Embed Size (px)

Citation preview

Credit investorpresentationAugust 2017

© Metso© Metso2

IMPORTANT: You must read the following before continuing. The following applies to this document, the oral presentation of the information in this document by Metso Corporation (the “Company”) or any person on behalf of the Company, and

any question-and-answer session that follows the oral presentation (collectively, the “Information”). In accessing the Information, you agree to be bound by the following terms and conditions.

The Information may not be reproduced, redistributed, published or passed on to any other person, directly or indirectly, in whole or in part, for any purpose. If this document has been received in error, it must be returned immediately to the

Company. The Information is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of, or located in, any locality, state, country or other jurisdiction where such distribution or use would be

contrary to law or regulation or which would require any registration or licensing within such jurisdiction. The Information is not for publication, release or distribution in the United States, the United Kingdom, Japan or in any other jurisdiction in

which offers or sales would be prohibited by applicable law.

This document and its contents may not be viewed by persons within the United States or “U.S. Persons” (as defined in Regulation S under the Securities Act of 1933, as amended (the “Securities Act”)). The offer and sale of the securities

referred to herein (the “Securities”) has not been registered under the Securities Act and the Securities may not be offered or sold in the United States or to U.S. persons unless so registered, or an exemption from the registration requirements

of the Securities Act is available. The Company does not intend to register any portion of the offering of the Securities in the United States or to conduct a public offering of the Securities in the United States. By accessing the Information, you

represent that you are a non-U.S. person that is outside the United States.

The Information is directed solely at: (i) persons outside the United Kingdom, (ii) investment professionals specified in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 as amended (the “Order”), (iii)

high net worth entities, and other persons to whom it may lawfully be communicated, falling within Article 49(2)(a) to (d) of the Order and (iv) persons to whom an invitation or inducement to engage in investment activity (within the meaning of

section 21 of the Financial Services and Markets Act 2000) in connection with the issue or sale of any securities of the Company or any member of its group may otherwise lawfully be communicated or caused to be communicated (all such

persons together being referred to as “Relevant Persons”). Any investment activity to which the Information relates will only be available to and will only be engaged in with Relevant Persons. Any person who is not a Relevant Person should

not act or rely on the Information. By accessing the Information, you represent that you are a Relevant Person.

The Information and the offering of the Securities are only addressed to and directed at persons in member states of the European Economic Area (the “EEA”), who are “Qualified Investors” within the meaning of Article 2(1)(e) of the Prospectus

Directive. The Securities are only available to, and any invitation, offer or agreement to subscribe, purchase or otherwise acquire the Securities will be engaged in only with Qualified Investors. The Information should not be acted upon or relied

upon in any member state of the EEA by persons who are not Qualified Investors. For the purposes of this provision the expression “Prospectus Directive” means Directive 2003/71/EC (and amendments thereto, including the 2010 PD

Amending Directive, to the extent implemented in the Relevant Member State), and includes any relevant implementing measure in the Relevant Member State and the expression “2010 PD Amending Directive” means Directive 2010/73/EU.

The Securities have not been and will not be registered under the Financial Instruments and Exchange Act of Japan (Act No. 25 of 1948), as amended (the “FIEA”). Accordingly, the Information may not be distributed and the Securities may not

be offered or sold, directly or indirectly, in Japan or to, or for the benefit of, a resident of Japan (which term as used herein means any person resident in Japan, including any corporation or other entity organized under the laws of Japan) or to

others for re-offering or resale, directly or indirectly, in Japan or to, or for the benefit of, any resident in Japan, except pursuant to an exemption from the registration requirements of, and otherwise in compliance with, FIEA and other relevant

laws and regulations of Japan.

The Information does not constitute or form part of, and should not be construed as an offer or the solicitation of an offer to subscribe for or purchase any securities of the Company, and nothing contained therein shall form the basis of or be

relied on in connection with any contract or commitment whatsoever, nor does it constitute a recommendation regarding any securities of the Company. Prospective investors are required to make their own independent investigations and

appraisals of the business and financial condition of the Company and the nature of the Securities before taking any investment decision with respect to the Securities.

The Information has been prepared by the Company. Nordea Bank AB (publ), Citigroup Global Markets Limited, Danske Bank A/S and OP Corporate Bank plc (together, the “Co-Dealer Managers”, and together with the Dealer Managers, the

“Dealer Managers”) acting in connection with the offering of the Securities are acting exclusively for the Company and no one else, and will not be responsible for providing advice in connection with the Information to any other party. Subject to

applicable law, none of the Dealer Managers accepts any responsibility whatsoever and makes no representation or warranty, express or implied, for the contents of the Information, including its accuracy, completeness or verification or for any

other statement made or purported to be made in connection with the Company and nothing in this document or at this presentation shall be relied upon as a promise or representation in this respect, whether as to the past or the future. The

Dealer Managers accordingly disclaim all and any liability whatsoever, whether arising in tort, contract or otherwise (save as referred above) which any of them might otherwise have in respect of the Information or any such statement.

The Information contains forward-looking statements. All statements other than statements of historical fact included in the Information are forward-looking statements. Forward-looking statements give the Company’s current expectations and

projections relating to its financial condition, results of operations, plans, objectives, future performance and business. These statements may include, without limitation, any statements preceded by, followed by or including words such as

“target,” “believe,” “expect,” “aim,” “intend,” “may,” “anticipate,” “estimate,” “plan,” “project,” “will,” “can have,” “likely,” “should,” “would,” “could” and other words and terms of similar meaning or the negative thereof. Such forward-looking

statements involve known and unknown risks, uncertainties and other important factors beyond the Company’s control that could cause the Company’s actual results, performance or achievements to be materially different from the expected

results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company’s present and future business strategies and the

environment in which it will operate in the future.

No representation, warranty or undertaking, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the Information or the opinions contained therein. The Information has

not been independently verified and will not be updated. The Information, including but not limited to forward-looking statements, applies only as of the date of this document and is not intended to give any assurances as to future results. The

Company expressly disclaims any obligation or undertaking to disseminate any updates or revisions to the Information, including any financial data or forward-looking statements, and will not publicly release any revisions it may make to the

Information that may result from any change in the Company’s expectations, any change in events, conditions or circumstances on which these forward-looking statements are based, or other events or circumstances arising after the date of

this document. Market data used in the Information not attributed to a specific source are estimates of the Company and has not been independently verified.

