Embed Size (px)

Citation preview

Global Investment Returns Yearbook

2017 - Slide Deck Elroy Dimson, Paul Marsh and Mike Staunton | London Business School Richard Kersley, Michael O'Sullivan | Credit Suisse

Credit Suisse Research Institute

February 2017

Credit Suisse Global Investment Returns Yearbook 2017

Credit Suisse is proud to publish the 2017

edition of the Global Investment Returns Yearbook.

The Yearbook is produced in conjunction with

Elroy Dimson, Paul Marsh and Mike Staunton, recognized as leading authorities

on the analysis of the long-run performance and trends of stocks, bonds, Treasury bills (cash), inflation and currencies.

The Yearbook provides an analysis of investment returns stretching back 117 years,

spanning all five asset categories in 23 countries.

As well as the typical long term perspective to

current events it brings, this year’s edition provides fresh analysis of factor investing

strategies. Are smart beta strategies…smart?

Richard Kersley Head Global Thematic Research, Global Markets, Credit Suisse +44 20 7888 0313 [email protected]

Michael O'Sullivan Chief Investment Officer, International Wealth Management, Credit Suisse +41 44 332 81 73 michael.o'[email protected]

2

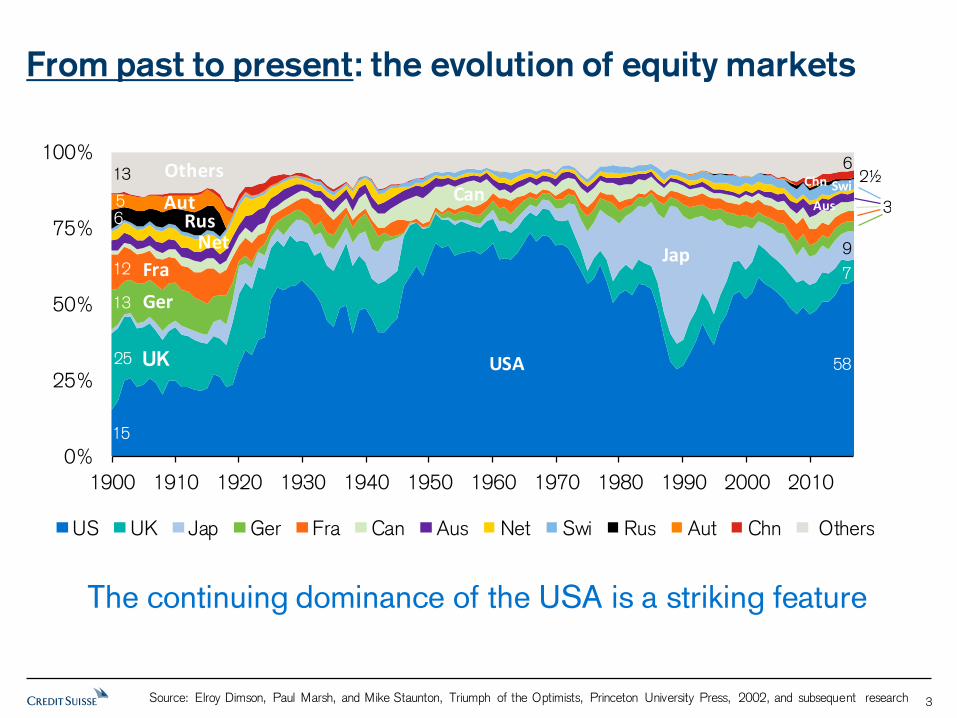

From past to present: the evolution of equity markets

0%

25%

50%

75%

100%

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

US UK Jap Ger Fra Can Aus Net Swi Rus Aut Chn Others

58

7

9

3

2½6

15

13

56

12

13

25 UK

AutRus

Ger

Fra

USA

Jap

Can

Net

OthersSwi

Aus

Chn

The continuing dominance of the USA is a striking feature

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 3

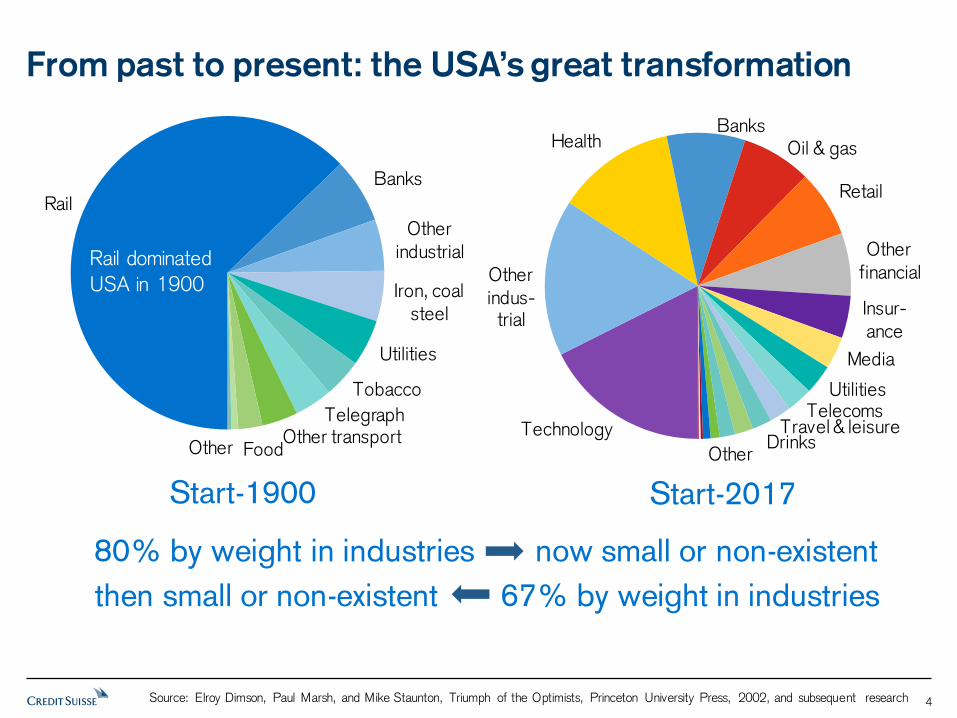

From past to present: the USA’s great transformation

Rail

Banks

Other

industrial

Iron, coalsteel

Utilities

Tobacco

TelegraphOther transport

FoodOther

Start-1900 Start-2017

80% by weight in industries now small or non-existent

then small or non-existent 67% by weight in industries

Technology

Other indus-trial

HealthBanks

Oil & gas

Retail

Other

financial

Insur-

ance

Media

UtilitiesTelecoms

Travel & leisureDrinks

Other

Rail dominated

USA in 1900

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 4

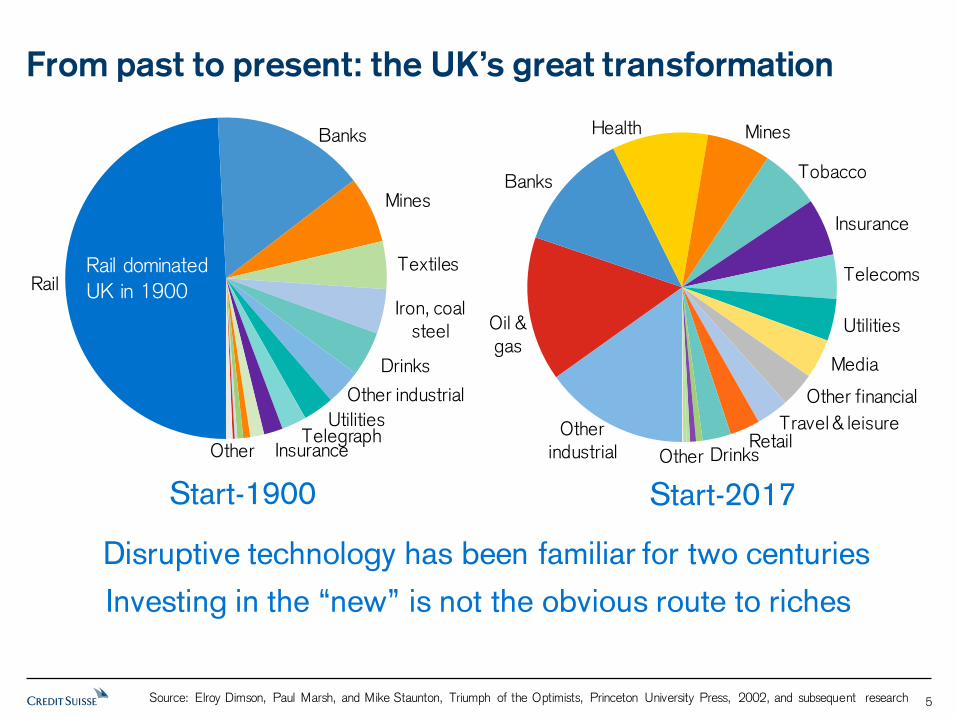

From past to present: the UK’s great transformation

Start-1900 Start-2017

Disruptive technology has been familiar for two centuries

Investing in the “new” is not the obvious route to riches

Rail

Banks

Mines

Textiles

Iron, coal

steel

Drinks

Other industrial

UtilitiesTelegraph

InsuranceOtherOther

industrial

Oil &

gas

Banks

Health Mines

Tobacco

Insurance

Telecoms

Utilities

Media

Other financial

Travel & leisureRetail

DrinksOther

Rail dominated

UK in 1900

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 5

The past: Real returns and dividends, 1900–2016

We should focus on real return. Real return is largely dividends.

1,402

11.9 9.8

2.6

0

1

10

100

1,000

10,000

1900 10 20 30 40 50 60 70 80 90 2000 10

Equities: return 6.4% p.a. Equities: capital gain 2.1% p.a.

Bonds 2.0% p.a. Bills 0.8% p.a.

0.1

Reinv-

ested

divi-

dends

513

8.1

3.3

0

1

10

100

1,000

1900 10 20 30 40 50 60 70 80 90 2000 10

Equities: return 5.5% p.a. Equities: capital gain 0.8% p.a.

Bonds 1.8% p.a. Bills 1.0% p.a.

