Embed Size (px)

Citation preview

Cross Border Gas Pipelinesfor Energy Stability

Contents

Regional Integration; a pressing

need01Energy cooperation; South and

Central Asia02Global Energy Trends; Pakistan’s

energy scenario03Cross Border Pipelines; Pakistan’s

Perspective04TAPI, IP and ancillary

infrastructure network 05

Why TAPI and IP – Enabling energy

security and regional integration06Implementation Challenges;

Pakistan’s perspective07LNG; Emergence of alternative08

Pipelines; Impact of non-execution09

Future of Cross Border Pipelines10

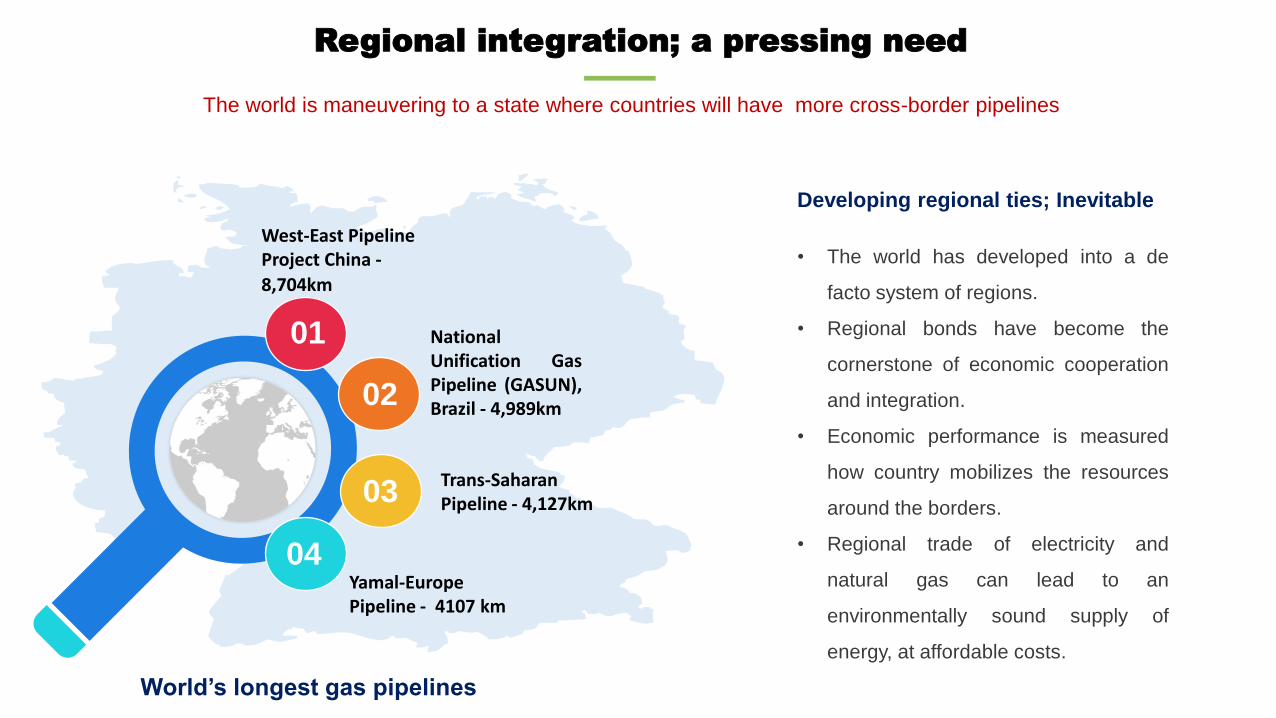

Regional integration; a pressing need

The world is maneuvering to a state where countries will have more cross-border pipelines

West-East Pipeline Project China -

8,704km

Trans-Saharan Pipeline - 4,127km

NationalUnification GasPipeline (GASUN),Brazil - 4,989km

Yamal-EuropePipeline - 4107 km

01

02

03

04

• The world has developed into a de

facto system of regions.

• Regional bonds have become the

cornerstone of economic cooperation

and integration.

• Economic performance is measured

how country mobilizes the resources

around the borders.

• Regional trade of electricity and

natural gas can lead to an

environmentally sound supply of

energy, at affordable costs.

