Embed Size (px)

Citation preview

Credit Model Calibration –

Post-Basel II – Maximising

Data & Model Accuracy

RiskMinds - December 11, 2014

Amsterdam, Netherlands

Dr Scott D. Aguais, Managing Director

Aguais & Associates Ltd.

2Scott D. Aguais Aguais & Associates Ltd.

Presentation Overview

Key Presentation Points

1. Aggregate credit & default data to develop/calibrate wholesale credit models & support regulatory capital management remains problematic

2. Industry & regulators moving toward aggregate benchmarking given data limitations – AIRB vs ‘AERB’

3. PD models & benchmarks have tended to exhibit over-prediction or ‘conservatism’ in recent years

4. PDs & defaults also exhibit substantial, systematic variation across time –20% of this is predictable motivating Dual Ratings – PIT vs TTC

5. Model development objectives should always focus on developing the most accurate, unbiased predictions relative to observed realisations to support advanced risk management

6. Dual Ratings – support multiple objectives – required for IFRS9 & Stress Testing

3

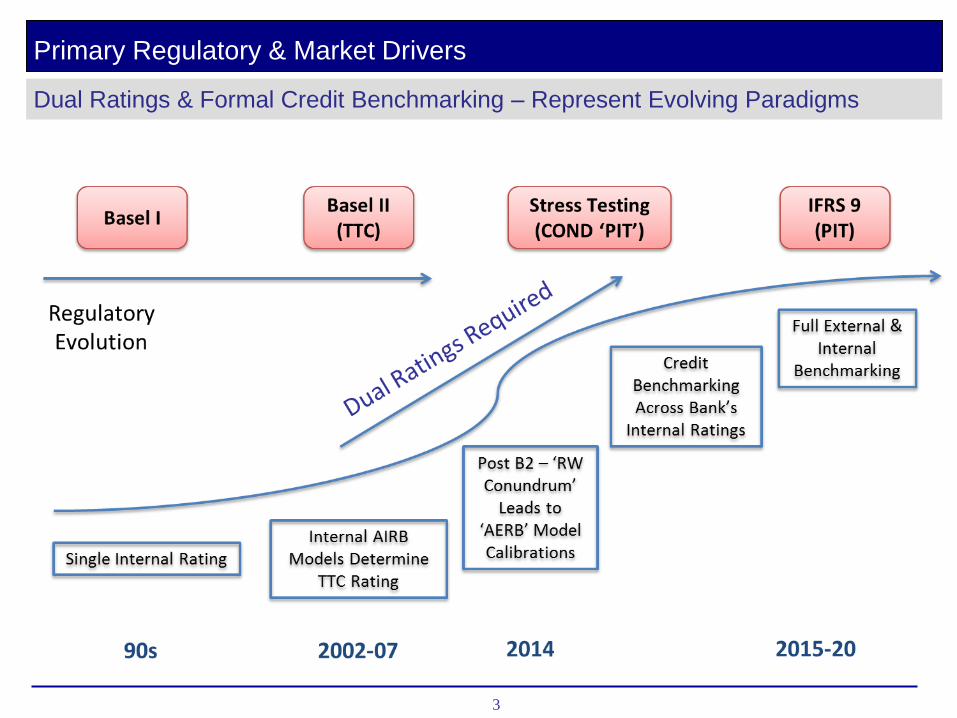

Primary Regulatory & Market Drivers

Dual Ratings & Formal Credit Benchmarking – Represent Evolving Paradigms

4Scott D. Aguais Aguais & Associates Ltd.

Last 25 Years - Credit Risk Data Initiatives & Sources

Use External Agency

Ratings & Default to

Develop Corp PD Models

‘AgencyReplication’

1990s

Credit Benchmark:Initiative to

collect & distribute Bank’s

AIRB PDs

2000s

Market-Based PD ModelsMKMV EDFs

2010 2015 +

PECDCLoan Loss Data Collection ‘By

Banks for Banks’Supports LGDBenchmarking

Credit Derivative MarketsPricing

Risk Neutral PD

AIRB Regulatory

BenchmarkingFSA HPEEBA/FRB

Etc

Basel IISubstantial

focus on collecting &

using Internal Credit Data for ‘Internal’ Model

Calibration

AERB

Dual Ratings & Formal Credit Benchmarking – Represent Evolving Paradigms

5Scott D. Aguais Aguais & Associates Ltd.

Focus on Wholesale PD Credit Model Development & Calibration

PDs can Vary Substantially….. Accurate Models Requires ‘Richer’ Models

• External ratings & PDs used extensively for benchmarking

• But defaults & Pds can vary by:

• Obligor type – corps vs FIs etc.

• Can be subject to ‘structural change’ & excessive ‘conservatism’ – asymmetric ‘penalty factors skew ratings toward ‘bot wanting to be too low’

• Vary systematically across time – PIT vs TTC views of PDs

6Scott D. Aguais Aguais & Associates Ltd.

