Embed Size (px)

Citation preview

Credit, Housing, Commodities and the Economy

Financial Planning Association Financial Planning Association Annual NorCal Conference

May 27, 2008

Janet L. YellenPresident and CEO

Federal Reserve Bank of San Francisco

May 27, 2008 Federal Reserve Bank of San Francisco 2

Overview

Financial turmoil and the credit crunch

Downturn in housing markets

Surge in commodity prices

Implications for the outlook and policy

May 27, 2008 Federal Reserve Bank of San Francisco 3

The unwinding of a credit market bubble

A bubble-like situation had developed in the credit markets.

Very low long-term real interest rates

Investors accepted meager rewards for risk

Abundance of liquidity was reflected in:

Easy financing for leveraged buyouts

Carry trades

Rapid growth in subprime lending

Suggested a benign view of underlying risks.

May 27, 2008 Federal Reserve Bank of San Francisco 4

What caused the bubble?

Securitization and financial engineering appeared to improve risk-return tradeoff.

Up-front origination fees undermined strong underwriting incentives.

Institutions in the “shadow banking sector” sought to increase leverage and reach for yield.

Overreliance on credit ratings that proved unreliable.

Some lessons:

Inadequate risk management by many sophisticated institutions.

Shortcomings in financial supervision and regulation.

May 27, 2008 Federal Reserve Bank of San Francisco 5

Underwriting standards deteriorated

70

72

74

76

78

80

82

84

86

88

90

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

0

5

10

15

20

25

30

35

40

45

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Combined Loan-to-Value Ratios (2/28 Subprime Mortgages)

Percent without Full Documentation (2/28 Subprime Mortgages)

May 27, 2008 Federal Reserve Bank of San Francisco 6

What caused the bubble?

Securitization and financial engineering appeared to improve risk-return tradeoff.

Up-front origination fees undermined strong underwriting incentives.

Institutions in the “shadow banking sector” sought to increase leverage and reach for yield.

Overreliance on credit ratings that proved unreliable.

Some lessons:

Inadequate risk management by many sophisticated institutions.

Shortcomings in financial supervision and regulation.

May 27, 2008 Federal Reserve Bank of San Francisco 7

Subprime mortgage delinquencies are rising

1999 2001 2003 2005 20076

8

10

12

14

16

18

20

22

Subprime ARM

Subprime FRM

Mortgage Delinquency RatesReported quarterly; fraction of outstanding loans Percent

Delinquent mortgages are 30 days or more past due but not in foreclosure.

May 27, 2008 Federal Reserve Bank of San Francisco 8

Subprime delinquencies rose as house price appreciation slowed

Mortgage Delinquency Rates and OFHEO House Price Index Changes

0

5

10

15

20

25

30

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

percent

-1

1

3

5

7

9

11

13

15

percent

Delinquency rates*, subprime ARMs (left scale)

OFHEO Index, 4-quarter growth (right scale)

Sources: Office of Federal Housing Enterprise Oversight and Mortgage Bankers Association * 60 days or more past due or in foreclosure

May 27, 2008 Federal Reserve Bank of San Francisco 9

Subprime delinquencies and house price changes vary inversely across MSAs

May 27, 2008 Federal Reserve Bank of San Francisco 10

Prime mortgage delinquencies are rising too

1999 2001 2003 2005 20070

2

4

6

8

10

12

14

16

18

20

22

Subprime ARM

Subprime FRM

PrimeARM

PrimeFRM

Mortgage Delinquency RatesReported quarterly; fraction of outstanding loans Percent

Delinquent mortgages are 30 days or more past due but not in foreclosure.

May 27, 2008 Federal Reserve Bank of San Francisco 11

Subprime problems triggered financial market disruptions

Rising subprime delinquencies triggered disruptions in the markets for asset-backed securities (ABS).

Contagion to municipal bonds and other ABS markets

Prices fell, imposing losses on ABS holders.