Developing regional ties; Inevitable

World’s longest gas pipelines

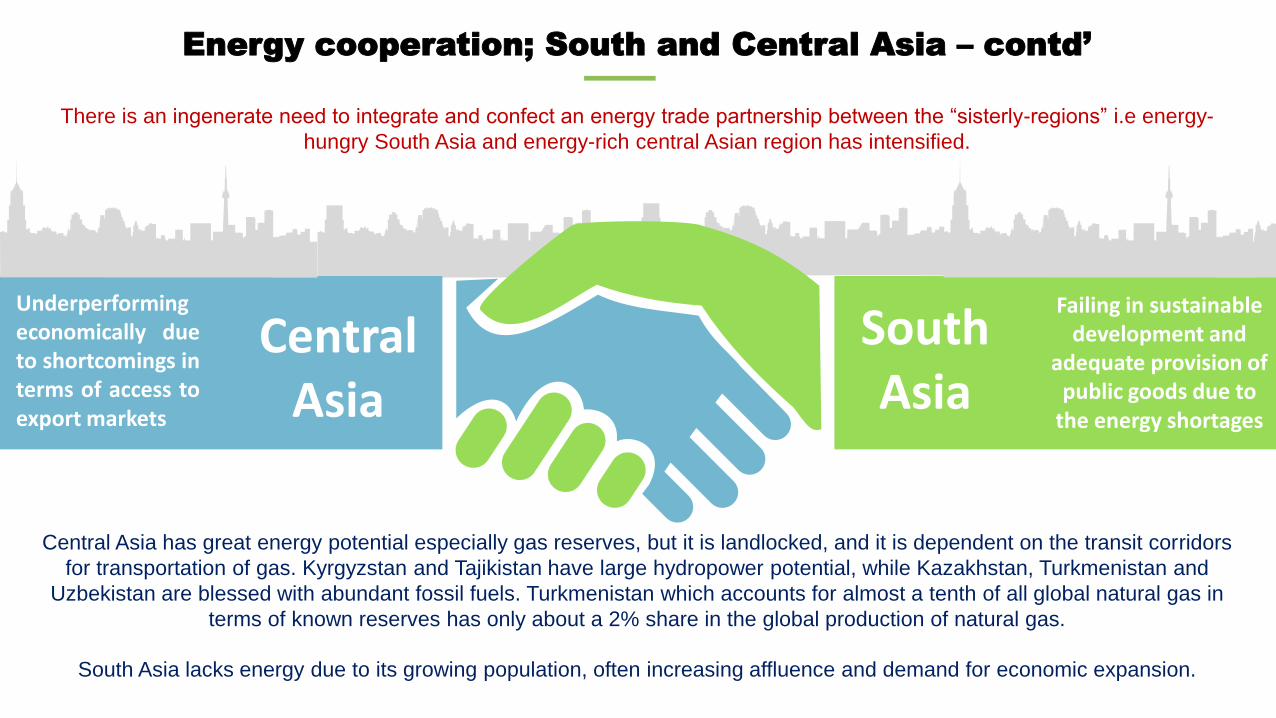

Energy cooperation; South and Central Asia – contd’

There is an ingenerate need to integrate and confect an energy trade partnership between the “sisterly-regions” i.e energy-

hungry South Asia and energy-rich central Asian region has intensified.

Failing in sustainable development and

adequate provision of public goods due to

the energy shortages

Underperformingeconomically dueto shortcomings interms of access toexport markets

Central Asia

South Asia

Central Asia has great energy potential especially gas reserves, but it is landlocked, and it is dependent on the transit corridors

for transportation of gas. Kyrgyzstan and Tajikistan have large hydropower potential, while Kazakhstan, Turkmenistan and

Uzbekistan are blessed with abundant fossil fuels. Turkmenistan which accounts for almost a tenth of all global natural gas in

terms of known reserves has only about a 2% share in the global production of natural gas.

South Asia lacks energy due to its growing population, often increasing affluence and demand for economic expansion.

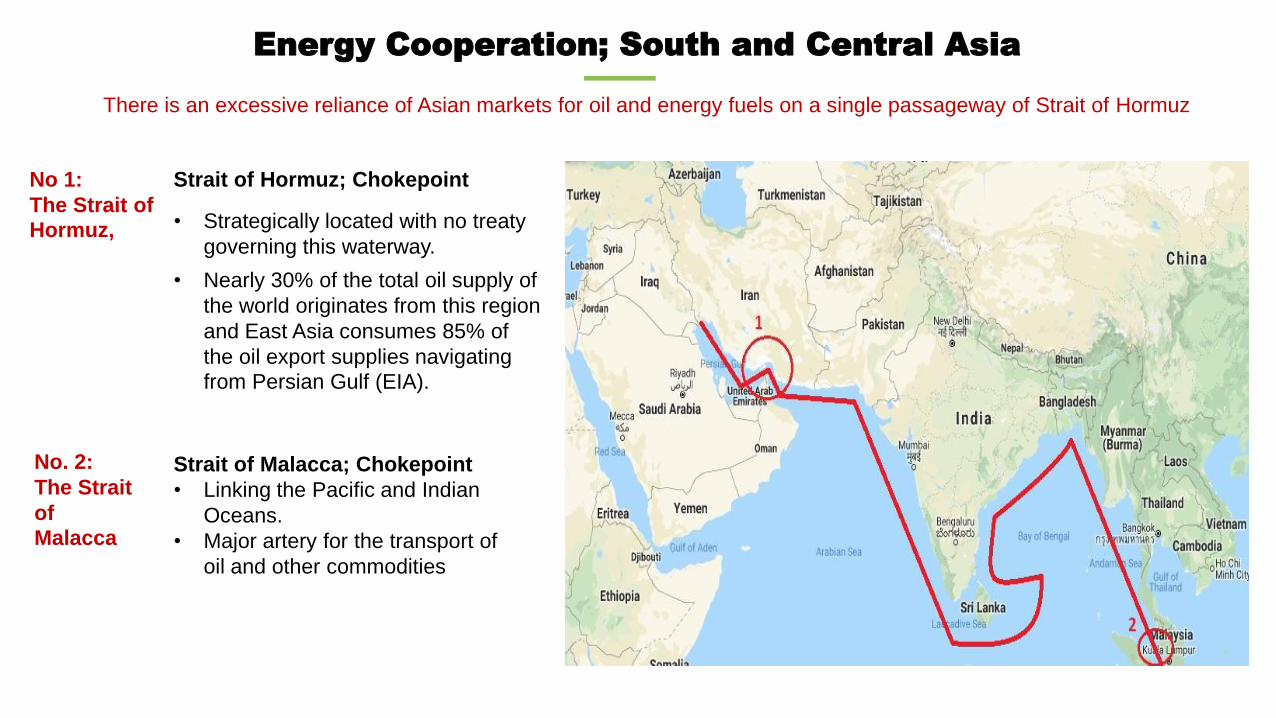

Energy Cooperation; South and Central Asia

There is an excessive reliance of Asian markets for oil and energy fuels on a single passageway of Strait of Hormuz

Strait of Hormuz; Chokepoint

• Strategically located with no treaty

governing this waterway.

