Embed Size (px)

Citation preview

Crew Resource Management in Oil & Gas Industry

Upstream India – Drilling Sector

Presented by: Tapas Kumar Basu

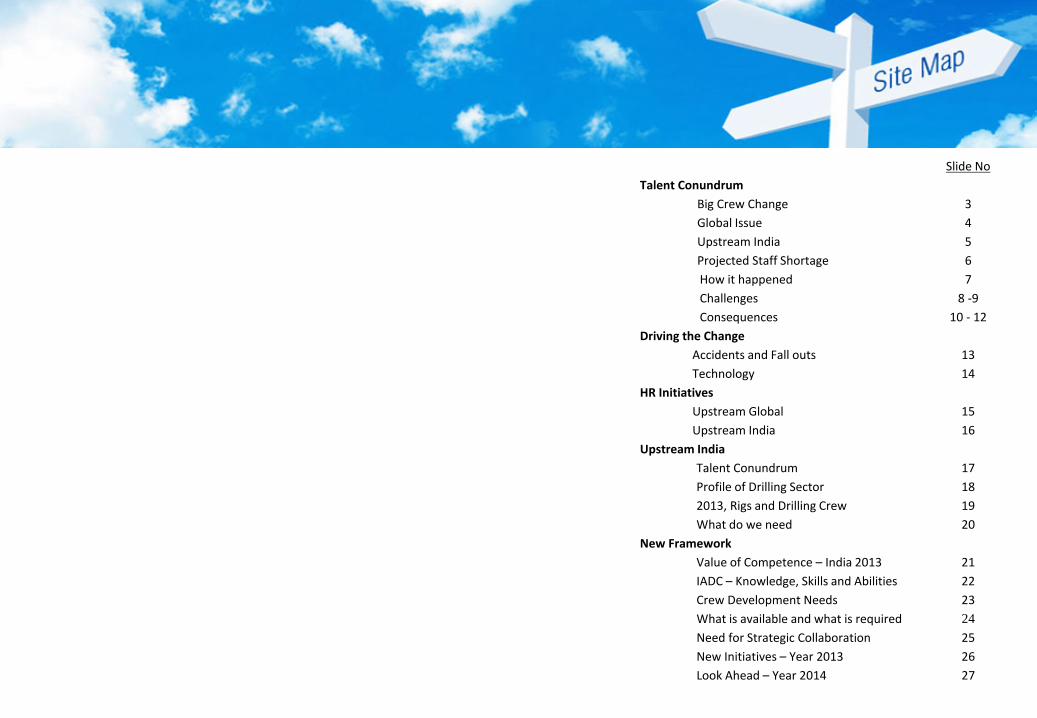

Slide No Talent Conundrum

Big Crew Change 3 Global Issue 4 Upstream India 5 Projected Staff Shortage 6 How it happened 7 Challenges 8 -9 Consequences 10 - 12

Driving the Change Accidents and Fall outs 13 Technology 14

HR Initiatives Upstream Global 15 Upstream India 16

Upstream India Talent Conundrum 17 Profile of Drilling Sector 18 2013, Rigs and Drilling Crew 19 What do we need 20

New Framework Value of Competence – India 2013 21 IADC – Knowledge, Skills and Abilities 22 Crew Development Needs 23 What is available and what is required 24 Need for Strategic Collaboration 25 New Initiatives – Year 2013 26 Look Ahead – Year 2014 27

Slide No: ‹3›

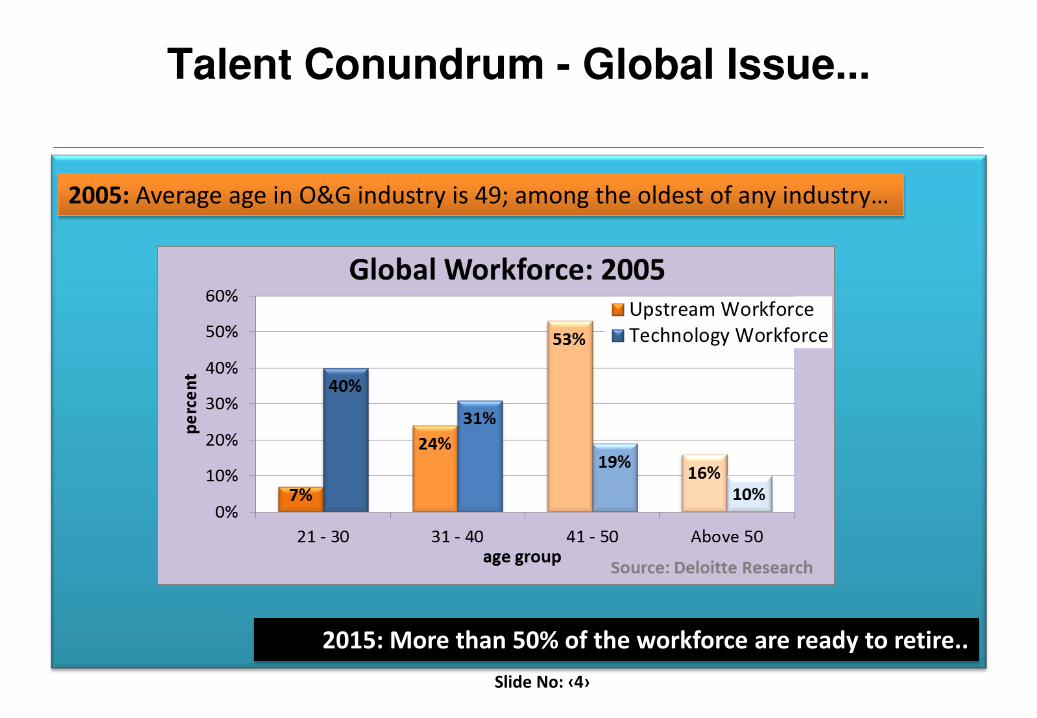

Slide No: ‹4›

2005: Average age in O&G industry is 49; among the oldest of any industry…

2015: More than 50% of the workforce are ready to retire..

