Embed Size (px)

Citation preview

Chris TarryAviation Industry Research and Advisory

CTAIRA

Dreams and Realities

Will the airline industry ever be sufficiently profitable?

Chris Tarry

Guildford

June 11th 2003

Chris TarryAviation Industry Research and Advisory

CTAIRA

A simple business strategy for airlines

Survive

Compete

Prosper

Chris TarryAviation Industry Research and Advisory

CTAIRA

The real cyclical issue – the life cycleFor the airline industry :

Is maturity and decline the only option?

Does structural rigidity mean an inability to change?

Has the managerial prerogative at some airlines been ceded?

Is the fundamental and necessary change impossible?

Are the costs of change too high?

Will there be further exits?

Opportunities for segmental new entrants

Chris TarryAviation Industry Research and Advisory

CTAIRA

Airline traffic and capacity trends

Passnger traffic and capacity index 1972-2002

0

100

200

300

400

500

600

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

Ind

ex 1

972=

100

Passenger traff ic Passenger capacity

Chris TarryAviation Industry Research and Advisory

CTAIRA

Long term industry trends

Load factors and margins 1970 -2000

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

% lo

ad f

acto

r

35.00

45.00

55.00

65.00

75.00

Operating margin Load factor est BE load factor

Chris TarryAviation Industry Research and Advisory

CTAIRA

Reported traffic and GDP

GDP, ASK and RPK 1972-2002

-10

-5

0

5

10

15

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

E

% c

hang

e GDP change

Change (ASK)

RPK change

Data: IMF/IATA

Chris TarryAviation Industry Research and Advisory

CTAIRA

Forecasting issues – traffic and real GDP

Capacity and traffic ratios with GDP

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

10.0019

72

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

x

RPK/GDP

ASK/GDP

Data: IMF, IATA

Chris TarryAviation Industry Research and Advisory

CTAIRA

US Airlines: scheduled traffic and GDP

US airlines: Scheduled traffic and GDP changes

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

% c

han

ge

Traffic Real GDP

Source: BTS/IMF

Chris TarryAviation Industry Research and Advisory

CTAIRA

US traffic multipliers

US airlines : passenger traffic multiplier with GDP

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

Source: BTS/IMF

Chris TarryAviation Industry Research and Advisory

CTAIRA

Long term US yield trends in a mature market

US Domestic yields

0

2

4

6

8

10

12

14

16

18

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

US

c

Nominal Real (1978 cents) Linear (Real (1978 cents)) Linear (Nominal)

