Embed Size (px)

Citation preview

David Casey Eastern Star Gas Limited

ASX Small to Mid Caps Grand Hyatt Hotel, New York

Narrabri CSG Project Update

26 February 2009

David Casey, Managing Director

Australian CBM Industry

ASX Small to Mid Caps Presentation - Grand Hyatt, New YorkNarrabri Coal Seam Gas Project26 February 2009

4

Australian CBM Industry Update

Geographic Spread of CBM IndustryGeographic Spread of CBM Industry

ESG

Origin-Conoco

QGC-BG

Santos-Petronas

Arrow-Shell

AGL

Pure Energy

Other

Industry ObservationsIndustry Observations

CBM potential exceeds Queensland market

Multiple LNG projects proposed for Queensland

Value of Australian CSG industry recognised:

- BG Group US$4B takeover of QGC.

- ConocoPhillips US$8B for 50% of Origin Energy

- Petronas US$2.5B for 40% of Santos CSG.

- Shell US$0.6B for 30% of Arrow Energy acreage.

- BG Group now bidding US$0.6B for Pure Energy

NSW potential now being realised

ESG has Largest Acreage on the East CoastESG has Largest Acreage on the East Coast

0.671.35 1.65

0.68 0.77 0.74

1.88

0.77 1.00

3.17

0.400.00

1.00

2.00

3.00

4.00

5.00

BG/QGC

BG/Orig

in (fa

iled)

Petron

as/San

tosBG/O

rigin

(faile

d)She

ll/Arro

wQGC/Sun

Conoc

o/Orig

inBG/Q

GCAGL/G

louce

ster

AGL/SGL

BG/PureA

$/M

cf

A$/Mcf 3P A$/Mcf 2P

1.57

4.91

2.51

1.47

2.72

1.74

4.02

1.99

Averages of completedtransactions

weighted arithmetic2P: $2.85 $2.79 3P: $1.09 $1.23

2.11

4.17

3.47

1.91

5

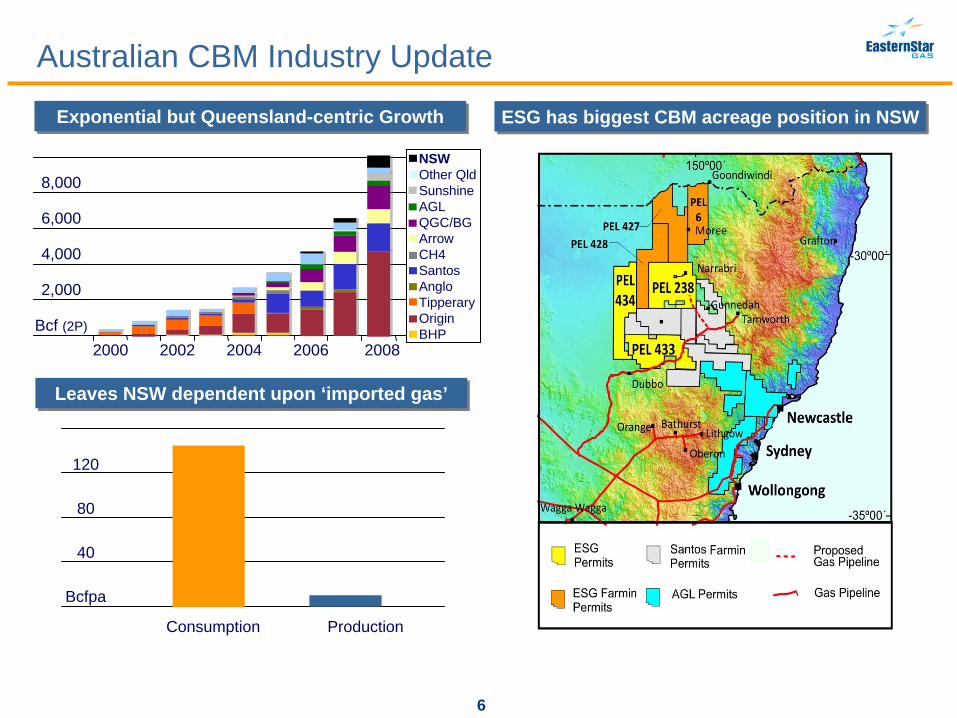

Australian CBM Industry Update

Transaction MetricsTransaction Metrics

BG: BG Group; QGC: Queensland Gas Company; Origin: Origin Energy; Arrow: Arrow Energy; Sun: Sunshine Gas;Gloucester: Gloucester Basin Project; SGL: Sydney Gas Limited; Pure: Pure Energy Resources

