Embed Size (px)

Citation preview

Financial statements Regulatory Framework & Interpretation

A report on Vinamilk Corporation

Prepared for: Ms. Kim Oanh Vu

Unit 10: Financial Accounting and Reporting

Banking Academy, Hanoi

BTEC HND in Business (Finance)

Word number: 3,323

Prepared by

Ph m Thúy H ng – Cow – F04Bạ ằ

Registration No. ITPF04-055

Submission Date: 9th January 2013

Cow-F04B-FR A2 Page 1

Financial statements Regulatory Framework & Interpretation

Cow-F04B-FR A2 Page 2

Financial statements Regulatory Framework & Interpretation

Table of ContentsEXECUTIVE SUMMARY.....................................................................................................................................3

INTRODUCTION...................................................................................................................................................4

I. THE REGULATORY FRAME WORK FOR FINANCIAL REPORTING.......................................5

1.1 The different users of financial statement and their needs.................................................5

1.2 Assessment of the implications for users...............................................................................6

1.2.1 Liquidity ratio...................................................................................................................................6

1.2.2 Debt and gearing ratio...........................................................................................................6

1.2.3 Efficiency ratio.......................................................................................................................... 7

1.2.4 Shareholders investment ratio..........................................................................................7

1.3 Legal and regulatory influences on financial statements................................................7

1.3.1 Companies Act 1985...............................................................................................................7

1.3.2 Partnership Act 1890.............................................................................................................8

1.3.3 International European Directives...................................................................................8

1.3.4 International Accounting standard..................................................................................9

1.3.5 UK Accounting standard....................................................................................................10

2 INTERPRETATION OF FINANCIAL STATEMENTS...................................................................12

2.1 Accounting ratios calculation...................................................................................................12

2.1.1 Profitability..............................................................................................................................12

2.1.2 Liquidity.................................................................................................................................... 13

2.1.3 Debt/gearing ratio................................................................................................................14

2.1.4 Efficiency ratio........................................................................................................................15

2.1.5 Investment ratio....................................................................................................................15

2.2 A report on incorporating & interpreting accounting ratios with suitable

comparisons................................................................................................................................................... 17

CONCLUSION......................................................................................................................................................23

Cow-F04B-FR A2 Page 3

Financial statements Regulatory Framework & Interpretation

REFERENCES...................................................................................................................................................... 24

APPENDIX............................................................................................................................................................ 26

EXECUTIVE SUMMARY

This report is prepared for the Director of Finance of Vinamilk Corporation. . Vinamilk

is the leading Dairy & Beverage Company and also one of the 5 largest companies in term

of market capital listed in Vietnam. The brand “Vinamilk”, with its extensive market share

and position, has gone into consumers’ mind. Vinamilk’s quality products are designed to

offer the community a “healthy and beautiful life”.

This report provides the regulatory framework for financial reporting as well as interpretation

of financial statement. Methods of analysis include horizontal and ratios.

The report finds the prospects of Vinamilk in its current position are quite positive. Some

weaknesses expressed through some specific ratios will be mentioned. Some

recommendations could be:

- Increase sales

- Improve asset turnover

- Increase dividend yield

- Decrease current ratio

Cow-F04B-FR A2 Page 4

Financial statements Regulatory Framework & Interpretation

INTRODUCTION

This report aims to discuss about the regulatory framework for financial reporting and

the interpretation of financial statements. In more particular, several following issues

will be addressed:

- The different users of financial statements and their needs

- The legal and regulatory influences on financial statements

- The implication of users

- How regulations are dealt with by accounting and reporting standards

- Accounting ratios calculating

- Report incorporating and interpreting accounting ratios, including suitable

comparisons.

Not only provide the theory related to financial terms, this paper also provides relevant

analysis and explanation in each area. Doing this report, some information sources were used

Such as: Internet and books, some lectures, journal articles, and business magazines were

also use to utilize data related to the topic in the scenario.

Cow-F04B-FR A2 Page 5

Financial statements Regulatory Framework & Interpretation

I. THE REGULATORY FRAME WORK FOR FINANCIAL REPORTING

1.1 The different users of financial statement and their needs

Employees: Vinamilk’s employees needs information in financial reporting to

assess company’s profitability and its consequence on their future remuneration

and job security (Accouting-Simplified, n.d.). They require information on the

ability of Vinamilk to meet wage demands and avoid redundancies. These

information are, for example: profitability, revenue, liability and so on which can be

shown in income statement.

Government: Vietnam’s government need Vinamilk’s financial reports to assess

tax, prepare for various statistic on productivity, commerce, etc. and the various

returns required by law. They might require such information as the detail sales,

activity, profits, investments, stocks, dividend paid, the proportion of profits

absorbed by taxation and so on. Those information are shown in Vinamilk’s income

statement and balance sheet.

Suppliers: Vinamilk has build relationship with some suppliers like: Fonterra

(SEA), Tetra Pak Indochina, Perstima Binh Duong and so on. Suppliers need to know

about the current status of the company through: profit, liability, sales, cash and so

on to assess their power over Vnamilk and Vinamilk’s ability to pay for the

materials supplied. Those information can be shown in income statement, cash flow

statement and balance sheet.

