Embed Size (px)

DESCRIPTION

CPA Report Third Edition 2010

Citation preview

CPA ReportSouth Carolina Association of Certified Public Accountants

T h i r d E d i t i o n 2 0 1 0

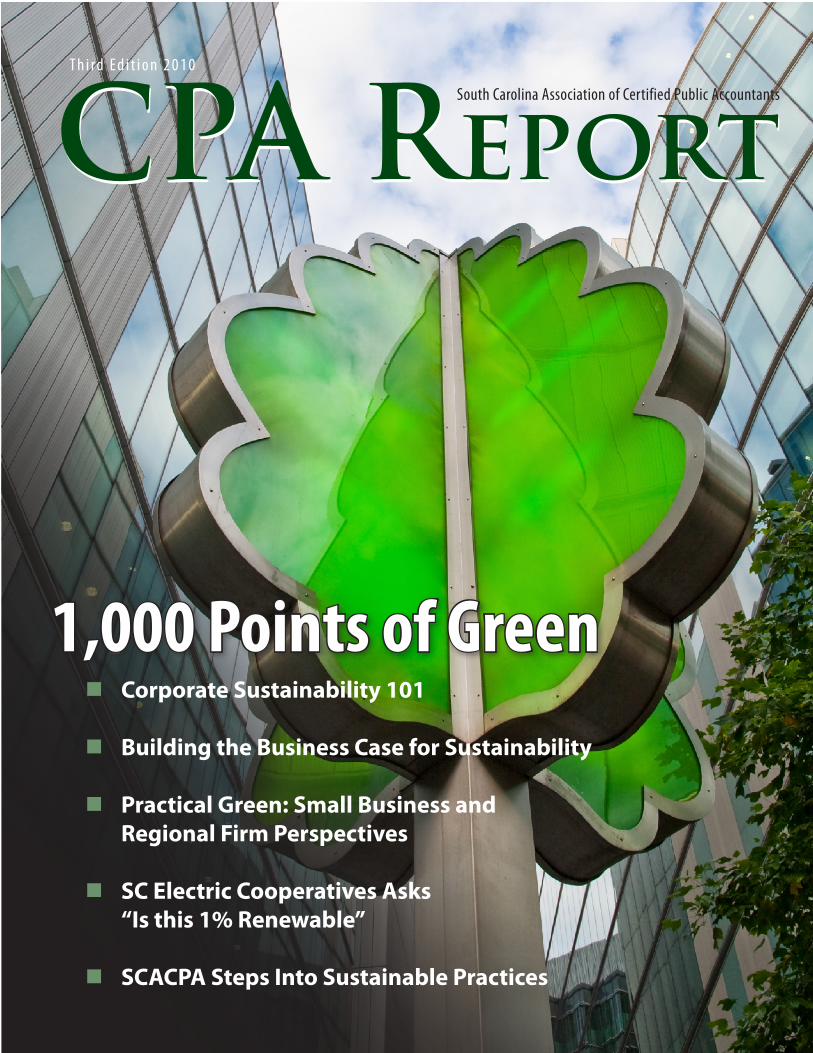

Corporate Sustainability 101

Building the Business Case for Sustainability

Practical Green: Small Business and Regional Firm Perspectives

SC Electric Cooperatives Asks “Is this 1% Renewable”

SCACPA Steps Into Sustainable Practices

1,000 Points of Green

CPA Report

South Carolina CPA Report 2 (888) 557-4814 | www.scacpa.org

Charleston 2430 Mall Drive, Suite 360 Greenville

843-884-3912 Charleston, SC 29406 864-245-8788

www.american-pensions.com

South Carolina CPA Report 3(888) 557-4814 | www.scacpa.org 33

Special Section: 1,000 Points of Green

In This Issue

In Every Issue5 From the President

6 Association News

8 On Your Behalf

24 Member Profiles

27 Board of Accountancy News

30 Chapter Connections

32 Member News

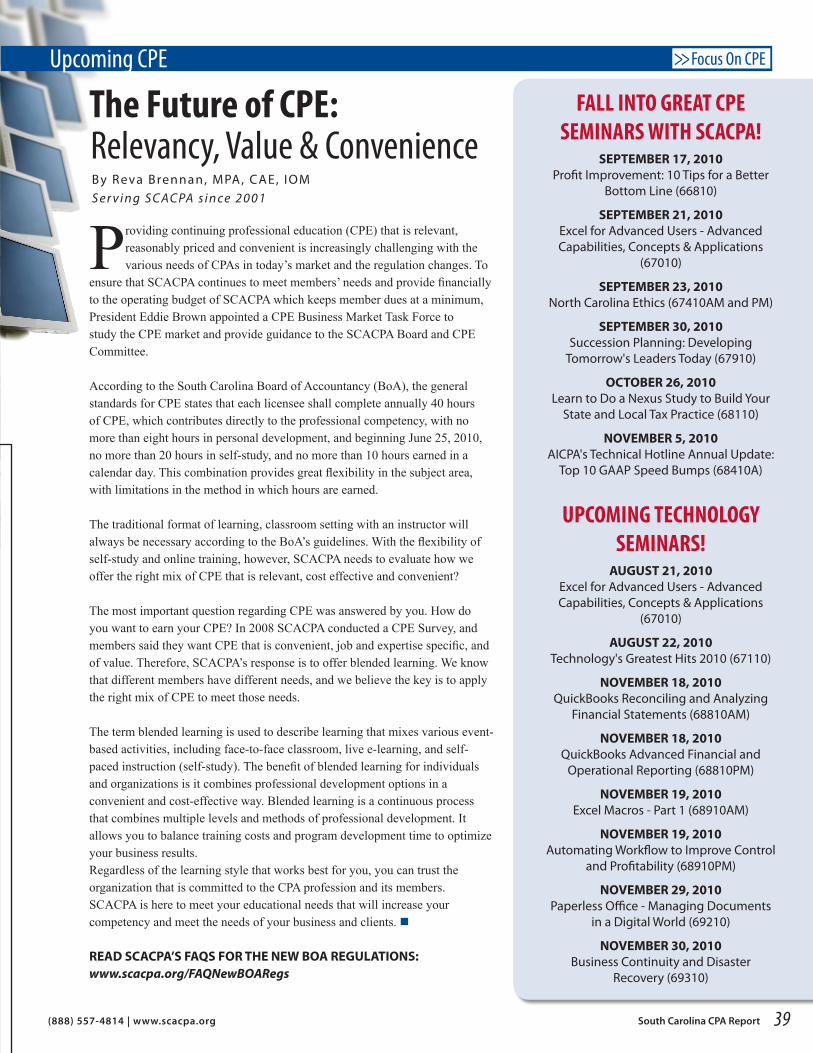

39 Upcoming CPE

42 Classifieds/Advertiser Index

11 Introduction: Sustainability and the CPA

12 Corporate Sustainability 101

14 Building the Business Case for Sustainability

17 Practical Green: Small Business and Regional Firm Perspectives

20 South Carolina Electric Cooperatives “Walk the Talk” on

Energy Efficiency and Renewables

22 SCACPA Steps Into Sustainable Practices

24 Member Profiles: Meet Members of the Sustainability Task Force

26 Report on Spring 2010 Meeting of AICPA Council

28 Essential Overview of Peer Review and Accounting Matters

34 CPA Day at the State House

35 Oath Ceremony Users New CPAs Into the Profession

36 Health Care Reform Series, Part I

OFFICERSCharles E. “Eddie” Brown, CPA, President

Timothy L. Baker, CPA, President Elect

Michael R. Putich, CPA, Vice President

Sharon E. Mann, CPA, Secretary-Treasurer

Charles M. Redfern III, CPA, Past President

BOARD OF DIRECTORSClarence Coleman Jr., CPA, Ph.D.

Alys Anne Dennis, CPAJ. Bratton Fennell, CPA

Malynda M. Grimsley, CPAPenny A. Lewis, CPA

A. D. “Dave” Masters, CPAJ. Patrick McDermott, CPA

James W. McIlrath, CPAWilliam C. Robinson, CPA

L. Kent Satterfield, CPAPhilip R. Snipes, CPA

Michael J. Targia, CPA, CFARobert M. Tilton, CPAJada C. McAbee, CPABeth T. Zamorski, CPA

EXECUTIVE DIRECTOR Erin P. Hardwick, CAE

EDITORKatherine M. Swartz, CAE

ASSISTANT EDITORAllison K. Caldwell

GRAPHIC DESIGNER Lisa S. McGee

CONTRIBUTING wRITERSReva Brennan, MPA, CAE, IOM

Ronald J. Calcaterra William M. Grooms, PhD, CPA John F. Hamilton, CPA, CMA

Erin P. Hardwick, CAE Mark T. Hobbs, CPA

Anthony G. Masino, JD, CPA J. Patrick McDermott, CPA

John J. Meindl Jr. Mark Riley

Derrick B. Stark, CPA V. Carroll Webster, MBA, CPA

2010 EDITORIAL BOARDMargaret L. Lattimore, CPA, Chair

Ellen K. Adkins, CPA, MBACharles E. Alvis, CPA, MPA, MBA

John B. Brantley, CPAJackie F. Breland, CPA

Neil A. Brown, CPA, MAcc, CFPAmanda S. Colgate, CPA

Lisa S. Cooke, CPAMalynda M. Grimsley, CPA

Karen A. Hursey, CPALesley H. Kelly, CPA

Marsha G. LePhew, CPAA. D. “Dave” Masters, CPA

Derrick B. Stark, CPACatherine B. Stoddard, CPAVictor C. Webster, CPA, MBA

South Carolina Association of Certified Public Accountants Magazine

Volume 40, Third Edition 2010

Statements of fact and opinion are made by the authors alone and do not imply an opinion on the part of the officers or members of the SCACPA. Advertising rates will be furnished on request to SCACPA, 570 Chris Drive, West Columbia, SC 29169, (803) 791-4181. Publication of an advertisement in The CPA Report does not constitute an endorsement of the product or service by The CPA Report or the SCACPA.

CPA ReportSouth Carolina Association of CPAs

Charleston 2430 Mall Drive, Suite 360 Greenville

843-884-3912 Charleston, SC 29406 864-245-8788

www.american-pensions.com

Maybe Itʼs Time to Audit Your Health Plan? Healthcare is changing these days; maybe your benefit plan should too. Southeastern Insurance Consultants can help. Because when it comes to understanding the new healthcare landscape, nobody knows more than SIC. From working with state and federal government to help shape new legislation, to understanding legal compliance and benefit administration, the benefit pros at SIC are at the forefront of the industry. And as one of the largest benefit companies in South Carolina, SIC has the ability to back it up, providing first-class service to keep you in informed and in control. Call us today for a free audit of your plan.