Slide No: ‹5›

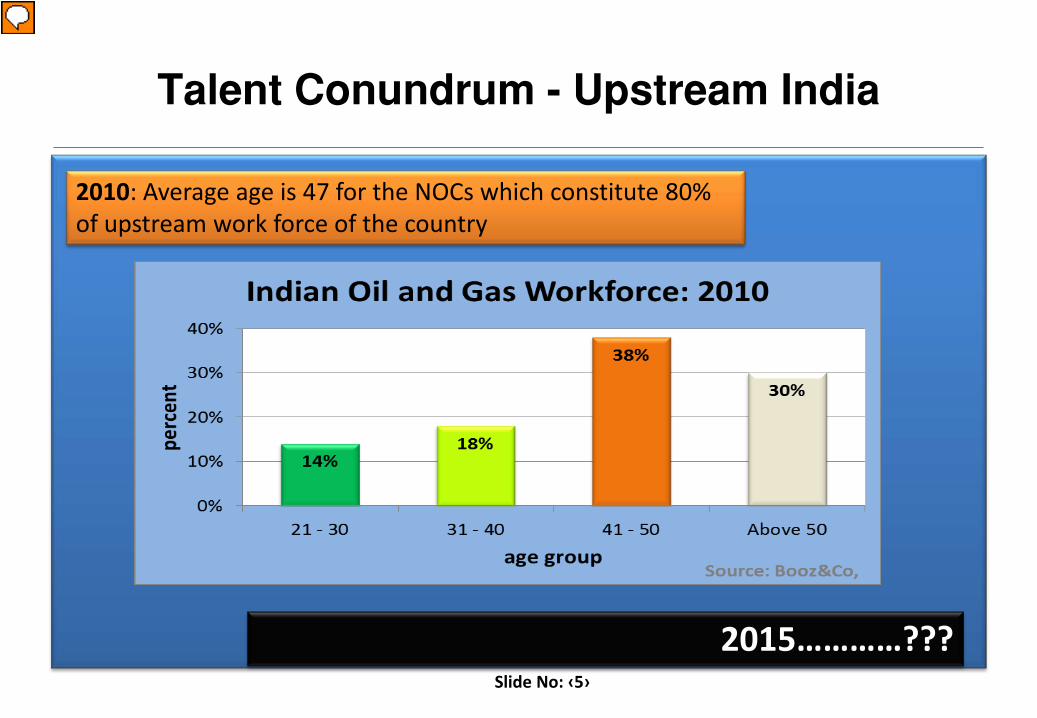

2010: Average age is 47 for the NOCs which constitute 80% of upstream work force of the country

2015…………???

Slide No: ‹6›

……Short supply of competent crew and looming talent crisis

Slide No: ‹7›

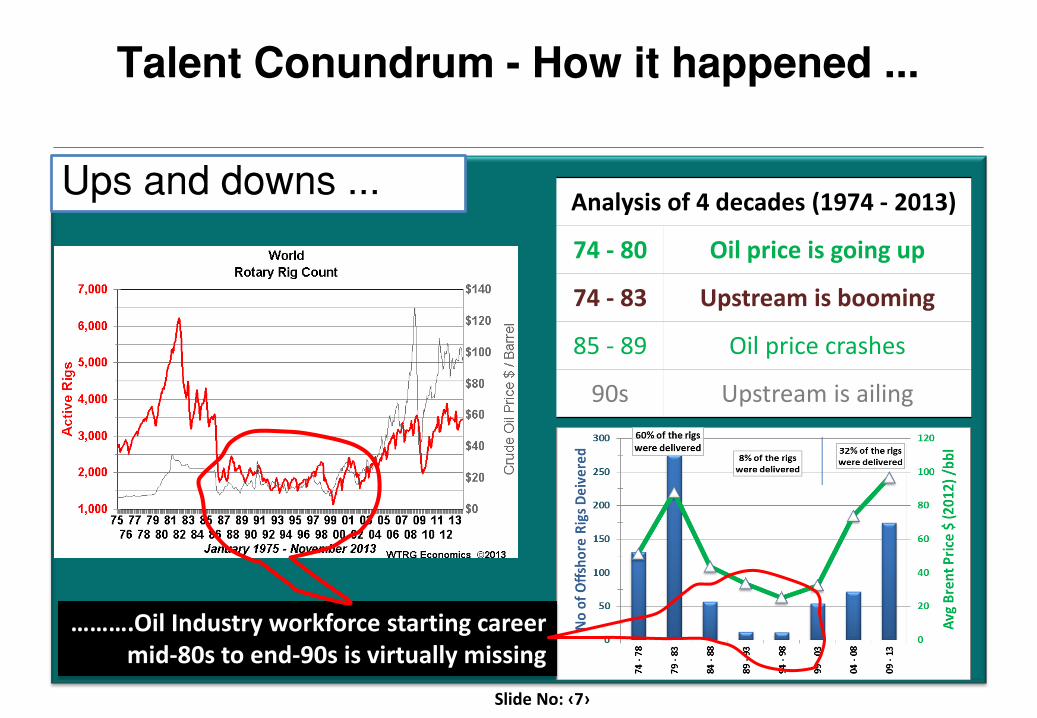

Analysis of 4 decades (1974 - 2013)

74 - 80 Oil price is going up

74 - 83 Upstream is booming

85 - 89 Oil price crashes

90s Upstream is ailing

……….Oil Industry workforce starting career mid-80s to end-90s is virtually missing

Slide No: ‹8›

More challenges as we go forward….