Exponential but Queensland-centric GrowthExponential but Queensland-centric Growth

6

Australian CBM Industry Update

120

80

40

Bcfpa

Consumption Production

Leaves NSW dependent upon ‘imported gas’Leaves NSW dependent upon ‘imported gas’

8,000

6,000

4,000

2,000

Bcf (2P)

2000 2002 2004 2006 2008

NSWOther QldSunshineAGLQGC/BGArrowCH4SantosAngloTipperaryOriginBHP

ESG has biggest CBM acreage position in NSWESG has biggest CBM acreage position in NSW

ESG Corporate Overview

ASX Small to Mid Caps Presentation - Grand Hyatt, New YorkNarrabri Coal Seam Gas Project26 February 2009

8

Present Financial PositionPresent Financial Position

ESG Corporate Overview

HighlightsHighlights

ASX (‘ESG’) and OTCQX (‘ESGLY’) Listed.

World-class management & technical teams.

Coordinated approach to Project development:

Shares on issue 762 million

Market

Capitalisation1A$465 million

Cash & Receivable2 A$31.8 million

Debt nil

Notes:Notes:

1.1. Share price A$0.61 at close 20 February 2009Share price A$0.61 at close 20 February 2009

2.2. Cash as at 31 December 2008, plus $4.7m receivableCash as at 31 December 2008, plus $4.7m receivable

“Eastern Star’s Visionis to be NSW’s leading supplier of natural gas”

“Eastern Star’s Visionis to be NSW’s leading supplier of natural gas”

Certified Gas Reserves in place

Reserves upgrade programme underway.

MoU’s in place for sale of ~70 Bcf/a of gas.

HoA in place for transmission pipeline

access.

9

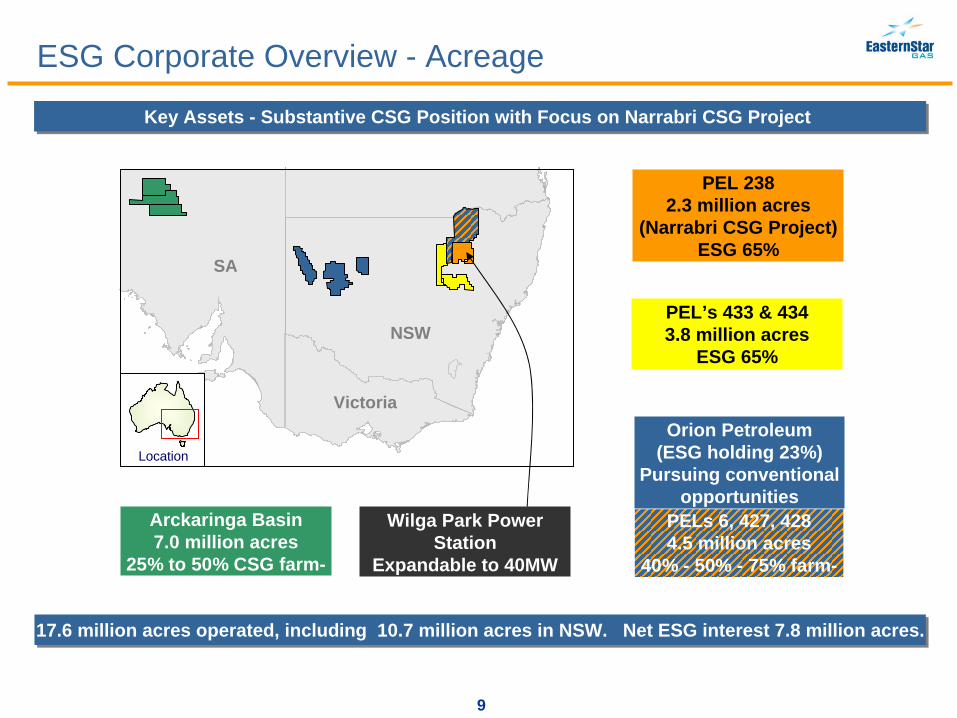

ESG Corporate Overview - Acreage

Key Assets - Substantive CSG Position with Focus on Narrabri CSG Project Key Assets - Substantive CSG Position with Focus on Narrabri CSG Project