Southeastern Insurance Consultants, LLC

PO Box 1396, Irmo, SC 29063 | Toll Free: 866-567-2227 | Office: 803-732-7284 | Lowcountry Office: 843-342-5018

Southeastern Insurance Consultants… Our knowledge, your benefit!

The Exclusive Provider of Health and Dental Insurance Programs to SCACPA

Why Southeastern Insurance Consultants? Multiple Plan Options (POS, HMO, HSA, etc.)

Sole Proprietor Coverage – SCACPA plan (offered through SIC) is one of the only plans to allow sole proprietors to take advantage of group plan options.

Dental Insurance

Life Insurance – Medical plan participants receive $20,000 Life & AD&D coverage.

Additional benefit options – Short/Long Term Disability, Retirement Plans (401k, SEP, etc.), Wellness Plans, Benefit Consulting, Supplemental benefits, Individual/Child Plans

South Carolina

CPA

South Carolina CPA Report 5(888) 557-4814 | www.scacpa.org

SUSTAINABILITY

(888) 557-4814 | www.scacpa.org

From the President

Reflections on the CPA profession, life, love and just about anything else that captures the interest of SCACPA’s 2010 President Eddie Brown

C.E. “Eddie” Brown, CPASCACPA member since 1976

As shareholder of Swaim Brown, PA, Eddie practices in the areas of corporate and individual tax planning and strategy, international tax, business consulting, estate planning, business planning, M&A, succession planning, manufacturing, real estate and construction. Eddie is actively involved with AICPA, SCACPA, Estate Planning Council of Spartanburg and serves as trustee of the South Carolina Baptist Foundation.

While attending the AICPA Council meetings, I try to represent SCACPA properly and gather sufficient, timely knowledge of professional

developments. As I perused the agenda of last fall’s Council meeting, I felt somewhat taken aback to see a session on sustainability. To be honest, I questioned the applicability of sustainability to the CPA profession. But as I kept an open mind about the subject, a light seemed to quickly turn on—the GREEN light. It soon became clear during the presentation that this issue is a win-win-win scenario. When businesses, organizations, communities and their constituents and stakeholders blend efforts to advance a positive social and ecological attitude with a profitable approach, all are winners.

Upon my return, I was asked to pull together a sustainability CPE session for the 2009 CPA Summit & Tax Conference. With newfound enthusiasm I took on the challenge and was pleased to see such a good turnout for the 7:30 a.m. “early bird” session. The participation and interest shown was exciting and encouraging.

I asked the Executive Committee to allow for a Sustainability Task Force and received immediate support. Few committees or task forces have had so many volunteers at the onset. It is astounding to see the interest our members have for sustainability. This task force has graciously responded to the market-driven aspects of the economic, social and ecological impact upon our

clients, organizations and communities. They are also working to bring awareness of pertinent issues before our membership. The Sustainability Task Force will soon be reporting to our board with

recommendations of what we can do to help address this global issue professionally. I encourage each of you to keep an eye on their work.

There is also opportunity for SCACPA to share synergy with efforts of the AICPA and its committees working on the same issues. I have personally approached the chairman of the AICPA and asked that South Carolina be considered to have a representative at the global table. At the same time, we all need to guide our firms and organizations, employers and clients to step up and be on the leading edge of long-term sustainability.

There is great opportunity to make an impact and much work yet to be done. I have asked not only the Sustainability Task Force but also the board and other leaders to make 2010 a year of awareness. Hopefully more CPAs will have their own green light turned on as a result of our efforts. I challenge each member to consider being a positive part in providing A Thousand Points of Green across our beloved state of South Carolina. To be continued…for years to come.

THE GREEN LIGHT

“When businesses, organizations, communities and their constituents and stakeholders blend efforts to advance a positive social and ecological attitude with a profitable approach, all are winners. I challenge each member to consider being a positive part in providing One Thousand Points of Green across South Carolina.”

Maybe Itʼs Time to Audit Your Health Plan? Healthcare is changing these days; maybe your benefit plan should too. Southeastern Insurance Consultants can help. Because when it comes to understanding the new healthcare landscape, nobody knows more than SIC. From working with state and federal government to help shape new legislation, to understanding legal compliance and benefit administration, the benefit pros at SIC are at the forefront of the industry. And as one of the largest benefit companies in South Carolina, SIC has the ability to back it up, providing first-class service to keep you in informed and in control. Call us today for a free audit of your plan.

Southeastern Insurance Consultants, LLC

PO Box 1396, Irmo, SC 29063 | Toll Free: 866-567-2227 | Office: 803-732-7284 | Lowcountry Office: 843-342-5018

Southeastern Insurance Consultants… Our knowledge, your benefit!

The Exclusive Provider of Health and Dental Insurance Programs to SCACPA

Why Southeastern Insurance Consultants? Multiple Plan Options (POS, HMO, HSA, etc.)

Sole Proprietor Coverage – SCACPA plan (offered through SIC) is one of the only plans to allow sole proprietors to take advantage of group plan options.

Dental Insurance

Life Insurance – Medical plan participants receive $20,000 Life & AD&D coverage.

Additional benefit options – Short/Long Term Disability, Retirement Plans (401k, SEP, etc.), Wellness Plans, Benefit Consulting, Supplemental benefits, Individual/Child Plans

South Carolina

CPA Follow Eddie Brown as he blogs weekly, http://scacpa.org.wordpress.com

South Carolina CPA Report 6 (888) 557-4814 | www.scacpa.org

Deadline Approaching for 2010 Member Awards NominationsKnow a fellow CPA providing extraordinary service to SCACPA or the profession at large? Perhaps a fellow chapter member actively involved in chapter activities and your local community, or a young colleague who displays significant leadership qualities in the accounting profession? SCACPA is seeking Member Awards nominations for the 2010 CPA Summit & Tax Conference in November. Recognize and reward exemplary accounting professionals in South Carolina—nominate today! Deadline is September 1, 2010. For more information or to submit a nomination, visit www.scacpa.org/awards.

Staff Contact: Emily Allen

Alan

a Jor

dan

Association News

Erin Hardwick Honored as South Carolina Association Executive of the YearThe South Carolina Society of Association Executives (SCSAE) recognized SCACPA Executive Director Erin Hardwick, CAE as Executive of the Year at its fifth annual conference in June. SCSAE’s Executive of the Year Award is the highest honor for an association executive. This award is presented to those whose accomplishments have been outstanding; only 25 executives have been awarded this honor. Hardwick was honored by the SCSAE with a plaque and a signed concurrent resolution of the recognition from the SC Senate and House of Representatives.

SCACPA: Best in the Business!SCACPA recently received three Best in the Business awards from the South Carolina Society of Association Executives (SCSAE) for programs, projects, events and activities accomplished during 2009:

• Best Magazine or Journal: The South Carolina CPA Report• Best Electronic Communications: 2009 CPA Summit Registration confirmation e-mail• Honorable Mention: www.scacpa.org

Congratulations to Emily Allen and Katherine Swartz, CAE, who serve as staff team leaders for these member programs.

Share Your Financial Literacy Knowledge with GED CandidatesSCACPA is committed to helping all South Carolinians gain practical financial skills—and you can help! In April, the SCACPA Financial Literacy Task Force embarked on Project GED in an effort to make a basic financial skills presentation to all 50 GED programs statewide by October 31. The Common Sense for Your Dollars and Cents toolkit for members includes a presentation, student handouts and tips on corresponding with the teacher and students. A small time investment of less than five hours can provide a lifetime of reward for students in need in your area. Get involved at www.scacpa.org/ProjectGED.

Staff Contact: Katherine Swartz

CPA ReportSouth Carolina Association of Certified Public Accountants

S e c o n d E d i t i o n 2 0 1 0

THE CPA PIPELINE

WHY IS IT CRITICAL?

An Interview with South Carolina’s

Accounting Doctoral Scholars

The AP Accounting Project

The New CPA Exam

Season 2010

Join a SCACPA Committee Today!Over the past few years, SCACPA’s Board of Directors has made a commitment to becoming a more open organization that provides increased opportunities for participation. With that in mind, we are conducting an open call for interested and qualified individuals to contribute to the future growth and success of SCACPA. This is your opportunity to share your expertise and experience! As a committee or task force member, you will devote time, energy, and ideas to move SCACPA projects and programs forward as envisioned by the Board of Directors, and in turn, lead the profession in supporting a wide-range of efforts on behalf of our members, communities and CPAs across the state. Learn more at www.scacpa.org/Volunteer.

Staff Contact: Reva Brennan

Seeking CPAs Specialty Areas The Peer Review Program is in need of team members in a number of specialty areas. If you are interested in being a consultant to a peer reviewer but not necessarily performing peer reviews, we need you!

Staff Contact: Glenna Minor

South Carolina CPA Report 7(888) 557-4814 | www.scacpa.org 7

SOUTH CAROLINA ASSOCIATION OF CPAs570 Chris Drive, West Columbia, South Carolina 29169(803) 791-4181 or Toll-free (888) 557-4814Fax (803) 791-4196 | www.SCACPA.org

OUR MISSIONTo support all CPAs – whether in public practice, industry, government or education – with lifelong learning opportunities necessary for their success and to promote high ethical standards and legislative advocacy for both the public good and the profession. We accomplish this mission through the following activities:

AdvocacyCertification & LicensingCommunications

SCACPA STAFFErin P. Hardwick, CAE, Executive Director Ext. 104, [email protected]

Reva E. Brennan, MPA, CAE, IOM, Associate Director Ext. 103, [email protected]

Karen M. Hancock, CPA, Finance Director Ext. 108, [email protected]

Glenna P. Minor, Peer Review & Member Services Manager Ext. 107, [email protected]

Katherine M. Swartz, CAE, Member Services Director Ext. 105, [email protected]

April C. Cox, Education Manager Ext. 110, [email protected]

Emily M. Allen, Communications Coordinator Ext. 106, [email protected]

Sandra P. Oxner, CMP, CMMM, Chapter & Special Events CoordinatorExt. 112, [email protected]

Recruiting & EducationStandards & Performance

IRS & SC DOR want to Hear from YouThe SCACPA Taxation Task Force will host their annual meeting with the Internal Revenue Service and South Carolina Department of Revenue Wednesday, October 27. During this meeting key staff of the IRS and DOR will address issues and concerns of the CPAs of South Carolina as provided in the annual survey. This is an ideal opportunity to share the things you think the agencies are doing well as well asissues that they should address. A report of the meeting will be provided in the First Edition 2011 of theCPA Report.There you’ll find eight important questions and a chance to share what works, what doesn’t and areas in

which you’ve had reoccurring issues with these agencies. Participants can also enter a drawing to win a complimentary registration for the upcoming 2010 CPA Annual Summit and Member Meeting, November 11-12.

