Embed Size (px)

Citation preview

Ubaldo Tambini

Credit Bureau analytics: Approaches, experiences

and impacts

Financial Infrastructure Week 2015

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

CRIF IN A NUTSHELL

Global player in Credit management

Services and Solutions for

Consumer, MFI & Commercial Lending

•25 years in business, 2,500 employees

•18 credit bureaus managed

•3100+ financial institutions in 49 countries

•500+ millions credit decisions yearly processed

•500+ software installations

•100+ predictive analytics and risk management

consultants

•Credit Rating Agency certified for Europe by ESMA.

•Best in Class in Sales & Application, Loan Decision,

Loan Processing & Enterprise support (CEB Tower Group)

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

CREDIT BUREAU ANALYTICS: OUR EXPERIENCE

•EUROPE, Americas, Asia

Different continents

• Individuals - e.g. Russia, Italy, Poland, India,…

• Sole traders – e.g. Slovak Republic, Czech Republic, Italy, ….

• Companies – e.g. Czech Republic, Italy, Greece, India,

• MFI – e.g. India, Mexico,..

Different types of subjects

• Bank institution - e.g. Ireland, Italy, Poland,…

• Non- bank institution - e.g. The Czech republic, Italy, …

• Utilities - e.g. Italy

Different types of contributors

• Credit history

• Negative information from public data source

• Business informations

• Payment history from telco&utilities operators

• Socio-demografic data

Different types of information

Mix of different experiences that helps CRIF to develop most powerful and reliable Credit Bureau Scores even where data are limited and business environment is rapidly changing

