Embed Size (px)

Citation preview

John GerspachChief Financial Officer

February 12, 2013

Credit Suisse Financial Services Forum

1

2012 Results

Citicorp

Citi Holdings

Expenses and Capital

Conclusions

Agenda

2

2

2012 Highlights

Improved core business performance in 2012

Revenue, volume and net income growth in each business

Stable net interest margin

Continued strong credit quality

Reported results reflected the continued impact of legacy issues

Continuing to wind-down Citi Holdings

Strong capital and liquidity position

3

3

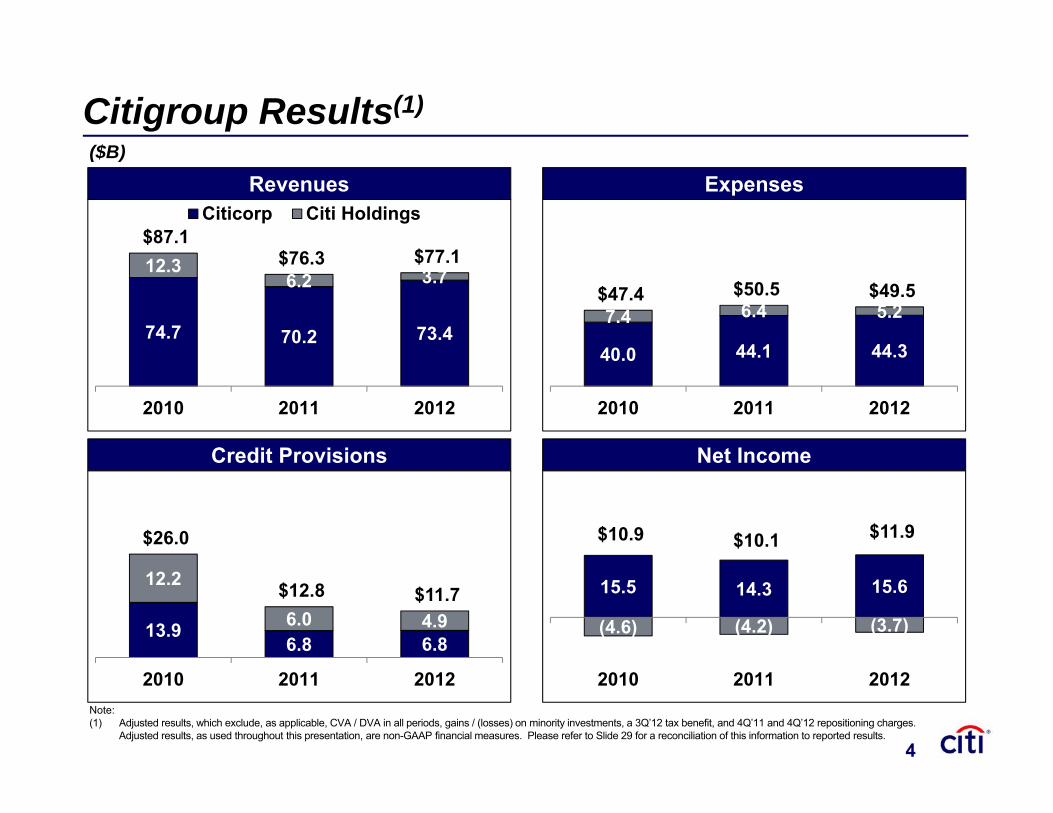

Credit Provisions Net Income

($B)

ExpensesRevenues

Citigroup Results(1)

74.7 70.2 73.4

12.3 6.2 3.7

$87.1 $76.3 $77.1

2010 2011 2012

Citicorp Citi Holdings

13.96.8 6.8

12.2

6.0 4.9

$26.0

$12.8 $11.7

2010 2011 2012

40.0 44.1 44.3

7.4 6.4 5.2$47.4 $50.5 $49.5

2010 2011 2012

15.5 14.3 15.6

(4.6) (4.2) (3.7)

$10.9 $10.1 $11.9

2010 2011 2012Note:(1) Adjusted results, which exclude, as applicable, CVA / DVA in all periods, gains / (losses) on minority investments, a 3Q’12 tax benefit, and 4Q’11 and 4Q’12 repositioning charges.

Adjusted results, as used throughout this presentation, are non-GAAP financial measures. Please refer to Slide 29 for a reconciliation of this information to reported results. 4

4

2012 Results

Citicorp

Citi Holdings

Expenses and Capital

Conclusions

Agenda

5

5

Citicorp – Executing a Global Strategy

Integrated global business On the ground in ~100 countries across North America, Latin America,

Europe, Asia and Africa Local market deposit-gathering and asset funding Unique ability to facilitate EM-DM and EM-EM flows

Focused client strategy High quality consumer and corporate client base Focused on retail banking in the world’s largest, most important cities Institutional emphasis on largest multi-national corporations and investors

Disciplined model Scale and scope of business designed to meet clients’ demand for global

financial services Allocating capital and resources to businesses and markets with the

greatest potential returns

6

67

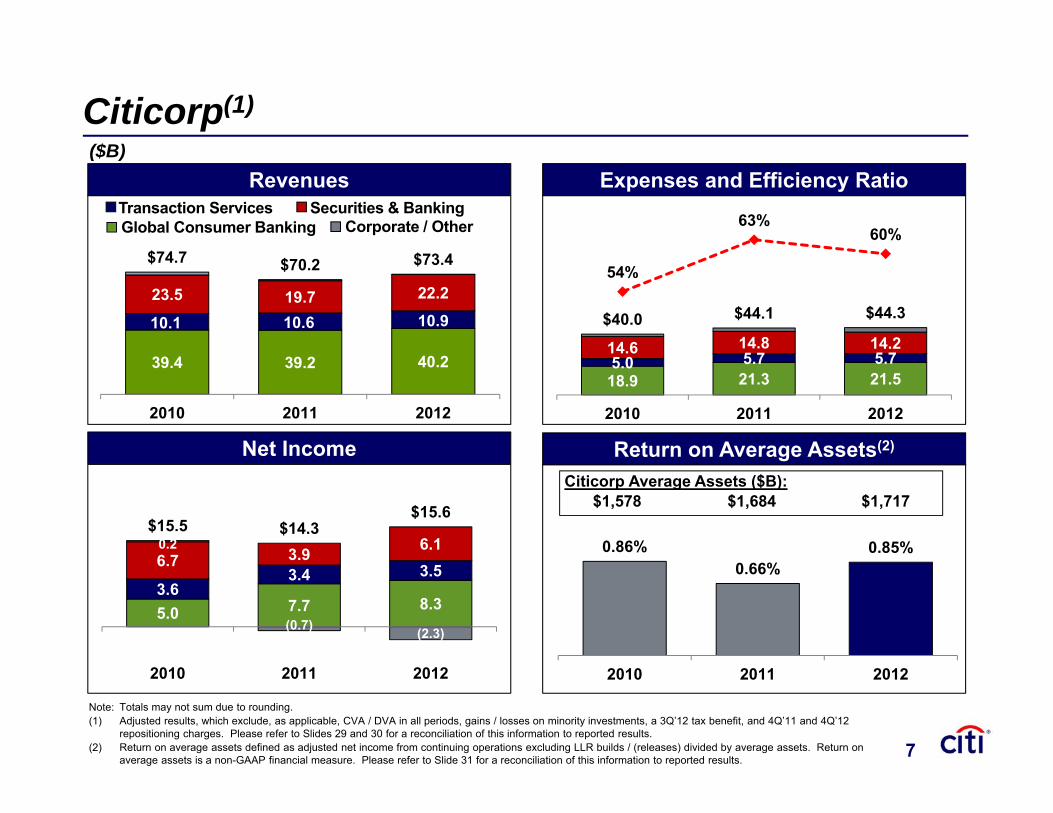

39.4 39.2 40.2

10.1 10.6 10.923.5 19.7 22.2

$74.7 $70.2 $73.4

2010 2011 2012

0.86%0.66%

0.85%

2010 2011 2012

Citicorp Average Assets ($B):$1,578 $1,684 $1,717

Citicorp(1)

5.0 7.7 8.33.6

3.4 3.56.7 3.9 6.10.2

(0.7) (2.3)

$15.5 $14.3$15.6

2010 2011 2012

Net Income

Revenues($B)

Return on Average Assets(2)

Note: Totals may not sum due to rounding.(1) Adjusted results, which exclude, as applicable, CVA / DVA in all periods, gains / losses on minority investments, a 3Q’12 tax benefit, and 4Q’11 and 4Q’12

repositioning charges. Please refer to Slides 29 and 30 for a reconciliation of this information to reported results. (2) Return on average assets defined as adjusted net income from continuing operations excluding LLR builds / (releases) divided by average assets. Return on

average assets is a non-GAAP financial measure. Please refer to Slide 31 for a reconciliation of this information to reported results.

Expenses and Efficiency Ratio

18.9 21.3 21.55.0 5.7 5.714.6 14.8 14.2

$40.0 $44.1 $44.3

54%

63%60%

2010 2011 2012

Global Consumer BankingTransaction Services Securities & Banking

Corporate / Other

7

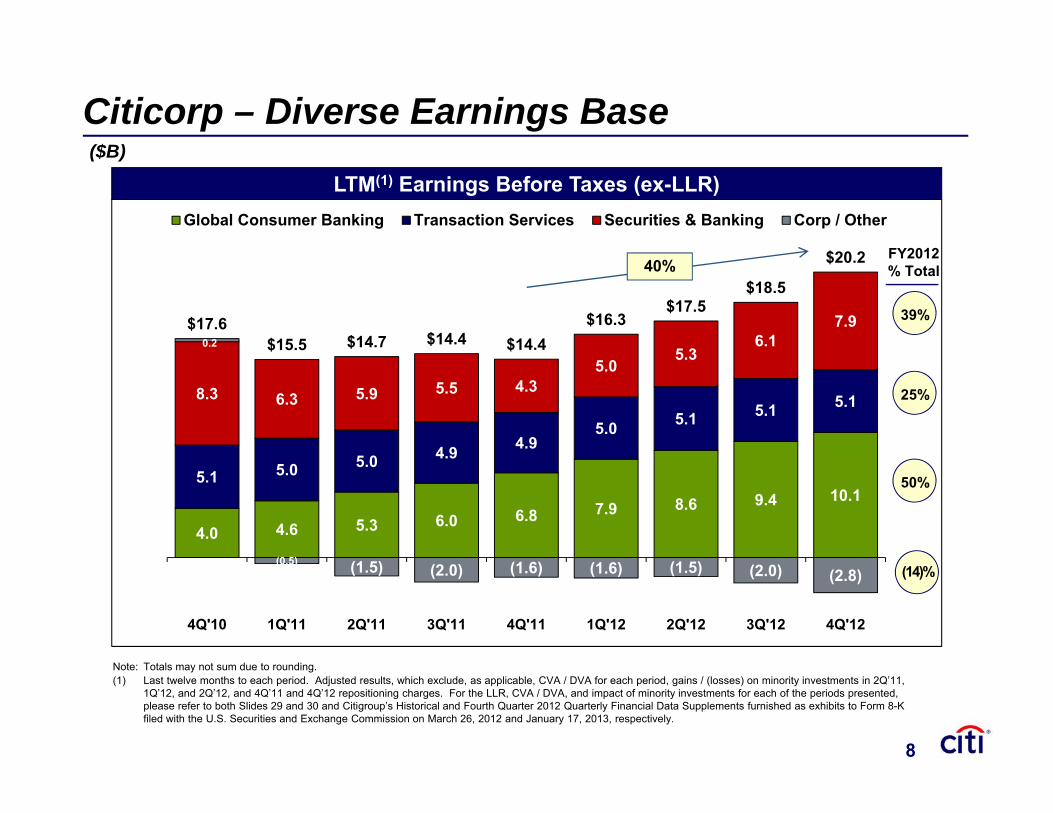

4.0 4.6 5.3 6.0 6.8 7.9 8.6 9.4 10.15.1 5.0 5.0 4.9 4.9

5.0 5.1 5.1 5.18.3 6.3 5.9 5.5 4.3 5.0

5.3 6.1

7.9 0.2

(0.5) (1.5) (2.0) (1.6) (1.6) (1.5) (2.0) (2.8)

$17.6 $15.5 $14.7 $14.4 $14.4

$16.3 $17.5

$18.5

$20.2

4Q'10 1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

Global Consumer Banking Transaction Services Securities & Banking Corp / Other

LTM(1) Earnings Before Taxes (ex-LLR)

Citicorp – Diverse Earnings Base

Note: Totals may not sum due to rounding. (1) Last twelve months to each period. Adjusted results, which exclude, as applicable, CVA / DVA for each period, gains / (losses) on minority investments in 2Q’11,

1Q’12, and 2Q’12, and 4Q’11 and 4Q’12 repositioning charges. For the LLR, CVA / DVA, and impact of minority investments for each of the periods presented, please refer to both Slides 29 and 30 and Citigroup’s Historical and Fourth Quarter 2012 Quarterly Financial Data Supplements furnished as exhibits to Form 8-K filed with the U.S. Securities and Exchange Commission on March 26, 2012 and January 17, 2013, respectively.