Post Basel II Implementation – The ‘Risk-Weight Conundrum’

AIRB Model Calibration – Internal, Limited Model Calibration Data Falls Short

Risk Weight %1

75th Percentile

50th Percentile

25th Percentile

• Regulators are applying model constraints to create comparable risk measures

• Outlying banks need accurate benchmarking to reach the ‘level playing field’ & ‘manage’ regulatory compliance

Bank A

Bank B

Bank C

Bank D

1 Risk Weight is a function of the Client PD & transaction LGD and Maturity

✓

✗✗

✗

CFO requires lower risk weights

Regulator requires higher risk weights

RWs Vary Widely – Under ‘AERB’ - Some Banks Gain, Some Lose

7Scott D. Aguais Aguais & Associates Ltd.

Agency Default Rates Vary by Obligor Type – Use of Different Underlying Curves

An ‘A’ is not an ‘A’ is not an ‘A’…..

• Models can replicate alphabet ratings by calibrating to agency default rates –which are different for different obligor types !

• ‘Regulatory friendly’ given 20 year time series = ‘long run’

• But most banks calibrate PD models to a single global curve

Implied1yr PD

100%

AAA AA+ AA AA- A+ A A- BBB+ BBB BBB- BB+ BB BB- B+ B B- CCC+ CCC CCC- CC+ CC CC- D

Non Bank FIsBanks Corporates

Sovereigns

Observed Defaults Vary Across Obligor Types

8

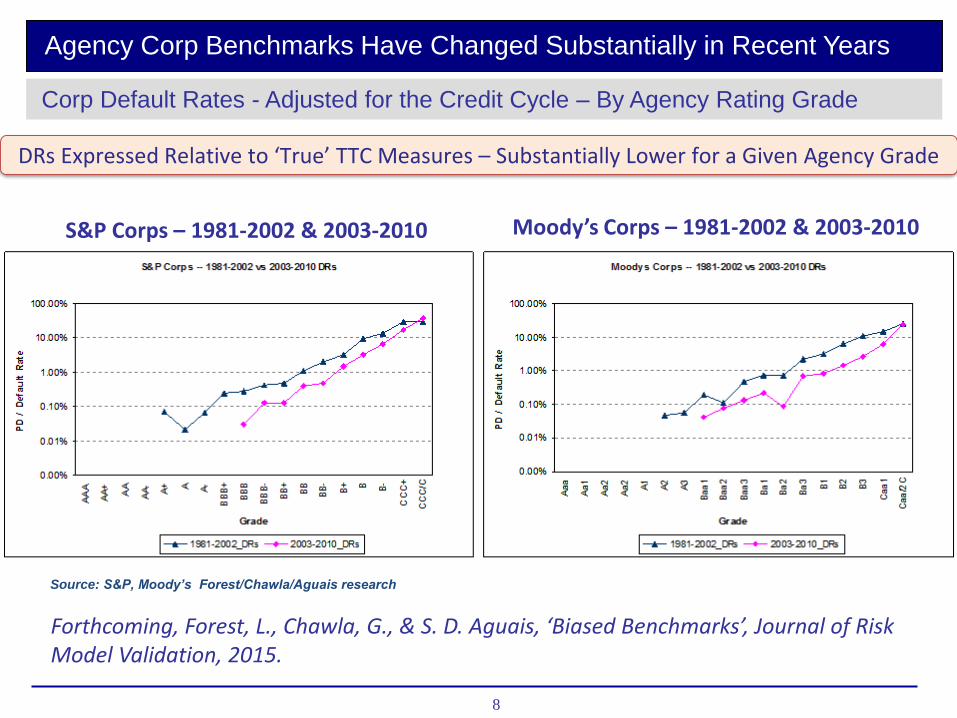

Agency Corp Benchmarks Have Changed Substantially in Recent Years

DRs Expressed Relative to ‘True’ TTC Measures – Substantially Lower for a Given Agency Grade

S&P Corps – 1981-2002 & 2003-2010

Corp Default Rates - Adjusted for the Credit Cycle – By Agency Rating Grade

Moody’s Corps – 1981-2002 & 2003-2010

Forthcoming, Forest, L., Chawla, G., & S. D. Aguais, ‘Biased Benchmarks’, Journal of Risk Model Validation, 2015.

Source: S&P, Moody’s Forest/Chawla/Aguais research

9Scott D. Aguais Aguais & Associates Ltd.

