Embed Size (px)

Citation preview

IOTA CASE STUDY WORKSHOP

Auditing Multinational Enterprises - Transfer Pricing Issues

27 – 29 APRIL 2011

ROME, ITALY

INDEX

1. AGENDA BACKGROUND NOTE

PRACTICAL INFORMATION

LIST OF PARTICIPANTS

COMPOSITION OF WORK GROUPS

2. PRESENTATIONS

3. CASE STUDIES

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study Workshop – AGENDA

- 1 -

IOTA Case Study Workshop

Auditing Multinational Enterprises - Transfer Pricing Issues

Rome, Italy 27-29 April 2011

AGENDA

DAY 1 27 APRIL 2011

0900 - 0930 Introduction to IOTA – Setting the scene

IOTA TAC

0930 - 0950 Recent Developments in the Field of Transfer Pricing in Italy

Mr. Luigi Magistro, Italian Revenue Agency

0950 - 1030 Application of the Revised 2010 Transfer Pricing Guidelines

Mr. Wolfgang Bϋttner, OECD Plenary Discussion

1030 – 1100 Coffee Break 1100 - 1230 Case Study 1 – Italy

Mr. Antongiulio Buffardo & Ms. Rosanna D'Ettorre

1230 - 1400 Lunch 1400 - 1600 Case Study 2 – Belgium

Incl. Coffee Break Mr. Willem Raes & Mr. Bauduin Frogneux

1630 Social Event

Cultural visit at the museum Dinner

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study Workshop – AGENDA

- 2 -

DAY 2 28 APRIL 2011

0900 - 0910 Introduction Day Two

IOTA TAC

0910 - 1040 Case Study 3 - Slovakia

Ms. Dalila Kutisova Luknarova

1040 – 1100 Coffee Break 1100 - 1230 Case Study 4 - Germany

Ms. Anke Schwengel

1230 - 1400 Lunch 1400 - 1530 Case Study 5 - Switzerland

Mr. Thomas Brunner & Mr. Jan Edelmann

1530 – 1600 Coffee Break 1600 - 1730 Case Study 6 - France

Ms. Stéphane Lesage

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study Workshop – AGENDA

- 3 -

DAY 3 29 APRIL 2011

0900 - 0910 Introduction Day Three

IOTA TAC

0910 - 1040 Case Study 7 - Finland

Ms. Minna Wilander & Mr. Sami Koskinen

1040 – 1110 Coffee Break 1110 - 1200 Summary, Evaluation and Close 1200 Lunch

ADDITIONAL CASES:

Case Study 8 - Germany

Mr. Uwe Schmitt

Case Study 9 - Poland

Mr. Paweł Parzych

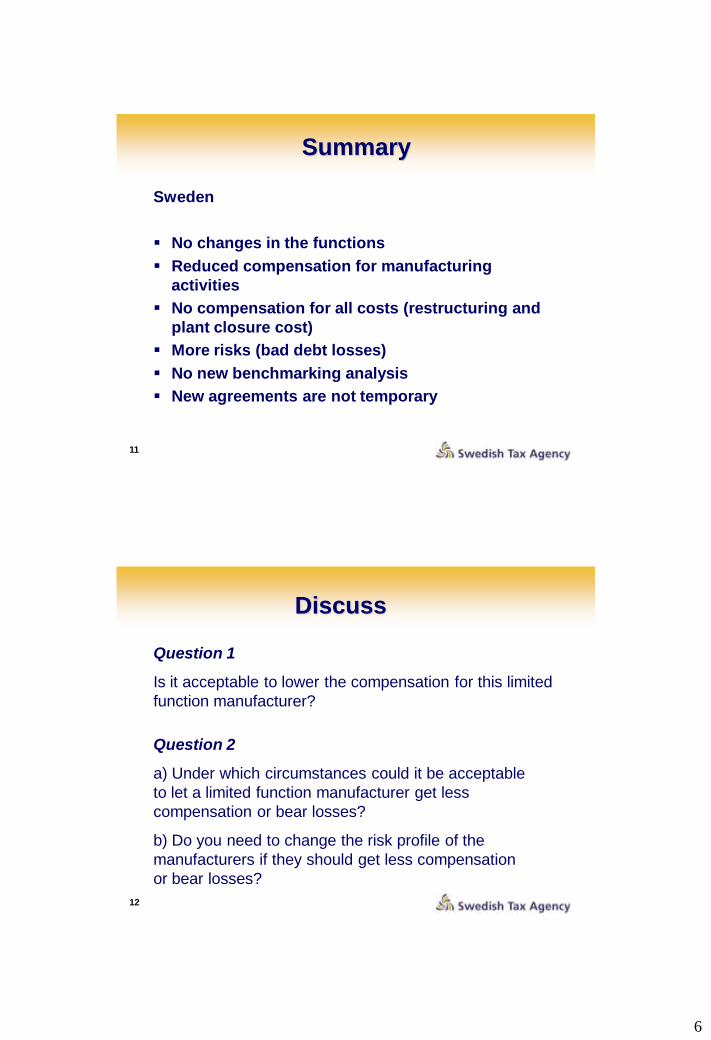

Case Study 10 - Sweden

Mr. Henrik Karlsson & Ms. Åsa Olsson

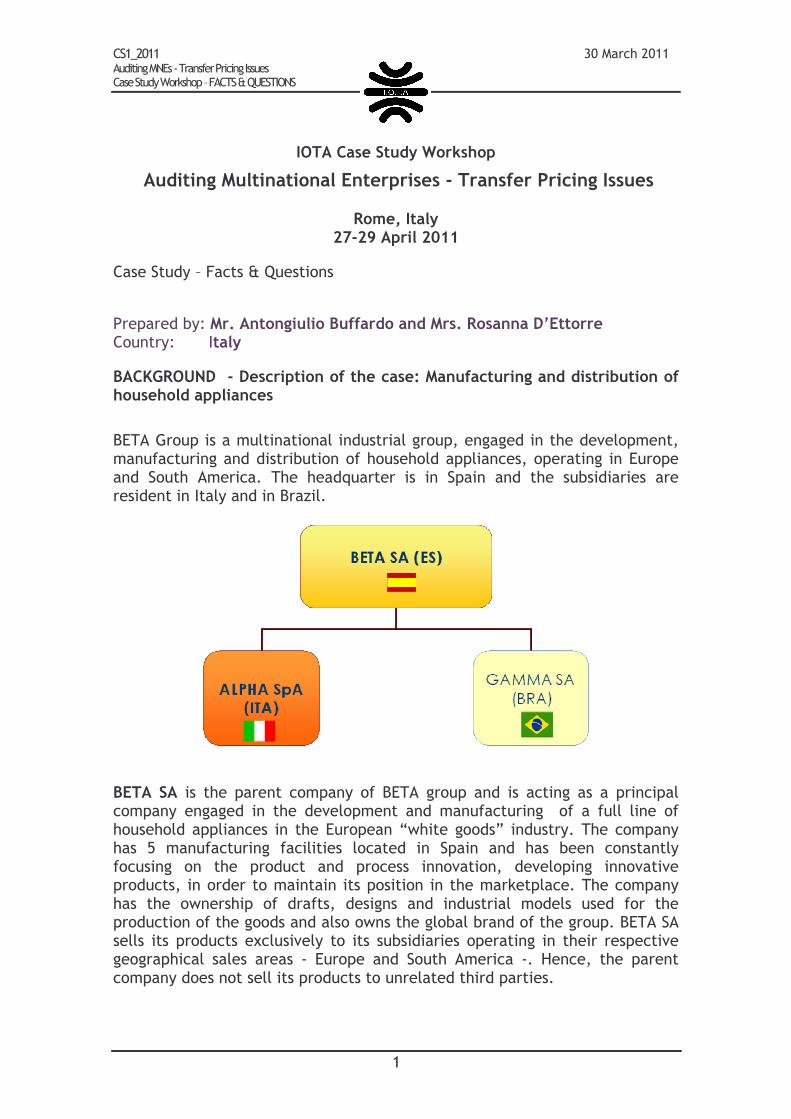

CS1_2011 Auditing MNE’s - Transfer Pricing Issues Case Study Workshop – BACKGROUND NOTE

1

IOTA Case Study Workshop

Auditing Multinational Enterprises - Transfer Pricing Issues

Rome, Italy 27-29 April 2011

BACKGROUND NOTE

Background

Globalisation and technological advances are changing the shape of the world economy. More than two-thirds of the global trading business community involves multinational enterprises. Well over 50% of global trading consists of associated party transactions which are subject to transfer pricing for taxation purposes.

With the increase in international transactions in a globalised world, a potential for tension and conflict among countries arises when it comes to the question of which country has the rights to taxation in respect of certain cross-border transactions. Transfer pricing issues therefore remain as important as ever in terms of the international taxation scene.

As the transfer pricing of goods and services across borders is fundamental to the taxing rights of different countries, it is currently receiving increased attention, especially in light of the fact that most tax administrations across Europe struggle to maintain their desired levels of revenue.

To maintain a fair share of the multinational tax pie – tax administrations are implementing and updating their rules and regulations on international transactions as well as increasing their audit activities.

In July 2010, the OECD released a revision to Chapters I-III of the Transfer Pricing Guidelines: those chapters that deal with the arm’s length principle, transfer pricing methods and comparability analysis, as well as the introduction of a new Chapter IX addressing how transfer pricing principles and corresponding treaty rules should apply to business restructuring. The document provides the principles and recommendations used for transfer pricing analysis in many countries throughout the world.

It is entirely reasonable that a tax administration wants to have confidence that any performance of transactions are in alignment with the OECD guidelines, all appropriate costs are included, inappropriate costs excluded and an arm's length price applied. The level of confidence required and how it is acquired can be achieved in various ways depending on the particular circumstances of the case and a tax administration's overall approach to transfer pricing audits.

In this context the way tax authorities deal with multinational enterprises is of fundamental importance. The emphasis of the event, therefore, is on how most expediently and efficiently tax auditors may conclude that the arm's length

CS1_2011 Auditing MNE’s - Transfer Pricing Issues Case Study Workshop – BACKGROUND NOTE

2

principle as well as other relevant methods has been applied by multinational enterprises in carrying out of certain transactions.

Objectives

This is a popular event on the IOTA timetable during which it is intended to explore the specific compliance and international audit issues that auditors of transfer pricing cases face when dealing with multinational enterprises; and to exchange knowledge and experiences through a series of participative group work sessions.

By the use of cases, carefully selected by Transfer Pricing experts from the examples provided by delegates, it is the intention of this workshop to:

• Examine the implications of the new OECD Guidelines for Multinational Enterprises and Tax Administrations, in particular Chapters I-III, on transfer pricing; including the practical application of the comparability method and profit method (transactional net margin method and profit split method) in auditing multinational enterprises, using examples;

• Allow delegates, in small groups, to review the problems, issues and aspects raised by the cases in order to compare approaches to the relevant transfer pricing methods adopted by IOTA tax administrations;

• Examine the “good practice” approaches that are adopted to deal with multinational enterprises by IOTA members participating in the workshop and disseminate information learned;

• Build and develop a network of contacts between delegates to aid in the understanding and equitable application of transfer pricing throughout IOTA tax administrations.

Expected Outputs

By the end of this workshop the participants should be able to demonstrate a better understanding of transfer pricing aspects in auditing multinational enterprises. Participants should also be better aware of the the special challenges transfer pricing can present to the audit practices with regards to applying the relevant methodology for establishing arm’s length transfer pricing and to suggest possible approaches to improve the conduct of transfer pricing examinations in multinational enterprises. Participants should be able to share this knowledge with other tax auditors working in this field.

Target Audience

Participants should ideally be senior tax administrators involved in auditing multinational enterprises. They should have a combined experience of both practical audit and in dealing with transfer pricing cases.

Please note that it is not possible to provide any interpretation facilities at this event and IOTA expects that all participants will have sufficient language skills to deliver the case and defend their position in the discussions in English.

CS1_2011 Auditing MNE’s - Transfer Pricing Issues Case Study Workshop – BACKGROUND NOTE

3

Methodology

The workshop will be totally practical in nature, combining presentations of selected case studies with the opportunity for all participants to share their own views and opinions on the approach to resolving the transfer pricing issues raised in each case study.

The aim will therefore be to focus the workshop around a series of selected case studies and highlighted issues in the area of transfer pricing and to provide the opportunity for the participants to work together in smaller groups to discuss approaches and solutions to these individual cases and issues.

The groups will finally bring their ideas and suggestions into the plenary sessions when the various suggested approaches and solutions can be debated by the wider group.

Requested Input

It is a requirement that each member administration submits a case study or transfer pricing issue from the work experience of the participant(s) as a condition of their participation.

A number of these case studies and issues will be selected for use in the group work sessions during the workshop. Those delegates whose case studies or transfer pricing issues are selected will be required to present their cases and issues and act as a resource and facilitator during the session when their case studies are being discussed, answering any additional questions that are asked by the other participants and preparing a brief summary for publication in the post-event report.

To facilitate the discussions and the group work sessions the submitted case study/problem will need to be structured and presented in the following way:

1. Description of the case or the transfer pricing issue. It is crucial to point out why and in what way the companies are associated. For clarity reasons it is advisable to focus on only one transfer pricing problem.

2. Details of the approach to the audit and the specific/standard transfer pricing method applied during the audit. This should include a short presentation of the case, including an overview of the transactions, the chosen method and the reasons why it was selected for the purpose of the particular case or problem under discussion.

3. Proposed Solution based on the audit results or expected outcome.

Please note that all case studies should be made anonymous to ensure the confidentiality of taxpayer’s data.