Disclaimer

© Metso© Metso

1. Metso in brief & operating environment

2. Business review

3. Financial review

4. Credit rating & financing

Contents

3

© Metso© Metso

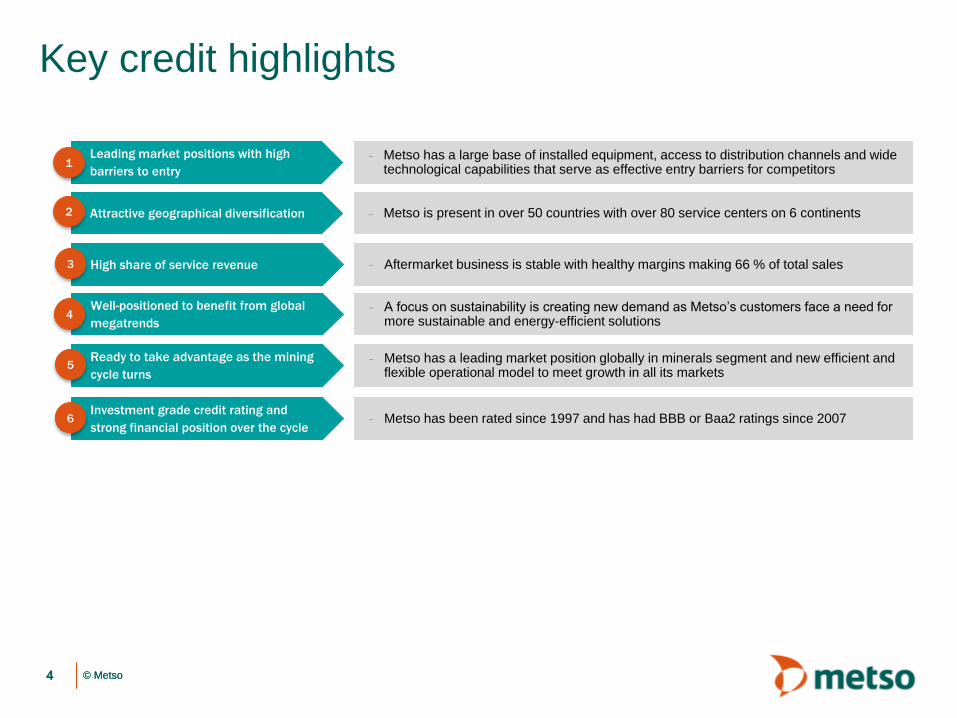

Key credit highlights

4

1

2

Attractive geographical diversification – Metso is present in over 50 countries with over 80 service centers on 6 continents

Well-positioned to benefit from global

megatrends

– A focus on sustainability is creating new demand as Metso’s customers face a need formore sustainable and energy-efficient solutions

– Metso has a large base of installed equipment, access to distribution channels and widetechnological capabilities that serve as effective entry barriers for competitors

Leading market positions with high

barriers to entry

– Metso has been rated since 1997 and has had BBB or Baa2 ratings since 2007Investment grade credit rating and

strong financial position over the cycle

1

6

2

4

Ready to take advantage as the mining

cycle turns

– Metso has a leading market position globally in minerals segment and new efficient andflexible operational model to meet growth in all its markets

5

High share of service revenue – Aftermarket business is stable with healthy margins making 66 % of total sales3

© Metso© Metso

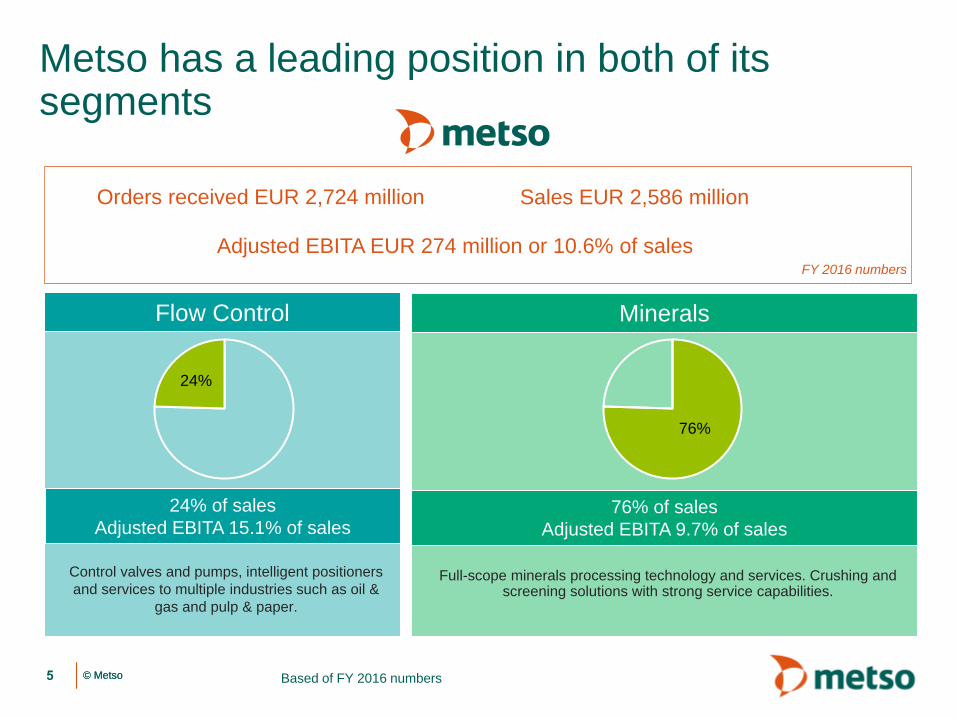

Full-scope minerals processing technology and services. Crushing and screening solutions with strong service capabilities.

Control valves and pumps, intelligent positioners

and services to multiple industries such as oil &

gas and pulp & paper.