• Nearly 30% of the total oil supply of

the world originates from this region

and East Asia consumes 85% of

the oil export supplies navigating

from Persian Gulf (EIA).

No 1:

The Strait of

Hormuz,

Strait of Malacca; Chokepoint

• Linking the Pacific and Indian

Oceans.

• Major artery for the transport of

oil and other commodities

No. 2:

The Strait

of

Malacca

Global Energy Trends; Pakistan’s energy scenario

In line with the global energy projections, there is an increasing demand of energy in Pakistan. Oil and gas are by far the

dominating sources of energy in Pakistan.

Pakistan; Net energy Importer

Import is creating a dent on Pakistan’s

economic stand and specifically the

foreign exchange reserves.

Perceptible recourse is to adopt an

appropriate energy mix offering

reliability, affordability and

sustainability.

Renewable energy and Gas imports

can provide short term solutions

“There is a strong consumption growth trajectory for renewable energy sources and gas.”

Pakistan

The geopolitical landscape of the

world is being remade by the

increasing demand for energy

resources.

Rising automation, industrialization

and prosperity is mainly driving this

increase in global energy demand.

Global energy demand mostly met

by fossil fuels (Oil: 30%, Coal: 27%

and Gas: 20%).

Global energy demand will increase

by at least a quarter between now

and 2040.

(Source: www.enerdata.com)

Global

A primary analysis of the energy

demand mix reveals that renewable

energy has the largest growth in long

term followed by gas establishing a

strong consumption growth trajectory

over the last few years and is

expected to continue in future.

Since 2010, average global gas

consumption has grown by 1.8% per

year, making it the fastest growing

energy source after renewable

power.