Three easy steps to having your concerns addressed!1. Visit www.scacpa.org2. Complete the online survey by Thursday, September 303. Read the First Edition 2011 of the CPA Report

Staff Contact: Reva Brennan

Report from SCACPA’s 2010 Nominating Committee

Timothy Baker Michael Putich

Sharon Mann Malynda Grimsley

Mark Crocker Dave Masters

Robert Tilton

Note: Once elected by the membership as president-elect the individual moves automatically to president in the subsequent year, and therefore election to the position of president is not required.

Mark T. Hobbs CPA, Committee Chair

South Carolina Association of CPAs officers serve for one year elected by SCACPA membership with term beginning January 1, 2011.

SCACPA OFFICERS: President*

Timothy L. Baker, CPA

President Elect Michael R. Putich, CPA

Vice President Sharon E. Mann CPA

Secretary/TreasurerMalynda M. Grimsley, CPA

At-Large Elections: Mark Crocker, Unexpired Term,

2011- 2012

Dave Masters, Second Term, 2011-2013

Robert Tilton, 2011-2013

South Carolina CPA Report 8 (888) 557-4814 | www.scacpa.org

SCACPA Board of Directors Update The SCACPA board of directors met April 28 in Columbia. During the meeting, past president Bob Baldwin, CPA, PFS, AEP, who chaired a task force to modernize the SCACPA Constitution and Bylaws, presented a final draft to the board. The project combined the Constitution and Bylaws into one document and updated various sections. The SCACPA board postponed approving the bylaws until members had the opportunity to comment. Comments were accepted through electronic communications during June and July. The board will review these comments and approve the final version at its August meeting.

President Eddie Brown led a discussion about the need for a Rapid Response Team for federal legislative action. There are frequent requests from the AICPA for state associations to weigh in on various legislative proposals, often with a quick deadline. The SCACPA Board appointed four members to serve on a Rapid Response Team:• R. Doug Crowley, CPA, CVA, Ford

and Crowley, CPA, LLC, Legislative & Advocacy Committee member

• Charles “Chuck” L. Talbert III, CPA, McAbee Talbert Halliday & Company, past Legislative & Advocacy Committee Chair

• J. Pat McDermott, CPA, The Beach Company, SCACPA’s AICPA Council Representative

• Jason C. Sweatt, CPA, Elliott Davis, LLC, 2010 Legislative & Advocacy Committee Chair

SCACPA staff will notify team members when federal legislative calls to action are received, and SCACPA’s board will stay attuned through real-time communication on opinions and actions needed.

The SCACPA board will meet August 5-6 in Beaufort for its annual strategic planning session. This two-day meeting will be facilitated by Maryland Association of CPAs Executive Director Tom Hood.

2010 CPA Day at the State House The fifth annual CPA Day event was held in Columbia on April 28. It brought hundreds of people together and gained greater visibility for the CPA profession as a viable entity in the legislative arena. Read more and see photos on pages 34-35 and on www.scacpa.org/Facebook.

Legislative ReportState ActivitiesSCACPA proactively worked two main issues during the 2010 legislative session: 1) getting tax conformity passed earlier in the calendar year, and 2) assisting the SC Board of Accountancy in gaining greater independence in their operational affairs.

We were successful in getting stand-alone tax conformity legislation passed through the Senate, House and governor’s office earlier than ever (March 31); however, the goal is to get tax conformity legislation passed even earlier in 2011.

In a cooperative effort with several other professional regulating boards, SCACPA led

the initiative to gain greater independence for our respective boards. The proposal received support from the House leadership and survived several committee hearings, but ultimately died on the House floor as debate raged over the state budget. Because the concern over how our Board of Accountancy is allowed to operate under the state agency of Labor, Licensing and Regulation, this will remain an issue going forward. We are revisiting our approach to resolving the concerns and will develop a strategy this fall.

Federal IssuesCongress has kept the CPA profession’s lobbyists busy this year. SCACPA and other state associations are frequently asked to weigh in on federal legislation that could impact you as a practicing CPA. Among the legislation that SCAPCA has weighed in on include: • The IRS’s tax preparer registration

proposal• The provision that would change how

S corporation owners compensation is treated

• The “aiding and abetting” provision in the financial service reform legislation

The South Carolina Board of

Accountancy passed new regulations

effective June 25, 2010. Among

various changes to existing

regulations, the new provisions could

impact your CPE, especially self-study.

For details on these changes go to

www.scacpa.org/NewBOARegulations.

On Your BEHALFSecond Quarter Report

For the profession, by the profession—that’s what the South Carolina Association of CPAs is all about. SCACPA’s board of directors, committees and task forces, and young CPAs leadership cabinet are hard at work making decisions, providing guidance and embarking on projects and programs that strengthen the profession and enable members to improve their knowledge, network and technical skills.

South C

arol

ina

Ass

ociation of Certified Public A

ccountants

1 9 1 5

Since

by Er in P. Hardwick , CAES e r v i n g S C AC PA s i n ce 2 0 0 5

South Carolina CPA Report 9(888) 557-4814 | www.scacpa.org

• Legislation that would require that the federal comptroller general be a CPA

CPA-PAC in ActionThe CPA-PAC trustees met May 7 to review all candidates running for the House of Representatives. The trustees focused on those who were facing strong primary opposition and carefully considered which candidates to support, taking into account their past support of business friendly issues as well as those affecting the CPA profession. The total contributed for primary elections was $8,750.

Receiving contributions from CPA-PACRep. Merita A. "Rita" Allison (Spartanburg)Rep. Don C. Bowen (Anderson)Rep. Robert L. Brown (Charleston)Speaker Pro Tempore Harry F. Cato* (Greenville)Rep. Richard E. Chalk, Jr.* (Beaufort)Rep. Daniel “Dan” T. Cooper (Anderson)Rep. Marion B. Frye (Lexington)Rep. Nelson L. Hardwick (Horry)Rep. James H. Harrison (Richland) Rep. R. Keith Kelly* (Spartanburg) Rep. Lewis E. "Gene" Pinson (Greenwood) Rep. J. Roland Smith (Aiken)Rep. William E. "Bill" Sandifer III (Oconee)Rep. F. Michael "Mike" Sottile (Charleston)* denotes those who did not win their primary race.

A sincere thank you goes to the following South Carolina CPAs who serve as Key Person Contacts and volunteered to hand-deliver contribution checks to their local legislator:

Caprice Atterbury, CPAJohn F. Camp, CPA

Patrick P. Carey Jr., CPAChris B. Benfield, CPA

R. Keith Dooley, CPA, PFSJames W. McIlrath, CPADouglas A. Snyder, CPAW. Ashley Thiem, CPANancy O. Upton, CPARobert D. Wade, CPA

In August, CPA-PAC Trustees will convene to consider potential contributions to candidates for state constitutional offices as well as candidates for the House with general election opposition. Contributions to candidates help SCACPA and the profession connect with key policy-makers. It’s part of all-important relationship-building for a time when those relationships may be needed to protect the CPA profession. Generous donations given by individual members and CPA firms are the sole means by which SCACPA can show its support of certain legislators. Some 240 (seven percent) of SCACPA members have donated more than $13,000 to the CPA-PAC in 2010.

Firms which have donated a cumulative total of $10,000 in 2010:

Derrick, Stubbs and Stith, LLP Dixon Hughes PLLC

Elliott Davis, LLC McAbee Talbert Halliday & Company

Schmoyer and Company, PCScott McElveen, LLP WebsterRogers LLP

Thank you to each and every member and firm who acknowledges and supports this important process!

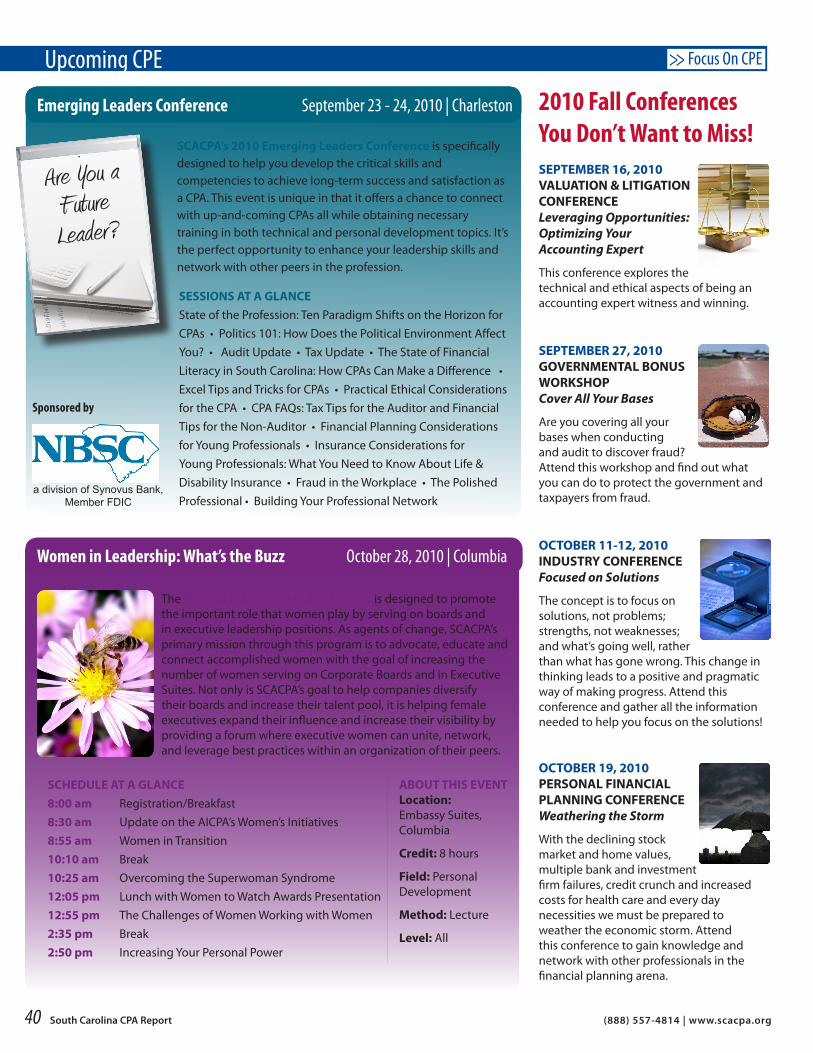

Three New Conferences Draw EnthusiasmSCACPA’s Board President Eddie Brown has charged committees, chapters and staff with achieving a “wow” this year in our respective areas. As a result, in the area of CPE, three new conferences will launch this year: 1. Nonprofit Conference: Held April 29 in

partnership with the SC Association of Nonprofit Organizations. More than 100 people attended the conference, which exceeded attendance goals.