Metso has a leading position in both of its segments

Sales EUR 2,586 millionOrders received EUR 2,724 million

Adjusted EBITA EUR 274 million or 10.6% of sales

Based of FY 2016 numbers5

24%

Flow Control Minerals

24% of sales

Adjusted EBITA 15.1% of sales76% of sales

Adjusted EBITA 9.7% of sales

FY 2016 numbers

76%

© Metso© Metso

We are well-positioned in all our customerindustriesOur offering covers services, products and systems for our customer industries

6

Services

Segment Share of orders received Share of order backlog Business drivers

• Declining ore grades require more ore to be

processed

• Increasing demand for sustainable and

energy-efficient solutions

• Increasing demand for digital solutions and

new technologies

• Demand for energy and changes in energy

mix

• Modernization investments

• Drive for more cost-efficient solutions

• New production technologies

• Demand for process safety and uptime

• Increasing focus on sustainability

78%

Minerals

Source: Metso Financial Statements 2016

22%

Flow Control

82%

18%

• Construction industry investments

• Need for total cost-per-ton solutions

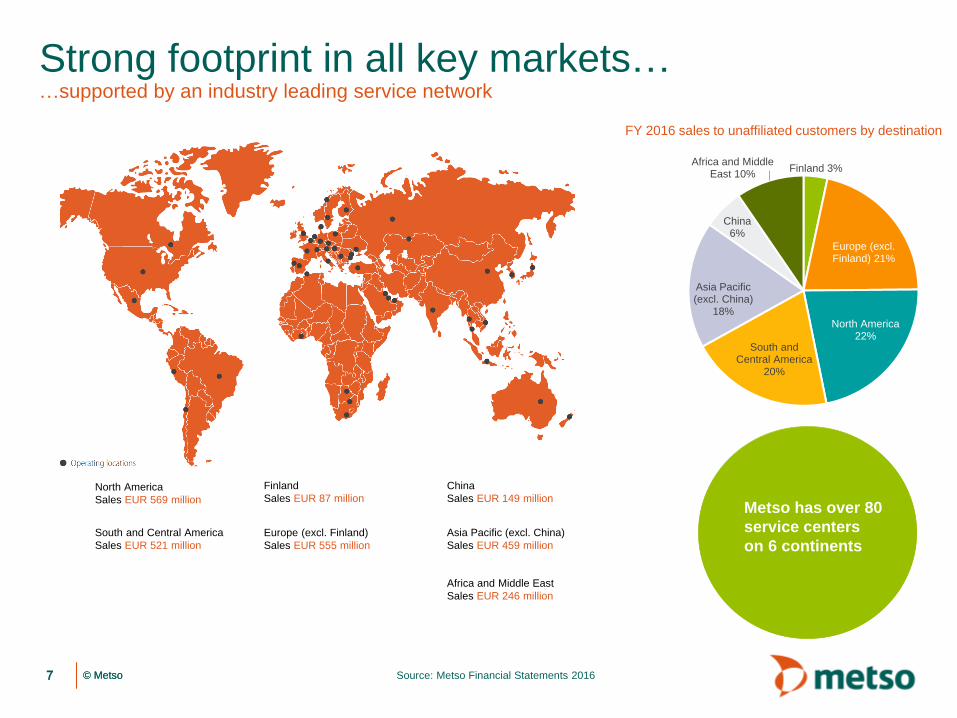

© Metso© Metso Source: Metso Financial Statements 20167

North America

Sales EUR 569 million

Europe (excl. Finland)

Sales EUR 555 million

South and Central America

Sales EUR 521 million

China

Sales EUR 149 million

Africa and Middle East

Sales EUR 246 million

Asia Pacific (excl. China)

Sales EUR 459 million

Strong footprint in all key markets……supported by an industry leading service network

Metso has over 80

service centers

on 6 continents

Finland

Sales EUR 87 million

Finland 3%

Europe (excl. Finland) 21%

North America22%

South and Central America

20%

Asia Pacific (excl. China)

18%

China6%

Africa and Middle East 10%

FY 2016 sales to unaffiliated customers by destination

© Metso© Metso

1. Metso in brief & operating environment

2. Business review

3. Financial review

4. Credit rating & financing

Contents

8

© Metso© Metso

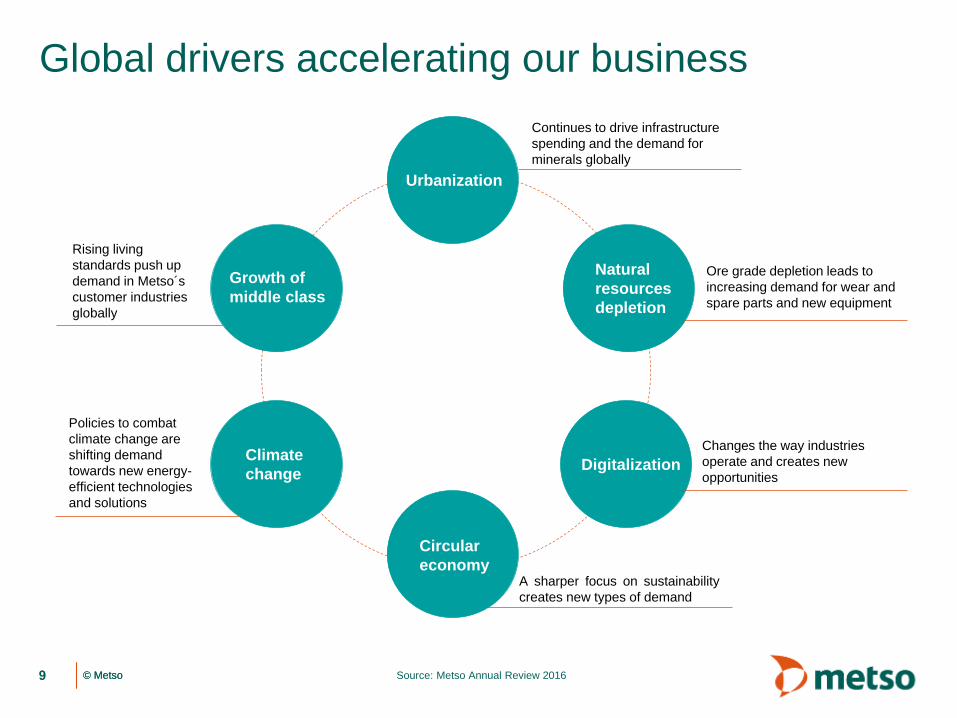

Global drivers accelerating our business

Source: Metso Annual Review 20169

Urbanization

Growth of

middle class

Natural

resources

depletion

Climate

change

Circular

economy

Digitalization

Continues to drive infrastructure

spending and the demand for

minerals globally

Ore grade depletion leads to

increasing demand for wear and

spare parts and new equipment

Changes the way industries

operate and creates new

opportunities

A sharper focus on sustainability

creates new types of demand

Policies to combat

climate change are

shifting demand

towards new energy-

efficient technologies

and solutions

Rising living

standards push up

demand in Metso´s

customer industries

globally

© Metso© Metso

Our strategy drives customer success

10

Systems

Products

Services

MineralsFlow Control

Targeting

profitable

growth

with a

clear focus

Leading flow control provider with offerings for oil & gas, mining and process industries

Leading technology and services provider for end-to-end minerals processing

Our business model relies heavily on services

where we have the strongest position and

product portfolio in the market.

