Embed Size (px)

Citation preview

Global Industrials & EU Autos Conference

Creating Long Term Value for Shareholders

March 17, 2015

Joy Global

March 2015 2015 Global Industrials & EU Autos Conference2

© 2015 Joy Global Inc. All rights reserved

All statements in this presentation other than historical facts are forward looking statements within the

meaning of the Private Securities Litigation Reform Act of 1995 and involve risks and uncertainties that

may cause actual results to differ materially from those indicated by such forward looking statements.

These statements are identified by forward looking terms such as “anticipate,” “believe,” “estimate,”

“expect,” “indicate,” “may be,” “objective,” “plan,” “predict,” “will be,” and similar expressions. Such

statements are based on our current expectations and we undertake no obligation to update such

statements to reflect new information, events, or otherwise. In addition to the assumptions and other

factors referred to in this presentation, cautionary factors and other information are set forth in our

public filings with the Securities and Exchange Commission, including those set forth under “Risk

Factors” in our Annual Report on Form 10-K and Quarterly Reports on Form 10-Q.

Non-GAAP Measures: The company from time to time refers to various non-GAAP financial measures.

We believe that this information is useful to understanding the operating results and ongoing

performance of our underlying businesses. See our public filings in the investor relations section of our

website www.joyglobal.com for reconciliations of material non-GAAP financial measures to their

related GAAP measures.

Forward Looking Statements

March 2015 2015 Global Industrials & EU Autos Conference3

© 2015 Joy Global Inc. All rights reserved

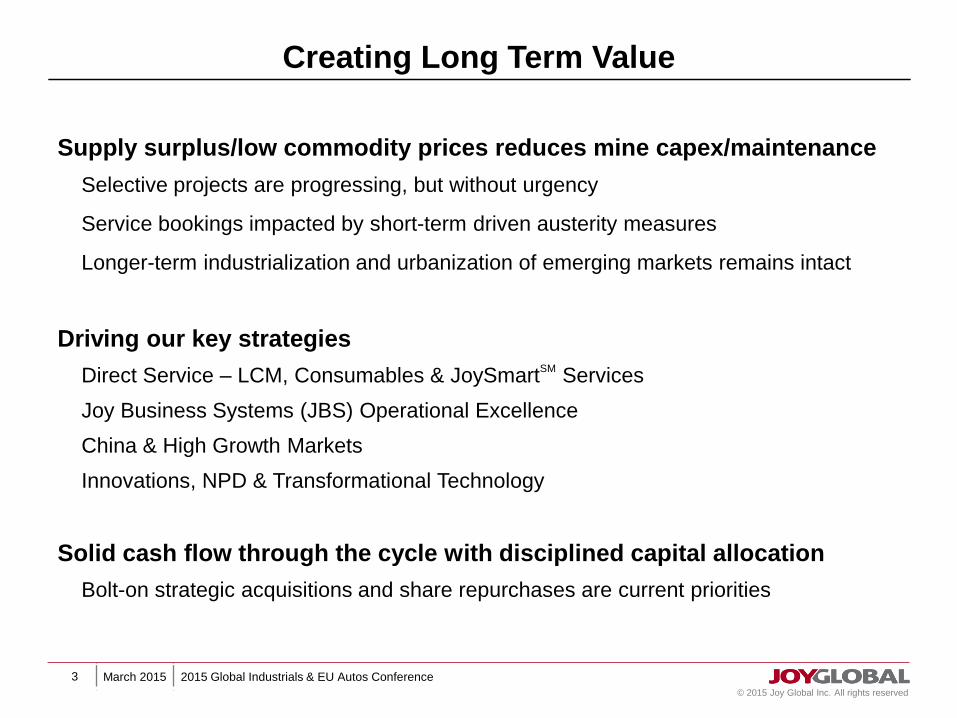

Driving our key strategies

Direct Service – LCM, Consumables & JoySmartSM

Services

Joy Business Systems (JBS) Operational Excellence

China & High Growth Markets

Innovations, NPD & Transformational Technology

Solid cash flow through the cycle with disciplined capital allocation

Bolt-on strategic acquisitions and share repurchases are current priorities

Supply surplus/low commodity prices reduces mine capex/maintenance

Selective projects are progressing, but without urgency

Service bookings impacted by short-term driven austerity measures

Longer-term industrialization and urbanization of emerging markets remains intact

