Embed Size (px)

Citation preview

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of McKinsey & Company

is strictly prohibited

Last update 1 April, 2020

Overall and Kenya perspective

COVID-19: Africa Economic Impact -Kenya deep-dive

DOCUMENT INTENDED TO PROVIDE INSIGHT AND BEST

PRACTICES RATHER THAN SPECIFIC RECOMMENDATIONS

McKinsey & Company 2

COVID-19 is, first and foremost, a global humanitarian challenge.Thousands of health professionals are heroically battling the virus, putting their own lives at risk. Governments and industry are working together to understand and address the challenge, support victims and their families and communities, and search for treatments and a vaccine.

Government and businesses around the world need to act promptly. This document is meant to help senior leaders understand the COVID-19 situation and how it may unfold, and take steps to protect their employees, customers, supply chains and financial results.

Read more on Mckinsey.com

Current as of April 1, 2020

McKinsey & Company 3

Executive Summary

With >5,300 confirmed cases and >170 deaths as of 31 March 2020, the COVID-19 pandemic has disrupted millions of people’s livelihoods

across the continent, with a disproportionate impact on poor households and small and informal businesses. The pace of this disruption is

likely to accelerate in the weeks ahead. This document addresses three key questions about the economic impact of the pandemic in Africa:

What are likely economic scenarios that Africa will face due to the COVID-19 epidemic?

We modelled four scenarios anchored in the evolution of the global and domestic epidemiology situation. The most optimistic – the global

and Africa virus spread is contained, with an overall economic slowdown. The least optimistic – the global virus is resurgent, the Africa

virus outbreak is widespread, and the global economy faces a prolonged downturn

How will these scenarios impact Africa’s GDP growth in 2020?

Even in the most optimistic scenario – where Africa is able to contain the virus spread, GDP growth could fall from 3.9% to 0.4% in 2020

driven by spread of the virus within Africa i.e. disruptions to ways of working and therefore incomes and consumption (~50%), the global

impact of the virus i.e. supply chains and exports (~30%), and oil effects impacting expenditure across the board (~20%). If Africa fails to

contain the virus, GDP growth could fall up to 8pp to -3.9%, driven by prolonged reductions in domestic consumption, and non-oil exports

Of the five countries we modelled in detail -- Nigeria, South Africa, Morocco, Angola and Kenya – all but Kenya are likely to experience a

contraction in all four scenarios

What can government, development partners, and private sector actors to do today to limit the impact of these disruptions?

Africa faces a unique set of challenges that demand bold and tailored action to the crisis: fragile healthcare systems, limited fiscal

capacity, highly informal economies with many SMES, a young and fast urbanizing population with widespread poverty. African

governments may need to be both targeted and creative in their response to the crisis. They may also need close collaboration with the

private sector and development partners. We identify actions for each player in this document

Current as of April 1, 2020

Sources: McKinsey analysis, Africa’s Business Revolution by Acha Leke, Mutsa Chironga and Georges Desvaux; UN Population Prospects 2019; ILO;, State of Small Business Report South Africa 2018;;

World Bank WDI; MGI Power of Parity Africa 2019

McKinsey & Company 4

Contents

Current as of April 1, 2020

COVID-19

pandemic:

where we

are today?

01Economic

impact of the

crisis in Africa

02Impact on

Kenya’s

economy

03Potential

economic

mitigation

measures

04

McKinsey & Company 5

Current as of April 1, 2020

Sources: World Health Organization, CDC, news reports

~75%New reported cases in Europe as of April 1th

>37,000

Deaths

>50New countries with cases March 23rd-29th

<1%China’s share of new reported cases March 23rd-29th

>145

Countries or territories with evidence of local transmission2

~90

Countries or territories with more than 100 reported cases1

Countries or territories with reported cases1

>200

Reported confirmed cases

>770,000Impact to date

The global spread is accelerating with more reports of local transmissionLatest as of April 1, 2020

1. Previously counted only countries; now aligned with new WHO reports;

excluding cruise ship;

2. Previously noted as community transmission in McKinsey documents; now

aligned with WHO definition

McKinsey & Company 5

McKinsey & Company 6

COVID-19 appears to be more dangerous than the fluLatest as of March 18, 2020

Current as of April 1, 2020

1. Evidence on exact numbers are emerging, however expected to decrease as viral containment measures intensify and treatments are developed

2. WHO statement as 3.4% and latest calculated as deaths/ cases; dependent on conditions such as the patient's age, community immunity, and health system capabilities

3. In outbreak setting or the introduction of a new disease

4. Case Fatality numbers reflect outbreak settings and factors such as the patient's age, community immunity and health system capabilities

5. Estimates are very context and time specific, however are provided from prior outbreaks based on academic lit review

6. WHO estimates 15% severe and 5% critical

S. Korea case fatality rate after widespread

testing. CFR appears higher where cases

missed or health systems overwhelmed2

Features of the disease to date1

Higher reproduction than the flu

1.5-2x

~0.9%

Of cases have a severe/critical form of the

disease6

Up to 20%

Comparison to other diseases5

Early identification of the disease, intensification of viral control, and treatment, when available, will reduce

reproduction number and case fatality

Reproduction

number3 (average

number

of people infected

by each infected

person

in outbreak setting)

D

G

K

I

A

E

FJ

Zika

Chickenpox

SARS-CoV

COVID-19

Polio3

Measles3

Influenza 1918

Smallpox

MERS-CoV

Ebola (West

Africa 2014)

Influenza H1N1 2009

Influenza

H2N2 1957B

C

H

Medium (2-15%) High (>15%)Low (<2%)

Mediu

m (

2-4

)H

igh (

>4)

Low

(2

-4)

Case Fatality1 (proportion of deaths among confirmed cases)

Sources: World Health Organization, CDC, Nature, The Lancet, PLOS One The Journal of Infectious Diseases, BMC Infectious Diseases, Infectious Disease Modelling, news reports

McKinsey & Company 7

~5,300 confirmed COVID-19 cases in Africa…

Current as of April 1, 2020

At April 1, 9.00a GMT, >5,300 confirmed COVID-19 cases, >170 deaths across 47 African countries1

McKinsey & Company 7

Day

…but the pandemic is progressing at a slower rate than Europe

COVID-10: first 46 days for Africa and Europe1

Comparison of the total number of COVID-19 cases

reported over the first 46 days since first case reported in

each region

To

tal

CO

VID

-19 c

ases (

000s)

Note: The numbers in Africa may be lower due to limited testing in the continent compared to Europe

556

1326

131

656582

50

162 246

142

83

362

19152

23

9

6

70

3

63

7

19

3

128

10

114

8

6

46

7

26

33

11

8

34

168

15

14

Isolated cases

Small cluster

Communitytransmission

5

0

10

15

20

2521205 240 4310 4115 22 23 373127 29 30 32 33 34 35 36 38 39 40 42 44 45 462826

Africa Europe

Current as of April 1, 2020

Sources: WHO situation reports, JHU global dashboard, press search; https://www.who.int/emergencies/diseases/novel-coronavirus-2019/situation-reports

1. We defined <20 cases as isolated, 20-100 cases as small clusters, and >100 as community transmission. Small clusters can include cases that are locally transmitted as well as imported

McKinsey & Company 8

Contents

Current as of April 1, 2020

COVID-19

pandemic:

where we

are today?