Chris TarryAviation Industry Research and Advisory

CTAIRA

US Airlines: Fare changes vs. 2 years ago

Source: ATA

US fares vs 2 years ago

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

Jan-

02

Feb

-02

Mar

-02

Apr

-02

May

-02

Jun-

02

Jul-0

2

Aug

-02

Sep

-02

Oct

-02

Nov

-02

Dec

-02

Jan-

03

Feb

-03

Mar

-03

Apr

-03

% c

han

ge

International Domestic

Chris TarryAviation Industry Research and Advisory

CTAIRA

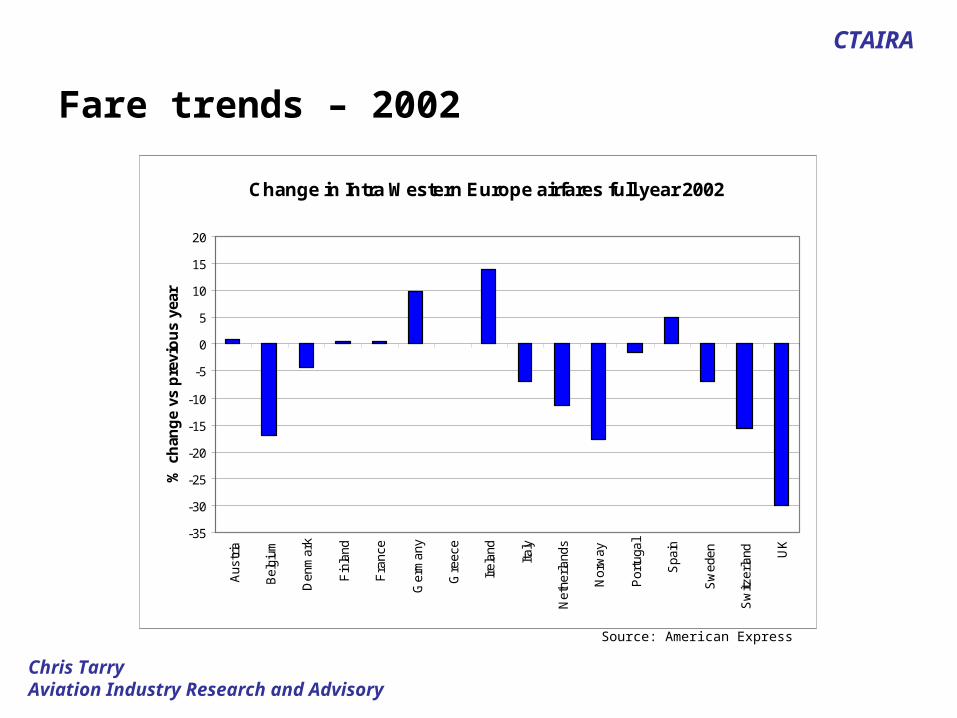

Fare trends – 2002

Source: American Express

Change in Intra Western Europe airfares full year 2002

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

20A

ustr

ia

Bel

gium

Den

mar

k

Fin

land

Fra

nce

Ger

man

y

Gre

ece

Irel

and

Italy

Net

herla

nds

Nor

way

Por

tuga

l

Spa

in

Sw

eden

Sw

itzer

land U

K

% c

han

ge

vs p

revi

ou

s ye

ar

Chris TarryAviation Industry Research and Advisory

CTAIRA

AEA members overall

AEA Airlines all markets vs 2 years ago

-18.00

-16.00

-14.00

-12.00

-10.00

-8.00

-6.00

-4.00

-2.00

0.00

Jan-

02

Feb

-02

Mar

-02

Apr

-02

May

-02

Jun-

02

Jul-0

2

Aug

-02

Sep

-02

Oct

-02

Nov

-02

Dec

-02

Jan-

03

Feb

-03

Mar

-03

Apr

-03

% c

han

ge

Traff ic Capacity

Data: AEA

Chris TarryAviation Industry Research and Advisory

CTAIRA

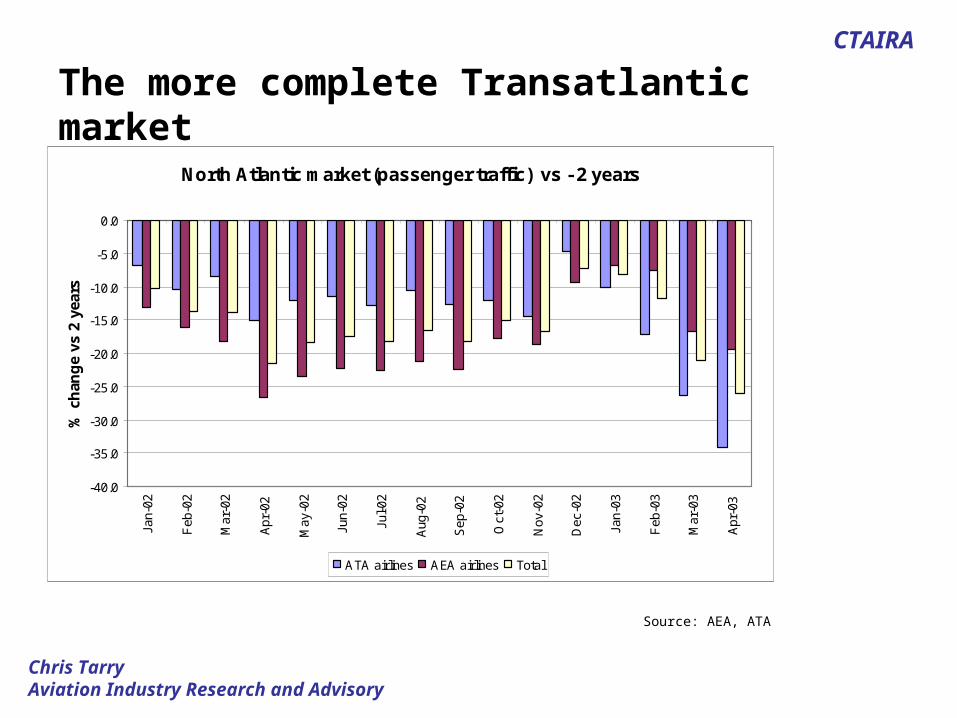

The more complete Transatlantic market

Source: AEA, ATA

North Atlantic market (passenger traffic) vs - 2 years

-40.0

-35.0

-30.0

