Embed Size (px)

Citation preview

Currency Swaps

1

Currency Swap: Definition

A currency swap is an exchange of a liability in one currency for a liability in another currency.

Nature: • US corporation with operations in France can

obtain comparatively better terms by borrowing dollars, but prefers a loan in euros.

• French corporation with operations in the US can obtain comparatively better terms by borrowing euros, but prefers a loan in dollars.

• The two companies could go to a swap bank who could arrange for a loan swap.

2

Example

As a example, suppose the British Petroleum Company plans to issue five-year bonds worth £100 million at 7.5% interest, but actually needs an equivalent amount in dollars, $150 million (current $/£ rate is $1.50/£), to finance its new refining facility in the U.S.

Also, suppose that the Piper Shoe Company, a U. S. company, plans to issue $150 million in bonds at 10%, with a maturity of five years, but it really needs £100 million to set up its distribution center in London.

3

Example

To meet each other's needs, suppose that both companies go to a swap bank that sets up the following agreements:

4

Example

Agreement 1:

1. The British Petroleum Company will issue 5-year £100 million bonds paying 7.5% interest. It will then deliver the £100 million to the swap bank who will pass it on to the U.S. Piper Company to finance the construction of its British distribution center.

2. The Piper Company will issue 5-year $150 million bonds. The Piper Company will then pass the $150 million to swap bank that will pass it on to the British Petroleum Company who will use the funds to finance the construction of its U.S. refinery.

5

Example

Agreement 2:

1. The British company, with its U.S. asset (refinery), will pay the 10% interest on $150 million ($15 million) to the swap bank who will pass it on to the American company so it can pay its U.S. bondholders.

2. The American company, with its British asset (distribution center), will pay the 7.5% interest on £100 million ((.075)( £100m) = £7.5 million), to the swap bank who will pass it on to the British company so it can pay its British bondholders.

6

Example

Agreement 3:

1. At maturity, the British company will pay $150 million to the swap bank who will pass it on to the American company so it can pay its U.S. bondholders.

2. At maturity, the American company will pay £100 million to the swap bank who will pass it on to the British company so it can pay its British bondholders.

7

ValuationEquivalent Bond Position

Equivalent Bond Position In the above swap agreement, the American company

will receive $15 million each year for five years and a principal of $150 million at maturity and will pay £7.5 million each year for five years and £100 million at maturity.

8

ValuationEquivalent Bond Position

Equivalent Bond Position To the American company, this swap agreement is

equivalent to a position in two bonds:

1. A long position in a dollar-denominated, five-year, 10% annual coupon bond with a principal of $150 million and trading at par

2. A short position in a sterling-denominated, five-year, 7.5% annual coupon bond with a principal of £100 million and trading at par

9

ValuationEquivalent Bond Position

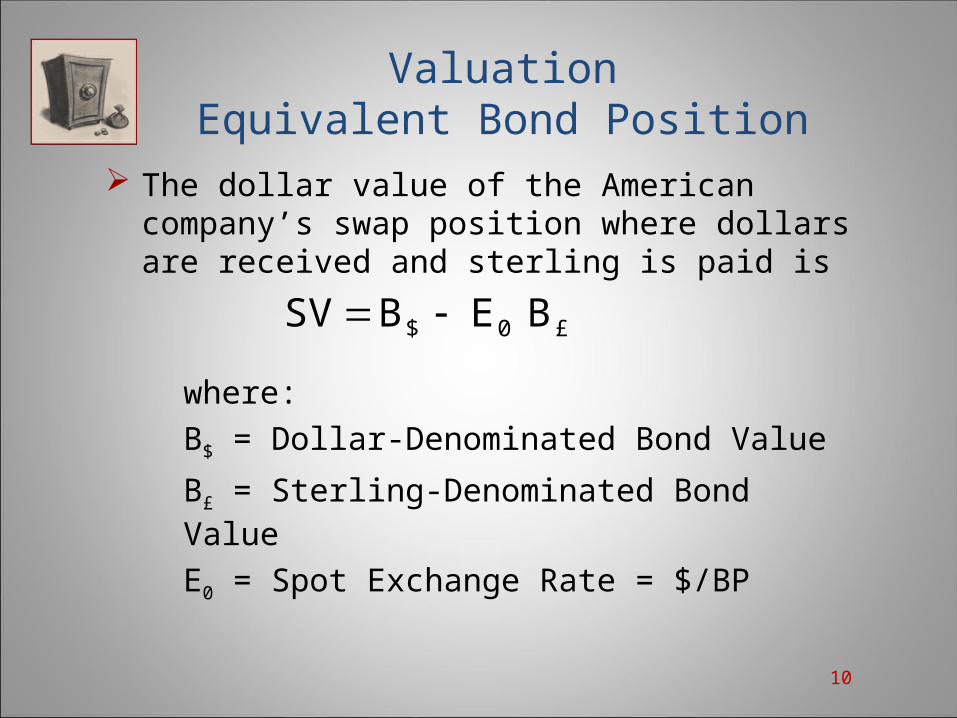

The dollar value of the American company’s swap position where dollars are received and sterling is paid is

where:

B$ = Dollar-Denominated Bond Value

B£ = Sterling-Denominated Bond Value

E0 = Spot Exchange Rate = $/BP

10

£0$ BEBSV

ValuationEquivalent Bond Position

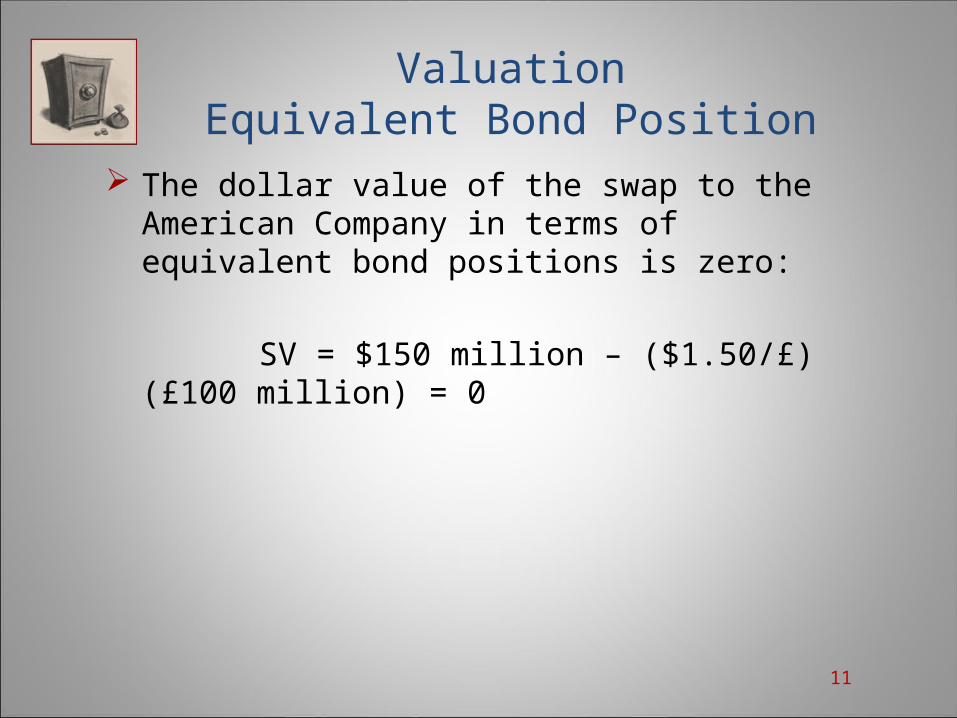

The dollar value of the swap to the American Company in terms of equivalent bond positions is zero:

SV = $150 million – ($1.50/£)(£100 million) = 0

11

ValuationEquivalent Bond Position

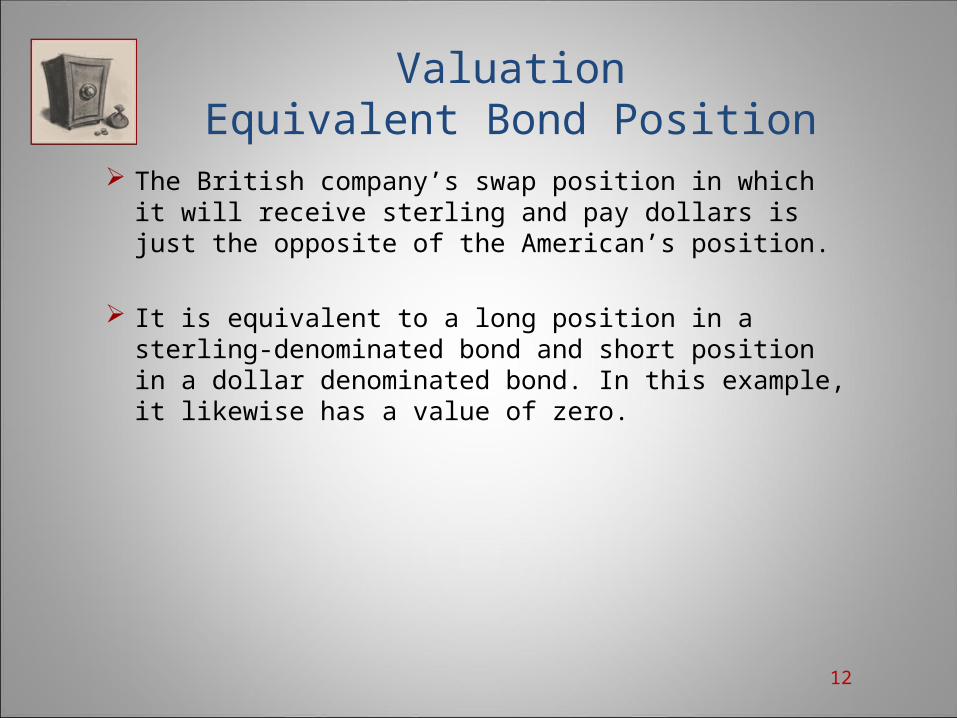

The British company’s swap position in which it will receive sterling and pay dollars is just the opposite of the American’s position.

It is equivalent to a long position in a sterling-denominated bond and short position in a dollar denominated bond. In this example, it likewise has a value of zero.