Slide No: ‹9›

Slide No: ‹10›

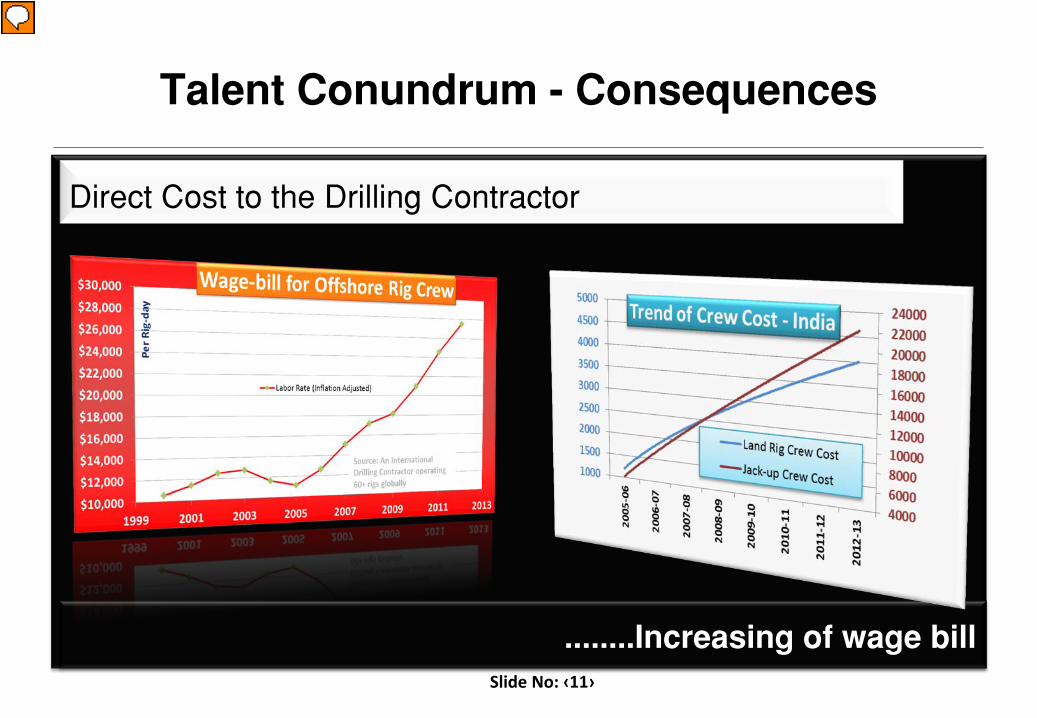

Slide No: ‹11›

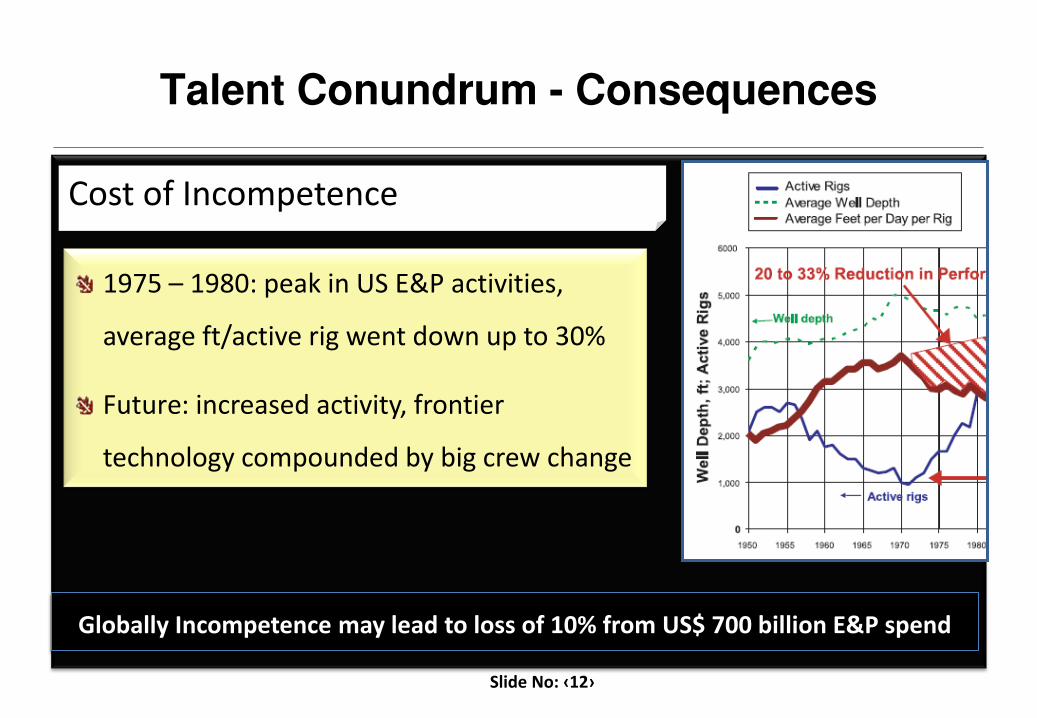

Cost of Incompetence

Slide No: ‹12›

1975 – 1980: peak in US E&P activities,

average ft/active rig went down up to 30%

Future: increased activity, frontier

technology compounded by big crew change

Globally Incompetence may lead to loss of 10% from US$ 700 billion E&P spend

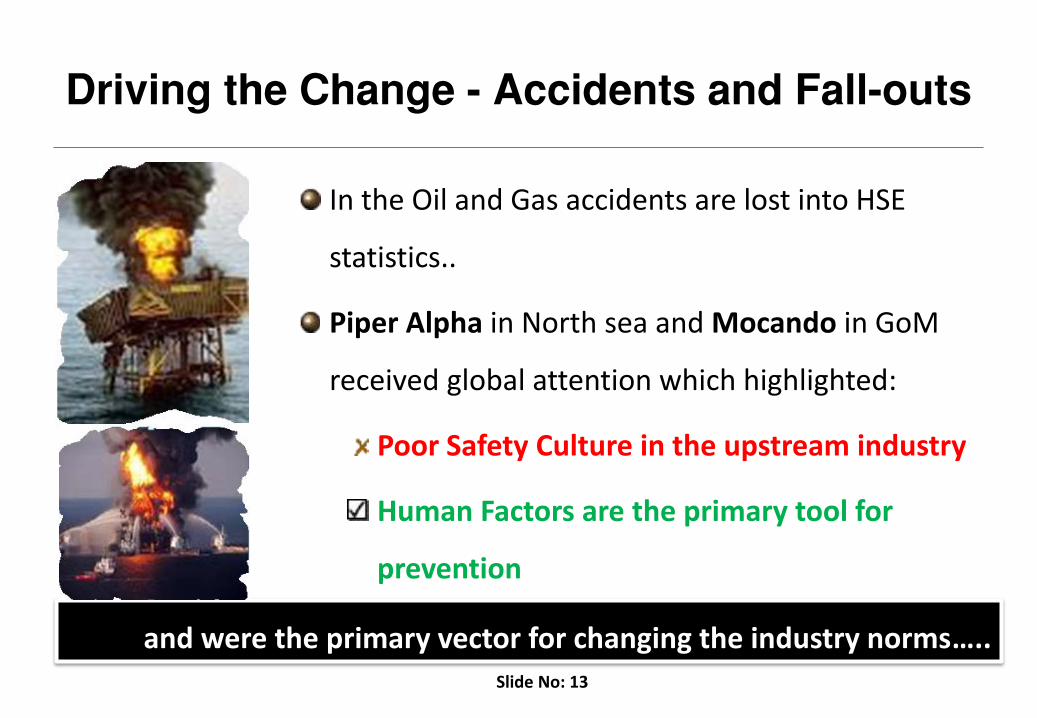

Slide No: 13

In the Oil and Gas accidents are lost into HSE

statistics..

Piper Alpha in North sea and Mocando in GoM

received global attention which highlighted:

Poor Safety Culture in the upstream industry

Human Factors are the primary tool for

prevention

and were the primary vector for changing the industry norms…..

Slide No: ‹14›