Creating Long Term Value

March 2015 2015 Global Industrials & EU Autos Conference4

© 2015 Joy Global Inc. All rights reserved

March 2015 2015 Global Industrials & EU Autos Conference5

© 2015 Joy Global Inc. All rights reserved

Hard Rock

Mining Systems

Drills Draglines

Shovels

Loaders

Conveyor SystemsHybrid Shovels/Excavators

Surface CM

Systems

Joy Truckless

Mining Systems

Crushing & Conveying

Longwall Systems

Continuous

Miners

Entry Development

LHDs

Flexible

Conveyor

Trains

Joy Global’s Mine Map of the Future

Market-Leading Full-System Solutions

March 2015 2015 Global Industrials & EU Autos Conference6

© 2015 Joy Global Inc. All rights reserved

Total Joy Global Sales (last 12 months)

Global Leader in…

Americas

North: 38%

Latin America: 21%

China: 10%

Australasia: 15%

Eurasia: 7%

Africa: 9%

Original

Equipment: 30%

Consumables: 8%

Service: 62%

Coal: 59%

Other: 7%Gold: 1%Potash / Salt: 1%

Oil Sands: 3%

Iron Ore: 8%

Copper: 20%

Tunneling: 1%

Commodities We Serve

Life Cycle Management

Geographies We Service

March 2015 2015 Global Industrials & EU Autos Conference7

© 2015 Joy Global Inc. All rights reserved

Source: IEA, EIA, Energy Annual, ICSG, LME, World Bank Development Indicators, World Energy Outlook 2014

1

72768

62123

1774

8

1101

190

18

431

Half the world’s population does not have adequate access to electricity

99

71

121 Lacking adequate electricity (GW)

Have no electricity

Millions of People

Coal capacity under construction

Increasing urbanization rates will drive demand

for electricity and electrical infrastructure

'12 '20 '25 '30 '35 '40

Liquids Nuclear Renewables Nat Gas Coal

12

0

100

200

'00 '10 '25

0

100

200

'00 '10 '25

CopperThermal Coal

China Rest of WorldIndia

Coal Remains a Prominent Source

For Electricity Generation

Urbanization Populations Lead to

Higher Commodity Demand

China & India Driving

Commodity Demand (2010 = 100)