PEL 2382.3 million acres

(Narrabri CSG Project)ESG 65%

PEL’s 433 & 4343.8 million acres

ESG 65%

Arckaringa Basin7.0 million acres

25% to 50% CSG farm- in

Orion Petroleum(ESG holding 23%)

Pursuing conventional opportunities

PELs 6, 427, 4284.5 million acres

40% - 50% - 75% farm- in

Location

NSW

SA

Victoria

Wilga Park Power Station

Expandable to 40MWESG 65%

17.6 million acres operated, including 10.7 million acres in NSW. Net ESG interest 7.8 million acres.17.6 million acres operated, including 10.7 million acres in NSW. Net ESG interest 7.8 million acres.

10

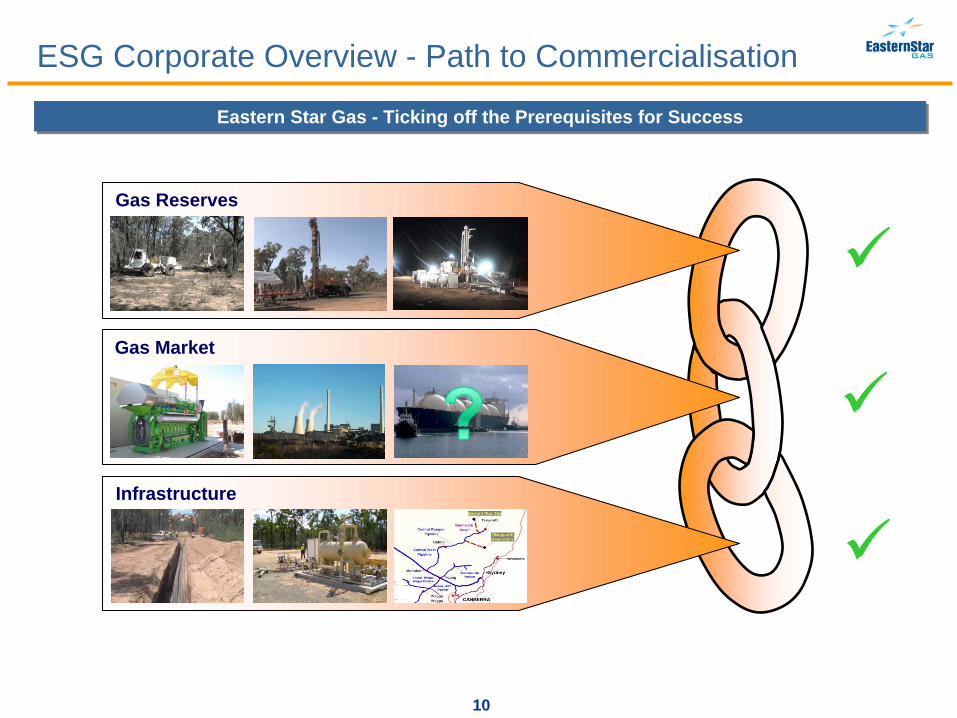

ESG Corporate Overview - Path to Commercialisation

Eastern Star Gas - Ticking off the Prerequisites for SuccessEastern Star Gas - Ticking off the Prerequisites for Success

Gas Reserves

Infrastructure

Gas Market

Narrabri CSG Project - Reserves

ASX Small to Mid Caps Presentation - Grand Hyatt, New York Narrabri Coal Seam Gas Project26 February 2009

12

Narrabri CSG Project -Gas Reserves

Independently Certified Gas Reserves PEL 238Independently Certified Gas Reserves PEL 238 2P Reserves - Comparative Performance2P Reserves - Comparative Performance

Already Achieved Target

2,000

1,600

1,200

800

400

BcfSep 07 Dec 07 Sep 08 Dec 09 2010/11

5-fold increasein 12 months

0

100

200

300

400

1 2 3 4 5 6 7 8 9 10 11 12 13Months from first reserves certification

PJ

ESG PEL238 JV (NSAI) QGC (NSAI) Arrow (NSAI)