DIFFERENT TYPES OF CREDIT BUREAU SCORES

Italy

Czech Republic

Slovak Republic

India

Jamaica

Vietnam

Tajikistan

Ireland

Mexico

Germany

Greece

Indonesia

Poland

Bureau van Dijk

Croatia

Dominican Republic

Honduras

Canada

Guatemala

Brazil

Russia

UAE

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

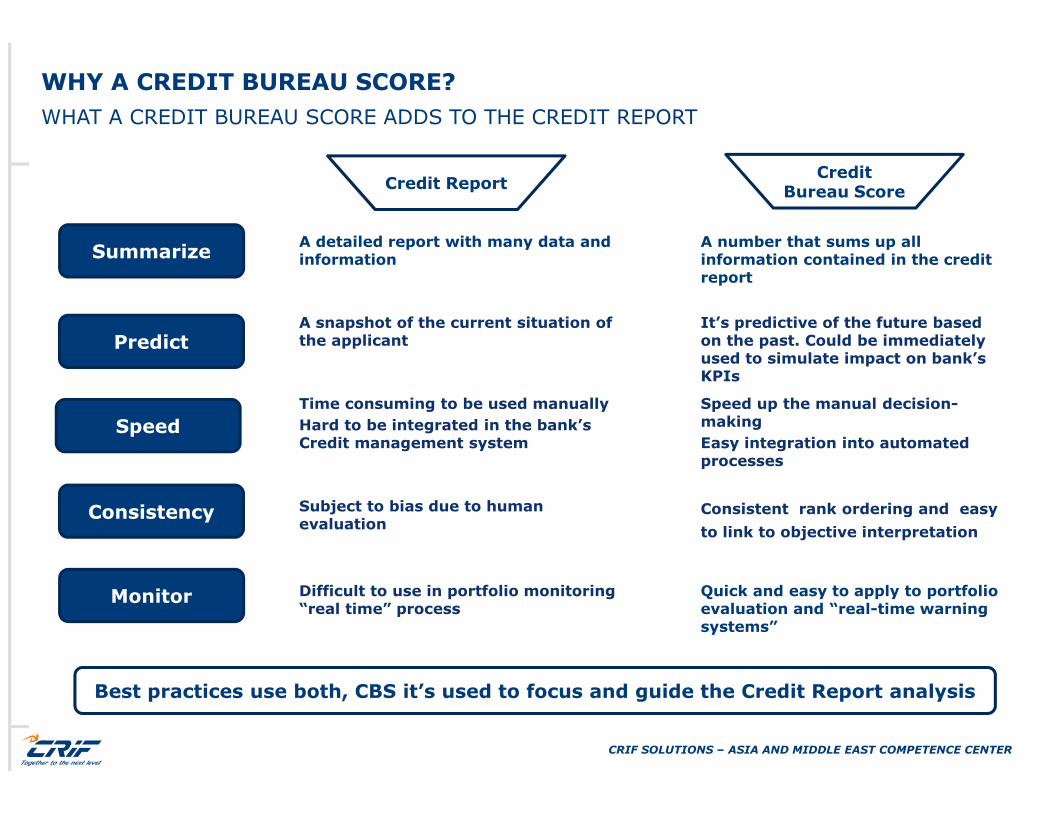

WHY A CREDIT BUREAU SCORE?

WHAT A CREDIT BUREAU SCORE ADDS TO THE CREDIT REPORT

Summarize

Speed

Predict

Credit ReportCredit

Bureau Score

A detailed report with many data and information

A number that sums up all information contained in the credit report

A snapshot of the current situation of the applicant

It’s predictive of the future based on the past. Could be immediately used to simulate impact on bank’s KPIs

Time consuming to be used manually

Hard to be integrated in the bank’s Credit management system

Speed up the manual decision-making

Easy integration into automated processes

Subject to bias due to human evaluation

Consistent rank ordering and easy

to link to objective interpretation

Difficult to use in portfolio monitoring “real time” process

Quick and easy to apply to portfolio evaluation and “real-time warning systems”

Best practices use both, CBS it’s used to focus and guide the Credit Report analysis

Consistency

Monitor

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

…

Other data

A SCORE IS NOT THE END OF THE STORY

TYPICAL EVOLUTION OF CREDIT BUREAU RELATED ANALYTICS

Bureau Credit report

GlocalScore

Credit Bureau Score

Collec-tion

Mktg

NO-HITScore

Sophistication

Fraud

BusInfo

Telcos

OverallRisk evaluation

processing

Applic-ation

Portfolio manage

ment

Utilities

Scope

“Big Data”

FSIBouncedCheques

Today topics

• “NO HIT” SCORES, an example from India

• “WATER” SCORE, an example from Italy

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

“NO-HIT” SCORE, an example from India

“WATER” SCORE, an example from Italy

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

THE NO-HIT SPIRAL

• 'No-hits' are cases where a bureau enquiry does not yield any result, implying a 'new-to-credit' population.

• Usually 30-40% of bureau enquiries in India are new

• 20-40% of population that is offered credit for the first time belongs to high risk category, and we are unable to capture that embedded risk

• New scorecard development must focus on how to understand this better and create mitigation strategies

