Embed Size (px)

Citation preview

Danske MarketsSmall/MidCap Seminar

December 2008

Agenda

• Introduction to BoConcept• BoConcept's franchise model• Latest financial development – 1H 2008/09• Targets, strategy and short term actions• Q&As

Contact:Hans Barslund, EVP & CFOE-mail: [email protected]

TO MAKE BOCONCEPT®

NO. 1 BRANDWITHIN URBAN INTERIORS

OUR VISIONwhat we want to achieve

:

INTRODUCTION TO BOCONCEPT

BoConcept anno 2008

• International retail-oriented concept holder within furniture and lifestyle products for private homes

• Focuses on development, support and supply to global franchise based retail chain, BoConcept, which operates in 47 countries

– 239 BoConcept Brand Stores• Most important sales channel• 400-800 sqm individual operated franchise stores on high-traffic

locations• BoConcept products exclusively

– 114 BoConcept Studios• 100-400 sqm shop-in-shops• BoConcept's products supplements other brands

• BoConcept core competencies:– Design and branding– 'Best practice' in store management– Supply Chain Management and sourcing– Production of board furniture

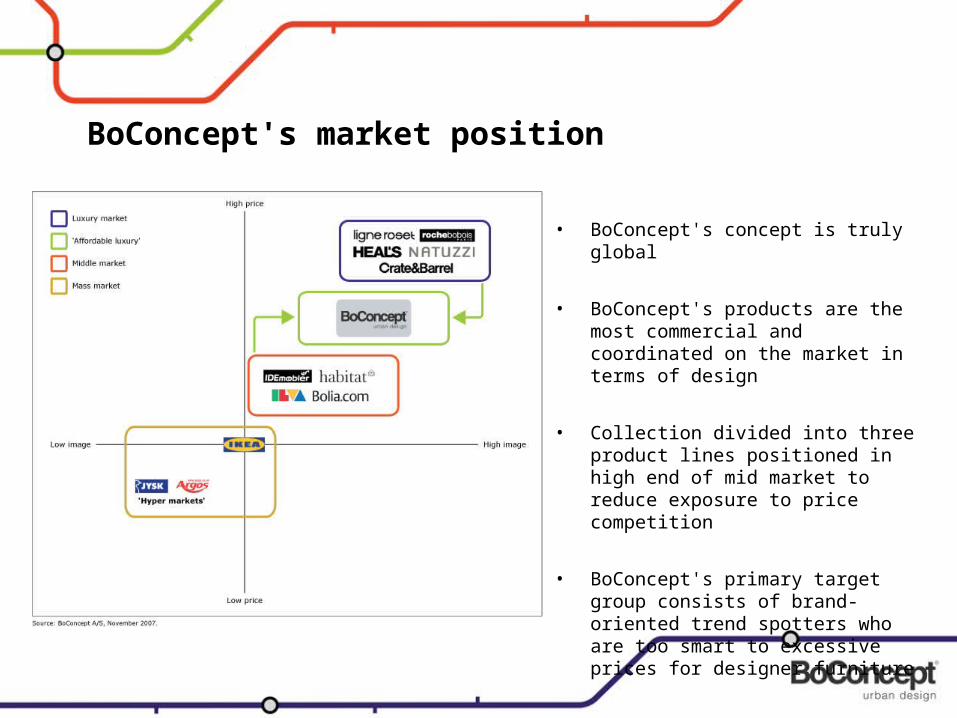

BoConcept's market position

• BoConcept's concept is truly global

• BoConcept's products are the most commercial and coordinated on the market in terms of design

• Collection divided into three product lines positioned in high end of mid market to reduce exposure to price competition

• BoConcept's primary target group consists of brand-oriented trend spotters who are too smart to excessive prices for designer furniture

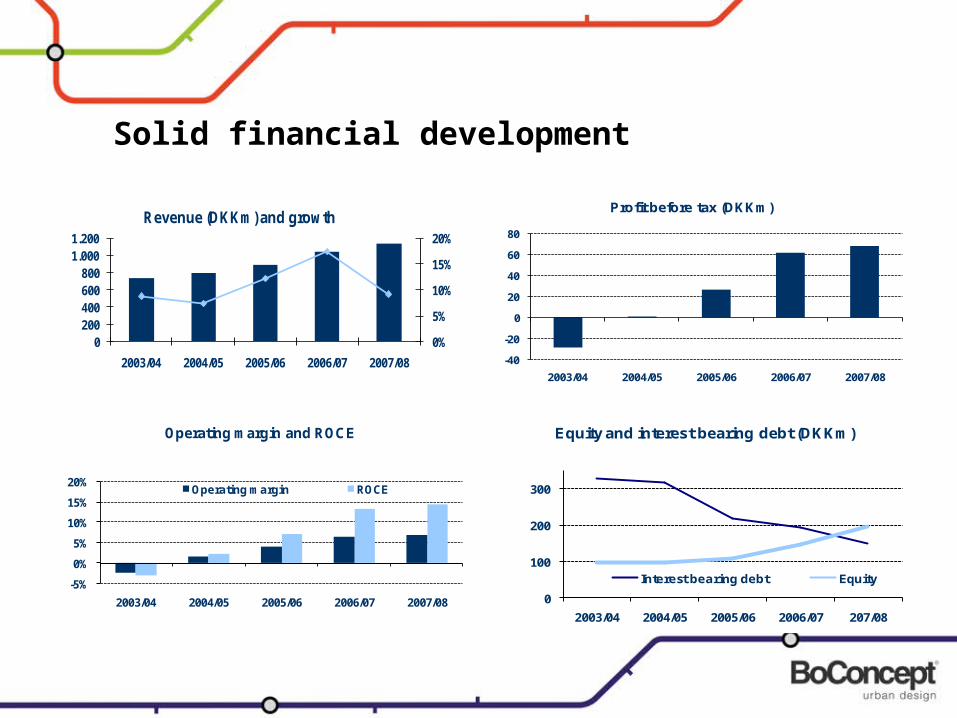

Solid financial development

0%

5%

10%

15%

20%

0200400600800

1.0001.200

2003/04 2004/05 2005/06 2006/07 2007/08

Revenue (DKKm) and growth

-40

-20

0

20

40

60

80

2003/04 2004/05 2005/06 2006/07 2007/08

Profit before tax (DKKm)