We build on our leading technically advanced

product portfolio.

Our strong emphasis is on services and product businesses. We aim to balance the share of system deliveries to optimize the profitability and risk level of our complete business portfolio.

© Metso© Metso

We have a strong market position in all ourbusinesses

Source: Industry statistics and Metso estimates11

Strong niche position in

automated

on/off valves

A global leader in slurry

pumps

Strong position in

control valves+

#1Mining

crushers and

grinding mills

#1Aggregates

crushing and

screening

#1Metal

recycling

equipment

#1Services

for minerals

processing

#3Intelligent

valve

controllers

#1Pulp and

paper

valves

Our market positions

© Metso© Metso

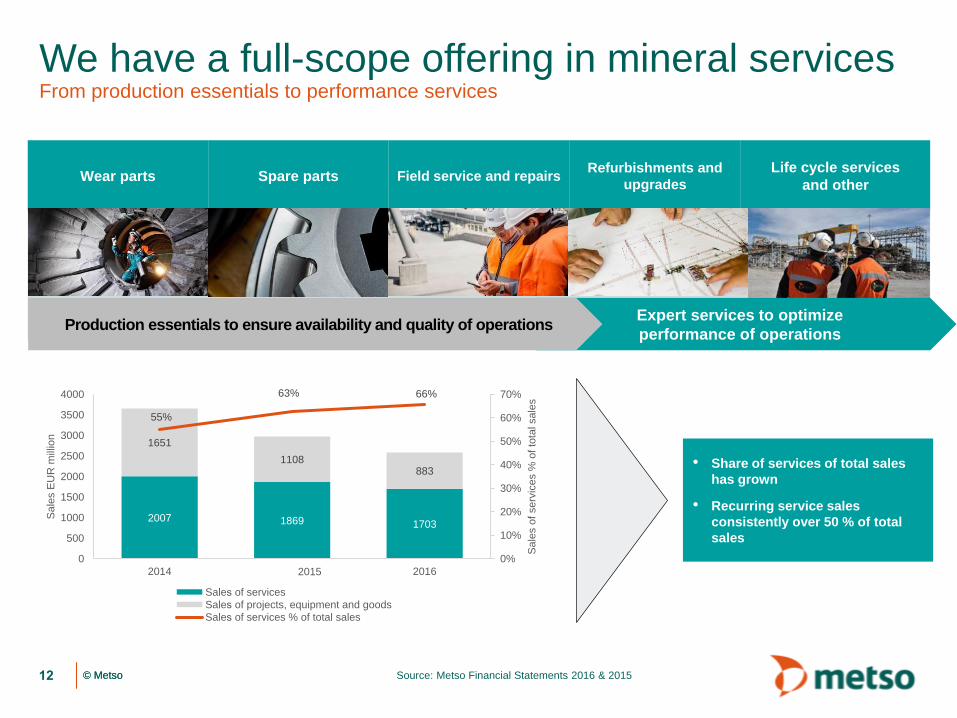

We have a full-scope offering in mineral servicesFrom production essentials to performance services

Source: Metso Financial Statements 2016 & 2015

Wear parts Spare parts Field service and repairsRefurbishments and

upgrades

Life cycle services

and other

Image of field service

guys

Expert services to optimize

performance of operationsProduction essentials to ensure availability and quality of operations