The World Needs More Energy & Minerals

March 2015 2015 Global Industrials & EU Autos Conference8

© 2015 Joy Global Inc. All rights reserved

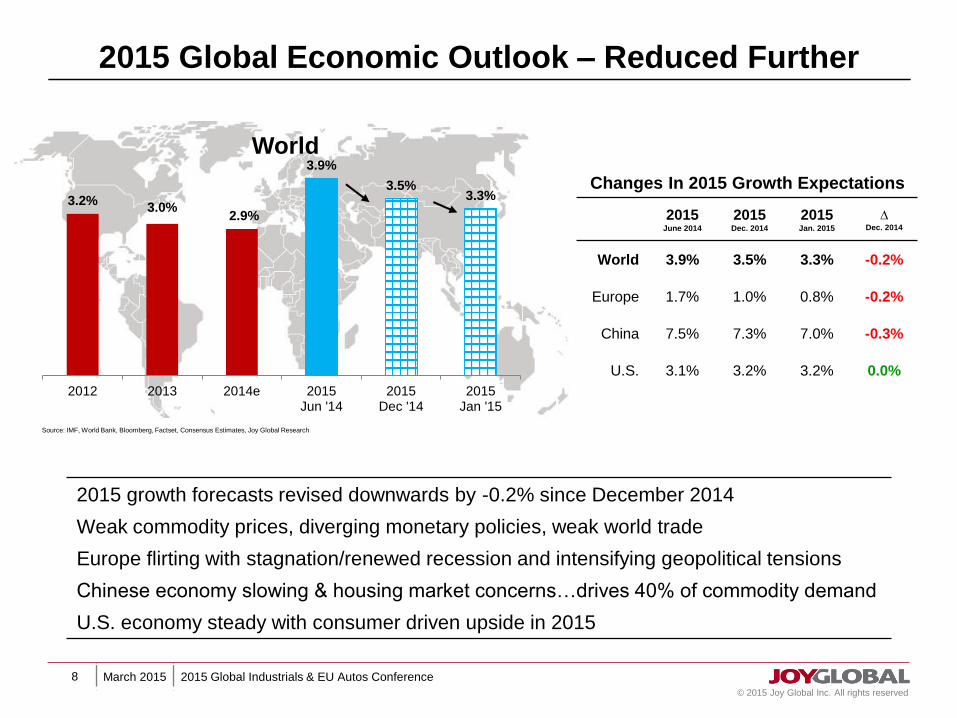

3.2%3.0%

2.9%

3.9%

3.5%3.3%

2012 2013 2014e 2015Jun '14

2015Dec '14

2015Jan '15

World

Changes In 2015 Growth Expectations

2015June 2014

2015Dec. 2014

2015Jan. 2015

∆ Dec. 2014

World 3.9% 3.5% 3.3% -0.2%

Europe 1.7% 1.0% 0.8% -0.2%

China 7.5% 7.3% 7.0% -0.3%

U.S. 3.1% 3.2% 3.2% 0.0%

2015 growth forecasts revised downwards by -0.2% since December 2014

Weak commodity prices, diverging monetary policies, weak world trade

Europe flirting with stagnation/renewed recession and intensifying geopolitical tensions

Chinese economy slowing & housing market concerns…drives 40% of commodity demand

U.S. economy steady with consumer driven upside in 2015

Source: IMF, World Bank, Bloomberg, Factset, Consensus Estimates, Joy Global Research

2015 Global Economic Outlook – Reduced Further

March 2015 2015 Global Industrials & EU Autos Conference9

© 2015 Joy Global Inc. All rights reserved

Global Copper Markets: Near-Term Price Pressure

Copper Prices ($/lb.) Near-Term Price Pressure

Reduced economic outlook pressuring prices;

hovering around $2.65/lb (-8% since Dec. 1)

Demand exposure to Chinese construction & semi-

conductors sectors remains largest threat

Near-term macro fear outweighing fundamentals:Market in deficit of ~640,000 tonnes through Nov.

Global inventories at 1.02mt ⬇38% from peak (Apr. ’13)

Global Copper Production - LTM

Long-Term Fundamentals Remain Strong

New supply growth forecast to drive market to average

surplus of ~355,000 tonnes in ‘15 & ‘16

Market returns to longer-term deficit driven by global

growth & slowing investment in new capacity

Structural headwinds; declining ore grades, labor

disputes, ore deposits going underground14

15

16

17

18

19

Jan-07 Aug-08 Mar-10 Oct-11 May-13 Dec-14

Million tonnes

Mined Copper Production Run-Rate ⬇1.1%

Global copper production LTM run-rate @ 18.43mt,

down 1.1% from 18.64mt

Mined copper production (LTM-basis) ⬇1.8% and

⬇4.0% in Chile and Peru respectively since June

$2.40

$2.50

$2.60

$2.70

$2.80

$2.90

$3.00

12/1/14 1/1/15 2/1/15 3/4/15

March 2015 2015 Global Industrials & EU Autos Conference10

© 2015 Joy Global Inc. All rights reserved

US Coal: Headwinds Persist

US Coal Production (mt)

Nat. Gas Forward Curves ($/mmBtu)

US Coal Consumption Electric Power Sector (mt)