12

ValuationEquivalent Bond Position

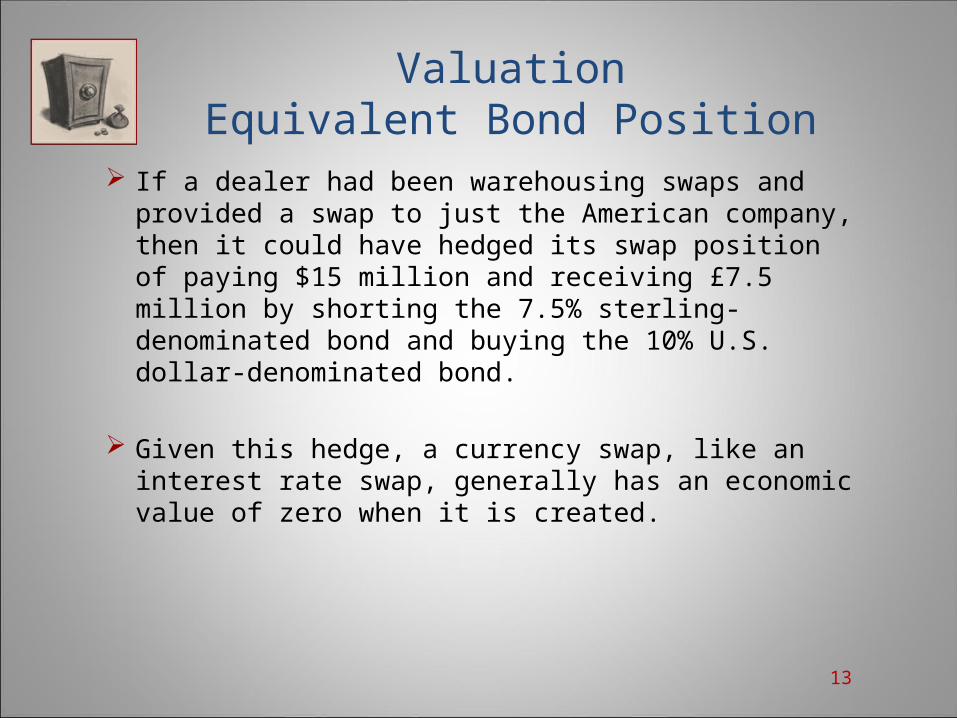

If a dealer had been warehousing swaps and provided a swap to just the American company, then it could have hedged its swap position of paying $15 million and receiving £7.5 million by shorting the 7.5% sterling-denominated bond and buying the 10% U.S. dollar-denominated bond.

Given this hedge, a currency swap, like an interest rate swap, generally has an economic value of zero when it is created.

13

ValuationEquivalent Bond Position

The zero economic value of the swap positions will change over time with changes in U.S. rates, British rates, and the spot exchange rate.

The value of a dollar received/foreign currency paid swap is inversely related to U.S. interest rates and the exchange rate and directly related to the foreign rate.

The value of a foreign currency received/dollar paid swap, valued in dollars, is directly related to U.S. rates and the exchange rate and inversely related to the foreign rate.

14

ValuationEquivalent Forward Exchange Position

Equivalent Forward Exchange Position Instead of viewing its swap as a bond position, the British company

could alternatively view its interest agreement to pay $15 million for £7.5 million each year for five years and it principal agreement to pay $150 million for £100 million at maturity as a series of long currency forward contracts in years 1, 2, 3, 4, and 5.

In contrast, the American company could view its swap agreements to sell £7.5million each year for $15 million and sell £100 million at maturity for $150 million as a series of short currency forward contracts.

15

ValuationEquivalent Forward Exchange Position

Equivalent Forward Exchange Position In the absence of arbitrage, the value of the American company’s

swap of dollar’s received/British pounds paid should be equal to:1. The sum the present values of $15 million received each year from the

swap minus the dollar cost of buying £7.5 million at the forward exchange rate (Eft).

2. The present value of the $150 million received at year five minus the dollar cost of buying £100 million at the five-year forward exchange rate.

The dollar value of the British position is just the opposite.

16

ValuationEquivalent Forward Exchange Position

Equivalent Forward Exchange Position Note that in the absence of arbitrage, the values of the

swap positions as forward contracts are equal to their values as bond positions:

17

FC0$

M

1tt

US

ft BEB)R1(

)PaidFC(E)ceivedRe($SV

Comparative Advantage

The currency swap in the above example represents an exchange of equivalent loans.

Most currency swaps, though, are the result of financial and non-financial corporations exploiting a comparative advantage resulting from different rates in different currencies for different borrowers.

18

Comparative Advantage: Example

Example Suppose the American and British companies have

access to both British (BP) and American ($) lending markets.

Suppose the American company is more creditworthy and can obtain lower rates than the British company in both the US and British markets.

19

Comparative Advantage: Example

Example: Suppose the American company can obtain 10%

U.S. dollar-denominated loans in the U.S. market and 7.25% sterling-denominated loans in the British market, whereas the best the British company can obtain is 11% in the U.S. market and 7.5% in the British market

20

21

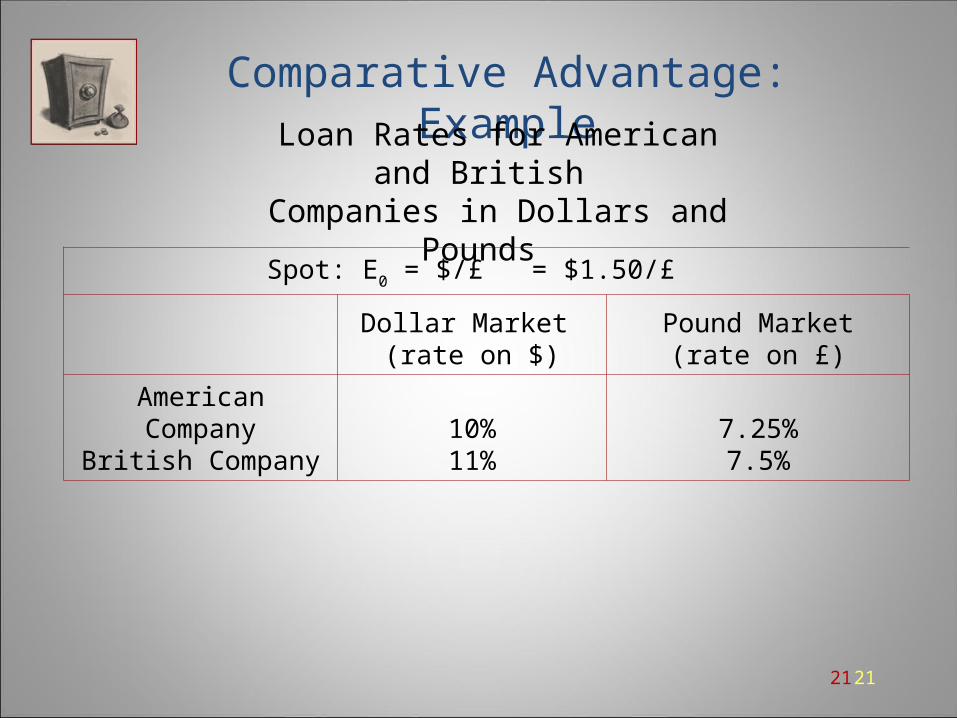

Comparative Advantage: Example

Loan Rates for American and British Companies in Dollars and Pounds

Spot: E0 = $/£ = $1.50/£

Dollar Market (rate on $)

Pound Market (rate on £)

American Company

British Company10%11%

7.25%7.5%

21

Example The American company has a comparative advantage in

the US market: It pays 1% less than the British company in the US

market, compared to only .25% less in the British market.