0.1

2.7

Reinv-

ested

divi-

dends

United Kingdom

United States

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 6

Long-run asset returns for all countries, 1900–2016

Prospectively, the world equity premium (versus bills) is 3–3½%

4.3

5.1

6.4

-6

-4

-2

0

2

4

6

Aut Ita Bel Fra Ger Prt Spa Jap Eur Nor WxU Ire Swi Net Wld Den Fin UK Can Swe NZ US Aus SAf

Equities Bonds Bills

Annualized real return (%)

Historical equity risk

premium vs. bonds = 3.2%

Historical equity risk

premium vs. bills = 4.2%

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 7

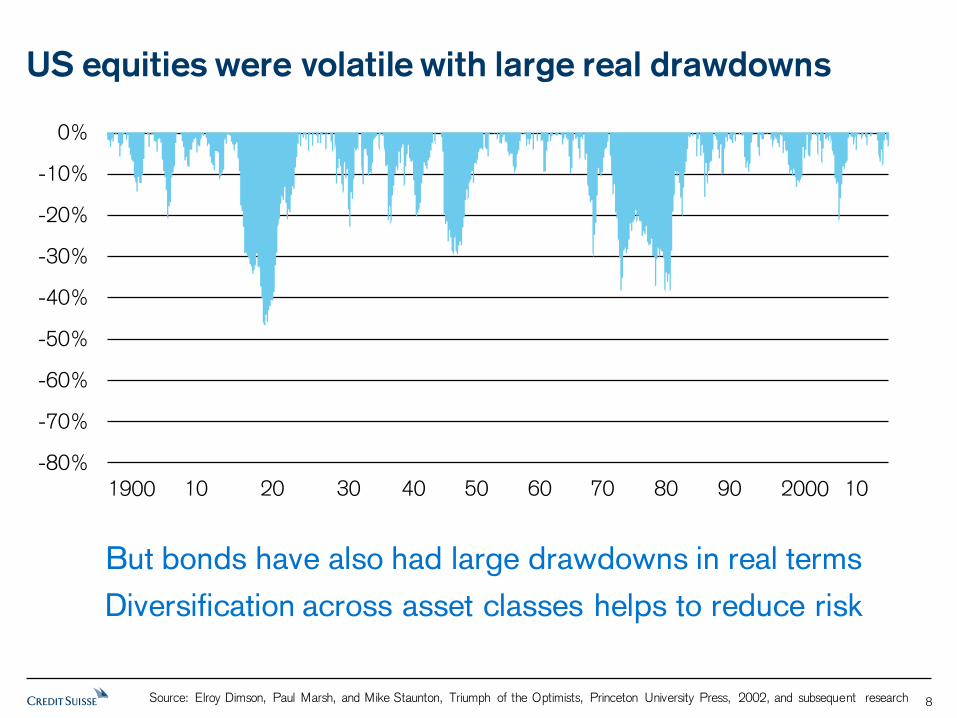

US equities were volatile with large real drawdowns

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

But bonds have also had large drawdowns in real terms

Diversification across asset classes helps to reduce risk

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

Bonds

Equities-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 8

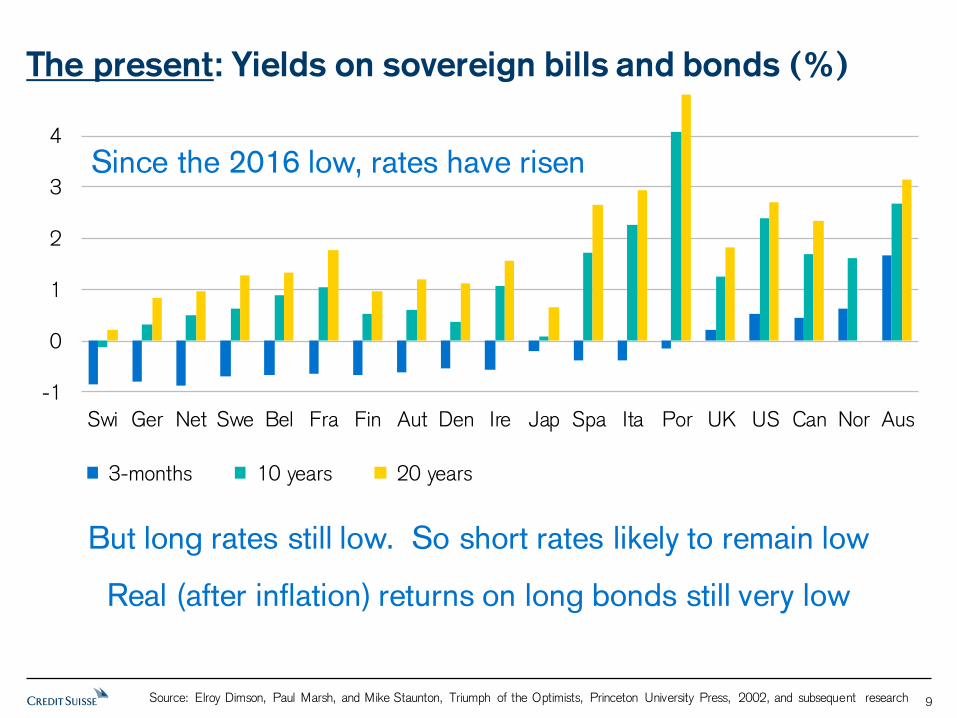

But long rates still low. So short rates likely to remain low

Real (after inflation) returns on long bonds still very low

-1

0

1

2

3

4

Swi Ger Net Swe Bel Fra Fin Aut Den Ire Spa Ita Jap Por UK US Can Nor Aus

3-months 10 years 20 years

In 2016 rates hit all-time low

-1

0

1

2

3

4

Swi Ger Net Swe Bel Fra Fin Aut Den Ire Jap Spa Ita Por UK US Can Nor Aus

3-months 10 years 20 years

The present: Yields on sovereign bills and bonds (%)

Since the 2016 low, rates have risen

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 9

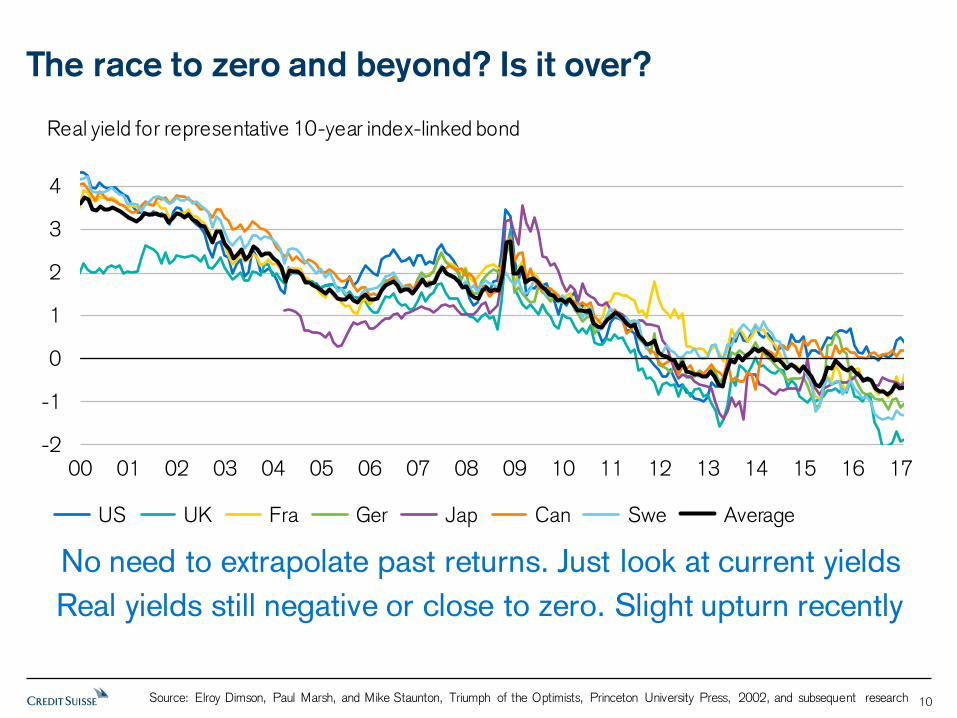

The race to zero and beyond? Is it over?

-2

-1

0

1

2

3

4

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

US UK Fra Ger Jap Can Swe Average

Real yield for representative 10-year index-linked bond

No need to extrapolate past returns. Just look at current yields

Real yields still negative or close to zero. Slight upturn recently

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 10

Real interest rates impact subsequent real equity and bond returns

Low real interest rates means a low return world

- 5.4

1.4

4.2 5.2 5.2

7.6 9.0

11.0

- 10.0

- 3.4

2.2

4.0

5.6

9.8

- 11

- 2.2

0.1

1.4

2.8

4.6

9.4

-15

-10

-5

0

5

10

Low 5% Next 15% Next 15% Next 15% Next 15% Next 15% Next 15% Top 5%

Equities next 5 years % p.a. Bonds next 5 years % p.a. Real interest rate boundary %

Percentiles of real interest rates across 2,317 country - years

Real rate of return (%)

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 11

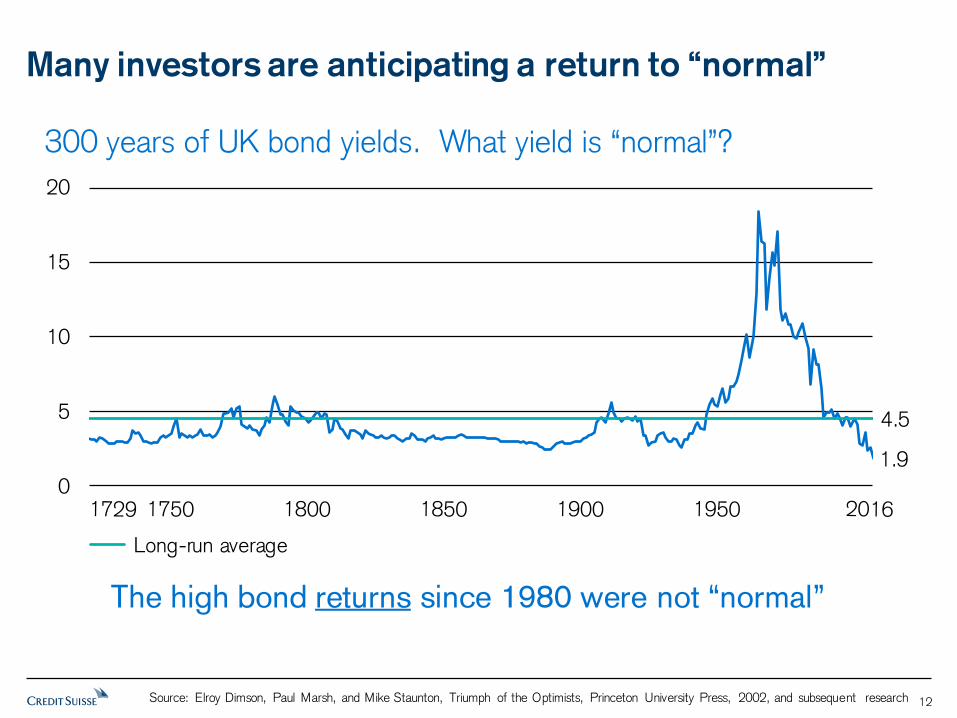

Many investors are anticipating a return to “normal”

1.9

4.5

0

5

10

15

20

Long-run average

The high bond returns since 1980 were not “normal”

300 years of UK bond yields. What yield is “normal”?

