I J K L

Elements of better VA disclosures

In order to address these issues, a framework for better VA

disclosure needs to accomplish four things:

24

Area of Improvement Description

1 Prove new business written is

profitable

• Portray new business profitability through objective metrics that can be compared across

companies and linked to overall capital efficiency goals

2 Demonstrate the effectiveness of

hedging

• Allow the assessment of how much slippage has incurred between the hedge portfolio and the

liability target, and how much unhedged positions have moved

3 Support valuation of the in force

business

• Provide pertinent information to investors to better assess the risk-adjusted economics of the in-

force to inform valuations

4 Investors’ dislike for VAs is

indiscriminate

• Establish that under harsh, yet conceivable, stress scenarios, the combination of hedging, re-

insurance and other balance sheet resources is sufficient to protect key capital ratios

These disclosures should improve transparency to the financial

performance of VA blocks and enable investors to make informed

judgment on proper valuation and ultimately reduce the

opaqueness discount.

G H I J K L

REACTIONS TO VA PRICING DIFFICULTIES

Pricing of target volatility funds requires care and impact on statutory requirements should be further analyzed

26

Volatility managed funds and other new product features are now

common feature to reduce benefit cost and/or reduce challenges

associated with hedging

Dimension Benefits of volatility managed funds Considerations of volatility managed funds

1 Cost of

guarantee

• Potential for moderate reduction in economic losses

• Downside protected from fund rebalancing mechanisms,

preserving account value and lowering claims

• Cost of guarantee lowered, but heavily dependent on

algorithm of volatility managed fund

2 Statutory • Minimal • Impact on statutory requirements is minimal compared to

impact on economics

3 Hedging • Delta sensitivity is lowered markedly with volatility

managed funds

• Material reduction in Vega exposure offers strong benefits

from risk management standpoint

G H I J K L

Case study parameters on volatility managed funds

Modeling of rebalancing strategies

(static versus historical volatility)

Static strategy – asset allocation between equity and bond is fixed

(75% equity 25% bond) at each time step

– equity return >> bond return, sell equity and buy

bond

– bond return >> equity return, purchase equity

and sell bond

“Exponentially Weight Moving Average” – allocation between equity and bond depends on

historical annualized rolling portfolio volatility

– weighting of more recent returns more heavily

(exponentially weighted)

– at each time step, historical annualized volatility

is compared to a target volatility (15%)

VIX

– Based on stochastic projection of VIX index

27

Model specifications

Interest rate Two-factor Hull-White

Volatility Heston

Projection period 40 years

Rebalancing frequency Monthly

*Correlation between equity and interest rates

Product specifications

Issue age 55

Starting AV $100,000

Rollup rate 3%

Rollup frequency Monthly

Ratchet Annually for 10 years

Withdrawal rate 5%

Contract fee 1.81%

MER fee 0.85%

G H I J K L

Impact of volatility managed strategies on Greek sensitivities

28

-$40

-$20

$0

$20

$40

$60

$80

$100

Reserve Delta Reserve Gamma Reserve Rho Reserve Vega

Vega changes most materially relative to a static strategy

Static EWMA VIX

Greek Potential impact of target volatility strategies

Delta • Reduction in dollar Delta • Less transactions in equity futures, reducing transaction costs and cost of hedging

Gamma • Reduction in dollar Gamma for VIX strategy • Mitigate hedge breakage during market volatility (Gamma or gap risk is typically not hedged)

Rho • Reduction in dollar Rho • Less transactions of interest rate swaps/Treasury futures in low interest rate environment

Vega • Significant reduction in Vega • Reduce need to enter into long dated puts or variance swaps

G H I J K L

Exchange offers have demonstrated success across VA markets to eliminate liabilities from balance sheet through offers