-5%

0%

5%

10%

15%

20%

2003/04 2004/05 2005/06 2006/07 2007/08

Operating margin and ROCE

Operating margin ROCE

0

100

200

300

2003/04 2004/05 2005/06 2006/07 207/08

Equity and interest bearing debt (DKKm)

Interest bearing debt Equity

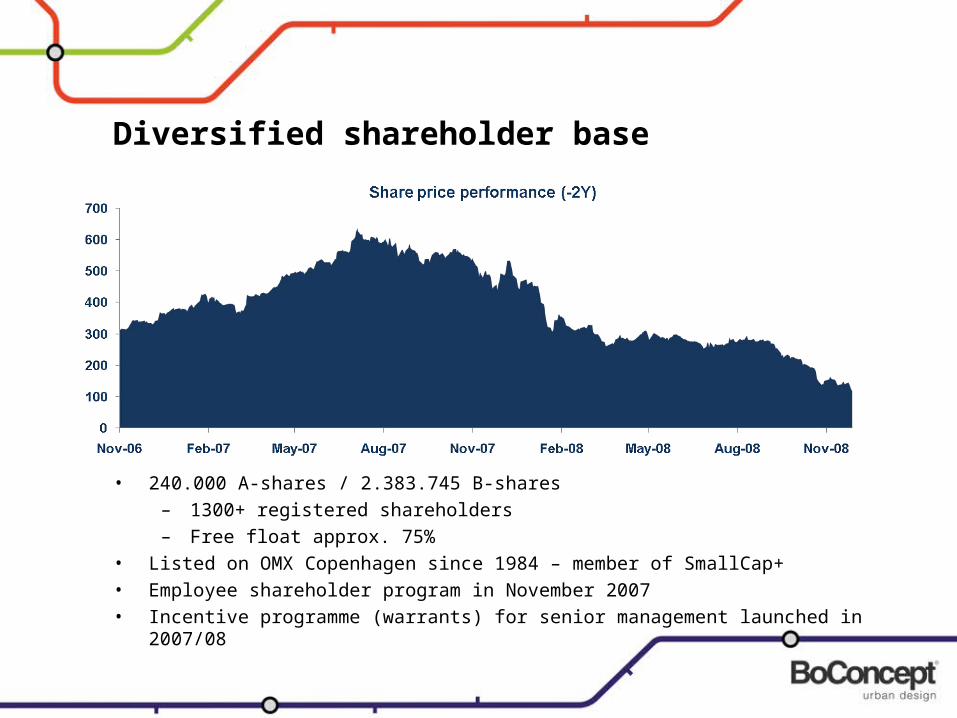

Diversified shareholder base

• 240.000 A-shares / 2.383.745 B-shares– 1300+ registered shareholders– Free float approx. 75%

• Listed on OMX Copenhagen since 1984 – member of SmallCap+• Employee shareholder program in November 2007• Incentive programme (warrants) for senior management launched in

2007/08

THROUGH PASSIONATE AND PERSISTENT PERFORMANCE WE MAKE CUSTOMISED AND COORDINATED DESIGN FURNITURE AND ACCESSORIES AFFORDABLE TO THE URBAN-MINDED SHOPPER

OUR MISSIONwhat we do to achieve our vision

:

BOCONCEPT'S FRANCHISE MODEL

Award winning franchise model

• BoConcept's franchise model is based on a proven concept which has been in place since 1999

• Strong focus on growth in number of Brand Stores since 2004

• Today, 145 franchisees run 239 Brand Stores – an increasing number of franchisees are opening Brand Store no. 2 and 3

• Average turnover in Brand Stores is EUR 1.5m p.a. (significant spread)

• BoConcept offers franchisees massive support to increase same store sales by optimising performance

Deliverables from BoConcept to franchisee

• Coordinated product and accessories program with centralized warehouse handling offering millions of product combinations to customers

• Centralized branding and marketing platform– Catalogue and web-site (decoration and trend inspiration)– Store design and planning– Events and campaigns– Ads and newsletters– PR and communication platform

• Yearly retail conference (BiC) with introduction of new product range, new concepts, marketing activities, workshops etc.

• Continued training and education of sales staff via BoConcept University

• Full IT platform

• Dedicated local Retail Operation Manager (ROM) to ensure ongoing optimal operational performance (store report, budgeting, action plans, best practice sharing)