01Economic

impact of the

crisis in

Africa

02 03 04Impact on

Kenya’s

economy

Potential

economic

mitigation

measures

McKinsey & Company 9

Four scenarios defined for Africa, considering both the health and economic situations

Current as of April 1, 2020

Sources: McKinsey analysis

2 Global resurgent virus, and prolonged downturnUS and Europe require significant quarantine measures through

much of the year; Asia faces a resurgence of infection leading to a

double dip slowdown

Africa outbreak contained

Most countries experience isolated cases or small cluster

outbreaks, but with carefully managed restrictions, there is no

widespread outbreak, and most economic impacts are driven

through global knock-on effects on trade, and travel

1 Global virus contained, and economic slowdownContinued recovery in Asia; Europe and US face a sharp downturn

but are able to control the epidemic and release most quarantine

measures by early Q3

Africa outbreak contained

Most countries experience isolated cases or small cluster

outbreaks, but with carefully managed restrictions, there is no

widespread outbreak, and most economic impacts are driven

through global knock-on effects on trade, and travel

4 Global resurgent virus, and prolonged downturnUS and Europe require significant quarantine measures through

much of the year; Asia faces a resurgence of infection leading to a

double dip slowdown”

Africa outbreak widespread

Significant outbreaks occur in most major African economies,

leading to a significant economic downturn though reduced

consumption, and global knock-on effects on trade and travel

Contained Widespread

Africa transmission

Glo

bal

tran

sm

issio

n

Co

nta

ine

dR

es

urg

en

tGlobal situation Domestic situation

3 Global virus contained, and economic slowdownContinued recovery in Asia; Europe and US face a sharp downturn

but are able to control the epidemic and release most quarantine

measures by early Q3

Africa outbreak widespread

Significant outbreaks occur in most major African economies,

leading to a significant economic downturn though reduced

consumption, and global knock-on effects on trade and travel

McKinsey & Company 10

Three major challenges face African countries around the COVID-19 crisis in the coming months

Current as of April 1, 2020

Implication

Global

COVID-19

pandemic

Africa

COVID-19

pandemic

Pressure on interest rates and currency devaluation

Rising deficits and increase pressure on debt markets

Limited access to hard currency

Reduced tax revenues

Oil impact

Economic

Fiscal

Monetary

Reduced household expenditure and consumption

Businesses – many of them SMEs -- under significant cost

pressure, potential of closure and bankruptcies

Lower productivity, job losses particularly for non-

essential sectors.

Slow down in overall economic growth, acute in hard-hit

sectors (e.g., tourism), potential for recession

Long term human capital issues (e.g., delayed schooling

or dropouts)

ImpactChallenge

F

D Limited movement of people due to

travel bans (domestic, international,

diaspora)

E Disruption to ways of working for

individuals, businesses and governments

Reduction in government and

business revenues for oil exporters,

but lower costs for oil importers and

consumers

C Delayed / reduced FDI as partners re-

direct capital locally

B Lower demand in global markets for

non-oil goods exports

Disruption in global supply chains

exposed to inputs from Asia, Europe and

the Middle East

A

In model, will continue to refine

Sources: McKinsey analysis

Not yet in model

Disclaimer: Current modelling as of 3/29/20 assumes no fiscal stimulus packages

from governments, or monetary impacts of currency and credit ratings (fix 2018 prices).

The next model iteration will be more sensitive to these elements, and shared accordingly

McKinsey & Company 11

Africa’s GDP growth could decline by between 3pp and 8pp depending on the scenarioRecall: Baseline GDP growth for 2020: 3.9% growth1

Current as of April 1, 2020

Africa transmission

Glo

ba

l tr

an

sm

iss

ion

Global situation Africa Transmission

2 Global resurgent virus, and prolonged downturn

Africa outbreak contained

1 Global virus contained, and economic slowdown

Africa outbreak contained

3.90

2020 GDP Growth Projection

0.40

~3pp

Pre-COVID19 GDP growth Scenario modelled GDP growth

2020 GDP Growth Projection

-1.40

3.90 ~5pp

2020 GDP Growth Projection

-3.90

3.90 ~8pp

Source: McKinsey analysis, AfDB African Statistical Yearbook

1. AfDB estimate, other analyst estimates range between 3.2% (e.g., UNECA) to 3.8% (e.g., Oxford Economics Research)

4 Global resurgent virus, and prolonged downturn

Africa outbreak widespread

3 Global virus contained, and economic slowdown

Africa outbreak widespread

-2.10

2020 GDP Growth Projection

3.90 ~6pp

The economic loss across

scenarios range from

between ~3-8pp of GDP

In three out of the four

scenarios looked at, Africa

as a whole could be forced

into a contraction

Across scenarios, Africa

COVID-19 effects (i.e. way

of working and limited

travel) is the most

significant lever,

accounting for between

~35-50% of total GDP loss.

Globally driven disruptions

(i.e. supply chain, non-oil

exports, and FDI) account

for about one third of total

disruptions, and the oil

effect accounts for the

remainder (20-30%)

Key insights

Contained Widespread

Co

nta

ine

dR

es

urg

en

t

Disclaimer: Current modelling as of 3/29/20 assumes no fiscal stimulus packages

from governments, or monetary impacts of currency and credit ratings (fix 2018

prices). The next model iteration will be more sensitive to these elements

McKinsey & Company 12

Contents

Current as of April 1, 2020

COVID-19

pandemic:

where we

are today?