12

2007 1869 1703

1651

1108883

55%

63% 66%

0%

10%

20%

30%

40%

50%

60%

70%

0

500

1000

1500

2000

2500

3000

3500

4000

2014 2016

Sale

s o

f serv

ices %

of to

tal sale

s

Sale

s E

UR

mill

ion

2015

Sales of services

Sales of projects, equipment and goods Sales of services % of total sales

• Share of services of total sales

has grown

• Recurring service sales

consistently over 50 % of total

sales

© Metso13

Short-term market outlook for 2017

Mining

45% of sales

80% services *

Aggregates

25% of sales

45% services *

Flow Control

25% of sales

60% services *

satisfactory good good good good

Equipment Equipment Equipment ServicesServicesServices

Previously: weak

* Based on 12 months rolling sales

good

© Metso© Metso

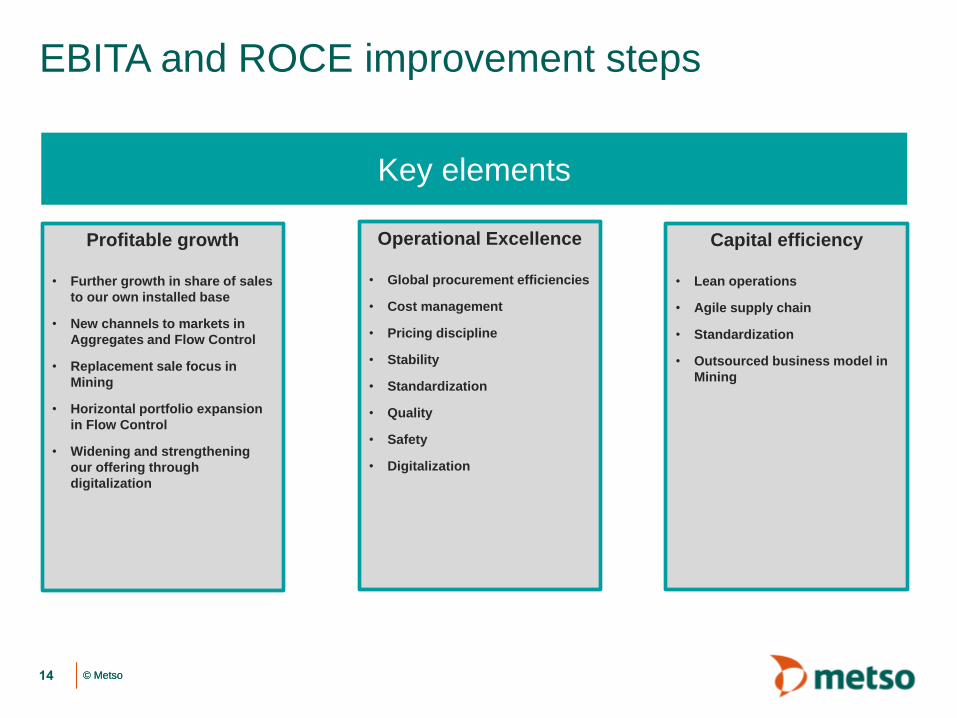

EBITA and ROCE improvement steps

14

Key elements

Operational Excellence

• Global procurement efficiencies

• Cost management

• Pricing discipline

• Stability

• Standardization

• Quality

• Safety

• Digitalization

Capital efficiency

• Lean operations

• Agile supply chain

• Standardization

• Outsourced business model in

Mining

Profitable growth

• Further growth in share of sales

to our own installed base

• New channels to markets in

Aggregates and Flow Control

• Replacement sale focus in

Mining

• Horizontal portfolio expansion

in Flow Control

• Widening and strengthening

our offering through

digitalization

© Metso© Metso

1. Metso in brief & operating environment

2. Business review

3. Financial review

4. Credit rating & financing

Contents

15

© Metso© Metso

56

77 77

64 66 70

9.311.5 12.1

9.4 10.2 10.4

0

5

10

15

20

0

20

40

60

80

Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

EUR million

Adjusted EBITA Adjusted EBITA %

%

433 444 423 441496 480

1.06 1.01 1.02 1.001.17

1.08

0.0

0.4

0.8

1.2

1.6

0

200

400

Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

EUR million

Services sales Services orders received Services book-to-bill

663761

628 672733 749

1.10 1.130.98 0.99

1.13 1.11

0.0

0.4

0.8

1.2

1.6

0

200

400

600

800

Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

EUR million

Orders received Book-to-bill

601671 638 676 648 675

-20-15-10-505101520

0

200

400

600

Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

EUR million

Sales Sales growth y-on-y

%

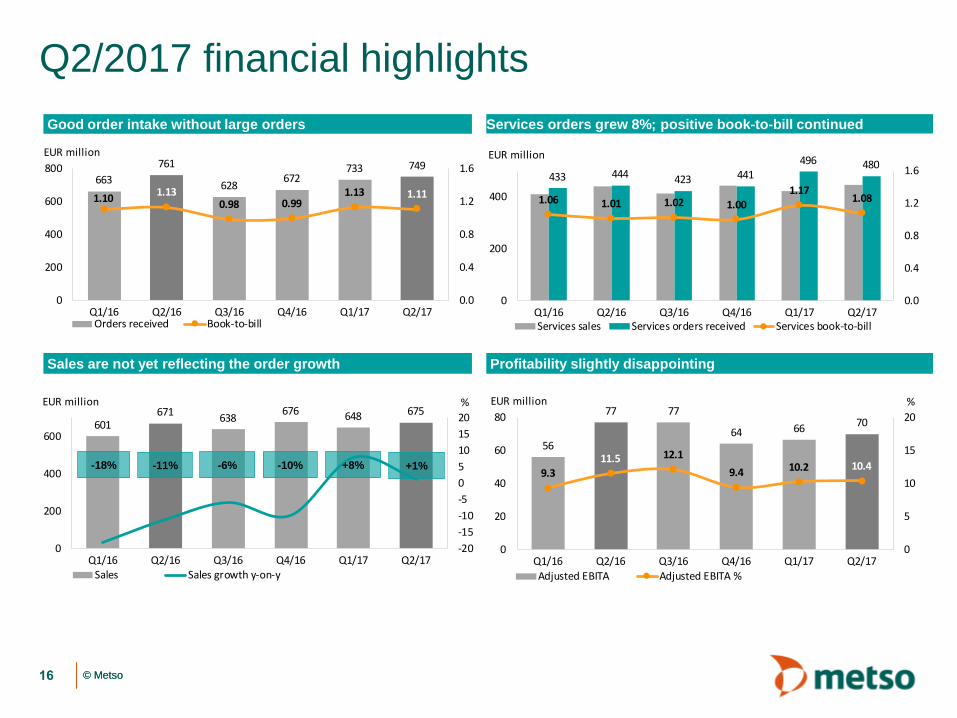

Q2/2017 financial highlights

Profitability slightly disappointing

Services orders grew 8%; positive book-to-bill continuedGood order intake without large orders

Sales are not yet reflecting the order growth

-11%-18% -10%-6% +8%

16

+1%

© Metso© Metso

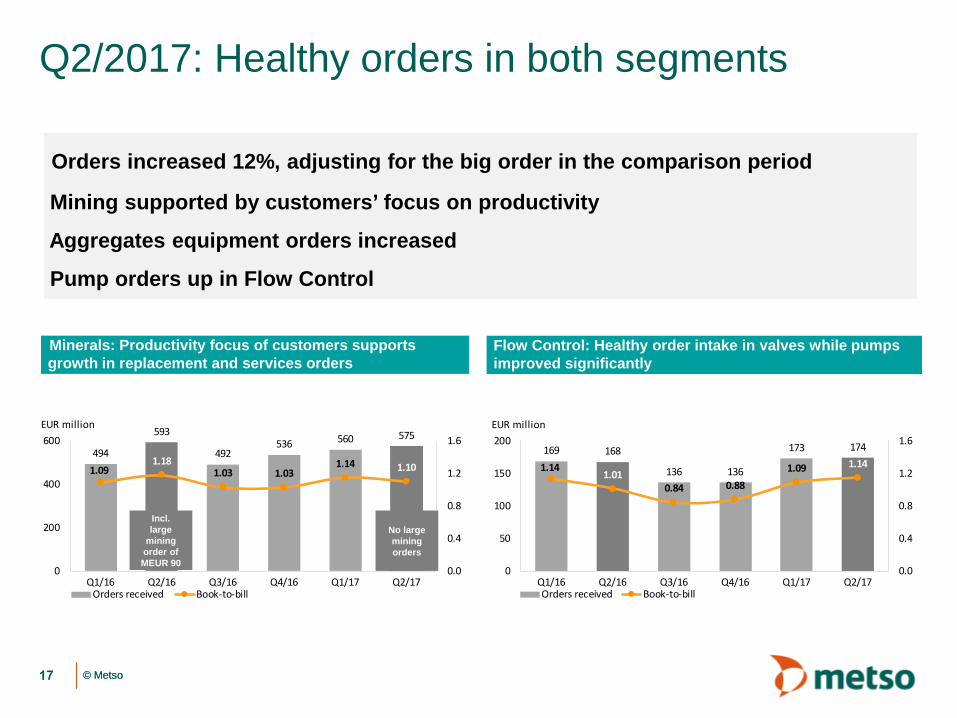

Q2/2017: Healthy orders in both segments

Orders increased 12%, adjusting for the big order in the comparison period

Mining supported by customers’ focus on productivity

Aggregates equipment orders increased

Pump orders up in Flow Control

Minerals: Productivity focus of customers supports

growth in replacement and services orders

Flow Control: Healthy order intake in valves while pumps

improved significantly

17

494

593

492536 560 575

1.091.18

1.03 1.031.14 1.10

0.0

0.4

0.8

1.2

1.6

0

200

400

600

Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

EUR million

Orders received Book-to-bill

169 168

136 136

173 174

1.141.01

0.84 0.881.09 1.14

0.0

0.4

0.8

1.2

1.6

0

50

100

150

200

Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

EUR million

Orders received Book-to-bill

Incl.