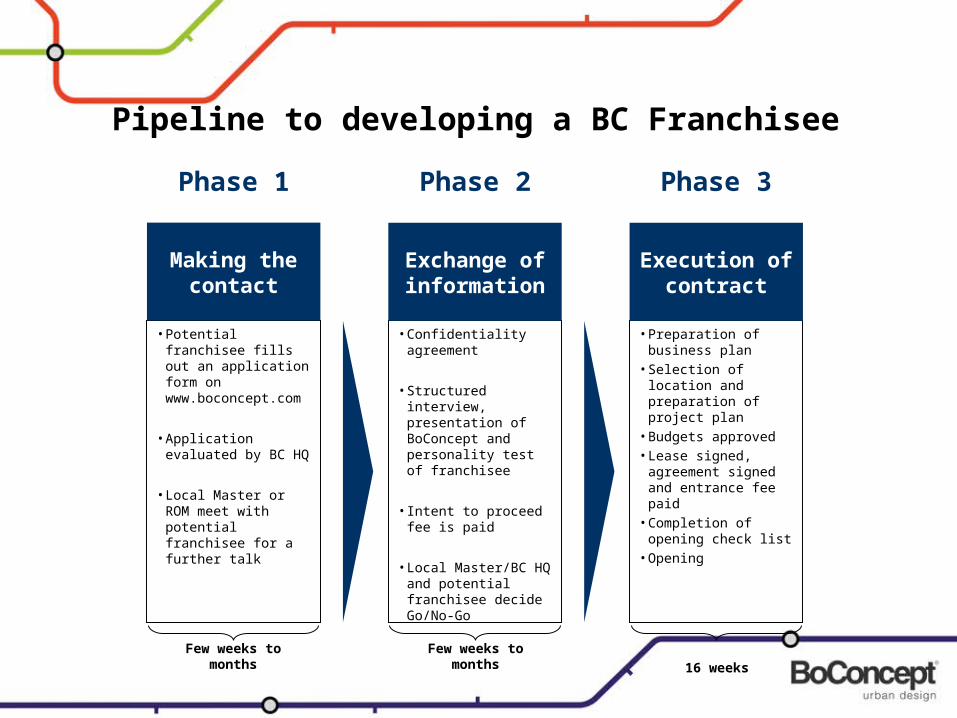

•Preparation of business plan

•Selection of location and preparation of project plan

•Budgets approved•Lease signed,

agreement signed and entrance fee paid

•Completion of opening check list

•Opening

Pipeline to developing a BC Franchisee

Phase 1

•Confidentiality agreement

•Structured interview, presentation of BoConcept and personality test of franchisee

•Intent to proceed fee is paid

•Local Master/BC HQ and potential franchisee decideGo/No-Go

•Potential franchisee fills out an application form on www.boconcept.com

•Application evaluated by BC HQ

•Local Master or ROM meet with potential franchisee for a further talk

Making thecontact

Exchange ofinformation

Execution ofcontract

Phase 2 Phase 3

Few weeks to months

Few weeks to months 16 weeks

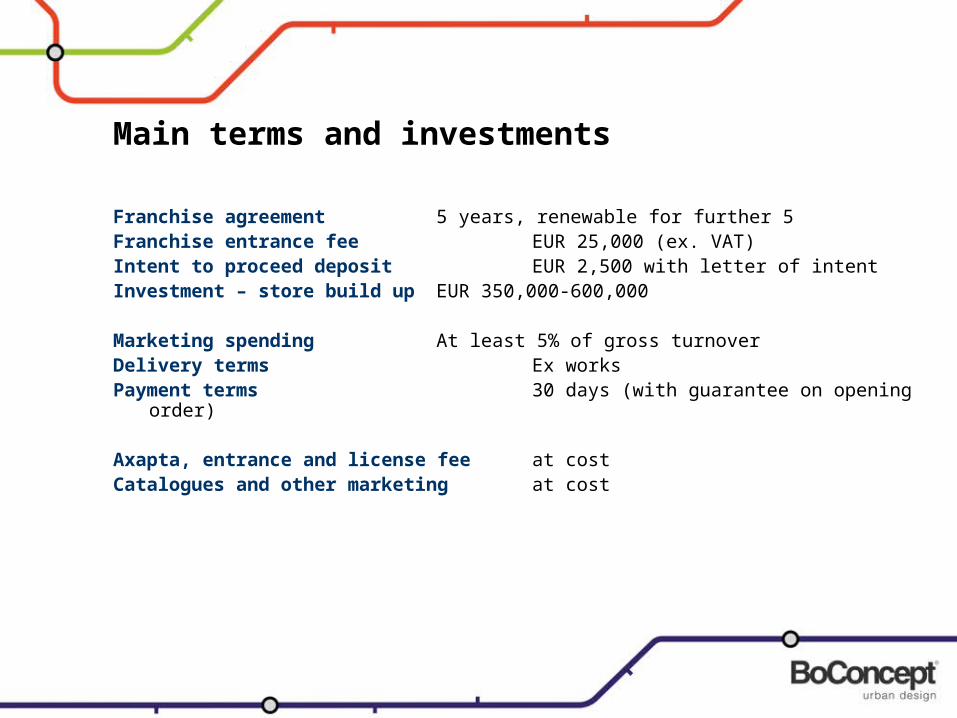

Main terms and investments

Franchise agreement 5 years, renewable for further 5Franchise entrance fee EUR 25,000 (ex. VAT)Intent to proceed deposit EUR 2,500 with letter of intent Investment – store build up EUR 350,000-600,000

Marketing spending At least 5% of gross turnoverDelivery terms Ex worksPayment terms 30 days (with guarantee on opening

order)