10% OF NO-HIT POPULATION CAN INCREASE OVERALL RISK BY 3 TIMES

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

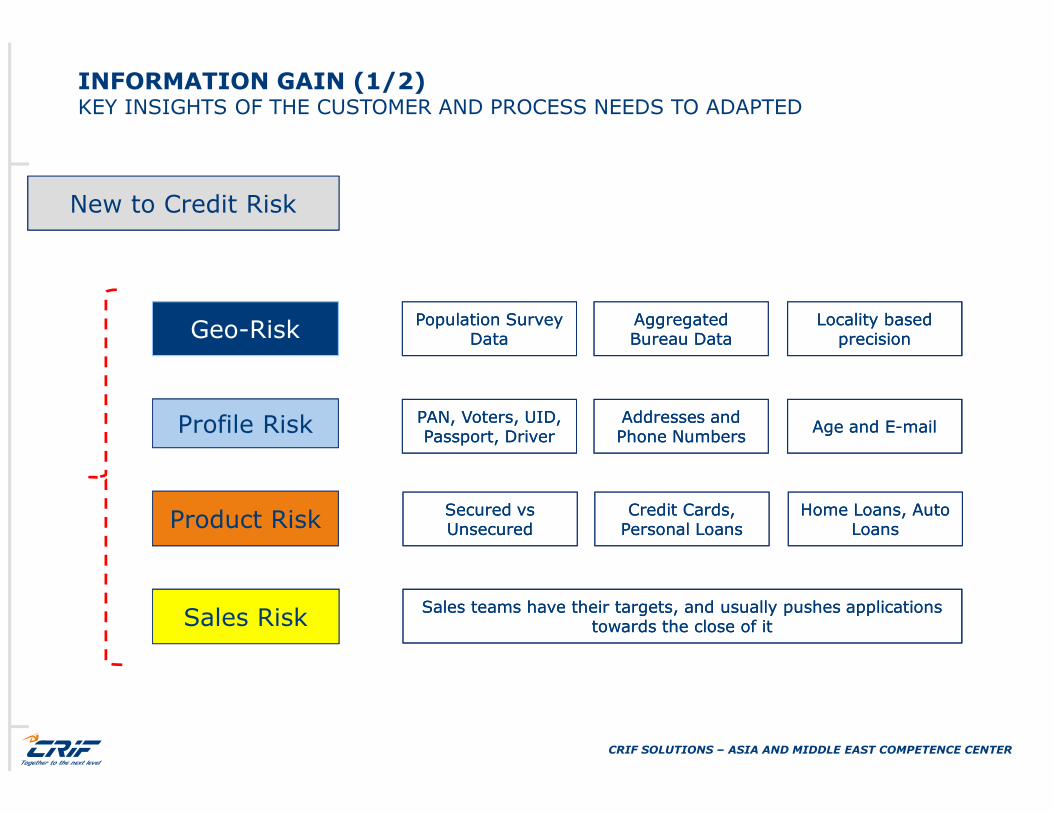

INFORMATION GAIN (1/2)KEY INSIGHTS OF THE CUSTOMER AND PROCESS NEEDS TO ADAPTED

Geo-Risk

Profile Risk

Product Risk

Sales Risk

New to Credit Risk

Population Survey Data

Population Survey Data

Aggregated Bureau DataAggregated Bureau Data

Locality based precision

Locality based precision

PAN, Voters, UID, Passport, Driver

PAN, Voters, UID, Passport, Driver

Addresses and Phone NumbersAddresses and Phone Numbers

Age and E-mailAge and E-mail

Secured vs UnsecuredSecured vs Unsecured

Credit Cards, Personal LoansCredit Cards,

Personal LoansHome Loans, Auto

LoansHome Loans, Auto

Loans

Sales teams have their targets, and usually pushes applications towards the close of it

Sales teams have their targets, and usually pushes applications towards the close of it