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 12

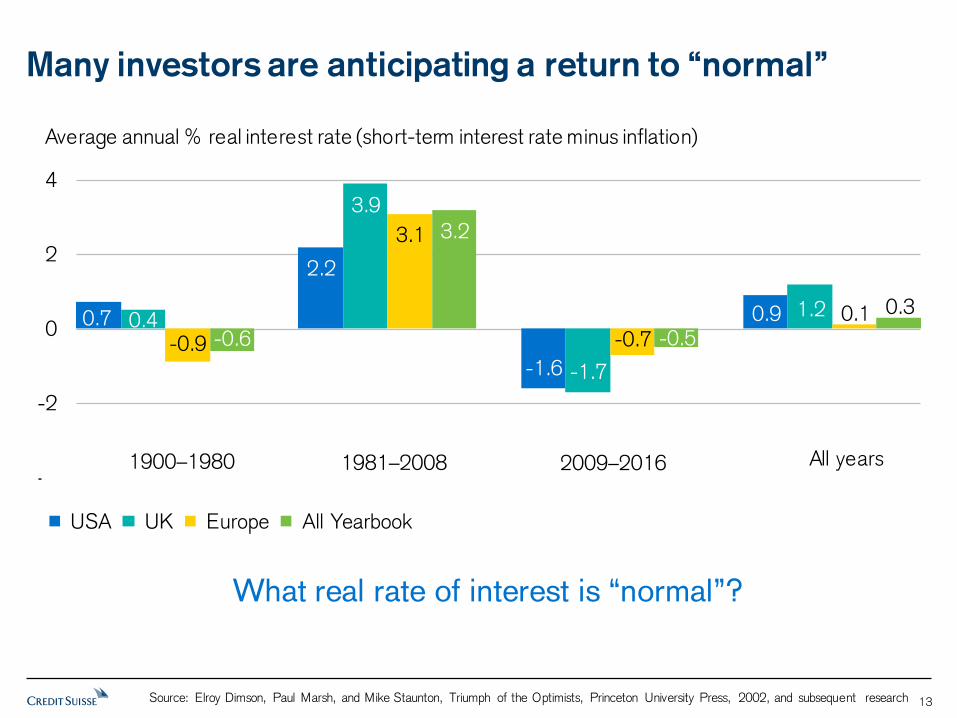

Many investors are anticipating a return to “normal”

What real rate of interest is “normal”?

0.7

2.2

-1.6

0.90.4

3.9

-1.7

1.2

-0.9

3.1

-0.70.1

-0.6

3.2

-0.5

0.3

-4

-2

0

2

4

USA UK Europe All Yearbook

Average annual % real interest rate (short-term interest rate minus inflation)

1900–1980 1981–2008 2009–2016 All years

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 13

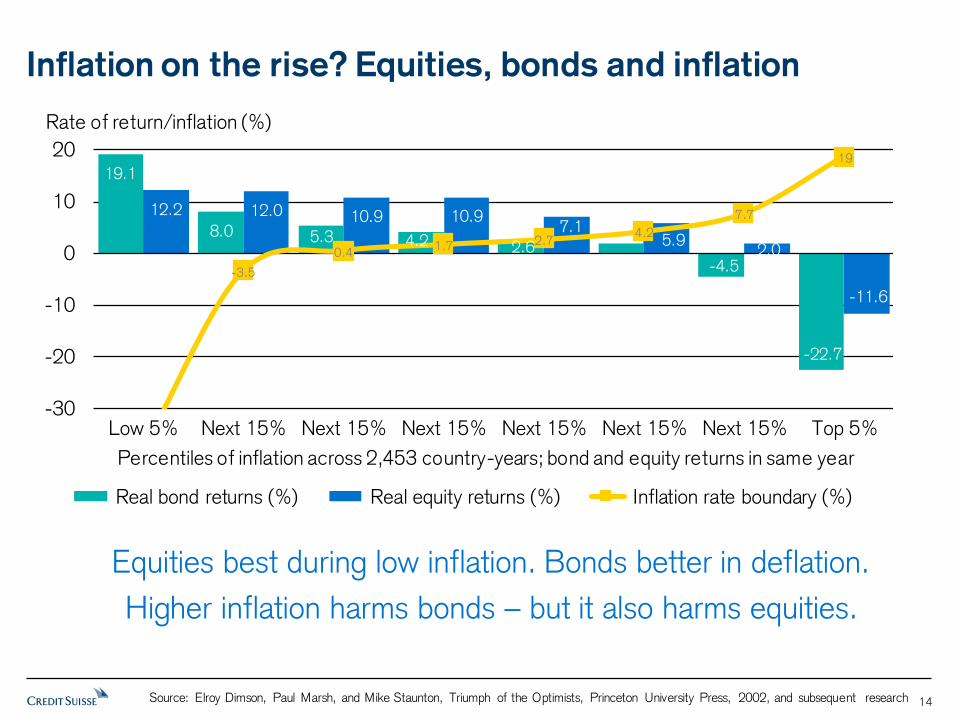

Inflation on the rise? Equities, bonds and inflation

Equities best during low inflation. Bonds better in deflation.

Higher inflation harms bonds – but it also harms equities.

19.1

8.0 5.3 4.2 2.6-4.5

-22.7

12.2 12.0 10.9 10.97.1

5.92.0

-11.6

-3.5

0.41.7 2.7

4.2

7.7

19

-30

-20

-10

0

10

20

Low 5% Next 15% Next 15% Next 15% Next 15% Next 15% Next 15% Top 5%

Real bond returns (%) Real equity returns (%) Inflation rate boundary (%)

Percentiles of inflation across 2,453 country-years; bond and equity returns in same year

Rate of return/inflation (%)

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 14

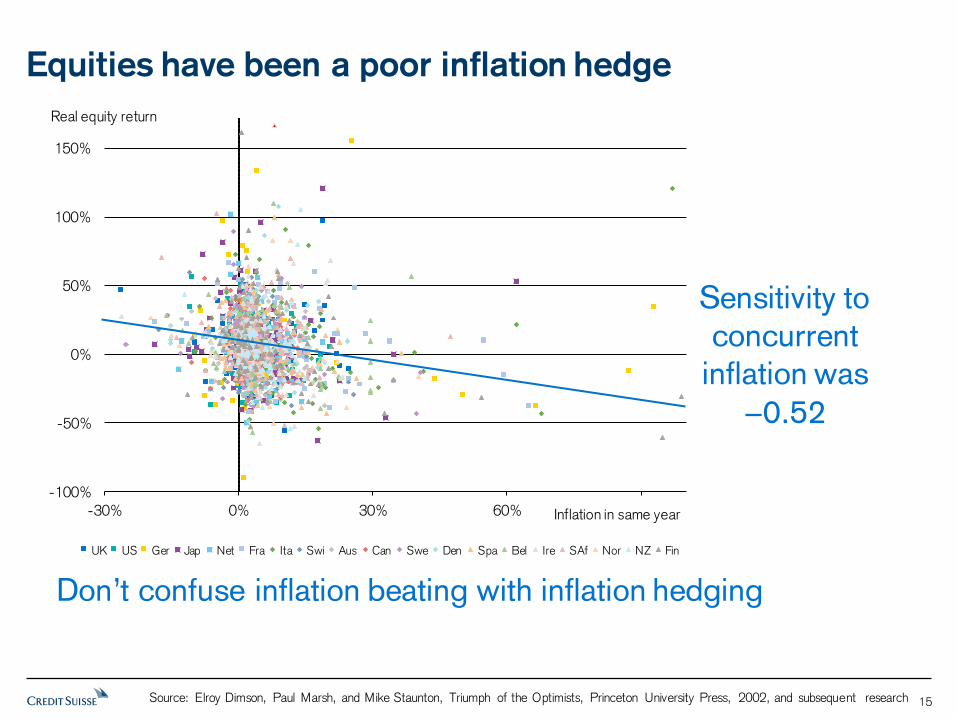

Equities have been a poor inflation hedge

Sensitivity to

concurrent

inflation was

−0.52

Don’t confuse inflation beating with inflation hedging

-100%

-50%

0%

50%

100%

150%

-30% 0% 30% 60% 90%

UK US Ger Jap Net Fra Ita Swi Aus Can Swe Den Spa Bel Ire SAf Nor NZ Fin

Inflation in same year

Real equity return

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 15

The future: What equity premium can we expect?

We estimate the long-run equity premium vs bills to be 3–3½%

5.1

4.1

0.5

0.5

3.3

0.8

0

1

2

3

4

5

Historical equity

real return

Real dividend

growth

Change in

P/D ratio

Average

dividend yield

Treasury bill

return

Expected equity

risk premium

Annualised (% p.a.)

