Embed Size (px)

Citation preview

22/03/2018 © IFCN 2017 | 1

Dairy World & Recent Market Trends

Amit Saha

IFCN Senior Researcher; Dairy economist

Competitiveness and internationalization of livestock sectors. Ministry of Agriculture and Fisheries, Food and Environment, Spain – 20.3.18

22/03/2018 © IFCN 2017 | 2

World milk price is still very volatile

IFCN Combined World Milk Price Indicator

?

22/03/2018 © IFCN 2017 | 3

Agenda

1. The IFCN Network Concept

2. Globalization of dairy sector

3. Dairy markets & its drivers

4. Farm competitiveness

5. Sum up

22/03/2018 © IFCN 2017 | 4

Mission:

We create a better understanding of the dairy world by providing

comparable data, knowledge and inspiration.

IFCN - The Dairy Research Network

The IFCN Network approach – consisting of three pillars

- the IFCN Research Network of researchers

- the IFCN Supporter Partner Network of companies/institutions

- the IFCN Research Center with > 15 dairy economists

22/03/2018 © IFCN 2017 | 5

IFCN Network 2018

IFCN Country Data Partners 110 Countries, 98% of world milk production covered

IFCN Supporter Partners >120

New companies in 2017/18:

Milcobel, DZ Bank, AGCO, Cobank, KDD, Kalleh, Leiber,

Etex, TopCon, Novozyme, Nordic dry, Kemin, Aavin,

Randox, smaXtec

New institutions 2017: GASL, WWF, NDDB

IFCN Institutional Partners

22/03/2018 © IFCN 2017 | 6

Agenda

1. The IFCN Network Concept

2. Globalization of dairy sector

3. Dairy markets & its drivers

4. Farm competitiveness

5. Sum up

22/03/2018 © IFCN 2017 | 7

Who is importing what?Dairy imports by product groups in 2015

Source: IFCN Dairy Report 2016, page 81

22/03/2018 © IFCN 2017 | 8

Key driver: Milk surplus & deficit by region

ME = Milk equivalents, based on fat and protein only

ME = milk equivalents

22/03/2018 © IFCN 2017 | 9

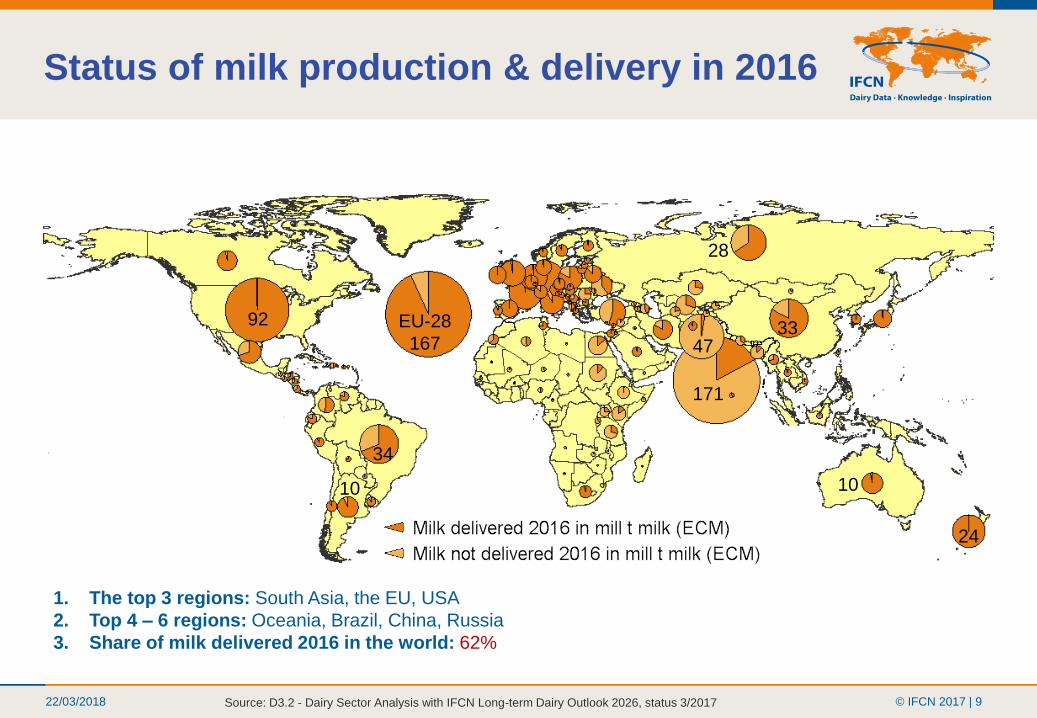

1. The top 3 regions: South Asia, the EU, USA

2. Top 4 – 6 regions: Oceania, Brazil, China, Russia

3. Share of milk delivered 2016 in the world: 62%

Status of milk production & delivery in 2016