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

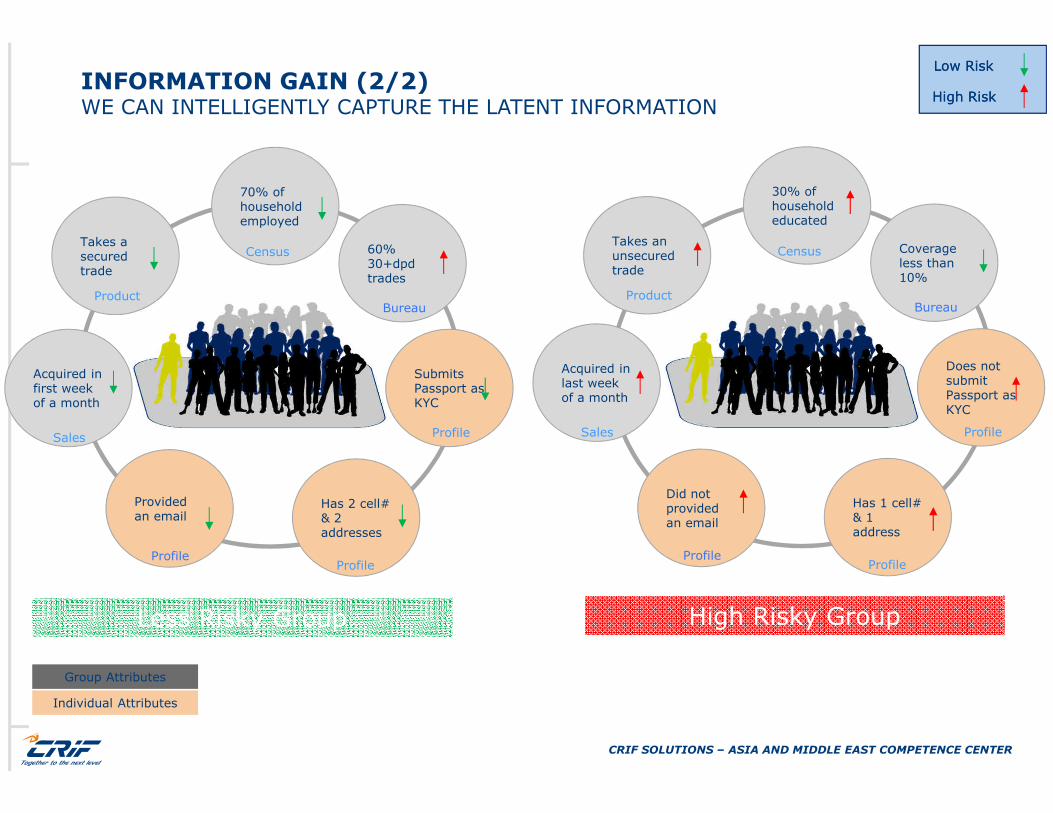

INFORMATION GAIN (2/2)WE CAN INTELLIGENTLY CAPTURE THE LATENT INFORMATION

Takes a secured trade

Has 2 cell# & 2 addresses

Provided an email

Acquired in first week of a month

Submits Passport as KYC

60% 30+dpd trades

70% of household employed

Census

ProductBureau

ProfileSales

ProfileProfile

High Risky GroupLess Risky Group

Takes an unsecured trade

Has 1 cell# & 1 address

Did not provided an email

Does not submit Passport as KYC

Coverage less than 10%

30% of household educated

Census

ProductBureau

Profile

ProfileProfile

Acquired in last week of a month

Sales

Group Attributes

Individual Attributes

Low RiskLow Risk

High RiskHigh Risk

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

BENEFITS

Increased match rate Default Rate Segregation

Significant differentiation in default rates

Significant differentiation in default rates

• Simple solutions to provide discriminatory scores for the entire customer base

• Can also be applied for low bureau tenure customers

• Default rates are usually high for ‘new to credit’ ~15%

• Will have the ability to segment

7x

Population Split 20% 80%

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

“NO-HIT” SCORE, an example from India

“WATER” SCORE, an example from Italy

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

PROJECT BACKGROUND

One consequence of the current economic situation is credit restriction

For a part of the population, the difficulty in accessing credit is linked to a lack of credit information in the Eurisc credit reporting system

Can access to credit be made easier through good management of water bill payments?

11

22

33

How can we help those (few) new applicants with no / “thin” credit history in EURISC?How can we help those (few) new applicants with no / “thin” credit history in EURISC?