The British company has a comparative advantage in the British market: It pays .25% more than the American company in the

British market, compared to 1% more in the US market.

Comparative Advantage: Example

22

Comparative Advantage: Example

When a comparative advantage exist, a swap bank is in a position to benefit one or both parties.

23

Comparative Advantage: Example

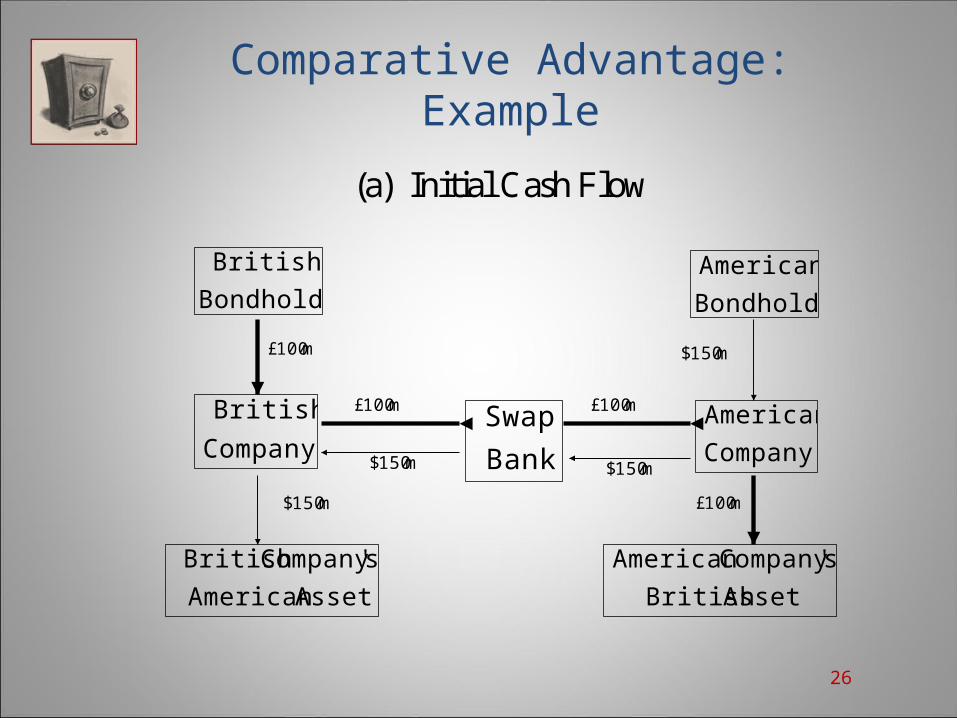

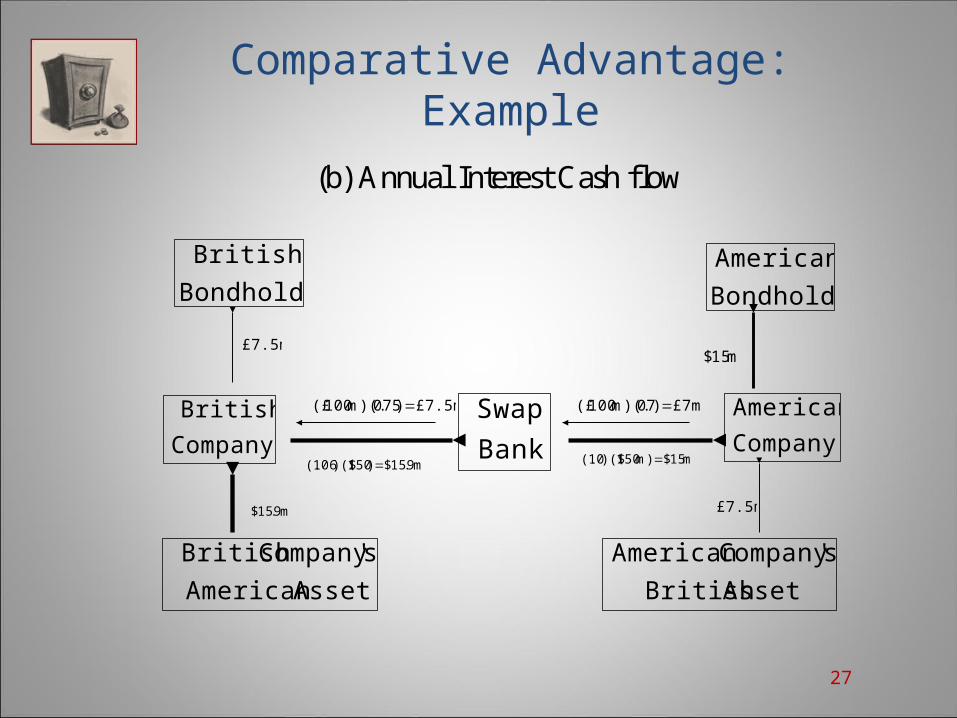

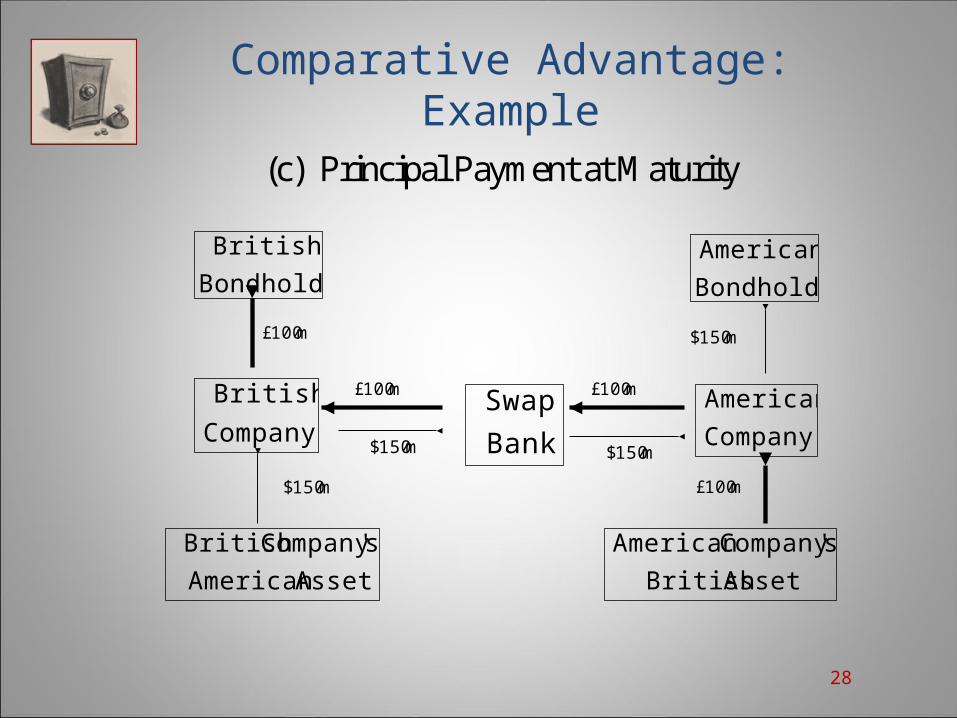

Example: Suppose in this case a swap bank sets up the following

swap arrangement:

1. The American company borrows $150 million at 10%, and then agrees to swap it for £100 million loan at 7%.

2. The British company borrows £100 million at 7.5%, and then agrees to swap it for $150 million loan at 10.6%.

24

Comparative Advantage: Example

The next three exhibit slides show the initial swap of the principals, annual cash flows of interest, and final exchange of the principals.

25

Comparative Advantage: Example

26

(a) Initial Cash Flow

Bondholder

British

Company

British

AssetAmerican

s'CompanyBritish

m100£

Bondholder

American

Company

American

AssetBritish

s'CompanyAmerican

m150$Bank

Swap

m150$

m150$

m150$

m100£

m100£

m100£

Comparative Advantage: Example

27

(b) Annual Interest Cash flow