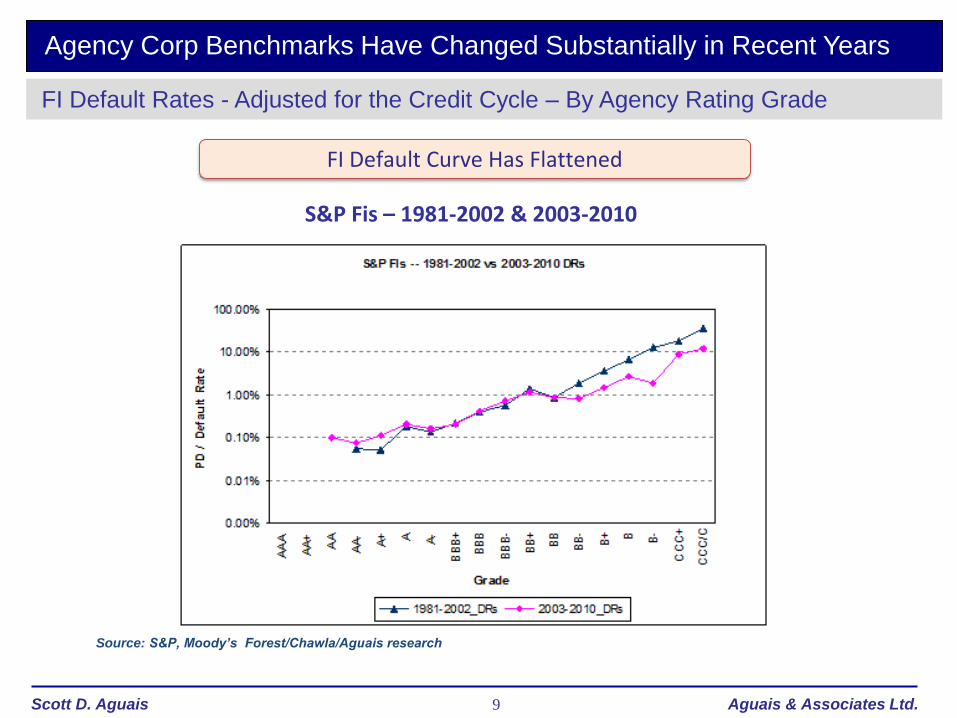

S&P Fis – 1981-2002 & 2003-2010

Agency Corp Benchmarks Have Changed Substantially in Recent Years

FI Default Rates - Adjusted for the Credit Cycle – By Agency Rating Grade

FI Default Curve Has Flattened

Source: S&P, Moody’s Forest/Chawla/Aguais research

10Scott D. Aguais Aguais & Associates Ltd.

Dual Ratings Required for Key Regulatory Objectives – IFRS9 & Stress Testing

‘Point‐in‐time risk parameters (PDpit and LGDpit) should be forward looking projections of default rates and loss rates and capture current trends in the business cycle. In contrast to through‐the‐cycle parameters they should not be business cycle neutral. PDpit and LGDpit should be used for all credit risk related calculations except RWA under both, the baseline and the adverse scenario. Contrary to regulatory parameters, they are required for all portfolios, including STA and F‐IRB.’

EBA – ‘Methodology EU-wide Stress Test 2014’Version 1.8, 3 March 2014, P 26

Dual Ratings – PIT vs TTC Measures are Required

11

Dual Ratings – PIT vs TTC Measures are Required

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

Z-G

ap

NA Corp Z Credit

Index

Legacy Credit

Models

Predicted by Credit-

Cycle Model

Legacy Credit

Models

Predicted by Credit-

Cycle model

Legacy Credit

Models

1990 20091998 1999 2001 2002 2007 2011-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

Z-G

ap

NA Corp Z Credit

Index

Legacy Credit

Models

Predicted by Credit-

Cycle Model

Legacy Credit

Models

Predicted by Credit-

Cycle model

Legacy Credit

Models

Predicted by Credit-

Cycle model

Legacy Credit

Models

1990 20091998 1999 2001 2002 2007 20111990 20091998 1999 2001 2002 2007 2011

Source: Moody’s KMV,

Current Credit Models Are Blind to Credit Cycles – 20% Prediction is Therefore Powerful