2. Emerging Leaders Conference: September 23-24 (Charleston). Planned and hosted by SCACPA’s Young CPA Leadership Cabinet.

3. Women in Leadership Conference: October 28 (Columbia). Features sessions on leadership and includes a Women to Watch recognition program.

2011 SCACPA BOARD NOMINATIONS Notice of Annual Business Meeting The annual business meeting of the SC Association of Certified Public Accountants (SCACPA) will take place on Thursday, November 11 from 8:00-8:45 a.m. at the Embassy Suites Hotel in Columbia. The business meeting will include a membership vote on:

• Minutes from the 2009 business meeting; • review and approval of the 2011 operational budget; • and, the election of officers and directors.

All members are encouraged to participate.

The report of SCACPA’s 2010 Nominating Committee for the election of officers and at-large board members follows.

The report of SCACPA’s 2010 Nominating Committee for the election of officers and at-large board members is featured on page 7.

Erin P. Hardwick, CAE has served as SCACPA’s executive director since 2005. She has more than 25 years of experience in association and non-profit executive leadership and is one of 18 Certified Association Executives in South Carolina, the highest credential

in the association management profession. She currently serves on the SC Secretary of State’s Nonprofit Advisory Council, the Saluda Shoals Park Foundation Board of Directors and the SC Council on Economic Education Board of Directors.

People, Planet & Profit | SUSTAINABILITY and THE CPA

Aon Insurance Services is a division of Affinity Insurance Services, Inc.; in CA, MN & OK, (CA License #0795465) Aon Insurance Services is a division of AIS Affinity Insurance Agency, Inc.; and in NY, AIS Affinity Insurance Agency.

One or more of the CNA companies provide the products and/or services described. The information is intended to present a general overview for illustrative purposes only. It is not intended to constitute a binding contract. Please remember that only the relevant insurance policy can provide the actual terms, coverages, amounts, conditions and exclusions for an insured. All products and services may not be available in all states and may be subject to change without notice. CNA is a registered trademark of CNA Financial Corporation. Copyright © 2010 CNA. All rights reserved. E-5929-0910 SC

Endorsed by: Endorsed by: Underwritten by:Nationally Administered by:

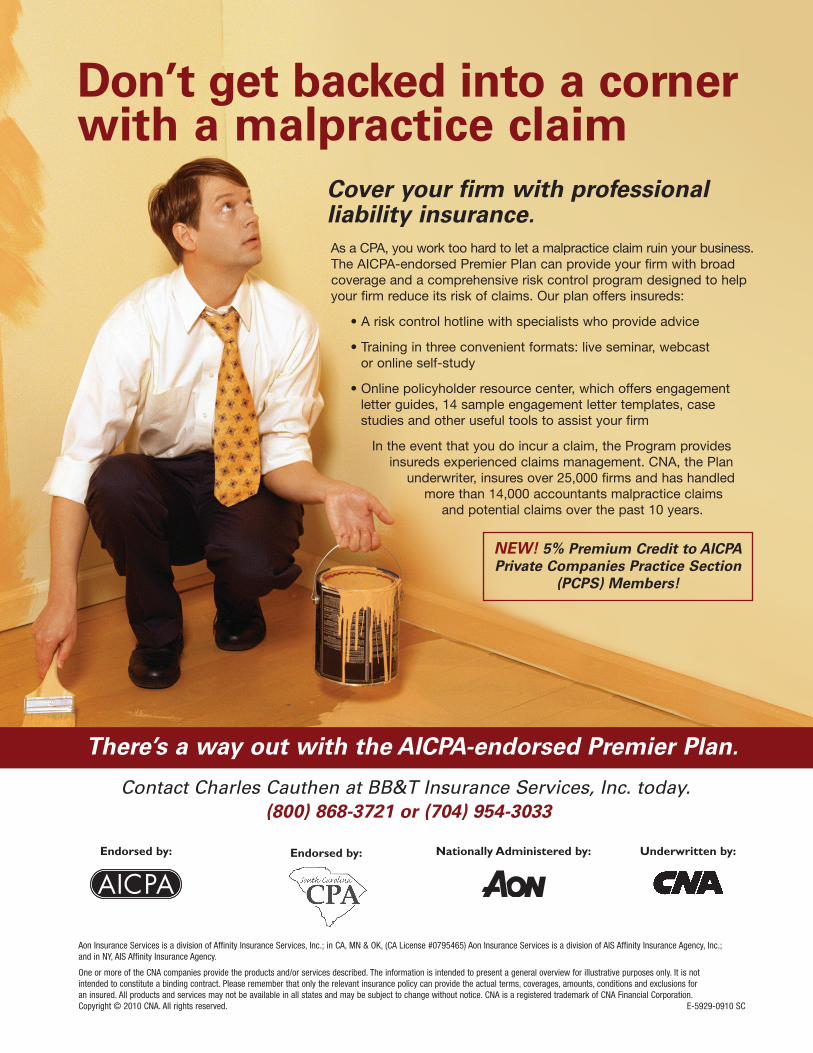

Don’t get backed into a cornerwith a malpractice claim

Cover your firm with professional liability insurance.

There’s a way out with the AICPA-endorsed Premier Plan.

Contact Charles Cauthen at BB&T Insurance Services, Inc. today.(800) 868-3721 or (704) 954-3033

As a CPA, you work too hard to let a malpractice claim ruin your business.The AICPA-endorsed Premier Plan can provide your firm with broad coverage and a comprehensive risk control program designed to help your firm reduce its risk of claims. Our plan offers insureds:

• A risk control hotline with specialists who provide advice

• Training in three convenient formats: live seminar, webcast or online self-study

• Online policyholder resource center, which offers engagement letter guides, 14 sample engagement letter templates, case studies and other useful tools to assist your firm

In the event that you do incur a claim, the Program provides insureds experienced claims management. CNA, the Plan

underwriter, insures over 25,000 firms and has handled more than 14,000 accountants malpractice claims

and potential claims over the past 10 years.

NEW! 5% Premium Credit to AICPAPrivate Companies Practice Section

(PCPS) Members!

E-5929-0910 SC_E-5929-0910 SC 6/9/10 9:54 AM Page 1

South Carolina CPA Report 11(888) 557-4814 | www.scacpa.org

People, Planet & Profit | SUSTAINABILITY and THE CPA

Aon Insurance Services is a division of Affinity Insurance Services, Inc.; in CA, MN & OK, (CA License #0795465) Aon Insurance Services is a division of AIS Affinity Insurance Agency, Inc.; and in NY, AIS Affinity Insurance Agency.

One or more of the CNA companies provide the products and/or services described. The information is intended to present a general overview for illustrative purposes only. It is not intended to constitute a binding contract. Please remember that only the relevant insurance policy can provide the actual terms, coverages, amounts, conditions and exclusions for an insured. All products and services may not be available in all states and may be subject to change without notice. CNA is a registered trademark of CNA Financial Corporation. Copyright © 2010 CNA. All rights reserved. E-5929-0910 SC

Endorsed by: Endorsed by: Underwritten by:Nationally Administered by:

Don’t get backed into a cornerwith a malpractice claim

Cover your firm with professional liability insurance.

There’s a way out with the AICPA-endorsed Premier Plan.

Contact Charles Cauthen at BB&T Insurance Services, Inc. today.(800) 868-3721 or (704) 954-3033

As a CPA, you work too hard to let a malpractice claim ruin your business.The AICPA-endorsed Premier Plan can provide your firm with broad coverage and a comprehensive risk control program designed to help your firm reduce its risk of claims. Our plan offers insureds:

• A risk control hotline with specialists who provide advice

• Training in three convenient formats: live seminar, webcast or online self-study

• Online policyholder resource center, which offers engagement letter guides, 14 sample engagement letter templates, case studies and other useful tools to assist your firm

In the event that you do incur a claim, the Program provides insureds experienced claims management. CNA, the Plan

underwriter, insures over 25,000 firms and has handled more than 14,000 accountants malpractice claims

and potential claims over the past 10 years.

NEW! 5% Premium Credit to AICPAPrivate Companies Practice Section

(PCPS) Members!

E-5929-0910 SC_E-5929-0910 SC 6/9/10 9:54 AM Page 1

Introduction: Sustainability and the CPA, page 11

Corporate Sustainability 101, page 12

Building the Business Case for Sustainability, page 14

Practical Green: Small Business and Regional Firm Perspectives, page 17

South Carolina Electric Cooperatives on Energy Efficiency and Renewables, page 20

SCACPA Steps Into Sustainable Practices, page 22

Member Profiles: Meet Members of the Sustainability Task Force, page 24

SPECIAL SECTION:1,000 Points of Green

SUSTAINABILITY AND THE CPAIt is without debate that business operates in a global environment. Sustainability is having an impact on the definition and practice of accounting and the accountant’s role, perhaps more so than any other business or legislative initiative. Until now, the primary role of CPAs in the area of sustainability has been focused upon collecting, analyzing and reporting on sustainability-related information for internal and external usage. The role of CPAs as it pertains to sustainability is expected to dramatically increase in the areas of accounting, reporting, assurance and management. It is a topic of great interest and opportunity, marked by 16 professional bodies and representing a significant share of the world’s chartered accountants who provide their seal of approval to the principles of Accounting for Sustainability Forum. It is not a matter of if, but when U.S. accounting practices will adopt sustainability guidelines.

“CPAs have an important role

to play in sustainability. In addition

to their widely recognized expertise in

measurement, accounting, reporting and

assurance, CPAs in business are best able

to connect the dots between strategy, risk,

financial performance and reporting.”