8

($B)

40%

39%

25%

50%

(14)%

FY2012% Total

8

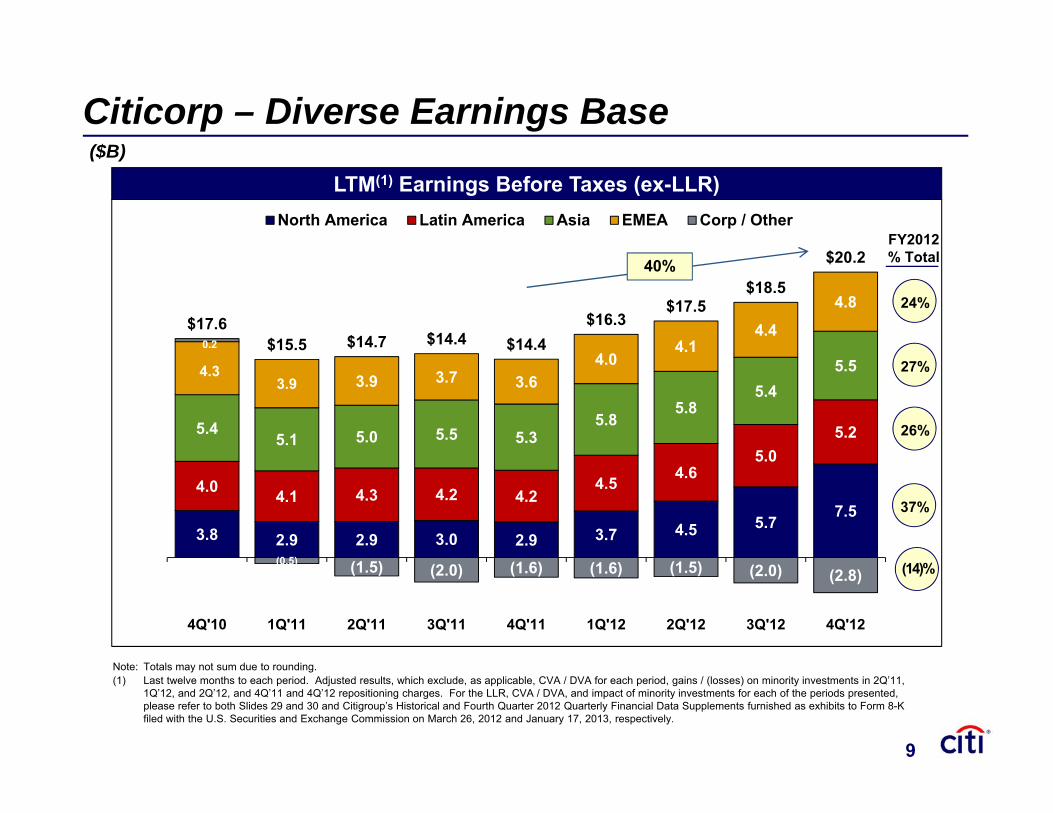

3.8 2.9 2.9 3.0 2.9 3.7 4.5 5.77.5

4.0 4.1 4.3 4.2 4.24.5 4.6

5.05.25.4

5.1 5.0 5.5 5.3 5.8

5.8 5.4

5.5 4.3 3.9 3.9 3.7 3.6

4.0 4.1

4.4

4.8

0.2

(0.5) (1.5) (2.0) (1.6) (1.6) (1.5) (2.0) (2.8)

$17.6$15.5 $14.7 $14.4 $14.4

$16.3$17.5

$18.5

$20.2

4Q'10 1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

North America Latin America Asia EMEA Corp / Other

LTM(1) Earnings Before Taxes (ex-LLR)

Citicorp – Diverse Earnings Base

Note: Totals may not sum due to rounding.(1) Last twelve months to each period. Adjusted results, which exclude, as applicable, CVA / DVA for each period, gains / (losses) on minority investments in 2Q’11,

1Q’12, and 2Q’12, and 4Q’11 and 4Q’12 repositioning charges. For the LLR, CVA / DVA, and impact of minority investments for each of the periods presented, please refer to both Slides 29 and 30 and Citigroup’s Historical and Fourth Quarter 2012 Quarterly Financial Data Supplements furnished as exhibits to Form 8-K filed with the U.S. Securities and Exchange Commission on March 26, 2012 and January 17, 2013, respectively.

9

($B)

40%

24%

27%

26%

(14)%

FY2012% Total

37%

9

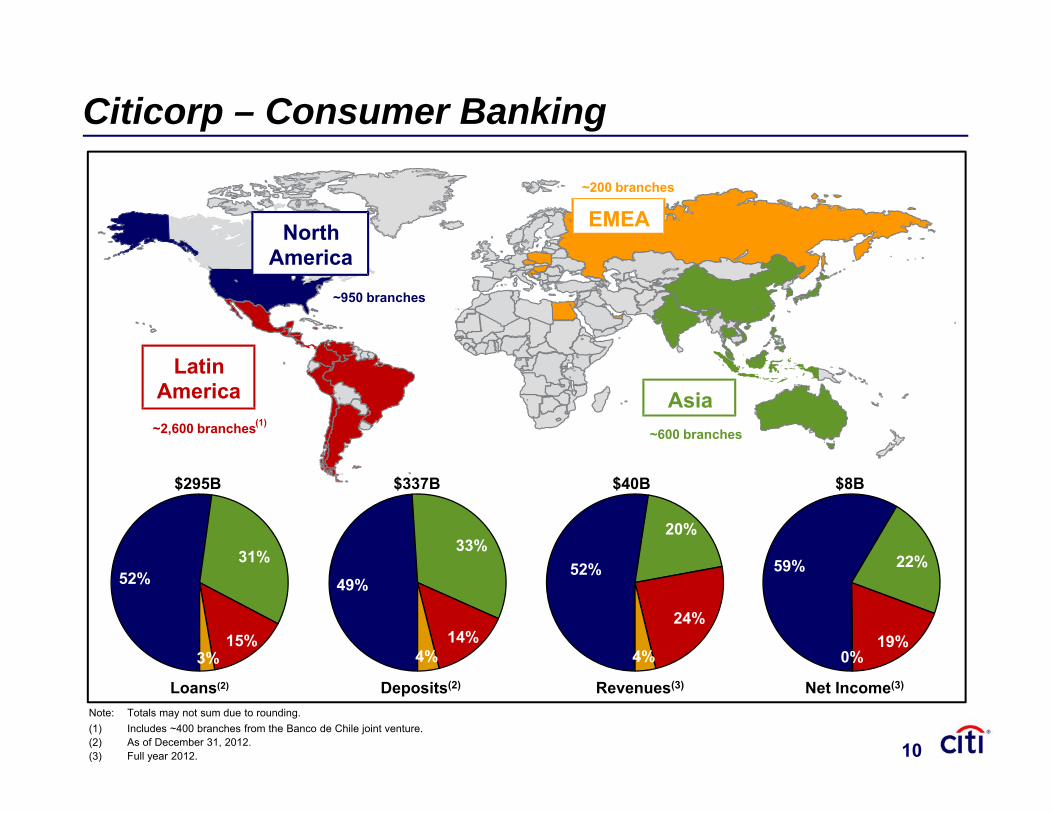

Citicorp – Consumer Banking

$337B$295B $40B $8B

52%

20%

24%

4%

Revenues(3)

59% 22%

19%0%

Net Income(3)

52%31%

15%3%

Loans(2)

49%

33%

14%4%

Deposits(2)

Note: Totals may not sum due to rounding. (1) Includes ~400 branches from the Banco de Chile joint venture.(2) As of December 31, 2012.(3) Full year 2012.

Asia

EMEA

Latin America

North America

~950 branches

~2,600 branches(1)~600 branches

~200 branches

10

10

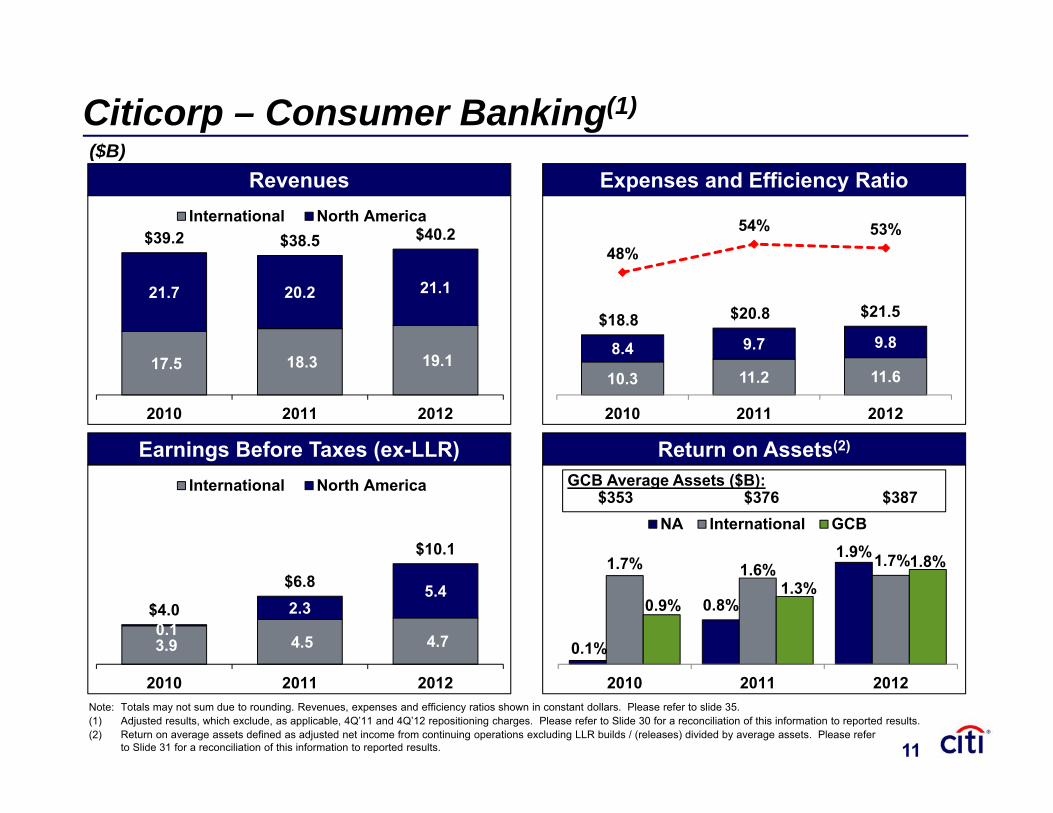

Note: Totals may not sum due to rounding. Revenues, expenses and efficiency ratios shown in constant dollars. Please refer to slide 35. (1) Adjusted results, which exclude, as applicable, 4Q’11 and 4Q’12 repositioning charges. Please refer to Slide 30 for a reconciliation of this information to reported results. (2) Return on average assets defined as adjusted net income from continuing operations excluding LLR builds / (releases) divided by average assets. Please refer

to Slide 31 for a reconciliation of this information to reported results.

0.1%

0.8%

1.9%1.7% 1.6% 1.7%

0.9%1.3%

1.8%

2010 2011 2012

NA International GCB

Revenues

Citicorp – Consumer Banking(1)

Earnings Before Taxes (ex-LLR)

($B)Expenses and Efficiency Ratio

17.5 18.3 19.1

21.7 20.2 21.1

$39.2 $38.5 $40.2

2010 2011 2012

International North America

Return on Assets(2)

10.3 11.2 11.6

8.4 9.7 9.8$18.8 $20.8 $21.5

48%

54% 53%

2010 2011 2012

GCB Average Assets ($B):$353 $376 $387

3.9 4.5 4.7 0.1

2.35.4

$4.0

$6.8

$10.1

2010 2011 2012

International North America

11

11

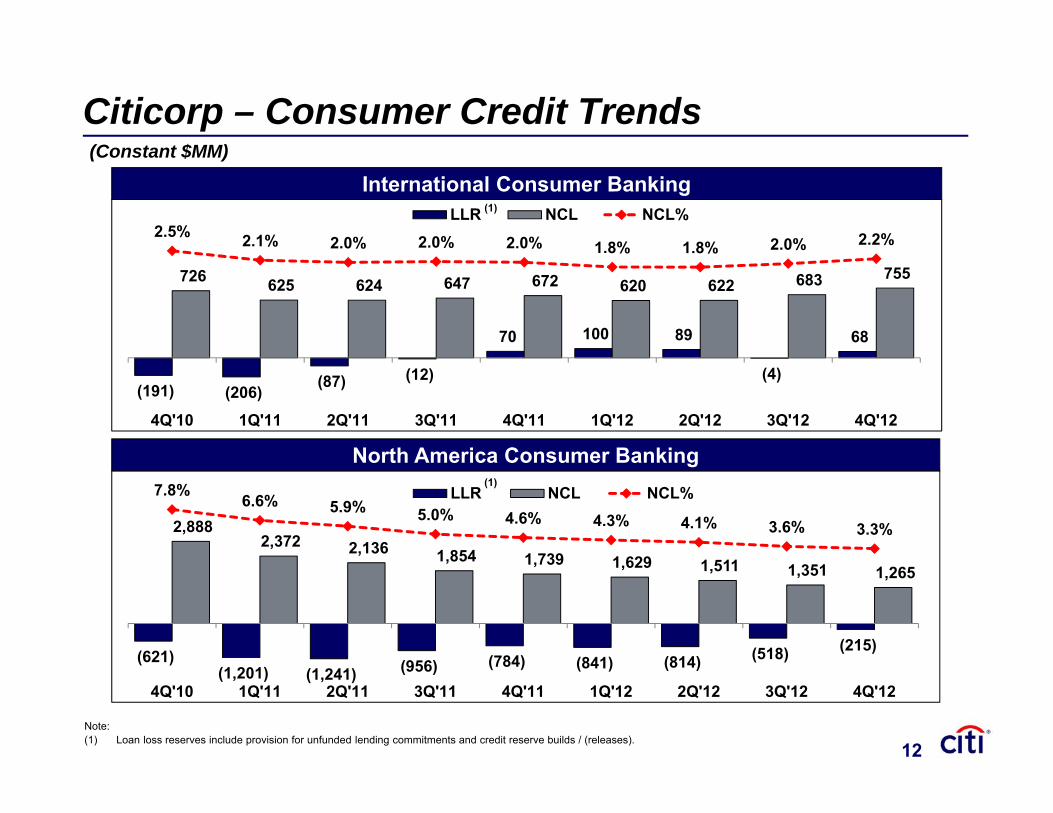

Citicorp – Consumer Credit Trends (Constant $MM)

