Embed Size (px)

Citation preview

defining d-fine

Wolfgang Pleyer

XXV Heidelberg Physics Graduate Days, October 5, 2010

defining d-fine

Our Company

� d-fine in a nutshell

Our People

� Our international team

� Publications and Conference Contributions

� The d-fine Career Model

Agenda

Slide # 2© 2010 d-fine All rights reserved.

� The d-fine Career Model

� Your Life at d-fine

Our Services

� Our Market Position

� Our Clients

� Our Services

� Our IT Expertise

Work Examples

defining d-fine

Our Company

Slide # 3© 2010 d-fine All rights reserved.

Our Company

defining d-fine

� With over 250 professionals and offices in Frankfurt, Munich,

London and Hong Kong, d-fine is a leading consulting firm for

demanding quantitative and technical consulting projects

� d-fine is built around

– Quantitative finance

– Risk management

– Accounting issues and reporting

d-fine in a nutshell

Slide # 4© 2010 d-fine All rights reserved.

– Accounting issues and reporting

– IT integration

� We help our clients with all trading, back office, loan

management, risk management and asset/liability projects

– From analysis and design to industry-strength solutions

– From mathematical modelling to business process implementations

– From retail and corporate loans to exotic credit and equity derivatives

– From internal market risk Models to IFRS

– From capital allocation to risk-adjusted portfolio management

– From internal rating systems to fully fledged Basel II(I) and Solvency II implementations

defining d-fine

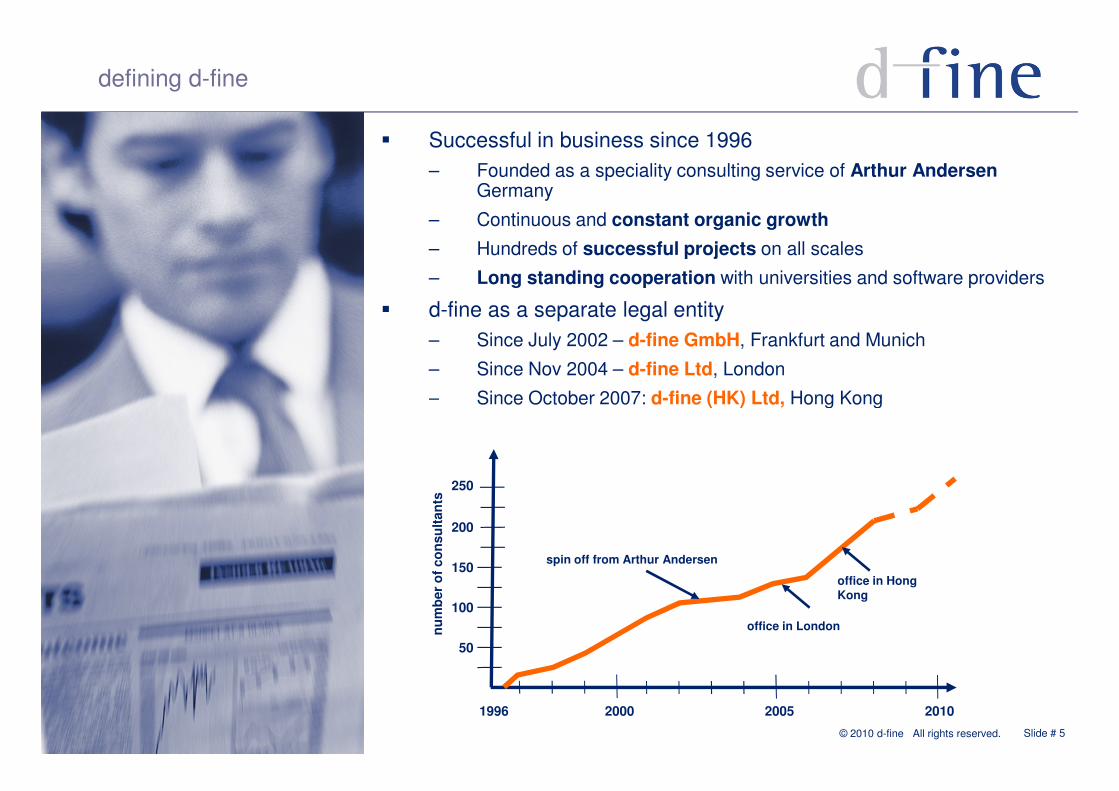

� Successful in business since 1996

– Founded as a speciality consulting service of Arthur AndersenGermany

– Continuous and constant organic growth

– Hundreds of successful projects on all scales

– Long standing cooperation with universities and software providers

� d-fine as a separate legal entity

– Since July 2002 – d-fine GmbH, Frankfurt and Munich

– Since Nov 2004 – d-fine Ltd, London

– Since October 2007: d-fine (HK) Ltd, Hong Kong

Slide # 5© 2010 d-fine All rights reserved.