Please make sure that your case study is submitted at the latest by 30th

March 2011 by email (mail to: [email protected]). E-registration form is to be submitted by the same date. As the number of participants is limited to 48 persons, entries of delegates will be accepted on a first registered first in basis.

Eugenijus Soldatkovas Jerry Taylor IOTA Technical Advisory Committee

IOTA 1

INTRA-EUROPEAN ORGANISATION OF TAX ADMINISTRATIONS

AUDITING MULTINATIONAL ENTERPRISES - TRANSFER PRICING ISSUES

Rome, Italy, 27-29 April 2011

PRACTICAL INFORMATION

CONTACT PERSONS

Intra-European Organisation of Tax Administrations (IOTA) 1075 Budapest, Rumbach Sebestyén u. 14. Hungary Website: www.iota-tax.org Contact person for technical aspects – Mr. Eugenijus Soldatkovas Tel.: (+36 1) 478 3035 E-mail: [email protected] For logistical aspects – Ms. Borbála Farkas Tel.: (36 1) 478 3036 Fax: (36 1) 341 5177 E-mail: [email protected]

Hosting administration: Italian Revenue Agency Via C. Colombo 426 00145 Rome Italy Contact person for administrative aspects: Ms. Maria Paola Mastroeni Tel: (39 06) 5054 5335 Fax: (39 06) 5054 5336 E-mail: [email protected]

Contact person for logistical aspects: Ms. Valeria Sperandeo Tel: (39 06) 5054 5077 E-mail: [email protected] Mr. Alessandro Lentini Tel: (39 06) 5054 5987 E-mail: [email protected]

IOTA 2

ARRIVALS AND DEPARTURES

Delegates are kindly requested to organise and cover their transport from airport/train/bus stations to the hotel and back. Airport arrivals:

• Leonardo Da Vinci Airport (Fiumicino)

International Airport of Fiumicino (http://www.adr.it/home/fiumicino_en.htm), is situated approximately 30 km west of the city centre. ATM machines are located in the Arrivals Hall.

When arriving at Fiumicino airport you may take a taxi or use public transport. The cheapest way to reach the city is by using train or bus shuttle.

Taxi

In correspondence of the Terminals 1,2, 3 and 5 of Fiumicino airport a taxi service is available. The cost of a ride to the hotel is 40 EUR (fixed fee, included luggage).

The cars for the taxi service of the City of Rome are white and can be recognized by the sign "TAXI" on the top and by the identifying license number on the doors, on the back and inside the car.

Train

“Ferrovie dello Stato” (FS) set up a direct connection to/from Termini railway station and a connection by metro. The “Leonardo Express” departs from/to Termini every 30 minutes and takes about 30 minutes without intermediate stops. The cost is 14 EUR;

Timetable can be found on the website of Ferrovie delle Stato.

(http://www.ferroviedellostato.it/homepage_en.html)

Bus shuttle

Daily connections between the airport and Termini station are guaranteed by a shuttle bus operated by SIT. The buses are parked in front of Terminal 3. For information about bus times, routes and fares go to: www.sitbusshuttle.it

In order to get to the hotel from Termini railway station, see below (Arrival by train).

• Giovan Battista Pastine Airport (Ciampino)

International airport of Ciampino (http://www.adr.it/home/ciampino_en.htm), situated approximately 15 km south of the city centre. ATM machines are located in the Arrivals Hall.

When arriving at Ciampino airport you may take a taxi or a bus shuttle.

The cheapest way to reach the city is by using bus shuttle.

Taxi

At Ciampino airport, in correspondence of the exit, a taxi service is available. The cost of a ride to the hotel is around 30 EUR (fixed fee, included luggage).

The cars for the taxi service of the City of Rome are white and can be recognized by the sign "TAXI" on the top and by the identifying licence number on the doors, on the back and inside the car.

IOTA 3

Bus shuttle

Daily connections between the airport and FS Roma Termini station are guaranteed by the bus services operated by SIT and TERRAVISION. The buses are parked in dedicated bus bays opposite International Departures. For information about bus times, routes and fares go to:

www.sitbusshuttle.it and www.terravision.eu

In order to get to the hotel, from Termini railway station, see below (Arrival by train)

Please note that the hotel can arrange for you a pick-up service. Contact directly the hotel for any further information.

Arrivals by train

From the Piazza dei Cinquecento in front of the Termini Station, take B underground train in direction Laurentina and get off at the Cavour stop. Please note that each IOTA member administration is responsible for supplying their delegates with travel and health insurance for the duration of any IOTA Event.

VISAS

In the event visas are required for entry into Italy by nationals of a country, each participant is responsible for obtaining it prior to travelling to Rome. Information about countries whose citizens do not require visas to enter the Republic of Italy can be found on the website of the Italian Ministry of Foreign Affairs (http://www.esteri.it). Upon request, IOTA will send individual invitations to be used for that purpose.

ACCOMMODATION AND VENUE

Delegates will be accommodated in: Grand Hotel Palatino Via Cavour, 213/M 00184 Roma, Italia Ph. +39 06 4814927 Fax +39 06 4740726

[email protected] http://www.fhhotelgroup.it/eng/grand_hotel_palatino/grand_hotel_palatino.htm

IOTA 4

The Grand Hotel Palatino is located in the heart of ancient Rome, only a short walk from the Colosseum and from the “Fori Imperiali” (Imperial Forums). It is also very near to the most fashionable Roman shopping area, and not far from the Termini railway station and the underground station. The hotel position is ideal for those who arrive by plane as well as by train.

Please note that, due to Easter holidays (24 April) and the beatification of Pope Giovanni Paolo II (1 May), it is not possible to stay longer than the duration of the meeting in this hotel. For the same reason, it is not possible to host more than 50 delegates.

VENUE

The meeting will be held in the Grand Hotel Grand Hotel Palatino, in the room Cesarini in the basement.

FINANCIAL ARRANGEMENTS

For delegates from Full and Associate Member Tax Administrations (up to two delegate per Administration) and for speakers invited by IOTA, IOTA will cover the cost of accommodation up to three nights and meals starting with the dinner on 26th April and closing with the lunch on 29th April 2011.

The Members are tax administrations of: Albania, Armenia, Austria, Azerbaijan, Belgium, Belarus, Bosnia and Herzegovina, Bulgaria, Croatia, the Czech Republic, Cyprus, Denmark, Estonia, Finland, the Former Yugoslav Republic of Macedonia, France, Georgia, Germany, Greece, Hungary, Iceland, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, Moldova, Montenegro, the Netherlands, Norway, Poland, Portugal, Republic of Srpska (Bosnia and Herzegovina), Romania, Russian Federation, Serbia, Slovakia, Slovenia, Spain, Sweden, Switzerland, Ukraine, United Kingdom.

The Associate member is the Tax Committee of the Ministry of Finance of the Republic of Kazakhstan.

IOTA will book hotel accommodation only for the duration of the event. Any extension beyond these days requires an individual contact with a hotel. IOTA is not responsible for any modifications, cancellations or damages related to this booking of the delegate. In case of cancellation after the given deadline of a planned journey to an event, for which the participant has already been registered, the member administration will be held responsible for the costs resulting from such cancellation. If the journey or event is cancelled because of the fault of the organiser these costs are borne by the organiser.

For your information the negotiated price for accommodation (including breakfast and VAT) is 155 EUR per night for a double room single use, the cost of the double room is 196 EUR per night. A newly introduced city tax of 3 euro has to be added to the cost per night.

MEALS

IOTA will cover all meals for all participants, starting with the dinner on 26th April and closing with the lunch on 29th April 2011.

SOCIAL EVENTS

Upon arrival on 26th April 2011 a welcome cocktail will be available at the hotel from 19:00. On 27th April 2011 a social event (cultural visit + dinner) will be organised by the Italian Revenue Agency. Further details will be provided during the first day of the meeting.

MONEY

The Italian currency is the EURO. In the centre of Rome there are many opportunities to change your money. Banks in Rome provide complete foreign exchange and banking services. Currency

IOTA 5

exchanges are to be found all over town. Banks are usually open from 9.00 till 16.00. You can also withdraw money using a credit card at a number of "Bancomat" that can be found outside most banks. Credit cards such as VISA, Mastercard/Eurocard, and American Express are usually accepted in hotels, restaurants and shops in Rome.

LOCAL TIME

GMT+1 HOUR.

OTHER

LOCAL WEATHER

To check the current local weather you may visit the following webpage: http://www.accuweather.com/en-gb/it/lazio/rome/quick-look.aspx

WE LOOK FORWARD TO MEETING YOU AND WE HOPE THAT YOU ENJOY YOUR STAY IN ROME!

CASE STUDY WORKSHOP AUDITING MULTINATIONAL ENTERPRISES – TRANSFER

PRICING ISSUES

27-29 APRIL 2011 ROME, ITALY

LIST OF PARTICIPANTS

Albania Giomela Gjini Director of Tax Procedures Department General Taxation Directorate Tel: 355 4 2276812 E-mail: [email protected] Albania Enkelejda Brahaj Head of Indirect Tax Unit General Taxation Directorate Tel: 355 4 2276812 E-mail: [email protected] Armenia Samvel Yeghikyan Chief Tax Inspector State devenue Committee Tel: 374 91 40 22 35 E-mail: [email protected] Austria Doris Hack Legal Consultant Large Taxpayer Audit Division Tel: 43 664 854 26 70 E-mail: [email protected] Austria Horst Rinnhofer Auditor Large Trader Auditing Tel: 436648542645 E-mail: [email protected]

Azerbaijan Dayanat Huseynzada Chief State Tax Inspector Ministry of Taxes Tel: 99412 4038821 E-mail: [email protected] Azerbaijan Yavar Ahmadov Head of Audit Division Ministry of Taxes Tel: 99412 4038821 E-mail: [email protected] Belgium Willem Raes inspector principal of fiscal administration Service public federal Finance Tel: 32 2 5764107 E-mail: [email protected] Belgium Bauduin Frogneux inspecteur principal d'administration fiscale spf finance Tel: 32 2 57 71631 E-mail: [email protected] Bulgaria Dessislava Yordanova chief revenue expert NRA Tel: 359298593401 E-mail: [email protected] Croatia Marija Pocrnic Tax officer in Large Taxpayers Unit Ministry of Finance - Tax Administration Tel: 38516501517 E-mail: [email protected] Croatia Bozo Jaksic Senior Tax Advisor in department for Tax and Contributions Assesment Ministry of Finance - Tax Administration Tel: 38516501447 E-mail: [email protected]

Czech Republic Jakub Charbulák Transfer Pricing Specialist General Financial Directorate Tel: 420 257 043 424 E-mail: [email protected] Estonia Signe Uustal senior tax auditor Estonian Tax and Customs Board Tel: 372 676 4064 E-mail: [email protected] Finland Minna Wilander Senior Advisor Finnish Tax Administration Tel: 358 408210765 E-mail: [email protected] Finland Sami Koskinen Tax Expert The Finnish Tax Administration Tel: 358 9 7311 4926 E-mail: [email protected] France Stéphane LESAGE Head of a tax audit team specialized in luxury goods DGFiP Tel: 33 1 55 93 51 96 E-mail: [email protected] Georgia George Machavariani Head of Second Division of Main Inspection Division of Audit Department Revenue Service Tel: 995 99 40 26 16 E-mail: [email protected]

Germany Uwe Schmitt Tax auditor for foreign tax issues Zentrales Konzernprüfungsamt Stuttgart Tel: 496212921289 E-mail: [email protected] Germany Anke Schwengel Tax auditor Revenue office for the auditing of large scale enterprises Detmold Tel: 57413342467 E-mail: [email protected] Germany Günther Boelmann Auditor Federal Central Tax Unit Tel: 49 177 535 7601 E-mail: [email protected], [email protected] Germany Markus Volkmann Federal Central Tax Unit Tel: 49 172 2436049 E-mail: [email protected] Hungary Ágnes Fotiadi Head of Unit National Tax and Customs Administration, Tax Directorate General for Priority Cases and Large Taxpayers Tel: 36 1 461 3589 E-mail: [email protected] Hungary Zoltán RAPP, dr. Senior Analyst National Tax and Customs Administration, Tax Directorate General for Priority Cases and Large Taxpayers Tel: 36 1 461 3484 E-mail: [email protected]

Italy Rosanna D'Ettorre Tax officer - APA Team revenue agency Tel: 39 0650542004 E-mail: [email protected] Italy Antongiulio Buffardo Tax officer - APA Team Revenue Agency Tel: 39 0650542006 E-mail: [email protected] Latvia Zane Smutova Chief Tax Inspector State Revenue Service Tel: 371 67097515 E-mail: [email protected] Latvia Liene Moiseja Chief Tax Inspector State Revenue Service Tel: 371 67097501 E-mail: [email protected] Kazakhstan Yertole Tulegenov Head of Division The Tax Committee of the Ministry of Finance of Republic of Kazakhstan Tel: 7 7172 717072 E-mail: [email protected] Kazakhstan Aliya Jetibayeva Head of Legal Division The Tax Committee of the Ministry of Finance of Republic of Kazakhstan Tel: 7 7172 717938 E-mail: [email protected]

Lithuania Lukas Krupavičius Chef specialist of International Transaction Control Division of Large Taxpayers Monitoring and Consulting Department State Tax Inspectorate under the Ministry of Finance of the Republic of Lithuania Tel: 3702687879 E-mail: [email protected] Netherlands Aarnout Hamelink Senior Expert Transfer Pricing Netherlands Tax ans Customs administration Tel: 31102905830 E-mail: [email protected] Norway Guro Runestad senior advicer Norwegian tax administration Tel: 47 934 11 735 E-mail: [email protected] Norway Siv-Olaug Berge Walde Senior Adviser Norwegian Tax Administration Tel: 4740479696 E-mail: [email protected] Poland Bogumil Kowal senior tax inspector Fiscal Control Office Tel: 48 22 207 96 21 E-mail: [email protected] Poland Bożena Dąbrowska Ministry of Finance Tel: 48 22 694 31 70 E-mail: [email protected]