Heavy ABS exposure of banks and “shadow banks”--highly leveraged institutions that “borrow short” to hold long-term assets including ABS.

Includes investment banks, hedge funds, SIVs/conduits.

May 27, 2008 Federal Reserve Bank of San Francisco 12

The emergence of a credit crunch

Financial institutions are deleveraging—scaling back their balance sheets.

Commercial banks experienced unanticipated buildup of loans on their balance sheets.

Many financial institutions are raising capital.

But banks are tightening credit terms and restricting availability.

May 27, 2008 Federal Reserve Bank of San Francisco 13

Banks are tightening credit standards

90 92 94 96 98 00 02 04 06 08-40

-20

0

20

40

60

80

100Net percent of respondents tightening credit standardsCredit Conditions, Domestic and Commercial Banks

Q2

C&I

ConsumerCommercialreal estate

Prime

Residential

Source: Federal Reserve Senior Loan Officer Opinion Survey

May 27, 2008 Federal Reserve Bank of San Francisco 14

1999 2000 2001 2002 2003 2004 2005 2006 20070

10

20

30

40

50

60

Billionsof $Private-Label RMBS and CMBS Issuance

3-month moving average

Apr.

RMBS

CMBS

Source: Asset-Backed Alert

New issuance of ABS has plummeted

May 27, 2008 Federal Reserve Bank of San Francisco 15

The interbank lending market is under stress

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May0

20

40

60

80

100

120

Spread between LIBOR and Expected Funds RateDaily closing; expected funds rate from Overnight Indexed Swap (OIS) contract

Basis points

5/22

Three-month

One-month

LIBOR: London InterBank Offered Rate

May 27, 2008 Federal Reserve Bank of San Francisco 16

Corporate bond spreads have risen

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun3

4

5

6

7

8

9

10

11

12

Corporate Long-Term Bond Yields Daily closing

Percent

High-yield-indexbonds

A-indexbonds

5/22

10-yeartreasury

May 27, 2008 Federal Reserve Bank of San Francisco 17

Fed initiatives to improve market liquidity

Enhanced discount window lendingReduced rate spread and lengthened term of lending

Established Term Auction Facility (TAF)Term discount window loans at auction rate; $150 billion

Initiated term repurchase (repo) transactionsAgency debt accepted as collateral for 28-day repos; $100 billion

Established Term Securities Lending Facility (TSLF)Lends Treasuries for highly rated ABS; up to $200 billion

Provided financing for acquisition of Bear Stearns Term financing to support purchase by JP Morgan; $29 billion

Established Primary Dealer Credit Facility (PDCF)Overnight borrowing from discount window by primary dealers

May 27, 2008 Federal Reserve Bank of San Francisco 18

Selected Federal Reserve Assets

0

100

200

300

400

500

600

700

800

900

1000

Jul-07 Sep-07 Nov-07 Jan-08 Mar-08 May-08

Billions of $

0

100

200

300

400

500

600

700

800

900

1000

Billions of $

Other $94.3 b

Primary Dealer CreditFacility $16.6 b

Primary Credit $14.4 b

Term Auction CreditFacility $125.0 b

Repurchase Agreements $95.8 b

Term Sec Lending Facility $138.1 b

Overnight Sec LendingFacility $12.5 b

US Treasuries held outrightless securities to dealers $369.5 b

week of May 14

New facilities change the composition of Fed’s balance sheet

May 27, 2008 Federal Reserve Bank of San Francisco 19

Spreads on MBS receded in wake of Fed initiatives

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-080

50

100

150

200

250

300

350

400

Fannie Mae, 30 yr option adjusted spreadFreddie Mac, 30 yr option adjusted spreadCMBS, 10 yr AAA spread over swap

Basis pointsMBS Spreads

5/14

5/21

Sources: Asset-Backed Alert and Bloomberg

May 27, 2008 Federal Reserve Bank of San Francisco 20

The housing price-to-rent ratio soared

Price-rent ratio

15

17

19

21

23

25

27

29

1970 1974 1978 1982 1986 1990 1994 1998 2002 2006Source: BLS. Data are adjusted as in Gallin (forthcoming)

May 27, 2008 Federal Reserve Bank of San Francisco 21

150

200

250

300

350

400

450

500

550

600

78 82 86 90 94 98 02 06400

800

1200

1600

2000

2400

Housing Thousands, seasonally adjusted

Mar.