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 16

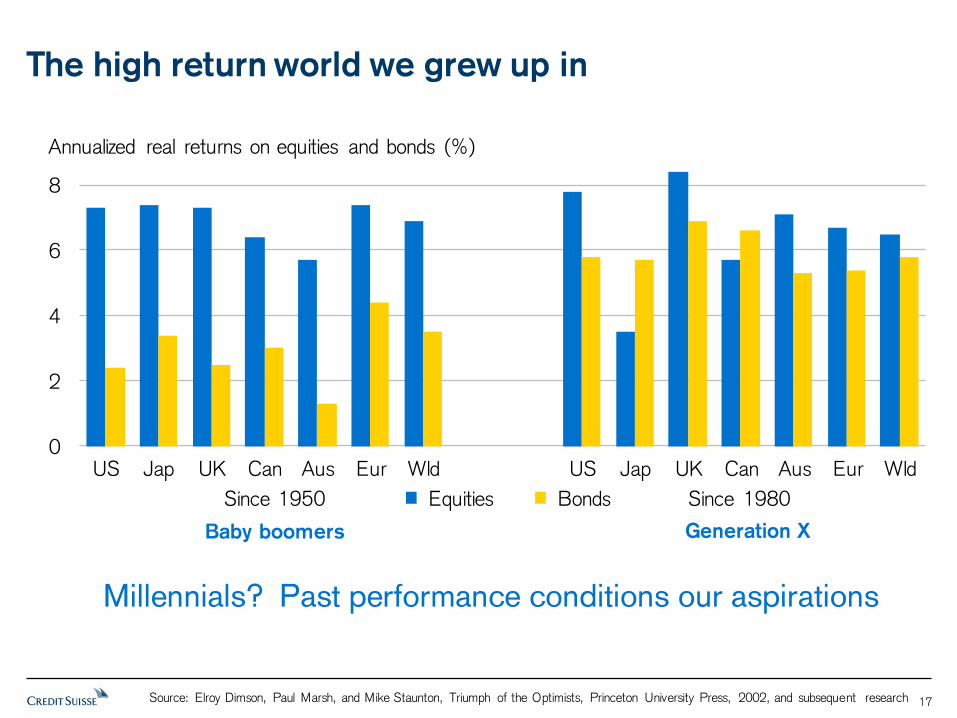

The high return world we grew up in

Millennials? Past performance conditions our aspirations

0

2

4

6

8

US Jap UK Can Aus Eur Wld US Jap UK Can Aus Eur Wld

Since 1950 Since 1980 Equities Bonds

Annualized real returns on equities and bonds (%)

Baby boomers Generation X

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 17

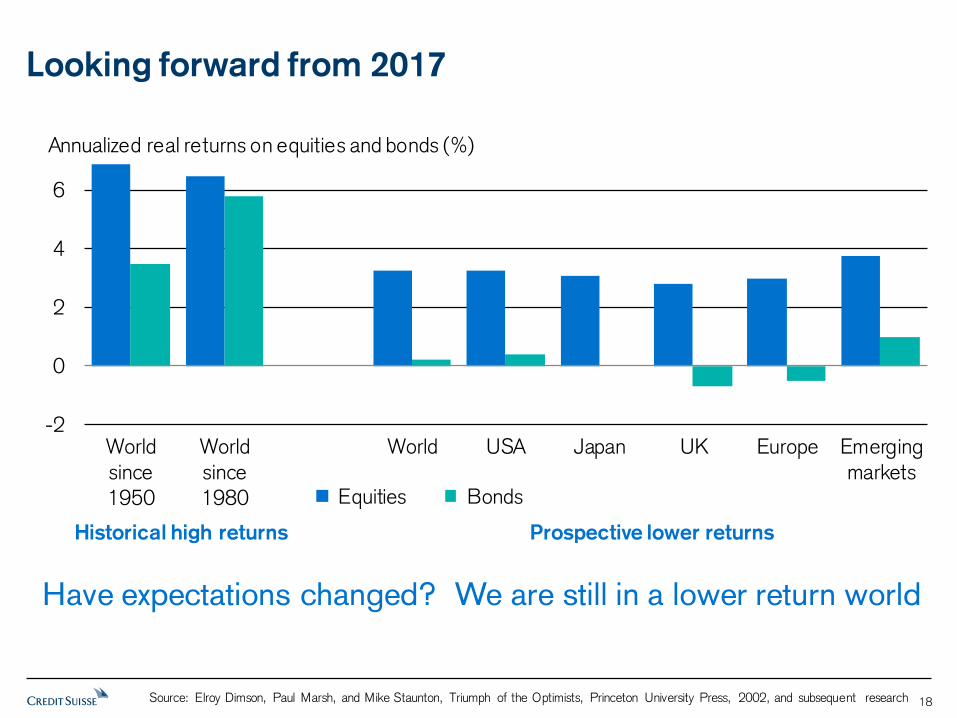

Looking forward from 2017

-2

0

2

4

6

World

since

1950

World

since

1980

World USA Japan UK Europe Emerging

markets

Historical high returns Prospective lower returns

Equities Bonds

Annualized real returns on equities and bonds (%)

We are still in a lower return world Have expectations changed?

-2

0

2

4

6

World

since

1950

World

since

1980

World USA Japan UK Europe Emerging

markets

Historical high returns Prospective lower returns

Equities Bonds

Annualized real returns on equities and bonds (%)

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 18

Real interest rates are low, and bond yields are low

– expected returns on all assets are lower than past returns

– modest rises in inflation are unlikely to impact real returns

Long-run equity premium (vs bills) is around 3–3½%

– lower than the historical average

– equities will stay volatile, but diversification lowers risk

What to do about the low-return world?

– the Yearbook provides a long-term perspective

– the current ‘vogue’ is to seek returns from smart beta…

The future

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 19

Investors ditching active management (USA, 2007–16)

Sources: Investment Company Institute, Simfund, Credit Suisse

Cumulati

ve asset

flow

(USD bn)

20

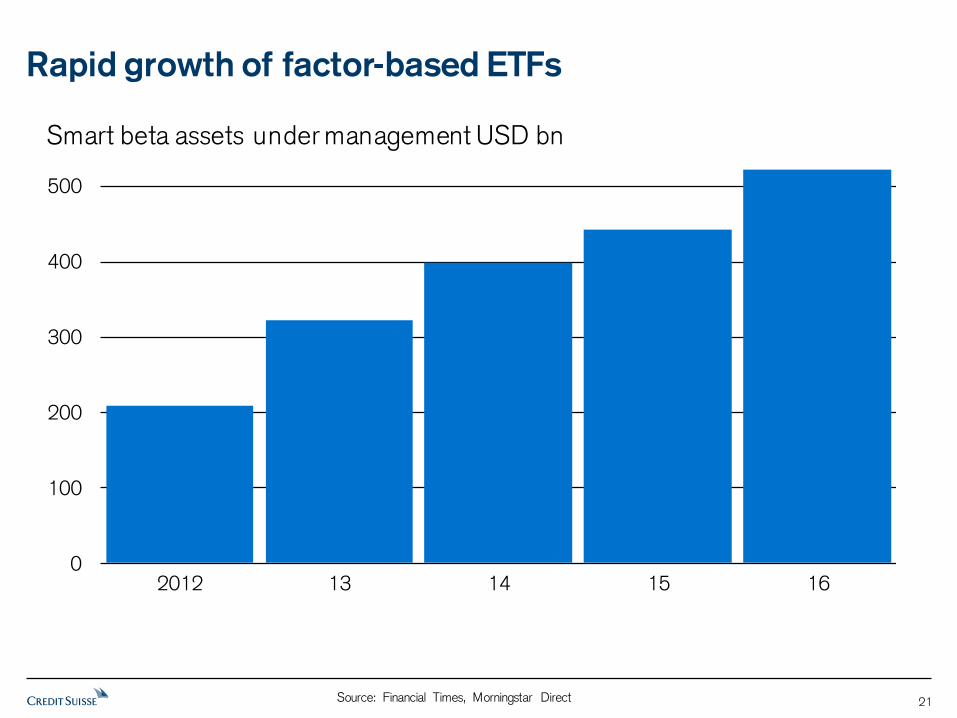

Rapid growth of factor-based ETFs

Source: Financial Times, Morningstar Direct

0

100

200

300

400

500

2012 13 14 15 16

Smart beta assets under management USD bn

21

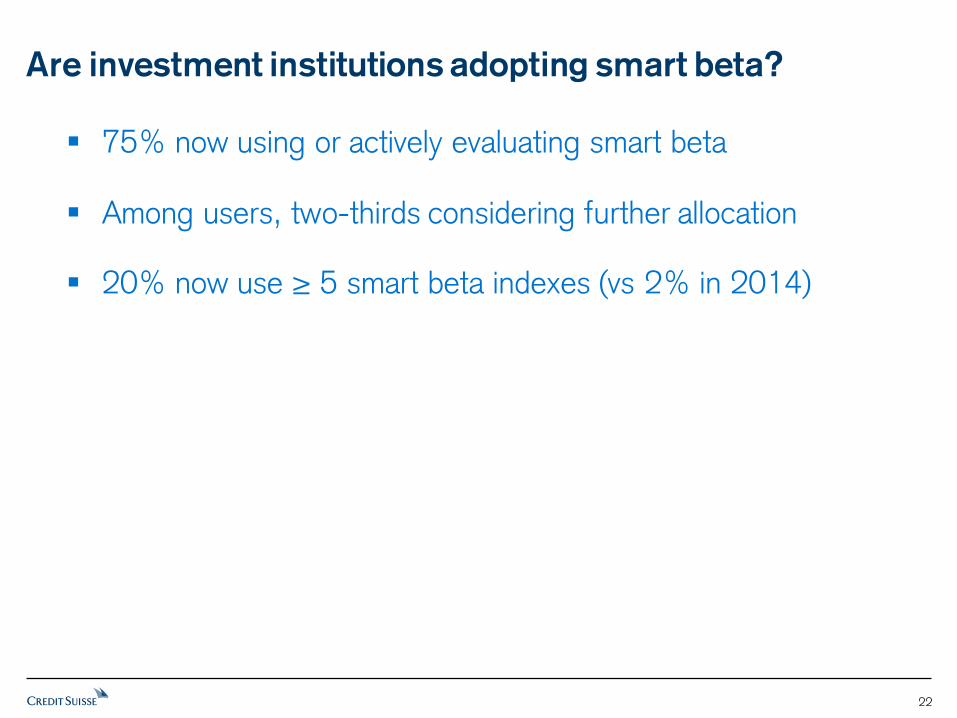

Are investment institutions adopting smart beta?