Romania Alina Sirzea Inspector, General Directorate for the Administration of Large Taxpayers National Agency for Fiscal Administration Tel: 40748197534 E-mail: [email protected] Romania Madalina Oita Inspector, General Directorate for the Administration of Large Taxpayers National Agency for Fiscal Administration Tel: 40757384916 E-mail: [email protected] Russian Federation Svetlana Bondarchuk head of the directorate Federal Service of Russia Tel: 8 495 913 03 79 E-mail: [email protected] Russian Federation Vladimir Golishevsky Deputy Head of the Division for the Analysis of the International Taxation, Analytical Directorate. Fedral Tax Service of Russia Tel: 8 495 913 03 79 E-mail: [email protected] Serbia Zoran Vasic Assistant Director - Education and Communication Sector Ministry of Finance - Tax Administration Tel: 381 113950 680 E-mail: [email protected] Serbia Tijana Martinovic Tax Advisor - Contact Centre Ministry of Finance - Tax Administration Tel: 381 11 3310091 E-mail: [email protected]

Slovakia Dalila Kutisova Luknarova Head of International Taxation Auditing Department Tax Office for Selected Taxpayers Tel: 421 2 5737 8752 E-mail: [email protected] Spain Ignacio del Río Head of Regional Tax Auditing Unit Spanish Tax Agency Tel: 34 91 582 72 57 E-mail: [email protected] Sweden Henrik Karlsson Swedish Tax Agency Tel: 46 105735083 E-mail: [email protected] Sweden Åsa Olsson Swedish Tax Agency Tel: 46 105736699 E-mail: [email protected] Switzerland Thomas Brunner Tax Expert Federal Tax Administration, Audit Department Tel: 41 31 322 79 09 E-mail: [email protected] Switzerland Jan Edelmann Tax Expert Federal Tax Administration, Audit Department Tel: 41 31 322 72 21 E-mail: [email protected]

The former Yugoslav Republic of Macedonia Slavica Kiroska Deputy Head of the General Tax Inspectorate Public Revenue Office Tel: 389 2 3299 592 E-mail: [email protected] OECD Wolfgang Büttner Senior Advisor Tax Treaty, Transfer Pricing and Financial Transactions Division CTP/TTP Tel: 33 1 45 24 9648 E-mail: [email protected]

IOTA

IOTA Eugenijus Soldatkovas Technical Taxation Advisor IOTA Secreteriat Tel: 3614783035 Fax: 3613415177 E-mail: [email protected] IOTA Jerry Taylor Technical Taxation Advisor IOTA Secreteriat Tel: 3614783039 Fax: 3613415177 E-mail: [email protected]

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study Workshop – WORK GROUPS

IOTA Case Study Workshop

Auditing Multinational Enterprises - Transfer Pricing Issues

Rome, Italy 27-29 April 2011

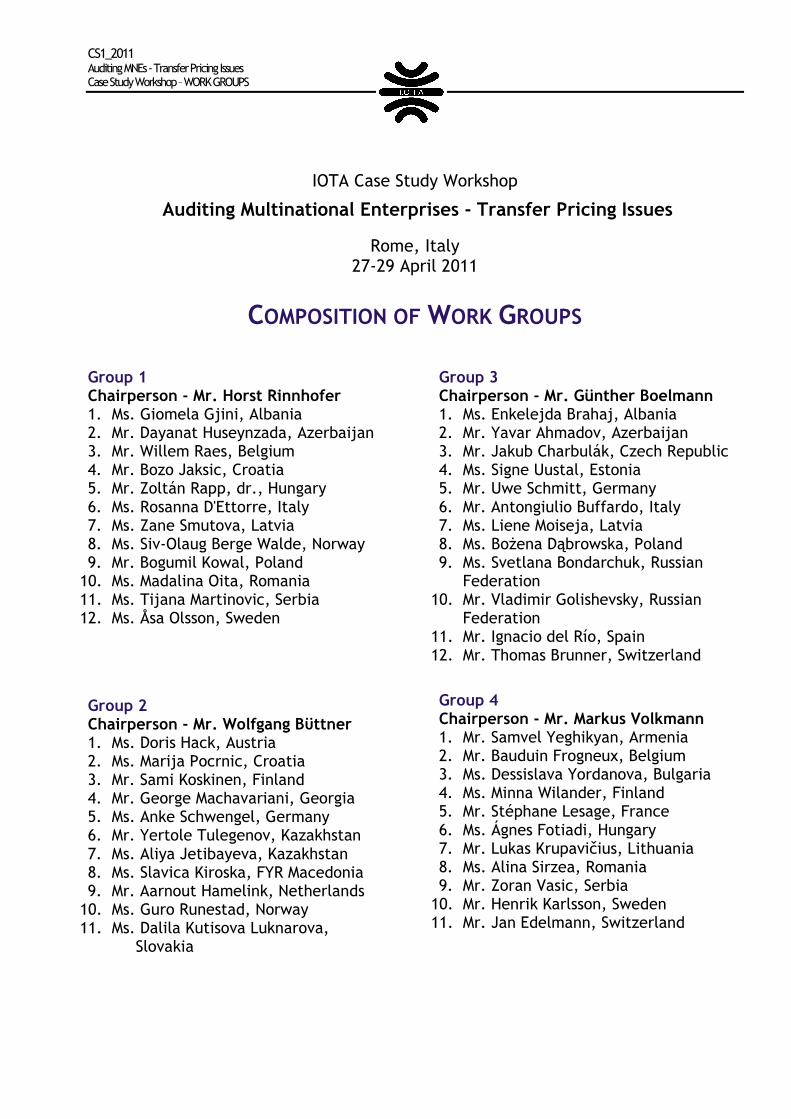

COMPOSITION OF WORK GROUPS Group 1 Chairperson - Mr. Horst Rinnhofer 1. Ms. Giomela Gjini, Albania 2. Mr. Dayanat Huseynzada, Azerbaijan 3. Mr. Willem Raes, Belgium 4. Mr. Bozo Jaksic, Croatia 5. Mr. Zoltán Rapp, dr., Hungary 6. Ms. Rosanna D'Ettorre, Italy 7. Ms. Zane Smutova, Latvia 8. Ms. Siv-Olaug Berge Walde, Norway 9. Mr. Bogumil Kowal, Poland

10. Ms. Madalina Oita, Romania 11. Ms. Tijana Martinovic, Serbia 12. Ms. Åsa Olsson, Sweden

Group 2 Chairperson - Mr. Wolfgang Bϋttner 1. Ms. Doris Hack, Austria 2. Ms. Marija Pocrnic, Croatia 3. Mr. Sami Koskinen, Finland 4. Mr. George Machavariani, Georgia 5. Ms. Anke Schwengel, Germany 6. Mr. Yertole Tulegenov, Kazakhstan 7. Ms. Aliya Jetibayeva, Kazakhstan 8. Ms. Slavica Kiroska, FYR Macedonia 9. Mr. Aarnout Hamelink, Netherlands

10. Ms. Guro Runestad, Norway 11. Ms. Dalila Kutisova Luknarova,

Slovakia

Group 3 Chairperson - Mr. Günther Boelmann 1. Ms. Enkelejda Brahaj, Albania 2. Mr. Yavar Ahmadov, Azerbaijan 3. Mr. Jakub Charbulák, Czech Republic 4. Ms. Signe Uustal, Estonia 5. Mr. Uwe Schmitt, Germany 6. Mr. Antongiulio Buffardo, Italy 7. Ms. Liene Moiseja, Latvia 8. Ms. Bożena Dąbrowska, Poland 9. Ms. Svetlana Bondarchuk, Russian

Federation 10. Mr. Vladimir Golishevsky, Russian

Federation 11. Mr. Ignacio del Río, Spain 12. Mr. Thomas Brunner, Switzerland

Group 4 Chairperson - Mr. Markus Volkmann 1. Mr. Samvel Yeghikyan, Armenia 2. Mr. Bauduin Frogneux, Belgium 3. Ms. Dessislava Yordanova, Bulgaria 4. Ms. Minna Wilander, Finland 5. Mr. Stéphane Lesage, France 6. Ms. Ágnes Fotiadi, Hungary 7. Mr. Lukas Krupavičius, Lithuania 8. Ms. Alina Sirzea, Romania 9. Mr. Zoran Vasic, Serbia

10. Mr. Henrik Karlsson, Sweden 11. Mr. Jan Edelmann, Switzerland

Presentations

1

IOTA

CASE STUDY WORKSHOP

Auditing Multinational Enterprises

Transfer Pricing Issues

Rome, Italy 27-29 April 2011

2

INTRODUCTION

Increasing awareness of the Italian tax

authorities to transfer pricing issues

audits

applications for APAs

recent developments in the tax system

2

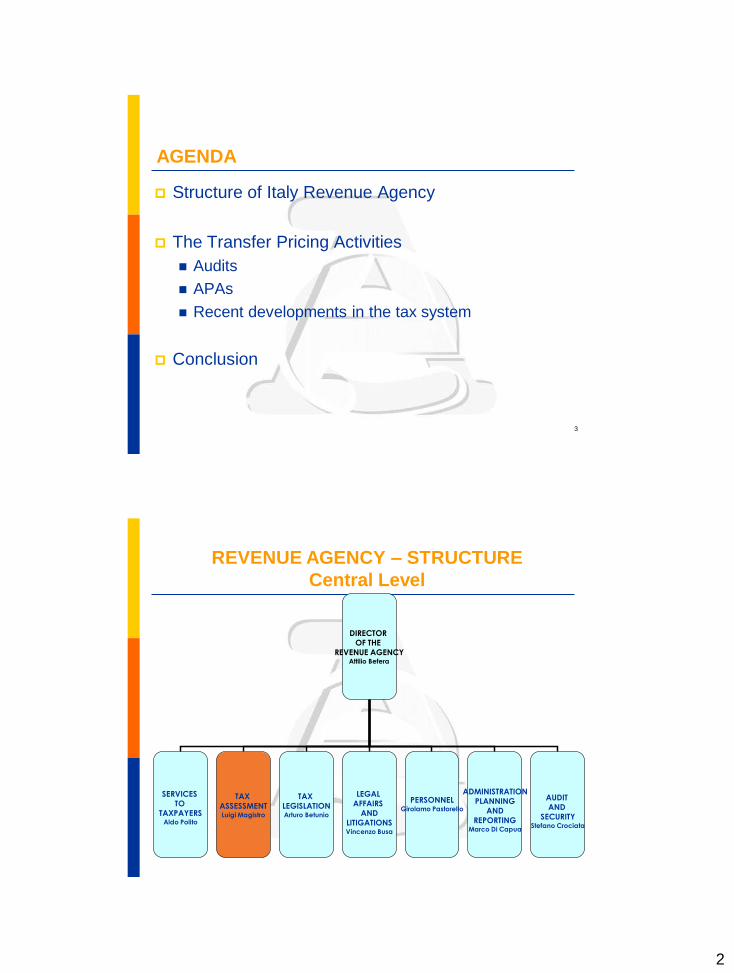

AGENDA

Structure of Italy Revenue Agency

The Transfer Pricing Activities

Audits

APAs

Recent developments in the tax system

Conclusion

3

31 August 2010 4

REVENUE AGENCY – STRUCTURE

Central Level

DIRECTOR

OF THE

REVENUE AGENCYAttilio Befera

SERVICES

TO

TAXPAYERSAldo Polito

TAX

ASSESSMENTLuigi Magistro

TAX

LEGISLATIONArturo Betunio

LEGAL

AFFAIRS

AND

LITIGATIONSVincenzo Busa

PERSONNELGirolamo Pastorello

AUDIT

AND

SECURITYStefano Crociata

ADMINISTRATION

PLANNING

AND

REPORTINGMarco Di Capua

3

5

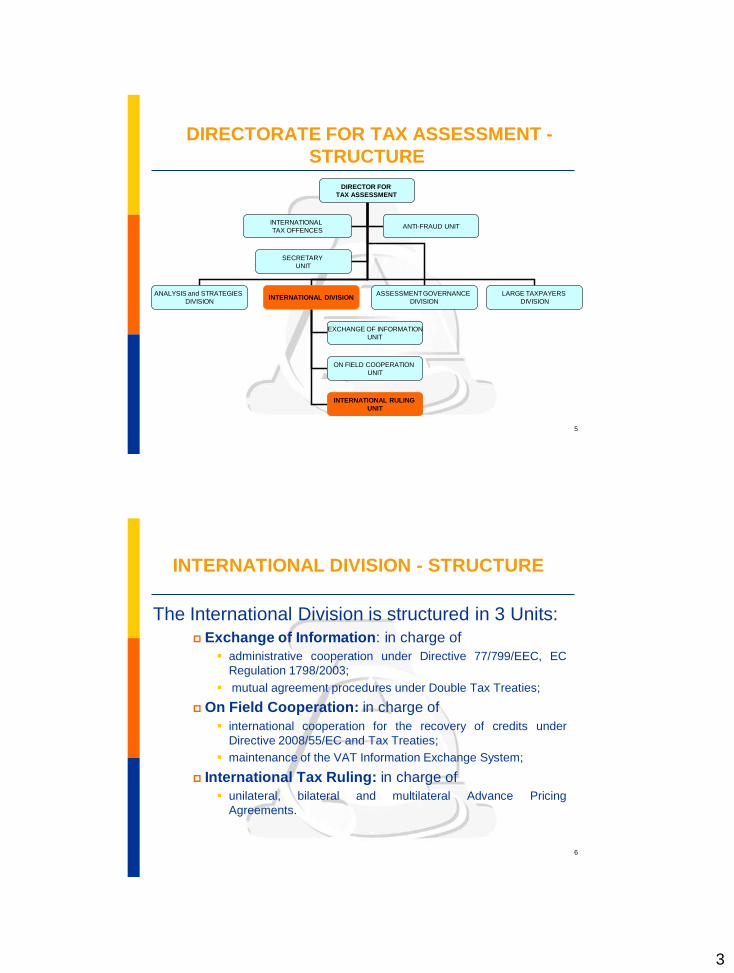

DIRECTORATE FOR TAX ASSESSMENT -

STRUCTURE

DIRECTOR FOR

TAX ASSESSMENT

ANALYSIS and STRATEGIES

DIVISIONINTERNATIONAL DIVISION

EXCHANGE OF INFORMATION

UNIT

ON FIELD COOPERATION

UNIT

INTERNATIONAL RULING

UNIT

ASSESSMENT GOVERNANCE

DIVISION

LARGE TAXPAYERS

DIVISION

INTERNATIONAL

TAX OFFENCESANTI-FRAUD UNIT

SECRETARY

UNIT

INTERNATIONAL DIVISION - STRUCTURE

The International Division is structured in 3 Units:

Exchange of Information: in charge of

administrative cooperation under Directive 77/799/EEC, EC

Regulation 1798/2003;

mutual agreement procedures under Double Tax Treaties;

On Field Cooperation: in charge of

international cooperation for the recovery of credits under

Directive 2008/55/EC and Tax Treaties;

maintenance of the VAT Information Exchange System;

International Tax Ruling: in charge of

unilateral, bilateral and multilateral Advance Pricing

Agreements.