Shareholders: Vinamilk’s shareholders needs the financial report of the company

for analyzing the viability and profitability of company’s investment and

determining their decision in the future. They mainly requirement information

about the profit Vinamilk gain and the dividend for them. They expect to receive a

dividend payments as their shares of the profits. They are interested in the profit

and loss statement.

Lenders: They always concern about the capacity of Vinamilk to pay its liabilities as

they fall due for payment. Therefore, they of course require information on

Cow-F04B-FR A2 Page 6

Financial statements Regulatory Framework & Interpretation

Vinamilk’s ability to meet its financial obligations through the information about

company’s liability, cash, profit which can be shown in income statement.

Customers: Vinamilk has a large market share which account for 39% of the

country. Vinamilk’s customers need the financial information from the company

because it effects to their credibility to the company and their buying decisions.

Customers might care mainly about Vinamilk’s profit which can be shown in profit

and loss statement

General public: they care about Vinamilk’s financial statement to interpret and

observe how they fair in performance. They obtain indicaes from it which is sued to

advise their investing public. Those can be profit, liability, cash and so on which can

be shown in Vinamilk’s income statement, balance sheet and cash flow statement.

I.2 Assessment of the implications for users

1.2.1 Liquidity ratio

Liquidity ratio measures company’s capacity to meet short-term financial

commitments as they become due. This ratio includes three more ratios which

are: current ratio, quick ratio and cash ratio. Based on the analysis about needs of

different users above, it seems that the users have the most concern about this

ratio are lenders and suppliers. For example, Fonterra (SEA) is a milk supplier of

Vinamilk, during the process of supplying milk for Vinamilk, the accountant of

Fonterra needs to track the liquidity ratio of Vinamilk to make sure that Vinamilk

can afford the expense of milk they supply under the contract. Regards to

lenders, when Vinamilk borrow money from banks, Agribank for example, the

bank will care about liquidity ratio to see if Vinamilk can pay off the debts.

1.2.2 Debt and gearing ratio

Debt and gearing ratio is quite similar, they refers to the relationship between

the various long-term form of financing and equity share capital. The users that

are interested in these ratios are lenders and stockholders. The debt capital of

Vinamilk can be debentures, loan stock, preference share capital and so on. While

equity capital consists of ordinary share capital, share premium and so on. Take

gearing ratio in particular, Agribank, who lends Vinamilk a long-term loan, will

Cow-F04B-FR A2 Page 7

Financial statements Regulatory Framework & Interpretation

care about gearing ratio. If the ratio is over than 50%, it means that Vinamilk is

likely to have difficulties in the future when it wants to borrow more from the

bank. Or with shareholders, the more highly geared the company, the greater the

percentage change in profit available for ordinary shareholders for any given

percentage change in profit before interest and tax.

1.2.3 Efficiency ratio

This ratio is used to measure how well Vinamilk can manage income and

expenses. It includes three more ratios, receivable payment period, inventory

turnover period and payable turnover. There could be variety of users care about

this ratio. Take inventory turnover ratio for example, it measure how well

Vinamilk is turning their inventory into sales. Milk suppliers would care about

this because if this ratio is high, it means that the demand for the product being

sold is low, that can make Vinamilk decrease the amount of milk purchase.

1.2.4 Shareholders investment ratio

This ratio is helpful for investors at large and shareholders in particular. They

use this ratio to assess their investment in the company. This ratio includes some

other ones like: P/E, dividend yield, dividend cover ratio and so on. Take

dividend yield ratio as an example, it would help shareholder to measure

percentage return that Vinamilk pays out to them in form of dividend. They

usually expect high dividend yield ratio because it means they can get higher

from Vinamilk. However, some investors may look for the stability of the high

dividend yield rather than its growth. They do not want to lose out in the long

term because of high dividends in the short term. Therefore, Vinamilk should

ensure that the high dividend yield is not just a temporary phenomenon but

sustainable.

1.3 Legal and regulatory influences on financial statements

1.3.1 Companies Act 1985

In 1985, all existing companies legislation was brought together in a number of

consolidating Acts, of which by far the most important is the Companies Act 1985

(CA1985). The Companies Act 1985 requires companies to include a note to the

Cow-F04B-FR A2 Page 8

Financial statements Regulatory Framework & Interpretation

accounts stating that the accounts have been prepared in accordance with applicable

accounting standards or, alternatively, giving details of significant departures from

those standards.

The form and content of the accounts are regulated primarily by CA 1985. As far as

the preparation of accounts is concerned, the overriding requirement of companies’

legislation is that accounts should show a ‘true and fair view’.

Additionally, the legislation such as Company Act 1985 or Company Act 1989 also

required that the accounts of any limited company above a certain size must be

audited. An audit, for this purpose, may be defined as an ‘independent examination

of, and expression of opinion on, the financial statements of an enterprise’. This

means in practice that a limited company must engage a firm of chartered or certified

accountants to conduct an examination of its accounting records and its financial

statements in order to form an opinion as to whether the accounts which are to be

published present a ‘true and fair view’. At the conclusion of their audit work, the

auditors issue a report which is published as part of the accounts.

1.3.2 Partnership Act 1890

The formation of a partnership is relatively simple and does not require any

formalities. According to the Partnership Act 1890 a partnership automatically comes

into existence when persons are “carrying on a business in common with a view of

profit”.