01Impact on

Kenya’s

economy

03 04Economic

impact of the

crisis in Africa

02Potential

economic

mitigation

measures

McKinsey & Company 13

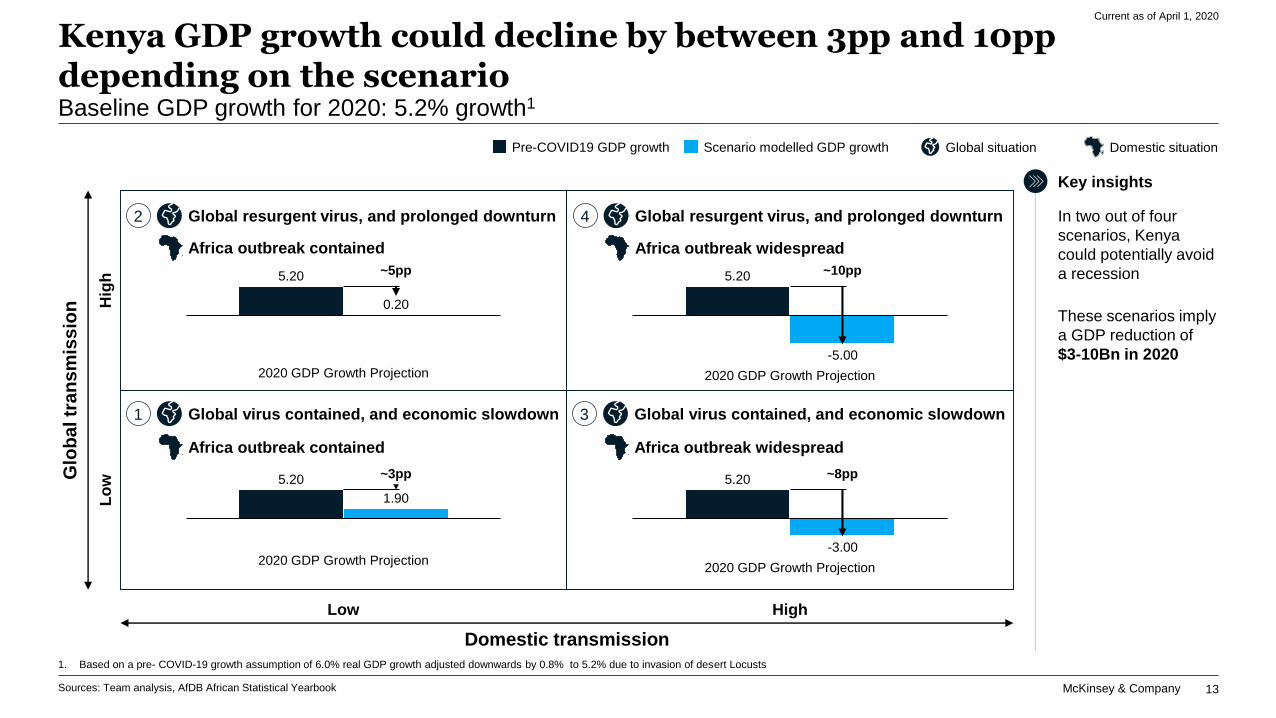

Kenya GDP growth could decline by between 3pp and 10pp depending on the scenarioBaseline GDP growth for 2020: 5.2% growth1

Current as of April 1, 2020

Low High

Domestic transmission

Glo

ba

l tr

an

sm

iss

ion

Lo

wH

igh

Global situation Domestic situation

2 Global resurgent virus, and prolonged downturn

Africa outbreak contained

1 Global virus contained, and economic slowdown

Africa outbreak contained

2020 GDP Growth Projection

1.90

5.20 ~3pp

Pre-COVID19 GDP growth Scenario modelled GDP growth

2020 GDP Growth Projection

0.20

5.20 ~5pp

2020 GDP Growth Projection

5.20

-5.00

~10pp

Sources: Team analysis, AfDB African Statistical Yearbook

1. Based on a pre- COVID-19 growth assumption of 6.0% real GDP growth adjusted downwards by 0.8% to 5.2% due to invasion of desert Locusts

4 Global resurgent virus, and prolonged downturn

Africa outbreak widespread

3 Global virus contained, and economic slowdown

Africa outbreak widespread

2020 GDP Growth Projection

5.20

-3.00

~8pp

In two out of four

scenarios, Kenya

could potentially avoid

a recession

These scenarios imply

a GDP reduction of

$3-10Bn in 2020

Key insights

McKinsey & Company 14

Impact on Kenya GDP growth driven by reduction in household consumption and supply chain disruptionsBaseline GDP for 2020: USD 98bn1

Current as of April 1, 2020

1. Based on a pre- COVID-19 growth assumption of 6.0% real GDP growth adjusted downwards by 0.8% to 5.2% due to the ongoing invasion of desert Locusts

2. Accounts for reduced household, private and government expenditure

3. Accounts for consumption disrupted by restricted movement and international travel restrictions

4. Assumes average 2020 price of $35/bbl in 2020 for Scenario 1 & 2, and average $25/bbl in 2020 for Scenario 3 & 4

Source: KNBS; AfDB; IMF

Impact on GDP growth in 2020 across scenarios, %New GDP

growth (%)

Delta

$bn

2.3-8.0

6.0

Pre-COVID growth Expected 2020

growth rate

Tourism

(limited travel)3

0.8

Adjustment for

locust invasion1

5.2

Disruption to

household &

business spend2

1.9 – (5.0)

1.3-2.4

Supply chain

disruption

0.9-1.41.2-1.5

Oil dynamics4 Projected GDP

6.0

5.2

1.9-(5.0)(3.2) - (10.0)

We use AFDB GDP 2019 growth rate of

6.0% while Kenya Monetary Policy

Committee (MPC) uses 6.2%

McKinsey & Company 15

Manufacturing and tourism affiliated sectors to be hugely impacted by the outbreak

Current as of April 1, 2020

Sector Percentage point change in sector contribution at 2020F GDP of $98Bn1

Education, Healthcare, and Defence

Manufacturing

Construction & Real Estate

Wholesale & Retail

Hotel and restaurant

Transport and storage

ICT

Financial services

Business services

Agriculture

Mining

Utilities

Arts, entertainment, recreation, others

-2pp

-4pp

+0pp

-7pp

-1pp

-2pp

-15pp

-30pp

-15pp

+15pp

-3pp

-2pp

-7pp

1. Based on a pre- COVID-19 growth assumption of 6.0% real GDP growth adjusted downwards by 0.8% to 5.2% due to invasion of desert Locusts | 2/Percentage of sector contribution to 2020F GDP.

Percentage point

change (best case)

34%

1%

9%

8%

2%

5%

7%

1%

8%

1%

6%

9%

8%

% Baseline

2020F GDP2

Decline heavily driven by

decreasing consumption

and supply chain disruption

Tourism expected to

decline by between 60-90%

depending on the scenario

-6pp

-6pp

+1pp

-15pp

-3pp

-3pp

-60pp

-60pp

-35pp

+40pp

-8pp

-5pp

-10pp

Percentage point

change (worst case)

McKinsey & Company 16

Kenya: Methodology and key assumptions

Current as of April 1, 2020

1. Methodology to arrive at financial impact. For all, financial impact is then multiplied by GDP multiplier to calculate GDP impact

2. Day-to-day impact of travel bans, including reduced domestic transport, and reduced consumption of goods and services, captured in disruption to way of working lever

3. The most direct implication to disruption in ways of working will be a reduction in disposable income at a macro-level as described. Given large share of informal sector workers, these impacts are difficult to size. We therefore used reduction in household spend as a proxy for

the impact of disruption to ways of working, and will avoid double counting on this lever

4. Includes both raw material food purchases, and purchases from retail outlets, largely driven by urban to rural migration patterns

5. Includes clothing, and personal care expenditure

Lever

F Oil impact Oil intensity (boe per GDP) x

GDP x savings per barrel

Oil price: $35/bbl average over 2020

Energy intensity: 0.5bbl/1000USD GDP

Oil price: $35/bbl average over 2020

Energy intensity: 0.5bbl/1000USD GDP

Oil price: $35/bbl average over 2020

Energy intensity: 0.5bbl/1000USD GDP

D Limited travel2 Travel & Tourism revenues x

disruption factor based on

origin of travelers

Domestic: 2 month disruption of 90%, 25%

lower for rest of year

International: 4 month disruption of 90%,

followed by 60% lower for remainder of year

Domestic: 4 month disruption of 90%, 25%

lower for rest of year

International: 4 month disruption of 90%,

followed and 60% lower for remainder of year

All: 4 month disruption of 90%, 60% lower for

rest of year

All: 4 month disruption of 90%, 75% lower for

rest of year

Disruption to

ways of working

(with direct

passthrough to

spend)3

E Household expenditures x

disruption factor (on a

category level)