large

mining

order of

MEUR 90

No large

mining

orders

© Metso© Metso

37

54 5247

43

55

8.210.8 10.8

9.1 8.910.5

0

5

10

15

20

0

20

40

60

Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

EUR million

Adjusted EBITA Adjusted EBITA %

%

453504 477

522 489523

-20-15-10-505101520

0

200

400

600

Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

EUR million

Minerals Services sales Minerals Equipment salesSales growth y-on-y

%

Minerals Q2: Aggregates’ improvement offset by mining

Sales driven by double-digit growth in aggregates equipment; other businesses flat

Mining services margins affected by higher raw material prices and sales mix

-10%-20% -9%-5% +8%

EUR million Q2/2017 Q2/2016 Change % H1/2017 H1/2016 Change % 2016Orders received 575 593 -3 1,135 1,087 4 2,115

Services orders 370 337 10 756 672 13 1,348Sales 523 504 4 1,012 957 6 1,956

Services sales 347 340 2 673 663 2 1,325Adjusted EBITA 54.9 54.3 1 98.3 91.2 8 190.3

% of sales 10.5 10.8 9.7 9.5 9.7Return on operative capital employed

(ROCE), annualized, % 16.3 14.7 13.4

Personnel at the end of the period 8,567 8,701 -2 8,370

18

+4%

© Metso© Metso

1922

2826 25

1612.8 13.2

17.5 16.6 15.6

10.8

0

5

10

15

20

25

0

10

20

30

Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

EUR million

Adjusted EBITA Adjusted EBITA %

%

148167 161 155 159 152

-20-15-10-505101520

0

50

100

150

200

Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

EUR million

Flow Control Services sales Flow Control Equipment salesSales growth y-on-y

%

Flow Control Q2: First half performance flatwith positive book-to-bill

Sales reflecting H2/16 order intake

Low sales and related under-absorption as well as sales mix impacted profitability

-14%-13% -14%-10% +7%

EUR million Q2/2017 Q2/2016 Change % H1/2017 H1/2016 Change % 2016Orders received 174 168 4 347 337 3 609

Services orders 110 107 3 220 205 7 393Sales 152 167 -9 311 315 -1 631

Services sales 98 99 -1 195 185 5 378Adjusted EBITA 16.4 22.1 -26 41.2 41.1 0 95.0