29

Assessment of exchange offer target

Size / Homo-geneity

Mitigating adverse selection

Variance in economic vs

perceived value

Overall assessment

for offer target Commentary

Old

er

des

ign

s

Guaranteed Minimum Death Benefit

• Subject to anti-selection if policyholders have non-uniform health status • Typically have low perceived value compared to economic value, in

particular for enhanced death benefits • Enhanced death benefits are excellent offer targets

Guaranteed Minimum Accumulation Benefit

• Relatively homogeneous, with low expected lapse rates • Low perceived value compared to intrinsic value • Benefits that are past surrender charge and are close to expiry are

excellent offer targets

Mo

de

rn d

es

ign

s

Guaranteed Minimum Withdrawal Benefit (non-lifetime)

• Relatively homogeneous, typically return of premium • Lower perceived value than lifetime withdrawal benefit

Guaranteed Minimum Income Benefit

• Not homogeneous, as older regimes require election of annuitization not present in modern designs

• Target older regimes of income benefits that require election of annuitization, as perceived value is likely lower compared to more recent regimes

Guaranteed Minimum Lifetime Withdrawal Benefit

• Variety of designs makes product heterogeneous • Highly lapse supported product makes mitigating adverse selection difficult • High economic values (rich features) and high perceived values (lifetime

income desired) make for poor offer targets

Significant characteristics across dimension Some characteristics across dimension Minimal characteristics across dimension

G H I J K L

Rejuvenated VA reinsurance market offers more flexibility with regard to VA pricing frameworks

30

Markets Description

1 Reinsurers

• Highly rated reinsurers are increasingly inquisitive about VA risks due to following reasons:

– Improve transparency around policyholder behavior frameworks

– Improved transparency around GAAP/IFRS profitability targets

– Emphasis on “sustainable products” with continued emphasis on volatility managed funds that afford policyholder

up-side

• Increased potential for diversification for reinsurers

• Most of the broader reinsurance market we have spoken with has expressed interest in variable annuity products

2 Banks

• Increased transparency being impetus for increased demand to take on risks in VA contracts

• Union Hamilton / Wells Fargo reinsurance deal for one of Lincoln’s largest living benefit rider started in 2013

• Banks have expressed similar inquisitions into taking on VA risks

The increased demand for VA reinsurance will certainly alter the VA

product development and / or pricing landscape

G H I J K L

APPENDIX

Surrender Charge

The standard cash flows involved in a variable annuity contract are depicted below

Variable Annuity – key cash flow

diagram

32

Variable Annuity – key cash flow descriptions

Cashflow Description

Initial

Commission

• Paid by insurer to adviser at policy issue

• Typically ~ 5% of deposit

Trailer

Commission

• Paid by insurer to adviser in Years 2+ while business is

inforce

• Typically 0.5% – 1%. May be a function of deposit or AV

Investment

Management

Fee

• Fee charged for the management of the funds

in policy

• Typically 150 – 200 bps of AV

• Investment manager shares IMF with insurer

Insurance

charge

• Sometimes called M&E

• Typically 10 – 20 bps of AV

Rider charge • Fee to support rider

• Ranges between 50 – 100 bps of GV

Admin charge • Fee for contract admin; usually $30

Surrender

charge

• Paid by policyholder to insurer in the event of lapse (to

compensate for commissions paid)

• Typically 7 – 8%; declining by 1% pa

Separate

Account

Policyholder

Investment manager

Advisor

General

Account

Deposit

Commission

(Initial +

Trailer)

IMF = Investment

Management Fee

IMF

Insurance charge

Administrative Charges

Rider charge

Expenses

(e.g.,

Marketing,

Maintenance)

Revenue

sharing

Dimension Description Solution Focal

Point

1 GLB rider charge • Adequacy of GLB rider charge should be

addressed on an on-going basis • Risk neutral valuation

2 Profitability of

contract

• Contract profitability should be analyzed

through stochastic scenarios with focus on

both mean and tail results

• Stochastic simulation, with focus across variety of

CTE(x%)