Axapta, entrance and license fee at costCatalogues and other marketing at cost

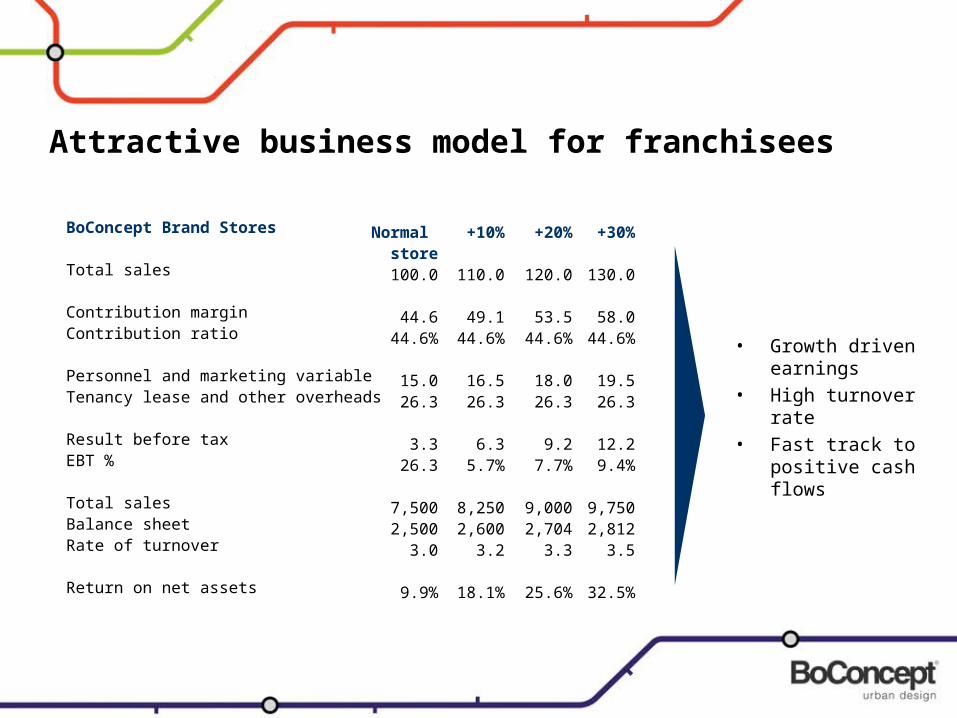

BoConcept Brand Stores

Total sales

Contribution marginContribution ratio

Personnel and marketing variableTenancy lease and other overheads

Result before taxEBT %

Total salesBalance sheetRate of turnover

Return on net assets

Normal store100.0

44.644.6%

15.026.3

3.326.3

7,5002,500

3.0

9.9%

+10%

110.0

49.144.6%

16.526.3

6.35.7%

8,2502,600

3.2

18.1%

+20%

120.0

53.544.6%

18.026.3

9.27.7%

9,0002,704

3.3

25.6%

+30%

130.0

58.044.6%

19.526.3

12.29.4%

9,7502,812

3.5

32.5%

Attractive business model for franchisees

• Growth driven earnings

• High turnover rate

• Fast track to positive cash flows

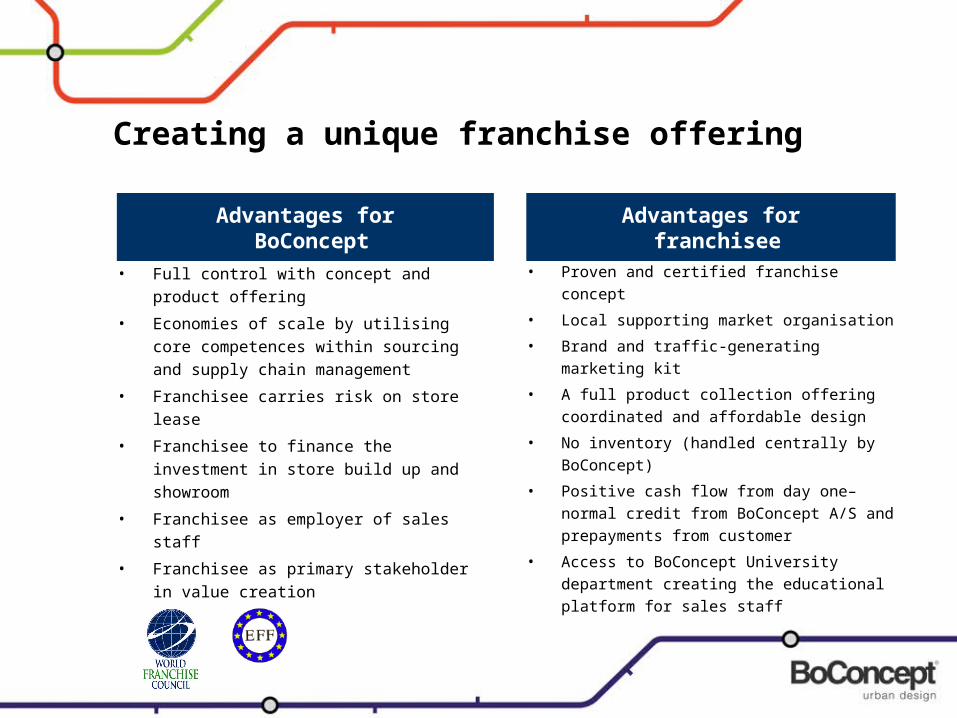

Creating a unique franchise offering

• Full control with concept and product offering

• Economies of scale by utilising core competences within sourcing and supply chain management

• Franchisee carries risk on store lease

• Franchisee to finance the investment in store build up and showroom

• Franchisee as employer of sales staff

• Franchisee as primary stakeholder in value creation

• Proven and certified franchise concept

• Local supporting market organisation

• Brand and traffic-generating marketing kit

• A full product collection offering coordinated and affordable design

• No inventory (handled centrally by BoConcept)

• Positive cash flow from day one– normal credit from BoConcept A/S and prepayments from customer

• Access to BoConcept University department creating the educational platform for sales staff

Advantages for BoConcept

Advantages for franchisee

RESPECT – always show you care

THINK SMARTER – always look for the better solution

PLAY THE TEAM – always use your freedom responsibly

LOVE CITY LIVE – always know what’s going on

OUR CORE VALUEShow we always act

:

LATEST FINANCIAL DEVELOPMENT1H 2008/09

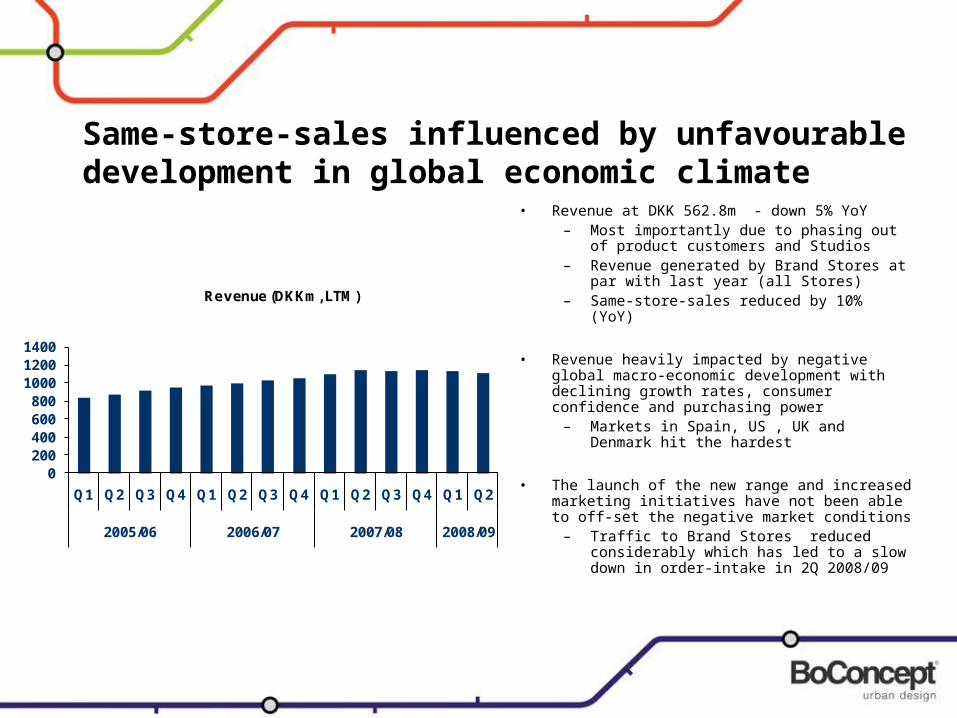

Same-store-sales influenced by unfavourable development in global economic climate