– Since October 2007: d-fine (HK) Ltd, Hong Kong

2000 2005 20101996

50

100

150

200

250

nu

mb

er

of

co

nsu

ltan

ts

spin off from Arthur Andersen

office in London

office in Hong Kong

defining d-fine

Our People

Slide # 6© 2010 d-fine All rights reserved.

Our People

defining d-fine

Our international team

� Deep technical and mathematical skills- 60% physicists, 25% mathematicians, 15% Other (IT, MBA, Economics, ...)

- 75% PhD level degrees, 25% master level degrees- Typically in top percentile of their class at university

� Well balanced profiles- Analytical abilities- Technology expertise- Social and management skills

� Continuous and intensive training

Slide # 7© 2010 d-fine All rights reserved.

� Continuous and intensive training- MSc in Mathematical Finance @ University of Oxford- MSc in Quantitative Finance @ Frankfurt School of Finance & Management- MBA @ l'Ecole des Hautes Etudes Commerciales (HEC) de Lausanne- MBA @ Mannheim Business School- CFA (Chartered Financial Analyst)- Actuary- Corporate Finance with University of Warwick- State of the art know-how through internal research, cooperation with leading

universities, regular attendance at conferences and seminars

� Extensive finance industry and implementation know-how- Practical applicability of models irrespective of level of theoretical

sophistication- Wealth of experience gained through successful delivery of hundreds of

projects

- Our senior staff can look back on many years of hands-on client engagements

defining d-fine

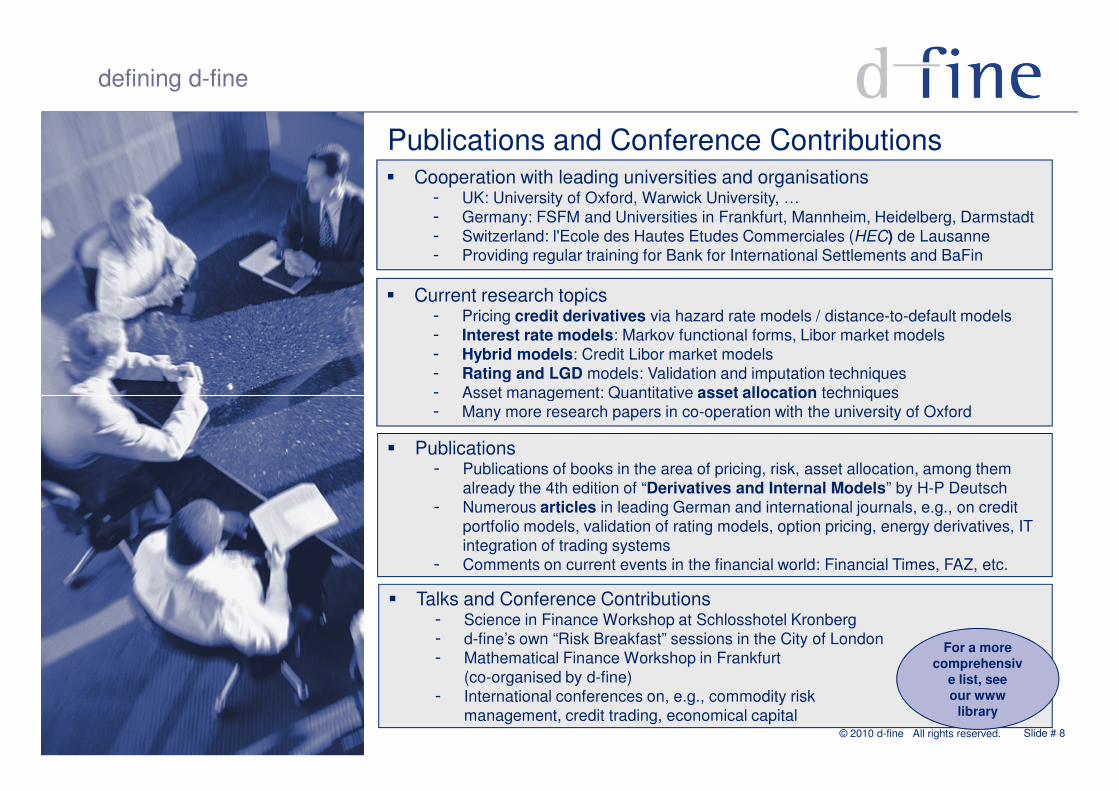

Publications and Conference Contributions� Cooperation with leading universities and organisations