Bondholder

British

Company

British

AssetAmerican

s'CompanyBritish

£7m)07)(.m100(£

Bondholder

American

Company

American

AssetBritish

s'CompanyAmerican

Bank

Swap

m9.15$)150)($106(.

£7.5m)075)(.m100(£

£7.5m

m15$)m150)($10(.

£7.5m

m9.15$

m15$

Comparative Advantage: Example

28

(c) Principal Payment at Maturity

Bondholder

British

Company

British

AssetAmerican

s'CompanyBritish

m100£

Bondholder

American

Company

American

AssetBritish

s'CompanyAmerican

m150$Bank

Swap

m150$

m150$

m150$

m100£

m100£

m100£

Comparative Advantage:

Swap Bank’s Position In this swap arrangement:

The American company benefits by paying 0.25% less than it could obtain by borrowing British pounds directly in the British market

The British company gains by paying 0.4% less than it could obtain directly from the U.S. market.

29

Comparative Advantage:

Swap Bank’s Position The swap bank in this case will receive $15.9 million

each year from the British company, while only having to pay $15 million to the American company, for a net dollar receipt of $ 0.9 million.

On the other hand, the swap bank will receive only £7 million from the American company, while having to pay £7.5 million to the British company, for a net sterling payment of £0.5 million.

30

Comparative Advantage:

Swap Bank’s Position

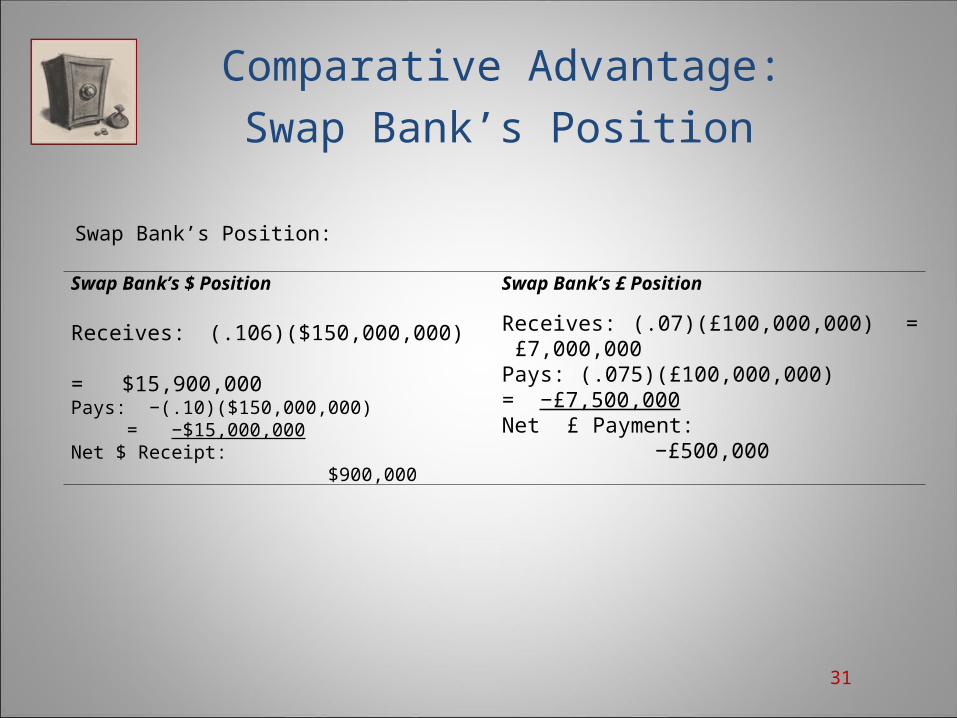

Swap Bank’s Position:

31

Swap Bank’s $ Position

Receives: (.106)($150,000,000) = $15,900,000Pays: −(.10)($150,000,000) = −$15,000,000Net $ Receipt: $900,000

Swap Bank’s £ Position

Receives: (.07)(£100,000,000) = £7,000,000Pays: (.075)(£100,000,000) = −£7,500,000 Net £ Payment: −£500,000

Comparative Advantage:

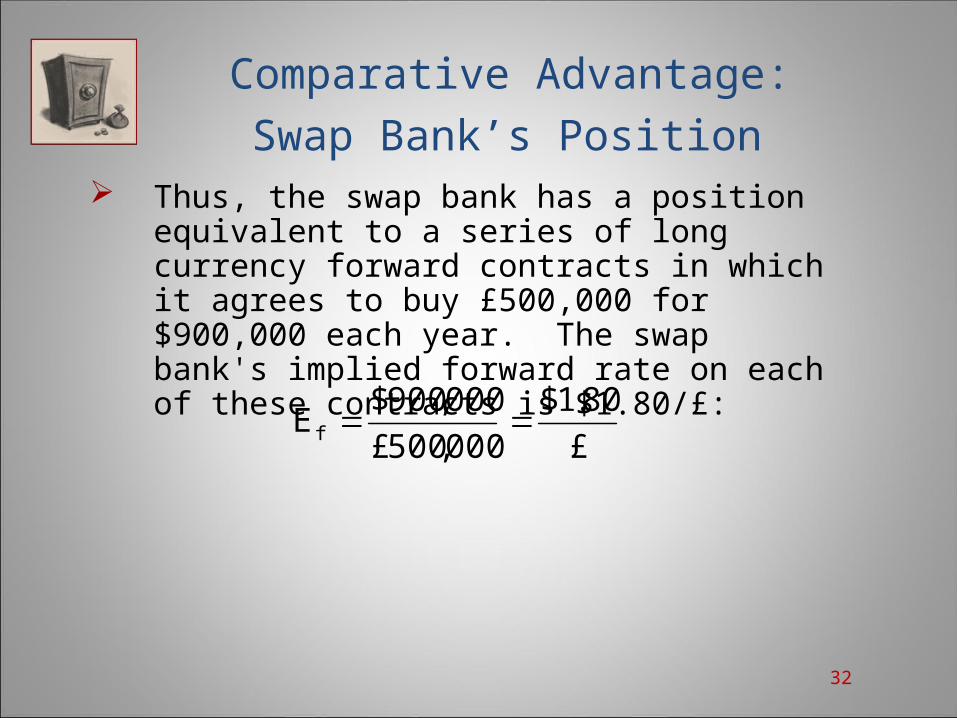

Swap Bank’s Position Thus, the swap bank has a position equivalent to a

series of long currency forward contracts in which it agrees to buy £500,000 for $900,000 each year. The swap bank's implied forward rate on each of these contracts is $1.80/£:

32

£

80.1$

000,500£

000,900$E f

Comparative Advantage:

Swap Bank’s Position The swap bank can hedge its position with currency

forward contracts.

If the forward rate is less than $1.80/£, then the bank could gain from hedging the swap agreement with forward contracts to buy £500,000 each year each year for the next five years.

33

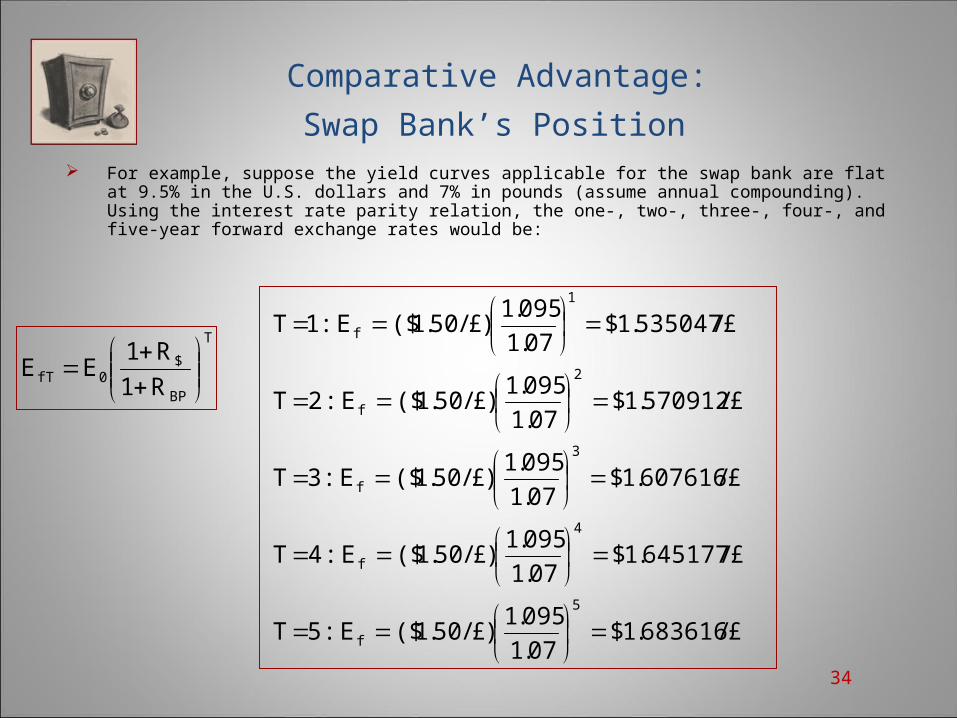

Comparative Advantage:

Swap Bank’s Position For example, suppose the yield curves applicable for the swap bank are flat at 9.5% in the

U.S. dollars and 7% in pounds (assume annual compounding). Using the interest rate parity relation, the one-, two-, three-, four-, and five-year forward exchange rates would be:

34

T

BP

$0fT R1

R1EE

£/683616.1$07.1

095.1)£/50.1($E:5T

£/645177.1$07.1

095.1)£/50.1($E:4T

£/607616.1$07.1

095.1)£/50.1($E:3T

£/570912.1$07.1

095.1)£/50.1($E:2T

£/535047.1$07.1

095.1)£/50.1($E:1T

5

f

4

f

3

f

2

f

1

f

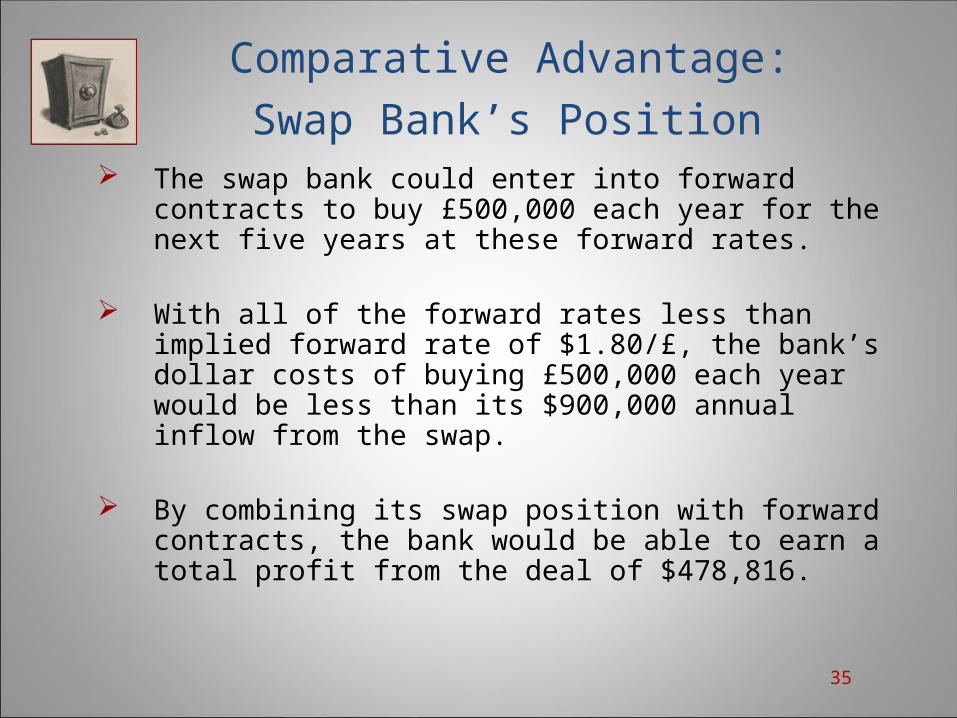

Comparative Advantage:

Swap Bank’s Position The swap bank could enter into forward contracts to

buy £500,000 each year for the next five years at these forward rates.

With all of the forward rates less than implied forward rate of $1.80/£, the bank’s dollar costs of buying £500,000 each year would be less than its $900,000 annual inflow from the swap.

By combining its swap position with forward contracts, the bank would be able to earn a total profit from the deal of $478,816.