F&B4: 2 month disruption of 15%6

Transport: 2 month disruption of 50%

Education: 2 month disruption of 25%

Retail5: 2 month disruption of 20%

Health and ICT: 2 month increase of 50%

F&B4: 2 month disruption of 15%6

Transport: 2 month disruption of 50%

Education: 2 month disruption of 25%

Retail5: 2 month disruption of 20%

Health and ICT: 2 month increase of 50%

F&B4: 6 month disruption of 15%

Transport: 6 month disruption of 50%

Education: 6 month disruption of 25%

Retail5: 6 month disruption of 20%

Health and ICT: 6 month increase of 50%

F&B4: 6 month disruption of 20%

Transport: 6 month disruption of 50%

Education: 6 month disruption of 25%

Retail5: 6 month disruption of 30%

Health and ICT: 6 month increase of 50%

Business expenditures x

disruption factor

(on a sector level)

Govt. spend on business x

disruption factor

(on a sector level)

Capital investment: 4% lower domestic

investment for 2020

Govt spending on business: 10% lower for 6

months

Capital investment: 8% lower domestic

investment for 2020

Govt spending on business: 10% lower for 6

months

Capital investment: 8% lower domestic

investment for 2020

Govt spending on business: 20% lower for 9

months

Capital investment: 8% lower domestic

investment for 2020

Govt spending on business: 20% lower for 9

months

Methodology1

A Supply chain import

disruption

Base case import assumptions

x disruption factor (on a

product, and trade partner

granularity

China: 1 month disruption of 50%, followed by 2

month disruption of 25%

RoW: 1 month disruption of 50%, followed by 2

month disruption of 25%

China: 1 month disruption of 50%, followed by 2

month disruption of 25%

RoW: 2 month disruption of 50%, followed by 2

month disruption of 25%

All: Extra 2 month disruption of 25% for a region

that accounts for 25% of all imports (second

outbreak)

China: 1 month disruption of 50%, followed by 2

month disruption of 25%

RoW: 1 month disruption of 50%, followed by 2

month disruption of 25%

All: 2 month disruption of 25% for internal lag

China: 1 month disruption of 50%, followed by 2

month disruption of 25%

RoW: 2 month disruption of 50%, followed by 2

month disruption of 25%

All: Extra 2 month disruption of 25% for a region

that accounts for 25% of all imports (second

outbreak)

B Non-oil goods

exportsBase case export assumptions

x disruption factor on a

product, and trade partner

granularity

Flowers: 90% disruption in flowers for 2 months,

followed by 50% disruption of another 2 months

Other agriculture: 25% disruption for 2 months

Other goods: 25-50% disruption for 2 months,

10-25% disruption for 2 months

Flowers: 90% disruption in flowers for 4

months, followed by 50% disruption of another 2

months

Other agriculture: 25% disruption for 4 months,

10% disruption for 2 months

Other goods: 25-50% disruption for 4 months,

25% disruption for 2 months

Flowers: 90% disruption in flowers for 4

months, followed by 25% disruption of another 2

months

Other agriculture: 25% disruption for 4 months

Other goods: 25-50% disruption for 4 months,

10-25% disruption for 2 months

Flowers: 90% disruption in flowers for 4 months,

followed by 50% disruption of another 2 months

Other agriculture: 25% disruption for 4 months,

10% disruption for 2 months

Other goods: 25-50% disruption for 4 months,

25% disruption for 2 months

C Foreign investment FDI inflow: FDI x disruption

factor and duration

Adjustment: 10% lower FDI flows for 2020 Adjustment: 30% lower FDI flows for 2020 Adjustment: 20% lower FDI flows for 2020 Adjustment: 30% lower FDI flows for 2020

Oil price: $25/bbl average over 2020

Energy intensity: 0.5bbl/1000USD GDP

Global economic slowdown

Africa outbreak contained1 2

Global prolonged downturn:

Africa outbreak contained3

Global economic slowdown

Africa outbreak widepsread 4Global prolonged downturn:

Africa outbreak widespread

McKinsey & Company 17

Contents

Current as of April 1, 2020

COVID-19

pandemic:

where we

are today?

01Potential

economic

mitigation

measures

04Economic

impact of the

virus in Africa

02Impact on

Kenya’s

economy

03

McKinsey & Company 18

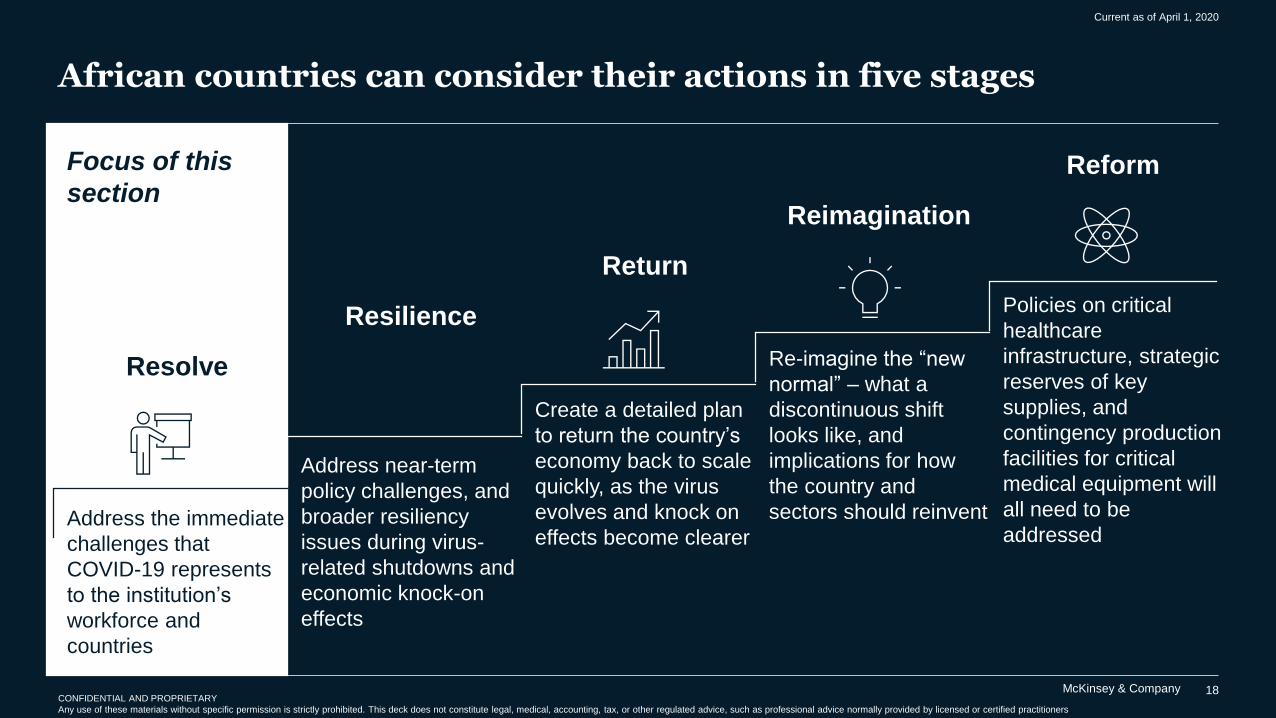

Create a detailed plan

to return the country’s

economy back to scale

quickly, as the virus

evolves and knock on

effects become clearer

Policies on critical

healthcare

infrastructure, strategic

reserves of key

supplies, and

contingency production

facilities for critical

medical equipment will

all need to be

addressed

African countries can consider their actions in five stages

Reform

CONFIDENTIAL AND PROPRIETARY

Any use of these materials without specific permission is strictly prohibited. This deck does not constitute legal, medical, accounting, tax, or other regulated advice, such as professional advice normally provided by licensed or certified practitioners