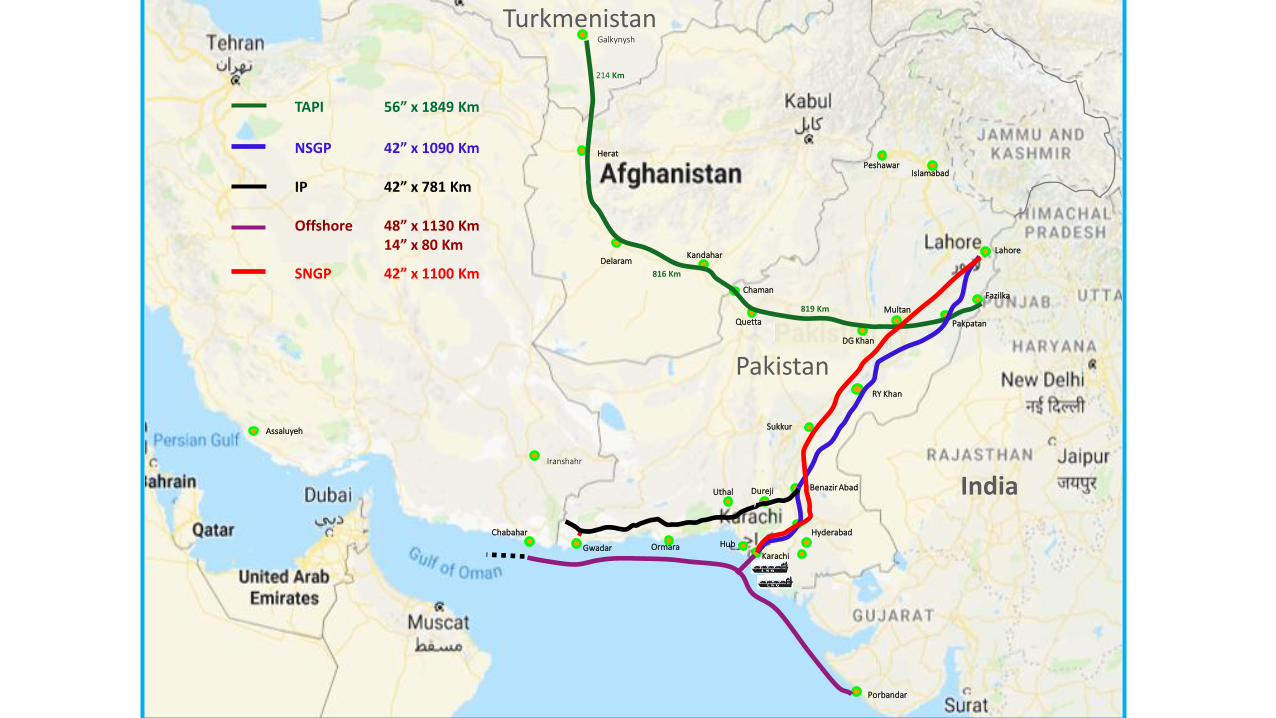

Gwadar

Multan

Galkynysh

Peshawar

Benazir Abad

Sukkur

RY Khan

Islamabad

Porbandar

KarachiOrmara

Chabahar

Assaluyeh

Chaman

Hyderabad

Iranshahr

Lahore

Quetta

Fazilka

PakistanDG Khan

India

Turkmenistan

Herat

KandaharDelaram

DurejiUthal

Pakpatan

Hub

819 Km

816 Km

214 Km

TAPI 56” x 1849 Km

NSGP 42” x 1090 Km

IP 42” x 781 Km

Offshore 48” x 1130 Km14” x 80 Km

SNGP 42” x 1100 Km

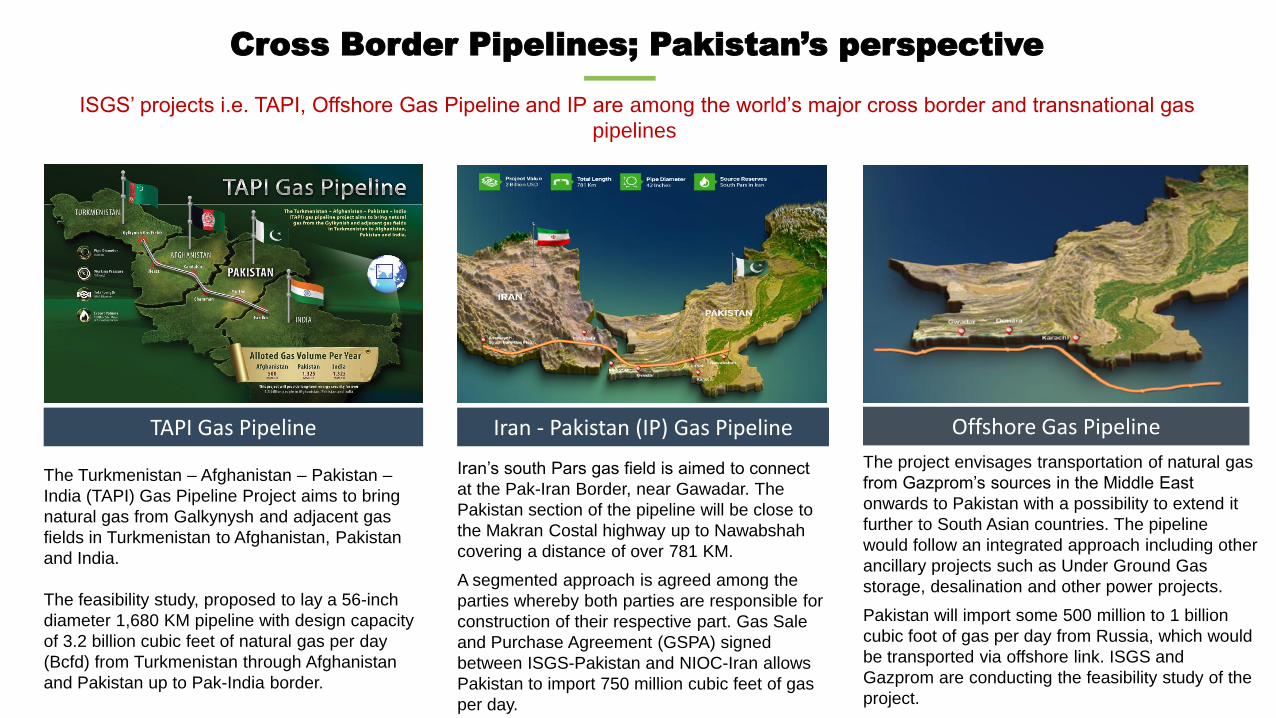

TAPI Gas Pipeline Offshore Gas PipelineIran - Pakistan (IP) Gas Pipeline

Project 1 Project 2 Project 3 Project 4

The project envisages transportation of natural gas

from Gazprom’s sources in the Middle East

onwards to Pakistan with a possibility to extend it

further to South Asian countries. The pipeline

would follow an integrated approach including other

ancillary projects such as Under Ground Gas

storage, desalination and other power projects.

Pakistan will import some 500 million to 1 billion

cubic foot of gas per day from Russia, which would

be transported via offshore link. ISGS and

Gazprom are conducting the feasibility study of the

project.

The Turkmenistan – Afghanistan – Pakistan –

India (TAPI) Gas Pipeline Project aims to bring

natural gas from Galkynysh and adjacent gas

fields in Turkmenistan to Afghanistan, Pakistan

and India.

The feasibility study, proposed to lay a 56-inch

diameter 1,680 KM pipeline with design capacity

of 3.2 billion cubic feet of natural gas per day

(Bcfd) from Turkmenistan through Afghanistan

and Pakistan up to Pak-India border.

Cross Border Pipelines; Pakistan’s perspective

ISGS’ projects i.e. TAPI, Offshore Gas Pipeline and IP are among the world’s major cross border and transnational gas

pipelines

Iran’s south Pars gas field is aimed to connect

at the Pak-Iran Border, near Gawadar. The

Pakistan section of the pipeline will be close to

the Makran Costal highway up to Nawabshah

covering a distance of over 781 KM.

A segmented approach is agreed among the

parties whereby both parties are responsible for

construction of their respective part. Gas Sale

and Purchase Agreement (GSPA) signed

between ISGS-Pakistan and NIOC-Iran allows

Pakistan to import 750 million cubic feet of gas

per day.