6

4

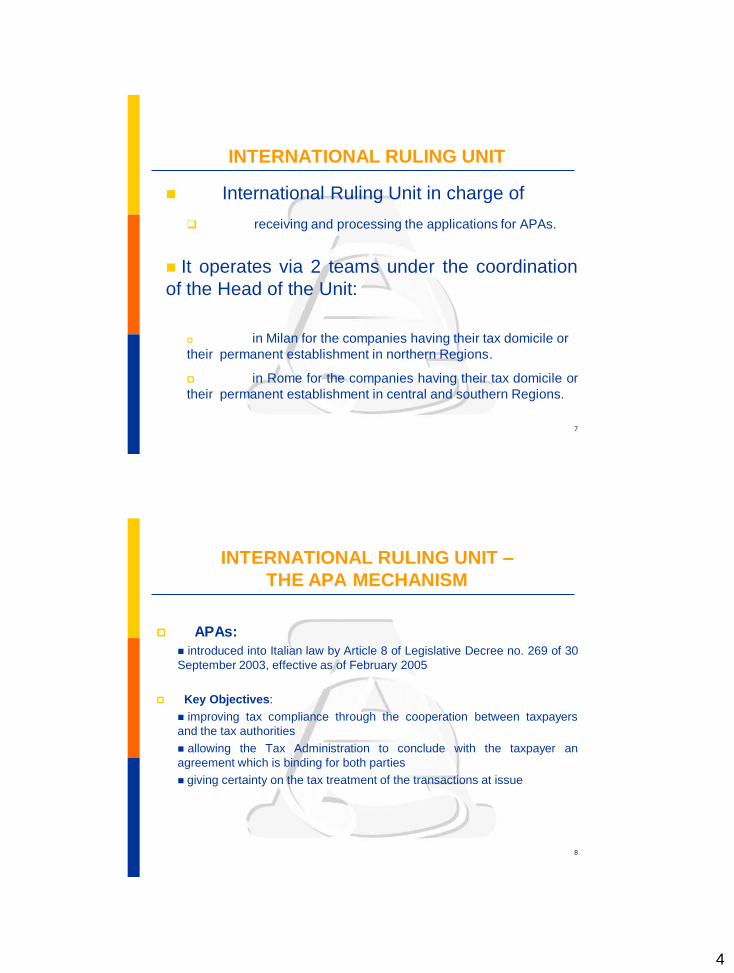

INTERNATIONAL RULING UNIT

7

International Ruling Unit in charge of

receiving and processing the applications for APAs.

It operates via 2 teams under the coordination

of the Head of the Unit:

in Milan for the companies having their tax domicile or

their permanent establishment in northern Regions.

in Rome for the companies having their tax domicile or

their permanent establishment in central and southern Regions.

8

INTERNATIONAL RULING UNIT –

THE APA MECHANISM

APAs:

introduced into Italian law by Article 8 of Legislative Decree no. 269 of 30

September 2003, effective as of February 2005

Key Objectives:

improving tax compliance through the cooperation between taxpayers

and the tax authorities

allowing the Tax Administration to conclude with the taxpayer an

agreement which is binding for both parties

giving certainty on the tax treatment of the transactions at issue

5

9

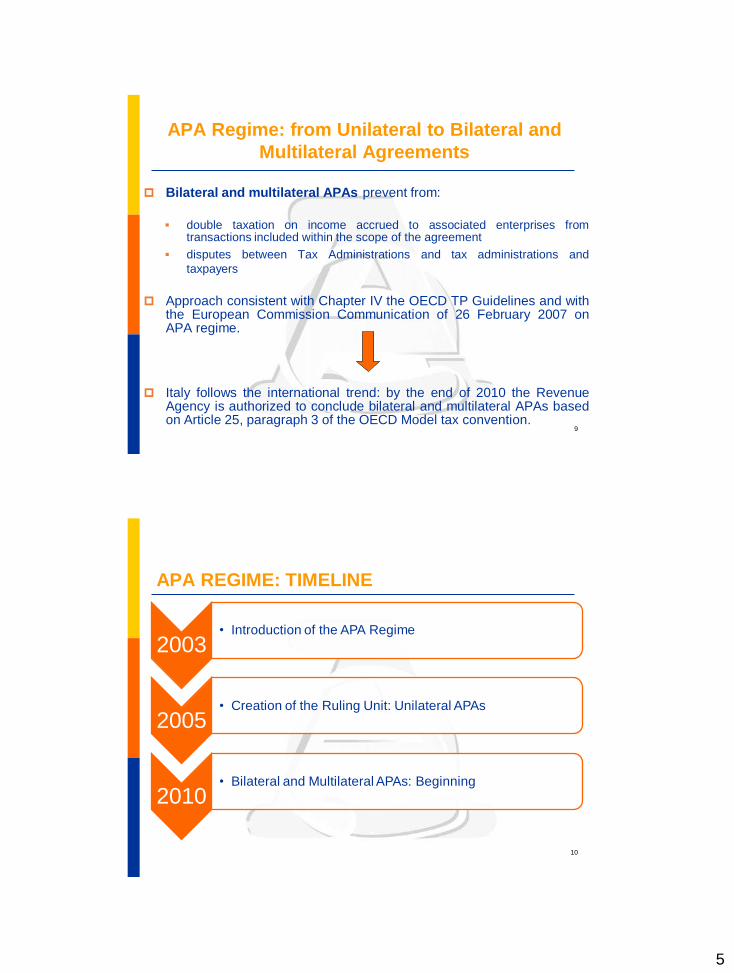

APA Regime: from Unilateral to Bilateral and

Multilateral Agreements

Bilateral and multilateral APAs prevent from:

double taxation on income accrued to associated enterprises fromtransactions included within the scope of the agreement

disputes between Tax Administrations and tax administrations and

taxpayers

Approach consistent with Chapter IV the OECD TP Guidelines and withthe European Commission Communication of 26 February 2007 onAPA regime.

Italy follows the international trend: by the end of 2010 the RevenueAgency is authorized to conclude bilateral and multilateral APAs basedon Article 25, paragraph 3 of the OECD Model tax convention.

APA REGIME: TIMELINE

2003• Introduction of the APA Regime

2005• Creation of the Ruling Unit: Unilateral APAs

2010• Bilateral and Multilateral APAs: Beginning

10

6

11

AUDIT ACTIVITY

Audits are carried out by local structures:

Provincial Directorates in charge of for SMEs

Regional Directorates in charge of for large sized enterprises, with

the support of the Large taxpayers Division.

Tax auditors can ask for technical support to the central Units.

Development of a people’s network with appropriate knowledge and

operational skills able to interact with the Central Assessment

Directorate.

12

RECENT DEVELOPMENTS:

ITALIAN TP DOCUMENTATION REGIME

Article 26 of Law-Decree 78/2010

Regulation by the Italian Revenue Agency Commissioner (September2010)

Administrative Circular Letter 58/E (December 2010)

Consistency with:

OECD 2010 Version of the TPG

Code of Conduct on TP documentation for MNEs in the EuropeanUnion

Principles of good faith and fair cooperation between taxpayers and theTax Administration (Italian Taxpayer Charter)

7

13

TP DOCUMENTATION REGIME:

UNDERLYING RATIONALE

• System based on the concept of “burden” rather than “obligation”

• Obligation = person required to adopt a specific behaviour, whose

execution can be obtained through enforcement

• Burden = person required to adopt a specific behaviour in his

own interest, otherwise:

– a favourable provision would not apply; or

– a negative provision would apply.

14

TP DOCUMENTATION REGIME: LEGISLATION

If an upward transfer pricing adjustment is made, penalties provided

for by law for unfaithful tax return - 100–200 % of the additional tax or

minor credit - do not apply if the following conditions are met:

1. The taxpayer submits in the course of the visit/examination/audit to

the Tax Administration proper documentation compliant with the

Regulation of the Director of the Revenue Agency; and

2. The taxpayer holds the aforesaid documentation shall notify their

option to the Tax Administration in their annual tax return

8

15

CONTENTS OF TP DOCUMENTATION –

MASTER FILE & COUNTRY FILE

• Concept of “appropriate” documentation

• 3 CATEGORIES

• Holding

• Sub-Holding

• Controlled Enterprises

• Master File: general description of the multinational group (sub-

group)

• Country File: specific information on the resident company and on

the transfer pricing policy adopted

16

BENEFITS

A. FOR THE TAX ADMINISTRATION

identifying the relevant inter-company transactions

determining if the taxpayer’s transfer pricing policy is in accordance

with the arm’s length principle

B. FOR THE TAXPAYER

providing protection from related administrative penalties in the event

of a subsequent upward income adjustment

minor risk level to be targeted for tax audits

9

17

USEFULNESS OF STANDARDIZED

DOCUMENTATION

Audit purposes:

effective assessment of the major risks in the taxpayer’s transfer pricing policy

hint of lower risk

Prevention purposes:

entering into an APA

www.agenziaentrate.it

MANY THANKS!

18

OECD

1

Centre for Tax Policy and Administration

Organisation for Economic Co-operation and Development

Overview of the 2010 Revision of theOECD Transfer Pricing Guidelines

IOTA Case Study WorkshopAuditing Multinational Enterprises

- Transfer Pricing Issues –

Rome27–29 April 2011

Wolfgang Büttner

OECD

www.oecd.org/ctp/tp/cpm

Comparability and Profit Methods

(revised Chapters I-III)

Transfer Pricing Aspects of

Business Restructurings

- New Chapter IX -

2010 Revision of the

OECD Transfer Pricing Guidelines

www.oecd.org/ctp/tp/br

OECD

2

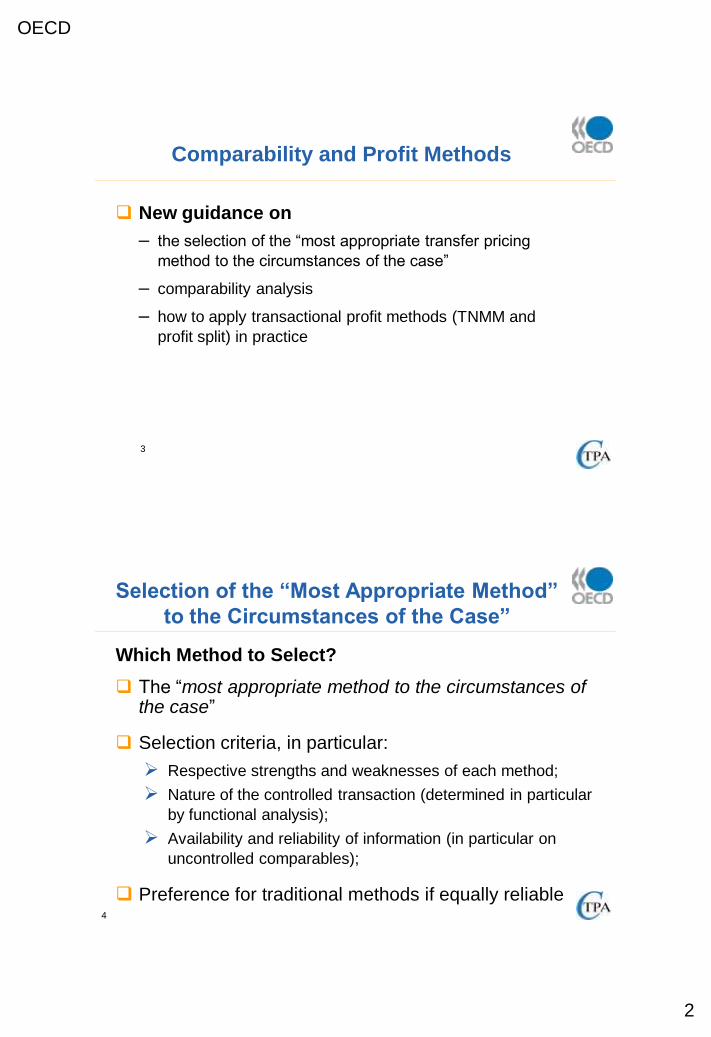

Comparability and Profit Methods

New guidance on

– the selection of the “most appropriate transfer pricing

method to the circumstances of the case”

– comparability analysis

– how to apply transactional profit methods (TNMM and

profit split) in practice

3

Which Method to Select?