US Coal Consumption Facing Headwinds in 2015

Power plant closures and MATS implementation

Heating-degree days ~4% above 10-year ave

Coal burn ⬇0.5% in 2014 (~4mt); declines 5% (45mt) in ‘15

Exports ⬇16% in ’14 @ 98mt; decline 8% to ~90mt in ’15

Q1 Production Down; Full-Year Expected Down ~25mt

Coal production 996mt in 2014; ⬆1.2% year-over-year

US production down ~1% through Feb

Falling natural gas prices, decreased exports, mild winter

Full-year 2015 coal production expected down ~25mt

Natural Gas Forward Curve Shifting Downward

Natural gas spot at $2.79/mmBtu March 2nd

Record gas production swells inventories, ⬆5% to 10-yr ave

Forward curve for 2015 points to $3.01/mmBtu

PRB competitive; ILB coal under additional pressures

1043 1039

932

973

931

823

861 857

816 825

650

750

850

950

1050

1150

2007 2008 2009 2010 2011 2012 2013 2014 2015e 2016e

2.00

2.50

3.00

3.50

4.00

4.50

Feb-15 Oct-15 Jun-16 Feb-17 Oct-17

Current

1-Month Ago

3-Months Ago

85.8

70.970

75

80

85

90

95

100

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2010 - 2014 5-Yr Ave

2014 2015

March 2015 2015 Global Industrials & EU Autos Conference11

© 2015 Joy Global Inc. All rights reserved

Seaborne Coal & Iron Ore Markets Remain Oversupplied

Thermal Coal Remains Near 5-Lows

Current prices at ~$64/t; ~30% of thermal coal @ loss

Oversupply to exist through 2015 (Aus. & Indonesia)

60% of Indian power plant’s; < than 7 days of coal

Mine closures, pricing pressure, reduce costs

Met Coal Q1 ‘15 Contract Down QoQ At $117/t

Spot prices range bound between $110 and $120

>50% of global producers underwater

Supply response slower than expected

Globally ~26mt of met coal curtailments

~15mt more needed to balance market

Cuts expected to improve pricing in 2H 2015

Seaborne Thermal Coal ($/t)

Seaborne Met Coal ($/t)

Iron Ore Prices Touch 5-Year Lows

Current prices at ~$65/t; lowest since June 2009

~65mt of Chinese iron ore being idled/closed

Iron ore prices ⬇~48% in 2014

Structural support level between $65 and $80

“Sticky” Chinese production…getting stickier as Beijing

contemplates tax cuts on domestic production

Iron Ore ($/t)

100

120

140

160

180

Jan-13 Feb-14 Mar-15

$/tonne

Spot HCC

Forecast HCC

Quarterly Contract

50

60

70

80

90

100

110

120

Mar-12 Dec-12 Sep-13 Jun-14 Mar-15

NWE marker CIF

Richards Bay FOB

Newcastle FOB

$40

$80

$120

$160

Jan-13 Jun-13 Nov-13 Apr-14 Sep-14 Feb-15

March 2015 2015 Global Industrials & EU Autos Conference12

© 2015 Joy Global Inc. All rights reserved

China Coal Market ConsolidatingChinese Electricity Consumption LTM

Chinese Coal Prices

Chinese Domestic Coal Production (mt)

Source: IHS Energy, CCM

4200

4600

5000

5400

Jan-12 Dec-12 Nov-13 Oct-14

Billion kWh

150

200

250

300

350

400

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2009 - 2013 2013 2014

Chinese Electricity Production Slowing…

Electricity production ⬆4.9% in ’14 vs. ⬆8.2% in ‘13

Thermal power ~77% of Chinese electricity production

down from 82% in 2011

Hydro generation and alternative sources gaining share

Coal consumption ⬇2.1% through Nov (@ 3.65bt)

Chinese Coal Market Facing Supply Controls…

Government policies curb output ~85mt (Aug – Dec)

Production ⬇~2.5% in 2014 at ~3.6bt

Further cuts expected in 2015 as oversupply remains

Stricter import restrictions began January 1st; delays at

ports as imported materials are facing higher quality

requirements and testing before transport

Chinese coal imports at 291mt in 2014 (⬇11% YoY);

headwinds into 2015 as regulations take hold

Prices likely have bottomed but marginal upside exists;