Exploration successes in deepwater and ultra-deepwater

Complex Rigs, Subsea Systems and Production Facilities

Expensive exploration program

Many new entrants in deepwater drilling and services

Currently, demand driven by exploration work;

Will increase manifold as development activity begin

Journey into Deep/ Ultra-deepwater

....importance of Safety and Performance had never been so important

Slide No: 15

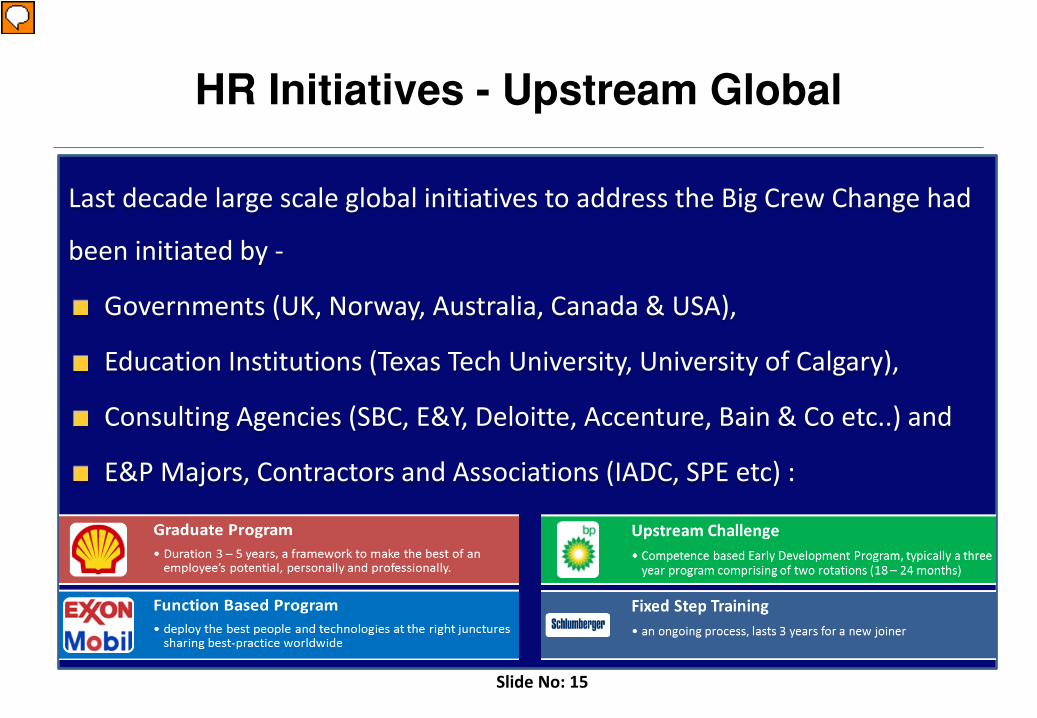

Last decade large scale global initiatives to address the Big Crew Change had

been initiated by -

Governments (UK, Norway, Australia, Canada & USA),

Education Institutions (Texas Tech University, University of Calgary),

Consulting Agencies (SBC, E&Y, Deloitte, Accenture, Bain & Co etc..) and

E&P Majors, Contractors and Associations (IADC, SPE etc) :