% of sales 10.8 13.2 13.2 13.0 15.1Return on operative capital employed

(ROCE), annualized, % 25.1 24.9 28.5

Personnel at the end of the period 2,685 2,878 -7 2,663

19

-9%

© Metso© Metso

126 130 125 135 126 127

20.919.4 19.6 20.0 19.5 18.8

0

5

10

15

20

25

0

50

100

150

200

Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

EUR million

SGA SGA %

%

176196

181 184 184 187

29.2 29.2 28.4 27.2 28.4 27.7

0

5

10

15

20

25

30

0

50

100

150

200

250

Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

EUR million

Gross profit Gross margin

%

480

240 207153

91

174

70

-25 -63

100

-0.3

0.0

0.3

0.6

0.9

1.2

1.5

-100

100

300

500

Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

EUR million

Net debt Net debt/EBITDA

124 120129

83

59

103 103

127

5846

0

100

200

300

400

500

0

50

100

150

Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

EUR million

Cash flow from operations Cash flow from operations, rolling 12 months

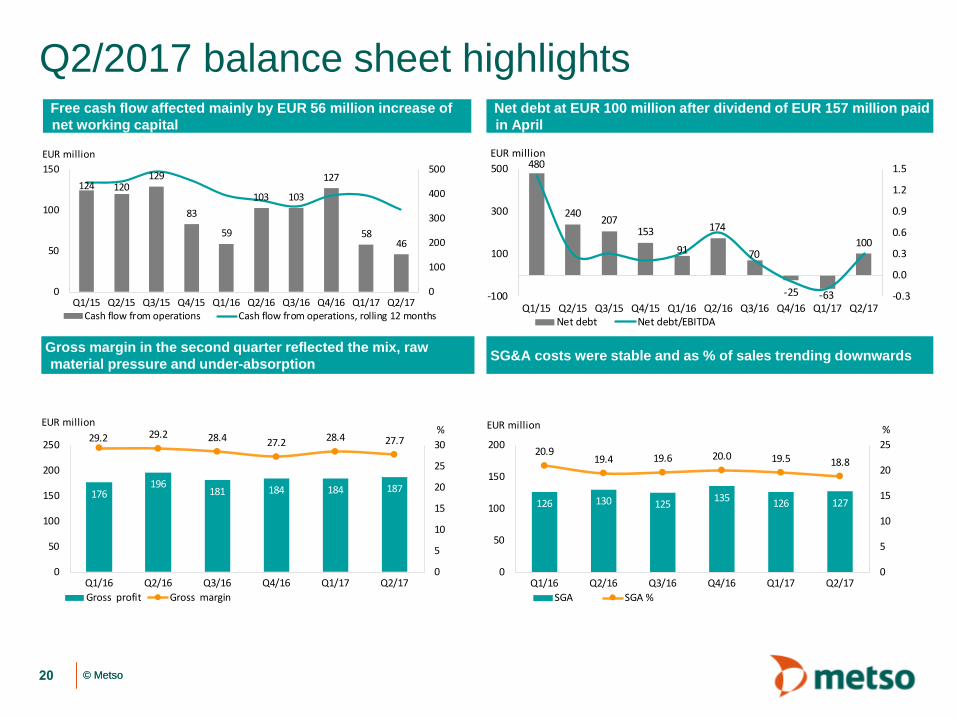

Q2/2017 balance sheet highlights

SG&A costs were stable and as % of sales trending downwards

Net debt at EUR 100 million after dividend of EUR 157 million paid

in April

Free cash flow affected mainly by EUR 56 million increase of

net working capital

Gross margin in the second quarter reflected the mix, raw

material pressure and under-absorption

20

© Metso© Metso

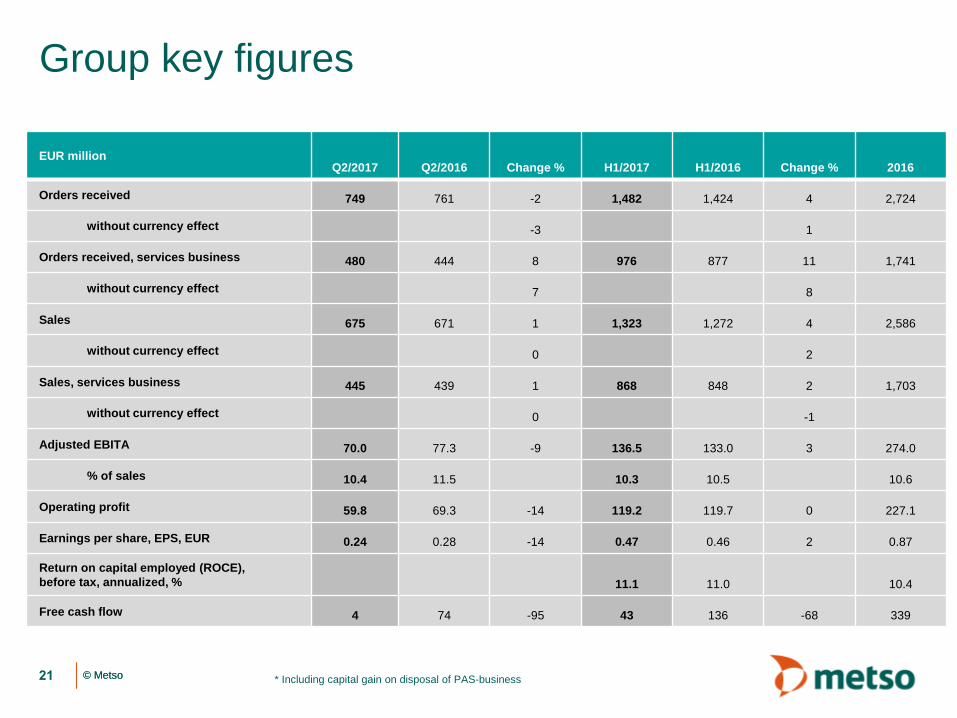

Group key figures

* Including capital gain on disposal of PAS-business21

EUR millionQ2/2017 Q2/2016 Change % H1/2017 H1/2016 Change % 2016

Orders received 749 761 -2 1,482 1,424 4 2,724

without currency effect -3 1

Orders received, services business 480 444 8 976 877 11 1,741

without currency effect 7 8

Sales 675 671 1 1,323 1,272 4 2,586

without currency effect 0 2

Sales, services business 445 439 1 868 848 2 1,703

without currency effect 0 -1

Adjusted EBITA 70.0 77.3 -9 136.5 133.0 3 274.0

% of sales 10.4 11.5 10.3 10.5 10.6

Operating profit 59.8 69.3 -14 119.2 119.7 0 227.1

Earnings per share, EPS, EUR 0.24 0.28 -14 0.47 0.46 2 0.87

Return on capital employed (ROCE),

before tax, annualized, % 11.1 11.0 10.4

Free cash flow 4 74 -95 43 136 -68 339

© Metso© Metso

1. Metso in brief & operating environment

2. Business review

3. Financial review

4. Credit rating & financing

Contents

22

© Metso

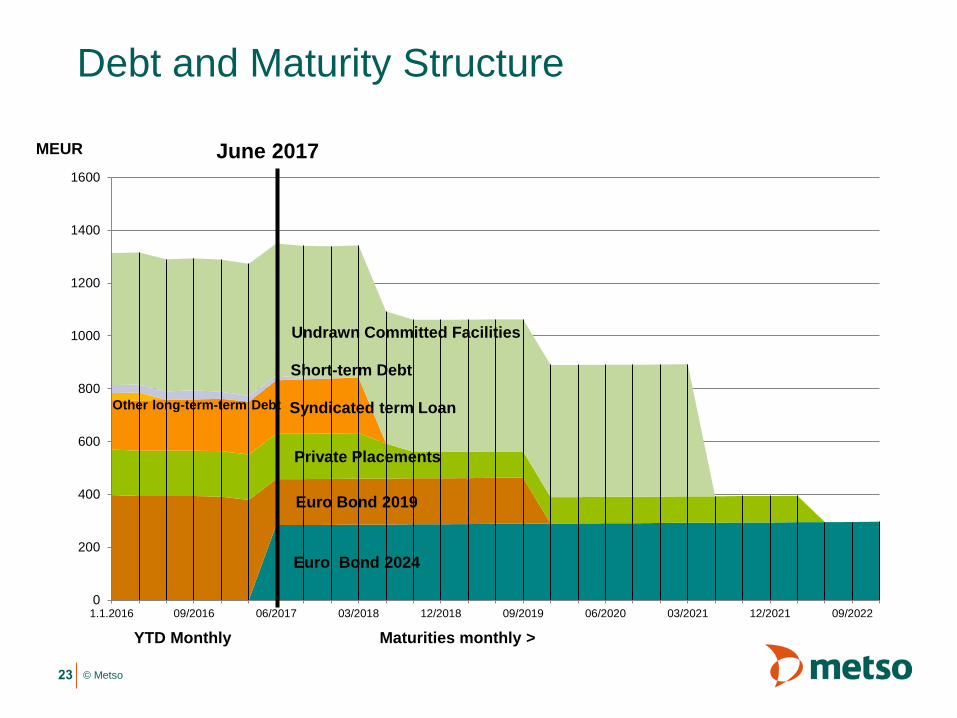

Debt and Maturity Structure

0

200

400

600

800

1000

1200

1400

1600

1.1.2016 09/2016 06/2017 03/2018 12/2018 09/2019 06/2020 03/2021 12/2021 09/2022

23

YTD Monthly Maturities monthly >

June 2017MEUR

Euro Bond 2024

Private Placements

Short-term Debt

Undrawn Committed Facilities