(191) (206) (87) (12)

70 100 89

(4)

68

726 625 624 647 672 620 622 683 755

2.5% 2.1% 2.0% 2.0% 2.0% 1.8% 1.8% 2.0% 2.2%

4Q'10 1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

LLR NCL NCL%

International Consumer Banking

(621)(1,201) (1,241) (956) (784) (841) (814) (518) (215)

2,888 2,372 2,136 1,854 1,739 1,629 1,511 1,351 1,265

7.8% 6.6% 5.9% 5.0% 4.6% 4.3% 4.1% 3.6% 3.3%

4Q'10 1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

LLR NCL NCL%

North America Consumer Banking

Note:(1) Loan loss reserves include provision for unfunded lending commitments and credit reserve builds / (releases).

(1)

(1)

12

12

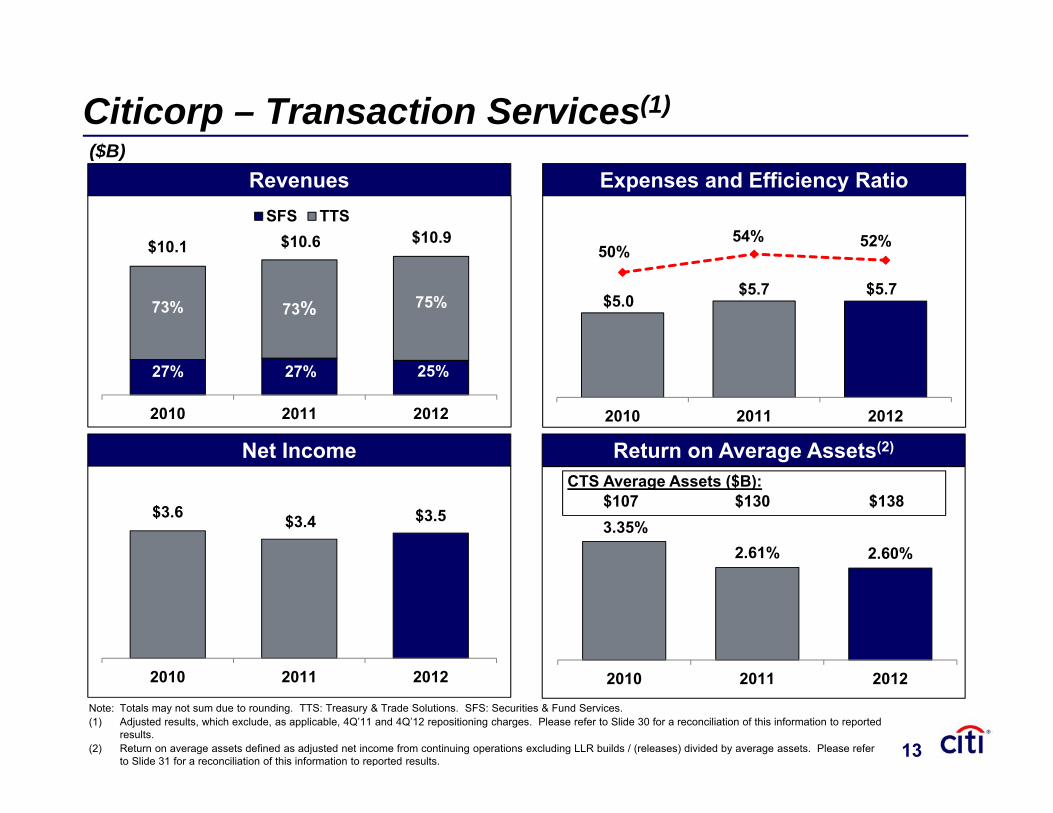

$5.0$5.7 $5.7

50%54% 52%

2010 2011 20122010 2011 2012

SFS TTS

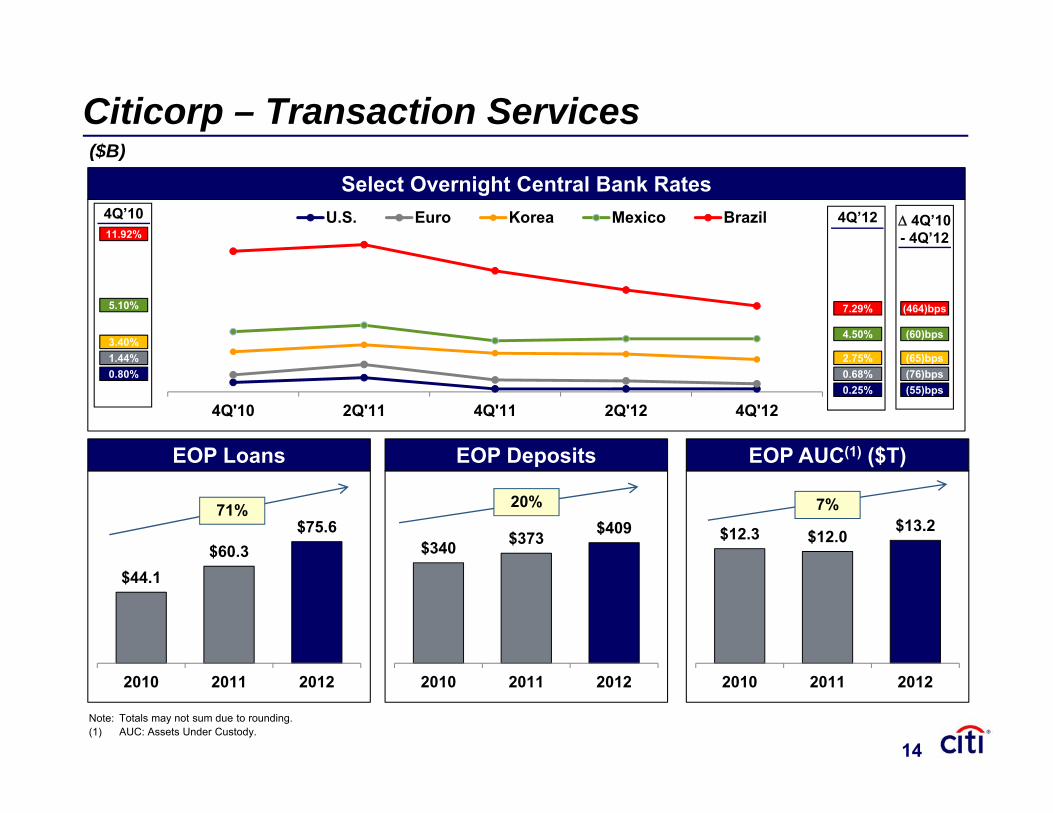

Citicorp – Transaction Services(1)

$3.6 $3.4 $3.5

2010 2011 2012

Net Income

Revenues

25%27%

75%73%

$10.1 $10.6 $10.9

27%

73%

($B)

Return on Average Assets(2)

3.35%2.61% 2.60%

2010 2011 2012

CTS Average Assets ($B):$107 $130 $138

Note: Totals may not sum due to rounding. TTS: Treasury & Trade Solutions. SFS: Securities & Fund Services.(1) Adjusted results, which exclude, as applicable, 4Q’11 and 4Q’12 repositioning charges. Please refer to Slide 30 for a reconciliation of this information to reported

results. (2) Return on average assets defined as adjusted net income from continuing operations excluding LLR builds / (releases) divided by average assets. Please refer

to Slide 31 for a reconciliation of this information to reported results.

Expenses and Efficiency Ratio

13

13

4Q'10 2Q'11 4Q'11 2Q'12 4Q'12

U.S. Euro Korea Mexico Brazil 4Q’1211.92%

3.40%

5.10%

1.44%0.80%

7.29%

2.75%

4.50%

0.68%0.25%

4Q’10 4Q’10- 4Q’12

(464)bps

(65)bps

(60)bps

(76)bps(55)bps

Citicorp – Transaction Services

$44.1$60.3

$75.6

2010 2011 2012

EOP Loans

Select Overnight Central Bank Rates($B)

Note: Totals may not sum due to rounding.(1) AUC: Assets Under Custody.

$340 $373 $409

2010 2011 2012

20%

EOP Deposits

$12.3 $12.0 $13.2

2010 2011 2012

7%

EOP AUC(1) ($T)

71%

14

14

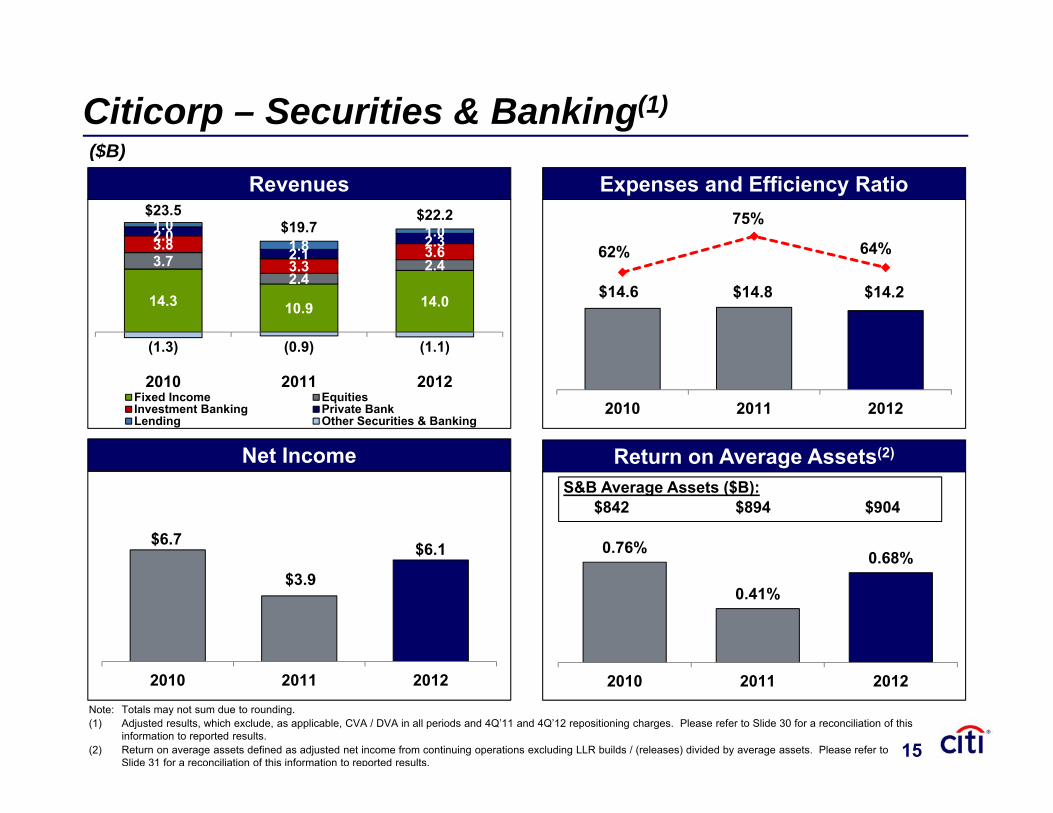

$14.6 $14.8 $14.2

62%

75%

64%

2010 2011 2012

0.76%

0.41%

0.68%

2010 2011 2012

S&B Average Assets ($B): $842 $894 $904

14.3 10.9 14.0

3.7 2.4

2.4 3.8

3.3 3.6

2.0 2.1

2.3 1.0

1.8 1.0

(1.3) (0.9) (1.1)

$23.5$19.7

$22.2

2010 2011 2012Fixed Income EquitiesInvestment Banking Private BankLending Other Securities & Banking

Citicorp – Securities & Banking(1)

$6.7

$3.9

$6.1

2010 2011 2012

Net Income

Revenues($B)

Return on Average Assets(2)

Note: Totals may not sum due to rounding.(1) Adjusted results, which exclude, as applicable, CVA / DVA in all periods and 4Q’11 and 4Q’12 repositioning charges. Please refer to Slide 30 for a reconciliation of this

information to reported results. (2) Return on average assets defined as adjusted net income from continuing operations excluding LLR builds / (releases) divided by average assets. Please refer to

Slide 31 for a reconciliation of this information to reported results.