EU-28

167

10

34

92

10

24

33

171

47

28

Source: D3.2 - Dairy Sector Analysis with IFCN Long-term Dairy Outlook 2026, status 3/2017

22/03/2018 © IFCN 2017 | 10

Rank 2016 Company nameOrigin & main operation

countries

Milk intake,

in mill. t ME

Estimated

turnover per kg

milk, in USD

Market share in

% of world milk

production

1 Dairy Farmers of America USA 28.1 0.5 3.6%

2 Fonterra New Zealand/ others 22.1 0.6 2.8%

3 Groupe Lactalis France/others 15.1 1.3 1.9%

4 Arla Foods Denmark/Sweden/UK 14.2 0.8 1.8%

5 Nestlé Switzerland/others 14.0* 1.9* 1.8%

6 FrieslandCampina Netherlands/others 12.6* 1.0* 1.6%

7 Dean Foods USA 10.3 0.8 1.3%

8 DMK (incl.DOC Kaas) Germany/Netherlands 7.8 0.9 1.0%

9 Saputo Canada/USA/others 7.7 1.1 1.0%

10 California Dairies USA 7.7 0.5 1.0%

11 Danone France/others 7.5 2.4 1.0%

12 Yili Group China 6.8* 1.4* 0.9%

13 Amul (GCMMF) India 6.5 0.8 0.8%

14 Müller Germany/UK/others 6.3 1.2 0.8%

15 Glanbia Group Ireland/USA/others 6.1 0.7 0.8%

16 Agropur Canada/USA 5.8 1.0 0.7%

17 Land O' Lakes USA 5.8* 0.7* 0.7%

18 Mengniu China 5.8 1.4 0.7%

19 Groupe Sodiaal France 5.2 1.1 0.7%

20 Schreiber foods USA 4.5* 1.1* 0.6%

Sum of Top 20 200 1.0 25.4%

IFCN Top 20 milk processors list 2016

Data related to the mainly 2015

* IFCN estimation

22/03/2018 © IFCN 2017 | 11

USA

Source: IFCN Monthly Real Time Data

Spain

1. The world milk price

influences national milk

prices

2. Each country follow the

red line -

3. But we have special

patterns like e.g.

USA: 2014 + 2015

EU/Spain: 2007;2017/18

USD

/10

0kg

EC

M

Transmission from world to national milk price

22/03/2018 © IFCN 2017 | 12

Rotterdam declaration: 1 billion peopleFAO: It is likely that the dairy sector supports the livelihoods of up to one billion people worldwide.

3.09

mill

2009 IDF summit – 0,7- 1 bill people on farmMathematics on dairy farms

1. 120-130 mill dairy farms

2. 5 people/ farming family

=> > 600 million people

Mathematics supply chain

1. 71 mill Jobs in the dairy chain

(Range = 36- 258 mill)