The “most appropriate method to the circumstances of the case”

Selection criteria, in particular:

Respective strengths and weaknesses of each method;

Nature of the controlled transaction (determined in particular

by functional analysis);

Availability and reliability of information (in particular on

uncontrolled comparables);

Preference for traditional methods if equally reliable4

Selection of the “Most Appropriate Method”

to the Circumstances of the Case”

OECD

3

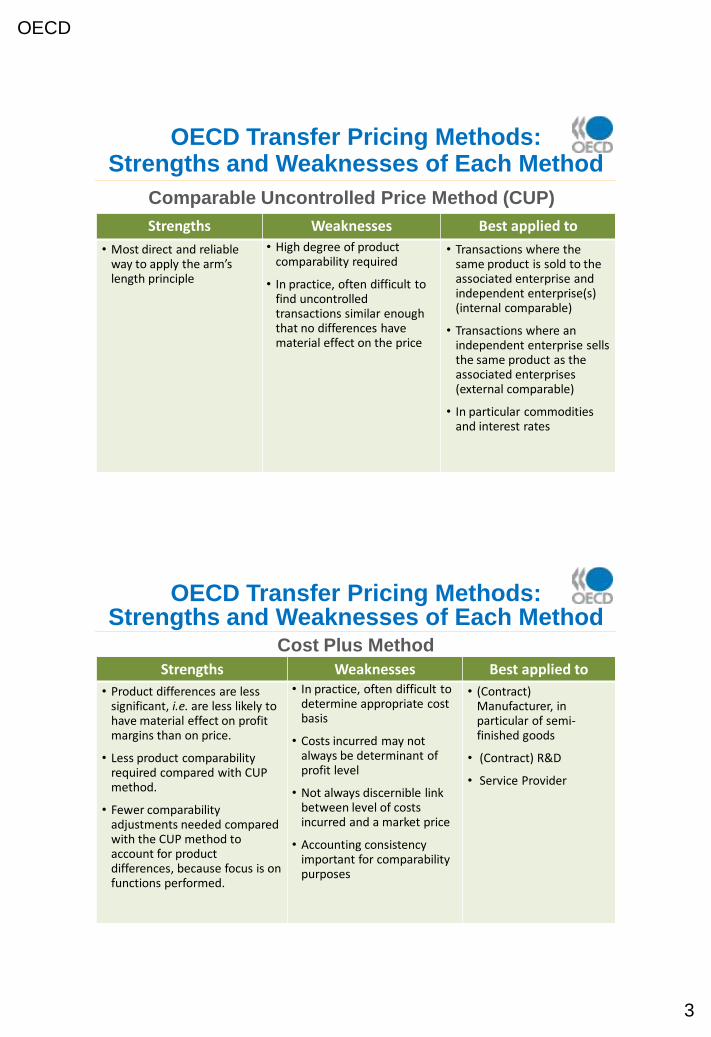

Comparable Uncontrolled Price Method (CUP)

5

OECD Transfer Pricing Methods:Strengths and Weaknesses of Each Method

Strengths Weaknesses Best applied to

• Most direct and reliable way to apply the arm’s length principle

• High degree of product comparability required

• In practice, often difficult to find uncontrolled transactions similar enough that no differences have material effect on the price

• Transactions where the same product is sold to the associated enterprise and independent enterprise(s) (internal comparable)

• Transactions where an independent enterprise sells the same product as the associated enterprises(external comparable)

• In particular commodities and interest rates

Cost Plus Method

6

Strengths Weaknesses Best applied to

• Product differences are less significant, i.e. are less likely to have material effect on profit margins than on price.

• Less product comparability required compared with CUP method.

• Fewer comparability adjustments needed compared with the CUP method to account for product differences, because focus is on functions performed.

• In practice, often difficult to determine appropriate cost basis

• Costs incurred may not always be determinant of profit level

• Not always discernible link between level of costs incurred and a market price

• Accounting consistency important for comparability purposes

• (Contract) Manufacturer, in particular of semi-finished goods

• (Contract) R&D

• Service Provider

OECD Transfer Pricing Methods:Strengths and Weaknesses of Each Method

OECD

4

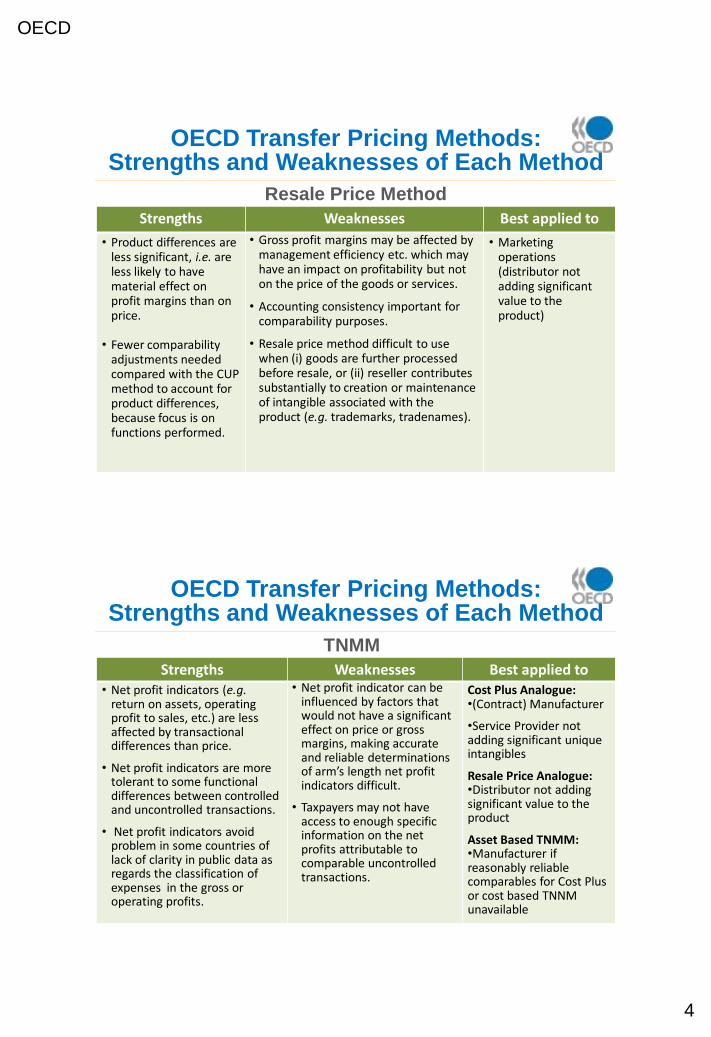

Resale Price Method

7

Strengths Weaknesses Best applied to

• Product differences are less significant, i.e. are less likely to have material effect on profit margins than on price.

• Fewer comparability adjustments needed compared with the CUP method to account for product differences, because focus is on functions performed.

• Gross profit margins may be affected by management efficiency etc. which may have an impact on profitability but not on the price of the goods or services.

• Accounting consistency important for comparability purposes.

• Resale price method difficult to use when (i) goods are further processed before resale, or (ii) reseller contributes substantially to creation or maintenance of intangible associated with the product (e.g. trademarks, tradenames).

• Marketing operations (distributor not adding significant value to the product)

OECD Transfer Pricing Methods:Strengths and Weaknesses of Each Method

TNMM

8

Strengths Weaknesses Best applied to• Net profit indicators (e.g.

return on assets, operating profit to sales, etc.) are less affected by transactional differences than price.

• Net profit indicators are more tolerant to some functional differences between controlled and uncontrolled transactions.

• Net profit indicators avoid problem in some countries of lack of clarity in public data as regards the classification of expenses in the gross or operating profits.

• Net profit indicator can be influenced by factors that would not have a significant effect on price or gross margins, making accurate and reliable determinations of arm’s length net profit indicators difficult.

• Taxpayers may not have access to enough specific information on the net profits attributable to comparable uncontrolled transactions.

Cost Plus Analogue:•(Contract) Manufacturer

•Service Provider not adding significant unique intangibles

Resale Price Analogue:•Distributor not adding significant value to the product

Asset Based TNMM:•Manufacturer if reasonably reliable comparables for Cost Plus or cost based TNNM unavailable

OECD Transfer Pricing Methods:Strengths and Weaknesses of Each Method

OECD

5

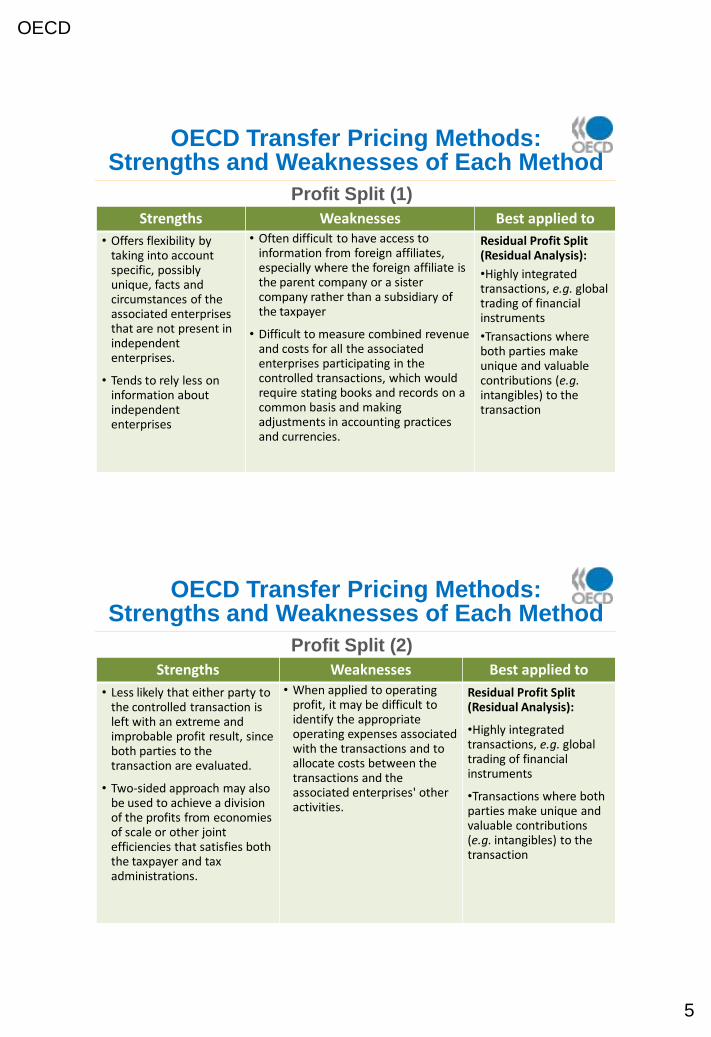

Profit Split (1)

9

Strengths Weaknesses Best applied to

• Offers flexibility by taking into account specific, possibly unique, facts and circumstances of the associated enterprises that are not present in independent enterprises.

• Tends to rely less on information about independent enterprises

• Often difficult to have access to information from foreign affiliates, especially where the foreign affiliate is the parent company or a sister company rather than a subsidiary of the taxpayer

• Difficult to measure combined revenue and costs for all the associated enterprises participating in the controlled transactions, which would require stating books and records on a common basis and making adjustments in accounting practices and currencies.

Residual Profit Split (Residual Analysis):

•Highly integrated transactions, e.g. global trading of financial instruments

•Transactions where both parties make unique and valuable contributions (e.g. intangibles) to the transaction

OECD Transfer Pricing Methods:Strengths and Weaknesses of Each Method

Profit Split (2)

10

Strengths Weaknesses Best applied to

• Less likely that either party to the controlled transaction is left with an extreme and improbable profit result, since both parties to the transaction are evaluated.

• Two-sided approach may also be used to achieve a division of the profits from economies of scale or other joint efficiencies that satisfies both the taxpayer and tax administrations.

• When applied to operating profit, it may be difficult to identify the appropriate operating expenses associated with the transactions and to allocate costs between the transactions and the associated enterprises' other activities.

Residual Profit Split (Residual Analysis):

•Highly integrated transactions, e.g. global trading of financial instruments

•Transactions where both parties make unique and valuable contributions (e.g. intangibles) to the transaction

OECD Transfer Pricing Methods:Strengths and Weaknesses of Each Method

OECD

6

Profit split for cases where both parties to thecontrolled transaction make significant, uniquecontributions (e.g. intangibles); highly integratedactivities

Difficulties in finding or adjusting comparables notsufficient to select profit split if this method is notappropriate given the functional analysis of thetransaction

Note: a one-sided method can be seen as a residual profit

split whereby 100% of the residual is attributed to the non-

tested party11

Selection of the “Most Appropriate Method”

to the Circumstances of the Case”

Objective: find the most reliable comparables

No requirement for an exhaustive search of all possiblesources of comparables

Acknowledge limitations in availability of information andcompliance costs

“Reasonably reliable comparables”: defined as the mostreliable comparables in the circumstances of the case,keeping in mind the above limitations

Typical (non-compulsory) 10-step process to be followedto perform a comparability analysis

Comparability Analysis

OECD

7

New guidance on the choice of the tested party;

Use of databases;

Internal/external comparables;

Secret comparables;

Foreign comparables;

Loss-making comparables;

Difficulties in finding comparables;

Comparability adjustments

Comparability Analysis

Lack of comparables does not mean that the taxpayer’s

controlled transaction is not arm’s length

Lacking evidence of what independent parties have done

in comparable circumstances...