Expenses and Efficiency Ratio

15

15

2012 Results

Citicorp

Citi Holdings

Expenses and Capital

Conclusions

Agenda

16

16

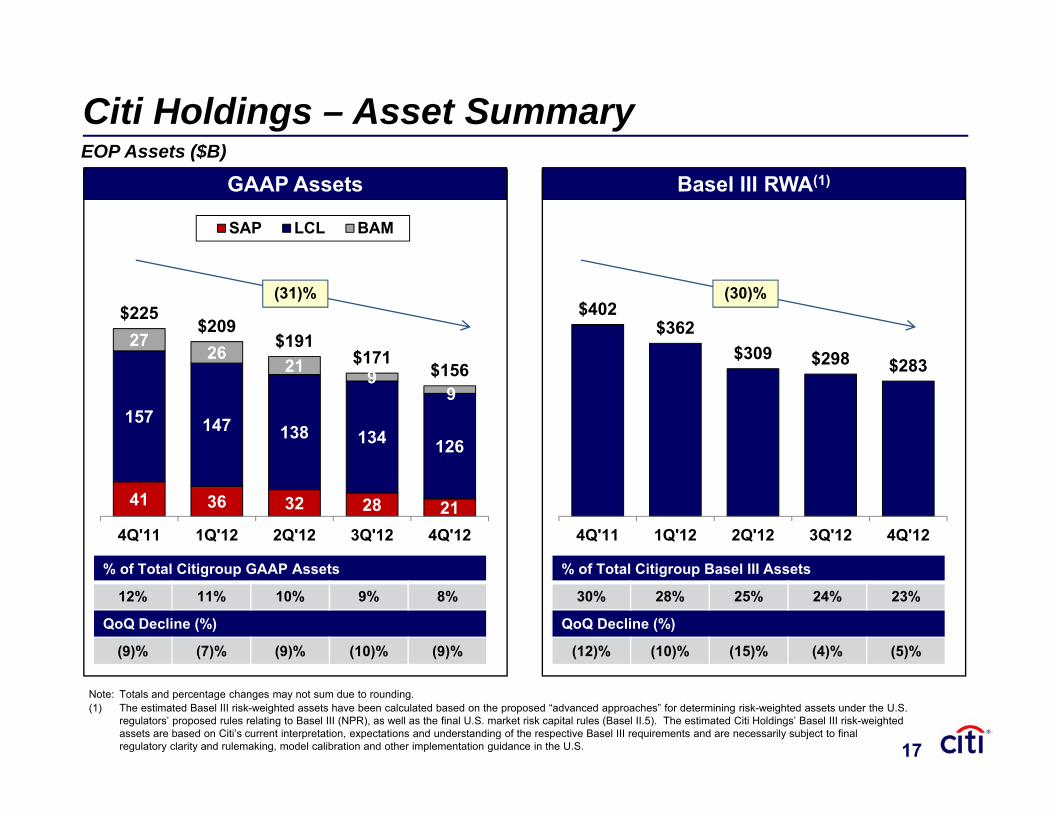

Note: Totals and percentage changes may not sum due to rounding. (1) The estimated Basel III risk-weighted assets have been calculated based on the proposed “advanced approaches” for determining risk-weighted assets under the U.S.

regulators’ proposed rules relating to Basel III (NPR), as well as the final U.S. market risk capital rules (Basel II.5). The estimated Citi Holdings’ Basel III risk-weighted assets are based on Citi’s current interpretation, expectations and understanding of the respective Basel III requirements and are necessarily subject to final regulatory clarity and rulemaking, model calibration and other implementation guidance in the U.S.

Citi Holdings – Asset Summary EOP Assets ($B)

% of Total Citigroup GAAP Assets

12% 11% 10% 9% 8%

QoQ Decline (%)

(9)% (7)% (9)% (10)% (9)%

41 36 32 28 21

157 147 138 134 126

27 26

21 9 9

$225$209

$191$171

$156

4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

SAP LCL BAM

(31)%

GAAP Assets

% of Total Citigroup Basel III Assets

30% 28% 25% 24% 23%

QoQ Decline (%)

(12)% (10)% (15)% (4)% (5)%

$402$362

$309 $298 $283

4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

(30)%

Basel III RWA(1)

17

17

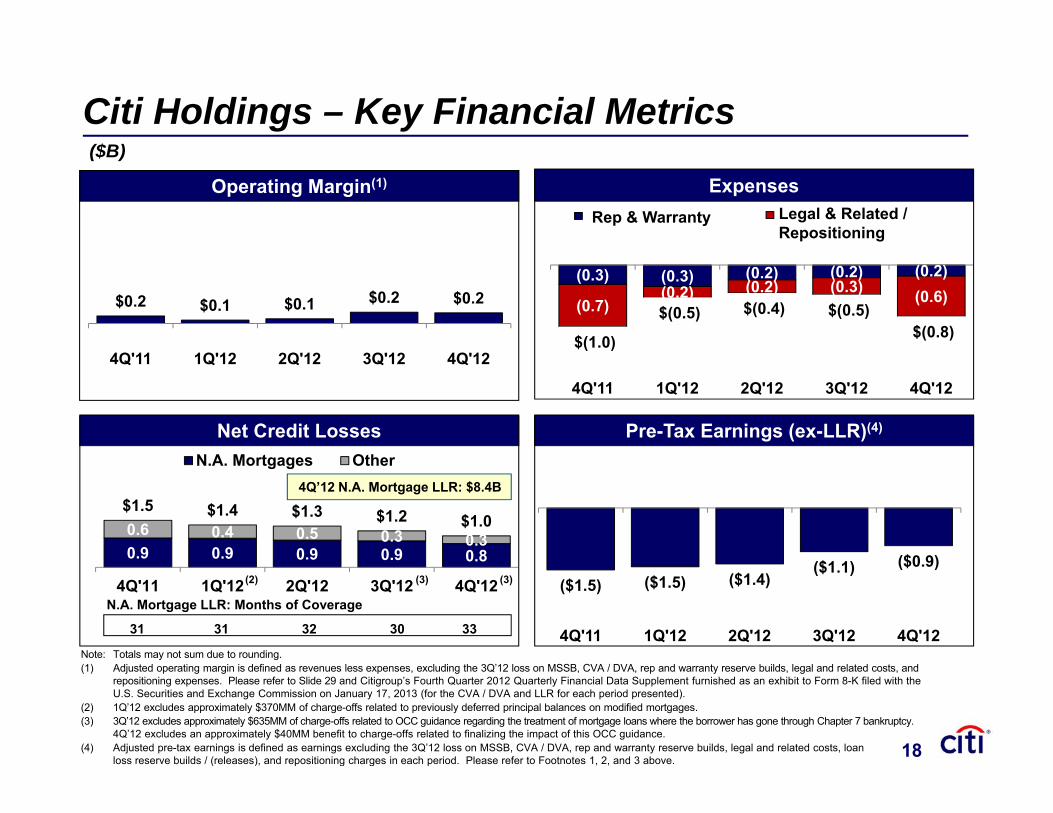

Note: Totals may not sum due to rounding.(1) Adjusted operating margin is defined as revenues less expenses, excluding the 3Q’12 loss on MSSB, CVA / DVA, rep and warranty reserve builds, legal and related costs, and

repositioning expenses. Please refer to Slide 29 and Citigroup’s Fourth Quarter 2012 Quarterly Financial Data Supplement furnished as an exhibit to Form 8-K filed with the U.S. Securities and Exchange Commission on January 17, 2013 (for the CVA / DVA and LLR for each period presented).

(2) 1Q’12 excludes approximately $370MM of charge-offs related to previously deferred principal balances on modified mortgages.(3) 3Q’12 excludes approximately $635MM of charge-offs related to OCC guidance regarding the treatment of mortgage loans where the borrower has gone through Chapter 7 bankruptcy.

4Q’12 excludes an approximately $40MM benefit to charge-offs related to finalizing the impact of this OCC guidance.(4) Adjusted pre-tax earnings is defined as earnings excluding the 3Q’12 loss on MSSB, CVA / DVA, rep and warranty reserve builds, legal and related costs, loan

loss reserve builds / (releases), and repositioning charges in each period. Please refer to Footnotes 1, 2, and 3 above.

$0.2 $0.1 $0.1 $0.2 $0.2

4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

($1.5) ($1.5) ($1.4)($1.1) ($0.9)

4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

Citi Holdings – Key Financial Metrics ($B)

Net Credit Losses Pre-Tax Earnings (ex-LLR)(4)

Expenses

0.9 0.9 0.9 0.9 0.8 0.6 0.4 0.5 0.3 0.3

$1.5 $1.4 $1.3 $1.2 $1.0

4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

N.A. Mortgages Other

N.A. Mortgage LLR: Months of Coverage

(2)

4Q’12 N.A. Mortgage LLR: $8.4B

(3)

31 31 32 30 33

(3)

Operating Margin(1)

(0.3) (0.3) (0.2) (0.2) (0.2)

(0.7)(0.2) (0.2) (0.3) (0.6)

$(1.0)

$(0.5) $(0.4) $(0.5)$(0.8)

4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

Rep & Warranty Legal & Related / Repositioning

18

18

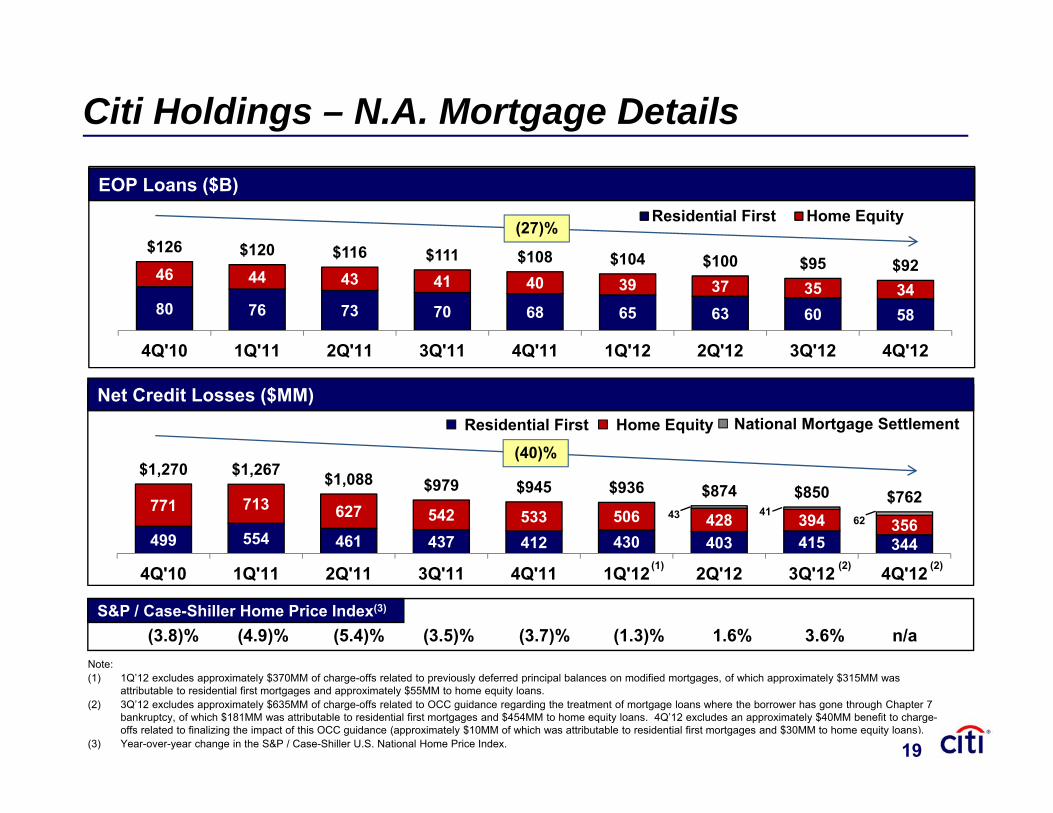

Note:(1) 1Q’12 excludes approximately $370MM of charge-offs related to previously deferred principal balances on modified mortgages, of which approximately $315MM was

attributable to residential first mortgages and approximately $55MM to home equity loans. (2) 3Q’12 excludes approximately $635MM of charge-offs related to OCC guidance regarding the treatment of mortgage loans where the borrower has gone through Chapter 7

bankruptcy, of which $181MM was attributable to residential first mortgages and $454MM to home equity loans. 4Q’12 excludes an approximately $40MM benefit to charge-offs related to finalizing the impact of this OCC guidance (approximately $10MM of which was attributable to residential first mortgages and $30MM to home equity loans).

(3) Year-over-year change in the S&P / Case-Shiller U.S. National Home Price Index.