2. 5 people/ family

=> >355 million people

2010 FAO/IFCN –>750 mill on farm

One Billion people =

> 600 mill farm + >355 mill chain +

XXX induced jobs / spin offs

2015 IFCN work for GDP > 950 mill

22/03/2018 © IFCN 2017 | 13

Agenda

1. The IFCN Network Concept

2. Globalization of dairy sector

3. Dairy markets & its drivers

4. Farm competitiveness

5. Sum up

22/03/2018 © IFCN 2017 | 14

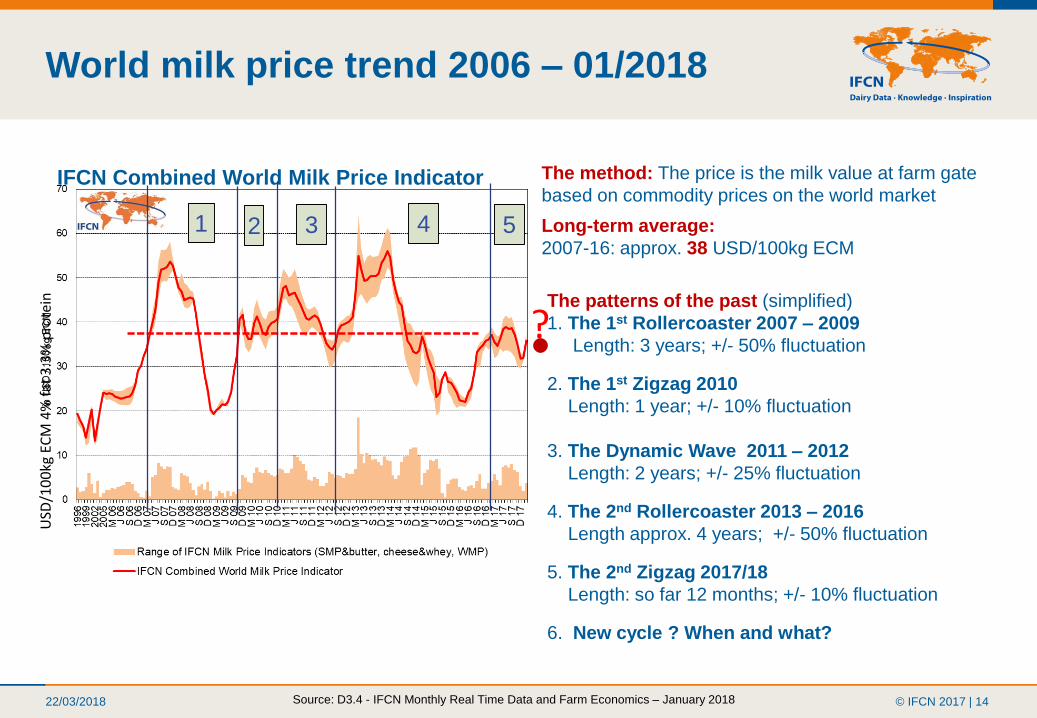

World milk price trend 2006 – 01/2018

IFCN Combined World Milk Price Indicator

The patterns of the past (simplified)

1. The 1st Rollercoaster 2007 – 2009

Length: 3 years; +/- 50% fluctuation

2. The 1st Zigzag 2010

Length: 1 year; +/- 10% fluctuation

3. The Dynamic Wave 2011 – 2012

Length: 2 years; +/- 25% fluctuation

4. The 2nd Rollercoaster 2013 – 2016

Length approx. 4 years; +/- 50% fluctuation

5. The 2nd Zigzag 2017/18

Length: so far 12 months; +/- 10% fluctuation

6. New cycle ? When and what?

Source: D3.4 - IFCN Monthly Real Time Data and Farm Economics – January 2018

1 2 3 4

The method: The price is the milk value at farm gate

based on commodity prices on the world market

Long-term average:

2007-16: approx. 38 USD/100kg ECM 5

USD

/10

0kg

EC

M 4

% f

at 3

.3%

pro

tein

?

22/03/2018 © IFCN 2017 | 15

What drives dairy economics?

Why short term outlook

How IFCN can support you with real time data

22/03/2018 © IFCN 2017 | 16

World milk production change 1997-2016

The indicator used:

All milk = milk from all types of animal,

standardised to 4% fat, 3.3% protein

The trends for the last 10 years:

17 mill t / 2.3%/year Ø growth

3 crisis years: 2009; 2012; 2016

2014 record production year: + 25 mill t

Situation 2016:

846 mill t milk production

+ 9.9 mill t growth (+ 1.2%)

= lowest growth since 1998

2017e

?