New housesfor sale(right scale)

Housing starts(left scale)

Vacant housesfor sale(left scale)

Apr.

Q1

Housing markets have hit the skids

May 27, 2008 Federal Reserve Bank of San Francisco 22

House prices are still heading down

1988 1993 1998 2003 200860

85

110

135

160

185

210

235

House PricesCase-Shiller national index with futures

Q4

Index

Futures

May 27, 2008 Federal Reserve Bank of San Francisco 23

The price of crude oil has jumped

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009152535455565758595105115125135

$/BarrelPrice of OilWest Texas Intermediate; weekly closing price

Futures 5/22

May 27, 2008 Federal Reserve Bank of San Francisco 24

Prices of other commodities are also up

2000 2001 2002 2003 2004 2005 2006 2007 20080

2

4

6

8

10

12

14

100

200

300

400

500

600

700

800

900

1000

Prices of Wheat, Corn and MetalsMonthly average $/Bushel

Hard Wheat

YellowCorn

CRB Metals Index(left scale)

Spot Price

May

May 27, 2008 Federal Reserve Bank of San Francisco 25

Consumer spending growth and sentiment are down

Consumer Sentiment and PCE Growth

55

65

75

85

95

105

115

1999 2001 2003 2005 2007-2.00

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Consumer sentiment (left scale)*PCE growth (right scale)

*Source for consumer sentiment is Reuters/Michigan Survey.

Index 1966 = 100 4-quarter percent change

May 27, 2008 Federal Reserve Bank of San Francisco 26

3.5

4.0

4.5

5.0

5.5

6.0

6.5

2000 2001 2002 2003 2004 2005 2006 2007129

130

131

132

133

134

135

136

137

138

139

Employment SituationSeasonally adjusted

Nonfarm Payroll Employment(right scale)

Millions of EmployeesPercent

Unemployment Rate(left scale)

Empl. ChangeJan.Feb.Mar.Apr.

-76 K-83 K-81 K-20 K

Employment is shrinking and unemployment rising

May 27, 2008 Federal Reserve Bank of San Francisco 27

Capital spending has slowed

2000 2001 2002 2003 2004 2005 2006 2007 200845

50

55

60

65

70

Mar.

Billions of $

Shipments

Orders

Nondefense Capital Goods (Ex. Aircraft)Seasonally adjusted; 3-month moving average

May 27, 2008 Federal Reserve Bank of San Francisco 28

U.S. net exports are a source of strength

U.S. Net ExportsBillions of chained 2000 dollars

1995 1997 1999 2001 2003 2005 2007-700

-600

-500

-400

-300

-200

-100

0

May 27, 2008 Federal Reserve Bank of San Francisco 29

Economic growth has stalled

2000 2001 2002 2003 2004 2005 2006 2007

Q1

-2

0

2

4

6

8

Real Gross Domestic Product (GDP)Percent change at seasonally adjusted annual rate Percent