Address the immediate

challenges that

COVID-19 represents

to the institution’s

workforce and

countries

Address near-term

policy challenges, and

broader resiliency

issues during virus-

related shutdowns and

economic knock-on

effects

Re-imagine the “new

normal” – what a

discontinuous shift

looks like, and

implications for how

the country and

sectors should reinvent

Resolve

Resilience

Return

Reimagination

Focus of this

section

Current as of April 1, 2020

McKinsey & Company 19

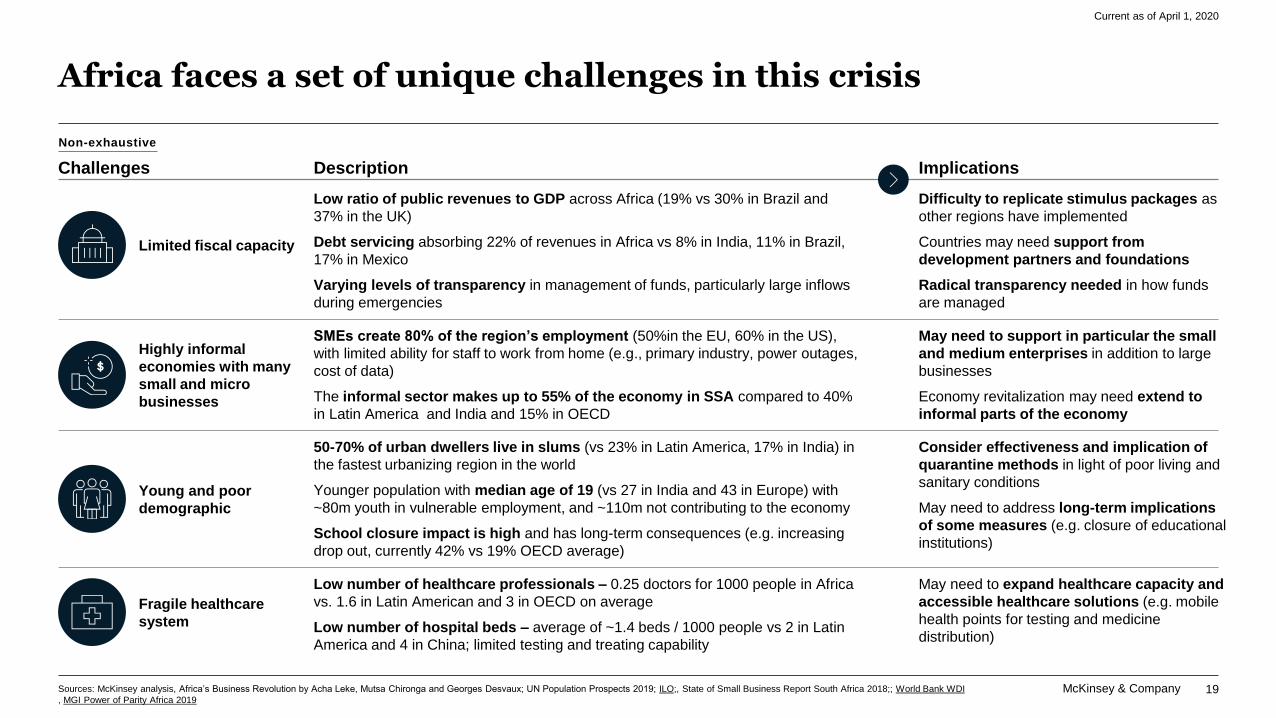

Africa faces a set of unique challenges in this crisis

Current as of April 1, 2020

Challenges Description Implications

Sources: McKinsey analysis, Africa’s Business Revolution by Acha Leke, Mutsa Chironga and Georges Desvaux; UN Population Prospects 2019; ILO;, State of Small Business Report South Africa 2018;; World Bank WDI

, MGI Power of Parity Africa 2019

Non-exhaustive

Fragile healthcare

system

Limited fiscal capacity

Low ratio of public revenues to GDP across Africa (19% vs 30% in Brazil and

37% in the UK)

Debt servicing absorbing 22% of revenues in Africa vs 8% in India, 11% in Brazil,

17% in Mexico

Varying levels of transparency in management of funds, particularly large inflows

during emergencies

Difficulty to replicate stimulus packages as

other regions have implemented

Countries may need support from

development partners and foundations

Radical transparency needed in how funds

are managed

Highly informal

economies with many

small and micro

businesses

SMEs create 80% of the region’s employment (50%in the EU, 60% in the US),

with limited ability for staff to work from home (e.g., primary industry, power outages,

cost of data)

The informal sector makes up to 55% of the economy in SSA compared to 40%

in Latin America and India and 15% in OECD

May need to support in particular the small

and medium enterprises in addition to large

businesses

Economy revitalization may need extend to

informal parts of the economy

Young and poor

demographic

50-70% of urban dwellers live in slums (vs 23% in Latin America, 17% in India) in

the fastest urbanizing region in the world

Younger population with median age of 19 (vs 27 in India and 43 in Europe) with

~80m youth in vulnerable employment, and ~110m not contributing to the economy

School closure impact is high and has long-term consequences (e.g. increasing

drop out, currently 42% vs 19% OECD average)

Consider effectiveness and implication of

quarantine methods in light of poor living and

sanitary conditions

May need to address long-term implications

of some measures (e.g. closure of educational

institutions)

Low number of healthcare professionals – 0.25 doctors for 1000 people in Africa

vs. 1.6 in Latin American and 3 in OECD on average

Low number of hospital beds – average of ~1.4 beds / 1000 people vs 2 in Latin

America and 4 in China; limited testing and treating capability

May need to expand healthcare capacity and

accessible healthcare solutions (e.g. mobile

health points for testing and medicine

distribution)

McKinsey & Company 20

Four sets of stakeholders could work together to addressthe crisis in Africa

Development PartnersMultilateral institutions

Bilateral institution and country partners

Foundations

Private Sector

Businesses

Private Sector Associations

Public SectorGovernments

African Union

Regional Economic Bodies

CitizensIndividuals

Civil SocietyCitizens

Public Sector

Private

Sector

Development

Partners

Combatting the

Covid-19 Crisis

in Africa

Current as of April 1, 2020

McKinsey & Company 21

Governments may need to focus urgently on five key areas

Contain the epidemic Prepare the health ecosystem

Protect jobs Support most vulnerable populations

Digital tracking

and monitoring

Proactive

communication

Anticipate

and manage

the health

crisis

Secure food

supply chain

and essential

services

Ensure

support for

vulnerable

populations

Anticipate

and manage

the impact

on the

economy

Drugs and medical

equipment (testing

kits, masks,

ventilators, etc.)