A Systematic Component of Credit Cycles is Predicable – By Industry & Region

12

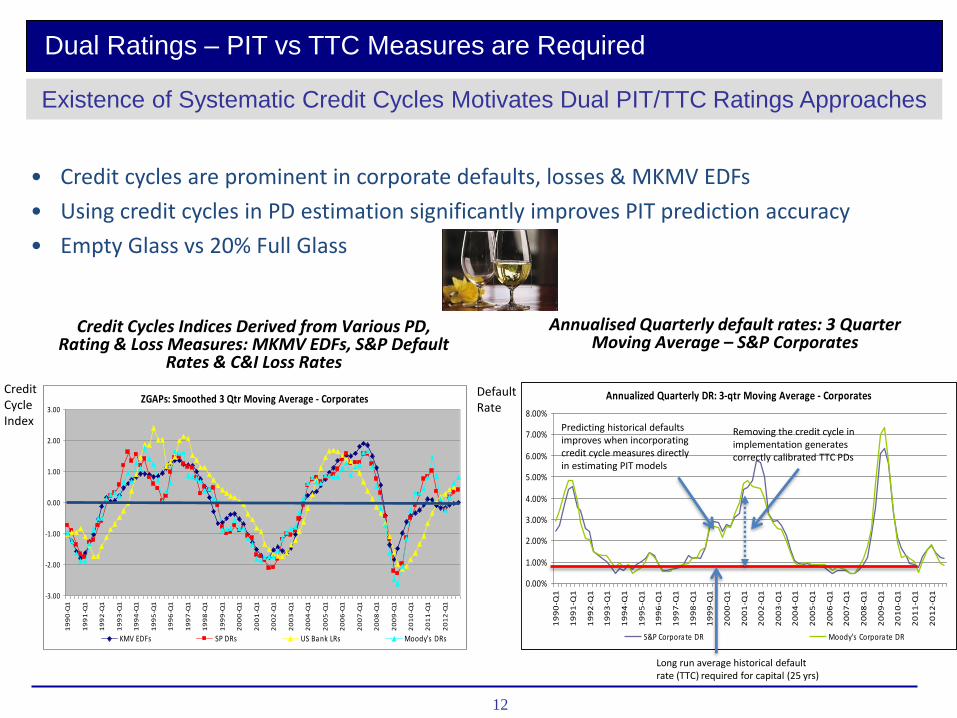

Existence of Systematic Credit Cycles Motivates Dual PIT/TTC Ratings Approaches

• Credit cycles are prominent in corporate defaults, losses & MKMV EDFs

• Using credit cycles in PD estimation significantly improves PIT prediction accuracy

• Empty Glass vs 20% Full Glass

ZGAPs: Smoothed 3 Qtr Moving Average - Corporates

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

19

90

-Q1

19

91

-Q1

19

92

-Q1

19

93

-Q1

19

94

-Q1

19

95

-Q1

19

96

-Q1

19

97

-Q1

19

98

-Q1

19

99

-Q1

20

00

-Q1

20

01

-Q1

20

02

-Q1

20

03

-Q1

20

04

-Q1

20

05

-Q1

20

06

-Q1

20

07

-Q1

20

08

-Q1

20

09

-Q1

20

10

-Q1

20

11

-Q1

20

12

-Q1

KMV EDFs SP DRs US Bank LRs Moody's DRs

Credit Cycles Indices Derived from Various PD, Rating & Loss Measures: MKMV EDFs, S&P Default

Rates & C&I Loss Rates

Annualised Quarterly default rates: 3 Quarter Moving Average – S&P Corporates

Annualized Quarterly DR: 3-qtr Moving Average - Corporates

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

19

90

-Q1

19

91

-Q1

19

92

-Q1

19

93

-Q1

19

94

-Q1

19

95

-Q1

19

96

-Q1

19

97

-Q1

19

98

-Q1

19

99

-Q1

20

00

-Q1

20

01

-Q1

20

02

-Q1

20

03

-Q1

20

04

-Q1

20

05

-Q1

20

06

-Q1

20

07

-Q1

20

08

-Q1

20

09

-Q1

20

10

-Q1

20

11

-Q1

20

12

-Q1

S&P Corporate DR Moody's Corporate DR

Default Rate

Predicting historical defaults improves when incorporating credit cycle measures directly in estimating PIT models

Removing the credit cycle in implementation generates correctly calibrated TTC PDs

Long run average historical default rate (TTC) required for capital (25 yrs)