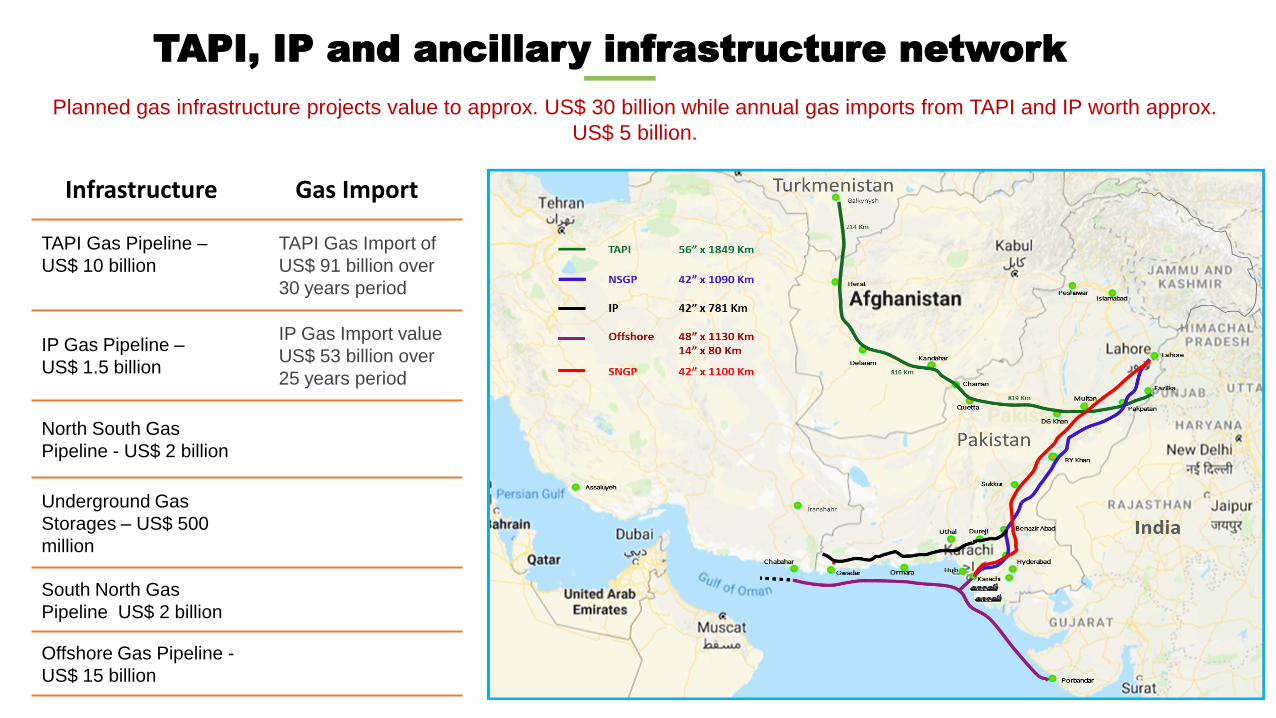

Infrastructure Gas Import

TAPI Gas Pipeline –

US$ 10 billion

TAPI Gas Import of

US$ 91 billion over

30 years period

IP Gas Pipeline –

US$ 1.5 billion

IP Gas Import value

US$ 53 billion over

25 years period

North South Gas

Pipeline - US$ 2 billion

Underground Gas

Storages – US$ 500

million

South North Gas

Pipeline US$ 2 billion

Offshore Gas Pipeline -

US$ 15 billion

TAPI, IP and ancillary infrastructure network

Planned gas infrastructure projects value to approx. US$ 30 billion while annual gas imports from TAPI and IP worth approx.

US$ 5 billion.

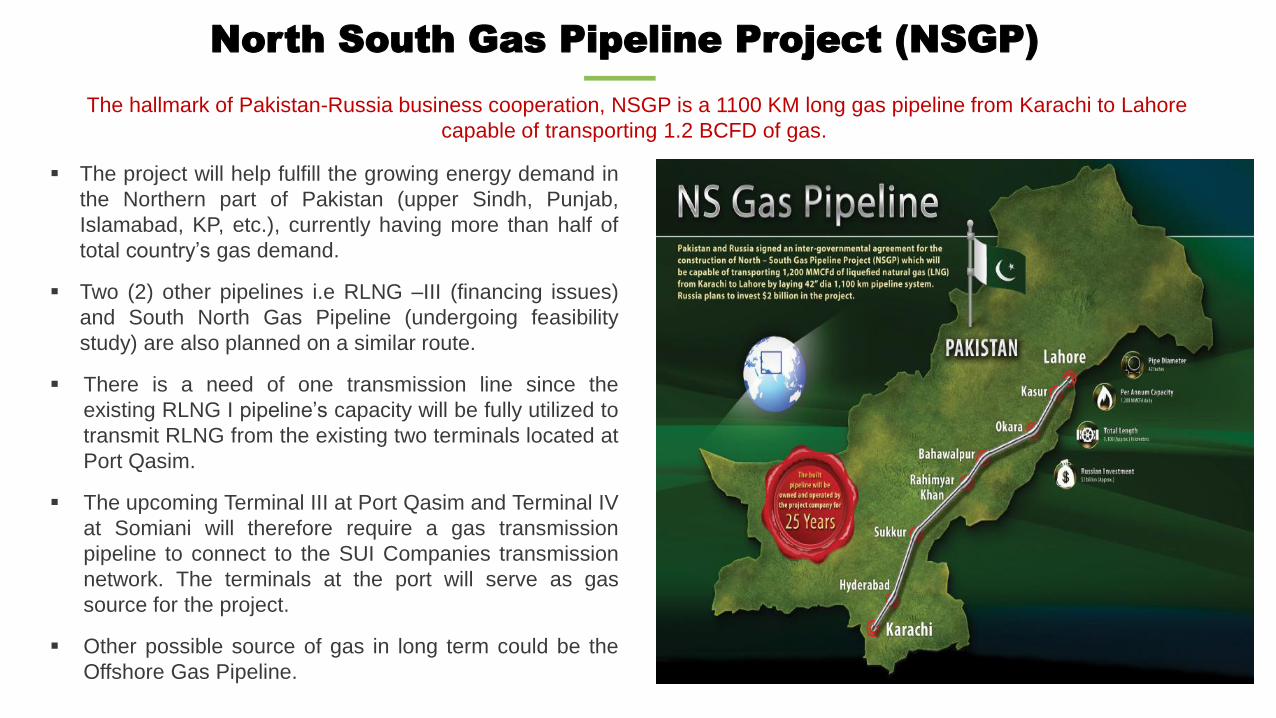

North South Gas Pipeline Project (NSGP)

The project will help fulfill the growing energy demand in

the Northern part of Pakistan (upper Sindh, Punjab,

Islamabad, KP, etc.), currently having more than half of

total country’s gas demand.