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

Jan-

02

Feb

-02

Mar

-02

Apr

-02

May

-02

Jun-

02

Jul-0

2

Aug

-02

Sep

-02

Oct

-02

Nov

-02

Dec

-02

Jan-

03

Feb

-03

Mar

-03

Apr

-03

% c

han

ge

vs 2

yea

rs

ATA airlines AEA airlines Total

Chris TarryAviation Industry Research and Advisory

CTAIRA

Forecasting issues –revenue and nominal GDP

Data: IMF, ICAO

Nominal GDP multiplier for Airline Industry revenue

-6.00

-5.00

-4.00

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.0019

71

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

X

Chris TarryAviation Industry Research and Advisory

CTAIRA

Economic Forecasts: Current Prices

1999 2000 2001 2002 2003E 2004E

AUSTRALIA 5.2 7.1 6.3 6.2 7.7 6.0

CHINA,P.R.:HONG KONG -2.6 3.4 -0.7 -0.6 1.3 2.5

FRANCE 3.7 4.7 3.3 2.9 3.0 3.9

GERMANY 2.6 2.6 2.0 1.8 1.6 3.2

ITALY 3.3 5.3 4.6 3.1 3.6 4.1

JAPAN -1.3 0.8 -1.2 -1.4 -0.5 0.1

KOREA 8.6 8.1 4.4 5.9 5.2 8.6

SINGAPORE 0.5 14.3 -3.6 2.4 3.9 5.3

SPAIN 7.1 7.8 6.9 6.5 6.1 6.0

UNITED KINGDOM 5.0 5.3 4.3 4.7 4.8 4.8

UNITED STATES 5.6 5.9 2.6 3.6 4.1 5.8

Source: IMF

Chris TarryAviation Industry Research and Advisory

CTAIRA

Europe: Changing market terminology

Low cost airlineLow fare airlineNew entrant airlineTravellerCustomer Business travellerProductCommoditySegment

Chris TarryAviation Industry Research and Advisory

CTAIRA

Product issues

What constitutes the product offer?The flight?

Flexibility?

Timing?

Frequency?

Airport attractiveness?

On board service?