- UK: University of Oxford, Warwick University, …- Germany: FSFM and Universities in Frankfurt, Mannheim, Heidelberg, Darmstadt

- Switzerland: l'Ecole des Hautes Etudes Commerciales (HEC) de Lausanne - Providing regular training for Bank for International Settlements and BaFin

� Current research topics- Pricing credit derivatives via hazard rate models / distance-to-default models

- Interest rate models: Markov functional forms, Libor market models- Hybrid models: Credit Libor market models- Rating and LGD models: Validation and imputation techniques

- Asset management: Quantitative asset allocation techniques

Slide # 8© 2010 d-fine All rights reserved.

� Publications- Publications of books in the area of pricing, risk, asset allocation, among them

already the 4th edition of “Derivatives and Internal Models” by H-P Deutsch- Numerous articles in leading German and international journals, e.g., on credit

portfolio models, validation of rating models, option pricing, energy derivatives, IT integration of trading systems

- Comments on current events in the financial world: Financial Times, FAZ, etc.

� Talks and Conference Contributions- Science in Finance Workshop at Schlosshotel Kronberg- d-fine’s own “Risk Breakfast” sessions in the City of London- Mathematical Finance Workshop in Frankfurt

(co-organised by d-fine)

- International conferences on, e.g., commodity risk

management, credit trading, economical capital

- Asset management: Quantitative asset allocation techniques- Many more research papers in co-operation with the university of Oxford

For a more

comprehensiv

e list, see

our www

library

defining d-fine

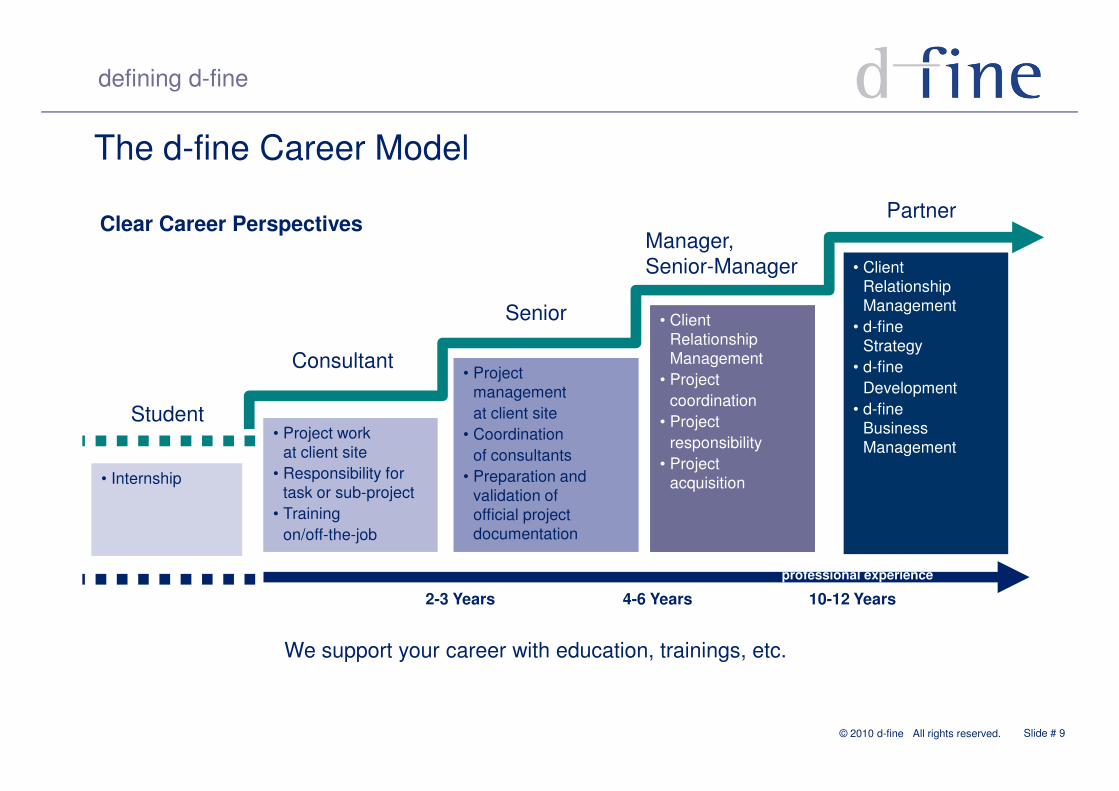

The d-fine Career Model

Consultant

Senior

Manager,

Senior-Manager

Partner

• Project management

• Client Relationship Management

• Project

coordination

• Client

Relationship Management

• d-fineStrategy

• d-fine

Development

Clear Career Perspectives

Slide # 9© 2010 d-fine All rights reserved.