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

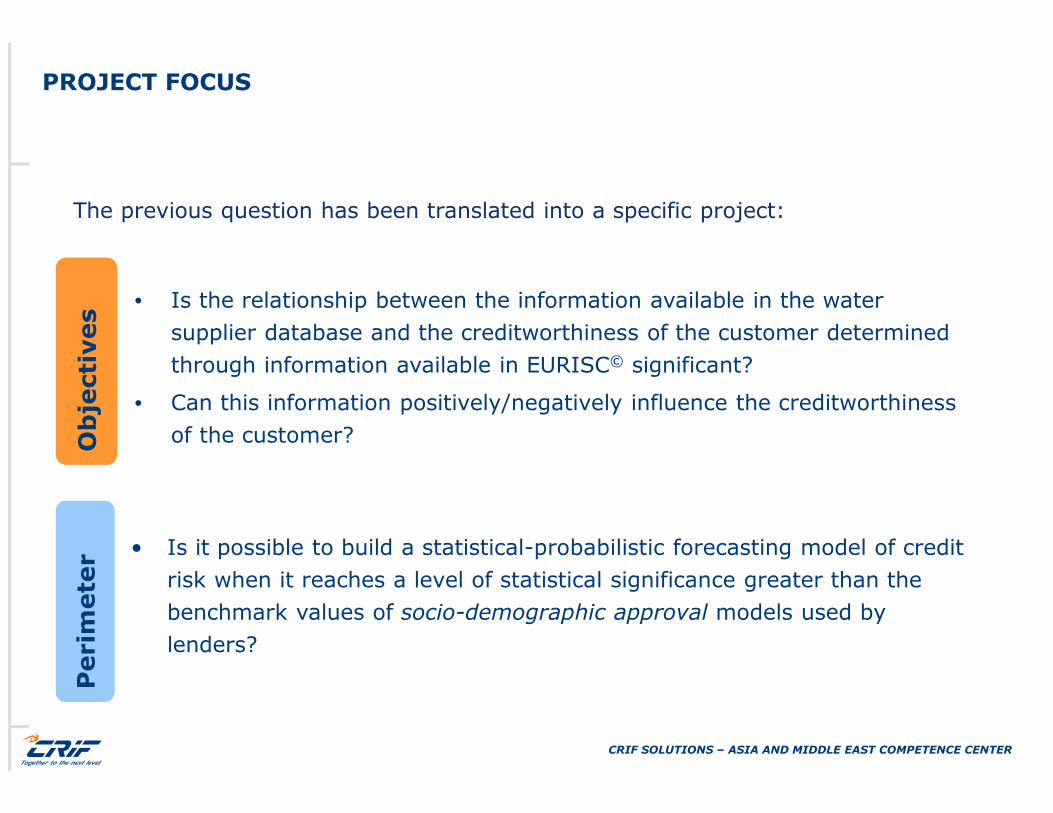

PROJECT FOCUS

• Is the relationship between the information available in the water

supplier database and the creditworthiness of the customer determined

through information available in EURISC© significant?

• Can this information positively/negatively influence the creditworthiness

of the customer?

The previous question has been translated into a specific project:

Ob

jecti

ves

Ob

jecti

ves

Perim

ete

rP

erim

ete

r • Is it possible to build a statistical-probabilistic forecasting model of credit

risk when it reaches a level of statistical significance greater than the

benchmark values of socio-demographic approval models used by

lenders?

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

THE DATA CONNECTION

• An Italian water supplier (WS) has provided CRIF with a database of

information relating to its residential customers, through which the candidate

variables used to develop statistical forecasting models are calculated

WSResidentialCustomerDB

Hashing

• Predictive information • Definition of performance

• Building of estimation sample

Is there correlation between the WS information and the creditworthiness of the customer?

EURISC©

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

DEVELOPMENT SAMPLE

WS data used for the estimation

April X December X+8

time

Date of first entry in Eurisc©

WS data cover a period of 8 years

July X+6 June X+8

1

2

3

4

5

Sample Window(t0 )

June X+9

Eurisc data observation

1 – Excluded from the development sample because there is no credit history in Eurisc© (performance cannot be calculated) / Used for Model Validation

2 – Excluded from the development sample because no payment history with WS before t0

3 –Excluded from the development sample because entered in Eurisc before the window chosen for t0