On ground service

It depends – Each of us will value and price the attributes differently

Chris TarryAviation Industry Research and Advisory

CTAIRA

The London area experience

Source: CAA

% change in intra EU schduled passenger numbers

-20.00

-10.00

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

1998 1999 2000 2001 2002

% c

han

ge

LGW LHR LCY LTN STN

Chris TarryAviation Industry Research and Advisory

CTAIRA

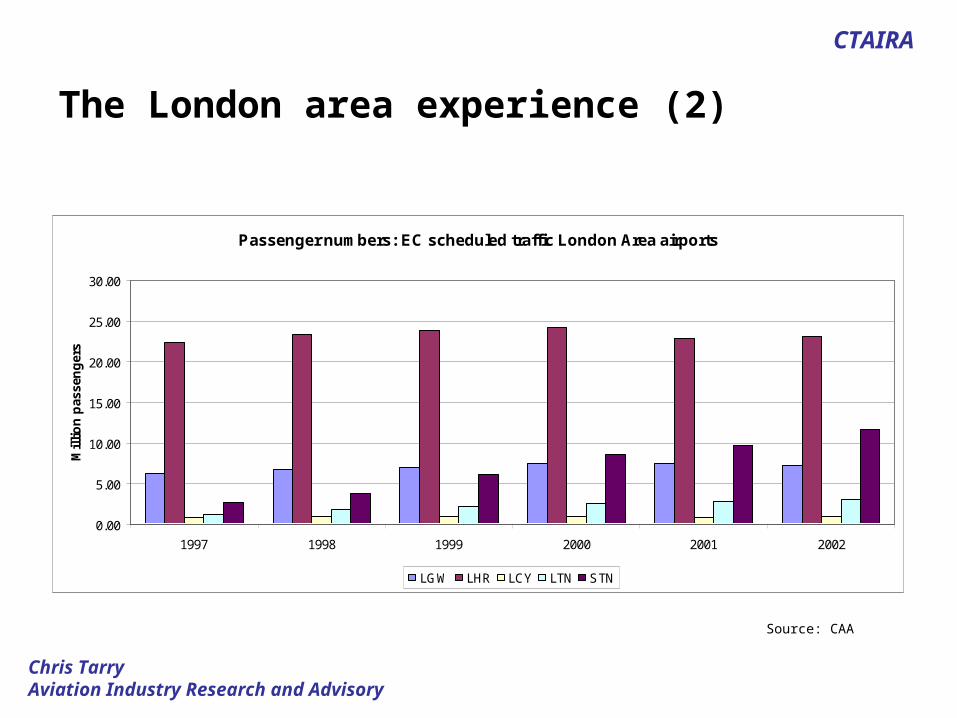

The London area experience (2)

Source: CAA

Passenger numbers: EC scheduled traffic London Area airports

0.00

5.00

10.00

15.00

20.00

25.00

30.00

1997 1998 1999 2000 2001 2002

Mil

lio

n p

asse

ng

ers

LGW LHR LCY LTN STN

Chris TarryAviation Industry Research and Advisory

CTAIRA

The London area experience (3)

Source: CAA

Changing shares: London area EC scheduled traffic

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

1997 1998 1999 2000 2001 2002

% o

f th

e to

tal

LGW LHR LCY LTN STN

Chris TarryAviation Industry Research and Advisory

CTAIRA

The Mainline response (1)

With a focus on:Price discriminators

Quality discriminators

Now able to offer “more options”Club to Full fare Economy

Full Fare Economy to Restricted Economy

Fundamentally changed “rules of engagement”

Chris TarryAviation Industry Research and Advisory

CTAIRA

Mainline response (2)