Partnerships are usually regulated by contractual agreements between the partners,

although this is not compulsory. What the Partnership Act 1890 seeks to do is to

compensate for the lack of a Partnership Agreement or fill in any gaps in a Partnership

Agreement by implying certain terms. (Anon., 2012)

Ultimately, the purpose of the Partnership Act 1890 is to treat all partners fairly and

equally because a partnership is a relationship which requires utmost good faith. This

is a duty which applies throughout the life of the partnership until a partner’s

retirement; although it is worth noting that a retired partner continues to be liable for

any breaches of duty whilst they were a partner. (Anon., 2012)

1.3.3 International European Directives

EU directives lay down certain end results that must be achieved in every Member

State. National authorities have to adapt their laws to meet these goals, but are free to

Cow-F04B-FR A2 Page 9

Financial statements Regulatory Framework & Interpretation

decide how to do so. Directives may concern one or more Member States, or all of

them.

Each directive specifies the date by which the national laws must be adapted - giving

national authorities the room for manoeuvre within the deadlines necessary to take

account of differing national situations.

Directives are used to bring different national laws into line with each other, and are

particularly common in matters affecting the operation of the single market (e.g.

product safety standards). (Europa, n.d.)

1.3.4 International Accounting standard

International Financial Reporting Standards (IFRSs) are produced by the International

Accounting Standards Board (IASB). The IASB develops IFRSs through an

international process that involves the world-wide accountancy profession, the

preparers and users of financial statements, and national standard setting bodies. In

many countries, some or all companies are required to follow IFRSs, rather than

national standards. (Education, 2010)

The advantages to investors is clear. IFRSs make it easier to compare the accounts of

companies in different countries. They also incorporate many improvements on most

current standards. As things stand, the problem of differences in accounting standards

will continue to exist for some time.

However, IFRSs do not completely eliminate national differences. In the EU an IFRS

only applies after it has been through an approval process and most other countries

have similar procedures. There may also be differences in interpretation of IFRSs by

national standards bodies, and by national standards that fill in gaps in IFRSs (e.g.

valuations of particular types of asset).

Major changes in the UK that resulted from the adoption of IFRSs include:

The treatment of goodwill

The value of options issued as remuneration being shown as a cost on the face

of the P & L

The use of fair value rather than book value for assets acquired in a takeover

Valuation of embedded options.

Cow-F04B-FR A2 Page 10

Financial statements Regulatory Framework & Interpretation

(Moneyterms, n.d.)

1.3.5 UK Accounting standard

The Financial Reporting Council (FRC)

FRC is responsible for funding and ensures the smooth running of the standard

setting process. Its most important task is to set a general work programme for

ASB, along with a guide to broad policy issues. (BPP, 2010). In more particular,

the role of FRC includes:

Investigating cases of accounts that may not adhere to the requirements

of accounting standards and the Companies Act.

Acting as a disciplinary body for accountants, although it only

investigates cases of "public interest" referred to it by the accountancy

bodies.

Authorising accountants' professional bodies to act as supervisory bodies

for the profession and to offer professional qualifications. It also

overseas these bodies.

Setting accounting standards

The oversight of actuaries and setting actuarial standards.

The standards setting part of the FRC's responsibilities are limited in scope

because of the adoption of IFRSs. The FRC's standard setting arm, the ASB, now

sees its main role as influencing the development of IFRSs. (Moneyterms, n.d.)

The Accounting Standards Board (ASB)

The role of the Accounting Standards Board (ASB) was to issue accounting

standards. It was recognised for that purpose under the Companies Act 1985. It

took over the task of setting accounting standards from the Accounting Standards

Committee (ASC) in 1990.

The ASB also collaborated with accounting standard-setters from other countries

and the International Accounting Standards Board (IASB) both in order to

influence the development of international standards and in order to ensure that

its standards were developed with due regard to international developments.

(FRC, n.d.)

The Financial Reporting Review Panel (FRRP)

Cow-F04B-FR A2 Page 11

Financial statements Regulatory Framework & Interpretation

The FRRP examines accounts published by companies if it appears that

Companies Act requirements have been breached. In particular, the requirement

that accounts should show a true and fair view. (BPP, 2010)

The Urgent Issues Task Force (UITF)

The UITF was part of the previous standard setting arrangements and assisted the

ASB by investigating areas where conflicts or unsatisfactory interpretation of an

accounting standard or Companies Act provision existed or may have developed

in the future

The UITF reached a consensus on the issues it investigated and published

abstracts to guide the preparation of financial statements. In order for accounts to

present a true and fair view, they must comply with UITF Abstracts. UITF

Abstracts and Information Sheets are available to download from the UITF

pages of the FRC website. (ICAEW, n.d.)

Cow-F04B-FR A2 Page 12

Financial statements Regulatory Framework & Interpretation

2 INTERPRETATION OF FINANCIAL STATEMENTS

2.1 Accounting ratios calculation

2.1.1 Profitability

Formula Indication Vinamilk 2011 Interpretation

Gross Profit Margin

Gross ProfitRevenue

Measure how much profit firms can

make on its cost of sales

29.85% Vinamilk earned 298.5 VND for each

thousand VND of its turnover in

2011

Return on capital employed (ROCE)

Profit before interest∧taxationCapital Employed

= ¿Profit before interest∧taxationTotal assets−current liablity

It is the rate of return a business is

making on the total capital employed in

the business

39.5% Vinamilk can generate 39.5% of

earning from capital employed. In

other words, it can earn 393 VND

from 1000 VND of total capital

employed.