Slide No: ‹16›

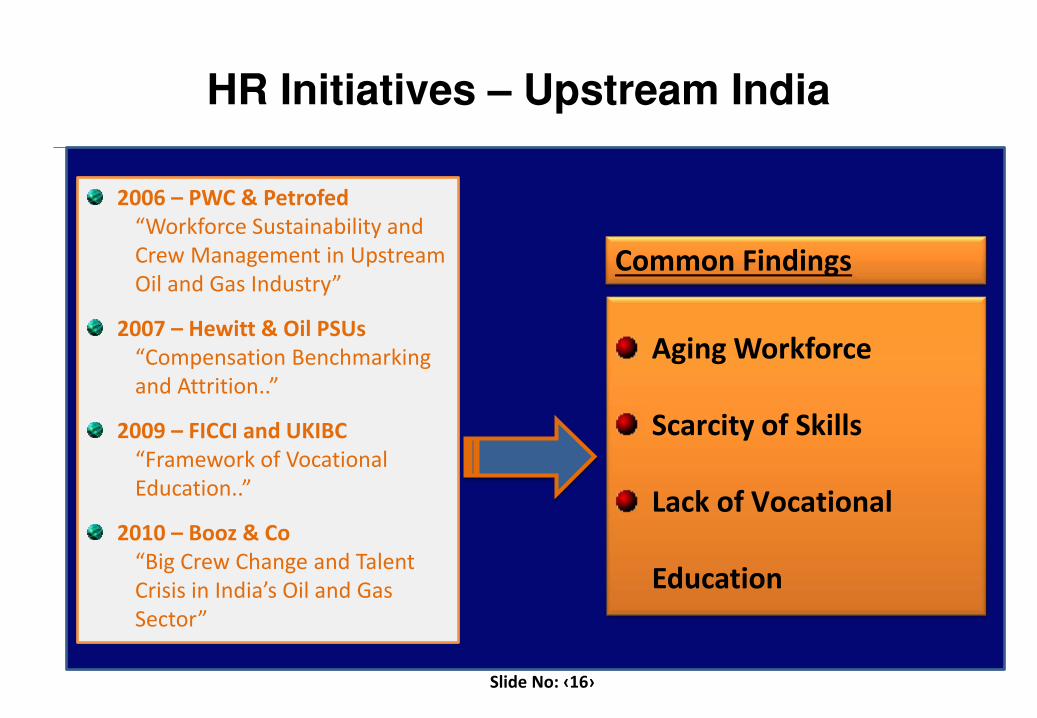

2006 – PWC & Petrofed “Workforce Sustainability and Crew Management in Upstream Oil and Gas Industry”

2007 – Hewitt & Oil PSUs “Compensation Benchmarking and Attrition..”

2009 – FICCI and UKIBC “Framework of Vocational Education..”

2010 – Booz & Co “Big Crew Change and Talent Crisis in India’s Oil and Gas Sector”

Common Findings

Aging Workforce

Scarcity of Skills

Lack of Vocational

Education

Slide No: ‹17›

4

5

6

7

8

9

10

11

30

32

34

36

38

40

42

44

2005 2006 2007 2008 2009 2010 2011 2012 2013

E&P

Budg

et (b

n U

S$)