Fare structure simplification

Easier internet booking process

Raising awareness of value proposition

Chris TarryAviation Industry Research and Advisory

CTAIRA

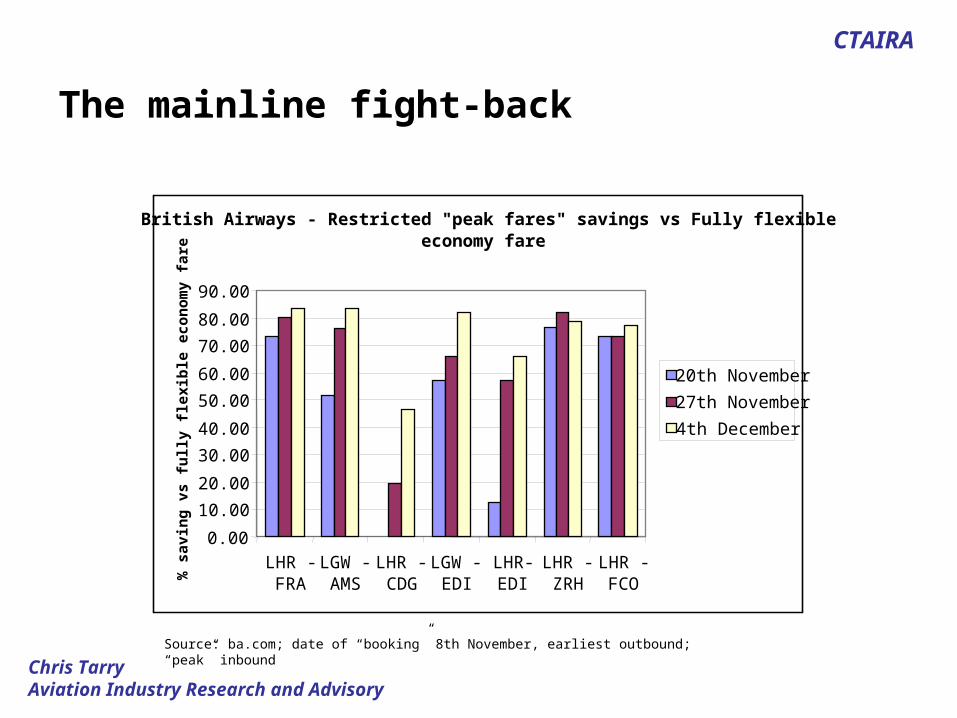

The mainline fight-back

Source: ba.com; date of “booking” 8th November, earliest outbound; “peak” inbound

British Airways - Restricted "peak fares" savings vs Fully flexible economy fare

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

LHR -FRA

LGW -AMS

LHR -CDG

LGW -EDI

LHR-EDI

LHR -ZRH

LHR -FCO

% s

avin

g v

s fu

lly

flex

ible

eco

no

my

fare

20th November

27th November

4th December

Chris TarryAviation Industry Research and Advisory

CTAIRA

The mainline fight-back

British Airways: lowest restricted "peak fares" + fully flexible one way - saving or loss vs fully flexible return

-60.00

-50.00

-40.00

-30.00

-20.00

-10.00

0.00

10.00

20.00

30.00

40.00

LHR -FRA

LGW -AMS

LHR -CDG

LGW -EDI

LHR-EDI

LHR -ZRH

LHR -FCO

% s

avin

g o

r lo

ss v

s fu

lly f

lexi

ble

eco

no

my

fare

20th November

27th November

4th December

Source: ba.com; date of “booking” 8th November, earliest outbound; “peak” inbound

Chris TarryAviation Industry Research and Advisory

CTAIRA

The UK in an intra-European context

Source: American Express

Intra European economy fares as % of European average Q4 2002

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0S

witz

erla

nd

Aus

tria

Bel

gium Ita

ly

Ger

man

y

Den

mar

k

Fra

nce

Fin

land

Net

herla

nds

Sw

eden U

K

Gre

ece

Irel

and

Spa

in

% o

f E

uro

pea

n a

vera

ge

Economy Leisure

Economy

Chris TarryAviation Industry Research and Advisory

CTAIRA

Traffic experience at British Airways

Source: Company reports

British Airways: UK and Europe RPKs and ASKs vs - 2 years

-18.00

-16.00

-14.00

-12.00

-10.00

-8.00

-6.00

-4.00

-2.00

0.00

Apr-02

May-02

Jun-02

Jul-02 Aug-02

Sep-02

Oct-02

Nov-02

Dec-02

Jan-03

Feb-03

Mar-03

Apr-03

% c

han

ge

vs -

2 y

ears

Traff ic Capacity

Chris TarryAviation Industry Research and Advisory

CTAIRA

Traffic mix issues - overall

Source: British Airways

British Airways Premium traffic trends index 1996=100

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00A

pril

May

June

July

Aug

ust

Sep

tem

ber

Oct

ober

Nov

embe

r

Dec

embe

r

Janu

ary

Feb

ruar

y

Mar

ch

Ind

ex 1

996

= 1

00

FY2001 FY2002 FY 2003 FY 2004

Chris TarryAviation Industry Research and Advisory

CTAIRA

Traffic mix issues - overall

Source: British Airways

British Airways non-Premium traffic index 1996 = 100

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

Apr

il

May

June

July

Aug

ust

Sep

tem

ber

Oct

ober

Nov

embe

r

Dec

embe

r

Janu

ary

Feb

ruar

y

Mar

ch

1996

= 1

00

FY2001 FY2002 FY 2003 FY 2004

Chris TarryAviation Industry Research and Advisory

CTAIRA

British Airways: Operating profit and margin

British Airways: Operating profit and margin trends

-100

0

100

200

300

400

500

600

700

800

900

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

£m

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

%

Operating profit Margin

Chris TarryAviation Industry Research and Advisory

CTAIRA

British Airways: Capacity and traffic trends (1)