499 554 461 437 412 430 403 415 344

771 713 627 542 533 506 428 394 356 43 41

62

$1,270 $1,267 $1,088 $979 $945 $936 $874 $850 $762

4Q'10 1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

(3.8)% (4.9)% (5.4)% (3.5)% (3.7)% (1.3)% 1.6% 3.6% n/a

Citi Holdings – N.A. Mortgage Details

S&P / Case-Shiller Home Price Index(3)

80 76 73 70 68 65 63 60 58

46 44 43 41 40 39 37 35 34

$126 $120 $116 $111 $108 $104 $100 $95 $92

4Q'10 1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

Residential First Home Equity

EOP Loans ($B)

(2)

National Mortgage SettlementResidential First Home Equity

(1)

(40)%

(2)

Net Credit Losses ($MM)

(27)%

19

19

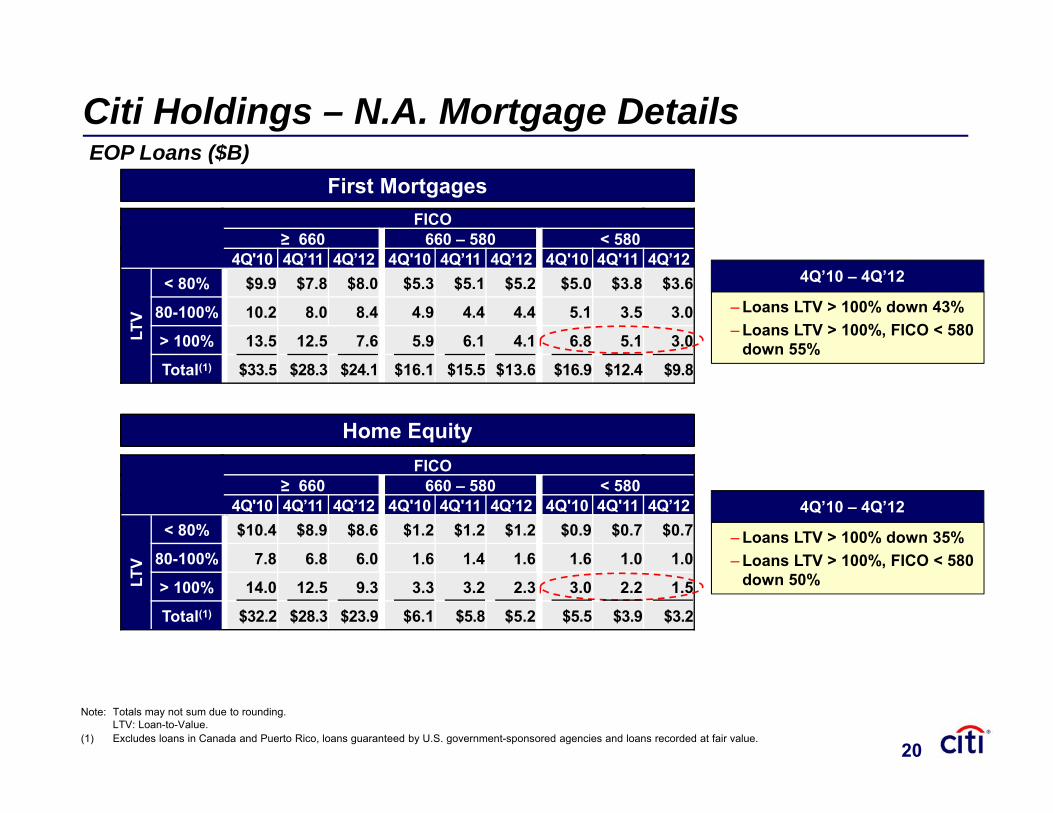

Citi Holdings – N.A. Mortgage Details

Note: Totals may not sum due to rounding. LTV: Loan-to-Value.

(1) Excludes loans in Canada and Puerto Rico, loans guaranteed by U.S. government-sponsored agencies and loans recorded at fair value.

FICO≥ 660 660 – 580 < 580

4Q'10 4Q’11 4Q’12 4Q'10 4Q’11 4Q’12 4Q'10 4Q'11 4Q’12

LTV

< 80% $9.9 $7.8 $8.0 $5.3 $5.1 $5.2 $5.0 $3.8 $3.6

80-100% 10.2 8.0 8.4 4.9 4.4 4.4 5.1 3.5 3.0

> 100% 13.5 12.5 7.6 5.9 6.1 4.1 6.8 5.1 3.0

Total(1) $33.5 $28.3 $24.1 $16.1 $15.5 $13.6 $16.9 $12.4 $9.8

First Mortgages

Home Equity

‒Loans LTV > 100% down 35% ‒Loans LTV > 100%, FICO < 580

down 50%

4Q’10 – 4Q’12

EOP Loans ($B)

FICO≥ 660 660 – 580 < 580

4Q'10 4Q’11 4Q’12 4Q'10 4Q'11 4Q’12 4Q'10 4Q'11 4Q’12

LTV

< 80% $10.4 $8.9 $8.6 $1.2 $1.2 $1.2 $0.9 $0.7 $0.7

80-100% 7.8 6.8 6.0 1.6 1.4 1.6 1.6 1.0 1.0

> 100% 14.0 12.5 9.3 3.3 3.2 2.3 3.0 2.2 1.5

Total(1) $32.2 $28.3 $23.9 $6.1 $5.8 $5.2 $5.5 $3.9 $3.2

‒Loans LTV > 100% down 43% ‒Loans LTV > 100%, FICO < 580

down 55%

4Q’10 – 4Q’12

20

20

2012 Results

Citicorp

Citi Holdings

Expenses and Capital

Conclusions

Agenda

21

21

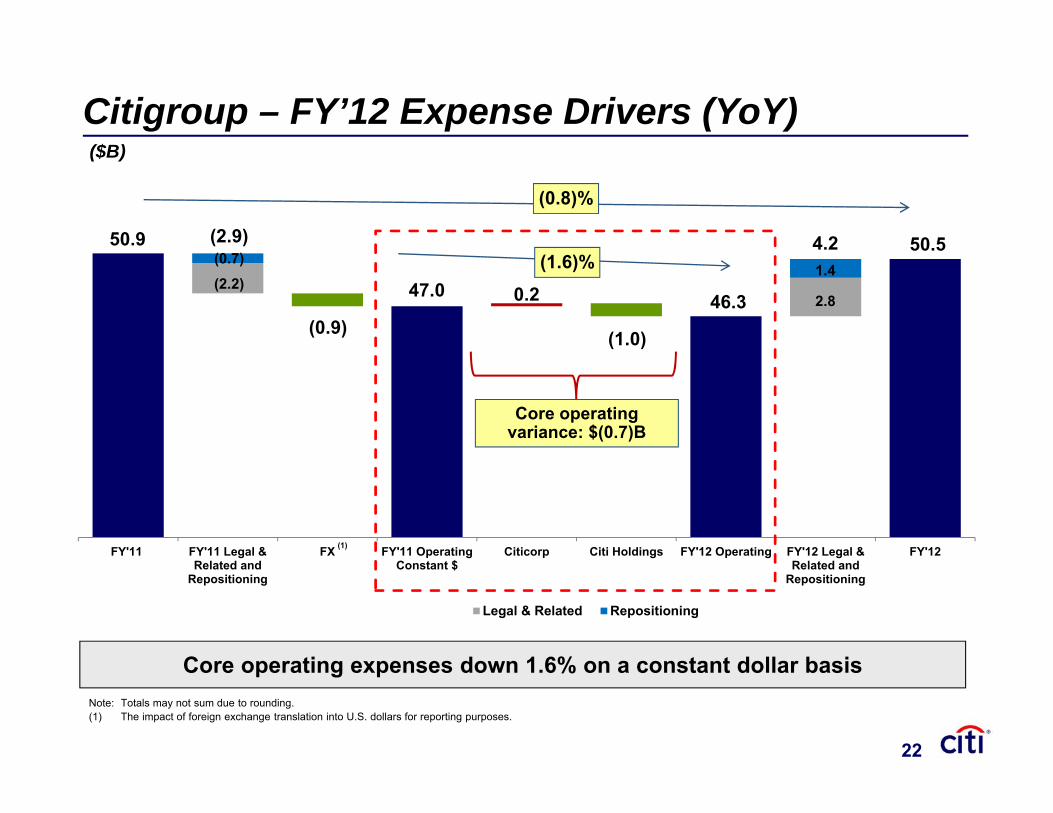

FY'11 FY'11 Legal &Related and

Repositioning

FX FY'11 OperatingConstant $

Citicorp Citi Holdings FY'12 Operating FY'12 Legal &Related and

Repositioning

FY'12

Legal & Related Repositioning

Citigroup – FY’12 Expense Drivers (YoY)

Core operating variance: $(0.7)B

Core operating expenses down 1.6% on a constant dollar basisNote: Totals may not sum due to rounding.(1) The impact of foreign exchange translation into U.S. dollars for reporting purposes.

(1.6)%

($B)

(1)

(0.8)%

(2.9) 4.2

(0.9)

(2.2)(0.7)

1.4

2.80.2

(1.0)

50.9

47.0 46.3

50.5

22

22

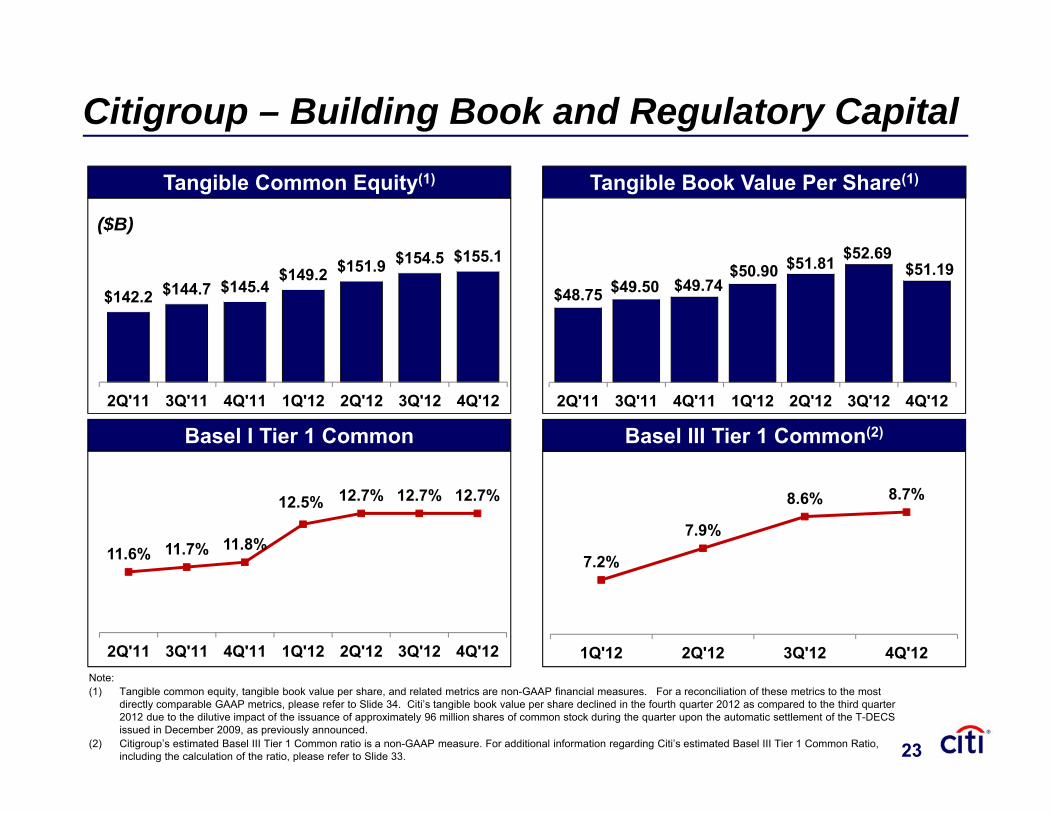

7.2%

7.9%

8.6% 8.7%

1Q'12 2Q'12 3Q'12 4Q'12

$142.2 $144.7 $145.4 $149.2 $151.9 $154.5 $155.1

2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

Basel I Tier 1 Common Basel III Tier 1 Common(2)

($B)

Tangible Book Value Per Share(1)Tangible Common Equity(1)

Citigroup – Building Book and Regulatory Capital

11.6% 11.7% 11.8%

12.5% 12.7% 12.7% 12.7%

2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

$48.75 $49.50 $49.74$50.90 $51.81 $52.69

$51.19

2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

Note:(1) Tangible common equity, tangible book value per share, and related metrics are non-GAAP financial measures. For a reconciliation of these metrics to the most

directly comparable GAAP metrics, please refer to Slide 34. Citi’s tangible book value per share declined in the fourth quarter 2012 as compared to the third quarter 2012 due to the dilutive impact of the issuance of approximately 96 million shares of common stock during the quarter upon the automatic settlement of the T-DECS issued in December 2009, as previously announced.