CreditCycleIndex

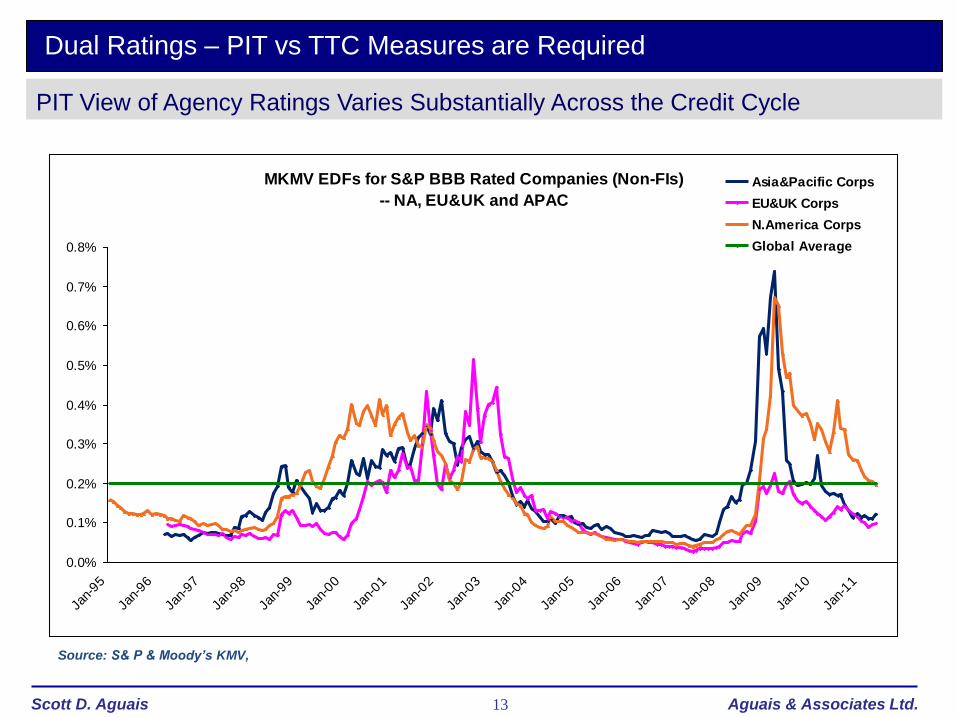

Dual Ratings – PIT vs TTC Measures are Required

13Scott D. Aguais Aguais & Associates Ltd.

PIT View of Agency Ratings Varies Substantially Across the Credit Cycle

MKMV EDFs for S&P BBB Rated Companies (Non-FIs)

-- NA, EU&UK and APAC

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Asia&Pacific Corps

EU&UK Corps

N.America Corps

Global Average

Dual Ratings – PIT vs TTC Measures are Required

Source: S& P & Moody’s KMV,

14

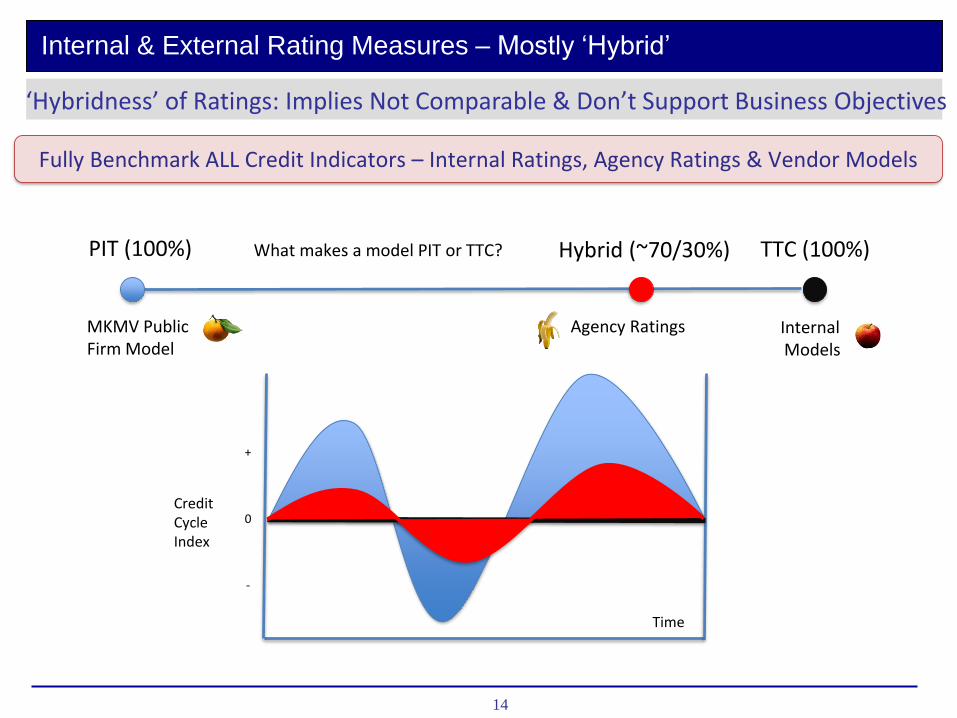

Internal & External Rating Measures – Mostly ‘Hybrid’

‘Hybridness’ of Ratings: Implies Not Comparable & Don’t Support Business Objectives

Time

CreditCycleIndex

0

+

-

PIT (100%)

Internal Models

TTC (100%)Hybrid (~70/30%)

Agency RatingsMKMV Public Firm Model

What makes a model PIT or TTC?

Fully Benchmark ALL Credit Indicators – Internal Ratings, Agency Ratings & Vendor Models