22/03/2018 © IFCN 2017 | 17

Current dairy world situationDecember 2017 – February 2018 IFCN Estimates

Source: Data product – 3.4 IFCN Monthly Real Time Data, 15.02.2018

World milk and feed prices in USD / 100 kg ECM

22/03/2018 © IFCN 2017 | 18

Milk demand per capita 2016

Source: D3.2 - Dairy Sector Analysis with IFCN Long-term Dairy Outlook 2026

The indicator: There is a comparable milk demand indicator

Milk demand ranges from 13 kg in Indonesia to over 300 kg per capita in EU countries

22/03/2018 © IFCN 2017 | 19

China: Imports are recovering

Russia: Imports still not back on

pre-ban level

Algeria/ Egypt: Imports show

downward trend with current

devaluation against USD

Dairy import changes in 2017 vs 2016

0.7

Source: D3.2 - Dairy Sector Analysis with IFCN Long-term Dairy Outlook 2026, status 8/2017

-0.3

0.7

-0.3

-0.50.5

Monthly total dairy commodities imports volume

by top dairy net importers in milk equivalents

% change to previous year

2014 +6%

2015 -1%

2016 4%

Jan-Sep 2017 +2.4%

Total world dairy imports

1000 t M

E

22/03/2018 © IFCN 2017 | 20

Agenda

1. The IFCN Network Concept

2. Globalization of dairy sector

3. Dairy markets & its drivers

4. Farm competitiveness

5. Sum up

22/03/2018 © IFCN 2017 | 21

Farm comparison analysis in 2017

Participating countries 2017

Coverage: 52 countries; 89% of world

production, 159 typical farm types

A typical farm type represents in each

country a certain production system and

x% farm and y% cows

Time period: data for calendar year 2016** Seasonal data for New Zealand

Why? Better understand and predict a

specific segmentation of farm classes, we

define the typical farm class.

Method concept

a) Typical farm concept

b) Model TIPI-CAL

c) Validation loops & quality check

d) The cooperation between researchers

22/03/2018 © IFCN 2017 | 22

Countries where IFCN Typical farms are analyzedLegend:

Examples of typical farm types

ES-65NW: Typical Average size family dairy farm in Galicia region, North West Spain- herd size of 65 cows