Tota

l Wor

kfor

ce (x

100

0) --

>

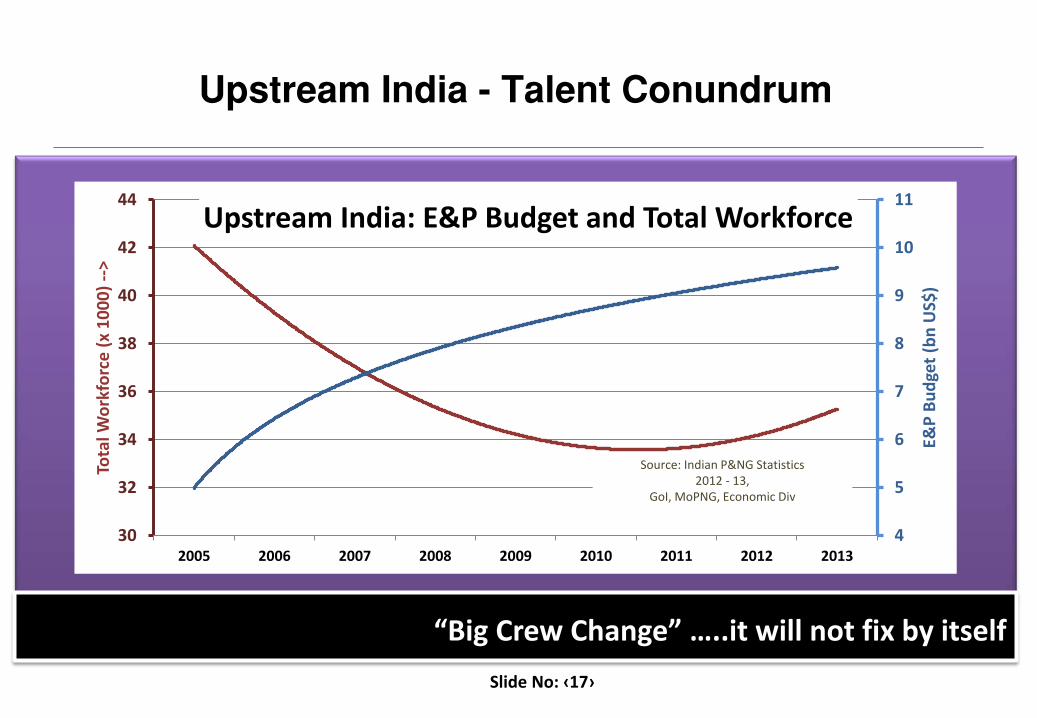

Upstream India: E&P Budget and Total Workforce

Source: Indian P&NG Statistics 2012 - 13,

GoI, MoPNG, Economic Div

“Big Crew Change” …..it will not fix by itself

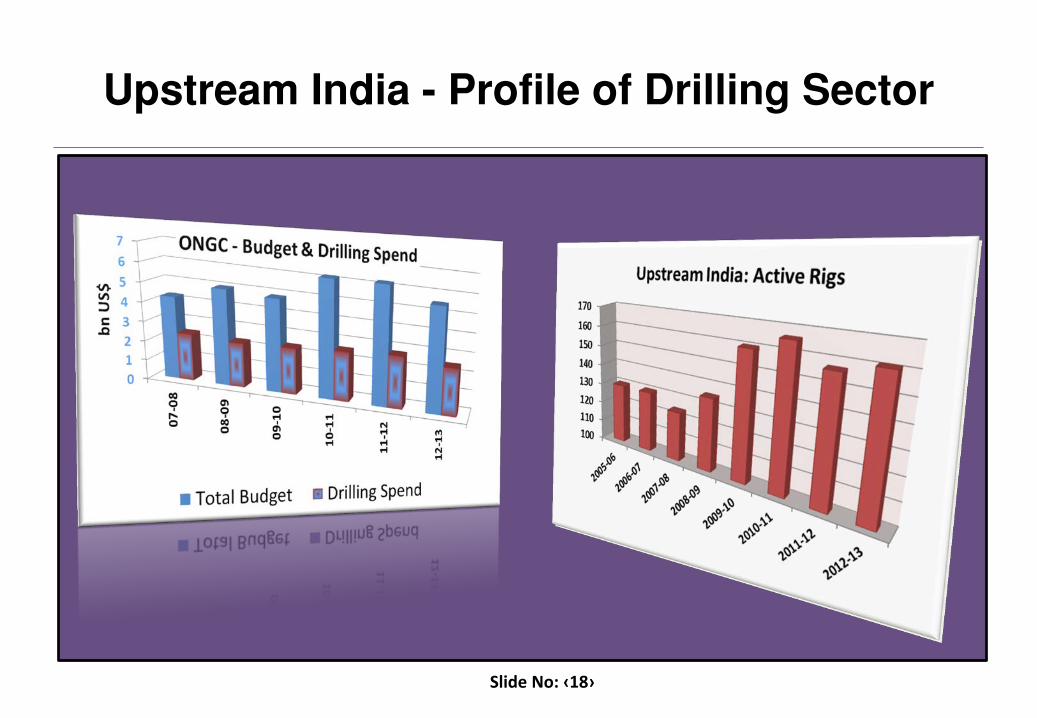

Slide No: ‹18›

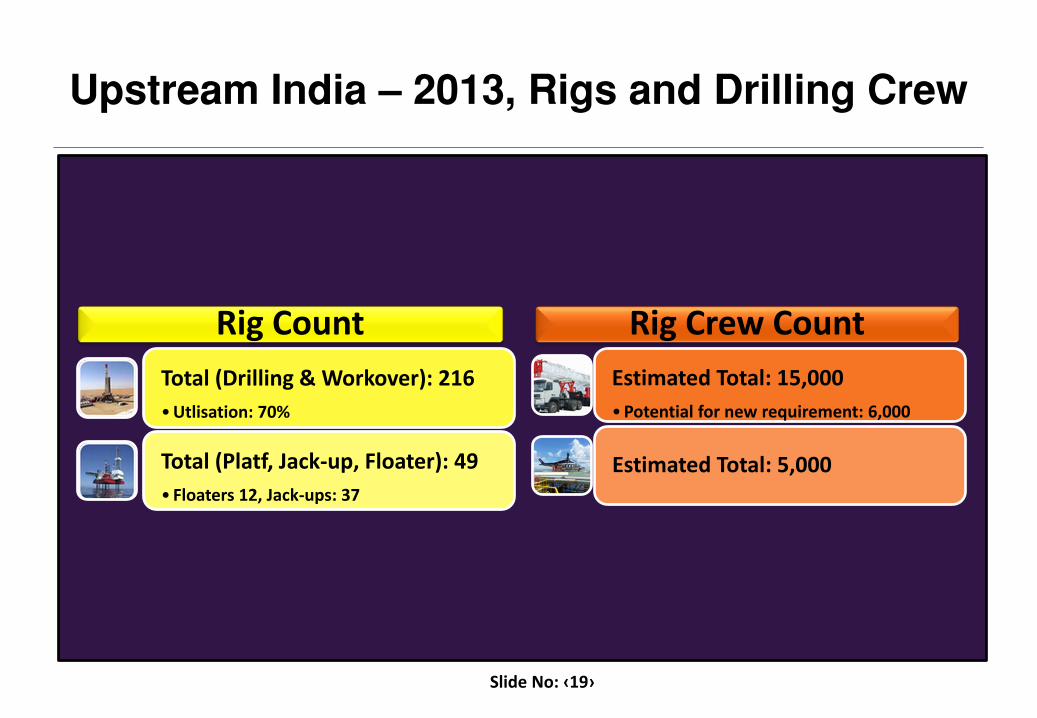

Slide No: ‹19›

Rig Count Total (Drilling & Workover): 216 •Utlisation: 70%

Total (Platf, Jack-up, Floater): 49 • Floaters 12, Jack-ups: 37

Rig Crew Count Estimated Total: 15,000 •Potential for new requirement: 6,000

Estimated Total: 5,000

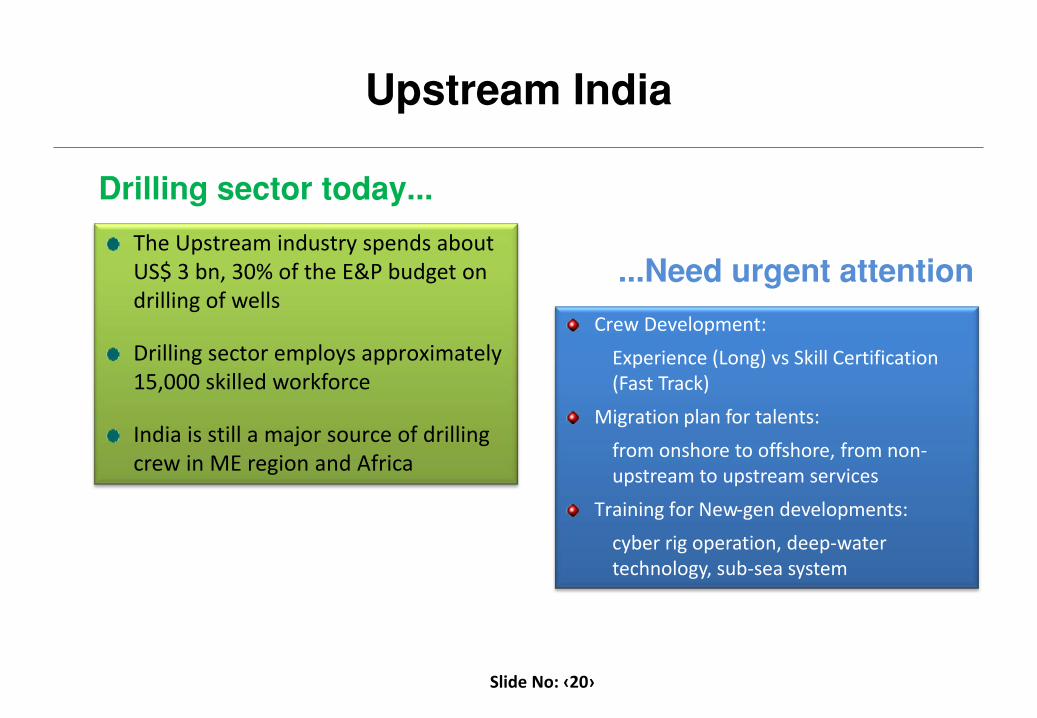

Slide No: ‹20›

The Upstream industry spends about US$ 3 bn, 30% of the E&P budget on drilling of wells