prices ⬇~16% YTD, but ⬆~6% since early-October

March 2015 2015 Global Industrials & EU Autos Conference13

© 2015 Joy Global Inc. All rights reserved

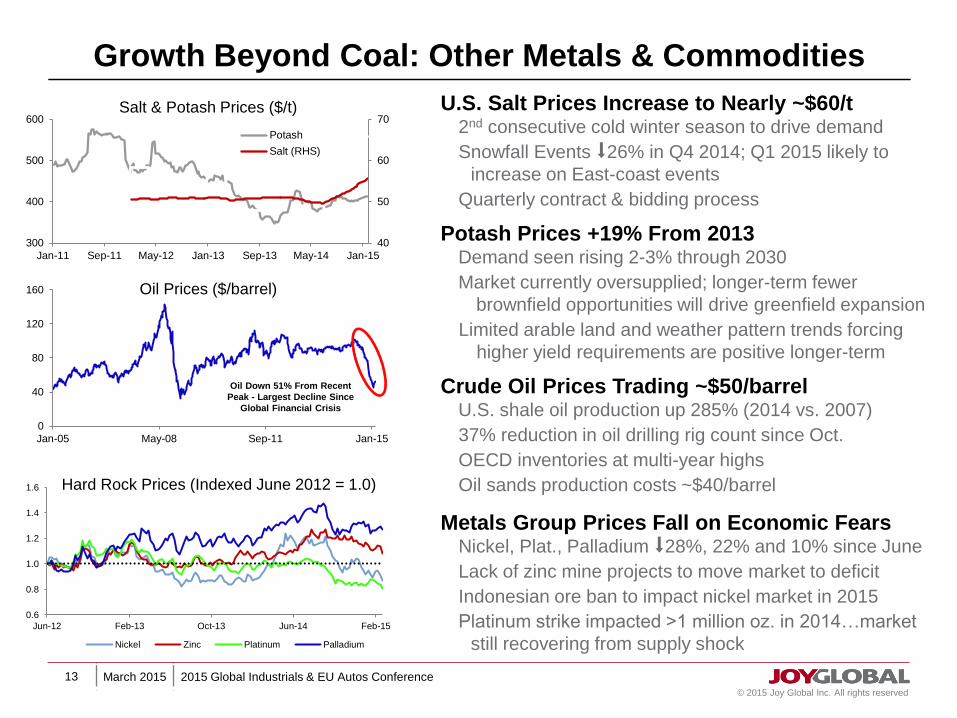

Growth Beyond Coal: Other Metals & Commodities

Salt & Potash Prices ($/t)

Hard Rock Prices (Indexed June 2012 = 1.0)

Crude Oil Prices Trading ~$50/barrelU.S. shale oil production up 285% (2014 vs. 2007)

37% reduction in oil drilling rig count since Oct.

OECD inventories at multi-year highs

Oil sands production costs ~$40/barrel

Metals Group Prices Fall on Economic FearsNickel, Plat., Palladium ⬇28%, 22% and 10% since June

Lack of zinc mine projects to move market to deficit

Indonesian ore ban to impact nickel market in 2015

Platinum strike impacted >1 million oz. in 2014…market

still recovering from supply shock

U.S. Salt Prices Increase to Nearly ~$60/t2nd consecutive cold winter season to drive demand

Snowfall Events ⬇26% in Q4 2014; Q1 2015 likely to

increase on East-coast events

Quarterly contract & bidding process

Oil Prices ($/barrel)

0.6

0.8

1.0

1.2

1.4

1.6

Jun-12 Feb-13 Oct-13 Jun-14 Feb-15

Nickel Zinc Platinum Palladium

0

40

80

120

160

Jan-05 May-08 Sep-11 Jan-15

Oil Down 51% From Recent

Peak - Largest Decline Since

Global Financial Crisis

40

50

60

70

300

400

500

600

Jan-11 Sep-11 May-12 Jan-13 Sep-13 May-14 Jan-15

Potash

Salt (RHS)

Potash Prices +19% From 2013 Demand seen rising 2-3% through 2030

Market currently oversupplied; longer-term fewer

brownfield opportunities will drive greenfield expansion

Limited arable land and weather pattern trends forcing

higher yield requirements are positive longer-term

March 2015 2015 Global Industrials & EU Autos Conference14

© 2015 Joy Global Inc. All rights reserved

Joy Global Service Strategy

Understand the MarketDefine the market and our ability to provide a competitive advantage