– Carol Scott, AICPA Vice President for

Business, Industry & Government

South Carolina CPA Report 12 (888) 557-4814 | www.scacpa.org

People, Planet & Profit | SUSTAINABILITY and THE CPA

This is the first of a two-part series that will address the concept of corporate sustainability and its

relevance to business and the accounting profession. The first part defines and makes a business case for sustainability. The second part, to be included in the fourth edition of The CPA Report, will provide framework to define, measure and implement sustainability as well as insights into the role and future of sustainability as it applies to CPAs.

wHAT IS SUSTAINABILITY?A simple question, but the answer can result in numerous definitions or even blank stares. The multiple definitions provided within this article are not due to a misunderstanding of the topic—quite the opposite. In fact, these definitions can be derived from the multiple uses of sustainability by individuals, groups or organizations. Sustainability can, therefore, have a variety of contextual meanings that relate to economic, agricultural, community and business development as well as personal lifestyles. This is perhaps why a single definition is lacking that permeates the sustainability “industry.” Furthermore, growing use of the term around the world has resulted in broadened interpretations by politicians, business professionals and the media.

THE FOUR EsAmong the variety of practitioners and their inherent definitions, four common areas seem to be addressed: 1) Environment and Ecology; 2) Economy and Employment; 3) Equity and Equality and 4) Education. Within each of these areas are common themes relating to living within limits, understanding interconnections between economy, society and the environment, and equitable distribution and management of resources and opportunities. In terms of business, Corporate Sustainability is seen as more of an evolution of the traditional ethical corporate behavior

known as corporate social responsibility (CSR)1. Predominated by philanthropy and volunteerism, Corporate Sustainability is increasingly superseding traditional definitions and practices to include all business practices built around social and environmental considerations.

INFLUENCING THE DEFINITIONAttempts to define Corporate Sustainability have been influenced by two key sources. The first was the 1987 United Nations World Commission on Environment and Development report titled Brundtland Commission2 Our Common Future3. This report related sustainability directly to corporations and the economy by coining and defining the term sustainable development as “development that meets the needs of the present without compromising the ability of future generations to meet their own needs.”

The second was the Triple Bottom Line concept cited by John Elkington in 19994: “…business goals were inseparable from the societies and the environments within which they operate. While short-term economic gain could be chased, a failure to account for social and environmental impacts would make those business practices unsustainable.” Though both of these principles sound practical and even logical as they apply to helping define Corporate Sustainability, the business community has realized that they are not easy to apply to a workable definition because they are simply not easy to measure and appear at times to be more qualitative than quantitative.

A wORK IN PROGRESSThe definition of Corporate Sustainability continues to evolve, and there appears to be two common categories of application today. There are those who define and practice Corporate Sustainability as a program (reduce, reuse, recycle). This can be construed as more of a “feel-good”

Corporate Sustainability 101by John J . Meindl , J r.

John Meindl is a senior fellow in the Center for Corporate Learning and Development and an adjunct professor at Furman University. He is a board member

of several companies and a managing partner in a private investment firm where he actively educates and encourages the consideration and deployment of sustainable business initiatives to garner strategic advantage. Meindl will be presenting a CPE session entitled Sustainability and the CPA at five of the nine SCACPA Professional Issues Updates this fall.

South Carolina CPA Report 13(888) 557-4814 | www.scacpa.org

Sustainability Defined

Merriam-Webster: “1. Capable of being sustained. 2. Of, relating to, or being a method of harvesting or using a resource so that the resource is not depleted or permanently damaged. 3. Of, or relating to, a lifestyle involving the use of sustainable methods.”

Global Footprint Network5 (www.footprintnetwork.org): “It is based on the recognition that when resources are consumed faster than they are produced or renewed, the resource is depleted and eventually used up. In a sustainable world, society's demand on nature is in balance with nature's capacity to meet that demand.”

Dow Jones Sustainability Index6: “Corporate Sustainability is a business approach that creates long-term shareholder value by embracing opportunities and managing risks deriving from economic, environmental and social developments.”

PricewaterhouseCoopers7: “Aligning an organization’s products and services with stakeholder expectations, thereby adding economic, environmental and social value.”

References1: http://en.wikipedia.org/wiki/Corporate_social_responsibility; 2: www.un.org/documents/ga/res/42/ares42-187.htm; 3: http://worldinbalance.net/intagreements/1987-brundtland.php; 4: www.johnelkington.com/TBL-elkington-chapter.pdf; 5: www.footprintnetwork.org; 6: www.sustainability-indexes.com/07_htmle/sustainability/corpsustainability.html; 7: www.pwc.com/gx/en/sustainability/index.jhtml

B A N K I N G I N S U R A N C E I N V E S T M E N T SBB&T. Member FDIC. Only deposit products are FDIC insured. ©2010 BB&T. BBT.com

YOU’RE LOOKING FOR A PARTNER WITH COMPREHENSIVE FINANCIAL

SOLUTIONS. You’re looking for someone to help you meet your goals. To help you

take advantage of opportunities. Someone who understands your strengths and

weaknesses, and who knows what will work for you – and when. You’re looking

for a partner who is both reliable and responsive. You’ve just found one. Let us

help you find your next financial opportunity.

Business to business and person to person.

People, Planet & Profit | SUSTAINABILITY and THE CPA

definition. Though there is economic and social value in these types of programs (usually marginal), businesses in this program-driven category do so more from the perspective of something nice to do or have.

The second group includes those who not only want to feel good, but actually measure good as it pertains to business impact. Corporate Sustainability for these practitioners is defined more as a business process or strategy. Corporate Sustainability involves the concept of eco-efficiency through the reduction of costs and cost-structures, and creates long-term stakeholder value. This strategy is accomplished through consideration of the interrelationship between the environment, economy and society. Sustainability is defined and practiced as a basis from which to innovate, improve productivity, reduce risk, generate revenue, build brand, increase corporate valuation and positively impact society— which may be defined as measuring goodwill.

South Carolina CPA Report 14 (888) 557-4814 | www.scacpa.org

Building The Business Case for Sustainability

People, Planet & Profit | SUSTAINABILITY and THE CPA

The business case for sustainability can be argued from both negative and positive rationales. Given

the fact that business operates in a finite world, it can be positioned simply as a case for business survival—although business models and inherent practices are linear in nature. Certain resources are in decline, while the market for and associated consumption of those resources is still growing. This business case is based on a “not if, but when” scenario. It is a negative business case or rationale.

On the other hand, sustainable business practices implemented in a variety of industries are providing bottom-line results. This is a positive business case or rationale. Case studies are heralding various forms of return being realized from sustainability: Operating cost re-structuring and

reduction Operating risk and liability management Product/service innovation Brand integration and reputation value Development of new markets Increased employee morale Safety

ONE SIZE DOES NOT FIT ALLThough many successful business case examples appear logical and enticing, it is important to know recognize that one size does not fit all. Examples of success are sometimes easily deemed best practices and, as a result, copied blindly. Every organization has its own set of drivers—strengths, dependencies, weaknesses, etc.—in terms of distinguishing values from initiatives, especially new ones. The rewards may not translate from one business to the next. Organizational drivers need to be understood and rationalized in any sustainability business case.

A business case for sustainability based on achieving long-term, or systemic, success has to be rooted in more than statistics or logic. Many organizations who implement

sustainable business process can amply demonstrate significant achievements and bottom-line results. Those who do not implement sustainable processes can also demonstrate those same achievements and significant results. Businesses who ignore or limit their efforts for sustainability usually believe that current social constraints trying to be placed on human activities as well as ecological limits are temporary roadblocks to progress. They may also believe these obstacles can be overcome with better science or technology.

On the other hand, businesses who implement sustainability as a key business strategy do so because they truly believe in the existence of inviolable laws of nature. They understand and believe human actions must conform and comply with nature, or otherwise suffer eventual consequences. For these organizations, it is not only an internal operating belief but also a market perspective. The key to a successful business case for sustainability is deeply rooted in beliefs about the future, not the facts of yesterday that can influence business today. Many studies and analyses have been conducted on successful companies that have and are making sustainability part of their corporate DNA. Upon close examination of these companies are found the attributes of leadership, insight and courage.

As the data shows, the business case for sustainability pursued more from the perspective of opportunity (positive) than survival (negative) is compelling and worthy of analysis and pursuit. If one is simply waiting on another’s business case instead of making their own, it may be too late. As Microsoft’s Bill Gates stated, “If you can show me a business case, you’re too late.”10

Businesses in pursuit of opportunity are given chances every day to influence and create their own future—it is a matter of perspective, vision and decision making.

by John J . Meindl , J r.

South Carolina CPA Report 15(888) 557-4814 | www.scacpa.org

People, Planet & Profit | SUSTAINABILITY and THE CPA

Companies Do Well by Doing Well

Over an 11-year period, a Harvard University study1 on the concept of stakeholder management found socially

responsible and sustainable corporations had sales growth four times and employment growth eight times that of “shareholder first” companies.

The Dow Jones Groups Sustainability Index (DJGSI) performed a five-year study2 in which they found companies engaged in sustainable business practices averaged 36.1 percent better than the traditional Dow Jones Group Index. The report found that “sustainability strategies had a significant impact on the cost of external financing, return on invested capital, sales growth and the fade-rate of a firm’s competitive advantage.”

Goldman Sachs’s research3 found that companies that are considered leaders in environmental, social and governance (ESG) policies also lead in stock performance by an average of 25 percent.

Kholberg, Kravis, Roberts & Company (KKR)4, a global alternative asset management company states that “the business case for environmental management has never been stronger.”5 In fact, KKR is expanding its Green Portfolio Program6 to cover 20 percent of the companies in its portfolio.

Carlyle Group7, one of the world’s largest private investment firms, has teamed up with the Environmental Defense Fund8 to create EcoValue Screen9, a method Carlyle can utilize in undertaking due diligence pertaining to perspective investments.

References1: www.hks.harvard.edu/m-rcbg/CSRI/publications/workingpaper_10_kytle_ruggie.pdf; http://hbswk.hbs.edu/item/5859.html; www.cim.sfu.ca/pages/resources_shouldnt.htm; 2: www.corostrandberg.com/pdfs/Business_Case_for_Sustainability_21.pdf; 3: www.thecro.com/?q=node/490&spesh=printme; 4: www.kkr.com/index.cfm; 5: www.kkr.com/releasedetail.cfm?ReleaseID=389022&KeepThis=true&TB_iframe=true&height=461&width=592; 6: www.kkr.com/new_initiatives/edf_partnerships.cfm ; 7: www.carlyle.com/; 8: www.edf.org/ http://blogs.edf.org/innovation/category/partnerships/page/2/; 9: http://blogs.wsj.com/privateequity/2010/03/18/carlyle-group-teams-up-with-edf/; 10: http://blogs.natlogic.com/friend/2010/03/making_the_business_case_for_s.html

YOUR ROAD TO SUCCESS

2010 Professional Issues Update Series

AUGUST12 Florence, Southeastern Institute of Manufacturing & Technology (SIMT), 60910FL13 Myrtle Beach, Horry-Georgetown Technical College, 60910MB30 Rock Hill, Baxter M. Hood Conference Center, 60910RH31 Spartanburg, Converse College, 60910SP

SEPTEMBER27 Hilton Head (Hardeeville), Palmetto Electric Cooperative, 60910SE 28 North Charleston, Embassy Suites Hotel Airport/ Convention Center, 60910CH

OCTOBER1 Columbia, Embassy Suites Hotel, 60910CO4 Greenville, Embassy Suites Hotel & Conference Center, 60910GR5 Anderson, Anderson University, Thrift Library, 60910AN

9 CITIES • 4 HOURS OF FREE CPE!

PIU INFORMATION

COST: Members, $0Non-members, $100*

Students, $20*

CREDIT HOURS: 4

CREDIT AREA: Personal Development

*Upon approval, registration fee includes 2010 membership in SCACPA

(up to five months of membership). Former members of SCACPA may be

subject to reinstatement fees.