Two (2) other pipelines i.e RLNG –III (financing issues)

and South North Gas Pipeline (undergoing feasibility

study) are also planned on a similar route.

There is a need of one transmission line since the

existing RLNG I pipeline’s capacity will be fully utilized to

transmit RLNG from the existing two terminals located at

Port Qasim.

The upcoming Terminal III at Port Qasim and Terminal IV

at Somiani will therefore require a gas transmission

pipeline to connect to the SUI Companies transmission

network. The terminals at the port will serve as gas

source for the project.

Other possible source of gas in long term could be the

Offshore Gas Pipeline.

The hallmark of Pakistan-Russia business cooperation, NSGP is a 1100 KM long gas pipeline from Karachi to Lahore

capable of transporting 1.2 BCFD of gas.

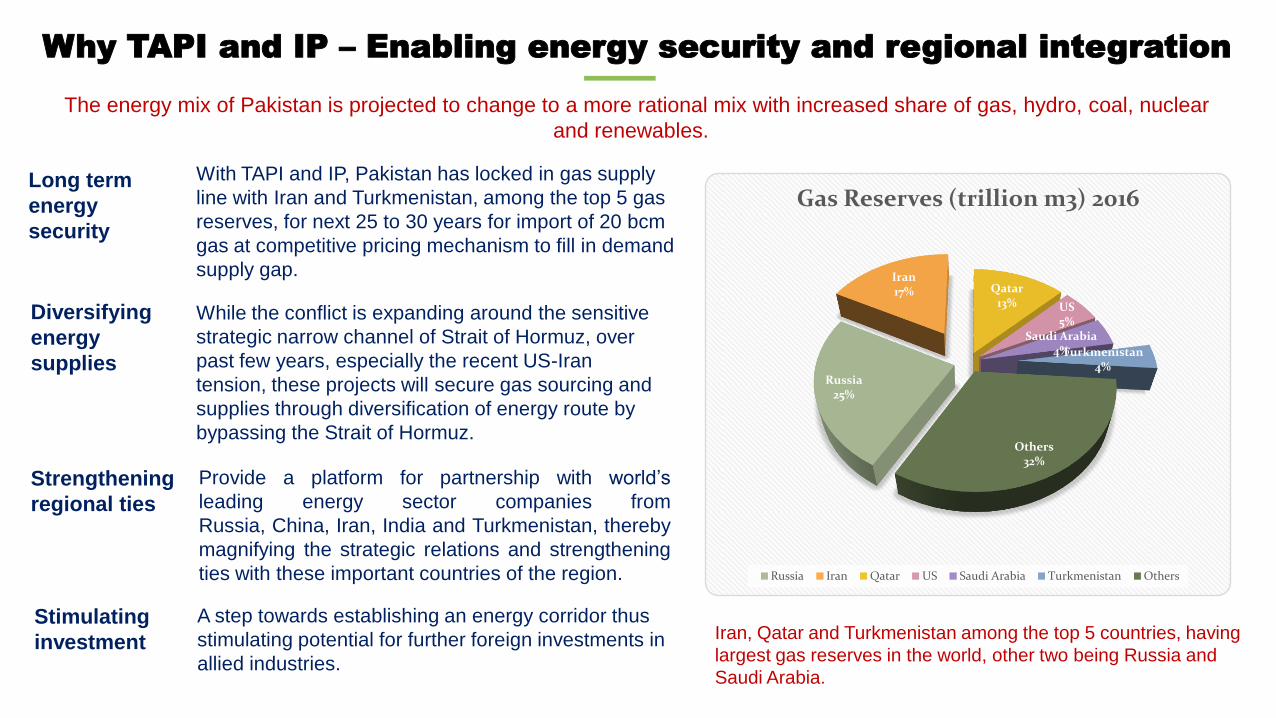

Why TAPI and IP – Enabling energy security and regional integration

The energy mix of Pakistan is projected to change to a more rational mix with increased share of gas, hydro, coal, nuclear

and renewables.

Iran, Qatar and Turkmenistan among the top 5 countries, having

largest gas reserves in the world, other two being Russia and

Saudi Arabia.

Russia25%

Iran17% Qatar

13% US5%

Saudi Arabia4%Turkmenistan

4%

Others32%

Gas Reserves (trillion m3) 2016

Russia Iran Qatar US Saudi Arabia Turkmenistan Others

With TAPI and IP, Pakistan has locked in gas supply

line with Iran and Turkmenistan, among the top 5 gas

reserves, for next 25 to 30 years for import of 20 bcm

gas at competitive pricing mechanism to fill in demand

supply gap.

While the conflict is expanding around the sensitive

strategic narrow channel of Strait of Hormuz, over

past few years, especially the recent US-Iran

tension, these projects will secure gas sourcing and

supplies through diversification of energy route by

bypassing the Strait of Hormuz.

Provide a platform for partnership with world’s

leading energy sector companies from

Russia, China, Iran, India and Turkmenistan, thereby

magnifying the strategic relations and strengthening

ties with these important countries of the region.

A step towards establishing an energy corridor thus

stimulating potential for further foreign investments in

allied industries.