Student• Project work

at client site

• Responsibility for task or sub-project

• Training

on/off-the-job

management

at client site

• Coordination

of consultants

• Preparation andvalidation of official project documentation

coordination

• Project

responsibility

• Projectacquisition

Development

• d-fine Business Management

• Internship

2-3 Years 4-6 Years 10-12 Years

professional experience

We support your career with education, trainings, etc.

defining d-fine

Your Life at d-fine

Free Choice of Location• You may live wherever you like• We take care of your business travel

and accommodation

Attractive compensation• Competitive fixed salary plus bonus• Pension fund and insurance• 30 days annual leave (in Germany)• Company car programme

Absolutely unique further education • cooperation with Oxford-University, Frankfurt School of

Slide # 10© 2010 d-fine All rights reserved.

• cooperation with Oxford-University, Frankfurt School of Management & Finance, Warwick Business School, HEC Lausanne

• CFA, MBA and MSc possible• regular attendance at international seminars and

conferences• Soft-Skill and other In HouseTrainings

...last not least: interesting projects at top companies all over Europe

Great working atmosphere• dynamic and un-bureaucratic structure• work among „like-minded“ people

defining d-fine

Our Services

Slide # 11© 2010 d-fine All rights reserved.

Our Services

defining d-fine

Our Market Position

Bu

sin

ess K

no

w H

ow

Large

Strategy consulting

d-fine

Combines business know how and technical expertise of a large multi-disciplinary firm, but independent of any audit business

Slide # 12© 2010 d-fine All rights reserved.

IT consulting

Bu

sin

ess K

no

w H

ow

Technology Skills and Implementation Ability

Large professional

services firms

„Big Four“

defining d-fine

� Large, medium sized, and specialised banks� Insurances, asset managers, hedge funds� International industry corporations

Our clients

►

Our client list (abridged):

ampegaGerlingARAGBarclays Capital (UK)BayernLBBBVA (ES)

Hannover RückHBOS (UK)HSBC (UK)HSH NordbankHVB

Slide # 13© 2010 d-fine All rights reserved.

►

BBVA (ES)CommerzbankCOMINVESTCQS Management (UK)Daewoo Securities (ROK)DaimlerDBS (SG) DekaBankDeutsche Bank Deutsche BundesbankDG HypDeutsche PostbankDVB BankDZ Bank E.ONEurohypo

HVBKfWLandesbank Baden-WürttembergLandesbank BerlinMEAGNRW.BankRaiffeisen International (AT)RZB (AT)SchiffsbankSiemens Financial ServicesSparkasse KölnBonnStandard Bank (UK)ToyotaUnion InvestmentVW Financial Services (DE/UK)WestLB