Return on Equity (ROE)

Profit after taxEquity shareholder s' fund

Measure how much profit a company

generates with the money shareholders

have invested

33.81% Vinamilk can generate 338.1 VND in

total 1000 VND of shareholders’

equity

Asset turnover ratio

Cow-F04B-FR A2 Page 13

Financial statements Regulatory Framework & Interpretation

SalesCapital Employed

Measures a company’s efficiency at

using its assets in generating sales or

revenue from its capital

1.75 Vinamilk can generate the revenue

of sales 1.75 times from capital

2.1.2 Liquidity

Formula Indication Vinamilk 2011 Interpretation

Current ratio

Current assetsCurrent liablities

Measure the ability of the company to

pay back its short-term liabilities with

its short-term assets. For most

industrial companies, 1.5 may be an

acceptable current ratio

3.21 Current ratio of Vinamilk is much

more than 1.5. It means that

Vinamilk may not be using its

current assets or its short-term

financing facilities efficiently.

Quick ratio

Current assets−stocksCurrent liablities

Measure the ability of the company to

pay back its short-term obligations

with its most liquid assets. A company

with a Quick Ratio of less than 1 cannot

currently pay back its current liabilities.

2.06 Quick ratio of Vinamilk is higher than

1. It means that this company

currently can pay back its current

liabilities.

Cash ratio

Cow-F04B-FR A2 Page 14

Financial statements Regulatory Framework & Interpretation

Cash+CashequivalentsCurrent Liabilities

Measure how quick firms can repay its

short term debts. In some countries a

cash ratio of not less than 0.2 is

considered as acceptable.

1.07 This result shows that Vinamilk has

sufficient cash and cash equivalents

to repay its current debt.

2.1.3 Debt/gearing ratio

Formula Indication Vinamilk

2011

Interpretation

Debt ratio

TotaldebtsTotalassets

Measure a company’s total debt to its

total assets. 50% is considered as a

safe limit

19.93% Debt ratio of Vinamilk is lower than

50%. It means that most of

Vinamilk’s assets are financed

through equity. safe

Gearing ratio

Long−termdebtShareholder s' equity+Long−termdebt

Focus on the capital structure of the

business – that means the proportion

of finance that is provided by debt

relative to the finance provided by

equity (or shareholders).

1.26% Gearing ratio of Vinamilk is lower

than 25%. It means that Vinamilk is

described as having “low gearing”