Long term

energy

security

Diversifying

energy

supplies

Strengthening

regional ties

Stimulating

investment

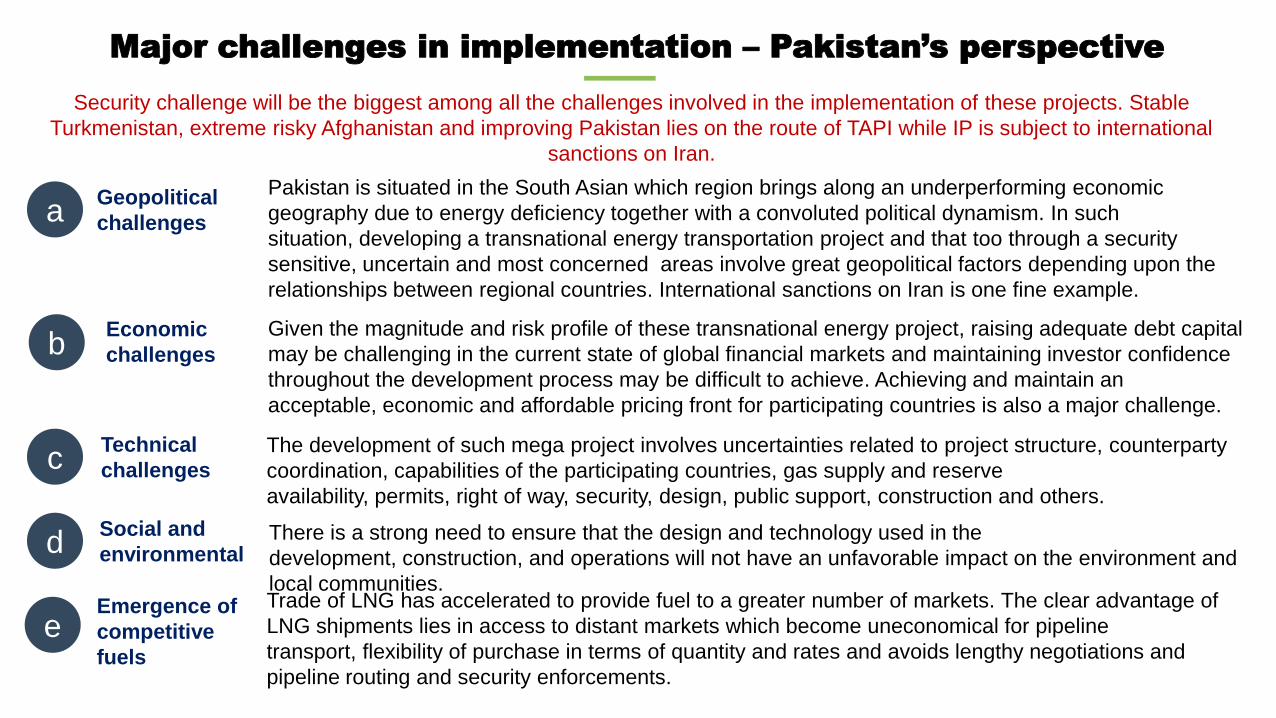

Major challenges in implementation – Pakistan’s perspective

Security challenge will be the biggest among all the challenges involved in the implementation of these projects. Stable

Turkmenistan, extreme risky Afghanistan and improving Pakistan lies on the route of TAPI while IP is subject to international

sanctions on Iran.

Pakistan is situated in the South Asian which region brings along an underperforming economic

geography due to energy deficiency together with a convoluted political dynamism. In such

situation, developing a transnational energy transportation project and that too through a security

sensitive, uncertain and most concerned areas involve great geopolitical factors depending upon the

relationships between regional countries. International sanctions on Iran is one fine example.

Given the magnitude and risk profile of these transnational energy project, raising adequate debt capital

may be challenging in the current state of global financial markets and maintaining investor confidence

throughout the development process may be difficult to achieve. Achieving and maintain an

acceptable, economic and affordable pricing front for participating countries is also a major challenge.

The development of such mega project involves uncertainties related to project structure, counterparty

coordination, capabilities of the participating countries, gas supply and reserve

availability, permits, right of way, security, design, public support, construction and others.

Geopolitical

challenges

Economic

challenges

Technical

challenges

Social and

environmentalThere is a strong need to ensure that the design and technology used in the

development, construction, and operations will not have an unfavorable impact on the environment and

local communities.

a

b

c

d

Emergence of

competitive

fuels

Trade of LNG has accelerated to provide fuel to a greater number of markets. The clear advantage of

LNG shipments lies in access to distant markets which become uneconomical for pipeline

transport, flexibility of purchase in terms of quantity and rates and avoids lengthy negotiations and

pipeline routing and security enforcements.