defining d-fine

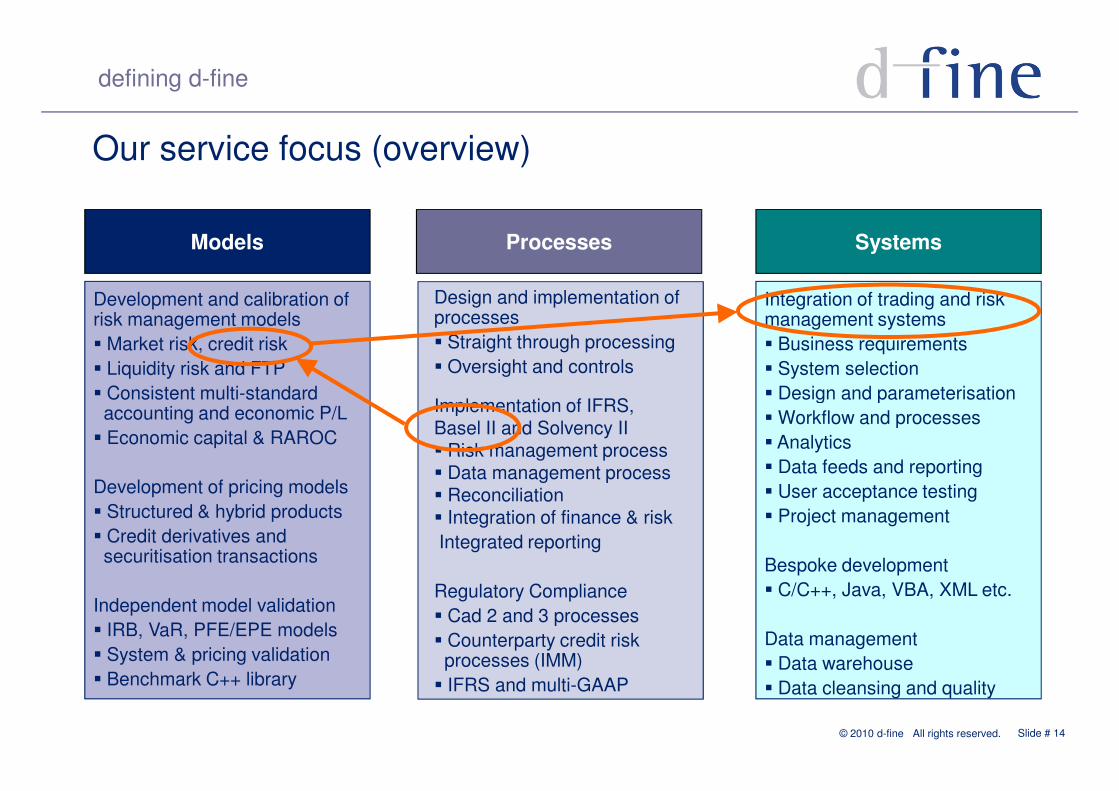

Our service focus (overview)

Models Processes Systems

Development and calibration of risk management models

� Market risk, credit risk

� Liquidity risk and FTP

� Consistent multi-standard

Design and implementation of processes

� Straight through processing

� Oversight and controls

Implementation of IFRS,

Integration of trading and risk management systems

� Business requirements

� System selection

� Design and parameterisation

Slide # 14© 2010 d-fine All rights reserved.

� Consistent multi-standardaccounting and economic P/L

� Economic capital & RAROC

Development of pricing models

� Structured & hybrid products

� Credit derivatives andsecuritisation transactions

Independent model validation

� IRB, VaR, PFE/EPE models

� System & pricing validation

� Benchmark C++ library

Implementation of IFRS,Basel II and Solvency II� Risk management process� Data management process� Reconciliation� Integration of finance & risk

Integrated reporting

Regulatory Compliance

� Cad 2 and 3 processes

� Counterparty credit riskprocesses (IMM)

� IFRS and multi-GAAP

� Design and parameterisation

� Workflow and processes

� Analytics

� Data feeds and reporting

� User acceptance testing

� Project management

Bespoke development

� C/C++, Java, VBA, XML etc.

Data management

� Data warehouse

� Data cleansing and quality

defining d-fine

Our Services

� Independent valuation of Financial Products– Validation of client’s pricing models

– Benchmarking vs d-fine’s bespoke ‘MoCo’ library

– Selection of pricing models, hedging calculations, portfolio viewpoint

– From simple instruments to complex OTC derivatives and structured Products

– Development of risk management methodologies

Slide # 15© 2010 d-fine All rights reserved.

– Development of risk management methodologies

– Containing interest rate risk, equity risk, FX risk, all other market risks, and credit risk

� IAS/IFRS implementation

– IAS 39 incl. hedge accounting tools

– Full fledge implementations

� CAD 2, Basel II(I), CRD (CAD 3) implementation– Internal models for market risk

– Internal ratings based models (IRB)

– Internal Capital Adequacy Assessment Process (ICAAP)

– FSA Prudential Sourcebook (PRU)

– Liquidity Standards (Basel III)

defining d-fine

Our Services (cont’d)

� Development of Rating Systems– Retail IRB, Foundation IRB, Advanced IRB

– PD, LGD, CCF, EAD calculation

– Corporate, Retail, Banks, non-banking Financial Institutions,Funds, Project Finance

� System specification, validation, selection, customisation and implementation– For trading front and back office

Slide # 16© 2010 d-fine All rights reserved.