15

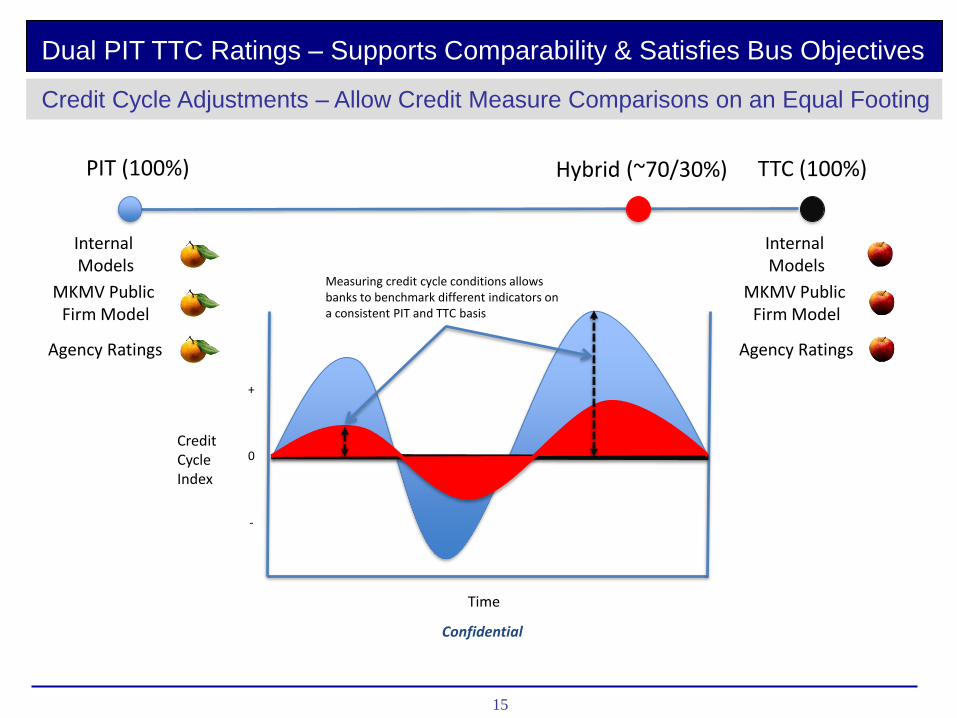

Dual PIT TTC Ratings – Supports Comparability & Satisfies Bus Objectives

Credit Cycle Adjustments – Allow Credit Measure Comparisons on an Equal Footing

Time

CreditCycleIndex

PIT (100%)

Internal Models

Agency Ratings

MKMV Public Firm Model

TTC (100%)Hybrid (~70/30%)

Measuring credit cycle conditions allows banks to benchmark different indicators on a consistent PIT and TTC basis