May 27, 2008 Federal Reserve Bank of San Francisco 30

Headline inflation has risen

1

2

3

4

PCE Price Inflation12 month percent change

Percent

Overall PCEPrice Index

Core PCEPrice Index

2000 2001 2002 2003 2004 2005 2006 2007 2008

May 27, 2008 Federal Reserve Bank of San Francisco 31

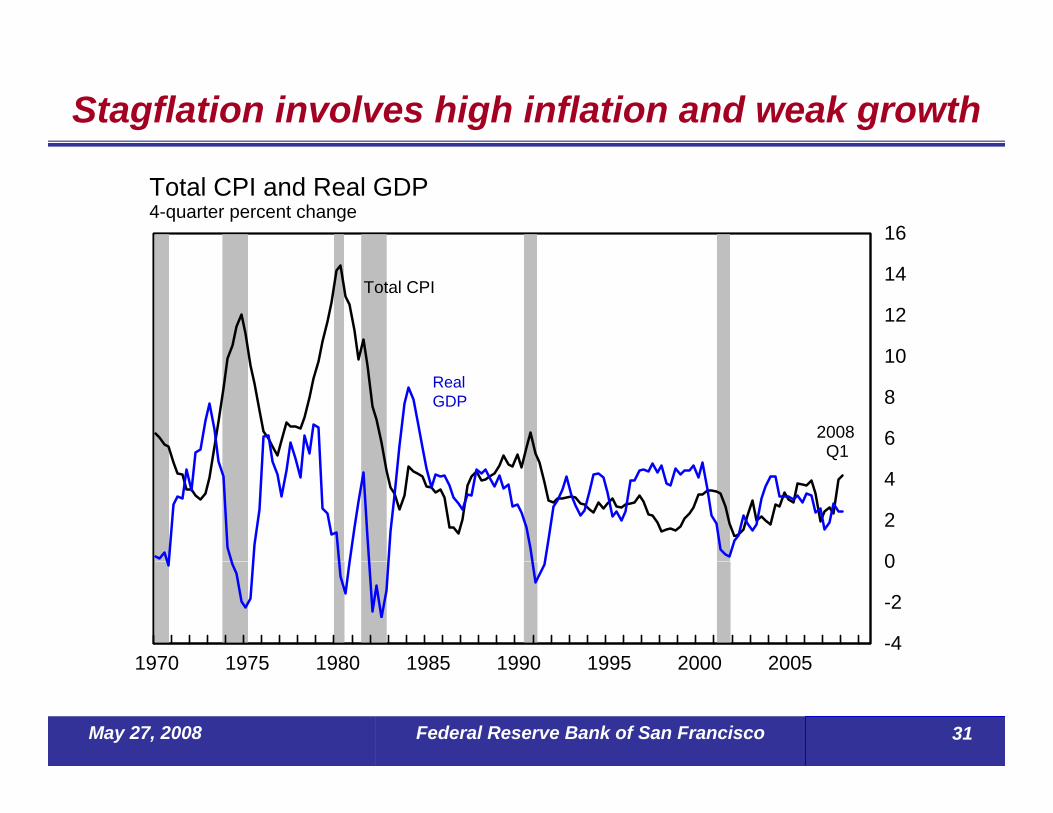

Stagflation involves high inflation and weak growth

Total CPI and Real GDP4-quarter percent change

1970 1975 1980 1985 1990 1995 2000 2005-4

-2

0

2

4

6

8

10

12

14

16

Total CPI

2008Q1

Core CPIReal GDP

May 27, 2008 Federal Reserve Bank of San Francisco 32

Stagflation involves a wage-price spiral

Total CPI and Unit Labor Cost4-quarter percent change

1970 1975 1980 1985 1990 1995 2000 2005-4

-2

0

2

4

6

8

10

12

14

16

Unit Labor Cost

Total CPI

2008Q1

May 27, 2008 Federal Reserve Bank of San Francisco 33

University of Michigan Inflation Expectations

0.0

2.0

4.0

6.0

8.0

10.0

12.0

1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Rate of inflation

Michigan 12 months out

Michigan 5-10 years out

Inflation expectations drive the wage-price spiral

May 27, 2008 Federal Reserve Bank of San Francisco 34

Monetary policy has eased

Interest RatesDaily closing

Percent

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun1

2

3

4

5

6

7

1

2

3

4

5

6

7

Federal Funds Target

2-yr. Treasury

5/22

Discount Rate

2007 2008