Solve our Customer’s Toughest Challenges

Focus on most costly and critical issues

Keep people out of harm’s way

Offer Compelling Solutions

Significant payback

< 3 years, preferably < 1 year

Deliver the Best Solution, Product and System

Joy Global Brand Promise

Every Customer is a ReferenceSM

Provide exceptional service

Delight the customer

Superior

Products

Smartly

Connected

Diverse

Experts

Smart

Products

World-class

Performance

Lowest

Cost per Ton

March 2015 2015 Global Industrials & EU Autos Conference15

© 2015 Joy Global Inc. All rights reserved

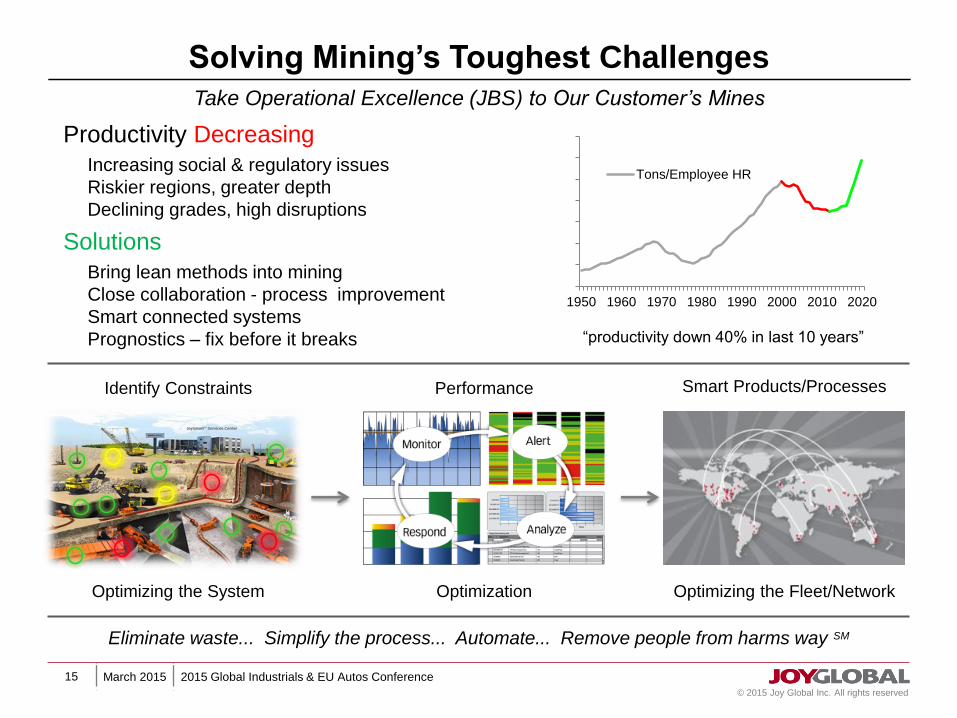

Solving Mining’s Toughest Challenges

Identify Constraints

Optimizing the System Optimizing the Fleet/Network

Smart Products/ProcessesPerformance

Take Operational Excellence (JBS) to Our Customer’s Mines

Productivity Decreasing

Increasing social & regulatory issues

Riskier regions, greater depth

Declining grades, high disruptions

Solutions

Bring lean methods into mining

Close collaboration - process improvement

Smart connected systems

Prognostics – fix before it breaks “productivity down 40% in last 10 years”

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

1950 1960 1970 1980 1990 2000 2010 2020

Tons/Employee HR

Eliminate waste... Simplify the process... Automate... Remove people from harms way SM

Optimization

March 2015 2015 Global Industrials & EU Autos Conference16

© 2015 Joy Global Inc. All rights reserved

Strategies: Creating Competitive Advantage

Safety • Time • Cost • Quality • Customer Satisfaction

World-Class

COE’s

JBS Operational Excellence

Consistent global world-class components, processes,

methods, and metrics throughout the global network with

the ability to rapidly customize locally

Direct Service

Hard Rock Mining Systems

Innovations Creating Growth

MTI New LHD’s

Transformational Technology

China & High Growth Markets

Accelerating our Competitive Advantage in China

LCM Consumables JoySmartTM Services Zero Harm • Velocity • Productivity • Quality • References