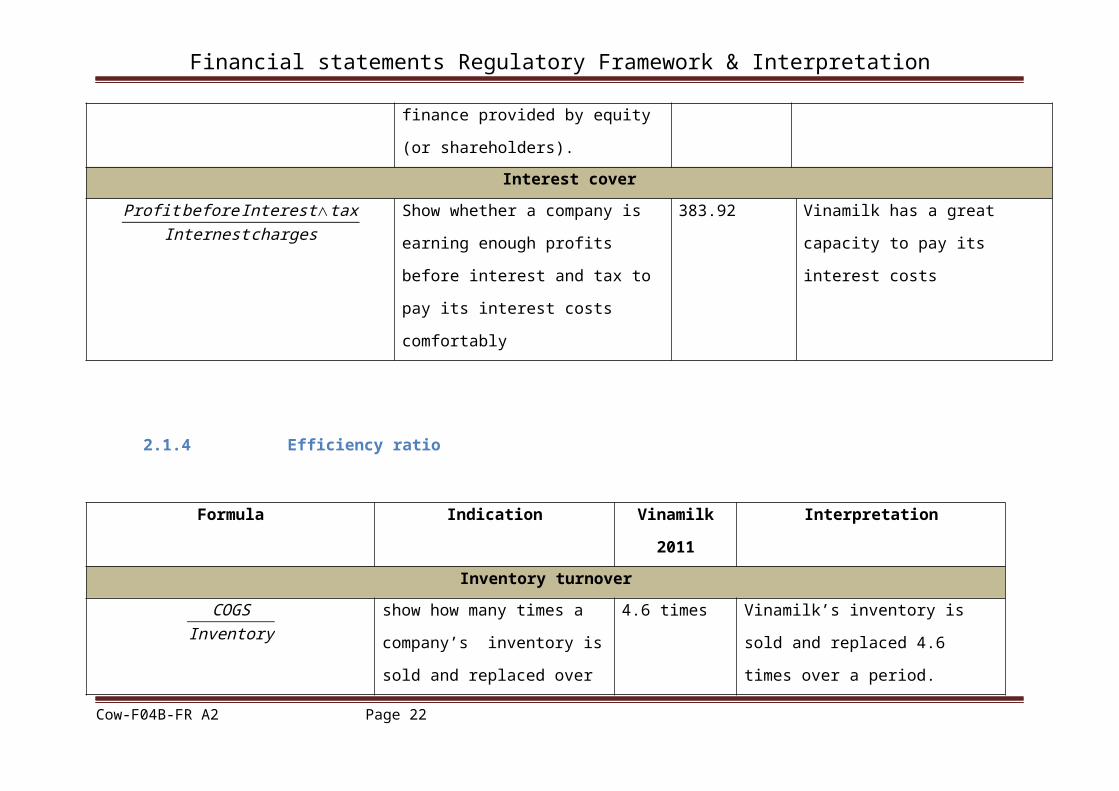

Interest cover

Cow-F04B-FR A2 Page 15

Financial statements Regulatory Framework & Interpretation

Profit before Interest∧taxInternest charges

Show whether a company is earning

enough profits before interest and tax

to pay its interest costs comfortably

383.92 Vinamilk has a great capacity to

pay its interest costs

2.1.4 Efficiency ratio

Formula Indication Vinamilk 2011 Interpretation

Inventory turnover

COGSInventory

show how many times a

company’s inventory is sold and

replaced over a period

4.6 times Vinamilk’s inventory is sold and

replaced 4.6 times over a period.

Inventory days

InventoryCost of sales

x365 Indicate the average number of

days goods remain in inventory

before being sold

79.41 days Vinamilk’s goods are remained

averagely 79.41 days before being

sold

2.1.5 Investment ratio

Formula Indication Vinamilk 2011 Interpretation

Cow-F04B-FR A2 Page 16

Financial statements Regulatory Framework & Interpretation

Earnings per share

Net earnings for ordinary shareholderNumber of ordinary shares

Give investors a means of determining

the amount the business earned on

their stock share investments.

7.717 The earnings Vinamilk generated per

one share of stock in 2011 is 7.717

VND

Price-earnings

Share priceEPS

A ratio of the current market price of

the stock in the stock market and the

net profit earned by the company per

share

11.53 times Investors had to pay 11.53 VND for

every 1 VND of Vinamilk’s earnings

in 2011.

Dividend yield

Dividend per shareMarket value per share

Measure how many percentage return a

company pays out to shareholders in

the form of dividends

3% Investors have potential to earn 3%

on their investment for each VND

they invest in Vinamilk in 2011

Dividend cover

EPSDividend per oridnary shares

show how much the corporation’s net

profit is paid out as dividends

2.58 times Vinamilk’s profit attribute to

shareholders was 2.58 times the

amount of dividend paid out.

Cow-F04B-FR A2 Page 17

Financial statements Regulatory Framework & Interpretation

2.2 A report on incorporating and interpreting accounting ratios with suitable

comparisons

VINAMILK’S RATIO REPORT

To: Director of Finance

From: Client Service Manager

Date: 9 January 2013

Performance and financial position of Vinamilk

As required, I have analysed the the performance and position of Vinamilk with

special reference to accounting ratios. The calucation of the ratios is shown in the

previous part and also in Appendix. Thu purpose of this paper is to assess the

operating and financial position of Vinamilk

General comments

Vinamilk Corporation is the leading producer of dairy products in Vietnam based

on sales volume and revenue. Since Vinamilk was establish in 2976, its position

in dairy market is non-stop developing through the significant growth of market

share as well as production portfolio. This company has built the largest

distribution network in Vietnam and have leveraged the network to introduce

new products to the markets. It is forecasted that Vinamilk Corporation will be

continually developing and growing in the future.

Profitability

Gross margin ratio for three years

2011 2010 200929.85% 32.17% 35.84%

There is an decrease in gross margin ratio of Vinamilk from 2009 to 2011. This

ratio indicates the efficiency of the company, therefore it can be said that

Vinamilk achieved higher efficiency ratings since 2009 but it tend to be

Cow-F04B-FR A2 Page 18

Financial statements Regulatory Framework & Interpretation

decreased. Vinamilk should try to increase it the future. It should be able to make

a decent profit as long as overhead costs are controlled.

ROCE ratio for three years:

2011 2010 200939.50% 52.38% 39.71%

Based on the indication of ROCE ratio above, it is clear that the higher the

percentage figure, the better. From 2009 to 2011, the ROCE ratio of Vinamilk

increased from 2009 to 2010. However it went down in 2011 and fall at 39.50%.

it means that Vinamilk should improve its operating in the future to recover the

ROCE and make it developed. To do that, Vinamilk should improve the top line

without a corresponding increase in capital employed, and try to maintain

operating profit but reduce the value of capital employed.