(2) Citigroup’s estimated Basel III Tier 1 Common ratio is a non-GAAP measure. For additional information regarding Citi’s estimated Basel III Tier 1 Common Ratio, including the calculation of the ratio, please refer to Slide 33. 23

23

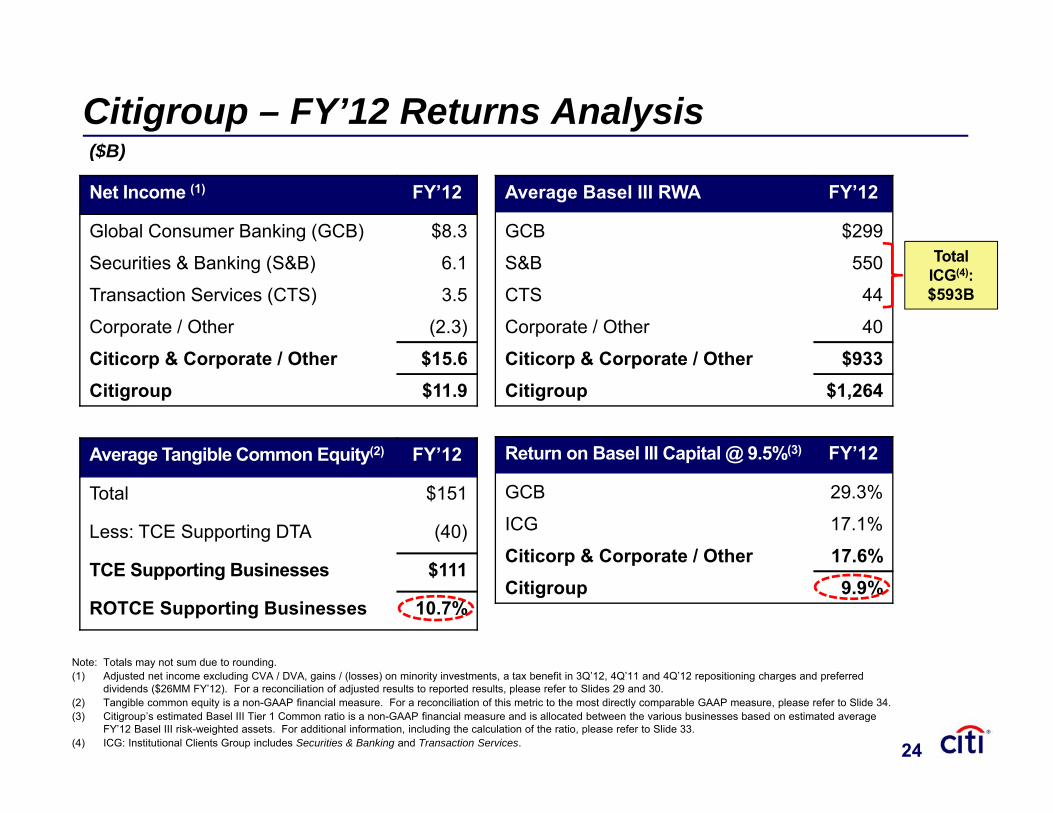

Average Tangible Common Equity(2) FY’12

Total $151

Less: TCE Supporting DTA (40)

TCE Supporting Businesses $111

ROTCE Supporting Businesses 10.7%

Citigroup – FY’12 Returns Analysis

Note: Totals may not sum due to rounding. (1) Adjusted net income excluding CVA / DVA, gains / (losses) on minority investments, a tax benefit in 3Q’12, 4Q’11 and 4Q’12 repositioning charges and preferred

dividends ($26MM FY’12). For a reconciliation of adjusted results to reported results, please refer to Slides 29 and 30.(2) Tangible common equity is a non-GAAP financial measure. For a reconciliation of this metric to the most directly comparable GAAP measure, please refer to Slide 34.(3) Citigroup’s estimated Basel III Tier 1 Common ratio is a non-GAAP financial measure and is allocated between the various businesses based on estimated average

FY’12 Basel III risk-weighted assets. For additional information, including the calculation of the ratio, please refer to Slide 33.(4) ICG: Institutional Clients Group includes Securities & Banking and Transaction Services.

Net Income (1) FY’12

Global Consumer Banking (GCB) $8.3

Securities & Banking (S&B) 6.1

Transaction Services (CTS) 3.5

Corporate / Other (2.3)

Citicorp & Corporate / Other $15.6Citigroup $11.9

Return on Basel III Capital @ 9.5%(3) FY’12

GCB 29.3%

ICG 17.1%

Citicorp & Corporate / Other 17.6%Citigroup 9.9%

Average Basel III RWA FY’12

GCB $299

S&B 550

CTS 44

Corporate / Other 40

Citicorp & Corporate / Other $933Citigroup $1,264

($B)

Total ICG(4):$593B

24

24

2012 Results

Citicorp

Citi Holdings

Expenses and Capital

Conclusions

Agenda

25

25

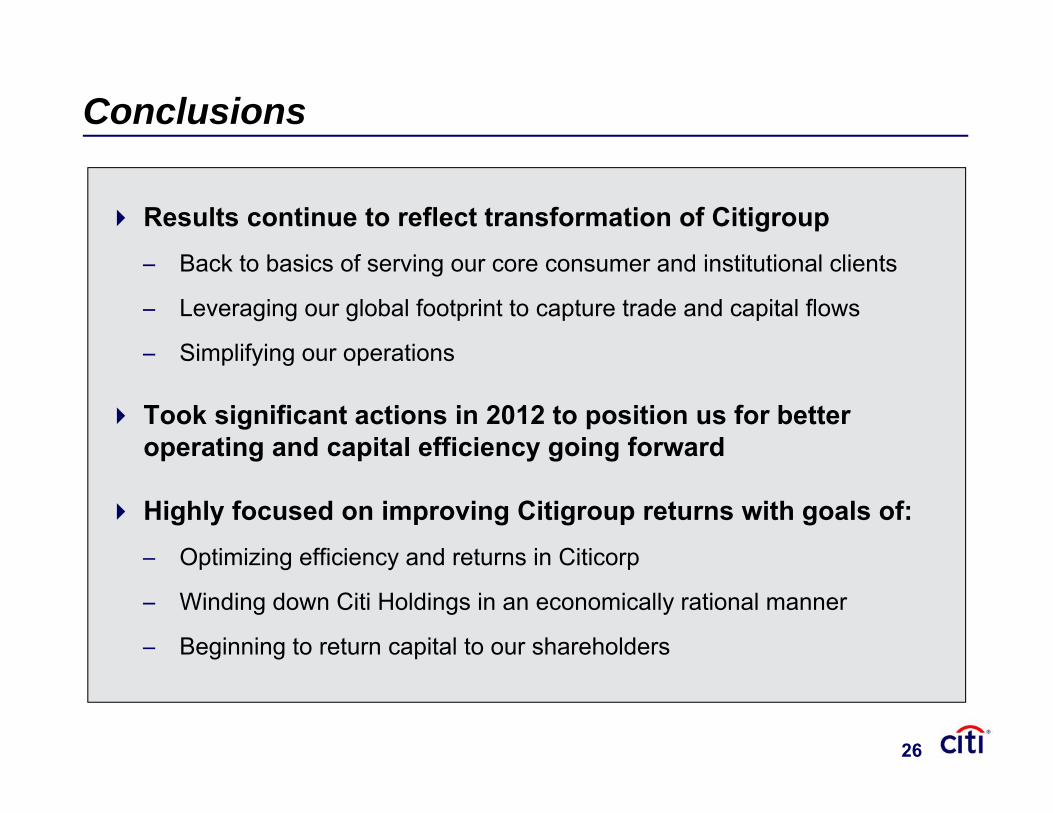

Conclusions

Results continue to reflect transformation of Citigroup– Back to basics of serving our core consumer and institutional clients

– Leveraging our global footprint to capture trade and capital flows

– Simplifying our operations

Took significant actions in 2012 to position us for better operating and capital efficiency going forward

Highly focused on improving Citigroup returns with goals of:– Optimizing efficiency and returns in Citicorp

– Winding down Citi Holdings in an economically rational manner

– Beginning to return capital to our shareholders

26

26

Certain statements in this document are “forward-looking statements” within the meaning of the

rules and regulations of the U.S. Securities and Exchange Commission. These statements are

based on management’s current expectations and are subject to uncertainty and changes in

circumstances. These statements are not guarantees of future results or occurrences. Actual

results and capital and other financial condition may differ materially from those included in

these statements due to a variety of factors, including the precautionary statements included in

this document and those contained in Citigroup’s filings with the U.S. Securities and Exchange

Commission, including without limitation the “Risk Factors” section of Citigroup’s 2011 Form

10-K. Any forward-looking statements made by or on behalf of Citigroup speak only as to the

date they are made, and Citi does not undertake to update forward-looking statements to

reflect the impact of circumstances or events that arise after the date the forward-looking

statements were made.

27

John GerspachChief Financial Officer

February 12, 2013

Credit Suisse Financial Services Forum

28

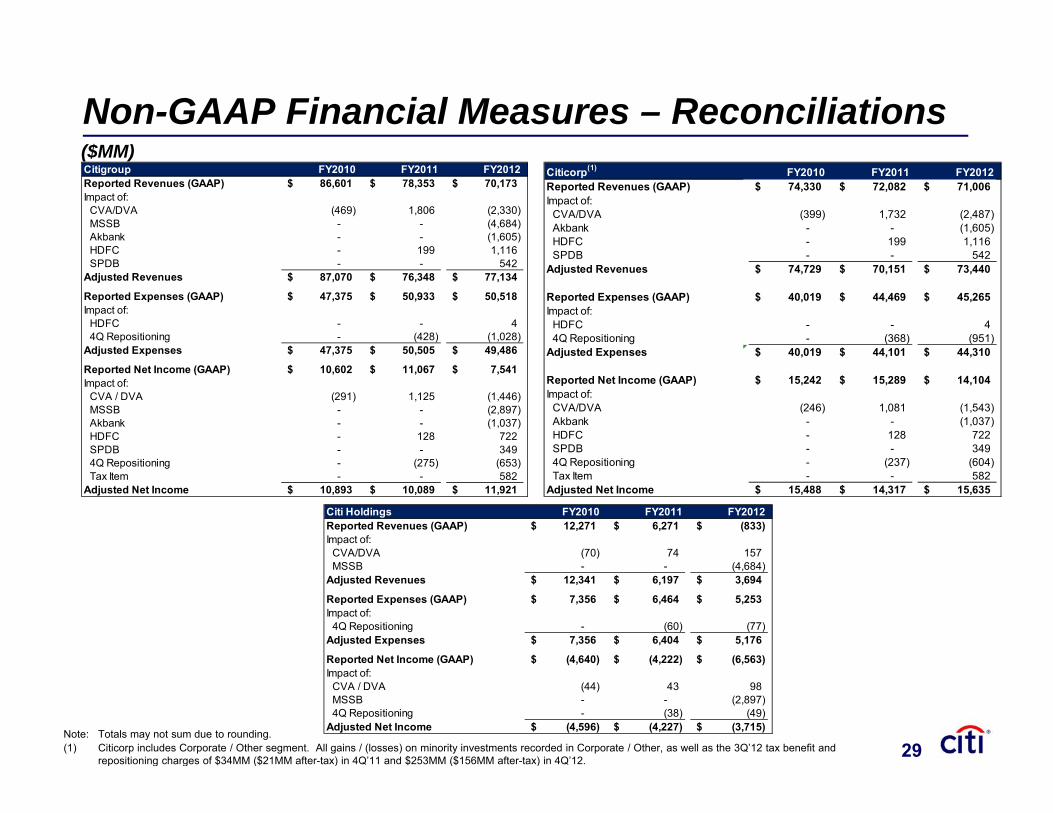

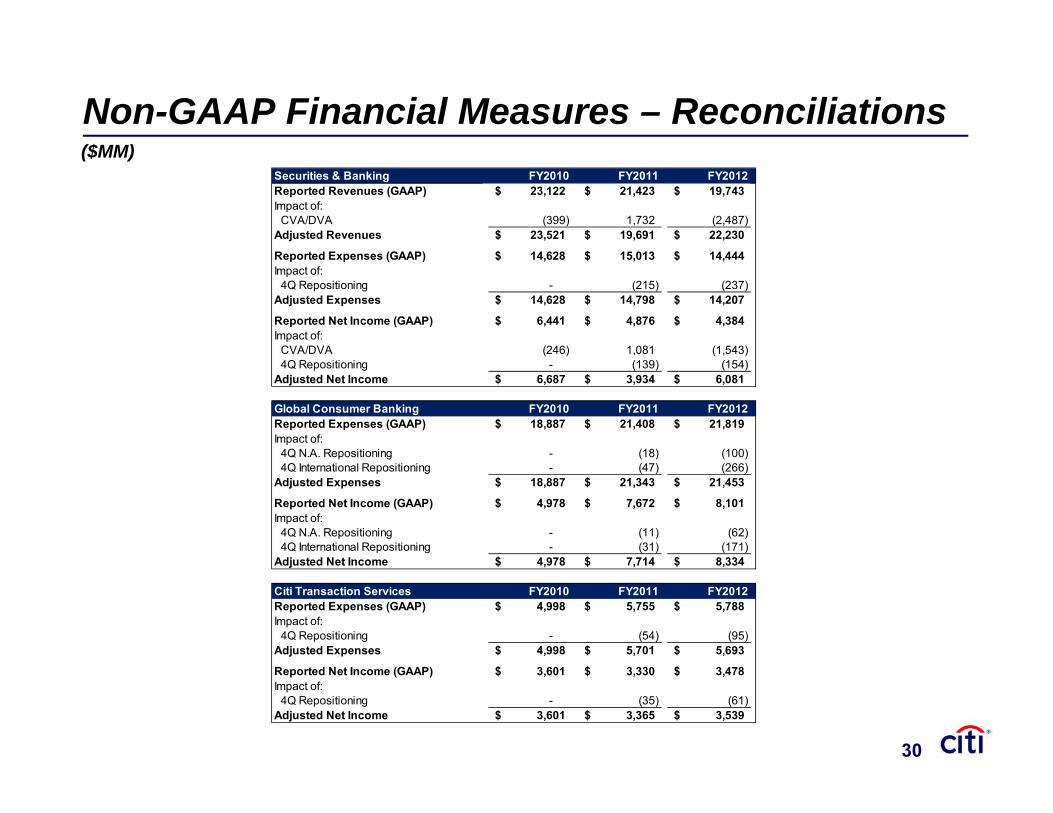

Non-GAAP Financial Measures – Reconciliations($MM)