• Revenue at DKK 562.8m - down 5% YoY– Most importantly due to phasing out of

product customers and Studios– Revenue generated by Brand Stores at

par with last year (all Stores)– Same-store-sales reduced by 10%

(YoY)

• Revenue heavily impacted by negative global macro-economic development with declining growth rates, consumer confidence and purchasing power

– Markets in Spain, US , UK and Denmark hit the hardest

• The launch of the new range and increased marketing initiatives have not been able to off-set the negative market conditions

– Traffic to Brand Stores reduced considerably which has led to a slow down in order-intake in 2Q 2008/09

0200400600800

100012001400

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2005/06 2006/07 2007/08 2008/09

Revenue (DKKm, LTM)

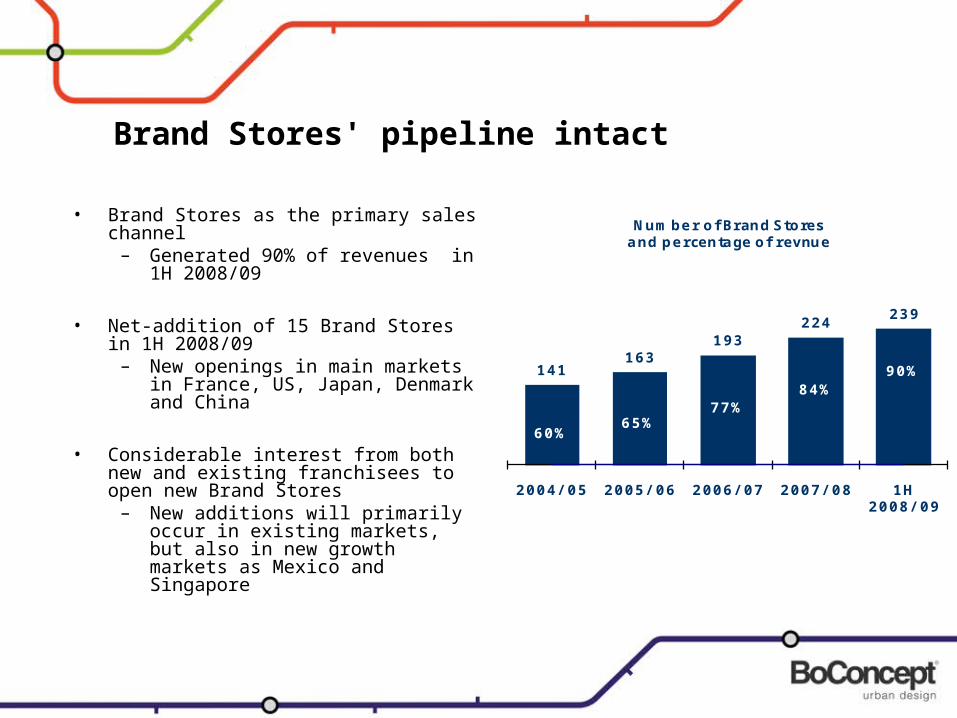

Brand Stores' pipeline intact

• Brand Stores as the primary sales channel

– Generated 90% of revenues in 1H 2008/09

• Net-addition of 15 Brand Stores in 1H 2008/09

– New openings in main markets in France, US, Japan, Denmark and China

• Considerable interest from both new and existing franchisees to open new Brand Stores

– New additions will primarily occur in existing markets, but also in new growth markets as Mexico and Singapore

141163

193224

239

60%65%

77%84%

90%

2004/ 05 2005/ 06 2006/ 07 2007/ 08 1H 2008/ 09

Number of Brand Stores and percentage of revnue

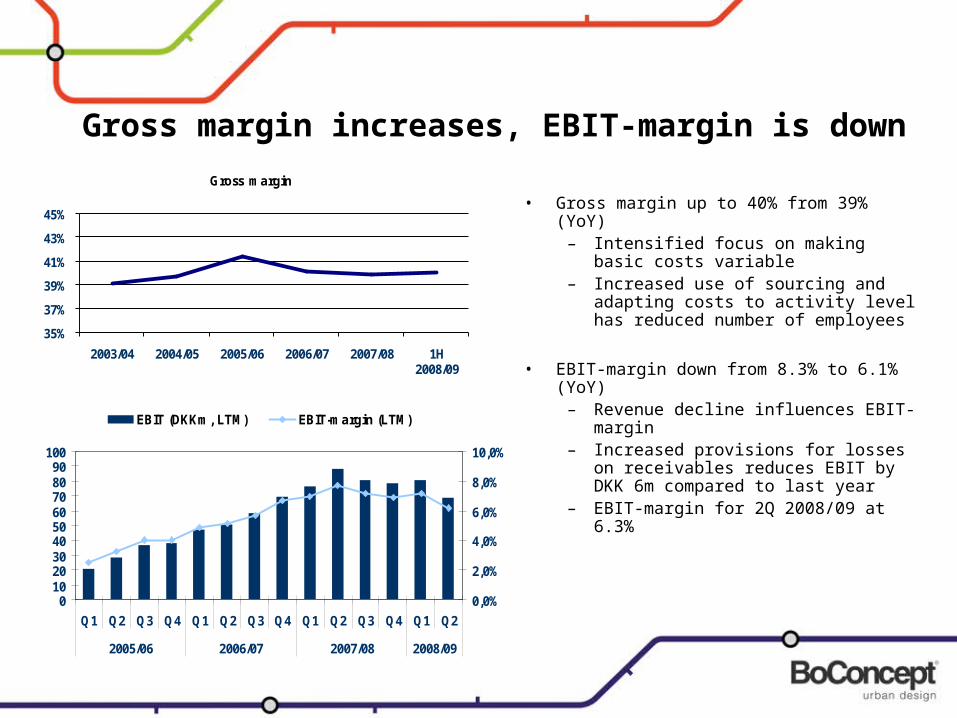

Gross margin increases, EBIT-margin is down

• Gross margin up to 40% from 39% (YoY)