... need to determine whether the conditions of the

taxpayer’s controlled transaction are comparable to what

independent parties would have agreed

Lack of comparables

14

Lack of Comparables

OECD

8

1) Due to uniqueness of the controlled transaction?

2) Due to lack of comparable independent enterprises (vertically integrated industry; small market)?

3) Due to limitation on publicly available information on potential comparables?

In the first case: profit split, especially if valuable,unique intangibles contributed by both parties

In the two other cases: is the risk of error greater witha one-sided method applied with “imperfectcomparables” or with a profit split applied with nocomparables?

Lack of comparables

15

Lack of Comparables

Traditional transaction methods (CUP, Cost Plus, Resale Price)

unchanged

Transactional Profit Methods (TNMM and Profit Split):

Further guidance on practical application

TNMM: selection and determination of the net profit margin

indicator

Profit Split: determination of profit to be split and of splitting

factors

Berry ratios

Transfer Pricing Methods

OECD

9

New Guidance on the Use of Profit Split

How to split the combined profits in a profit split method?

Preference for “objective” allocation keys, e.g. based oncosts, assets or other relevant contributions of the partiesto the transaction

The allocation key must reflect the parties’ contribution tothe creation of value in the particular case

OECD reluctant to accept completely subjective keys(such as “value chain analysis”)

No fixed allocations keys that would not account for thefacts and circumstances of the case17

Case Studies

��������� � ��� �� �������������������������������������������������������� �!� "�#�$�����%�&'����(���

�

��

����������� ��� ��������

�� ������� ������������������������������������������������

�� !�������"#�"$�������"%&&�

����������#�$����% �&����� ���

���"����)�*�� �'�������������(����� ���� �� ��'���������) *������� �� �����*�������������

(��+, ��- . ) ����) �������������������/�� ��������������� � �����0���������������� �����������

�+����, � �"�����- �.����� �.���������.��� �"/������������ ����0�. "- ���/�- ��������������������)��� �� �� ��� .��"".�����/� "������� ������ "����� � �� � �- ����1� � �� ��2������ ��� ��� �"��� ��� � �� ��)��������� �����������������.��������+�3�.1���

�

�

(���� �� ��� � �� "����� � - "��� �� +���� �� �"� ��� ��� ������ �� � "�����".�� - "��� ������� ��� � �� ��0�. "- ���� ��� - ����������� � �� � ��..� .���� �� ��� .��"".������ ��� � �� ��� "���45 ���� � ��6� ��������1�� �� � - "��� �� 7� - ����������� ���.������ . ����� ��� �"��� ��� �� )���� � �����.��� ������� �� � �� "� ����� ��� "� ����� ��� 0�� �/� ��0�. "���� ��� 0��0��"� �����/� ��� ������ �- ������ ����" ���� �� ���� ��- �!��".��1�� ��� - "��� �� � �� 5���� �"� �� �����/� �������� ��� ��������.� - ��.�� ����� � �� � ��"� ����� �� ��� ��� ������.� � 5���� ���. ).�)���� ��� ���� �"1�+���������..�� ���� "� ������ �8�.���0�.�� � � ���� ��)��������� "������� ��� � ���� ���"����0���� ��" ��.� �.��� ���� �� ��� "�� ��� � �� � �- ����� �1� 9 ����/� � �� "������ - "���� ���� ����..�����"� ������� �����.����� ����"�����1����

��������� � ��� �� �������������������������������������������������������� �!� "�#�$�����%�&'����(���

�

��

�� �� , � �"� �� � ��� ��.�� ��0��������� )�������� " ��� .� 1� ��� "������ � � �� �� ��� )�������� ���- ����*� 5� ���/� � .���/� � !���� ��� ���0����1� ���0��������- �������.�����0�� ������0����/���� ���" ����.������������� ������ - ���/���.�� ���8�������5���������������" ���1��1�2 �� ��� ��� � �� ��.��� ��)������� �� +���� ��1� ��� ��� ������� ��� � ��- ����������� ���"���.�- ��.�� �� ��� .��"".�����/��..���4� "�� !����.���6/� � ���������� )�� � �"������� ����- �!� 5���� )�� "����� � - "��1�$��� ��- ��/� �." � �"�� ������)����� ��� ��.�� ��� � ������� ��� "�� � �� 4� "�� !���� .���6� ��� - ���������� ��� � �� ������� .���� �� "� ������ - ��� )�� � ��"������ - "���+������1��, - - � ��/� � �� +�3�.��� � - "��/� ��� )�� �������� �� � � - - ���� ����/���0 .0��� �8�.���0�.�� ��� � �� ������)��� �� ��� � �� � �- ����� �� � �� , � �":��"� ������- ����������)��"������ - "��1���." ��"����*���

� � ��..��.������ ������)�� �/� �� ��� ��� ��0 .0��� ��� � �� ��������� �������� ����� "�����.� �- ".�- ����� �� �� �� �"� - �!������ " .���/� � ����)������� ���"" ���)�����- ��;�

� � - ���������/� �� ��� "� ������ � �"���.� 4� "� � !���� .���6/�5 �� � �����"" ����� �)��� .���8�.���0�.��5�� ��������.�����;�

� �

����� ���

��.��� �8� ��- �������� �� ������� �<�9 �� �"�� � �� ����.� ���� ���=� ��� � ������ ��� ��0��������� � �� ������� �� )��5���� �<�9 �� �"�� ��� � �� "������ - "���+������1�� ���������������� ������ ��"��� ���)���<�9 ���"�� �� ��� .��"".���������� - " ������- ����������)��� ��"������ - "��/������� .. 5��/��

� $�..�.���� �����.������>5� ���/�� .���/�� !���?;��

� � - �� � - " �����/� � ����� ��� � �� - ����������� "� ����� �� � ��4� "�� !����.���61�

�

�

�

� ����������"��������������8 �)�����)��� ���8"������������� ���� ���<�9 ���"������- ����������)�� ��5�� ��. 5����!�"� ��.��"��� �- ���� ������������� ��1��� �� ������������ �- ���������������0�����/�� ����������� �� .�� ���� ���." ��

��������� � ��� �� �������������������������������������������������������� �!� "�#�$�����%�&'����(���

�

��

��"������� ������.�- ������ ����- ).����� - " �����1�� ��"���������- ������ ��5�������������)��� ���8"����� ��- ����������������� ��1����� ���8"����"".������ �����������"�������- �� ���)������ ��� �������� ��� ��)������������ ��� ������ ��0�.).��� - "�).����1����� ������� �� ������ ��/�� �������� �.�������!��.����� ���<�9 ���"��5����� - ".���� ��� � �� �8 ����0�1� ������/� � �� ���� ��� �8- ����� � �� "� �����"��� �- ��� )�� �<�9 �� �"�� ��� 0�������� ��� "��� �- �/� �� � ������)�� �/� - ���� - ".�8������� ���� ��� �� ����������)����������� ��- ����� �1� �� 0��/� � �� �8"���� ��� .� � ��0 .0��� ��� - ����������� "� ����/� ���.������0�� ������0�����/������� .. 5�*�����������������0��.�4� "�� !����.����- ��.�6;��� - ����������� � - ".�- ������ �.�- ����� � � )�� ����� � � � - " ������"��� ����)��+�����;���� ���- ).���� "��� ���� � - " ������ ��� - ���������� � - ".�- �������.�- ����� � ��� ������ � � ��.�3��� �� �"���.� �� ��������- ��.��� ��� - ".����� ���� �":��� !����.���1��� ���2����.�/��8����� ���������� ������5������� �.�������!��.���������- ��� ��������������������"�������� .��� �1�9 �����/� � �� ��� ����� � � ��� )����� ) ��� ������ ��� "��� �- ��� ��� ���!�����- ���)����<�9 ���"�1���<�9 ���"��"��� �- ��� ��� .. 5���������� ��*��

� )�����0�����/��

� @�����)��� ��������� 5���� ��" ��.��.�������� �� ����� ��&�.����� ��� .��� ���- ���� ��)�������"� ������0��������/��.���"� - �� ��� @������� �� ��"�������" .����������� 5���� ��" ��.��.������� �� ����� ��������.����������0���- ���- ����� �� 0������" ����.������0������� � - - ����.����� ������.������������ @�0�. "- ���/�- ���- ��������������� ��� ����.������5 �!�

�� � ������������*�

�� ����������� ��4� "�� !����.���6�� A����� �% ���0�. "- ����>� ������ ��"� ���������"� �������� 0�� �?�� &�.����� ��� .��� ��0��� ������. ���������� � ��������� ��- ��������������������

��<�9 ���"�����- ���� ��� .. 5�������!�*��

��������� � ��� �� �������������������������������������������������������� �!� "�#�$�����%�&'����(���

�

B�

� )�����0����/��

�? �� ��������!�*���

� � ������� ��"� �����.�)�.������ ��0��� ���> )� .������ �!�?�� ��"".�����!���

�+? �!������!�*�

�� +����" ���� ���������- ���"� - �� ��� ����� �����- ���- ���� ����.������5 �!�� ��������" .�����

��? ����������!���

�� � ��� ..���� �� �������0).���� ���- �� ��"�- ���� ��"�).���

�� � ����������/�

��? ��������������!�*�

�� ��"".�����!���� ��0��� ��� ���!�� >�1�1� ������ ��� �� �� � ��/� ���!� �� . ��� �� � ��� ���

������?��+? �!������!�*�

�� A��!����.����� �� ��������- �!�����- ����

��? �� �����.�)�.�������!�*�

�� � ������������� - �����..� ��"� �������

��<�9 ���"�� 5���� ��� .. 5����������).�������*��

�? �!������������).��/��

� �.�����" ��� .� ��������. �.��.������� ���- ���� ����.������5 �!�� �� - �� �.��- "��������������.������������

�+? �����������).��/��

�

� (5���� �"� �� �����/� �������� ��� ��������.� - ��.�� ��.���� � � 4� "�� !����.���6�

�

��������� � ��� �� �������������������������������������������������������� �!� "�#�$�����%�&'����(���

�

7�

�3 - ����. �

�1 ���� ��� "��� �/����������� �.�������� �.�- �� ��"".��).��� �� �����C�

�1 ���� ���8"����� .��� ��>�� ?�����).��� �� �����C�

�1 � ���������� �<�9 �� �"�� ������ �.� ��� ���!� "� ��.�/� 5 �� 5 �.�� � ���""� � �)�C�

�

�

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study - Slovakia – FACTS & QUESTIONS

1

IOTA Case Study Workshop

Auditing Multinational Enterprises - Transfer Pricing Issues

Rome, Italy 27-29 April 2011

CASE STUDY – FACTS & QUESTIONS

Prepared by: Dalila Kutišová Luknárová Country: Slovak Republic

BACKGROUND – Description of the case

� Alfa Germany is a private car manufacturer. From 2000, Alfa Germany began producing private cars in its subsidiary Alfa SK in the Slovak Republic.

� Beta Germany is a sub-supplier of Alfa Germany – it manufactures the bumpers for private cars produced in Alfa Germany. Beta Germany manufactures bumpers according to the customer´s design on request. After gaining customer approval of the design, Beta Germany determines the technical, engineering and design of the bumpers. Beta Germany is owner of the know-how required for manufacturing the bumpers.

� Alfa Germany and Beta Germany are non-related parties.

� In 2000, Alfa Germany decided that the sub-supplier (bumpers manufacturer) for its subsidiary Alfa SK (private car manufacturer in the Slovak Republic) had to be located close to Alfa SK –at a maximum distance of 50 km from car manufacturer Alfa SK.

� So as not to lose a part of its contracts, Beta Germany incorporated its subsidiary Beta SK in the Slovak Republic.

� Alfa Germany concluded a long-term general agreement with Beta Germany (for 15 years) for supplies of bumpers manufactured in the Slovak Republic by Alfa SK and subsequently repudiated its contract with its subsidiary Beta SK.

� Beta Germany approves the selling price for each series of the bumpers.

� The orders for each series of bumpers are forwarded directly by Alfa SK to Beta SK. In accordance with the specifications in the requests sent by Alfa SK, Beta SK secures the material inputs, required projects technology and manufacturing process, provides logistics, calculations and controls the quality of the products.

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study - Slovakia – FACTS & QUESTIONS

2

� Beta SK packs and supplies the completed orders to the customer – Alfa SK. Beta SK invoices the customer and the customer pays it direct to Beta SK.

� The result of this is that any profit/loss remains in the Slovak Republic in Beta SK.

� Throughout the period of the long-term contract with Alfa SK, for its repudiation of the contract with Beta Germany, Beta SK pays Beta Germany a commission of 4 % of its annual turnover on an annual basis.

� In addition, on an annual basis, Beta SK has to pay to the parent company, Beta Germany, the difference from the created profit arising in the past year between the material costs actually expended on the specific order increased by 5 %, other costs increased by 10 % and sales achieved from the specific order. The material costs represent 75 % of production costs.

QUESTIONS

1. Is this kind of practice correct? Would an independent company accept a price calculated on such a cost-plus basis for the performance of comparable activities under comparable conditions?

2. Would an independent company under the same conditions agree to payment of the additional fee – a commission on annual turnover?

3. Can the contract repudiation be regarded as business restructuring pursuant to Chapter IX of OECD Guidelines on Transfer Pricing?