Bcf

PEL 238 Certified Gas Reserves(ESG’s 65% interest)

1P 2P 3P

13.7 Bcf 218 Bcf 845 Bcf

13

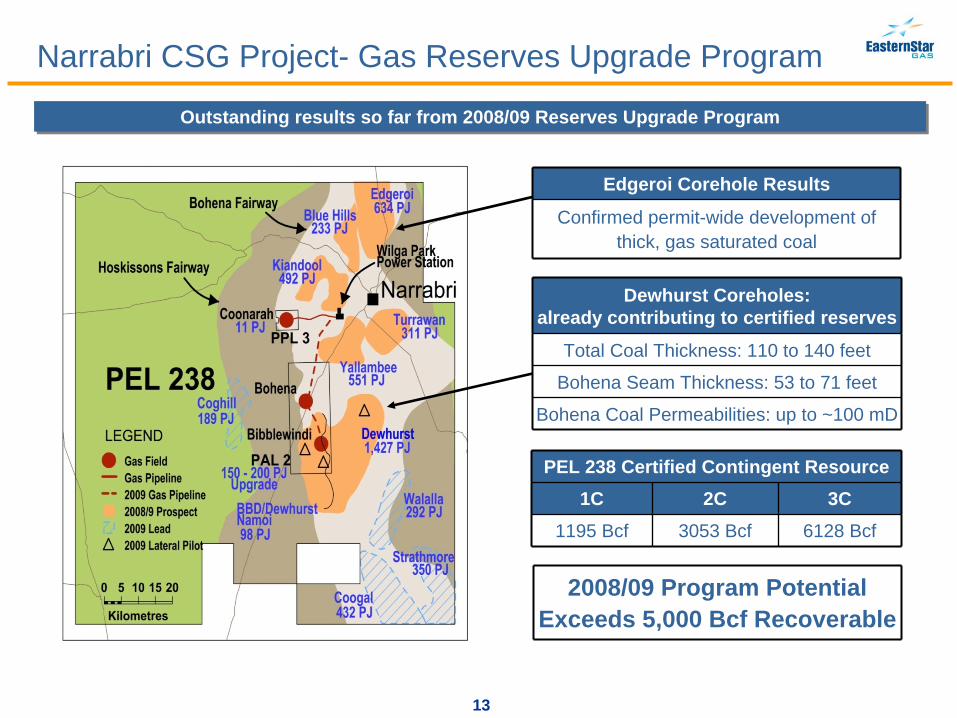

Outstanding results so far from 2008/09 Reserves Upgrade ProgramOutstanding results so far from 2008/09 Reserves Upgrade Program

Narrabri CSG Project- Gas Reserves Upgrade Program

Dewhurst Coreholes:already contributing to certified reserves

Total Coal Thickness: 110 to 140 feet

Bohena Seam Thickness: 53 to 71 feet

Bohena Coal Permeabilities: up to ~100 mD

Edgeroi Corehole Results

Confirmed permit-wide development of thick, gas saturated coal

2008/09 Program PotentialExceeds 5,000 Bcf Recoverable

PEL 238 Certified Contingent Resource1C 2C 3C

1195 Bcf 3053 Bcf 6128 Bcf

14

Narrabri CSG Project - Multi-lateral Wells

Advantages of multi-lateral WellsAdvantages of multi-lateral Wells Schramm TXD rig is now on siteSchramm TXD rig is now on site

Exploit coal architecture, maximise gas production.

Maximise return on investment.

Minimise environmental impacts.

Significant scope for future optimisation of well design to enhance project economics.

Unique Architecture of Bohena CoalUnique Architecture of Bohena Coal

Typical Coal

BohenaCoal

15

Narrabri CSG Project - Multi-lateral Wells

Schramm TXD Drilling Rig on site at NarrabriSchramm TXD Drilling Rig on site at Narrabri

16

Narrabri CSG Project - Multi-lateral Wells

Animation: Drilling of Multi-lateral Production PilotAnimation: Drilling of Multi-lateral Production Pilot

Animation goes here in the live version, but is not included in the handout version

Narrabri CSG Project - Markets

ASX Small to Mid Caps Presentation – Grand Hyatt, New YorkNarrabri Coal Seam Gas Project26 February 2009