– Intensified focus on making basic costs variable

– Increased use of sourcing and adapting costs to activity level has reduced number of employees

• EBIT-margin down from 8.3% to 6.1% (YoY)

– Revenue decline influences EBIT-margin

– Increased provisions for losses on receivables reduces EBIT by DKK 6m compared to last year

– EBIT-margin for 2Q 2008/09 at 6.3%

35%

37%

39%

41%

43%

45%

2003/04 2004/05 2005/06 2006/07 2007/08 1H 2008/09

Gross margin

0102030405060708090

100

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2005/06 2006/07 2007/08 2008/09

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

EBIT (DKKm, LTM) EBIT-margin (LTM)

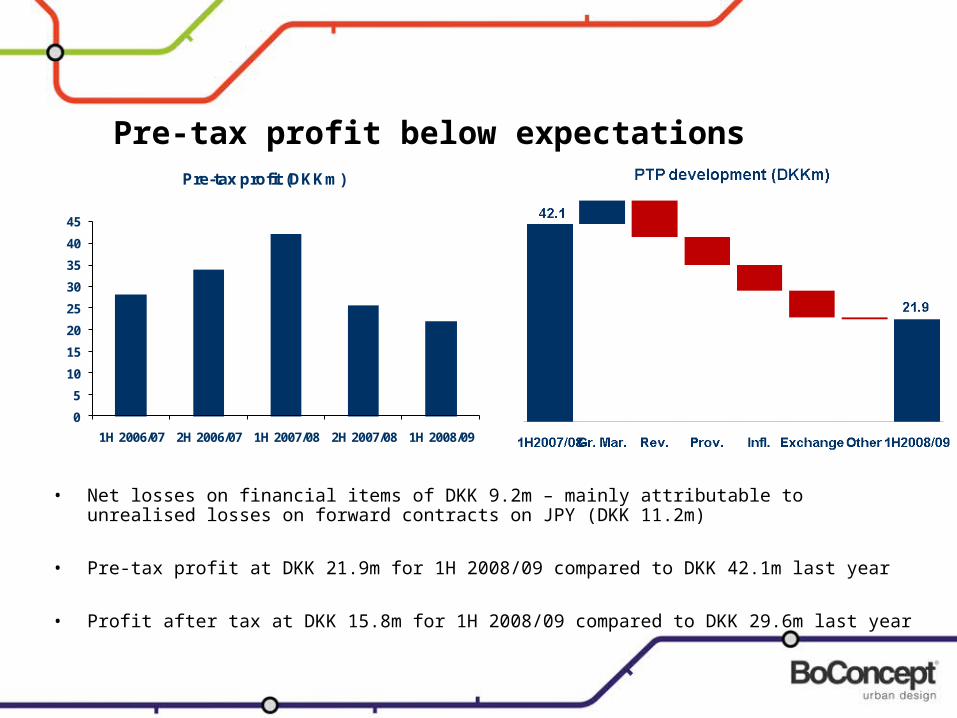

Pre-tax profit below expectations

• Net losses on financial items of DKK 9.2m – mainly attributable to unrealised losses on forward contracts on JPY (DKK 11.2m)

• Pre-tax profit at DKK 21.9m for 1H 2008/09 compared to DKK 42.1m last year

• Profit after tax at DKK 15.8m for 1H 2008/09 compared to DKK 29.6m last year

0

5

10

15

20

25

30

35

40

45

1H 2006/07 2H 2006/07 1H 2007/08 2H 2007/08 1H 2008/09

Pre-tax profit (DKKm)

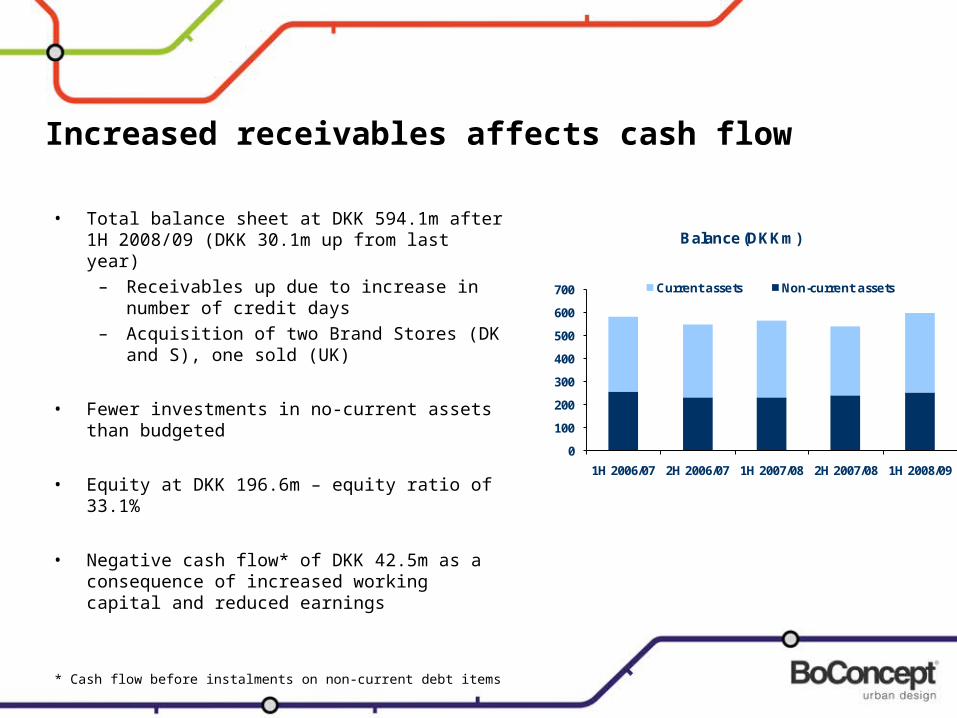

Increased receivables affects cash flow

• Total balance sheet at DKK 594.1m after 1H 2008/09 (DKK 30.1m up from last year)