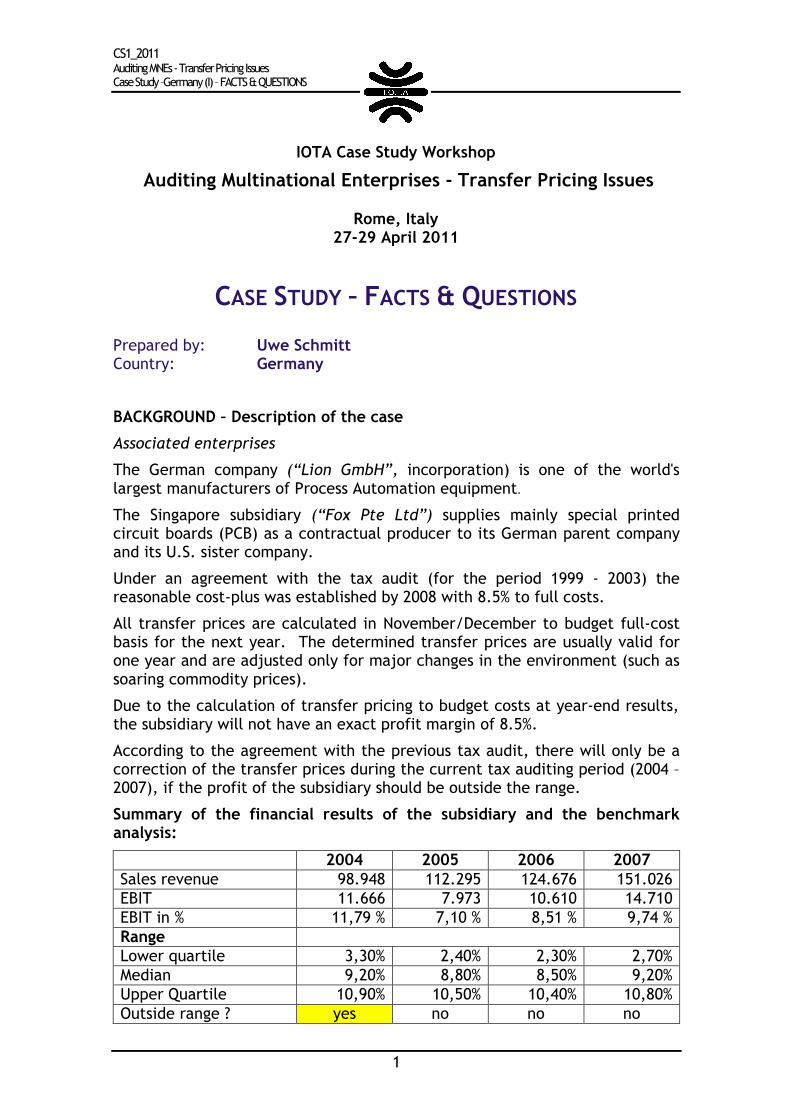

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study – Germany (II) – FACTS & QUESTIONS

1

IOTA Case Study Workshop

Auditing Multinational Enterprises - Transfer Pricing Issues

Rome, Italy 27-29 April 2011

CASE STUDY – FACTS & QUESTIONS

Prepared by: Anke Schwengel Country: Germany

BACKGROUND – Description of the case

1. Information about the company

The parent company (P), a large scale enterprise, is a German legal entity. Company P develops and produces electronic articles in Germany and distributes its products all over the world.

In the end of 2007 the 100 % subsidiary S, a Hungarian legal entity, was founded, because the customer of one special product is located in Hungary and this customer had insisted on a subsidiary in Hungary. The activities of company S began in 2008 and are concentrated in assembly, painting and printing on components of the special product.

The Key Account Management, the Pre-/After Sales Support and the Marketing are still completely in P’s responsibility. Company P develops and produces the components of the product in Germany and then sells the semi-finished products to company S. Company S finishes the products (by assembling the components, painting and printed on) and then sells them to the Hungarian customer. The Logistic concerning the finished products (inclusive Storekeeping, Transport and Factura) is in the responsibility of company S.

The owner of the essential intangible assets (the process and product know-how and the connection to the customer) is still company P.

In January 2008 companies P and S signed a “Manufacturing License and Distribution Agreement”, this agreement regulates the remuneration for the benefit of being allowed to use the intangible assets.

In December 2009 (21/12/2009) companies P and S signed a further agreement, which regulates the remuneration in a little bit different way.

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study - Germany (II) – FACTS & QUESTIONS

2

2. Transfer Pricing Method

The company P uses a two-steps transfer pricing method. a) First step: Cost plus method

The price for the routine function “production” of the semi-finished products is based on the cost plus method (all costs plus a mark up of 5 %).

b) Second step: Transactional profit method

The price for using the intangible assets is regulated in the “Manufactoring License and Distribution Agreement”. The remuneration is calculated on basis of the whole profit margin concerning the product. The difference between the profit margin for the routine function “production” and the whole profit margin in principle shall be distributed (allocated) to companies P and S according to the company’s calculations and analysis (here not further explained because of its complexity and irrelevance in this case). The agreement stipulates further, that company S must have a minimum profit (EBIT) of 5 %, because company S has to be considered as a low risk enterprise. If company S doesn’t reach an EBIT of more than 5 %, there is no payment of royalties. Quite the opposite: if the EBIT is less 5 %, company P has to pay compensation! In the later agreement (dated 21/12/2009) is regulated, that company P in principle has to pay a compensation for launching costs, if company’s S EBIT is less 5 %. But when company S produces bad quality or delivers damaged products and if the percentage of the returned sales is more than 5 % higher than usual, company P is not obliged to pay any compensation.

3. Problems

Because of the regulations in the “Manufactoring License and Distribution Agreement” in 2008 company P had to pay a compensation of 6.900.000 Euros (€). Without the compensation payment company S would have made a loss of 4.300.000 €, after consideration of the compensation payment, the profit and loss account for 2008 shows a surplus of 2.600.000 €. Now the guideline of company’s S minimum profit margin (5 %) is exactly fulfilled.

The payment of 6.900.000 € has reduced company’s P profit 2008 and is described in the bookkeeping as a benefit payment for the introduction on the market (for launching costs). The percentage of the returned sales in 2008 is unknown. In 2009 the EBIT was far less 5 %, but company P didn’t pay any

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study - Germany (II) – FACTS & QUESTIONS

3

compensation, because the company had established that the percentage of the returned sales was more than 10 % higher than it was normally in comparable enterprises.

In both years (2008 and 2009) company S didn’t pay any remuneration for using the intangible assets.

The company states that the guarantee of 5 % EBIT for company S is necessary and determined by market forces. Company S only buys the components and finishes the products when the Hungarian customer has already ordered and therefore must be considered as a low risk enterprise. Company S is founded to work exclusively for the parent company P and because of this P has to pay for the launching costs. Company S is merely responsible for rejects (bad quality, returned sales) and delays in delivery, there were no other risks. QUESTIONS

1. Would you accept the transfer pricing method (two-steps and a guarantee of the 5 %-EBIT for company S, no remuneration for using the intangible assets)?

2. Is this transfer pricing method applied in accordance with the Arm’s Length Principle and the OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations, and in particular:

a) Company S buys the semi-finished products and sells the finished products in its own name. This is different from doing only industrial services for company P. Is the cost-plus method (first step) the correct transfer pricing method?

b) Who has to bear the launching costs usually?

c) Is an EBIT of minimum 5 % appropriate to the functions and risks of company S (as a low risk producer)? What do you think would be the maximum margin?

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study - Switzerland – FACTS & QUESTIONS

1

IOTA Case Study Workshop

Auditing Multinational Enterprises - Transfer Pricing Issues

Rome, Italy 27-29 April 2011

CASE STUDY – FACTS & QUESTIONS

Prepared by: Thomas Brunner, Jan Edelmann Country: Switzerland

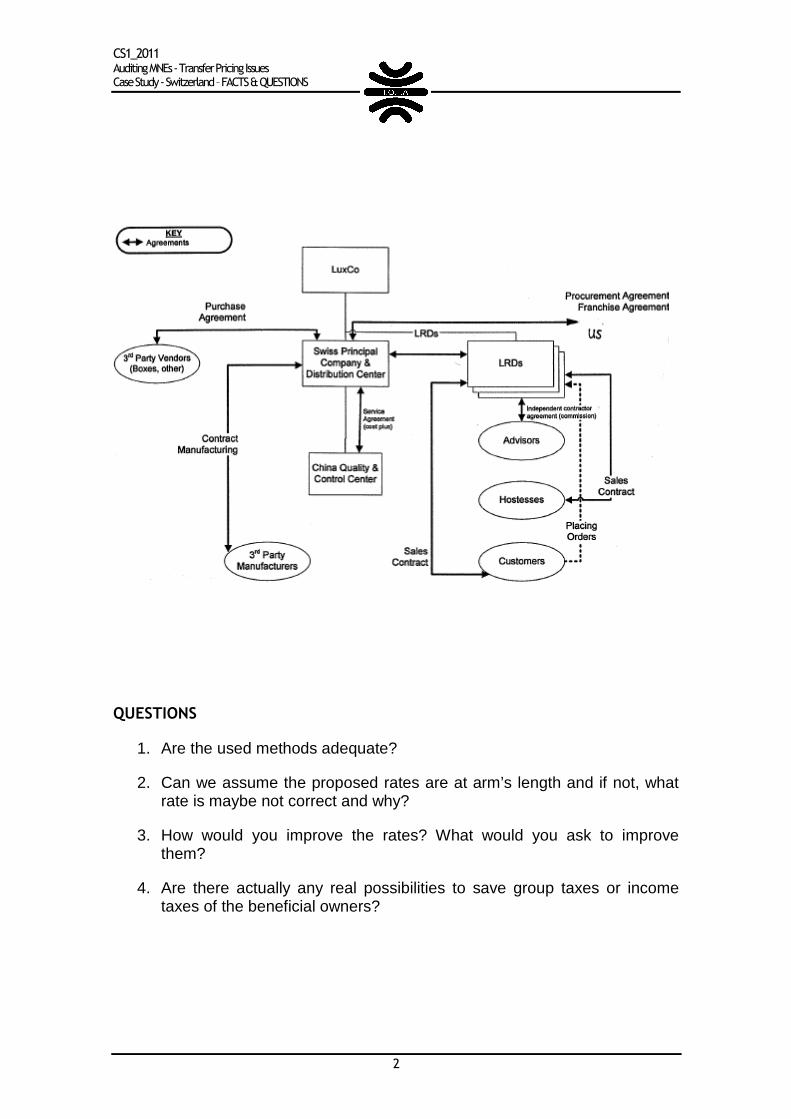

BACKGROUND – Description of the case

A group develops and manufactures beauty products and is selling them on the US and Canada Market. With its recent entrance into the European market, the group is building up a principal in Switzerland. The principial’s focus is on building up the vendor market, the European distribution center and the procurement for the whole group. By increase the principal should take more and more charge of marketing activities. The success of the group is based on direct selling system, similar to “Tupperware Parties”. The principal is directly hold by a holding based in Luxembourg and the Luxembourg holding is directly hold by a privately hold US-LLC. It’s planned that the Swiss principal holds a Chinese representation or legal entity with purpose of procurement and quality control. The remuneration is not yet defined and is not a question on this case study. The company asked for a tax ruling (means “APA”) to confirm arm’s length ranges for the following intercompany transactions: Low risk distributors: Cost plus, mark up 5 % US Holder of IP: Franchise fee of 7 % (decreasing over some years) Swiss principal for group procurement: Cost plus on Swiss costs, mark up 2,6 %

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study - Switzerland – FACTS & QUESTIONS

2

QUESTIONS

1. Are the used methods adequate?

2. Can we assume the proposed rates are at arm’s length and if not, what rate is maybe not correct and why?

3. How would you improve the rates? What would you ask to improve them?

4. Are there actually any real possibilities to save group taxes or income taxes of the beneficial owners?

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study -France – FACTS & QUESTIONS

1

IOTA Case Study Workshop

Auditing Multinational Enterprises - Transfer Pricing Issues

Rome, Italy 27-29 April 2011

CASE STUDY – FACTS & QUESTIONS

Prepared by: Stéphane Lesage Country: France

BACKGROUND – Description of the case

Case: commission agent and high quality standards

Facts

• Description of the case

Polo France is a French company and has been part of a multinational group, Polo Group, since 2007. The ultimate owner, Polo Incorporated, is registered in USA. The group (Polo Group) is engaged in the business of manufacturing, selling and promoting high quality apparel and has sales activities all over the world.

Polo France, whole-owned by Polo Inc., is the sales company located in France.

The trademark Polo is associated with a company known for high standards and excellence.

Polo Inc.:

- holds the right and interest in the trademark Polo but doesn’t charge any license fee for the Polo brand,

- wished to maintain the image of the trademark throughout the world

and to promote the Polo products.

Polo France operates a “flagship store” and has to maintain to the exacting high quality standards demanded by Polo Inc. to promote the image of the Polo Group.

The locations of the Polo France’s stores are imposed by Polo Inc. in famous addresses in Paris.

So, to respect the high quality standards of the Polo Group, the French company bears important costs of implantation (like expensive rents, works, the design and decoration…).