3 Reserve / Capital

requirements

• Impact of reserve and capital requirements

should be integrated into profit analysis of

base contract

• Utilize inner loop functionality, using real world

scenarios to determine capital adequacy

4 Impact of hedging • Hedging impact should be analyzed in profit

analysis

• Variety of approaches available, with most

sophisticated being inner-loop nested stochastic

scenarios to simulate payoff of hedge assets

5 VA reinsurance

market

• With increased demand for VA reinsurance

solutions, pricing frameworks should

understand landscape of reinsurers and

banks in market

• Reinsurance can help reduce tail risk or diversify

existing VA block of business

Elements of pricing framework will help companies maintain profitability in variety of economic scenarios

Robust VA pricing framework will help companies maintain profitability in

variety of economic scenarios

33 Significant impact to pricing Insignificant impact to pricing

Today, the most common type of guarantee is the Guaranteed Minimum Withdrawal Benefits (GMWB) and Income Benefit (GMIB), which are similar

Guarantee description Insurer provides policyholder with a guaranteed withdrawal amount that never declines and

continues for life

Insurers incur guarantee claims equal to all withdrawals once the account value is

exhausted

Withdrawals can be fixed in number (e.g., 20 withdrawals permitted for 5% withdrawal rate)

or allowed for the lifetime of the insured

ROP GMWB – Policyholder taking regular withdrawals

Age /Time

Withdrawals incur

guarantee claims Withdrawals reduce account

value

Strong market performance can

increase account value…

…but persistent withdrawals

tend to reduce it over time

Policyholder withdrawal

from account value

ROP benefit

base

Policyholder withdrawal

funded by insurer (i.e., claim) Account value

Consistency of VA guarantee valuation

Issue / context Currently, FAS 133 is used for valuation of most Guaranteed Minimum

Withdrawal Benefits (GMWB) and Guaranteed Minimum Accumulation Benefits (GMAB), while SOP 03-01 is used for all other GMxBs

– FAS 133 produces valuations more consistent with economics, larger in magnitude and more sensitive to market changes

– SOP 03-1 produces valuations that are starkly different than the economics, smaller in magnitude and less market-sensitive

Two VA contracts with highly similar risk and value characteristics could receive very different values in the stress test

Outline of alternatives This could create significant differences in stress test results for two insurers with

similar long-run risk and value profiles

35

Status quo Apply market consistent treatment for all VAs

Description • FAS 133 for valuation of most GMWBs and GMABs, SOP

03-1 for other GMxBs

• Fees are not capitalized

• FAS 133 for all VAs

• Fees are not capitalized

Pros (+) /

Cons (−)

+ Consistent with current GAAP accounting framework

– Inconsistent treatment of liabilities with similar risk profiles

– SOP 03-1 valuation is inconsistent with “economics”

+ Consistent accounting treatment of all VAs

+ Aligned with actual “economics”

– Requires additional work by supervised insurers

– Relies on unaudited financials

A B C D E F

Prove new business written is profitable

Provide the product’s ROE if full capital markets hedging were

utilized (in other words an ROE that is not geared to capital

market risks, or “fully hedged” ROE), in addition to the ROE

using their own individual hedging strategy, across a number of

market scenarios

36

Interest Rate Scenario Spread Scenario Equity Scenario ROE – hedged as

planned

ROE – fully

hedged

June 2012 rates frozen for 5

years then rising 50 bps per

year across term spectrum

Single A staying at 100 bps above

Treasury

0% p.a. …. ….

2% p.a. ….

4 % p.a. ….

June 2012 rates frozen until June

2014, then rising by 1% p.a. for

10 yrs, then frozen again

Single A staying at 100 bps above

Treasury

0% p.a. ….

2% p.a. ….

4 % p.a. ….

Single A widening to 150 bps above

Treasury by 2014 …. ….

Interest rate term structure

remains frozen at current 2012

levels

Single A staying at 100 bps above

Treasury

0% p.a.

2% p.a.

4 % p.a.

G H I J K L