– Receivables up due to increase in number of credit days

– Acquisition of two Brand Stores (DK and S), one sold (UK)

• Fewer investments in no-current assets than budgeted

• Equity at DKK 196.6m – equity ratio of 33.1%

• Negative cash flow* of DKK 42.5m as a consequence of increased working capital and reduced earnings

0

100

200

300

400

500

600

700

1H 2006/07 2H 2006/07 1H 2007/08 2H 2007/08 1H 2008/09

Balance (DKKm)

Current assets Non-current assets

* Cash flow before instalments on non-current debt items

CUSTOMISEDURBAN DESIGN

OUR BRAND SOULthe most singular way to describe our brand

:

TARGETS, STRATEGY AND SHORT TERM ACTIONS- FOCUS AND DIRECTION REMAINS

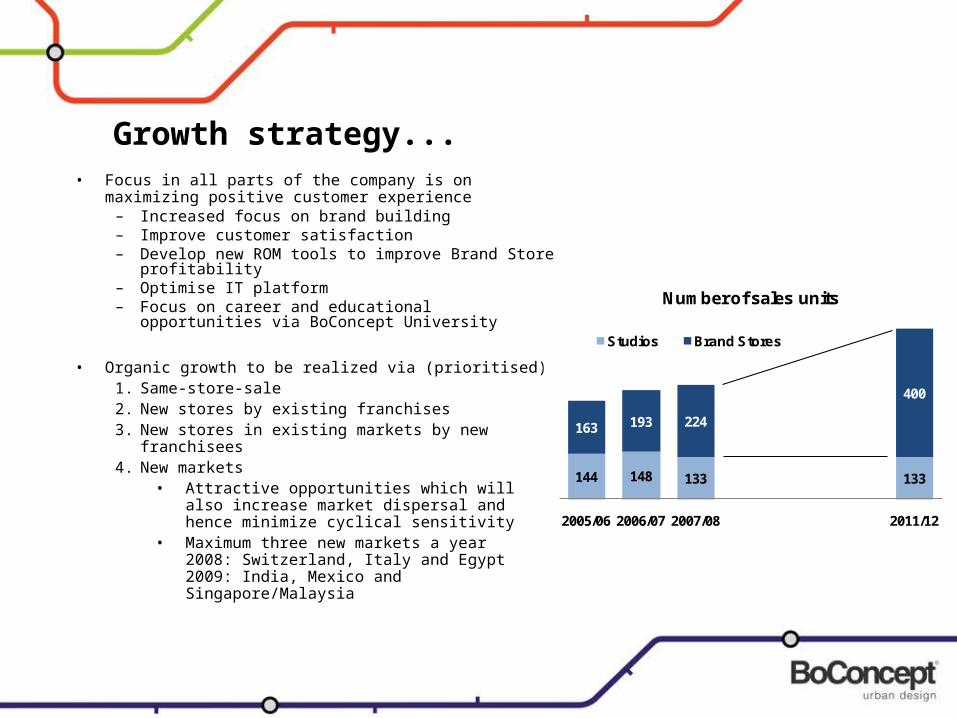

Growth strategy...• Focus in all parts of the company is on maximizing

positive customer experience – Increased focus on brand building– Improve customer satisfaction– Develop new ROM tools to improve Brand Store

profitability – Optimise IT platform– Focus on career and educational opportunities

via BoConcept University

• Organic growth to be realized via (prioritised)1. Same-store-sale2. New stores by existing franchises 3. New stores in existing markets by new

franchisees4. New markets

• Attractive opportunities which will also increase market dispersal and hence minimize cyclical sensitivity

• Maximum three new markets a year2008: Switzerland, Italy and Egypt2009: India, Mexico and Singapore/Malaysia

144 148 133 133

163 193 224

400

2005/06 2006/07 2007/08 2011/12

Number of sales units

Studios Brand Stores

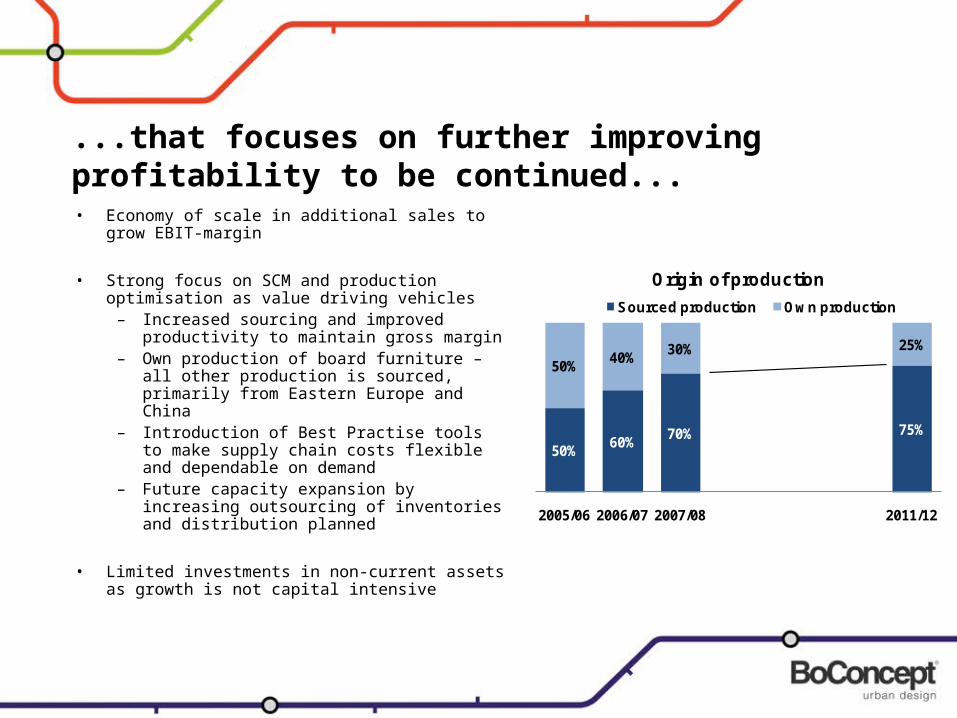

...that focuses on further improving profitability to be continued...• Economy of scale in additional sales to

grow EBIT-margin

• Strong focus on SCM and production optimisation as value driving vehicles

– Increased sourcing and improved productivity to maintain gross margin

– Own production of board furniture – all other production is sourced, primarily from Eastern Europe and China