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study - France – FACTS & QUESTIONS

2

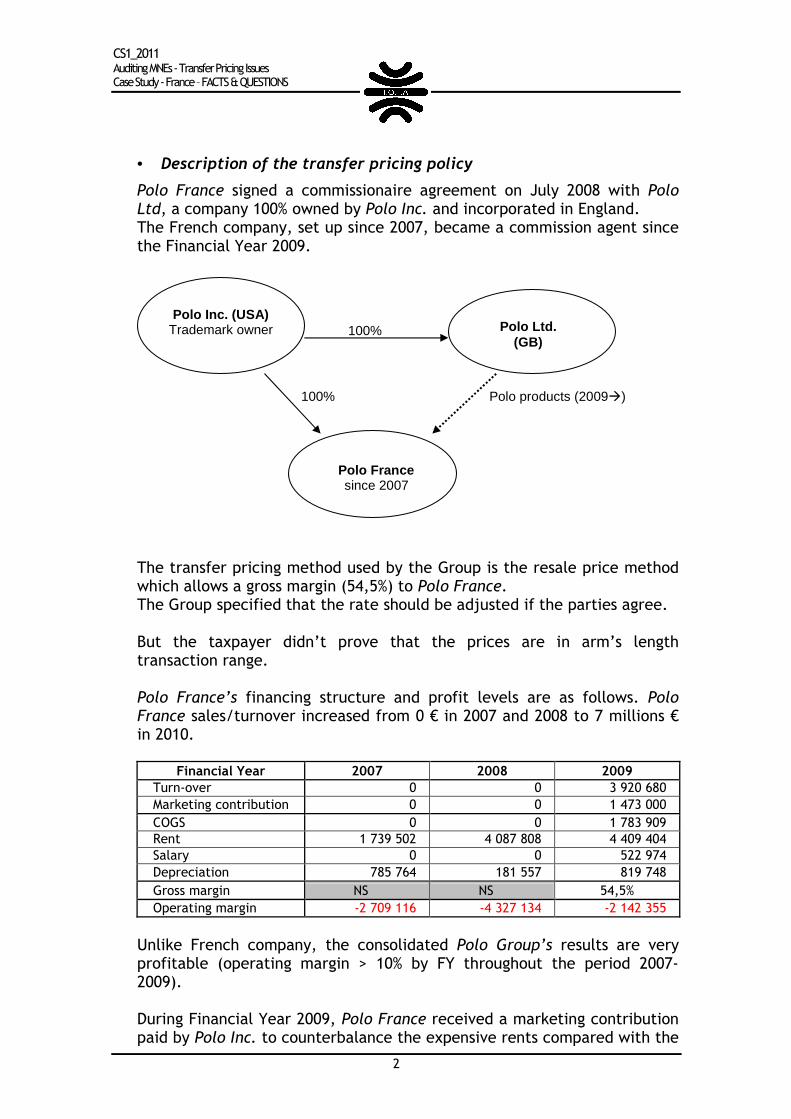

• Description of the transfer pricing policy

Polo France signed a commissionaire agreement on July 2008 with Polo Ltd, a company 100% owned by Polo Inc. and incorporated in England. The French company, set up since 2007, became a commission agent since the Financial Year 2009. 100% 100% Polo products (2009�) The transfer pricing method used by the Group is the resale price method which allows a gross margin (54,5%) to Polo France. The Group specified that the rate should be adjusted if the parties agree. But the taxpayer didn’t prove that the prices are in arm’s length transaction range. Polo France’s financing structure and profit levels are as follows. Polo France sales/turnover increased from 0 € in 2007 and 2008 to 7 millions € in 2010.

Financial Year 2007 2008 2009

Turn-over 0 0 3 920 680

Marketing contribution 0 0 1 473 000

COGS 0 0 1 783 909

Rent 1 739 502 4 087 808 4 409 404

Salary 0 0 522 974

Depreciation 785 764 181 557 819 748

Gross margin NS NS 54,5%

Operating margin -2 709 116 -4 327 134 -2 142 355

Unlike French company, the consolidated Polo Group’s results are very profitable (operating margin > 10% by FY throughout the period 2007-2009).

During Financial Year 2009, Polo France received a marketing contribution paid by Polo Inc. to counterbalance the expensive rents compared with the

Polo Inc. (USA) Trademark owner Polo Ltd.

(GB)

Polo France since 2007

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study - France – FACTS & QUESTIONS

3

others stores of the Group in France which are not located in so prestigious locations. In conclusion, the Polo Group considered that:

- the French company became a commission agent since the Financial Year 2009 only,

- this method respects the arm’s length principles and is compliant with the OECD guidelines.

QUESTIONS

1. When really began the activity of Polo France? During the Financial Year 2007 (setting-up) or Financial Year 2009 (commissionaire agreement)?

2. Should the tax authorities accept a market penetration scheme for the French company?

3. Is it acceptable to admit the method of transfer pricing without adjustment? And how should an adjustment be calculated?

4. Or are there any alternative methods that could be used instead of, or in addition to, the method suggested by the Group?

20.4.2011

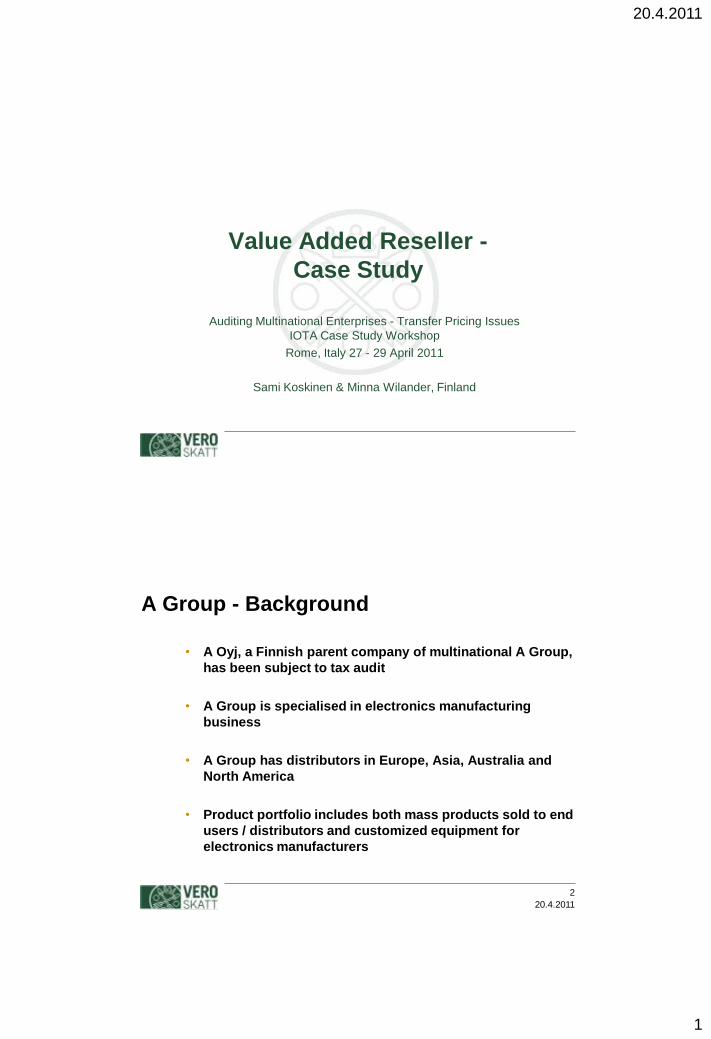

1

Value Added Reseller -

Case Study

Auditing Multinational Enterprises - Transfer Pricing Issues

IOTA Case Study Workshop

Rome, Italy 27 - 29 April 2011

Sami Koskinen & Minna Wilander, Finland

20.4.2011

2

A Group - Background

• A Oyj, a Finnish parent company of multinational A Group,

has been subject to tax audit

• A Group is specialised in electronics manufacturing

business

• A Group has distributors in Europe, Asia, Australia and

North America

• Product portfolio includes both mass products sold to end

users / distributors and customized equipment for

electronics manufacturers

20.4.2011

2

20.4.2011

3

A Oyj - Functional analysis

• Functions of A Oyj

• manufacturing, R&D, sourcing, brand management, most of the

marketing functions

• A Oyj bears

• business risk, sales strategy risk, currency risk and the risks

related to it’s above mentioned functions

• A Oyj owns

• patents, customer lists, trademarks and software

• A Group: the value added is generated in sales,

distribution and after-sales services

20.4.2011

4

VAR - Functional analysis

• Group distributors

• sales and marketing of products

• bear customer, market, price and warehousing risks

• A Group classifies it’s distributors as VAR’s (value added

resellers)

• TP documentation; ”VAR is a company that adds some feature to

an existing product and sells it. The value can come from

professional services such as integrating, customizing, consulting,

training and implementation. The value can also be by developing

a specific application for the product designed for customer’s

needs which is then resold as a new package.”

20.4.2011

3

20.4.2011

5

A Group - TP Method Used

• The major intra-group transactions are the sales of

finished or semi-finished products from A Oyj to the

VAR’s

• Setting the prices of intra-group sales transactions

• A Group uses market price -based gross price list for both VAR’s

and external customers (with a variable coefficient)

• A Oyj did not diclose the list

• A Group has applied Resale Price Method, RPM in testing

the transfer prices

• comparables’ weighted average interquartile range of gross

margins was between 19,9 % and 34,1 %, median was 27,5 %

• VARs’ gross margins varied between 21,4 % - 30,8 %, with an

average gross margin of 25,4 %

20.4.2011

6

Tax Auditors - On applicability of RPM

• Resale Price Method is not applicable

• VAR’s add value to the goods by customizing and offering related

services before the resale

• Comparability factors: requires reasonably high level of similarity

of functions, risks and assets as well as the characteristics of

goods to ascertain comparability

• Accounting standards, similarity of costs included - > A Oyj has

used material costs information instead of lacking COGS to

calculate GM for some of the comparables

• TNMM should be applied instead, PLI = EBIT margin

• Require lesser degree of comparability of functions, risks and

goods sold than RPM

• Facts and circumstances

20.4.2011

4

20.4.2011

7

A Group - On applicability of RPM (1)

• RPM is most suitable

• OECD: should in principal be applied to distributors

• VAR’s are risk-bearing distributors and therefore no certain level

of EBIT margin can be guaranteed

• Price setting is based on a gross price list wich is used also both

for internal and external transactions

• Most of the revenue accrues and value generates from services

• Only 10 % of the products are customized

• TNMM is not suitable

• Other facts than functions or characteristics of products affect the

EBIT margins - > A Oyj cannot affect the EBIT margins of VAR’s

• Application of TNMM would in fact characterize the VAR’s as

LRD’s

20.4.2011

8

A Group - On applicability of RPM (2)

• Tax payer has a better understanding of the most suitable

method

• Reliability in RPM can be added by qualitative search

steps

• Using the same method when setting the price and testing

the arm’s length nature is more reliable

• A Oyj’s EBIT margins for internal transactions have been

higher than top quartile EBIT margins

20.4.2011

5

20.4.2011

9

A Group - Questions

• What kind of guidance of application do OECD Guidelines

provide for testing the arm’s length nature of transactions

with a related party distributor?

• What kind of factors affect the selection of the most

applicable method in this case?

• What would be your solution?

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study - Finland – FACTS & QUESTIONS

1

IOTA Case Study Workshop

Auditing Multinational Enterprises - Transfer Pricing Issues

Rome, Italy 27-29 April 2011

CASE STUDY – FACTS & QUESTIONS

Prepared by: Minna Wilander / Sami Koskinen Country: Finland

BACKGROUND – Description of the case

The Audit A Oyj has been subject to tax audit covering the fiscal years 2006-2008. The main issue was to audit the arm’s length nature of the intra-group prices of sales operations. In the audit, Group’s transfer pricing documentation, including functional and economical analyses regarding manufacturing functions of A Oyj and distribution functions of Group’s sales companies, was analyzed.

Transfer Pricing Documentation of Group A In the documentation, the operations of the Group were presented as follows (documentation text intended):

A Oyj, established in 1995, is the head office of a global, full-service electronic appliances supplier Group A. A Oyj is focused entirely on producing, developing, selling and marketing the appliances. A Oyj’s products are sold in more than 100 countries. In addition to direct sales, A Oyj also supplies products to distributors, machine and equipment manufacturers and brand label customers. Group A has own sales subsidiaries in Sweden, Norway, Germany, the Netherlands, Belgium, France, Great Britain, Austria, Italy, Spain, Russia, India and Australia.

The main intra-group transaction flows were the electronics sales to group sales companies. According to Group’s A transfer pricing documentation, the sales companies are comparable to a value added reseller (VAR). Group A has classified VAR as follows:

A value-added reseller is a company that adds some feature to an existing product and sells it. The value can come from professional services such as integrating, customizing, consulting, training and implementation. The value can also be by developing a specific

CS1_2011 Auditing MNEs - Transfer Pricing Issues Case Study -Finland – FACTS & QUESTIONS

2

application for the product designed for the customer’s needs which is then resold as a new package.

Transfer pricing in Group A is based on external market prices of the similar products. A Oyj has developed a synthetic gross price list. The gross prices, however, are not applied as such. For each subsidiary a coefficient is defined and the product prices are received by multiplying the gross price with the coefficient. For start-up phase sales offices in new market areas the coefficient is slightly lower during the first years. Also for specific subsidiary end customers (often OEM customers) rebates or lower coefficient are defined. In addition, there are also order-specific rebates (for example important references or big project). However, the list was not enclosed for the auditors.

The value- added is defined according to the documentation:

“The most important value added functions of Group A are sales, distribution and after sales services in the parent company and subsidiary and R&D functions at the parent company”.

The functional analysis of the Group A is as follows:

A Oyj is manufacturing the products and carries therefore all the risks related to the production. A Oyj is also responsible for all the R&D functions, component sourcing, testing, production planning and logistics of the products. A Oyj carries the warranty risks and risks related to design quality and IPR.

A Oyj and the subsidiaries are all performing contract negotiations and concluding frame and sales agreements, however, the emphasis being at parent’s side. Market analysis, customer segmentation and analysis is done both in A Oyj and in the sales subsidiaries. A Oyj and sales subsidiaries have the customer contacts, and offers are prepared and negotiated in both units. All units also give after sales services, but mostly the sales subsidiaries.