0

+

-

Internal Models

Agency Ratings

MKMV Public Firm Model

Confidential

16

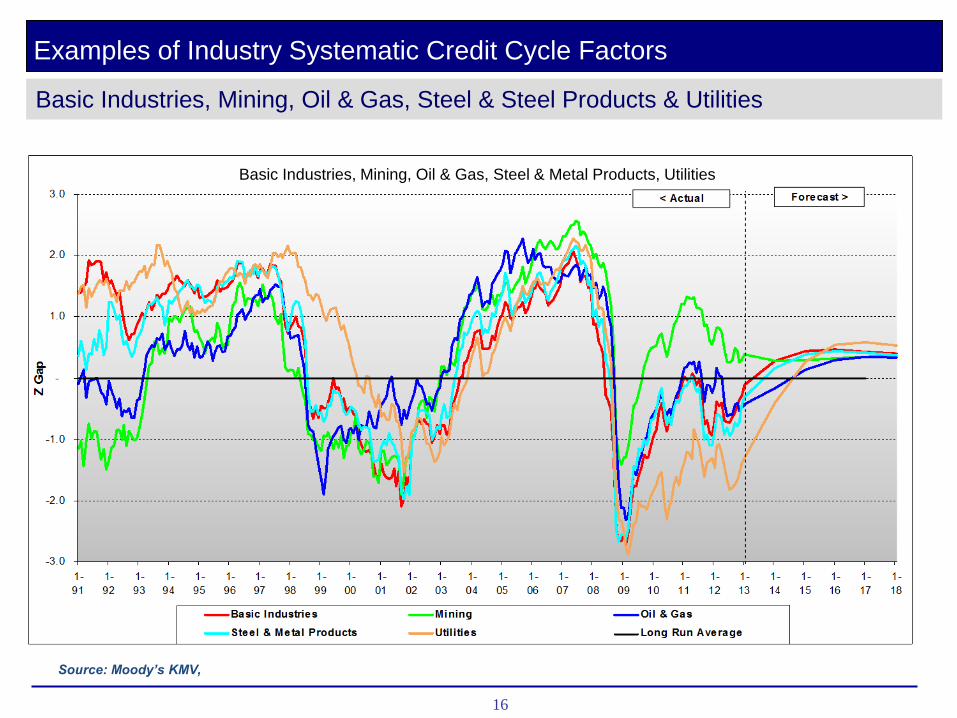

Examples of Industry Systematic Credit Cycle Factors

Basic Industries, Mining, Oil & Gas, Steel & Steel Products & Utilities

Basic Industries, Mining, Oil & Gas, Steel & Metal Products, Utilities

Source: Moody’s KMV,

17

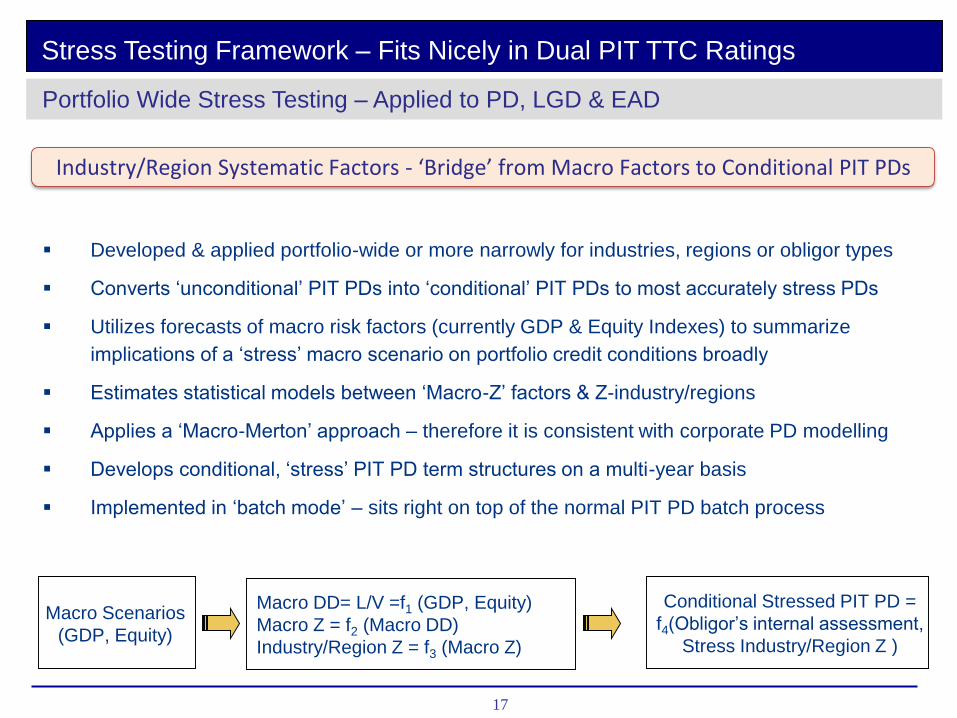

Portfolio Wide Stress Testing – Applied to PD, LGD & EAD

Stress Testing Framework – Fits Nicely in Dual PIT TTC Ratings

Conditional Stressed PIT PD =

f4(Obligor’s internal assessment,

Stress Industry/Region Z )

Macro DD= L/V =f1 (GDP, Equity)

Macro Z = f2 (Macro DD)

Industry/Region Z = f3 (Macro Z)

Macro Scenarios

(GDP, Equity)

Industry/Region Systematic Factors - ‘Bridge’ from Macro Factors to Conditional PIT PDs

Developed & applied portfolio-wide or more narrowly for industries, regions or obligor types

Converts ‘unconditional’ PIT PDs into ‘conditional’ PIT PDs to most accurately stress PDs

Utilizes forecasts of macro risk factors (currently GDP & Equity Indexes) to summarize

implications of a ‘stress’ macro scenario on portfolio credit conditions broadly

Estimates statistical models between ‘Macro-Z’ factors & Z-industry/regions

Applies a ‘Macro-Merton’ approach – therefore it is consistent with corporate PD modelling

Develops conditional, ‘stress’ PIT PD term structures on a multi-year basis

Implemented in ‘batch mode’ – sits right on top of the normal PIT PD batch process

18Scott D. Aguais Aguais & Associates Ltd.

History & Stress Simulation for UK Macro ‘Z’ – Two Different Stress Scenarios

Stress Testing Framework – Fits Nicely in Dual PIT TTC Ratings

Portfolio Stress Tests – Conditional ‘Stress’ PIT Measures – Macro/Industry/Regions/Obligors

19Scott D. Aguais Aguais & Associates Ltd.