– For trading front and back office

– For risk management and risk controlling (e.g. VaR)

– For treasury and ALM

� Development of optimisation techniques for– Asset and capital allocation (e.g. triple-alpha)

– Risk adjusted portfolio optimisation (RAROC)

– Asset liability management (ALM)

� In house training at any level from top management to technical experts– On quantitative finance or risk management techniques

– On specific IT systems

– On Basel II, CRD, CAD 3, IAS 39, ICAAP, PRU

defining d-fine

Our IT Expertise – Systems (abridged)

� Trading systems– Calypso, Front Arena, Kondor+, Murex

– Summit, Sophis Risque, Trema …

� ALM and Treasury systems– Almonde, Algorithmics ALM,

– Simcorp Dimension

– Fermat, RiskPro, Trema...

Slide # 17© 2010 d-fine All rights reserved.

– Fermat, RiskPro, Trema...

� Market and Reference Data systems– Asset Control, Xenomorph, ...

– Data Vendors

• ThomsonReuters, Bloomberg, Mark-it Partners, …

� Risk Management systems – Algorithmics Suite / RiskWatch

– FERMAT, Misys RiskVision

– Sungard Adaptiv, Credient, ...

– SAS Risk Dimensions, ...

defining d-fine

Our IT Expertise – Tools (abridged)

� C(++) – various system APIs & pricing libraries– Risk++ (Algorithmics)

– Formula Engine/C-API (Asset Control)

– Xenomorph Analytics Modules

– d-fine’s bespoke ‘MoCo’ library

� Java – platform independent software clients– Various GUIs for Asset Control

� Data base / scripting / macro languages

Slide # 18© 2010 d-fine All rights reserved.

� Data base / scripting / macro languages– Various SQL dialects

– Python (Front Arena AEL)

– PERL (data pre-processing for e.g. Algo, AC)

– SAS, S-PLUS (e.g., development of Rating and LGD Models)

– UNIX shell scripts (process scheduling)

� Middleware / EAI– XML data modelling

– IBM MQSeries

– Vitria BusinessWare

– Reuters Tibco

– webMethods

defining d-fine

Work Examples

Slide # 19© 2010 d-fine All rights reserved.

Work Examples

defining d-fine

Examples of our Work: Credit Rating Systems

0%

20%

40%

60%

80%

100%

))(()( 1

alldefault

*xxy

−ΦΦ=

X=all

Y=defaults

M

freq

uen

cy

M

freq

uen

cy

0

50

100

150

200

250

300

350

400

0 25 50 75 1000

1

2

3

4

5

6

0 25 50 75 100

all defaulted

metric = scoremetric = score

Cumulative

Distributions Fit:

Power Curve, Lorenz Curve, Receiver

Operations Characteristic

Slide # 20© 2010 d-fine All rights reserved.

0% 20% 40% 60% 80% 100%M

freq

uen

cy

M

freq

uen

cy

0

50

100

150

200

250

300

350

400

0 25 50 75 1000

1

2

3

4

5

6

0 25 50 75 100

metric = scoremetric = score

( )( )Mxxx

yPDMPD

=∂

∂⋅=

0%

2%

4%

6%

0 20 40 60 80 100Score M

PD

(M)

rating class

( )