75% now using or actively evaluating smart beta

Among users, two-thirds considering further allocation

20% now use ≥ 5 smart beta indexes (vs 2% in 2014)

22

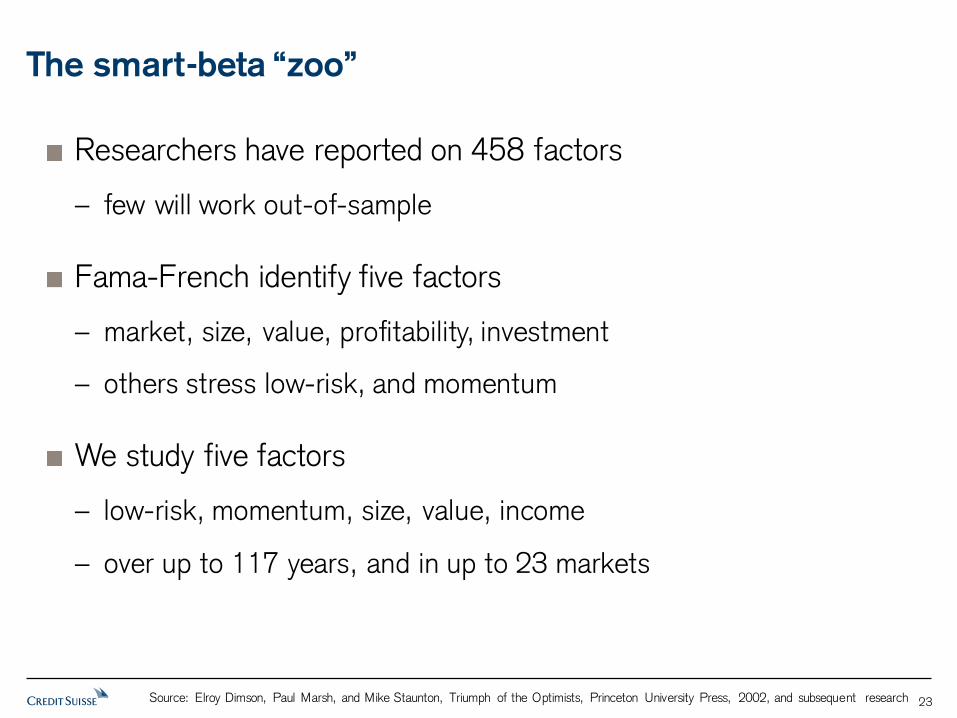

The smart-beta “zoo”

Researchers have reported on 458 factors

– few will work out-of-sample

Fama-French identify five factors

– market, size, value, profitability, investment

– others stress low-risk, and momentum

We study five factors

– low-risk, momentum, size, value, income

– over up to 117 years, and in up to 23 markets

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 23

Low-risk investing

Classic strategy (published 1972)

– low beta portfolio gives superior risk-adjusted return

– now labelled as BAB (Bet Against Beta)

Recent approach uses idiosyncratic volatility

– low-volatility portfolio gives superior return…

– … compared to high-volatility portfolio

Many variants of these “low-vol” strategies

– an approach that has become popular since the GFC

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 24

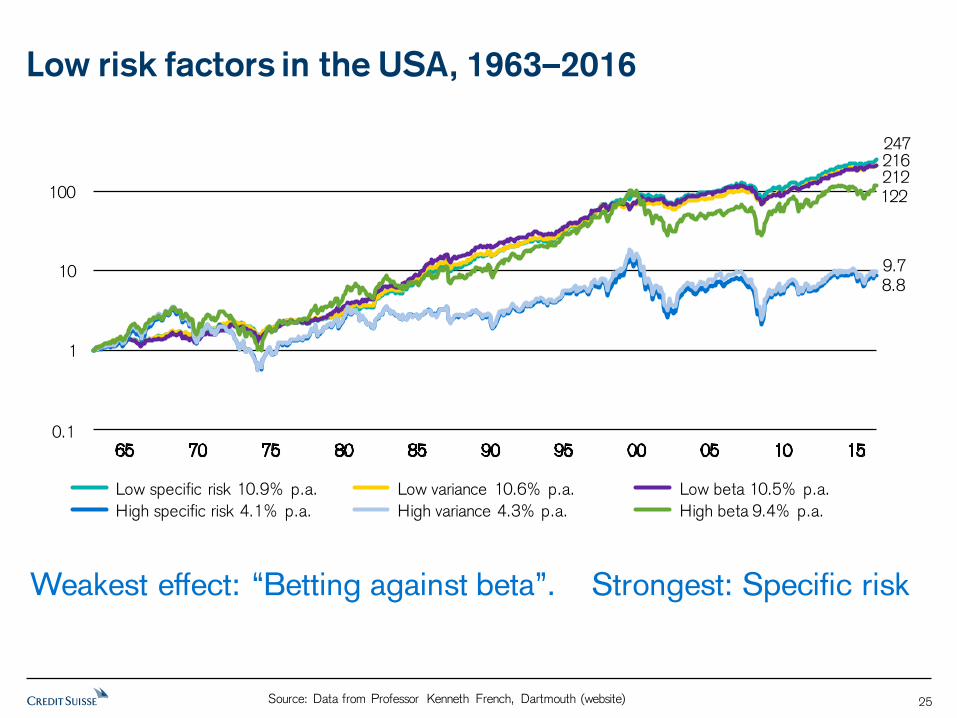

Low risk factors in the USA, 1963–2016

247

212

8.8 9.7

122

0

1

10

100

1,000

Low specific risk 10.9% p.a. Low variance 10.6% p.a. Low beta 10.5% p.a.

High specific risk 4.1% p.a. High variance 4.3% p.a. High beta 9.4% p.a.

0.1

216

Weakest effect: “Betting against beta”

Source: Data from Professor Kenneth French, Dartmouth (website)

Weakest effect: “Betting against beta”. Strongest: Specific risk

25

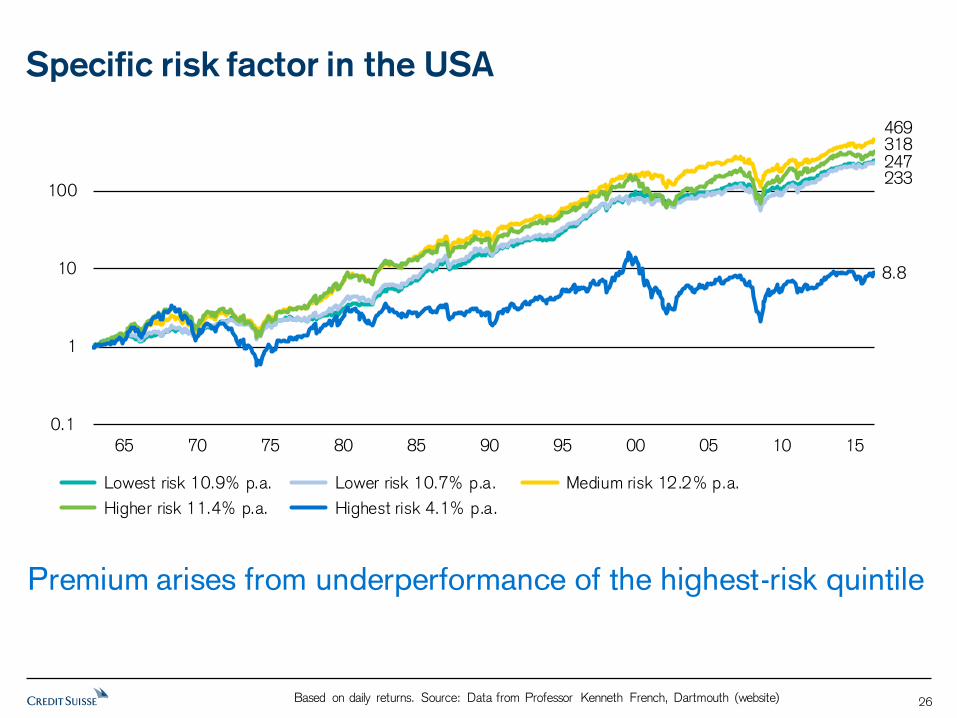

Specific risk factor in the USA

247233

469318

8.8

0

1

10

100

1,000

Lowest risk 10.9% p.a. Lower risk 10.7% p.a. Medium risk 12.2% p.a.

Higher risk 11.4% p.a. Highest risk 4.1% p.a.

0.1

Premium arises from underperformance of the highest-risk quintile

Based on daily returns. Source: Data from Professor Kenneth French, Dartmouth (website) 26

Specific risk factor in the UK

35.924.9

3.9

0

1

10

100

Lowest risk 11.6% p.a. Medium risk 10.3% p.a. Highest risk 4.2% p.a.

0.1

Same methodology using daily data: UK results similar to USA

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 27

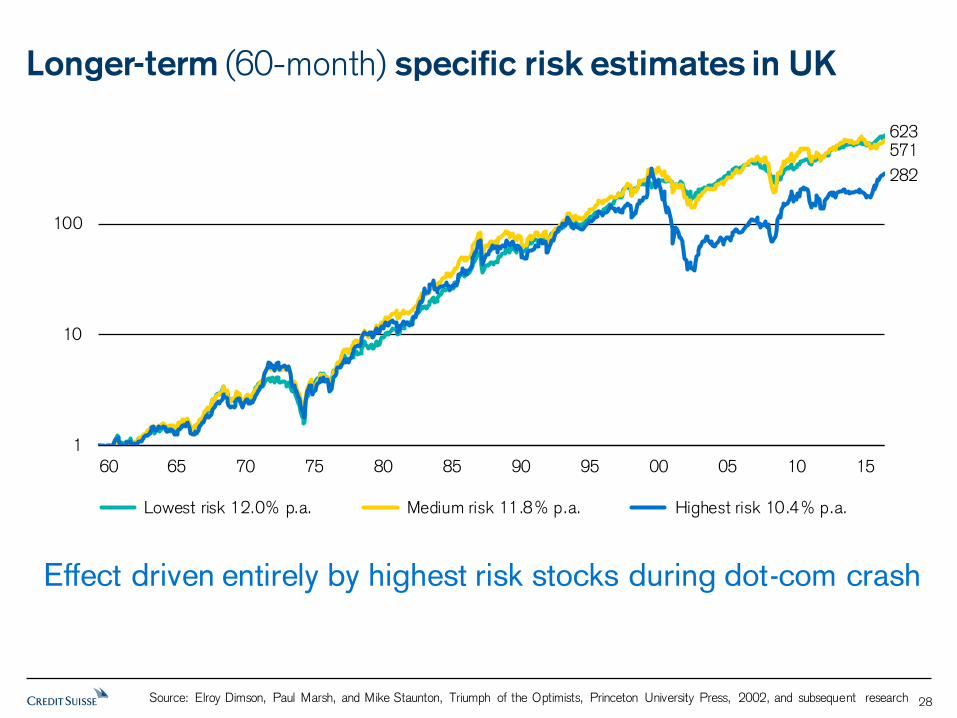

Longer-term (60-month) specific risk estimates in UK

Effect driven entirely by highest risk stocks during dot-com crash

623571

282

1

10

100

1,000

Lowest risk 12.0% p.a. Medium risk 11.8% p.a. Highest risk 10.4% p.a.