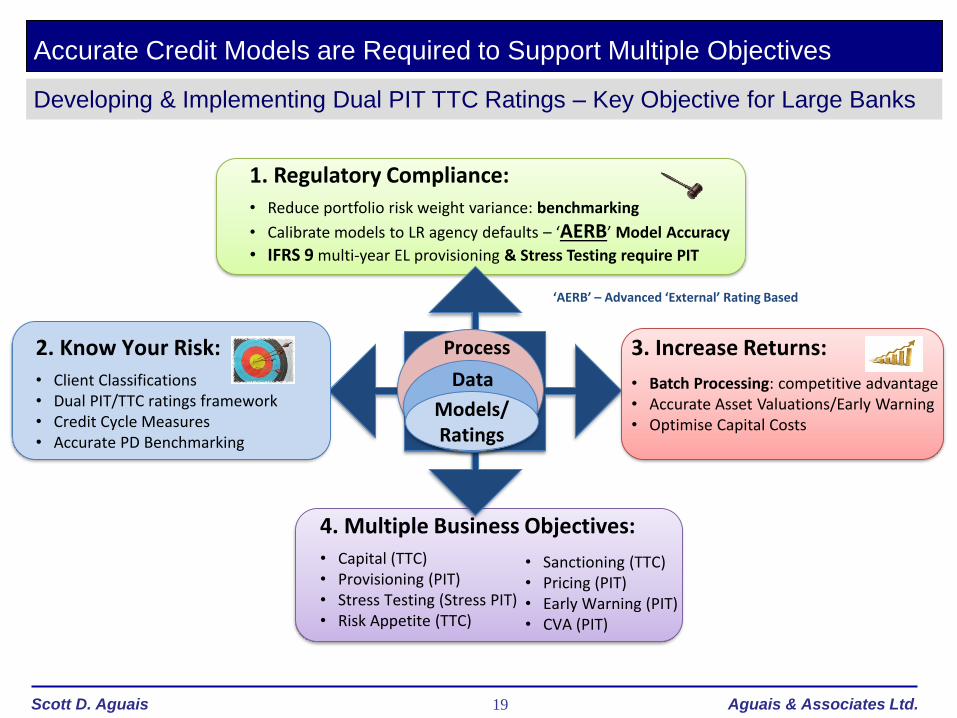

Accurate Credit Models are Required to Support Multiple Objectives

Developing & Implementing Dual PIT TTC Ratings – Key Objective for Large Banks

4. Multiple Business Objectives:

• Capital (TTC)• Provisioning (PIT)• Stress Testing (Stress PIT)• Risk Appetite (TTC)

• Sanctioning (TTC)• Pricing (PIT)• Early Warning (PIT)• CVA (PIT)

Models/Ratings

Data

Process

1. Regulatory Compliance:

• Reduce portfolio risk weight variance: benchmarking

• Calibrate models to LR agency defaults – ‘AERB’ Model Accuracy

• IFRS 9 multi-year EL provisioning & Stress Testing require PIT

3. Increase Returns:

• Batch Processing: competitive advantage• Accurate Asset Valuations/Early Warning• Optimise Capital Costs

2. Know Your Risk:

• Client Classifications• Dual PIT/TTC ratings framework• Credit Cycle Measures• Accurate PD Benchmarking

‘AERB’ – Advanced ‘External’ Rating Based

20Scott D. Aguais Aguais & Associates Ltd.

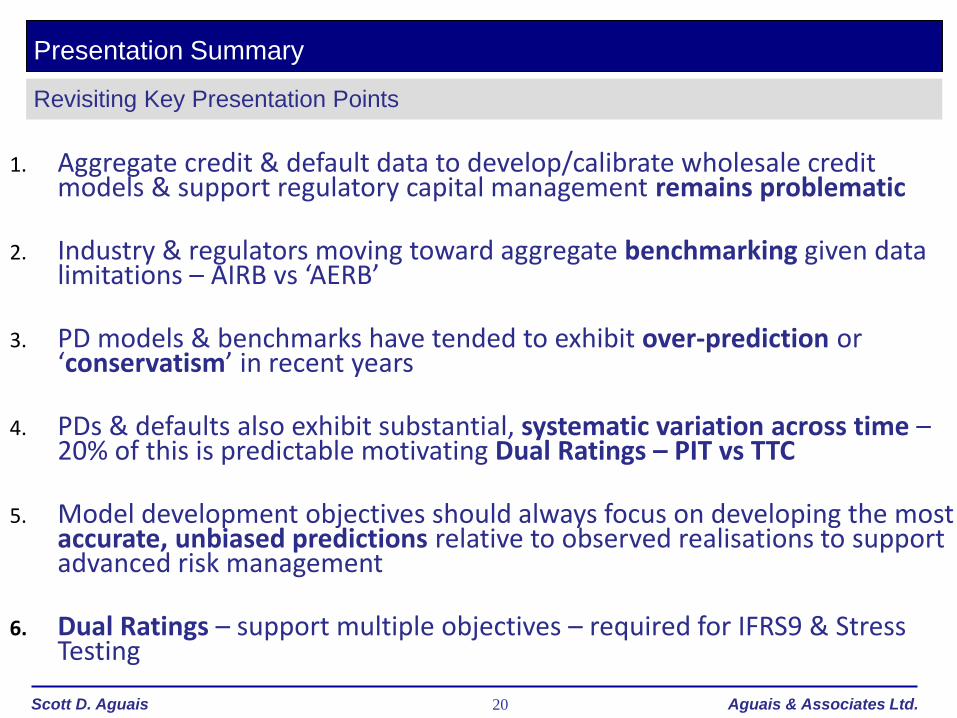

Presentation Summary

Revisiting Key Presentation Points

1. Aggregate credit & default data to develop/calibrate wholesale credit models & support regulatory capital management remains problematic

2. Industry & regulators moving toward aggregate benchmarking given data limitations – AIRB vs ‘AERB’

3. PD models & benchmarks have tended to exhibit over-prediction or ‘conservatism’ in recent years

4. PDs & defaults also exhibit substantial, systematic variation across time –20% of this is predictable motivating Dual Ratings – PIT vs TTC

5. Model development objectives should always focus on developing the most accurate, unbiased predictions relative to observed realisations to support advanced risk management

6. Dual Ratings – support multiple objectives – required for IFRS9 & Stress Testing