PD

dxxy

G−

−⋅

=∫

1

12

1

0

Discriminary Power,

Gini Coefficient,

Accuracy Ratio

Default Probabilty

Default

Probabilty

defining d-fine

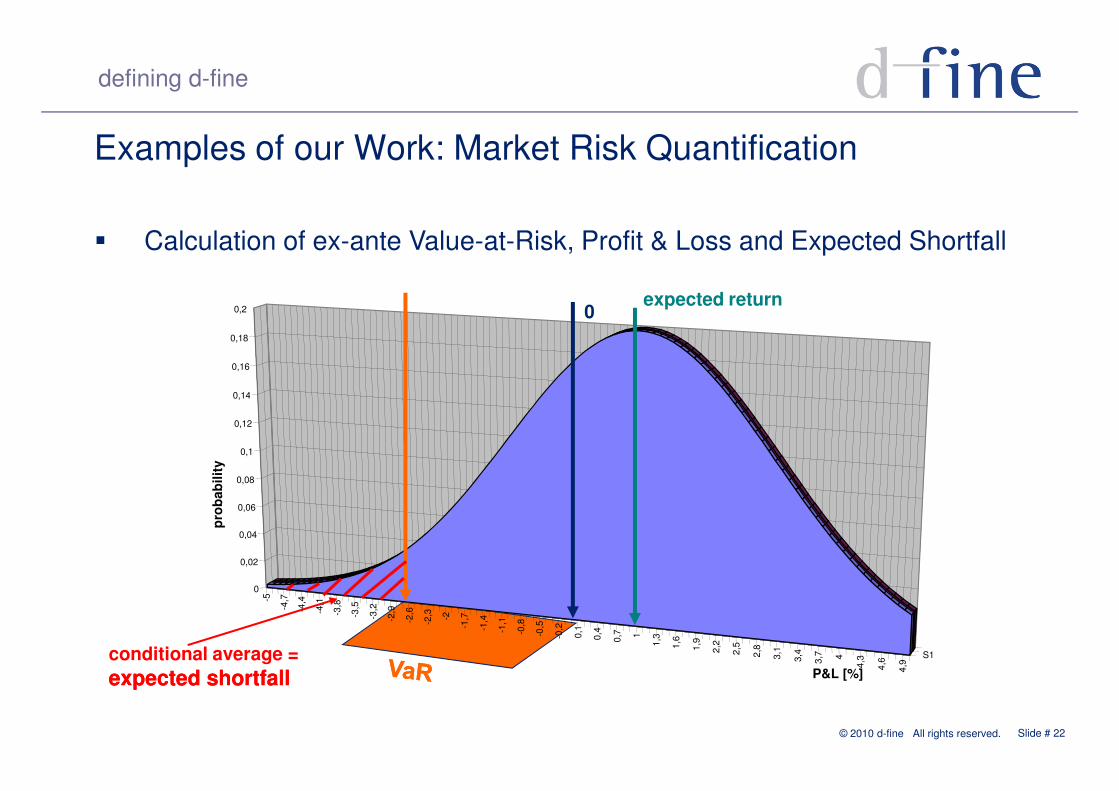

Examples of our Work: Market Risk Quantification

STOXX 50

1%

2%

3%

4%

5%

6%

7%

Dail

y R

etu

rns

4000

5000

6000

7000

Slide # 21© 2010 d-fine All rights reserved.

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

04.0

1.2

000

04.0

3.2

000

04.0

5.2

000

04.0

7.2

000

04.0

9.2

000

04.1

1.2

000

04.0

1.2

001

04.0

3.2

001

04.0

5.2

001

04.0

7.2

001

04.0

9.2

001

04.1

1.2

001

04.0

1.2

002

04.0

3.2

002

04.0

5.2

002

04.0

7.2

002

04.0

9.2

002

04.1

1.2

002

04.0

1.2

003

04.0

3.2

003

Dail

y R

etu

rns

0

1000

2000

3000

Returns

Value at Risk

Expected Shortfall

Volatility

Price

defining d-fine

Examples of our Work: Market Risk Quantification

� Calculation of ex-ante Value-at-Risk, Profit & Loss and Expected Shortfall

0,14

0,16

0,18

0,2 0expected return

Slide # 22© 2010 d-fine All rights reserved.

-5

-4,7

-4,4

-4,1

-3,8

-3,5

-3,2

-2,9

-2,6

-2,3 -2

-1,7

-1,4

-1,1

-0,8

-0,5

-0,2

0,1

0,4

0,7 1

1,3

1,6

1,9

2,2

2,5

2,8

3,1

3,4

3,7 4

4,3

4,6

4,9

S1

0

0,02

0,04

0,06

0,08

0,1

0,12

0,14

pro

bab

ilit

y

P&L [%]

conditional average =

expected shortfallexpected shortfall

defining d-fine

95

100

105

95% quantile (symmetric)

Examples of our Work: Monte Carlo Simulation

� Modelling the P&L distribution with Monte-Carlo simulations of correlated market parameters with stochastic volatility (e.g. GARCH-Models)

( ) dtXtdttSd )()(ln σµ +=

Drift (stochastic) Volatility Random Number

Slide # 23© 2010 d-fine All rights reserved.