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 28

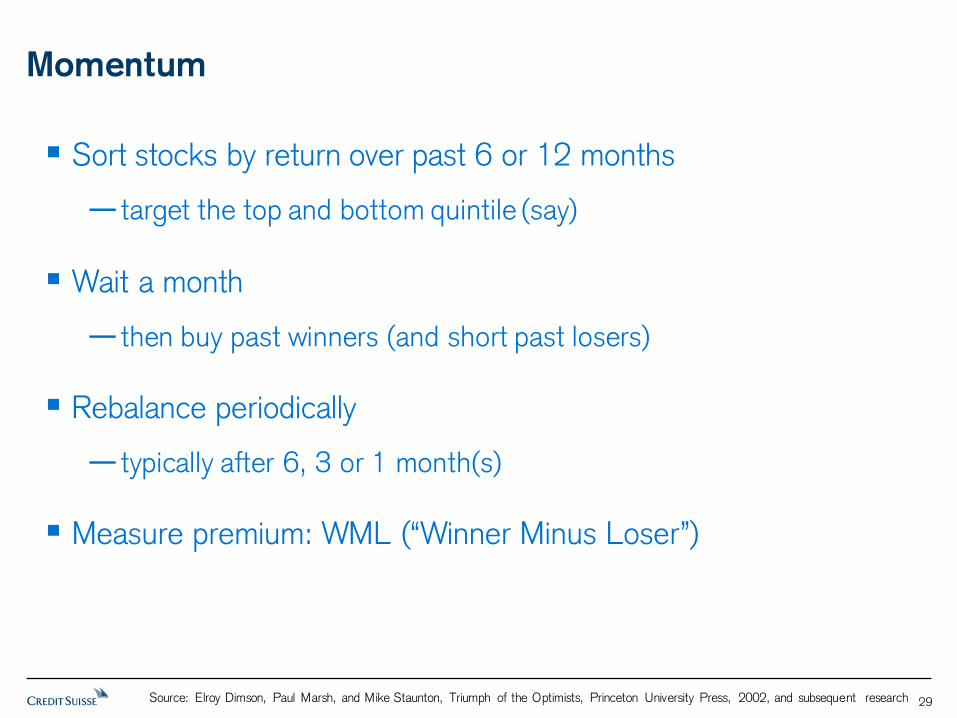

Momentum

Sort stocks by return over past 6 or 12 months

—target the top and bottom quintile (say)

Wait a month

—then buy past winners (and short past losers)

Rebalance periodically

—typically after 6, 3 or 1 month(s)

Measure premium: WML (“Winner Minus Loser”)

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 29

The momentum premium, 1900*–2016

United States† United Kingdom‡

* from 1926 in the US † Based on a 6/1/6 momentum strategy ‡ Based on a 12/1/1 momentum strategy

Large long-run, pre-cost returns; but volatile with high turnover

2,131,993

3,634

0

1

10

100

1,000

10,000

100,000

1,000,000

10,000,000

Winner 17.5% per year Loser 9.5% per year

Cumulative difference

between winners and

losers 7.4%

0.1

5,043,966

61

0

1

10

100

1,000

10,000

100,000

1,000,000

10,000,000

1900 10 20 30 40 50 60 70 80 90 2000 10

Winner 14.1% per year Loser 3.6% per year

Cumulative difference

between winners and

losers 10.4%0.1

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 30

Unusually, the factor premium was larger after the original study

.71.79

-0.5

0.0

0.5

1.0

1.5

Jap Chi Rus Spa US Can Aus Swe Prt Fra Aut Avg Ger Neth Ita Bel Swi Fin Ire UK Nor Den NZ SAf

Griffin, Ji & Martin: to end-2000 Full period to end-2016 (updated by Dimson, Marsh & Staunton)

Winner minus loser returns, % per month

Momentum returns around the world

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 31

Other factors: the size premium, 1926*–2015

United States

The smallest firms have performed the best, but not consistently

* from 1955 in the UK

Sources: US CRSP capitalization deciles are from Morningstar; UK Small and Mid-caps are Numis indices

United Kingdom

33,879

4,690

53,263

0

1

10

100

1,000

10,000

100,000

26 30 35 40 45 50 55 60 65 70 75 80 85 90 95 00 05 10 15

Micro-caps 12.7% per year Small-caps 12.1% per year

Larger-caps 9.7% per year

0.1

27,256

6,861

3,220

1,087

1

10

100

1,000

10,000

100,000

1955 60 65 70 75 80 85 90 95 2000 05 10 15

Micro-caps 17.9% per year Small-caps 15.3% per year

Mid-caps 13.9% per year Large-caps 12.0% per year

32

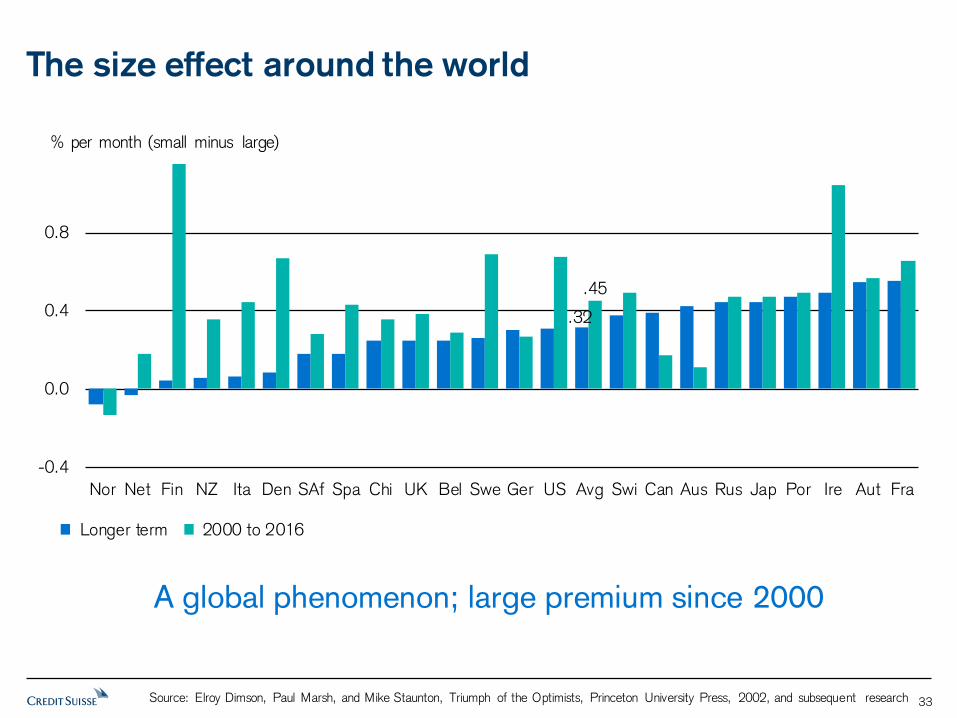

The size effect around the world

.32

.45

-0.4

0.0

0.4

0.8

Nor Net Fin NZ Ita Den SAf Spa Chi UK Bel Swe Ger US Avg Swi Can Aus Rus Jap Por Ire Aut Fra

Longer term 2000 to 2016

% per month (small minus large)

A global phenomenon; large premium since 2000

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 33

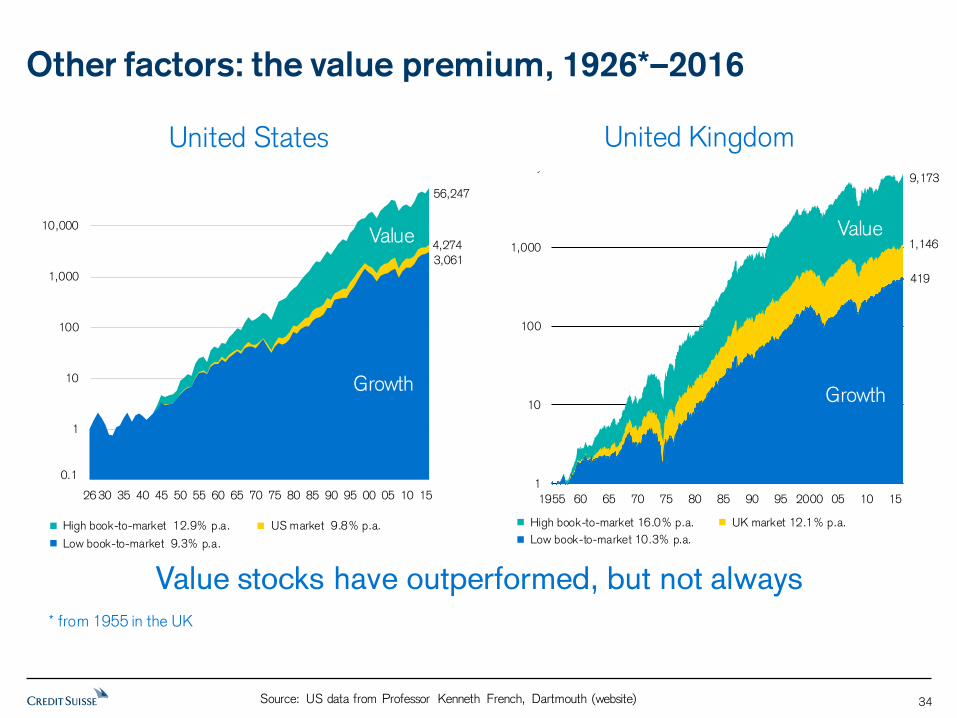

Other factors: the value premium, 1926*–2016

* from 1955 in the UK

United States United Kingdom

Value stocks have outperformed, but not always

56,247

4,274

3,061

0

1

10

100

1,000

10,000

100,000

26 30 35 40 45 50 55 60 65 70 75 80 85 90 95 00 05 10 15

High book-to-market 12.9% p.a. US market 9.8% p.a.

Low book-to-market 9.3% p.a.

0.1

9,173

1,146

419

1

10

100

1,000

10,000

1955 60 65 70 75 80 85 90 95 2000 05 10 15

High book-to-market 16.0% p.a. UK market 12.1% p.a.

Low book-to-market 10.3% p.a.