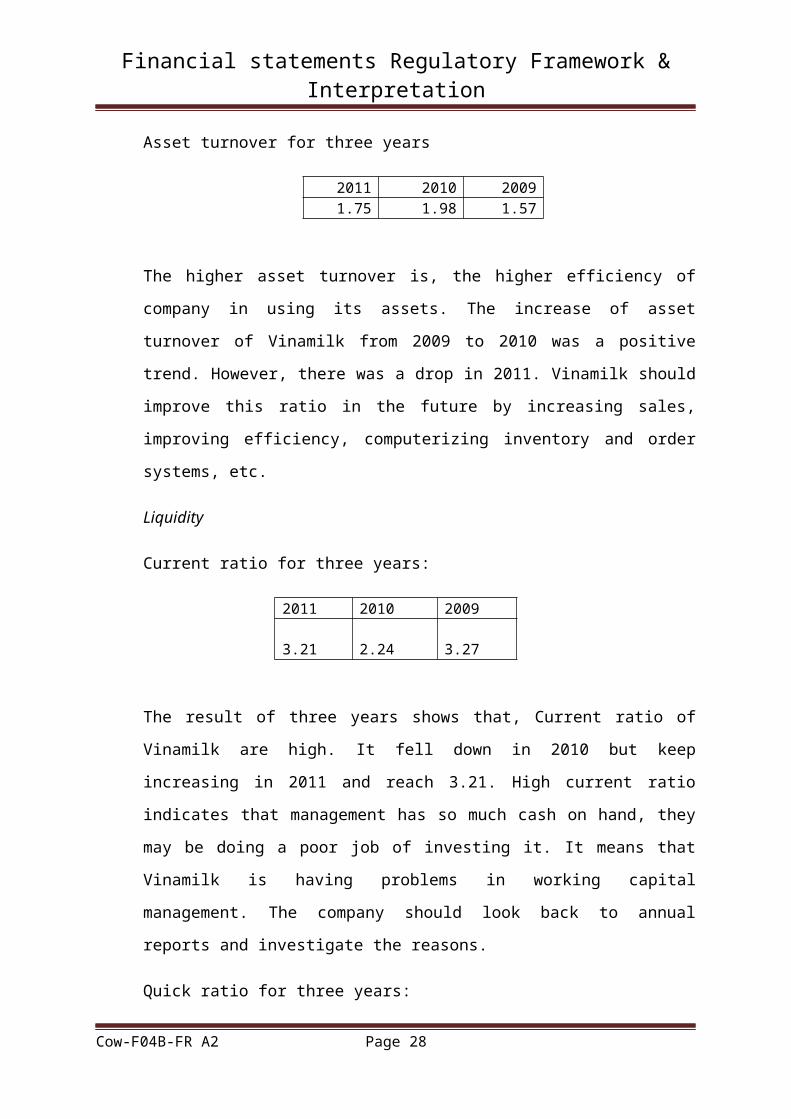

Asset turnover for three years

2011 2010 20091.75 1.98 1.57

The higher asset turnover is, the higher efficiency of company in using its assets.

The increase of asset turnover of Vinamilk from 2009 to 2010 was a positive

trend. However, there was a drop in 2011. Vinamilk should improve this ratio in

the future by increasing sales, improving efficiency, computerizing inventory and

order systems, etc.

Liquidity

Current ratio for three years:

2011 2010 2009 3.21

2.24

3.27

The result of three years shows that, Current ratio of Vinamilk are high. It fell

down in 2010 but keep increasing in 2011 and reach 3.21. High current ratio

indicates that management has so much cash on hand, they may be doing a poor

Cow-F04B-FR A2 Page 19

Financial statements Regulatory Framework & Interpretation

job of investing it. It means that Vinamilk is having problems in working capital

management. The company should look back to annual reports and investigate

the reasons.

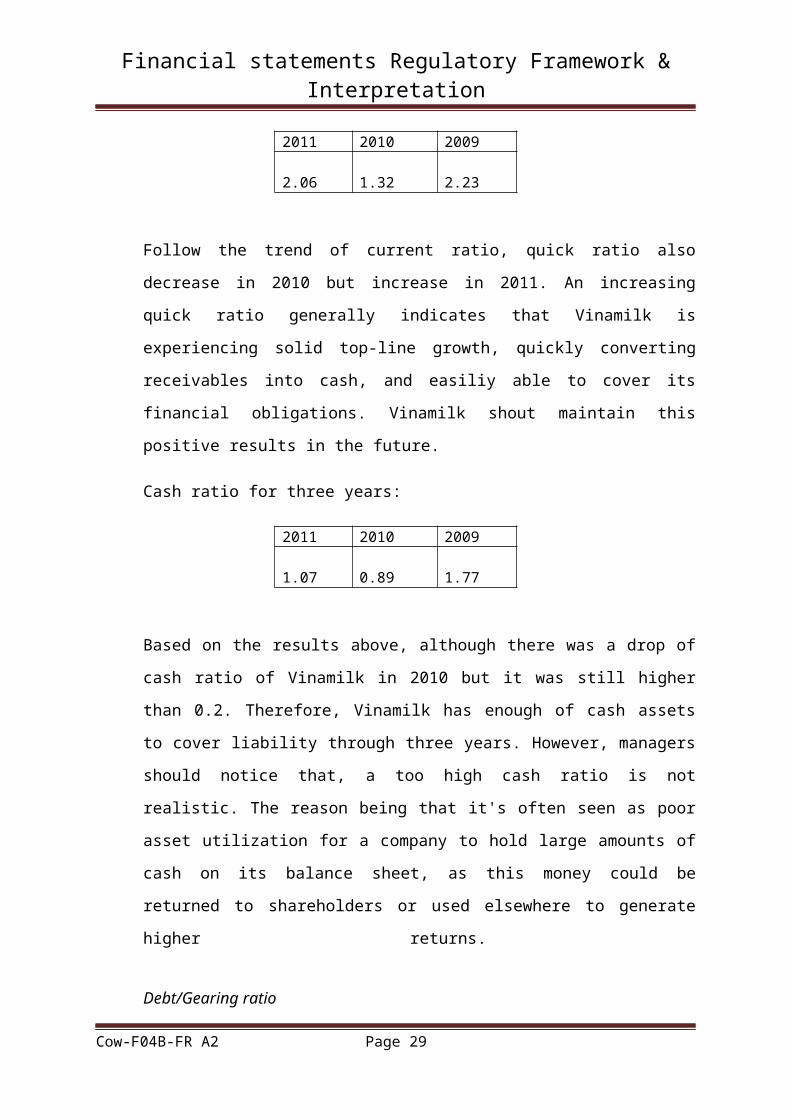

Quick ratio for three years:

2011 2010 2009 2.06

1.32

2.23

Follow the trend of current ratio, quick ratio also decrease in 2010 but increase

in 2011. An increasing quick ratio generally indicates that Vinamilk is

experiencing solid top-line growth, quickly converting receivables into cash, and

easiliy able to cover its financial obligations. Vinamilk shout maintain this

positive results in the future.

Cash ratio for three years:

2011 2010 2009 1.07

0.89

1.77

Based on the results above, although there was a drop of cash ratio of Vinamilk in

2010 but it was still higher than 0.2. Therefore, Vinamilk has enough of cash

assets to cover liability through three years. However, managers should notice

that, a too high cash ratio is not realistic. The reason being that it's often seen as

poor asset utilization for a company to hold large amounts of cash on its balance

sheet, as this money could be returned to shareholders or used elsewhere to

generate higher returns.

Debt/Gearing ratio

Debt ratio of three years:

2011 2010 200919.93% 26.07% 21.32%

Cow-F04B-FR A2 Page 20

Financial statements Regulatory Framework & Interpretation

There is an increase of debt ratio from 2009 to 2010, and then fall down to

19.93% in 2011. They are all under 50% meaning not much proportion of

Vinamilk’s assets is claimed by creditors. Vinamilk should maintain this result in

the future and avoid increasing because an increasing Debt Ratio is generally a

negative sign, showing the company may not have been able to secure long-term,

lower interest financing, instead having to secure short-term, higher interest

short term financing.

Gearing ratio of three years:

2011 2010 20091.26% 2.01% 3.71%

There was an increase of gearing ratio from 2009 to 2011. All of them were

under 25% it means that Vinamilk is considered as low-gearing company. It

means in Vinamilk, the largest proportion of the funding has come from

investment by shareholders. As low gearing will be a result of a low level of

borrowings, this can indicate that Vinamilk is growing through reinvestment of

profits, minimizing risk.

Interest cover of three years:

2011 2010 2009383.92 709.50 456.17

Though there was an decrease from 2010 to 2011, interest cover of Vinamilk in

general are very high. It means that Vinamilk is easily able to meet its interest

obligations from profits. This company should remain this positive results in the

future.

Efficiency

Inventory turnover of three years:

2011 2010 20094.60 4.50 5.14

Cow-F04B-FR A2 Page 21

Financial statements Regulatory Framework & Interpretation

There was a drop of Vinamilk’s inventory in 2010 but it was increased again in

2011 and reached 4.6 times. Those figures are considered quite high. It indicates

that Vinamilk has good performance in controlling inventory levels. It should

remain the increasing inventory turnover in the future

Inventory days of three years:

2011 2010 200979.41 81.11 71.05

Vinamilk’s days of inventory was increased in 2010 but fell down in 2011. In

general, the smaller the number of days, the more efficient the company is, as it is

holding inventory for less time and less money is tied up in inventory. However,

sometimes, An increasing number of days in inventory can be a good thing if

sales are rising and the company is building inventory to meet an anticipated

increase in demand.

Investment ratio

Earnings per share for three years

2011 2010 2009 7.717

10.244

6.769

There was an significant increase of Vinamilk’s earnings per share from 2009 to

2010. However, it was decreased in 2011. The higher EPS is, the better,

therefore, Vinamilk should try to increase its EPS in the future because a high

EPS indicates that the company is generating and increasing amount of earnings.

Price/Earning ratio for three years:

2011 2010 200911.53 5.59 7.39

There is no absolute guide to the maximum safe PE ratio. It tends to vary from

industry to industry. Therefore, it could not be sure whether PE ratio of Tran’s

Cow-F04B-FR A2 Page 22

Financial statements Regulatory Framework & Interpretation

company is high or low. The decrease of PE between 2009 and 2010 may reflect

slower expected earnings growth, or higher risk earnings.

Dividend yield ratio for three years:

2011 2010 20093% 7% 6%

There was a significant decrease in Vinamilk’s yield ratio in 2011. It might be a

negative sign for Vinamilk because investors do not want to get low from

dividend. High dividend yield maybe an indication of a stock’s current

attractiveness. Therefore, Vinamilk should try to increase the dividend yield ratio

in the future. Also, it should notice that investors may look for the stability of the

high dividend yield rather than its growth. They do not want to lose out in the

long term because of high dividends in the short term. Therefore, Vinamilk

should ensure that the high dividend yield is not just a temporary phenomenon

but sustainable.