Drilling sector employs approximately 15,000 skilled workforce

India is still a major source of drilling crew in ME region and Africa

Crew Development: Experience (Long) vs Skill Certification (Fast Track)

Migration plan for talents: from onshore to offshore, from non-upstream to upstream services

Training for New-gen developments: cyber rig operation, deep-water technology, sub-sea system

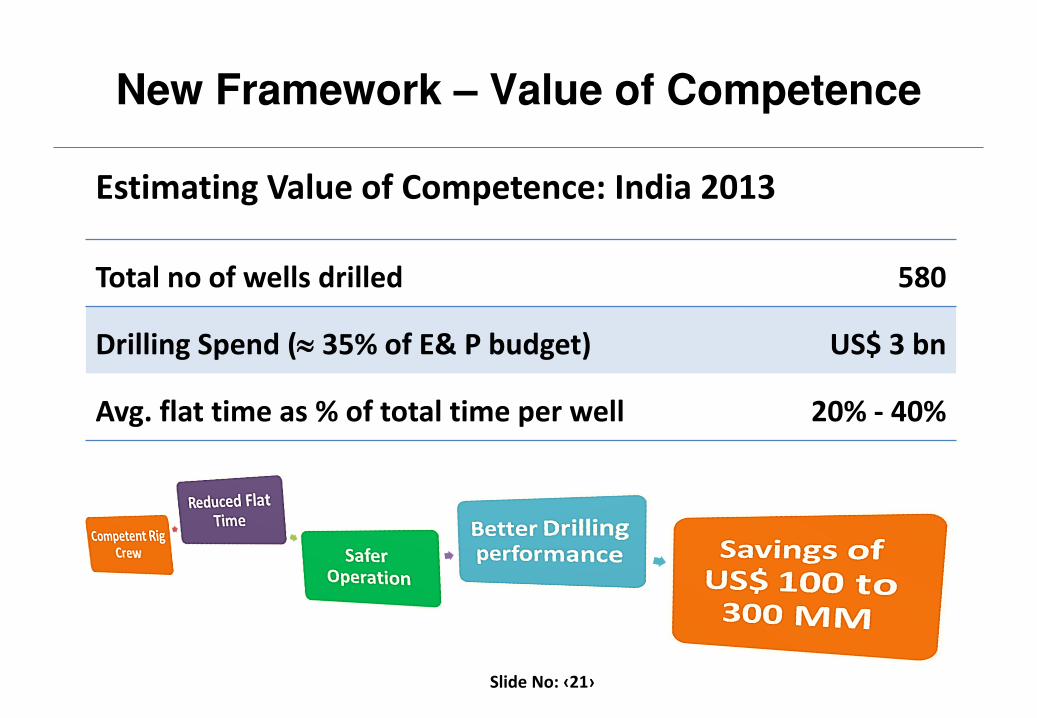

Estimating Value of Competence: India 2013

Slide No: ‹21›

Total no of wells drilled 580

Drilling Spend (≈ 35% of E& P budget) US$ 3 bn

Avg. flat time as % of total time per well 20% - 40%

Slide No: 22

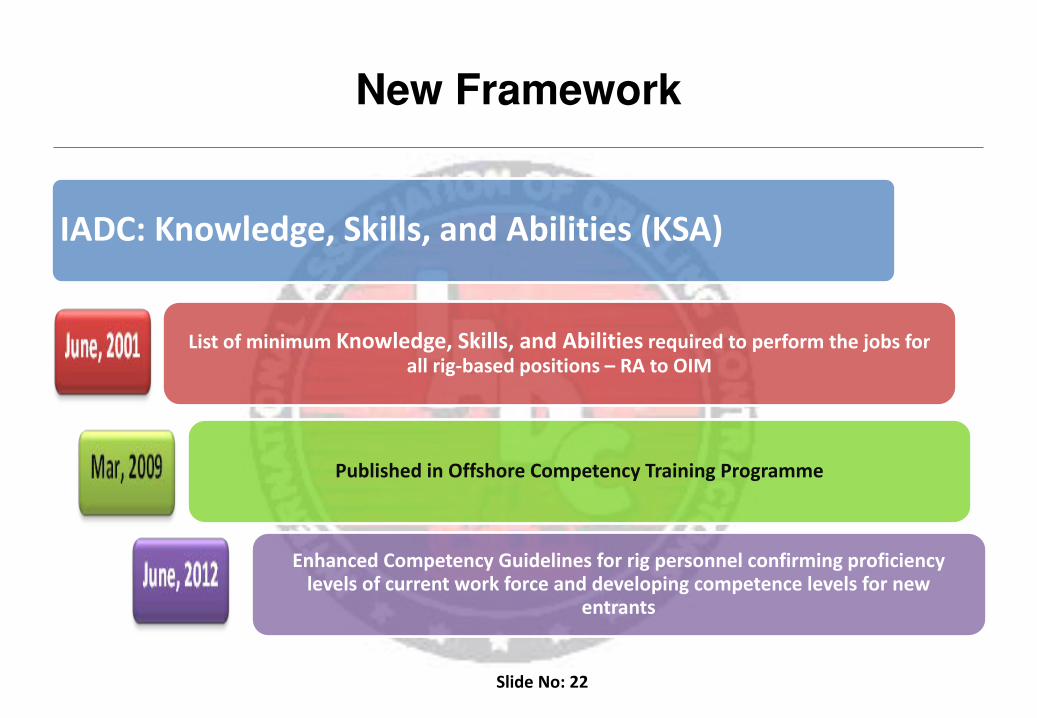

IADC: Knowledge, Skills, and Abilities (KSA)

List of minimum Knowledge, Skills, and Abilities required to perform the jobs for all rig-based positions – RA to OIM