– Introduction of Best Practise tools to make supply chain costs flexible and dependable on demand

– Future capacity expansion by increasing outsourcing of inventories and distribution planned

• Limited investments in non-current assets as growth is not capital intensive

50%60%

70% 75%

50%40%

30% 25%

2005/06 2006/07 2007/08 2011/12

Origin of production

Sourced production Own production

...but current market conditions are demanding

Situation• Decreasing global growth and

consumer confidence reduces traffic to Brand Stores and adds pressure on order-intake and same-store-sales

• Positive reception of new collection has not been able to off-set the negative impact from the recent macro-economic development

• Absence of additional sales limits EBIT-margins as Economy of Scale is not achieved

Actions from BoConcept• Focussed effort to increase same-

store-sales– Tactical marketing to increase traffic to

Brand Stores– Local activities (low cost)– Market aligned 2009/10– Interior decoration set-up to be rolled

out by Feb. 2009

• Working pipeline to increase net-additions of Brand Stores on all markets

• Intensify efforts to make production costs variable

– Increase sourcing– Adjust own-production

• General cost cuts– 90-100 in head count reductions since

beginning of financial year

Own-production consolidation

• BoConcept will close its board furniture factory in Herning and concentrate production on Ølgod facility

– Will ensure future cost-efficient operation– Focus on utilising capacity and introduce a more technology

advanced production process– Administrative functions remains in Herning

• The concentration of production in Ølgod will happen gradually and be fully in effect by Feb. 2009

• Closing down production in Herning is expected to bring about annual savings of min. DKK 10m p.a. from 2009/10

– In 2008/09 restructuring costs incidental to the shutdown are expected to amount to DKK 10m

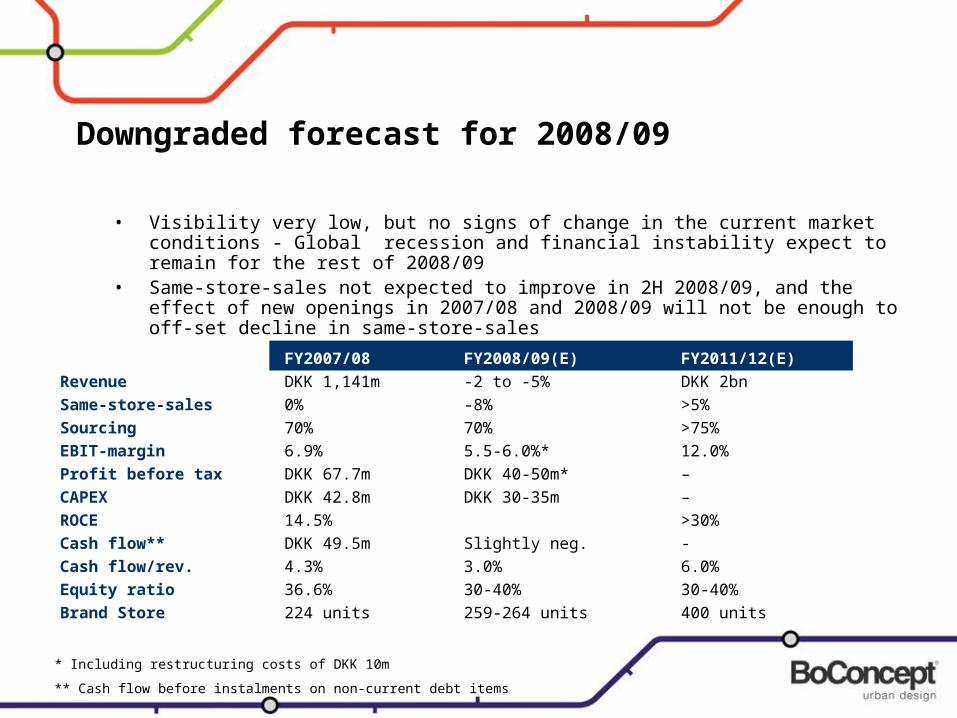

Downgraded forecast for 2008/09

• Visibility very low, but no signs of change in the current market conditions - Global recession and financial instability expect to remain for the rest of 2008/09

• Same-store-sales not expected to improve in 2H 2008/09, and the effect of new openings in 2007/08 and 2008/09 will not be enough to off-set decline in same-store-sales

FY2007/08DKK 1,141m0%70%6.9%DKK 67.7mDKK 42.8m14.5%DKK 49.5m4.3%36.6%224 units

RevenueSame-store-salesSourcingEBIT-marginProfit before taxCAPEXROCECash flow**Cash flow/rev.Equity ratioBrand Store

FY2008/09(E)-2 to -5%-8%70%5.5-6.0%*DKK 40-50m*DKK 30-35m

Slightly neg.3.0%30-40%259-264 units

FY2011/12(E)DKK 2bn>5%>75%12.0%––>30%-6.0%30-40%400 units

* Including restructuring costs of DKK 10m

** Cash flow before instalments on non-current debt items

In summary• BoConcept's design and concept is perfectly aligned with global mega-trend –

market position in high end of mid-market continues to expand

• BoConcept's business model, concept and core competencies showed their strength

– Attractive franchise model enables strong future growth in number of Brand Stores

– Momentum and profitability to be secured and grown via an increased number of sales units, adjusted marketing and product mix as well as continued focus on sourcing and improved productivity in own-production

• 2008/09 will be a challenging year influenced by macro economic set-back on main markets in USA and Western Europe (ex. France)

– Strong focus on marketing efforts and customer experience to increase traffic to shops, and on growing net-additions to Brand Stores base

– Further develop production efficiency to maintain gross margins

• Strategy and targets of the long term growth plan maintained– Road to steep and profitable non-capital intensive growth paved

Q&AFOR FURTHER INFOMATION VISIT OUR WEBSITEwww.boconcept.dk