Dividend cover ratio for three years:

2011 2010 2009 2.58

2.56

2.26

There was not much changes in Vinamilk’s dividend cover ratio from 2009 to 2011

but it has a trend to be increased. They are all higher than 1.5, meaning this company

is earning enough in profits to cover the dividend. Also, the increase of dividend

cover over three years indicates a good sign for Tran’s company because the

higher the cover, the better the ability to maintain dividends it profits drop, and

the more easily the company can meeting the obligation to pay dividends.

Vinamilk should maintain this trend in the future to ensure company’s good

operation and attract more investors.

Conclusion

According to the analysis above, speaking in general, Vinamilk has a stable

development and strong financial position. The profitability, liquidity, efficiency

Cow-F04B-FR A2 Page 23

Financial statements Regulatory Framework & Interpretation

and investment ratio generally have positive results and trend. To have better

performance in the future, Vinamilk should improve some considered ratios

which mentioned in the report.

Cow-F04B-FR A2 Page 24

Financial statements Regulatory Framework & Interpretation

CONCLUSION

Through this report, it can be seen that, firstly, different users of financial statements

and their needs were clarified. Come with that, the assessment of the implications for

users were also mentioned in this report. The next part is about the legal and regulatory

influences on financial statement was presented through the understanding of

Companies Act 1985, Partnership 1890, international European Directives,

International Accounting standard, and UK Accounting Standard.

The second main part is about interpretation of financial statement. Applying to

Vinamilk Corporation, important accounting ratios were calculated, analysed through

the report for Vinamilk’s Director of Finance, to evaluate the financial position of

Vinamilk

Cow-F04B-FR A2 Page 25

Financial statements Regulatory Framework & Interpretation

REFERENCES

Accouting-Simplified, n.d. Accouting-Simplified.com. [Online]

Available at: http://accounting-simplified.com/financial/users-of-accounting-

information.html

[Accessed 18 November 2012].

Anon., 2012. Darlingtons. [Online]

Available at: http://www.business-law.co.uk/blog/partnership-act-1890

[Accessed 7 January 2012].

Education, B. P., 2010. Management Accounting and Financial Reporting . In: London:

BPP learning media ltd, p. 279.

Europa, n.d. European Commission. [Online]

Available at: http://ec.europa.eu/eu_law/introduction/what_directive_en.htm

[Accessed 8 January 2013].

FRC, n.d. Financial Reporting Council. [Online]

Available at: http://www.frc.org.uk/About-the-FRC/FRC-structure/Former-FRC-

structure/Accounting-Standards-Board.aspx

[Accessed 8 January 2013].

ICAEW, n.d. Library & Information Service. [Online]

Available at: http://www.icaew.com/en/library/subject-gateways/accounting-

standards/knowledge-guide-to-uk-accounting-standards

[Accessed 8 January 2013].

Moneyterms, n.d. Money Terms Co.UK. [Online]

Available at: http://moneyterms.co.uk/ifrs/

[Accessed 8 January 2013].

Moneyterms, n.d. Money Terms CO.Uk. [Online]

Available at: http://moneyterms.co.uk/frc/

[Accessed 8 January 2013].

Cow-F04B-FR A2 Page 26

Financial statements Regulatory Framework & Interpretation

Reaich, N., 2012. Bized. [Online]

Available at: http://www.bized.co.uk/notes/2012/07/introduction-users-accounts

[Accessed 19 November 2012].

Cow-F04B-FR A2 Page 27

Financial statements Regulatory Framework & Interpretation

APPENDIX

Calculation of financial ratio for Vinamilk (2009-2011)

Vinamilk

(2011)

Vinamilk

(2010)

Vinamilk

(2009)

Profitability ratio

Gross profit margin 29.85% 32.17% 35.84%

Asset turnover 1.75 1.98 1.57

ROE 33.81% 45.40% 35.80%

ROCE 39.39% 52.38% 39.71%

Liquidity ratio

Current ratio 3.21 2.24 3.27

Quick ratio 2.06 1.32 2.23

Cash ratio 1.07 0.89 1.77

Debt/gearing ratio

Debt ratio 19.93% 26.07% 21.32%

Capital gearing ratio 1.26% 2.01% 3.71%

Interest cover 382.92 709.50 456.17

Efficiency ratio

Inventory turnover 4.60 4.50 5.14

Inventory days 79.41 81.11 71.05

Investment ratio

EPS 7.717 10.244 6.769

Price-earnings 11.53 5.59 7.39

Dividend yield 3% 7% 6%

Dividend cover 2.58 2.56 2.26

Cow-F04B-FR A2 Page 28

Financial statements Regulatory Framework & Interpretation

Cow-F04B-FR A2 Page 29

Financial statements Regulatory Framework & Interpretation

Figures taken from Annual Report of Vinamilk (2008-2010 and Hanoimilk (2011)

Vinamilk

(2011)

Vinamilk

(2010)

Vinamilk

(2009)

Sales 22070 16081 10820

COGS 15039 10579 6735

Gross profit 6588 5173 3878

Profit after tax 4218 3616 2376

Interest expense 13 6 6

PBIT 4978 4251 2731

Assets 15582 10773 8482

Current assets 9467 5919 5069

Inventory 3272 2351 1311

Cash + cash equivalent 3156 613 426

Short-term investment 736 1742 2314

Short-term receivables 2169 1124 728

Current liabilities 2946 2645 1552

.

Cow-F04B-FR A2 Page 30