Infrastructure

(hospitals, beds,

etc.)

Health

professionals

Diagnostic,

Testing, and

isolating

patients

Preventive

measures (e.g.,

restrictions,

lockdowns)

Secure the food supply Maintain the access to essential services

Setup and

operationalisation

Measures to

protect jobs

TelecomsHealth &

EducationUtilities Others

Tracking

and

monitoring

Appropriate

pricing of

priority products

Supply of

priority

products

Economy Short term stimulus Prepare for recovery

Setup

National

Nerve Center

Scenario

analysis

Impact on

economy and

pubic finance

Measures to

help firms

survive the

crisis

Anticipation of the post crisis and

preparation of the ‘next normal’

Retrain existing

workforce for

current crisis

needs

Social safety net

mechanisms and

distribution

Others

Measures to

maintain

financial

stability

A

x Detail follows

B

C

D

E

Current as of April 1, 2020

McKinsey & Company 22

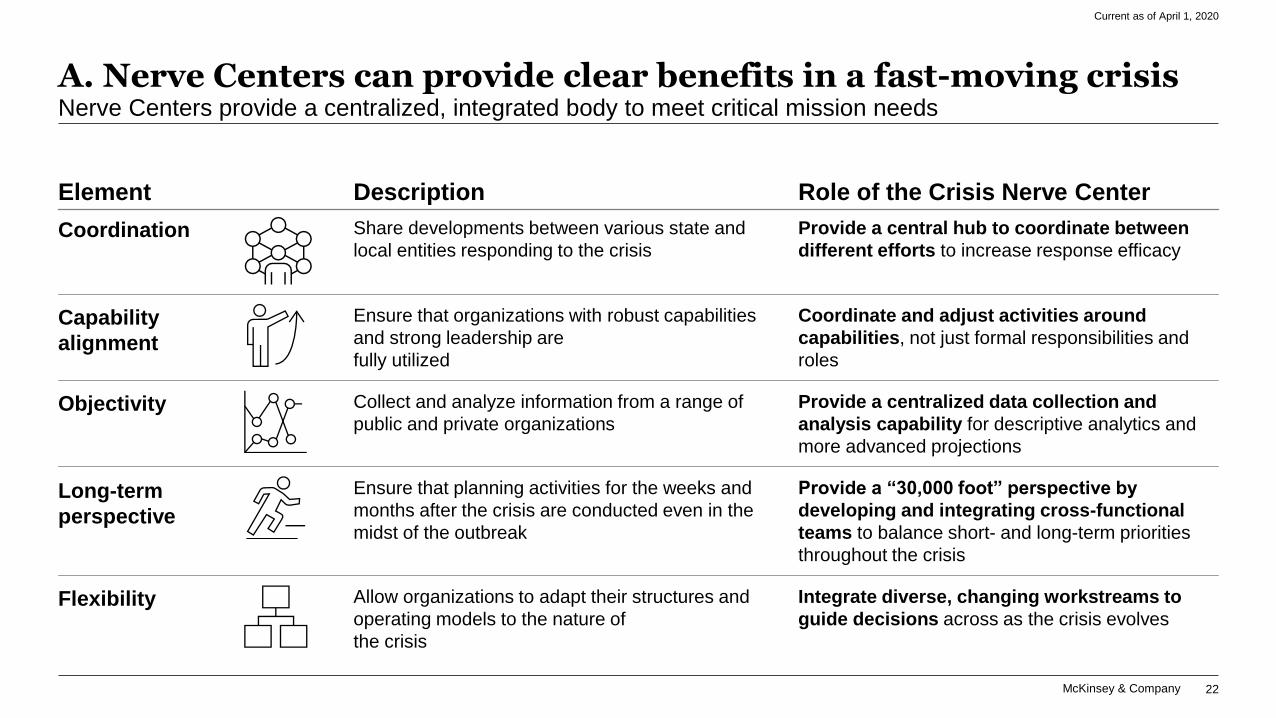

Description Role of the Crisis Nerve CenterElement

Coordination

Capability

alignment

A. Nerve Centers can provide clear benefits in a fast-moving crisisNerve Centers provide a centralized, integrated body to meet critical mission needs

Objectivity

Long-term

perspective

Flexibility

Share developments between various state and

local entities responding to the crisis

Provide a central hub to coordinate between

different efforts to increase response efficacy

Coordinate and adjust activities around

capabilities, not just formal responsibilities and

roles

Provide a centralized data collection and

analysis capability for descriptive analytics and

more advanced projections

Provide a “30,000 foot” perspective by

developing and integrating cross-functional

teams to balance short- and long-term priorities

throughout the crisis

Integrate diverse, changing workstreams to

guide decisions across as the crisis evolves

Allow organizations to adapt their structures and

operating models to the nature of

the crisis

Ensure that planning activities for the weeks and

months after the crisis are conducted even in the

midst of the outbreak

Collect and analyze information from a range of

public and private organizations

Ensure that organizations with robust capabilities

and strong leadership are

fully utilized

Current as of April 1, 2020

McKinsey & Company 23

A. Nerve Centre with a public-private partnership can focus on optimizing supply chain, analytics capabilities, and raising funding

Private sector Public sector

High relevance Moderate relevance

Offer social interventions to businesses (e.g., tax relief)

Test potential COVID-19 cases and track spread of the disease

Create policies to reduce the impact of the disease (e.g., work-from-home policies)

Ensure businesses have basic hygiene equipment and follow best practices

Raise required capital for additional materials, equipment, hazard pay, etc.

Acquire, procure, and manage inventory for critical supplies

Increase capacity of facilities and beds to cater for surges

Ensure sufficient supply of medical professionals

Train employees on proper protocols and procedures for handling potential cases

Boost data and analytics capabilities to manage inventory and optimize supply-chain

Implement operating model to ensure coordinated actions and responses

Implement economic stimulus plan to reduce the impact of COVID-19 in key industries

Sources: McKinsey McKinsey analysis

1

2

3

4

5

6

7

8

9

10

11

12

EARLY PERSPECTIVE

RELEVANT TO DEVELOPING COUNTRY CONTEXT

Current as of April 1, 2020

McKinsey & Company 24

B. There are a number of healthcare interventions Governments can consider to effectively respond to the COVID-19 outbreak

Sources: McKinsey McKinsey analysis

Interventions

Prevent the virus

from becoming

widespread

1. Test potential COVID-19 cases and conduct contact tracing

2. Create policies to reduce the impact of the disease (e.g., work-from-home policies)

3. Ensure businesses have basic hygiene equipment and follow best practices

Description

Control the virus 4. Raise required capital for additional materials, equipment, hazard pay, etc.

5. Acquire, procure, and manage inventory for critical supplies (e.g., ventilators, requirements for

isolation rooms, face masks, etc.).