e

Emergence of alternative fuel product - LNG

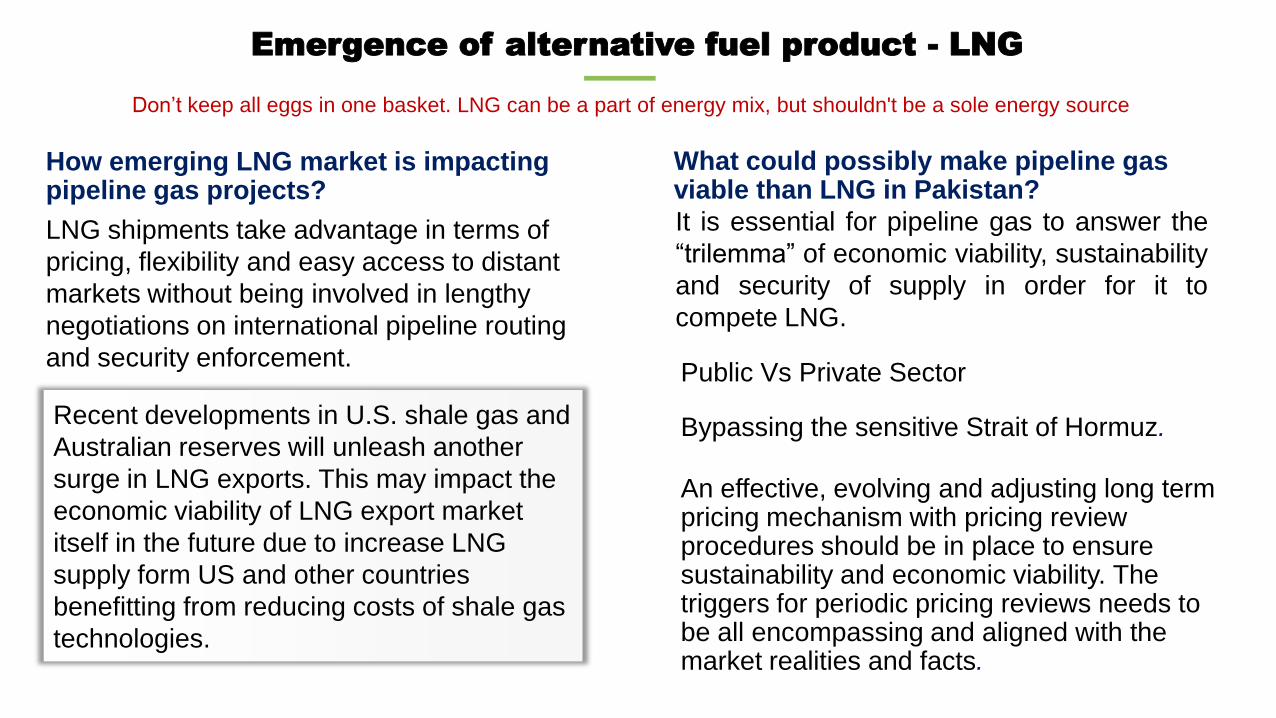

Don’t keep all eggs in one basket. LNG can be a part of energy mix, but shouldn't be a sole energy source

What could possibly make pipeline gas viable than LNG in Pakistan?

It is essential for pipeline gas to answer the

“trilemma” of economic viability, sustainability

and security of supply in order for it to

compete LNG.

LNG shipments take advantage in terms of

pricing, flexibility and easy access to distant

markets without being involved in lengthy

negotiations on international pipeline routing

and security enforcement.Public Vs Private Sector

Bypassing the sensitive Strait of Hormuz.

An effective, evolving and adjusting long term pricing mechanism with pricing review procedures should be in place to ensure sustainability and economic viability. The triggers for periodic pricing reviews needs to be all encompassing and aligned with the market realities and facts.

Recent developments in U.S. shale gas and

Australian reserves will unleash another

surge in LNG exports. This may impact the

economic viability of LNG export market

itself in the future due to increase LNG

supply form US and other countries

benefitting from reducing costs of shale gas

technologies.

How emerging LNG market is impacting pipeline gas projects?

Implication of non-execution of TAPI and IP

One can’t find any argument or justification for Pakistan not to import energy supplies especially natural gas because its

own indigenous reserves are depleting, and the demand is on rise.

IPTAPI

Non-execution of TAPI gas project shall put

crippling effects on Turkmenistan.

Afghanistan links it to the future development

and also a source of earning foreign exchange in

the form of gas transit fee.

Both India and Pakistan rely heavily on energy

imports to fulfil their rising energy demands, they

equally need TAPI pipeline. They would each get

42% of the gas supply. However, the high-octane

bilateral relationships between two countries and

the perpetual fear of escalating tension are big

hurdles to the TAPI project.

Iran is facing an extreme economic pressure owing

to international and US sanctions. Any measure to

support the economy and foreign exchange of the

country is a life support for nation’s economy.

Pakistan is among the largest consumer of energy

and is short on indigenous

resources, therefore, requires more projects other

than TAPI Pipeline to fulfill its fast growing needs of

energy.

Gazprom is making efforts to institute an offshore

pipeline natural gas from Gazprom’s sources in the

Middle East onwards to Pakistan with a possibility

to extend it further to South Asian countries.

Future of gas pipeline projects in Pakistan

There are no two views about of the vitality of Gas Pipeline projects for long term energy security of Pakistan, however, the

viability of such projects is an apprehension to address.

The gas pipeline projects i.e TAPI and IP will bring

much needed energy to energy deficient Pakistan.

Industrial and power units planned along the route

can use this natural gas for their production.

Presence and support of major energy players i.e

Russia and China in the region will be the key.

Russia is leading the world gas markets by

investing billions in infrastructure projects.

Implementation of these project will improve

regional development, strengthening regional

economic linkages and consolidating

cooperation, inter-regional harmony and political

bonds.

The Pipeline & Gas Journal survey based on

Energy Web Atlas data, indicates 145,353 miles of

pipelines were planned or under construction

worldwide at the start of year 2019.

The midstream sector is on a wave of pipeline

construction activity alongwith construction of LNG

facilities driven by the continuing global shift toward

natural gas, the rapid growth of shale

production, and the infrastructure demands created

by changing patterns of interregional trade.

A massive pipeline “Power of Siberia” linking one

of the most remote parts of Russia with a far-flung

region of China has begun delivering gas.

How gas pipeline are shaping the future of global energy markets?

What is the future of the gas pipeline in Pakistan?

Thank you