Be sure to reserve your seat today –these popular programs fill up fast!

“Although I keep up with the news, I appreciated the overview of financial events from the last year and learned how some headlines tie to CPAs in ways I had not considered.”

“It is important to know how others view my profession.”

SPONSORSBB&T Insurance Services, Inc., the AICPA Professional Liability Plan

Southeastern Insurance Consultants, the SCACPA Employee Benefit Plan

CHAPTER CO-HOSTSSCACPA Chapter Network

Furman University Now offering a Post Graduate Diploma in Corporate Sustainability

REGISTER TODAY: www.scacpa.org/PIU

South Carolina

CPA

People, Planet & Profit | SUSTAINABILITY and THE CPAYour clients can benefi t from the new HIRE Act right now!

We can show you how.From reduced payroll taxes to increased tax credits, we’ll show you how the new Hiring Incentives to RestoreEmployment (HIRE) Act can generate immediate savings that may positively impact your clients’ bottom line.

But that’s not all. We’ll also help your clients stay compliant in a complex and fast-changing environmentthat challenges the resources and skill sets of companies of all sizes.

Legislation is constantly changing, and ADP keeps you up to date on the issues that impact your clients. Now more than ever, accountants are choosing ADP for the expertise and experience that counts.

Calculate your clients’ potential savings at www.adp.comor call us at 1-888-5-ADP-SAVE.

HR / Payroll / Benefi ts Administration / Tax / Retirement Subject to eligibility requirements contained in the HIRE Act. The information contained herein is for informational purposes only and should not be construed as legal or accounting advice. The ADP Logo is a registered trademark of ADP, Inc. ©2010 ADP, Inc.

ADPUES10005 Hire Act SBS_CPA_Report_SC.indd 1 3/30/10 1:23 PM

South Carolina CPA Report 17(888) 557-4814 | www.scacpa.org

People, Planet & Profit | SUSTAINABILITY and THE CPA

RECYCLESome green initiatives are less about direct cost savings and more products of our cul-ture. To understand our commitment to our aluminum, plastic and non-confidential paper recycling program, one must understand a little about my partner. I would not describe her as a “greenie,” but she is practical. To her, it is nonsense to throw away aluminum and plastics because it is as easy to recycle them as to not do so. We simply default to recycle. The problem is that, unlike our first office space, there is no recycle service available to our new building. I thought our move might be the end of our recycling program, but I was wrong. Being practical green, my staff decided to bag up the recycle bin each week and put it in the back of my truck so I could put it out with our recycling at home.

Practical green is not always about shrewd cost savings, but it is about considering the environmental elements of operating a busi-ness and nurturing its profits and culture. We are fortunate in this day and age to have access to the information and services that allow us to make sustainability good business and not just a moral consideration. As you read the great ideas and information in this publication and elsewhere, start with the things that you already do and how new ideas and suggestions can enhance your business as well as the com-munity and the globe. Try practical green.

Your clients can benefi t from the new HIRE Act right now!

We can show you how.From reduced payroll taxes to increased tax credits, we’ll show you how the new Hiring Incentives to RestoreEmployment (HIRE) Act can generate immediate savings that may positively impact your clients’ bottom line.

But that’s not all. We’ll also help your clients stay compliant in a complex and fast-changing environmentthat challenges the resources and skill sets of companies of all sizes.

Legislation is constantly changing, and ADP keeps you up to date on the issues that impact your clients. Now more than ever, accountants are choosing ADP for the expertise and experience that counts.

Calculate your clients’ potential savings at www.adp.comor call us at 1-888-5-ADP-SAVE.

HR / Payroll / Benefi ts Administration / Tax / Retirement Subject to eligibility requirements contained in the HIRE Act. The information contained herein is for informational purposes only and should not be construed as legal or accounting advice. The ADP Logo is a registered trademark of ADP, Inc. ©2010 ADP, Inc.

ADPUES10005 Hire Act SBS_CPA_Report_SC.indd 1 3/30/10 1:23 PM

Practical Green: The Small Business Perspective

As small business owners, environmen-tal sustainability sometimes seems distant because it would seem to

require a grandiose effort in which the ultimate success or failure is not closely tied to our specific contributions. As owners of a home medical equipment consulting and billing company with ten employees, my partner and I have found it easier to build meaningful sus-tainable programs in our office when, instead of thinking of environmental matters as a sin-gular issue, we consider them in the context of our business, our community and our existing values. We call it “practical green.”

REUSELike a lot of small business owners, we started a small consulting practice in a niche market with little more investment than blood, sweat and tears. As we opened our first office, we needed desks and filing cabinets and all of the other stuff you take for granted when someone else buys it. Given the budget of a start up, we followed the newspaper classifieds for used of-fice furniture, and kept an eye out for any other source of previously owned (less expensive) alternatives. We only bought solid furniture that was in good shape and looked either new or purposefully vintage, gaving our first office a decidedly warm vibe.

We were not, admittedly, thinking of all of the stuff we were keeping out of landfills or the overall waste stream at the time. The fiscal limitations that governed our business, how-ever, contributed to our culture today and cre-ated a fantastic byproduct: the importance of reuse. We actually liked the thrill of the hunt—purchasing new stuff seemed almost like a cop out. I bought my first desk from the garage of a retired insurance agent; I actually had to help him move his wife’s pottery supplies to get to it and load it into my trailer. It was more than 20 years old when I bought it, and I still use

it today. Over the years, we have purchased used desks, school house-sized white boards, filing cabinets, reception area furniture, framed pictures and other decorative elements, all of which would have likely ended up in a landfill somewhere.

REDUCEOver the last decade or so, paperless or paper-reduced offices have become a ubiquitous example of sustainable initiatives aimed at reducing the energy and natural resources associated with paper consumption. That was the last thing on my mind, however, when I put a second monitor on each workstation in my office. Instead, I was more worried about how much time my staff, otherwise billable between $50 and $200 an hour, were spending going back and forth to the network printer. So in our usual style, we looked for monitors of the same make and model as those we already had (some used) on eBay and other online retailers. Our initiative took about two months to complete, but in the end, every worksta-tion had matching dual monitors and we spent surprisingly little money. We also reaped the following benefits: Security protocols improved. We encrypted our client files and expanded our disaster contingency in ways that were just not possible with paper files. We also installed a fax server so that incoming faxes were forwarded directly to recipients rather than sit in the open on a fax machine for any passersby to peruse.Client service improved. When clients called, our staff was able to pull up files and knowledgeably discuss specific engagement matters before the greetings and small talk were concluded.

Not to mention, we also went from using eight to ten cases of paper per month to about three cases per calendar quarter.

by Derr ick B. Stark , CPAS C AC PA m e m b e r s i n ce 1 9 9 6

Derrick B. Stark, CPA, CVA is managing member of ClaraVista LLC, a reimbursement and consulting firm serving home medical equipment suppliers throughout the US. Derrick’s areas of expertise include data analytics and application development. He is

past chair of the SCACPA Young CPAs Committee is serves on the Editorial Board. Derrick may be reached at [email protected].

South Carolina CPA Report 18 (888) 557-4814 | www.scacpa.org

People, Planet & Profit | SUSTAINABILITY and THE CPA “I’VE GOT AN UNEASY FEELING ABOUT THIS CLIENT SITUATION”

PROVID ING PROFESSIONAL LIAB ILITY INSURANCE TO CPAS FOR NEARLY A QUARTER CENTURY

Based on an actual conversation between a Senior Partner at a CPA firm and a CAMICO Risk Management Specialist.

CPA: So, my staff member recently noticed some irregularities

in the trial balance provided by my client’s bookkeeper. When I

brought this to my client’s attention, he reacted very negatively

– asking how we could have missed this before, implying it was

somehow our fault. I didn’t know what to say – I’m sure we’ve met

professional standards and our workpapers should support that.

What can I do?

CAMICO: This surprises many CPAs, but after 24 years of

providing professional liability insurance, CAMICO has found

that following professional standards alone may unfortunately not

be enough to avoid a claim.

CPA: Really!? I thought following the rules would keep me safe.

CAMICO: That would seem logical, but in addition to meeting

professional standards, juries expect CPAs to look out for

irregularities and advise and warn clients of risks. So, if something

looks unusual, investigate it, document it and communicate it.

Do you have an engagement letter for this client?

CPA: Yes, the on-call CAMICO Risk Management Specialist

helped us tailor the wording to clearly spell out what services we

were providing and what was not included — it says our firm is

not responsible for detecting fraud and other irregularities — and

the client signed it.

CAMICO: Great! With the client acknowledging the terms of

your services, you have an excellent first line of defense. Now

let’s focus on your next steps, so you can help your client with

their issue without putting yourself at further risk.

CPA: Thank you. It’s good to be able to talk with an expert about

this – it gives me real peace of mind.

DAV I D P O R T E R

1 . 8 0 0 . 6 5 2 . 1 7 7 2

D P O R T E R @ CA M I C O . C O M

CAMICO PROFESSIONAL LIABILITY INSURANCE

IS ENDORSED BY:

AICPA has an ongoing sustainability initiative which, among other things, encompasses being

environmentally friendly. This is not intended to take positions on more controversial issues. We as CPAs deal with ordinary issues daily that, by a slight change in behavior, could be a statement of our recognition of the need to make the best use of the earth’s resources. Some efforts yield a by-product that is more resource-friendly—such going paperless in much of what we do, including file retention. Many firms, companies and governmental entities have gone through or are considering “less paper initiatives,” the thrust of which is to gain efficiencies available through the use of on screen review, electronic files, etc. The byproduct is more deliberate use of paper. Our behavior in many cases is already adjusted to the point that it seems almost unusual at times to hear someone printing or copying a large job.