Changes in capacity and traffic 1984 - 2003

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

% c

han

ge

vs p

revi

ou

s ye

ar

ATK RTK

Chris TarryAviation Industry Research and Advisory

CTAIRA

British Airways: Capacity and traffic trends (2)

British Airways: Traffic, capacity and revenue 1984-2003

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Ind

ex 1

984

= 1

00

Yield per RTK Yield per ATK ATK RTK

Chris TarryAviation Industry Research and Advisory

CTAIRA

British Airways: Load factors and profit margins

British Airways - load factors and margins

-5.00

0.00

5.00

10.00

15.00

20.00

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

% m

arg

in

56.00

58.00

60.00

62.00

64.00

66.00

68.00

70.00

72.00

load

fac

tor

%

Op margin Load factor B/E load factor

Chris TarryAviation Industry Research and Advisory

CTAIRA

Changes in break even load factors

Source: company data

British Airways: Breakeven and yield

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Yield per ATK Break even Load Factor % change

Chris TarryAviation Industry Research and Advisory

CTAIRA

British Airways: Average revenue per passenger

British Airways; Passenger revenue per passenger

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

200.00

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

£

Chris TarryAviation Industry Research and Advisory

CTAIRA

British Airways: Volume sensitivities

Source: company data

British Airways; Costs revenues and capacity

20

22

24

26

28

30

32

34

36

38

40

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

pen

ce

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

% c

han

ge

Cost per ATK Revenue per ATK ATK change

Chris TarryAviation Industry Research and Advisory

CTAIRA

British Airways: Revenues and Costs (index)

British Airways: Cost and Revenue per ATK

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Ind

ex 1

984=

100

Cost per ATK Revenue per ATK

Chris TarryAviation Industry Research and Advisory

CTAIRA

British Airways: Productivity measures compared

Source: Company data

British Airways; Measures of employee productivity

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

AT

Ks

per

em

plo

yee

(000

)

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Em

plo

yee mu

ltiplier (x)

ATKs per employee Employee multiplier

Chris TarryAviation Industry Research and Advisory

CTAIRA

British Airways : Productivity measures compared

Source: Company data

British Airways: Productivity measures compared (1992=100)

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Ind

ex F

Y 1

992=

100

ATKs per employee Employee multiplier

Chris TarryAviation Industry Research and Advisory

CTAIRA

British Airways: Total performance measurement

Data:: British Airways

British Airways: Total performance measurement

60.00

70.00

80.00

90.00

100.00

110.00

120.00

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Ind

ex 1

993

= 1

00

Traff ic revenue per ATK Revenue per f lying hour Net operating cost per f lying hour

Chris TarryAviation Industry Research and Advisory

CTAIRA

For the mainline airlines - what needs to be done? Reduce of structural excess supply

Differentiate increasingly commoditised products

Address the gap between “customer and the traveller”

React to changing market structures

Structurally reduction of cost

Improve shareholder returns

Chris TarryAviation Industry Research and Advisory

CTAIRA

Will airlines make sufficient profits?

It depends, but the consequences of failure include:

– Increased perception of financial risk increases

– Increased cost of capital

– Falling asset values

– Greater separation between “haves and have-nots”

– Survivability

Chris TarryAviation Industry Research and Advisory

CTAIRA

This report has been prepared and issued by Chris Tarry Aviation Industry Research and Advisory Limited a business that is not registered to give investment advice.

This report is for information purposes only and should not be construed as giving investment advice. Chris Tarry Aviation Industry Research and Advisory Limited accepts no responsibility or liability whatsoever for any expense, loss or damage arising out of or in any way connected with the use of all or any part of this report.

No part of this report may be reproduced or distributed in any manner without permission of Chris Tarry Aviation Industry Research and Advisory Limited.

Chris Tarry Aviation Industry Research and Advisory Limited [email protected] +44 1892 512034