Note: Totals may not sum due to rounding. (1) Citicorp includes Corporate / Other segment. All gains / (losses) on minority investments recorded in Corporate / Other, as well as the 3Q’12 tax benefit and

repositioning charges of $34MM ($21MM after-tax) in 4Q’11 and $253MM ($156MM after-tax) in 4Q’12.29

Citigroup FY2010 FY2011 FY2012Reported Revenues (GAAP) 86,601$ 78,353$ 70,173$ Impact of:

CVA/DVA (469) 1,806 (2,330) MSSB - - (4,684) Akbank - - (1,605) HDFC - 199 1,116 SPDB - - 542

Adjusted Revenues 87,070$ 76,348$ 77,134$

Reported Expenses (GAAP) 47,375$ 50,933$ 50,518$ Impact of:

HDFC - - 4 4Q Repositioning - (428) (1,028)

Adjusted Expenses 47,375$ 50,505$ 49,486$

Reported Net Income (GAAP) 10,602$ 11,067$ 7,541$ Impact of:

CVA / DVA (291) 1,125 (1,446) MSSB - - (2,897) Akbank - - (1,037) HDFC - 128 722 SPDB - - 349 4Q Repositioning - (275) (653) Tax Item - - 582

Adjusted Net Income 10,893$ 10,089$ 11,921$

Citicorp(1) FY2010 FY2011 FY2012Reported Revenues (GAAP) 74,330$ 72,082$ 71,006$ Impact of:

CVA/DVA (399) 1,732 (2,487) Akbank - - (1,605) HDFC - 199 1,116 SPDB - - 542

Adjusted Revenues 74,729$ 70,151$ 73,440$

Reported Expenses (GAAP) 40,019$ 44,469$ 45,265$ Impact of:

HDFC - - 4 4Q Repositioning - (368) (951)

Adjusted Expenses 40,019$ 44,101$ 44,310$

Reported Net Income (GAAP) 15,242$ 15,289$ 14,104$ Impact of:

CVA/DVA (246) 1,081 (1,543) Akbank - - (1,037) HDFC - 128 722 SPDB - - 349 4Q Repositioning - (237) (604) Tax Item - - 582

Adjusted Net Income 15,488$ 14,317$ 15,635$

Citi Holdings FY2010 FY2011 FY2012Reported Revenues (GAAP) 12,271$ 6,271$ (833)$ Impact of:

CVA/DVA (70) 74 157 MSSB - - (4,684)

Adjusted Revenues 12,341$ 6,197$ 3,694$

Reported Expenses (GAAP) 7,356$ 6,464$ 5,253$ Impact of:

4Q Repositioning - (60) (77) Adjusted Expenses 7,356$ 6,404$ 5,176$

Reported Net Income (GAAP) (4,640)$ (4,222)$ (6,563)$ Impact of:

CVA / DVA (44) 43 98 MSSB - - (2,897) 4Q Repositioning - (38) (49)

Adjusted Net Income (4,596)$ (4,227)$ (3,715)$

29

Non-GAAP Financial Measures – Reconciliations($MM)

30

Securities & Banking FY2010 FY2011 FY2012Reported Revenues (GAAP) 23,122$ 21,423$ 19,743$ Impact of:

CVA/DVA (399) 1,732 (2,487) Adjusted Revenues 23,521$ 19,691$ 22,230$

Reported Expenses (GAAP) 14,628$ 15,013$ 14,444$ Impact of:

4Q Repositioning - (215) (237) Adjusted Expenses 14,628$ 14,798$ 14,207$

Reported Net Income (GAAP) 6,441$ 4,876$ 4,384$ Impact of:

CVA/DVA (246) 1,081 (1,543) 4Q Repositioning - (139) (154)

Adjusted Net Income 6,687$ 3,934$ 6,081$

Global Consumer Banking FY2010 FY2011 FY2012Reported Expenses (GAAP) 18,887$ 21,408$ 21,819$ Impact of:

4Q N.A. Repositioning - (18) (100) 4Q International Repositioning - (47) (266)

Adjusted Expenses 18,887$ 21,343$ 21,453$

Reported Net Income (GAAP) 4,978$ 7,672$ 8,101$ Impact of:

4Q N.A. Repositioning - (11) (62) 4Q International Repositioning - (31) (171)

Adjusted Net Income 4,978$ 7,714$ 8,334$

Citi Transaction Services FY2010 FY2011 FY2012Reported Expenses (GAAP) 4,998$ 5,755$ 5,788$ Impact of:

4Q Repositioning - (54) (95) Adjusted Expenses 4,998$ 5,701$ 5,693$

Reported Net Income (GAAP) 3,601$ 3,330$ 3,478$ Impact of:

4Q Repositioning - (35) (61) Adjusted Net Income 3,601$ 3,365$ 3,539$

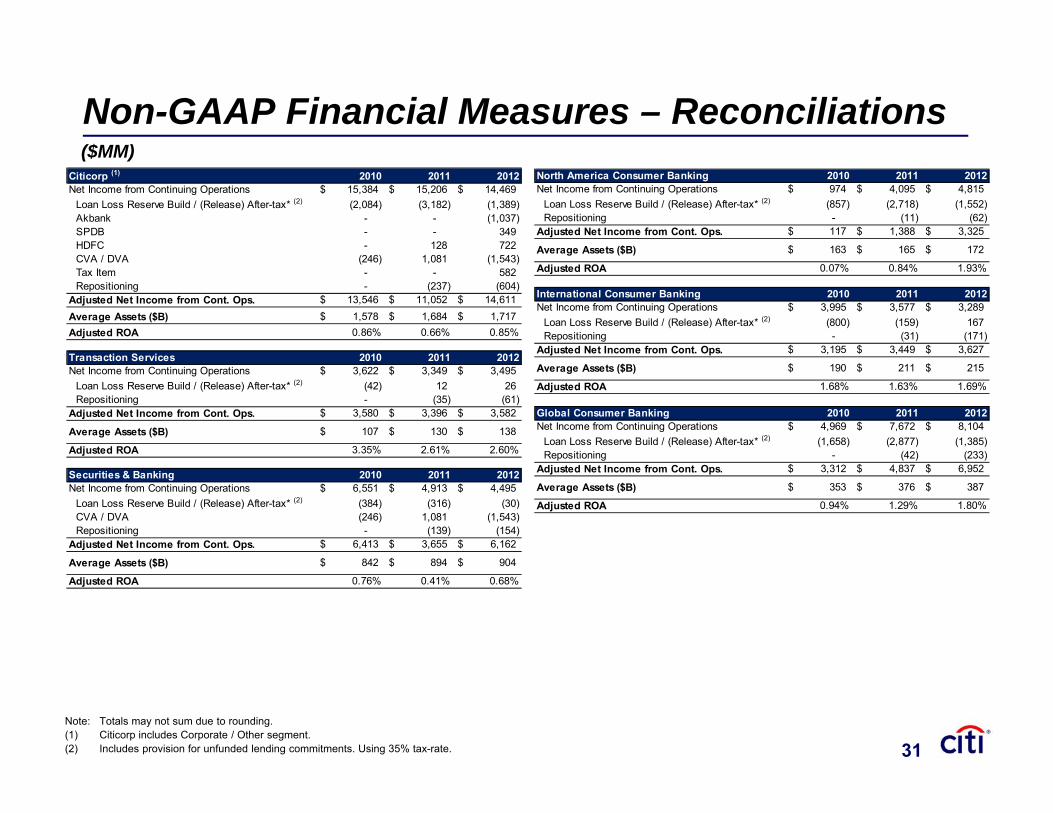

30Note: Totals may not sum due to rounding. (1) Citicorp includes Corporate / Other segment. (2) Includes provision for unfunded lending commitments. Using 35% tax-rate.

Non-GAAP Financial Measures – Reconciliations($MM)

North America Consumer Banking 2010 2011 2012Net Income from Continuing Operations 974$ 4,095$ 4,815$

Loan Loss Reserve Build / (Release) After-tax* (2) (857) (2,718) (1,552) Repositioning - (11) (62)

Adjusted Net Income from Cont. Ops. 117$ 1,388$ 3,325$

Average Assets ($B) 163$ 165$ 172$

Adjusted ROA 0.07% 0.84% 1.93%

International Consumer Banking 2010 2011 2012Net Income from Continuing Operations 3,995$ 3,577$ 3,289$

Loan Loss Reserve Build / (Release) After-tax* (2) (800) (159) 167 Repositioning - (31) (171)

Adjusted Net Income from Cont. Ops. 3,195$ 3,449$ 3,627$

Average Assets ($B) 190$ 211$ 215$

Adjusted ROA 1.68% 1.63% 1.69%

Global Consumer Banking 2010 2011 2012Net Income from Continuing Operations 4,969$ 7,672$ 8,104$

Loan Loss Reserve Build / (Release) After-tax* (2) (1,658) (2,877) (1,385) Repositioning - (42) (233)

Adjusted Net Income from Cont. Ops. 3,312$ 4,837$ 6,952$

Average Assets ($B) 353$ 376$ 387$

Adjusted ROA 0.94% 1.29% 1.80%

Citicorp (1) 2010 2011 2012Net Income from Continuing Operations 15,384$ 15,206$ 14,469$

Loan Loss Reserve Build / (Release) After-tax* (2) (2,084) (3,182) (1,389) Akbank - - (1,037) SPDB - - 349 HDFC - 128 722 CVA / DVA (246) 1,081 (1,543) Tax Item - - 582 Repositioning - (237) (604)

Adjusted Net Income from Cont. Ops. 13,546$ 11,052$ 14,611$ Average Assets ($B) 1,578$ 1,684$ 1,717$ Adjusted ROA 0.86% 0.66% 0.85%

Transaction Services 2010 2011 2012Net Income from Continuing Operations 3,622$ 3,349$ 3,495$

Loan Loss Reserve Build / (Release) After-tax* (2) (42) 12 26 Repositioning - (35) (61)

Adjusted Net Income from Cont. Ops. 3,580$ 3,396$ 3,582$

Average Assets ($B) 107$ 130$ 138$

Adjusted ROA 3.35% 2.61% 2.60%

Securities & Banking 2010 2011 2012Net Income from Continuing Operations 6,551$ 4,913$ 4,495$

Loan Loss Reserve Build / (Release) After-tax* (2) (384) (316) (30) CVA / DVA (246) 1,081 (1,543) Repositioning - (139) (154)

Adjusted Net Income from Cont. Ops. 6,413$ 3,655$ 6,162$

Average Assets ($B) 842$ 894$ 904$

Adjusted ROA 0.76% 0.41% 0.68%

31

31

Non-GAAP Financial Measures – Reconciliations($MM)

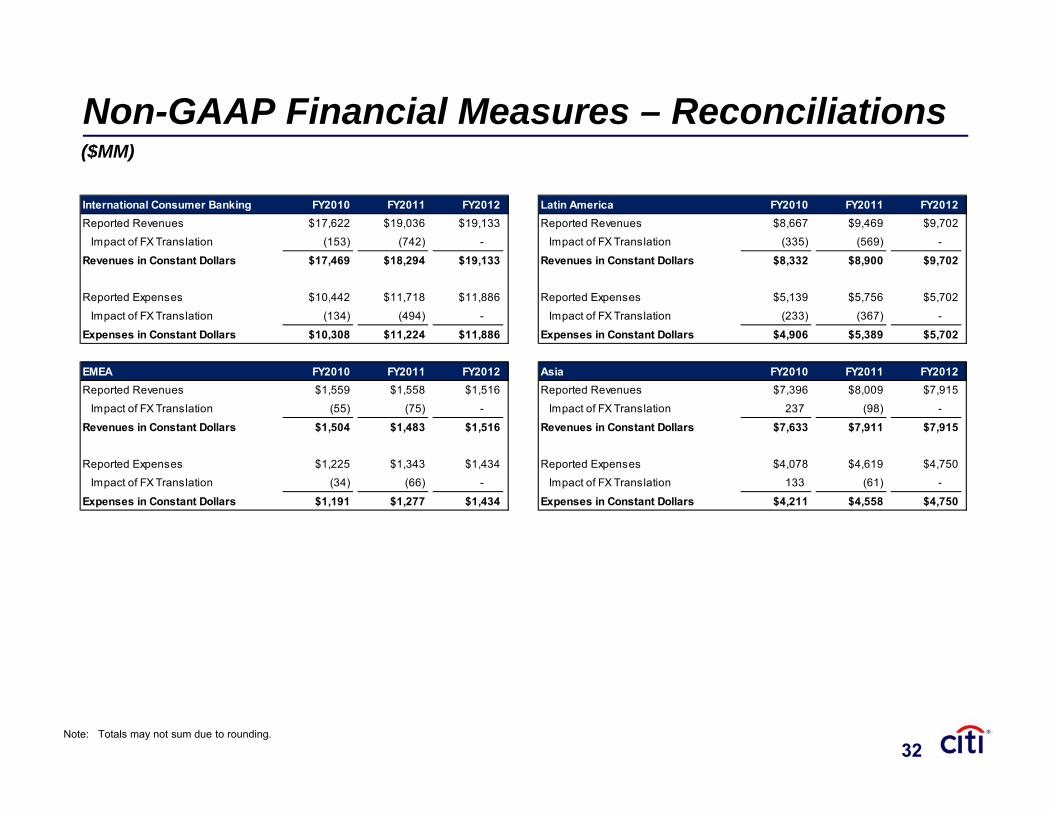

Note: Totals may not sum due to rounding.