Syndicated term LoanOther long-term-term Debt

Euro Bond 2019

© Metso© Metso

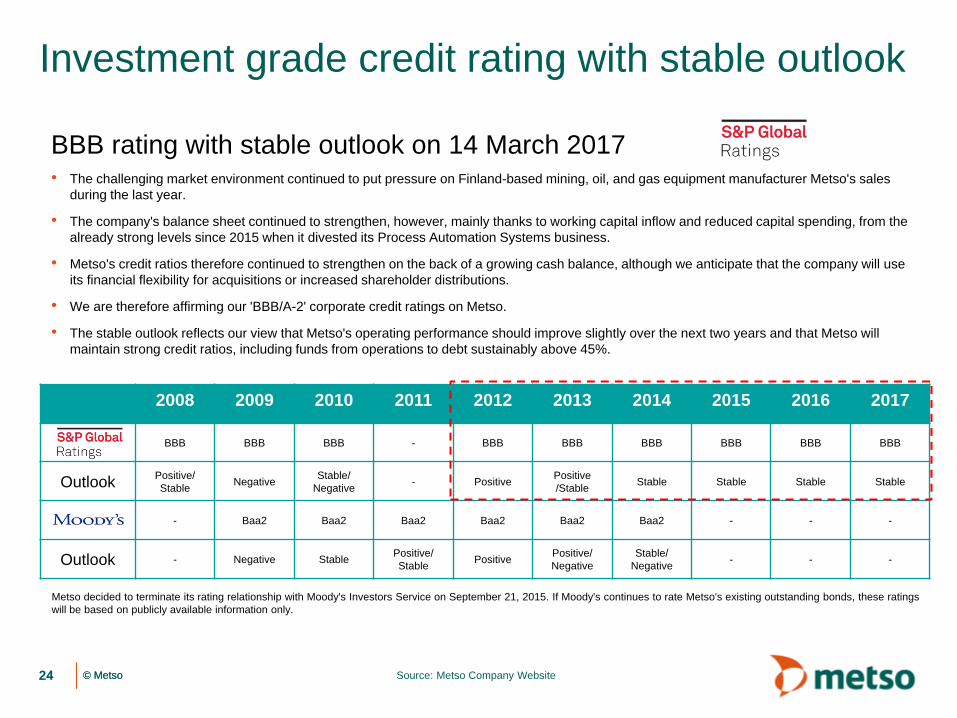

Investment grade credit rating with stable outlook

24 Source: Metso Company Website

BBB rating with stable outlook on 14 March 2017• The challenging market environment continued to put pressure on Finland-based mining, oil, and gas equipment manufacturer Metso's sales

during the last year.

• The company's balance sheet continued to strengthen, however, mainly thanks to working capital inflow and reduced capital spending, from the

already strong levels since 2015 when it divested its Process Automation Systems business.

• Metso's credit ratios therefore continued to strengthen on the back of a growing cash balance, although we anticipate that the company will use

its financial flexibility for acquisitions or increased shareholder distributions.

• We are therefore affirming our 'BBB/A-2' corporate credit ratings on Metso.

• The stable outlook reflects our view that Metso's operating performance should improve slightly over the next two years and that Metso will

maintain strong credit ratios, including funds from operations to debt sustainably above 45%.

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

BBB BBB BBB - BBB BBB BBB BBB BBB BBB

OutlookPositive/

StableNegative

Stable/

Negative- Positive

Positive

/StableStable Stable Stable Stable

- Baa2 Baa2 Baa2 Baa2 Baa2 Baa2 - - -

Outlook - Negative StablePositive/

StablePositive

Positive/

Negative

Stable/

Negative- - -

Metso decided to terminate its rating relationship with Moody's Investors Service on September 21, 2015. If Moody's continues to rate Metso's existing outstanding bonds, these ratings

will be based on publicly available information only.

© Metso© Metso

Appendix

25

© Metso© Metso

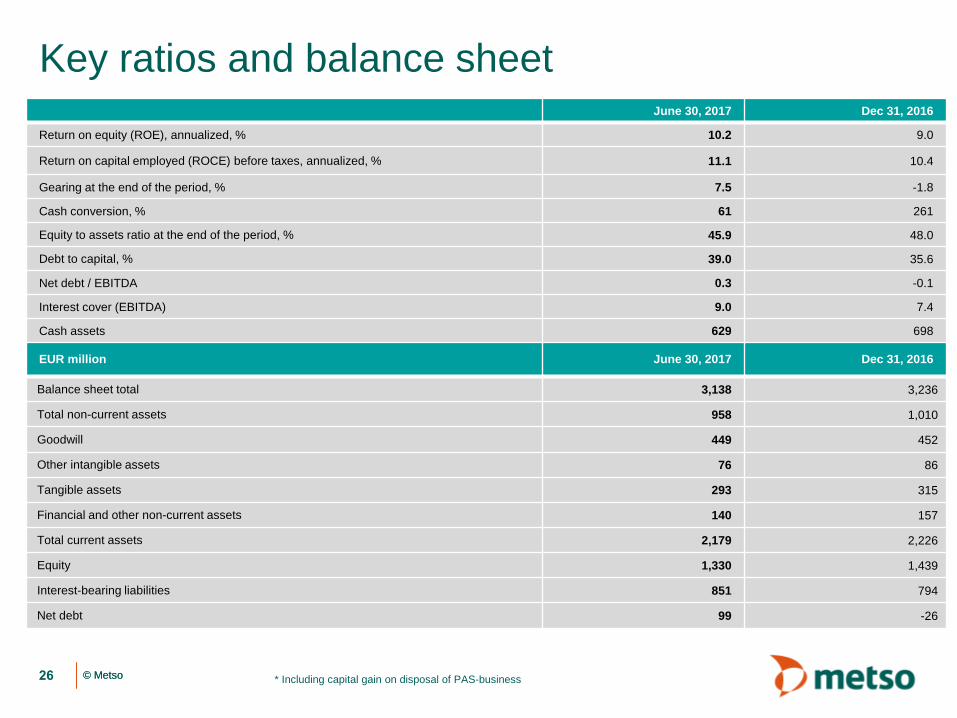

Key ratios and balance sheet

* Including capital gain on disposal of PAS-business

EUR million June 30, 2017 Dec 31, 2016

Balance sheet total 3,138 3,236

Total non-current assets 958 1,010

Goodwill 449 452

Other intangible assets 76 86

Tangible assets 293 315

Financial and other non-current assets 140 157

Total current assets 2,179 2,226

Equity 1,330 1,439

Interest-bearing liabilities 851 794

Net debt 99 -26

26

June 30, 2017 Dec 31, 2016

Return on equity (ROE), annualized, % 10.2 9.0

Return on capital employed (ROCE) before taxes, annualized, % 11.1 10.4

Gearing at the end of the period, % 7.5 -1.8

Cash conversion, % 61 261

Equity to assets ratio at the end of the period, % 45.9 48.0

Debt to capital, % 39.0 35.6

Net debt / EBITDA 0.3 -0.1

Interest cover (EBITDA) 9.0 7.4

Cash assets 629 698

company/metso metsogroup metsoworldmetsoworld metsogroup

www.metso.com