Lead with Service

$8B Market$2B Market

March 2015 2015 Global Industrials & EU Autos Conference17

© 2015 Joy Global Inc. All rights reserved

Technologies: Creating New Revenue Streams

Hardrock Mining Systems

Innovations creating growth

Hybrid Shovel / Excavator

Electric Rope Shovel competitive advantage

• Long-life, reliable, lowest TCO

Diesel/Electric Hybrid

• Smaller, fuel efficient, flexible

• ~3% increase in availability

• ~15% lower total cost of ownership

Hard Rock

MTI Acquisition

New LHD’s and transformational technology

High Performance Low Seam Longwall

Unique solutions for low seams

• Highest productivity/lowest TCO

• 40% increase production

• 70% reduction in manpower

March 2015 2015 Global Industrials & EU Autos Conference18

© 2015 Joy Global Inc. All rights reserved

One Joy Global: Focused on the Customer

Direct to customers & markets

World class Products, Service,

Processes, People and Financials

Accelerating cost reduction programs

Savings exceeding targets

-$29-$22

-$10 - $20

$40

$75

$50$52

$81

-40

-20

0

20

40

60

80

100

FY13 FY14 FY15

$ MillionsAnnounced Cost

Announced Savings

Actual Savings

March 2015 2015 Global Industrials & EU Autos Conference19

© 2015 Joy Global Inc. All rights reserved

Joy Global Direct Service NetworkEvery Customer is a ReferenceSM

Consistent global world-class

components, processes, methods and

metrics throughout the global network with

the ability to rapidly customize locally

Surface

Hard Rock

Underground

Flawless from the Start

JBS Operational ExcellenceProducts/Process/People

Life Cycle Management

Prognostics & Health

Management

Performance

Life Cycle Management

March 2015 2015 Global Industrials & EU Autos Conference20

© 2015 Joy Global Inc. All rights reserved

0%

10%

20%

30%

40%

FY05 FY08 FY11 FY14

Trade Working Capital Velocity(TWC % Sales)

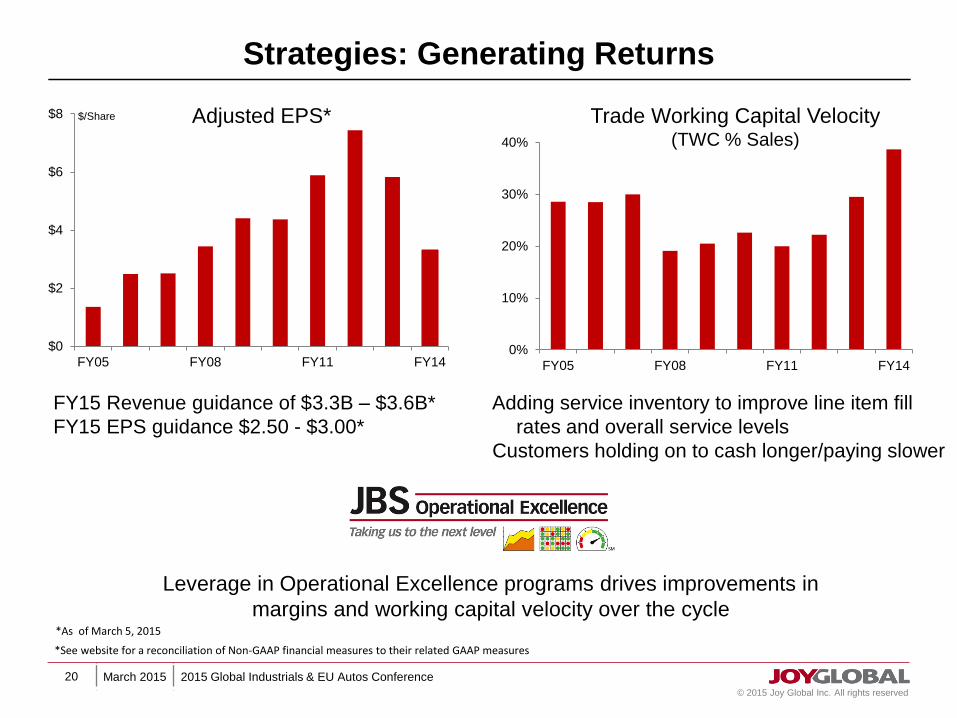

Strategies: Generating Returns

Adding service inventory to improve line item fill

rates and overall service levels

Customers holding on to cash longer/paying slower

$0

$2

$4

$6

$8

FY05 FY08 FY11 FY14

$/Share Adjusted EPS*

Leverage in Operational Excellence programs drives improvements in

margins and working capital velocity over the cycle

FY15 Revenue guidance of $3.3B – $3.6B*

FY15 EPS guidance $2.50 - $3.00*

*See website for a reconciliation of Non-GAAP financial measures to their related GAAP measures