Here are a few practical suggestions for modifying behavior, much of which is already in place in many organizations.

PAPER AND OTHER CONSUMABLE PRODUCTS Eliminate Styrofoam or plastic cups. Find reusable replacements. Don’t use paper or plastic plates and utensils when it can be avoided. Recycle aluminum, plastic, paper and magazines. Provide convenient collection boxes and arrange for a collection service. Subscribe to e-publications and eliminate former staff and duplicates from mailing lists. Increase the use of recycled paper and other products. Buy with that intention when possible.

Further reduce the use of paper that results in more shredding. Think twice before printing. Determine how the shredding service disposes shredded paper. Is it done in an environmentally friendly way? If not, consider other companies. Print on both sides of the paper when that is plausible. Consider the use of a fax server as a means of receiving but not printing faxes. Use whiteboards or projection equipment to present meeting agendas rather than printing them. Use forms available electronically for internal communication such as for vacation requests, expense reports, CPE requests, etc. If you are in public practice, ask clients whether they want the information electronically or on a thumb drive. Don’t assume a client wants a printed copy of their tax return, or provide only upon request. Electricity Consider using laptop computers rather than desktops. Laptops tend to be more power efficient and provide greater mobility. New computers, monitors and applicances are generally more energy-efficient than older versions. Donate older equipment to local charities, many of which will pick equipment from your office. Turn off unnecessary equipment and lights when you leave the office for the day or for an extended period of time. Be sure to develop an internal policy regarding turning off or sleep modes for computer workstations. Integrate energy-efficient light bulbs and remove light bulbs that are not in use. Do not use portable heaters or fans unless there is a confirmable ineffectiveness in the ability of the central system to heat or cool your area.

TRAVEL Before travelling, think about whether you can handle the matter with a phone call or e-mail. When you travel to meetings or other events, car pool with others when you can.

OTHER CONSIDERATIONS Consider limiting or eliminating the use of bottled water. Tap water is usually fine, or consider a filtered water service. Recycle ink cartridges and batteries. Set up collection boxes for ink cartridges from home that you wish to recycle. Some office supply stores will give a credit on the purchase of ink cartridges when empties are brought in for recycling. Buy eco-friendly soap, dish washing detergent, etc. Eliminate aerosol products from the office.

These are but a few ideas that do not require additional spending but result in savings in most circumstances. We believe these practices are not about political statements or cost-benefit studies, but about being good stewards of the resources we depend on in our profession and being practical with their use. Slight modifications in our behavior may yield disproportionate results.

Practical Green: The Regional Firm Perspectiveby V. Carrol l Webster, MBA, CPASCACPA member s ince 1975

Carroll Webster has served as Managing Partner of WebsterRogers LLP for some 24 years. Formerly, he was an associate professor at Francis Marion University. Webster has been active in the CPA profession both nationally

and in South Carolina. He is a past president of SCACPA and served six years as South Carolina’s elected representative on the Governing Council of the American Institute of CPAs.

People, Planet & Profit | SUSTAINABILITY and THE CPA “I’VE GOT AN UNEASY FEELING ABOUT THIS CLIENT SITUATION”

PROVID ING PROFESSIONAL LIAB ILITY INSURANCE TO CPAS FOR NEARLY A QUARTER CENTURY

Based on an actual conversation between a Senior Partner at a CPA firm and a CAMICO Risk Management Specialist.

CPA: So, my staff member recently noticed some irregularities

in the trial balance provided by my client’s bookkeeper. When I

brought this to my client’s attention, he reacted very negatively

– asking how we could have missed this before, implying it was

somehow our fault. I didn’t know what to say – I’m sure we’ve met

professional standards and our workpapers should support that.

What can I do?

CAMICO: This surprises many CPAs, but after 24 years of

providing professional liability insurance, CAMICO has found

that following professional standards alone may unfortunately not

be enough to avoid a claim.

CPA: Really!? I thought following the rules would keep me safe.

CAMICO: That would seem logical, but in addition to meeting

professional standards, juries expect CPAs to look out for

irregularities and advise and warn clients of risks. So, if something

looks unusual, investigate it, document it and communicate it.

Do you have an engagement letter for this client?

CPA: Yes, the on-call CAMICO Risk Management Specialist

helped us tailor the wording to clearly spell out what services we

were providing and what was not included — it says our firm is

not responsible for detecting fraud and other irregularities — and

the client signed it.

CAMICO: Great! With the client acknowledging the terms of

your services, you have an excellent first line of defense. Now

let’s focus on your next steps, so you can help your client with

their issue without putting yourself at further risk.

CPA: Thank you. It’s good to be able to talk with an expert about

this – it gives me real peace of mind.

DAV I D P O R T E R

1 . 8 0 0 . 6 5 2 . 1 7 7 2

D P O R T E R @ CA M I C O . C O M

CAMICO PROFESSIONAL LIABILITY INSURANCE

IS ENDORSED BY:

People, Planet & Profit | SUSTAINABILITY and THE CPA

South Carolina CPA Report 20 (888) 557-4814 | www.scacpa.org

Is this “1% Renewable”? SC Electric Cooperatives ‘Walk the Talk’ on Energy Efficiency and Renewables

Energy efficiency and renewable energy became media buzzwords in recent years, but they’ve been the

talk—and the walk—of South Carolina’s electric cooperatives for at least a decade. About 1.5 million South Carolinians in all 46 counties use power delivered by 20 electric distribution cooperatives. Central Electric Power Cooperative purchases and transmits power on behalf of all 20 co-ops. Collectively, Central’s member co-ops build and maintain the state’s largest power distribution system, with more than 70,000 miles of power line covering 70 percent of South Carolina.

Today, cooperatives are responding to the desire to reduce greenhouse gas emissions quickly and the growing demand for power. Some people say we can meet demand through efficiency and renewable energy. The reality is we need all the efficiency and renewable energy we can get, as well as all the electricity we can get from traditional sources. And we must deliver this power to South Carolinians at a price they can afford.

wHY EFFICIENCY MATTERSExperts predict a 30 percent increase in the demand for electricity by 2030. This demand comes at a price to consumers’ wallets and the environment. A 600-megawatt (MW) plant generates enough electricity to power more than 400,000 homes. The cost to build a plant generating this much electricity is approximately $1.5 billion for a coal-fired plant, $3 billion for nuclear and $400 million for natural gas. Consumers pay to have these plants built through their monthly electric bills. These plants also impact the environment: a 600 MW coal plant adds four million tons of CO2 to the atmosphere each year.

wHAT CO-OPS ARE DOINGIn 2007, S.C. co-ops committed up to 1.1 percent of their wholesale power costs (approximately $12 million per year) to invest in renewable energy and energy

efficiency projects. A co-op commissioned study that year found that renewable resources could potentially produce enough energy to meet the energy needs of 13 to 18 percent of the co-op members in the state. Yet, even at this point, the co-ops had already been supporting one form of renewable energy for several years.

GREEN POwERIn 2001 some co-ops began marketing Green Power1, the first renewable energy program for consumers in the state, in cooperation with Santee Cooper. The state-owned utility produces most of the power used by South Carolina’s electric cooperatives. Today, all 20 distribution co-ops in South Carolina give their members the opportunity to purchase Green Power. Santee Cooper generates Green Power at five landfill generation plants around South Carolina. Naturally occurring methane, a potent greenhouse gas, is captured for use as fuel.

In general, Green Power facilities are more expensive to install than power plants that generate electricity using traditional fuel sources such as coal. Members who chose to support the program pay a higher price for it than for conventional service. All of the added revenues collected as part of the Green Power program go to offset the higher cost associated with generating this power.

Ronald J. Calcaterra is president and chief executive officer of Central Electric Power Cooperative, Inc., South Carolina’s generation and transmission electric

cooperative, headquartered in Columbia. He has served the company and the members of South Carolina’s electric cooperatives for more than 30 years.

by Ronald J . Calcaterr ra , Pres ident and Chief Execut ive O ff icer, Centra l E lec tr ic Power Cooperat ive, I nc.

“A co-op commissioned study that year found

that renewable resources could potentially produce

enough energy to meet the energy needs of 13 to

18 percent of the co-op members in the state.”

South Carolina CPA Report 21(888) 557-4814 | www.scacpa.org

People, Planet & Profit | SUSTAINABILITY and THE CPA

Statewide, more than 3,600 residential members purchase the higher-cost Green Power. EFFICIENCY FIRSTWhile alternative energy sources show promise, Central’s leadership recognized early on that promoting energy efficiency was a sure-fire, here-and-now way to help members cut energy costs and power plants cut emissions. The “low-hanging fruit” in the energy-efficiency orchard was lighting, which accounts for about 10 percent of the average home’s energy consumption. What’s more, cost-effective technology already existed—such as energy-efficient compact fluorescent lighting (CFLs)—to lighten the co-ops’ lighting load. CFLs use 75 percent less energy than standard incandescent bulbs and last up to ten times longer.

In 2008, S.C. co-ops began the Do the Light Switch2 program distributing CFLs to co-op members. By the end of 2010, co-ops will

have distributed more than two million CFLs to residential consumers. In one year, those two million CFLs could save over 114,000 megawatt-hours—enough to power almost 10,000 homes and reduce CO2 emissions by over 200,000 tons. When the CFL program is completed at seven million CFL’s, we expect to reduce total energy requirements by more than two to three percent of current levels. This represents a savings of $20 to 30 million per year to S.C. cooperative members.

SEEKING SOLUTIONSDo the Light Switch was just the beginning. The co-ops received a $3.4 million grant this year from the state Energy Office for a Residential Energy Efficiency Pilot Program. The pilot will examine energy efficiency alternatives to determine which gets the most bang for the buck. These alternatives include roofing and other weatherization of mobile homes, installation of energy efficient appliances, and the installation of solar

water heaters. Energy usage data will be obtained before and after each program to determine the cost benefit ratio. The program will be expanded for those programs that show promise in achieving energy savings at the lowest cost.