35

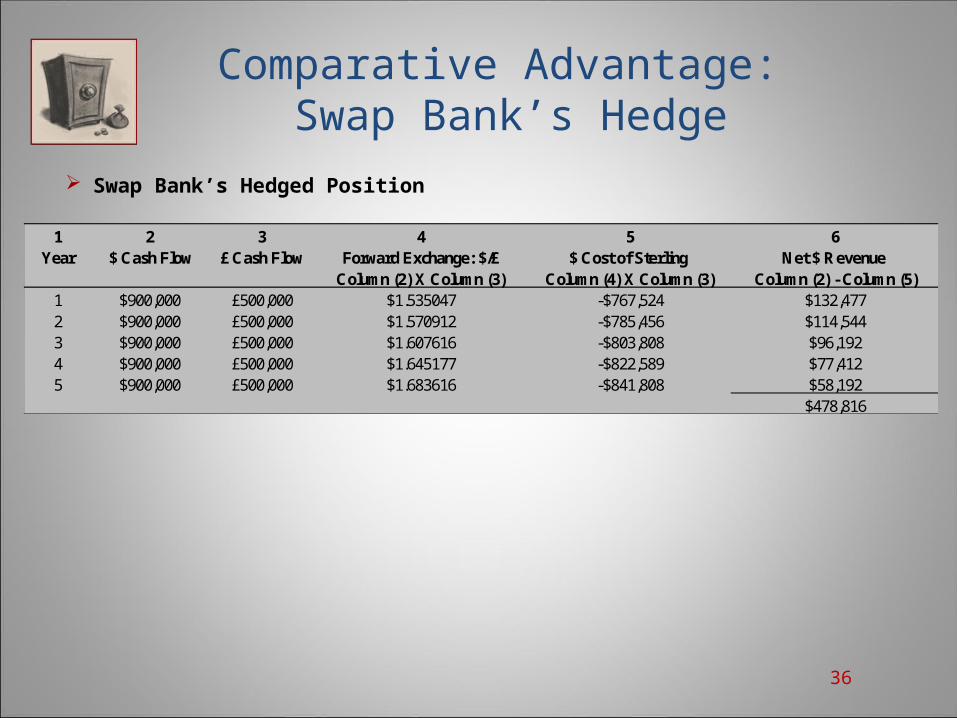

Comparative Advantage: Swap Bank’s Hedge

Swap Bank’s Hedged Position

36

1 2 3 4 5 6Year $ Cash Flow £ Cash Flow Forward Exchange: $/£ $ Cost of Sterling Net $ Revenue

Column (2) X Column (3) Column (4) X Column (3) Column (2) - Column (5)1 $900,000 £500,000 $1.535047 -$767,524 $132,4772 $900,000 £500,000 $1.570912 -$785,456 $114,5443 $900,000 £500,000 $1.607616 -$803,808 $96,1924 $900,000 £500,000 $1.645177 -$822,589 $77,4125 $900,000 £500,000 $1.683616 -$841,808 $58,192

$478,816

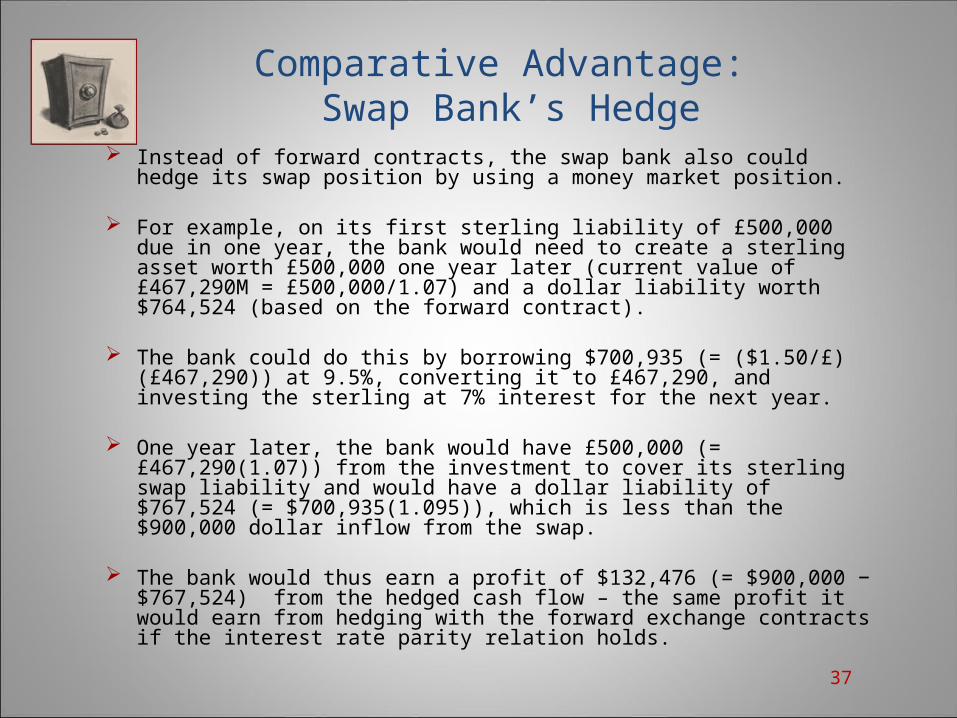

Comparative Advantage: Swap Bank’s Hedge

Instead of forward contracts, the swap bank also could hedge its swap position by using a money market position.

For example, on its first sterling liability of £500,000 due in one year, the bank would need to create a sterling asset worth £500,000 one year later (current value of £467,290M = £500,000/1.07) and a dollar liability worth $764,524 (based on the forward contract).

The bank could do this by borrowing $700,935 (= ($1.50/£) (£467,290)) at 9.5%, converting it to £467,290, and investing the sterling at 7% interest for the next year.

One year later, the bank would have £500,000 (= £467,290(1.07)) from the investment to cover its sterling swap liability and would have a dollar liability of $767,524 (= $700,935(1.095)), which is less than the $900,000 dollar inflow from the swap.

The bank would thus earn a profit of $132,476 (= $900,000 −$767,524) from the hedged cash flow – the same profit it would earn from hedging with the forward exchange contracts if the interest rate parity relation holds.

37

Summary

The presence of comparative advantage creates a currency swap market in which swap banks look at the borrowing rates offered in different currencies to different borrowers and at the forward exchange rates and money market rates that they can obtain for hedging.

Based on these different rates, they will arrange swaps that provide each borrower with rates better than the ones they can directly obtain and a profit for them that will compensate them for facilitating the deal and assuming the credit risk of each counterparty.

38

Non-Generic Currency Swaps

The generic currency swap has been modified to accommodate different uses.

Of particular note is the cross-currency swap that is a combination of the currency swap and interest rate swap. • This swap calls for an exchange of floating-rate payments in

one currency for fixed-rate payments in another.

39

Non-Generic Currency Swaps

Non-Generic Currency Swaps:1. Currency swaps with amortizing principals

2. Cancelable and extendable currency swaps

3. Forward currency swaps

4. Options on currency swaps

40

![Currency Basis Swap Valuation - Theory & Practise1112789/...[8]. This study will focus on the valuation of cross currency swaps in the first line and the second line of defence. Furthermore,](https://img.pdfslide.us/doc/110x75/60bd7d04481a2a45c604a377/currency-basis-swap-valuation-theory-practise-1112789-8-this-study.jpg)