Published in Offshore Competency Training Programme

Enhanced Competency Guidelines for rig personnel confirming proficiency levels of current work force and developing competence levels for new

entrants

Slide No: ‹23›

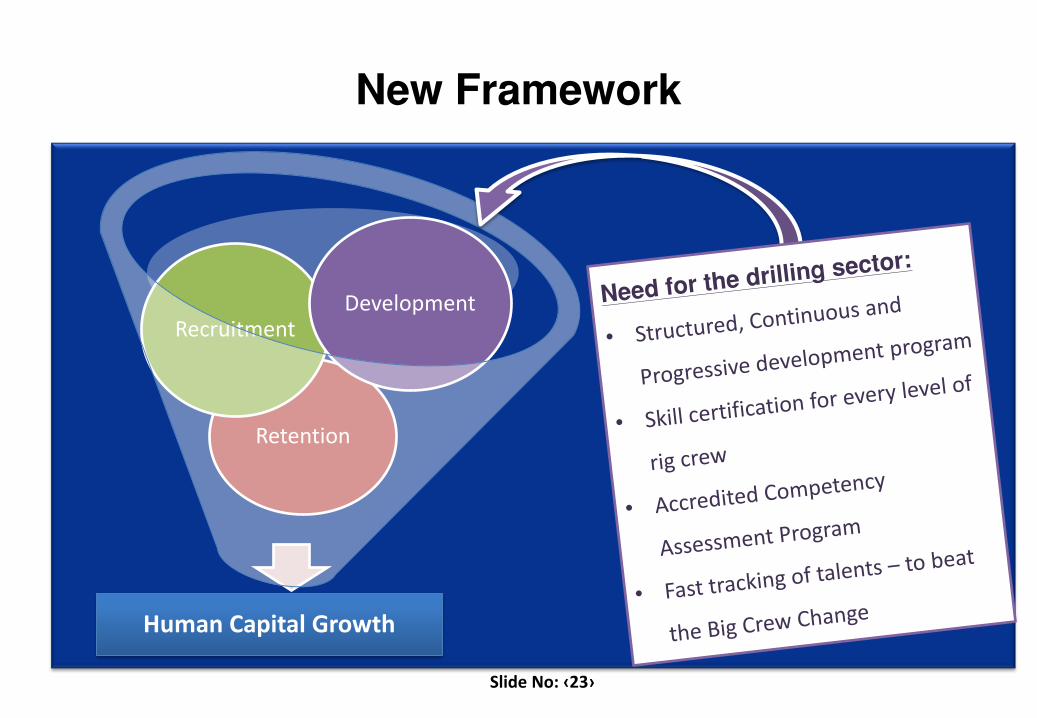

Human Capital Growth

Retention

Recruitment Development

Slide No: ‹24›

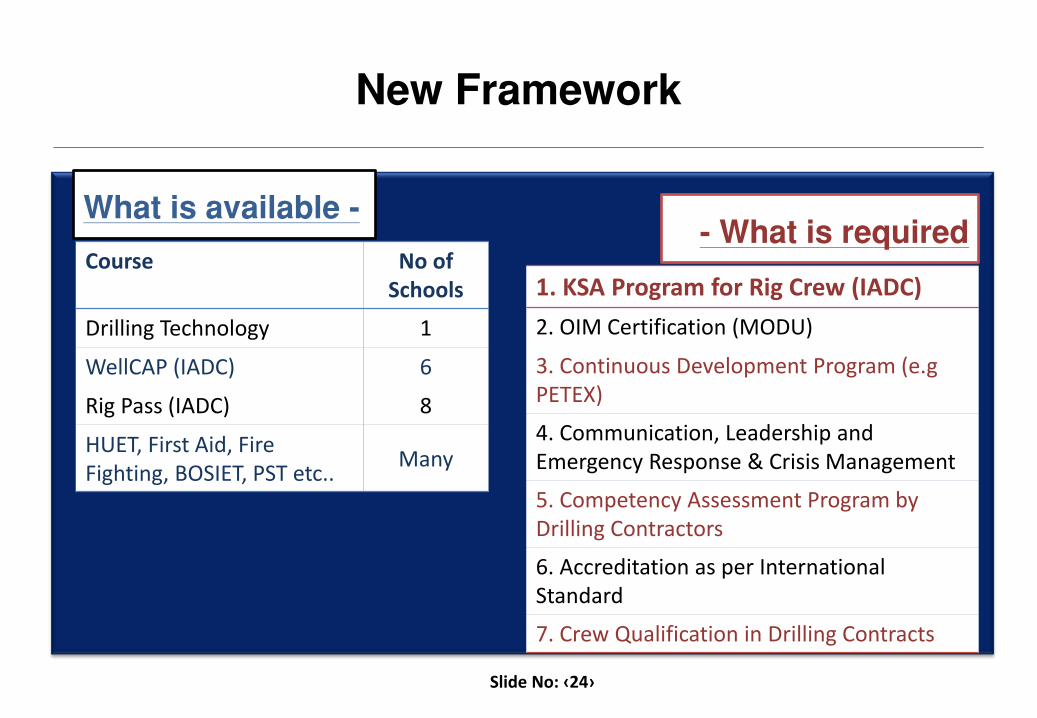

Course No of Schools

Drilling Technology 1

WellCAP (IADC) 6

Rig Pass (IADC) 8

HUET, First Aid, Fire Fighting, BOSIET, PST etc.. Many

1. KSA Program for Rig Crew (IADC) 2. OIM Certification (MODU)

3. Continuous Development Program (e.g PETEX)

4. Communication, Leadership and Emergency Response & Crisis Management

5. Competency Assessment Program by Drilling Contractors

6. Accreditation as per International Standard

7. Crew Qualification in Drilling Contracts

Slide No: ‹25›

E&P Operators

Contractors

IADC, SPE

Universities

Regulators

Though major stakeholders in

developing competent crew are

E&P companies and the drilling

contractors, the success of the

program can be achieved by

collaborative efforts to create

consensus, sustainability and value

chain

Slide No: ‹26›

Major Drilling Contractors from both Offshore and Onshore sector have started reviewing the new framework for the crew development

Year 2013 IADC SCAC: A new sub-committee to define the KSA for Drilling Crew;

Slide No: ‹27›

…Year 2014

•IADC, Operators and Contractors: Agree on the KSA or KSA-revised, progressive 1

•Contractors, Simulation Experts and Training Institutes: Create Infrastructure 2

•Contractors: Recruit, Train Crew as per KSA, Develop and Implement Competence Assessment Program (CAP) and Continuous Education Program (CEP)

3