Latin America FY2010 FY2011 FY2012Reported Revenues $8,667 $9,469 $9,702

Impact of FX Translation (335) (569) -

Revenues in Constant Dollars $8,332 $8,900 $9,702

Reported Expenses $5,139 $5,756 $5,702

Impact of FX Translation (233) (367) -

Expenses in Constant Dollars $4,906 $5,389 $5,702

Asia FY2010 FY2011 FY2012Reported Revenues $7,396 $8,009 $7,915

Impact of FX Translation 237 (98) -

Revenues in Constant Dollars $7,633 $7,911 $7,915

Reported Expenses $4,078 $4,619 $4,750

Impact of FX Translation 133 (61) -

Expenses in Constant Dollars $4,211 $4,558 $4,750

International Consumer Banking FY2010 FY2011 FY2012Reported Revenues $17,622 $19,036 $19,133

Impact of FX Translation (153) (742) -

Revenues in Constant Dollars $17,469 $18,294 $19,133

Reported Expenses $10,442 $11,718 $11,886

Impact of FX Translation (134) (494) -

Expenses in Constant Dollars $10,308 $11,224 $11,886

EMEA FY2010 FY2011 FY2012Reported Revenues $1,559 $1,558 $1,516

Impact of FX Translation (55) (75) -

Revenues in Constant Dollars $1,504 $1,483 $1,516

Reported Expenses $1,225 $1,343 $1,434

Impact of FX Translation (34) (66) -

Expenses in Constant Dollars $1,191 $1,277 $1,434

32

32

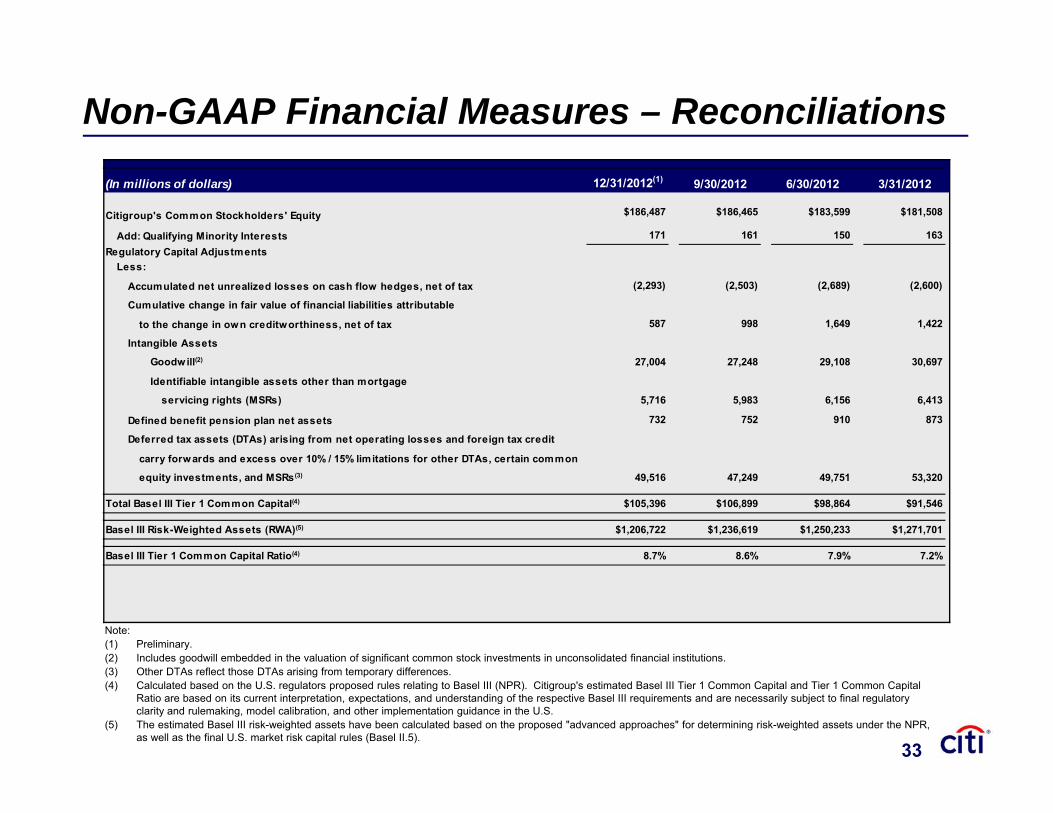

Note:(1) Preliminary.(2) Includes goodwill embedded in the valuation of significant common stock investments in unconsolidated financial institutions.(3) Other DTAs reflect those DTAs arising from temporary differences.(4) Calculated based on the U.S. regulators proposed rules relating to Basel III (NPR). Citigroup's estimated Basel III Tier 1 Common Capital and Tier 1 Common Capital

Ratio are based on its current interpretation, expectations, and understanding of the respective Basel III requirements and are necessarily subject to final regulatory clarity and rulemaking, model calibration, and other implementation guidance in the U.S.

(5) The estimated Basel III risk-weighted assets have been calculated based on the proposed "advanced approaches" for determining risk-weighted assets under the NPR, as well as the final U.S. market risk capital rules (Basel II.5).

Non-GAAP Financial Measures – Reconciliations

33

(In millions of dollars) 12/31/2012(1) 9/30/2012 6/30/2012 3/31/2012

Citigroup's Common Stockholders' Equity $186,487 $186,465 $183,599 $181,508

Add: Qualifying Minority Interests 171 161 150 163Regulatory Capital Adjustments

Less:

Accumulated net unrealized losses on cash flow hedges, net of tax (2,293) (2,503) (2,689) (2,600)

Cumulative change in fair value of financial liabilities attributable

to the change in own creditworthiness, net of tax 587 998 1,649 1,422

Intangible Assets

Goodwill(2) 27,004 27,248 29,108 30,697

Identifiable intangible assets other than mortgage

servicing rights (MSRs) 5,716 5,983 6,156 6,413

Defined benefit pension plan net assets 732 752 910 873

Deferred tax assets (DTAs) arising from net operating losses and foreign tax credit

carry forwards and excess over 10% / 15% limitations for other DTAs, certain common

equity investments, and MSRs(3) 49,516 47,249 49,751 53,320

Total Basel III Tier 1 Common Capital(4) $105,396 $106,899 $98,864 $91,546

Basel III Risk-Weighted Assets (RWA)(5) $1,206,722 $1,236,619 $1,250,233 $1,271,701

Basel III Tier 1 Common Capital Ratio(4) 8.7% 8.6% 7.9% 7.2%

33

($ millions, except per share amounts) 3Q'10 4Q'10 1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12

Citigroup's Total Stockholders' Equity $162,913 $163,468 $171,037 $176,364 $177,372 $177,806 $181,820 $183,911 $186,777 Less: Preferred Stock 312 312 312 312 312 312 312 312 312

Common Stockholders' Equity 162,601 163,156 170,725 176,052 177,060 177,494 181,508 183,599 186,465

Less: Goodwill 25,797 26,152 26,339 26,621 25,496 25,413 25,810 25,483 25,932

Intangible Assets (other than Mortgage Servicing Rights) 7,705 7,504 7,280 7,136 6,800 6,600 6,413 6,156 5,963

Goodwill and Intangible Assets - Recorded as Assets Held for Sale / Assets of Discont. Operations Held for Sale - - 165 - - - - - -

Net Deferred Tax Assets Related to Goodwill and Intangible Assets 59 56 53 50 47 44 41 38 35

Tangible Common Equity (TCE) $129,040 $129,444 $136,888 $142,245 $144,717 $145,437 $149,244 $151,922 $154,535Average Tangible Common Equity $125,169 $129,242 $133,166 $139,567 $143,481 $145,077 $147,341 $150,583 $154,535

Common Shares Outstanding at Quarter-end 2,905 2,906 2,921 2,918 2,924 2,924 2,932 2,933 2,933

Tangible Book Value Per Share $44.42 $44.55 $46.87 $48.75 $49.50 $49.74 $50.90 51.81$ 52.70$

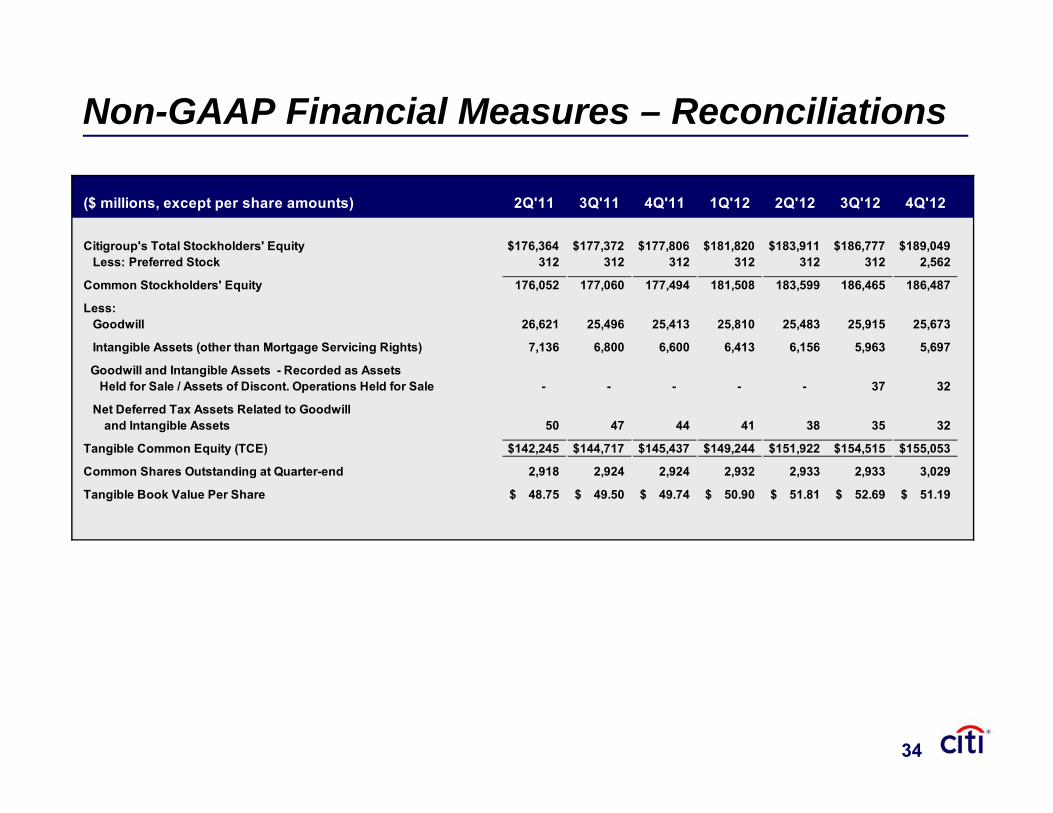

Non-GAAP Financial Measures – Reconciliations

34

($ millions, except per share amounts) 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12 4Q'12

Citigroup's Total Stockholders' Equity $176,364 $177,372 $177,806 $181,820 $183,911 $186,777 $189,049 Less: Preferred Stock 312 312 312 312 312 312 2,562

Common Stockholders' Equity 176,052 177,060 177,494 181,508 183,599 186,465 186,487

Less: Goodwill 26,621 25,496 25,413 25,810 25,483 25,915 25,673

Intangible Assets (other than Mortgage Servicing Rights) 7,136 6,800 6,600 6,413 6,156 5,963 5,697

Goodwill and Intangible Assets - Recorded as Assets Held for Sale / Assets of Discont. Operations Held for Sale - - - - - 37 32

Net Deferred Tax Assets Related to Goodwill and Intangible Assets 50 47 44 41 38 35 32

Tangible Common Equity (TCE) $142,245 $144,717 $145,437 $149,244 $151,922 $154,515 $155,053

Common Shares Outstanding at Quarter-end 2,918 2,924 2,924 2,932 2,933 2,933 3,029

Tangible Book Value Per Share 48.75$ 49.50$ 49.74$ 50.90$ 51.81$ 52.69$ 51.19$