*As of March 5, 2015

March 2015 2015 Global Industrials & EU Autos Conference21

© 2015 Joy Global Inc. All rights reserved

$0

$200

$400

$600

$800

$1,000

2007 2008 2009 2010 2011 2012 2013 2014

$ Millions

$0

$100

$200

$300

2008 2010 2012 2014 2016e

$ Millions

Cash Flow: Solid Throughout the Cycle

Adjusted Cash from Ops Before Pension Contribution

$0

$200

$400

$600

2007 2009 2011 2013 2015 2017

$ Millions Unfunded

Pension Liability

CAPEX

Strategies coupled with profitability & asset

efficiency deliver solid cash flow

Cash from operations before pension

contributions FY15: 10-15% of revenues

Dividend raised to $0.20 in June 2014; 14%

increase

~$50M per year cash contribution

OpEx, NPD, Service Footprint

March 2015 2015 Global Industrials & EU Autos Conference22

© 2015 Joy Global Inc. All rights reserved

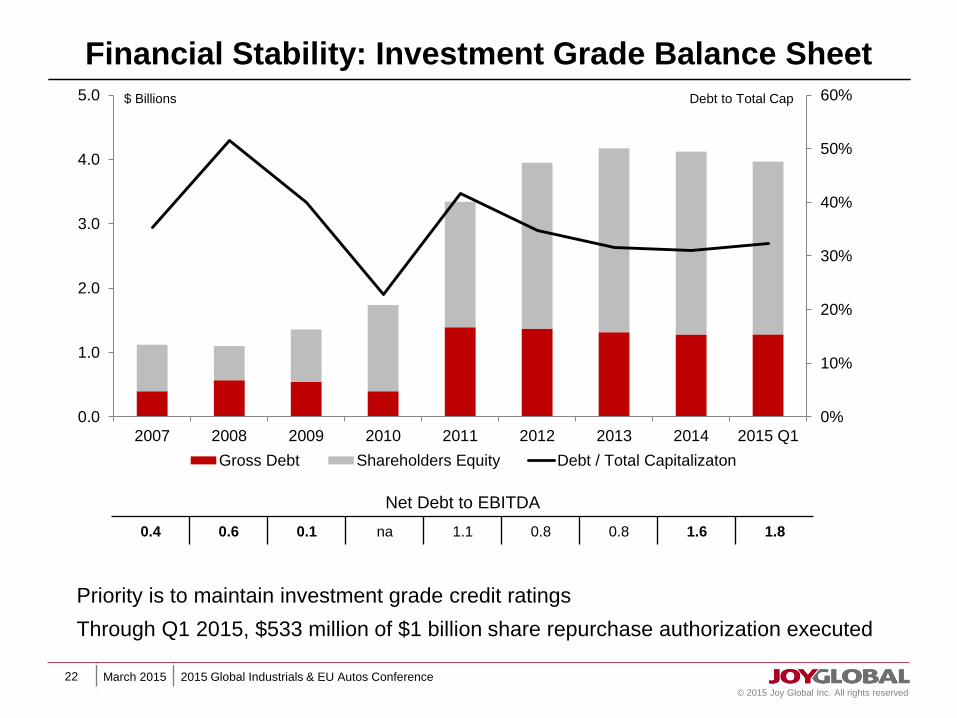

Financial Stability: Investment Grade Balance Sheet

0%

10%

20%

30%

40%

50%

60%

0.0

1.0

2.0

3.0

4.0

5.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 Q1

Debt to Total Cap$ Billions

Gross Debt Shareholders Equity Debt / Total Capitalizaton

Priority is to maintain investment grade credit ratings

Through Q1 2015, $533 million of $1 billion share repurchase authorization executed

Net Debt to EBITDA

0.4 0.6 0.1 na 1.1 0.8 0.8 1.6 1.8

March 2015 2015 Global Industrials & EU Autos Conference23

© 2015 Joy Global Inc. All rights reserved

Creating Long Term Value

23

Industry-leading product positions

R&D and acquisitions enhance product range and leveraging systems

Investments expand position in underground hard rock & high growth markets

Industry-leading service infrastructure

Based on Life Cycle Management

Direct service network extended by JoySmartTM

Services

Financial strength

Strong balance sheet and solid margins/cash flow

Managing long-term performance

Operational efficiency

High growth market strategies

Investing in technologies that unlock value for customers and create growth

JOY:NYSE

100 E. Wisconsin Ave.Suite 2780

Milwaukee, WI 53202 USA

www.joyglobal.com