65

70

75

80

85

90

0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150 160 170 180 190 200 210 220 230 240 250

time [days]

sto

ck p

rice

[€]

95% quantile (symmetric)

( ) dtXtdttSd )()(ln σµ +=

outliers

defining d-fine

24%

26%

28%

30%

32%

34%

36%

38%

40%

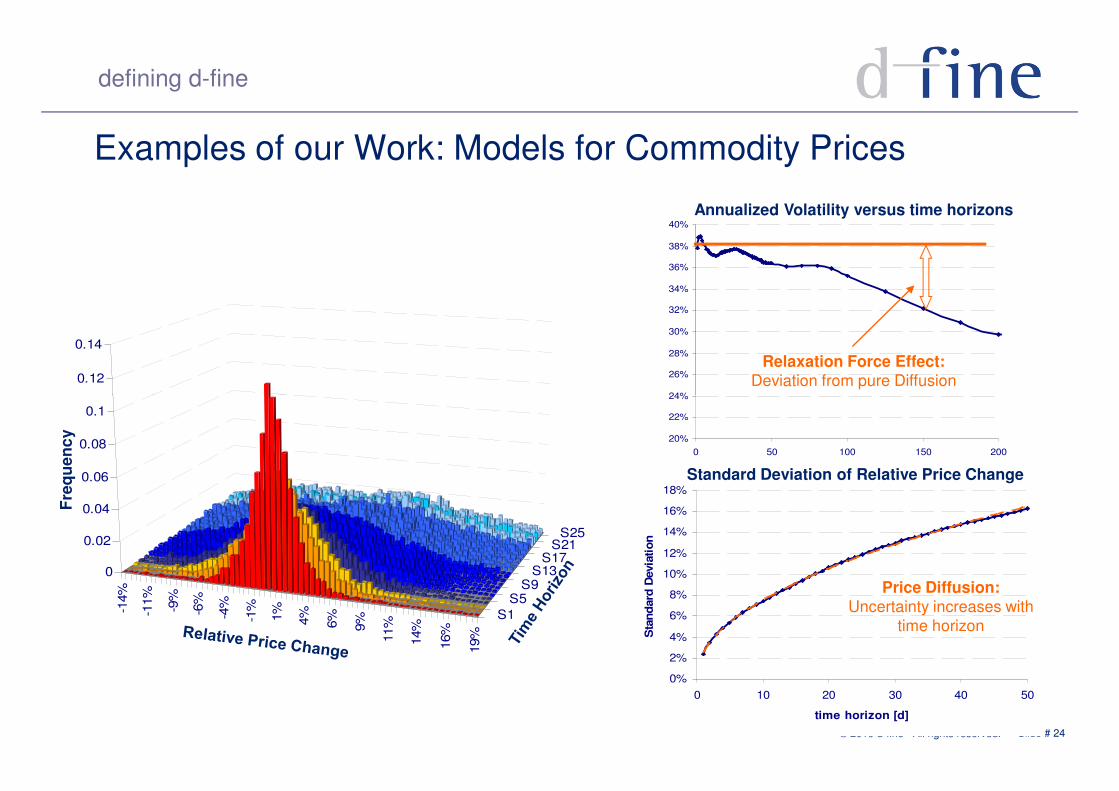

Examples of our Work: Models for Commodity Prices

0.12

0.14

Annualized Volatility versus time horizons

Relaxation Force Effect: Deviation from pure Diffusion

Slide # 24© 2010 d-fine All rights reserved.

20%

22%

24%

0 50 100 150 200

-14%

-11%

-9%

-6%

-4%

-1%

1%

4%

6%

9%

11%

14%

16%

19%

S1

S5S9

S13S17

S21S25

0

0.02

0.04

0.06

0.08

0.1

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0 10 20 30 40 50

time horizon [d]

Sta

nd

ard

Devia

tio

n

Standard Deviation of Relative Price Change

Fre

qu

en

cy

Price Diffusion:Uncertainty increases with

time horizon

defining d-fine

� State of the Art numerical methods like, e.g., Matrix Diagonalization, Copulas, Finite-Differences, Elements etc.

Examples of our Work: Pricing Exotic Derivatives

Slide # 25© 2010 d-fine All rights reserved.

� for instance credit derivatives like CDO2

� for instance wheather derivatives using ARFIMA-FIGARCH Models:

[ ] [ ] 22 )1)(()(1)(1 i

d

ii BBBhB εψεβωβ −−−+=−

defining d-fine

� A process model for a Fonds manager and implementation of the business processes

� Data Management

Examples of our Work: Work Flows and Process Definitions

Slide # 26© 2010 d-fine All rights reserved.

defining d-fine

Your Contact

Wolfgang PleyerPartner

d-fine

FrankfurtMünchenLondon

Slide # 272010 d-fine All rights reserved

Partner

+49 69 – 90737-303

e-Mail: [email protected]

London Hong KongZürich

Zentrale

d-fine GmbHOpernplatz 260313 Frankfurt am MainDeutschland

T. +49 69-90737-0F: +49 69-90737-200

www.d-fine.de