6. Increase capacity of facilities and beds to cater for surges

7. Ensure sufficient supply of medical professionals

8. Train medical professionals on proper protocols and procedures for handling potential cases

9. Boost data and analytics capabilities to manage inventory and optimize supply-chain

10. Clarify key new responsibilities and operating model for top teams in context of potential epidemic

Current as of April 1, 2020

McKinsey & Company

Working Draft - Current as of April 1, 2020 - 1900 GMT

25

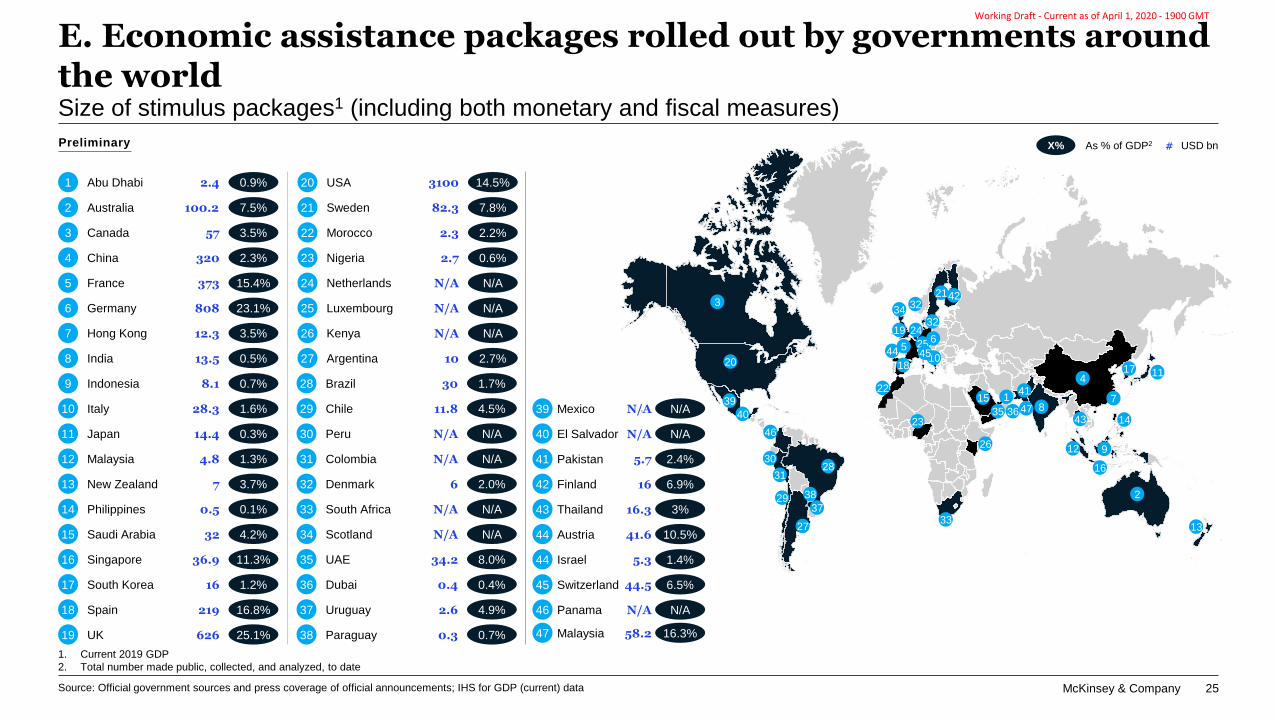

E. Economic assistance packages rolled out by governments around the worldSize of stimulus packages1 (including both monetary and fiscal measures)

1. Current 2019 GDP

2. Total number made public, collected, and analyzed, to date

# USD bnX% As % of GDP2

Source: Official government sources and press coverage of official announcements; IHS for GDP (current) data

India 13.5 0.5%8

Indonesia 8.1 0.7%9

Italy 28.3 1.6%10

Japan 14.4 0.3%11

Malaysia 4.8 1.3%12

New Zealand 7 3.7%13

Philippines 0.5 0.1%14

Saudi Arabia 4.2%15

Singapore 36.9 11.3%16

Australia 100.2 7.5%2

Abu Dhabi 2.4 0.9%1

Canada 57 3.5%3

China 320 2.3%4

15.4%France5

Germany6

Hong Kong 12.3 3.5%7

South Korea 1617 1.2%

808

373

23.1%

Preliminary

USA20

Sweden 82.321 7.8%

Morocco 2.322 2.2%

Nigeria 2.723 0.6%

Netherlands N/A24 N/A

Luxembourg N/A N/A25

Kenya N/A N/A26

Argentina 10 2.7%27

Brazil 30 1.7%28

Chile 11.8 4.5%29

Colombia N/A N/A31

Peru N/A30 N/A

Denmark 6 2.0%32

South Africa N/A N/A33

UAE 34.2 8.0%35

Scotland N/A34 N/A

3100 14.5%

Dubai 0.4 0.4%36

18 17

13

15

5 25

10

12 9

1

16

2

8

3

14

11

6

20

4

19

23

26

21

22

24

27

28

29

30

31

32

7

35

33

3432

36

37

38

39

40

41

42

43

45

46

44

N/A N/AMexico39

N/A N/AEl Salvador40

5.7 2.4%Pakistan41

16 6.9%Finland42

16.3 3%Thailand43

41.6 10.5%Austria44

5.3 1.4%Israel44

Spain 21918 16.8%

19 UK 626 25.1%

32

Uruguay 2.637 4.9%

38 Paraguay 0.3 0.7%

44.5 6.5%Switzerland45

N/A N/A46 Panama

58.2 16.3%47 Malaysia

47

McKinsey & Company

Working Draft - Current as of April 1, 2020 - 1900 GMT

26

1,000,000

100,000

10,000

E. Size of stimulus measures announced, with increasing numbers of global COVID-19 cases

Cumulative size of stimulus response2 (as % of GDP)

1. Total number made public, collected, and analyzed, to date; only covers countries with more than one package release

2. Countries are repeated in cases where stimulus packages or measures have been announced on different dates; size of stimulus response is the aggregate

amount spent at that point in time

3. Number of cases recorded on the day of the stimulus announcement

0

16

6

15

11

Feb 16

9

14

Feb 09

2

Mar 15 Mar 29Feb 23

12

3

1

Mar 08 Mar 22

10

4

17

13

8

5

7

Austria

UAE

Saudi Arabia

Sweden

Canada

Australia

UK

Japan

Denmark

UK

Saudi

Arabia

Japan

Switzerland

Malaysia

Australia

Hong Kong

UAE

UK Hong Kong

SwedenUSA

Austria

Thailand

USA

USA

Hong KongSingapore

Australia

Singapore

Italy

UK

USA

Canada

Malaysia

India

Thailand

Switzerland

India

Source: WHO Covid-19 Dashboard, IHS Data for GDP, Official government sources and press coverage of official announcements

Total stimulus size at time of first announcement Total stimulus size at time of second announcement

Total stimulus size at time of third announcement Total stimulus size at time of fourth announcement