Value

Growth Growth

Value

Source: US data from Professor Kenneth French, Dartmouth (website) 34

The value effect around the world

2.1 2.5

-10

-5

0

5

10

Ire Fin Den Swi Ita Por NZ US Bel Ger UK Spa Wld Fra SAf Net Swe Can Aus Aut Nor Jap Chi Rus

Longer term Since 2000

Source: MSCI value and growth indexes

Value beat growth in most countries over the long-run

% per year (value minus growth)

35

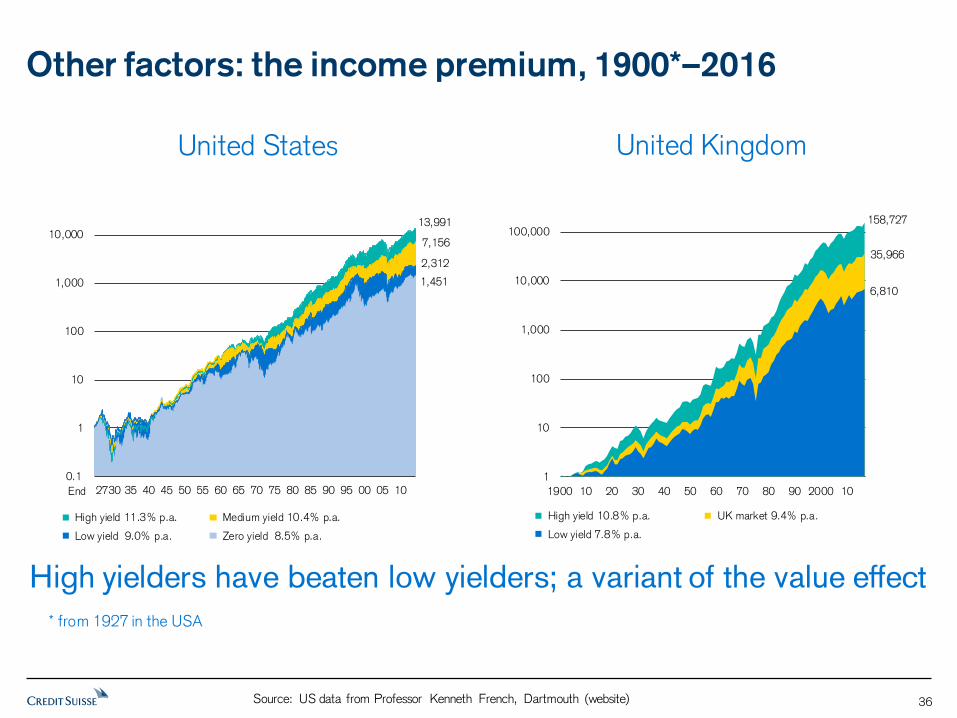

Other factors: the income premium, 1900*–2016

* from 1927 in the USA

High yielders have beaten low yielders; a variant of the value effect

United States United Kingdom

1,451

13,991

7,156

2,312

0

1

10

100

1,000

10,000

100,000

High yield 11.3% p.a. Medium yield 10.4% p.a.

Low yield 9.0% p.a. Zero yield 8.5% p.a.

0.1

End

158,727

35,966

6,810

1

10

100

1,000

10,000

100,000

1,000,000

1900 10 20 30 40 50 60 70 80 90 2000 10

High yield 10.8% p.a. UK market 9.4% p.a.

Low yield 7.8% p.a.

Source: US data from Professor Kenneth French, Dartmouth (website) 36

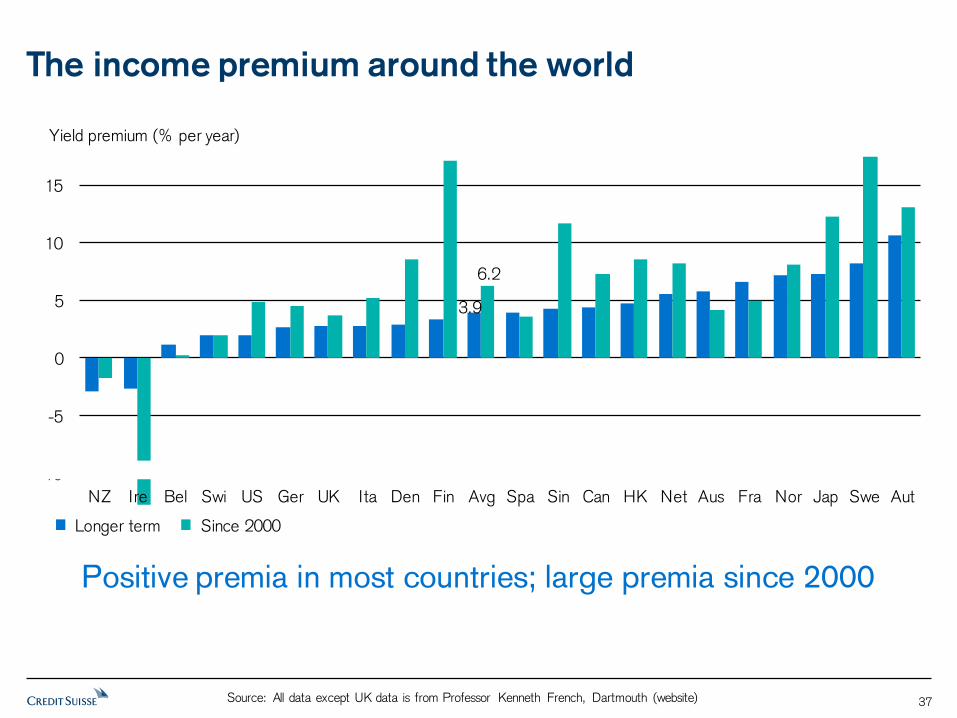

The income premium around the world

Positive premia in most countries; large premia since 2000

Source: All data except UK data is from Professor Kenneth French, Dartmouth (website)

3.9

6.2

-10

-5

0

5

10

15

NZ Ire Bel Swi US Ger UK Ita Den Fin Avg Spa Sin Can HK Net Aus Fra Nor Jap Swe Aut

Longer term Since 2000

Yield premium (% per year)