NZ-369

NZ-1052

Source: D3.2 - Dairy Sector Analysis with Long-term Outlook 2026

ID

US-80WI

US-500WI

PL-16E

PL-65S

CN-200

CN-1450

IN-2N

IN-20N

BR-23S

BR-60S

DE-30SDE-139N

KE-2

KE-10

UA-200

UA-550

ES-65NWES-93S

22/03/2018 © IFCN 2017 | 23

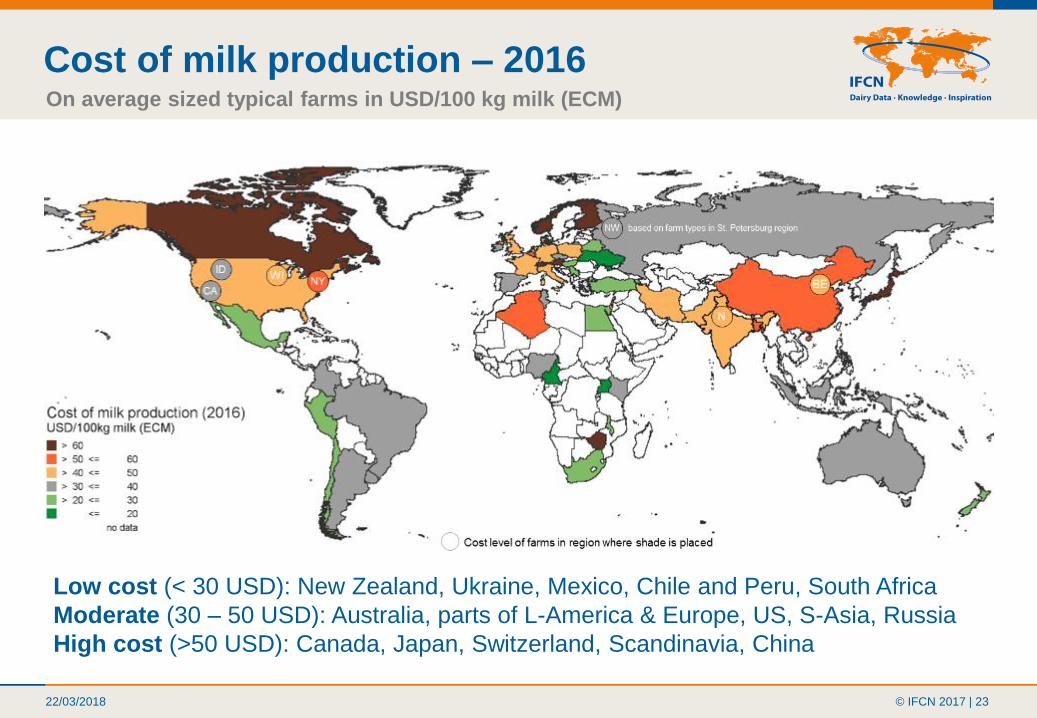

Cost of milk production – 2016 On average sized typical farms in USD/100 kg milk (ECM)

Low cost (< 30 USD): New Zealand, Ukraine, Mexico, Chile and Peru, South Africa

Moderate (30 – 50 USD): Australia, parts of L-America & Europe, US, S-Asia, Russia

High cost (>50 USD): Canada, Japan, Switzerland, Scandinavia, China

22/03/2018 © IFCN 2017 | 24

Cost and labour competitiveness 2016

• Sustainable farming

systems needed

• Economic Drivers: Milk

price, cost of production,

labour returns

• Policy drivers: Farm

support

• Larger sized farms are

more sustainable but

need policy support in EU

USD

/ 1

00

Kg

Milk

(EC

M)

USD

/ H

ou

r

22/03/2018 © IFCN 2017 | 25

Cost trend analysis of typical farmsFor 6 countries 2000 - 2017

Spain, USA, New Zealand China, India, Brazil • Costs in the ES, DE and NZ

decreased from 2014

onwards

• Drivers for cost ( ) in ES:

low feed price, euro devaln

• Costs are stabilizing in the

range of 30-40 USD per 100

kg milk (ECM)

• Exception: NZ:below 30 USD

CN: 60 to 50 USD

• Cost estimations in 2017

similar to 2016 except IN, BR

• Precursor for increased

production in 2017 ->better

milk price at 36 USD

2017e: estimated for 2017

Source: IFCN Farm Economic Data D5.1

22/03/2018 © IFCN 2017 | 26

Benchmarking ideas is possible and can be

used identify value creating startegies

Environmental sustainabilityEconomic sustainability Social sustainability

Indicator: Costs from profit

and loss account – non-milk

returns + opportunity costs

Indicator: Green House Gas

Emissions calculated with a

partial Life Cycle Assessment for

milk production until the farm

gate

Indicator: Farm income

(including decoupled subsidies)

per hour family labour input in

relation to the national minimum

wage rate

DE-N = Base, farm now; S1 – S5 = 5 different scenarios / ideas

22/03/2018 © IFCN 2017 | 27

Agenda

1. The IFCN Network Concept

2. Globalization of dairy sector

3. Dairy markets & its drivers

4. Farm competitiveness

5. Sum up

22/03/2018 © IFCN 2017 | 28

Our key messages today

1. Dairy Globalization: Most likely to continue at a much

faster pace, new local and global markets and growth on

the anvil

2. Dairy Story: 1 Billion+ people livelihood relate to dairy

3. Dairy markets: Price volatility is a reality-real time

information is the key; Demand driven markets likely to

remain bearish in 2018

4. Farm economics: Stable margin in 2017 estimated leading

to increased milk supplies. Milk production costs stabilizing

at 35-40 USD per 100 kg ECM.

22/03/2018 © IFCN 2017 | 29

Thank you for your attention

IFCN Dairy Research CenterNetwork of IFCN Researchers Network of IFCN Supporters

A great number of people have collaborated since the year 2000

to make this presentation possible.