Preliminary

Cu

mu

lativ

e n

um

ber o

f CO

VID

-19

ca

se

s, g

lob

ally

(#)

Size of stimulus response1 vs. number of global COVID-19 cases

Global number of COVID cases

McKinsey & Company 27

Private sector companies may need to consider shifting their operating model/ governance structure to a crisis response mode …

Current as of April 1, 2020

A shift from business as usual … … to remote agile model

2-3 months A few days to 2 weeks

Goes to business Goes to legal Goes to operations

Experience from other markets suggests that businesses across key markets outside of South Africa

may have 2-4 weeks to make shifts in how they serve clients, support staff members and manage

stakeholders

Long decision making process

Multiple steps and hand-offs in decision implementation

Fragmented teams working in silos

Decentralised decision making

Quick decision making

Streamlining decision making and relaxing onerous

governance requirements

Single team reporting directly to CEO

Semi-autonomous team with decision making authority

McKinsey & Company 28

Private Sector

focus areas

… and focus on 6 key areasBased on discussions with risk and health professionals and more than 200 companies across sectors

Current as of April 1, 2020

BWorkforce

protection

CSupply Chain

Stabilization

DCustomer

engagement

EStress-test

financials

AOperate nerve

center

FGovernment

support

Tiering (all/some/no WFH) | Infra setup (VPN, laptops, desktops) | Broadband availability3 Personnel & contractors

Staggering work shifts/times | Prevention (e.g., Social distancing) | Closures4 Facility & On-site norms

Multi-channel communications | Confidential reporting mechanisms | Source of truth2 Two Way Communication

Critical part identification | Parts rationing | Location optimization 2 Inventory management

Operational impact assessment | Production capacity optimization3 Production & Operations

Prevention interventions across customer journey | Cust. team training | Execution monitoring2 Customer protection

Relevant scenarios based on latest epidemiological & economic outlook1 Scenario definition

Financials in different scenarios, especially working capital requirements2 Financial stress tests

Local & federal regulators and public health officials | Support to Government5 Health & Govt engagement

Portfolio of policies and actions incl. prevention and incident response1 Policy & Management

Customer comms re: COVID-practices | Fact-based reports on issues | Situation comms3 Customer outreach

Comms to B2B customers (e.g., microsite) | Scenario-based risk comms1 B2B transparency

Ports | Logistics capacity pre-booking | Route optimization5 Logistics

Cross-tier risk transparency | Supplier restart | Order mgmt. | New supplier qualifications1 Supplier engagement

S&OP SKU-level demand signal estimates by macro scenario | Production and sourcing plan4 Demand management

Trigger-based portfolio of actions (across all workstreams above)2 Portfolio of actions

Align leaders on scenarios | Roundtable exercises 3 Leadership alignment

Offer expertise support to Governments (e.g., via the National nerve center)1 Sharing expertise

Implement supportive measures (e.g., reduced data costs, delayed interest payments, etc.)2 Providing support

Single source of truth for issue resolution & tapping surge resources where needed1 Issue map & management

Monetary and product donations to funds for support of vulnerable population3 Donations

McKinsey & Company 29

F. Manufacturing example: 15 immediate actions to control cost and ensure business continuity To create transparency and ensure agility during crisis management

Current as of April 1, 2020

Sources: McKinsey team analysis

Set up control

tower to help

implement

strategic and

tactical actions

with transparency

and execution

excellence

Recommended actions

Operations

Materials

Logistics

5 Expedite qualification process of new partners and suppliers without sacrificing quality

14 Pre-book air freight/rail/truck capacity

15 Optimize mode of transportation and route to reduce lead-time and cost

7 Work with supplier to source PPE for production lines (government is requiring glasses, gloves and masks)

3 Conduct scenario analysis to understand financial and operational implications in continuous shutdown with 3-6

month demand

4 Optimize limited production capacity based on aligned prioritization criteria (customer, profit, production efficiency,

strategic importance of goods, etc.)

Strategic

8 Determine truly critical components and understand risks of suppliers of each tier

9 Understand current inventory buffer and coordinate cross-regionally

10 Build up critical material inventory with help from distributors, brokers or alternative sources especially for

suppliers from Hubei

11 Monitor extending lead times to gauge performance and capacity against supplier promises

12 Consider short-term support to suppliers/partners along the value chain (e.g., low-interest loan) to accelerate

faster work resumption in exchange for supply stability and exclusivity

13 Re-balance the sourcing volume from impacted sites to other sites based on sourcing strategy such as single,

dual, multi, if shutdown persists

6 Implement solid business recovery action catalogue/policy/process on infectious disease situation and be able to

restart as soon as possible

Demand 1 Reshape demand if applicable and communicate with customers on inventory availability and actual production

capacity. Consider pricing action for uncertain demand outlook

2 Adjust demand forecast timely with inputs from distributors and major customers

Tactical1

1. Tactical actions are temporary actions that might not continue after the crisis, while strategic actions have long term impact on the supply chains

McKinsey & Company 30

Development partners can consider even bolder actions to support the continent through the crisis

Current as of April 1, 2020

Economy

Business

environment

Household

welfare

Ideas

3

5

2

1

These ideas are in addition to supporting governments on some of their key interventions detailed on the prior pages

Private-sector liquidity fund. Offer grants, interest free loans or debt for equity swaps to support

businesses and limit job losses.

Africa “Solidarity fund” where businesses and individuals could contribute to a fund earmarked for

immediate relief for the most vulnerable households and micro-businesses (“hustlers”).

Africa Green Program. A get-to-work program that plants millions of trees across the continent, using

a currently out-of-work labor force at reduced salary, could provide employment and help solve global

and local climate change issues.

Africa recovery plan. An extensive stimulus package or economic development plan, modelled on the

Marshall Plan that provided aid to Europe after World War II.

African procurement platform. A common platform to procure medical supplies and equipment to

combat the pandemic could provide an Africa-wide solution to challenges that each individual country is

trying to address.

4

EXAMPLES -- NOT EXHAUSTIVE

McKinsey & Company 31

Look forward: Our next perspective will focus on resilience

CONFIDENTIAL AND PROPRIETARY

Any use of these materials without specific permission is strictly prohibited. This deck does not constitute legal, medical, accounting, tax, or other regulated advice, such as professional advice normally provided by licensed or certified practitioners

Address near-term

policy challenges, and

broader resiliency issues

during virus-related

shutdowns and

economic knock-on

effects

Reform

ResolveResilience

ReturnReimagination

Focus of this

section

▪ How big do fiscal stimulus packages need to for meaningful impact?

▪ How do governments manage their roles to both protect the health of

vulnerable populations and protect the economy? When, and how, is

the decision on returning to work going to be made?

▪ How systematic can reforms be (e.g., entire sectors be re-structured

and reformed as part of any intervention package)?

▪ What are the best ways to provide targeted support to the most

vulnerable populations?

▪ What would be the long-term human-capital implications of these

measures, and how could we mitigate those? For example, school

closures are necessary now but may negatively impact quality of

education and drop-out rates.

Address the immediate

challenges that COVID-

19 represents to the

institution’s workforce

and countries

NOT EXHAUSTIVE

Current as of April 1, 2020