37

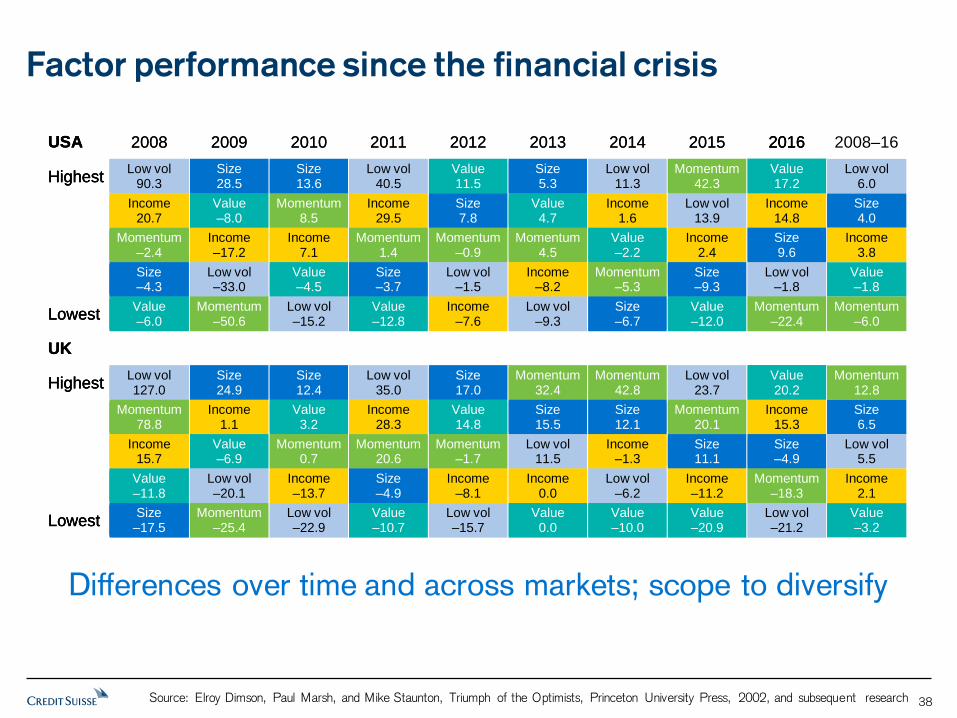

Factor performance since the financial crisis

USA 2016

Highest Value 17.2

Income

14.8

Size 9.6

Low vol

–1.8

Lowest Momentum

–22.4

UK

Highest Value 20.2

Income

15.3

Size –4.9

Momentum

–18.3

Lowest Low vol –21.2

USA 2008 2009 2010 2011 2012 2013 2014 2015 2016

Highest Low vol

90.3 Size 28.5

Size 13.6

Low vol 40.5

Value 11.5

Size 5.3

Low vol 11.3

Momentum 42.3

Value 17.2

Income

20.7 Value –8.0

Momentum 8.5

Income 29.5

Size 7.8

Value 4.7

Income 1.6

Low vol 13.9

Income 14.8

Momentum

–2.4 Income –17.2

Income 7.1

Momentum 1.4

Momentum –0.9

Momentum 4.5

Value –2.2

Income 2.4

Size 9.6

Size –4.3

Low vol –33.0

Value –4.5

Size –3.7

Low vol –1.5

Income –8.2

Momentum –5.3

Size –9.3

Low vol –1.8

Lowest Value –6.0

Momentum –50.6

Low vol –15.2

Value –12.8

Income –7.6

Low vol –9.3

Size –6.7

Value –12.0

Momentum –22.4

UK

Highest Low vol 127.0

Size 24.9

Size 12.4

Low vol 35.0

Size 17.0

Momentum 32.4

Momentum 42.8

Low vol 23.7

Value 20.2

Momentum

78.8 Income

1.1 Value

3.2 Income

28.3 Value 14.8

Size 15.5

Size 12.1

Momentum 20.1

Income 15.3

Income

15.7 Value –6.9

Momentum 0.7

Momentum 20.6

Momentum –1.7

Low vol 11.5

Income –1.3

Size 11.1

Size –4.9

Value –11.8

Low vol –20.1

Income –13.7

Size –4.9

Income –8.1

Income 0.0

Low vol –6.2

Income –11.2

Momentum –18.3

Lowest Size –17.5

Momentum –25.4

Low vol –22.9

Value –10.7

Low vol –15.7

Value 0.0

Value –10.0

Value –20.9

Low vol –21.2

USA 2008 2009 2010 2011 2012 2013 2014 2015 2016 2008–16

Highest Low vol

90.3 Size 28.5

Size 13.6

Low vol 40.5

Value 11.5

Size 5.3

Low vol 11.3

Momentum 42.3

Value 17.2

Low vol 6.0

Income

20.7 Value –8.0

Momentum 8.5

Income 29.5

Size 7.8

Value 4.7

Income 1.6

Low vol 13.9

Income 14.8

Size 4.0

Momentum

–2.4 Income –17.2

Income 7.1

Momentum 1.4

Momentum –0.9

Momentum 4.5

Value –2.2

Income 2.4

Size 9.6

Income 3.8

Size –4.3

Low vol –33.0

Value –4.5

Size –3.7

Low vol –1.5

Income –8.2

Momentum –5.3

Size –9.3

Low vol –1.8

Value –1.8

Lowest Value –6.0

Momentum –50.6

Low vol –15.2

Value –12.8

Income –7.6

Low vol –9.3

Size –6.7

Value –12.0

Momentum –22.4

Momentum –6.0

UK

Highest Low vol 127.0

Size 24.9

Size 12.4

Low vol 35.0

Size 17.0

Momentum 32.4

Momentum 42.8

Low vol 23.7

Value 20.2

Momentum 12.8

Momentum

78.8 Income

1.1 Value

3.2 Income

28.3 Value 14.8

Size 15.5

Size 12.1

Momentum 20.1

Income 15.3

Size 6.5

Income

15.7 Value –6.9

Momentum 0.7

Momentum 20.6

Momentum –1.7

Low vol 11.5

Income –1.3

Size 11.1

Size –4.9

Low vol 5.5

Value –11.8

Low vol –20.1

Income –13.7

Size –4.9

Income –8.1

Income 0.0

Low vol –6.2

Income –11.2

Momentum –18.3

Income 2.1

Lowest Size –17.5

Momentum –25.4

Low vol –22.9

Value –10.7

Low vol –15.7

Value 0.0

Value –10.0

Value –20.9

Low vol –21.2

Value –3.2

Differences over time and across markets; scope to diversify

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 38

Distinguish factors vs premiums

— factor: an influence on security returns

— premium: a superior expected return

Premiums may be evident over the long run

— some (size, value) may be harvested passively

— some (low-vol, momentum) require portfolio churning

Factor exposures can have a large performance impact

— investors can unwittingly take large positions

Factors can become too expensive

— popularity can make them an over-crowded trade

Smart beta

Source: Elroy Dimson, Paul Marsh, and Mike Staunton, Triumph of the Optimists, Princeton University Press, 2002, and subsequent research 39

General disclaimer / Important information This document was produced by and the opinions expressed are those of Credit Suisse (“CS”) as of the date of writ ing and are subject to change. It has been prepared solely for information purposes and for the use of the recipient. It does not const itute an offer or an invitat ion by or on behalf of CS to any person to buy or sell any security. Nothing in this material const itutes investment, legal, accounting or tax advice, or a representat ion that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise const itutes a personal recommendation to you. The price and value of investments mentioned and any income that might accrue may fluctuate and may fall or rise. Any reference to past performance is not a guide to the future. The information and analysis contained in this document have been compiled or arrived at from sources believed to be reliable but CS does not make any representat ion as to their accuracy or completeness and does not accept liability for any loss arising from the use hereof. A Credit Suisse Group company may have acted upon the information and analysis contained in this publicat ion before being made available to clients of CS. Investments in emerging markets are speculat ive and considerably more volat ile than investments in established markets. Some of the main risks are polit ical risks, economic risks, credit risks, currency risks and market risks. Investments in foreign currencies are subject to exchange rate fluctuat ions. Any quest ions about topics raised in this piece or your investments should be made direct ly to your local relat ionship manager or other advisers. Before entering into any transact ion, you should consider the suitability of the transact ion to your part icular circumstances and independently review (with your professional advisers as necessary) the specific financial risks as well as legal, regulatory, credit, tax and accounting consequences. This document may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the report refers to website material of CS, CS has not reviewed any such site and takes no responsibility for the content contained therein. Such address or hyperlink (including addresses or hyperlinks to CS's own website material) is provided solely for your convenience and information and the content of any such website does not in any way form part of this document. Accessing such website or following such link through this report or CS's website shall be at your own risk. This report is issued and distributed in European Union (except Switzerland): by Credit Suisse (UK) Limited and Credit Suisse Securit ies (Europe) Limited. Credit Suisse Securit ies (Europe) Limited and Credit Suisse (UK) Limited, both authorized by the Prudential Regulat ion Authority and regulated by the Financial Conduct Authority and the Prudential Regulat ion Authority, are associated but independent legal entit ies within Credit Suisse; Germany: Credit Suisse Securit ies (Europe) Limited Niederlassung Frankfurt am Main regulated by the Bundesanstalt fuer Finanzdienst leistungsaufsicht ("BaFin"); United States and Canada: Credit Suisse Securit ies (USA) LLC; Switzerland: Credit Suisse AG authorized and regulated by the Swiss Financial Market Supervisory Authority (FINMA); Brazil: Banco de Invest imentos Credit Suisse (Brasil) S.A or its affiliates; Mexico: Banco Credit Suisse (México), S.A. (transact ions related to the securit ies mentioned in this report will only be effected in compliance with applicable regulat ion); Japan: by Credit Suisse Securit ies (Japan) Limited, Financial Instruments Firm, Director-General of Kanto Local Finance Bureau ( Kinsho) No. 66, a member of Japan Securit ies Dealers Associat ion, The Financial Futures Associat ion of Japan, Japan Investment Advisers Associat ion, Type II Financial Instruments Firms Associat ion; Hong Kong: Credit Suisse (Hong Kong) Limited; Australia: Credit Suisse Equit ies (Australia) Limited; Thailand: Credit Suisse Securit ies (Thailand) Limited, regulated by the Office of the Securit ies and Exchange Commission, Thailand, having registered address at 990 Abdulrahim Place, 27th Floor, Unit 2701, Rama IV Road, Silom, Bangrak, Bangkok10500, Thailand, Tel. +66 2614 6000; Malaysia: Credit Suisse Securit ies (Malaysia) Sdn Bhd, Credit Suisse AG, Singapore Branch; India: Credit Suisse Securit ies (India) Private Limited (CIN no.U67120MH1996PTC104392) regulated by the Securit ies and Exchange Board of India as Research Analyst (registrat ion no. INH 000001030) and as Stock Broker (registrat ion no. INB230970637; INF230970637; INB010970631; INF010970631), having registered address at 9th Floor, Ceejay House, Dr.A.B. Road, Worli, Mumbai - 18, India, T- +91-22 6777 3777; South Korea: Credit Suisse Securit ies (Europe) Limited, Seoul Branch; Taiwan: Credit Suisse AG Taipei Securit ies Branch; Indonesia: PT Credit Suisse Securit ies Indonesia; Philippines: Credit Suisse Securit ies (Philippines ) Inc., and elsewhere in the world by the relevant authorized affiliate of the above. Additional Regional Disclaimers Hong Kong: Credit Suisse (Hong Kong) Limited ("CSHK") is licensed and regulated by the Securit ies and Futures Commission of Hong Kong under the laws of Hong Kong, which differ from Australian laws. CSHKL does not hold an Australian financial services license (AFSL) and is exempt from the requirement to hold an AFSL under the Corporat ions Act 2001 (the Act) under Class Order 03/1103 published by the ASIC in respect of financial services provided to Australian wholesale clients (within the meaning of sect ion 761G of the Act). Research on Taiwanese securit ies produced by Credit Suisse AG, Taipei Securit ies Branch has been prepared by a registered Senior Business Person. Malaysia: Research provided to residents of Malaysia is authorized by the Head of Research for Credit Suisse Securit ies (Malaysia) Sdn Bhd, to whom they should direct any queries on +603 2723 2020. Singapore: This report has been prepared and issued for distribut ion in Singapore to inst itut ional investors, accredited investors and expert investors (each as defined under the Financial Advisers Regulat ions) only, and is also distributed by Credit Suisse AG, Singapore branch to overseas investors (as defined under the Financial Advisers Regulat ions). By virtue of your status as an inst itut ional investor, accredited investor, expert investor or overseas investor, Credit Suisse AG, Singapore branch is exempted from complying with certain compliance requirements under the Financial Advisers Act, Chapter 110 of Singapore (the "FAA"), the Financial Advisers Regulat ions and the relevant Notices and Guidelines issued thereunder, in respect of any financial advisory service which Credit Suisse AG, Singapore branch may provide to you. UAE: This information is being distributed by Credit Suisse AG (DIFC Branch), duly licensed and regulated by the Dubai Financial Services Authority (“DFSA”). Related financial services or products are only made available to Professional Clients or Market Counterpart ies, as defined by the DFSA, and are not intended for any other persons. Credit Suisse AG (DIFC Branch) is located on Level 9 East, The Gate Building, DIFC, Dubai, United Arab Emirates. UK: The protect ions made available by the Financial Conduct Authority and/or the Prudential Regulat ion Authority for retail clients do not apply to investments or services provided by a person outside the UK, nor will the Financial Services Compensat ion Scheme be available if the issuer of the investment fails to meet its obligat ions. To the extent communicated in the United Kingdom (“UK”) or capable of having an effect in the UK, this document const itutes a financial promotion which has been approved by Credit Suisse (UK) Limited which is authorized by the Prudential Regulat ion Authority and regulated by the Financial Conduct Authority and the Prudential Regulat ion Authority for the conduct of investment business in the UK. The registered address of Credit Suisse (UK) Limited is Five Cabot Square, London, E14 4QR. Please note that the rules under the UK’s Financial Services and Markets Act 2000 relat ing to the protect ion of retail clients will not be applicable to you and t hat any potent ial compensation made available to “eligible claimants” under the UK’s Financial Services Compensat ion Scheme will also not be available to you. Tax treatment depends on the individual circumstances of each client and may be subject to changes in future EU: This report has been produced by subsidiaries and affiliates of Credit Suisse operat ing under its Global Markets Division and/or Internat ional Wealth Management Division. This document may not be reproduced either in whole, or in part, without the written permission of the authors and Credit Suisse. © 2017 Credit Suisse Group AG and/or its affiliates. All rights reserved

Global Disclaimer / Important Information

40