18

Narrabri CSG Project - Markets and Infrastructure

Stages 1 & 2: Wilga Park Progressive Expansion to 40 MW; Early Access to NSW Gas MarketStages 1 & 2: Wilga Park Progressive Expansion to 40 MW; Early Access to NSW Gas Market

First 3 MW unit on-line May 2009

Wilga ParkPower Station

BibblewindiFlowline

Longford

SydneyNewcastle

Tamworth

Brisbane

Gladstone

Townsville

Mt Isa Moranbah

WallumbillaBallera

Narrabri

Melbourne

FlowlineExtension

ExistingPipelines

GasProcessing

Lateral toAPA System

HoA in place with APA Group (owner and operator of existing pipelines)

Existing system accesses NSW and East Coast gas markets

19

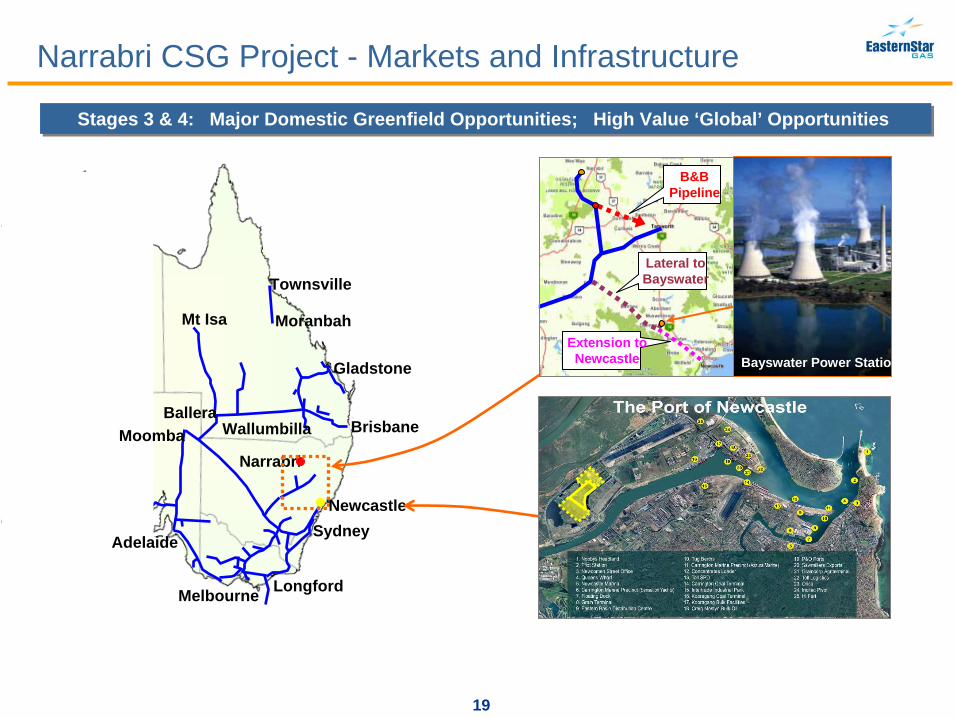

Narrabri CSG Project - Markets and Infrastructure

Stages 3 & 4: Major Domestic Greenfield Opportunities; High Value ‘Global’ Opportunities Stages 3 & 4: Major Domestic Greenfield Opportunities; High Value ‘Global’ Opportunities

Longford

Sydney

Brisbane

Gladstone

Townsville

Mt Isa Moranbah

WallumbillaBallera

Narrabri

Melbourne

Moomba

Adelaide

Newcastle

B&BPipeline

Lateral toBayswater

Extension toNewcastle Bayswater Power Station

20

This presentation may contain forward looking statements that are subject to risk factors associated with oil and gas businesses. It is believed that the expectations reflected in these statements are reasonable but they may be affected by a variety of variables and changes in underlying assumptions which could cause actual results or trends to differ materially, including but not limited to: price fluctuations, actual demand, currency fluctuations, drilling and production results, reserve estimates, loss of market, industry competition, environmental risks, physical risks, legislative, fiscal and regulatory developments, economic and financial market conditions in various countries and regions, political risks, project delay or advancement, approvals and cost estimates.

Investors should undertake their own analysis and obtain independent advice before investing in ESG shares.

All references to dollars, cents or $ in this presentation are to Australian currency, unless otherwise stated.

Disclaimer