4 , 5 – Included in the development sample

WS Customer

Performance window in EURISC

Sample Window

WS Data Perimeter

Performance Observation

No credit history

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

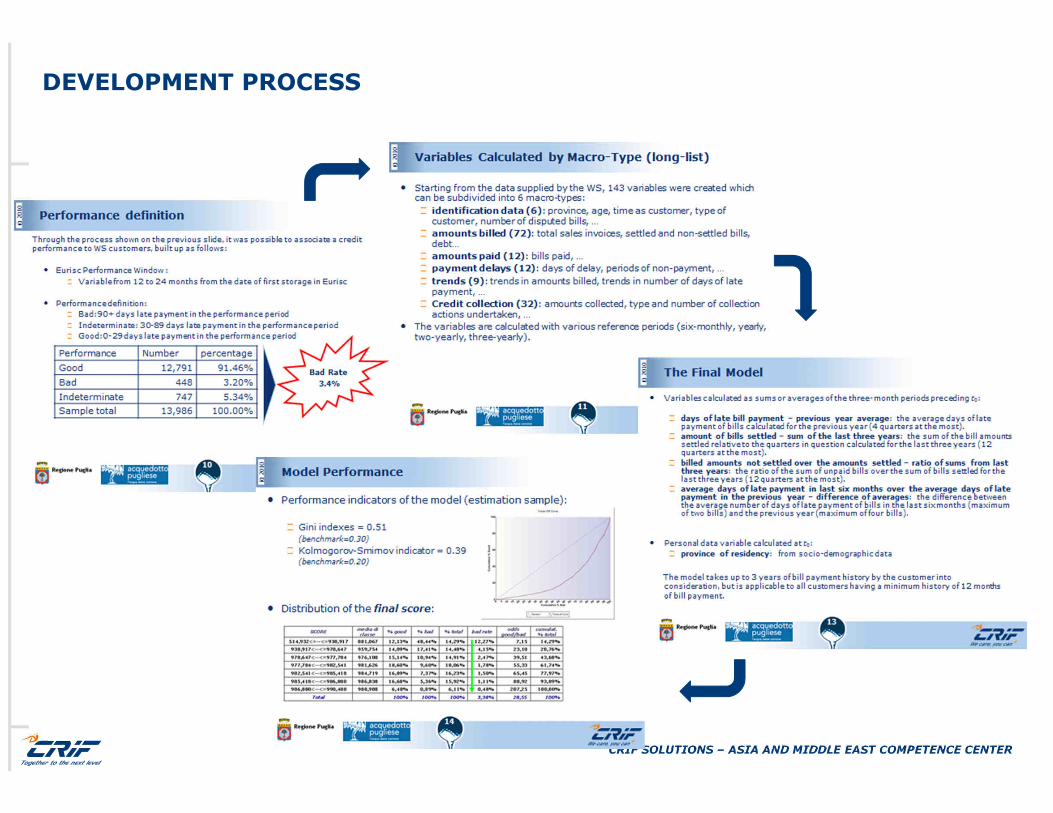

DEVELOPMENT PROCESS

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

RESULTS

• The answer to our initial questions is yes: WATER SUPPLY data allows a positive assessment to be assigned to customers who pay bills regularly and punctually.

• In particular for 83% of people without credit data, the certification obtained through utility bill payment data could make it easier for them to obtain credit.

• In conclusion, a 'good' customer that finds it difficult to access credit through traditional channels, could benefit from the application of this model and receive a positive evaluation in relation to their potential ability to repay.

Certified by WS

SCORE Media di

Classe

% in

classe Classe

Bad Rate

Atteso

514.932<=--<=938.917 881.067 7.15% 1 12.27%

938.917<--<=970.647 959.753 9.69% 2 4.15%

970.647<--<=977.784 976.107 16.10% 3 2.47%

977.784<--<=982.541 981.626 19.02% 4 1.78%

982.541<--<=985.418 984.718 10.26% 5 1.50%

985.418<--<=986.880 986.838 30.92% 6 1.11%

986.880<--<=990.488 988.987 6.85% 7 0.48%

CRIF SOLUTIONS – ASIA AND MIDDLE EAST COMPETENCE CENTER

Examples

CB BASED ANALYTICS FOR THE END-TO-END CREDIT MANAGEMENT

Engage Originate Manage Collect

Govern

Assess risks

Comply

Manage people

Priv

ate

an

d c

on

fiden

tial

www.crif.com

Analytics, Risk management, Credit processes

CRIF CREDIT SOLUTIONS

A team of high skilled people, with a deep knowledge and a wide internationalexperience on credit risk management and analytics. We deliver best practicesdecision strategies and operational processes for top players clients withinfinancial services, telcos and utilities industries in more than 30 countries overthe world.

Atlanta – Bologna – Dubai - Istanbul - London – Pune – Prague

Ubaldo TambiniCredit Solutions Director

Asia and Middle East

'48 Burj Gate', Downtown Burj Khalifa, Shaikh Zayed Road, Dubai, UAE

E-mail: [email protected]: +39 3351209311