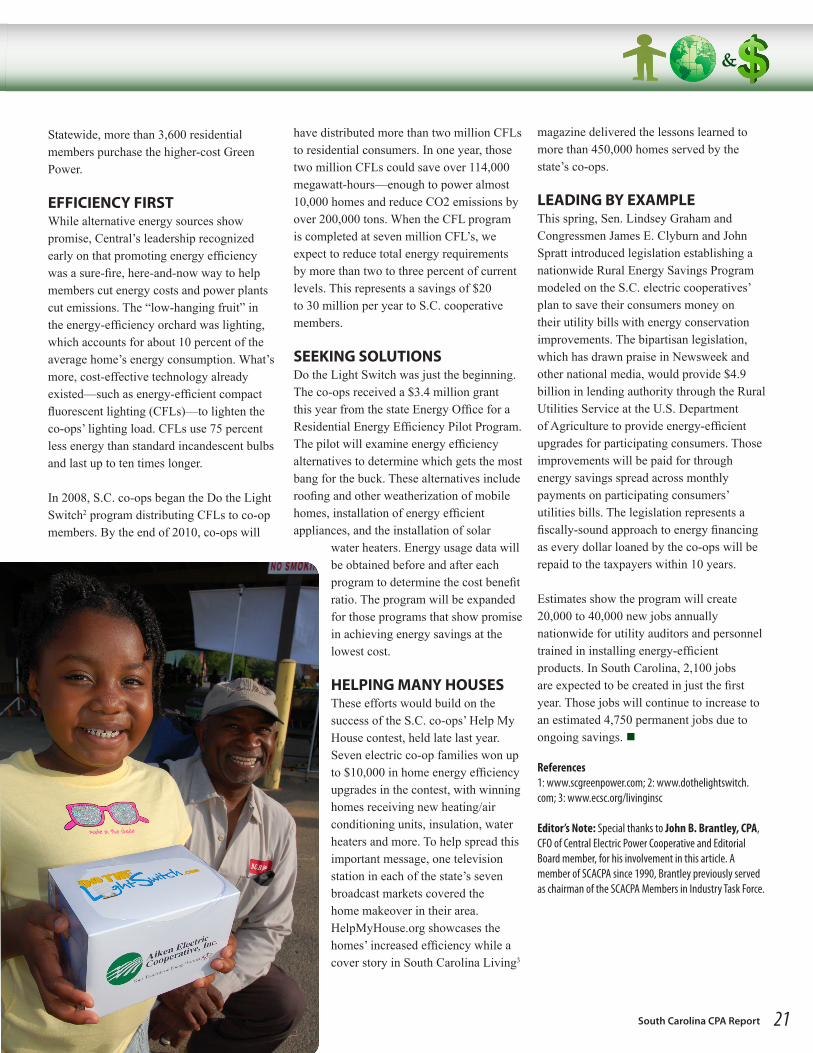

HELPING MANY HOUSES These efforts would build on the success of the S.C. co-ops’ Help My House contest, held late last year. Seven electric co-op families won up to $10,000 in home energy efficiency upgrades in the contest, with winning homes receiving new heating/air conditioning units, insulation, water heaters and more. To help spread this important message, one television station in each of the state’s seven broadcast markets covered the home makeover in their area. HelpMyHouse.org showcases the homes’ increased efficiency while a cover story in South Carolina Living3

magazine delivered the lessons learned to more than 450,000 homes served by the state’s co-ops.

LEADING BY EXAMPLEThis spring, Sen. Lindsey Graham and Congressmen James E. Clyburn and John Spratt introduced legislation establishing a nationwide Rural Energy Savings Program modeled on the S.C. electric cooperatives’ plan to save their consumers money on their utility bills with energy conservation improvements. The bipartisan legislation, which has drawn praise in Newsweek and other national media, would provide $4.9 billion in lending authority through the Rural Utilities Service at the U.S. Department of Agriculture to provide energy-efficient upgrades for participating consumers. Those improvements will be paid for through energy savings spread across monthly payments on participating consumers’ utilities bills. The legislation represents a fiscally-sound approach to energy financing as every dollar loaned by the co-ops will be repaid to the taxpayers within 10 years.

Estimates show the program will create 20,000 to 40,000 new jobs annually nationwide for utility auditors and personnel trained in installing energy-efficient products. In South Carolina, 2,100 jobs are expected to be created in just the first year. Those jobs will continue to increase to an estimated 4,750 permanent jobs due to ongoing savings.

References1: www.scgreenpower.com; 2: www.dothelightswitch.com; 3: www.ecsc.org/livinginsc

Editor’s Note: Special thanks to John B. Brantley, CPA, CFO of Central Electric Power Cooperative and Editorial Board member, for his involvement in this article. A member of SCACPA since 1990, Brantley previously served as chairman of the SCACPA Members in Industry Task Force.

South Carolina CPA Report 22 (888) 557-4814 | www.scacpa.org

Charleston and Grand Strand RegionVictoria G. Dotson – Vice President & Manager of Trust Services

Peter Alan Curcio – Senior Trust Officer843.724.0801

Elsewhere in South CarolinaMary Ann Brown – Senior Trust Officer

843.815.5507

www.firstfederal.com

When you recommend a trust manager to your clients,you’re putting your relationship on the line. You want torefer them to a trust officer who looks out for them thesame way you do. At First Federal, we do.

Our trust officers are easily accessible and they’re alwaysglad to meet when it is most convenient for your client.We can establish a trust with fewer assets than you mightthink – and at First Federal, all of our trust clients receivethe same high level of personal service. That’s a level ofservice other banks can’t match.

We’re one of the strongest and most trusted banks inSouth Carolina, with the resources to help our clientsaccumulate, preserve and protect their wealth with all thetrust services you’d expect, plus:

• Conservatorships• Special Needs Trusts• Irrevocable Life Insurance Trusts

And through our Estate Settlement Services, we evenwork on a contract basis with clients who don’t have aFirst Federal trust account.

If you’re interested in referring a prospective trust client toFirst Federal, please call one of our trust officers today.They’re looking forward to hearing from you.

Our trust officers providethe same level of personal

service that you do.

FRST-1523 SC CPA Report - 8.5” x 11” - Full Bleed - 4C

FRST-1523_Attorneys_SCCPAReport.qxd:Layout 2 2/10/09 2:50 PM Page 1

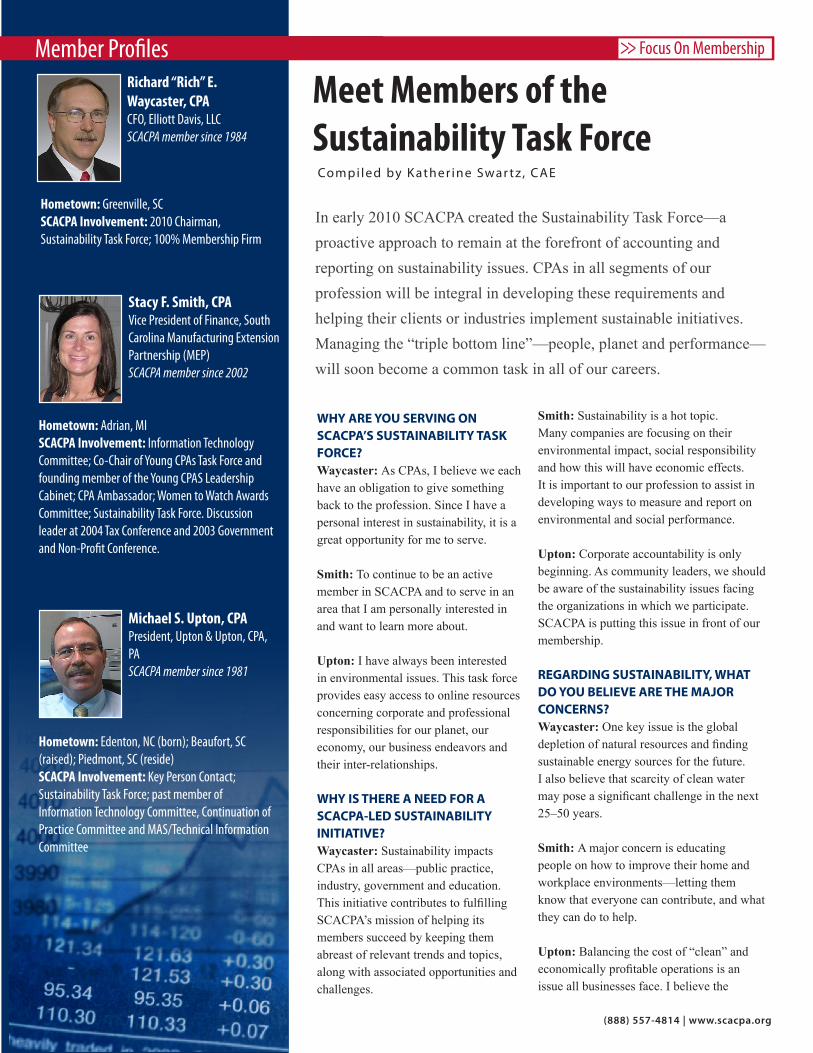

Introducing the SCACPA Sustainability Task ForceUnder direction of Rich Waycaster, CPA, the new task force has eight members and has divided its projects into three primary areas:

TECHNICAL STANDARDS &ADVOCACY Climate Change Reporting Standard: compose educational piece on how this will affect our profession. Research and follow developments in other service industries as well as state and national CPA organizations. Monitor and catalog reporting and assurance guidance and standards, regulatory/legislative alerts and tax credits/opportunities. Become a resource for information regarding certification, measurement and verification, including industry-specific topics. Identify and track “hot areas.” Identify South Carolina CPA service offerings in consulting, assurance, tax and niche fields.

1,000 POINTS OF GREEN PROGRAM Research and endorse a green program for small business. Guide SCACPA’s internal green initiative. Provide tools, checklists and implementation strategies for members. Monitor and report impact of green initiatives on South Carolina’s economy. Develop recognition tactics such as “Green Business of the Year” or “Green CPA Firm of the Year.”

AwARENESS AND PROMOTIONS Develop and maintain online content including resources, links and hot issues. Design brochures for educational awareness. Promote 1,000 Points of Green Program. Promote and schedule relevant CPE for SCACPA members. Promote university and other resource programs available to members.

People, Planet & Profit | SUSTAINABILITY and THE CPA

What Is SCACPA Doing? Members, Planet and Profit: Sustainability & Your Associationby K ather ine Swar tz , CAES e r v i n g S C AC PA s i n ce 2 0 0 6

Katherine Swartz, CAE is SCACPA’s member services director, co-staff liaison to the Sustainability Task Force, staff leader of the SCACPA Green Team and managing

editor of The CPA Report. With more than ten years experience in the association management and non-profit sectors, Katherine is a Certified Association Executive, the highest credential in the association management profession.

Just like many of our member firms and organizations, SCACPA can benefit from the triple bottom line microscope. Our 200-